Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - Zomedica Corp. | exh_321.htm |

| EX-31.2 - EXHIBIT 31.2 - Zomedica Corp. | exh_312.htm |

| EX-31.1 - EXHIBIT 31.1 - Zomedica Corp. | exh_311.htm |

| EX-23.1 - EXHIBIT 23.1 - Zomedica Corp. | exh_231.htm |

| EX-10.23 - EXHIBIT 10.23 - Zomedica Corp. | exh_1023.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

| (Mark One) | FORM 10-K |

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

or

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______________________________ to ______________________________

Commission file number:

001-38298

ZOMEDICA PHARMACEUTICALS CORP.

(Exact name of registrant as specified in its charter)

| Alberta, Canada | N/A | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| Incorporation or organization) | Identification No.) |

| 100 Phoenix Drive, Suite 190, Ann Arbor, Michigan | 48108 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (734) 369-2555

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Shares, no par value | NYSE American | |

| _____________________________________ | ___________________________________________ |

Securities registered pursuant to section 12(g) of the Act: None

______________________________________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

☐ Yes ☒ No

Indicate by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ☒ Yes ☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer ¨

Accelerated filer ¨

Non-accelerated filer ¨ (Do not check if a smaller reporting company)

Smaller reporting company ☒

Emerging growth company ☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by a check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

Note.—If a determination as to whether a particular person or entity is an affiliate cannot be made without involving unreasonable effort and expense, the aggregate market value of the common stock held by non-affiliates may be calculated on the basis of assumptions reasonable under the circumstances, provided that the assumptions are set forth in this Form.

As of June 30, 2017, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was approximately $67.2 million based on the closing sale price as reported on the TSX Venture Exchange based on the exchange rate of CDN$1.2977 to U.S.$1.00 as published by the Bank of Canada as at June 30, 2017. Our common shares began trading on the NYSE American on November 21, 2017.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

The number of the registrant’s common shares outstanding as of February 27, 2018, was 90,449,869.

| -2- |

TABLE OF CONTENTS

| -3- |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 under Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that are based on management’s beliefs and assumptions and on information currently available to management. Some of the statements under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business” and elsewhere in this Annual Report on Form 10-K contain forward-looking statements. In some cases, you can identify forward-looking statements by the following words: “may,” “will,” “could,” “would,” “should,” “expect,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “project,” “potential,” “continue,” “ongoing” or the negative of these terms or other comparable terminology, although not all forward-looking statements contain these words.

These statements involve risks, uncertainties and other factors that may cause actual results, levels of activity, performance or achievements to be materially different from the information expressed or implied by these forward-looking statements. Although we believe that we have a reasonable basis for each forward-looking statement contained in this prospectus, we caution you that these statements are based on a combination of facts and factors currently known by us and our projections of the future, about which we cannot be certain. Forward-looking statements in this prospectus include, but are not limited to, statements about:

| • | the success, cost and timing of our research and development activities, validation studies and pivotal trials, including with respect to our lead product candidates, ZM-017, ZM-012, ZM-006, ZM-007 and ZM-011; |

| • | our ability to obtain regulatory approval from the FDA-CVM and/or the USDA-CVB for our pharmaceutical and diagnostic product candidates, as applicable; |

| • | our ability to obtain funding for our operations; |

| • | the ability of our CROs to appropriately conduct our safety studies and certain development activities; |

| • | the ability of our CMOs to manufacture and supply our product candidates in accordance with cGMP and our clinical needs; |

| • | our plans to develop and commercialize any product candidates for which we receive regulatory approval; |

| • | our ability to develop and commercialize product candidates that can compete effectively against the product candidates developed and commercialized by our competitors; |

| • | the size and growth of the veterinary diagnostics and therapeutics markets; |

| • | our ability to obtain and maintain intellectual property protection for our current and future product candidates; |

| • | regulatory developments in the United States; |

| • | the loss of key scientific or management personnel; |

| • | our expectations regarding the period during which we will be an “emerging growth company” under the JOBS Act; |

| • | the accuracy of our estimates regarding expenses, future revenues, capital requirements and needs for additional financing; and |

| • | our status as a PFIC for U.S. federal income tax purposes. |

In addition, you should refer to the “Risk Factors” section of this Annual Report on Form 10-K for a discussion of other important factors that may cause actual results to differ materially from those expressed or implied by these forward-looking statements. As a result of these factors, we cannot assure you that the forward-looking statements in this Annual Report on Form 10-K will prove to be accurate. Furthermore, if the forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified time frame, or at all. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

| -4- |

| Item 1. | Business. |

BUSINESS

Overview

We are a development stage veterinary diagnostic and pharmaceutical company creating products for companion animals (canine, feline, and equine) by focusing on the unmet needs of clinical veterinarians. We believe that we have identified and are developing diagnostics and therapeutics that have the potential to significantly improve the diagnosis and treatment of various diseases affecting companion animals. We believe that there are significant unmet medical needs for pets, and that the pet diagnostic and therapeutic segments of the animal health industry are likely to grow substantially as new diagnostic tools and treatments are identified, developed, and marketed specifically for companion animals.

Together with our strategic partner, we are developing liquid biopsy assays and related consumables for the detection of cancer in companion animals. The regulatory pathway to obtain pre-market regulatory approval of companion animal diagnostics is significantly shorter than for similar diagnostic products intended for human use. In certain cases, pre-market regulatory approval may be unnecessary, depending on the intended use of the diagnostic.

We also have identified a number of drugs that have proven safe and effective in humans that we are developing for use in companion animals. We believe this development approach enables us to reduce the risks associated with obtaining regulatory approval for unproven product candidates and shortens the development timeline necessary to bring our product candidates to market. We have four drug product candidates in early development and have identified several other potential product candidates for further investigation.

In addition, we are investigating the development of alternative drug delivery technologies for our drug product candidates. Many of the human-approved therapeutics used in companion animals are only available in pill or injectable form. However, it can be difficult to give a companion animal an injection or to assure that the animal has swallowed a pill. As a result, we believe that compliance with treatment regimens is a significant problem for veterinarians and pet owners. The challenges associated with medicating pets are unique, and we believe that developing product candidates that can be easily taken by the pet or easily administered by pet owners will help increase compliance.

Market Opportunity

U.S. consumers spent an estimated $69.4 billion on their pets in 2017, according to the American Pet Products Association, or APPA, an increase of 4% from 2016. The veterinary care segment has been among the fastest growing segments of the overall U.S. pet market. This segment accounted for an estimated $16.6 billion in revenue in 2017, an increase of 4% from 2016. According to dvm360 Magazine’s State of the Profession survey for 2015, diagnostics comprise 18%, and vaccinations, pharmaceuticals and biologicals comprise 25% of gross revenue at the veterinary practice level.

The dvm360 Magazine survey also states that 61% of respondents indicated that they were providing more diagnostic services than the prior year. Similarly, a 2016 Credit Suisse survey of veterinarians found that 73% of respondents expected their diagnostic testing to increase over the next 12 months. According to MarketsandMarkets™, the veterinary diagnostics market is expected to grow at a CAGR of 9.3% between 2017 and 2022, reaching $3.62 billion in sales by 2022, with North America accounting for the largest market share in 2016. The companion animal segment is expected to register the highest growth during the forecast period.

