UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark one)

| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from

to

|

|

|

|

|

| Commission File Number |

|

Exact name of registrants as specified in their charters |

|

I.R.S. Employer

Identification Number |

|

|

|

| 001-36684 |

|

DOMINION ENERGY MIDSTREAM PARTNERS, LP |

|

46-5135781 |

|

|

|

|

|

DELAWARE

(State or other jurisdiction of incorporation or organization) |

|

|

|

|

|

|

|

120 TREDEGAR STREET

RICHMOND, VIRGINIA (Address

of principal executive offices) |

|

23219

(Zip Code) |

|

|

|

| |

|

(804) 819-2000

(Registrants’ telephone number) |

|

|

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

| Title of Each

Class |

|

Name of Each Exchange

on Which Registered |

| Common Units Representing Limited Partner Interests |

|

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by

check mark whether the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the

Act. Yes ☐ No ☒

Indicate by check mark whether the

registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and

(2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required

to submit and post such files). Yes ☒ No ☐

Indicate by

check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s

knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting

company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

|

|

|

|

| Large accelerated filer |

|

☒ |

|

Accelerated filer |

|

☐ |

| Non-accelerated filer |

|

☐ (Do not check if a smaller reporting company) |

|

Smaller reporting company |

|

☐ |

|

|

|

|

Emerging growth company |

|

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended

transition period for complying with any new or revised accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the

Act). Yes ☐ No ☒

The aggregate market value of the

registrant’s common units held by non-affiliates was approximately $1.4 billion based on the closing price of its common units as reported on the New York Stock Exchange as of the last day of its

most recently completed second fiscal quarter. At February 23, 2018, Dominion Energy Midstream Partners, LP had 67,959,770 common units and 31,972,789 subordinated units outstanding.

Dominion Energy Midstream Partners, LP

Unless the context otherwise requires, references in this Annual Report on Form 10-K

to “Cove Point,” “the Predecessor,” “our predecessor,” and “we,” “our,” “us,” “our partnership” or like terms when used in a historical context (periods prior to October 20,

2014), refer to Dominion Energy Cove Point LNG, LP as our predecessor for accounting purposes. When used in the present tense or prospectively (periods beginning October 20, 2014), “Dominion Energy Midstream,” “we,”

“our,” “us” or like terms refer to Dominion Energy Midstream Partners, LP; one of its wholly-owned subsidiaries, Cove Point GP Holding Company, LLC, Iroquois GP Holding Company, LLC, Dominion Energy Carolina Gas Transmission, LLC

(beginning April 1, 2015) or Dominion Energy Questar Pipeline, LLC and its subsidiaries (beginning December 1, 2016); or all of them taken as a whole.

GLOSSARY OF TERMS

The following abbreviations or acronyms used in this Form 10-K are defined below:

|

|

|

| Abbreviation or Acronym |

|

Definition |

| 2005 Agreement |

|

An agreement effective March 1, 2005, which Cove Point entered into with the Sierra Club and the

Maryland Conservation Council, Inc. |

| 2017 Tax Reform Act |

|

An Act to Provide for Reconciliation Pursuant to Titles II and V of the Concurrent Resolution on the Budget

for Fiscal Year 2018 (previously known as The Tax Cuts and Jobs Act) enacted on December 22, 2017 |

| Additional Return Distributions |

|

The additional cash distribution equal to 3.0% of Cove Point’s Modified Net Operating Income in excess

of $600 million distributed each year |

| Adjusted EBITDA |

|

EBITDA after adjustment for EBITDA attributable to predecessors and a noncontrolling interest in Cove Point

held by Dominion Energy, less income from equity method investees, plus distributions from equity method investees |

| AFUDC |

|

Allowance for funds used during construction |

| AIP |

|

Annual Incentive Plan |

| AOCI |

|

Accumulated other comprehensive income (loss) |

| ARO |

|

Asset retirement obligation |

| Atlantic Coast Pipeline |

|

Atlantic Coast Pipeline, LLC, a limited liability company owned by Dominion Energy, Duke Energy Corporation,

Piedmont Natural Gas Company, Inc. and Southern Company Gas |

| Bcf |

|

Billion cubic feet |

| Bcfe |

|

Billion cubic feet equivalent |

| Blue Racer |

|

Blue Racer Midstream, LLC, a joint venture between Dominion Energy and Caiman |

| BRP |

|

Retirement Benefit Restoration Plan |

| CAA |

|

Clean Air Act |

| Caiman |

|

Caiman Energy II, LLC |

| CAP |

|

IRS Compliance Assurance Process |

| CD&A |

|

Compensation Discussion and Analysis |

| CEO |

|

Chief Executive Officer |

| CFO |

|

Chief Financial Officer |

| CGN Committee |

|

Compensation, Governance and Nominating Committee of Dominion Energy’s Board of Directors |

| Charleston Project |

|

Project to provide 80,000 Dths/day of firm transportation service from an existing interconnect with Transco

in Spartanburg County, South Carolina to customers in Dillon, Marlboro, Sumter, Charleston, Lexington and Richland counties, South Carolina |

| Clean Power Plan |

|

Guidelines issued by the EPA in August 2015 for states to follow in developing plans to reduce CO2 emissions from existing fossil fuel-fired electric generating units, stayed by the U.S. Supreme Court in February 2016 pending resolution of court challenges by certain states |

| Columbia to Eastover Project |

|

Project to provide 15,800 Dths/day of firm transportation service from an existing interconnect with Southern

