Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - FOSTER L B CO | ex-3122017.htm |

| EX-32.0 - EXHIBIT 32.0 - FOSTER L B CO | ex-3202017.htm |

| EX-31.1 - EXHIBIT 31.1 - FOSTER L B CO | ex-3112017.htm |

| EX-23 - EXHIBIT 23 - FOSTER L B CO | ex-232017.htm |

| EX-21 - EXHIBIT 21 - FOSTER L B CO | ex-212017.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One) | |

☒ | Annual Report Pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2017 | |

Or

☐ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the transition period from to |

Commission File Number 0-10436

L.B. FOSTER COMPANY

(Exact name of registrant as specified in its charter)

Pennsylvania | 25-1324733 | |

(State of Incorporation) | (I.R.S. Employer Identification No.) | |

415 Holiday Drive, Pittsburgh, Pennsylvania | 15220 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code:

(412) 928-3400

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange On Which Registered | |

Common Stock, Par Value $0.01 | NASDAQ Global Select Market | |

Preferred Stock Purchase Rights | NASDAQ Global Select Market | |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (section 232.405 of this chapter) during the preceding 12 months (or for shorter period that the registrant was required to submit and post such files). ☒ Yes ☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ☐ | Accelerated filer | ☒ | |||

Non-accelerated filer | ☐ (Do not check if a smaller reporting company) | Smaller reporting company | ☐ | |||

Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter was $174,226,746.

Class | Outstanding at February 21, 2018 | |

Common Stock, Par Value $0.01 | 10,346,213 shares | |

Documents Incorporated by Reference:

Portions of the Proxy Statement prepared for the 2017 Annual Meeting of Shareholders are incorporated by reference in Items 10, 11, 12, 13 and 14 of Part III of this Form 10-K. The 2018 Proxy Statement will be filed with the U.S. Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates.

1

TABLE OF CONTENTS

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

Item 16. | ||

2

Forward-Looking Statements

This Annual Report on Form 10-K contains “forward- looking” statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended. Many of the forward-looking statements are located in “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Forward-looking statements provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to any historical or current fact. Sentences containing words such as “believe,” “intend,” “plan,” “may,” “expect,” “should,” “could,” “anticipate,” “estimate,” “predict,” “project,” or their negatives, or other similar expressions of a future or forward-looking nature generally should be considered forward-looking statements. Forward-looking statements in this Annual Report on Form 10-K may concern, among other things, L.B. Foster Company’s (the “Company’s”) expectations relating to our strategy, goals, projections, and plans regarding our financial position, liquidity, capital resources, and results of operations; the outcome of litigation and product warranty claims; decisions regarding our strategic growth initiatives, market position, and product development; all of which are based on current estimates that involve inherent risks and uncertainties. The Company has based these forward-looking statements on current expectations and assumptions about future events. While the Company considers these expectations and assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory, and other risks and uncertainties, most of which are difficult to predict and many of which are beyond the Company’s control. The Company cautions readers that various factors could cause the actual results of the Company to differ materially from those indicated by forward-looking statements. Accordingly, investors should not place undue reliance on forward-looking statements as a prediction of actual results. Among the factors that could cause the actual results to differ materially from those indicated in the forward-looking statements are risks and uncertainties related to: environmental matters, including any costs associated with any remediation and monitoring; a resumption of the economic slowdown we have experienced in previous years in the markets we serve; the risk of doing business in international markets; our ability to effectuate our strategy, including cost reduction initiatives, and our ability to effectively integrate acquired businesses and realize anticipated benefits; costs of and impacts associated with shareholder activism; a decrease in freight or passenger rail traffic; the timeliness and availability of materials from our major suppliers as well as the impact on our access to supplies of customer preferences as to the origin of such supplies, such as customers' concerns about conflict minerals; labor disputes; the continuing effective implementation of an enterprise resource planning system; changes in current accounting estimates and their ultimate outcomes; the adequacy of internal and external sources of funds to meet financing needs, including our ability to negotiate any additional necessary amendments to our credit agreement; the Company’s ability to manage its working capital requirements and indebtedness; domestic and international taxes, including estimates that may impact these amounts, including as a result of any interpretations, regulatory actions, and amendments to the Tax Cuts and Jobs Act; foreign currency fluctuations; inflation; domestic and foreign government regulations; economic conditions and regulatory changes caused by the United Kingdom’s pending exit from the European Union; sustained declines in energy prices; a lack of state or federal funding for new infrastructure projects; an increase in manufacturing or material costs; the ultimate number of concrete ties that will have to be replaced pursuant to the previously disclosed product warranty claim of the Union Pacific Railroad (“UPRR”) and an overall resolution of the related contract claims as well as the possible costs associated with the outcome of the lawsuit filed by the UPRR; the loss of future revenues from current customers; and risks inherent in litigation. Should one or more of these risks or uncertainties materialize, or should the assumptions underlying the forward-looking statements prove incorrect, actual outcomes could vary materially from those indicated. Significant risks and uncertainties that may affect the operations, performance, and results of the Company’s business and forward-looking statements include, but are not limited to, those set forth under Item 1A, “Risk Factors,” and elsewhere in our Annual Report on Form 10-K and our other periodic filings with the Securities and Exchange Commission.

The forward-looking statements in this report are made as of the date of this report and we assume no obligation to update or revise any forward-looking statement, whether as a result of new information, future developments, or otherwise, except as required by the federal securities laws.

3

PART I

(Dollars in thousands, except share data unless otherwise noted)

ITEM 1. BUSINESS

Summary Description of Businesses

Formed in 1902, L.B. Foster Company is a Pennsylvania corporation with its principal office in Pittsburgh, PA. L.B. Foster Company is a leading manufacturer and distributor of products and services for the transportation and energy infrastructure with locations in North America and Europe. As used herein, “Foster,” the “Company,” “we,” “us,” and “our” or similar references refer collectively to L.B. Foster Company and its divisions and subsidiaries, unless the context otherwise requires.

The following table shows, for the last three fiscal years, the net sales generated by each business segment as a percentage of total net sales:

Percentage of Net Sales | |||||||||

2017 | 2016 | 2015 | |||||||

Rail Products and Services | 48 | % | 49 | % | 53 | % | |||

Construction Products | 30 | 30 | 28 | ||||||

Tubular and Energy Services | 22 | 21 | 19 | ||||||

100 | % | 100 | % | 100 | % | ||||

Financial information concerning these segments is set forth in Part II, Item 8, Financial Statements and Supplementary Data, Note 2 Business Segments, to the Consolidated Financial Statements contained in this Annual Report on Form 10-K, which is incorporated by reference into this Item 1.

Rail Products and Services

The Company’s Rail Products and Services (“Rail”) segment is comprised of several manufacturing and distribution businesses that provide a variety of products and services for freight and passenger railroads and industrial companies throughout the world. The Rail segment has sales offices throughout the Americas and Europe, and frequently bids on rail projects where it offers products manufactured by the Company, or sourced from numerous supply chain partners, and aftermarket services. The Rail segment is comprised of the following business units: Rail Products, Rail Technologies, and CXT Concrete Ties.

Rail Products

The Rail Products business is comprised of the Company’s Rail Distribution, Allegheny Rail, and Transit divisions.

Rail Distribution sells new rail mainly to passenger and shortline freight railroads, industrial companies, and rail contractors for the replacement of existing lines or expansion of new lines. Rail accessories sold by the Rail Distribution division include track spikes, bolts, angle bars, and other products required to install or maintain rail lines. These products are manufactured by the Company or purchased from other manufacturers and distributed accordingly. Rail Distribution also sells trackwork products to Class II and III railroads, industrial, and export markets.