Packaged Facts’ Pet Medications, in its U.S. report for 2017, estimated the size of the U.S. pet medication market, the largest companion animal market worldwide, at $8.6 billion in 2017, up from $7 billion in 2015. Future Market Insights estimates that the global companion animal drug market is expected to grow at a compounded annual growth rate of 4.9% from 2015 - 2025.

We believe that several factors have contributed and will continue to contribute to an increase in spending on pet therapeutics. Companion animals are generally living longer, with the average lifespan for dogs increasing by half a year to 11 years between 2002 and 2012, according to a study by Banfield Pet Hospital. As a result, companion animals increasingly require medical treatment. In 2015, the American Animal Hospital Association estimated that the average dog will account for approximately $3,600 in veterinary bills over its lifespan. According to Pet Supplies Plus, baby boomers are adopting pets in record numbers. In its December 2015 issue, Pet Business magazine predicted that the millennial generation would continue the trend of the baby boomers in their enthusiasm for and interest in their pets and pet products and services. This, we believe, along with the increasing awareness of, as the U.S. Public Health Service states, “the mental and emotional benefits of companion animals” and our use of companion animals to address or assist in a range of health and wellness issues including post-traumatic stress disorder and autism, will bolster the growth and development of the pet therapeutics market.

| -5- |

Pet owners in the United States generally pay for diagnostics and therapeutics for their companion animals out-of-pocket. According to statistics from the North American Pet Health Insurance Association, only about 1.8 million dogs and cats were covered by an insurance plan in 2016. This represents less than 1% of the nearly 184 million dogs and cats that the American Pet Products Association estimates are owned in the United States. We believe that this results in less pricing pressure than in human health care, although the limited adoption of insurance may also reduce pet owners ability to pay for diagnostics and therapeutics recommended by their veterinarians.

Development of Companion Animal Diagnostics

The development of companion animal diagnostics continues to evolve with the addition of new technologies to diagnostic portfolios. We believe that these new technologies may allow for the following:

| · | Enhanced capability to detect the frequency of occurrence and severity of diseases and conditions that impact companion animals; |

| · | Increased accuracy, lower cost and faster means to obtain test results; |

| · | Wider availability of new diagnostic tools; and |

| · | Enhanced economic benefits for veterinarians. |

Compared to human diagnostic development, the development of companion animal diagnostics is generally faster and less expensive since it typically requires smaller clinical studies, with fewer subjects. We believe that the lower cost of developing companion animal diagnostics enables us to pursue multiple diagnostic candidates simultaneously and to spread the risk of failure across a number of candidates, rather than concentrating all of our resources on one diagnostic candidate that may ultimately fail to achieve regulatory approval or market acceptance.

Development of Companion Animal Therapeutics

Compared to human drug development, the development of companion animal therapeutics is generally faster, more predictable, and less expensive, since it requires fewer clinical studies involving fewer subjects and can be conducted directly in the target species. Based on our progress since commencing business in May 2015, we believe that we will be able to develop a product candidate, from the initial opening of an INAD with the FDA-CVM through to marketing approval, in approximately three to five years at a cost of approximately $3 million to $5 million per product candidate. According to the Tufts Center for the Study of Drug Development, the successful development of a new drug for use in humans can take more than 10 years and requires an average out-of-pocket expenditure of approximately $1.4 billion. The lower cost associated with the development of companion animal therapeutics permits us to pursue multiple product candidates simultaneously and to spread the risk of failure across a number of product candidates, rather than concentrating all of our resources on one novel candidate that may ultimately fail to achieve regulatory approval or market acceptance.

Because we are developing product candidates based on drugs that have been successfully developed and approved for human use—as opposed to drugs based on new active pharmaceutical ingredients (APIs)—we believe that we will be able to avoid or minimize the expenses associated with the human drug development process and more rapidly advance our development programs, while continuing to comply with current good manufacturing practices, or cGMP, for our product candidates. Since we are not pursuing entirely new chemical entities with our drug product candidates, we believe the risk of failure of a specific drug product candidate is significantly lower compared to developing a novel compound.

| -6- |

The respective businesses of developing and commercializing therapeutics for companion animals and humans share a number of characteristics, including the need to:

| · | Demonstrate safety and efficacy in clinical trials; |

| · | Obtain FDA-CVM or other regulatory approval for marketing; |

| · | Manufacture the therapeutics in facilities compliant with cGMP requirements; and |

| · | Market the therapeutics only for their intended indication based on claims permitted in the product label, and not for other uses, which is referred to as “off-label” use. |

However, despite these similarities, there are a number of important differences between the companion animal therapeutics and human therapeutics businesses, including:

| · | Faster, less expensive and more predictable development. The development of therapeutics for companion animals requires fewer clinical studies in fewer subject animals than the development of human therapeutics and, unlike human therapeutics, studies are conducted directly in the target species. We believe that our strategy of selecting APIs with demonstrated efficacy and safety in humans and that are currently being used by veterinarians in their human compounded form enhances the predictability of results and probability of success of our pivotal trials relative to novel compounds that have not been previously validated. |

| · | Role and incentives for veterinary practices. In the United States, veterinarians generally serve the dual role of doctor and pharmacist, and pet owners typically purchase medications directly from their veterinarians. However, veterinarians often are required to have human drugs specially compounded by third-party compounding pharmacies for use in smaller companion animals, resulting in the loss of much of the associated prescription revenue and an increase in the uncertainty around precise dosing and administration. We believe that therapeutics specifically developed for companion animals will enable veterinarians to provide potentially superior treatment options, while also increasing revenue streams from the sale of these therapeutics. |

| · | Less generic competition and strong brand loyalty. There is less generic competition in the companion animal therapeutics industry than in the human health care industry. According to the Generic Animal Drug Alliance, 86% of FDA-approved animal drugs do not have a generic version. We believe that stronger brand loyalty and a lack of the mandatory generic drug substitution that exists in the human pharmaceutical market, partially explains the low penetration of generics in veterinary medicine. |

Unmet Medical Needs

Diagnostics

We believe that there is a significant unmet medical need for cost-effective and accurate disease/condition detection solutions for veterinarians. We believe that we have identified potential diagnostic assays that have the potential to satisfy unmet needs or improve upon existing diagnostic processes frequently used by companion animal veterinarians.

For example, cancer is a prevalent disease in canines that can be difficult and costly to diagnose using existing diagnostic testing. According to the Veterinary Cancer Society, 50% of all dogs over the age of 10 will develop cancer and one in four dogs will develop cancer at some stage in their life. Diagnosing certain cancers in canines is difficult because the location of the tumor may make it difficult or risky to obtain cell material through a biopsy. In addition, the overall health of a canine may increase the risk of performing a biopsy. Other diagnostic technologies, such as advanced imaging, are expensive while others, such as histopathologic examination, may take several days or more to provide a definitive diagnosis. Many more canine cancer cases may go undetected due to cost constraints and other factors. To address these shortcomings, we are developing a circulating tumor cell detection assay for use in the detection of certain cancers in companion animals.

| -7- |

Therapeutics

Despite the growing market for pet therapeutics, there are relatively few treatment options approved for use in companion animals, as compared to those approved for humans. As a result, veterinarians often must resort to prescribing products approved for use in humans, but not approved or formulated for use in companion animals. According to the FDA’s Electronic Animal Drug Product Listing Directory, approximately 54% of the therapeutics used in animals are unapproved for such use. As a result, veterinarians must rely upon trial and error or untested rules of thumb to assess the proper dosage needed to be effective in the particular species without undue risk of side effects. The veterinarian must also find a way to administer the human product to animals and determine the actual dosage amount, tasks which are important and potentially overlooked as practical considerations in the treatment of companion animals. To do this, veterinarians often rely on compounding pharmacies to formulate human drugs into species’ appropriate doses and formulations. As a result, veterinarians are forced to rely on therapeutics not proven safe and effective for their patients and on formulations for which no regulatory approval has been obtained. At the same time, the use of compounding pharmacies results in the veterinary clinic’s loss of much of the associated prescription revenue.