Natural Gas Company, LLC in Aiken County, South Carolina and provide for a receipt point change of 2,200 Dths/day under an existing contract from an existing interconnect with Transco in Cherokee County, South Carolina for a total 18,000 Dths/day,

to a new delivery point for the International Paper Company at its pulp and paper mill known as the Eastover Plant in Richland County, South Carolina |

| CO2 |

|

Carbon dioxide |

| Cove Point |

|

Dominion Energy Cove Point LNG, LP |

| Cove Point Facilities |

|

Collectively, the Liquefaction Project, Cove Point LNG Facility and Cove Point Pipeline |

| Cove Point Holdings |

|

Cove Point GP Holding Company, LLC |

| Cove Point LNG Facility |

|

An LNG terminalling and storage facility located on the Chesapeake Bay in Lusby, Maryland owned by Cove

Point |

| Cove Point Pipeline |

|

An approximately 136-mile natural gas pipeline owned by Cove Point

that connects the Cove Point LNG Facility to interstate natural gas pipelines |

| CPCN |

|

Certificate of Public Convenience and Necessity |

| CRA |

|

Compliance Resolution Agreement |

| CWA |

|

Clean Water Act |

| DCPI |

|

Dominion Cove Point, Inc. |

| DECG |

|

Dominion Energy Carolina Gas Transmission, LLC |

| DECG Acquisition |

|

The acquisition of DECG by Dominion Energy Midstream from Dominion Energy on April 1, 2015 |

| DECG Predecessor |

|

Dominion Energy as the predecessor for accounting purposes for the period from Dominion Energy’s

acquisition of DECG from SCANA on January 31, 2015 until the DECG Acquisition |

| DECGS |

|

Dominion Energy Carolina Gas Services, Inc. |

| DEPC |

|

Dominion Energy Payroll Company, Inc. |

| DEQPS |

|

Dominion Energy Questar Pipeline Services, Inc. |

| DES |

|

Dominion Energy Services, Inc. |

| DETI |

|

Dominion Energy Transmission, Inc. |

| DGP |

|

Dominion Gathering and Processing, Inc. |

| DOE |

|

U.S. Department of Energy |

| DOL |

|

U.S. Department of Labor |

| Dominion Energy |

|

The legal entity, Dominion Energy, Inc., one or more of its consolidated subsidiaries (other than Dominion

Energy Midstream GP, LLC and its subsidiaries) or operating segments, or the entirety of Dominion Energy, Inc. and its consolidated subsidiaries |

|

|

|

| Abbreviation or Acronym |

|

Definition |

| Dominion Energy Gas |

|

The legal entity, Dominion Energy Gas Holdings, LLC, one or more of its consolidated subsidiaries or

operating segment, or the entirety of Dominion Energy Gas Holdings, LLC and its consolidated subsidiaries |

| Dominion Energy Midstream |

|

The legal entity, Dominion Energy Midstream Partners, LP, one or more of its consolidated subsidiaries, Cove

Point Holdings, Iroquois GP Holding Company, LLC, DECG (beginning April 1, 2015) and Dominion Energy Questar Pipeline (beginning December 1, 2016), or the entirety of Dominion Energy Midstream Partners, LP and its consolidated

subsidiaries |

| Dominion Energy Midstream LTIP |

|

Dominion Energy Midstream Partners, LP 2014 Long-Term Incentive Plan |

| Dominion Energy Questar |

|

The legal entity, Dominion Energy Questar Corporation, one or more of its consolidated subsidiaries or

operating segment, or the entirety of Dominion Energy Questar Corporation and its consolidated subsidiaries |

| Dominion Energy Questar Pipeline |

|

The legal entity, Dominion Energy Questar Pipeline, LLC, one or more of its consolidated subsidiaries, or the

entirety of Dominion Energy Questar Pipeline, LLC and its consolidated subsidiaries |

| Dominion Energy Questar Pipeline Acquisition |

|

The acquisition of Dominion Energy Questar Pipeline by Dominion Energy Midstream from Dominion Energy on

December 1, 2016 |

| Dominion Energy Questar Pipeline Contribution Agreement |

|

Contribution, Conveyance and Assumption Agreement between Dominion Energy and Dominion Energy Midstream dated

October 28, 2016 |

| Dominion Energy Questar Pipeline Predecessor |

|

Dominion Energy as the predecessor for accounting purposes for the period from Dominion Energy’s

acquisition of Dominion Energy Questar Pipeline on September 16, 2016 until the Dominion Energy Questar Pipeline Acquisition |

| DOT |

|

U.S. Department of Transportation |

| Dth |

|

Dekatherm |

| Duke |

|

The legal entity, Duke Energy Corporation, one or more of its consolidated subsidiaries or operating

segments, or the entirety of Duke Energy Corporation and its consolidated subsidiaries |

| EA |

|

Environmental assessment |

| Eastern Market Access Project |

|

Project to provide 294,000 Dths/day of firm transportation service to help meet demand for natural gas for

Washington Gas Light Company, a local gas utility serving customers in D.C., Virginia and Maryland, and Mattawoman Energy, LLC for its new electric power generation facility to be built in Maryland |

| EBITDA |

|

Earnings before interest and associated charges, income tax expense, depreciation and

amortization |

| Edgemoor Project |

|

Project to provide 45,000 Dths/day of firm transportation service from an existing interconnect with Transco

in Cherokee County, South Carolina to customers in Calhoun and Lexington counties, South Carolina |

| EPA |

|

U.S. Environmental Protection Agency |

| EPACT |

|

Energy Policy Act of 2005 |

| ERISA |

|

Employee Retirement Income Security Act of 1974 |

| ESRP |

|

Executive Supplemental Retirement Plan |

| Export Customers |

|

ST Cove Point, LLC, a joint venture of Sumitomo Corporation and Tokyo Gas Co., Ltd., and GAIL Global (USA)