The Company’s Allegheny Rail Products (“ARP”) division engineers and fabricates insulated rail joints and related accessories for freight and passenger railroads and industrial customers. Insulated joints are manufactured at the Company’s facilities in Pueblo, CO and Niles, OH.

The Company’s Transit Products division supplies power rail, direct fixation fasteners, coverboards, and special accessories primarily for passenger railroad systems. These products are fabricated at Company facilities or by subcontractors and are usually sold by sealed bid to passenger railroads or to rail contractors.

Rail Technologies

The Company’s Rail Technologies business unit engineers, manufactures, and fabricates friction management products and application systems, railroad condition monitoring systems and equipment, wheel impact load detection, rail anchors and spikes, wayside data collection and management systems, epoxy and nylon-encapsulated insulated rail joints, and track fasteners, and provides aftermarket services. The Company’s friction management products control the friction at the rail/wheel interface, helping our customers reduce fuel consumption, improve operating efficiencies, extend the life of operating assets such as rail and wheels, reduce track stresses, and lower related maintenance and operating costs. Friction management products include mobile and wayside systems that apply lubricants and liquid or solid friction modifiers. These products and systems are designed, engineered, manufactured, and fabricated by certain wholly-owned subsidiaries located in the United States, Canada, United Kingdom, and Germany.

4

CXT Concrete Ties

L.B. Foster’s subsidiary, CXT Incorporated, manufactures engineered concrete railroad ties for freight and passenger railroads and industrial companies at its facility in Spokane, WA.

Construction Products

The Construction products segment is composed of the following business units: Piling Products, Fabricated Bridge Products, and Precast Concrete Products.

Piling Products

Sheet piling products are interlocking structural steel sections that are generally used to provide lateral support at construction sites. Bearing piling products are steel H-beam sections which are driven into the ground for support of structures such as bridge piers and high-rise buildings. Piling is often used in water and land applications including cellular cofferdams and OPEN CELL® structures in inland river systems and ports.

Piling products are sourced from various manufacturers and either sold or rented to project owners and contractors. The piling division, via a sales force deployed throughout the United States, markets and sells piling domestically and internationally. This division offers its customers various types and dimensions of structural beam piling, sheet piling, and pipe piling. The Company is the primary distributor of domestic steel sheet piling for its primary supplier.

Fabricated Bridge Products

The fabricated products facility in Bedford, PA manufactures a number of fabricated steel and aluminum products primarily for the highway, bridge, and transit industries including concrete reinforced steel grid deck, open steel grid deck, aluminum bridge railing, and stay-in-place steel bridge forms.

Precast Concrete Products

The Precast Concrete Products unit primarily manufactures concrete buildings for national, state, and municipal parks. This unit manufactures restrooms, concession stands, and other protective storage buildings available in multiple designs, textures, and colors. The Company is a leading high-end supplier in terms of volume, product options, and capabilities. The unit also manufactures various other precast products such as burial vaults, bridge beams, box culverts, septic tanks, and other custom pre-stressed and precast concrete products. The products are manufactured in Spokane, WA, Hillsboro, TX, and Waverly, WV.

Tubular and Energy Services

The Tubular and Energy Services segment has four primary business units: Protective Coatings, Threaded Products, Precision Measurement Systems, and Test and Inspection Services. The segment provides products and services predominantly to the mid and upstream oil and gas markets.

Protective Coatings

There are two pipeline service locations that make up the Protective Coatings business unit. The Birmingham, AL facility coats the outside diameter and, to a lesser extent, the inside diameter of pipe primarily for oil & gas transmission pipelines. This location partners with its primary customer, a pipe manufacturer, to market fusion bonded epoxy coatings, abrasion resistant coatings, and internal linings for a wide variety of pipe diameters for pipeline projects throughout North America. The second location is in Willis, TX. The Willis facility applies specialty outside and inside diameter coatings for a wide variety of pipe diameters for oil & gas transmission, mining, and waste water pipelines. This location also provides custom coatings for specialty fittings and connections.

Threaded Products

The Company’s Magnolia, TX facility cuts, threads, and paints pipe primarily for water well applications for the agriculture industry, municipal water authorities, and Oil Country Tubular Goods (“OCTG”) markets.

Precision Measurement Systems

The Company manufactures and provides a turnkey solution for metering and injection systems for the oil and, to a lesser extent, gas industry. The Willis, TX location operates a fabrication plant that builds metering systems for custody transfer applications including crude oil and other petroleum-based products. These systems are used at well sites, pipelines, refineries, chemical plants, and loading/unloading facilities. The Willis location also manufactures and installs additive and dye injection systems. These systems are used to inject performance additives and/or dyes into petroleum products.

Test and Inspection Services

The Company provides inspection and tubular integrity management services for the upstream oil and gas industry. Services include non-destructive testing, inspection, and other asset integrity services such as repair and threading for OCTG and drill tools. Inspection and testing of these products, which include replaceable and re-usable products such as casing,

5

production tubing, drill pipe, directional motors, drill collars, and related equipment, is a critical preventative measure to ensure personnel and well-site safety, enhance efficiency, and avoid costly equipment failures and well-site shutdowns. The Company offers these services in every major oil and gas producing region throughout the United States.

L B Pipe Joint Venture

The Company is a member of a joint venture, L B Pipe & Coupling Products, LLC (“L B Pipe JV”), in which it maintains a 45% ownership interest. L B Pipe JV manufactures, markets, and sells various machined components and precision couplings products for the energy, water well, and construction markets and is scheduled to terminate on June 30, 2019. The Company has classified its ownership interest as an asset held for sale during the current period. More information concerning L B Pipe JV is set forth in Part II, Item 8, Financial Statements and Supplementary Data, Note 8 Investments, to the Consolidated Financial Statements included herein, which is incorporated by reference into this Item 1.

Marketing and Competition

L.B. Foster Company generally markets its Rail Products and Services directly in all major industrial areas of the United States, Canada, and Europe. The Construction Products and Tubular and Energy Services are primarily marketed domestically. The Company employs a sales force of approximately 71 people that is supplemented with a network of agents across Europe, South America, and Asia to reach current customers and cultivate potential customers in these areas. For the years ended 2017, 2016, and 2015, approximately 19%, 19%, and 16%, respectively, of the Company’s total sales were outside the United States.

The major markets for the Company’s products are highly competitive. Product availability, quality, service, and price are principal factors of competition within each of these markets. No other company provides the same product mix to the various markets the Company serves. However, there are one or more companies that compete with the Company in each product line. Therefore, the Company faces significant competition from different groups of companies.

During 2017, 2016, and 2015, no single customer accounted for more than 10% of the Company’s consolidated net sales.

Raw Materials and Supplies

Most of the Company’s products are purchased in the form of finished or semi-finished products. The Company purchases the majority of its supplies from domestic and foreign steel producers. Generally, the Company has a number of vendor options. However, the Company has an arrangement with a steel mill to distribute steel sheet piling in North America. Should sheet piling from its present supplier not be available for any reason, the Company risks not being able to provide such product to its customers.

The Company’s purchases from foreign suppliers are subject to foreign currency exchange rate changes as well as the usual risks associated with changes in international conditions and to United States and international laws that could impose import restrictions on selected classes of products and for anti-dumping duties if products are sold in the United States at prices that are below specified prices.