We believe that therapeutics specifically developed for companion animals can extend and improve the quality of the lives of such animals, help veterinarians achieve improved medical outcomes, and make the process of administering therapeutics to companion animals much safer and more convenient. Advances in human medicines have created new therapeutics for managing many chronic diseases. Pets often suffer from many of these same diseases. In many cases, the biology of these diseases in companion animals is very similar to that in humans, which explains why animal efficacy models are used for human drug development. Because of the similarity of the diseases and their symptoms and effects, many human drugs, when formulated properly and administered in proper doses, are effective in companion animals. However, most human drugs are not specially formulated or approved for use in animals.

Many of the human therapeutics used in companion animals are only available in pill or injectable form. However, it can be difficult to give a companion animal a shot or to assure that it has swallowed a pill. It can also be difficult to divide human pills into small enough portions to achieve an appropriate dosage for companion animals. Consequently, we believe that compliance with treatment regimens is a significant problem for veterinarians and pet owners. The challenges associated with medicating pets are unique, and we believe that developing product candidates that can be easily taken by the pet or that can be easily administered by pet owners will help increase compliance.

| -8- |

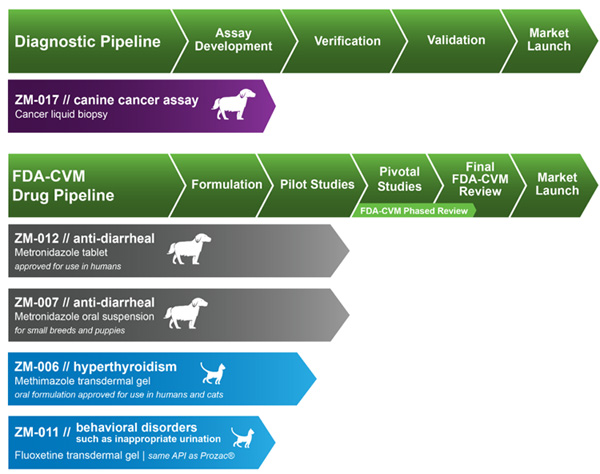

Product Pipeline

Diagnostics

Together with our strategic partner, we are developing a circulating tumor cell, or CTC, assay, also known as a “liquid biopsy,” for use by veterinarians as a cancer diagnostic. The liquid biopsy is a blood test that we believe has the potential to detect the presence of CTCs, which are cells that have shed from a primary tumor into neighboring blood vessels and are transported throughout the body’s circulatory system. Diagnosing certain cancers in canines is difficult because the location of the tumor may make it difficult or risky to obtain cell material through a biopsy. In addition, the overall health of a canine may increase the risk of performing a biopsy. Other diagnostic technologies, such as advanced imaging, are expensive while others, such as histopathologic examination, may take several days or more to provide a definitive diagnosis. We believe that the detection of CTCs in the blood could provide strong clinical support for a cancer diagnosis without the need for an invasive tissue biopsy or other expensive or time-consuming diagnostic test. We intend to develop and market ZM-017, a liquid biopsy for the detection of certain cancers in canines. If we successfully develop ZM-017, we expect that ZM-017 will provide veterinarians with a faster, more affordable, and less invasive test for certain cancers in canines compared to existing detection methods.

We expect to commence clinical validation of ZM-017 in the first half of 2018. Assuming that we successfully complete that clinical validation, we expect to commence the marketing of ZM-017 during the second half of 2018.

Therapeutics

We have four drug product candidates. Our lead drug product candidate is ZM-012, a novel tablet formulation of metronidazole targeting the treatment of acute diarrhea in dogs. An Investigational New Animal Drug, or INAD, was opened for ZM-012 with the Food and Drug Administration’s Center for Veterinary Medicine, or FDA-CVM, in April 2016. The API in ZM-012 is metronidazole, which has been the subject of multiple studies in humans and has been approved for use in humans for decades. We do not believe that the API in ZM-012 is protected by any patents or other proprietary rights of third parties in the U.S. We have finalized the formulation of ZM-012 as a beef-flavored oral tablet intended for dogs greater than nine pounds or four kilograms and we completed pilot testing of ZM-012 in the fourth quarter of 2017. In December 2017, we had a pre-submission meeting with the FDA-CVM to present the regulatory strategy and development plan for ZM-012. Based on the feedback we received from the FDA-CVM, we are making certain changes to the development plan for ZM-012 which we believe will not delay its development. We expect to commence a pivotal safety study of ZM-012 in the first half of 2018, which we expect to complete in the second half of 2018.

| -9- |

Our second drug product candidate is ZM-007, an oral suspension formulation of metronidazole and a complementary formulation to ZM-012, targeting the treatment of acute diarrhea in small dog breeds and puppies under nine pounds or four kilograms. An INAD was opened for ZM-007 with the FDA-CVM in October 2016. We have finalized the formulation and completed pilot testing of ZM-012. We expect to hold a pre-submission meeting in the first half of 2018 with the FDA-CVM specific to the product development strategy for ZM-007 as a bioequivalent to ZM-012. Drugs that are considered to be bioequivalent are, for regulatory purposes, essentially the same, meaning the absence of significant difference between the extent and rate of absorption over the course of a specific period of time at the same dose and under the same conditions. If deemed acceptable by the FDA-CVM, the implementation of this bioequivalent strategy is contingent on FDA-CVM approval of the new animal drug application (NADA) for ZM-012. If the FDA-CVM permits us to rely on the bioequivalence of ZM-007 to ZM-012, we anticipate that this regulatory pathway will conserve significant development costs because a bioequivalence study could replace the need for pivotal safety and efficacy studies for ZM-007.

Our third drug product candidate is ZM-006, a transdermal gel formulation of methimazole targeting hyperthyroidism in cats. Hyperthyroidism is one of the most commonly diagnosed endocrine disorders in middle-aged to older cats according to the American Association of Feline Practitioners. We are investigating ZM-006 pursuant to an INAD opened with the FDA-CVM in June 2016. The API in ZM-006, methimazole, has been the subject of multiple studies in humans and has been approved for oral use in humans for decades. Our transdermal gel formulation is intended to provide an alternative to an oral tablet formulation already approved by the FDA-CVM for cats. We do not believe that the API in ZM-006 is protected by any patents or other proprietary rights of third parties. ZM-006 is intended for application to the cat’s ear using an applicator pen. The formulation of ZM-006 has been completed. We expect to complete pilot testing of ZM-006 in the first half of 2018, and assuming that such pilot testing is successful, we intend to commence and complete a pivotal safety study of ZM-006 in the second half of 2018.