LNG, LLC |

| FASB |

|

Financial Accounting Standards Board |

| FERC |

|

Federal Energy Regulatory Commission |

| FERC Order |

|

FERC order issued on September 29, 2014 that granted authorization for Cove Point to construct, modify

and operate the Liquefaction Project, subject to conditions, and also granted authorization to enhance the Cove Point Pipeline |

| FIPs |

|

Failures in individual performance |

| FTA |

|

Free Trade Agreement |

| FTA Authorization |

|

Authorization from the DOE for the export of up to 1.0 Bcfe/day of natural gas to countries that have or will

enter into an FTA for trade in natural gas |

| FW Cook |

|

Frederic W. Cook & Co. |

| GAAP |

|

U.S. generally accepted accounting principles |

| Gas Infrastructure |

|

Gas Infrastructure Group operating segment |

| GHG |

|

Greenhouse gas |

| Hyrum Project |

|

Project to provide 100,000 Dths/day of firm transportation service to help meet growing demand for natural

gas for Questar Gas Company, an affiliated local gas utility serving customers in Utah, Wyoming and Idaho |

| IDR |

|

Incentive distribution right |

| Import Shippers |

|

The three LNG import shippers consisting of BP Energy Company, Shell NA LNG, Inc. and Statoil |

| IRA |

|

Individual retirement account |

| IRC |

|

Internal Revenue Code |

| Iroquois |

|

Iroquois Gas Transmission System, L.P. |

| IRS |

|

Internal Revenue Service |

| Keys Energy Project |

|

Project to provide 107,000 Dths/day of firm transportation service from Cove Point’s interconnect with

Transco in Fairfax County, Virginia to Keys Energy Center, LLC’s power generating facility in Prince George’s County, Maryland |

| Liquefaction Project |

|

A natural gas export/liquefaction facility at Cove Point |

| LNG |

|

Liquefied natural gas |

|

|

|

| Abbreviation or Acronym |

|

Definition |

| LTIP |

|

Long-term incentive plan |

| Maryland Commission |

|

Public Service Commission of Maryland |

| MD&A |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| MLP |

|

Master limited partnership, equivalent to publicly traded partnership |

| Modified Net Operating Income |

|

Cove Point’s Net Operating Income plus any interest expense included in the computation of Net Operating

Income |

| Mtpa |

|

Million metric tons per annum |

| NEO |

|

Named executive officers |

| Net Operating Income |

|

Cove Point’s gross revenues from operations minus its interest expense and operating expenses, but

excluding depreciation and amortization, as determined for U.S. federal income tax purposes |

| NG |

|

Collectively, North East Transmission Co., Inc. and National Grid IGTS Corp. |

| NGA |

|

Natural Gas Act of 1938, as amended |

| NGPSA |

|

Natural Gas Pipeline Safety Act of 1968, as amended |

| NJNR |

|

NJNR Pipeline Company |

| Non-FTA Authorization |

|

Authorization from the DOE for the export of up to 0.77 Bcfe/day of natural gas to countries that do not have

an FTA for trade in natural gas |

| Non-Open Access Services |

|

Non-open access, proprietary

non-jurisdictional services with rates, terms and conditions that are determined by arm’s length negotiations with customers |

| NYSE |

|

New York Stock Exchange |

| Offering |

|

The initial public offering of common units of Dominion Energy Midstream |

| Open Access Services |

|

Open access jurisdictional services with cost-based rates and terms and conditions that are part of a tariff

approved by FERC |

| organizational design initiative |

|

In the first quarter of 2016, Dominion Energy announced an organizational design initiative that reduced its

total workforce during 2016, the goal of which was to streamline its leadership structure and push decision making lower while also improving efficiency |

| OSHA |

|

Federal Occupational Safety and Health Act, as amended |

| PHMSA |

|

Pipeline and Hazardous Materials Safety Administration |

| ppb |

|

Parts-per-billion |

| predecessors |

|

Collectively, DECG Predecessor and Dominion Energy Questar Pipeline Predecessor |

| Preferred Equity Interest |

|

A perpetual, non-convertible preferred equity interest in Cove Point

entitled to the Preferred Return Distributions and the Additional Return Distributions |

| Preferred Return Distributions |

|

The first $50.0 million of annual cash distributions made by Cove Point |

| Private Placement Agreement |

|

Series A Preferred Unit and Common Unit Purchase Agreement between Dominion Energy Midstream and purchasers

(certain affiliates of Stonepeak Infrastructure Partners, Magnetar Financial LLC, First Reserve Advisors, L.L.C., Kayne Anderson Capital Advisors, L.P. and Tortoise Capital Advisors, LLC) dated October 27, 2016 |

| PSD |

|

Prevention of Significant Deterioration |

| PSIA |

|

Pipeline Safety Improvement Act of 2002 |

| RGGI |

|

Regional Greenhouse Gas Initiative |

| ROFO Assets |

|

Any of the common equity interests in Cove Point or the indirect ownership interests in Blue Racer or

Atlantic Coast Pipeline subject to the right of first offer agreement with Dominion Energy entered into in connection with the Offering |

| ROIC |

|

Return on invested capital |

| SCANA |

|

SCANA Corporation |

| SCE&G |

|

South Carolina Electric & Gas Company |

| SEC |

|

Securities and Exchange Commission |

| SEIF |

|

Maryland Strategic Energy Investments Fund |

| Series A Preferred Units |

|

Series A convertible preferred units representing limited partner interests in Dominion Energy Midstream,

issued in December 2016 |

| St. Charles Transportation Project |

|

Project to provide 132,000 Dths/day of firm transportation service from Cove Point’s interconnect with

Transco in Fairfax County, Virginia to Competitive Power Venture Maryland, LLC’s power generating facility in Charles County, Maryland |

| Statoil |

|

Statoil Natural Gas, LLC |

| Storage Customers |

|

The four local distribution companies that receive firm peaking services from Cove Point, consisting of

Atlanta Gas Light Company; Public Service Company of North Carolina, Incorporated; Virginia Natural Gas, Inc. and Washington Gas Light Company |

| Transco |

|

Transcontinental Gas Pipe Line, LLC |

| TSR |

|

Total shareholder return |

| VIE |

|

Variable interest entity |

| Virginia Power |

|

The legal entity, Virginia Electric and Power Company, one or more of its consolidated subsidiaries or

operating segments, or the entirety of Virginia Electric and Power Company and its consolidated subsidiaries |

| VOC |

|

Volatile organic compounds |

| Wexpro |

|

The legal entity, Wexpro Company, one or more of its consolidated subsidiaries, or the entirety of Wexpro

Company and its consolidated subsidiaries |

| White River Hub |

|

White River Hub, LLC |

Part I

Item 1. Business

OVERVIEW

Dominion Energy Midstream is a

growth-oriented Delaware limited partnership formed on March 11, 2014 by Dominion Energy to grow a portfolio of natural gas terminaling, processing, storage, transportation and related assets. Dominion Energy Midstream’s common units began

trading on the NYSE on October 15, 2014, under the ticker symbol “DM.” At December 31, 2017, Dominion Energy owned the general partner, 50.6% of the common and subordinated units and 37.5% of the convertible preferred interests

in Dominion Energy Midstream. In connection with the Offering, Dominion Energy Midstream acquired the Preferred Equity Interest and the general partner interest in Cove Point from Dominion Energy.

Cove Point owns and operates the Cove Point LNG Facility and the Cove Point Pipeline. Cove Point has historically generated a significant

portion of its revenue and earnings from annual reservation payments under certain regasification, storage and transportation contracts. Upon operational commencement of the Liquefaction Project, the majority of Cove Point’s revenue and

earnings will be generated from annual reservation payments under certain terminaling, storage and transportation contracts.

On

April 1, 2015, Dominion Energy Midstream acquired from Dominion Energy all of the issued and outstanding membership interests of DECG, an open access, transportation-only interstate pipeline company in South Carolina and southeastern Georgia,

for total consideration of $500.8 million. See Note 4 to the Consolidated Financial Statements for additional information regarding this acquisition.

On September 29, 2015, Dominion Energy Midstream acquired NG’s 20.4% and

NJNR’s 5.53% partnership interests in Iroquois and, in exchange, Dominion Energy Midstream issued common units representing limited partner interests in Dominion Energy Midstream to both NG and NJNR. The Iroquois investment, accounted for under

the equity method, was recorded at $216.5 million. See Note 4 to the Consolidated Financial Statements for additional information regarding this equity method investment.

On December 1, 2016, Dominion Energy Midstream acquired from Dominion Energy all of the issued and outstanding membership interests of

Dominion Energy Questar Pipeline, which owns and operates interstate natural gas pipelines and storage facilities in the western U.S., for total consideration of $1.29 billion. See Note 4 to the Consolidated Financial Statements for additional

information regarding this acquisition.

Dominion Energy Midstream manages its daily operations through one operating segment, Gas

Infrastructure, which consists of gas transportation, LNG terminalling services and storage. In addition to Gas Infrastructure, Dominion Energy Midstream also reports a Corporate and Other segment, which primarily includes specific items

attributable to its operating segment that are not included in profit measures evaluated by executive management in assessing the operating segment’s performance or in allocating resources. See Note 25 to the Consolidated Financial Statements

for further discussions of Dominion Energy Midstream’s operating segment, which information is incorporated herein by reference.

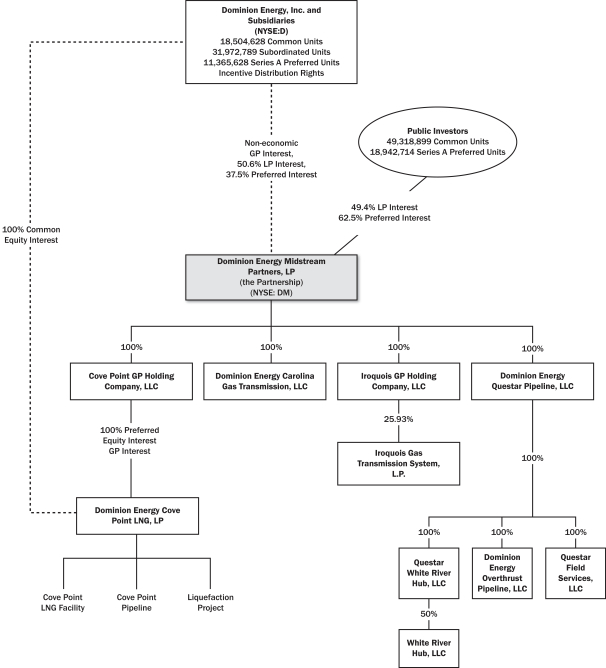

ORGANIZATIONAL STRUCTURE

The following simplified diagram depicts Dominion Energy Midstream’s organizational and ownership structure at December 31, 2017.

ASSETS AND OPERATIONS

Dominion Energy Midstream’s ongoing principal sources of cash flow include distributions received from Cove Point from our Preferred Equity Interest,

cash generated from the operations of DECG and Dominion Energy Questar Pipeline and distributions received from our noncontrolling partnership interests in Iroquois and White River Hub.

Preferred Equity Interest

One of our primary cash flow generating

assets is the Preferred Equity Interest which is entitled to Preferred Return Distributions so long as Cove Point has sufficient cash and undistributed Net Operating Income (determined on a cumulative basis from the closing of the Offering) from

which to make Preferred Return Distributions. Preferred Return Distributions will be made on a quarterly basis and will not be cumulative. The Preferred Equity Interest is also entitled to the Additional Return Distributions and should benefit from

the expected increased cash flows and income associated with the Liquefaction Project once it is commercially operational.

We believe

that Cove Point has generated cash and cumulative Net Operating Income in excess of that required to make Preferred Return Distributions until the Liquefaction Project is commercially operational, expected in March 2018. We expect the cash flows and

Net Operating Income from the Liquefaction Project, once commercially operational, to replace and substantially exceed Cove Point’s cash flows and Net Operating Income from its existing import contracts and associated transportation contracts.

See description of the Liquefaction Project under Assets and Operations—Cove Point. Until the Liquefaction Project is completed, Cove Point was prohibited from making a distribution on its common equity interests unless it has a

distribution reserve sufficient to pay two quarters of Preferred Return Distributions (and two quarters of similar distributions with respect to any other preferred equity interest in Cove Point). Cove Point fully funded this distribution reserve in

October 2016, but there can be no assurance that funds will be sufficient for such purpose or that Cove Point will have sufficient cash and undistributed Net Operating Income to permit it to continue to make Preferred Return Distributions. The

distribution reserve was fully utilized to fund the quarterly Preferred Return Distributions paid in November 2017 and February 2018. We do not expect to cause Cove Point to make distributions on its common equity, or the Additional Return

Distributions, prior to the Liquefaction Project commencing commercial service. No distribution reserve will be established for the Additional Return Distributions.

Cove Point

Cove Point is a Delaware limited partnership, of which

Dominion Energy Midstream owns the preferred equity interests and the general partner interest and Dominion Energy owns the common equity interests. Cove Point’s operations currently consist of LNG import and storage services at the Cove Point

LNG Facility and the transportation of domestic natural gas and regasified LNG to Mid-Atlantic markets via the Cove Point Pipeline. Following binding commitments from counterparties, Cove Point requested and

received regulatory approval to operate the Cove Point LNG

Facility as a bi-directional facility, able to import LNG and regasify it as natural gas or to liquefy domestic natural gas and export it as LNG.

COVE POINT’S IMPORT/STORAGE/REGASIFICATION

FACILITIES

The Cove Point LNG Facility includes an offshore pier, LNG storage tanks, regasification facilities and associated

equipment required to (i) receive imported LNG from tankers, (ii) store LNG in storage tanks, (iii) regasify LNG and (iv) deliver regasified LNG to the Cove Point Pipeline. The Cove Point LNG Facility has a contractual peak

regasification capacity of approximately 1.8 million Dths/day and an aggregate LNG storage capacity of 695,000 cubic meters of LNG, or approximately 14.6 Bcfe, of which approximately 53% was contracted at December 31, 2017. The available

capacity reflects the expiration of an agreement with Statoil in 2017. In addition, the Cove Point LNG Facility has an existing liquefier (unrelated to the Liquefaction Project) capable of liquefying approximately 15,000 Dths/day of natural gas.

This liquefaction capacity is primarily used to liquefy natural gas received from domestic customers that store LNG in our tanks for use during peak periods of natural gas demand. Cove Point offers both Open Access Services and Non-Open Access Services. Cove Point’s two-berth pier is located approximately 1.1 miles offshore in the Chesapeake Bay. Cove Point operates the Cove Point LNG Facility

on an integrated basis with no equipment exclusively used for the benefit of Open Access Services or Non-Open Access Services.

Cove Point currently provides services under (i) long-term agreements with the Import Shippers for an aggregate of 1.0 million

Dths/day of firm and off-peak regasification capacity, and (ii) long-term agreements for an aggregate 204,000 Dths/day of firm capacity with the Storage Customers who receive firm peaking services,

whereby the Storage Customers deliver domestic natural gas to the Cove Point LNG Facility to be liquefied and stored during the summer for withdrawal on a limited number of days at peak times during the winter. Through December 31, 2016, Cove Point

had 800,000 Dths/day of regasification and firm transportation capacity under contract with Statoil, one of the Import Shippers, which decreased to a maximum of 277,650 Dths/day of such capacity through its expiration in the second quarter of 2017.

In 2017, the Import Shippers comprised approximately 25% of total consolidated operating revenues for Dominion Energy Midstream. Cove Point’s customers are required to pay fixed monthly charges, regardless of whether they use the amount of

capacity they have paid to reserve at the Cove Point LNG Facility. The available storage and most of the transportation capacity of the Cove Point LNG Facility will be utilized in connection with the Liquefaction Project.

COVE POINT’S PIPELINE FACILITIES

The Cove Point Pipeline is a 36-inch diameter bi-directional underground,

interstate natural gas pipeline that extends approximately 88 miles from the Cove Point LNG Facility to interconnections with pipelines owned by Transco in Fairfax County, Virginia, and with Columbia Gas Transmission LLC and DETI, both in Loudoun

County, Virginia. In 2009, the original pipeline was expanded to include a 36-inch diameter loop that extends approximately 48 miles, roughly 75% of which is parallel to the

original pipeline. Cove Point has two compressor stations, with approximately 30,840 installed compressor horsepower, at its interconnections with the three upstream interstate pipelines. The

Loudoun Compressor Station is located at the western end of the Cove Point Pipeline where it interconnects with the pipeline systems of DETI and Columbia Gas Transmission LLC. The Pleasant Valley Compressor Station is located roughly 13 miles to the

southeast of the Loudoun Compressor Station, where the Cove Point Pipeline interconnects with Transco’s pipeline system.

