Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - Blackstone Real Estate Income Trust, Inc. | breit-ex322_8.htm |

| EX-32.1 - EX-32.1 - Blackstone Real Estate Income Trust, Inc. | breit-ex321_10.htm |

| EX-31.2 - EX-31.2 - Blackstone Real Estate Income Trust, Inc. | breit-ex312_6.htm |

| EX-31.1 - EX-31.1 - Blackstone Real Estate Income Trust, Inc. | breit-ex311_9.htm |

| EX-21.1 - EX-21.1 - Blackstone Real Estate Income Trust, Inc. | breit-ex211_1154.htm |

| EX-10.1 - EX-10.1 - Blackstone Real Estate Income Trust, Inc. | breit-ex101_1419.htm |

| EX-4.1 - EX-4.1 - Blackstone Real Estate Income Trust, Inc. | breit-ex41_1418.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES |

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission File Number: 333-213043

Blackstone Real Estate Income Trust, Inc.

(Exact name of Registrant as specified in its charter)

|

|

|

|

Maryland |

81-0696966 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

345 Park Avenue

New York, New York 10154

(Address of principal executive offices) (Zip Code)

(212) 583-5000

(Registrant’s telephone number, including area code)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

☐ |

|

Accelerated filer |

☐ |

|

Non-accelerated filer |

☒ |

(Do not check if a smaller reporting company) |

Smaller reporting company |

☐ |

|

|

|

|

Emerging growth company |

☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Yes ☒ No ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act. Yes ☐ No ☒

As of March 19, 2018, the issuer had the following shares outstanding: 163,218,275 shares of Class S common stock, 9,741,552 shares of Class T common stock, 6,823,284 shares of Class D common stock, and 47,020,960 shares of Class I common stock.

|

|

|

|

Page |

|

PART I. |

|

|

|

|

|

|

|

|

|

ITEM 1. |

|

1 |

|

|

|

|

|

|

|

ITEM 1A. |

|

6 |

|

|

|

|

|

|

|

ITEM 1B. |

|

57 |

|

|

|

|

|

|

|

ITEM 2. |

|

58 |

|

|

|

|

|

|

|

ITEM 3. |

|

58 |

|

|

|

|

|

|

|

ITEM 4. |

|

58 |

|

|

|

|

|

|

|

PART II. |

|

|

|

|

|

|

|

|

|

ITEM 5. |

|

59 |

|

|

|

|

|

|

|

ITEM 6. |

|

65 |

|

|

|

|

|

|

|

ITEM 7. |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

66 |

|

|

|

|

|

|

ITEM 7A. |

|

78 |

|

|

|

|

|

|

|

ITEM 8. |

|

78 |

|

|

|

|

|

|

|

ITEM 9. |

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

79 |

|

|

|

|

|

|

ITEM 9A. |

|

79 |

|

|

|

|

|

|

|

ITEM 9B. |

|

79 |

|

|

|

|

|

|

|

PART III. |

|

|

|

|

|

|

|

|

|

ITEM 10. |

|

80 |

|

|

|

|

|

|

|

ITEM 11. |

|

80 |

|

|

|

|

|

|

|

ITEM 12. |

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

80 |

|

|

|

|

|

|

ITEM 13. |

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

80 |

|

|

|

|

|

|

ITEM 14. |

|

80 |

|

|

|

|

|

|

|

PART IV. |

|

|

|

|

|

|

|

|

|

ITEM 15. |

|

81 |

|

|

|

|

|

|

|

ITEM 16. |

|

83 |

|

|

|

|

||

|

84 |

|||

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements include statements about our business, including, in particular, statements about our plans, strategies and objectives. You can generally identify forward-looking statements by our use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “anticipate,” “estimate,” “believe,” “continue” or other similar words. These statements include our plans and objectives for future operations, including plans and objectives relating to future growth and availability of funds, and are based on current expectations that involve numerous risks and uncertainties. Assumptions relating to these statements involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to accurately predict and many of which are beyond our control. Although we believe the assumptions underlying the forward-looking statements, and the forward-looking statements themselves, are reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurance that these forward-looking statements will prove to be accurate and our actual results, performance and achievements may be materially different from that expressed or implied by these forward-looking statements. In light of the significant uncertainties inherent in these forward looking statements, the inclusion of this information should not be regarded as a representation by us or any other person that our objectives and plans, which we consider to be reasonable, will be achieved.

You should carefully review Item 1A — “Risk Factors” section of this Annual Report on Form 10-K for a discussion of the risks and uncertainties that we believe are material to our business, operating results, prospects and financial condition. Except as otherwise required by federal securities laws, we do not undertake to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

References herein to “Blackstone Real Estate Income Trust,” the “Company,” “BREIT,” “we,” “us,” or “our” refer to Blackstone Real Estate Income Trust, Inc., a Maryland corporation, and its subsidiaries unless the context specifically requires otherwise.

General Description of Business and Operations

BREIT is a non-exchange traded, perpetual life real estate investment trust ("REIT") that acquires primarily stabilized income-oriented commercial real estate in the United States and to a lesser extent real estate-related securities. We are externally managed by BX REIT Advisors L.L.C. (the “Adviser”), a subsidiary of The Blackstone Group L.P. (“Blackstone”). We are the sole general partner of BREIT Operating Partnership L.P. (“BREIT OP”), a Delaware limited partnership, and we own all or substantially all of our assets through BREIT OP. We currently operate our business in five reportable segments: Multifamily, Industrial, Hotel, and Retail Properties, and Real Estate-Related Securities. Our objective is to bring Blackstone’s leading real estate investment platform with an institutional fee structure to individual investors.

We intend to qualify as a REIT under the Internal Revenue Code of 1986, as amended (the “Code”) for U.S. federal income tax purposes beginning with the taxable year ended December 31, 2017. We generally will not be subject to U.S. federal income taxes on our taxable income to the extent we annually distribute all of our net taxable income to stockholders and maintain our qualification as a REIT.

We have registered with the Securities and Exchange Commission (the “SEC”) an offering of up to $5.0 billion in shares of common stock (in any combination of purchases of Class S, Class T, Class D and Class I shares of our common stock), consisting of up to $4.0 billion in shares in our primary offering and up to $1.0 billion in shares pursuant to its distribution reinvestment plan (the “Offering”). The share classes have different upfront selling commissions and ongoing stockholder servicing fees. As of January 1, 2017, we satisfied the minimum offering requirement and our board of directors authorized the release of proceeds from escrow. We intend to continue selling shares in the Offering on a monthly basis.

As of March 19, 2018, we had received net proceeds of $2.3 billion from selling an aggregate of 226,804,071 shares of our common stock (consisting of 163,218,275 Class S shares, 9,741,552 Class T shares, 6,823,284 Class D shares, and 47,020,960 Class I shares). We have primarily used the net proceeds to make investments in real estate and real estate-related securities.

1

Our Adviser

We are externally managed by our Adviser, and pursuant to the advisory agreement between us and the Adviser (the “Advisory Agreement”), we have delegated to the Adviser the authority to source, evaluate and monitor our investment opportunities and to make decisions related to the acquisition, management, financing and disposition of our assets, in accordance with our investment objectives, guidelines, policies and limitations, as well as provide us with our executive management team. Our board of directors will at all times have oversight and policy-making authority over us, including responsibility for governance, financial controls, compliance and disclosure.