Our fourth drug product candidate is ZM-011, a transdermal gel formulation of fluoxetine, most commonly known as Prozac®, its human pharmaceutical brand name. Fluoxetine in pill or compounded form is frequently prescribed by veterinarians to treat feline behavioral disorders such as inappropriate urination. We are investigating ZM-011 pursuant to an INAD opened with the FDA-CVM in January 2017. The API, fluoxetine, has been the subject of multiple studies in humans and has been approved for use in humans for decades. We do not believe that the API in ZM-011 is protected by any patents or other proprietary rights of third parties. ZM-011 is a transdermal gel formulation intended for application to the cat’s ear using an applicator pen. The formulation of ZM-011 has been completed. We expect to complete pilot testing of ZM-011 in the second half of 2018.

License Agreements

In January 2017, we entered into a collaborative research agreement with Celsee, Inc., or Celsee, a developer of diagnostics for the detection and quantification of cells and other markers. Subsequent to this agreement, in December 2017, we entered into a license and supply agreement with Celsee for exclusive global rights to develop and market Celsee’s liquid biopsy platform. The agreement with Celsee covers the development and commercialization of liquid biopsy assays and related consumables for the detection of cancer in companion animals. We will be responsible for the clinical development and commercialization of the assays. Celsee will supply us on an exclusive basis with the assays and the consumables for the products to be developed under the agreement pursuant to a rolling forecast to be provided by us at prices specified in the agreement. We will be responsible for the marketing and sale of the assays and the related consumables. The agreement, which is exclusive in the field of veterinary cancer diagnostic applications, has a term of seven years (subject to termination in certain circumstances) and automatically renews for additional one-year terms thereafter.

| -10- |

We have agreed to pay Celsee up-front fees of $500,000 and to issue to Celsee unregistered common shares having a value of $250,000, consisting of an aggregate of 112,314 common shares to be issued at an ascribed price of $2.2259. Celsee is entitled to additional payments totaling up to an additional $1 million, payable 50 percent in cash and 50 percent in additional unregistered common shares, upon the achievement of specified milestones—namely, completion of product development (in respect of 50 percent of the foregoing cash and share payments) and upon successful completion of manufacturing milestones (as to the remaining 50 percent of the foregoing cash and share payments). Future issuances of shares will be subject to TSX-V approval and will be priced relative to market at the time of issuance. Celsee is entitled to certain registration rights with respect to the common shares issued by us under the agreement.

In April 2016, we entered into a collaboration agreement with CTX Technology, Inc., or CTX, which has developed a peptide-based skin penetration platform technology for the topical delivery of a range of APIs. Under this agreement, we have an option to obtain an exclusive worldwide license to use CTX’s technology platform in animals. In the event that we exercise the option, we would be required to pay CTX a one-time license fee of $20,000 and to pay CTX a royalty in the low single digits on any products that we sell that incorporates their technology. Unless we exercise our option prior thereto, this agreement will terminate on March 1, 2019.

Research and Development

Together with our strategic partner, we are performing development work on a liquid biopsy diagnostic platform for potential use in companion animals. Our drug product candidate development programs focus on the development of product candidates for target indications that have already demonstrated safety and efficacy in humans and the development of therapeutics based on these drugs for appropriate target indications in companion animals. In addition, we are investigating the development of alternative drug delivery systems for our drug product candidates. We use various contract research organizations, or CROs, to assist in performing our research and development activities.

In connection with these activities, we have incurred and will continue to incur significant research and development expenses. Our research and development expenses were $2,751,326 for the year ended December 31, 2017 and $1,518,589 for the year ended December 31, 2016.

Sales and Marketing

We intend to commercialize any product candidate for which we receive regulatory approval in the United States with a direct sales force. We intend to sell products directly to veterinarians, who typically mark up the diagnostics and therapeutics that they prescribe for pet owners. We believe that veterinarians are self-motivated to prescribe innovative therapeutics that are safe, effective, and supported by reliable clinical data and regulatory approval in order to improve the health of companion animals, while also generating additional revenue.

We will focus on marketing directly to both reference labs and the end user, veterinarians. It is common utility for veterinarians to send diagnostic samples to reference labs for analysis. Our strategic plan will be to sell the ZM-017 diagnostic equipment to a reference lab(s), while driving utilization of the test with the end user, veterinary community/market, back to the lab.

We also intend to selectively utilize distributors, which we believe will enable us to expand our commercial reach to a majority of all veterinarians in our chosen markets. We believe that we can compete effectively with a combination of our own direct sales force and complementary distributors.

To support our marketing efforts, we introduced a unique “Voice of the Vet™” program in the fourth quarter of 2016 to gather insights and better understand the needs of veterinarians and their practices, and to gauge interest for potential future product offerings, while building brand awareness as a valued veterinary partner. Our Voice of the Vet™ program allows veterinarians, practice managers and veterinary technicians to participate in conversations where they can share ideas and experiences with each other, as well as with us through an interactive platform. As part of our commercialization strategy, we also plan to participate in large veterinary meetings and to establish partnerships with leading veterinary colleges.

| -11- |

Manufacturing

We have no internal manufacturing capabilities for our diagnostic and therapeutic product candidates.

Under our license and supply agreement, Celsee is responsible for the manufacture and supply of the CTC platform technology and consumables to us. Celsee has primary responsibility for assuring that all products will be manufactured in accordance with applicable laws and meet all agreed upon specifications.

To ensure a dependable and high quality supply of the APIs for our pilot studies and pivotal trials, we rely on cGMP-compliant contract manufacturers. Because the APIs in our drug product candidates are used in human drugs that are no longer subject to patent protection, we believe that there are multiple contract manufacturers for our drug product candidates that have demonstrated the ability to provide high-quality formulated products more cost effectively than we could on our own. We believe that the contract manufacturers of our trial supplies will be able to provide commercial supplies of any of our drug product candidates that are approved for marketing.

While we and our contract manufacturers have historically been able to obtain supplies of the APIs for development of our drug product candidates, neither we nor our contract manufacturers have long-term supply agreements with the API manufacturers. We also have no agreements for commercial-scale supply of the API or manufacture of any of our drug product candidates.

Intellectual Property

We intend to rely primarily upon a combination of in-licensing exclusive rights, regulatory exclusivity, proprietary know-how, and confidentiality agreements to protect our diagnostic assays, product formulations, processes, methods and other technologies and to preserve any trade secrets and operate without infringing on the proprietary rights of other parties, both in the United States and in other countries. We currently have no issued patents.

Because our drug product candidates are based on approved human drugs that no longer are subject to patent protection, there is little, if any, composition-of-matter patent protection available for the API in these product candidates. Where feasible, however, we intend to pursue the broadest intellectual property protection possible for our compounds and any proprietary technology through enhanced formulations of our drug product candidates. However, even intellectual property protection, if available, may not afford us with complete protection against competitors.

