Attached files

| file | filename |

|---|---|

| EX-32.2 - CERTIFICATION PURSUANT TO SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002 - NEW YORK TIMES CO | ex322_12312017.htm |

| EX-21 - SUBSIDIARIES OF THE COMPANY - NEW YORK TIMES CO | ex21_12312017.htm |

| EX-32.1 - CERTIFICATION PURSUANT TO SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002 - NEW YORK TIMES CO | ex321_12312017.htm |

| EX-31.2 - RULE 13A-14(A)/15D-14(A) CERTIFICATION - NEW YORK TIMES CO | ex312_12312017.htm |

| EX-31.1 - RULE 13A-14(A)/15D-14(A) CERTIFICATION - NEW YORK TIMES CO | ex311_12312017.htm |

| EX-23.1 - CONSENT OF ERNST & YOUNG LLP - NEW YORK TIMES CO | ex231_12312017.htm |

| EX-10.17 - LETTER AGREEMENT - NEW YORK TIMES CO | ex1017_12312017.htm |

| EX-10.16 - LETTER AGREEMENT - NEW YORK TIMES CO | ex1016_12312017.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2017 | Commission file number 1-5837 | |||

THE NEW YORK TIMES COMPANY

(Exact name of registrant as specified in its charter)

New York | 13-1102020 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

620 Eighth Avenue, New York, N.Y. | 10018 | |

(Address of principal executive offices) | (Zip code) | |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Class A Common Stock of $.10 par value | New York Stock Exchange | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | þ | Accelerated filer | ¨ | |

Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |

Emerging growth company | ¨ | |||

If an emerging growth company, indicate by the check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate worldwide market value of Class A Common Stock held by non-affiliates, based on the closing price on June 25, 2017, the last business day of the registrant’s most recently completed second quarter, as reported on the New York Stock Exchange, was approximately $2.7 billion. As of such date, non-affiliates held 66,205 shares of Class B Common Stock. There is no active market for such stock.

The number of outstanding shares of each class of the registrant’s common stock as of February 23, 2018 (exclusive of treasury shares), was as follows: 164,017,902 shares of Class A Common Stock and 803,763 shares of Class B Common Stock.

Documents incorporated by reference

Portions of the Proxy Statement relating to the registrant’s 2018 Annual Meeting of Stockholders, to be held on April 19, 2018, are incorporated by reference into Part III of this report.

INDEX TO THE NEW YORK TIMES COMPANY 2017 ANNUAL REPORT ON FORM 10-K |

ITEM NO. | ||||||

16 | ||||||

PART I |

FORWARD-LOOKING STATEMENTS |

This Annual Report on Form 10-K, including the sections titled “Item 1A — Risk Factors” and “Item 7 —Management’s Discussion and Analysis of Financial Condition and Results of Operations,” contains forward-looking statements that relate to future events or our future financial performance. We may also make written and oral forward-looking statements in our Securities and Exchange Commission (“SEC”) filings and otherwise. We have tried, where possible, to identify such statements by using words such as “believe,” “expect,” “intend,” “estimate,” “anticipate,” “will,” “could,” “project,” “plan” and similar expressions in connection with any discussion of future operating or financial performance. Any forward-looking statements are and will be based upon our then-current expectations, estimates and assumptions regarding future events and are applicable only as of the dates of such statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

By their nature, forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those anticipated in any such statements. You should bear this in mind as you consider forward-looking statements. Factors that we think could, individually or in the aggregate, cause our actual results to differ materially from expected and historical results include those described in “Item 1A — Risk Factors” below, as well as other risks and factors identified from time to time in our SEC filings.

ITEM 1. BUSINESS |

OVERVIEW

The New York Times Company (the “Company”) was incorporated on August 26, 1896, under the laws of the State of New York. The Company and its consolidated subsidiaries are referred to collectively in this Annual Report on Form 10-K as “we,” “our” and “us.”

We are a global media organization focused on creating, collecting and distributing high-quality news and information. Our continued commitment to premium content and journalistic excellence makes The New York Times brand a trusted source of news and information for readers and viewers across various platforms. Recognized widely for the quality of our reporting and content, our publications have been awarded many industry and peer accolades, including 122 Pulitzer Prizes and citations, more than any other news organization.

The Company includes newspapers, print and digital products and investments. We have one reportable segment with businesses that include:

• | our newspaper, The New York Times (“The Times”); |

• | our websites, including NYTimes.com; |

• | our mobile applications, including The Times’s core news applications, as well as interest-specific applications, including our Crossword and Cooking products; and |

• | related businesses, such as The Times news services division; our product review and recommendation website, Wirecutter; our digital archive distribution; NYT Live (our live events business); our digital marketing agencies and other products and services under The Times brand. |

We generate revenues principally from subscriptions and advertising. Subscription revenues consist of revenues from subscriptions to our print and digital products (which include our news products, as well as our Crossword and Cooking products) and single-copy sales of our print newspaper. Advertising revenue is derived from the sale of our advertising products and services on our print and digital platforms. Revenue information for the Company appears under “Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Revenues, operating profit and identifiable assets of our foreign operations are not significant.

During 2017, we continued to make significant investments in our journalism, while taking further steps to position our organization to operate more efficiently in a digital environment. During the year, The Times continued to break stories and produce investigative reports that sparked global conversations on wide-ranging topics. We also launched groundbreaking digital journalism projects and a popular daily news podcast, The Daily, and created

THE NEW YORK TIMES COMPANY – P. 1

special inserts in our print newspaper, including a monthly section dedicated to children. In addition, we continued to create innovative digital advertising solutions across our platforms and expand our creative services offerings.

We believe that the significant growth over the last year in subscriptions to our products demonstrates the success of our “subscription-first” strategy and the willingness of our readers to pay for high-quality journalism. We had approximately 3.6 million subscriptions to our products as of December 31, 2017, more than at any point in our history.

During the year, we exited our joint venture investments in Women in the World, LLC, a live-event conference business, and Donahue Malbaie Inc. (“Malbaie”), a Canadian newsprint company, and we are in the process of exiting our joint venture investment in Madison Paper Industries (“Madison”), a partnership that previously operated a paper mill. These investments were accounted for under the equity method. For additional information on these investments, see “Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 5 of the Notes to the Consolidated Financial Statements.

The Company sold the New England Media Group in 2013 and the results of operations for this business have been presented as discontinued operations for all periods presented. See Note 13 of the Notes to the Consolidated Financial Statements for additional information regarding our discontinued operations.

PRODUCTS

The Company’s principal business consists of distributing content generated by our newsroom through our digital and print platforms. In addition, we distribute selected content on third-party platforms.

Our core news website, NYTimes.com, was launched in 1996. Since 2011, we have charged consumers for content provided on this website and our core news mobile application. Digital subscriptions can be purchased individually or through group corporate or group education subscriptions. Our metered model offers users free access to a set number of articles per month and then charges users for access to content beyond that limit. In addition to subscriptions to our news product, we offer standalone subscriptions to other digital products, namely our Crossword and Cooking products. Certain digital news product subscription packages include complimentary access to our Crossword and Cooking products.

The Times’s print edition, a daily (Mon. - Sat.) and Sunday newspaper in the United States, commenced publication in 1851. The Times also has an international edition that is tailored and edited for global audiences. First published in 2013 and previously called the International New York Times, the international edition succeeded the International Herald Tribune, a leading daily newspaper that commenced publishing in Paris in 1887. Our print newspapers are sold in the United States and around the world through individual home-delivery subscriptions, bulk subscriptions (primarily by schools and hotels) and single-copy sales. All print home-delivery subscribers are entitled to receive unlimited digital access.

SUBSCRIPTIONS AND AUDIENCE

Our content reaches a broad audience through our print, web and mobile platforms. As of December 31, 2017, we had approximately 3.6 million paid subscriptions across 208 countries and territories to our print and digital products.