Our Adviser is a part of Blackstone, an alternative asset management business that includes the management of investment vehicles focused on private equity, real estate, public debt and equity, non-investment grade credit, real assets, and secondary funds, all on a global basis. Through its different businesses, Blackstone had total assets under management of $434.1 billion as of December 31, 2017.

In connection with the performance of its duties, our Adviser benefits from the resources, relationships, and expertise of the 426 professionals in Blackstone’s global real estate group, which is the largest private equity real estate manager in the world with $115.3 billion of investor capital under management as of December 31, 2017. Jonathan D. Gray, who is the president and chief operating officer of Blackstone, is a member of the board of directors of Blackstone and is a member of our Adviser’s investment committee.

Our chief executive officer, chief financial officer, and other executive officers are senior Blackstone real estate professionals. Our Adviser, our executive officers, and other personnel supplied to us by our Adviser are each not obligated to dedicate any specific amount of time to our business. Our Adviser is subject to the supervision and oversight of our board of directors and has only such functions and authority as our board of directors delegates to it. Pursuant to the Advisory Agreement, our Adviser is entitled to receive a base management fee, and expense reimbursements. In addition, BREIT Special Limited Partner L.L.C. (the “Special Limited Partner”), a wholly-owned subsidiary of Blackstone, is entitled to receive a performance participation allocation. See Note 11 to our consolidated financial statements and Item 13 “Certain Relationships and Related Transactions, and Director Independence” in this Annual Report on Form 10-K for more detail on the terms of the Advisory Agreement.

Investment Objectives

Our investment objectives are to invest in assets that will enable us to:

|

|

• |

provide current income in the form of regular, stable cash distributions to achieve an attractive distribution yield; |

|

|

• |

preserve and protect invested capital; |

|

|

• |

realize appreciation in net asset value (“NAV”) from proactive investment management and asset management; and |

|

|

• |

provide an investment alternative for stockholders seeking to allocate a portion of their long-term investment portfolios to commercial real estate with lower volatility than listed public real estate companies. |

Investment Strategy

Our investment strategy is to acquire primarily stabilized income-oriented commercial real estate in the United States. To a lesser extent, we also invest in real estate-related securities to provide current income and a source of liquidity for our share repurchase plan, cash management and other purposes.

Our investment strategy capitalizes on Blackstone’s scale and the real-time information provided by its real estate holdings to identify and acquire our target investments at attractive pricing. We also benefit from Blackstone’s reputation and ability to transact in scale with speed and certainty, and its long-standing and extensive relationships in the real estate industry. After acquisition, we leverage Blackstone Real Estate’s established asset management team, which focuses on value creation through the oversight and improvement of the operating performance of Blackstone Real Estate’s portfolio holdings.

Our investments in primarily stabilized income-oriented commercial real estate in the United States focus on a range of asset types. These may include multifamily, industrial, hotel, retail, and office assets, as well as others, including, without limitation, healthcare, student housing, senior living, data centers, manufactured housing and storage properties. For a breakdown of our portfolio by asset type see the “Investments in Properties” section below.

Our real estate-related securities strategy is designed to generate current income and an attractive investment return. We also believe that our real estate-related securities will help maintain sufficient liquidity to satisfy monthly repurchase requests under our share

2

repurchase plan and manage cash before investing subscription proceeds into properties. We utilize the Blackstone Real Estate Debt Strategies (“BREDS”) team to assist in this portion of the portfolio. The BREDS team leverages the competitive advantages of the broader Blackstone Real Estate platform and its own proprietary investment models to seek attractive real estate-related securities investment opportunities throughout the capital structure.

We believe that our structure as a perpetual-life REIT will allow us to acquire and manage our investment portfolio in a more active and flexible manner. We do not have a pre-determined operational period or the need to provide a “liquidity” event at the end of that period.

Investments in Properties

We invest primarily in stabilized income-oriented commercial real estate in the United States. We may invest to a limited extent in Canadian cities and potentially elsewhere, including as part of portfolio acquisitions where certain properties are located outside the United States. We may also acquire assets that require some amount of capital investment in order to be renovated or repositioned or unstabilized assets that require lease-up. We generally will limit investment in new developments on a standalone basis, but may consider development that is ancillary to an overall investment.

We do not designate specific geography or sector allocations for the portfolio; rather we invest in regions or asset classes where we see the best opportunities that support our investment objectives.

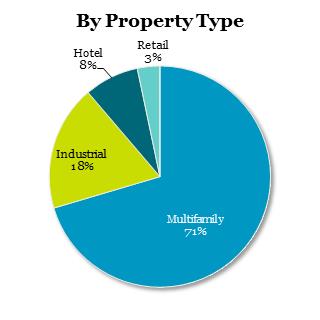

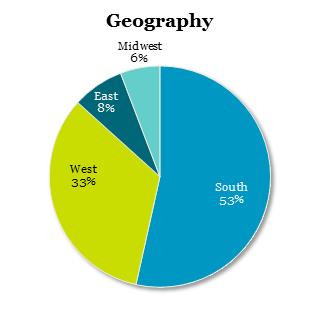

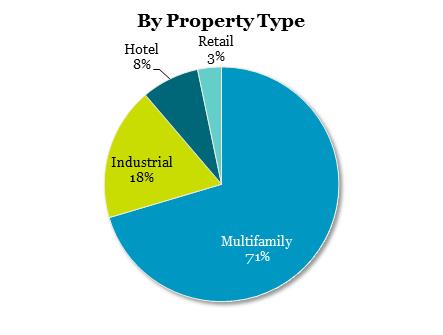

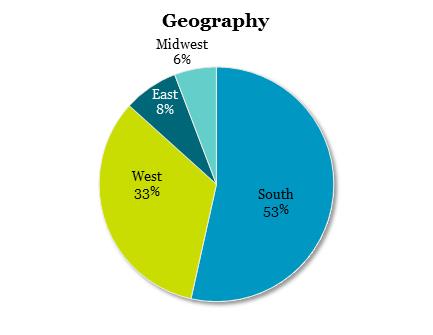

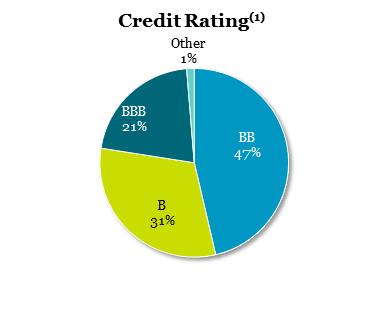

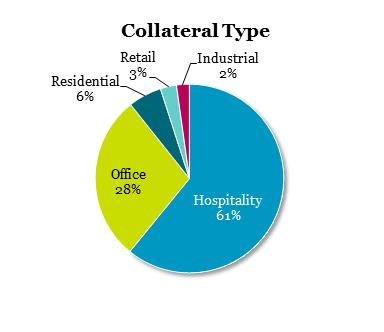

The following charts describe the diversification of our investments in real properties based on fair value as of December 31, 2017:

|

|

|

Investments in Real Estate-Related Securities

Our real estate-related securities investments focus on non-distressed public and private real estate debt, including, but not limited to, commercial mortgage-backed securities (“CMBS”), residential mortgage-backed securities (“RMBS”), mortgages, loans, mezzanine and other forms of debt, and may also include preferred equity. Additionally, while we do not intend to make open market purchases of common stock in public equity REITs or other companies focused on owning real property, we may make such investments in companies with mortgages as one of their core businesses.