We depend upon the skills, knowledge and experience of our management personnel, as well as that of our other employees, advisors, consultants and contractors, none of which are patentable. To help protect our know-how, and any inventions for which patents may be difficult to obtain or enforce, we require all of our employees, consultants, advisors and other contractors to enter into customary confidentiality and inventions agreements that prohibit the disclosure of confidential information and, where applicable, require disclosure and assignment to us of the ideas, developments, discoveries and inventions important to our business.

Competition

Diagnostics

Our potential competitors include large human pharmaceutical and medical diagnostics companies, small businesses focused on animal health, and reference laboratory services provided by academic institutions and in-clinic product providers. These competitors include Idexx Laboratories, Inc., Antech Diagnostics, a unit of VCA Inc., Abaxis, Inc., Heska Corporation and Zoetis Inc.

| -12- |

Therapeutics

If our drug product candidate is the first one approved by the FDA-CVM for use in animals, it may be eligible for between three and seven years of regulatory exclusivity in the United States, depending on the type of product and its intended use. However, while there are fewer competitors in the pet therapeutics industry than in the human pharmaceutical industry, the development and commercialization of new animal health medicines is highly competitive, and we expect competition from major pharmaceutical, biotechnology and specialty animal health medicine companies.

Our potential competitors include large animal health companies, which currently derive a significant portion of their revenue from livestock medications. Large animal health companies include Merck Animal Health, the animal health division of Merck & Co., Inc.; Elanco, the animal health division of Eli Lilly and Company; Bayer Animal Health, the animal health division of Bayer AG; Novartis Animal Health, the animal health division of Novartis AG; Boehringer Ingelheim Animal Health, the animal health division of Boehringer Ingelheim GmbH; and Zoetis, Inc., as well as European companies such as Virbac S.A., Vetoquinol S.A., and Dechra Pharmaceuticals PLC. We are also aware of several smaller early stage companies that are developing products for use in the pet therapeutics market, including Kindred Biosciences, Inc., Aratana Therapeutics, Inc., Parnell Pharmaceuticals Holdings Ltd., and Jaguar Animal Health, Inc. Our drug product candidates will also face competition from medicines and products approved for use in humans that are used off-label for pets. Private organizations, academic institutions and government agencies conducting animal health product research are also considered potential competitors.

General

Many of our competitors and potential competitors have substantially more financial, technical, and human resources than we do. Many also have far more experience in the development, manufacture, regulation and worldwide commercialization of animal diagnostics and animal health medicines, including pet therapeutics. We also expect to compete with academic institutions, governmental agencies and private organizations that are conducting research in the fields of animal diagnostics and animal health medicines. If such competing products achieve regulatory approval and commercialization prior to our product candidates, or if our intellectual property protection and efforts to obtain regulatory exclusivity fail to provide us with exclusive marketing rights for some of our products, we may be unable to effectively compete in the markets in which we participate.

Government Regulation

Diagnostic Product Candidates

Our diagnostic product candidates may be subject to regulatory review by the USDA-CVB and/or post-marketing oversight by the USDA-CVB or FDA-CVM. Generally speaking, full diagnostic kits aimed at the detection or diagnosis of an infectious disease in animals, including the materials required for testing along with instructions for use and interpretation of results, used at the point-of-care, including in-office diagnostic tests, may be subject to pre-market regulatory review and approval by the USDA-CVB. The USDA-CVB’s review process for diagnostics is subject to some variability based on the type of diagnostic kit being reviewed, however, the USDA-CVB will generally review the results of specific tests that are required to be conducted in accordance with the USDA-CVB’s testing criteria. These include diagnostic sensitivity/specificity studies, conducted using a large number of samples of U.S. origin, reproducibility/repeatability/suitability studies used to evaluate test kits under field conditions in participating laboratories and ruggedness studies in which manufacturers measure the ruggedness or robustness of the diagnostic test kits based on the capacity of the assay to remain unaffected by small variations in or deviations from the instructions for use (for example, not allowing the samples to reach the designated temperature). Diagnostic products and testing kits that do not claim to detect or diagnose an infectious disease and that are not designed for use at the point-of-care are generally subject only to post-marketing oversight by the FDA-CVM or the USDA-CVB. While the sale of these products does not require premarket approval by the FDA-CVM and does not subject us to the FDA-CVM’s cGMP requirements, these products must not be adulterated, mislabeled or misbranded under the Federal Food, Drug and Cosmetic Act, or the FDC Act, and are subject to post-marketing review.

| -13- |

Drug Product Candidates

The FDA-CVM regulates animal pharmaceuticals under the FDC Act. In order to obtain regulatory approval to market a drug product candidate in the U.S., an applicant must demonstrate that the product candidate is safe, effective and produced by a consistent method of manufacture. Post-approval monitoring of products is required by law, with reports being provided to the FDA-CVM's Surveillance and Compliance group. Reports of product quality defects, adverse events or unexpected results are required in accordance with the law.

Prior to commencing testing of a drug product candidate, an applicant is required to open an INAD with the FDA-CVM. Formulation work and pilot testing occurs once the INAD is opened. This is followed by a pre-submission conference with the FDA-CVM to discuss and agree on a proposed development plan, including the design of pivotal safety and clinical trials that would support approval of a new animal drug application, or NADA.

Early pilot studies may be conducted in laboratory animals to establish clinical endpoints and the dose range for a new drug product candidate. Data on how well the drug is absorbed when dosed by different routes of administration and the relationship of the dose to the effectiveness are studied.

During development, the applicant will usually submit a proposed pivotal trial protocol to the FDA-CVM for review and concurrence prior to conducting the trial. The applicant must gather and submit data on manufacturing, safety and effectiveness to the FDA-CVM for review, which will be conducted according to timelines specified in the Animal Drug User Fee Act, or ADUFA. ADUFA also imposes certain fees including a sponsor fee of $75,150 per year, an application fee of $238,100 per product candidate submission, and certain administrative application and manufacturing fees imposed per product candidate per year based on sales.

The pivotal clinical trial must be conducted with the formulation of the drug product candidate that is intended to be commercialized, and is a multi-site, randomized, controlled study, generally with a placebo control. To reduce bias in the study, individuals doing the assessment are not told whether the subject is in the group receiving the treatment being tested or the placebo group.

Once all data have been submitted and reviewed for each technical section - safety, effectiveness and chemistry, manufacturing and controls, or CMC - the FDA-CVM issues a “technical section complete letter” as each section review is completed, and when all three letters have been issued, the applicant prepares a draft of the Freedom of Information Summary, the proposed labeling, and all other relevant information, and submits these for FDA review. An administrative NADA is a NADA that is submitted after all of the technical sections that fulfill the requirements for the approval of the new drug product candidate have been reviewed by FDA-CVM and FDA-CVM has issued a technical section complete letter for each of those technical sections. Although this process is not required and submission of a non-administrative NADA is also acceptable, we plan to take advantage of the administrative NADA process to obtain a timelier phased review. Because FDA-CVM has already reviewed the individual technical sections before the administrative NADA is filed, FDA-CVM is committed under ADUFA to reviewing and acting on 90% of administrative NADAs within 60 days after submission. The FDA-CVM user fee goal is to review and act on 90% of non-administrative NADAs within 180 days after submission. After approval, we will be required to collect reports of adverse events and submit them on a regular basis to the FDA.