Backlog

The dollar amount of firm, unfilled customer orders at December 31, 2017 and 2016 by business segment is as follows:

December 31, | ||||||||

2017 | 2016 | |||||||

Rail Products and Services | $ | 68,850 | $ | 62,743 | ||||

Construction Products | 71,318 | 71,954 | ||||||

Tubular and Energy Services | 26,737 | 12,759 | ||||||

Total | $ | 166,905 | $ | 147,456 | ||||

Approximately 5% of the December 31, 2017 backlog is related to projects that will extend beyond 2018.

Research and Development

Expenditures for research and development approximated $2,241, $3,511, and $3,937 in 2017, 2016, and 2015, respectively. These expenditures were predominately associated with expanding product lines and capabilities within the Company’s Rail Technologies business.

Patents and Trademarks

The Company owns a number of domestic and international patents and trademarks primarily related to its Rail Technologies products. Our business segments are not dependent upon any individual patent or related group of patents, or any licenses or distribution rights. We believe that, in the aggregate, the rights under our patents, trademarks, and licenses are generally important to our operations, but we do not consider any individual patent or trademark, or any licensing or distribution rights related to a specific process or product, to be of material importance in relation to our total business.

6

Environmental Disclosures

Information regarding environmental matters is included in Part II, Item 8, Financial Statements and Supplementary Data, Note 19 Commitments and Contingent Liabilities, to the Consolidated Financial Statements included herein, which is incorporated by reference into this Item 1.

Employees and Employee Relations

At December 31, 2017, the Company had approximately 1,475 employees, 1,282 located within the Americas and 193 located in Europe. There were 819 hourly production workers and 656 salaried employees. Of the hourly production workers, approximately 146 are represented by unions. The Company has not suffered any major work stoppages during the past five years and considers its relations with its employees to be satisfactory.

Two collective bargaining agreements covering approximately 41 and 77 employees were successfully renegotiated during 2017 and are now scheduled to expire in March 2020 and September 2021, respectively.

Substantially all of the Company’s hourly paid employees are covered by one of the Company’s noncontributory, defined benefit plans or defined contribution plans. Substantially all of the Company’s salaried employees are covered by defined contribution plans.

Financial Information about Liquidity and Capital Resources

Information concerning the Company’s liquidity and capital resources and the Company’s working capital requirements can be found in Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, included herein, which is incorporated by reference into this Item 1.

Financial Information about Geographic Areas

Financial information about geographic areas is set forth in Part II, Item 8, Financial Statements and Supplementary Data, Note 2 Business Segments, to the Consolidated Financial Statements included herein, which is incorporated by reference into this Item 1.

Financial Information about Segments

Financial information about segments is set forth in Part II, Item 8, Financial Statements and Supplementary Data, Note 2 Business Segments, to the Consolidated Financial Statements included herein, which is incorporated by reference into this Item 1.

Code of Ethics

L.B. Foster Company has a legal and ethical conduct policy applicable to all directors and employees, including its Chief Executive Officer, Chief Financial Officer, and Controller. This policy is posted on the Company’s website, www.lbfoster.com. The Company intends to satisfy the disclosure requirement regarding certain amendments to, or waivers from, provisions of its policy by posting such information on the Company’s website. In addition, our ethics hotline can also be used by employees and others for the anonymous communication of concerns about financial controls, human resource concerns, and other reporting matters.

Available Information

The Company makes certain filings with the Securities and Exchange Commission (“SEC”), including its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments and exhibits to those reports, available free of charge through its website, www.lbfoster.com, as soon as reasonably practicable after they are filed with the SEC. These filings are also available at the SEC’s Public Reference Room at 100 F Street N.E. Washington, D.C. 20549 or by calling 1-800-SEC-0330. These filings are also available on the internet at www.sec.gov. The Company’s press releases and recent investor presentations are also available on its website.

7

Executive Officers of the Registrant

Information concerning the executive officers of the Company is set forth below.

Name | Age | Position | ||

Robert P. Bauer | 59 | President and Chief Executive Officer | ||

Patrick J. Guinee | 48 | Vice President, General Counsel and Secretary | ||

John F. Kasel | 52 | Senior Vice President - Rail and Construction | ||

Brian H. Kelly | 58 | Vice President - Human Resources and Administration | ||

Gregory W. Lippard | 49 | Vice President - Rail Sales and Products and Services | ||

James P. Maloney | 50 | Senior Vice President, Chief Financial Officer, and Treasurer | ||

Christopher T. Scanlon | 42 | Controller and Chief Accounting Officer | ||

William F. Treacy | 58 | Vice President - Tubular and Energy Services | ||

Mr. Bauer was elected President and Chief Executive Officer upon joining the Company in 2012. Prior to joining the Company, beginning in 2011, Mr. Bauer previously served as President of the Refrigeration Division of the Climate Technologies business of Emerson Electric Company, a diversified global manufacturing and technology company. From 2002 until 2011, Mr. Bauer served as President of Emerson Network Power’s Liebert Division.

Mr. Guinee was elected Vice President, General Counsel and Secretary in 2014. Prior to joining the Company, Mr. Guinee served as Vice President - Securities & Corporate and Assistant Secretary at Education Management Corporation from 2013 to early 2014, and was employed by H. J. Heinz Company from 1997 to 2013, last serving as Vice President - Corporate Governance & Securities and Assistant Secretary.

Mr. Kasel was elected Senior Vice President - Rail and Construction in September 2017, having previously served as Senior Vice President - Rail Products and Services since 2012, Senior Vice President - Operations and Manufacturing since 2005, and Vice President - Operations and Manufacturing since 2003. Mr. Kasel served as Vice President of Operations for Mammoth, Inc., a Nortek company from 2000 to 2003.

Mr. Kelly was elected Vice President - Human Resources and Administration in 2012, having previously served as Vice President, Human Resources since 2006. Prior to joining the Company, Mr. Kelly headed Human Resources for 84 Lumber Company from 2004. Previously, he served as a Director of Human Resources for American Greetings Corp. from 1994 to 2004.

Mr. Lippard was elected Vice President - Rail Sales and Products and Services in September 2017, having previously served as Vice President - Rail Product Sales since 2000. Prior to re-joining the Company in 2000, Mr. Lippard served as Vice President - International Trading for Tube City, Inc. from 1998. Mr. Lippard served in various other capacities with the Company since his initial employment in 1991.

Mr. Maloney was elected Senior Vice President, Chief Financial Officer, and Treasurer in September 2017. Prior to joining the Company, Mr. Maloney served as Chief Financial Officer of First Insight, Inc. from 2014 to 2017. Mr. Maloney served as Vice President - Global Financial Planning and Supply Chain Finance for H. J. Heinz Company from 2012 to 2014. He served as Director of Finance from 2009 to 2012 and Controller from 2005 to 2009 for Heinz North American operating unit.

Mr. Scanlon was elected Controller and Chief Accounting Officer in 2012. Prior to joining the Company, Mr. Scanlon served as the Online Higher Education Division Controller of Education Management Corporation from 2009 to 2012. Mr. Scanlon served as Manager of Central Accounting Services for Bayer Corporation from 2007 until 2009.

Mr. Treacy was elected Vice President - Tubular and Energy Services in September 2017, having previously served as Director of Technology and General Manager, Transit Products within the Rail Products and Services segment since 2013. Prior to joining the Company, Mr. Treacy served as Interim President of Tuthill Vacuum and Blower Systems from 2012 to 2013. Mr. Treacy previously served as General Manager, Crane Vending Solutions for Crane Co. from 2009 to 2011 and was employed by Parker Hannifin from 2000 to 2009, last serving as Vice President of Operations Development.