Borrowing Policies

We use financial leverage to provide additional funds to support our investment activities. This allows us to make more investments than would otherwise be possible, resulting in a broader portfolio. Subject to the limitation on indebtedness for money borrowed in our charter described below, our target leverage ratio is in the range of 60% of our gross real estate assets (measured using the greater of fair market value and the cost of gross real estate assets, including equity in our securities portfolio), inclusive of property-level and entity-level debt net of cash, but excluding debt on our securities portfolio. Indebtedness incurred (i) in connection with funding a

3

deposit in advance of the closing of an investment or (ii) as other working capital advances, will not be included as part of the calculation above. Furthermore, the refinancing of any amount of existing indebtedness will not be deemed to constitute incurrence of new indebtedness so long as no additional amount of net indebtedness is incurred in connection therewith.

Our real estate-related securities portfolio may have embedded leverage, including through the use of reverse repurchase agreements and derivatives, including, but not limited to, total return swaps, securities lending arrangements and credit default swaps. During times of increased investment and capital market activity, but subject to the limitation on indebtedness for money borrowed in our charter described below, we may employ greater leverage in order to build a broader portfolio of assets. We may leverage our portfolio by assuming or incurring secured or unsecured property-level or entity-level debt.

Under our charter, we have a limitation that precludes us from borrowing in excess of 300% of our net assets, which approximates borrowing 75% of the cost of our investments (unless a majority of our independent directors approves any borrowing in excess of the limit and we disclose the justification for doing so to our stockholders), but such restriction does not restrict the amount of indebtedness we may incur with respect to any single investment.

For an overview of our borrowings, see Item 7 — “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources.”

Taxation of the Company

We intend to be taxed as a REIT, under the Code commencing with our taxable year ended December 31, 2017, the year in which the proceeds from the Offering were released from escrow. We generally must distribute annually at least 90% of our taxable net income, subject to certain adjustments and excluding any net capital gain, in order for U.S. federal income tax not to apply to our earnings that we distribute. To the extent that we satisfy this distribution requirement, but distribute less than 100% of our net taxable income, we will be subject to U.S. federal income tax on our undistributed taxable income. In addition, we will be subject to a 4% nondeductible excise tax if the actual amount that we pay out to our stockholders in a calendar year is less than a minimum amount specified under U.S. federal tax laws.

Our qualification as a REIT also depends on our ability to meet various other requirements imposed by the Code, which relate to organizational structure, diversity of stock ownership, and certain restrictions with regard to the nature of our assets and the sources of our income. Even if we qualify as a REIT, we may be subject to certain U.S. federal income and excise taxes and state and local taxes on our income and assets. If we fail to maintain our qualification as a REIT for any taxable year, we may be subject to material penalties as well as federal, state, and local income tax on our taxable income at regular corporate rates and we would not be able to qualify as a REIT for the subsequent four full taxable years.

Furthermore, we have one or more taxable REIT subsidiaries (“TRSs”) which pay federal, state, and local income tax on their net taxable income. See Item 1A—“Risk Factors—Risks Related to our REIT Status and Certain Other Tax Items” for additional tax status information.

The Tax Cuts and Jobs Act

Enactment of the Tax Act

On December 22, 2017, the federal tax legislation commonly known as the Tax Cuts and Jobs Act (the “Tax Act”), was signed into law. The Tax Act makes fundamental changes to the Code, including several provisions of the Code that affect the taxation of REITs and their security holders. The most significant of these provisions are described below. The individual and collective impact of these changes on REITs such as the Company and their security holders is uncertain, and may not become evident for some period. Prospective investors should consult their tax advisors regarding the implications of the Tax Act on the Company and their investment.

Pass-Through Business Income Tax Rate Lowered through Deduction

Under the Tax Act, United States holders that are individuals, trusts or estates generally may deduct 20% of “qualified REIT dividends” (i.e., REIT dividends other than capital gain dividends and portions of REIT dividends designated as qualified dividend income eligible for capital gain tax rates). The overall deduction is limited to 20% of the sum of the taxpayer’s taxable income (less net capital gain) and certain cooperative dividends, subject to further limitations based on taxable income. The deduction, if allowed in full, equates to a reduction in the maximum effective United States federal income tax rate on ordinary REIT dividends from 39.6% to 29.6%. As with the other individual income tax changes, the deduction provisions are effective beginning in 2018. Without further legislation, the deduction will sunset and no longer apply after 2025.

4

Maximum Corporate Tax Rate Lowered to 21%; Elimination of Corporate Alternative Minimum Tax

The Tax Act reduces the 35% maximum federal corporate income tax rate to a maximum 21% corporate rate, and reduces the dividends-received deduction for certain corporate subsidiaries. The Tax Act also permanently eliminates the corporate alternative minimum tax. These provisions are effective beginning in 2018. As disclosed above, we have one or more TRSs which would be subject to a maximum tax rate of 21% under the Tax Act.

Net Operating Loss Modifications

Net operating loss (“NOL”) provisions are modified by the Tax Act. The Tax Act limits the NOL deduction to 80% of taxable income (before the deduction). It also generally eliminates NOL carrybacks for individuals and non-REIT corporations (NOL carrybacks did not apply to REITs under prior law), but allows indefinite NOL carryforwards. The new NOL rules apply to losses arising in taxable years beginning in 2018. As disclosed above, we have one or more TRSs which would be subject to the NOL provisions under the Tax Act.

Environmental Matters

As an owner of real estate, we are subject to various environmental laws of federal, state and local governments. Compliance with federal, state and local environmental laws has not had a material, adverse effect on our business, assets, results of operations, financial condition and ability to pay distributions, and we do not believe that our existing portfolio will require us to incur material expenditures to comply with these laws and regulations.

Competition

We face competition from various entities for investment opportunities in properties, including other REITs, pension funds, insurance companies, investment funds and companies, partnerships and developers. In addition to third-party competitors, other programs sponsored by the Adviser and its affiliates, particularly those with investment strategies that overlap with ours, will seek investment opportunities under Blackstone’s prevailing policies and procedures. Many of these entities may have greater access to capital to make investments than we have.

In the face of this competition, we have access to our Adviser’s and Blackstone’s professionals and their industry expertise and relationships, which we believe provide us with a competitive advantage and help us source, evaluate and compete for potential investments. We believe these relationships will enable us to compete more effectively for attractive investment opportunities. However, we may not be able to achieve our business goals or expectations due to the competitive risks that we face. For additional information concerning these competitive risks, see Item 1A—“Risk Factors—Risks Related to Our Investment Activities.”

Employees

We have no employees. Our operations are conducted by the Adviser.

