Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - Ciner Resources LP | exhibit312-december312017.htm |

| EX-32.1 - EXHIBIT 32.1 - Ciner Resources LP | exhibit321-december312017.htm |

| EX-10.16 - EXHIBIT 10.16 - Ciner Resources LP | a1016wyw079420sodlse.htm |

| EX-21.1 - EXHIBIT 21.1 - Ciner Resources LP | exhibit211-december312017.htm |

| EX-95.1 - EXHIBIT 95.1 - Ciner Resources LP | exhibit951-december312017.htm |

| EX-32.2 - EXHIBIT 32.2 - Ciner Resources LP | exhibit322-december312017.htm |

| EX-31.1 - EXHIBIT 31.1 - Ciner Resources LP | exhibit311-december312017.htm |

| EX-23.2 - EXHIBIT 23.2 - Ciner Resources LP | exhibit232-december312017.htm |

| EX-23.1 - EXHIBIT 23.1 - Ciner Resources LP | exhibit231-december312017.htm |

| EX-10.18 - EXHIBIT 10.18 - Ciner Resources LP | a1018wyw0111731sodlse.htm |

| EX-10.17 - EXHIBIT 10.17 - Ciner Resources LP | a1017wyw0111730sodlse.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One) | |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 31, 2017

OR | |

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______ to ________ | |

Commission file number: 001-36062

CINER RESOURCES LP

(Exact name of registrant as specified in its charter)

DELAWARE (State or other jurisdiction of Incorporation or Organization) | 46-2613366 (I.R.S. Employer Identification No.) |

Five Concourse Parkway

Suite 2500

Atlanta, Georgia 30328

(Address of Principal Executive Offices) (Zip Code)

Registrant’s telephone number, including area code: (770) 375-2300

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common units representing limited partnership interests | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ | Accelerated filer þ | Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Emerging growth company x | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. x

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes ¨ No þ

The aggregate market value, as of June 30, 2017, of the common units held by non-affiliates of the registrant, based on the reported closing price of such units on the New York Stock Exchange on such date ($27.40 per common unit), was approximately $139.2 million.

The registrant had 19,725,696 common units and 399,000 general partner units outstanding at March 2, 2018, the most recent practicable date.

Documents Incorporated by Reference: None

1

CINER RESOURCES LP

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

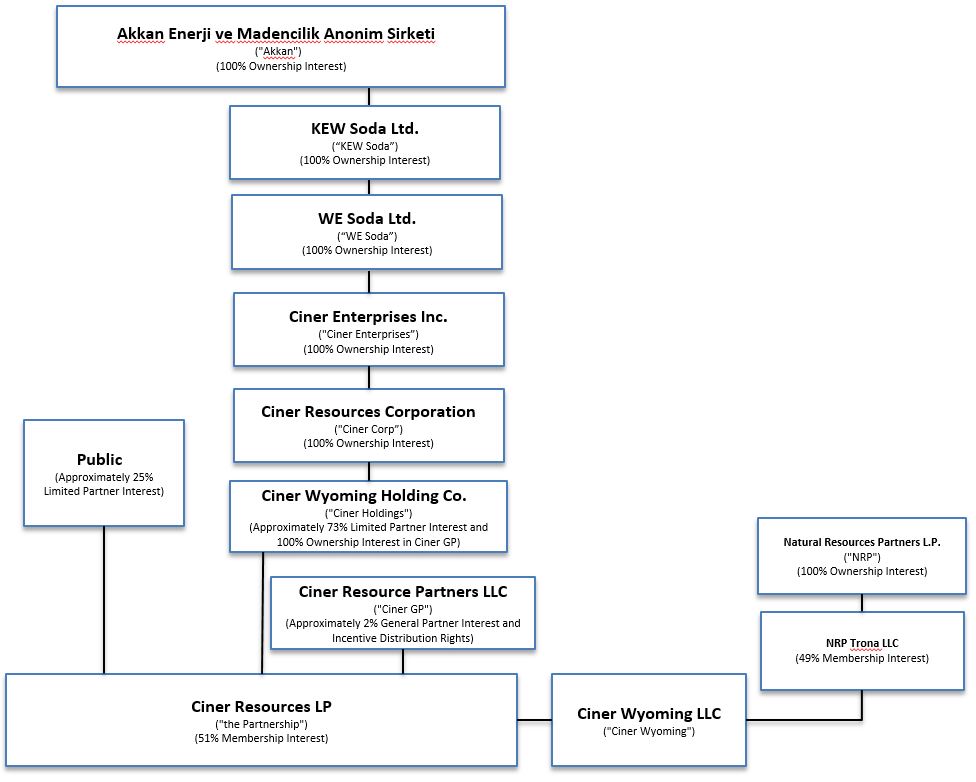

References in this Annual Report on Form 10-K (“Report”) to the “Predecessor,” “we,” “our,” “us,” or like terms, when used in a historical context (periods prior to September 18, 2013, the closing date of our initial public offering (“IPO”), refer to Ciner Wyoming Holding Co., a Delaware company (“Ciner Holdings”) and its subsidiary, our predecessor for accounting purposes. References in this Report to “CINR,” the “Partnership,” “we,” “our,” “us,” or like terms, when used in the present tense or prospectively (starting September 18, 2013), refer to Ciner Resources LP, a Delaware limited partnership, and its subsidiary. References to “Ciner Wyoming” refer to Ciner Wyoming LLC, a Delaware limited liability company and consolidated subsidiary of the Partnership. References to “our general partner” or “Ciner GP” refer to Ciner Resource Partners LLC, a Delaware limited liability company and the general partner of Ciner Resources LP and a direct wholly-owned subsidiary of Ciner Holdings, which is a direct wholly-owned subsidiary of Ciner Resources Corporation, a Delaware corporation (“Ciner Corp”). Ciner Corp is a direct wholly-owned subsidiary of Ciner Enterprises Inc., a Delaware corporation (“Ciner Enterprises”), which is a direct wholly-owned subsidiary of WE Soda Ltd., a U.K. corporation (“WE Soda”). WE Soda is a direct wholly-owned subsidiary of KEW Soda Ltd., a U.K. corporation (“KEW Soda”), which is a direct wholly-owned subsidiary of Akkan Enerji ve Madencilik Anonim Şirketi (“Akkan”). Akkan is directly and wholly owned by Turgay Ciner, the Chairman of the Ciner Group (“Ciner Group”), a Turkish conglomerate of companies engaged in energy and mining (including soda ash mining), media and shipping markets. All our soda ash processed is currently sold to various domestic and international customers, including American Natural Soda Ash Corporation (“ANSAC”) and Ciner Ic ve Dis Ticaret Anonim Sirketi (“CIDT”), both of which are our affiliates for export sales.

We include cross references to captions elsewhere in this Annual Report on Form 10-K, which we refer to as this “Report,” where you can find related additional information. The following table of contents tells you where to find these captions.

2

Page Number | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

Item 16. | ||

3

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS

This Report contains, and our other public filings and oral and written statements by us and our management may include, statements that constitute “forward-looking statements” within the meaning of the United States securities laws. Forward-looking statements include the information concerning our possible or assumed future results of operations, reserve estimates, business strategies, financing plans, competitive position, potential growth opportunities, potential operating performance, the effects of competition and the effects of future legislation or regulations. Forward-looking statements include all statements that are not historical facts and in some cases may be identified by the use of forward-looking terminology such as the words “believe,” “expect,” “plan,” “intend,” “seek,” “anticipate,” “estimate,” “predict,” “forecast,” “project,” “potential,” “continue,” “may,” “will,” “could,” “should” or the negative of these terms or similar expressions. Examples of forward-looking statements include, but are not limited to, statements concerning cash available for distribution and future distributions, if any, and such distributions are subject to the approval of the board of directors of our general partner and will be based upon circumstances then existing. We have based our forward-looking statements on management’s beliefs and assumptions and on information currently available to us.

Forward-looking statements involve risks, uncertainties and assumptions. You should not put undue reliance on any forward-looking statements. After the date of this Report, we do not have any intention or obligation to update any forward-looking statement, whether as a result of new information or future events, and expressly disclaim any obligation to do so except as required by applicable law.

The risk factors discussed in Item 1A. “Risk Factors” and the factors discussed in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” could cause our actual results to differ materially from those expressed in forward-looking statements. These factors should not be construed as exhaustive and there may also be other risks that we are unable to predict at this time. All forward-looking statements included in this Report are expressly accompanied and qualified in their entirety by these cautionary statements.

