Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Horizon Global Corp | hzn-123117xexh322.htm |

| EX-32.1 - EXHIBIT 32.1 - Horizon Global Corp | hzn-123117xexh321.htm |

| EX-31.2 - EXHIBIT 31.2 - Horizon Global Corp | hzn-123117xexh312.htm |

| EX-31.1 - EXHIBIT 31.1 - Horizon Global Corp | hzn-123117xexh311.htm |

| EX-23.1 - EXHIBIT 23.1 - Horizon Global Corp | hzn-123117xexh231.htm |

| EX-21.1 - EXHIBIT 21.1 - Horizon Global Corp | hzn-123117xexh211.htm |

| EX-2.3 - EXHIBIT 2.3 - Horizon Global Corp | exhibit23brinkspaexcdocx.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

__________________________________________________________________________________________________

Form 10-K

(Mark One) | ||

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2017 | ||

Or | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to | ||

Commission file number 001-37427

__________________________________________________________________________________________________

HORIZON GLOBAL CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

Delaware (State or Other Jurisdiction of Incorporation or Organization) | 47-3574483 (IRS Employer Identification No.) | |

2600 W. Big Beaver Road, Suite 555

Troy, Michigan 48084

(Address of Principal Executive Offices, Including Zip Code)

(248) 593-8820

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class: | Name of Each Exchange on Which Registered: | |

Common stock, $0.01 par value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definition of “accelerated filer,” “large accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o | Emerging growth company x | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Yes x No o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the common stock held by non-affiliates of the Registrant as of June 30, 2017 was approximately $352.3 million, based upon the closing sales price of the Registrant’s common stock, $0.01 par value, reported for such date on the New York Stock Exchange. For purposes of this calculation only, directors and executive officers are deemed to be affiliates of the Registrant.

As of February 26, 2018, the number of outstanding shares of the Registrant’s common stock, $0.01 par value, was 24,950,906 shares.

Portions of the Registrant’s Proxy Statement for the 2018 Annual Meeting of Stockholders are incorporated herein by reference in Part III of this Annual Report on Form 10-K to the extent stated herein.

Horizon Global Corporation

Index

2

Forward-Looking Statements

This Annual Report on Form 10-K may contain “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements speak only as of the date they are made and give our current expectations or forecasts of future events. These forward-looking statements can be identified by the use of forward-looking words, such as “may,” “could,” “should,” “estimate,” “project,” “forecast,” “intend,” “expect,” “anticipate,” “believe,” “target,” “plan” or other comparable words, or by discussions of strategy that may involve risks and uncertainties.

These forward-looking statements are subject to numerous assumptions, risks and uncertainties which could materially affect our business, financial condition or future results including, but not limited to, risks and uncertainties with respect to: the Company’s integration of the Westfalia Group (defined herein); the Company’s ability to successfully complete the acquisition of the Brink Group (defined herein); leverage; liabilities imposed by the Company’s debt instruments; market demand; competitive factors; supply constraints; material and energy costs; technology factors; litigation; government and regulatory actions; the Company’s accounting policies; future trends; general economic and currency conditions; various conditions specific to the Company’s business and industry; and other risks that are discussed in, Part I, Item 1A, “Risk Factors.” The risks described in this Annual Report on Form 10-K are not the only risks facing our Company. Additional risks and uncertainties not currently known to us or that we currently deemed to be immaterial also may materially adversely affect our business, financial position and results of operations or cash flows.

The cautionary statements set forth above should be considered in connection with any subsequent written or oral forward-looking statements that we or persons acting on our behalf may issue. We caution readers not to place undo reliance on the statements, which speak only as of the date of this Annual Report on Form 10-K. We do not undertake any obligation to review or confirm analysts’ expectations or estimates or to release publicly any revisions to any forward-looking statement to reflect events or circumstances after the date of this Annual Report on Form 10-K or to reflect the occurrence of unanticipated events, except as otherwise required by law.

We disclose important factors that could cause our actual results to differ materially from our expectations implied by our forward-looking statements under Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and elsewhere in this Annual Report on Form 10-K. These cautionary statements qualify all forward-looking statements attributed to us or persons acting on our behalf. When we indicate that an event, condition or circumstance could or would have an adverse effect on us, we mean to include effects upon our business, financial and other conditions, results of operations, prospects and ability to service our debt.

3

PART I

Item 1. Business

Overview

Horizon Global Corporation, which we refer to herein as “Horizon,” “Horizon Global,” “we” or the “Company,” became an independent, publicly traded company as the result of a spin-off, which we refer to herein as the “spin-off,” from TriMas Corporation, or “TriMas,” on June 30, 2015.

We are a leading designer, manufacturer and distributor of a wide variety of high-quality, custom-engineered towing, trailering, cargo management and other related accessory products on a global basis, serving the automotive aftermarket, retail and original equipment, or “OE,” channels.

The Company is organized into three reportable segments: Horizon Americas, Horizon Asia-Pacific, and Horizon Europe-Africa. Horizon Americas has operations in North and South America, and we believe has been a leader in towing and trailering-related products sold through retail, aftermarket, OE, e-commerce and industrial channels. Horizon Asia‑Pacific and Horizon Europe‑Africa focus their sales and manufacturing efforts outside of North and South America. Horizon Asia‑Pacific operates primarily in Australia, Thailand, and New Zealand, while Horizon Europe‑Africa operates primarily in Germany, France, the United Kingdom, Romania, and South Africa. We believe Horizon Asia‑Pacific and Horizon Europe‑Africa have been leaders in towing related products sold through the OE and aftermarket channels in their regions.

Our products are used in two primary categories across the world: commercial applications, or “Work,” and recreational activities, or “Play.” Some of the markets in our Work category include agricultural, automotive, construction, fleet, industrial, marine, military, mining and municipalities. Some of the markets in our Play category include equestrian, power sports, recreational vehicle, specialty automotive, truck accessory and other specialty towing applications. We believe that the primary brands we offer are among the most recognized in the markets we serve and are known for quality, safety and performance. Our products reach end consumers through many avenues, including independent installers, warehouse distributors, dealers, OE, retail stores and online retailers.

We believe no individual competitor serving the channels we participate in can match our broad product portfolio, which we categorize into the following four groups:

▪ | Towing: This product category includes devices and accessories installed on a tow-vehicle for the purpose of attaching a trailer, camper, etc. such as hitches, fifth wheels, gooseneck hitches, weight distribution systems, wiring harnesses, draw bars, ball mounts, crossbars, towbars, security and other towing accessories; |

▪ | Trailering: This product category includes control devices and components of the trailer itself such as brake controls, jacks, winches, couplers, interior and exterior vehicle lighting and brake replacement parts; |

▪ | Cargo Management: This product category includes a wide variety of products used to facilitate the transportation of various forms of cargo, to secure that cargo or to organize items. Examples of these products are bike racks, roof cross bar systems, cargo carriers, luggage boxes, car interior protective products, rope, tie-downs, tarps, tarp straps, bungee cords, loading ramps and interior travel organizers; and |

▪ | Other: This product category includes a diverse range of items in our portfolio that do not fit into any of the previous three main categories. Items in this category include tubular push bars, side steps, sports bars, skid plates, and oil pans. |

We have positioned our product portfolio to create a variety of options based on price-point, ranging from entry-level to premium-level products across most of our markets. We believe the brands we offer in our aftermarket channel have significant customer recognition, with the four most significant being Reese®, Hayman-Reese™, Draw-Tite® and Westfalia®. We believe all four have substantial market share and have been leading brands in the towing market for over 50 years. These brands provide the foundation of our market position based on worldwide commercial and consumer acceptance. We also maintain a collection of regionally recognized brands that include Aqua Clear™, Bulldog®, BTM, DHF, Engetran, Fulton®, Kovil, Parkside®, Reese Secure™, Reese Explorer™, Reese Power Sports, Reese Towpower™, ROLA®, Tekonsha®, Trojan®, WesBarg® and Witter Towbar Systems. In addition to these product brands, we historically marketed our products to our OE customers in the Asia-Pacific segment, and more recently in the Americas, under the name TriMotive.

