Attached files

| file | filename |

|---|---|

| EX-32.1 - EX-32.1 - RLJ ENTERTAINMENT, INC. | rlje-ex321_7.htm |

| EX-31.2 - EX-31.2 - RLJ ENTERTAINMENT, INC. | rlje-ex312_9.htm |

| EX-31.1 - EX-31.1 - RLJ ENTERTAINMENT, INC. | rlje-ex311_10.htm |

| EX-23.1 - EX-23.1 - RLJ ENTERTAINMENT, INC. | rlje-ex231_6.htm |

| EX-21.1 - EX-21.1 - RLJ ENTERTAINMENT, INC. | rlje-ex211_8.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2017

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period from to

Commission File Number 001-35675

RLJ ENTERTAINMENT, INC.

(Exact name of registrant as specified in its charter)

|

Nevada |

45-4950432 |

|

(State or other jurisdiction of incorporation) |

(I.R.S. Employer Identification Number) |

8515 Georgia Avenue, Suite 650, Silver Spring, Maryland, 20910

(Address of principal executive offices, including zip code)

(301) 608-2115

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

|

Title of Each Class: |

|

Name of Each Exchange on Which Registered: |

|

|

|

Common Stock, par value $0.001 |

|

NASDAQ Capital Market |

|

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☐ NO ☒

Indicate by check mark if the registrant is not required to file report pursuant to Section 13 or Section 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☒ NO ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ☒ NO ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer |

☐ |

|

|

Accelerated filer |

☐ |

|

Non-accelerated filer |

☐ |

(Do not check if a smaller reporting company) |

|

Smaller reporting company |

☒ |

|

|

|

|

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☒

The aggregate market value of the voting stock held by non-affiliates computed on June 30, 2017, based on the sales price of $3.31 per share: Common Stock - $10,958,026. All directors and executive officers have been deemed, solely for the purpose of the foregoing calculation, to be “affiliates” of the registrant; however, this determination does not constitute an admission of affiliate status for any of these shareholders.

The number of shares outstanding of the registrant’s common stock as of February 28, 2018: 14,564,678

DOCUMENTS INCORPORATED BY REFERENCE

None.

Form 10-K Annual Report

For the Year Ended December 31, 2017

TABLE OF CONTENTS

|

|

|

|

|

4 |

|

|

|

|

|

|

|

|

|

|

ITEM 1. |

|

|

4 |

|

|

|

ITEM 1A. |

|

|

11 |

|

|

|

ITEM 1B. |

|

|

17 |

|

|

|

ITEM 2. |

|

|

18 |

|

|

|

ITEM 3. |

|

|

18 |

|

|

|

ITEM 4. |

|

|

18 |

|

|

|

|

|

|

|

|

|

|

|

|

|

19 |

|

|

|

|

|

|

|

|

|

|

ITEM 5. |

|

|

19 |

|

|

|

ITEM 6. |

|

|

20 |

|

|

|

ITEM 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

20 |

|

|

ITEM 7A. |

|

|

36 |

|

|

|

ITEM 8. |

|

|

37 |

|

|

|

ITEM 9. |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

74 |

|

|

ITEM 9A. |

|

|

74 |

|

|

|

ITEM 9B. |

|

|

75 |

|

|

|

|

|

|

|

|

|

|

|

|

|

76 |

|

|

|

|

|

|

|

|

|

|

ITEM 10. |

|

|

76 |

|

|

|

ITEM 11. |

|

|

81 |

|

|

|

ITEM 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

85 |

|

|

ITEM 13. |

|

Certain Relationships and Related Transactions and Director Independence |

|

87 |

|

|

ITEM 14. |

|

|

91 |

|

|

|

|

|

|

|

|

|

|

|

|

|

92 |

|

|

|

|

|

|

|

|

|

|

ITEM 15. |

|

|

92 |

|

|

|

ITEM 16. |

|

|

94 |

|

|

|

|

|

|

|

|

|

|

|

|

95 |

||

|

|

|

|

|

|

|

|

Certifications |

|

|

|

|

|

This Annual Report on Form 10-K for the year ended December 31, 2017 (or Annual Report) includes forward-looking statements that involve risks and uncertainties within the meaning of the Private Securities Litigation Reform Act of 1995. Other than statements of historical fact, all statements made in this Annual Report are forward-looking, including, but not limited to, statements regarding industry prospects, future results of operations or financial position, and statements of our intent, belief and current expectations about our strategic direction, prospective and future results and condition. In some cases, forward-looking statements may be identified by words such as “will,” “should,” “could,” “may,” “might,” “expect,” “plan,” “possible,” “potential,” “predict,” “anticipate,” “believe,” “estimate,” “continue,” “future,” “intend,” “project” or similar words. The use of “we,” “our” or “us” within this Annual Report is referring to RLJ Entertainment, Inc. and its subsidiaries.

Forward-looking statements involve risks and uncertainties that are inherently difficult to predict, which could cause actual outcomes and results to differ materially from our expectations, forecasts and assumptions. Factors that might cause such differences include, but are not limited to:

|

|

• |

Our financial performance, including our ability to achieve improved results from operations and improved earnings before income tax, depreciation and amortization, non-cash royalty expense, interest expense, non-cash exchange gains and losses on intercompany accounts, goodwill impairments, restructuring costs, change in fair value of stock warrants and other derivatives, stock-based compensation, basis-difference amortization in equity earnings of affiliate and dividends received from affiliate in excess of equity earnings of affiliate (or Adjusted EBITDA); |

|

|

• |

Our expectation that revenues and financial performance of our digital channels will continue to grow and have a positive effect on our liquidity, cash flows and operating results; |

|

|

• |

The effects of limited cash liquidity on operational performance; |

|

|

• |

Our obligations under the credit agreement; |

|

|

• |

Our ability to satisfy financial ratios; |

|

|

• |

Our ability to generate sufficient cash flows from operating activities; |

|

|

• |

Our ability to fund planned capital expenditures and development efforts; |

|

|

• |

Our inability to gauge and predict the commercial success of our programming; |

|

|

• |

Our ability to maintain relationships with customers, employees and suppliers, including our ability to enter into revised payment plans, when necessary, with our vendors that are acceptable to all parties; |

|

|

• |

Our ability to realize anticipated synergies and other efficiencies in connection with the AMC transaction, as defined in this Annual Report under Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources – Capital Resources – Senior Term Notes; |

|

|

• |

Delays in the release of new titles or other content; |

|

|

• |

The effects of disruptions in our supply chain; |

|

|

• |

The loss of key personnel; or |

|

|

• |

Our public securities’ limited liquidity and trading. |

You should carefully consider and evaluate all of the information in this Annual Report, including the risk factors listed above and elsewhere, including “Item 1A. Risk Factors” below. If any of these risks occur, our business, results of operations and financial condition could be harmed, the price of our common stock could decline, and you may lose all or part of your investment, and future events and circumstances could differ significantly from those anticipated in the forward-looking statements contained in this Annual Report. Unless otherwise required by law, we undertake no obligation to release publicly any updates or revisions to any such forward-looking statements that may reflect events or circumstances occurring after the date of this Annual Report.