Officers are elected annually at the organizational meeting of the Board of Directors following the annual meeting of stockholders.

8

ITEM 1A. RISK FACTORS

Risks and Uncertainties

We operate in a changing environment that involves numerous known and unknown risks and uncertainties that could have a material adverse effect on our business, financial condition, and results of operations. The following risks highlight some of the more significant factors that have affected us and could affect us in the future. We may also be affected by unknown risks or risks that we currently believe are immaterial. If any such events actually occur, our business, financial condition, and results of operations could be materially adversely affected. You should carefully consider the following factors and other information contained in this Annual Report on Form 10-K before deciding to invest in our common stock.

Our inability to successfully manage joint ventures, divestitures, and other significant transactions could harm our financial results, business, and prospects.

As part of our business strategy, we may divest businesses or assets, enter into strategic alliances and joint ventures, and make investments to realize anticipated benefits, which actions involve a number of inherent risks and uncertainties. We can give no assurances that the opportunities will be consummated or that financing will be available. We may not be able to achieve the synergies and other benefits we expect from strategic transactions as successfully or rapidly as projected, if at all.

Our future performance and market value could cause additional write-downs of long-lived and intangible assets in future periods.

We are required under U.S. generally accepted accounting principles to review intangible assets for impairment when events or changes in circumstances indicate that the carrying value may not be recoverable. Goodwill is required to be tested for impairment at least annually. Factors that may be considered to be a change in circumstances indicating that the carrying value of our intangible assets may not be recoverable include, but are not limited to, a decline in stock price and resulting market capitalization, a significant decrease in the market value of an asset, or a significant decrease in operating or cash flow projections. No impairments of goodwill or long-lived assets were recorded in 2017.

During the third quarter of 2015, we performed an interim goodwill test and concluded that the carrying amounts of the Test and Inspection Services and Precision Measurement Systems business units’ goodwill exceeded the implied fair values of that goodwill. We recognized an aggregate non-cash goodwill impairment charge of $80,337 to write down the carrying values to the implied fair values, of which $69,908 represented the full carrying value of the goodwill related to the Test and Inspection Services business unit and the remaining $10,429 related to the Precision Measurement Systems business unit.

During the second and third quarters of 2016, we performed an interim goodwill test and concluded that the carrying amounts of the Rail Technologies, Protective Coatings, and Precision Measurement Systems business units’ goodwill exceeded the implied fair values of the respective goodwill. We recognized an aggregate non-cash goodwill impairment charges of $61,142 to write down the carrying values to the implied fair values, of which $16,560 represented the full carrying value of goodwill related to the 2013 Ball Winch acquisition and $11,873 represented the remaining carrying value related to the Precision Measurement Systems business unit. We also performed interim long-lived asset recoverability tests during the second and third quarters of 2016 and concluded that the long-lived assets related to the Test and Inspection Services and Precision Measurement Systems business units had carrying values in excess of the asset groups’ fair value. We recognized non-cash definite-lived intangible asset impairment charges of $59,786 to write down the carrying values to the implied fair values, of which $42,982 related to Test and Inspection Services and $16,804 related to Precision Measurement Systems. Finally, in 2016, we recognized $14,956 non-cash tangible long-lived impairment charges related to the carrying value of certain long-lived tangible assets exceeding their fair value, all of which related to Test and Inspection Services.

No assurances can be given that we will not be required to record future significant charges related to tangible or intangible asset impairments.

Our indebtedness could materially adversely affect our business, financial condition, and results of operations and prevent us from fulfilling our obligations.

Our indebtedness could materially adversely affect our business, financial condition, and results of operations. For example, it could:

•require us to dedicate a substantial portion of our cash flows to payments of our indebtedness, which would reduce the availability of our cash flow to fund working capital, capital expenditures, expansion efforts, and other general corporate purposes;

•limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate;

•place us at a competitive disadvantage compared to our competitors that have less debt; and

•limit, among other things, our ability to borrow additional funds for working capital, capital expenditures, or general corporate purposes.

9

Our inability to comply with covenants in place or our inability to make the required principal and interest payments may cause an event of default, which could have a substantial adverse impact to our business, financial condition, and results of operations. There is no assurance that refinancings or asset dispositions could be effected on a timely basis or on satisfactory terms, if at all, particularly if credit market conditions deteriorate. Furthermore, there can be no assurance that refinancings or asset dispositions would be permitted by the terms of our credit agreements or debt instruments. Our existing credit agreements contain, and any future debt agreements we may enter into may contain, certain financial tests and other covenants that limit our ability to incur indebtedness, acquire other businesses, and may impose various other restrictions. Our ability to comply with financial tests may be adversely affected by changes in economic or business conditions beyond our control, and these covenants may limit our ability to take advantage of potential business opportunities as they arise. We cannot be certain that we will be able to comply with the financial tests and other covenants, or, if we fail to do so, that we will be able to obtain waivers or amended terms from our lenders. An uncured default with respect to one or more of the covenants could result in the amounts outstanding being declared immediately due and payable, which may also trigger an obligation to redeem our outstanding debt securities and repay all other outstanding indebtedness. Any such acceleration of our indebtedness would have a material adverse effect on our business, financial condition, and results of operations.

Prolonged low energy prices and other unfavorable changes in U.S., global, or regional economic and market conditions could adversely affect our business.

We could be adversely impacted by prolonged negative changes in economic conditions affecting either our suppliers or customers as well as the capital markets. Negative changes in government spending may result in delayed or permanent deferrals of existing or potential projects. No assurances can be given that we will be able to successfully mitigate various prolonged uncertainties including materials cost variability, delayed or reduced customer orders and payments, and access to available capital resources outside of operations.

In addition, volatile market conditions and low energy prices could continue for an extended period, which would negatively affect our business prospects. Historically, oil and natural gas prices have been volatile and are subject to fluctuations in response to changes in supply and demand, market uncertainty, and a variety of additional factors that are beyond our control. Sustained declines or significant and frequent fluctuations in the price of oil and natural gas may have a material adverse effect on our operations and financial condition.

Our ability to maintain or improve our profitability could be adversely impacted by cost pressures.

Our profitability is dependent upon the efficient use of our resources. Rising inflation, labor costs, labor disruptions, and other increases in costs in the geographic areas in which we operate could have a significant adverse impact on our profitability and results of operations.

Management projections, estimates, and judgments may not be indicative of our future performance.

Our management is required to use certain estimates in preparing our financial statements, including accounting estimates to determine reserves related to litigation, deferred tax assets, and the fair market value of certain assets and liabilities. Certain asset and liability valuations are subject to management’s judgment and actual results are influenced by factors outside our control.

We are required to maintain a valuation allowance for deferred tax assets and record a charge to income and equity if we determine, based on available evidence at the time the determination is made, that it is more likely than not that some portion or all of the deferred tax assets will not be realized. This evaluation process involves significant management judgment about assumptions that are subject to change from period to period. The use of different estimates can result in changes in the amounts of deferred tax items recognized, which can result in equity and earnings volatility because such changes are reported in current period earnings. See Part II, Item 8, Financial Statements and Supplementary Data, Note 14 Income Taxes, to the Consolidated Financial Statements included herein, for additional discussion of our deferred taxes.

Our business operates in highly competitive markets and a failure to react to changing market conditions could adversely impact our business.