Paid digital-only subscriptions totaled approximately 2,644,000 as of December 31, 2017, an increase of approximately 42% compared with December 25, 2016. This amount includes standalone paid subscriptions to our Crossword and Cooking products, which totaled approximately 413,000 as of December 31, 2017.

The number of paid digital-only subscriptions also includes estimated group corporate and group education subscriptions (which collectively represent approximately 7% of total paid digital subscriptions to our news products). The number of paid group subscriptions is derived using the value of the relevant contract and a discounted basic subscription rate. The actual number of users who have access to our products through group subscriptions is substantially higher.

In the United States, The Times had the largest daily and Sunday print circulation of all seven-day newspapers for the three-month period ended September 30, 2017, according to data collected by the Alliance for Audited Media (“AAM”), an independent agency that audits circulation of most U.S. newspapers and magazines.

For the fiscal year ended December 31, 2017, The Times’s average print circulation (which includes paid and qualified circulation of the newspaper in print) was approximately 540,000 for weekday (Monday to Friday) and

P. 2 – THE NEW YORK TIMES COMPANY

1,066,000 for Sunday. (Under AAM’s reporting guidance, qualified circulation represents copies available for individual consumers that are either non-paid or paid by someone other than the individual, such as copies delivered to schools and colleges and copies purchased by businesses for free distribution.)

Internationally, average circulation for the international edition of our newspaper (which includes paid circulation of the newspaper in print and electronic replica editions) for the fiscal years ended December 31, 2017, and December 25, 2016, was approximately 173,000 (estimated) and 197,000, respectively. These figures follow the guidance of Office de Justification de la Diffusion, an agency based in Paris and a member of the International Federation of Audit Bureaux of Circulations that audits the circulation of most newspapers and magazines in France. The final 2017 figure will not be available until April 2018.

According to comScore Media Metrix, an online audience measurement service, in 2017, NYTimes.com had a monthly average of approximately 97 million unique visitors in the United States on either desktop/laptop computers or mobile devices. Globally, including the United States, NYTimes.com had a 2017 monthly average of approximately 136 million unique visitors on either desktop/laptop computers or mobile devices, according to internal data estimates.

ADVERTISING

We have a comprehensive portfolio of advertising products and services that we provide across print, web and mobile platforms. Our advertising revenue is divided into three main categories:

Display Advertising

Display advertising is principally from advertisers promoting products, services or brands, such as financial institutions, movie studios, department stores, American and international fashion and technology. In print, column-inch ads are priced according to established rates, with premiums for color and positioning. The Times had the largest market share in 2017 in print advertising revenue among a national newspaper set that consists of USA Today, The Wall Street Journal and The Times, according to MediaRadar, an independent agency that measures advertising sales volume and estimates advertising revenue.

On our web and mobile platforms, display advertising comprises banners, video, rich media and other interactive ads. Display advertising also includes branded content on The Times’s platforms. Branded content is longer form marketing content that is distinct from The Times’s editorial content. In 2017, digital and print display advertising represented approximately 87% of our advertising revenues.

Classified and Other Advertising

Classified advertising includes line ads sold in the major categories of real estate, help wanted, automotive and other. In print, classified advertisers pay on a per-line basis. On our web and mobile platforms, classified advertisers pay on either a per-listing basis for bundled listing packages, or as an add-on to their print ad.

Other advertising primarily includes creative services fees associated with our branded content studio and our digital marketing agencies, including HelloSociety and Fake Love, each of which the Company acquired in 2016; advertising revenue generated by our product review and recommendation website, Wirecutter, which the Company also acquired in 2016; revenues from preprinted advertising, also known as free-standing inserts; revenues generated from branded bags in which our newspapers are delivered; and advertising revenues from our news services business. In 2017, digital and print classified and other advertising represented approximately 13% of our advertising revenues.

Our business is affected in part by seasonal patterns in advertising, with generally higher advertising volume in the fourth quarter due to holiday advertising.

THE NEW YORK TIMES COMPANY – P. 3

COMPETITION

Our print, web and mobile products compete for subscriptions and advertising with other media in their respective markets. Competition for subscription revenue and readership is generally based upon platform, format, content, quality, service, timeliness and price, while competition for advertising is generally based upon audience levels and demographics, advertising rates, service, targeting capabilities and advertising results.

Our print newspaper competes for subscriptions and advertising primarily with national newspapers such as The Wall Street Journal and The Washington Post; newspapers of general circulation in New York City and its suburbs; other daily and weekly newspapers and television stations and networks in markets in which The Times is circulated; and some national news and lifestyle magazines. The international edition of our newspaper competes with international sources of English-language news, including the Financial Times, Time, Bloomberg Business Week and The Economist.

As our industry continues to experience a shift from print to digital media, our products face competition for audience, subscriptions and advertising from a wide variety of digital media, including news and other information websites and mobile applications, news aggregation sites, sites that cover niche content, social media platforms, and other forms of media. In addition, we compete for advertising on digital advertising networks and exchanges and real-time bidding and other programmatic buying channels.

Our websites and mobile applications most directly compete for audience, subscriptions and advertising with other U.S. news and information websites and mobile applications, including The Washington Post, The Wall Street Journal, CNN, Yahoo! News, Buzzfeed, HuffPost, Vox and Vice. We also compete for audience and advertising against customized news feeds and news aggregation websites such as Facebook Newsfeed, Apple News and Google News. Internationally, our websites and mobile applications compete against international online sources of English-language news, including BBC News, CNN, The Guardian, the Financial Times, The Wall Street Journal, The Economist, HuffPost and Reuters.

OTHER BUSINESSES

We derive revenue from other businesses, which primarily include:

• | The Times news services division, which transmits articles, graphics and photographs from The Times and other publications to approximately 1,800 newspapers, magazines and websites in over 100 countries and territories worldwide. It also comprises a number of other businesses that primarily include digital archive distribution, which licenses electronic databases to resellers in the business, professional and library markets; magazine licensing; news digests; book development and rights and permissions; |

• | The Company’s NYT Live business, a platform for our live journalism that convenes thought leaders from business, academia and government at conferences and events to discuss topics ranging from education to sustainability to the luxury business; and |

• | Wirecutter, a product review and recommendation website acquired in October 2016 that serves as a guide to technology gear, home products and other consumer goods. This website generates affiliate referral revenue (revenue generated by offering direct links to merchants in exchange for a portion of the sale price), which we record as other revenues. |

PRINT PRODUCTION AND DISTRIBUTION

The Times is currently printed at our production and distribution facility in College Point, N.Y., as well as under contract at 26 remote print sites across the United States. We also utilize excess printing capacity at our College Point facility for commercial printing. The Times is delivered to newsstands and retail outlets in the New York metropolitan area through a combination of third-party wholesalers and our own drivers. In other markets in the United States and Canada, The Times is delivered through agreements with other newspapers and third-party delivery agents.

The international edition of The Times is printed under contract at 39 sites throughout the world and is sold in over 130 countries and territories. It is distributed through agreements with other newspapers and third-party delivery agents.

P. 4 – THE NEW YORK TIMES COMPANY

RAW MATERIALS

The primary raw materials we use are newsprint and coated paper, which we purchase from a number of North American and European producers. A significant portion of our newsprint is purchased from Resolute Forest Products Inc., a large global manufacturer of paper, market pulp and wood products with which we shared ownership in Malbaie before we sold our interest in the fourth quarter of 2017.

In 2017 and 2016, we used the following types and quantities of paper:

(In metric tons) | 2017 | 2016 | ||||

Newsprint | 90,500 | 97,800 | ||||

Coated and Supercalendared Paper(1) | 16,500 | 19,500 | ||||

(1) The Times uses a mix of coated and supercalendered paper for The New York Times Magazine, and coated paper for T: The New York Times Style Magazine.