3

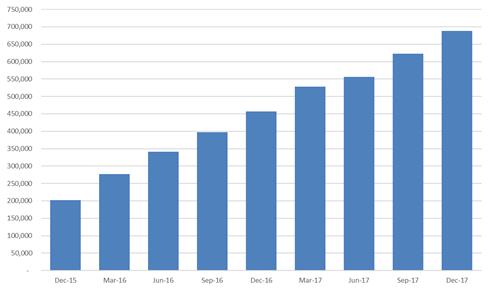

RLJ Entertainment, Inc. (RLJE or the Company) is a premium digital channel company serving distinct audiences through its proprietary subscription-based digital channels, Acorn TV and UMC or Urban Movie Channel. Acorn TV features high-quality British and international mysteries and dramas. UMC showcases compelling urban programming including feature films, documentaries, original series, stand-up comedy and other exclusive content for African-American and urban audiences. The digital channels have consistently experienced substantial year-over-year growth rate since launch in 2011 and 2015, respectively. The table below shows quarterly subscriber growth from December 2015 to December 2017.

We exclusively control, co-produce, and own a large library of content primarily consisting of British mysteries and dramas, independent feature films and urban content. In addition to supporting our digital channels, the value of our content library is monetized through our intellectual property (or IP) licensing and wholesale distribution operations. These activities allow us to control all windows of exploitation of our content. Our IP licensing operations consist of content that we own and includes our 64% investment in Agatha Christie Ltd. (or ACL), while our wholesale distribution operations consist of content we license from others.

Strategic Growth of the Company

We expect to increase our subscriber growth to one million subscribers within 12 to 18 months. To that end, our growth initiatives include the following:

|

|

• |

Development and acquisition of compelling, exclusive and original programming targeted to distinct audiences; |

|

|

• |

Continued promotional support of our digital channels and program releases; |

|

|

• |

Expansion of the distribution and geographic footprint of our digital channels; and |

|

|

• |

Continued enhancement of our subscribers’ experience through continuously improving mobile apps and digital platforms. |

We believe that the convergence of television (TV) and the internet will promote the continued migration of consumers from bundled offerings to a la carte subscriptions significantly benefitting digital over-the-top (or OTT) platforms like Acorn TV and UMC. As a result, we have aligned our goals to (i) continue to develop unique brands that appeal to and capture dedicated audiences, (ii) develop strong content offerings that consumers are willing to purchase and (iii) provide superior service. Our goal is to continue to develop strong media brands that are a preferred destination and a “must-have” subscription for our audiences.

4

We develop or acquire content that is intended to satisfy the desire of our niche audiences. We also acquire finished programs through long-term exclusive contracts. We invest in content that we believe will increase our digital channel subscribers’ interests and subscriptions as well as exceed our internal return-on-investment.

Sales and Marketing

We maintain our own sales force and also direct selling relationships with the majority of our broadcast and cable/satellite partners and retail customers. Our in-house marketing department manages promotional efforts across a wide range of off-line and online platforms.

Segments

Management views our operations based on three distinct reporting segments: (1) the Digital Channels segment; (2) the IP Licensing segment; and (3) the Wholesale Distribution segment. Operations and net assets that are not associated with any of these operating segments are reported as “Corporate” when disclosing and discussing segment information. The Digital Channels segment distributes film and television content through our proprietary subscription-based digital channels, Acorn TV and UMC. The IP Licensing segment includes intellectual property rights that we own, produce and then license; and includes our 64% ownership of ACL. Our Wholesale Distribution segment consists of the worldwide exploitation of exclusive content in various formats including digital (download-to-rent and electronic sell-through, or EST), television video on demand (VOD) through cable and satellite, broadcast, streaming, and DVD and Blu-ray through third-party media and retail outlets. The Wholesale Distribution and IP Licensing segments exploit content to third parties such as Amazon, Best Buy, iTunes, Netflix, Target and Walmart.

Total revenues by reporting segment for the periods presented are as follows:

|

|

|

Years Ended December 31, |

|

|||||

|

(In thousands) |

|

2017 |

|

|

2016 |

|

||

|

Digital Channels |

|

$ |

27,194 |

|

|

$ |

16,262 |

|

|

IP Licensing |

|

|

47 |

|

|

|

168 |

|

|

Wholesale Distribution |

|

|

59,063 |

|

|

|

63,808 |

|

|

Total revenues |

|

$ |

86,304 |

|

|

$ |

80,238 |

|

Our reported revenues exclude the revenues of ACL as we account for ACL using the equity method of accounting. ACL’s net revenues were $18.5 million and $19.5 million for the years ended December 31, 2017 and 2016, respectively.

Total assets for each reporting segment and Corporate as of December 31, 2017 and 2016 are as follows:

|

|

|

December 31, |

|

|||||

|

(In thousands) |

|

2017 |

|

|

2016 |

|

||

|

Digital Channels |

|

$ |

11,148 |

|

|

$ |

5,941 |

|

|

IP Licensing |

|

|

23,981 |

|

|

|

18,648 |

|

|

Wholesale Distribution |

|

|

104,987 |

|

|

|

102,748 |

|

|

Corporate |

|

|

7,473 |

|

|

|

8,643 |

|

|

Total Assets |

|

$ |

147,589 |

|

|

$ |

135,980 |

|

Digital Channels

A summary of the Digital Channels segment’s revenues and expenses is as follows:

|

|

|

Years Ended December 31, |

|

|||||

|

(In thousands) |

|

2017 |

|

|

2016 |

|

||

|

Revenues |

|

$ |

27,194 |

|

|

$ |

16,262 |

|

|

Operating costs and expenses |

|

|

(17,364 |

) |

|

|

(9,297 |

) |

|

Depreciation and amortization |

|

|

(1,055 |

) |

|

|

(618 |

) |

|

Digital Channels segment contribution |

|

$ |

8,775 |

|

|

$ |

6,347 |

|

5

The Digital Channels segment exploits much of the same film and television content as the Wholesale Distribution segment but exploits the content to consumers through various proprietary subscription video on demand (or SVOD) channels. To date, we have two primary digital channels, which are Acorn TV and UMC. We are continually rolling-out new programming on our digital channels and attracting new subscribers. As of December 31, 2017, our Digital Channels segment had over 680,000 subscribers compared to 457,000 subscribers at December 31, 2016.

IP Licensing

A summary of the IP Licensing segment’s revenues and expenses is as follows:

|

|

|

Years Ended December 31, |

|

|||||

|

(In thousands) |

|

2017 |

|

|

2016 |

|

||

|

Revenues |

|

$ |

47 |

|

|

$ |

168 |

|

|

Operating costs and expenses |

|

|

(455 |

) |

|

|

(554 |

) |

|

Depreciation and amortization |

|

|

(128 |

) |

|

|

(134 |

) |

|

Share in ACL earnings |

|

|

5,955 |

|

|

|

3,078 |

|

|

IP Licensing segment contribution |

|

$ |

5,419 |

|

|

$ |

2,558 |

|

Our IP Licensing segment includes our 64% interest in ACL and owned intellectual property that is either owned or created by us and is licensed for exploitation worldwide.