We face strong competition in each of the markets in which we participate. A slow response to competitor pricing actions and new competitor entries into our product lines could negatively impact our overall pricing. Efforts to improve pricing could negatively impact our sales volume in all product categories. We may be required to invest more heavily to maintain and expand our product offerings. There can be no assurance that new product offerings will be widely accepted in the markets we serve. Significant negative developments in any of these areas could adversely affect our financial results and condition.

10

If we are unable to protect our intellectual property and prevent its improper use by third parties, our ability to compete may be harmed.

We own a number of patents and trademarks under the intellectual property laws of the United States, Canada, Europe, and other countries where product sales are possible. However, we have not perfected patent and trademark protection of our proprietary intellectual property for all products in all countries. The decision not to obtain patent and trademark protection in other countries may result in other companies copying and marketing products that are based upon our proprietary intellectual property. This could impede growth into new markets where we do not have such protections and result in a greater supply of similar products in such markets, which in turn could result in a loss of pricing power and reduced revenue.

Our success is in part dependent on the accuracy and proper utilization of our management information and communications systems.

We are currently working through an enterprise resource program (“ERP”) system transition. Certain divisions of our Company migrated into the new ERP system during 2016 while certain other divisions may be transitioned during 2018 and subsequent years. The system implementation is intended to enable us to better meet the information requirements of our users, increase our integration efficiencies, and identify additional synergies in the future. The implementation of our ERP system is complex because of the wide range of processes and systems to be integrated across our business. Project delays, business interruptions, or loss of expected benefits could have a material adverse effect on our business, financial condition, or results of operations. Any disruptions, delays, or deficiencies in the design, operation, or implementation of our various systems, or in the performance of our systems, particularly any disruptions, delays, or deficiencies that impact our operations, could adversely affect our ability to effectively run and manage our business, including our ability to receive, process, ship, and bill for orders in a timely manner or our ability to properly manage our inventory or accurately present our inventory availability or pricing.

We are subject to cybersecurity risks and may incur increasing costs in an effort to minimize those risks.

Our business employs systems and websites that allow for the storage and transmission of proprietary or confidential information regarding our customers, employees, job applicants, and other parties, including financial information, intellectual property, and personal identification information. Security breaches and other disruptions could compromise our information, expose us to liability, and harm our reputation and business. The steps we take to deter and mitigate these risks may not be successful. We may not have the resources or technical sophistication to anticipate or prevent current or rapidly evolving types of cyber-attacks. Data and security breaches can also occur as a result of non-technical issues, including an intentional or inadvertent breach by our employees or by persons with whom we have commercial relationships. Any compromise or breach of our security could result in a violation of applicable privacy and other laws, legal and financial exposure, negative impacts on our customers’ willingness to transact business with us, and a loss of confidence in our security measures, which could have an adverse effect on our results of operations and our reputation.

We are dependent upon key customers.

We could be adversely affected by changes in the business or financial condition of a customer or customers. A prolonged decrease in capital spending by our railroad customers could negatively impact our sales and profitability. As a result of the ongoing litigation and termination of the amended 2005 concrete tie supply agreement with Union Pacific Railroad (“UPRR”), our CXT Concrete Tie sales to, and new orders from, UPRR have ceased which adversely affected our results beginning in 2015.

No assurances can be given that a significant downturn in the business or financial condition of a current customer, or customers, or potential litigation with a current customer, would not also impact our results of operations and/or financial condition.

An adverse outcome in any pending or future litigation or pending or future warranty claims against the Company or its subsidiaries or our determination that a customer has a substantial product warranty claim could negatively impact our financial results and/or our financial condition.

We are party to various legal proceedings. In addition, from time to time our customers assert claims against us relating to the warranties which apply to products we sell. There is the potential that a result materially adverse to us or our subsidiaries in pending or future legal proceedings or pending or future product warranty claims could materially exceed any accruals we have established and adversely affect our financial results and/or financial condition. In addition, we could suffer a significant loss of business from a customer who is dissatisfied with the resolution of a warranty claim. For example, UPRR terminated our amended 2005 concrete tie supply agreement over allegedly defective ties and reduced new orders for other products which negatively affected our results beginning in 2015.

11

In January 2015, UPRR filed a lawsuit against the Company asserting that we were in material breach of our amended 2005 concrete tie supply agreement with UPRR due to claimed failures to provide warranty ties to replace alleged defective concrete ties. UPRR seeks various types of relief including incidental, consequential, and other damages in amounts to be determined at trial under various legal theories. See Part II, Item 8, Financial Statements and Supplementary Data, Note 19 Commitments and Contingent Liabilities, to the Consolidated Financial Statements included herein, for additional information regarding UPRR’s lawsuit.

We continue to work with UPRR in an attempt to reach a resolution on this matter. However, such discussions may not be successful, and the results of litigation and any settlement or judgment amounts resulting from this matter may not be within the range of our estimated accrual. Consequently, while we believe the claims in the UPRR lawsuit are without merit, and we intend to vigorously defend ourselves and have asserted a counterclaim for damages in the UPRR lawsuit, an adverse outcome could result in a substantial judgment against us that could have a material adverse effect on our financial condition, results of operations, liquidity, and capital resources. No assurances can be given that prior to any settlement or judgment, we will not recognize additional material charges because our warranty reserve accrual for UPRR is based upon our current estimate of the number of defective concrete ties that need to be replaced and facts could emerge which would cause us to materially increase this estimate.

A portion of our sales are derived from our international operations, which expose us to certain risks inherent in doing business on an international level.

Doing business outside the United States subjects the Company to various risks, including changing economic and political conditions, work stoppages, exchange controls, currency fluctuations, armed conflicts, and unexpected changes in United States and foreign laws relating to tariffs, trade restrictions, transportation regulations, foreign investments, and taxation. Increasing sales to foreign countries exposes the Company to increased risk of loss from foreign currency fluctuations and exchange controls as well as longer accounts receivable payment cycles. We have little control over most of these risks and may be unable to anticipate changes in international economic and political conditions and, therefore, unable to alter our business practices in time to avoid the adverse effect of any of these possible changes.

Changes in exchange rates for foreign currencies may reduce international demand for our products or increase our labor or supply costs in non-U.S. markets. Fluctuations in the relative values of the United States dollar, Canadian dollar, British pound, and Euro may result in volatile earnings to reflect exchange rate translation in our Canadian and European sales and operations. If the United States dollar strengthens in value as compared to the value of the Canadian dollar, British pound, or Euro, our reported earnings in dollars from sales in those currencies will be unfavorable. Conversely, a favorable result will be reported if the United States dollar weakens in value as compared to the value of the Canadian dollar, British pound, or Euro.

Economic conditions and regulatory changes caused by the United Kingdom’s pending exit from the European Union could adversely affect our business.

In June 2016, the United Kingdom (“U.K.”) held a referendum in which voters approved an exit from the European Union (“E.U.”), commonly referred to as “Brexit”. The U.K. government has initiated a process to withdraw from the E.U. and has begun negotiating the terms of its separation. Since the announcement of Brexit, there has been volatility in currency exchange rate fluctuations between the U.S. dollar relative to the U.K. pound. The announcement of Brexit and pending withdrawal of the U.K. from the E.U. may also create market volatility and could continue to contribute to instability in global financial and foreign exchange markets, political institutions, and regulatory agencies. The majority of our U.K. operations are heavily concentrated within the U.K. borders; however, this could adversely affect the future growth of our U.K. operations into other European locations. Our U.K. operations represented approximately 10% of our total revenue for the twelve-month periods ended December 31, 2017, 2016, and 2015.

Material modification to NAFTA and certain other international trade agreements could affect our business, financial condition, and results of operations.