For information pertaining to net sales and operating profit attributed to our reportable segments, refer to Note 15, “Segment Information,” included in Item 8, “Financial Statements and Supplementary Data,” within this Annual Report on Form 10-K.

4

Our Industry

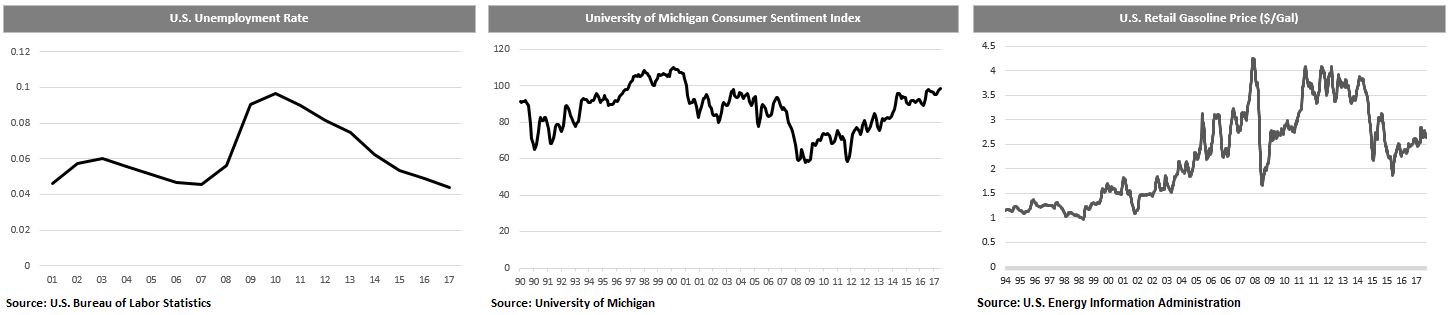

Our products are sold into a diverse set of end-markets; the primary applications relate to automotive accessories for light and recreational vehicles. Purchases of automotive accessory parts are discretionary and we believe demand is driven by macro-economic factors including (i) employment trends, (ii) consumer sentiment and (iii) fuel prices, among others.

We believe all of these metrics impact both our Work- and Play-related sales. In addition, we believe the Play-related sales are more sensitive to changes in these indices, given the Play-related sales tend to be more directly related to disposable income levels. In general, recent decreases in unemployment and fuel prices, coupled with increases in consumer sentiment, are positive trends for our businesses.

Aftermarket and Retail Channels

We sell our products in the aftermarket and retail channels to a wide range of customers, including national and regional distributors, installers, and both traditional brick and mortar and e-commerce merchants, including automotive, home hardware, farm and fleet, and mass merchants. More recent trends in the aftermarket and retail channels include:

▪ | Channel Consolidation: In the more mature market of the United States, there has been increasing consolidation in distribution networks with larger, more sophisticated aftermarket distributors and retailers gaining market share. In kind, these distributors generally require larger, more sophisticated suppliers with product expertise, category management and supply chain services and capabilities, as well as a global manufacturing and services footprint. We provide customers in this category the opportunity to rationalize their supply base of vendors in our product lines by virtue of our broad offering and product expertise; and |

▪ | Growth of Online Capabilities: Reaching consumers directly through online capabilities, including e-commerce, is having an increasing impact on the global automotive aftermarket and retail channels. Establishment of a robust online presence is critical for suppliers regardless of whether or not they participate directly in e-commerce. We believe we are positioned well to take advantage of this continuing trend, given our established online presence. We support consumers by offering a wide range of information on our products and services, including installation videos, custom-fit guides and links to authorized dealers and both brick and mortar and e-commerce merchants. |

OE Channels

The OE channel is comprised of automobile manufacturers and their dealer networks, referred to collectively as automotive OE, as well as non-automotive manufacturers of agricultural equipment, trailers, and other custom assemblies, collectively referred to as industrial OE. The two main components of this channel are original equipment manufacturers (“OEM”) and original equipment suppliers (“OES”). While OE demand is typically driven by planned production, suppliers also grow by increasing their product content on each unit produced through sales of existing product lines or expansion into new product line offerings. Given the consolidation and globalization throughout the automotive industry, suppliers combining a global presence with strong engineering, technology, manufacturing, supply chain and customer support will be best positioned to take advantage of automotive OE business opportunities.

More recent trends in the global OE supplier market include:

▪ | Global Platform/Supplier Consolidation: Automotive OEs are adopting global vehicle platforms to decrease product development costs and increase manufacturing efficiency and profitability. As a result, automotive OEs are selecting suppliers that have the capacity to manufacture and deliver products on a worldwide basis as well as the flexibility to adapt products to local variations. Suppliers with a global supply chain and efficient manufacturing capabilities are best positioned to benefit from this trend. We believe we are uniquely positioned to take advantage of this trend as a result of our global manufacturing footprint, highly developed supply chain relationships and track record of success in solving application challenges in our product lines; |

5

▪ | Outsourcing of Design and Manufacturing of Vehicle Parts and Systems: Automotive OEs continually strive to simplify their assembly processes, lower costs and reduce development times. As a result, they have increasingly relied on suppliers to perform many of the design, engineering, research and development and assembly functions traditionally performed by automotive OEs. Suppliers with extensive design and engineering capabilities are in the best position to benefit from this trend as they are able to offer value-added solutions with superior features and convenience. We believe certain automotive OEs have sought us out to assist with their engineering challenges to increase towing capacity and for the many solutions provided by our existing products; and |

▪ | Shorter Product Development Cycles: Due to frequent shifts in government regulations and customer preferences, OEs are requiring suppliers to continue to provide new designs and product innovations. These trends are prevalent in mature markets as well as, emerging markets, which are advancing rapidly towards the regulatory standards and consumer preferences of the more mature markets. Suppliers with strong technologies, robust engineering and development capabilities are best positioned to meet OE demands for rapid innovation. Our broad product offerings, product expertise, and global engineering footprint enables us to rapidly deploy solutions meeting the changing customer needs. |

Competitive Strengths

We believe our reportable segments share and benefit from the following competitive strengths:

▪ | Diverse Product Portfolio of Market Leading Brands. We believe we benefit from a diverse portfolio of high-quality and highly-engineered products sold under globally recognized and market leading brand names. By offering a wide range of products, we are able to provide a complete solution to satisfy our customers’ towing, trailering and cargo management needs, as well as serve diverse channels through effective brand management. Our brands are well-known in their respective product areas and channels. We believe that we are the leading supplier of towing products and among the leading suppliers of trailering products globally. |

▪ | Global Scale with Flexible Manufacturing Footprint and Supply Chain. We were built through internal growth and a series of acquisitions to become the only truly global automotive accessories company with the products we offer. We have the ability to produce low-volume, customized, quick-turn products in our global manufacturing facilities, while our sourcing arrangements with third-party suppliers provides us with the flexibility to manufacture or source high-volume products as end-market demand fluctuates. Our flexible manufacturing capability, low-cost manufacturing facilities and established supply chain allow us to quickly and efficiently respond to changes in end-market demand. |

▪ | Long-Term Relationships with a Diverse Customer Base. Our customers encompass a broad range of OEs, mass merchants, e-commerce websites, distributors, dealers, and independent installers, representing multiple channels to reaching the end consumer. Blue chip customers include Walmart, Ford Motor Company, FCA, Volkswagen, BMW, Mercedes-Benz, AutoZone, Amazon, Toyota, Canadian Tire, LKQ, U-Haul, Home Depot and Etrailer, among others. Our customer relationships are well established, with many exceeding 20 years. These strong partnerships can provide stability to our revenue base through economic cycles. We believe Horizon’s diverse product portfolio, global scale and flexible manufacturing capabilities enable us to provide a unique value proposition to customers. |

▪ | Globally Competitive Cost Structure. Since becoming an independent public company, we have focused on margin improvement activities, identifying and acting on projects to reduce our cost structure. With focused, identifiable projects under way or complete, we believe we will benefit from improved operating margins and cash flow that can then be deployed to high-value creation activities. The combination of our strong brand names, leading market position, flexible manufacturing and sourcing operations have historically resulted in significant cash flow generation. |

▪ | Experienced Management Team. Our management team is led by our Chief Executive Officer, Mark Zeffiro, who was a senior executive at TriMas for over seven years and has more than 25 years of financial, operational and business leadership experience with companies such as Black & Decker and General Electric Company. David Rice, our Chief Financial Officer, joined TriMas in 2005 and brings more than 30 years of financial, audit and leadership experience to the role. David was previously division finance officer of Cequent Performance Products. Carl Bizon, President of Horizon Americas, has over 23 years of experience, including nearly eight years as the President of Horizon’s international business, including both Europe-Africa and Asia-Pacific. The leadership team of Horizon Asia‑Pacific includes Jason Kieseker, who joined the Horizon business in 2001 and has held various leadership roles within our Horizon Asia‑Pacific business. The leadership team of Horizon Europe‑Africa includes Paul Caruso, who has over 30 years of experience in a variety of roles within the industrial and automotive markets. |

6

Key Business Priorities

Horizon Global established three strategic platforms for value creation focused on business improvement and transformation, supported by a company culture of continuous improvement.

▪ | Margin Expansion. Our first priority is to drive the organization to a 10% operating margin level. We believe the investments made in our facilities and equipment over the past few years, along with our efforts to realign or operations, should provide the foundation for additional margin expansion. We are developing an organization in which all team members are focused on constantly improving the efficiency of all operations through the adoption of lean and continuous improvement practices. |

▪ | Capital Structure. Our second priority is to improve our capital structure. Our net leverage ratio, as defined in certain of the agreements covering our indebtedness, at December 31, 2017 was approximately 3.2 times (expected to be 5.0 times subsequent to the acquisition of Brink International B.V. (“Brink Group”), which is discussed below). Our long-term net leverage ratio target is less than 2 times. We aim to accomplish this goal through both margin improvement as well as paying down our fixed obligations, and should we decide to do so, we have a structure in place that allows us to prepay debt in addition to the amortization required under our term debt. |

▪ | Organic Growth. Our third priority is to grow the business 3% to 5% on an organic basis, annually. We have identified five broad areas of focused growth activities, involving geographic markets and sales channels, which we believe are particularly aligned with our competitive strengths. |

Growth Strategies

Prior to becoming an independent public company, Horizon operated on a regional basis under separate management teams, with independent business decisions and resource allocations made by the Horizon Americas, Horizon Asia‑Pacific and Horizon Europe‑Africa leaders. As a public company, we are reorganizing our global operations to operate as a single combined entity. As a result, we believe that we have multiple opportunities to integrate, improve and grow our business, whether via organic initiatives or via acquisitions of new products or in new geographies, through the following strategies:

▪ | Original Equipment. The global market for accessories and vehicle personalization is increasing and automotive manufacturers are looking for suppliers to partner with to create genuine accessories to meet this need. Historically, this has been a regional effort, but the growth of global automotive OE has increased the need for global suppliers. Our geographic footprint, existing customer relationships and the increase in global vehicle platforms align to present us with unique opportunities to grow with our automotive OE customers. |

▪ | E-commerce. We intend to leverage the breadth of our product portfolio and global manufacturing footprint to expand our presence in the high growth e-commerce channel. This strategy is applicable in our developed markets where a focus on content delivery and customer support drive growth. It is also a powerful tool as we look at developing new, less mature markets around the world, enabling a direct connection with the users of our product set. |

▪ | Latin American Markets. Since entering the Latin American market, we have witnessed a desire to accessorize vehicles among new entrants to the middle class. We expanded our global footprint and product portfolio in Brazil by acquiring DHF Soluções Automotivas Ltda and Engetran Engenharia, Indústria, e Comércio de Peças e Acessórios Veiculares Ltda, respectively, which are included in Horizon Americas. We believe these expansions into new geographies, as well as our manufacturing presence in Mexico, provide opportunities for growth, while supporting both new and existing global customers. |

▪ | Chinese Market. China is in the early stages of adoption for towing and trailering products. As this adoption rate increases, there is an opportunity for us to bring our experience in the safe use of these products into the market in a meaningful capacity. The rapidly growing middle class, in concert with a developing interest in an outdoor recreational lifestyle, is expected to result in incremental demand for our automotive aftermarket products and accessories. We intend to leverage our existing relationships with global automotive OEs and our global manufacturing and distribution network to expand our sales in this developing economy. |

▪ | Product Innovation. Our focus in multi-generational product planning is to formalize the process by which we integrate the feedback and needs of users into our product development engine. We look to move beyond simply responding to the feedback that we receive, to anticipating the functionality future products need to possess to enrich the lives of our users. |

7

Marketing, Customers and Distribution

Horizon employs a dedicated sales force in each of our primary channels. In serving our customers globally, we rely upon our strong historical customer relationships, custom engineering capability, brand recognition, broad product offerings, our established distribution network and varied merchandising strategies to bolster our towing, trailering, cargo management and accessory product sales. Significant Horizon customers include Ford Motor Company, Volkswagen, Toyota and General Motors/Holden in the OE channel; Walmart, Tractor Supply Company and Super Retail Group in the retail channel; and LKQ, U-Haul and Redneck Trailer Supplies in the aftermarket channel. No customer represented greater than 10% of total revenue during the years ended December 31, 2017, 2016 or 2015.

Competition

The competitive environment for automotive accessory products is highly fragmented and is characterized by numerous smaller suppliers, even the largest of which tend to focus in narrow product categories. We believe there is no individual competitor that has the breadth of product portfolio on a global basis in the markets we serve. Significant towing competitors include Curt Manufacturing, B&W Trailer Hitches, The Bosal Group, Brink Group, Buyers Products Company, Demco Products, PullRite, Westin Automotive Products and Camco. Significant trailering competitors include Pacific Rim, Dutton-Lainson, Shelby, Ultra-Fab, Sea-Sense and Atwood. In addition, competition in the cargo management product category primarily comes from Thule, Yakima, Bell, Masterlock and Saris.

Acquisition Strategy

We believe that our businesses have significant opportunities to grow through disciplined strategic acquisitions. We typically seek bolt-on acquisitions, in which we acquire another industry participant or adjacent product lines that enhance the strengths of our core businesses. When evaluating acquisition targets, we look for opportunities to expand our existing product offerings, gain access to new customers and end markets, add new early life cycle technologies, as well as add additional distribution channels, expand our geographic footprint and/or capitalize on scale and cost efficiencies.

Westfalia Acquisition

On October 4, 2016, we completed our previously announced acquisition of Westfalia-Automotive Holding GmbH and TeIJs Holding B.V., which we refer to collectively as the “Westfalia Group” or “Westfalia”. Pursuant to the purchase agreement, we acquired all of the outstanding equity interests of the Westfalia Group for cash consideration of approximately $99.2 million and the issuance to certain of the sellers of 2,704,310 shares of our common stock in a transaction exempt from registration requirements of the Securities Act of 1933, or the “Securities Act.” We funded the cash payment, as well as the repayment of certain of the Westfalia Group’s debt, through a combination of cash on hand and $152.0 million of incremental borrowings under our Term B Loan.

The Westfalia Group is a leading European towing company. Headquartered in Rheda-Wiedenbrück, Germany, with operating facilities in 11 countries, it manufactures towing and trailering products, including more than 1,700 different types of towbars, wiring kits and carrier systems for cars and light utility vehicles. It holds in excess of 300 issued patents and published patent applications protecting its unique line of towing and trailering products. The brands under which it markets its products include Westfalia, Terwa and Siarr.

The acquisition of the Westfalia Group positions us as a leading manufacturer of towing and trailering equipment in Europe and further complements our broad portfolio. We believe the acquisition will expand our opportunities for revenue and margin growth, increase our market share and augment our global OE footprint with access to new markets and customers.

Brink Group

On December 13, 2017, we entered into a definitive agreement to acquire the Brink Group, subject to the satisfaction of customary closing conditions, including receipt of regulatory approvals. We plan to finance the acquisition through new long-term debt and cash on hand. The Company expects to close the acquisition in the second quarter of 2018.

The Brink Group is an industry-leading innovator and manufacture of towbars, wiring kits, and towing accessories. Headquartered in Staphorst, Netherlands, with operations in eight countries, it manufactures towing and trailering solutions serving the automotive OE and aftermarket channels. This acquisition will strengthen our global platform and enhance our product portfolio.

8

Materials and Supply Arrangements

We are sensitive to price movements in our raw materials supply base. Our largest material purchases are for steel, copper, and aluminum. We also consume a significant amount of energy via utilities in our facilities. Historically, when we have experienced increasing costs of steel, we have successfully worked with our suppliers to manage cost pressures and disruptions in supply. Price increases used to offset inflation or a disruption of supply in core materials have generally been successful, although sometimes delayed. Increases in price for these purposes represent a risk in execution.

Employees and Labor Relations

As of December 31, 2017, we employed approximately 4,300 people, of which approximately 13% were located in the United States. In the United States, we have no collective bargaining agreements. Employee relations have generally been satisfactory.

On July 21, 2015, we announced the decision to close our manufacturing facility in Ciudad Juarez, Mexico along with our distribution warehouse in El Paso, Texas, within our Horizon Americas segment, impacting approximately 214 hourly and 47 salaried employees. During the second quarter of 2016, we vacated the El Paso, Texas and Juarez, Mexico sites.

Seasonality and Backlog

We experience some seasonality in our business. Sales of towing and trailering products in the northern hemisphere, where we generate the majority of our sales, are generally stronger in the second and third calendar quarters, as trailer OEs, distributors and retailers acquire product for the spring and summer selling seasons. Our growing businesses in the southern hemisphere are stronger in the first and fourth calendar quarters. We do not consider order backlog to be a material factor in our businesses.

Environmental Matters

We are subject to increasingly stringent environmental laws and regulations, including those relating to air emissions, wastewater discharges and chemical and hazardous waste management and disposal. Some of these environmental laws hold owners or operators of land or businesses liable for their own and for previous owners’ or operators’ releases of hazardous or toxic substances or wastes. Other environmental laws and regulations require the obtainment and compliance with environmental permits. To date, costs of complying with environmental, health and safety requirements have not been material. However, the nature of our operations and our long history of industrial activities at certain of our current or former facilities, as well as those acquired, could potentially result in material environmental liabilities.

While we must comply with existing and pending climate change legislation, regulation and international treaties or accords, current laws and regulations have not had a material impact on our business, capital expenditures or financial position. Future events, including those relating to climate change or greenhouse gas regulation could require us to incur expenses related to the modification or curtailment of operations, installation of pollution control equipment or investigation and cleanup of contaminated sites.

Intangible Assets

Our identified intangible assets, consisting of customer relationships, trademarks and trade names and technology, are recorded at approximately $90.2 million as of December 31, 2017, net of accumulated amortization. The valuation of each of our identified intangibles was performed using broadly accepted valuation methodologies and techniques.

Customer Relationships. We have developed and maintained stable, long-term selling relationships with customer groups for specific branded products and/or focused market product offerings within each of our businesses. Useful lives assigned to customer relationship intangibles range from five to 25 years and have been estimated using historic customer retention and turnover data. Other factors considered in evaluating estimated useful lives include the diverse nature of focused markets and products of which we have significant share, how customers in these markets make purchases and these customers’ position in the supply chain. We also monitor and evaluate the impact of other evolving risks including the threat of lower cost competitors and evolving technology.

Trademarks and Trade Names. Each of our operating groups designs and manufactures products for focused markets under various trade names and trademarks. Our trademark/trade name intangibles are well-established and considered long-lived assets that require maintenance through advertising and promotion expenditures. Because it is our practice and intent to maintain and to continue to support, develop and market these trademarks/trade names for the foreseeable future, we consider our rights in these trademarks/trade names to have an indefinite life, except as otherwise dictated by applicable law. During the second quarter of 2016, we made a decision to simplify our brand offering in the Horizon Americas segment. This resulted in the impairment of trade names with an aggregate carrying value of $2.4 million. During the fourth quarter of 2016, we performed our annual assessment of indefinite-lived intangible assets. Based on this assessment, we determined that certain trade names with an aggregate carrying value of $6.9 million were impaired. This resulted in impairment charges of $6.2 million. No impairments were recorded in 2017.

9

For additional information, refer to Note 6, “Goodwill and Other Intangible Assets,” included in Item 8, “Financial Statements and Supplementary Data,” within this Annual Report on Form 10-K.

Technology. We hold a number of U.S. and foreign patents, patent applications, and proprietary product and process-oriented technologies. We have, and will continue to dedicate, technical resources toward the further development of our products and processes in order to maintain our competitive position in the industrial, commercial and consumer end markets that we serve. Estimated useful lives for our technology intangibles range from three to 15 years and are determined in part by any legal, regulatory or contractual provisions that limit useful life. Other factors considered include the expected use of the technology by the operating groups, the expected useful life of the product and/or product programs to which the technology relates, and the rate of technology adoption by the industry.

International Operations

Approximately 52.6% of our net sales for the year ended December 31, 2017 were derived outside of the United States. We may significantly expand our international operations through organic growth and acquisitions. In addition, approximately 94.9% of our consolidated property and equipment - net as of December 31, 2017 were located outside of the United States. We operate manufacturing facilities in Australia, Brazil, France, Germany, Romania, Mexico, New Zealand, South Africa, and Thailand. For information pertaining to the net sales and total assets attributed to our international operations, refer to Note 15, “Segment Information,” included in Item 8, “Financial Statements and Supplementary Data,” within this Annual Report on Form 10-K.

Website Access to Company Reports

We use our Investor Relations website, www.horizonglobal.com, as a channel for routine distribution of important information, including news releases, analyst presentations and financial information. We post filings as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC, including our annual, quarterly, and current reports on Forms 10-K, 10-Q and 8-K, our proxy statements and any amendments to those reports or statements. All such postings and filings are available on our Investor Relations website free of charge. The SEC also maintains a website, www.sec.gov, that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC. The content on any website referred to in this Annual Report on Form 10-K is not incorporated by reference into this Annual Report on Form 10-K unless expressly noted.

10

Item 1A. Risk Factors

You should carefully consider each of the risks described below, together with information included elsewhere in this Annual Report on Form 10-K and other documents we file with the SEC. The risks that are highlighted below are not the only ones that we face. Some of our risks relate principally to our business and the industry in which we operate, while others relate principally to our spin-off from TriMas, to the securities markets in general and ownership of our common stock. If any of the following risks actually occur, our business, financial condition or results of operations could be negatively affected.

Risks Relating to our Business and our Industry

Our businesses depend upon general economic conditions and we serve some customers in highly cyclical industries; as such, we may be subject to the loss of sales and margins due to an economic downturn or recession.

Our financial performance depends, in large part, on conditions in the markets that we serve in both the U.S. and global economies. Some of the industries that we serve are highly cyclical, such as the agricultural, automotive, construction, horse/livestock, industrial, marine, military, recreational, trailer and utility markets. We may experience a reduction in sales and margins as a result of a downturn in economic conditions or other macroeconomic factors. Lower demand for our products may also negatively affect the capacity utilization of our production facilities, which may further reduce our operating margins.

Many of the markets we serve are highly competitive, which could limit the volume of products that we sell and reduce our operating margins.

Many of our products are sold in competitive markets. We believe that the principal points of competition in our markets are product quality and price, design and engineering capabilities, product development, conformity to customer specifications, reliability and timeliness of delivery, customer service and effectiveness of distribution. Maintaining and improving our competitive position will require continued investment by us in manufacturing, engineering, quality standards, marketing, customer service and support of our distribution networks. We may have insufficient resources in the future to continue to make such investments and, even if we make such investments, we may not be able to maintain or improve our competitive position. We also face the risk of lower-cost foreign manufacturers located in China, Southeast Asia, India and other regions competing in the markets for our products, and we may be driven as a consequence of this competition to increase our investment overseas. Making overseas investments can be highly complicated and we may not always realize the advantages we anticipate from any such investments. Competitive pressure may limit the volume of products that we sell and reduce our operating margins.

We may be unable to successfully implement our business strategies. Our ability to realize our business strategies may be limited.

Our businesses operate in relatively mature industries and it may be difficult to successfully pursue our growth strategies and realize material benefits therefrom. Even if we are successful, other risks attendant to our businesses and the economy generally may substantially or entirely eliminate the benefits.

We may not achieve our strategic goals for margin expansion, capital structure improvement and organic growth; our past performance in these areas may not be indicative of future performance. Failure to achieve our strategic goals may adversely impact our results of operations.

Our strategic platforms for value creation and goals for margin expansion, capital structure improvement and organic growth are subject to risk and uncertainty and depend on general economic, credit, capital market and other conditions that are beyond our control and are subject to fluctuation. Our past performance with respect to margin expansion, capital structure improvement and organic growth, both before and after the spin-off, should be considered independent from, and may not be a reliable indicator of, future performance. These strategic goals may need to be revised or may not be met for a number of reasons, including changes in general economic conditions in the United States and abroad, changes in credit and capital market conditions, increased competition in the markets for our products, increases in raw material or energy costs and changes in technology and manufacturing techniques.

Increases in our raw material or energy costs or the loss of critical suppliers could adversely affect our profitability and other financial results.

We are sensitive to price movements in our raw materials supply base. Our largest material purchases are for steel, copper and aluminum. The prices for these products have historically been volatile, fluctuate with market conditions and may increase as a result of various factors, including: a reduction in the number of suppliers due to restructurings, bankruptcies and consolidations, declining supply due to mine or mill closures and other factors that adversely impact supplier profitability, including increases in supplier operating expenses caused by rising raw material and energy costs. We may be unable to completely offset the impact with price increases on a timely basis due to outstanding commitments to our customers, competitive considerations or our customers’ resistance to accepting such price increases and our financial performance may be adversely impacted by further price

11

increases. A failure by our suppliers to continue to supply us with certain raw materials or component parts on commercially reasonable terms, or at all, could have a material adverse effect on us. To the extent there are energy supply disruptions or material fluctuations in energy costs, our margins could be materially adversely impacted.

Our products are typically highly engineered or customer-driven and we are subject to risks associated with changing technology and manufacturing techniques that could place us at a competitive disadvantage.

We believe that our customers rigorously evaluate their suppliers on the basis of product quality, price competitiveness, technical expertise and development capability, new product innovation, reliability and timeliness of delivery, product design capability, manufacturing expertise, operational flexibility, customer service and overall management. Our success depends on our ability to continue to meet our customers’ changing expectations with respect to these criteria. We anticipate that we will remain committed to product research and development, advanced manufacturing techniques and service to remain competitive, which entails significant costs. We may be unable to address technological advances, implement new and more cost-effective manufacturing techniques, or introduce new or improved products, whether in existing or new markets, so as to maintain our businesses’ competitive positions or to grow our businesses as desired.

We depend on the services of key individuals and relationships, the loss of which could materially harm us.

Our success will depend, in part, on the efforts of our senior management, including our Chief Executive Officer. Our future success will also depend on, among other factors, our ability to attract and retain other qualified personnel. The loss of the services of any of our key employees or the failure to attract or retain employees could have a material adverse effect on us.

A future impairment of our intangible assets or goodwill could have a material negative impact on our financial results.

At December 31, 2017, our intangible assets and goodwill were approximately $90.2 million and $138.2 million, respectively. Intangibles and goodwill each represented approximately 14% and 21% of our total assets, respectively. If we experience declines in sales and operating profit or do not meet our current and forecasted operating budget, we may be subject to future impairment charges. Because of the significance of these assets, any future impairment could have a material adverse effect on our financial results.

We may face liability associated with the use of products for which patent ownership or other intellectual property rights are claimed.

We may be subject to claims or inquiries regarding alleged unauthorized use of a third party’s intellectual property. An adverse outcome in any intellectual property litigation could subject us to significant liabilities to third parties, require us to license technology or other intellectual property rights from others, require us to comply with injunctions to cease marketing or using certain products or brands, or require us to redesign, re-engineer, or re-brand certain products or packaging, any of which could affect our business, financial condition and operating results. If we are required to seek licenses under patents or other intellectual property rights of others, we may not be able to acquire these licenses on acceptable terms, if at all. In addition, the cost of responding to an intellectual property infringement claim, in terms of legal fees and expenses and the diversion of management resources, whether or not the claim is valid, could have a material adverse effect on our business, results of operations and financial condition.

We may be unable to adequately protect our intellectual property.

While we believe that our patents, trademarks and other intellectual property have significant value, it is uncertain that this intellectual property or any intellectual property acquired or developed by us in the future, will provide a meaningful competitive advantage. Our patents or pending applications may be challenged, invalidated or circumvented by competitors or rights granted thereunder may not provide meaningful proprietary protection. Moreover, competitors may infringe on our patents or successfully avoid them through design innovation. Policing unauthorized use of our intellectual property is difficult and expensive, and we may not be able to, or have the resources to, prevent misappropriation of our proprietary rights, particularly in countries where the laws may not protect such rights as fully as in the United States. The cost of protecting our intellectual property may be significant and could have a material adverse effect on our financial condition and future results of operations.

We may incur material losses and costs as a result of product liability, recall and warranty claims that may be brought against us.

We are subject to a variety of litigation incidental to our business, including claims for damages arising out of use of our products, claims relating to intellectual property matters and claims involving employment matters and commercial disputes.

We currently carry insurance and maintain reserves for potential product liability claims. However, our insurance coverage may be inadequate if such claims do arise and any liability not covered by insurance could have a material adverse effect on our business. Although we have been able to obtain insurance in amounts we believe to be appropriate to cover such liability to date, our

12

insurance premiums may increase in the future as a consequence of conditions in the insurance business generally or our situation in particular. Any such increase could result in lower net income or cause the need to reduce our insurance coverage. In addition, a future claim may be brought against us that could have a material adverse effect on us. Any product liability claim may also include the imposition of punitive damages, the award of which, pursuant to certain state laws, may not be covered by insurance. Our product liability insurance policies have limits that, if exceeded, may result in material costs that could have an adverse effect on our future profitability. In addition, warranty claims are generally not covered by our product liability insurance. Further, any product liability or warranty issues may adversely affect our reputation as a manufacturer of high-quality, safe products, divert management’s attention, and could have a material adverse effect on our business.

Our business may be materially and adversely affected by compliance obligations and liabilities under environmental laws and regulations.

We are subject to increasingly stringent environmental laws and regulations, including those relating to air emissions, wastewater discharges and chemical and hazardous waste management and disposal. Some of these environmental laws hold owners or operators of land or businesses liable for their own and for previous owners’ or operators’ releases of hazardous or toxic substances or wastes. Other environmental laws and regulations require the obtainment and compliance with environmental permits. To date, costs of complying with environmental, health and safety requirements have not been material. However, the nature of our operations and our long history of industrial activities at certain of our current or former facilities, as well as those acquired, could potentially result in material environmental liabilities.

While we must comply with existing and pending climate change legislation, regulation and international treaties or accords, current laws and regulations have not had a material impact on our business, capital expenditures or financial position. Future events, including those relating to climate change or greenhouse gas regulation could require us to incur expenses related to the modification or curtailment of operations, installation of pollution control equipment or investigation and cleanup of contaminated sites.

We have a substantial amount of debt. To service our debt, we will require a significant amount of cash. Our ability to generate cash depends on many factors beyond our control. If we cannot generate the required cash, we may not be able to make the necessary payments required under our debt.

At December 31, 2017, we had total long-term debt of approximately $293.7 million (without giving effect to the equity component of our convertible senior notes or any debt discount). Our ability to make payments on our debt, fund our other liquidity needs, and make planned capital expenditures will depend on our ability to generate cash in the future. Our historical financial results have been, and we anticipate that our future financial results will be, subject to fluctuations. Our ability to generate cash, to a certain extent, is subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control. We cannot guarantee that our business will generate sufficient cash flow from our operations or that future borrowings will be available to us in an amount sufficient to enable us to make payments of our debt, fund other liquidity needs and make planned capital expenditures.

The degree to which we are currently leveraged could have important consequences for shareholders. For example, it could:

▪ | require us to dedicate a substantial portion of our cash from operations to the payment of debt service, reducing the availability of our cash flow to fund working capital, capital expenditures, acquisition and other general corporate purposes; |

▪ | increase our vulnerability to adverse economic or industry conditions; |

▪ | limit our ability to obtain additional financing in the future to enable us to react to changes in our business; or |

▪ | place us at a competitive disadvantage compared to businesses in our industry that have less debt. |

Additionally, any failure to comply with covenants in the instruments governing our debt could result in an event of default which, if not cured or waived, would have a material adverse effect on us.

Our borrowing costs may be impacted by our credit ratings developed by various rating agencies.

Two major ratings agencies, Standard & Poor’s and Moody’s, evaluate our credit profile on an ongoing basis and have each assigned ratings for our long-term debt. If our credit ratings were to decline, our ability to access certain financial markets may become limited, the perception of us in the view of our customers, suppliers and security holders may worsen and as a result, we may be adversely affected.

13

We have significant operating lease obligations and our failure to meet those obligations could adversely affect our financial condition.

We lease many of our manufacturing facilities and certain capital equipment. Our rental expense in 2017 under these operating leases was approximately $20.0 million. A failure to pay our rental obligations would constitute a default allowing the applicable landlord to pursue any remedy available to it under applicable law, which would include taking possession of our property and, in the case of real property, evicting us. These leases are categorized as operating leases and are not considered indebtedness for purposes of our debt instruments.

We may be subject to further unionization and work stoppages at our facilities or our customers may be subject to work stoppages, which could seriously impact the profitability of our business.

As of December 31, 2017, approximately 52% of our work force was unionized under several different unions. We are not aware of any present active union organizing drives at any of our other facilities. We cannot predict the impact of any further unionization of our workplace.

Many of our direct or indirect customers have unionized work forces. Strikes, work stoppages or slowdowns experienced by these customers or their suppliers could result in slowdowns or closures of assembly plants where our products are included. In addition, organizations responsible for shipping our customers’ products may be impacted by occasional strikes or other activity. Any interruption in the delivery of our customers’ products could reduce demand for our products and could have a material adverse effect on us.

Our healthcare costs for active employees and future retirees may exceed our projections and may negatively affect our financial results.

We provide healthcare benefits for active employees through comprehensive hospital, surgical and major medical benefit provisions, all of which are subject to various cost-sharing features. If our costs under our benefit programs for active employees exceed our projections, our business and financial results could be materially adversely affected. Additionally, foreign competitors and many domestic competitors provide fewer benefits to their employees, and this difference in cost could adversely impact our competitive position.

A significant portion of our sales is derived from international sources, which exposes us to certain risks which may adversely affect our business and our financial results.

We have extensive operations outside of the United States. Approximately 53% of our net sales for the year ended December 31, 2017 were derived from sales by our subsidiaries located outside of the United States. In addition, we may significantly expand our international operations through internal growth and acquisitions. International operations, particularly sales to emerging markets and manufacturing in non-U.S. countries, are subject to risks which are not present within U.S. markets, which include, but are not limited to, the following:

▪ | volatility of currency exchange between the U.S. dollar and currencies in international markets; |

▪ | changes in local government regulations and policies including, but not limited to, foreign currency exchange controls or monetary policy, governmental embargoes, repatriation of earnings, expropriation of property, duty or tariff restrictions, investment limitations and tax policies |

▪ | political and economic instability and disruptions, including labor unrest, civil strife, acts of war, guerrilla activities, insurrection and terrorism; |

▪ | legislation that regulates the use of chemicals; |

▪ | disadvantages of competing against companies from countries that are not subject to U.S. laws and regulations, including the Foreign Corrupt Practices Act (“FCPA”); |

▪ | compliance with international trade laws and regulations, including export control and economic sanctions, such as anti-dumping duties; |

▪ | difficulties in staffing and managing multi-national operations; |

▪ | limitations on our ability to enforce legal rights and remedies; |

▪ | tax inefficiencies in repatriating cash flow from non-U.S. subsidiaries that could affect our financial results and reduce our ability to service debt; |

▪ | reduced protection of intellectual property rights; |

14

▪ | increasingly complex laws and regulations concerning privacy and data security, including the European Union’s General Data Protection Regulation; and |

▪ | other risks arising out of foreign sovereignty over the areas where our operations are conducted. |

We are also exposed to risks relating to U.S. policy with respect to companies doing business in foreign jurisdictions, particularly in light of the new U.S. presidential administration. Legislation or other changes in the U.S. tax laws could increase our U.S. income tax liability and adversely affect our after-tax profitability. In addition, the new U.S. presidential administration has introduced greater uncertainty with respect to future tax, trade regulations and trade agreements. Changes in tax policy, trade regulations or trade agreements, such as the disallowance of tax deductions on imported merchandise or the imposition of new tariffs on imported products, could have a material adverse effect on our business and results of operations.

In addition, we could be adversely affected by violations of the FCPA and similar worldwide anti-bribery laws as well as export controls and economic sanction laws. The FCPA and similar anti-bribery laws in other jurisdictions generally prohibit companies and their intermediaries from making improper payments to non-U.S. officials for the purpose of obtaining or retaining business.

Our reputation, ability to do business, and results of operations may be impaired by improper conduct by any of our employees, agents, or business partners.

While we strive to maintain high standards, we cannot provide assurance that our internal controls and compliance systems will always protect us from acts committed by our employees, agents, or business partners that would violate U.S. and/or non-U.S. laws or fail to protect our confidential information, including the laws governing payments to government officials, bribery, fraud, anti-kickback and false claims rules, competition, export and import compliance, money laundering, and data privacy laws, as well as the improper use of proprietary information or social media. Any such allegations, violations of law or improper actions could subject us to civil or criminal investigations in the United States and in other jurisdictions, could lead to substantial civil or criminal, monetary and non-monetary penalties, and related shareholder lawsuits, could lead to increased costs of compliance, could damage our reputation and could have a material effect on our financial statements.

Our growth strategy includes acquisitions. If we are unable to identify attractive acquisition candidates, successfully integrate acquired operations or realize the intended benefits of our acquisitions, we may be adversely affected.

We may pursue strategic acquisition opportunities. Any acquisition will likely require integration expenses and actions that could negatively impact our results of operations, some of which we may not be able to fully anticipate beforehand. In addition, attractive acquisition candidates may not be identified and acquired in the future, financing for acquisitions may be unavailable on satisfactory terms and we may be unable to accomplish our strategic objectives in effecting a particular acquisition. We may encounter various risks in acquiring other companies, including the possible inability to integrate an acquired business into our operations, diversion of management’s attention and unanticipated problems or liabilities, some or all of which could materially and adversely affect our business strategy and financial condition and results of operations.

We may not realize the growth opportunities and cost synergies that are anticipated from acquisitions.

We completed the acquisition of the Westfalia Group in October 2016 and we expect to acquire the Brink Group in the second quarter of 2018. The benefits that are expected to result from these acquisitions will depend, in part, on our ability to realize the anticipated growth opportunities and cost synergies as a result of these acquisitions. Our success in realizing these growth opportunities and cost synergies, and the timing of this realization, depends on the successful integration of the Westfalia Group and the Brink Group. There is a significant degree of difficulty and management distraction inherent in the process of integrating acquisitions as sizable as the Westfalia Group and the Brink Group. The process of integrating operations could cause an interruption of, or loss of, momentum in ours and the Westfalia Group or the Brink Group’s activities. Members of our senior management may be required to devote considerable amounts of time to the integration process, which will decrease the time they will have to manage our business, service existing customers, attract new customers, and develop new products or strategies. If senior management is not able to effectively manage the integration process, or if any significant business activities are interrupted as a result of the integration process, our business could suffer. There can be no assurance that we will successfully or cost-effectively integrate the Westfalia Group or the Brink Group. The failure to do so could have a material adverse effect on our business, financial condition, and results of operations.

Even if we are able to integrate the Westfalia Group and the Brink Group successfully, this integration may not result in the realization of the full benefits of the growth opportunities and cost synergies that we currently expect from this integration, and we cannot guarantee that these benefits will be achieved within anticipated time frames or at all. For example, we may not be able to eliminate duplicative costs. Moreover, we may incur substantial expenses in connection with these integrations. While it is anticipated that certain expenses will be incurred to achieve cost synergies, such expenses are difficult to estimate accurately, and may exceed current estimates. Accordingly, the benefits from these acquisitions may be offset by costs incurred to, or delays in, integrating the businesses.

15

Our acquisition agreements by which we have acquired companies include indemnification provisions that may not fully protect us and may result in unexpected liabilities.

Certain of the agreements related to the acquisition of businesses require indemnification against certain liabilities related to the operations of the company for the previous owner. We cannot be assured that any of these indemnification provisions will fully protect us, and as a result we may incur unexpected liabilities that adversely affect our profitability and financial position.

Increased information technology security threats and more sophisticated and targeted computer crime could pose a risk to our systems, networks, and products.

Increased global information technology security threats and more sophisticated and targeted computer crime pose a risk to the security of our systems and networks and the confidentiality, availability and integrity of our data and communications. While we attempt to mitigate these risks by employing a number of measures, monitoring of our networks and systems, and maintenance of backup and protective systems, our systems, networks and products remain potentially vulnerable to advanced persistent threats. Depending on their nature and scope, such threats could potentially lead to the compromising of confidential information and communications, improper use of our systems and networks, manipulation and destruction of data, defective products, production downtimes and operational disruptions, which in turn could adversely affect our reputation, customer relationships, competitiveness and results of operations. We may be required to incur significant costs to remedy damages caused by these disruptions or security breaches or to protect against disruption or security breaches in the future.

A major failure of our information systems could harm our business.

We depend on integrated information systems to conduct our business. We may experience operating problems with our information systems as a result of system failures, viruses, computer hackers or other causes. Any significant disruption or slowdown of our systems could cause customers to cancel orders or cause standard business processes to become inefficient or ineffective.

The accounting method for convertible debt securities that may be settled in cash, such as our convertible senior notes, could have a material effect on our reported financial results.

Under Accounting Standards Codification (“ASC”) 470-20, “Debt with Conversion and Other Options”, which we refer to as ASC 470-20, an entity must separately account for the liability and equity components of the convertible debt instruments (such as our convertible senior notes) that may be settled entirely or partially in cash upon conversion in a manner that reflects the issuer’s economic interest cost. The effect of ASC 470-20 on the accounting for our convertible senior notes is that the equity component is required to be included in the additional paid-in capital section of stockholders’ equity on our consolidated balance sheet and the value of the equity component would be treated as original issue discount for purposes of accounting for the debt component of our convertible senior notes. As a result, we will be required to record a greater amount of non-cash interest expense in current periods presented as a result of the amortization of the discounted carrying value of our convertible senior notes to their face amount over the term of the convertible senior notes. We will report lower net income in our financial statements because ASC 470-20 will require interest to include both the current period’s amortization of the debt discount and the instrument’s coupon interest, which could adversely affect our reported or future financial results, the trading price of our common stock and the trading price of the convertible senior notes.

In addition, under certain circumstances, convertible debt instruments (such as our convertible senior notes) that may be settled entirely or partly in cash are currently accounted for utilizing the treasury stock method, the effect of which is that the shares issuable upon conversion of our convertible senior notes are not included in the calculation of diluted earnings per share except to the extent that the conversion value of our convertible senior notes exceeds their principal amount. Under the treasury stock method, for diluted earnings per share purposes, the transaction is accounted for as if the number of shares of common stock that would be necessary to settle such excess, if we elected to settle such excess in shares, are issued. We cannot be sure that the accounting standards in the future will continue to permit the use of the treasury stock method. If we are unable to use the treasury stock method in accounting for the shares issuable upon conversion of our convertible senior notes, then our diluted earnings per share would be adversely affected.

The conditional conversion features of our 2.75% Convertible Senior Notes due 2022, if triggered, may adversely affect our financial condition.

In the event the conditional conversion features of the Convertible Notes are triggered, holders of the Convertible Notes will be entitled to convert the Convertible Notes at any time during specified periods at their option. If one or more holders elect to convert their Convertible Notes, unless we elect to satisfy our conversion obligation by delivering solely shares of our common stock, we would be required to make cash payments to satisfy all or a portion of our conversion obligation based on the conversion rate, which could adversely affect our liquidity. In addition, even if holders do not elect to convert their Convertible Notes, we could be required under applicable accounting rules to reclassify all or a portion of the outstanding principal of the Convertible Notes as a current rather than long-term liability, which could result in a material reduction of our net working capital.

16

The convertible note hedge and warrant transactions that we entered into in connection with the offering of the Convertible Senior Notes due 2022 may affect the value of the Convertible Notes and our common stock.

In connection with the offering of the Convertible Notes, we entered into convertible note hedge transactions with certain option counterparties. The Convertible Note Hedges are expected generally to reduce the potential dilution upon conversion of the Convertible Notes and/or offset any cash payments we are required to make in excess of the principal amount of converted Convertible Notes, as the case may be. We also entered into warrant transactions with each option counterparty. The Warrants could separately have a dilutive effect on our common stock to the extent that the market price per share of our common stock exceeds the strike price of the Warrants. In connection with establishing its initial hedge of the Convertible Note Hedges and Warrants, each option counterparty or an affiliate thereof may have entered into various derivative transactions with respect to our common stock concurrently with or shortly after the pricing of the Convertible Notes. This activity could increase (or reduce the size of any decrease in) the market price of our common stock or the Convertible Notes at that time. In addition, each option counterparty or an affiliate thereof may modify its hedge position by entering into or unwinding various derivatives with respect to our common stock and/or purchasing or selling our common stock or other securities of ours in secondary market transactions prior to the maturity of the Convertible Notes (and is likely to do so during any observation period related to a conversion of the Convertible Notes). This activity could also cause or avoid an increase or a decrease in the market price of our common stock or the Convertible Notes. In addition, if any such Convertible Note Hedges and Warrants fail to become effective, each option counterparty may unwind its hedge position with respect to our common stock, which could adversely affect the value of our common stock and the value of the Convertible Notes.

We are subject to counterparty risk with respect to the convertible note hedge transactions.

Each option counterparty to the Convertible Note Hedges is a financial institution, and we will be subject to the risk that it might default under the Convertible Note Hedges. Our exposure to the credit risk of an option counterparty will not be secured by any collateral. Global economic conditions have from time to time resulted in the actual or perceived failure or financial difficulties of many financial institutions. If an option counterparty becomes subject to insolvency proceedings, we will become an unsecured creditor in those proceedings with a claim equal to our exposure at that time under our transactions with the option counterparty. Our exposure will depend on many factors but, generally, the increase in our exposure will be correlated to the increase in the market price and in the volatility of our common stock. In addition, upon a default by an option counterparty, we may suffer adverse tax consequences and more dilution than we currently anticipate with respect to our common stock. We can provide no assurances as to the financial stability or viability of any option counterparty.

Risks Relating to the Spin-off

Our historical consolidated financial information is not necessarily indicative of our future financial condition, results of operations or cash flows nor do they reflect what our financial condition, results of operations or cash flows would have been as an independent public company during the periods presented.

Some of the historical consolidated financial information included in this Annual Report on Form 10-K does not reflect what our financial condition, results of operations or cash flows would have been as an independent public company during all periods presented and is not necessarily indicative of our future financial condition, future results of operations or future cash flows. This is primarily a result of the following factors:

▪ | these historical consolidated financial results include allocations of expenses for services historically provided by TriMas, and those allocations may be significantly lower than the comparable expenses we would have incurred as an independent company; |

▪ | our working capital requirements and capital expenditures historically have been satisfied as a part of TriMas’ corporate-wide capital allocation and cash management programs; as a result, our debt structure and cost of debt and other capital may be significantly different from that reflected in our historical consolidated financial statements; |

▪ | the historical consolidated financial information may not fully reflect the increased costs associated with being an independent public company, including significant changes that have occurred in our cost structure, management, financing arrangements and business operations as a result of our spin-off from TriMas; and |

▪ | the historical consolidated financial information may not fully reflect the effects of certain liabilities that will be incurred or have been assumed by us and may not fully reflect the effects of certain assets and liabilities that have been retained by TriMas. |

We remain subject to continuing contingent liabilities of TriMas following the spin-off.