4

PART I

Item 1. Business

Overview

The Partnership was formed in April 2013 by Ciner Holdings. The Partnership owns a controlling interest comprised of 51.0% membership interest in Ciner Wyoming, which is one of the largest and lowest cost producers of natural soda ash in the world, serving a global market from our facility in the Green River Basin of Wyoming. Our facility has been in operation for more than 50 years.

The following table sets forth certain operating data regarding our business:

Year Ended December 31, | ||||||||||||||

2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||

Operating and Other Data: | (thousands of short tons, except for ratio data) | |||||||||||||

Trona ore consumed | 4,001.3 | 4,050.4 | 4,040.3 | 3,869.5 | 3,921.5 | |||||||||

Ore to ash ratio(1) | 1.50: 1.0 | 1.50: 1.0 | 1.52: 1.0 | 1.52: 1.0 | 1.59: 1.0 | |||||||||

Soda ash volume produced | 2,666.9 | 2,695.3 | 2,662.9 | 2,543.9 | 2,461.5 | |||||||||

Soda ash volume sold | 2,705.4 | 2,735.7 | 2,655.4 | 2,548.3 | 2,492.2 | |||||||||

(1) | Ore to ash ratio expresses the number of short tons of trona ore used to produce one short ton of soda ash and liquor and includes our deca rehydration recovery process. In general, a lower ore to ash ratio results in lower costs and improved efficiency. |

Trona, a naturally occurring soft mineral, is also known as sodium sesquicarbonate and consists primarily of sodium carbonate, or soda ash, sodium bicarbonate and water. We process trona ore into soda ash, which is an essential raw material in flat glass, container glass, detergents, chemicals, paper and other consumer and industrial products. The vast majority of the world’s accessible trona reserves are located in the Green River Basin. According to historical production statistics, approximately one-quarter of global soda ash is produced by processing trona, with the remainder being produced synthetically through chemical processes. The processing of soda ash from trona is the cheapest manner in which to produce soda ash. The costs associated with procuring the materials needed for synthetic production are greater than the costs associated with mining trona for trona-based production. In addition, trona-based production consumes less energy and produces fewer undesirable by-products than synthetic production.

Our principal executive offices are located at Five Concourse Parkway, Suite 2500, Atlanta, Georgia 30328, and our telephone number is (770) 375-2300. We make available, free of charge on our website at www.ciner.us.com our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, as soon as reasonably practicable after we electronically file such material with, or furnish such material to, the Securities and Exchange Commission, or the SEC. A hard copy of our annual report on Form 10-K may also be requested free of charge by emailing investorrelations@ciner.us.com.

Our website also includes our Code of Conduct, our Corporate Governance Guidelines, our Internal Reporting and Whistleblower Protection Policy, our Insider Trading Policy and the charters of our Audit Committee and Conflicts Committee. The information on our website, or information about us on any other website, is not incorporated by reference into this Report. The SEC maintains an internet site at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

Our Competitive Strengths

We believe that the following competitive strengths enable us and will continue to allow us to execute our business strategies successfully and to achieve our objective of generating and growing cash available for distribution to our unitholders:

Cost Advantages of Producing Soda Ash from Trona. We believe that as a producer of soda ash from trona, we have a significant competitive advantage compared to synthetic producers of soda ash. The manufacturing and processing costs for producing soda ash from trona are lower than other manufacturing techniques partly because the costs associated with procuring the materials needed for synthetic production are greater than the costs associated with mining trona for trona-based production. In addition, we believe trona-based production consumes less energy and produces fewer undesirable by-products than synthetic production. Stronger economic conditions globally in 2017 have led to an increase in commodity prices in general. This trend has also led to an increase in the input costs of manufacturing synthetic soda ash last year. Also, our inland freight costs have been rising since 2014, likely at a faster pace than what has been experienced by our competitors in other regions of the world. In spite of this and based on our estimates and industry sources, we believe the average cost of production per short ton of soda ash (before freight and logistics costs) from trona is approximately 40% to 50% the cost per short ton of soda ash from synthetic production. In addition, synthetic producers of soda ash incur additional costs associated with storing or disposing of, or attempting to resell, the by-products the synthetic

5

processes produce. Even after taking into account the higher freight costs associated with our soda ash exports, we believe we can be cost competitive with synthetic soda ash operations in most parts of the world, which are typically located closer to customers than we are. We believe that our competitive cost structure, including logistics costs, allows us to be competitive in many parts of the world on a landed cost basis.

Synergies created from Ciner Group. Since Ciner Group’s acquisition of our business, Ciner Group is now the largest global producer of natural soda ash derived from trona-based sources, with production assets in both Turkey and the US. Ciner Group has long-standing relationships with many global customers that we believe will improve our positioning with key customer accounts in North America and Europe. Ciner Group also owns and operates port facilities in Turkey, and recently one of its other North American subsidiaries entered into an agreement to exclusively import soda ash into a port on the east coast of the US. Ciner Corp, which is the exclusive sales agent for the Partnership, will serve as the exclusive marketer of that material. We believe by having access to that material, Ciner will be able to offer its customers an improved level of service, greater certainty of supply and over time lower our overall cost to serve. In addition, we believe there are opportunities to leverage technologies across the group to enhance our relative competitive cost position.

Substantial Reserve Life from Significant Reserves. As of December 31, 2017, Hollberg Professional Group (“HPG”), an independent mining and geological consulting firm, estimated we had proven and probable reserves of approximately 240.1 million short tons of trona, which is equivalent to 131.2 million short tons of soda ash. Based on our current mining rate of 4.0 million short tons of trona per year, we have enough proven and probable trona reserves to continue mining trona using current methods for approximately 60 years. Please see Item 1, Business, “Trona Reserves” for more information.

Certain Operational Advantages Compared to Other U.S. Trona-Based Producers. We believe we have certain operational advantages over other soda ash producers in the Green River Basin due to the operational characteristics of our facilities as described below. These advantages are manifested in our high productivity and efficiency rates.

• | Location of our mining beds and high purity trona. Our mining beds are located 800 to 1100 feet below the surface, which is significantly closer to the surface than the mining beds of other operators in the Green River Basin. The relatively shallow depth of our beds compared to other Green River Basin trona mines contributes to favorable ground conditions and improved mining efficiency. We have a competitive advantage because we can mine and roof bolt continuously while mining. In addition, the trona in our mining beds has a higher concentration of soda ash as compared to the trona mined at other locations in the Green River Basin, which is typically imbedded or mixed with greater amounts of halite and other impurities. Our trona ore is generally composed of approximately 85% to 89% pure trona. |

• | Advantageous facility layout. Our surface site includes a high capacity network of ponds that we use to recapture soda ash lost in processing trona through a process we introduced in 2009 called deca rehydration (“DECA”). Primarily as a result of this process, we have been able to reduce our ore to ash ratio by 5.7% over the past five years. While other producers in the Green River Basin also utilize deca rehydration, our pond complex enables us to spread deca-saturated water over a large surface area, which facilitates evaporation and access to the resulting deca. Additionally, we can transfer water from one pond to another, a process we call “de-watering,” leaving the first pond dry. De-watering enables us to use front loaders and other hauling equipment to move dry deca from that “de-watered” pond to our processing facility. Other producers in the area instead need to utilize costly dredging techniques to extract deca from their ponds, and the recovered deca is wet, and therefore requires more energy to process than dry deca. Introducing dry deca into our process has also reduced our energy consumption per short ton of soda ash produced. Please read “Risk Factors-Risks Inherent in Our Business and Industry-Mining development, exploration and processing operations pose numerous hazards and uncertainties that may negatively affect our business” for more information about this process. |

Partly due to these operational advantages over other domestic producers, we believe we have the most efficient soda ash production facility in the Green River Basin both in terms of short tons of soda ash produced per employee and in energy consumed per short ton of soda ash produced. In 2017, we used approximately 3.7 MMBtus of energy per short ton of soda ash processed, as compared to an average of 5.5 MMBtus of energy for the other three operators in the Green River Basin according to the Wyoming Department of Environmental Quality and our internal estimates. For the year ended December 31, 2017, we produced approximately 5,603 short tons of soda ash per employee. Based on historical production statistics we believe this production metric exceeds that of the other three operators in the Green River Basin.