The current Presidential administration has made comments suggesting it is not supportive of certain international trade agreements, including the North American Free Trade Agreement (“NAFTA”). At this time, it remains unclear what the current administration and Congress would or would not do with respect to these international trade agreements. While the Company is a net exporter out of the United States, potential material modifications to NAFTA, or certain other international trade agreements, may adversely impact our business, financial condition, and results of operations.

12

Violations of foreign governmental regulations, including the U.S. Foreign Corrupt Practices Act and similar worldwide anti-corruption laws, could result in fines, penalties, and criminal sanctions against the Company, its officers, or both and could adversely affect our business.

Our foreign operations are subject to governmental regulations in the countries in which we operate as well as U.S. laws. These include regulations relating to currency conversion, repatriation of earnings, taxation of our earnings and the earnings of our personnel, and the increasing requirement in some countries to make greater use of local employees and suppliers, including, in some jurisdictions, mandates that provide for greater local participation in the ownership and control of certain local business assets.

The U.S. Foreign Corrupt Practices Act and similar other worldwide anti-corruption laws, such as the U.K. Bribery Act, prohibit improper payments for the purpose of obtaining or retaining business. Although we have established an internal control structure, corporate policies, compliance, and training processes to reduce the risk of violation, we cannot ensure that these procedures protect us from violations of such policies by our employees or agents. Failure to comply with applicable laws or regulations could subject us to fines, penalties, and suspension or debarment from contracting. Events of non-compliance could harm our reputation, reduce our revenues and profits, and subject us to criminal and civil enforcement actions. Violations of such laws or allegations of violation could disrupt our business and result in material adverse results to our operating results or future profitability.

Certain divisions of our business depend on a small number of suppliers. The loss of any such supplier could have a material adverse effect on our business, financial condition, and result of operations.

In our Rail Products businesses, we rely on a limited number of suppliers for key products that we sell to our customers. In addition, our Piling business is predominantly dependent upon one supplier for sheet piling while our Protective Coatings business is predominately dependent on two suppliers of epoxy coating. A significant downturn in the business of one or more of these suppliers, a disruption in their manufacturing operations, an unwillingness to continue to sell to us, or a disruption in the availability of existing and new piling and rail products may adversely impact our financial results.

Fluctuations in the price, quality, and availability of the primary raw materials used in our business could have a material adverse effect on our operations and profitability.

Most of our businesses utilize steel as a significant product component. The steel industry is cyclical and prices and availability are subject to these cycles as well as to international market forces. We also use significant amounts of cement and aggregate in our CXT Concrete Ties and Precast Concrete Products businesses. No assurances can be given that our financial results would not be adversely affected if prices or availability of these materials were to change in a significantly unfavorable manner.

Labor disputes may have a material adverse effect on our operations and profitability.

Four of our manufacturing facilities are staffed by employees represented by labor unions. Approximately 146 employees employed at these facilities are currently working under three separate collective bargaining agreements. Disputes with regard to the terms of these agreements or our potential inability to renegotiate acceptable contracts with these unions could result in, among other things, strikes, work stoppages, slowdowns, or lockouts, which could cause a disruption of our operations and have a material adverse effect on our results of operations, financial condition, and liquidity.

Actions of activist shareholders could be disruptive and potentially costly and the possibility that activist shareholders may seek changes that conflict with our strategic direction could cause uncertainty about the strategic direction of our business.

In February 2016, the Company entered into an agreement with an activist investor, Legion Partners Asset Management, LLC and various of its affiliates (collectively, “Legion Partners”) that had filed a Schedule 13D with the SEC with respect to the Company. Pursuant to that agreement, the Company agreed to appoint a representative of Legion Partners to the Company’s Board of Directors and Legion Partners agreed to various standstill provisions and to vote for the Company’s director nominees at the Company’s 2016 and 2017 Annual Meetings of Shareholders. This agreement expired by its terms on February 13, 2018.

13

Although our agreement with Legion Partners expired by its terms in February 2017, activist investors may attempt to effect changes in the Company’s strategic direction and how the Company is governed, or to acquire control over the Company. Some investors seek to increase short-term shareholder value by advocating corporate actions such as financial restructuring, increased borrowing, special dividends, stock repurchases, or even sales of assets or the entire company. While the Company welcomes varying opinions from all shareholders, activist campaigns that contest or conflict with our strategic direction could have an adverse effect on the Company’s results of operations and financial condition as responding to proxy contests and other actions by activist shareholders can disrupt our operations, be costly and time-consuming, and divert the attention of the Company’s board and senior management from the pursuit of business strategies. In addition, perceived uncertainties as to our future direction as a result of changes to the composition of our Board may lead to the perception of a change in the direction of the business, instability or lack of continuity, which may be exploited by our competitors, may cause concern to our current or potential customers, may result in the loss of potential business opportunities and may make it more difficult to attract and retain qualified personnel and business partners. These types of actions could cause significant fluctuations in our stock price based on temporary or speculative market perceptions or other factors that do not necessarily reflect the underlying fundamentals and prospects of our business.

Our success is highly dependent on the continued service and availability of qualified personnel.

Much of our future success depends on the continued availability and service of key personnel, including our Chief Executive Officer, the executive team, and other highly skilled employees. Changes in demographics, training requirements, and the availability of qualified personnel could negatively affect our ability to compete and lead to a reduction in our profitability.

We may not foresee or be able to control certain events that could adversely affect our business.

Unexpected events including fires or explosions at our facilities, natural disasters, armed conflicts, unplanned outages, equipment failures, failure to meet product specifications, or a disruption in certain of our operations, may cause our operating costs to increase or otherwise impact our financial performance.

Shifting federal, state, local, and foreign regulatory policies impose risks to our operations.

We are subject to regulation by federal, state, local, and foreign regulatory agencies. We are required to comply with numerous laws and regulations and to obtain numerous authorizations, permits, approvals, and certificates from governmental agencies. Compliance with emerging regulatory initiatives, delays, discontinuations, or reversals of existing regulatory policies in the markets in which we operate could have an adverse effect on our business, results of operations, cash flows, and financial condition.

The Tax Cuts and Jobs Act (the “Act”) was enacted on December 22, 2017. The Act reduces the U.S. federal corporate tax rate from 35% to 21%, requires companies to pay a one-time transition tax on previously deferred earnings of certain foreign subsidiaries, and creates new taxes on certain foreign sourced earnings. Our 2017 financial results include a provisional tax expense of $3,298 related to the one-time transition tax, partially offset by a provisional $1,508 tax benefit related to the remeasurement of certain deferred tax assets and liabilities. We will continue to refine our provisional tax amounts during 2018, as we gain a more thorough understanding of the tax law, as further guidance is issued, and as we evaluate our income tax accounting policies with regard to certain provisions of the Act.

A substantial portion of our operations are heavily dependent on governmental funding of infrastructure projects. Many of these projects have “Buy America” or “Buy American” provisions. Significant changes in the level of government funding of these projects could have a favorable or unfavorable impact on our operating results. Additionally, government actions concerning “Buy America” provisions, taxation, tariffs, the environment, or other matters could impact our operating results.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

14

ITEM 2. PROPERTIES

The location and general description of the principal properties which are owned or leased by L.B. Foster Company, together with the segment of the Company’s business using such properties, are set forth in the following table:

Location | Function | Acres | Business Segment | Lease Expiration | ||||

Bedford, PA | Bridge component fabricating plant | 16 | Construction | Owned | ||||

Birmingham, AL | Protective coatings facility | 32 | Tubular and Energy | 2022 | ||||

Burnaby, British Columbia, Canada | Friction management products plant | N/A | Rail | 2021 | ||||

Channelview, TX | Threading, test, and inspection facility | 73 | Tubular and Energy | Owned | ||||

Columbia City, IN | Rail processing facility and yard storage | 22 | Rail | Owned | ||||

Hillsboro, TX | Precast concrete facility | 9 | Construction | Owned | ||||

Kimball, NE | Threading, test, and inspection facility | 145 | Tubular and Energy | Owned | ||||

Leming, TX | Threading, test, and inspection facility | 63 | Tubular and Energy | Owned | ||||

Magnolia, TX | Threading facility and joint venture manufacturing facility | 35 | Tubular and Energy | Owned | ||||

Morgantown, WV | Test and inspection facility | N/A | Tubular and Energy | 2018 | ||||

Niles, OH | Rail fabrication, friction management products, and yard storage | 35 | Rail | Owned | ||||

Petersburg, VA | Piling storage facility | 35 | Construction | Owned | ||||

Pueblo, CO | Rail joint manufacturing facility | 9 | Rail | Owned | ||||

Saint-Jean-sur-Richelieu, Quebec, Canada | Rail anchors and track spikes manufacturing plant | 17 | Rail | Owned | ||||

Sheffield, United Kingdom | Track component and friction management products facility | N/A | Rail | 2019 | ||||

Spokane, WA | CXT concrete tie plant | 13 | Rail | 2018 | ||||

Spokane, WA | Precast concrete facility | 5 | Construction | 2018 | ||||

Waverly, WV | Precast concrete facility | 85 | Construction | Owned | ||||

Willis, TX | Protective coatings facility | 16 | Tubular and Energy | Owned | ||||

Willis, TX | Measurement services facility | 68 | Tubular and Energy | Owned | ||||

Included in the table above are certain facilities leased by the Company for which there is no acreage included in the lease. For these properties a “N/A” has been included in the “Acres” column.

Including the properties listed above, the Company has a total of 17 sales offices, including its headquarters in Pittsburgh, PA and 32 warehouses, plants, and yard facilities located throughout the United States, Canada, and Europe. The Company’s facilities are in good condition and suitable for the Company’s business as currently conducted and as currently planned to be conducted.

ITEM 3. LEGAL PROCEEDINGS

Information regarding the Company’s legal proceedings and other commitments and contingencies is set forth in Part II, Item 8, Financial Statements and Supplementary Data, Note 19 Commitments and Contingent Liabilities, to the Consolidated Financial Statements included herein, which is incorporated by reference into this Item 3.

ITEM 4. MINE SAFETY DISCLOSURES

This item is not applicable to the Company.

15

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

Stock Market Information

(Dollars in thousands, except share data unless otherwise noted)

The Company had 309 common shareholders of record on February 21, 2018. Common stock prices are quoted daily through the NASDAQ Global Select Market quotation service (Symbol: FSTR). The following table sets forth the range of high and low sales prices per share of our common stock for the periods indicated:

2017 | 2016 | |||||||||||||||||||||||

Quarter | High | Low | Dividends | High | Low | Dividends | ||||||||||||||||||

First | $ | 15.86 | $ | 11.80 | $ | — | $ | 18.53 | $ | 8.80 | $ | 0.04 | ||||||||||||

Second | 21.95 | 12.15 | — | 20.77 | 10.12 | 0.04 | ||||||||||||||||||

Third | 23.25 | 17.00 | — | 12.50 | 9.25 | 0.04 | ||||||||||||||||||

Fourth | 27.45 | 21.15 | — | 15.65 | 9.25 | — | ||||||||||||||||||

Dividends

During the fourth quarter 2016, the Board of Directors decided to suspend the Company’s quarterly dividend.

The Company’s November 7, 2016 credit facility permits it to pay dividends and distributions and make redemptions with respect to its stock providing no event of default or potential default (as defined in the facility agreement) has occurred prior to or after giving effect to the dividend, distribution, or redemption. Dividends, distributions, and redemptions are capped at $1,700 per year when funds are drawn on the facility.

16

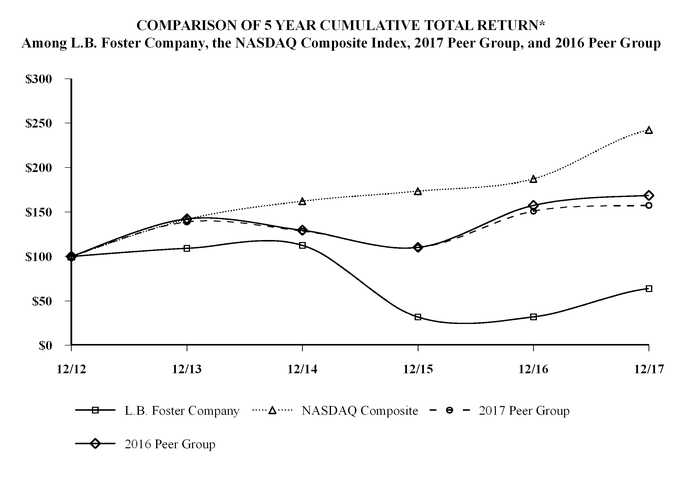

Performance Graph

(In whole dollars)

In 2017, the Company changed its peer group to align it with the Company’s comparator group as used by the Company’s compensation committee to evaluate the Company’s compensation practices. The Company’s 2017 peer group (“2017 Peer Group”) consists of Alamo Group, Inc., American Railcar Industries, Inc., Ampco-Pittsburgh Corporation, CIRCOR International, Inc., Columbus McKinnon Corporation, Gibraltar Industries, Inc., Hawkins, Inc., Haynes International, Inc., Houston Wire & Cable Company, Insteel Industries Inc., Lindsay Corporation, Lydall Inc., Manitex International, Inc., NN Inc., Orion Marine Group, Inc., Quanex Building Products Corporation, Raven Industries Inc., Sterling Construction Co. Inc., and The Gorman-Rupp Company.

Prior to 2017, the Company's peer group (“2016 Peer Group”) consisted of Alamo Group, Inc., AM Castle & Co., American Railcar Industries, Inc., CIRCOR International, Inc., Columbus McKinnon Corporation, Gibraltar Industries, Inc., Houston Wire & Cable Company, Insteel Industries Inc., Lindsay Corporation, Lydall Inc., MYR Group, Inc., NN Inc., Northwest Pipe Co., Olympic Steel Inc., Orion Marine Group, Inc., Quanex Building Products Corporation, Raven Industries Inc., and Sterling Construction Co. Inc.

The following tables compare total shareholder returns for the Company over the last five years to the NASDAQ Composite Index and the peer groups assuming a $100 investment made on December 31, 2012. Each of the four measures of cumulative total return assumes reinvestment of dividends. The stock performance shown on the graph below is not necessarily indicative of future price performance.

* | $100 invested on 12/31/2012 in stock or index, including reinvestment of dividends. Fiscal year ended December 31. |

12/12 | 12/13 | 12/14 | 12/15 | 12/16 | 12/17 | |||||||||||||

L.B. Foster Company | $ | 100.00 | $ | 109.16 | $ | 112.41 | $ | 31.86 | $ | 32.00 | $ | 63.89 | ||||||

NASDAQ Composite | 100.00 | 141.63 | 162.09 | 173.33 | 187.19 | 242.29 | ||||||||||||

2017 Peer Group | 100.00 | 138.84 | 128.55 | 109.99 | 150.91 | 157.39 | ||||||||||||

2016 Peer Group | 100.00 | 142.21 | 129.37 | 110.18 | 157.34 | 168.61 | ||||||||||||

17

Securities Authorized for Issuance Under Equity Compensation Plans

The following table sets forth information at December 31, 2017 with respect to compensation plans under which equity securities of the Company are authorized for issuance.