EMPLOYEES AND LABOR RELATIONS

We had approximately 3,790 full-time equivalent employees as of December 31, 2017.

As of December 31, 2017, nearly half of our full-time equivalent employees were represented by unions. The following is a list of collective bargaining agreements covering various categories of the Company’s employees and their corresponding expiration dates. As indicated below, one collective bargaining agreement, under which less than 1% of our full-time equivalent employees are covered, will expire within one year and negotiations for a new contract are ongoing. We cannot predict the timing or the outcome of these negotiations.

Employee Category | Expiration Date |

Machinists | March 30, 2018 |

Mailers | March 30, 2019 |

Typographers | March 30, 2020 |

Drivers | March 30, 2020 |

NewsGuild of New York | March 30, 2021 |

Paperhandlers | March 30, 2021 |

Pressmen | March 30, 2021 |

Stereotypers | March 30, 2021 |

AVAILABLE INFORMATION

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments to those reports, and the Proxy Statement for our Annual Meeting of Stockholders are made available, free of charge, on our website at http://www.nytco.com, as soon as reasonably practicable after such reports have been filed with or furnished to the SEC.

THE NEW YORK TIMES COMPANY – P. 5

ITEM 1A. RISK FACTORS |

You should carefully consider the risk factors described below, as well as the other information included in this Annual Report on Form 10-K. Our business, financial condition or results of operations could be materially adversely affected by any or all of these risks, or by other risks or uncertainties not presently known or currently deemed immaterial, that may adversely affect us in the future.

We face significant competition in all aspects of our business.

We operate in a highly competitive environment. We compete for subscription and advertising revenue with both traditional publishers and other content providers. Competition among companies offering online content is intense, and new competitors can quickly emerge. Some of our current and potential competitors may have greater resources than we do, which may allow them to compete more effectively than us.

Our ability to compete effectively depends on many factors both within and beyond our control, including among others:

• | our ability to continue delivering high-quality journalism and content that is interesting and relevant to our audience; |

• | the popularity, usefulness, ease of use, performance and reliability of our digital products compared with those of our competitors; |

• | the engagement of our current users with our print and digital products, and our ability to reach new users; |

• | our ability to develop, maintain and monetize our products; |

• | the pricing of our products; |

• | our marketing and selling efforts, including our ability to differentiate our products from those of our competitors; |

• | our ability to provide marketers with a compelling return on their investments; |

• | our ability to attract, retain, and motivate talented employees, including journalists and product and technology specialists; |

• | our ability to manage and grow our operations in a cost-effective manner; and |

• | our reputation and brand strength relative to those of our competitors. |

Our success depends on our ability to respond and adapt to changes in technology and consumer behavior.

Technology in the media industry continues to evolve rapidly. Advances in technology have led to an increased number of methods for the delivery and consumption of news and other content. These developments are also driving changes in the preferences and expectations of consumers as they seek more control over how they consume content.

Changes in technology and consumer behavior pose a number of challenges that could adversely affect our revenues and competitive position. For example, among others:

• | we may be unable to develop products for mobile devices or other digital platforms that consumers find engaging, that work with a variety of operating systems and networks and that achieve a high level of market acceptance; |

• | we may introduce new products or services, or make changes to existing products and services, that are not favorably received by consumers; |

• | there may be changes in user sentiment about the quality or usefulness of our existing products or concerns related to privacy, security or other factors; |

• | news aggregation websites and customized news feeds may reduce our traffic levels by creating a disincentive for users to visit our websites or use our digital products; |

• | consumers’ increased reliance on mobile devices for the consumption of news and other content may contribute to a decline in engagement with our products; |

P. 6 – THE NEW YORK TIMES COMPANY

• | changes implemented by social media platforms and search engines, including those affecting how content is displayed and/or prioritized, could affect our business; |

• | failure to successfully manage changes in search engine optimization and social media traffic to increase our digital presence and visibility may reduce our traffic levels; |

• | we may be unable to maintain or update our technology infrastructure in a way that meets market and consumer demands; and |

• | the distribution of our content on delivery platforms of third parties may lead to limitations on monetization of our products, the loss of control over distribution of our content and loss of a direct relationship with our audience. |

Responding to these changes may require significant investment. We may be limited in our ability to invest funds and resources in digital products, services or opportunities, and we may incur expense in building, maintaining and evolving our technology infrastructure.

Unless we are able to use new and existing technologies to distinguish our products and services from those of our competitors and develop in a timely manner compelling new products and services that engage users across platforms, our business, financial condition and prospects may be adversely affected.

Our advertising revenues are affected by numerous factors, including economic conditions, market dynamics, audience fragmentation and evolving digital advertising trends.

We derive substantial revenues from the sale of advertising in our products. Advertising spending is sensitive to overall economic conditions, and our advertising revenues could be adversely affected if advertisers respond to weak and uneven economic conditions by reducing their budgets or shifting spending patterns or priorities, or if they are forced to consolidate or cease operations.

In determining whether to buy advertising, our advertisers consider the demand for our products, demographics of our reader base, advertising rates, results observed by advertisers, and alternative advertising options.

Although print advertising revenue continues to represent a majority of our total advertising revenue (57% of our total advertising revenues in 2017), the overall proportion continues to decline. The increased popularity of digital media among consumers, particularly as a source for news and other content, has driven a corresponding shift in demand from print advertising to digital advertising. However, our digital advertising revenue has not replaced, and may not replace in full, print advertising revenue lost as a result of the shift.

The increasing number of digital media options available, including through social networking platforms and news aggregation websites, has expanded consumer choice significantly, resulting in audience fragmentation. Competition from new content providers and platforms, some of which charge lower rates than we do or have greater audience reach and targeting capabilities, and the significant increase in inventory of digital advertising space, have affected and will likely continue to affect our ability to attract and retain advertisers and to maintain or increase our advertising rates. In recent years, large digital platforms, such as Facebook, Google and Amazon, which have greater audience reach and targeting capabilities than we do, have commanded an increased share of the digital display advertising market, and we anticipate that this trend will continue.

The digital advertising market itself continues to undergo significant change. Digital advertising networks and exchanges, real-time bidding and other programmatic buying channels that allow advertisers to buy audiences at scale are playing a more significant role in the advertising marketplace and may cause further downward pricing pressure. New delivery platforms may also lead to a loss of distribution and pricing control and loss of a direct relationship with consumers. In addition, changes in the standards for the delivery of digital advertising could also negatively affect our digital advertising revenues.

Technologies have been developed, and will likely continue to be developed, that enable consumers to circumvent digital advertising on websites and mobile devices. Advertisements blocked by these technologies are treated as not delivered and any revenue we would otherwise receive from the advertiser for that advertisement is lost. Increased adoption of these technologies could adversely affect our advertising revenues, particularly if we are unable to develop effective solutions to mitigate their impact.

THE NEW YORK TIMES COMPANY – P. 7

As the digital advertising market continues to evolve, our ability to compete successfully for advertising budgets will depend on, among other things, our ability to engage and grow digital audiences and prove the value of our advertising and the effectiveness of our platforms to advertisers.

We may experience further downward pressure on our advertising revenue margins.

The character of our digital advertising business continues to change, as demand for newer forms of advertising, such as branded content and other customized advertising, and video advertising, increases. The margin on revenues from some of these newer advertising forms is generally lower than the margin on revenues we generate from our print advertising and traditional digital display advertising. Consequently, we may experience further downward pressure on our advertising revenue margins as a greater percentage of advertising revenues comes from these newer forms.

The inability of the Company to retain and grow our subscriber base could adversely affect our results of operations and business.