Conflicts of Interest

We are subject to conflicts of interest arising out of our relationship with Blackstone, including the Adviser and its affiliates. See Item 1A — “Risk Factors — Risks Related to Conflicts of Interest.”

Available Information

Stockholders may obtain copies of our filings with the SEC, free of charge from the website maintained by the SEC at www.sec.gov or from our website at www.breit.com. Our SEC filings are available to be read or copied at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. Information regarding the operation of the Public Reference Room can be obtained by calling the SEC at 1-800-SEC-0330.

We are providing the address to our website solely for the information of investors. The information on our website is not a part of, nor is it incorporated by reference into, this report.

5

You should specifically consider the following material risks in addition to the other information contained in this Annual Report on Form 10-K. The occurrence of any of the following risks might have a material adverse effect on our business and financial condition. The risks and uncertainties discussed below are not the only ones we face, but do represent those risks and uncertainties that we believe are most significant to our business, operating results, financial condition, prospects and forward-looking statements. As used herein, the term “you” refers to our current stockholders or potential investors in our common stock, as applicable.

Risks Related Our Organizational Structure

We have a limited operating history and there is no assurance that we will be able to successfully achieve our investment objectives.

We have a limited operating history and may not be able to achieve our investment objectives. We cannot assure you that the past experiences of affiliates of the Adviser will be sufficient to allow us to successfully achieve our investment objectives. As a result, an investment in our shares of common stock may entail more risk than the shares of common stock of a REIT with a substantial operating history.

We have held our current investments for only a short period of time and you will not have the opportunity to evaluate our future investments before we make them, which makes your investment more speculative.

We have held our current investments for a limited period of time and are not able to provide you with any information to assist you in evaluating the merits of any specific properties or real estate-related securities that we may acquire, except for investments that may be described in one or more supplements to the prospectus for the Offering (the “Prospectus”). Because we have not held our current investments for a long period of time, it may be difficult for you to evaluate our success in achieving our investment objectives. We will seek to invest substantially all of the future net offering proceeds from the Offering, after the payment of fees and expenses, in the acquisition of or investment in interests in properties and real estate-related securities. However, because you will be unable to evaluate the economic merit of our future investments before we make them, you will have to rely entirely on the ability of the Adviser to select suitable and successful investment opportunities. Furthermore, the Adviser will have broad discretion in selecting the types of properties we will invest in and the tenants of those properties, and you will not have the opportunity to evaluate potential investments. These factors increase the risk that your investment may not generate returns comparable to other real estate investment alternatives.

The Adviser manages our portfolio pursuant to very broad investment guidelines and generally is not required to seek the approval of our board of directors for each investment, financing or asset allocation decision made by it, which may result in our making riskier investments and which could adversely affect our results of operations and financial condition.

Our board of directors approved very broad investment guidelines that delegate to the Adviser the authority to execute acquisitions and dispositions of real estate properties and real estate-related securities on our behalf, in each case so long as such investments are consistent with the investment guidelines and our charter. There can be no assurance that the Adviser will be successful in applying any strategy or discretionary approach to our investment activities. Our board of directors reviews our investment guidelines on an annual basis (or more often as it deems appropriate) and reviews our investment portfolio periodically. The prior approval of our board of directors or a committee of independent directors will be required only as set forth in our charter (including for transactions with affiliates of the Adviser) or for the acquisition or disposition of assets that are not in accordance with our investment guidelines. In addition, in conducting periodic reviews, our directors rely primarily on information provided to them by the Adviser. Furthermore, transactions entered into on our behalf by the Adviser may be costly, difficult or impossible to unwind when they are subsequently reviewed by our board of directors.

There is no public trading market for shares of our common stock; therefore, your ability to dispose of your shares will likely be limited to repurchase by us. If you do sell your shares to us, you may receive less than the price you paid.

There is no current public trading market for shares of our common stock, and we do not expect that such a market will ever develop. Therefore, repurchase of shares by us will likely be the only way for you to dispose of your shares. We will repurchase shares at a price equal to the transaction price of the class of shares being repurchased on the date of repurchase (which will generally be equal to our prior month’s NAV per share), and not based on the price at which you initially purchased your shares. Subject to limited exceptions, shares repurchased within one year of the date of issuance will be repurchased at 95% of the transaction price. As a result, you may receive less than the price you paid for your shares when you sell them to us pursuant to our share repurchase plan. See Item 5 — “Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities — Share Repurchase Program.”

6

Your ability to have your shares repurchased through our share repurchase plan is limited. We may choose to repurchase fewer shares than have been requested to be repurchased, in our discretion at any time, and the amount of shares we may repurchase is subject to caps. Further, our board of directors may modify, suspend or terminate our share repurchase plan if it deems such action to be in our best interest and the best interest of our stockholders.

We may choose to repurchase fewer shares than have been requested in any particular month to be repurchased under our share repurchase plan, or none at all, in our discretion at any time. We may repurchase fewer shares than have been requested to be repurchased due to lack of readily available funds because of adverse market conditions beyond our control, the need to maintain liquidity for our operations or because we have determined that investing in real property or other illiquid investments is a better use of our capital than repurchasing our shares. In addition, the total amount of shares that we will repurchase is limited, in any calendar month, to shares whose aggregate value (based on the repurchase price per share on the date of the repurchase) is no more than 2% of our aggregate NAV as of the last day of the previous calendar month and, in any calendar quarter, to shares whose aggregate value is no more than 5% of our aggregate NAV as of the last day of the previous calendar quarter. Further, our board of directors may modify, suspend or terminate our share repurchase plan if it deems such action to be in our best interest and the best interest of our stockholders. If the full amount of all shares of our common stock requested to be repurchased in any given month are not repurchased, funds will be allocated pro rata based on the total number of shares of common stock being repurchased without regard to class and subject to the volume limitation. All unsatisfied repurchase requests must be resubmitted after the start of the next month or quarter, or upon the recommencement of the share repurchase plan, as applicable.

The vast majority of our assets consist of properties that cannot generally be readily liquidated without impacting our ability to realize full value upon their disposition. Therefore, we may not always have a sufficient amount of cash to immediately satisfy repurchase requests. Should repurchase requests, in our judgment, place an undue burden on our liquidity, adversely affect our operations or risk having an adverse impact on the company as a whole, or should we otherwise determine that investing our liquid assets in real properties or other illiquid investments rather than repurchasing our shares is in the best interests of the company as a whole, then we may choose to repurchase fewer shares than have been requested to be repurchased, or none at all. Because we are not required to authorize the recommencement of the share repurchase plan within any specified period of time, we may effectively terminate the plan by suspending it indefinitely. See Item 5 — “Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities — Share Repurchase Program.”

Economic events that may cause our stockholders to request that we repurchase their shares may materially adversely affect our cash flow and our results of operations and financial condition.

Economic events affecting the U.S. economy, such as the general negative performance of the real estate sector, could cause our stockholders to seek to sell their shares to us pursuant to our share repurchase plan at a time when such events are adversely affecting the performance of our assets. Even if we decide to satisfy all resulting repurchase requests, our cash flow could be materially adversely affected. In addition, if we determine to sell assets to satisfy repurchase requests, we may not be able to realize the return on such assets that we may have been able to achieve had we sold at a more favorable time, and our results of operations and financial condition, including, without limitation, breadth of our portfolio by property type and location, could be materially adversely affected.

