Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - AMERICOLD REALTY TRUST | q42017-pressrelease.htm |

| 8-K - 8-K - AMERICOLD REALTY TRUST | americold-form8xk4q17earni.htm |

Tacoma, WA Facility

Earnings Press Release and Supplemental Financial Information

Fourth Quarter and Year Ended December 31, 2017

| ||

Financial Supplement | Fourth Quarter 2017 | |

Table of Contents | |

Highlights | |

Company Profile | |

Earnings Release | |

Financial Information | |

Consolidated Balance Sheet | |

Consolidated Statement of Income | |

Reconciliation of Net Earnings to FFO, Core FFO, and AFFO | |

Reconciliation of Net Earnings to EBITDA and Core EBITDA | |

Debt Detail and Maturities | |

Operations Overview | |

Revenue and Contribution by Segment | |

Overall Occupancy Trend | |

Warehouse Portfolio | |

Fixed Commitment and Lease Maturity Schedules | |

Maintenance Capital Expenditures and Maintenance Expense | |

Total Global Warehouse Performance | |

Same-store Financial Performance | |

Same-store Key Operating Metrics | |

Capital Deployment | |

Current Development Projects | |

Notes and Definitions | |

2

| ||

Financial Supplement | Fourth Quarter 2017 | |

Corporate Profile

We are the world’s largest owner and operator of temperature-controlled warehouses. We are organized as a self-administered and self-managed REIT with proven operating, development and acquisition expertise. As of December 31, 2017, we operated a global network of 158 temperature-controlled warehouses encompassing approximately 934 million cubic feet, with 140 warehouses in the United States, six warehouses in Australia, seven warehouses in New Zealand, two warehouses in Argentina and three warehouses in Canada. In addition, we hold a minority interest in the China JV, as described in Note 3 of the Consolidated Financial Statements included in Item 8 of our 2017 Annual Report on Form 10-K, which owns or operates 13 temperature-controlled warehouses located in China.

Corporate Headquarters

10 Glenlake Parkway South Tower, Suite 600

Atlanta, Georgia 30328

Telephone: (678) 441-1400

Website: www.americold.com

Senior Management

Fred Boehler: Chief Executive Officer, President and Trustee

Marc Smernoff: Chief Financial Officer and Executive Vice President

Andrea Darweesh: Chief Human Resources Officer and Executive Vice President

Thomas Musgrave: Chief Information Officer and Executive Vice President

James C. Snyder, Jr.: Chief Legal Officer and Executive Vice President

Thomas Novosel: Chief Accounting Officer and Senior Vice President

Board Members

Jeffrey M. Gault: Chairman of the Board of Trustees

James R. Heistand: Lead Independent Trustee

Fred Boehler: Chief Executive Officer, President and Trustee

George J. Alburger, Jr.: Trustee

Bradley J. Gross: Trustee

Joel A. Holsinger: Trustee

Michelle M. MacKay: Trustee

Mark R. Patterson: Trustee

Andrew P. Power: Trustee

Investor Relations

To request more information or to be added to our e-mail distribution list, please visit our website: www.americold.com

(Please proceed to the Investor Relations section)

Analyst Coverage | ||

Firm | Analyst Name | Contact |

Baird Equity Research | David B. Rodgers | 216-737-7341 |

Bank of America Merrill Lynch | Joshua Dennerlein | 646-855-1681 |

Goldman Sachs | Andrew Rosivach | 212-902-2796 |

J.P. Morgan | Michael W. Mueller | 212-622-6689 |

RBC | Michael Carroll | 440-715-2649 |

SunTrust Robinson Humphrey | Ki Bin Kim | 212-303-4124 |

Stock Listing Information

The stock of Americold Realty Trust is traded on the New York Stock Exchange under the symbol "COLD".

3

| ||

Financial Supplement | Fourth Quarter 2017 | |

AMERICOLD REALTY TRUST ANNOUNCES FOURTH QUARTER AND FULL YEAR 2017 RESULTS

- Global Warehouse Segment Revenue Grows 6.0% Year-Over-Year -

- Completed Initial Public Offering -

- Declared First Quarter 2018 Dividend -

Atlanta, GA, March 28, 2018 - Americold Realty Trust (NYSE: COLD) (the "Company"), the world’s largest owner and operator of temperature-controlled warehouses, today announced financial and operating results for the quarter and year ended December 31, 2017. The Company completed its initial public offering on January 23, 2018 and the results detailed below reflect the pre-IPO entity, except where noted.

“We are extremely pleased with our full year 2017 results, which showed strong year over year growth including Global Warehouse segment revenue and segment contribution (NOI) increasing 6.0% and 10.9%, respectively. With the successful completion of our initial public offering in January 2018, we are now the first publicly traded owner-operator dedicated to temperature-controlled infrastructure. Our portfolio of mission critical assets, focused management, and customer-centric operating platform provide a meaningful competitive advantage as we focus on creating long-term shareholder value through the execution of our internal and external growth strategy,” stated Fred Boehler, President and Chief Executive Officer of Americold Realty Trust.

Full Year Highlights

• | Total revenue increased 3.6% to $1.54 billion of which Global Warehouse segment revenue grew 6.0% to $1.15 billion, both over prior year |

• | Total contribution (NOI) increased 8.2% to $374.1 million; of which Global Warehouse segment contribution (NOI) was up 10.9% to $348.3 million, both over prior year |

• | Net loss of $0.6 million compared to net income of $4.9 million for the prior year |

• | Core EBITDA of $287.1 million, a 9.9% increase over prior year |

• | Adjusted Funds from Operations (“AFFO”) of $94.6 million, a 33.0% increase over prior year |

• | Global Warehouse segment same store revenue grew 6.1% to $1.12 billion, with segment contribution (NOI) improving 9.8% to $346.9 million, both over prior year |

• | Same store occupancy for the Global Warehouse segment expanded 110 basis points, over prior year to 78.3% |

• | Opened a new 6.8 million refrigerated cubic foot facility in Clearfield, Utah, and commenced construction on two development projects, a 5.2 million refrigerated cubic foot facility in Middleboro, MA and a 15.7 million refrigerated cubic foot automated high-rise expansion of an existing facility in suburban Chicago |

Highlights Subsequent to Year End

• | Completed initial public offering (“IPO”) in January 2018, generating net proceeds of $494 million to the Company through the issuance of 33.4 million common shares of beneficial interest |

• | Closed new $925 million senior secured credit facility |

• | Declared a pro-rata dividend of $0.13958 per common share payable on April 16, 2018 to shareholders of record on March 30, 2018, representing a full quarterly dividend of $0.1875 per share, which equates to $0.75 per share on an annual basis |

4

| ||

Financial Supplement | Fourth Quarter 2017 | |

Fourth Quarter and Full Year 2017 Financial Results

Total revenue for the fourth quarter 2017 was $401.7 million, a 1.8% increase from the same quarter of the prior year. For the full-year 2017, total revenue grew to $1.54 billion, an increase of 3.6% to 2016.

For the fourth quarter of 2017, the Company reported net income of $8.0 million, compared to net income of $12.4 million, for the same quarter of the prior year. For the full year 2017, the Company reported a net loss of $0.6 million, compared to net income of $4.9 million, for the prior year.

Total contribution (NOI) for the fourth quarter 2017 was $100.4 million, compared to total contribution (NOI) of $101.0 million for the same quarter of the prior year. The Company's fourth quarter 2016 revenues and contribution (NOI) were favorably impacted by the timing of revenue recognition associated with certain annual customer contractual volume commitments totaling approximately $5 million. Excluding this impact, total contribution (NOI) improved $4.4 million, or 4.4% for the same quarter of the prior year. For the full year 2017, total contribution (NOI) was $374.1 million, an 8.2 % increase over 2016.

Core EBITDA was $78.7 million for the fourth quarter of 2017, compared to $82.0 million for the same quarter of the prior year. Fourth quarter 2016 Core EBITDA benefited from the same volume commitment revenue related items mentioned above, and approximately $2.0 million of other income related to business interruption insurance proceeds. Excluding these favorable items recorded in the fourth quarter of 2016, Core EBITDA improved $3.7 million, or 4.9% from the same quarter of the prior year. For the full year 2017, Core EBITDA grew to $287.1 million, a 9.9% increase over 2016.

For the fourth quarter of 2017, Core Funds from Operations (“Core FFO”) was $32.7 million, compared to $31.5 million for same quarter of the prior year. For the full year 2017, Core FFO was $106.1 million, compared to $69.2 million for the prior year.

For the fourth quarter of 2017, AFFO was $24.0 million, compared to $28.3 million for same quarter of the prior year. For the full year 2017, AFFO was $94.6 million, compared to $71.1 million for the prior year. AFFO excludes certain expenses and income items that do not represent core expenses and income streams and the full definition and reconciliation can be found in the Company’s supplemental financial information.

Fourth Quarter and Full Year 2017 Global Warehouse Segment Results

For full year 2017, the Global Warehouse segment were $1.15 billion, a 6.0% increase over 2016. Segment contribution (NOI) was $348.3 million, or 30.4% of segment revenue for full year 2017, compared to $314.0 million, or 29.1% of revenue, for the prior year. This represents 10.9% improvement in segment profitability over 2016 and an expansion of 130 basis points in segment margin year-over-year.

For the fourth quarter of 2017, the Global Warehouse segment reported revenue of $297.6 million, a 2.3% increase over the fourth quarter of 2016. Segment contribution (NOI) was $93.9 million, or 31.6% of segment revenue for the fourth quarter, compared to $92.2 million, or 31.7% of revenue, for the same quarter of the prior year. This represents a 1.9% improvement in segment contribution (NOI) over the fourth quarter of 2016. Normalizing for the portion of the revenue recognition associated with certain annual customer contractual volume commitments associated with our global warehouse segment, approximately $4.0 million,

5

| ||

Financial Supplement | Fourth Quarter 2017 | |

the year over year improvement in revenue and contribution (NOI) would have been 3.7% and 6.4%, respectively. Additionally, normalized contribution (NOI) margin would have expanded 100 basis points to 31.7% from 30.7%.

The Company ended 2017 with 146 total facilities in its Global Warehouse segment portfolio. Of the 146 total facilities, 139 meet the Company’s definition of facilities with at least 24 months of consecutive "normalized operations" and are reported as "same store". The remaining seven facilities are in various stages of operations and are classified as "non-same store".