Other Regulatory Considerations

Regulatory rules relating to human food safety, food additives, or drug residues in food will not apply to our product candidates because our product candidates are not intended for use in food animals or food production animals.

| -14- |

Advertising and promotion of animal health products is controlled by regulations in the United States. These rules generally restrict advertising and promotion to those claims and uses that have been reviewed and authorized by the FDA-CVM.

Any drug product candidate, if approved, may eventually face generic competition in the United States. In the United States, a generic animal drug may be approved pursuant to an Abbreviated New Animal Drug Application, or ANADA. Instead of demonstrating the drug’s safety and effectiveness in the target species as required in a NADA, a generic applicant must only show that the proposed generic product is the same as, and bioequivalent to, the approved brand name product. However, if any of our drug product candidates is the first one approved by the FDA-CVM for use in animals, it will be eligible for between three and seven years of regulatory exclusivity in the United States, depending on the type of product and its intended use.

We will be required to conduct post-approval monitoring of any approved product and to submit reports of product quality defects, adverse events or unexpected results, and be subject to regulatory inspection from time to time. Safety, quality, or efficacy concerns can lead to product recalls, withdrawals or suspended or declining sales, as well as product liability and other claims.

Employees

As of December 31, 2017, we had 20 employees, including one employee who is a doctor of veterinary medicine. Of our employees, four are engaged in research and development activities, five are engaged in business development and marketing activities, and eleven are engaged in corporate and administrative activities. None of our employees are represented by labor unions or covered by collective bargaining agreements.

Properties

Our corporate headquarters is located in Ann Arbor, Michigan, where we lease approximately 7,900 square feet pursuant to a lease that expires February 2022. Our research and development laboratory is also located in Ann Arbor, Michigan, where we lease approximately 4,800 square feet pursuant to a lease that expires in August 2018. We have the option to extend that lease for three additional years. We believe that our facilities are sufficient for our existing and expected future needs.

Legal Proceedings

We are not currently a party to any material legal proceedings.

Corporate Information

Zomedica Pharmaceuticals Corp. (formerly, Wise Oakwood Ventures Inc.) was originally incorporated as Wise Oakwood Ventures Inc. on January 7, 2013 under the Business Corporations Act (Alberta). On October 28, 2013, we completed our initial public offering in Canada and became classified as a Capital Pool Company, as defined under the rules of the TSX Venture Exchange, or TSX-V. On April 21, 2016, we changed our name to Zomedica Pharmaceuticals Corp. and consolidated our common shares on a one-for-two and one-half (2½) basis. ZoMedica Pharmaceuticals Inc., or ZoMedica Inc., was incorporated on May 14, 2015 under the Canada Business Corporations Act. On April 21, 2016, we completed a qualifying transaction, or the Qualifying Transaction, under TSX-V Policy 2.4 – Capital Pool Companies, consisting of a three-cornered amalgamation among our company, ZoMedica Inc. and our wholly-owned subsidiary. Under the Qualifying Transaction, ZoMedica Inc. and our subsidiary were amalgamated to form Zomedica Pharmaceuticals Ltd., or Zomedica Ltd. As consideration for the amalgamation, shareholders of ZoMedica Inc. became the owners of 97.6% (non-diluted) of our common shares, and ZoMedica Ltd. became our wholly-owned subsidiary. Subsequent to the Qualifying Transaction, Zomedica Ltd. was vertically amalgamated into our company. We have one wholly-owned subsidiary, Zomedica Pharmaceuticals, Inc., a Delaware company. ZoMedica Inc. entered into the Qualifying Transaction in order to accomplish the following:

| · | Enable its shareholders to own shares in a company that was publicly traded on the TSX-V; |

| · | Expand its shareholder base to include the public shareholders of Wise Oakwood; and |

| · | Obtain access to the cash resources raised by Wise Oakwood in its initial public offering. |

| -15- |

On November 10, 2017, our shares were approved for listing on the NYSE American under the symbol “ZOM”. On November 20, 2017 the U.S. Securities and Exchange Commission declared our registration statement on Form S-1 effective. Our common shares commenced trading on the NYSE American on November 21, 2017.

Our principal executive offices are located at 100 Phoenix Drive, Suite 190, Ann Arbor, MI 48108, and our telephone number is (734) 369-2555. Our website address is www.zomedica.com. The information contained in, or accessible through, our website is not part of the registration statement of which this prospectus forms a part.

| Item 1A. | Risk Factors. |

RISK FACTORS

Risks Related to Our Business

We have a limited operating history, are not profitable and may never become profitable.

We are a development stage veterinary diagnostic and pharmaceutical company creating products for companion animals (canine, feline, and equine) by focusing on the unmet needs of clinical veterinarians. Since the commencement of our business in May 2015, our operations have been primarily limited to the identification of product candidates and research and development of our diagnostic and drug product candidates, ZM-017, a non-invasive diagnostic assay or blood test for the detection of certain cancers in canines, ZM-012 and ZM-007, an anti-diarrheal in pill form and oral suspension respectively that is intended for use in dogs, ZM-006, a transdermal gel treatment for hyperthyroidism, a metabolic disorder, which is intended for use in cats and ZM-011, a transdermal gel treatment for behavioral disorders intended for use in cats. As a result, we have limited historical operations upon which to evaluate our business and prospects and we have not yet demonstrated an ability to obtain approval for any of our product candidates or successfully overcome the risks and uncertainties frequently encountered by companies in emerging fields such as the companion animal pharmaceuticals and health care solutions industry.

We also have not generated any revenue to date, and we expect to continue to incur significant research and development costs and other expenses. Our net loss and comprehensive loss for the years ended December 31, 2017 and December 31, 2016 was $8,065,072 and $5,740,492, respectively. Our accumulated deficit as of December 31, 2017 was $15,626,100. As of December 31, 2017, we had total shareholders' equity of $4,387,085. We expect to continue to incur losses for the foreseeable future, which will increase significantly from historical levels as we expand our product development activities (including conducting required clinical studies and trials), seek necessary approvals for our product candidates, and begin commercialization activities. Even if we succeed in developing and broadly commercializing one or more of our product candidates, we expect to continue to incur losses for the foreseeable future, and we may never become profitable. If we fail to achieve or maintain profitability, then we may be unable to continue our operations at planned levels and be forced to reduce or cease operations.

We will need to raise additional capital to achieve our goals.

We do not have any products approved for sale. Although we believe we do not require pre-market approval from the U.S. Food and Drug Administration’s Center for Veterinary Medicine, or the FDA-CVM, to market and sell ZM-017, the CTC diagnostic assay we are developing, we do not expect to commence marketing of ZM-017 until the second half of 2018.

Until, and unless, we receive approval from the FDA-CVM for our drug product candidates, we cannot market or sell our drug products in the United States and will have no material drug product revenue. Our lead drug product candidates, ZM-012, ZM-007, ZM-006 and ZM-011 are in the formulation, optimization and/or pilot study stage, and we have not yet begun pivotal trials. We anticipate that each of our drug product candidates will require from three to five years of development at a cost of approximately $3 million to $5 million per drug product candidate before we expect to be able to apply for marketing approval in the United States.

We are also seeking to identify potential complementary opportunities in the veterinary diagnostics and therapeutics sectors. We will continue to expend substantial resources for the foreseeable future to develop our existing product candidates and any other product candidates we may develop or acquire. These expenditures will include: costs of identifying additional potential product candidates; costs associated with drug formulation; costs associated with conducting pilot and pivotal trials and clinical studies; costs associated with completing other research and development activities; costs associated with payments to technology licensors and maintaining other intellectual property; costs of obtaining regulatory approvals; costs associated with securing contract manufacturers to meet our commercial manufacturing and supply capabilities; and costs associated with marketing and selling any of our products approved for sale. We also may incur unanticipated costs. Because the outcome of our development activities and commercialization efforts is inherently uncertain, the actual amounts necessary to successfully complete the development and commercialization of our existing or future product candidates may be greater or less than we anticipate.

| -16- |

As a result, we will need to obtain additional capital to fund the development of our business. Except for our $5,000,000 unsecured working capital loan facility, we have no existing agreements or arrangements with respect to any financings, and any such financings may result in dilution to our shareholders, the imposition of debt covenants and repayment obligations or other restrictions that may adversely affect our business or the value of our common shares.

Our future capital requirements depend on many factors, including, but not limited to:

| • | the scope, progress, results and costs of researching and developing our existing or future diagnostics and product candidates; |

| • | the timing of, and the costs involved in, obtaining regulatory approvals for any of our existing or future diagnostics or product candidates; |

| • | the number and characteristics of the diagnostics and/or product candidates we pursue; |

| • | the cost of contract manufacturers to manufacture our existing and future diagnostics and product candidates and any products we successfully commercialize; |

| • | the cost of commercialization activities if any of our existing or future diagnostics and product candidates are approved for sale, including marketing, sales and distribution costs; |

| • | the expenses needed to attract and retain skilled personnel; |

| • | the costs associated with being a public company; |

| • | our ability to establish and maintain strategic collaborations, licensing or other arrangements and the financial terms of such agreements; and |

| • | the costs involved in preparing and filing patent applications, maintaining any successfully obtained patents and protecting and enforcing any such patents. |

Additional funds may not be available when we need them on terms that are acceptable to us, or at all. If adequate funds are not available to us on a timely basis, we may be required to delay, limit, reduce or terminate one or more of our product development programs or any future commercialization efforts.

We are substantially dependent on the success of our lead product candidates, and cannot be certain that any of them will be approved for marketing, to the extent applicable, or successfully commercialized.

We have no products approved for sale in any jurisdiction and are focused primarily on the development of our lead diagnostic and drug product candidates, ZM-017, ZM-012, ZM-007, ZM-006 and ZM-011. Accordingly, our near-term prospects, including our ability to generate material product revenue, or enter into potential strategic transactions, will depend heavily on the successful development and commercialization of one or more of our lead candidates, which in turn will depend on a number of factors, including the following:

| • |

the successful completion of clinical validation of our diagnostic product candidate which may take significantly longer than we anticipate and will depend, in part, upon the satisfactory performance of third-party contractors; | |

| • | the successful completion of pilot testing and pivotal efficacy and safety trials of one or more of our drug product candidates, which may take significantly longer than we anticipate and will depend, in part, upon the satisfactory performance of third-party contractors; |

| • | our ability to demonstrate to the satisfaction of the FDA-CVM or the USDA Center for Veterinary Biologics, or USDA-CVB, as applicable, the safety and efficacy of our drug product candidates and to obtain regulatory approvals; |

| • | the ability of our third-party contract manufacturers to manufacture supplies of any of our product candidates and to develop, validate and maintain viable commercial manufacturing processes that are compliant with Good Manufacturing Practices or GMP; |

| • | our ability to successfully market any product candidate for which marketing approval is received, whether alone or in collaboration with others; |

| • | the availability, perceived advantages, relative cost, relative safety and relative efficacy of our product candidates compared to alternative and competing treatments; |

| • | the acceptance of our product candidates as safe and effective by veterinarians, pet owners and the animal health community; |

| -17- |

| • | our ability to achieve and maintain compliance with all regulatory requirements applicable to our business; and |

| • | our ability to obtain and enforce our intellectual property rights and obtain marketing exclusivity for our product candidates, and avoid or prevail in any third-party patent interference, patent infringement claims or administrative patent proceedings initiated by third parties or the United States Patent and Trademark Office (“USPTO”). |

Many of these factors are beyond our control. Accordingly, we cannot assure you that we will be successful in developing or commercializing any of our product candidates. If we are unsuccessful or are significantly delayed in developing and commercializing ZM-017, ZM-012, ZM-007, ZM-006 or ZM-011 or any of our other product candidates, our business and prospects will be materially adversely affected and you may lose all or a portion of your investment.

We face unproven markets for our products candidates.

The companion animal therapeutic and diagnostic markets are less developed than the human therapeutic and diagnostic markets and as a result no assurance can be given that our product candidates will be successful. Veterinarians, pet owners or other veterinary health providers in general may not accept or utilize any products that we may develop.

The companion animal care industry is subject to rapidly changing technology, which could make our product candidates obsolete.

The companion animal care industry is characterized by rapid technological changes, frequent new product introductions and enhancements, and evolving industry standards, all of which could make our product candidates obsolete. Our future success will depend on our ability to keep pace with the evolving needs of our customers on a timely and cost-effective basis and to pursue new market opportunities that develop as a result of technological and scientific advances. We must continuously enhance our product offerings to keep pace with evolving standards of care. If we do not update our product offerings to reflect new scientific knowledge or new standards of care, our product candidates could become obsolete, which would have a material adverse effect on our business, financial condition, and results of operations.

Our ability to successfully develop and commercialize our existing and any future product candidates will depend on several factors, including:

| • | our ability to convince the veterinary community of the clinical utility of our products and their potential advantages over existing tests and therapies; |

| • | the willingness or ability by pet owners to pay for our products and the willingness of veterinarians to recommend our products; |

| • | the willingness of veterinarians to utilize our diagnostic tests; and |

| • | where applicable, the willingness of testing labs to buy our assay equipment. |

Our dependence on suppliers could limit our ability to develop and commercialize certain products

We rely on third-party suppliers to provide components in our product candidates, manufacture products that we do not manufacture ourselves and perform services that we do not provide ourselves. Because these suppliers are independent third parties with their own financial objectives, actions taken by them could have a materially negative effect on our results of operations. The risks of relying on suppliers include our inability to enter into contracts with third-party suppliers on reasonable terms, inconsistent or inadequate quality control, relocation of supplier facilities, supplier work stoppages and suppliers’ failure to comply with applicable regulations or their contractual obligations. Problems with suppliers could materially negatively impact our ability to complete development, supply the market, lead to higher costs or damage our reputation with our customers.

| -18- |

In addition, we currently purchase many products and materials from sole or single sources. Some of the products that we purchase from these sources are proprietary and, therefore, cannot be readily or easily replaced by alternative sources. To mitigate risks associated with sole and single source suppliers, we will seek when possible to enter into long-term contracts that provide for an uninterrupted supply of products at predictable prices. However, some suppliers may decline to enter into long-term contracts and we are required to purchase products with short term contracts or on a purchase order basis. There can be no assurance that suppliers with which we do not have contracts will continue to supply our requirements for products, that suppliers with which we do have contracts will always fulfill their obligations under these contracts, or that any of our suppliers will not experience disruptions in their ability to supply our requirements for products. In cases where we purchase sole and single source products or components under purchase orders, we are more susceptible to unanticipated cost increases or changes in other terms of supply. In addition, under some contracts with suppliers we have minimum purchase obligations, and our failure to satisfy those obligations may result in loss of some or all of our rights under these contracts or require us to compensate the supplier. If we are unable to obtain adequate quantities of products in the future from sole and single source suppliers, we may be unable to supply the market, which could have a material adverse effect on our results of operations.