The amount and source of distributions we may make to our stockholders is uncertain, and we may be unable to generate sufficient cash flows from our operations to make distributions to our stockholders at any time in the future.

We have not established a minimum distribution payment level, and our ability to make distributions to our stockholders may be adversely affected by a number of factors, including the risk factors described in the Prospectus. We have a limited track record and may not generate sufficient income to make distributions to our stockholders. Our board of directors (or a committee of our board of directors) will make determinations regarding distributions based upon, among other factors, our financial performance, debt service obligations, debt covenants, REIT qualification and tax requirements and capital expenditure requirements. Among the factors that could impair our ability to make distributions to our stockholders are:

|

|

• |

our inability to invest the proceeds from sales of our shares on a timely basis in income-producing properties; |

|

|

• |

our inability to realize attractive risk-adjusted returns on our investments; |

|

|

• |

high levels of expenses or reduced revenues that reduce our cash flow or non-cash earnings; and |

|

|

• |

defaults in our investment portfolio or decreases in the value of our investments. |

As a result, we may not be able to make distributions to our stockholders at any time in the future, and the level of any distributions we do make to our stockholders may not increase or even be maintained over time, any of which could materially and adversely affect the value of your investment.

7

We may pay distributions from sources other than our cash flow from operations, including, without limitation, the sale of assets, borrowings or offering proceeds, and we have no limits on the amounts we may pay from such sources.

We may not generate sufficient cash flow from operations to fully fund distributions to stockholders, particularly during the early stages of our operations. Therefore, particularly in the earlier part of the Offering, we may fund distributions to our stockholders from sources other than cash flow from operations, including, without limitation, the sale of assets, borrowings, return of capital or offering proceeds (including from sales from our common stock or Operating Partnership units to the Special Limited Partner, an affiliate of Blackstone). The extent to which we pay distributions from sources other than cash flow from operations will depend on various factors, including the level of participation in our distribution reinvestment plan, the extent to which the Adviser elects to receive its management fee in Class I shares or Class I units and the Special Limited Partner elects to receive distributions on its performance participation interest in Class I units, how quickly we invest the proceeds from this and any future offering and the performance of our investments, including our real estate-related securities portfolio. Funding distributions from the sales of assets, borrowings, return of capital or proceeds of the Offering will result in us having less funds available to acquire properties or other real estate-related investments. As a result, the return you realize on your investment may be reduced. Doing so may also negatively impact our ability to generate cash flows. Likewise, funding distributions from the sale of additional securities will dilute your interest in us on a percentage basis and may impact the value of your investment especially if we sell these securities at prices less than the price you paid for your shares. We may be required to continue to fund our regular distributions from a combination of some of these sources if our investments fail to perform, if expenses are greater than our revenues or due to numerous other factors. We have not established a limit on the amount of our distributions that may be paid from any of these sources.

To the extent we borrow funds to pay distributions, we would incur borrowing costs and these borrowings would require a future repayment. The use of these sources for distributions and the ultimate repayment of any liabilities incurred could adversely impact our ability to pay distributions in future periods, decrease our NAV, decrease the amount of cash we have available for operations and new investments and adversely impact the value of your investment.

We may also defer operating expenses or pay expenses (including the fees of the Adviser or distributions to the Special Limited Partner) with shares of our common stock or Operating Partnership units in order to preserve cash flow for the payment of distributions. The ultimate repayment of these deferred expenses could adversely affect our operations and reduce the future return on your investment. The payment of expenses in shares of our common stock or with Operating Partnership units will dilute your ownership interest in our portfolio of assets. There is no guarantee any of our operating expenses will be deferred and the Adviser and Special Limited Partner are under no obligation to receive future fees or distributions in shares of our common stock or Operating Partnership units and may elect to receive such amounts in cash.

Payments to the Adviser or the Special Limited Partner in the form of common stock or Operating Partnership units they elect to receive in lieu of fees or distributions will dilute future cash available for distribution to our stockholders.

The Adviser or the Special Limited Partner may choose to receive, and have in the past received, our common stock or Operating Partnership units in lieu of certain fees or distributions. The holders of all Operating Partnership units are entitled to receive cash from operations pro rata with the distributions being paid to us and such distributions to the holder of the Operating Partnership units will reduce the cash available for distribution to us and to our stockholders. Furthermore, under certain circumstances the Operating Partnership units held by the Adviser or the Special Limited Partner are required to be repurchased, in cash at the holder’s election, and there may not be sufficient cash to make such a repurchase payment; therefore, we may need to use cash from operations, borrowings, offering proceeds or other sources to make the payment, which will reduce cash available for distribution to you or for investment in our operations. Repurchases of our shares or Operating Partnership units from the Adviser paid to the Adviser as a management fee are not subject to the monthly and quarterly volume limitations or the Early Purchase Deduction, and such sales receive priority over other shares being put for repurchase during such period. Repurchases of our shares or Operating Partnership units from the Special Limited Partner distributed to the Special Limited Partner with respect to its performance participation interest are not subject to the Early Purchase Deduction, but, in the case of shares, such repurchases are subject to the monthly and quarterly volume limitations and do not receive priority over other shares being put for repurchase during such period.

Purchases and repurchases of our shares of our common stock are not made based on the current NAV per share of our common stock.

Generally, our offering price per share and the price at which we make repurchases of our shares will equal the NAV per share of the applicable class as of the last calendar day of the prior month, plus, in the case of our offering price, applicable upfront selling commissions and dealer manager fees. The NAV per share as of the date on which you make your subscription request or repurchase request may be significantly different than the offering price you pay or the repurchase price you receive. In addition, we may offer and repurchase shares at a price that we believe reflects the NAV per share of such stock more appropriately than the prior month’s NAV per share, including by updating a previously disclosed offering price, in cases where we believe there has been a material change (positive or negative) to our NAV per share since the end of the prior month. In such cases, the offering price and repurchase price will not equal our NAV per share as of any time.

8

Valuations and appraisals of our properties and real estate-related securities are estimates of fair value and may not necessarily correspond to realizable value.

For the purposes of calculating our monthly NAV, our properties will generally initially be valued at cost, which we expect to represent fair value at that time. Thereafter, valuations of properties will be determined by the Adviser based in part on appraisals of each of our properties by independent third-party appraisal firms reviewed by our independent valuation advisor at least once per year in accordance with valuation guidelines approved by our board of directors. The Adviser will also conduct a monthly valuation of our properties that will be reviewed and confirmed for reasonableness by our independent valuation advisor. Likewise, our investments in real estate-related securities will initially be valued at cost, and thereafter will be valued monthly at fair market value. Although monthly valuations of each of our real properties will be reviewed and confirmed for reasonableness by our independent valuation adviser, such valuations are based on asset and portfolio level information provided by the Adviser, including historical operating revenues and expenses of the properties, lease agreements on the properties, revenues and expenses of the properties, information regarding recent or planned capital expenditures and any other information relevant to valuing the real estate property, which information will not be independently verified by our independent valuation adviser. In addition, our investments in real estate-related securities, while a component of NAV, will be valued by the Adviser, based on market quotations or at fair value, and will not be reviewed by our independent valuation advisor or appraised.

