Attached files

| file | filename |

|---|---|

| EX-23.5 - EX-23.5 - ConvergeOne Holdings, Inc. | d507706dex235.htm |

| EX-23.4 - EX-23.4 - ConvergeOne Holdings, Inc. | d507706dex234.htm |

| EX-23.3 - EX-23.3 - ConvergeOne Holdings, Inc. | d507706dex233.htm |

| EX-23.2 - EX-23.2 - ConvergeOne Holdings, Inc. | d507706dex232.htm |

| EX-4.3 - EX-4.3 - ConvergeOne Holdings, Inc. | d507706dex43.htm |

Table of Contents

As filed with the U.S. Securities and Exchange Commission on March 22, 2018

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

ConvergeOne Holdings, Inc.

(Exact name of registrant as specified in our charter)

| Delaware | 7372 | 81-4619427 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

3344 Highway 149

Eagan, MN 55121

(888) 321-6227

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

John A. McKenna, Jr.

President and Chief Executive Officer,

and Chairman of the Board

ConvergeOne Holdings, Inc.

3344 Highway 149

Eagan, MN 55121

(888) 321-6227

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Mehdi Khodadad

John T. McKenna

Alan Hambelton

Cooley LLP

3175 Hanover Street

Palo Alto, CA 94304

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer |

☐ |

Accelerated filer | ☐ | |||||

| Non-accelerated filer |

☒ |

(Do not check if a smaller reporting company) | Smaller reporting company | ☐ | ||||

| Emerging growth company |

☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

Calculation of Registration Fee

|

| ||||||||

| Title of Each Class of Securities to be Registered |

Amount to be Registered(1) |

Proposed Maximum Offering Price Per Security |

Proposed Maximum Aggregate Offering Price |

Amount of Registration Fee | ||||

| Common stock, $0.0001 par value per share |

22,189,750 | $ 8.545(2) | $189,611,414 | $23,607 | ||||

| Warrants to purchase common stock |

311,250 | $ 0.955(3) | — (5) | — (5) | ||||

| Common stock, $0.0001 par value per share, underlying the Warrants |

8,936,249 | $12.455(4) | $111,300,982 | $13,857 | ||||

| Total |

$300,912,396 | $37,464 | ||||||

|

| ||||||||

|

| ||||||||

| (1) | In the event of a stock split, stock dividend or other similar transaction involving the registrant’s common stock, in order to prevent dilution, the number of shares of common stock registered hereby shall be automatically increased to cover the additional common shares in accordance with Rule 416(a) under the Securities Act. |

| (2) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(c) under the Securities Act. The price per share and aggregate offering price are based on the average of the high and low prices of the Registrant’s common stock on March 16, 2018, as reported on the Nasdaq Capital Market. |

| (3) | Estimated in accordance with Rule 457(c) under the Securities Act. The price per share is based on the average of the high and low prices of the Registrant’s warrants on March 16, 2018, as reported on the Nasdaq Capital Market. |

| (4) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(i) under the Securities Act. The price per share is based upon (a) the exercise price per warrant of $11.50 per share plus (b) the average of the high and low prices of the Registrant’s warrants on March 16, 2018 as reported on the Nasdaq Capital Market. |

| (5) | No separate fee due in accordance with Rule 457(i). |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. The selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, Dated March 22, 2018

PRELIMINARY PROSPECTUS

30,814,749 Shares of Common Stock

311,250 Warrants to Purchase Common Stock

The selling stockholders named in this prospectus (the “Selling Stockholders”) may offer and sell from time to time up to 22,189,750 shares of our common stock, par value $0.0001 per share, and warrants to purchase up to 311,250 shares of common stock, consisting of:

| • | up to 17,959,375 shares of common stock issued in a private placement pursuant to subscription agreements entered into on November 30, 2017 (the “PIPE Shares”); |

| • | up to 3,919,125 shares of common stock (the “Founders Shares”) issued in a private placement to Forum Investors I, LLC (the “Sponsor”) and subsequently distributed to the Sponsor’s members; |

| • | up to 311,250 warrants to purchase shares of common stock issued in a private placement to the Sponsor (the “Placement Warrants”) and subsequently distributed to the Sponsor’s members; and |

| • | up to 311,250 shares of common stock issuable upon exercise of the Placement Warrants. |

In addition, this prospectus relates to the offer and sale of up to 8,624,999 shares of common stock that are issuable by us upon the exercise of outstanding warrants that were previously registered (the “Public Warrants”).

The selling stockholders may offer, sell or distribute all or a portion of the securities hereby registered publicly or through private transactions at prevailing market prices or at negotiated prices. We will not receive any of the proceeds from such sales of the shares of common stock or warrants, except with respect to amounts received by us upon the exercise of the warrants. We will bear all costs, expenses and fees in connection with the registration of these securities, including with regard to compliance with state securities or “blue sky” laws. The selling stockholders will bear all commissions and discounts, if any, attributable to their sale of shares of common stock or warrants. See “Plan of Distribution” beginning on page 104 of this prospectus.

We are an “emerging growth company” as defined in Section 2(a) of the Securities Act of 1933, as amended, and are subject to reduced public company reporting requirements. This prospectus complies with the requirements that apply to an issuer that is an emerging growth company.

Our common stock and warrants are listed on the Nasdaq Capital Market under the symbols “CVON” and “CVONW”, respectively. On March 21, 2018, the last reported sales price of our common stock was $8.73 per share and the last reported sales price of our warrants was $0.96 per warrant.

Investing in our securities involves a high degree of risk. You should review carefully the risks and uncertainties described under the heading “Risk Factors” beginning on page 5 of this prospectus, and under similar headings in any amendment or supplements to this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

, 2018

Table of Contents

You should rely only on the information contained in this prospectus, any supplement to this prospectus or in any free writing prospectus, filed with the Securities and Exchange Commission. Neither we nor the selling stockholders have authorized anyone to provide you with additional information or information different from that contained in this prospectus filed with the Securities and Exchange Commission. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. The selling stockholders are offering to sell, and seeking offers to buy, our securities only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of our securities. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside the United States: Neither we nor the selling stockholders, have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of our securities and the distribution of this prospectus outside the United States.