Revenue from subscriptions to our print and digital products makes up a majority of our total revenue. Subscription revenue is sensitive to discretionary spending available to subscribers in the markets we serve, as well as economic conditions. To the extent poor economic conditions lead consumers to reduce spending on discretionary activities, our ability to retain current and obtain new subscribers could be hindered, thereby reducing our subscription revenue. In addition, the growth rate of new subscriptions to our news products that are driven by significant news events, such as an election, may not be sustainable.

Print subscriptions have declined over the last several years, primarily due to increased competition from digital media formats (which are often free to users), higher subscription rates and a growing preference among many consumers to receive all or a portion of their news from sources other than a print newspaper. If we are unable to offset continued revenue declines resulting from falling print subscriptions with revenue from home-delivery price increases, our print subscription revenue will be adversely affected.

Subscriptions to content provided on our digital platforms generate substantial revenue for us, and our future growth depends upon our ability to retain and grow our digital subscription base and audience. To do so will require us to evolve our subscription model, address changing consumer demands and developments in technology and improve our digital product offering while continuing to deliver high-quality journalism and content that is interesting and relevant to readers. There is no assurance that we will be able to successfully maintain and increase our digital subscriber base or that we will be able to do so without taking steps such as reducing pricing or incurring subscription acquisition costs that would affect our margin or profitability.

Failure to execute cost-control measures successfully could adversely affect our profitability.

Over the last several years, we have taken steps to reduce operating costs across the Company, and we plan to continue our cost-management efforts. Some of these cost management efforts require significant up-front investment. If we do not achieve expected savings from these efforts, our total operating costs will be greater than anticipated. In addition, if we do not manage cost-management efforts properly, such efforts may affect the quality of our products and therefore our ability to generate future revenues. And to the extent our cost-management efforts result in reductions in staff and employee compensation and benefits, our ability to attract and retain key employees could be adversely affected.

Significant portions of our expenses are fixed costs that neither increase nor decrease proportionately with revenues. In addition, our ability to make short-term adjustments to manage our costs or to make changes to our business strategy may be limited by certain of our collective bargaining agreements. If we are not able to implement further cost-control efforts or reduce our fixed costs sufficiently in response to a decline in our revenues, our results of operations will be adversely affected.

P. 8 – THE NEW YORK TIMES COMPANY

The size and volatility of our pension plan obligations may adversely affect our operations, financial condition and liquidity.

We sponsor several single-employer defined benefit pension plans. Although we have frozen participation and benefits under all but two of these qualified pension plans, and have taken other steps to reduce the size and volatility of our pension plan obligations, our results of operations will be affected by the amount of income or expense we record for, and the contributions we are required to make to, these plans.

We are required to make contributions to our plans to comply with minimum funding requirements imposed by laws governing those plans. As of December 31, 2017, our qualified defined benefit pension plans were underfunded by approximately $69 million. Our obligation to make additional contributions to our plans, and the timing of any such contributions, depends on a number of factors, many of which are beyond our control. These include: legislative changes; assumptions about mortality; and economic conditions, including a low interest rate environment or sustained volatility and disruption in the stock and bond markets, which impact discount rates and returns on plan assets.

As a result of required contributions to our qualified pension plans, we may have less cash available for working capital and other corporate uses, which may have an adverse impact on our results of operations, financial condition and liquidity.

In addition, the Company sponsors several non-qualified pension plans, with unfunded obligations totaling $245 million. Although we have frozen participation and benefits under these plans, and have taken other steps to reduce the size and volatility of our obligations under these plans, a number of factors, including changes in discount rates or mortality tables, may have an adverse impact on our results of operations and financial condition.

Our participation in multiemployer pension plans may subject us to liabilities that could materially adversely affect our results of operations, financial condition and cash flows.

We participate in, and make periodic contributions to, various multiemployer pension plans that cover many of our current and former production and delivery union employees. Our required contributions to these plans could increase because of a shrinking contribution base as a result of the insolvency or withdrawal of other companies that currently contribute to these plans, the inability or failure of withdrawing companies to pay their withdrawal liability, low interest rates, lower than expected returns on pension fund assets or other funding deficiencies. Our withdrawal liability for any multiemployer pension plan will depend on the nature and timing of any triggering event and the extent of that plan’s funding of vested benefits.

If a multiemployer pension plan in which we participate has significant underfunded liabilities, such underfunding will increase the size of our potential withdrawal liability. In addition, under federal pension law, special funding rules apply to multiemployer pension plans that are classified as “endangered,” “critical” or “critical and declining.” If plans in which we participate are in critical status, benefit reductions may apply and/or we could be required to make additional contributions.

We have recorded significant withdrawal liabilities with respect to multiemployer pension plans in which we formerly participated (primarily in connection with the sales of the New England Media Group in 2013 and the Regional Media Group in 2012) and may record additional liabilities in the future. In addition, we have recorded withdrawal liabilities for actual and estimated partial withdrawals from several plans in which we continue to participate. Until demand letters from some of the multiemployer plans’ trustees are received, the exact amount of the withdrawal liability will not be fully known and, as such, a difference from the recorded estimate could have an adverse effect on our results of operations, financial condition and cash flows. Several of the multiemployer plans in which we participate are specific to the newspaper industry, which continues to undergo significant pressure. A withdrawal by a significant percentage of participating employers may result in a mass withdrawal declaration by the trustees of one or more of these plans, which would require us to record additional withdrawal liabilities.

If, in the future, we elect to withdraw from these plans or if we trigger a partial withdrawal due to declines in contribution base units or a partial cessation of our obligation to contribute, additional liabilities would need to be recorded that could have an adverse effect on our business, results of operations, financial condition or cash flows.

THE NEW YORK TIMES COMPANY – P. 9

Security breaches and other network and information systems disruptions could affect our ability to conduct our business effectively and damage our reputation.

Our systems store and process confidential subscriber, employee and other sensitive personal and Company data, and therefore maintaining our network security is of critical importance. In addition, we rely on the technology and systems provided by third-party vendors (including cloud-based service providers) for a variety of operations, including encryption and authentication technology, employee email, domain name registration, content delivery to customers, administrative functions (including payroll processing and certain finance and accounting functions) and other operations.

We regularly face attempts by third parties to breach our security and compromise our information technology systems, and we believe these attempts are increasing in number and in technical sophistication. These attackers may use a blend of technology and social engineering techniques (including denial of service attacks, phishing attempts intended to induce our employees and users to disclose information or unwittingly provide access to systems or data and other techniques), with the goal of service disruption or data exfiltration. Information security threats are constantly evolving, increasing the difficulty of detecting and successfully defending against them. To date, no incidents have had, either individually or in the aggregate, a material adverse effect on our business, financial condition or results of operations.

In addition, our systems, and those of third parties upon which our business relies, may be vulnerable to interruption or damage that can result from natural disasters, fires, power outages, acts of terrorism or other similar events.

We have implemented controls and taken other preventative measures designed to strengthen our systems against attacks, including measures designed to reduce the impact of a security breach at our third-party vendors. Although the costs of the controls and other measures we have taken to date have not had a material effect on our financial condition, results of operations or liquidity, there can be no assurance as to the costs of additional controls and measures that we may conclude are necessary in the future.

There can also be no assurance that the actions, measures and controls we have implemented will be effective against future attacks or be sufficient to prevent a future security breach or other disruption to our network or information systems, or those of our third-party providers. Such an event could result in a disruption of our services, improper disclosure of personal data or confidential information, or theft or misuse of our intellectual property, all of which could harm our reputation, require us to expend resources to remedy such a security breach or defend against further attacks, divert management’s attention and resources or subject us to liability under laws that protect personal data, or otherwise adversely affect our business.

Our brand and reputation are key assets of the Company, and negative perceptions or publicity could adversely affect our business, financial condition and results of operations.