Within the parameters of our valuation guidelines, the valuation methodologies used to value our properties will involve subjective judgments and projections and may not be accurate. Valuation methodologies will also involve assumptions and opinions about future events, which may or may not turn out to be correct. Valuations and appraisals of our properties and real estate-related securities will be only estimates of fair value. Ultimate realization of the value of an asset depends to a great extent on economic, market and other conditions beyond our control and the control of the Adviser and our independent valuation adviser. Further, valuations do not necessarily represent the price at which an asset would sell, since market prices of assets can only be determined by negotiation between a willing buyer and seller. As such, the carrying value of an asset may not reflect the price at which the asset could be sold in the market, and the difference between carrying value and the ultimate sales price could be material. In addition, accurate valuations are more difficult to obtain in times of low transaction volume because there are fewer market transactions that can be considered in the context of the appraisal. There will be no retroactive adjustment in the valuation of such assets, the offering price of our shares of common stock, the price we paid to repurchase shares of our common stock or NAV-based fees we paid to the Adviser and Blackstone Advisory Partners L.P. (the “Dealer Manager”), an affiliate of the Adviser, to the extent such valuations prove to not accurately reflect the realizable value of our assets. Because the price you will pay for shares of our common stock in the Offering, and the price at which your shares may be repurchased by us pursuant to our share repurchase plan are generally based on our prior month’s NAV per share, you may pay more than realizable value or receive less than realizable value for your investment.

Our NAV per share amounts may change materially if the appraised values of our properties materially change from prior appraisals or the actual operating results for a particular month differ from what we originally budgeted for that month.

We anticipate that the annual appraisals of our properties will be conducted on a rolling basis, such that properties may be appraised at different times but each property would be appraised at least once per year. When these appraisals are reflected in our NAV calculations, there may be a material change in our NAV per share amounts for each class of our common stock from those previously reported. In addition, actual operating results for a given month may differ from what we originally budgeted for that month, which may cause a material increase or decrease in the NAV per share amounts. We will not retroactively adjust the NAV per share of each class reported for the previous month. Therefore, because a new annual appraisal may differ materially from the prior appraisal or the actual results from operations may be better or worse than what we previously budgeted for a particular month, the adjustment to reflect the new appraisal or actual operating results may cause the NAV per share for each class of our common stock to increase or decrease, and such increase or decrease will occur on the day the adjustment is made.

It may be difficult to reflect, fully and accurately, material events that may impact our monthly NAV.

The Adviser’s determination of our monthly NAV per share will be based in part on appraisals of each of our properties provided annually by independent third-party appraisal firms in individual appraisal reports reviewed by our independent valuation advisor in accordance with valuation guidelines approved by our board of directors. As a result, our published NAV per share in any given month may not fully reflect any or all changes in value that may have occurred since the most recent appraisal. The Adviser will review appraisal reports and monitor our properties and real estate-related securities, and is responsible for notifying the independent valuation adviser of the occurrence of any property-specific or market-driven event it believes may cause a material valuation change in the real estate valuation, but it may be difficult to reflect fully and accurately rapidly changing market conditions or material events that may impact the value of our properties and real estate-related securities or liabilities between valuations, or to obtain quickly complete information regarding any such events. For example, an unexpected termination or renewal of a material lease, a material increase or decrease in vacancies or an unanticipated structural or environmental event at a property may cause the value of a property to change materially, yet obtaining sufficient relevant information after the occurrence has come to light and/or analyzing fully the

9

financial impact of such an event may be difficult to do and may require some time. As a result, the NAV per share may not reflect a material event until such time as sufficient information is available and analyzed, and the financial impact is fully evaluated, such that our NAV may be appropriately adjusted in accordance with our valuation guidelines. Depending on the circumstance, the resulting potential disparity in our NAV may be in favor of either stockholders who repurchase their shares, or stockholders who buy new shares, or existing stockholders.

NAV calculations are not governed by governmental or independent securities, financial or accounting rules or standards.

The methods used by our Adviser and State Street to calculate our NAV, including the components used in calculating our NAV, is not prescribed by rules of the SEC or any other regulatory agency. Further, there are no accounting rules or standards that prescribe which components should be used in calculating NAV, and our NAV is not audited by our independent registered public accounting firm. We calculate and publish NAV solely for purposes of establishing the price at which we sell and repurchase shares of our common stock, and you should not view our NAV as a measure of our historical or future financial condition or performance. The components and methodology used in calculating our NAV may differ from those used by other companies now or in the future.

In addition, calculations of our NAV, to the extent that they incorporate valuations of our assets and liabilities, are not prepared in accordance with generally accepted accounting principles. These valuations may differ from liquidation values that could be realized in the event that we were forced to sell assets. You should carefully review the disclosure of our valuation policies and how NAV will be calculated, including the illustrative hypothetical calculation of NAV, under “Net Asset Value Calculation and Valuation Guidelines.”

We face risks associated with the deployment of our capital.

In light of the nature of our continuous offering and our investment strategy and the need to be able to deploy capital quickly to capitalize on potential investment opportunities, if we have difficulty identifying and purchasing suitable properties on attractive terms, there could be a delay between the time we receive net proceeds from the sale of shares of our common stock in the Offering and the time we invest the net proceeds. We may also from time to time hold cash pending deployment into investments or have less than our targeted leverage, which cash or shortfall in target leverage may at times be significant, particularly at times when we are receiving high amounts of offering proceeds and/or times when there are few attractive investment opportunities. Such cash may be held in an account for the benefit of our stockholders that may be invested in money market accounts or other similar temporary investments.

In the event we are unable to find suitable investments such cash may be maintained for longer periods which would be dilutive to overall investment returns. This could cause a substantial delay in the time it takes for your investment to realize its full potential return and could adversely affect our ability to pay regular distributions of cash flow from operations to you. It is not anticipated that the temporary investment of such cash into money market accounts or other similar temporary investments pending deployment into investments will generate significant interest, and investors should understand that such low interest payments on the temporarily invested cash may adversely affect overall returns. In the event we fail to timely invest the net proceeds of the Offering or do not deploy sufficient capital to meet our targeted leverage, our results of operations and financial condition may be adversely affected.

Our board of directors may, in the future, adopt certain measures under Maryland law without stockholder approval that may have the effect of making it less likely that a stockholder would receive a “control premium” for his or her shares.