To the extent there is a conflict between the information contained in this prospectus, on the one hand, and the information contained in any document incorporated by reference filed with the Securities and Exchange Commission before the date of this prospectus, on the other hand, you should rely on the information in this prospectus. If any statement in a document incorporated by reference is inconsistent with a statement in another document incorporated by reference having a later date, the statement in the document having the later date modifies or supersedes the earlier statement.

i

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements provide our current expectations or forecasts of future events. Forward-looking statements include statements about our expectations, beliefs, plans, objectives, intentions, assumptions and other statements that are not historical facts. The words “anticipates,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predicts,” “project,” “should,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this prospectus include, but are not limited to, statements about our:

| • | ability to grow and retain our client base; |

| • | ability to provide effective client support and induce our clients to renew and upgrade the technology offerings and services we provide for them; |

| • | ability to expand our sales organization to address effectively existing and new markets that we intend to target; |

| • | ability to forecast and maintain an adequate rate of revenue growth and appropriately plan our expenses; |

| • | expectations regarding future expenditures; |

| • | future mix of revenue and effect on gross margins; |

| • | attraction and retention of qualified employees and key personnel; |

| • | ability to compete effectively in a competitive industry; |

| • | ability to protect and enhance our corporate reputation and brand; |

| • | expectations concerning our relationships and actions with our technology partners and other third parties; |

| • | impact from future regulatory, judicial, and legislative changes in our industry; |

| • | ability to locate and acquire complementary technologies or services and integrate those into our business; and |

| • | future arrangements with, or investments in, other entities or associations. |

These forward-looking statements are based on information available as of the date of this prospectus, and current expectations, forecasts and assumptions, and involve a number of risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing our views as of any subsequent date, and we do not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

In addition, statements that we “believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to such party as of the date of this prospectus, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and these statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain and investors are cautioned not to unduly rely upon these statements.

You should not place undue reliance on these forward-looking statements. As a result of a number of known and unknown risks and uncertainties, our actual results or performance may be materially different from those expressed or implied by these forward-looking statements.

ii

Table of Contents

In this document:

“Business Combination” means the business combination between C1 Investment Corp. and Forum Merger Corporation, consummated on February 22, 2018.

“C1” means C1 Investment Corp.

“Clearlake” means Clearlake Capital Group, L.P., together with its affiliates and related persons.

“Forum” means Forum Merger Corporation.

“Forum IPO” means Forum’s initial public offering.

“Founders Shares” means Class F common stock purchased by Sponsor on December 28, 2016 which, upon the closing of the Business Combination, converted on a one-for-one basis into common stock.

“Merger Agreement” means the Merger Agreement, dated as of November 30, 2017, by and among Forum Merger Corporation, FMC Merger Subsidiary Corp., FMC Merger Subsidiary LLC, C1 Investment Corp. and Clearlake Capital Management III, L.P.

“PIPE Investment” refers to the sale of shares of common stock in a private placement whereby certain investors committed to purchase 17,959,375 shares of common stock for an aggregate purchase price of $143,675,000.

“PIPE Shares” means the shares of common stock sold in the PIPE Investment.

“Placement Warrants” means warrants to purchase shares of common stock issued in a private placement to Sponsor and subsequently distributed to the Sponsor’s members.

“Sponsor” means Forum Investors I, LLC.

“warrants” means the “Placement Warrants” and the “Public Warrants.”

1

Table of Contents

The following summary highlights selected information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common stock, you should carefully read this entire prospectus, including our financial statements and the related notes included in this prospectus and the information set forth under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The “Company,” “ConvergeOne” “we,” “our,” “us” or similar terms mean ConvergeOne Holdings, Inc. and our consolidated subsidiaries.

General

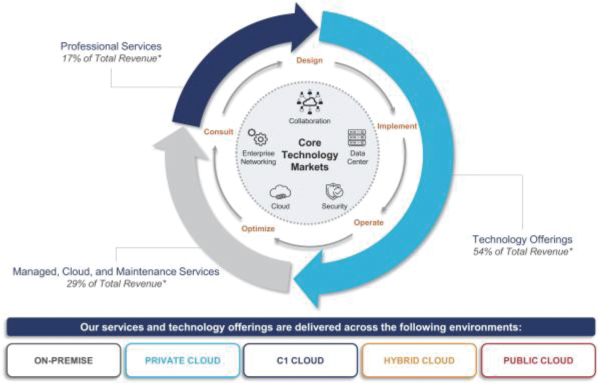

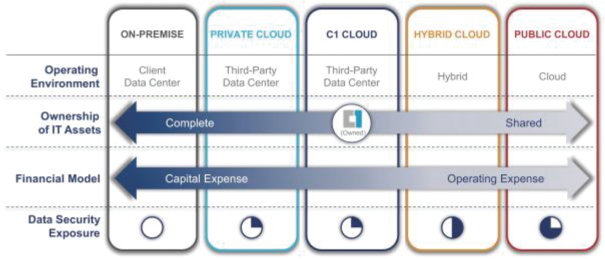

We are a leading IT services provider of collaboration and technology solutions for large and medium enterprises. We serve clients through our comprehensive engagement model which includes the full lifecycle of services from consultation and design through implementation, optimization, and ongoing support. Approximately 46% and 51% of our total revenue in 2016 and 2017, respectively, was derived from our services offerings, which include professional and managed, cloud, and maintenance services. Our deep technical expertise enables us to deliver complex, multi-vendor solutions across a number of delivery models, including on-premise and in private, hybrid, C1 Cloud, and public cloud environments. We served over 3,400, 3,700, and 7,200 clients in 2015, 2016, and 2017, respectively, which includes clients served in 2017 by companies we acquired in 2017. From 2015 to 2017, we served 57% of the Fortune 100, 43% of the Fortune 500, and 36% of the Fortune 1000, which includes clients served in the same period by companies we acquired in 2017.

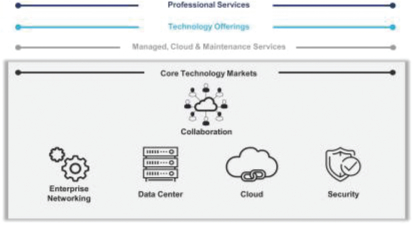

Through our leading professional services capabilities, we design thousands of solutions each year across our core technology markets: (i) collaboration and (ii) enterprise networking, data center, cloud, and security, each of which is complemented by our industry-leading managed, cloud, and maintenance services. Managed, cloud, and maintenance services typically have multi-year contractual terms with high renewal rates and accounted for 29% and 33% of our total revenue in 2016 and 2017, respectively. Through our relationships with more than 300 leading and next-generation technology partners, our engineers deliver optimal services and solutions to clients regardless of their existing infrastructure.

Collaboration technology is essential to modern business, enabling workforce mobility and driving globalization through connectivity across any device. Collaboration solutions create significant competitive advantages through enhanced productivity, innovative ways of working together, and omni-channel customer engagement models. With our more than 20-year focus on collaboration solutions, we believe we will benefit from the rapid growth of this market. We derived approximately 68% and 66% of our total revenue in 2016 and 2017, respectively, from our services and technology offerings in the collaboration market.