Wholesale Distribution

A summary of the Wholesale Distribution segment’s revenues and expenses is as follows:

|

|

|

Years Ended December 31, |

|

|||||

|

(In thousands) |

|

2017 |

|

|

2016 |

|

||

|

Revenues |

|

$ |

59,063 |

|

|

$ |

63,808 |

|

|

Operating costs and expenses |

|

|

(51,084 |

) |

|

|

(60,169 |

) |

|

Depreciation and amortization |

|

|

(1,966 |

) |

|

|

(1,714 |

) |

|

Wholesale Distribution segment contribution |

|

$ |

6,013 |

|

|

$ |

1,925 |

|

The Wholesale Distribution segment consists of worldwide exploitation of exclusive content in various formats through third party media and retail outlets.

Outside North America and the United Kingdom (or U.K.), we sublicense distribution in the areas of television, digital and home entertainment through distribution partners such as Universal Music Group International, Universal Pictures Australia and Warner Music Australia, each of which pays us a royalty for their distribution of our products.

6

We focus on compelling British mystery and drama television, action and thriller independent feature films and diverse urban content, and documentaries. We exploit our titles through our various brands as follows:

|

|

|

Known for specializing in the best of British television, Acorn Media Group (or Acorn) monetizes high-quality dramas and mysteries via our digital channel Acorn TV in the United States (or U.S.) and Canada and to the broadcast/cable and home video windows within the North American, U.K. and Australian markets. In addition to consistently receiving strong national public relations coverage, our primary marketing to consumers is through Acorn TV offering viewers thousands of hours of compelling content including Acorn TV original productions and exclusive premieres of popular series. We further leverage the Acorn brand through a marketing and wholesale partnership with direct-to-consumer specialist Universal Screen Arts (or USA). USA purchases wholesale inventory from us and pays us a license fee for the exclusive right to publish a branded Acorn direct-to-consumer catalog and website (acornonline.com), which market and sell Acorn content on DVD and Blu-ray alongside complementary merchandise. Our Acorn brand generates revenues that are reported in the Digital Channels, IP Licensing (Agatha Christie revenues) and Wholesale Distribution segments (digital download and home video sales).

|

Our subsidiaries with a permanent presence in the U.K. television programming community, provide us access to new content and manage and develop our intellectual property rights. Our owned content includes 28 Foyle’s War made-for-TV films and, through our 64% ownership interest in ACL, the Agatha Christie branded library. The bestselling novelist of all time, Agatha Christie has sold more than 2 billion books, and her work contains a variety of short story collections, more than 80 novels, 19 plays and a film library of over 100 TV productions. Acorn is known for mystery and drama franchises and has been releasing TV movie adaptations featuring Agatha Christie’s two most famous characters, Hercule Poirot and Miss Marple, for over a decade with both series ranking among our all-time bestselling lines. Through ACL, we manage the vast majority of Agatha Christie publishing and television/film assets worldwide and across all mediums and actively develop new content and productions. In addition to film and television projects, in 2014, ACL published its first book since the death of Agatha Christie, The Monogram Murders, and has subsequently published its second book, Closed Casket, in 2016. The Agatha Christie family retains a 36% holding, and James Prichard, Agatha Christie’s great-grandson, is the Chairman of ACL.

|

|

|

UMC is a premium subscription-based service which features quality urban content showcasing feature films, documentaries, original series, stand-up comedy and other exclusive content for African American and urban audiences. Select UMC content is also monetized in the home video window in partnership with the Wholesale Distribution segment. |

|

|

|

RLJE Films is a leading film and television licensee focusing on action, thriller, and horror independent feature films and urban content in partnership with our digital channel UMC. RLJE Films acquires exclusive long-term film rights across all distribution channels, with terms ranging generally from 5 to 25 years. RLJE Films content is currently distributed primarily in the U.S. and Canada through theatrical, broadcast/cable, physical and digital platforms. All of the revenues generated by the RLJE Films are included in our Wholesale Distribution segment. |

Trademarks

We currently use several registered trademarks including: RLJ Entertainment, Acorn, Acorn Media, Acorn TV and UMC - Urban Movie Channel. We also currently use registered trademarks through our 64%-owned subsidiary ACL including: Agatha Christie, Miss Marple and Poirot.

7

The above-referenced trademarks, among others, are registered with the U.S. Patent and Trademark Office and various international trademark authorities. In general, trademarks remain valid and enforceable as long as the marks are used in connection with the related products and services and the required registration renewals are filed. We believe our trademarks have value in the marketing of our products. It is our policy to protect and defend our trademark rights.

Outsourced Services

Under a Distribution Services and License Agreement with Sony Pictures Home Entertainment (or SPHE), SPHE acts as our exclusive manufacturer in North America to meet our physical goods manufacturing requirements (DVD and Blu-ray) and to provide related fulfillment and other logistics services in exchange for certain fees. Our agreement with SPHE expires in August 2019. SPHE also provides certain operational services, including credit and collections, merchandising, returns processing and certain information technology (IT) functions. Under our relationship with SPHE, we are responsible for the credit risk from the end customer with respect to accounts receivable and also the risk of inventory loss with respect to the inventory they manage on our behalf.

On June 24, 2016, we entered into a licensing agreement with USA whereby USA took over our Acorn U.S. catalog/ecommerce business and became the official, exclusive, direct-to-consumer seller of Acorn product in the U.S.

In the U.S., we outsource our video delivery, streaming services and cloud hosting for our web portfolio and digital channels.

In the U.K., we have a fulfillment and logistics services arrangement with Sony DADC UK Limited, which is similar to the arrangement we have with SPHE in North America. Australian fulfilment and logistics are provided by Regency Media Pty Ltd.

Seasonality

Our subscriber growth and our Wholesale Distribution segment revenues exhibit a seasonal pattern. For our Digital Channels segment, the seasonality exists because of variations in when consumers buy internet-connected screens and when they tend to increase their viewing. For our Wholesale Distribution segment, the release timing of certain high-profile content as well as the holiday season impact the revenue stream. The fourth quarter typically represents our strongest quarter in terms of Wholesale Distribution segment revenues.

Competition

The market for entertainment video is intensely competitive and subject to rapid change. We face competition from other digital channels with similar genre and target audiences, independent distribution companies, major motion picture studios and broadcast and internet outlets in securing exclusive content distribution rights.

We also face competition from online and direct-to-consumer retailers, as well as alternative forms of leisure entertainment, including video games, the internet and other computer-related activities. Consumers can choose from a large supply of competing entertainment content from other suppliers. The success of any of our titles depends upon audience acceptance of a given program in relation to consumer tastes and cultural trends as well as the other titles released into the marketplace at or around the same time. Many of these competitors are larger than us.

Sales of digital downloading, streaming, VOD and other broadcast formats are largely driven by what is visually available to the consumer, which can be supported by additional placement fees or previous sales success. Programming is available online, delivered to smartphones, tablets, laptops, personal computers, or direct to the consumers’ TV set through multiple internet-ready devices, cable or satellite VOD and other subscription-based digital channels. For our physical wholesale distribution, our DVD and Blu-ray products compete for a finite amount of brick-and-mortar retail and rental shelf space.

Our ability to continue to successfully compete in our markets is largely dependent upon our ability to develop and secure unique and appealing content, and to anticipate and respond to various competitive factors affecting the industry, including new or changing program formats, changes in consumer preferences, regional and local economic conditions, discount pricing strategies and competitors’ promotional activities.

Industry Trends

Juniper Research reports that OTT revenues will hit $120 billion by 2020 and over 25% of households will subscribe to SVOD services by 2022.