Corporations organized under Maryland law with a class of registered securities and at least three independent directors are permitted to elect to be subject, by a charter or bylaw provision or a board of directors resolution and notwithstanding any contrary charter or bylaw provision, to any or all of five provisions:

|

|

• |

staggering the board of directors into three classes; |

|

|

• |

requiring a two-thirds vote of stockholders to remove directors; |

|

|

• |

providing that only the board of directors can fix the size of the board; |

|

|

• |

providing that all vacancies on the board, regardless of how the vacancy was created, may be filled only by the affirmative vote of a majority of the remaining directors in office and for the remainder of the full term of the class of directors in which the vacancy occurred; and |

|

|

• |

providing for a majority requirement for the calling of a special meeting of stockholders. |

10

These provisions may discourage an extraordinary transaction, such as a merger, tender offer or sale of all or substantially all of our assets, all of which might provide a premium price for stockholders’ shares. In our charter, we have elected that vacancies on our board of directors be filled only by the remaining directors and for the remainder of the full term of the directorship in which the vacancy occurred. Through other provisions in our charter and bylaws, we vest in our board of directors the exclusive power to fix the number of directorships, provided that the number is not less than three. We have not elected to be subject to any of the other provisions described above, but our charter does not prohibit our board of directors from opting into any of these provisions in the future.

Further, under the Maryland Business Combination Act, we may not engage in any merger or other business combination with an “interested stockholder” (which is defined as (1) any person who beneficially owns, directly or indirectly, 10% or more of the voting power of our outstanding voting stock and (2) an affiliate or associate of ours who, at any time within the two-year period prior to the date in question, was the beneficial owner, directly or indirectly, of 10% or more of the voting power of our then outstanding stock) or any affiliate of that interested stockholder for a period of five years after the most recent date on which the interested stockholder became an interested stockholder. A person is not an interested stockholder if our board of directors approved in advance the transaction by which he would otherwise have become an interested stockholder. In approving a transaction, our board of directors may provide that its approval is subject to compliance, at or after the time of approval, with any terms or conditions determined by our board of directors. After the five-year period ends, any merger or other business combination with the interested stockholder or any affiliate of the interested stockholder must be recommended by our board of directors and approved by the affirmative vote of at least:

|

|

• |

80% of all votes entitled to be cast by holders of outstanding shares of our voting stock; and |

|

|

• |

two-thirds of all of the votes entitled to be cast by holders of outstanding shares of our voting stock other than those shares owned or held by the interested stockholder with whom or with whose affiliate the business combination is to be effected or held by an affiliate or associate of the interested stockholder. |

These supermajority voting provisions do not apply if, among other things, our stockholders receive a minimum payment for their common stock equal to the highest price paid by the interested stockholder for its shares.

The statute permits various exemptions from its provisions, including business combinations that are exempted by our board of directors prior to the time the interested stockholder becomes an interested stockholder. Our board of directors has adopted a resolution exempting any business combination involving us and any person, including Blackstone, the Dealer Manager and the Adviser, from the provisions of this law, provided that such business combination is first approved by our board of directors.

Our charter permits our board of directors to cause us to issue preferred stock on terms that may subordinate the rights of the holders of our current common stock or discourage a third party from acquiring us.

Our board of directors is permitted, subject to certain restrictions set forth in our charter, to authorize the issuance of shares of preferred stock without stockholder approval. Further, our board of directors may classify or reclassify any unissued shares of common or preferred stock into other classes or series of stock and establish the preferences, conversion or other rights, voting powers, restrictions, limitations as to dividends and other distributions, qualifications, and terms or conditions of redemption of the stock and may amend our charter from time to time to increase or decrease the aggregate number of shares or the number of shares of any class or series that we have authority to issue without stockholder approval. Thus, our board of directors could authorize us to issue shares of preferred stock with terms and conditions that could subordinate the rights of the holders of our common stock or have the effect of delaying, deferring or preventing a change in control of us, including an extraordinary transaction such as a merger, tender offer or sale of all or substantially all of our assets, that might provide a premium price for holders of our common stock.

Maryland law limits, in some cases, the ability of a third party to vote shares acquired in a “control share acquisition.”

The Maryland Control Share Acquisition Act provides that “control shares” of a Maryland corporation acquired in a “control share acquisition” have no voting rights except to the extent approved by stockholders by a vote of two-thirds of the votes entitled to be cast on the matter. Shares of stock owned by the acquirer, by officers or by employees who are directors of the corporation, are excluded from shares entitled to vote on the matter. “Control shares” are voting shares of stock which, if aggregated with all other shares of stock owned by the acquirer or in respect of which the acquirer can exercise or direct the exercise of voting power (except solely by virtue of a revocable proxy), would entitle the acquirer to exercise voting power in electing directors within specified ranges of voting power. Control shares do not include shares the acquiring person is then entitled to vote as a result of having previously obtained stockholder approval. A “control share acquisition” means the acquisition of issued and outstanding control shares. The control share acquisition statute does not apply: (1) to shares acquired in a merger, consolidation or statutory share exchange if the Maryland corporation is a party to the transaction; or (2) to acquisitions approved or exempted by the charter or bylaws of the Maryland

11

corporation. Our bylaws contain a provision exempting from the Control Share Acquisition Act any and all acquisitions of our stock by any person. There can be no assurance that this provision will not be amended or eliminated at any time in the future.

Maryland law and our organizational documents limit our rights and the rights of our stockholders to recover claims against our directors and officers, which could reduce your and our recovery against them if they cause us to incur losses.

Maryland law provides that a director will not have any liability as a director so long as he or she performs his or her duties in accordance with the applicable standard of conduct. In addition, our charter generally limits the personal liability of our directors and officers for monetary damages subject to the limitations of the North American Securities Administrators Association’s Statement of Policy Regarding Real Estate Investment Trusts, as revised and adopted on May 7, 2007 and Maryland law. Maryland law and our charter provide that no director or officer shall be liable to us or our stockholders for monetary damages unless the director or officer (1) actually received an improper benefit or profit in money, property or services or (2) was actively and deliberately dishonest as established by a final judgment as material to the cause of action. Moreover, our charter generally requires us to indemnify and advance expenses to our directors and officers for losses they may incur by reason of their service in those capacities unless their act or omission was material to the matter giving rise to the proceeding and was committed in bad faith or was the result of active and deliberate dishonesty, they actually received an improper personal benefit in money, property or services or, in the case of any criminal proceeding, they had reasonable cause to believe the act or omission was unlawful. Further, we have entered into separate indemnification agreements with each of our officers and directors. As a result, you and we may have more limited rights against our directors or officers than might otherwise exist under common law, which could reduce your and our recovery from these persons if they act in a manner that causes us to incur losses. In addition, we are obligated to fund the defense costs incurred by these persons in some cases. However, our charter provides that we may not indemnify our directors or officers, or the Adviser and its affiliates, for any liability or loss suffered by them or hold our directors or officers, the Adviser and its affiliates harmless for any liability or loss suffered by us, unless they have determined, in good faith, that the course of conduct that caused the loss or liability was in our best interests, they were acting on our behalf or performing services for us, the liability or loss was not the result of negligence or misconduct by our non-independent directors, the Adviser and its affiliates, or gross negligence or willful misconduct by our independent directors, and the indemnification or agreement to hold harmless is recoverable only out of our net assets or the proceeds of insurance and not from the stockholders.

Maryland law and our organizational documents limit our stockholders’ ability to amend our charter or dissolve us without the approval of our board of directors.

Although the Statement of Policy Regarding Real Estate Investment Trusts published by the North American Securities Administrators Association (“NASAA”) indicates that stockholders are permitted to amend our charter or terminate us without the necessity for concurrence by our board of directors, we are required to comply with the Maryland General Corporation Law, which provides that any amendment to our charter or any dissolution of our company must first be declared advisable by our board of directors. Therefore, our stockholders may vote to authorize the amendment of our charter or the dissolution of our company, but only after such action has been declared advisable by our board of directors. Accordingly, the only proposals to amend our charter or to dissolve our company that will be presented to our stockholders will be those that have been declared advisable by our board of directors and also require approval by our stockholders.

Your interest in us will be diluted if we issue additional shares. Your interest in our assets will also be diluted if the Operating Partnership issues additional units.

Holders of our common stock will not have preemptive rights to any shares we issue in the future. Our charter authorizes us to issue up to 2,100,000,000 shares of capital stock, of which 2,000,000,000 shares are classified as common stock, of which 500,000,000 shares are classified as Class T shares, 500,000,000 shares are classified as Class S shares, 500,000,000 shares are classified as Class D shares and 500,000,000 are classified as Class I shares, and 100,000,000 shares are classified as preferred stock. In addition, our board of directors may amend our charter from time to time to increase or decrease the aggregate number of authorized shares of capital stock or the number of authorized shares of capital stock of any class or series without stockholder approval. After you purchase shares of our common stock in the Offering, our board of directors may elect, without stockholder approval, to: (1) sell additional shares in this or future public offerings; (2) issue shares of our common stock or units in our Operating Partnership in private offerings; (3) issue shares of our common stock or units in our Operating Partnership upon the exercise of the options we may grant to our independent directors or future employees; (4) issue shares of our common stock or units in our Operating Partnership to the Adviser or the Special Limited Partner, or their successors or assigns, in payment of an outstanding obligation to pay fees for services rendered to us or the performance participation allocation; (5) issue shares of our common stock or units in our Operating Partnership to sellers of properties we acquire, or (6) issue equity incentive compensation to the senior executive officers of affiliated service providers or to third parties as satisfaction of obligations under incentive compensation arrangements. To the extent we issue additional shares of common stock after your purchase in the Offering, your percentage ownership interest in us will be diluted.

12

Because we hold all of our assets through the Operating Partnership, to the extent we issue additional units of our Operating Partnership after you purchase in the Offering, your percentage ownership interest in our assets will be diluted. Because certain classes of the units of our Operating Partnership may, in the discretion of our board of directors, be exchanged for shares of our common stock, any merger, exchange or conversion between our Operating Partnership and another entity ultimately could result in the issuance of a substantial number of shares of our common stock, thereby diluting the percentage ownership interest of other stockholders. Because of these and other reasons, our stockholders may experience substantial dilution in their percentage ownership of our shares or their interests in the underlying assets held by our Operating Partnership. Operating Partnership units may have different and preferential rights to the claims of common units of our Operating Partnership which correspond to the common stock held by our stockholders. Certain units in our Operating Partnership may have different and preferential rights to the terms of the common Operating Partnership units which correspond to the common stock held by our stockholders.

We are not required to comply with certain reporting requirements, including those relating to auditor’s attestation reports on the effectiveness of our system of internal control over financial reporting, accounting standards and disclosure about our executive compensation, that apply to other public companies.

The JOBS Act contains provisions that, among other things, relax certain reporting requirements for emerging growth companies, including certain requirements relating to accounting standards and compensation disclosure. We are classified as an emerging growth company. For as long as we are an emerging growth company, which may be up to five full fiscal years, unlike other public companies, we are not required to (1) provide an auditor’s attestation report on the effectiveness of our system of internal control over financial reporting pursuant to Section 404 of the Sarbanes-Oxley Act, (2) comply with any new or revised financial accounting standards applicable to public companies until such standards are also applicable to private companies under Section 102(b)(1) of the JOBS Act, (3) comply with any new requirements adopted by the Public Company Accounting Oversight Board (“PCAOB”) requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and the financial statements of the issuer, (4) comply with any new audit rules adopted by the PCAOB after April 5, 2012 unless the SEC determines otherwise, (5) provide certain disclosure regarding executive compensation required of larger public companies or (6) hold stockholder advisory votes on executive compensation.

Once we are no longer an emerging growth company, so long as our shares of common stock are not traded on a securities exchange, we will be deemed to be a “non-accelerated filer” under the Exchange Act, and as a non-accelerated filer, we will be exempt from compliance with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act. In addition, so long as we are externally managed by the Adviser and we do not directly compensate our executive officers, or reimburse the Adviser or its affiliates for salaries, bonuses, benefits and severance payments for persons who also serve as one of our executive officers or as an executive officer of the Adviser, we do not have any executive compensation, making the exemptions listed in (5) and (6) above generally inapplicable.

We cannot predict if investors will find our common stock less attractive because we choose to rely on any of the exemptions discussed above.

As noted above, under the JOBS Act, emerging growth companies can delay adopting new or revised accounting standards that have different effective dates for public and private companies until such time as those standards apply to private companies. We have elected to opt out of this transition period, and will therefore comply with new or revised accounting standards on the applicable dates on which the adoption of these standards is required for non-emerging growth companies. This election is irrevocable.

Our UPREIT structure may result in potential conflicts of interest with limited partners in our Operating Partnership whose interests may not be aligned with those of our stockholders.

Our directors and officers have duties to our corporation and our stockholders under Maryland law and our charter in connection with their management of the corporation. At the same time, we, as general partner, have fiduciary duties under Delaware law to our Operating Partnership and to the limited partners in connection with the management of our Operating Partnership. Our duties as general partner of our Operating Partnership and its partners may come into conflict with the duties of our directors and officers to the corporation and our stockholders. Under Delaware law, a general partner of a Delaware limited partnership owes its limited partners the duties of good faith and fair dealing. Other duties, including fiduciary duties, may be modified or eliminated in the partnership’s partnership agreement. The partnership agreement of our Operating Partnership provides that, for so long as we own a controlling interest in our Operating Partnership, any conflict that cannot be resolved in a manner not adverse to either our stockholders or the limited partners may be resolved in favor of our stockholders.

13

Additionally, the partnership agreement expressly limits our liability by providing that we and our officers, directors, agents and employees will not be liable or accountable to our Operating Partnership for losses sustained, liabilities incurred or benefits not derived if we or our officers, directors, agents or employees acted in good faith. In addition, our Operating Partnership is required to indemnify us and our officers, directors, employees, agents and designees to the extent permitted by applicable law from and against any and all claims arising from operations of our Operating Partnership, unless it is established that: (1) the act or omission was material to the matter giving rise to the proceeding and either was committed in bad faith or was the result of active and deliberate dishonesty; (2) the indemnified party received an improper personal benefit in money, property or services; or (3) in the case of a criminal proceeding, the indemnified person had reasonable cause to believe that the act or omission was unlawful.

The provisions of Delaware law that allow the fiduciary duties of a general partner to be modified by a partnership agreement have not been tested in a court of law, and we have not obtained an opinion of counsel covering the provisions set forth in the partnership agreement that purport to waive or restrict our fiduciary duties.

Your investment return may be reduced if we are required to register as an investment company under the Investment Company Act.