Our technical expertise and client-centric culture have led to long-standing and expanding client relationships. Our top 100 clients, based on 2017 revenue, excluding the impact of our 2017 acquisitions, had an average tenure of more than nine years. We generated 91% and 93% of our total revenue in 2016 and 2017, respectively, from clients we served in a prior year, excluding the impact of our 2017 acquisitions. Our Net Promoter Score (“NPS”) of 61 in 2016 was more than twice the technology vendor industry average of 30. NPS is a commonly used industry measure of customers’ overall satisfaction. According to this third-party survey, 86% of our clients indicated that they are “highly likely” to recommend us to other businesses and organizations.

Corporate Information

We were incorporated in Delaware in November 2016 as a blank check company under the name Forum Merger Corporation. Our principal executive offices are located at 3344 Highway 149, Eagan, Minnesota 55121, and our telephone number is (888) 321-6227. Our corporate website address is www.convergeone.com. Information contained on or accessible through our website is not a part of this prospectus, and the inclusion of our website address in this prospectus is an inactive textual reference only.

2

Table of Contents

On February 22, 2018, C1 Investment Corp. and Forum consummated the transactions contemplated by the Agreement and Plan of Merger, dated November 30, 2017, following the approval at the special meeting of the stockholders of Forum held on February 20, 2018. In connection with the closing of the Business Combination, we changed our name from Forum Merger Corporation to ConvergeOne Holdings, Inc.

ConvergeOne is a trademark of ConvergeOne, Inc., our wholly-owned subsidiary. The ConvergeOne logos are trademarks of ConvergeOne Holdings Corp., our wholly-owned subsidiary. We do not intend our use or display of other companies’ trade names or trademarks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

3

Table of Contents

The Offering

| Securities offered by the selling stockholders |

We are registering the resale by the selling stockholders named in this prospectus, or their permitted transferees, of an aggregate of 22,189,750 shares of common stock and warrants to purchase 311,250 shares of common stock, which includes: |

| • | up to 17,959,375 PIPE Shares; |

| • | up to 3,919,125 Founders Shares; and |

| • | up to 311,250 shares of common stock issuable upon exercise of the Placement Warrants. |

| In addition, we are registering 8,624,999 shares of common stock issuable upon exercise of the Public Warrants that were previously registered. |

| Sponsor Earnout Letter and Lock-Up Letter |

An aggregate of 2,156,250 of the Founder Shares are subject to forfeiture in the event that the Earnout Payments are not achieved, and may not be sold until such time. Such shares are also subject to 180-day lock-up agreement; provided, that if the volume-weighted average price of our common stock for 15 trading days is at least $12.50 per share, then 25% of such shares will be released from the lock-up agreement, but will remain subject to forfeiture and may not be sold. See the section titled “Certain Relationships and Related Person Transactions—Sponsor Earnout Letter and Lock-Up Letter” |

Terms of the offering

| The selling stockholders will determine when and how they will dispose of the shares of common stock and warrants registered under this prospectus for resale. |

| Shares outstanding prior to the offering |

As of March 1, 2018, we had 69,700,001 shares of common stock issued and outstanding. |

| Shares outstanding after the offering |

78,636,250 shares of common stock (assuming the exercise for cash of warrants to purchase 8,936,249 shares of common stock). |

| Use of proceeds |

We will not receive any of the proceeds from the sale of the warrants or shares of common stock by the selling stockholders except with respect to amounts received by us due to the exercise of the warrants. We expect to use the proceeds received from the exercise of the warrants, if any, for working capital and general corporate purposes. |

| Nasdaq ticker symbol |

Our common stock and warrants are listed on the Nasdaq Capital Market under the symbols “CVON” and “CVONW”, respectively. |

For additional information concerning the offering, see “Plan of Distribution” beginning on page 104.

4

Table of Contents

Investing in our securities involves a high degree of risk. You should consider carefully the risks and uncertainties described below, together with all of the other information in this prospectus, including our consolidated financial statements and related notes, before deciding whether to purchase any of our securities. If any of these risks actually occur, it could harm our business, financial condition, results of operations and cash flows and our prospects. In that event, the price of our securities could decline and you could lose part or all of your investment.

Risks Related to Our Business and Industry

Our results of operations and ability to grow could be negatively affected if we cannot adapt and expand our technology offerings and services in response to ongoing market changes.

The collaboration and technology solutions business and markets are characterized by rapid technological change, evolving industry standards, changing client preferences, and new product and service introductions. Our success depends on our ability to continue to develop and implement technology offerings and services that anticipate or timely respond to rapid and continuing changes in technology and industry developments and offerings by new technology providers to serve the evolving needs of our clients. Examples of areas of significant change in the industry include cloud, software-defined infrastructure, virtualization, security, mobility, data analytics, and Internet of Things, or IoT, the continued shift from maintenance to managed services and ultimately to cloud-based services, as-a-service solutions, security, and information technology automation. In addition, enterprises are continuing to shift from on-premise, hardware infrastructure to software-centric hosted solutions. Technological developments such as these may materially affect the cost and use of technology and services by our clients and could affect the nature of how our revenue is generated. These technologies, and others that may emerge, could reduce and, over time, replace some of our current business. In addition, clients may delay spending under existing contracts and engagements and may delay entering into new contracts while they evaluate new technologies. If we do not sufficiently invest in new technology, industry developments, and our personnel, or evolve and expand our business at sufficient speed and scale, or if we do not make the right strategic investments to respond to these developments and successfully drive innovation, our technology offerings and services, our results of operations, and our ability to develop and maintain a competitive advantage and to continue to grow could be negatively affected.

In addition, if we are unable to keep up with changes in technology and new hardware, software, and services offerings, for example, by providing the appropriate training to our account managers, sales technology specialists, engineers, and consultants to enable them to effectively sell and deliver such new offerings to clients, our business, results of operations, or financial condition could be adversely affected.

Our business depends on our technology partner relationships and the availability of their products.

We have relationships with over 100 technology partners, including Avaya, Cisco, Dell, IBM, Interactive Intelligence, and Microsoft. Our business depends on the sale and installation of a variety of hardware and software that we purchase for resale from technology partners, which include original equipment manufacturers, or OEMs, software publishers, and wholesale distributors. We are authorized by our technology partners to sell all or some of their technology offerings via direct marketing activities. Our authorization with each technology partner is subject to specific terms and conditions regarding but not limited to, sales channel restrictions, product return privileges, price protection policies, purchase discounts, and technology partner programs and funding, including purchase rebates, sales volume rebates, purchasing incentives, and cooperative advertising reimbursements. However, we do not have long-term contracts with many of our technology partners and many of these arrangements are terminable upon notice by either party. Material changes to the agreements with our technology partners, including changes to purchase discounts and rebate programs, or our failure to timely react to such changes, could have an adverse effect on our business, results of operations, or financial condition.