8

According to The Digital Entertainment Group (or DEG), consumer home entertainment spending in calendar 2017 exceeded $20.5 billion, up 5% from 2016. This increase was driven by the 20% increase in total digital spending showing that consumers are continuing to build their digital film libraries.

Total digital-format revenues include EST (digital ownership), VOD (digital rental) and subscription-based streaming. EST revenues for 2017 increased by 6% compared to 2016. VOD revenues decreased 7% in 2017 compared to 2016. Total subscription VOD increased by 31% in 2017 compared to 2016.

DEG reported that in 2016 the number of U.S. households with Blu-ray playback devices, including set-top boxes and game consoles, was 88 million. DEG also reported that the number of households with HDTV (including 4K UHD) is now more than 120 million, including 30 million 4K Ultra HD TVs.

Research and Markets’ report, “Global Blu-ray Media and Players Market, Forecast to 2023”, predicts a decline of the DVD format sales as a result of increased 4K UHD players and lower physical media demand. Unit shipments for the global Blu-ray media market are expected to decrease from 595 million in 2017 to 516 million in 2023.

Employees

As of March 1, 2018, we had 98 total employees. Of these employees, 76 are based in the US and 22 are based internationally in the U.K. and Australia.

Other Information

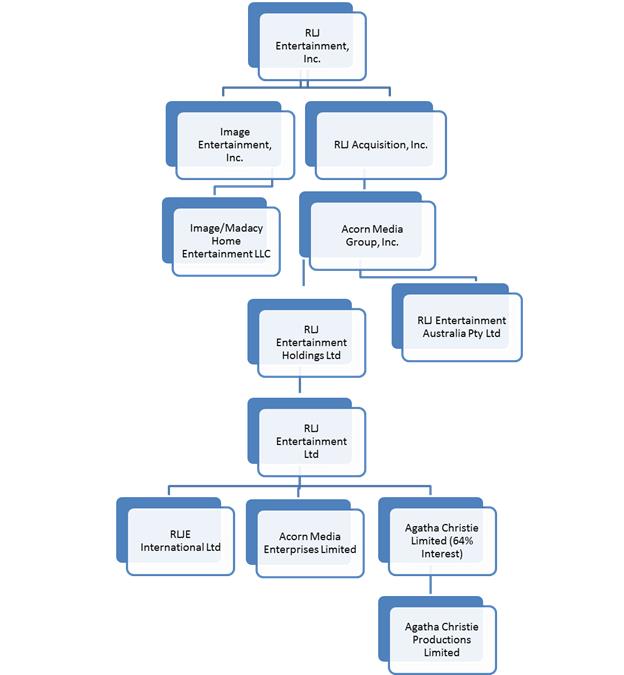

RLJE was incorporated in Nevada in April 2012. On October 3, 2012, we completed the business combination of RLJE, Image Entertainment, Inc. (or Image) and Acorn Media Group, Inc. (or Acorn Media or Acorn), which is referred to herein as the “Business Combination.” We have a direct presence in North America, the U.K. and Australia with strategic sublicense and distribution relationships covering Europe, Asia and Latin America.

9

A summary of our significant corporate entities and structure is as follows:

Under the menu “Investors—SEC Filings” on our website at www.rljentertainment.com, we provide free access to our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. The information contained on our website is not incorporated herein by reference and should not be considered part of this Annual Report.

10

Risks Relating to Our Liquidity and Credit Agreement

Our Credit Agreement contains covenants that may limit the way we conduct business. Our Credit Agreement contains various covenants limiting our ability to:

|

|

• |

incur or guarantee additional indebtedness; |

|

|

• |

grant security interests in any property; |

|

|

• |

pay dividends and make other restricted payments; |

|

|

• |

make investments; |

|

|

• |

enter into merger or acquisition transactions; |

|

|

• |

sell assets; and |

|

|

• |

enter into transactions with affiliates. |

These covenants may have an impact on our ability to raise additional debt or equity financing, compete effectively or take advantage of new business opportunities.

Our Credit Agreement includes covenants that require us to maintain specified financial ratios. Our ability to satisfy those financial ratios can be affected by events beyond our control, and we cannot be certain we will satisfy those ratios. Although we are currently in compliance with such financial ratios, there is no assurance that our financial results during the current fiscal year will enable us to meet these ratios or that the lender under the Credit Agreement will agree to modify these ratios in the future should we be unable to comply with them.

Our Credit Agreement provides that an “event of default” will occur under a number of circumstances, including (i) the failure to make payments when due, (ii) acceleration of payment obligations under other agreements, (iii) the failure to comply with the financial ratios and other covenants, (iv) breach of a representation or warranty in a material respect, (v) bankruptcy, (vi) judgments against RLJE or any of its subsidiaries over $250,000 individually or $500,000 in the aggregate at any time, (vii) a change of control, or (viii) a default under the investment documents with AMC Networks Inc. (or AMC). If an event of default occurs, the lender under our Credit Agreement may, unless we are able to negotiate an amendment, forbearance or waiver, require us to repay all amounts then outstanding under the Credit Agreement, which would have a material adverse effect on our liquidity, business, results of operations and financial condition.

We may not be able to generate the amount of cash needed to fund our future operations. Our ability to fund planned capital expenditures and development efforts will depend on our ability to generate cash in the future. Our ability to generate cash is in part subject to general economic, financial, competitive, regulatory and other factors that are beyond our control. We cannot assure you that our business will generate sufficient cash flow from operations to fund our liquidity needs.

Our liquidity depends on our cash-on-hand, operating cash flows and ability to collect cash receipts. At December 31, 2017, our cash and cash equivalents were approximately $6.2 million. Under the Credit Agreement, we are required to maintain $2.0 million for the fiscal year ending December 31, 2017 and $3.5 million for the fiscal year ending December 31, 2018 and all fiscal years thereafter for the term of the agreement. We rely on our cash-on-hand, operating cash flows and ability to collect cash receipts to fund our operations and meet our financial obligations. Delays or any failure to collect our trade accounts receivable would have a negative effect on our liquidity and could lead to an event of default under the Credit Agreement.

We have pledged our intellectual property assets to secure our Credit Agreement, and this represents a risk to our business, results of operations and financial condition. In order to secure the financing necessary to operate our business, we pledged all of our intellectual property rights as collateral to secure our obligations under the Credit Agreement. If we were to default on our obligations under the Credit Agreement, we could forfeit our intellectual property and, thereby, a primary source of revenue. This could have a material adverse effect on our business, results of operations and financial condition.

We may not be able to generate sufficient cash to service all our indebtedness, and we may be forced to take other actions, which may or may not be successful, to satisfy our obligations under our indebtedness. Our ability to make scheduled payments under our senior secured Credit Agreement depends on our financial and operating performance, which is subject to prevailing economic and competitive conditions and to certain financial, business and other factors beyond our control. We cannot assure you that we will maintain a level of cash flows from operating activities sufficient to permit us to pay the principal and interest due under the Credit Agreement or any future debt agreement. However, during 2017 we amended our senior secured Credit Agreement whereby

11

all interest payments are to be settled with shares of common stock, and principal debt payments are not required until 2020. If our cash flows and capital resources are insufficient to fund our future debt service and other obligations, we could face substantial liquidity problems and could be forced to reduce or delay capital expenditures and development efforts, sell assets or operations, seek additional capital or restructure or refinance our indebtedness. We cannot assure you that we would be able to take any of these actions, that these actions would be successful and permit us to meet our scheduled debt service obligations or that these actions would be permitted under the terms of our existing or future debt agreements, including the Credit Agreement.