The New York Times brand is a key asset of the Company, and we believe that it contributes significantly to the success of our business. We also believe that our continued success depends on our ability to preserve, grow and leverage the value of our brand. We believe that we have a powerful and trusted brand with an excellent reputation for high-quality journalism and content, but our brand could be damaged by incidents that erode consumer trust. For example, to the extent consumers perceive our journalism to be less reliable, whether as a result of negative publicity or otherwise, our ability to attract readers and advertisers may be hindered. In addition, we may introduce new products or services that users do not like and which may negatively affect our brand. We also may fail to provide adequate customer service, which could erode confidence in our brand. Our reputation could also be damaged by failures of third-party vendors we rely on in many contexts. Maintaining and enhancing our brand may require us to make significant investments, which may not be successful. To the extent our brand and reputation are damaged by these or other incidents, our revenues and profitability could be adversely affected.

Our international operations expose us to economic and other risks inherent in foreign operations.

We have news bureaus and other offices around the world, and our print, web and mobile products are generally available globally. We are focused on further expanding the international scope of our business, and face the inherent risks associated with doing business abroad, including:

• | effectively managing and staffing foreign operations, including complying with local laws and regulations in each different jurisdiction; |

P. 10 – THE NEW YORK TIMES COMPANY

• | ensuring the safety and security of our journalists and other employees working in foreign locations; |

• | navigating local customs and practices; |

• | government policies and regulations that restrict the digital flow of information, which could block access to, or the functionality of, our products; |

• | protecting and enforcing our intellectual property and other rights under varying legal regimes; |

• | complying with international laws and regulations, including those governing consumer privacy and the collection, use, retention, sharing and security of consumer and staff data; |

• | economic uncertainty, volatility in local markets and political or social instability; |

• | restrictions on foreign ownership, foreign investment or repatriation of funds; |

• | higher-than-anticipated costs of entry; and |

• | currency exchange rate fluctuations. |

Adverse developments in any of these areas could have an adverse impact on our business, financial condition and results of operations. We may, for example, incur increased costs necessary to comply with existing and newly adopted laws and regulations or penalties for any failure to comply. In addition, we have limited experience in developing and marketing our digital products in international regions and could be at a disadvantage compared with local and multinational competitors.

A significant increase in the price of newsprint, or significant disruptions in our newsprint supply chain or newspaper printing and distribution channels, would have an adverse effect on our operating results.

The cost of raw materials, of which newsprint is the major component, represented approximately 4% of our total operating costs in 2017. The price of newsprint has historically been volatile and could increase as a result of various factors, including:

•a reduction in the number of newsprint suppliers due to restructurings, bankruptcies and consolidations;

•increases in supplier operating expenses due to rising raw material or energy costs or other factors;

•currency volatility;

•duties on certain paper imports from Canada into United States; and

•inability to maintain existing relationships with our newsprint suppliers.

We also rely on suppliers for deliveries of newsprint, and the availability of our newsprint supply may be affected by various factors, including labor unrest, transportation issues and other disruptions that may affect deliveries of newsprint.

Outside the New York area, The Times is printed and distributed under contracts with print and distribution partners across the United States and internationally. Financial pressures, newspaper industry economics or other circumstances affecting these print and distribution partners could lead to reduced operations or consolidations of print sites and/or distribution routes, which could increase the cost of printing and distributing our newspapers.

If newsprint prices increase significantly or we experience significant disruptions in our newsprint supply chain or newspaper printing and distribution channels, our operating results may be adversely affected.

Acquisitions, divestitures, investments and other transactions could adversely affect our costs, revenues, profitability and financial position.

In order to position our business to take advantage of growth opportunities, we engage in discussions, evaluate opportunities and enter into agreements for possible acquisitions, divestitures, investments and other transactions. We may also consider the acquisition of, or investment in, specific properties, businesses or technologies that fall outside our traditional lines of business and diversify our portfolio, including those that may operate in new and developing industries, if we deem such properties sufficiently attractive.

THE NEW YORK TIMES COMPANY – P. 11

Acquisitions involve significant risks and uncertainties, including:

• | difficulties in integrating acquired operations (including cultural challenges associated with integrating employees from the acquired company into our organization); |

• | diversion of management attention from other business concerns or resources; |

• | use of resources that are needed in other parts of our business; |

• | possible dilution of our brand or harm to our reputation; |

• | the potential loss of key employees; |

• | risks associated with integrating financial reporting and internal control systems; and |

• | other unanticipated problems and liabilities. |

Competition for certain types of acquisitions, particularly digital properties, is significant. Even if successfully negotiated, closed and integrated, certain acquisitions or investments may prove not to advance our business strategy and may fall short of expected return on investment targets, which could adversely affect our business, results of operations and financial condition.

In addition, we have divested and may in the future divest certain assets or businesses that no longer fit with our strategic direction or growth targets. Divestitures involve significant risks and uncertainties that could adversely affect our business, results of operations and financial condition. These include, among others, the inability to find potential buyers on favorable terms, disruption to our business and/or diversion of management attention from other business concerns, loss of key employees and possible retention of certain liabilities related to the divested business.

Finally, we have made investments in companies, and we may make similar investments in the future. Investments in these businesses subject us to the operating and financial risks of these businesses and to the risk that we do not have sole control over the operations of these businesses. Our investments are generally illiquid and the absence of a market may inhibit our ability to dispose of them. In addition, if the book value of an investment were to exceed its fair value, we would be required to recognize an impairment charge related to the investment.

A significant number of our employees are unionized, and our business and results of operations could be adversely affected if labor agreements were to further restrict our ability to maximize the efficiency of our operations.

Nearly half of our full-time equivalent work force is unionized. As a result, we are required to negotiate the wage, benefits and other terms and conditions of employment with many of our employees collectively. Our results could be adversely affected if future labor negotiations or contracts were to further restrict our ability to maximize the efficiency of our operations. If we are unable to negotiate labor contracts on reasonable terms, or if we were to experience labor unrest or other business interruptions in connection with labor negotiations or otherwise, our ability to produce and deliver our products could be impaired. In addition, our ability to make adjustments to control compensation and benefits costs, change our strategy or otherwise adapt to changing business needs may be limited by the terms and duration of our collective bargaining agreements.

Failure to comply with laws and regulations, including with respect to privacy, data protection and consumer marketing practices, could adversely affect our business.

Our business is subject to government regulation in the jurisdictions in which we operate, and our websites, which are available worldwide, may be subject to laws regulating the Internet even in jurisdictions where we do not do business. Among others, we are subject to laws and regulations with respect to online privacy and the collection and use of consumer data, as well as laws and regulations with respect to consumer marketing practices.

Various federal and state laws and regulations, as well as the laws of foreign jurisdictions, govern the collection, use, retention, processing, sharing and security of the data we receive from and about our users. Failure to protect confidential user data, provide users with adequate notice of our privacy policies or obtain valid consent could subject us to liabilities imposed by these jurisdictions. Existing privacy-related laws and regulations are evolving and subject to potentially differing interpretations, and various federal and state legislative and regulatory bodies, as well as foreign legislative and regulatory bodies, may expand current or enact new laws regarding privacy and data protection. For example, the General Data Protection Regulation recently adopted by the European Union will impose more stringent data protection requirements, and significant penalties for noncompliance, beginning on May 25, 2018. In addition, the European Union’s forthcoming ePrivacy Regulation is expected to impose stricter data protection and

P. 12 – THE NEW YORK TIMES COMPANY

data collection requirements, which we expect will require certain changes in our marketing and advertising practices. The actions needed to comply with existing and newly adopted laws and regulations, or penalties for any failure to comply, could adversely affect our results of operations.

In addition, various federal and state laws and regulations, as well as the laws of foreign jurisdictions, govern the manner in which we market our subscription products, including with respect to pricing and subscription renewals. These laws and regulations often differ across jurisdictions. Failure to comply with these laws and regulations could result in claims against us by governmental entities or others, damage to our reputation and/or increased costs to change our practices.