The tables below summarize the fourth quarter and full year 2017 Global Warehouse full segment and same store metrics compared to the same period a year ago:

Global Warehouse - Total | Three Months Ended December 31, | Change | Year Ended December 31, | Change | |||||||||||||||||

Dollars in thousands | 2017 | 2016 | 2017 | 2016 | |||||||||||||||||

Global Warehouse revenues: | |||||||||||||||||||||

Rent and storage | $ | 131,695 | $ | 128,664 | 2.4 | % | $ | 501,604 | $ | 476,800 | 5.2 | % | |||||||||

Warehouse services | 165,903 | 162,330 | 2.2 | % | 644,058 | 604,067 | 6.6 | % | |||||||||||||

Total Warehouse revenues | 297,598 | 290,994 | 2.3 | % | 1,145,662 | 1,080,867 | 6.0 | % | |||||||||||||

Global Warehouse contribution (NOI) | $ | 93,930 | $ | 92,175 | 1.9 | % | $ | 348,328 | $ | 314,045 | 10.9 | % | |||||||||

Global Warehouse margin | 31.6 | % | 31.7 | % | -10 bps | 30.4 | % | 29.1 | % | 130 bps | |||||||||||

Units in thousands except per pallet data | |||||||||||||||||||||

Global Warehouse rent and storage: | |||||||||||||||||||||

Occupancy | |||||||||||||||||||||

Average occupied pallets | 2,625 | 2,595 | 1.2 | % | 2,509 | 2,470 | 1.6 | % | |||||||||||||

Average physical pallet positions | 3,232 | 3,213 | 0.6 | % | 3,216 | 3,231 | (0.5 | )% | |||||||||||||

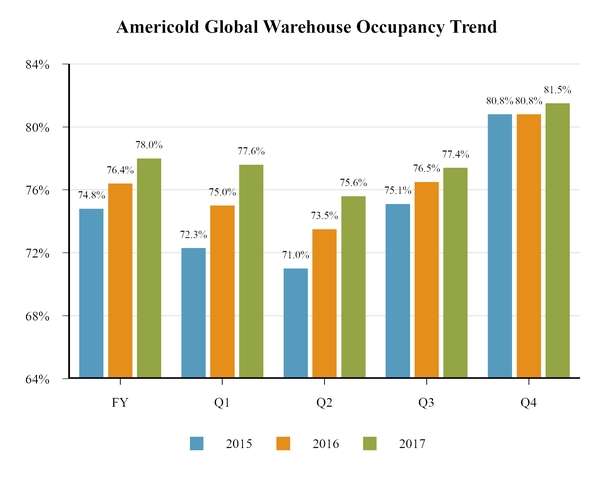

Occupancy percentage | 81.2 | % | 80.8 | % | 40 bps | 78.0 | % | 76.4 | % | 160 bps | |||||||||||

Same store rent and storage revenues per occupied pallet | $ | 50.16 | $ | 49.58 | 1.2 | % | $ | 199.96 | $ | 193.04 | 3.6 | % | |||||||||

Global Warehouse services: | |||||||||||||||||||||

Throughput pallets | 6,951 | 7,018 | (1.0 | )% | 27,626 | 27,123 | 1.9 | % | |||||||||||||

Same store warehouse services revenues per throughput pallet | $ | 23.87 | $ | 23.13 | 3.2 | % | 23.31 | 22.27 | 4.7 | % | |||||||||||

Global Warehouse - Same Store | Three Months Ended December 31, | Change | Year Ended December 31, | Change | |||||||||||||||||

Dollars in thousands | 2017 | 2016 | 2017 | 2016 | |||||||||||||||||

Global Warehouse same store revenues: | |||||||||||||||||||||

Rent and storage | $ | 128,825 | $ | 126,323 | 2.0 | % | $ | 491,174 | $ | 465,528 | 5.5 | % | |||||||||

Warehouse services | 162,633 | 159,556 | 1.9 | % | 631,287 | 591,994 | 6.6 | % | |||||||||||||

Total same store revenues | 291,458 | 285,879 | 2.0 | % | 1,122,461 | 1,057,522 | 6.1 | % | |||||||||||||

Global Warehouse same store contribution (NOI) | $ | 93,234 | $ | 92,278 | 1.0 | % | $ | 346,879 | $ | 315,809 | 9.8 | % | |||||||||

Global Warehouse same store margin | 32.0 | % | 32.3 | % | -30 bps | 30.9 | % | 29.9 | % | 100 bps | |||||||||||

Units in thousands except per pallet data | |||||||||||||||||||||

Global Warehouse same store rent and storage: | |||||||||||||||||||||

Occupancy | |||||||||||||||||||||

Average occupied pallets | 2,559 | 2,556 | 0.1 | % | 2,447 | 2,414 | 1.4 | % | |||||||||||||

Average physical pallet positions | 3,128 | 3,126 | 0.1 | % | 3,124 | 3,125 | — | % | |||||||||||||

Occupancy percentage | 81.8 | % | 81.8 | % | 0 bps | 78.3 | % | 77.2 | % | 110 bps | |||||||||||

Same store rent and storage revenues per occupied pallet | $ | 50.34 | $ | 49.41 | 1.9 | % | $ | 200.75 | $ | 192.87 | 4.1 | % | |||||||||

Global Warehouse same store services: | |||||||||||||||||||||

Throughput pallets | 6,799 | 6,895 | (1.4 | )% | 27,038 | 26,562 | 1.8 | % | |||||||||||||

Same store warehouse services revenues per throughput pallet | $ | 23.92 | $ | 23.14 | 3.4 | % | $ | 23.34 | $ | 22.29 | 4.7 | % | |||||||||

6

| ||

Financial Supplement | Fourth Quarter 2017 | |

Fixed Commitment Rent and Storage Revenue

At the end of 2017, annualized committed rent and storage revenue was $196.4 million, which represented 39.2% of our total Warehouse segment rent and storage revenue for the twelve months ended December 31, 2017.

Real Estate Portfolio

During the first quarter of 2017, the Company acquired a 9.6 million refrigerated cubic foot facility in San Antonio, TX which is fully leased to one customer under a long-term triple net lease. During the fourth quarter of 2017 the Company completed the construction of and began operations in its 6.8 million refrigerated cubic foot facility in Clearfield, UT.

During the third quarter of 2017, the Company commenced construction on a new 5.2 million refrigerated cubic foot facility based in Middleboro, MA and began construction of the 15.7 million refrigerated cubic foot high-rise expansion of one its suburban Chicago facilities, located in Rochelle, IL, which will incorporate state-of-art automation capabilities. These facilities are expected to be completed in the third and fourth quarter of 2018, respectively.

Total capital spend on these acquisitions and growth projects totaled $93.8 million for the full year 2017.

During 2017, the Company sold three facilities, two of which were idle. The two idle facilities were Norfolk, VA and West Point, MS. The third facility, Gloucester East Main, MA, maintained operations through its sale in the fourth quarter. During the third quarter, the Company exited a facility that it had leased in New Zealand.

Capital and Balance Sheet Activity

Subsequent to year-end, in January 2018, the Company completed its IPO and issued 33.4 million common shares of beneficial interest at $16.00 per share, including the full exercise of the underwriters’ option to purchase additional shares, raising aggregate net proceeds to the Company of approximately $494 million after deducting the underwriting discount and offering expenses.

In connection with the IPO, the Company closed on its new $925 million senior secured credit facility, consisting of a five-year, $525 million senior secured term loan A facility and a three-year, $400 million senior secured revolving credit facility. The credit facility has a $400 million accordion option, bringing total potential capacity to $1.325 billion. Borrowings under the entire facility bore interest at a floating rate of one-month LIBOR plus 250 basis points at origination. The spread varies between 235 and 300 basis points based on a leverage grid.

In the first quarter 2018, the Company utilized a portion of the net proceeds from the IPO, together with proceeds from the new senior secured facilities to repay $807 million outstanding under the Company’s senior secured Term Loan B facility and revolving credit facility. The Company also repaid $20.5 million of construction loan debt and canceled the commitment for future funding on those loans. In February 2018, the Company repaid $50 million on its outstanding senior term loan A facility, at which point the Company’s lender group increased its aggregate revolving credit commitments on the Company’s existing $400 million senior revolving credit facility by $50 million to $450 million.

7

| ||

Financial Supplement | Fourth Quarter 2017 | |

At March 23, 2018, the Company had total liquidity of $609 million, including cash and capacity on the Company’s revolving credit facility. The Company had total debt outstanding of approximately $1.57 billion, with a weighted average effective interest rate of 5.52% and a weighted average remaining term of 4.4 years. The Company has no material debt maturities during the remainder of 2018 and 2019.

Dividend

On March 15, 2018, the Company’s Board of Trustees declared a pro-rata dividend of $0.13958 per common share for the first quarter of 2018, payable on April 16, 2018 to shareholders of record on March 30, 2018, representing $0.1875 per share for a full quarter.

Investor Webcast and Conference Call

The Company will hold a webcast and conference call on Wednesday, March 28, 2018 at 5:00 p.m. Eastern Time to discuss fourth quarter and full year 2017 results. A live webcast of the call will be available via the Investors section of Americold Realty Trust's website at www.americold.com. To listen to the live webcast, please go to the site at least five minutes prior to the scheduled start time in order to register, download and install any necessary audio software. Shortly after the call, a replay of the webcast will be available for 90 days on the Company’s website.

The conference call can also be accessed by dialing 1-877-407-4018 or 1-201-689-8471. The telephone replay can be accessed by dialing 1-844-512-2921 or 1-412-317-6671 and providing the conference ID# 13677103. The telephone replay will be available starting shortly after the call until April 11, 2018.

The Company’s supplemental package will be available prior to the conference call in the Investor Relations section of the Company’s website at http://ir.americold.com.

About the Company

Americold is the world’s largest owner and operator of temperature-controlled warehouses. Based in Atlanta, Georgia, Americold owns and operates 158 temperature-controlled warehouses, with approximately 934 million cubic feet of storage, in the United States, Australia, New Zealand, Canada, and Argentina. Americold’s facilities are an integral component of the supply chain connecting food producers, processors, distributors and retailers to consumers. Americold serves over 2,600 customers and employs approximately 11,000 associates worldwide.