Risks Relating to Our Business

We have limited working capital and limited access to financing. Our cash requirements, at times, may exceed the level of cash generated by operations. Accordingly, we may have limited working capital.

Our ability to obtain adequate additional financing on satisfactory terms may be limited. With respect to debt financing, our Credit Agreement restricts us from incurring additional indebtedness. With respect to equity financing, our ability to sell our equity securities depends on general market conditions, including the demand for our common stock. We may be unable to raise capital through the sale of equity securities, and if we were able to sell equity, our existing stockholders could experience substantial dilution. If adequate financing is not available at all or is unavailable on acceptable terms, we may find we are unable to fund expansion, continue offering products and services, take advantage of acquisition opportunities, develop or enhance services or products, or respond to competitive pressures in the industry.

Our business requires a substantial investment of capital. The production, acquisition and distribution of programming require a significant amount of capital. Capital available for these purposes will be reduced to the extent that we are required to use funds otherwise budgeted for capital investment to fund our operations. Curtailed content investment over a sustained period could have a material adverse effect on future operating results and cash flows. Further, a significant amount of time may elapse between our expenditure of funds and the receipt of revenues from our television programs or motion pictures. This time lapse requires us to fund a significant portion of our capital requirements from our operating cash flow and from other financing sources. Although we intend to continue to mitigate the risks of our production exposure through pre-sales to broadcasters and distributors, tax credit programs, government and industry programs, co-financiers and other sources, we cannot assure you that we will continue to successfully implement these arrangements or that we will not be subject to substantial financial risks relating to the production, acquisition, completion and release of new television programs and motion pictures. In addition, if we increase (through internal growth or acquisition) our production slate or our production budgets, we may be required to increase overhead and/or make larger up-front payments to talent and, consequently, bear greater financial risks. Any of the foregoing could have a material adverse effect on our business, financial condition, operating results, liquidity and prospects.

Changes in competitive offerings for entertainment video could adversely impact our business. The market for entertainment video is intensely competitive and subject to rapid change. Through new and existing distribution channels, consumers have increasing options to access entertainment video. Traditional providers of entertainment video, including broadcasters and cable network operators, as well as internet-based ecommerce or entertainment video providers are increasing their internet-based video offerings. Several of these competitors have long operating histories, large customer bases, strong brand recognition and significant financial, marketing and other resources. They may secure better terms from suppliers, adopt more aggressive pricing and devote more resources to product development, technology, infrastructure, content acquisitions and marketing. New entrants may enter the market or existing providers may adjust their services with unique offerings or approaches to providing entertainment video. Companies also may enter into business combinations or alliances that strengthen their competitive positions. If we are unable to successfully or profitably compete with current and new competitors, our business will be adversely affected, and we may not be able to increase or maintain market share, revenues or profitability.

Our inability to gauge and predict the commercial success of our programming could adversely affect our business, results of operations and financial condition. Operating in the entertainment industry involves a substantial degree of risk. Each video program or feature film is an individual artistic work, and its commercial success is primarily determined by unpredictable audience reactions. The commercial success of a title also depends upon the quality and acceptance of other competing programs or titles released into the marketplace, critical reviews, the availability of alternative forms of entertainment and leisure activities, general economic conditions and other tangible and intangible external factors, all of which are subject to change and cannot be predicted. Timing is also sometimes relevant to a program’s success, especially when the program concerns a recent event or historically relevant material (e.g., an anniversary of a historical event which focuses media attention on the event and accordingly spurs interest in related content). Our success depends in part on the popularity of our content and our ability to gauge and predict it. Even if a film achieves success during its initial release, the popularity of a particular program and its ratings may diminish over time. Our inability to gauge and predict the commercial success of our programming could materially adversely affect our business, results of operations and financial condition.

12

We may be unable to recoup advances paid to secure exclusive distribution rights. Our most significant costs and cash expenditures relate to acquiring content for exclusive distribution. Most agreements to acquire content require upfront advances against royalties or net profits participations expected to be earned from future distribution. The amount we are willing to advance is derived from our estimate of net revenues that will be realized from our distribution of the title. Although these estimates are based on management’s knowledge of competitive title performance, current events and actions management may undertake in the future, actual results will differ from those estimates. If sales do not meet our original estimates, we may (i) not recognize the expected gross margin or net profit, (ii) not recoup our advances or (iii) record accelerated amortization and/or fair value write-downs of advances paid. We recorded impairments related to our investments in content of $1.6 million during 2017 and $2.8 million during 2016.

Our inability to maintain relationships with our program suppliers and vendors may adversely affect our business. We receive a significant amount of our revenues from the distribution of content for which we already have exclusive agreements with program suppliers. However, titles which have been financed by us may not be timely delivered as agreed or may not be of the expected quality. Delays or inadequacies in delivery of titles, including rights clearances, could negatively affect the performance of any given quarter or year. In addition, results of operations and financial condition may be materially adversely affected if:

|

|

• |

We are unable to renew our existing agreements as they expire; |

|

|

• |

Our current program suppliers do not continue to support digital, DVD or other applicable format in accordance with our exclusive agreements; |

|

|

• |

Our current content suppliers do not continue to license titles to us on terms acceptable to us; or |

|

|

• |

We are unable to establish new beneficial supplier relationships to ensure acquisition of exclusive or high-profile titles in a timely and efficient manner. |

Disputes over intellectual property rights could adversely affect our business, results of operations and financial condition. Our sales and net revenues depend heavily on the exploitation of intellectual property owned by us or third parties from whom we have licensed intellectual property. Should a dispute arise over, or a defect be found in, the chain of title in any of our key franchises, this could result in either a temporary suspension of distribution or an early termination of our distribution license. This could have a material adverse impact on our business, results of operations and financial condition.

We, and third parties that manage portions of our secure data, are subject to cybersecurity risks and incidents. Our direct-to-consumer business involves the storage and transmission of customers' personal information, shopping preferences and credit card information, in addition to employee information and our financial and strategic data. The protection of our customer, employee and company data is vitally important to us. While we have implemented measures to prevent security breaches and cyber incidents, any failure of these measures and any failure of third parties that assist us in managing our secure data could materially adversely affect our business, financial condition and results of operations.

A high rate of product returns may adversely affect our business, results of operations and financial condition. As with the major studios and other independent companies in this industry, we face the risk of experiencing a relatively high level of product returns as a percentage of our revenues for a given title. Additionally, our allowances for sales returns may not be adequate to cover any potential returns resulting from future retailer consolidation events within the home-video retail marketplace. When these occur the risk of inventory consolidation and higher returns increases. Having experienced a high rate of product returns over the past three years, 2017 saw a significant decline in returns. Changes in our business practices lead us to expect these levels to remain lower, but the risk of retail consolidation still exists.

We depend on third-party shipping and fulfillment companies for the delivery of our products. If these companies experience operational difficulties or disruptions, our business could be adversely affected. We rely on SPHE, our distribution facilitation and manufacturing partner in North America, and Sony DADC UK Limited in the U.K. to determine the best delivery method for our products. These partners rely entirely on arrangements with third-party shipping companies, principally Federal Express and UPS, for small package deliveries and less-than-truckload service carriers for larger deliveries, for the delivery of our products. The termination of arrangements between our partners and one or more of these third-party shipping companies, or the failure or inability of one or more of these third-party shipping companies to deliver products on a timely or cost-efficient basis from our partners to our customers, could disrupt our business, reduce net sales and harm our reputation. Furthermore, an increase in the amount charged by these shipping companies could negatively affect our gross margins and earnings.

Economic weakness may adversely affect our business, results of operations and financial condition. An economic downturn would have a significant negative effect on our revenues. As consumers reduce spending and scale back purchases of our products, we may experience higher product returns and lower sales, which would adversely affect our revenues and results of operations. Although domestic consumer spending has been strong over the last few years, weak consumer demand for our products may occur and may adversely affect our business, results of operations and financial condition.

13

Our high concentration of sales to and receivables from relatively few customers (and use of a third-party to manage collection of substantially all packaged goods receivables) may result in significant uncollectible accounts receivable exposure, which may adversely affect our liquidity, business, results of operations and financial condition. During 2017, sales to one customer accounted for 24.6% of our Wholesale Distribution segment revenues. Our top five customers accounted for approximately 55.0% of our Wholesale Distribution segment revenues during 2017. One customer accounted for 37.5% of revenues reported within our Digitals Channels segment during 2017. At December 31, 2017, Amazon, SPHE, Hulu, and Netflix accounted for approximately 25.0%, 22.2%, 15.2% and 13.9%, respectively, of our gross accounts receivable.

We may be unable to maintain favorable relationships with our retailers and distribution facilitators including SPHE and Sony DADC UK Limited. Further, our retailers and distribution facilitators may be adversely affected by economic conditions. If we lose any of our top customers or distribution facilitators, or if any of these customers reduces or cancels a significant order, it could have a material adverse effect on our liquidity, business, results of operations and financial condition.

We face credit exposure from our retail customers and may experience uncollectible receivables from these customers should they face financial difficulties. If these customers fail to pay their accounts receivable, file for bankruptcy or significantly reduce their purchases of our programming, it would have a material adverse effect on our business, financial condition, results of operations and liquidity.

A high concentration of our gross accounts receivables is attributable to SPHE and Sony DADC UK Limited, as they are our vendor of record for shipments of physical product to North American and U.K. retailers and wholesalers. As part of our arrangement with our distribution facilitation partners, SPHE and Sony DADC UK Limited collect the receivables from our end customers, provide us with monthly advance payments on such receivables (less a reserve), and then true up the accounts receivables accounting quarterly. While we remain responsible for the credit risk from the end customer, if SPHE or Sony DADC UK Limited should fail to adequately collect and pay us the accounts receivable they collect on our behalf, whether due to inadequate processes and procedures, inability to pay, bankruptcy or otherwise, our financial condition, results of operations and liquidity would be materially adversely affected.

We do not control the timing of dividends paid by ACL, which could negatively impact our cash flow. Although we hold a 64% interest in ACL, we do not control the board of directors of ACL. The members of the Agatha Christie family, who hold the remaining 36% interest in ACL, have the right to appoint the same number of directors as us and, in the event of deadlock on any decision of the board, also have a second or casting vote exercised by their appointee as chairman of ACL, which allows them to exercise control of ACL’s board of directors.

Under English law, the amount, timing and form of payment of any dividends or other distributions is a matter for ACL’s board of directors to determine, and, as a result, we cannot control when these distributions are made. If ACL’s board of directors decides not to authorize distributions, our cash flow may decrease, materially adversely affecting our business, results of operations, liquidity and financial condition.

Our business plan and future growth depend in part on our ability to commercialize the IP owned by ACL based on commissions for new programming from broadcasters, over whom we have no control. If we are unable to successfully implement this strategy, the results of operations and financial condition could be materially adversely affected. Our financial condition and results of operation will depend, in part, on our ability to commercialize the IP owned by ACL. Whether we are able to successfully commercialize the IP owned by ACL, including the creation of new content, will depend, in part, on ACL obtaining commissions for new programming from broadcasters (such as ITV, BBC and Sky in the U.K., and Fox, Disney and other studios in the U.S.). The ability to obtain commissions for new programming from broadcasters will depend on many factors outside of our control, including audience preferences and demand, financial condition of the broadcasters, the broadcasters’ budgets and access to financing, competitive pressures and the impact of actual and projected general economic conditions. We cannot guarantee that we will be able to obtain such commissions for new programming within our anticipated timeframe or at all. Without such commissions for new programming, we may not be able to successfully commercialize the IP of ACL in a timely or cost-effective manner, if at all. Failure to obtain commissions for new programming could adversely affect our market share, revenue, financial condition, results of operations, relationships with our distributors and retailers and our ability to expand our market, all of which would materially adversely affect our business, revenues and financial results.

The synergies and other efficiencies anticipated in connection with the transaction with AMC may not be realized. We expect, in conjunction with AMC, to pursue the aggregation of proprietary subscription video on demand activities and economies of scale with respect to manufacturing, sales and distribution of physical products. Although we believe that realizing these synergies would be beneficial to both us and AMC, the parties have not entered into a contract to pursue or otherwise implement these synergies. Accordingly, there is a risk that we and AMC may not agree on the means or terms to implement these synergies or that AMC, whether due to differing business interests or other reasons, may not pursue these synergies in the manner or at the

14

level we desire. AMC has investments in other media companies which may conflict or compete with our business. In addition, the integration of these operations will be a complex, costly and time-consuming process. As a result, we will be required to devote significant management attention and resources to integrating these operations.

We depend on key and highly skilled personnel to operate our business, and if we are unable to retain our current personnel or hire additional personnel, our ability to develop and successfully market our business could be harmed. Our success continues to depend to a significant extent on our ability to identify, attract, hire, train and retain qualified professional, creative, technical and managerial personnel. Moreover, we believe that our success greatly depends on the contributions of our Chairman, Robert L. Johnson, executive officers including Chief Executive Officer, Miguel Penella, Chief Financial Officer, Nazir Rostom, and other key executives. Although we have employment agreements with Messrs. Penella and Rostom, any of our employees may terminate their employment relationship with us at any time, and their knowledge of our business and industry would be extremely difficult to replace. The loss of any key employees or the inability to attract or retain qualified personnel could delay the acquisition of content and harm the market's perception of us. Competition for the caliber of talent required to acquire and exploit content continues to increase. If we are unable to attract and retain the qualified personnel we need to succeed, our business, results of operations and financial condition could suffer.

We face risks from doing business internationally. We exploit and derive revenues from television programs and feature films outside the U.S., directly in the U.K. and in Australia, and through various third-party licensees elsewhere. As a result, our business is subject to certain risks inherent in international business, many of which are beyond our control. These risks include:

|

|

• |

Laws and policies affecting trade, investment and taxes, including laws and policies relating to the repatriation of funds and withholding taxes, and changes in these laws; |

|

|

• |

Changes in local regulatory requirements, including restrictions on content, differing cultural tastes and attitudes; |

|

|

• |

Differing degrees of protection for intellectual property; |

|

|

• |

Financial instability and increased market concentration of buyers in foreign television markets, including in European pay television markets; |

|

|

• |

The instability of foreign economies and governments; |

|

|

• |

Fluctuating foreign exchange rates; and |

|

|

• |

War and acts of terrorism. |

Events or developments related to these and other risks associated with international trade could adversely affect our revenues from non-U.S. sources, which could have a material adverse effect on our business, financial condition, operating results, liquidity and prospects.

Changes to existing accounting pronouncements or taxation rules or practices may affect how we conduct our business and affect our reported results of operations. New accounting pronouncements or tax rules and varying interpretations of accounting pronouncements or taxation practice have occurred and may occur in the future. A change in accounting pronouncements or interpretations or taxation rules or practices can have a significant effect on our reported results and may even affect our reporting of transactions completed before the change is effective. Changes to existing rules and pronouncements, future changes, if any, or the questioning of current practices or interpretations may materially adversely affect our reported financial results or the way we conduct our business.

Changes in, or interpretations of, tax rules and regulations, and changes in geographic operating results, may adversely affect our effective tax rates. We are subject to income taxes in the U.S. and foreign tax jurisdictions. Our future effective tax rates could be affected by changes in tax laws or the interpretation of tax laws, by changes in the amount of revenues or earnings that we derive from international sources in countries with high or low statutory tax rates, or by changes in the valuation of our deferred tax assets and liabilities. Unanticipated changes in our tax rates could affect our future results of operations.

In addition, we may be subject to examination of our income tax returns by federal, state and foreign tax jurisdictions. We regularly assess the likelihood of outcomes resulting from possible examinations to determine the adequacy of our provision for income taxes. In making such assessments, we exercise judgment in estimating our provision for income taxes. While we believe our estimates are reasonable, we cannot assure you that final determinations from any examinations will not be materially different from those reflected in our historical income tax provisions and accruals. Any adverse outcome from any examinations may have a material adverse effect on our business and operating results.

15

The effects of the Tax Cuts and Jobs Act on our business have not yet been fully analyzed and could have an adverse effect on our net income. On December 22, 2017, the Tax Cuts and Jobs Act (the Act) was signed into law. The Act reduces the corporate tax rate to 21 percent from 35 percent, among other things. On that same day, Staff Accounting Bulletin No. 118 (or SAB 118) was issued to address the application of accounting principles generally accepted in the United States of America (or US GAAP) in situations when a registrant does not have the necessary information available, prepared, or analyzed (including computations) in reasonable detail to complete the accounting for certain income tax effects of the Act.. In accordance with SAB 118, we determined that the deferred tax expense recorded in connection with the remeasurement of certain deferred tax assets and liabilities was a provisional amount and a reasonable estimate at December 31, 2017. Additional work is necessary to do a more detailed analysis and any subsequent adjustment to these amounts will be recorded in 2018 when the analysis is complete.

Risks Relating to Our Industry

Our revenues and results of operations may fluctuate significantly. Our results of operations are difficult to predict and depend on a variety of factors. Our results of operations depend significantly upon the commercial success of the television programming and feature films that we exploit, which cannot be predicted with certainty. In particular, the underperformance in any given window or format of one or more motion pictures or television programs in any period may cause our revenues and earnings results for that period (and potentially, subsequent periods) to be less than anticipated, in some instances to a significant extent. Accordingly, our results of operations may fluctuate significantly from period to period, and the results of any one period may not be indicative of the results for any future periods.

Our results of operations also fluctuate due to the timing, mix, number and availability of our broadcast, home entertainment and theatrical motion picture releases, as well as license periods for our content. Our operating results may increase or decrease during a particular period or year due to differences in the number and/or mix of films released compared to the corresponding period in the prior year.

We may not be able to continue to attract and retain subscribers to our digital channels. We have experienced significant subscriber growth since we began our digital channels in 2011. Our ability to continue to attract subscribers will depend in part on our ability to consistently provide our subscribers with a valuable and quality streaming experience. Furthermore, the relative service levels, content offerings, pricing and related features of our competitors may adversely impact our ability to attract and retain subscribers. We compete for screen viewing time with traditional broadcast and cable, video-on-demand, internet-based movie and TV content providers, including both those that provide legal and illegal (or pirated) streaming video content, and streaming video retail stores, among others. If consumers do not perceive our service offering to be of value, or if we introduce new or adjust existing features or change the mix of content in a manner that is not favorably received by them, we may not be able to attract and retain subscribers.

Revenues from the sale of DVDs are declining. During calendar 2017, DVD continued to experience a decline in revenues for the category since the format debuted in 1997. We estimate that approximately 41% of our 2017 net revenue base is generated from the sale of physical goods, which includes revenues from the sale of DVDs, compared to 51% in 2016. The continued maturation of the standard DVD format may continue to adversely affect our business, results of operations and financial condition.

Decreasing retail shelf space for our industry may limit sales of our programming, which may adversely affect our business, results of operations and financial condition. We face increasing competition from major motion picture studios and other independent content suppliers for limited retail shelf space, which space has been shrinking in absolute terms as brick and mortar retailers have fewer stores and smaller space allocations for the home-video space within their stores. We believe competition can be especially challenging for independent labels like us, because the new releases of major studios often have extremely high visibility, greater marketing support and sales projections in the millions of units, which typically require much more shelf space to support.

It can be a challenge to obtain the product placement necessary to maximize sales, particularly among the limited number of major retailers who comprise our core brick and mortar customers. The continued retailer trend toward greater visibility for titles at the expense of quantity (i.e., “face out” rather than “spine out” placement) has the effect of reducing the total number of titles actually carried by a retailer.

We cannot accurately predict the overall effect shifting audience tastes, technological change or the availability of alternative forms of entertainment may have on distributors. In addition to uncertainty regarding the DVD market, there is uncertainty as to whether other developing distribution channels and formats, such as VOD and internet distribution of television and films, will widely accepted by consumers or provide us with opportunities for successful business exploitation. Moreover, to the extent that these emerging distribution channels and formats gain popular acceptance, the demand for delivery through DVDs may decrease.

16

Our stock price may be subject to substantial volatility, and stockholders may lose all or a substantial part of their investment. Our common stock currently trades on the Nasdaq Capital Market (NASDAQ). There is limited public float, and trading volume historically has been low and sporadic, making it difficult to buy or sell our stock. As a result of the low trading volume, the market price for our common stock may not necessarily be a reliable indicator of our fair market value. The price at which our common stock trades may fluctuate as a result of a number of factors, including the number of shares available for sale in the market, quarterly variations in our operating results, actual or anticipated announcements of new releases by us or competitors, the gain or loss of significant customers, changes in the estimates of our operating performance, fluctuations in the fair value of our common stock warrant liability and market conditions in our industry and the economy as a whole.

Any future issuances of equity may significantly affect the market price of our common stock. Future issuances of substantial amounts of our common stock, including shares that we may issue upon conversion or redemption of outstanding preferred stock, exercise of outstanding warrants, or conversion of other convertible securities, if any, could adversely affect the market price of our common stock. The amount of common stock issuable upon redemption of our preferred stock, although subject to a floor price, is not fixed in all circumstances, and therefore the actual amount of common stock issuable upon redemption cannot currently be determined. Similarly, the amount of common stock issuable upon exercise of one of the three warrants issued to AMC is not fixed in all circumstances, and therefore the actual amount of common stock issuable upon exercise cannot currently be determined. Additionally, our senior secured Credit Agreement with AMC requires us to settle all interest due with shares of common stock at a rate of $3.00 per share. The number of shares issuable to settle interest is therefore dependent upon when the Credit Agreement loans are repaid. Further, if we raise additional funds through the issuance of common stock or securities convertible into or exercisable for common stock, our stockholders may experience substantial dilution and the price of our common stock may fall. New equity securities issued may also have greater rights, preferences or privileges than our existing common stock.

Additional authorized shares of common stock available for issuance may adversely affect the market. We are authorized to issue 250,000,000 shares of our common stock. As of March 1, 2018, we had 14,564,678 shares of our common stock outstanding, excluding shares issuable upon conversion of our outstanding preferred stock and exercise of our outstanding warrants. As of March 1, 2018, we had outstanding preferred stock convertible into approximately 5,880,000 shares of our common stock, including dividends, at a conversion price of $3.00 per share and warrants to purchase 1,349,111 shares of common stock at $1.50 per share, warrants to purchase 150,000 shares of common stock at $2.37 per share, warrants to purchase 1,500,000 shares of common stock at $3.00, and warrants to purchase 18,333,000 shares of common stock at $3.00, respectively. To the extent the shares of common stock are issued, preferred stock is converted or warrants are exercised, holders of our common stock will experience dilution.

Provisions in our amended and restated articles of incorporation and Nevada law may inhibit a takeover of us, which could limit the price investors might be willing to pay in the future for our common stock and could entrench management. Our amended and restated articles of incorporation contain provisions that may discourage unsolicited takeover proposals that stockholders may consider to be in their best interests. These provisions include the ability of the board of directors to designate the terms of and issue new series of preferred shares, which may make more difficult the removal of management and may discourage transactions that otherwise could involve payment of a premium over prevailing market prices for our securities.

We are also subject to anti-takeover provisions under Nevada law, which could delay or prevent a change of control. Together these provisions may make more difficult the removal of management and may discourage transactions that otherwise could involve payment of a premium over prevailing market prices for our securities.

None.

17

Our principal executive office is located in Silver Spring, Maryland. We also maintain offices in Woodland Hills, California; London, England and Sydney, Australia with varying terms and expiration dates. All locations are leased. A summary of our locations is as follows:

|

Location |

|

Primary Purpose |

|

Lease Expiration |

|

Reporting Segment (1) |

|

Silver Spring, MD |

|

Executive Office/Administrative/Sales/ Content Acquisition |

|

November 15, 2020 |

|

Corporate/ Digital Channels |

|

Woodland Hills, CA |

|

Administrative/Sales/ Content Acquisition |

|

June 30, 2021 |

|

Digital Channels/ Wholesale Distribution |

|

London, England |

|

Content Development and Production/Sales/ Administration for the U.K. |

|

July 1, 2018 |

|

Digital Channels/IP Licensing/ Wholesale Distribution |

|

Sydney, Australia |

|

Sales/Administration |

|

Month-to-month |

|

Wholesale Distribution |

|

|

(1) |

The segment descriptions above reflect the location’s primary activity. |

We believe that our current offices are adequate to meet our business needs, and our properties and equipment have been well maintained.

In the normal course of business, we are subject to proceedings, lawsuits and other claims, including proceedings under government laws and regulations relating to content ownership and copyright matters. While it is not possible to predict the outcome of these matters, it is the opinion of management, based on consultations with legal counsel, that the ultimate disposition of known proceedings will not have a material adverse effect on our financial condition, results of operations or liquidity.

Not applicable.

18

|

ITEM 5. |

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information

Our common stock is traded on The NASDAQ Capital Market® under the symbol “RLJE”. The table below presents the quarterly high and low closing sales prices of our common stock reported by NASDAQ.

|

|

|

Common Stock |

|

|||||

|

|

|

High |

|

|

Low |

|

||

|

2017 |

|

|

|

|

|

|

|

|

|

First quarter |

|

$ |

2.52 |

|

|

$ |

1.46 |

|

|

Second quarter |

|

$ |

3.31 |

|

|

$ |

2.46 |

|

|

Third quarter |

|

$ |

4.46 |

|

|

$ |

2.91 |

|

|

Fourth quarter |

|

$ |

4.40 |

|

|

$ |

3.25 |

|

|

|

|

|

|

|

|

|

|

|

|

2016 |

|

|

|

|

|

|

|

|

|

First quarter |

|

$ |

2.97 |

|

|

$ |

1.41 |

|

|

Second quarter |

|

$ |

2.70 |

|

|

$ |

1.58 |

|

|

Third quarter |

|

$ |

2.90 |

|

|

$ |

1.88 |

|

|

Fourth quarter |

|

$ |

2.28 |

|

|

$ |

1.34 |

|

Stockholders

As of December 31, 2017, there were:

|

|

• |

14,071,423 shares of our common stock outstanding, which were held by approximately 268 holders of record; |

|

|

• |

warrants to purchase 18,333,000 shares of our common stock at a price of $3.00 per share held by AMC Networks; |

|

|

• |

warrants to acquire 1,349,111 shares of common stock at a price of $1.50 per share; 150,000 shares of common stock at a price of $2.37 per share, and 1,500,000 shares of our common stock at a price of $3.00 per share held by approximately 10 holders of record; and |

|

|

• |

15,198,000 shares or our preferred stock outstanding, convertible into 5,880,000 shares of common stock at a price of $3.00 per share, held by 5 holders of record. |

The number of holders of record does not include the number of persons whose securities are in nominee or “street name” accounts through brokers.

Dividend Policy

We have not paid any cash dividends on our common stock to date. The payment of cash dividends in the future will be dependent upon our revenues and earnings, if any, capital requirements and general financial condition. The payment of any dividends will be within the discretion of our board of directors at such time. It is the present intention of our board of directors to retain all earnings for use in our business operations and, accordingly, our board of directors does not anticipate declaring any dividends in the foreseeable future. In addition, our senior secured credit agreement with AMC restricts our ability to pay dividends on our common stock. For more information on these restrictions, please refer to Note 10, Debt of our consolidated financial statements and in the Liquidity and Capital Resources sections of Management’s Discussion and Analysis of Financial Condition and Results of Operations (or MD&A).

Securities Authorized for Issuance Under Equity Compensation Plans

See table under Part III, Item 12, Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters in the Equity Compensation Plan Information section.

Additional information with respect to the shares of our common stock that may be issued under our existing stock-based compensation plans is disclosed in our consolidated financial statements in Note 14, Stock-Based Compensation.

19

Item 6. Selected Financial Data is not required for smaller reporting companies.

The following discussion and analysis of our financial condition and results of operations contains forward-looking statements that involve risks and uncertainties, such as statements of our plans, objectives, expectations and intentions. As described under the heading "Forward-Looking Statements" of this Annual Report, our actual results could differ materially from those anticipated in our forward-looking statements. Factors that could contribute to such differences include those discussed elsewhere in this Annual Report, including in Item 1A of this Annual Report under the heading “Risk Factors.” You should not place undue reliance on our forward-looking statements, which apply only as of the date of this Annual Report. Except as may be required under federal law, we undertake no obligation to update publicly any forward-looking statements for any reason, even if new information becomes available or other events occur.

You should read the following discussion and analysis in conjunction with our consolidated financial statements and related footnotes included in Item 8 of this Annual Report.

OVERVIEW

General