Any failure, or perceived failure, by us to comply with laws and regulations that govern our business operations, as well as any failure, or perceived failure, by us to comply with our own posted policies, could result in claims against us by governmental entities or others and/or increased costs to change our practices. They could also result in negative publicity and a loss of confidence in us by our users and advertisers. All of these potential consequences could adversely affect our business and results of operations.

Our business may suffer if we cannot protect our intellectual property.

Our business depends on our intellectual property, including our valuable brands, content, services and internally developed technology. We believe our proprietary trademarks and other intellectual property rights are important to our continued success and our competitive position. Unauthorized parties may attempt to copy or otherwise unlawfully obtain and use our content, services, technology and other intellectual property, and we cannot be certain that the steps we have taken to protect our proprietary rights will prevent any misappropriation or confusion among consumers and merchants, or unauthorized use of these rights.

Advancements in technology have made the unauthorized duplication and wide dissemination of content easier, making the enforcement of intellectual property rights more challenging. In addition, as our business and the risk of misappropriation of our intellectual property rights have become more global in scope, we may not be able to protect our proprietary rights in a cost-effective manner in a multitude of jurisdictions with varying laws.

If we are unable to procure, protect and enforce our intellectual property rights, including maintaining and monetizing our intellectual property rights to our content, we may not realize the full value of these assets, and our business and profitability may suffer. In addition, if we must litigate in the United States or elsewhere to enforce our intellectual property rights or determine the validity and scope of the proprietary rights of others, such litigation may be costly and divert the attention of our management.

We have been, and may be in the future, subject to claims of intellectual property infringement that could adversely affect our business.

We periodically receive claims from third parties alleging infringement, misappropriation or other violations of their intellectual property rights. These third parties often include patent holding companies seeking to monetize patents they have purchased or otherwise obtained through asserting claims of infringement or misuse. Even if we believe that these claims of intellectual property infringement are without merit, defending against the claims can be time-consuming, be expensive to litigate or settle, and cause diversion of management attention.

These intellectual property infringement claims, if successful, may require us to enter into royalty or licensing agreements on unfavorable terms, use more costly alternative technology or otherwise incur substantial monetary liability. Additionally, these claims may require us to significantly alter certain of our operations. The occurrence of any of these events as a result of these claims could result in substantially increased costs or otherwise adversely affect our business.

We may not have access to the capital markets on terms that are acceptable to us or may otherwise be limited in our financing options.

From time to time the Company may need or desire to access the long-term and short-term capital markets to obtain financing. The Company’s access to, and the availability of, financing on acceptable terms and conditions in the future will be impacted by many factors, including, but not limited to: (1) the Company’s financial performance; (2) the Company’s credit ratings or absence of a credit rating; (3) liquidity of the overall capital markets and (4) the state of the economy. There can be no assurance that the Company will continue to have access to the capital markets on terms acceptable to it.

THE NEW YORK TIMES COMPANY – P. 13

In addition, macroeconomic conditions, such as continued or increased volatility or disruption in the credit markets, could adversely affect our ability to obtain financing to support operations or to fund acquisitions or other capital-intensive initiatives.

Our Class B Common Stock is principally held by descendants of Adolph S. Ochs, through a family trust, and this control could create conflicts of interest or inhibit potential changes of control.

We have two classes of stock: Class A Common Stock and Class B Common Stock. Holders of Class A Common Stock are entitled to elect 30% of the Board of Directors and to vote, with holders of Class B Common Stock, on the reservation of shares for equity grants, certain material acquisitions and the ratification of the selection of our auditors. Holders of Class B Common Stock are entitled to elect the remainder of the Board of Directors and to vote on all other matters. Our Class B Common Stock is principally held by descendants of Adolph S. Ochs, who purchased The Times in 1896. A family trust holds approximately 90% of the Class B Common Stock. As a result, the trust has the ability to elect 70% of the Board of Directors and to direct the outcome of any matter that does not require a vote of the Class A Common Stock. Under the terms of the trust agreement, the trustees are directed to retain the Class B Common Stock held in trust and to vote such stock against any merger, sale of assets or other transaction pursuant to which control of The Times passes from the trustees, unless they determine that the primary objective of the trust can be achieved better by the implementation of such transaction. Because this concentrated control could discourage others from initiating any potential merger, takeover or other change of control transaction that may otherwise be beneficial to our businesses, the market price of our Class A Common Stock could be adversely affected.

Adverse results from litigation or governmental investigations can impact our business practices and operating results.

From time to time, we are party to litigation and regulatory, environmental and other proceedings with governmental authorities and administrative agencies. See Note 18 of the Notes to the Consolidated Financial Statements regarding certain matters. Adverse outcomes in lawsuits or investigations could result in significant monetary damages or injunctive relief that could adversely affect our results of operations or financial condition as well as our ability to conduct our business as it is presently being conducted. In addition, regardless of merit or outcome, such proceedings can have an adverse impact on the Company as a result of legal costs, diversion of management and other personnel, and other factors.

ITEM 1B. UNRESOLVED STAFF COMMENTS |

None.

P. 14 – THE NEW YORK TIMES COMPANY

ITEM 2. PROPERTIES |

Our principal executive offices are located in our New York headquarters building in the Times Square area. The building was completed in 2007 and consists of approximately 1.54 million gross square feet, of which approximately 828,000 gross square feet of space have been allocated to us. We owned a leasehold condominium interest representing approximately 58% of the New York headquarters building until March 2009, when we entered into an agreement to sell and simultaneously lease back 21 floors, or approximately 750,000 rentable square feet, currently occupied by us (the “Condo Interest”). The sale price for the Condo Interest was $225.0 million. The lease term is 15 years, and we have three renewal options that could extend the term for an additional 20 years. We have an option to repurchase the Condo Interest for $250.0 million in 2019, and we have provided notice of our intent to exercise this option. We continue to own a leasehold condominium interest in seven floors in our New York headquarters building, totaling approximately 216,000 rentable square feet that were not included in the sale-leaseback transaction, all of which are currently leased to third parties.

We are engaged in a plan to consolidate the Company’s operations in our headquarters building from the 17 floors we previously occupied to 10, and to lease the remaining seven floors to third parties. We believe this plan will generate meaningful rental income to the Company and result in a more collaborative workspace.

In addition, we have a printing and distribution facility with 570,000 gross square feet located in College Point, N.Y., on a 31-acre site owned by the City of New York for which we have a ground lease. We have an option to purchase the property before the lease ends in 2019 for $6.9 million. As of December 31, 2017, we also owned other properties with an aggregate of approximately 3,000 gross square feet and leased other properties with an aggregate of approximately 205,000 rentable square feet in various locations.

ITEM 3. LEGAL PROCEEDINGS |

We are involved in various legal actions incidental to our business that are now pending against us. These actions are generally for amounts greatly in excess of the payments, if any, that may be required to be made. See Note 18 of the Notes to the Consolidated Financial Statements for a description of certain matters, which is incorporated herein by reference. Although the Company cannot predict the outcome of these matters, it is possible that an unfavorable outcome in one or more matters could be material to the Company’s consolidated results of operations or cash flows for an individual reporting period. However, based on currently available information, management does not believe that the ultimate resolution of these matters, individually or in the aggregate, is likely to have a material effect on the Company’s financial position.

ITEM 4. MINE SAFETY DISCLOSURES |

Not applicable.