Non-GAAP Financial Measures

This press release contains non-GAAP financial measures, including FFO, core FFO, AFFO, EBITDA and Core EBITDA and same store segment revenue and contribution. A reconciliation from U.S. GAAP net income available to common stockholders to FFO, a reconciliation from FFO to core FFO and AFFO, and definitions of FFO, and core FFO are included within the supplemental. A reconciliation from U.S. GAAP net income available to common stockholders to EBITDA, Core EBITDA, a definition of Core EBITDA and definitions of net debt to Core EBITDA are included within the supplemental.

8

| ||

Financial Supplement | Fourth Quarter 2017 | |

Forward-Looking Statements

This document contains statements about future events and expectations that constitute forward-looking statements. Forward-looking statements are based on our beliefs, assumptions and expectations of our future financial and operating performance and growth plans, taking into account the information currently available to us. These statements are not statements of historical fact. Forward-looking statements involve risks and uncertainties that may cause our actual results to differ materially from the expectations of future results we express or imply in any forward-looking statements, and you should not place undue reliance on such statements. Factors that could contribute to these differences include adverse economic or real estate developments in our geographic markets or the temperature-controlled warehouse industry; general economic conditions; risks associated with the ownership of real estate and temperature-controlled warehouses in particular; defaults or non-renewals of contracts with customers; potential bankruptcy or insolvency of our customers; uncertainty of revenues, given the nature of our customer contracts; increased interest rates and operating costs; our failure to obtain necessary outside financing; risks related to, or restrictions contained in, our debt financing; decreased storage rates or increased vacancy rates; difficulties in identifying properties to be acquired and completing acquisitions; risks related to expansions of existing properties and developments of new properties, including failure to meet budgeted or stabilized returns in respect thereof; acquisition risks, including the failure of such acquisitions to perform in accordance with projections; difficulties in expanding our operations into new markets, including international markets; our failure to maintain our status as a REIT; uncertainties and risks related to natural disasters and global climate change; possible environmental liabilities, including costs, fines or penalties that may be incurred due to necessary remediation of contamination of properties presently or previously owned by us; financial market fluctuations; actions by our competitors and their increasing ability to compete with us; labor and power costs; changes in real estate and zoning laws and increases in real property tax rates; the competitive environment in which we operate; our relationship with our employees, including the occurrence of any work stoppages or any disputes under our collective bargaining agreements; liabilities as a result of our participation in multi-employer pension plans; the cost and time requirements as a result of our operation as a publicly traded REIT; the concentration of ownership by Yucaipa, the GS Entities and the Fortress Entity; changes in foreign currency exchange rates; and the impact of anti-takeover provisions in our constituent documents and under Maryland law, which could make an acquisition of us more difficult, limit attempts by our shareholders to replace our trustees and affect the price of our common shares.

Words such as “anticipates,” “believes,” “continues,” “estimates,” “expects,” “goal,” “objectives,” “intends,” “may,” “opportunity,” “plans,” “potential,” “near-term,” “long-term,” “projections,” “assumptions,” “projects,” “guidance,” “forecasts,” “outlook,” “target,” “trends,” “should,” “could,” “would,” “will” and similar expressions are intended to identify such forward-looking statements. Examples of forward-looking statements included in this documents include, among others, statements about our expected expansion and development pipeline and our targeted return on invested capital on expansion and development opportunities. We qualify any forward-looking statements entirely by these cautionary factors. Other risks, uncertainties and factors, including those discussed under “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2017 and our other reports filed with the Securities and Exchange Commission, could cause our actual results to differ materially from those projected in any forward-looking statements we make. We assume no obligation to update or revise these forward-looking statements for any reason, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future.

9

| ||

Financial Supplement | Fourth Quarter 2017 | |

Contacts:

Americold Realty Trust

Investor Relations

Telephone: 678-459-1959

Email: investor.relations@americold.com

10

| ||

Financial Supplement | Fourth Quarter 2017 | |

Americold Realty Trust and Subsidiaries | |||||||

Consolidated Balance Sheets | |||||||

(In thousands, except shares and per share amounts) | |||||||

December 31, | |||||||

2017 | 2016 | ||||||

Assets | |||||||

Property, plant, and equipment: | |||||||

Land | $ | 389,443 | $ | 384,855 | |||

Buildings and improvements | 1,865,727 | 1,765,991 | |||||

Machinery and equipment | 555,453 | 532,855 | |||||

2,810,623 | 2,683,701 | ||||||

Accumulated depreciation and depletion | (1,010,903 | ) | (923,686 | ) | |||

Property, plant, and equipment – net | 1,799,720 | 1,760,015 | |||||

Capitalized leases: | |||||||

Buildings and improvements | 16,827 | 16,827 | |||||

Machinery and equipment | 59,389 | 41,831 | |||||

76,216 | 58,658 | ||||||

Accumulated depreciation | (41,051 | ) | (34,607 | ) | |||

Capitalized leases – net | 35,165 | 24,051 | |||||

Cash and cash equivalents | 48,873 | 22,834 | |||||

Restricted cash | 21,090 | 40,096 | |||||

Accounts receivable – net of allowance of $4,961 and $4,072 at December 31, 2017and 2016, respectively | 200,354 | 199,751 | |||||

Identifiable intangible assets – net | 26,645 | 24,254 | |||||

Goodwill | 188,169 | 186,805 | |||||

Investments in partially owned entities | 15,942 | 22,396 | |||||

Other assets | 59,287 | 47,429 | |||||

Total assets | $ | 2,395,245 | $ | 2,327,631 | |||

Liabilities, Series B Preferred Shares and shareholders’ deficit | |||||||

Liabilities: | |||||||

Borrowings under revolving line of credit | $ | — | $ | 28,000 | |||

Accounts payable and accrued expenses | 241,259 | 210,469 | |||||

Construction loan - net of deferred financing costs of $179 at December 31, 2017 | 19,492 | — | |||||

Mortgage notes and term loans - net of discount and deferred financing costs of $31,996 and $35,916, in the aggregate, at December 31, 2017 and 2016, respectively | 1,721,958 | 1,652,425 | |||||

Sale-leaseback financing obligations | 121,516 | 123,616 | |||||

Capitalized lease obligations | 38,124 | 27,932 | |||||

Unearned revenue | 19,196 | 17,863 | |||||

Pension and postretirement benefits | 16,756 | 21,799 | |||||

Deferred tax liability - net | 21,940 | 23,055 | |||||

Multi-Employer pension plan withdrawal liability | 9,134 | — | |||||

Total liabilities | 2,209,375 | 2,105,159 | |||||

Commitments and Contingencies | |||||||

Preferred shares of beneficial interest, $0.01 par value – authorized 375,000 Series B Cumulative Convertible Voting and Participating Preferred Shares; aggregate liquidation preference of $375,000; 375,000 shares issued and outstanding at December 31, 2017 and 2016 | 372,794 | 371,927 | |||||

Shareholders’ deficit: | |||||||

Preferred shares of beneficial interest, $0.01 par value – authorized 1,000 Series A Cumulative Non-Voting Preferred Shares; aggregate liquidation preference of $125; 125 shares issued and outstanding at December 31, 2017 and 2016 | — | — | |||||

Common shares of beneficial interest, $0.01 par value – authorized 250,000,000 shares; 69,370,609 shares issued and outstanding at December 31, 2017 and 2016 | 694 | 694 | |||||

Paid-in capital | 394,082 | 392,591 | |||||

Accumulated deficit and distributions in excess of net earnings | (581,470 | ) | (532,196 | ) | |||

Accumulated other comprehensive loss | (230 | ) | (10,544 | ) | |||

Total shareholders’ deficit | (186,924 | ) | (149,455 | ) | |||

Total liabilities, Series B Preferred Shares and shareholders’ deficit | $ | 2,395,245 | $ | 2,327,631 | |||

11

| ||

Financial Supplement | Fourth Quarter 2017 | |

Consolidated Statements of Operations | |||||||||||||||

(In thousands, except per share amounts) | |||||||||||||||

Three Months Ended December 31, | Year Ended December 31, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

Revenues: | |||||||||||||||

Rent, storage, and warehouse services revenues | $ | 297,598 | $ | 290,994 | $ | 1,145,662 | $ | 1,080,867 | |||||||

Third-party managed services | 63,628 | 64,390 | 242,189 | 252,411 | |||||||||||

Transportation services | 38,405 | 36,969 | 146,070 | 147,004 | |||||||||||

Other revenues | 2,089 | 2,209 | 9,666 | 9,717 | |||||||||||

Total revenues | 401,720 | 394,562 | 1,543,587 | 1,489,999 | |||||||||||

Operating expenses: | |||||||||||||||

Rent, storage, and warehouse services cost of operations | 203,669 | 198,817 | 797,334 | 766,822 | |||||||||||

Third-party managed services cost of operations | 60,485 | 59,916 | 229,364 | 237,597 | |||||||||||

Transportation services cost of operations | 35,188 | 33,114 | 133,120 | 132,586 | |||||||||||

Cost of operations related to other revenues | 2,011 | 1,764 | 9,664 | 7,349 | |||||||||||

Depreciation, depletion, and amortization | 29,545 | 29,817 | 116,741 | 118,571 | |||||||||||

Selling, general and administrative | 26,855 | 28,080 | 104,640 | 100,238 | |||||||||||

Impairment of long-lived assets | 700 | 9,820 | 9,473 | 9,820 | |||||||||||

Multi-Employer pension plan withdrawal expense | — | — | 9,167 | — | |||||||||||

Total operating expenses | 358,453 | 361,328 | 1,409,503 | 1,372,983 | |||||||||||

Operating income | 43,267 | 33,234 | 134,084 | 117,016 | |||||||||||

Other (expense) income: | |||||||||||||||

(Loss) income from partially owned entities | (21 | ) | 977 | (1,363 | ) | (128 | ) | ||||||||

Impairment of partially owned entities | — | — | (6,496 | ) | — | ||||||||||

Interest expense | (29,665 | ) | (29,274 | ) | (114,898 | ) | (119,552 | ) | |||||||

Interest income | 289 | 177 | 1,074 | 708 | |||||||||||

Loss on debt extinguishment and modification | — | — | (986 | ) | (1,437 | ) | |||||||||

Foreign currency exchange gain (loss) | 279 | 2,930 | (3,591 | ) | 464 | ||||||||||

Other (expense) income, net | (237 | ) | 1,312 | 918 | 2,142 | ||||||||||

Income (loss) before income tax and gain (loss) from sale of real estate, net of tax | 13,912 | 9,356 | 8,742 | (787 | ) | ||||||||||

Income tax (expense) benefit: | |||||||||||||||

Current | (5,317 | ) | 213 | (13,051 | ) | (6,465 | ) | ||||||||

Deferred | (721 | ) | (2,812 | ) | 3,658 | 586 | |||||||||

Total income tax expense | (6,038 | ) | (2,599 | ) | (9,393 | ) | (5,879 | ) | |||||||

Income (loss) before gain (loss) from sale of real estate, net of tax | 7,874 | 6,757 | (651 | ) | (6,666 | ) | |||||||||

Gain from sale of real estate, net of tax | 126 | 5,602 | 43 | 11,598 | |||||||||||

Net income (loss) | $ | 8,000 | $ | 12,359 | $ | (608 | ) | $ | 4,932 | ||||||

Less distributions on preferred shares of beneficial interest - Series A | (8 | ) | (8 | ) | (16 | ) | (16 | ) | |||||||

Less distributions on preferred shares of beneficial interest - Series B | (7,110 | ) | (7,110 | ) | (28,436 | ) | (28,436 | ) | |||||||

Less accretion on preferred shares of beneficial interest – Series B | (210 | ) | (229 | ) | (867 | ) | (936 | ) | |||||||

Net income (loss) attributable to common shares of beneficial interest | $ | 672 | $ | 5,012 | $ | (29,927 | ) | $ | (24,456 | ) | |||||

Weighted average common shares outstanding – basic | 70,051 | 69,923 | 70,022 | 69,890 | |||||||||||

Weighted average common shares outstanding – diluted | 109,918 | 106,272 | 70,022 | 69,890 | |||||||||||

Net income (loss) per common share of beneficial interest - basic | $ | 0.01 | $ | 0.07 | $ | (0.43 | ) | $ | (0.35 | ) | |||||

Net income (loss) per common share of beneficial interest - diluted | $ | 0.01 | $ | 0.05 | $ | (0.43 | ) | $ | (0.35 | ) | |||||

Distributions declared per common share of beneficial interest | $ | 0.07 | $ | 0.14 | $ | 0.29 | $ | 0.29 | |||||||

12

| ||

Financial Supplement | Fourth Quarter 2017 | |

Reconciliation of Net Earnings to FFO, Core FFO, and AFFO | |||||||||||||||

(In thousands) | |||||||||||||||

Three Months Ended December 31, | Year Ended December 31, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

Net income (loss) | $ | 8,000 | $ | 12,359 | $ | (608 | ) | $ | 4,932 | ||||||

Adjustments: | |||||||||||||||

Real estate related depreciation | 22,041 | 21,694 | 86,478 | 85,645 | |||||||||||

Net (gain) loss on sale of depreciable real estate | (126 | ) | (5,394 | ) | (43 | ) | (11,104 | ) | |||||||

Impairment charges on certain real estate assets | 700 | 9,820 | 9,473 | 9,820 | |||||||||||

Real estate depreciation on China JV | 302 | 196 | 1,183 | 1,268 | |||||||||||

Funds from operations | 30,917 | 38,675 | 96,483 | 90,561 | |||||||||||

Less distributions on preferred shares of beneficial interest | (7,118 | ) | (7,118 | ) | (28,452 | ) | (28,452 | ) | |||||||

Funds from operations attributable to common shareholders | $ | 23,799 | $ | 31,557 | $ | 68,031 | $ | 62,109 | |||||||

Adjustments: | |||||||||||||||

Net (gain) loss on sale of non-real estate assets | (168 | ) | 375 | (599 | ) | 464 | |||||||||

Severance and reduction in workforce costs (a) | 85 | 279 | 516 | 900 | |||||||||||

Terminated site operations costs (b) | 502 | (186 | ) | 2,677 | 6 | ||||||||||

Strategic alternative costs (c) | 3,770 | 2,335 | 8,136 | 4,666 | |||||||||||

Litigation settlements | — | 89 | — | 89 | |||||||||||

Impairment of partially owned entities (d) | — | — | 6,496 | — | |||||||||||

Loss on debt extinguishment and modification | — | — | 986 | 1,437 | |||||||||||

Inventory asset impairment | — | — | 2,108 | — | |||||||||||

Foreign currency exchange (gain) loss | (279 | ) | (2,930 | ) | 3,591 | (464 | ) | ||||||||

Excise tax settlement | 4,984 | — | 4,984 | — | |||||||||||

Multi-Employer pension plan withdrawal expense | — | — | 9,167 | — | |||||||||||

Core FFO applicable to common shareholders | $ | 32,693 | $ | 31,519 | $ | 106,093 | $ | 69,207 | |||||||

Adjustments: | |||||||||||||||

Amortization of loan costs and debt discounts | 2,215 | 1,964 | 8,604 | 7,193 | |||||||||||

Amortization of below/above market leases | 37 | 37 | 151 | 196 | |||||||||||

Straight-line net rent | 3 | (55 | ) | 101 | (564 | ) | |||||||||

Deferred income taxes expense (benefit) | 721 | 2,812 | (3,658 | ) | (586 | ) | |||||||||

Stock-based compensation expense (e) | 598 | 4,486 | 2,358 | 6,436 | |||||||||||

Non-real estate depreciation and amortization | 7,505 | 8,123 | 30,264 | 32,926 | |||||||||||

Non-real estate depreciation and amortization on China JV | 155 | 104 | 609 | 762 | |||||||||||

Recurring maintenance capital expenditures (f) | (19,915 | ) | (20,651 | ) | (49,906 | ) | (44,445 | ) | |||||||

Adjusted FFO applicable to common shareholders | $ | 24,012 | $ | 28,339 | $ | 94,616 | $ | 71,125 | |||||||

(a) | Represents one-time severance from prior management team and reduction in workforce costs associated with exiting or selling non-strategic warehouses. |

(b) | Represents repair expenses incurred to return leased sites to their original physical state at lease inception in connection with the termination of the applicable underlying lease. These terminations were part of our strategic efforts to exit or sell non-strategic warehouses as opposed to ordinary course lease expirations. Repair and maintenance expenses associated with our ordinary course operations are reflected as operating expenses on our statement of operations. |

(c) | Represents one-time operating costs associated with our review of strategic alternatives prior to the IPO. |

(d) | For 2017, represents an impairment charge related to our investment in the China JV based on a determination that the recorded investment was no longer recoverable from the projected future cash distributions we expect to receive from the China JV. |

(e) | Represents stock-based compensation expense related to equity awards under our pre-IPO equity incentive plans. |

(f) | Recurring maintenance capital expenditures include capital expenditures made to extend the life of, and provide future economic benefit from, our existing temperature-controlled warehouse network and its existing supporting personal property and information technology. |

13

| ||

Financial Supplement | Fourth Quarter 2017 | |

Reconciliation of Net Earnings to EBITDA and Core EBITDA | |||||||||||||||

(In thousands) | |||||||||||||||

Three Months Ended December 31, | Year Ended December 31, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

Net income (loss) | $ | 8,000 | $ | 12,359 | $ | (608 | ) | $ | 4,932 | ||||||

Adjustments: | |||||||||||||||

Depreciation, depletion and amortization | 29,545 | 29,817 | 116,741 | 118,571 | |||||||||||

Interest expense | 29,665 | 29,274 | 114,898 | 119,552 | |||||||||||

Income tax expense | 6,038 | 2,599 | 9,393 | 5,879 | |||||||||||

EBITDA | $ | 73,248 | $ | 74,049 | $ | 240,424 | $ | 248,934 | |||||||

Adjustments: | |||||||||||||||

Severance and reduction in workforce costs (a) | 85 | 279 | 516 | 900 | |||||||||||

Terminated site operations cost (b) | 502 | (186 | ) | 2,677 | 6 | ||||||||||

Strategic alternative costs (c) | 3,770 | 2,335 | 8,136 | 4,666 | |||||||||||

Litigation settlements | — | 89 | — | 89 | |||||||||||

Loss from partially owned entities | 21 | (977 | ) | 1,363 | 128 | ||||||||||

Non-recurring impairment of partially owned entities (d) | — | — | 6,496 | — | |||||||||||

Impairment of inventory and long-lived assets | 700 | 9,820 | 11,581 | 9,820 | |||||||||||

Loss (gain) on foreign currency exchange | (279 | ) | (2,930 | ) | 3,591 | (464 | ) | ||||||||

Stock-based compensation expense (e) | 598 | 4,486 | 2,358 | 6,436 | |||||||||||

Loss on debt extinguishment and modification | — | — | 986 | 1,437 | |||||||||||

Loss (gain) on real estate and other asset disposals | 65 | (5,000 | ) | (150 | ) | (10,590 | ) | ||||||||

Multi-Employer pension plan withdrawal expense | — | — | 9,167 | — | |||||||||||

Core EBITDA | $ | 78,710 | $ | 81,965 | $ | 287,145 | $ | 261,362 | |||||||

(a) | Represents one-time severance from prior management team and reduction in workforce costs associated with exiting or selling non-strategic warehouses. |

(b) | Represents repair expenses incurred to return leased sites to their original physical state at lease inception in connection with the termination of the applicable underlying lease. These terminations were part of our strategic efforts to exit or sell non-strategic warehouses as opposed to ordinary course lease expirations. Repair and maintenance expenses associated with our ordinary course operations are reflected as operating expenses on our statement of operations. |

(c) | Represents one-time operating costs associated with our review of strategic alternatives prior to the IPO. |

(d) | Represents an impairment charge related to our investment in the China JV based on a determination that the recorded investment was no longer recoverable from the projected future cash distributions we expect to receive from the China JV. We did not receive any cash distributions from the China JV since the formation of the joint venture. |

(e) | Represents stock-based compensation expense related to equity awards under our pre-IPO equity incentive plans. |

14

| ||

Financial Supplement | Fourth Quarter 2017 | |

Debt Detail and Maturities | |||||||||||||

Effective interest rate 7 as of December 31, 2017 | Outstanding principal amount at | ||||||||||||

Stated maturity date | Contractual interest rate 5 | December 31, 2017 | December 31, 2016 | ||||||||||

2010 Mortgage Loans cross-collateralized and cross-defaulted by 46 warehouses: | (In thousands) | ||||||||||||

Component A-1 | 1/2021 | 3.86% | 4.40% | $ | 56,941 | $ | 73,619 | ||||||

Component A-2-FX | 1/2021 | 4.96% | 5.38% | 150,334 | 150,334 | ||||||||

Component A-2-FL 1 | 1/2021 | LIBOR + 1.51% | 3.45% | 48,654 | 74,899 | ||||||||

Component B | 1/2021 | 6.04% | 6.48% | 60,000 | 60,000 | ||||||||

Component C | 1/2021 | 6.82% | 7.28% | 62,400 | 62,400 | ||||||||

Component D | 1/2021 | 7.45% | 7.92% | 82,600 | 82,600 | ||||||||

2013 Mortgage Loans cross-collateralized and cross-defaulted by 15 warehouses: | |||||||||||||

Senior note | 5/2023 | 3.81% | 4.14% | 194,223 | 200,252 | ||||||||

Mezzanine A | 5/2023 | 7.38% | 7.55% | 70,000 | 70,000 | ||||||||

Mezzanine B | 5/2023 | 11.50% | 11.75% | 32,000 | 32,000 | ||||||||

ANZ Term Loans secured by mortgages in properties owned by relevant subsidiaries: | |||||||||||||

Australian Term Loan 2 | 6/2020 | BBSY + 1.40% | 4.51% | 158,645 | 146,789 | ||||||||

New Zealand Term Loan 3 | 6/2020 | BKBM + 1.40% | 5.12% | 31,240 | 30,615 | ||||||||

Senior Secured Term Loan B Facility secured by stock pledge in qualified subsidiaries | 12/2022 | LIBOR + 3.75% with 1% floor or ABR + 2.75% with 2% floor | 5.79% | 806,918 | 704,833 | ||||||||

Total principal amount of mortgage notes and term loans | 1,753,955 | 1,688,341 | |||||||||||

Less deferred financing costs | (25,712 | ) | (28,473 | ) | |||||||||

Less debt discount | (6,285 | ) | (7,443 | ) | |||||||||

Total mortgage notes and term loans, net of deferred financing costs and debt discount | $ | 1,721,958 | $ | 1,652,425 | |||||||||

2015 Senior Secured Revolving Credit Facility secured by stock pledge in qualified subsidiaries | 12/2018 4 | LIBOR + 3.00% or ABR + 2.00% | 3.92% | $ | — | $ | 28,000 | ||||||

Construction Loans: | |||||||||||||

Warehouse Clearfield, UT secured by mortgage | 2/2019 | LIBOR + 3.25% or prime rate + 2.25% | 5.18% | $ | 19,671 | $ | — | ||||||

Less deferred financing costs | (179 | ) | — | ||||||||||

$ | 19,492 | $ | — | ||||||||||

Warehouse Middleboro, MA secured by mortgage | 8/2020 | LIBOR +2.75% or ABR +1.75% | — | $ | — | $ | — | ||||||

(1) | Component A-2-FL of the 2010 Mortgage Loans has a variable interest rate equal to one-month LIBOR plus 1.51%, with one-month-LIBOR subject to a floor of 1.00% per annum. In addition, we maintain an interest rate cap on the variable rate tranche that caps one-month LIBOR at 6.0%. The variable interest rate at December 31, 2017 was 2.98% per annum. |

(2) | As of December 31, 2017, the outstanding balance was AUD$203.0 million and the variable interest rate was 3.10% per annum (1.70% BBSY plus 1.40% margin) of which 75% is fixed via an interest rate swap at 4.06% per annum (2.66% BBSY plus 1.40% margin). |

(3) | As of December 31, 2017, the outstanding balance was NZD$44.0 million and the variable interest rate was 3.22% per annum (1.82% BKBM plus 1.40% margin), of which 75% is fixed via an interest rate swap at 4.93% per annum (3.53% BKBM plus 1.40% margin). |

(4) | Prior to the IPO we have the option to extend the stated maturity date of our Senior Secured Revolving Credit Facility to December 1, 2019, subject to certain conditions. |

(5) | References in this table to LIBOR are references to one-month LIBOR and references to BBSY and BKBM are to Australian Bank Bill Swap Bid Rate and New Zealand Bank Bill Reference Rate, respectively. |

(6) | Unused line, letter of credit and financing fees increase the stated interest rate. |

(7) | The effective interest rate includes effects of amortization of the deferred financing costs and debt discount. The weighted average effective interest rate for total debt was 5.68% and 5.67% as of December 31, 2017 and 2016, respectively. |

15

| ||

Financial Supplement | Fourth Quarter 2017 | |

Operations Overview

Revenue and Contribution by Segment | |||||||||||||||

(In thousands) | |||||||||||||||

Three Months Ended December 31, | Year Ended December 31, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

Segment revenues: | |||||||||||||||

Warehouse | $ | 297,598 | $ | 290,994 | $ | 1,145,662 | $ | 1,080,867 | |||||||

Third-Party Managed | 63,628 | 64,390 | 242,189 | 252,411 | |||||||||||

Transportation | 38,405 | 36,969 | 146,070 | 147,004 | |||||||||||

Quarry | 2,089 | 2,209 | 9,666 | 9,717 | |||||||||||

Total revenues | 401,720 | 394,562 | 1,543,587 | 1,489,999 | |||||||||||

Segment contribution: | |||||||||||||||

Warehouse | 93,930 | 92,175 | 348,328 | 314,045 | |||||||||||

Third-Party Managed | 3,143 | 4,474 | 12,825 | 14,814 | |||||||||||

Transportation | 3,217 | 3,855 | 12,950 | 14,418 | |||||||||||

Quarry | 77 | 447 | 2 | 2,368 | |||||||||||

Total segment contribution | 100,367 | 100,951 | 374,105 | 345,645 | |||||||||||

Reconciling items: | |||||||||||||||

Depreciation, depletion, and amortization | (29,545 | ) | (29,817 | ) | (116,741 | ) | (118,571 | ) | |||||||

Impairment of long-lived assets | (306 | ) | (9,820 | ) | (9,473 | ) | (9,820 | ) | |||||||

Multi-Employer pension plan withdrawal expense | (394 | ) | — | (9,167 | ) | — | |||||||||

Selling, general and administrative | (26,855 | ) | (28,080 | ) | (104,640 | ) | (100,238 | ) | |||||||

Income (Loss) from partially owned entities | (21 | ) | 977 | (1,363 | ) | (128 | ) | ||||||||

Impairment of partially owned entities | — | — | (6,496 | ) | — | ||||||||||

Interest expense | (29,665 | ) | (29,274 | ) | (114,898 | ) | (119,552 | ) | |||||||

Interest income | 289 | 177 | 1,074 | 708 | |||||||||||

Loss on debt extinguishment and modification | — | — | (986 | ) | (1,437 | ) | |||||||||

Foreign currency exchange gain (loss) | 279 | 2,930 | (3,591 | ) | 464 | ||||||||||

Other income, net | (237 | ) | 1,312 | 918 | 2,142 | ||||||||||

Income (loss) before income tax and gain (loss) from sale of real estate, net of tax | $ | 13,912 | $ | 9,356 | $ | 8,742 | $ | (787 | ) | ||||||

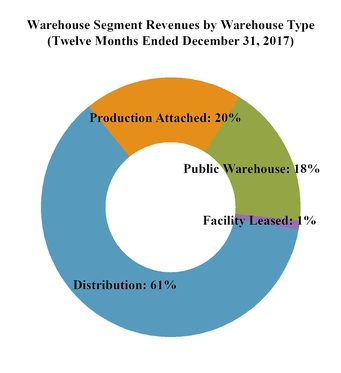

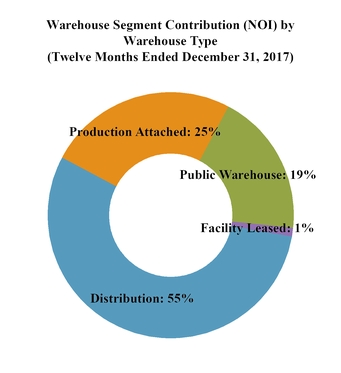

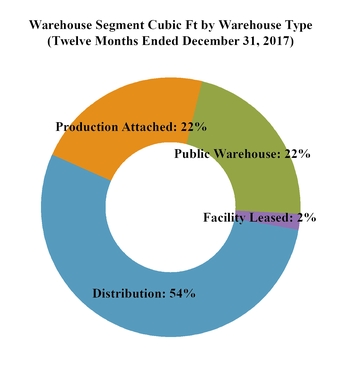

We view and manage our business through three primary business segments—warehouse, third-party managed and transportation. Our core business is our warehouse segment, where we provide temperature-controlled warehouse storage and related handling and other warehouse services. In our warehouse segment, we collect rent and storage fees from customers to store their frozen and perishable food and other products within our real estate portfolio. We also provide our customers with handling and other warehouse services related to the products stored in our buildings that are designed to optimize their movement through the cold chain, such as the placement of food products for storage and preservation, the retrieval of products from storage upon customer request, blast freezing, case-picking, kitting and repackaging and other recurring handling services.

Under our third-party managed segment, we manage warehouses on behalf of third parties and provide warehouse management services to several leading food retailers and manufacturers in customer-owned facilities, including some of our largest and longest-standing customers. We believe using our third-party management services allows our customers to increase efficiency, reduce costs, reduce supply-chain risks and focus on their core businesses. We also believe that providing third-party management services to many of our key customers underscores our ability to offer a complete and integrated suite of services across the cold chain.

In our transportation segment, we broker and manage transportation of frozen and perishable food and other products for our customers. Our transportation services include consolidation services (i.e., consolidating a customer’s products with those of other customers for more efficient shipment), freight under management services (i.e., arranging for and overseeing transportation of customer inventory) and dedicated transportation services, each designed to improve efficiency and reduce transportation and logistics costs to our customers. We provide these transportation services at cost plus a service fee or, in the case of our consolidation services, we charge a fixed fee.

We also operate a limestone quarry on the land we own around our Carthage, Missouri warehouse, which contains substantial limestone deposits. We do not view the operation of the quarry as an integral part of our business.

16

| ||

Financial Supplement | Fourth Quarter 2017 | |

Average Physical Occupancy(1)

(1) | We define average physical occupancy as the average number of occupied pallets divided by the estimated number of average physical pallet positions in our warehouses for the applicable period. We estimate the number of physical pallet positions by taking into account actual racked space and by estimating unracked space on an as-if racked basis. We base this estimate on the total cubic feet of each room within the warehouse that is unracked divided by the volume of an assumed rack space that is consistent with the characteristics of the relevant warehouse. On a warehouse by warehouse basis, rack space generally ranges from two to three feet depending upon the type of facility and the nature of the customer goods stored therein. The number of our pallet positions is reviewed and updated quarterly, taking into account changes in racking configurations and room utilization. |

Historically, providers of temperature-controlled warehouse space have offered storage services to customers on an as-utilized, on-demand basis. We have entered into fixed storage commitments with certain of our customers which give us, among other things, additional clarity around the expected occupancy of our warehouses. As of December 31, 2017, we had entered into contracts featuring fixed storage commitments or leases with 86 of our customers in our warehouse segment. Customers with fixed storage provisions commit to occupy a certain number of pallets at a designated storage rate for the applicable portion of their contractual term, whether the customer elects to physically store goods in a warehouse or not. As a result, certain pallets in our warehouses may generate storage revenue pursuant to fixed storage commitments despite not being physically occupied. We refer to economic occupancy as the aggregate number of physically occupied pallets and any additional pallets otherwise contractually committed for a given period. To the extent that a customer with a fixed storage provision elects not to utilize all of its committed pallets in a particular warehouse, we have the flexibility to deploy those pallets to facilitate shorter-term customers that desire space on an as-utilized, on demand basis.

17

| ||

Financial Supplement | Fourth Quarter 2017 | |

Warehouse Portfolio

Country / Region | # of warehouses | Cubic feet (in millions) | % of total cubic feet | Pallet positions (in thousands) | Average physical occupancy (1) | Revenues (2) (in millions) | Applicable segment contribution (NOI) (2)(3) (in millions) | Total customers (4) | ||||||||||||||||||

Owned / Leased (5) | ||||||||||||||||||||||||||

United States | ||||||||||||||||||||||||||

Central | 34 | 220.6 | 25 | % | 874.3 | 75 | % | $ | 233.7 | $ | 78.3 | 837 | ||||||||||||||

East | 23 | 165.9 | 19 | % | 534.4 | 77 | % | 247.3 | 65.7 | 738 | ||||||||||||||||

Southeast | 37 | 176.5 | 20 | % | 575.6 | 77 | % | 205.8 | 57.2 | 658 | ||||||||||||||||

West | 38 | 235.0 | 27 | % | 992.8 | 79 | % | 256.8 | 97.6 | 746 | ||||||||||||||||

United States Total / Average | 132 | 798.0 | 91 | % | 2,977.1 | 77 | % | $ | 943.7 | $ | 298.8 | 2,315 | ||||||||||||||

International | ||||||||||||||||||||||||||

Australia | 5 | 47.6 | 5 | % | 142.7 | 94 | % | $ | 156.4 | $ | 37.2 | 86 | ||||||||||||||

New Zealand | 7 | 22.8 | 3 | % | 72.9 | 85 | % | 32.5 | 9.3 | 96 | ||||||||||||||||

Argentina | 2 | 9.7 | 1 | % | 21.6 | 83 | % | 13.2 | 3.0 | 29 | ||||||||||||||||

International Total / Average | 14 | 80.2 | 9 | % | 237.2 | 90 | % | $ | 202.0 | $ | 49.5 | 202 | ||||||||||||||

Owned / Leased Total / Average | 146 | 878.2 | 100 | % | 3,214.3 | 78 | % | $ | 1,145.7 | $ | 348.3 | 2,428 | ||||||||||||||

Third-Party Managed | ||||||||||||||||||||||||||

United States | 8 | 41.5 | 74 | % | — | — | $ | 214.6 | $ | 8.7 | 4 | |||||||||||||||

Australia (6) | 1 | — | — | % | — | — | 9.2 | 2.5 | 1 | |||||||||||||||||

Canada | 3 | 14.3 | 26 | % | — | — | 18.4 | 1.6 | 2 | |||||||||||||||||

Third-Party Managed Total / Average | 12 | 55.8 | 100 | % | — | — | $ | 242.2 | $ | 12.8 | 6 | |||||||||||||||

Portfolio Total / Average | 158 | 933.9 | 100 | % | 3,215.0 | 78 | % | $ | 1,387.9 | $ | 361.2 | 2,429 | ||||||||||||||

(1) | We define average physical occupancy as the average number of occupied pallets divided by the estimated number of average physical pallet positions in our warehouses for the year ended December 31, 2017. We estimate the number of physical pallet positions by taking into account actual racked space and by estimating unracked space on an as-if racked basis. We base this estimate on the total cubic feet of each room within the warehouse that is unracked divided by the volume of an assumed rack space that is consistent with the characteristics of the relevant warehouse. On a warehouse by warehouse basis, rack space generally ranges from two to three feet depending upon the type of facility and the nature of the customer goods stored therein. The number of our pallet positions is reviewed and updated quarterly, taking into account changes in racking configurations and room utilization. |

(2) | Year ended December 31, 2017. |

(3) | We use the term “segment contribution (NOI)” to mean a segment’s revenues less its cost of operations (excluding any depreciation, depletion and amortization, impairment charges and corporate-level selling, general and administrative expenses). The applicable segment contribution (NOI) from our owned and leased warehouses and our third-party managed warehouses is included in our warehouse segment contribution (NOI) and third-party managed segment contribution (NOI), respectively. |

(4) | We serve some of our customers in multiple geographic regions and in multiple facilities within geographic regions. As a result, the total number of customers that we serve is less than the total number of customers reflected in the table above that we serve in each geographic region. |

(5) | As of December 31, 2017, we owned 110 of our U.S. warehouses and ten of our international warehouses, and we leased 22 of our U.S. warehouses and four of our international warehouses. As of December 31, 2017, seven of our owned facilities were located on land that we lease pursuant to long-term ground leases. |

(6) | Constitutes non-refrigerated, or “ambient,” warehouse space. This facility contains 330,527 square feet of ambient space. |

18

| ||

Financial Supplement | Fourth Quarter 2017 | |

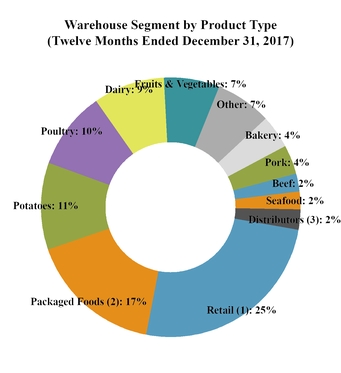

(1) | Retail reflects a broad variety of product types from retail customers. |

(2) | Packaged foods reflects a broad variety of temperature-controlled meals and foodstuffs. |

(3) | Distributors reflects a broad variety of product types from distributor customers. |

19

| ||

Financial Supplement | Fourth Quarter 2017 | |

Fixed Commitment and Lease Maturity Schedule

The following table sets forth a summary schedule of the expirations for any defined contracts featuring fixed storage commitments and leases in effect as of December 31, 2017. The information set forth in the table assumes no exercise of extension options under these contracts and leases.

Contract Expiration Year | Number of Contracts | Annualized Committed Rent & Storage Revenue(1) (in thousands) | % of Total Warehouse Rent & Storage Segment Revenue for the Twelve Months Ended December 31, 2017 | Total Warehouse Segment Revenue Generated by Contracts with Fixed Commitments & Leases for the Twelve Months Ended December 31, 2017 (in thousands) | Annualized Committed Rent & Storage Revenue at Expiration(2) (in thousands) | |||||||||||||

Month-to-Month | 37 | $ | 30,463 | 6.1 | % | $ | 107,162 | $ | 30,463 | |||||||||

2018 | 40 | 37,807 | 7.5 | % | 88,896 | 37,915 | ||||||||||||

2019 | 21 | 35,997 | 7.2 | % | 108,774 | 36,545 | ||||||||||||

2020 | 21 | 24,093 | 4.8 | % | 65,068 | 25,038 | ||||||||||||

2021 | 6 | 3,514 | 0.7 | % | 13,959 | 3,729 | ||||||||||||

2022 | 13 | 42,737 | 8.5 | % | 53,216 | 43,317 | ||||||||||||

2023 | 2 | 2,795 | 0.6 | % | 2,470 | 3,077 | ||||||||||||

2024 | 1 | 424 | 0.1 | % | 690 | 463 | ||||||||||||

2025 | — | — | — | % | — | — | ||||||||||||

2026 | 2 | 5,779 | 1.2 | % | 10,378 | 5,779 | ||||||||||||

2027 | 2 | 4,579 | 0.9 | % | 7,448 | 4,992 | ||||||||||||

2028 | — | — | — | % | — | — | ||||||||||||

2029 | 2 | 8,191 | 1.6 | % | 20,730 | 9,862 | ||||||||||||

Total | 147 | $ | 196,379 | 39.2 | % | $ | 478,790 | $ | 201,178 | |||||||||

(1) | Represents monthly fixed storage commitments and lease rental payments under the relevant expiring defined contract and lease as of December 31, 2017, plus the weighted average monthly warehouse services revenues attributable to these contracts and leases for the twelve months ended December 31, 2017, multiplied by 12. |

(2) | Represents annualized monthly revenues from fixed storage commitments and lease rental payments under the defined contracts and relevant expiring leases as of December 31, 2017 based upon the monthly revenues attributable thereto in the last month prior to expiration, multiplied by 12. |

20

| ||

Financial Supplement | Fourth Quarter 2017 | |

The following table sets forth a summary schedule of the expirations of our facility leased warehouses and other leases pursuant to which we lease space to third parties in our warehouse portfolio, in each case, in place as of December 31, 2017.

Lease Expiration Year | No. of Leases Expiring | Annualized Rent(1) (in thousands) | % of Total Warehouse Rent & Storage Segment Revenue for the Twelve Months Ended December 31, 2017 | Leased Square Footage (in thousands) | % Leased Square Footage | Annualized Rent at Expiration(2) (in thousands) | ||||||||||||||

Month-to-Month | 16 | $ | 2,667 | 0.5 | % | 245 | 10.7 | % | $ | 2,667 | ||||||||||

2018 | 9 | 1,482 | 0.3 | % | 188 | 8.2 | % | 1,489 | ||||||||||||

2019 | 6 | 1,730 | 0.3 | % | 369 | 16.2 | % | 1,793 | ||||||||||||

2020 | 6 | 3,294 | 0.7 | % | 353 | 15.5 | % | 3,432 | ||||||||||||

2021 | 3 | 890 | 0.2 | % | 420 | 18.4 | % | 1,323 | ||||||||||||

2022 | 2 | 989 | 0.2 | % | 144 | 6.3 | % | 989 | ||||||||||||

2023 | 2 | 2,795 | 0.6 | % | 493 | 21.6 | % | 3,077 | ||||||||||||

2024 | 1 | 424 | 0.1 | % | 70 | 3.1 | % | 463 | ||||||||||||

2025 | — | — | — | — | — | — | ||||||||||||||

2026 and thereafter | — | — | — | — | — | — | ||||||||||||||

Total | 45 | $ | 14,271 | 2.8 | % | 2,282 | 100 | $ | 15,233 | |||||||||||

(1) | Represents monthly rental payments under the relevant leases as of December 31, 2017, multiplied by 12. |

(2) | Represents monthly rental payments under the relevant leases in the calendar year of expiration, multiplied by 12. |

These leases had a weighted average remaining term of 32 months as of December 31, 2017.

• | Month-to-Month Warehouse Rate Agreements. Month-to-month warehouse rate agreements are agreements that establish storage fee rates on products stored in our warehouses and rates for value-added services on an as-utilized, on-demand basis, typically pursuant to terms set forth on a standardized warehouse receipt and related rate schedule, but that do not require the customer to use our network or for us to reserve space for these customers. Our standard terms and conditions afford us favorable contractual protections and are not subject to negotiation with customers that enter into month-to-month warehouse rate agreements. Month-to-month customer relationships |

21

| ||

Financial Supplement | Fourth Quarter 2017 | |

Recurring Maintenance Capital Expenditures and Repair and Maintenance Expenses

We utilize a strategic approach to recurring maintenance capital expenditures and repair and maintenance expenses to maintain the high quality and operational efficiency of our warehouses and ensure that our warehouses meet the “mission-critical” role they serve in the cold chain.

Recurring Maintenance Capital Expenditures

The following table sets forth our recurring maintenance capital expenditures for the years ended December 31, 2017, 2016 and 2015.

Year ended December 31, | |||||||||||

2017 | 2016 | 2015 | |||||||||

(In thousands, except per cubic foot amounts) | |||||||||||

Real estate | $ | 44,102 | $ | 36,153 | $ | 34,011 | |||||

Personal property | 1,890 | 3,213 | 3,678 | ||||||||

Information technology | 3,914 | 5,079 | 3,996 | ||||||||

Total recurring maintenance capital expenditures | $ | 49,906 | $ | 44,445 | $ | 41,685 | |||||

Total recurring maintenance capital expenditures per cubic foot | $ | 0.053 | $ | 0.047 | $ | 0.043 | |||||

Repair and Maintenance Expenses

The following table sets forth our repair and maintenance expenses for the years ended December 31, 2017, 2016 and 2015.

Year ended December 31, | |||||||||||

2017 | 2016 | 2015 | |||||||||

(In thousands, except per cubic foot amounts) | |||||||||||

Real estate | $ | 21,467 | $ | 20,956 | $ | 18,843 | |||||

Personal property | 31,254 | 30,888 | 31,257 | ||||||||

Total repair and maintenance expenses | $ | 52,721 | $ | 51,844 | $ | 50,100 | |||||

Repair and maintenance expenses per cubic foot | $ | 0.056 | $ | 0.055 | $ | 0.052 | |||||

Growth and Expansion Capital Expenditures

The following table sets forth our growth and expansion capital expenditures for the years ended December 31, 2017, 2016 and 2015.

Year ended December 31, | |||||||||||

2017 | 2016 | 2015 | |||||||||

(In thousands) | |||||||||||

Expansion and development initiatives | $ | 99,878 | $ | 27,529 | $ | 8,532 | |||||

Information technology | 5,973 | 4,649 | 4,031 | ||||||||

Total growth and expansion capital expenditures | $ | 105,851 | $ | 32,178 | $ | 12,563 | |||||

22

| ||

Financial Supplement | Fourth Quarter 2017 | |

Total Global Warehouse Performance

The following table presents the operating results of our warehouse segment for the years ended December 31, 2017 and 2016.

Year ended December 31, | Change | ||||||||||||||||

2017 actual | 2017 constant currency(1) | 2016 actual | Actual | Constant currency | |||||||||||||

(Dollars in thousands) | |||||||||||||||||

Rent and storage | $ | 501,604 | $ | 501,168 | $ | 476,800 | 5.2 | % | 5.1 | % | |||||||

Warehouse services | 644,058 | 640,805 | 604,067 | 6.6 | % | 6.1 | % | ||||||||||

Total warehouse segment revenues | 1,145,662 | 1,141,973 | 1,080,867 | 6.0 | % | 5.7 | % | ||||||||||

Power | 72,408 | 72,376 | 71,999 | 0.6 | % | 0.5 | % | ||||||||||

Other facilities costs (2) | 104,713 | 104,596 | 102,032 | 2.6 | % | 2.5 | % | ||||||||||

Labor | 509,951 | 507,715 | 484,822 | 5.2 | % | 4.7 | % | ||||||||||

Other services costs (3) | 110,262 | 109,898 | 107,969 | 2.1 | % | 1.8 | % | ||||||||||

Total warehouse segment cost of operations | 797,334 | 794,585 | 766,822 | 4.0 | % | 3.6 | % | ||||||||||

Warehouse segment contribution (NOI) | $ | 348,328 | $ | 347,388 | $ | 314,045 | 10.9 | % | 10.6 | % | |||||||

Warehouse rent and storage contribution (NOI) (4) | $ | 324,483 | $ | 324,196 | $ | 302,769 | 7.2 | % | 7.1 | % | |||||||

Warehouse services contribution (NOI) (5) | $ | 23,845 | $ | 23,192 | $ | 11,276 | 111.5 | % | 105.7 | % | |||||||

Total warehouse segment margin | 30.4 | % | 30.4 | % | 29.1 | % | 130 bps | 130 bps | |||||||||

Rent and storage margin(6) | 64.7 | % | 64.7 | % | 63.5 | % | 120 bps | 120 bps | |||||||||

Warehouse services margin(7) | 3.7 | % | 3.6 | % | 1.9 | % | 180 bps | 170 bps | |||||||||

The following table presents the operating results of our warehouse segment for the quarters ended December 31, 2017 and 2016.

Three Months ended December 31, | Change | ||||||||||||||||

2017 actual | 2017 constant currency(1) | 2016 actual | Actual | Constant currency | |||||||||||||

(Dollars in thousands) | |||||||||||||||||

Rent and storage | $ | 131,695 | $ | 131,817 | $ | 128,664 | 2.4 | % | 2.5 | % | |||||||

Warehouse services | 165,903 | 165,364 | 162,330 | 2.2 | % | 1.9 | % | ||||||||||

Total warehouse segment revenues | 297,598 | 297,181 | 290,994 | 2.3 | % | 2.1 | % | ||||||||||

Power | 16,939 | 16,957 | 16,975 | (0.2 | )% | (0.1 | )% | ||||||||||

Other facilities costs (2) | 26,878 | 26,930 | 24,423 | 10.1 | % | 10.3 | % | ||||||||||

Labor | 132,123 | 131,744 | 128,778 | 2.6 | % | 2.3 | % | ||||||||||

Other services costs (3) | 27,728 | 27,688 | 28,643 | (3.2 | )% | (3.3 | )% | ||||||||||

Total warehouse segment cost of operations | 203,668 | 203,319 | 198,819 | 2.4 | % | 2.3 | % | ||||||||||

Warehouse segment contribution (NOI) | $ | 93,930 | $ | 93,862 | $ | 92,175 | 1.9 | % | 1.8 | % | |||||||

Warehouse rent and storage contribution (NOI) (4) | $ | 87,878 | $ | 87,930 | $ | 87,266 | 0.7 | % | 0.8 | % | |||||||

Warehouse services contribution (NOI) (5) | $ | 6,052 | $ | 5,932 | $ | 4,909 | 23.3 | % | 20.8 | % | |||||||

Total warehouse segment margin | 31.6 | % | 31.6 | % | 31.7 | % | -10 bps | -10 bps | |||||||||

Rent and storage margin(6) | 66.7 | % | 66.7 | % | 67.8 | % | -110 bps | -110 bps | |||||||||

Warehouse services margin(7) | 3.6 | % | 3.6 | % | 3.0 | % | 60 bps | 60 bps | |||||||||

23

| ||

Financial Supplement | Fourth Quarter 2017 | |

(1) | The adjustments from our U.S. GAAP operating results to calculate our operating results on a constant currency basis are the effect of changes in foreign currency exchange rates relative to the comparable prior period. |

(2) | Includes real estate rent expense of $15.1 million and $16.7 million for the year ended December 31, 2017 and 2016, respectively. |

(3) | Includes non-real estate rent expense of $14.0 million and $12.0 million for the year ended December 31, 2017 and 2016, respectively. |

(4) | Calculated as rent and storage revenues less power and other facilities costs. |

(5) | Calculated as warehouse services revenues less labor and other services costs. |

(6) | Calculated as warehouse rent and storage contribution (NOI) divided by warehouse rent and storage revenues. |

(7) | Calculated as warehouse services contribution (NOI) divided by warehouse services revenues. |

24

| ||

Financial Supplement | Fourth Quarter 2017 | |

Same Store Analysis

The following table presents revenues, cost of operations, contribution (NOI) and margins for our same stores and non-same stores with a reconciliation to the total financial metrics of our warehouse segment for the year and the quarter ended December 31, 2017 and 2016.

Year ended December 31, | Change | ||||||||||||||||

2017 actual | 2017 constant currency(1) | 2016 actual | Actual | Constant currency | |||||||||||||

Same store revenues: | (Dollars in thousands) | ||||||||||||||||

Rent and storage | $ | 491,174 | $ | 490,725 | $ | 465,528 | 5.5 | % | 5.4 | % | |||||||

Warehouse services | 631,287 | 627,995 | 591,994 | 6.6 | % | 6.1 | % | ||||||||||

Total same store revenues | 1,122,461 | 1,118,720 | 1,057,522 | 6.1 | % | 5.8 | % | ||||||||||

Same store cost of operations: | |||||||||||||||||

Power | 70,101 | 70,076 | 68,974 | 1.6 | % | 1.6 | % | ||||||||||

Other facilities costs | 99,448 | 99,339 | 94,153 | 5.6 | % | 5.5 | % | ||||||||||

Labor | 498,978 | 496,689 | 473,325 | 5.4 | % | 4.9 | % | ||||||||||

Other services costs | 107,055 | 106,679 | 105,261 | 1.7 | % | 1.3 | % | ||||||||||

Total same store cost of operations | $ | 775,582 | $ | 772,783 | $ | 741,713 | 4.6 | % | 4.2 | % | |||||||

Same store contribution (NOI) | $ | 346,879 | $ | 345,937 | $ | 315,809 | 9.8 | % | 9.5 | % | |||||||

Same store rent and storage contribution (NOI)(2) | $ | 321,625 | $ | 321,310 | $ | 302,401 | 6.4 | % | 6.3 | % | |||||||

Same store services contribution (NOI)(3) | $ | 25,254 | $ | 24,627 | $ | 13,408 | 88.4 | % | 83.7 | % | |||||||

Total same store margin | 30.9 | % | 30.9 | % | 29.9 | % | 100 bps | 100 bps | |||||||||

Same store rent and storage margin(4) | 65.5 | % | 65.5 | % | 65.0 | % | 50 bps | 50 bps | |||||||||

Same store services margin(5) | 4.0 | % | 3.9 | % | 2.3 | % | 170 bps | 160 bps | |||||||||

Non-same store revenues: | |||||||||||||||||

Rent and storage | $ | 10,430 | $ | 10,443 | $ | 11,272 | (7.5 | )% | (7.4 | )% | |||||||

Warehouse services | 12,771 | 12,810 | 12,073 | 5.8 | % | 6.1 | % | ||||||||||

Total non-same store revenues | 23,201 | 23,253 | 23,345 | (0.6 | )% | (0.4 | )% | ||||||||||

Non-same store cost of operations: | |||||||||||||||||

Power | 2,307 | 2,300 | 3,025 | (23.7 | )% | (24.0 | )% | ||||||||||

Other facilities costs | 5,265 | 5,257 | 7,879 | (33.2 | )% | (33.3 | )% | ||||||||||

Labor | 10,973 | 11,026 | 11,497 | (4.6 | )% | (4.1 | )% | ||||||||||

Other services costs | 3,207 | 3,219 | 2,708 | 18.4 | % | 18.9 | % | ||||||||||

Total non-same store cost of operations | $ | 21,752 | $ | 21,802 | $ | 25,109 | (13.4 | )% | (13.2 | )% | |||||||

Non-same store contribution (NOI) | $ | 1,449 | $ | 1,451 | $ | (1,764 | ) | (182.1 | )% | (182.3 | )% | ||||||

Non-same store rent and storage contribution (NOI)(2) | $ | 2,858 | $ | 2,886 | $ | 368 | 676.6 | % | 684.2 | % | |||||||

Non-same store services contribution (NOI)(3) | $ | (1,409 | ) | $ | (1,435 | ) | $ | (2,132 | ) | (33.9 | )% | (32.7 | )% | ||||

Total warehouse segment revenues | $ | 1,145,662 | $ | 1,141,973 | $ | 1,080,867 | 6.0 | % | 5.7 | % | |||||||

Total warehouse cost of operations | $ | 797,334 | $ | 794,585 | $ | 766,822 | 4.0 | % | 3.6 | % | |||||||

Total warehouse segment contribution | $ | 348,328 | $ | 347,388 | $ | 314,045 | 10.9 | % | 10.6 | % | |||||||

(1) | The adjustments from our U.S. GAAP operating results to calculate our operating results on a constant currency basis is the effect of changes in foreign currency exchange rates relative to the comparable prior period. |

(2) | Calculated as rent and storage revenues less power and other facilities costs. |

(3) | Calculated as warehouse services revenues less labor and other services costs. |

(4) | Calculated as same store rent and storage contribution (NOI) divided by same store rent and storage revenues. |

(5) | Calculated as same store warehouse services contribution (NOI) divided by same store warehouse services revenues. |

25

| ||

Financial Supplement | Fourth Quarter 2017 | |

Quarter ended December 31, | Change | ||||||||||||||||

2017 actual | 2017 constant currency(1) | 2016 actual | Actual | Constant currency | |||||||||||||

Same store revenues: | (Dollars in thousands) | ||||||||||||||||

Rent and storage | $ | 128,825 | $ | 128,947 | $ | 126,323 | 2.0 | % | 2.1 | % | |||||||

Warehouse services | 162,633 | 162,093 | 159,556 | 1.9 | % | 1.6 | % | ||||||||||

Total same store revenues | 291,458 | 291,040 | 285,879 | 2.0 | % | 1.8 | % | ||||||||||

Same store cost of operations: | |||||||||||||||||

Power | 16,467 | 16,485 | 16,279 | 1.2 | % | 1.3 | % | ||||||||||

Other facilities costs | 25,416 | 25,468 | 22,946 | 10.8 | % | 11.0 | % | ||||||||||

Labor | 129,386 | 129,007 | 126,189 | 2.5 | % | 2.2 | % | ||||||||||

Other services costs | 26,955 | 26,915 | 28,187 | (4.4 | )% | (4.5 | )% | ||||||||||

Total same store cost of operations | $ | 198,224 | $ | 197,875 | $ | 193,601 | 2.4 | % | 2.2 | % | |||||||

Same store contribution (NOI) | $ | 93,234 | $ | 93,165 | $ | 92,278 | 1.0 | % | 1.0 | % | |||||||

Same store rent and storage contribution (NOI)(2) | $ | 86,942 | $ | 86,994 | $ | 87,098 | (0.2 | )% | (0.1 | )% | |||||||

Same store services contribution (NOI)(3) | $ | 6,292 | $ | 6,171 | $ | 5,180 | 21.5 | % | 19.1 | % | |||||||

Total same store margin | 32.0 | % | 32.0 | % | 32.3 | % | -30 bps | -30 bps | |||||||||

Same store rent and storage margin(4) | 67.5 | % | 67.5 | % | 68.9 | % | -140 bps | -140 bps | |||||||||

Same store services margin(5) | 3.9 | % | 3.8 | % | 3.2 | % | 70 bps | 60 bps | |||||||||

Non-same store revenues: | |||||||||||||||||

Rent and storage | $ | 2,870 | $ | 2,870 | $ | 2,341 | 22.6 | % | 22.6 | % | |||||||

Warehouse services | 3,270 | 3,271 | 2,774 | 17.9 | % | 17.9 | % | ||||||||||

Total non-same store revenues | 6,140 | 6,141 | 5,115 | 20.0 | % | 20.1 | % | ||||||||||

Non-same store cost of operations: | |||||||||||||||||

Power | 472 | 472 | 696 | (32.2 | )% | (32.2 | )% | ||||||||||

Other facilities costs | 1,462 | 1,462 | 1,477 | (1.0 | )% | (1.0 | )% | ||||||||||

Labor | 2,737 | 2,737 | 2,589 | 5.7 | % | 5.7 | % | ||||||||||

Other services costs | 773 | 773 | 456 | 69.5 | % | 69.5 | % | ||||||||||

Total non-same store cost of operations | $ | 5,444 | $ | 5,444 | $ | 5,218 | 4.3 | % | 4.3 | % | |||||||

Non-same store contribution (NOI) | $ | 696 | $ | 697 | $ | (103 | ) | (775.7 | )% | (776.7 | )% | ||||||

Non-same store rent and storage contribution (NOI)(2) | $ | 936 | $ | 936 | $ | 168 | 457.1 | % | 457.1 | % | |||||||

Non-same store services contribution (NOI)(3) | $ | (240 | ) | $ | (239 | ) | $ | (271 | ) | (11.4 | )% | (11.8 | )% | ||||

Total warehouse segment revenues | $ | 297,598 | $ | 297,181 | $ | 290,994 | 2.3 | % | 2.1 | % | |||||||

Total warehouse cost of operations | $ | 203,668 | $ | 203,319 | $ | 198,819 | 2.4 | % | 2.3 | % | |||||||

Total warehouse segment contribution | $ | 93,930 | $ | 93,862 | $ | 92,175 | 1.9 | % | 1.8 | % | |||||||

(1) | The adjustments from our U.S. GAAP operating results to calculate our operating results on a constant currency basis is the effect of changes in foreign currency exchange rates relative to the comparable prior period. |

(2) | Calculated as rent and storage revenues less power and other facilities costs. |

(3) | Calculated as warehouse services revenues less labor and other services costs. |

(4) | Calculated as same store rent and storage contribution (NOI) divided by same store rent and storage revenues. |

(5) | Calculated as same store warehouse services contribution (NOI) divided by same store warehouse services revenues. |

26

| ||

Financial Supplement | Fourth Quarter 2017 | |

Same-store Key Operating Metrics

The following table provides certain operating metrics to explain the drivers of our same store performance.

Year Ended December 31, | Change | |||||||||

Units in thousands except per pallet data | 2017 | 2016 | ||||||||

Same store rent and storage: | ||||||||||

Occupancy(1) | ||||||||||

Average occupied pallets | 2,447 | 2,414 | 1.4 | % | ||||||

Average physical pallet positions | 3,124 | 3,125 | — | % | ||||||

Occupancy percentage | 78.3 | % | 77.2 | % | 110 bps | |||||

Same store rent and storage revenues per occupied pallet | $ | 200.75 | $ | 192.87 | 4.1 | % | ||||

Constant currency same store rent and storage revenues per occupied pallet | $ | 200.56 | $ | 192.87 | 4.0 | % | ||||

Same store warehouse services: | ||||||||||

Throughput pallets | 27,038 | 26,562 | 1.8 | % | ||||||

Same store warehouse services revenues per throughput pallet | $ | 23.34 | $ | 22.29 | 4.7 | % | ||||

Constant currency same store warehouse services revenues per throughput pallet | $ | 23.22 | $ | 22.29 | 4.2 | % | ||||

Non-same store rent and storage: | ||||||||||

Occupancy | ||||||||||

Average occupied pallets | 62 | 56 | 9.6 | % | ||||||

Average physical pallet positions | 91 | 106 | (14.3 | )% | ||||||