Plan Category | Number of securities to be issued upon exercise of outstanding options, warrants, and rights (a) | Weighted-average exercise price of outstanding options, warrants, and rights (b) | Number of securities remaining available for future issuance under equity compensation plans (excluding securities to be issued upon exercise of outstanding options, warrants, or rights) (c) | ||||||||

Equity compensation plans approved by shareholders | 429,058 | (1) | $ | — | (2) | 210,332 | (3) | ||||

Equity compensation plans not approved by shareholders | — | — | — | ||||||||

Total | 429,058 | (1) | — | (2) | 210,332 | (3) | |||||

(1) | The number of performance share units included in this table reflects an assumed payout at maximum performance achievement. The performance share units were granted under the 2006 Omnibus Incentive Plan and were unvested and unearned at December 31, 2017. |

(2) | At December 31, 2017, there were no outstanding awards with an exercise price per share. This column does not reflect outstanding performance share units. |

(3) | Does not include the 429,058 performance share units included in column (a). |

Under the 2006 Omnibus Incentive Plan, since May 24, 2006, non-employee directors have been automatically awarded shares of the Company’s common stock as determined by the Board of Directors at each annual shareholder meeting at which such non-employee director is elected or re-elected. During 2017, pursuant to the 2006 Omnibus Incentive Plan, the Company issued approximately 28,000 fully-vested shares of the Company’s common stock for the annual non-employee director equity award. During 2017, the Company issued approximately 11,000 shares to certain non-employee directors who elected the option to receive fully-vested shares of the Company’s common stock in lieu of director cash compensation. Through December 31, 2017, there were 223,920 fully vested shares issued under the 2006 Omnibus Incentive Plan to non-employee directors. During the quarter ended June 30, 2017, the Nomination and Governance Committee and Board of Directors jointly approved the Deferred Compensation Plan for Non-Employee Directors under the 2006 Omnibus Incentive Plan, which permits non-employee directors of the Company to defer receipt of earned cash and/or stock compensation for service on the Board. During 2017, approximately 27,000 deferred share units were allotted to the accounts of non-employee directors pursuant to the Deferred Compensation Plan for Non-Employee Directors.

The Company grants eligible employees restricted stock and performance unit awards under the 2006 Incentive Omnibus Plan. The forfeitable restricted stock awards granted prior to March 2015 generally time-vest after a four-year period, and those granted after March 2015 generally time-vest ratably over a three-year period, unless indicated otherwise in the underlying restricted stock award agreement. Performance unit awards are offered annually under separate three-year long-term incentive programs. Performance units are subject to forfeiture and will be converted into common stock of the Company based upon the Company’s performance relative to performance measures and conversion multiples as defined in the underlying program.

With respect to awards made prior to December 31, 2016, the Company will withhold or employees may tender shares of restricted stock when issued to pay for withholding taxes. Since 2017, the Company will withhold shares of restricted stock for satisfaction of tax withholding obligations. During 2017, 2016, and 2015, the Company withheld 7,277, 20,186, and 25,340 shares, respectively, for this purpose. The values of the shares withheld were $103, $275, and $1,114 in 2017, 2016, and 2015, respectively. Awards made since January 1, 2018 provide that the Company will withhold shares of restricted stock to satisfy tax withholding obligations.

18

Issuer Purchases of Equity Securities

The Company’s purchases of equity securities for the three-month period ended December 31, 2017 were as follows:

Total number of shares purchased (1) | Average price paid per share | Total number of shares purchased as part of publicly announced plans or programs (2) | Approximate dollar value of shares that may yet be purchased under the plans or programs | |||||||||||

October 1, 2017 - October 31, 2017 | — | $ | — | — | $ | 29,933 | ||||||||

November 1, 2017 - November 30, 2017 | — | — | — | 29,933 | ||||||||||

December 1, 2017 - December 31, 2017 | — | — | — | 29,933 | ||||||||||

Total | — | $ | — | — | $ | 29,933 | ||||||||

(1) | Reflects shares withheld by the Company to pay taxes upon vesting of restricted stock. These shares do not impact the remaining authorization to repurchase shares under approved plans or programs. No such shares were withheld during the three-month period ended December 31, 2017. |

(2) | On December 9, 2015, the Board of Directors authorized the repurchase of up to $30,000 of the Company’s common shares until December 31, 2017. This authorization became effective January 1, 2016. The $30,000 repurchase authorization is restricted under the terms of the Second Amendment to the Second Amended and Restated Credit Agreement dated March 13, 2015, and as amended by the Second Amendment dated November 7, 2016 (“Second Amendment”). Dividends, distributions, and redemptions under the Second Amendment are capped at a maximum annual amount of $1,700 throughout the life of the repurchase authorization. For the three-month period ended December 31, 2017, there were no share repurchases as part of the authorized program. At December 31, 2017, approximately $29,933 remained of our $30,000 share repurchase program that was announced December 9, 2015. This repurchase program expired December 31, 2017. |

19

ITEM 6. SELECTED FINANCIAL DATA

(Dollars in thousands, except per share data)

The following selected financial data has been derived from our audited financial statements. The financial data presented below should be read in conjunction with the information contained in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Consolidated Financial Statements of the Company and the Notes thereto included elsewhere in this Annual Report on Form 10-K.

Year Ended December 31, | ||||||||||||||||||||

Income Statement Data | 2017 (a) | 2016 (b) | 2015 (c) | 2014 (d) | 2013 (e) | |||||||||||||||

Net sales | $ | 536,377 | $ | 483,514 | $ | 624,523 | $ | 607,192 | $ | 597,963 | ||||||||||

Operating profit (loss) (f) | $ | 15,739 | $ | (5,195 | ) | $ | 28,760 | $ | 37,082 | $ | 41,571 | |||||||||

Net income (loss) | $ | 4,113 | $ | (141,660 | ) | $ | (44,445 | ) | $ | 25,656 | $ | 29,290 | ||||||||

Basic earnings (loss) per common share | $ | 0.40 | $ | (13.79 | ) | $ | (4.33 | ) | $ | 2.51 | $ | 2.88 | ||||||||

Diluted earnings (loss) per common share | $ | 0.39 | $ | (13.79 | ) | $ | (4.33 | ) | $ | 2.48 | $ | 2.85 | ||||||||

Dividends paid per common share | $ | — | $ | 0.12 | $ | 0.16 | $ | 0.13 | $ | 0.12 | ||||||||||

(a) | 2017 includes provisional tax amounts related to the enactment of the U.S. Tax Cuts and Jobs Act, including additional tax expense of $3,298 related to the one-time transition tax and a $1,508 tax benefit related to the remeasurement of certain deferred tax assets and liabilities. More information about the tax reform can be found in Part II, Item 8, Financial Statements and Supplementary Data, Note 14 Income Tax, to the Consolidated Financial Statements included herein. |

(b) | 2016 includes long-lived tangible and intangible, including goodwill, asset impairments of $135,884. More information about the impairments can be found in Part II, Item 8, Financial Statements and Supplementary Data, Note 4 Goodwill and Other Intangible Assets, and Note 7 Property, Plant, and Equipment, to the Consolidated Financial Statements included herein. |