Safety Is a Value and the Most Important Part Of Our Business. At Ciner we pride ourselves on our safety record, and we are continually one of the leaders in the U.S. Mining Industry in relation to low incident rates and workplace injuries. We maintain a rigorous safety program, which includes training programs, site audit programs and hazard identification programs. Ciner Corp and its affiliates, our employees and all contractors who operate our assets or work at our facility are involved in our safety programs. As a direct result of our commitment to safety we have achieved many recognitions such as the Sentinels of Safety by the National Mining Association, The Industrial Minerals Association-North America Safety Achievement Award (Large Category) three times, Safe Sam Award by the Wyoming Mining Association, and the Wyoming State Mine Inspector’s Large Mine award multiple times. In October 2016, we achieved 2,000,000 man hours without a lost time injury. During the year ended December 31, 2017, our facility had two lost work day injuries and five recordable injuries as reported by MSHA. We also boast and support some of the nation’s best

6

rescue teams. Our mine rescue team has been National Mine Rescue Champions seven times, and our surface rescue team has won multiple competitions, including an international mine rescue competition, and has been an International Champion as well.

Stable Customer Relationships. We have an extensive base of more than 70 domestic customers in industries such as flat glass, container glass, detergents, chemicals, paper and other consumer and industrial products. We have long-term relationships with many of our customers due to our competitive pricing, reliable shipping and high quality soda ash. For the year ended December 31, 2017, the majority of our domestic net sales were made to customers with whom we have done business for over ten years. We believe that these relationships lead to stable cash flows. We have a strong, long-standing relationship with our primary export customer, ANSAC. ANSAC is a cooperative that serves as the primary international distribution channel for us and two other U.S. manufacturers of trona-based soda ash. ANSAC is one of the largest purchasers and exporters of soda ash in the world and, as a result, is able to leverage its economies of scale in the markets it serves. We believe that our customer relationships lead to more stable cash flows and allow us to plan production activity more accurately.

Experienced Management and Workforce. Our facility has been in continuous operation for over 50 years. We are able to build on the collective knowledge gained from our experience during this period to continually improve our operations and introduce innovative processes. In addition, many members of Ciner Wyoming’s senior management team have more than 20 years of relevant industry experience. Our executives lead a highly productive workforce with an average tenure of approximately 14.9 years. We believe our institutional knowledge, coupled with the relative seniority of our workforce, engenders a strong sense of teamwork and collegiality, which has led to one of the safest and most efficient operations in the industry today.

Our Business Strategies

Our primary business objective is to generate stable cash flows, allowing us to make quarterly cash distributions to our common unitholders and, over time, to increase those quarterly cash distributions. To achieve our objective, we intend to execute the following key business strategies:

Capitalize on the Growing Demand for Soda Ash. Since 2013, we have invested just over $66.0 million for de-bottlenecking projects that have improved our production capacity by 249,000 tons per year. We intend to continue these efforts over the next several years by investing approximately $15.0 million to $20.0 million annually to grow our capacity up to 3,000,000 tons, which would be roughly an additional 330,000 tons over current production. We believe that as one of the leading low-cost producers of trona-based soda ash, we are well-positioned to capitalize on the worldwide growth of soda ash. While consumption of soda ash within the United States is expected to remain relatively stable in the near future, overall worldwide demand for soda ash, based on third-party historical production statistics, is projected to grow from an estimated 57.1 million metric tons (equivalent to approximately 62.9 million short tons) in 2017 to almost 63.1 million metric tons (equivalent to approximately 69.5 million short tons) in 2022, which represents a compounded annual growth rate of 2.5%. Through ANSAC and our own exports, as well as our long-standing relationship with domestic customers, we believe that as global demand increases, we will be well positioned to maintain our market share in the principal markets in which we operate.

Continuous Improvement Initiatives to Lower Our Operating Expenses and Increase Utilization. We are working to build a culture of continuous improvement. We implemented initiatives in 2017 to improve the consistency of our ore flow to the surface for processing into soda ash and revamped our preventive maintenance practices. Both of these should lead to lowering our overall cost to produce and increase the consistency and overall output of our production. We plan to continue more initiatives in 2018 with a focus on lowering our overall cost of production.

Leverage Our Sponsor’s Capability to Build a Global Soda Ash Brand. When combining Ciner Wyoming’s production in Wyoming with Ciner Group’s two producing locations in Turkey, the Ciner Group globally produces more than 6.5 million tons, making it the world’s largest producer of low cost natural soda ash. Our sponsor’s platform includes unique low cost technology, logistics assets including ports and bulk ships, and world class cost competitive production assets geographically located to serve most key markets around the world. Starting in 2018, our sponsor has entered into an agreement for a new port on the eastern seaboard of the US to import soda ash for supply to select customers on the east coast. Ciner Corp, which is the sales agent for the Partnership, will serve as the exclusive marketing agent for that material and will have inventory to ship from not only Wyoming, but also this new port on the east coast that will ultimately improve security of supply to our customers in the region. We believe this will help Ciner Corp offer a unique value proposition to our customers and ultimately improve the cash flow and profitability of our domestic business.

Maintain Financial Flexibility. We intend to pursue a disciplined financial policy and seek to maintain a conservative capital structure that we believe will provide enhanced stability to our existing cash flows and allow us to consider attractive growth projects and strategic acquisitions in all market environments. See Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources - Debt” for additional information.

Expand Operations Strategically. In addition to capacity expansions and process improvements at our current facility, we plan to grow our business through various methods as they become available to us. This would include acquisitions of other businesses

7

that are involved in mining and processing minerals, such as soda ash, or logistics assets that could improve our efficiencies and grow our cash flows.

We can provide no assurance that we will be able to utilize our strengths described above. For further discussion of the risks that we face, see Item 1A, “Risk Factors.”

Our Organizational Structure

The following chart depicts our ownership structure as of March 2, 2018 and approximate ownership percentages:

On February 22, 2018, Akkan transferred its direct 100% ownership in Ciner Enterprises to KEW Soda, a U.K. company, which transferred such ownership to WE Soda, a U.K. company. WE Soda is 100% owned by KEW Soda, and KEW Soda is wholly owned by Akkan. This reorganization is a part of Ciner Group’s strategy to combine the global soda ash business under a common structure in the U.K.