The commercial potential of our product candidates is difficult to predict. The market for any product candidate, or for companion animal diagnostics and therapeutics overall, is uncertain and may be smaller than we anticipate, which could significantly and negatively impact our revenue, results of operations and financial condition.

We believe that the emerging nature of our industry and our unproven business plan make it difficult to estimate the commercial potential of any of our product candidates. The market for any product that we seek to commercialize will depend on important factors such as the cost, utility and ease of use of our diagnostic assays, the safety and efficacy of our drug candidates compared to other available treatments, including potentially less expensive human pharmaceutical alternatives with similar efficacy profiles, changing standards of care, preferences of veterinarians, the willingness of pet owners to pay for such products, and the availability of competitive alternatives that may emerge either during the product development process or after commercial introduction. If the market potential for our product candidates is less than we anticipate due to one or more of these factors, it could negatively impact our business, financial condition and results of operations. Further, the willingness of pet owners to pay for our product candidates, if approved, may be less than we anticipate, and may be negatively affected by overall economic conditions. Because relatively few pet owners purchase insurance for their companion animals, pet owners are more likely to have to pay for our products directly and may be unwilling or unable to pay for any such products.

All of our drug product candidates are based on APIs already demonstrated safe and effective in humans, and other companies may develop substantially similar products that may compete with our products.

Our lead drug product candidates, ZM-012, ZM-007, ZM-006 and ZM-011 include APIs already demonstrated safe and effective in humans and we expect that our future drug product candidates will be similarly based on such APIs. We do not engage in research or discovery of novel therapeutics, but focus on drug product candidates with APIs that have been successfully commercialized or demonstrated to be safe and effective in humans, which we sometimes refer to as validated. We expect that there will be little, if any, third-party patent protection of the APIs in our drug product candidates. As a result, our drug product candidates may face competition from their human equivalents in situations where such equivalents are available and used in unapproved animal indications, which is known as off-label use. There is no assurance that the eventual prices of our drug products will be lower than or competitive with the prices of the human equivalents used off-label, or that a palatable, easy-to-administer formulation will be sufficient to differentiate them from their human equivalents.

| -19- |

Our product candidates will face significant competition and may be unable to compete effectively.

The development and commercialization of veterinary diagnostics and pharmaceuticals is highly competitive and our success depends on our ability to compete effectively with other products in the market.

There are a number of competitors in the diagnostic market that have substantially greater financial and operational resources and established marketing, sales and service organizations. We expect to compete primarily with commercial clinical laboratories and hospitals’ clinical laboratories. Our principal competitors in the veterinary diagnostic market are Idexx Laboratories, Inc., Antech Diagnostics, a unit of VCA Inc., Abaxis, Inc., Heska Corporation and Zoetis Inc. We must develop our distribution channels and build our direct sales force in order to compete effectively in these markets. If we are unable to effectively manage our distribution channels in our highly competitive industry, we may fail to retain customers or obtain new customers and our business will suffer.

If our drug product candidates are approved, we expect to compete with large animal health companies including Merck Animal Health, the animal health division of Merck & Co., Inc.; Elanco, the animal health division of Eli Lilly and Company; Bayer Animal Health, the animal health division of Bayer AG; Novartis Animal Health, the animal health division of Novartis AG; Boehringer Ingelheim Animal Health, the animal health division of Boehringer Ingelheim GmbH; and Zoetis, Inc., as well as European companies such as Virbac S.A., Vetoquinol S.A., and Dechra Pharmaceuticals PLC We are also aware of several smaller early stage companies that are developing products for use in the pet therapeutics market, including Kindred Biosciences, Inc., Aratana Therapeutics, Inc., Parnell Pharmaceuticals Holdings Ltd., and Jaguar Animal Health, Inc. We also expect to compete with academic institutions, governmental agencies and private organizations that are conducting research in the field of animal health medicines.

We target drug product candidates for which the API, while having been approved for use in human drugs, has not been previously approved for use in animals. If we are the first to gain approval for the use of such API in animals, our drug products will enjoy between three and seven years of marketing exclusivity in the United States for the approved indication. We also plan to differentiate our products where possible with alternative drug delivery systems that are more conducive to dosing for the target companion animal species, but we cannot assure you that we will be able to prevent our competitors from developing substantially similar products and bringing those products to market earlier than we are able to.

Our drug product candidates will face competition from various products approved for use in humans that are used off-label in animals, and all of our products will face potential competition from new products in development. These and other potential competing products may benefit from greater brand recognition and brand loyalty than our drug product candidates may achieve.

Many of our competitors and potential competitors have substantially more financial, technical and human resources than we do. Many also have far more experience than we have in the development, manufacture, regulation and worldwide commercialization of animal health medicines, including pet therapeutics. We also expect to compete with academic institutions, governmental agencies and private organizations that are conducting research in the fields of animal diagnostics and animal health. If such competing products are commercialized prior to our product candidates, or if our intellectual property protection and efforts to obtain regulatory exclusivity fail to provide us with exclusive marketing rights for some of our therapeutic products, we may be unable to compete effectively in the markets in which we participate.

Our ability to develop, manufacture and commercialize our drug product candidates is dependent on our establishing and maintaining relationships with GMP-compliant third party manufacturers.

We have no internal manufacturing capabilities and we do not plan to develop such capabilities. As a result, our ability to manufacture and commercialize our product candidates is substantially dependent on our ability to ensure a dependable and high quality supply of the APIs required for our pilot studies and pivotal trials and for future commercial manufacturing. We currently believe that, because the APIs used in our drug product candidates have been used in human drugs, there are multiple GMP-compliant manufacturers available that will be able to supply these APIs and that the contract manufacturers we currently use for our trial supplies will be able to provide commercial supplies of any of our drug product candidates. While we have historically been able to obtain the necessary supplies of our APIs for our development work, we cannot be certain that either we or our contract manufacturers will continue to be able to provide the necessary API supply. Neither we nor our contract manufacturers have long-term supply contracts with API manufacturers and we have no agreements in place for the commercial-scale supply of any API or the manufacture of any of our drug product candidates. If we are unable to procure the requisite apply of an API or to contract with a GMP-complaint third-party manufacturer, we may be unable to continue to develop, manufacture or commercialize any of our product candidates and our business may fail to grow or develop.

| -20- |

The results of earlier studies may not be predictive of the results of our pivotal trials, and we may be unable to obtain regulatory approval for our existing or future drug product candidates under applicable regulatory requirements or maintain any regulatory approval obtained. The denial, delay or loss of any regulatory approval would prevent or delay our commercialization efforts and adversely affect our financial condition and results of operations.