THE NEW YORK TIMES COMPANY – P. 15

EXECUTIVE OFFICERS OF THE REGISTRANT

Name | Age | Employed By Registrant Since | Recent Position(s) Held as of February 27, 2018 | |||

Mark Thompson | 60 | 2012 | President and Chief Executive Officer (since 2012); Director-General, British Broadcasting Corporation (2004 to 2012) | |||

A.G. Sulzberger | 37 | 2009 | Publisher of The Times (since 2018); Deputy Publisher (2016 to 2017); Associate Editor (2015-2016); Assistant Editor (2012-2015) | |||

R. Anthony Benten | 54 | 1989 | Senior Vice President, Treasurer (since December 2016) and Corporate Controller (since 2007); Senior Vice President, Finance (2008 to 2016) | |||

Diane Brayton | 49 | 2004 | Executive Vice President, General Counsel (since January 2017) and Secretary (since 2011); Deputy General Counsel (2016); Assistant Secretary (2009 to 2011) and Assistant General Counsel (2009 to 2016) | |||

James M. Follo(1) | 58 | 2007 | Executive Vice President (since 2013) and Chief Financial Officer (since 2007); Senior Vice President (2007 to 2013) | |||

Meredith Kopit Levien | 46 | 2013 | Executive Vice President (since 2013) and Chief Operating Officer (since 2017); Chief Revenue Officer (2015 to 2017); Executive Vice President, Advertising (2013 to 2015); Chief Revenue Officer, Forbes Media LLC (2011 to 2013) | |||

(1) Mr. Follo will retire from the Company effective February 28, 2018. As previously disclosed, Roland Caputo, currently Executive Vice President, Print Products and Services Group, will serve as Interim Chief Financial Officer following Mr. Follo’s retirement and until the Company appoints a permanent Chief Financial Officer.

P. 16 – THE NEW YORK TIMES COMPANY

PART II |

ITEM 5. MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

MARKET INFORMATION

The Class A Common Stock is listed on the New York Stock Exchange. The Class B Common Stock is unlisted and is not actively traded.

The number of security holders of record as of February 23, 2018, was as follows: Class A Common Stock: 5,662; Class B Common Stock: 21.

We have paid quarterly dividends of $0.04 per share on the Class A and Class B Common Stock since late 2013. We currently expect to continue to pay comparable cash dividends in the future, although changes in our dividend program may be considered by our Board of Directors in light of our earnings, capital requirements, financial condition and other factors considered relevant. In addition, our Board of Directors will consider restrictions in any future indebtedness. See also “Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources — Third-Party Financing.”

The following table sets forth, for the periods indicated, the high and low closing sales prices for the Class A Common Stock as reported on the New York Stock Exchange.

2017 | 2016 | |||||||||||||||

Quarters | High | Low | High | Low | ||||||||||||

First Quarter | $ | 16.25 | $ | 13.05 | $ | 13.74 | $ | 12.25 | ||||||||

Second Quarter | 17.90 | 14.20 | 13.12 | 11.80 | ||||||||||||

Third Quarter | 19.95 | 17.35 | 13.17 | 11.54 | ||||||||||||

Fourth Quarter | 20.00 | 17.10 | 14.10 | 10.80 | ||||||||||||

ISSUER PURCHASES OF EQUITY SECURITIES(1)

Period | Total number of shares of Class A Common Stock purchased (a) | Average price paid per share of Class A Common Stock (b) | Total number of shares of Class A Common Stock purchased as part of publicly announced plans or programs (c) | Maximum number (or approximate dollar value) of shares of Class A Common Stock that may yet be purchased under the plans or programs (d) | ||||||||||

September 25, 2017 - October 29, 2017 | — | $ | — | — | $ | 16,236,612 | ||||||||

October 30, 2017 - November 26, 2017 | — | $ | — | — | $ | 16,236,612 | ||||||||

November 27, 2017 - December 31, 2017 | — | $ | — | — | $ | 16,236,612 | ||||||||

Total for the fourth quarter of 2017 | — | $ | — | — | $ | 16,236,612 | ||||||||

(1) | On January 13, 2015, the Board of Directors approved an authorization of $101.1 million to repurchase shares of the Company’s Class A Common Stock. As of December 31, 2017, repurchases under this authorization totaled $84.9 million (excluding commissions), and $16.2 million remained under this authorization. All purchases were made pursuant to our publicly announced share repurchase program. Our Board of Directors has authorized us to purchase shares from time to time, subject to market conditions and other factors. There is no expiration date with respect to this authorization. |

THE NEW YORK TIMES COMPANY – P. 17

UNREGISTERED SALES OF EQUITY SECURITIES

On September 26, 2017, and December 28, 2017, we issued 2,170 and 5,000 shares, respectively, of Class A Common Stock to holders of Class B Common Stock upon the conversion of such Class B Common Stock into Class A Common Stock. The conversions, which were in accordance with our Certificate of Incorporation, did not involve a public offering and were exempt from registration pursuant to Section 3(a)(9) of the Securities Act of 1933, as amended.

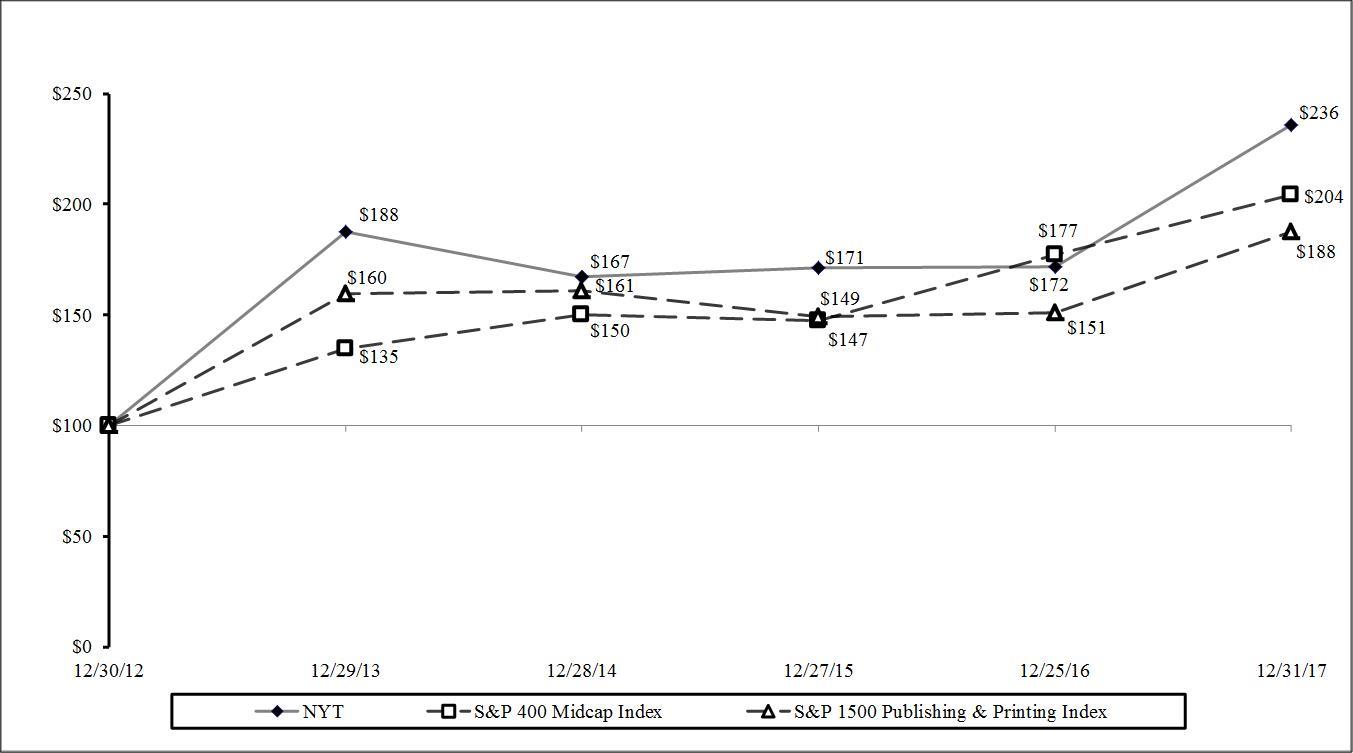

PERFORMANCE PRESENTATION

The following graph shows the annual cumulative total stockholder return for the five fiscal years ended December 31, 2017, on an assumed investment of $100 on December 30, 2012, in the Company, the Standard & Poor’s S&P 400 MidCap Stock Index and the Standard & Poor’s S&P 1500 Publishing and Printing Index. Stockholder return is measured by dividing (a) the sum of (i) the cumulative amount of dividends declared for the measurement period, assuming reinvestment of dividends, and (ii) the difference between the issuer’s share price at the end and the beginning of the measurement period, by (b) the share price at the beginning of the measurement period. As a result, stockholder return includes both dividends and stock appreciation.