The priorities and objectives of our partners may differ from ours. As most of our relationships are non-exclusive, our partners are not prohibited from competing with us or forming closer or preferred

5

Table of Contents

arrangements with our competitors. From time to time, technology partners may terminate or limit our right to sell some or all of their technology offerings or change the terms and conditions or reduce or discontinue the incentives that they offer us. For example, there is no assurance that, as our technology partners continue to sell directly to customers and through resellers, they will not limit or curtail the availability of their products to solutions providers like us. Any such termination or limitation or the implementation of such changes could have a negative impact on our business, results of operations, or financial condition.

In addition, our success is dependent on our ability to develop relationships with and sell hardware, software, and services from new emerging vendors, including vendors that we have not historically represented in the marketplace. To the extent that a vendor’s offering that is highly in demand is not available to us to provide in one or more client channels, and there is not a competitive offering from another vendor that we are authorized to sell in such client channels, or we are unable to develop relationships with new technology providers or companies that we have not historically represented, our business, results of operations, or financial condition could be adversely impacted.

In addition, the termination of key technology partner relationships as a result of the sale, spin-off, combination, bankruptcy, or other similar circumstances of any of our technology partners and/or certain of their business units, including any such sale to or combination with a vendor with whom we do not currently have a commercial relationship or whose products we do not sell, could have an adverse impact on our business, results of operations, or financial condition.

We rely on a small number of key vendors for a significant portion of our technology offerings revenue.

Although we purchase from a diverse vendor base, in 2017, products manufactured by Avaya and Cisco represented 21% and 39%, respectively, of our technology offerings revenue. The loss of, or change in business relationship with, either of these or any other key technology partners, the diminished availability or quality of their products, or backlogs for their products leading to manufacturer allocation, could reduce the supply and increase the cost of products we sell and negatively impact our competitive position. In addition, we rely on one distributor that supplies a significant portion of our Avaya products and the termination of this distributor relationship could negatively impact our business.

Avaya, which was our largest vendor as a percentage of our technology offerings revenue in 2015 and 2016, filed for reorganization under Chapter 11 in January 2017, filed its preliminary plan of reorganization in April 2017 and had its Chapter 11 plan of reorganization approved by the Bankruptcy Court in November 2017. As a result of Avaya’s restructuring, new or existing clients may elect to delay purchasing decisions with respect to Avaya technology offerings or may choose to replace existing Avaya technology offerings with the technology offerings of other vendors. Although we have partner relationships with a diverse vendor base, new or existing clients may elect to purchase such alternative technology offerings from a provider other than us or such alternative technology offerings may have lower margins. Delays in customer purchasing decisions, or an election by our clients to purchase alternative technology offerings from us or from other providers, could result in lower revenues and gross profits or margins or otherwise have an adverse effect on our business, although we cannot estimate the impact at this time.

If we are unable to expand or renew sales to existing clients, or attract new clients, our growth could be slower than we expect and our business may be harmed.

Our future growth depends upon expanding sales and renewals of our technology offerings and services with existing clients. Our clients may not purchase our technology offerings and services, or our clients may reduce their purchasing volumes, if we do not demonstrate the value proposition for their investment, and we may not be able to replace existing clients with new clients. In addition, our clients may not renew their contracts with us on the same terms, or at all, because of dissatisfaction with our service. If our clients do not renew their contracts, our revenue may grow more slowly than expected, may not grow at all, or may decline. Additionally, increasing incremental sales to our current client base may require increasingly sophisticated and costly sales efforts that are targeted at senior management. We plan to continue expanding our sales efforts but we may be

6

Table of Contents

unable to hire qualified sales personnel, may be unable to successfully train those sales personnel that we are able to hire, and sales personnel may not become fully productive on the timelines that we have projected, or at all. Additionally, although we dedicate significant resources to sales and marketing programs, these sales and marketing programs may not have the desired effect and may not expand sales. We cannot assure you that our efforts will increase sales to existing clients or additional revenue. If our efforts to upsell to our clients are not successful, our future growth may be limited.

Our ability to achieve significant growth in revenue in the future will also depend upon our ability to attract new clients. This may be particularly challenging where an organization has already invested substantial personnel and financial resources to integrate competing technology offerings and services into its business, as such organization may be reluctant or unwilling to invest in new technology offerings and services. If we fail to attract new clients and maintain and expand those client relationships, our revenue may grow more slowly than expected and our business may be harmed.

Demand for our technology offerings and services could be adversely affected by volatile, negative, or uncertain economic conditions and the effects of these conditions on our clients’ businesses.

Our revenue and profitability depend on the demand for our technology offerings and services, which could be negatively affected by numerous factors, many of which are beyond our control. Volatile, negative, or uncertain economic conditions affect our clients’ businesses and the markets we serve. Such economic conditions in our markets have undermined, and could in the future undermine, business confidence in our markets and cause our clients to reduce or defer their spending on new technology offerings and services, or may result in clients reducing, delaying or eliminating spending under existing contracts with us, which would negatively affect our business. Growth in the markets we serve could be at a slow rate, or could stagnate or contract, in each case for an extended period of time. Ongoing economic volatility and uncertainty and changing demand patterns affect our business in a number of other ways, including making it more difficult to accurately forecast client demand and effectively build our revenue and resource plans.

Economic volatility and uncertainty is particularly challenging because it may take some time for the effects and changes in demand patterns resulting from these and other factors to manifest themselves in our business and results of operations. Changing demand patterns from economic volatility and uncertainty could have a significant negative impact on our business, results of operations, or financial condition.

Substantial competition could reduce our market share and significantly harm our financial performance.

Our current competition includes:

| • | in-house IT departments; |

| • | global service providers and integrators; |

| • | local and regional providers; |

| • | resellers; and |

| • | equipment manufacturers. |

We expect the competitive landscape in which we compete to continue to change as new technologies are developed. While innovation can help our business as it creates new offerings for us to sell and provide complementary services, it can also disrupt our business model and create new and stronger competitors. For instance, while cloud-based solutions present an opportunity for us, cloud-based solutions and technologies that deliver technology solutions as a service could increase the amount of sales directly to clients rather than through solutions providers like us, or could reduce the amount of hardware we sell, leading to a reduction in our technology offerings revenue and/or profitability. In addition, some of our hardware and software technology partners sell, and could intensify their efforts to sell, their products directly to our clients. Moreover, traditional

7

Table of Contents

OEMs have increased their services capabilities through mergers and acquisitions with service providers, which could potentially increase competition in the market to provide comprehensive technology solutions to clients. If any of these trends becomes more prevalent, it could adversely affect our business, results of operations, or financial condition.

We focus on offering a high level of service to gain new clients and retain existing clients. To the extent we face increased competition to gain and retain clients, we may be required to reduce prices, increase advertising expenditures, or take other actions that could adversely affect our business, results of operations, or financial condition. Additionally, some of our competitors may reduce their prices in an attempt to stimulate sales, which may require us to reduce prices. This would require us to sell a greater number of products and services to achieve the same level of revenue and gross profit. If such a reduction in prices occurs and we are unable to attract new clients and sell increased quantities of products and services, our sales growth and profitability could be adversely affected.

Our future results will depend on our ability to continue to focus our resources and manage costs effectively.

We are continually implementing productivity measures and focusing on measures intended to further improve cost efficiency. We may be unable to realize all expected cost savings in connection with these efforts within the expected time frame, or at all, and we may incur additional and/or unexpected costs to realize them. Further, we may not be able to sustain any achieved savings in the future. Future results will depend on the success of these efforts.

If we are unable to control costs, we may incur losses, which could decrease our operating margins and significantly reduce or eliminate our profits. Our future profitability will depend on our ability to manage costs or increase productivity. An inability to effectively manage costs could adversely impact our business, results of operations, or financial condition.

Our profitability could suffer if we are not able to manage large and complex projects and complete fixed-price, fixed-timeframe contracts on budget and on time.

Our profitability and operating results are dependent on the scale of our projects and the prices we are able to charge for our technology offerings and services. We perform a significant portion of our work through fixed-price contracts, in which we assume full control of the project team and manage all facets of execution. As a significant portion of our projects are on a fixed-price model, we may be unable to accurately estimate the appropriate project price and successfully manage such projects. Although we use specified technical processes and our past experience to reduce the risks associated with estimating, planning, and performing fixed-price and fixed-timeframe projects, we face the risk of cost overruns, completion delays, and wage inflation in connection with these projects. If we fail to accurately estimate the resources or time required for a project or future rates of wage inflation, or if we fail to perform contractual obligations within the contractual timeframe, our profitability could suffer.

The challenges of managing larger and more complex projects include:

| • | maintaining high-quality control and process execution standards; |

| • | maintaining planned resource utilization rates on a consistent basis; |

| • | maintaining productivity levels and implementing necessary process improvements; |

| • | controlling project costs; |

| • | maintaining close client contact and high levels of client satisfaction; |

| • | recruiting and retaining sufficient numbers of skilled IT professionals; and |

| • | maintaining effective client relationships. |

8

Table of Contents

In addition, large and complex projects may involve multiple engagements or stages, and there is a risk that a client may choose not to retain us for additional stages or may cancel or delay additional planned engagements. Such cancellations or delays may make it difficult to plan our project resource requirements, and may result in lower profitability levels than we anticipated upon commencing engagements.

Our investments in new services and technologies may not be successful.

We continue to invest in new services and technologies, including cloud, software-defined infrastructure, virtualization, security, mobility, data analytics, and IoT. The complexity of these solutions, our learning curve in developing and supporting them, and significant competition in the markets for these solutions could make it difficult for us to market and implement these solutions successfully. Additionally, there is a risk that our clients may not adopt these solutions widely, which would prevent us from realizing expected returns on these investments. Even if these solutions are successful in the market, they still rely on third-party hardware and software and our ability to meet stringent service levels. If we are unable to deploy these solutions successfully or profitably, it could adversely impact our business, results of operations, or financial condition.

If we lose any of our key personnel, or are unable to attract and retain the talent required for our business, our business could be disrupted and our financial performance could suffer.

Our success is heavily dependent upon our ability to attract, develop, engage, and retain key personnel to manage and grow our business, including our key executive, management, sales, services, and technical personnel.

Our future success will depend to a significant extent on the efforts of our executive officers: John A. McKenna, Jr., our President, Chief Executive Officer and Chairman of the Board; John F. Lyons, our President, Field Organization; Paul K. Maier, our President, Services Organization; and Jeffrey E. Nachbor, our Chief Financial Officer, as well as the continued service and support of other key employees. Our future success also will depend on our ability to attract and retain highly skilled technology specialists, engineers, and consultants, for whom the market is extremely competitive. All of our officers and key employees are at-will employees, meaning that they can terminate their employment with us at any time. Further, we do not maintain “key man” life insurance policies for any of our officers or key employees.

Our inability to attract, develop, and retain key personnel could have an adverse effect on our relationships with our technology partners and clients and adversely affect our ability to expand our offerings of technology offerings and services. Moreover, our inability to train our sales, services, and technical personnel effectively to meet the rapidly changing technology needs of our clients could cause a decrease in the overall quality and efficiency of such personnel. Such consequences could adversely affect our business, results of operations, or financial condition.

Our ability to attract and retain business and personnel may depend on our reputation in the marketplace.

We believe our brand name and our reputation in the marketplace are important corporate assets that help distinguish our technology offerings and services from those of competitors and also contribute to our ability to recruit and retain talented personnel, in particular our engineers and consulting professionals. However, our corporate reputation is potentially susceptible to material damage by events such as disputes with clients, cybersecurity breaches, service outages, internal control deficiencies, delivery failures, or compliance violations. Similarly, our reputation could be damaged by actions or statements of current or former clients, directors, employees, competitors, vendors, partners, our joint ventures or joint venture partners, adversaries in legal proceedings, legislators, or government regulators, as well as members of the investment community or the media. There is a risk that negative information about us, even if based on rumor or misunderstanding, could adversely affect our business. Damage to our reputation could be difficult, expensive and time-consuming to repair, could make potential or existing clients reluctant to select us for new engagements, resulting in a loss of business, and could adversely affect our recruitment and retention efforts. Damage to our reputation could also reduce the value and effectiveness of our brand name and could reduce investor confidence in us, adversely affecting our share price.

9

Table of Contents

We have experienced rapid internal growth as well as growth through acquisitions in recent periods. If we fail to manage our growth effectively, or our business does not grow as expected, our operating results may suffer.

Our headcount and operations have grown substantially. We had approximately 2,185 employees as of December 31, 2017, as compared with approximately 1,349 employees as of December 31, 2015. This growth has placed, and will continue to place, a significant strain on our operational, financial, and management infrastructure. We anticipate further increases in headcount will be required to support increases in our technology offerings and continued expansion. To manage this growth effectively, we must continue to improve our operational, financial, and management systems and controls by, among other things:

| • | effectively attracting, training, and integrating a large number of new employees, particularly technical personnel and members of our management and sales teams; |

| • | further improving our key business systems, processes, and information technology infrastructure to support our business needs; |

| • | enhancing our information and communication systems to ensure that our employees are well-coordinated and can effectively communicate with each other and our clients; and |

| • | improving our internal control over financial reporting and disclosure controls and procedures to ensure timely and accurate reporting of our operational and financial results. |

If we fail to manage our expansion or implement our new systems, or if we fail to implement improvements or maintain effective internal controls and procedures, our costs and expenses may increase more than expected and we may not expand our client base, increase renewal rates, enhance our existing applications, develop new applications, satisfy our clients, respond to competitive pressures, or otherwise execute our business plan. If we are unable to manage our growth, our operating results likely will be harmed.

Future acquisitions could disrupt our business and may divert management’s attention, and if unsuccessful, harm our business.

We may choose to expand by making additional acquisitions that could be material to our business. We have in the past made several acquisitions of complementary businesses, including Arrow Systems Integration, Inc., in 2018, RGTS, Strategic Products and Services, Annese & Associates, Inc. and AOS in 2017 and SIGMAnet, MSN Communications, and Sunturn in 2015. Acquisitions involve many risks, including the following:

| • | an acquisition may negatively affect our results of operations and financial condition because it may require us to incur charges or assume substantial debt or other liabilities, may cause adverse tax consequences or unfavorable accounting treatment, may expose us to claims and disputes by third parties, including intellectual property claims and disputes, or may not generate sufficient financial return to offset additional costs and expenses related to the acquisition; |

| • | we may encounter difficulties or unforeseen expenditures in integrating the business, technologies, products, personnel, or operations of any company that we acquire, particularly if key personnel of the acquired company decide not to work for us; |

| • | an acquisition may disrupt our ongoing business, divert resources, increase our expenses, or distract our management; |

| • | an acquisition may result in a delay or reduction of client purchases for both us and the company we acquired due to client uncertainty about continuity and effectiveness of service from either company; |

| • | we may encounter difficulties in, or may be unable to, successfully sell any acquired technology offerings or services; |

10

Table of Contents

| • | an acquisition may involve the entry into geographic or business markets in which we have little or no prior experience or where competitors have stronger market positions; |

| • | the challenges inherent in effectively managing an increased number of employees in diverse locations; |

| • | the potential strain on our financial and managerial controls and reporting systems and procedures; |

| • | the potential known and unknown liabilities associated with an acquired company; |

| • | our use of cash to pay for acquisitions would limit other potential uses for our cash; |

| • | if we incur additional debt to fund such acquisitions, such debt may subject us to additional material restrictions on our ability to conduct our business as well as additional financial maintenance covenants; |

| • | the risk of impairment charges related to potential write-downs of acquired assets or goodwill in future acquisitions; |

| • | to the extent that we issue a significant amount of equity or equity-linked securities in connection with future acquisitions, existing stockholders may be diluted and earnings per share may decrease; and |

| • | managing the varying intellectual property protection strategies and other activities of an acquired company. |

We may not succeed in addressing these or other risks or any other problems encountered in connection with the integration of any acquired business. The inability to integrate successfully the business, technologies, products, personnel, or operations of any acquired business, or any significant delay in achieving integration, could harm our business, results of operations, or financial condition.

We may not be able to recognize revenue in the period in which our services are performed, which may cause our margins to fluctuate.

Our services are performed under both time-and-material and fixed-price contract arrangements. All revenue is recognized pursuant to applicable accounting standards. We recognize revenue from professional services, which includes the design, configuration, installation, and integration of business communication and data systems, as the services are performed and all obligations have been substantially met. Our failure to meet all the obligations, or otherwise meet a client’s expectations, may result in our having to record the cost related to the performance of services in the period that services were rendered, but delay the timing of revenue recognition to a future period in which all obligations have been met.

We may experience quarterly fluctuations in our operating results due to a number of factors, which makes our future results difficult to predict and could cause our operating results to fall below expectations.

Our quarterly operating results have fluctuated in the past and we expect them to fluctuate in the future due to a variety of factors, many of which are outside of our control. As a result, our past results may not be indicative of our future performance, and comparing our operating results on a period-to-period basis may not be meaningful. In addition to the other risks described herein, factors that may affect our quarterly operating results include:

| • | changes in spending on collaboration and technology offerings and services by our current or prospective clients; |

| • | pricing our technology offerings and services effectively so that we are able to attract and retain clients without compromising our operating results; |

| • | attracting new clients and increasing our existing clients’ use of our technology offerings and services; |

| • | the mix between wholesale and retail maintenance new contracts and renewals; |

11

Table of Contents

| • | client renewal rates and the amounts for which agreements are renewed; |

| • | seasonality and its effect on client demand; |

| • | awareness of our brand; |

| • | changes in the competitive dynamics of our market, including consolidation among competitors or clients and the introduction of new technologies and technology enhancements; |

| • | changes to the commission plans, quotas, and other compensation-related metrics for our sales representatives; |

| • | the amount and timing of payment for operating expenses, particularly sales and marketing expense; |

| • | our ability to manage our existing business and future growth, domestically and internationally; |

| • | unforeseen costs and expenses related to the expansion of our business, operations, and infrastructure, including disruptions in our hosting network infrastructure and privacy and data security; and |

| • | general economic and political conditions in our domestic and international markets. |

We may not be able to accurately forecast the amount and mix of future technology offerings and services, size or duration of contracts, revenue, and expenses and, as a result, our operating results may fall below our estimates.

We could be held liable for damages or our reputation could suffer from security breaches or disclosure of confidential information or personal data.

We are dependent on IT networks and systems to process, transmit, and securely store electronic information and to communicate among our locations and with our clients. Through our cloud technology offerings, we process, transmit, and store electronic information of our clients. Security breaches of this infrastructure could lead to shutdowns or disruptions of our systems and potential loss or unauthorized disclosure of confidential information or data, including personal data. In addition, many of our engagements involve projects that are critical to the operations of our clients’ businesses. The theft and/or unauthorized use or publication of our, or our clients’, confidential information or other proprietary business information as a result of such an incident could adversely affect our competitive position and reduce marketplace acceptance of our services. Any failure in the networks or computer systems used by us or our clients could result in a claim for substantial damages against us and significant reputational harm, regardless of our responsibility for the failure.

In addition, we often have access to or are required to manage, utilize, collect, and store sensitive or confidential client or employee data, including personal data. As a result, we are subject to numerous U.S. and non-U.S. laws and regulations designed to protect this information, such as the European Union Directive on Data Protection and various U.S. federal and state laws governing the protection of personal data. If any person, including any of our employees, negligently disregards or intentionally breaches controls or procedures with which we are responsible for complying with respect to such data, or otherwise mismanages or misappropriates that data, or if unauthorized access to or disclosure of data in our possession or control occurs, we could be subject to liability and penalties in connection with any violation of applicable privacy laws and/or criminal prosecution, as well as significant liability to our clients or our clients’ customers for breaching contractual confidentiality and security provisions or privacy laws. These risks will increase as we continue to grow our cloud-based offerings and services and store and process increasingly large amounts of our clients’ confidential information and data and host or manage parts of our clients’ businesses, especially in industries involving particularly sensitive data such as the financial services industry and the healthcare industry. The loss or unauthorized disclosure of sensitive or confidential client or employee data, including personal data, whether through breach of computer systems, systems failure, employee negligence, fraud or misappropriation, or otherwise, could damage our reputation and cause us to lose clients. Similarly, unauthorized access to or through

12

Table of Contents

our information systems and networks or those we develop or manage for our clients, whether by our employees or third parties, could result in negative publicity, legal liability, and damage to our reputation, which could in turn harm our business, results of operations, or financial condition.

If we cause disruptions in our clients’ businesses or provide inadequate service, our clients may have claims for substantial damages against us, which could cause us to lose clients, have a negative effect on our corporate reputation, and adversely affect our results of operations.

If we make errors in the course of delivering services to our clients or fail to consistently meet our service level obligations or other service requirements of our clients, these errors or failures could disrupt our client’s business, which could result in a reduction in our revenue or a claim for substantial damages against us. In addition, a failure or inability by us to meet a contractual requirement could subject us to penalties, cause us to lose clients or damage our brand or corporate reputation, and limit our ability to attract new business.

The services we provide are often critical to our clients’ businesses. Certain of our client contracts require us to comply with security obligations including maintaining network security and backup data, ensuring our network is virus-free, maintaining business continuity planning procedures, and verifying the integrity of employees that work with our clients by conducting background checks. Any failure in a client’s system, failure of our data center, cloud or other offerings, or breach of security relating to the services we provide to the client could damage our reputation or result in a claim for substantial damages against us. Any significant failure of our equipment or systems, or any major disruption to basic infrastructure in the locations in which we operate, such as power and telecommunications, could impede our ability to provide services to our clients, have a negative impact on our reputation, cause us to lose clients, and adversely affect our results of operations.

Under our client contracts, our liability for breach of our obligations is in some cases limited pursuant to the terms of the contract. Such limitations may be unenforceable or otherwise may not protect us from liability for damages. In addition, certain liabilities, such as claims of third parties for which we may be required to indemnify our clients, are generally not limited under our contracts. The successful assertion of one or more large claims against us in amounts greater than those covered by our current insurance policies could harm our business, results of operations, or financial condition. Even if such assertions against us are unsuccessful, we may incur reputational harm and substantial legal fees.

The length and unpredictability of the sales cycle for our technology offerings and services could delay new sales and cause our revenue and cash flows for any given quarter to fail to meet our projections or market expectations.

The sales cycle between our initial contact with a potential client and the signing of a contract to provide technology offerings and services varies. As a result of the variability and length of the sales cycle, we have a limited ability to forecast the timing of sales. A delay in or failure to complete transactions could harm our business and financial results, and could cause our financial results to vary significantly from quarter to quarter. Our sales cycle varies widely, reflecting differences in our potential clients’ decision-making processes, procurement requirements, and budget cycles, and is subject to significant risks over which we have little or no control, including:

| • | our clients’ budgetary constraints and priorities; |

| • | the timing of our clients’ budget cycles; and |

| • | the length and timing of clients’ approval processes. |

Reliance on shipments at the end of the quarter could cause our revenue for the applicable period to fall below expected levels. Our profitability depends, in part, on the volume of technology offerings and services sold, and we may be unable to achieve increases in our profit margins in the future.

As a result of client purchasing patterns and the efforts of our client engagement team to meet or exceed their performance objectives, we have historically generated a substantial portion of revenue during the last few

13

Table of Contents

weeks of each quarter. If expected revenue at the end of any quarter is delayed for any reason, including the failure of anticipated purchase orders to materialize, our inability to ship and demonstrate clients’ receipt of products prior to quarter-end to fulfill purchase orders received near the end of the quarter, our failure to manage inventory to meet demand, our inability to release new products on schedule, or any failure of our systems related to order review and processing, our revenue for that quarter could fall below our expectations, which could adversely impact our business, results of operations, or financial condition.

Seasonality may cause fluctuations in our revenue and profitability.

We believe there are significant seasonal factors that cause us to record higher revenue in some quarters compared to others. We believe this variability is largely due to our clients’ and technology partners’ fiscal year ends, as well as budgetary and spending patterns of our clients. For example, we have historically generated a higher portion of our sales in the second half of each year, at which point our cost of revenue and commission expense increases relative to any increase in revenue. The increased cost of revenue and commission expense, and other impacts of seasonality, may affect profitability in a given quarter. Our growth rate may have made seasonal fluctuations more difficult to detect. If our growth rate slows over time, seasonal or cyclical variations in our operations may become more pronounced, and our business, results of operations, or financial position may be adversely affected.

Our work with government clients exposes us to additional risks inherent in the government contracting environment.

We provide IT services to various government agencies, including federal, state, and local government entities. For 2016 and 2017, approximately 7% and 10%, respectively, of our total revenue was derived from sales to federal, state, and local governments. While our sales to public sector clients are diversified across various agencies and departments, changes in law, regulation, or the political climate, or an across-the-board change in government spending policies, including budget cuts at the federal level, could result in our public sector clients reducing their purchases and terminating their service contracts, which could adversely impact our business, results of operations, or financial condition.

Furthermore, we derive a substantial portion of our government contracts revenue from contracts awarded through competitive procurement processes, which can impose substantial costs upon us to prepare for and participate in competitions. Moreover, there is no assurance that our proposal will be selected for any future opportunity and even where we are awarded a contract, the award may be subject to protest by competitors, which may require the contracting agency or department to suspend our performance pending the outcome of the protest.

In addition, government contracts often contain additional audit rights, termination for convenience provisions, compliance, and disclosure obligations, and are subject to heightened reputational and contractual risks compared to contracts with commercial clients, including the risk of False Claims Act prosecutions and/or suspensions or debarment proceedings. The additional obligations and risks could affect not only our business with the particular government entities involved, but also our business with other entities of the same or other governmental bodies or with certain commercial clients, and could adversely impact our business, results of operations, or financial condition.

Our technology offerings and services could infringe upon the intellectual property rights of others or we might lose our ability to utilize the intellectual property of others.

We cannot be sure that our brand, technology offerings, and services, including, for example, the software solutions of others that we offer to our clients, do not infringe on the intellectual property rights of third parties, and these third parties could claim that we or our clients are infringing upon their intellectual property rights. These claims could harm our reputation, cause us to incur substantial costs or prevent us from offering some services or solutions in the future, or require us to rebrand. Any related proceedings could require us to expend significant resources over an extended period of time. In most of our contracts, we agree to indemnify our clients

14

Table of Contents

for expenses and liabilities resulting from claimed infringements of the intellectual property rights of third parties. In some instances, the amount of these indemnities could be greater than the revenue we receive from the client. Any claims or litigation in this area, regardless of merit, could be time-consuming and costly, damage our reputation, and/or require us to incur additional costs to obtain the right to continue to offer a service or solution to our clients. If we cannot secure this right at all or on reasonable terms, or, alternatively, substitute a non-infringing technology, our business, results of operations, or financial condition could be harmed. Similarly, if we are unsuccessful in defending a trademark claim, we could be forced to re-brand, which could harm our business, results of operations, or financial condition. Additionally, in recent years, individuals and firms have purchased intellectual property assets where their sole or primary purpose is to assert claims of infringement against technology providers and clients that use such technology. Any such action naming us or our clients could be costly to defend or lead to an expensive settlement or judgment against us. Moreover, such an action could result in an injunction being ordered against our client or our own services or operations, causing further damages.

If we are unable to protect our intellectual property rights from unauthorized use or infringement by third parties, our business could be adversely affected.

Our success depends, in part, upon our ability to protect our proprietary methodologies and other intellectual property. Existing laws offer only limited protection of our intellectual property rights, and the protection in some countries in which we operate or may operate in the future may be very limited. We rely upon a combination of confidentiality policies, nondisclosure and other contractual arrangements, and trade secret, copyright, and trademark laws to protect our intellectual property rights. These laws are subject to change at any time and could further limit our ability to protect our intellectual property. There is uncertainty concerning the scope of available intellectual property protection for software and business methods, which are fields in which we rely on intellectual property laws to protect our rights. The validity and enforceability of any intellectual property right we obtain may be challenged by others and, to the extent we have enforceable intellectual property rights, those intellectual property rights may not prevent competitors from reverse engineering our proprietary information or independently developing technology offerings and services similar to or duplicative of ours. Further, the steps we take in this regard might not be adequate to prevent or deter infringement or other misappropriation of our intellectual property by competitors, former employees or other third parties, and we might not be able to detect unauthorized use of, or take appropriate and timely steps to enforce, our intellectual property rights. Enforcing our rights might also require considerable time, money, and oversight, and we may not be successful in enforcing our rights.

If we are unable to collect our receivables from, or bill our unbilled services to, our clients, our business, results of operations, or financial condition could be adversely affected.

Our business depends on our ability to successfully obtain payment from our clients of the amounts they owe us for technology offerings sold or services performed. We typically evaluate the financial condition of our clients and usually bill and collect on relatively short cycles. We maintain allowances against receivables and unbilled services. Actual losses on client balances could differ from those that we currently anticipate and, as a result, we might need to adjust our allowances. There is no guarantee that we will accurately assess the creditworthiness of our clients. Macroeconomic conditions could also result in financial difficulties for our clients, including limited access to the credit markets, insolvency, or bankruptcy, and, as a result, could cause clients to delay payments to us, request modifications to their payment arrangements that could increase our receivables balance, or default on their payment obligations to us. Timely collection of client balances also depends on our ability to complete our contractual commitments and bill and collect our contracted revenue. If we are unable to meet our contractual requirements, we might experience delays in collection of and/or be unable to collect our client balances, and if this occurs, our business, results of operations, or financial condition could be adversely affected. In addition, if we experience an increase in the time to bill and collect for our services, our cash flows could be adversely affected.

15

Table of Contents

Increased costs of labor and employee health and welfare benefits may adversely impact our results of operations.

Given our large number of employees, labor-related costs represent a significant portion of our expenses. Salaries, wages, benefits, commissions, and other labor compensation costs excluding bonus and payroll tax for our full-time employees amounted to $133 million in 2017, which represented approximately 62% of our selling, general and administrative expenses and approximately 10% of our cost of revenue. An increase in labor costs, for example, as a result of increased competition for skilled labor, or employee benefit costs, such as health care costs or otherwise, could adversely impact our business, results of operations, or financial condition.

We rely on third-party companies to perform certain of our obligations to clients, which could impact our business if not performed.

We deliver and manage mission-critical software, systems and network solutions for our clients. We also offer certain services, such as implementation, installation, and deployment services, to our clients through various third-party providers who are engaged to perform these services on our behalf. We are also required, as a component of some of our contracts with our OEM partners, to utilize their engineers as part of our solutions. In addition, we support approximately 150 multinational clients through our Aura and Unified Comms alliances, offering access to more than 50 IT service providers in approximately 60 countries and enabling us to offer our managed services internationally. If we or our third-party services providers, including our alliance service providers, fail to provide high-quality services to our clients, or if such services result in a disruption of our clients’ businesses, we could be subject to legal claims, proceedings, and liability.

The interruption of the flow of products from suppliers could disrupt our supply chain.

A significant portion of the products we sell are manufactured or purchased by our technology partners outside of the United States, primarily in Asia. Political, social, or economic instability in Asia, or in other regions in which our technology partners purchase or manufacture the products we sell, could cause disruptions in trade, including exports to the United States. Other events that could also cause disruptions to our supply chain include:

| • | the imposition of additional trade law provisions or regulations or changes to existing trade laws provisions or regulations; |

| • | the imposition of additional duties, tariffs, and other charges on imports and exports; |

| • | foreign currency fluctuations; |

| • | natural disasters or other adverse occurrences at, or affecting, any of our suppliers’ facilities; |

| • | restrictions on the transfer of funds; |

| • | the financial instability or bankruptcy of manufacturers; and |

| • | significant labor disputes, such as strikes. |

We cannot predict whether the countries in which the products we sell are purchased or manufactured, or may be purchased or manufactured in the future, will be subject to new or additional trade restrictions or sanctions imposed by the U.S. or foreign governments, including the likelihood, type or effect of any such restrictions. Trade restrictions, including new or increased tariffs or quotas, embargoes, sanctions, safeguards, and customs restrictions against the products we sell, as well as foreign labor strikes and work stoppages or boycotts, could increase the cost or reduce the supply of product available to us and adversely affect our business, results of operations, or financial condition. In addition, our exports are subject to regulations and noncompliance with these requirements could have a negative effect on our business, results of operations, or financial condition.

16

Table of Contents

Our global operations are subject to complex risks, some of which might be beyond our control.

Our clients have operations across South America, Europe, Australia, and Asia. Although international revenue currently represents a small portion of our business, our revenue from clients outside of the United States may expand in the future as we expand our international presence. As a result, we may be subject to risks inherently associated with international operations, including risks associated with foreign currency exchange rate fluctuations, difficulties in enforcing intellectual property and/or contractual rights, the burdens of complying with a wide variety of foreign laws and regulations, potentially adverse tax consequences, tariffs, quotas, and other barriers, potential difficulties in collecting accounts receivable, international hostilities, terrorism, and natural disasters. Expansion of international operations also increases the likelihood of potential or actual violations of domestic and international anticorruption laws, such as the Foreign Corrupt Practices Act, or of U.S. and international export control and sanctions regulations. We may also face difficulties integrating any new facilities in different countries into our existing operations, as well as integrating employees that we hire in different countries into our existing corporate culture. If we are unable to manage the risks of our global operations, our business, results of operations, or financial condition could be adversely affected.

Changes in accounting rules could adversely affect our future financial results.