Our Operations

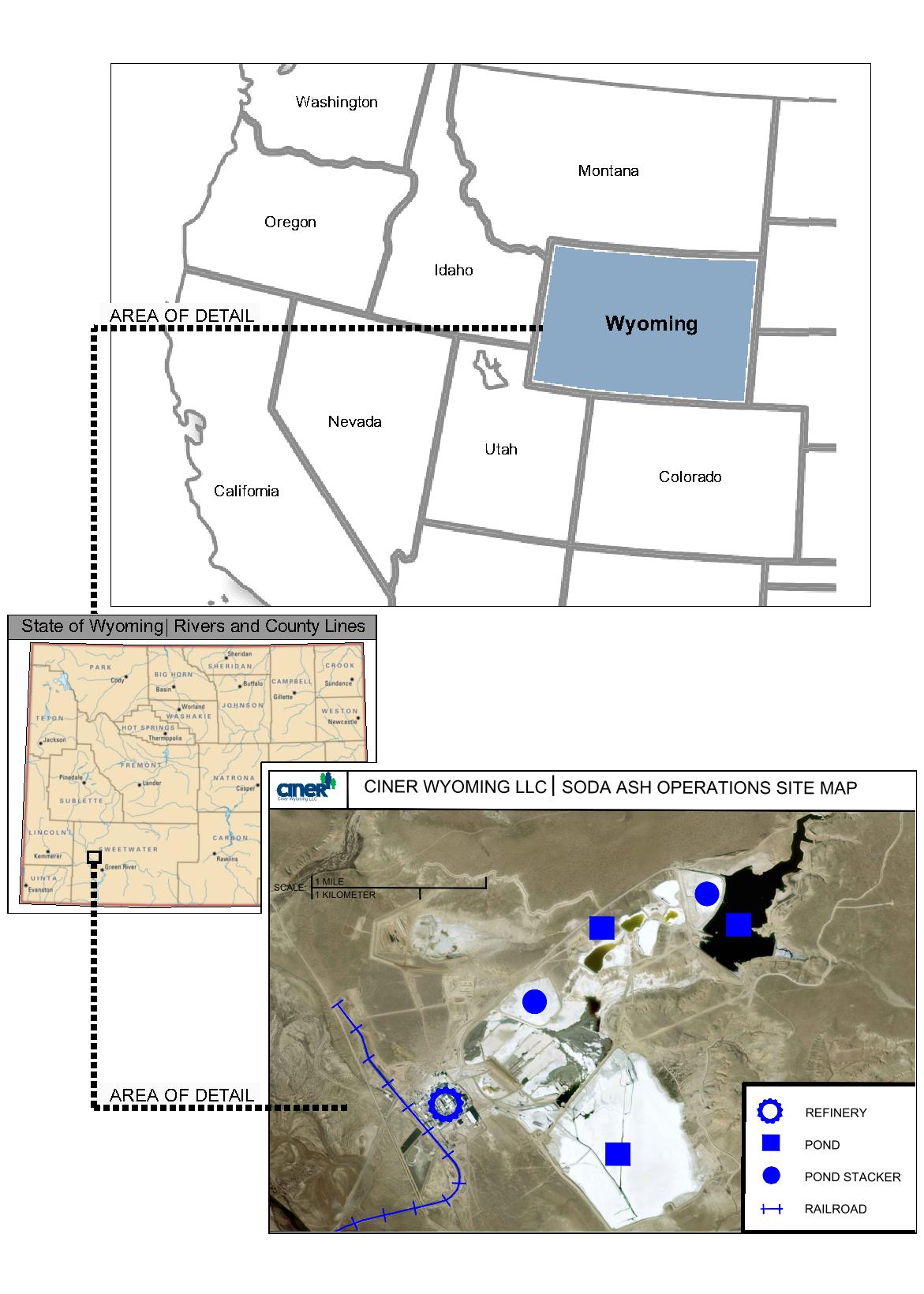

Our Green River Basin surface operations are situated on approximately 880 acres in Wyoming, and our mining operations consist of approximately 23,500 acres of leased and licensed subsurface mining area. Our facility is accessible by both road and rail. We use seven large continuous mining machines and fourteen underground shuttle cars in our mining operations. Our processing assets consist of material sizing units, conveyors, calciners, dissolver circuits, thickener tanks, drum filters, evaporators and rotary dryers.

8

The following map provides an aerial overview of our surface operations:

9

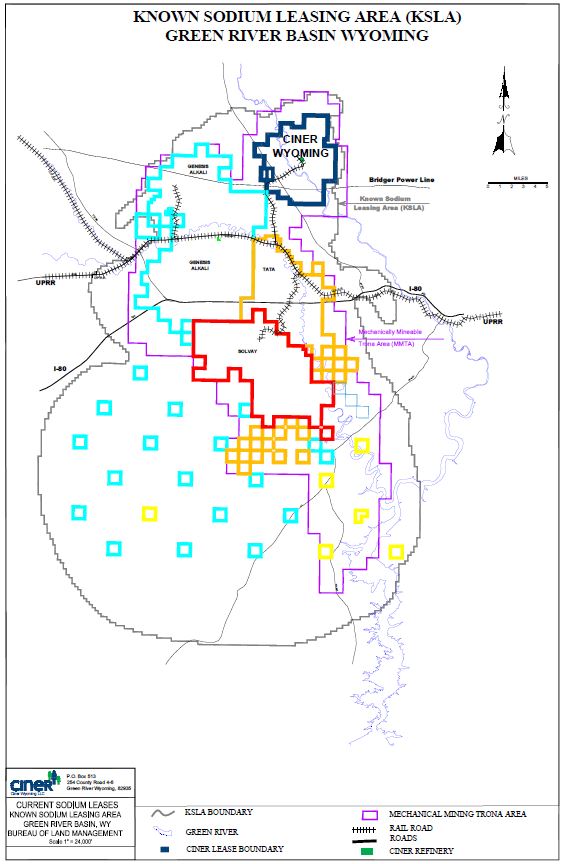

The following map shows the known sodium leasing area within the Green River Basin, including the boundaries of our leased and licensed subsurface mining area:

The Green River Basin geological formation holds the largest, and one of the highest purity, known deposits of trona ore in the world. Our reserves contain trona deposits having a purity between 85% to 89% by weight, which means that insoluble impurities and water make up approximately 11% to 15% of our trona.

10

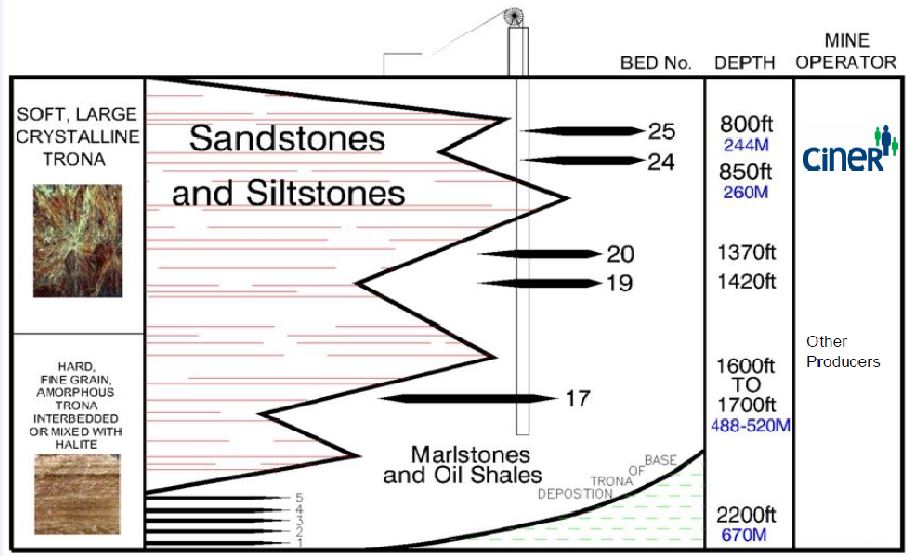

Our mining leases and license are located in two mining beds, designated by the U.S. Geological Survey as beds 24 and 25, at depths of 800 to 1100 feet, respectively, below the surface. Mining these beds affords us several competitive advantages. First, the depth of our beds is shallower than other actively mined beds in the Green River Basin, which allows us to use a continuous mining technique to mine trona and roof bolt the ceiling simultaneously. In addition, mining two beds that are on top of one another allows for production efficiencies because we are able to use a single hoisting shaft to service both beds.

The following graphic shows a cross-section of the strategic areas of the Green River Basin where we mine trona:

Source: Management.

We remove insoluble materials and other impurities by thickening and filtering the liquor. We then add activated carbon to our filters to remove organic impurities, which can cause color contamination in the final product. The resulting clear liquid is then crystallized in evaporators, producing sodium carbonate monohydrate. The crystals are then drawn off and passed through a centrifuge to remove excess water. We then dry the resulting material in a product dryer to form anhydrous sodium carbonate, or soda ash. The resulting processed soda ash is then stored in on-site storage silos to await shipment by bulk rail or truck to distributors and end customers. Our storage silos can hold up to 65,000 short tons of processed soda ash at any given time. Our facility is in good working condition and has been in service for over 50 years.

Deca Rehydration. The evaporation stage of our trona ore processing produces a precipitate and natural by-product called deca. “Deca”, short for sodium carbonate decahydrate, is one part soda ash and ten parts water. Solar evaporation causes deca to crystallize and precipitate to the bottom of the four main surface ponds at our Green River Basin facility. In 2009 we implemented a process called deca rehydration, which enables us to recover soda ash from the deca-rich purged liquor as a by-product of our refining process. We capture the soda ash contained in deca by allowing the deca crystals to evaporate in the sun and separating the dehydrated crystals from the soda ash. We then blend the separated deca crystals with partially processed trona ore at the dissolving stage of our production process described above. This process enables us to reduce our waste storage needs and convert what is typically a waste product into a usable raw material. Primarily as a result of this process, we have been able to reduce our ore to ash ratio by 5.7% over the past five years. Please read “Risk Factors-Risks Inherent in Our Business and Industry-Mining development, exploration and processing operations pose numerous hazards and uncertainties that may negatively affect our business” for more information about this process.

Energy Consumption. We believe we have one of the most efficient mining and soda ash production surface operations in the world. In 2017, we used approximately 3.7 MMBtus of energy in the form of electricity and natural gas to produce each short ton of soda ash. In addition, we believe this to be the lowest energy consumption of any soda ash producer in North America. We and other producers of soda ash in the Green River Basin benefit from relatively low cost and stable supplies of coal and natural gas in Wyoming, which further enhances our competitive cost advantage over other regions of the world. To reduce the impact of the

11

volatility in natural gas prices, we hedge a portion of our natural gas consumption requirements, which enables us to set the price for a portion of our forecasted natural gas purchases.

Shipping and Logistics. All of our soda ash is shipped by rail or truck from our Green River Basin operations. For the year ended December 31, 2017, we shipped approximately 95.6% of our soda ash to our customers initially via a single rail line owned and controlled by Union Pacific Railroad Company (“Union Pacific”), and our plant receives rail service exclusively from Union Pacific. Our agreement with Union Pacific expires on December 31, 2018 and there can be no assurance that it will be renewed on terms favorable to us or at all. The rail freight rate we are charged under our agreement increases annually based on a published index tied to certain rail industry metrics. If we do not ship a significant portion of our soda ash production on the Union Pacific rail line during a twelve-month period, we must pay Union Pacific a shortfall payment under the terms of our transportation agreement. For the year ended December 31, 2017 and 2016, we assisted the majority of our domestic customers in arranging their freight services. During 2017 and 2016, we had no shortfall payments and do not expect such payments in the future. We lease a fleet of more than 2,000 hopper cars that serve as dedicated modes of shipment to our domestic customers. For export, we ship our soda ash on unit trains consisting of more than 100 cars to two primary ports: Port Arthur, Texas and Portland, Oregon. From these ports, our soda ash is loaded onto ships for delivery to ports all over the world. ANSAC provides logistics and support services for all of our export sales. For domestic sales, Ciner Corp provides similar services.

Customers

Our largest customer is ANSAC, which buys soda ash from us (through our sales agent) and other of its member companies for export to its customers. For the year ended December 31, 2017, ANSAC and CIDT accounted for approximately 44.7% and 16.5% of our net sales, respectively. No other individual customer accounted for more than 10% of our net sales. ANSAC takes soda ash orders directly from its overseas customers and then purchases soda ash for resale from its member companies pro rata based on each member’s allocated volumes. ANSAC is the exclusive distributor for its members to the markets it serves. However, Ciner Corp, on our behalf, negotiates directly with, and we export to, customers in markets not served by ANSAC. In 2017, we had more than 70 domestic customers. During 2017, international sales were made through ANSAC as well as to CIDT, both of which are our export affiliates. We began selling soda ash in late 2016 to CIDT and continued into 2017. These sales were in markets not served by ANSAC. Our current 2018 outlook does not anticipate any further sales to CIDT.

For customers other than ANSAC, our sales agent typically enters into contracts, on our behalf, having terms ranging from one to three years. Under these contracts, our customers generally agree to purchase either minimum estimated volumes of soda ash or a certain percentage of their soda ash requirements. Although we do not have a “take or pay” arrangement with our customers, substantially all of our sales are made pursuant to written agreements and not through spot sales.

Our customers, including end users to whom ANSAC makes sales overseas, consist primarily of:

• | Glass manufacturing companies, which account for 50% or more of the consumption of soda ash around the world; and |

• | Chemical and detergent manufacturing companies. |

For accounts in North America, Ciner Corp, on our behalf, typically enters into sales contracts with our customers having terms of one to three years. Pursuant to these contracts, we supply an estimated annual tonnage of soda ash to a customer at a fixed price for a given calendar year. Generally speaking, we have long-term relationships with the majority of our customers, meaning we have been a supplier to them for more than ten years.

Leases and License

We are party to several mining leases and one license, as noted in the table below, which give us subsurface mining rights. Some of our leases are renewable at our option upon expiration. We pay royalties to the State of Wyoming, the U.S. Bureau of Land Management and Rock Springs Royalty Company (“Rock Springs”), an affiliate of Anadarko Petroleum, which are calculated based upon a percentage of the quantity or gross value of soda ash and related products at a certain stage in the mining process, or a certain sum per each ton of such products. These royalty payments are typically subject to a minimum domestic production volume from our Green River Basin facility, although we are obligated to pay minimum royalties or annual rentals to our lessors and licensor regardless of actual sales.

The royalty rates we pay to our lessors and licensor may change upon our renewal of such leases and license. Under our license with Rock Springs, the applicable royalty rate may vary based on a most favored nation clause in the license. The applicable royalty rate in the license may be adjusted if we pay a higher royalty rate to certain other mineral rights owners in Sweetwater County, Wyoming. The extent to which Rock Springs may increase the applicable royalty rate is currently the subject of litigation in Wyoming. Any increase in the royalty rates we are required to pay to our lessors and licensor, or any failure by us to renew any of our leases and license, could have a material adverse impact on our results of operations, financial condition or liquidity, and, therefore, may affect our ability to distribute cash to unitholders. See Item 3, “Legal Proceedings” for more information.

12

The following is a summary of the material terms of our leases and our license as of December 31, 2017:

Name of Lessor or Licensor | Number of Leases or Licenses as of December 31, 2017 | Total Approximate Acreage as of December 31, 2017 | Expiration Date Range | Renewals | Year of Commencement | Royalty Rate | ||||||

License with Rock Springs | 1 | 12,445 acres | N/A | Renewed until 2061 | 1962 | 8% of net sales (1) | ||||||

Leases with the U.S. Government | 4 | 7,934 acres | 2018-2027 | These leases will renew so long as we file an application for renewal with the Department of the Interior, Bureau of Land Management, within 90 days of expiration of the leases(2) | 1961 | 6% of gross output | ||||||

Leases with the State of Wyoming | 5 | 3,079 acres | 2019 | No contractual right to renewal, but leases have been historically renewed for consecutive 10-year periods | 1969 | 6% of gross value | ||||||

(1) | Royalty rate increase from 7% in 2014 to 8% in October 2015 is currently the subject of litigation in Wyoming. See Item 3, “Legal Proceedings,” for additional information. |

(2) | Renewals are typically for ten-year periods. |

The foregoing descriptions of the material terms of our leases and our license do not purport to be complete descriptions of our leases and our license, and are qualified in their entirety by reference to the full text of the leases and license, copies of which have been filed or incorporated by reference as exhibits to this Report. See Part IV, Item 15, “Exhibits and Financial Statement Schedules— Exhibit Index” for more information.

Trona Reserves

As of December 31, 2017, we had estimated proven and probable reserves of approximately 240.1 million short tons, which is equivalent to 131.2 million short tons of soda ash. The estimates of our proven and probable reserves were prepared by HPG for the year ended December 31, 2017. Based on our current mining rate of 4.0 million short tons of trona per year, we have enough proven and probable trona reserves to continue mining trona using current methods for approximately 60 years.

HPG calculated a mineral reserve estimate on our trona mineral assets, which are contained in beds 24 and 25 of the Green River Basin, at depths of 800 and 1100 feet below the surface, respectively. HPG estimates are based on geological data generated from historical exploration drill holes, borings within the mine space, and mine observations and measurements, including core samples. In addition, HPG reviewed and analyzed our reserve base maps and current mining plans, and developed a life of mine plan with respect to the predicted life of our reserves using a non-subsidence design.

Our trona reserve estimates include reserves that can be economically and legally extracted and processed into soda ash at the time of their determination. Our trona reserves are categorized as “proven (measured) reserves” and “probable (indicated) reserves,” which are defined as follows:

• | Proven (Measured) Reserves—Reserves for which: (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well-established. |

• | Probable (Indicated) Reserves—Reserves for which quantity and grade and/or quality are computed from information similar to that used for proven (measured) reserves, but the sites for inspection, sampling, and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven (measured) reserves, is high enough to assume continuity between points of observation. |

For purposes of categorizing our proven reserves, HPG estimates applied exploration and mine measurements and drill hole data within a one-quarter mile radius, and required at least 8-feet of trona thickness and a trona ore grade of at least 85% (with 15% of clays, shales and other impurities). For purposes of categorizing our probable reserves, HPG estimates applied exploration and mine measurements and drill hole data within a three-quarter mile radius, and required at least 8-feet of trona thickness and a trona ore grade of at least 85% (with 15% of clays, shales and other impurities). To assess the economic viability of our reserves, HPG reviewed our cost of products sold and average sales price of soda ash for the three years ended December 31, 2017.

13

In determining whether our reserves meet these proven and probable standards, HPG applied certain assumptions regarding the remaining life of our reserves, including, among other things, that:

• | our cost of products sold per short ton will remain consistent with our cost of products sold for the three years ended December 31, 2017, which was approximately $79 per short ton of soda ash; |

• | the weighted average net sales per short ton will remain consistent with our weighted average net sales price per short ton for three years ended December 31, 2017, which was approximately $180 per short ton of soda ash; |

• | we will achieve an annual mining rate of approximately 4.0 million short tons of trona; |

• | we will process soda ash with a 90% recovery rate without accounting for our deca rehydration process; |

• | the ore to ash ratio for the stated trona reserves is 1.835:1.0 (short tons of trona run-of-mine to short tons of soda ash, excluding our deca rehydration recovery process); |

• | our run-of-mine ore estimate contains dilution from the mining process; |

• | we will, in approximately 20-30 years, make necessary equipment modifications to operate at a seam height of 7-feet, although our current mining limit is 9.5 to 10 feet; |

• | we will, within the next one to six years, conduct “two-seam mining,” which means to perform continuous mining simultaneously on beds 24 and 25 in close proximity; |

• | our mining costs will remain consistent with 2017 levels until we begin two-seam mining at which time our mining costs may increase as much as 50% for those short tons that are mined using that method; |

• | our processing costs will remain consistent with 2017 levels; |

• | we will continue to conduct only conventional mining using the room and pillar method and a non-subsidence mine design; |

• | we have and will continue to have valid leases and license in place with respect to the reserves, and that these leases and license can be renewed for the life of the mine based on our extensive history of renewing leases and license; |

• | we have and will continue to have the necessary permits to conduct mining operations with respect to the reserves; and |

• | we will maintain the necessary tailings storage capacity to maintain tailings disposal between the mine and surface placement for the life-of-mine. |

Our reserves are subject to leases with the State of Wyoming and the U.S. Bureau of Land Management and a license with Rock Springs. See “Leases and License” above for a summary of these leases and our license, including expiration date ranges.

The following table presents our estimated proven and probable trona reserves at December 31, 2017:

Right of Access and Extraction | Proven Trona Reserves | Average Run-of-Mine Grade of Proven Trona Reserves (% Trona)(1) | Probable Trona Reserves | Average Run-of-Mine Grade of Probable Trona Reserves (% Trona)(1) | Total Proven and Probable Trona Reserves(2) | Soda Ash Produced from Total Proven and Probable Trona Reserves(3) | |||||||||||

(In millions of short tons except percentages)(4) | |||||||||||||||||

License with Rock Springs | 59.4 | 88.8 | % | 57.7 | 89.0 | % | 117.1 | 63.9 | |||||||||

Leases with the U.S. Government | 50.1 | 89.0 | % | 47.9 | 88.7 | % | 98.0 | 53.5 | |||||||||

Leases with the State of Wyoming | 6.9 | 89.4 | % | 18.1 | 88.7 | % | 25.0 | 13.7 | |||||||||

Total(5) | 116.4 | 88.9 | % | 123.7 | 88.9 | % | 240.1 | 131.1 | |||||||||

(1) | For purposes of these estimates, the minimum grade for reported tonnage is 85%. |

(2) | The average run-of-mine trona grade, or the percentage of the raw trona mined that comprises soda ash, of our proven and probable trona reserves is approximately 88.9%. These estimates assume out-of-seam dilution of 4 inches. The price used to estimate our proven and probable trona reserves was our historical average CIF (carriage, insurance and freight) sales price for the three years ended December 31, 2017, which was approximately $180 per short ton of soda ash. |

(3) | Soda ash conversion assumes a 90% recovery rate, resulting in an ore to ash ratio of 1.835:1.0. |

14

(4) | The sums of some of the rows and columns may not foot due to rounding. |

(5) | Except percentages, which are averages. |

Our reserve estimates will change from time to time as a result of mining activities, analysis of new engineering and geologic data, modification of mining plans or mining methods and other factors. For addition information, see Item 1A, Risk Factors, “Risks Inherent in Our Business and Industry” for more information regarding risks surrounding our reserves.

Competition

Soda ash is a commodity natural resource traded globally with numerous producers and consumers worldwide. We compete with both North American and international soda ash producers, including Ciner Group’s Turkish operations. There are two ways to consider how we compete: (1) versus our fellow North American competitors; and (2) versus our worldwide competitors. Against our principal North American competitors, which include subsidiaries of Genesis, Solvay and Tata in the Green River Basin and Searles Valley Minerals in California, we believe we have a number of competitive advantages, including operational advantages that improve our relative cost position, life of our mineral reserves, our strong safety record, customer relationships and an experienced management team and workforce. Against our principal worldwide competitors, Solvay, Tata and various Chinese producers, virtually all of their production is manufactured from synthetic processes and we believe, as a producer of soda ash from trona, we have competitive advantages, even after considering the fact that we generally have higher logistics costs to move the soda ash from Wyoming to regions around the world. The costs associated with procuring the materials needed for synthetic production are greater than the costs associated with mining trona. In addition, we believe trona-based production consumes less energy and produces fewer undesirable by-products than synthetic production. See “Our Competitive Strengths” above for additional information.

Insurance

Because all of our operations are conducted at a single facility, an event such as an explosion, fire, equipment malfunction or severe weather conditions could significantly disrupt our trona mining or soda ash production operations and our ability to supply soda ash to our customers. These hazards can also cause personal injury and loss of life, pollution or environmental damage and suspension of our surface and subsurface operations. To mitigate this risk, Ciner Enterprises or its affiliates maintains, on our behalf, property, casualty and business interruption insurance in amounts and with coverage and deductibles that we believe are adequate for our current operations. We continually evaluate our policy limits and deductibles as they relate to the overall cost and scope of our insurance coverage to account for changes or growth in our business.

Environmental Matters

Our mining and processing operations, which have been conducted at our Green River Basin facility for many years, are subject to strict regulation by federal, state and local authorities with respect to protection of the environment. We have a rigorous compliance program to ensure that our facilities comply with environmental laws and regulations. However, we are involved from time to time in administrative and judicial proceedings and inquiries relating to environmental matters. Modifications or changes in enforcement of existing laws and regulations or the adoption of new laws and regulations in the future, particularly with respect to environmental or climate change, or changes in the operation of our business or the discovery of additional or unknown environmental contamination, could require expenditures which might be material to our results of operations or financial conditions.

We summarize below certain environmental laws applicable to us that regulate discharges of substances into the air and water, the management and disposal of hazardous substances and wastes, the clean-up of contaminated sites, the protection of groundwater quality and availability, plant and wildlife protection, and climate change. Our failure to comply with any of the below laws may result in the assessment of administrative, civil and criminal penalties, the imposition of clean-up and site restoration costs and liens, the issuance of injunctions to limit or cease operations, the suspension or revocation of permits and other enforcement measures that could have the effect of limiting production from our operations.

Clean Air Act

The federal Clean Air Act and comparable state laws restrict the emission of air pollutants from many sources. Under the Clean Air Act, our facility has been issued a Title V operating permit, which regulates emissions to air from our operations. In particular, our operations are subject to technology-based standards pursuant to the Clean Air Act’s New Source Performance Standards for Nonmetallic Mineral Processing Plants, which limit particulate matter emissions. Under associated clean air act regulations this operation is also subject to Best Available Control Technology (BACT) requirements. In addition, our boilers are subject to technology-based standards pursuant to the Clean Air Act’s National Emission Standards for Hazardous Air Pollutants for Major Source: Industrial, Commercial and Institutional Boilers and Process Heaters, which were published in final form in January 2013. These laws and regulations may require us to obtain pre-approval for the construction or modification of certain projects or facilities expected to produce or significantly increase air emissions, obtain and strictly comply with stringent air permit requirements or utilize specific equipment or technologies to control emissions of certain pollutants.

15

Clean Water Act

The Federal Water Pollution Control Act, which we refer to as the Clean Water Act, and comparable state laws impose restrictions and controls regarding the discharge of pollutants into regulated waters. The discharge of pollutants into regulated waters is prohibited, except in accordance with the terms of a permit issued by the federal EPA or the state. We do not discharge any wastewater from our operations into the Green River, the nearest river system to our Green River Basin facility. However, the discharge of storm water runoff from our facility is governed by a general permit issued by the Wyoming Department of Environmental Quality. In particular, the general permit requires our compliance with a Storm Water Pollution Prevention Plan. We periodically monitor groundwater wells at our processing facility, most of which are proximate to our surface pond complex, for salinity, conductivity and other parameters pursuant to permits issued by the Wyoming Department of Environmental Quality. Permitted interceptor trenches are used to collect saline groundwater to prevent discharge and impact to the Green River.

Resource Conservation and Recovery Act

The federal Resource Conservation and Recovery Act, or RCRA, and analogous state laws, impose requirements for the careful generation, handling, storage, treatment and disposal of nonhazardous and hazardous solid wastes. Based on the amount of hazardous waste our operations generate (less than 100 kilograms per month), we have been classified under RCRA as a conditionally exempt small quantity generator.

Comprehensive Environmental Response, Compensation, and Liability Act

The federal Comprehensive Environmental Response, Compensation, and Liability Act, or CERCLA (otherwise known as “Superfund”), and comparable state laws impose liability in connection with the release of hazardous substances into the environment. CERCLA imposes liability, without regard to fault or the legality of the original conduct, on certain classes of persons that are considered to have contributed to the release of a hazardous substance into the environment. These persons include the current and past owner or operator of the disposal site or the site where the release occurred and those who disposed or arranged for the disposal of the hazardous substances at the site where the release occurred. Under CERCLA, such persons may be subject to joint and several liability for the costs of cleaning up the hazardous substances that have been released into the environment and for damages to natural resources. Wyoming’s Environmental Quality Act also creates the potential for liability in connection with the release of hazardous substances into the environment, and has been construed to impose liability without regard to fault. We have not received notice that we are a potentially responsible party at any Superfund site.

Climate Change Legislation and Regulations

In response to findings that emissions of carbon dioxide, methane and other greenhouse gases, or GHGs, present an endangerment to public health and the environment, the EPA has adopted rules requiring the monitoring and annual reporting of GHG emissions from specified sources, including soda ash processors like us. We are monitoring and reporting GHG emissions from our operations, and we believe we are in substantial compliance with the rules. In the past, the U.S. Congress has considered, but not enacted, legislation that would impose requirements to reduce emissions of GHGs. The State of California has enacted regulations establishing a so-called GHG “cap-and-trade” system designed to reduce GHG emissions. Our operations are not currently subject to any federal or state requirement to reduce GHG emissions. Although it is not possible at this time to predict how legislation or new regulations that may be adopted to address GHG emissions would impact our business, any such future laws and regulations limiting, or otherwise imposing a tax or financial penalty for, emissions of GHGs from our equipment and operations might be material to our results of operations or financial conditions.

Wyoming Department of Environmental Quality—Land Quality Division

Our operations are subject to oversight by the Land Quality Division of the Wyoming Department of Environmental Quality. In particular, our principal mine permit issued by the Land Quality Division requires us to “self-bond” for the estimated future cost to reclaim the area of our processing facility, surface pond complex and on-site sanitary landfill. As of December 31, 2017, the amount of the self-bond was $32.9 million. The amount of the bond is subject to change based upon periodic re-evaluation by the Land Quality Division. Also, our ability to self-bond may be impacted by future legislation. Please see Item IA, “Risk Factors--Risks Inherent in Our Business and Industry--Our inability to acquire, maintain or renew financial assurances related to the reclamation and restoration of mining property could have a material adverse effect on our business, financial condition and results of operations.” for more information.

Mining and Workplace Safety

The U.S. Mine Safety and Health Administration, or MSHA, is the primary regulatory organization governing safety matters associated with trona ore mining. Accordingly, MSHA regulates underground mines and the industrial mineral processing facilities associated with trona ore mines. MSHA administers the provisions of the Federal Mine Safety and Health Act of 1977 and enforces compliance with that statute’s mandatory safety and health standards. As part of MSHA’s oversight, representatives perform at least four unannounced inspections annually for our entire facility. In 2016, we had two citations issued by MSHA that resulted in a

16

shutdown of a portion of our operations and loss of production; however, these citations have since been vacated and no assessment was levied.

We also are subject to the requirements of the U.S. Occupational Safety and Health Act, or OSHA, and comparable state statutes that regulate the protection of the health and safety of workers. In addition, the OSHA Hazard Communication Standard requires that information be maintained about hazardous materials used or produced in operations and that this information be provided to employees, state and local government authorities and the public.

Our Green River Basin facility maintains a rigorous safety program. Ciner Corp and its affiliates’ employees and contractors who operate our assets are required to complete 40 hours of initial training, as well as eight-hour annual refresher sessions. These training programs cover all of the potential site-specific hazards present at the facility. As a direct result of our commitment to safety, the Green River Basin facility has had an exceptional safety record in recent years. During the year ended December 31, 2017, our facility had two lost work-day injuries and five recordable injuries as reported by MSHA. Over the five years ended December 31, 2017, the Green River Basin facility averaged 1.6 lost work day injuries per year and averaged 5.4 recordable injuries per year as reported by MSHA, which we believe to be better than the industry average.

Employees/Labor Relations

The personnel who operate our assets are employees of Ciner Corp and its affiliates. Under the joint venture agreement governing Ciner Wyoming, Ciner Wyoming reimburses us for employees who operate our assets and for support provided to Ciner Wyoming. As of December 31, 2017, Ciner Corp and its affiliates had approximately 476 full-time employees, of which 426 are employees that operate the mine at our facility in the Green River Basin. None of these employees was covered by a collective bargaining agreement as of December 31, 2017, and we did not experience any labor strikes or other significant labor problems during 2017.

In addition, under the Services Agreement, dated October 25, 2015, among the Partnership or General Partner and Ciner Corp (the “Service Agreement”), Ciner Corp has agreed to provide the Partnership with certain corporate, selling, marketing, and general and administrative services, in return for which the Partnership has agreed to pay Ciner Corp an annual management fee and reimburse Ciner Corp for certain third-party costs incurred in connection with providing such services.

Emerging Growth Company Status

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act, or the JOBS Act. For as long as we are an emerging growth company, unlike other public companies, we will not be required to:

• | provide an auditor’s attestation report on management’s assessment of the effectiveness of our system of internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002; |

• | present more than two years of audited financial statements, selected financial data and related Management’s Discussion and Analysis of Financial Condition and Results of Operations in this Report; |

• | comply with certain new requirements adopted by the Public Company Accounting Oversight Board, or the PCAOB; |

• | comply with certain new audit rules adopted by the PCAOB after April 5, 2012, unless the SEC determines otherwise; |

• | provide disclosures regarding executive compensation required of larger public companies; or |

• | obtain unitholder approval of any golden parachute payments not previously approved. |

We will cease to be an emerging growth company when any of the following conditions apply:

• | we have $1.07 billion or more in annual revenues; |

• | at least $700 million in market value of our common units are held by non-affiliates; |

• | we issue more than $1.0 billion of non-convertible debt over a three-year period; or |

• | the last day of the fiscal year following the fifth anniversary of our initial public offering has passed. |

In addition, an emerging growth company can delay its adoption of certain accounting standards until those standards would otherwise apply to private companies. However, we have made the irrevocable election to “opt out” of such extended transition period, and as a result, we will comply with any new or revised accounting standards on the relevant dates on which non-emerging growth companies must adopt such standards. December 31, 2018 will be the latest date that we will be an emerging growth company.

Glossary of Industry Terms

Industry terms are defined in the Glossary of Industry Terms, included at the end of this Report.

17

ITEM 1A. Risk Factors

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. You should carefully consider the following risk factors together with all of the other information included in this Report in evaluating an investment in our common units.

If any of the following risks were to occur, our business, financial condition, results of operations and our ability to distribute cash could be materially adversely affected. In that case, we might not be able to make distributions on our common units, the trading price of our common units could decline, and you could lose all or part of your investment.

Risks Inherent in Our Business and Industry

We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses, including cost reimbursements to our general partner and its affiliates, to enable us to pay any quarterly distribution on our units.

We may not have sufficient available cash each quarter to pay the quarterly distribution at the current distribution level of $0.5670 per unit, or $2.268 per unit on an annualized basis, at the minimum quarterly distribution level, or at all. In order to pay the quarterly distribution at the current distribution level, we will require available cash of approximately $11.4 million per quarter, or $45.6 million per year, based on the number of common and general partner units currently outstanding.

The amount of cash we can distribute on our units principally depends upon the amount of cash we generate from our operations, which will fluctuate from quarter to quarter based on several factors, some of which are beyond our control, including, among other things:

•the market prices for soda ash in the markets in which we sell;

•the volume of natural and synthetic soda ash produced worldwide;

• | domestic and international demand for soda ash in the flat glass, container glass, detergent, chemical and paper industries in which our customers operate or serve; |

•the freight costs we pay to transport our soda ash to customers or various delivery points;

•the cost of electricity and natural gas used to power our operations;

• | the amount of royalty payments we are required to pay to our lessors and licensor and the duration of our leases and license; |

• | political disruptions in the international markets we or our customers serve, including any changes in trade barriers; |

•our relationships with our customers and our or our sales agent’s ability to renew contracts;

•the creditworthiness of our customers;

• | regulatory action affecting the supply of, or demand for, soda ash, our ability to mine trona ore, our transportation logistics, our operating costs or our operating flexibility; |

•new or modified statutes, regulations, governmental policies and taxes or their interpretations; and

•prevailing U.S. and international economic conditions and foreign exchange rates.

In addition, the actual amount of cash we will have available for distribution will depend on other factors, some of which are beyond our control, including, among other things:

•the level and timing of capital expenditures we make;

• | the level of our operating, maintenance and general and administrative expenses, including reimbursements to our general partner for services provided to us; |

•the cost of acquisitions, if any;

•our debt service requirements and other liabilities;

•fluctuations in our working capital needs;

•our ability to borrow funds and access capital markets;

18

• | restrictions on distributions contained in debt agreements to which we, Ciner Wyoming or our affiliates are a party; |

•the amount of cash reserves established by our general partner; and

•other business risks affecting our cash levels.

Soda ash prices have been and in the future may be volatile, and lower soda ash prices will negatively affect our financial position and results of operations.

Our only product is soda ash, and the market price of soda ash directly affects the profitability of our operations. If the market price for soda ash declines, our revenue may decrease. Historically, the global market and, to a lesser extent, the domestic market for soda ash have been volatile, and those markets are likely to remain volatile in the future. In the past, we have reduced production to mitigate the impact of low soda ash prices. Volatility in soda ash prices can make it difficult to predict the cash we may have on hand at any given time, and a prolonged period of low soda ash prices may materially and adversely affect our financial position, liquidity (including our borrowing capacity under the Ciner Wyoming Credit Facility), ability to finance planned capital expenditures and results of operations.

Prices for soda ash may fluctuate in response to relatively minor changes in the supply of and demand for soda ash, market uncertainty and other factors beyond our control. These factors include, among other things:

•overall economic conditions;

•additional supply from suppliers selling into markets that we serve;

•the level of customer demand, including in the glassmaking industry;

•the level of production and exports of soda ash globally;

•the level of production of materials used to produce soda ash, including trona ore or synthetic materials, globally;

•the cost of energy consumed in the production of soda ash, including the price of natural gas, electricity and coal;

•the impact of non-ANSAC members increasing their capacity and exports;

•domestic and foreign governmental relations, regulations and taxes; and

•political conditions or hostilities and unrest in regions where we export soda ash.

A substantial portion of our costs are attributable to transportation and freight costs. Increases in freight costs could increase our costs significantly and adversely affect our results of operations.

Most soda ash is sold inclusive of transportation costs, which make up a substantial portion of the total delivered cost to the customer. We transport our soda ash by rail or truck and ocean vessel. As a result, our business and financial results are sensitive to increases in rail freight, trucking and ocean vessel rates. Increases in transportation costs, including increases resulting from emission control requirements, port taxes and fluctuations in the price of fuel, could make soda ash a less competitive product for glass manufacturers when compared to glass substitutes or recycled glass, or could make our soda ash less competitive than soda ash produced by competitors that have other means of transportation or are located closer to their customers. Our rail freight rates may increase year-over-year. Also, we may be unable to pass on our freight and other transportation costs in full because market prices for soda ash are generally determined by supply and demand forces.

A significant portion of our international sales of soda ash are to ANSAC, a U.S. export cooperative, and therefore adverse developments at ANSAC or its customers, or in any of the markets in which we make direct international sales, could adversely affect our ability to compete in certain international markets.

We, along with two other U.S. trona-based soda ash producers, utilize ANSAC as our exclusive export vehicle for sales to customers in all countries excluding Canada, South Africa and members of the European Community and European Free Trade Area, which provides us with the benefits of large purchases of soda ash and significant economies of scale in managing international sales and logistics. Because ANSAC makes sales to its end customers directly and then allocates a portion of such sales to each member, we do not have direct access to ANSAC’s customers and we have no direct control over the credit or other terms ANSAC extends to its customers. As a result, we are indirectly vulnerable to ANSAC’s customer relationships and the credit and other terms ANSAC extends to its customers, and if ANSAC ceased to exist, we would face costs and risks of securing those customers and related logistics arrangements on favorable terms. Any adverse change in ANSAC’s customer relationships could have a direct impact on ANSAC’s ability to make sales and our ability to make sales to ANSAC. In addition, to the extent ANSAC extends credit or other favorable terms to its end customers and those customers subsequently default under sales contracts or otherwise fail to perform, we would have no direct recourse against them.

19

Furthermore, from time to time international competition authorities have conducted inquiries into the potentially anti-competitive nature of ANSAC’s activities. The Secretariat of Economic Law of the Ministry Justice of Brazil has commenced an investigation into ANSAC’s activities in Brazil. Ciner Corp and the two other members of ANSAC have been named in these investigations. An unfavorable outcome in any such investigation could result in our having to pay fines or penalties, either on behalf of Ciner Corp or through ANSAC, or otherwise adversely affect the ability of ANSAC to continue serving export markets. In the event of an unfavorable outcome in any such investigation, the withdrawal of one or more members of ANSAC or the dissolution of ANSAC, we could be forced to use alternative methods to facilitate additional direct export sales and may be obligated to pay our respective portion of the net assets or deficit of the cooperative. Any of these developments could lead us to incur additional costs and may result in lower pricing for our export sales, which could have a negative impact on our results of operations, financial condition and our ability to distribute cash to our unitholders. For more information about ANSAC, see Item 1, “Business—Customers.”

An increase in natural gas prices, or an interruption in our natural gas supply, would negatively impact our competitive cost position when compared to other foreign and domestic soda ash producers.

We rely on natural gas as the main energy source in our soda ash production process, and therefore the cost of natural gas is a significant component of the total production cost for our soda ash. The monthly Henry Hub natural gas settlement prices, over the past five years, have ranged between $1.73 and $6.00. For the years ended December 31, 2017 and 2016, the average monthly Henry Hub natural gas settlement prices were $2.99 and $2.52 per MMBtu, respectively. Furthermore, the price of natural gas could increase as a result of reduced domestic drilling and production activity. Drilling and production operations are subject to extensive federal, state, local and foreign laws and government regulations concerning, among other things, emissions of pollutants and greenhouse gases, hydraulic fracturing, and the handling of natural gas and other substances used in connection with natural gas operations, such as drilling fluids and wastewater. In addition, natural gas operations are subject to extensive federal, state and local taxation. More stringent legislation, regulation or taxation of natural gas drilling activity in the United States could directly curtail such activity or increase the cost of drilling, resulting in reduced levels of drilling activity and therefore increased natural gas prices.

Any material increase in natural gas prices could adversely impact our operations by making us less competitive with other soda ash producers who do not use natural gas as a key input. If U.S. natural gas prices were to increase to a level where foreign soda ash producers were able to improve their competitive position on a unit cost basis, this would negatively affect our competitive cost position.

All of our operations are conducted at one facility. Any adverse developments at our facility could have a material adverse effect on our results of operations and therefore our ability to make cash distributions to our unitholders.

Because all of our operations are conducted at a single facility, an event such as an explosion, fire, equipment malfunction or severe weather conditions that adversely affect our facility could significantly disrupt our trona mining or soda ash production operations and our ability to supply soda ash to our customers. For example, in the the fourth quarter of 2016, MSHA required us to make temporary operational modifications, which caused us to lose a significant amount of ore production. While Ciner Enterprises or its affiliates maintains business interruption insurance, our policy includes a time element deductible, per occurrence, and is subject to customary limitations and exclusions. Any sustained disruption in our ability to meet our obligations under our sales agreements could have a material adverse effect on our results of operations and therefore our ability to distribute cash to unitholders.

Due to our lack of product diversification, adverse developments in the soda ash industry would adversely affect our results of operations and our ability to make cash distributions to our unitholders.

We rely exclusively on the revenues generated from the production and sale of soda ash. An adverse development in the market for soda ash in U.S. or foreign markets would have a significantly greater impact on our operations and cash available for distribution to our unitholders than it would on other companies that have a more diverse asset and product base. Some of the soda ash producers with which we compete sell a more diverse range of products to broader markets.