Stock Performance Comparison Between the S&P 400 Midcap Index, S&P 1500 Publishing & Printing Index and The New York Times Company’s Class A Common Stock

P. 18 – THE NEW YORK TIMES COMPANY

ITEM 6. SELECTED FINANCIAL DATA |

The Selected Financial Data should be read in conjunction with “Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Consolidated Financial Statements and the related Notes in Item 8. The results of operations for the New England Media Group, which was sold in 2013, have been presented as discontinued operations for all periods presented (see Note 13 of the Notes to the Consolidated Financial Statements). The pages following the table show certain items included in Selected Financial Data. All per share amounts on those pages are on a diluted basis. Fiscal year 2017 comprised 53 weeks and all other fiscal years presented in the table below comprised 52 weeks.

As of and for the Years Ended | ||||||||||||||||||||

(In thousands) | December 31, 2017 | December 25, 2016 | December 27, 2015 | December 28, 2014 | December 29, 2013 | |||||||||||||||

(53 Weeks) | (52 Weeks) | (52 Weeks) | (52 Weeks) | (52 Weeks) | ||||||||||||||||

Statement of Operations Data | ||||||||||||||||||||

Revenues | $ | 1,675,639 | $ | 1,555,342 | $ | 1,579,215 | $ | 1,588,528 | $ | 1,577,230 | ||||||||||

Operating costs | 1,488,131 | 1,410,910 | 1,393,246 | 1,484,505 | 1,411,744 | |||||||||||||||

Headquarters redesign and consolidation | 10,090 | — | — | — | — | |||||||||||||||

Restructuring charge | — | 14,804 | — | — | — | |||||||||||||||

Multiemployer pension plan withdrawal expense | — | 6,730 | 9,055 | — | 6,171 | |||||||||||||||

Postretirement benefit plan settlement gain | (37,057 | ) | — | — | — | — | ||||||||||||||

Pension settlement expense | 102,109 | 21,294 | 40,329 | 9,525 | 3,228 | |||||||||||||||

Early termination charge and other expenses | — | — | — | 2,550 | — | |||||||||||||||

Operating profit | 112,366 | 101,604 | 136,585 | 91,948 | 156,087 | |||||||||||||||

Gain/(loss) from joint ventures | 18,641 | (36,273 | ) | (783 | ) | (8,368 | ) | (3,215 | ) | |||||||||||

Interest expense and other, net | 19,783 | 34,805 | 36,050 | 53,730 | 58,073 | |||||||||||||||

Income from continuing operations before income taxes | 111,224 | 30,526 | 96,752 | 29,850 | 94,799 | |||||||||||||||

Income from continuing operations | 7,268 | 26,105 | 62,842 | 33,391 | 56,907 | |||||||||||||||

(Loss)/income from discontinued operations, net of income taxes | (431 | ) | (2,273 | ) | — | (1,086 | ) | 7,949 | ||||||||||||

Net income attributable to The New York Times Company common stockholders | 4,296 | 29,068 | 63,246 | 33,307 | 65,105 | |||||||||||||||

Balance Sheet Data | ||||||||||||||||||||

Cash, cash equivalents and marketable securities | $ | 732,911 | $ | 737,526 | $ | 904,551 | $ | 981,170 | $ | 1,023,780 | ||||||||||

Property, plant and equipment, net | 640,939 | 596,743 | 632,439 | 665,758 | 713,356 | |||||||||||||||

Total assets | 2,099,780 | 2,185,395 | 2,417,690 | 2,566,474 | 2,572,552 | |||||||||||||||

Total debt and capital lease obligations | 250,209 | 246,978 | 431,228 | 650,120 | 684,163 | |||||||||||||||

Total New York Times Company stockholders’ equity | 897,279 | 847,815 | 826,751 | 726,328 | 842,910 | |||||||||||||||

THE NEW YORK TIMES COMPANY – P. 19

As of and for the Years Ended | ||||||||||||||||||||

(In thousands, except ratios, per share and employee data) | December 31, 2017 | December 25, 2016 | December 27, 2015 | December 28, 2014 | December 29, 2013 | |||||||||||||||

(53 Weeks) | (52 Weeks) | (52 Weeks) | (52 Weeks) | (52 Weeks) | ||||||||||||||||

Per Share of Common Stock | ||||||||||||||||||||

Basic earnings/(loss) per share attributable to The New York Times Company common stockholders: | ||||||||||||||||||||

Income from continuing operations | $ | 0.03 | $ | 0.19 | $ | 0.38 | $ | 0.23 | $ | 0.38 | ||||||||||

(Loss)/income from discontinued operations, net of income taxes | — | (0.01 | ) | — | (0.01 | ) | 0.05 | |||||||||||||

Net income | $ | 0.03 | $ | 0.18 | $ | 0.38 | $ | 0.22 | $ | 0.43 | ||||||||||

Diluted earnings/(loss) per share attributable to The New York Times Company common stockholders: | ||||||||||||||||||||

Income from continuing operations | $ | 0.03 | $ | 0.19 | $ | 0.38 | $ | 0.21 | $ | 0.36 | ||||||||||

(Loss)/income from discontinued operations, net of income taxes | — | (0.01 | ) | — | (0.01 | ) | 0.05 | |||||||||||||

Net income | $ | 0.03 | $ | 0.18 | $ | 0.38 | $ | 0.20 | $ | 0.41 | ||||||||||

Dividends declared per share | $ | 0.16 | $ | 0.16 | $ | 0.16 | $ | 0.16 | $ | 0.08 | ||||||||||

New York Times Company stockholders’ equity per share | $ | 5.46 | $ | 5.21 | $ | 4.97 | $ | 4.50 | $ | 5.34 | ||||||||||

Average basic shares outstanding | 161,926 | 161,128 | 164,390 | 150,673 | 149,755 | |||||||||||||||

Average diluted shares outstanding | 164,263 | 162,817 | 166,423 | 161,323 | 157,774 | |||||||||||||||

Key Ratios | ||||||||||||||||||||

Operating profit to revenues | 6.7 | % | 6.5 | % | 8.6 | % | 5.8 | % | 9.9 | % | ||||||||||

Return on average common stockholders’ equity | 0.5 | % | 3.5 | % | 8.1 | % | 4.2 | % | 8.7 | % | ||||||||||

Return on average total assets | 0.2 | % | 1.3 | % | 2.5 | % | 1.3 | % | 2.4 | % | ||||||||||

Total debt and capital lease obligations to total capitalization | 21.8 | % | 22.6 | % | 34.3 | % | 47.2 | % | 44.8 | % | ||||||||||

Current assets to current liabilities | 1.80 | 2.00 | 1.53 | 1.91 | 3.36 | |||||||||||||||

Full-Time Equivalent Employees | 3,789 | 3,710 | 3,560 | 3,588 | 3,529 | |||||||||||||||

The items below are included in the Selected Financial Data.

2017 (53-week fiscal year)

The items below had a net unfavorable effect on our Income from continuing operations of $127.3 million, or $.77 per share: