Attached files

| file | filename |

|---|---|

| EX-10.68 - EXHIBIT 10.68 - CURO Group Holdings Corp. | ex-1068cghc2017incentplans.htm |

| EX-32.2 - EXHIBIT 32.2 - CURO Group Holdings Corp. | ex-322cfo906certification.htm |

| EX-32.1 - EXHIBIT 32.1 - CURO Group Holdings Corp. | ex-321ceo906certification.htm |

| EX-31.2 - EXHIBIT 31.2 - CURO Group Holdings Corp. | ex-312cfo302certification.htm |

| EX-31.1 - EXHIBIT 31.1 - CURO Group Holdings Corp. | ex-311ceo302certification.htm |

| EX-21.1 - EXHIBIT 21.1 - CURO Group Holdings Corp. | ex-211listofsubsidiaries.htm |

| EX-10.67 - EXHIBIT 10.67 - CURO Group Holdings Corp. | ex-1067noticeofacceleratio.htm |

| EX-10.66 - EXHIBIT 10.66 - CURO Group Holdings Corp. | ex-1066cghc2017rsunotice.htm |

| EX-10.65 - EXHIBIT 10.65 - CURO Group Holdings Corp. | ex-1065cghc2017rsunoticexn.htm |

| EX-10.64 - EXHIBIT 10.64 - CURO Group Holdings Corp. | ex-10642018ltipawardcommun.htm |

| EX-10.63 - EXHIBIT 10.63 - CURO Group Holdings Corp. | ex-10632018corpincentiveco.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-38315

CURO GROUP HOLDINGS CORP.

(Exact name of registrant as specified in its charter)

Delaware | 90-0934597 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

3527 North Ridge Road, Wichita, KS | 67205 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (316) 425-1410

Securities Registered Pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, $0.001 par value per share | New York Stock Exchange | |

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ | |

Non-accelerated filer | ☐ | (Do not check if a smaller reporting company) | ||

Smaller reporting company | ☐ | Emerging growth company | ☒ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of 6,666,667 shares of the registrant’s common stock, par value $0.001 per share, held by non-affiliates on December 31, 2017 was approximately $93,866,671.

At March 1, 2018 there were 45,561,419 shares of the registrant’s Common Stock, $0.001 par value per share, outstanding.

Documents incorporated by reference:

The information required by Part III of Form 10-K is incorporated herein by reference to the registrant's definitive Proxy Statement relating to its 2018 Annual Meeting of Shareholders, which will be filed with the Commission within 120 days after the end of the registrant's fiscal year.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

ANNUAL REPORT

YEAR ENDED DECEMBER 31, 2017

INDEX

2

PART I

ITEM 1. BUSINESS

Company Overview and History

We are a growth-oriented, technology-enabled, highly-diversified consumer finance company serving a wide range of underbanked consumers in the United States, Canada and the United Kingdom and are a market leader in our industry based on revenues. We believe that we have the only true omni-channel customer acquisition, onboarding and servicing platform that is integrated across store, online, mobile and contact center touchpoints. Our IT platform, which we refer to as the “Curo Platform,” seamlessly integrates loan underwriting, scoring, servicing, collections, regulatory compliance and reporting activities into a single, centralized system. We use advanced risk analytics powered by proprietary algorithms and over 15 years of loan performance data to efficiently and effectively score our customers’ loan applications. Since 2010, we have extended over $14.5 billion in total credit across approximately 38.1 million total loans, and our revenue of $963.6 million in 2017 represents a 24.8% compound annual growth rate, or CAGR, over the same time period.

The CURO business was founded in 1997 to meet the growing needs of consumers looking for access to credit. We set out to offer a variety of convenient, easily-accessible financial and loan services and over our 20 years of operations, expanded across the United States, Canada and the United Kingdom.

CURO Financial Technologies Corp., or CFTC (then known as Speedy Cash Holdings Corp.), was incorporated in Delaware in July 2008. In September 2008, our founders sold or otherwise contributed all of the outstanding equity of the various operating entities that comprised the CURO business to a wholly-owned subsidiary of CFTC in connection with an investment in CFTC by Friedman Fleischer & Lowe Capital Partners II, L.P. and its affiliated funds, or FFL Partners. Speedy Group Holdings Corp. was incorporated in Delaware in February 2013 as the parent company of CFTC. In May 2016, we changed the name of Speedy Group Holdings Corp. to CURO Group Holdings Corp. We similarly changed the names of some of its subsidiaries. The terms “CURO", "we,” “our,” “us,” and the “Company,” in this Annual Report refer to CURO Group Holdings Corp. and its directly and indirectly owned subsidiaries as a consolidated entity, except where otherwise stated.

In May 2011, we completed the acquisition of Cash Money Group, Inc., a Canadian entity, for approximately $104.5 million. In August 2012, we completed the acquisition of The Money Store, L.P., a Texas limited partnership which operated as The Money Box® Check Cashing for approximately $26.1 million. In February 2013, we completed the acquisition of Wage Day Advance Limited, a United Kingdom entity, for approximately $80.9 million. We subsequently effected a corporate name change of Wage Day Advance Limited to CURO Transatlantic Limited, although we still operate online in the United Kingdom as Wage Day Advance.

In 2015, we opened a state-of-the-art financial technology office in Chicago to continue to attract and retain talented IT development and data science professionals. As of December 31, 2017, this office is currently staffed with 25 professionals. In 2016, we launched LendDirect, as an online Installment Loan brand in Alberta, Canada. These loans are now offered in four provinces and at certain stores. In 2017, we launched Avio Credit, an online Installment Loan brand in the U.S. market. These loans are currently available in California, Missouri, South Carolina, Wisconsin, Alabama and Texas. In 2017, we also launched Juo Loans, an online Installment Loan brand in the U.K. market.

We operate in the United States under two principal brands, “Speedy Cash” and “Rapid Cash,” and launched our new brand “Avio Credit” in the United States in the second quarter of 2017. In the United Kingdom we operate online as “Wage Day Advance” and “Juo Loans” and, prior to their closure in the third quarter of 2017, our stores were branded “Speedy Cash.” In Canada, our stores are branded “Cash Money” and we offer “LendDirect” installment loans online and at certain stores. As of December 31, 2017, our store network consisted of 407 locations across 14 U.S. states and seven Canadian provinces and we offered our online services in 27 U.S. states, five Canadian provinces and the United Kingdom.

We offer a broad range of consumer finance products, including Unsecured Installment Loans, Secured Installment Loans, Open-End Loans and Single-Pay Loans. We have tailored our products to fit our customers’ particular needs as they access and build credit. Our product suite allows us to serve a broader group of potential borrowers than most of our competitors. The flexibility of our products, particularly our installment and open-end

3

products, allows us to continue serving customers as their credit needs evolve and mature. Our broad product suite creates a diversified revenue stream and our omni-channel platform seamlessly delivers our products across all contact points–we refer to it as “Call, Click or Come In.” We believe these complementary channels drive brand awareness, increase approval rates, lower our customer acquisition costs and improve customer satisfaction levels and customer retention.

We serve the large and growing market of individuals who have limited access to traditional sources of consumer credit and financial services. We define our addressable market as underbanked consumers in the United States, Canada and the United Kingdom. According to a study by the Center for Financial Services Innovation, there are as many as 121 million Americans who are currently underserved by financial services companies. According to studies by ACORN Canada and Pricewaterhouse Coopers LLP, the statistics in Canada and the United Kingdom are similar, with an estimated 15% of Canadian residents (approximately 5 million individuals) and an estimated 20 to 25% of United Kingdom residents (approximately 10 to 14 million individuals) classified as underbanked. Given our international footprint, this translates into an addressable target market of approximately 140 million individuals. We believe that with our scalable omni-channel platform and diverse product offerings, we are well positioned to gain market share as sub-scale players struggle to keep pace with the technological evolution taking place in the industry.

Initial Public Offering

We filed an amendment to our certificate of incorporation on December 6, 2017, that effected a 36-for-1 split of our common stock. Additionally, we filed an amended and restated certificate of incorporation on December 11, 2017, that, among other things, changed the authorized number of shares of our common stock to 250,000,000, consisting of 225,000,000 shares of common stock, with a par value of $0.001 per share and 25,000,000 shares of preferred stock, with a par value of $0.001 per share. All share and per share data have been retroactively adjusted for all periods presented to reflect the stock split as if the stock split had occurred at the beginning of the earliest period presented.

We completed our initial public offering ("IPO") of 6,666,667 shares of common stock on December 11, 2017, at a price of $14.00 per share, which provided net proceeds of $81.1 million. On December 7, 2017, our stock began trading on the New York Stock Exchange ("NYSE") under the symbol "CURO." In connection with the closing, the underwriters had a 30-day option to purchase up to an additional 1,000,000 shares at the initial public offering price, less the underwriting discount to over-allotments, which they exercised on January 5, 2018. The exercise of this option provided additional net proceeds of $13.0 million.

On March 7, 2018, we used a portion of the net proceeds from the IPO to redeem $77.5 million of the 12.00% Senior Secured Notes due 2022 and to pay related fees, expenses, premiums and accrued interest. See Note 25 - Subsequent Events of this Annual Report on Form 10-K for additional information about this transaction.

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act.

An emerging growth company may take advantage of specified reduced reporting and other requirements that are otherwise generally applicable to public companies. As an emerging growth company:

• | we are not required to present selected financial data for any period prior to the earliest audited period presented in our initial registration statement; |

• | we are not required to engage an auditor to report on the effectiveness of our internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002, or Sarbanes-Oxley Act; |

4

• | we are not required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board, or PCAOB, regarding a supplement to the auditor’s report providing additional information about the audit and the financial statements (i.e., an auditor discussion and analysis); |

• | we are not required to submit certain executive compensation matters to stockholder advisory votes, such as “say-on-pay,” “say-on-frequency” and “say-on-golden parachutes”; |

• | we are not required to disclose certain executive compensation-related items, such as the correlation between executive compensation and performance and comparisons of the Chief Executive Officer’s compensation to median employee compensation, or to include a compensation committee report, provided we comply with the scaled compensation disclosure rules applicable to smaller reporting companies; and |

• | we may take advantage of an extended transition period for complying with new or revised accounting standards, allowing us to delay the adoption of some accounting standards until those standards would otherwise apply to private companies. |

We have elected to take advantage of these reduced reporting and other requirements available to us as an emerging growth company.

We may take advantage of these provisions until we are no longer an emerging growth company. We could remain an emerging growth company until the last day of the fifth fiscal year after our IPO, or until the earliest of the following:

(i) the last day of the first fiscal year in which our total annual gross revenues are at least $1.07 billion;

(ii) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, or the Exchange Act, which would occur as of the end of the fiscal year in which, among other things, the market value of our voting and non-voting common equity securities held by non-affiliates is at least $700 million as of the last business day of our most recently completed second fiscal quarter; or

(iii) the date on which we have issued more than $1 billion in nonconvertible debt securities during the preceding three-year period.

Industry Overview

We operate in a segment of the financial services industry that provides lending products to underbanked consumers in need of convenient and flexible access to credit and other financial products. In the United States alone, according to a study by the Center for Financial Services Innovation, or CFSI, these underserved consumers in our target market spent an estimated $126.5 billion on fees and interest related to credit products similar to those we offer.

We believe our target consumers have a need for tailored financing products to cover essential expenses. According to a study by the Federal Reserve, 44% of American adults could not cover an emergency expense costing $400 or would cover it by selling an asset or borrowing money. Additionally, a study conducted by JP Morgan Chase & Co., which analyzed the transaction information of 2.5 million of its account holders, found that 41% of those sampled experienced month-to-month income swings of more than 30%.

We compete against a wide variety of consumer finance providers including online and branch-based consumer lenders, credit card companies, pawn shops, rent-to-own and other financial institutions that offer similar financial services. A study by CFSI has estimated that spending on credit products offered by our industry exhibited a 10.0% CAGR from 2010 to 2015. This growth has been accompanied by shrinking access to credit for our

5

customer base as evidenced by an estimated $142 billion reduction in the availability of non-prime consumer credit from the 2008 to 2009 credit crisis to 2015 (based on analysis of master pool trust data of securitizations for major credit card issuers).

In addition to the beneficial secular trends broadly impacting the consumer finance landscape, we believe we are well positioned to grow our market share as a result of several changes we have observed related to consumer preferences within alternative financial services. Specifically, we believe that a combination of evolving consumer preferences, increasing use of mobile devices and overall adoption rates for technology are driving significant change in our industry.

• | Shifting preference towards installment loans—We believe from our experience in offering installment loan products since 2008 that single-pay loans are becoming less popular or less suitable for a growing portion of our customers. Customers generally have shown a preference for our Installment Loan products, which typically have longer terms, lower periodic payments and a lower relative cost. Offering more flexible terms and lower payments also significantly expands our addressable market by broadening our products’ appeal to a larger proportion of consumers in the market. |

• | Increasing adoption of online channels—Our experience is that customers prefer service across multiple channels or touch points. Approximately 63% of respondents in a recent study by CFI Group said they conducted more than half of their banking activities electronically. That same group of respondents reported an overall level of satisfaction that met or exceeded the average. Our 2017 online revenue of $367.2 million represented 38% of our total revenues for the year. |

• | Increasing adoption of mobile apps and devices—With the proliferation of pay-as-you-go and other smartphone plans, many of our underbanked customers have moved directly to mobile devices for loan origination and servicing. According to a 2016 study by the Pew Research Center involving the United States, the United Kingdom and Canada, smartphone penetration is 72%, 68% and 67%, respectively. Additionally, 43% of respondents to a study by CFI Group said they conduct transactions using a mobile banking app. Five years ago, less than 30% of our U.S. customers reached us via a mobile device. In the fourth quarter of 2017, that percentage was over 80%. |

Our Strengths

We believe the following competitive strengths differentiate us and serve as barriers for others seeking to enter our market.

• | Unique omni-channel platform / site-to-store capability—We believe we have the only fully-integrated store, online, mobile and contact center platform to support omni-channel customer engagement. We offer a seamless “Call, Click or Come In” capability for customers to apply for loans, receive loan proceeds, make loan payments and otherwise manage their accounts in store, online or over the phone. Customers can utilize any of our three channels at any time and in any combination to obtain a loan, make a payment or manage their account. In addition, we have our “Site-to-Store” capability in which online customers that do not qualify for a loan online are referred to a store to complete a loan transaction with one of our associates. These aspects of our platform enable us to source a larger number of customers, serve a broader range of customers and continue serving these customers for longer periods of time. |

• | Industry leading product and geographic diversification—In addition to channel diversification, we have increased our diversification by product and geography allowing us to serve a broader range of customers with a flexible product offering. As part of this effort, we have also developed and launched new brands and will continue to develop new brands with differentiated marketing messages. These initiatives have helped diversify our revenue streams, enabling us to appeal to a wider array of borrowers. |

6

• | Leading analytics and information technology drives strong credit risk management—We have developed a bespoke, proprietary IT platform, referred to as the Curo Platform, which is a unified, centralized platform that seamlessly integrates activities related to customer acquisition, underwriting, scoring, servicing, collections, compliance and reporting. Our IT platform is underpinned by over 15 years of continually updated customer data comprising over 74 million loan records (as of December 31, 2017) used to formulate our robust, proprietary underwriting algorithms. This platform then automatically applies multi-algorithmic analysis to a customer’s loan application to produce a “Curo Score” which drives our underwriting decision. Globally, as of December 31, 2017, we have approximately 185 employees who write code and manage our networks and infrastructure for our IT platform. This fully-integrated IT platform enables us to make real-time, data-driven changes to our acquisition and risk models which yield significant benefits in terms of customer acquisition costs and credit performance. |

• | Multi-faceted marketing strategy drives low customer acquisition costs—Our marketing strategy includes a combination of strategic direct mail, television advertisements and online and mobile-based digital campaigns, as well as strategic partnerships. Our global Marketing, Risk and Credit Analytics team, consisting of approximately 74 professionals as of December 31, 2017, uses our integrated IT platform to cross reference marketing spend, new customer account data and granular credit metrics to optimize our marketing budget across these channels in real time to produce higher quality new loans. Besides these diversified marketing programs, our stores play a critical role in creating brand awareness and driving new customer acquisition. From January 2015 through the end of December 2017, we acquired nearly 2.0 million new customers in North America. |

• | Focus on customer experience—We focus on customer service and experience and have designed our stores, website and mobile application interfaces to appeal to our customers’ needs. We continue to augment our web and mobile app interfaces to enhance our “Call, Click or Come In” strategy, with a focus on adding functionality across all our channels. Our stores are branded with distinctive and recognizable signage, conveniently located and typically open seven days a week. Furthermore, we have highly experienced managers in our stores, which we believe is a critical component to driving customer retention, lowering acquisition costs and driving store-level margins. For example, the average tenure for our U.S. store managers is over seven years, for district managers is over 11 years, and for regional directors it is over 12 years. |

• | Strong compliance culture with centralized collections operations—We seek to consistently engage in proactive and constructive dialogue with regulators in each of our jurisdictions and have made significant investments in best-practice automated tools for monitoring, training and compliance management. As of December 31, 2017 our compliance group consisted of 27 individuals based in all of the countries in which we operate, and our compliance management systems are integrated into our proprietary IT platform. Additionally, our in-house centralized collections strategy, supported by our proprietary back-end customer database and analytics team, drives an effective, compliant and highly-scalable model. |

• | Demonstrated access to capital markets and diversified funding sources—We have raised over $1.1 billion of debt financing in six separate offerings since 2008, most recently in October 2017. We also closed a $150 million nonrecourse installment loan financing facility in 2016 and have routinely accessed banks and other lenders for revolving credit capacity. We believe this is a significant differentiator from our peers who may have trouble accessing capital markets to fund their business models if credit markets tighten. For more information, see Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources.” |

• | Experienced and innovative management team and sponsor—Our senior leadership team is among the most experienced in the industry with over a century of collective experience and an average tenure at CURO of over eight years. We also have deep bench strength across key functional areas including accounting, compliance, IT and legal. Our equity sponsor, FFL Partners, has been our partner since 2008 and has contributed significant resources to helping define our growth strategy. |

7

• | History of growth and profitability—Throughout our operating history we have maintained strong profitability and growth. Between 2010 and 2017 we grew revenue, Adjusted EBITDA, Net income and Adjusted Net Income at a CAGR of 24.8%, 25.0%, 13.8% and 19.8%, respectively. At the same time, we have grown our product offerings to better serve our growing and expanding customer base. |

Growth Strategy

• | Leverage our capabilities to continue growing installment and open-end products—Installment and open-end products accounted for 68% of our consolidated revenue for the year ending December 31, 2017, up from 19% in 2010, and we believe that our customers greatly prefer these products. We anticipate that these products will continue to account for a greater share of our revenue and provide us a competitive advantage versus other consumer lenders with narrower product focus. We believe that our ability to continue to be successful in developing and managing new products is based upon our capabilities in three key areas: |

• | Underwriting: Installment and open-end products generally have lower yields than single-pay products, which necessitates more stringent credit criteria supported by more sophisticated credit analytics. Our industry leading analytics platform combines data from over 74 million records (as of December 31, 2017) associated with loan information from third-party reporting agencies. |

• | Collections and Customer Service: Installment and open-end products have longer terms than single-pay loans, in some cases up to 48 months. These longer terms drive the need for a more comprehensive collection and default servicing strategy that emphasizes curing a default and putting the customer back on a track to repay the loan. We utilize a centralized collection model that prevents our branch management personnel from ever having to contact customers to resolve a delinquency. We have also invested in building new contact centers in all of the countries in which we operate, each of which utilize sophisticated dialer technologies to help us contact our customers in a scalable, efficient manner. |

• | Funding: The shift to larger balance installment loans with extended terms and open-end loans with revolving terms requires more substantial and more diversified funding sources. Given our deep and successful track record in accessing diverse sources of capital, we believe that we are well-positioned to support future new product transition. |

• | Serve additional types of borrowers—In addition to growing our existing suite of installment and open-end lending products, we are focused on expanding the total number of customers that we are able to serve through product, geographic and channel expansion. This includes expansion of our online channel, particularly in the United Kingdom, as well as continued targeted additions to our physical store footprint. We also continue to introduce additional products to address our customers’ preference for longer term products that allow for greater flexibility in managing their monthly payments. |

• | In the second quarter of 2017, we launched Avio Credit, a new online product branded in the United States targeting individuals in the 600-675 FICO band. This product is structured as an Unsecured Installment Loan with varying principal amounts and loan terms up to 48 months. As of April 2017, 10% of U.S. consumers had FICO scores between 600 and 649. A further 13.2% of U.S. consumers had FICO scores between 650 and 699, a portion of whom would fall into the credit profile targeted by our Avio Credit product. |

• | We expect to expand our LendDirect brand in Canada to include additional provinces and increase acquisition efforts in existing markets. We opened three LendDirect stores in Canada during the fourth quarter of 2017 and plan to open more in 2018. Seven million Canadians have a FICO score below 700. We estimate that the consumer credit opportunity for this customer |

8

segment exceeds C$165 billion. We believe these customers represent a highly-fragmented market with low penetration.

• | In the United Kingdom, we launched online longer-term loans in November 2017 with our Juo Loans brand. According to a study by the Financial Conduct Authority, the U.K. guarantor market in 2016 comprised £300 million in loans outstanding and had annual originations of approximately £200 million. A report by L.E.K. Consulting found that this market experienced double digit percentage growth from 2008 to 2017. We believe the U.K. guarantor loan market is currently dominated by one lender but otherwise largely made up of smaller participants with growth challenges. |

• | Continue to bolster our core business through enhancement of our proprietary risk scoring models— We continuously refine and update our credit models to drive additional improvements in our performance metrics. By regularly updating our credit underwriting algorithms we can continue to expand the value of each of our customer relationships through improved credit performance. By combining these underwriting improvements with data driven marketing spend, we believe our optimization efforts will produce margin expansion and earnings growth. |

• | Expand credit for our borrowers—Through extensive testing and our proprietary underwriting, we have successfully increased credit limits for customers, enabling us to offer “the right loan to the right customer.” The favorable take rates and successful credit performance have improved overall vintage and portfolio performance. For 2017, our average loan amount for Unsecured and Secured Installment Loans rose by $106 (a 21% increase) and $207 (a 19% increase), respectively, versus 2016. |

• | Continue to improve the customer journey and experience—We have projects in our development pipeline to enhance our “Call, Click or Come In” customer experience and execution, ranging from redesign of web and app interfaces to enhanced service features to payments optimization. |

• | Enhance our network of strategic partnerships—Our strategic partnership network generates applicants that we then close through our diverse array of marketing channels. By further leveraging these existing networks and expanding the reach of our partnership platform to include new relationships, we can increase the number of overall leads we receive. |

Customers

Our customers require essential financial services and value timely, transparent, affordable and convenient alternatives to banks, credit card companies and other traditional financial services companies. According to a recent study by FactorTrust, underbanked customers in the United States tend to have the following characteristics:

• | average age of 39 for applicants and 41 for borrowers; |

• | applicants are 47% male and 53% female; |

• | 41% are homeowners; |

• | 45% have a bachelor’s degree or higher; and |

• | the top five employment segments are Retail, Food Service, Government, Banking/Finance and Business Services. |

In the United States, our customers generally earn between $25,000 and $75,000 annually. In Canada, our customers generally earn between C$25,000 and C$60,000 annually. In the United Kingdom our customers generally earn between £18,000 and £31,000 annually. Our customers utilize the services provided by our industry for a variety of reasons, including that they often:

• | have immediate need for cash between paychecks; |

• | have been rejected for traditional banking services; |

9

• | maintain sufficient account balances to make a bank account economically efficient; |

• | prefer and trust the simplicity, transparency and convenience of our products; |

• | need access to financial services outside of normal banking hours; and |

• | reject complicated fee structures in bank products (e.g., credit cards and overdrafts). |

Products and Services

We provide Unsecured Installment Loans, Secured Installment Loans, Open-End Loans, Single-Pay Loans and a number of ancillary financial products, including check cashing, proprietary reloadable prepaid debit cards (Opt+), credit protection insurance in the Canadian market, gold buying, retail installment sales and money transfer services. We have designed our products and customer journey to be consumer-friendly, accessible and easy to understand. Our platform and product suite enable us to provide several key benefits that appeal to our customers:

• | transparent approval process; |

• | flexible loan structure, providing greater ability to manage monthly payments; |

• | simple, clearly communicated pricing structure; and |

• | full account management online and via mobile devices. |

Our centralized underwriting platform and its proprietary algorithms are used for every aspect of underwriting and scoring of our loan products. The customer application, approval, origination and funding processes differ by state, country and by channel. Our customers typically have an active phone number, open checking account, recurring income and a valid government-issued form of identification. For in-store loans, the customer presents required documentation, including a recent pay stub or support for underlying bank account activity for in-person verification. For online loans, application data is verified with third-party data vendors, our proprietary algorithms and/or tech-enabled account verification. Our proprietary, highly scalable, scoring system employs a champion/challenger process whereby models compete to produce the most successful customer outcomes and profitable cohorts. Our algorithms use data relevancy and machine learning techniques to identify approximately 60 variables from a universe of approximately 11,600 that are the most predictive in terms of credit outcomes. The algorithms are continuously reviewed and refreshed and are focused on a number of factors related to disposable income, expense trends and cash flows, among other factors, for a given loan applicant. The predictability of our scoring models is driven by the combination of application data, purchased third-party data and our robust internal database of over 74 million records (as of December 31, 2017) associated with loan information. These variables are then combined in a series of algorithms to create a score that allows us to scale lending decisions.

Geography and Channel Mix

For the years ended December 31, 2017, 2016 and 2015, approximately 77%, 73% and 71%, respectively, of our consolidated revenues were generated from services provided within the United States and approximately 19%, 23% and 23%, respectively, of our consolidated revenues were generated from services provided within Canada. For each of the years ended December 31, 2017 and 2016, approximately 60% and 61% of our long-lived assets were located within the United States, respectively and approximately 38% and 36% of our long-lived assets were located within Canada. See Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations ("MD&A")" in this Annual Report on Form 10-K for additional information on our geographic segments.

Stores: As of December 30, 2017, we had 407 stores in 14 U.S. states and seven provinces in Canada, which included the following:

• | 214 United States locations: Texas (91), California (36), Nevada (18), Arizona (13), Tennessee (11), Kansas (10), Illinois (8), Alabama (7), Missouri (5), Louisiana (5), Colorado (3), Oregon (3), Washington (2) and Mississippi (2); |

10

• | 193 Canadian locations: Ontario (124), Alberta (27), British Columbia (26), Saskatchewan (6), Nova Scotia (5), Manitoba (4) and New Brunswick (1). |

Online: We lend online in 27 states in the United States, five provinces in Canada and in England, Wales, Scotland and Northern Ireland in the United Kingdom.

Overview of Loan Products

The following charts reflect the revenue contribution, including CSO fees, of the products and services that we currently offer:

For the years ended December 31, 2017, 2016 and 2015, revenue generated through online channel was 38%, 33% and 30%, respectively, of consolidated revenue.

Below is an outline of the primary products we offered as of December 31, 2017:

Installment Unsecured | Installment Secured | Open-End | Single-Pay | |

Channel | Online and in-store: 15 U.S. States, Canada and the U.K. (1) | Online and in-store: 7 U.S. States | Online: KS, TN, ID, UT, RI, VA, DE and Canada. In-Store: KS, TN and Canada. | Online and in-store: 12 U.S. States, Canada and the U.K. (1) |

Average Loan Size (2) | $629 | $1,303 | $579 | $334 |

Duration | Up to 48 months | Up to 42 months | Revolving/Open-Ended | Up to 62 days |

Pricing | 15.1% average monthly interest rate (3) | 11.4% average monthly interest rate (3) | Daily interest rates ranging from 0.74% to 0.99% | Fees ranging from $13 to $25 per $100 borrowed |

(1) Online only in the United Kingdom | ||||

(2) Includes CSO loans | ||||

(3) Weighted average of the contractual interest rates for the portfolio as of December 31, 2017. Excludes CSO fees | ||||

Unsecured Installment Loans

Unsecured Installment Loans are fixed-term, fully amortizing loans with a fixed payment amount due each period during the term of the loan. Loans are originated and owned by us or third-party lenders pursuant to credit services organization and credit access business statutes, which we refer to as our CSO programs. For CSO programs, we arrange and guarantee the loans. Payments are due bi-weekly or monthly to match the customer's pay cycle. Customers may prepay without penalty or fees. Unsecured Installment Loan terms are governed by

11

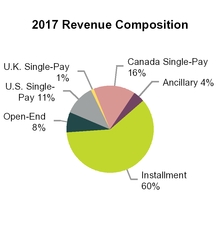

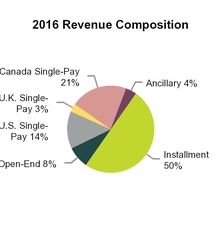

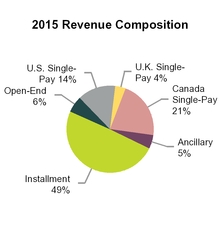

enabling state legislation in the United States, provincial and federal legislation and national regulations in Canada and national regulation in the United Kingdom. Unsecured Installment Loans comprised 49.8%, 39.9% and 38.7% of our consolidated revenue during the years ended December 31, 2017, 2016 and 2015, respectively. We believe that the flexible terms and lower payments associated with Installment Loans significantly expand our addressable market by allowing us to serve a broader range of customers with a variety of credit needs.

Secured Installment Loans

Secured Installment Loans are similar to Unsecured Installment Loans but are also secured by a vehicle title. These loans are originated and owned by us or by third-party lenders through our CSO programs. For these loans the customer provides clear title or security interest in the vehicle as collateral. The customer receives the benefit of immediate cash but retains possession of the vehicle while the loan is outstanding. The loan requires periodic payments of principal and interest with a fixed payment amount due each period during the term of the loan. Payments are due bi-weekly or monthly to match the customer's pay cycle. Customers may prepay without penalty or fees. Secured Installment Loan terms are governed by enabling state legislation in the United States. Secured Installment Loans comprised 10.5%, 9.8%, and 10.6% of our consolidated revenue during the years ended December 31, 2017, 2016 and 2015, respectively.

Open-End Loans

Open-End Loans are a line of credit for the customer without a specified maturity date. Customers may draw against their line of credit, repay with minimum, partial or full payment and redraw as needed. We report and earn interest on the outstanding loan balances drawn by the customer against their approved credit limit. Customers may prepay without penalty or fees. Typically, customers do not draw the full amount of their credit limit. Loan terms are governed by enabling state legislation in the United States. Unsecured Open-End Loans comprised 6.7%, 7.0% and 5.2% of our consolidated revenue during the years ended December 31, 2017, 2016 and 2015, respectively. Secured Open-End Loans are offered as part of our product mix in states with enabling legislation and accounted for approximately 0.9%, 1.0%, and 1.2% of our consolidated revenue during the years ended December 31, 2017, 2016 and 2015, respectively.

Single-Pay Loans

Single-Pay Loans are generally unsecured short-term, small-denomination loans whereby a customer receives cash in exchange for a post-dated personal check or a pre-authorized debit from the customer’s bank account. We agree to defer deposit of the check or debiting of the customer’s bank account until the loan due date, which typically falls on the customer’s next pay date. Single-Pay loans are governed by enabling state legislation in the United States, provincial and federal legislation in Canada and national regulation in the United Kingdom. Single-Pay Loans comprised 27.9%, 37.8%, and 39.6% of our consolidated revenue during the years ended December 31, 2017, 2016 and 2015, respectively. Single-Pay Loans originated in the U.S. comprised 11%, 14%, and 14% of our consolidated revenue during the years ended December 31, 2017, 2016 and 2015, respectively.

Ancillary Products

We also provide a number of ancillary financial products including check cashing, proprietary reloadable prepaid debit cards (Opt+), credit protection insurance in the Canadian market, gold buying, retail installment sales and money transfer services. We had over 120,000 active Opt+ cards as of December 31, 2017, which includes any card with a positive balance or transaction in the past 90 days. Opt+ customers have loaded over $1.7 billion to their cards since we started offering this product in 2011.

CSO Programs

Through our CSO programs, we act as a credit services organization/credit access business on behalf of customers in accordance with applicable state laws. We currently offer loans through CSO programs in stores and online in the state of Texas and online in the state of Ohio. In Texas we offer Unsecured Installment Loans and

12

Secured Installment Loans with a maximum term of 180 days. In Ohio we offer an Unsecured Installment Loan product with a maximum term of 18 months. As a CSO we earn revenue by charging the customer a fee, or the CSO fee, for arranging an unrelated third-party to make a loan to that customer.

We currently have relationships with four unaffiliated third-party lenders for our CSO programs. We periodically evaluate the competitive terms of our unaffiliated third-party lender contracts and such evaluation may result in the transfer of volume and loan balances between lenders. The process does not require significant effort or resources outside the normal course of business and we believe the incremental cost of changing or acquiring new unaffiliated third-party lender relationships to be immaterial.

When a customer executes an agreement with us under our CSO programs, we agree to provide certain services to the customer for a CSO fee payable to us by the customer. One of the services is to guarantee the customer’s obligation to repay the loan the customer receives from the third-party lender. CSO fees are calculated based on the amount of the customer’s outstanding loan. For CSO loans, each lender is responsible for providing the criteria by which the customer’s application is underwritten and, if approved, determining the amount of the customer loan. We in turn are responsible for assessing whether or not we will guarantee the loan. This guarantee represents an obligation to purchase specific loans if they go in to default.

The maximum amount payable under all such guarantees was $65.2 million at December 31, 2017, compared to $59.6 million at December 31, 2016. Should we be required to pay any portion of the total amount of the loans we have guaranteed, we will attempt to recover some or the entire amount from the customers. We hold no collateral in respect of the guarantees.

These guarantees are performance guarantees as defined in ASC Topic 460. Performance guarantees are initially accounted for pursuant to ASC Topic 460 and recognized at fair value and subsequently, pursuant to ASC Topic 450, as contingent liabilities when we incur losses as the guarantor. The initial measurement of the guarantee liability is recorded at fair value and reported in "Credit services organization guarantee liability" in our Consolidated Balance Sheets. The initial fair value of the guarantee is the price we would pay to a third party market participant to assume the guarantee liability. There is no active market for transferring the guarantee liability. Accordingly, we determine the initial fair value of the guarantee by estimating the expected losses on the guaranteed loans. The expected losses on the guaranteed loans are estimated by assessing the nature of the loan products, the credit worthiness of the borrowers in the customer base, our historical loan default history for similar loans, industry loan default history, and historical collection rates on similar products, current default trends, past-due account roll rates, changes to underwriting criteria or lending policies, new store development or entrance into new markets, changes in jurisdictional regulations or laws, recent credit trends and general economic conditions. We review the factors that support estimates of expected losses and the guarantee liability monthly. In addition, because the majority of the underlying loan customers make bi-weekly payments, loan-pool payment performance is evaluated more frequently than monthly.

Our guarantee liability was $17.8 million and $17.1 million at December 31, 2017 and 2016, respectively. This liability represents the unamortized portion of the guarantee obligation required to be recognized at inception of the performance guarantee in accordance with ASC Topic 460 and a contingent liability for those performance guarantees where it is probable that we will be required to purchase the guaranteed loan from the lender in accordance with ASC Topic 450.

CSO fees are calculated based on the amount of the customer’s outstanding loan. We comply with the applicable jurisdiction’s Credit Services Organization Act or a similar statute. These laws generally define the services that we can provide to consumers and require us to provide a contract to the customer outlining our services and the cost of those services to the customer. For services we provide under our CSO programs, we receive payments from customers on their scheduled loan repayment due dates. The CSO fee is earned ratably over the term of the loan as the customers make payments. If a loan is paid off early, no additional CSO fees are due or collected. The maximum CSO loan term is 180 days and 18 months in Texas and Ohio, respectively. During the years ended December 31, 2017 and 2016, approximately 53.6% and 53.2%, respectively, of Unsecured Installment Loans,

13

and 53.6% and 62.5%, respectively, of Secured Installment Loans originated under CSO programs were paid off prior to the original maturity date.

Since CSO loans are made by a third party lender, we do not include them in our Consolidated Balance Sheets as loans receivable. CSO fees receivable are included in “Prepaid expense and other” in our Consolidated Balance Sheets. We receive payments from customers for these fees on their scheduled loan repayment due dates.

The majority of revenue generated through our CSO programs was for Unsecured Installment Loans, which comprised 96.4%, 91.6% and 94.0% of total CSO revenue for the years ended December 31, 2017, 2016 and 2015, respectively.

Total revenue generated through our CSO programs comprised 26.6%, 26.1% and 24.6% of our consolidated revenue during the years ended December 31, 2017, 2016 and 2015, respectively.

Sales and Marketing

We are focused on capturing new accounts as demonstrated by the 2.0 million new customers we acquired between January 2015 and December 2017 in our U.S. market. In 2015, we experienced an increase in advertising expense as a result of a strategy to gain market share during a period of time when we believed the online market was disrupted. We returned to more normalized spend levels in 2016 and 2017 following the surge in advertising expense in 2015, but with better efficiency because of improved analytics and an accelerating shift to mobile and online.

United States

Our marketing efforts focus on a variety of targeted, direct response strategies. We use various forms of media to build brand awareness and drive customer traffic in stores, online and to our contact centers. These strategies include direct response spot television in each operating market, radio campaigns, point-of-purchase materials, a multi-listing and directory program for print and online yellow pages, local store marketing activities, prescreen direct mail campaigns, robust online marketing strategies and “send a friend” and word-of-mouth referrals from satisfied customers. We also utilize our unique capability to drive customers originated online to our store locations–a program we call “Site-to-Store.”

Canada

The Cash Money platform has built strong brand awareness as a leading provider of alternative financial solutions in Canada. Cash Money’s marketing efforts have historically included high frequency television buys, print media and targeted publications, as well as local advertising in the communities we serve.

United Kingdom

Wage Day has built a strong brand name as a leading on-line provider of short-term consumer loans to individuals in the United Kingdom. Wage Day’s marketing efforts include direct marketing of its existing customer base through a variety of channels, including email and text messaging, and new customer acquisition through leads purchased through its affiliates.

Over the past several years, we have redesigned and reformulated our U.K. loan products, including the introduction of new installment products in 2016 and 2017, and enhanced our customer acquisition, underwriting and collection capabilities.

Information Systems

14

The Curo Platform is our proprietary IT platform, which is a unified, centralized platform that seamlessly integrates activities related to customer acquisition, underwriting, scoring, servicing, collections, compliance and reporting. The Curo Platform is scalable and has been successfully implemented in the United States, Canada and the United Kingdom. The Curo Platform is designed to enable us to support and monitor compliance with regulatory and other legal requirements applicable to the financial products we offer. Our platform captures transactional history by store and by customer, which allows us to track loan originations, payments, defaults and payoffs, as well as historical collection activities on past-due accounts. In addition, our stores perform automated daily cash reconciliation at each store and every bank account in the system. This fully-integrated IT platform enables us to make real-time, data-driven changes to our acquisition and risk models, which yield significant benefits in terms of customer acquisition costs and credit performance. Each of our stores has secure, real-time access to corporate servers and the most up to date information to maintain consistent underwriting standards. All loan applications are scanned and electronic copies are centrally stored for convenient access and retrieval. Our IT platform contains over 15 years of continually updated customer data comprising over 74 million loan records (as of December 31, 2017) to formulate our robust, proprietary underwriting algorithms. This platform then automatically applies multi-algorithmic analysis to a customer’s loan application to produce a “Curo Score,” which drives our underwriting decision. Globally, as of December 31, 2017 we have over 185 employees who write code and manage our networks and infrastructure for our IT platform.

Collections

To enable store-level employees to focus on customer service and to improve effectiveness and compliance management, we operate centralized collection facilities in the United States, Canada and the United Kingdom. Our collections personnel are trained to optimize regulatory-compliant loan repayment while treating our customers fairly. Our collections personnel contact customers after a missed payment, primarily via phone calls, letters and emails and help the customer understand available payment arrangements or alternatives to satisfy the deficiency. We use a variety of collections strategies, including payment plans, settlements and adjustments to due dates. Collections teams are trained to apply different strategies and tools for the various stages of delinquency and also vary methodologies by product type.

Our collections centers in Wichita, Kansas, Toronto, Ontario and Nottingham, United Kingdom employed a total of over 265 collection professionals as of December 31, 2017.

We assign all our delinquent loan accounts in the United States to an affiliated third-party collection agency once they are 91 to 121 days past due. Under our policy, the precise number of days past due to trigger a referral varies by state and product and requires, among other things, that proper notice be delivered to the customer. Once a loan meets the criteria set forth in the policy, it is automatically referred for collection. We make changes to our policy periodically in response to various factors, including regulatory developments and market conditions. Our policy is established and implemented by our chief operating officer, senior vice president in charge of collections and our chief executive officer. As delinquent accounts are paid, the Curo Platform updates these accounts in real time. This ensures that collection activity will cease the moment a customer’s account is brought current or paid in full and considered in “good standing.” See Note 20 - “Related Party Transactions” in the Notes to Consolidated Financial Statements in this Annual Report for a description of our relationship with our third-party collection agency.

Competition

We believe that the primary factors upon which we compete are:

• | range of services; |

• | flexibility of product offering; |

• | convenience; |

• | reliability; |

• | fees; and |

15

• | speed. |

Our underbanked customers tend to value service that is quick and convenient, lenders that can provide the most appropriate structure and terms and payments that are affordable. We face competition in all of our markets from other alternative financial services providers, banks, savings and loan institutions, short-term consumer lenders and other financial services entities. Generally, the landscape is characterized by a small number of large, national participants with a significant presence in markets across the country and a significant number of smaller localized operators. Our competitors in the alternative financial services industry include monoline operators (both public and private) specializing in short-term cash advances, multiline providers offering cash advance services in addition to check cashing and other services and subprime specialty finance and consumer finance companies, as well as businesses conducting operations online and by phone.

Employees

As of December 31, 2017, we had approximately 4,180 employees worldwide, approximately 3,000 of whom work in our stores. None of our employees are unionized or covered by a collective bargaining agreement, and we consider our current employee relations to be good.

We believe that customer service is critical to our continued success and growth. As such, we have staffed each of our stores with a full-time Store Manager or Branch Manager, or Manager, that runs the day-to-day operations of the store. The Manager is typically supported by two to three Senior Assistant Managers and/or Assistant Managers and three to eight full-time Customer Advocates. A newer store will typically ramp up with a Manager, a Senior Assistant Manager, two Assistant Managers and two Customer Advocates. Customer Advocates conduct the point-of-sale activities and greet and interact with customers from a secured area behind expansive windows. We believe staff continuity is critical to our business. We believe that our pay rates are equal to or better than all of our major competitors and we constantly evaluate our benefit plans to maintain their competitiveness.

Regulatory Environment and Compliance

The alternative financial services industry is regulated at the federal, state and local levels in the United States; at the federal and provincial levels in Canada; and at the central government level in the United Kingdom. In general, these regulations are designed to protect consumers and the public, while providing standard guidelines for business operations. Laws and regulations typically impose restrictions and requirements, such as governing interest rates and fees, maximum loan amounts, the number of simultaneous or consecutive loans, required waiting periods between loans, loan extensions and refinancings, payment schedules (including maximum and minimum loan durations), required repayment plans for borrowers claiming inability to repay loans, disclosures, security for loans and payment mechanisms, licensing, and in certain jurisdictions database reporting and loan utilization information. We are also subject to federal, state, provincial and local laws and regulations relating to our other financial products, including laws and regulations governing recording and reporting certain financial transactions, identifying and reporting suspicious activities and safeguarding the privacy of customers’ non-public personal information. For more information regarding the regulations applicable to our business and the risks to which they subject us, see the section entitled “Risk Factors” in this Annual Report.

The legal environment is constantly changing as new laws and regulations are introduced and adopted, and existing laws and regulations are repealed, amended, modified and reinterpreted. We regularly work with authorities, both directly and through our active memberships in industry trade associations, to support our industry and to promote the development of laws and regulations that are equitable to businesses and consumers alike.

Regulatory authorities at various levels of government and voters have enacted, and will likely continue to propose, new rules and regulations impacting our industry. Due to the evolving nature of laws and regulations, further rulemaking could result in new or expanded regulations that may adversely impact current product offerings or alter the economic performance of our existing products and services. For example, a rule recently adopted by the CFPB threatens to do just that if and when it becomes effective. In addition, the CFPB is expected

16

to propose a rule that will restrict debt collector communications with consumers. Although the rule is not expected to apply directly to our activities, such a rule might impact third party debt collection on behalf of us, and the CFPB might use its supervisory authority to impose similar restrictions on the Company. We cannot provide any assurances that additional federal, state, provincial or local statutes or regulations will not be enacted in the future in any of the jurisdictions in which we operate. It is possible that future changes to statutes or regulations will have a material adverse effect on our results of operations and financial condition.

U.S. Regulations

U.S. Federal Regulations

The U.S. federal government and its respective agencies possess significant regulatory authority over consumer financial services. The body of laws to which we are subject has a significant impact on our operations. In November 2017, the CFPB published a rule specifically targeted at payday, vehicle title and certain high-cost installment loans ( “CFPB Rule”) that could have such an impact if it becomes effective.

Dodd-Frank: In 2010, the U.S. Congress passed the Dodd-Frank Act. Title X of this legislation created the CFPB, which became operational in July 2011. Title X provides the CFPB with broad rule-making, supervisory and enforcement powers with regard to consumer financial services. Title X of Dodd-Frank also contains so-called “UDAAP” provisions declaring unlawful “unfair,” “deceptive” and “abusive” acts and practices in connection with the delivery of consumer financial services and giving the CFPB the power to enforce UDAAP prohibitions and to adopt UDAAP rules defining unlawful acts and practices. Additionally, the FTC Act prohibits “unfair” and “deceptive” acts and practices and gives the FTC enforcement authority to prevent and redress violations of this prohibition.

CFPB Rule: Pursuant to its authority to adopt UDAAP rules, the CFPB published in the Federal Register on November 17, 2017 a new rule applicable to payday, title and certain high-cost installment loans. The provisions of this CFPB Rule directly applicable to us are scheduled to become effective in August 2019. However, the CFPB Rule remains subject to potential override by Congress pursuant to the Congressional Review Act. Moreover, CFPB leadership changed in November 2017 and the agency is currently headed by an Acting Director. The Acting Director or successor could suspend, delay or modify the CFPB Rule. Further, we expect that important elements of the CFPB Rule will be subject to legal challenge by trade groups or other private parties. Legislation was introduced in the House of Representatives December 1, 2017 to consider a review of the CFPB Rule. We cannot predict at this time whether Congress will allow the rule to stand or whether private legal challenges will be successful. Thus, it is impossible to predict whether and when the CFPB Rule will go into effect and, if so, whether and how it might be modified or the impact on our business and operations.

In its current form, the CFPB Rule establishes ability-to-repay, or ATR, requirements for “covered short-term loans” and “covered longer-term balloon-payment loans,” as well as payment limitations on these loans and “covered longer-term loans.” Covered short-term loans are consumer loans with a term of 45 days or less. Covered longer-term balloon payment loans include consumer loans with a term of more than 45 days where (i) the loan is payable in a single payment, (ii) any payment is more than twice any other payment, or (iii) the loan is a multiple advance loan that may not fully amortize by a specified date and the final payment could be more than twice the amount of other minimum payments. Covered longer-term loans are consumer loans with a term of more than 45 days where (i) the total cost of credit exceeds an annual rate of 36%, and (ii) the lender obtains a form of “leveraged payment mechanism” giving the lender a right to initiate transfers from the consumer’s account. Post-dated checks, authorizations to initiate ACH payments and authorizations to initiate prepaid or debit card payments are all leveraged payment mechanisms under the CFPB Rule.

The CFPB Rule excludes from coverage, among other loans: (1) purchase-money credit secured by the vehicle or other goods financed (but not unsecured purchase-money credit or credit that finances services as opposed to goods); (2) real property or dwelling-secured credit if the lien is recorded or perfected; (3) credit cards; (4) student loans; (5) non-recourse pawn loans; and (6) overdraft services and overdraft lines of credit. These exclusions do not apply to our loans.

17

Under the provisions of the CFPB Rule applicable to covered short-term loans and covered longer-term balloon payment loans, a lender will need to choose between:

• | A “full payment test,” under which the lender must make a reasonable determination of the consumer’s ability to repay the loan and cover major financial obligations and living expenses over the term of the loan and the succeeding 30 days. Under this test, the lender must take account of the consumer’s basic living expenses and obtain and generally verify evidence of the consumer’s income and major financial obligations. However, in circumstances where a lender determines that a reliable income record is not reasonably available, such as when a consumer receives and spends income in cash, the lender may reasonably rely on the consumer’s statements alone as evidence of income. Further, unless a housing debt obligation appears on a national consumer report, the lender may reasonably rely on the consumer's written statement. As part of the ATR determination, the CFPB Rule permits lenders and consumers to rely on income from third parties, such as spouses, to which the consumer has a reasonable expectation of access and permits lenders in certain circumstances to consider whether another person is regularly contributing to the payment of major financial obligations or basic living expenses. A 30-day cooling off period applies after a sequence of three covered short-term or longer-term balloon payment loans. |

• | A “principal-payoff option,” under which the lender may make up to three sequential loans, or Section 1041.6 Loans, without engaging in an ATR analysis. The first Section 1041.6 Loan in any sequence of Section 1041.6 Loans without a 30-day cooling off period between loans is limited to $500, the second is limited to a principal amount that is at least one-third smaller than the principal amount of the first, and the third is limited to a principal amount that is at least two-thirds smaller than the principal amount of the first. A lender may not use this option if (i) the consumer had in the past 30 days an outstanding covered short-term loan or an outstanding longer-term balloon payment loan that is not a Section 1041.6 Loan, or (ii) the new Section 1041.6 Loan would result in the consumer having more than six covered short-term loans (including Section 1041.6 Loans) during a consecutive 12-month period or being in debt for more than 90 days on such loans during a consecutive 12-month period. For Section 1041.6 Loans, the lender cannot take vehicle security or structure the loan as open-end credit. |

Covered longer-term loans that are not balloon loans are not subject to the foregoing requirements. However, such loans are subject to the CFPB Rule's “penalty fee prevention” provisions, which apply to all covered loans. Under these provisions:

• | If two consecutive attempts to collect money from a particular account of the borrower, made through any channel (e.g., paper check, ACH, prepaid card) are returned for insufficient funds, the lender cannot make any further attempts to collect from such account unless the borrower has provided a new and specific authorization for additional payment transfers. The CFPB Rule contains specific requirements and conditions for the authorization. While the CFPB has explained that these provisions are designed to limit bank penalty fees to which consumers may be subject, and while banks do not charge penalty fees on card authorization requests, the CFPB Rule nevertheless treats card authorization requests as payment attempts subject to these limitations. |

• | A lender generally must give the consumer at least three business days advance notice before attempting to collect payment by accessing a consumer’s checking, savings, or prepaid account. The notice must include information such as the date of the payment request, payment channel and payment amount (broken down by principal, interest, fees, and other charges), as well as additional information for “unusual attempts,” such as when the payment is for a different amount than the regular payment, initiated on a date other than the date of a regularly scheduled payment or initiated in a different channel that the immediately preceding payment attempt. |

The CFPB Rule also requires the CFPB’s registration of consumer reporting agencies as “registered information systems” to whom lenders must furnish information about covered short-term and longer-term balloon loans and

18

from whom lenders must obtain consumer reports for use in extending such credit. If there is no registered information system or if no registered information system has been registered for at least 180 days, lenders will be unable to make Section 1041.6 Loans. The CFPB expects that there will be at least one registered information system in time for lenders to avail themselves of the option to make Section 1041.6 Loan by the effective date of the CFPB Rule.

For a discussion of the potential impact of the CFPB Rule on us, see “-Risks Relating to the Regulation of Our Industry-The CFPB promulgated new rules applicable to our loans that could have a material adverse effect on our business and results of operations” in Item 1A. "Risk Factors" of this Annual Report.

CFPB Enforcement: In addition to the Dodd-Frank Act’s grant of rule-making authority, which resulted in the CFPB Rule, the Dodd-Frank Act gives the CFPB authority to pursue administrative proceedings or litigation for violations of federal consumer financial laws (including Dodd-Frank’s UDAAP provisions and the CFPB’s own rules). In these proceedings, the CFPB can obtain cease and desist orders (which can include orders for restitution or rescission of contracts, as well as other kinds of affirmative relief) and monetary penalties ranging from $5,000 per day for ordinary violations of federal consumer financial laws to $25,000 per day for reckless violations and $1 million per day for knowing violations. Also, where a company has violated Title X of the Dodd-Frank Act or CFPB regulations promulgated thereunder, the Dodd-Frank Act empowers state attorneys general and state regulators to bring civil actions for the kind of cease and desist orders available to the CFPB (but not for civil penalties). Potentially, if the CFPB, the FTC or one or more state officials believe we have violated the foregoing laws, they could exercise their enforcement powers in ways that would have a material adverse effect on us.

CFPB Supervision and Examination: Additionally, the CFPB has supervisory powers over many providers of consumer financial products and services, including explicit authority to examine (and require registration) of payday lenders. The CFPB released its Supervision and Examination Manual, which includes a section on Short-Term, Small-Dollar Lending Procedures, and began field examinations of industry participants in 2012. The CFPB commenced its first supervisory examination of us in October 2014. The scope of the CFPB’s examination included a review of our Compliance Management System, our Short-Term Small Dollar lending procedures, and our compliance with Federal consumer financial protection laws. The 2014 examination had no material impact on our financial condition or results of operations, and we received the final CFPB Examination Report in September 2015.

The CFPB commenced its second examination of us in February 2017 and completed the related field work in June 2017. The scope of the 2017 examination included a review of our our Compliance Management System, our substantive compliance with applicable federal laws, and matters requiring attention. The 2017 examination had no material impact on our financial condition or results of operations, and we received the final CFPB Examination Report in February 2018.

Reimbursement Offer; Possible Changes in Payment Practices: During 2017, it was determined that a limited universe of borrowers may have incurred bank overdraft or non-sufficient funds fees because of possible confusion about certain electronic payments we initiated on their loans. As a result, we have decided to reimburse such fees through payments or credits against outstanding loan balances, subject to per-customer dollar limitations, upon receipt of (1) claims from potentially affected borrowers stating that they were in fact confused by our practices and (2) bank statements from such borrowers showing that fees for which reimbursement is sought were incurred at a time that such borrowers might reasonably have been confused about our practices. Based on the terms of the reimbursement offer we are currently considering, we have recorded a $2.0 million liability for this matter as of December 31, 2017.

While we do not expect that matters arising from the CFPB examinations will have a material impact on us, we have made in recent years and are continuing to make, at least in part to meet CFPB expectations, certain enhancements to our compliance procedures and consumer disclosures. For example, we are in the process of evaluating our payment practices. Even in advance of the effective date of the CFPB Rule (and even if the CFPB Rule does not become effective for one reason or another), we may make changes to these practices in a manner

19

that will increase costs and/or reduce revenues.

Anti-Arbitration Rule. Under its authority to regulate pre-dispute arbitration provisions pursuant to Section 1028 of Dodd-Frank, in July 2017 the CFPB issued a final rule prohibiting the use of mandatory arbitration clauses with class action waivers in agreements for certain consumer financial products and services, effective as to arbitration agreements entered into on or after March 19, 2019. However, the Anti-Arbitration Rule was overturned by Congress on October 24, 2017, and the President signed the joint resolution on November 1, 2017 to repeal the Anti-Arbitration Rule. As a result, the rule will not become effective, and, pursuant to the Congressional Review Act, substantially similar rules may only be reissued with specific legislative authorization.

MLA: The Military Lending Act, or MLA, enacted in 2006 and implemented by the Department of Defense, or DoD, imposes a 36% cap on the “all-in” annual percentage rates charged on certain loans to active-duty members of the U.S. military, reserves and National Guard and their respective dependents. As initially adopted, the MLA and related DoD rules applied to our loans with terms up to 90 days. However, in 2016, the DoD expanded its MLA regulations, effective in October 2016, to encompass some of our longer-term Installment Loans that were not previously covered. As a result, we ceased offering short-term consumer loans to these applicants in 2007 and all loans to these applicants in 2016.

Enumerated Consumer Financial Services Laws, TCPA and CAN-SPAM: Federal law imposes additional requirements on us with respect to our consumer lending. These requirements include disclosure requirements under the Truth in Lending Act, or TILA, and Regulation Z. TILA and Regulation Z require creditors to deliver disclosures to borrowers prior to consummation of both closed-end and open-end loans and, additionally for open-end credit products, periodic statements and change in terms notices. For closed-end loans, the annual percentage rate, the finance charge, the amount financed, the total of payments, the number and amount of payments and payment due dates, late fees and security interests must all be disclosed. For open end credit, the borrower must be provided with key information that includes annual percentage rates and balance computation methods, various fees and charges, and security interests.