Cove Point

offers open-access transportation services, including firm transportation, off-peak firm transportation and interruptible transportation, with cost-based rates and terms and conditions that are subject to the

jurisdiction of FERC. Firm transportation services are generally provided based on a reservation-based fee that is designed to recover Cove Point’s fixed costs and earn a reasonable return. The firm transportation customers are required to pay

fixed monthly fees, regardless of whether they use their reserved capacity for the Cove Point Pipeline. Cove Point also provides certain incrementally priced, firm transportation services that are associated with expansion projects. The Export

Customers will be responsible for procuring their own natural gas supplies and transporting such supplies to the Cove Point Pipeline, which serves as the primary method of transportation of natural gas supplies to or from the Cove Point LNG

Facilities.

In June 2015, Cove Point executed two binding precedent agreements for the approximately $150 million Eastern Market

Access Project. In January 2018, Cove Point received FERC authorization to construct and operate the project facilities, which are expected to be placed into service in early 2019.

COVE POINT’S EXPORT/LIQUEFACTION FACILITIES

The Liquefaction Project, which will consist of one LNG train with a design nameplate outlet capacity of 5.25 Mtpa, is expected to be placed in service in

March 2018. Under normal operating conditions and after accounting for maintenance downtime and other losses, the firm contracted capacity for LNG loading onto ships will be approximately 4.6 Mtpa (0.66 Bcfe/day). Cove Point has authorization from

the DOE to export up to 0.77 Bcfe/day (approximately 5.75 Mtpa) should the liquefaction facilities perform better than expected. The Liquefaction Project will enable the Cove Point LNG Facility to liquefy domestically produced natural gas and export

it as LNG. The Liquefaction Project has been constructed on land already owned by Cove Point, which is within the developed area of the existing Cove Point LNG Facility, and will be integrated with a number of the facilities that are currently

operational. Domestic natural gas will be delivered to the Cove Point LNG Facility through the Cove Point Pipeline for liquefaction and will be exported as LNG. The total costs of developing the Liquefaction Project are estimated to be approximately

$4.1 billion, excluding financing costs. Through December 31, 2017, Cove Point incurred $4.0 billion of development and construction costs associated with the Liquefaction Project. Dominion Energy has indicated that it intends to

provide the funding necessary for the remaining costs for the Liquefaction Project, but it is under no obligation to do so.

Many of the

existing facilities at the Cove Point LNG Facility will be used to provide the liquefaction service. The Liquefaction Project will utilize existing storage tanks at the Cove Point LNG

Facility to store LNG produced by the new liquefaction facilities. The Liquefaction Project will utilize the existing off-shore two-berth pier and insulated LNG and gas piping from the pier to the on-shore Cove Point LNG Facility. Cove Point is constructing new facilities to liquefy the natural gas on

land it already owns (which encompasses more than 1,000 acres). No change will be made to the Cove Point LNG Facility’s current storage, import, or regasification capabilities and only minor modifications will be made to the Cove Point LNG

Facility itself, such as adding piping tie-ins and electrical/control connections to integrate the liquefaction facility with the existing LNG regasification facilities.

COVE POINT’S EXPORT CUSTOMERS

Cove Point has executed service contracts for the Liquefaction Project with the Export Customers, each of which has contracted for 50% of the available

capacity. The Export Customers together will have firm access to 6.8 Bcfe of the existing storage capacity, with the balance of the existing storage capacity available for Cove Point’s existing Import Shippers and Storage Customers. The Export

Customers have each entered into a 20-year agreement for the liquefaction and export services, which they may annually elect to switch to import services, provided that the other Export Customer agrees to

switch. In addition, each of the Export Customers has entered into an accompanying 20-year service agreement for firm transportation on the Cove Point Pipeline.

Upon commercial operation of the Liquefaction Project, a substantial portion of Cove Point’s revenues will be dependent upon the payment

of these two customers. Cove Point’s future results and liquidity are primarily dependent upon the payment of the Export Customers under their respective contracts, and on their continued willingness and ability to perform their contractual

obligations.

Cove Point will provide terminal services for the Export Customers as a tolling service, and the Export Customers will be

responsible for procuring their own natural gas supplies and transporting such supplies to or from the Cove Point LNG Facilities. To deliver the feed gas for liquefaction to the Cove Point LNG Facility, each Export Customer entered into a firm

transportation service agreement to utilize the Cove Point Pipeline, with a maximum firm transportation quantity of 430,000 Dths/day for each Export Customer. This amount of firm transportation capacity will enable Export Customers to deliver to the

Cove Point LNG Facility the feed gas, including fuel, required on days of peak liquefaction, utilizing both their firm liquefaction rights and an expected level of authorized overrun service. In the event of an election of import/regasification

service, each of the Export Customers will have a regasification capacity of 330,000 Dths/day.

DECG

DECG operates as an open access, transportation-only interstate pipeline company in South Carolina and southeastern Georgia. At December 31, 2017,

DECG’s natural gas system consisted of nearly 1,500 miles of transmission pipeline of up to 24 inches in diameter and five compressor stations with approximately 34,500 installed compressor horsepower. DECG’s system transports gas to its

customers from the transmission systems of Southern Natural Gas Company at Port Wentworth, Georgia and Aiken County,

South Carolina; Southern LNG, Inc. at Elba Island, near Savannah, Georgia; Elba Express Company at Port Wentworth, Georgia; and Transco in Cherokee and Spartanburg counties in South Carolina. All

of DECG’s operations are regulated by FERC.

DECG’s customers include SCE&G (which uses natural gas for electricity

generation and for gas distribution to retail customers), SCANA Energy Marketing, Inc. (which markets natural gas to industrial and “sale for resale” customers, primarily in the southeastern U.S.), municipalities, county gas authorities,

federal and state agencies, marketers, power generators and industrial customers primarily engaged in the manufacturing or processing of ceramics, paper, metal and textiles.

DECG’s revenues are primarily derived from reservation charges for firm services as provided for in its FERC-approved tariff. DECG’s

pipeline system has contracted pipeline capacity of approximately 790,073 Dths/day. More than 90% of this capacity is contracted beyond 2019.

In 2014, DECG executed three binding precedent agreements for the approximately $125 million Charleston Project. In February 2017, DECG

received FERC authorization to construct and operate the project facilities, which are expected to be placed into service in March 2018. The Charleston Project is supported by long-term contracts with terms ranging from 10 to 30 years.

Dominion Energy Questar Pipeline

Dominion Energy Questar Pipeline

owns and operates interstate natural gas pipelines and storage facilities in the western U.S., providing natural gas transportation and underground storage services in Utah, Wyoming and Colorado. Dominion Energy Questar Pipeline’s operations

are primarily regulated by FERC. At December 31, 2017, Dominion Energy Questar Pipeline owned and operated nearly 2,200 miles of natural gas transportation pipelines across northeastern and central Utah, northwestern Colorado and southwestern

Wyoming. Dominion Energy Questar Pipeline’s system ranges in diameter from lines that are less than four inches to 36 inches. Dominion Energy Questar Pipeline owns 18 transmission and storage compressor stations with approximately 221,200

combined installed compressor horsepower. Dominion Energy Questar Pipeline also owns gathering lines as well as processing facilities near Price, Utah, which provide for dew-point control to meet gas-quality specifications of downstream pipelines. Additionally, Dominion Energy Questar Pipeline owns and operates 50% of White River Hub, an 11-mile FERC-regulated natural

gas transportation pipeline in western Colorado, which is accounted for under the equity method.

Dominion Energy Questar Pipeline’s

transportation customers include its affiliate, Questar Gas Company, which provides the largest share of transportation revenues, as well as Enterprise Gas Processing, LLC, Rockies Express Pipeline LLC, Citadel Energy Marketing LLC, Wyoming

Interstate Company, LLC, Pacificorp, Encana Marketing (USA) Inc. and other unaffiliated end-users, marketers and producers in the Rocky Mountain region. The Dominion Energy Questar Pipeline systems

interconnect with several major, unaffiliated natural gas pipeline systems owned by Kern River Gas Transmission Company, Ruby Pipeline, LLC, Rockies Express Pipeline, LLC, Northwest Pipeline, LLC, Wyoming Interstate Company, TransColorado Gas

Transmission Company, LLC, and others.

Dominion Energy Questar Pipeline’s transportation revenues are primarily derived from

reservation charges for firm services as provided for in its FERC-approved tariff. At December 31, 2017, Dominion Energy Questar Pipeline’s pipeline system had contracted pipeline capacity of approximately 5,787,630 Dths/day. Approximately

16% of that capacity is committed to by Dominion Energy Questar Pipeline’s affiliate, Questar Gas Company. Of the total committed capacity, approximately 14% relates to contracts that expire in 2018, 80% relates to contracts that expire in 2019

or beyond, and the remaining 6% of contracts operate under evergreen contracts that contain customary termination features. Dominion Energy Questar Pipeline expects that the contracts expiring in 2018, including those with Questar Gas Company, will

be renewed under similar terms as the existing agreements.

Dominion Energy Questar Pipeline owns four natural gas storage facilities

totaling 55.8 Bcf of working gas storage capacity. The Clay Basin storage facility in northeastern Utah has a certificated capacity of 120.2 Bcf, including 54.0 Bcf of working gas. In addition, Dominion Energy Questar Pipeline owns three smaller

storage aquifers in northeastern Utah and western Wyoming.

Dominion Energy Questar Pipeline’s natural gas storage customers include

its affiliate, Questar Gas Company, which provides the largest share of storage revenues, as well as Puget Sound Energy Inc., Intermountain Gas Company and other unaffiliated customers.

Dominion Energy Questar Pipeline’s natural gas storage revenues are primarily derived from long-term contracts for storage capacity at

the Clay Basin storage facility. Approximately 27% of the total storage working gas capacity is contracted with Questar Gas Company. Of the total contracted working gas capacity, 15% of the volumes expire in 2018 while the remaining 85% are

contracted through 2019 or beyond. The contracts that expire in 2018 are all expected to be renewed under similar terms as the existing agreements.

In March 2017, Dominion Energy Questar Pipeline committed to upgrade certain facilities and increase capacity, including the Hyrum Project,

and entered into agreements to provide firm transportation service to Questar Gas Company, an affiliate, through 2027. Total costs of these projects are expected to be approximately $10 million through 2027.

In December 2017, Dominion Energy Questar Pipeline filed with FERC to convert a portion of existing interruptible storage capacity to firm

capacity and increase the minimum required deliverability at the Clay Basin storage facility by the end of 2018. Total costs of this project are estimated to be approximately $5 million.

Iroquois

Iroquois is a Delaware limited partnership which owns and

operates a 416-mile FERC-regulated interstate natural gas pipeline providing service to local gas distribution companies, electric utilities and electric power generators, as well as marketers and other end

users, through interconnecting pipelines and exchanges. Iroquois’ pipeline extends from the U.S.-Canadian border at Waddington, New York through the state of Connecticut to South Commack, Long Island, New York and continuing on from Northport,

Long Island, New York through the Long Island Sound to Hunts Point, Bronx, New York. At December 31, 2017,

Dominion Energy Midstream holds a 25.93% noncontrolling partnership interest in Iroquois, which is accounted for under the equity method.

RELATIONSHIP WITH DOMINION ENERGY

We view our relationship with Dominion Energy as a significant competitive strength. We believe this relationship will provide us with potential acquisition

opportunities from a broad portfolio of existing midstream assets that meet our strategic objectives, as well as access to personnel with extensive technical expertise and industry relationships. Dominion Energy has granted us a right of first offer

with respect to any future sale of its common equity interests in Cove Point. We may also acquire newly issued common equity or additional preferred equity interests in Cove Point in the future, provided that any issuances of additional equity

interests in Cove Point would require both our and Dominion Energy’s approval. Any additional equity interests that we acquire in Cove Point would allow us to participate in the significant growth in cash flows and income expected following

operational commencement of the Liquefaction Project. In connection with the Offering, Dominion Energy also granted us a right of first offer with respect to any future sale of its indirect ownership interest in Blue Racer, which is a midstream

company focused on the Utica Shale formation, and its indirect ownership interest in Atlantic Coast Pipeline, which is focused on constructing a natural gas pipeline running from West Virginia through Virginia to North Carolina. In addition,

acquisition opportunities, such as the DECG Acquisition and the Dominion Energy Questar Pipeline Acquisition, may arise from future midstream pipeline, terminaling, processing, transportation and storage assets acquired or constructed by Dominion

Energy.

Dominion Energy, headquartered in Richmond, Virginia, is one of the nation’s largest producers and transporters of energy.

Dominion Energy’s strategy is to be a leading provider of electricity, natural gas and related services to customers primarily in the eastern and Rocky Mountain regions of the U.S. At December 31, 2017, Dominion Energy served nearly

6 million utility and retail energy customers and operates one of the nation’s largest underground natural gas storage systems, with approximately 1 trillion cubic feet of storage capacity. Dominion Energy’s portfolio of midstream

pipeline, terminaling, processing, transportation and storage assets includes its indirect ownership interests in Blue Racer and Atlantic Coast Pipeline, both of which are described in more detail below, and the assets and operations of Dominion

Energy Gas and Dominion Energy Questar. Dominion Energy Gas consists primarily of (i) The East Ohio Gas Company d/b/a Dominion Energy Ohio, a regulated natural gas distribution company, (ii) DETI, an interstate natural gas transmission

pipeline company, and (iii) Dominion Iroquois, Inc., which holds a 24.07% noncontrolling partnership interest in Iroquois. Dominion Energy Questar consists primarily of Questar Gas Company, a regulated natural gas distribution company, and

Wexpro, a natural gas exploration and production company which supplies natural gas to Questar Gas Company under a cost-of-service framework.

Blue Racer is a midstream energy company focused on the design, construction, operation and acquisition of midstream assets. Blue Racer is

investing in natural gas gathering and

processing assets in Ohio and West Virginia, targeting primarily the Utica Shale formation, and is an equal partnership between Dominion Energy and Caiman, with Dominion Energy contributing

midstream assets, including both gathering and processing assets, and Caiman contributing private equity capital. Midstream services offered by Blue Racer include gathering, processing, fractionation, and natural gas liquids transportation and

marketing. Blue Racer is expected to develop additional new capacity designed to meet producer needs as the development of the Utica Shale formation increases.

Atlantic Coast Pipeline is a limited liability company owned at December 31, 2017 by Dominion Energy (48%), Duke (47%) and Southern

Company Gas (5%). Atlantic Coast Pipeline is focused on constructing an approximately 600-mile natural gas pipeline running from West Virginia through Virginia to North Carolina to increase natural gas

supplies in the region. Construction of the pipeline is subject to receiving all necessary regulatory and other approvals, including without limitation CPCNs from FERC and all required environmental permits. In October 2017, Atlantic Coast Pipeline

received the FERC order authorizing the construction and operation of the project, subject to other pending federal and state approvals, with the facilities expected to be in service in late 2019. DETI will provide the services necessary to oversee

the construction of, and to subsequently operate and maintain, the facilities and projects undertaken by, and subject to the approval of, Atlantic Coast Pipeline. The pipeline is expected to serve as a new, independent route for transportation of

shale and conventional interstate gas supplies for markets in the mid-Atlantic region of the U.S.

At December 31, 2017, Dominion Energy is our largest unitholder, holding 18,504,628 common units (27% of all outstanding), 11,365,628

Series A Preferred Units (38% of all outstanding) and 31,972,789 subordinated units (100% of all outstanding). Dominion Energy also owns our general partner and owns 100% of our IDRs. As a result of its significant ownership interests in us, we

believe Dominion Energy will be motivated to support the successful execution of our business strategies and will provide us with acquisition opportunities, although it is under no obligation to do so. Dominion Energy views us as a significant part

of its growth strategy, and we believe that Dominion Energy will be incentivized to contribute or sell additional assets to us and to pursue acquisitions jointly with us in the future. However, Dominion Energy will regularly evaluate acquisitions

and dispositions and may, subject to compliance with our right of first offer with respect to Cove Point, Blue Racer and Atlantic Coast Pipeline, elect to acquire or dispose of assets in the future without offering us the opportunity to participate

in those transactions. Moreover, Dominion Energy will continue to be free to act in a manner that is beneficial to its interests without regard to ours, which may include electing not to present us with future acquisition opportunities.

See Note 22 to the Consolidated Financial Statements for a discussion of the significant contracts entered into with Dominion Energy.

COMPETITION

All of the regasification and

storage capacity of the Cove Point LNG Facility, and all of the transportation capacity of the Cove Point Pipeline is either under contract or expected to be utilized by the Liquefaction Project. The Liquefaction Project’s capacity is also

fully contracted under long-term fixed reservation fee agreements. However, in the future Cove Point may compete with other independent terminal operators as well as major oil and gas companies on the basis of terminal location, services provided

and price. Competition from terminal operators primarily comes from refiners and distribution companies with marketing and trading arms.

DECG’s pipeline system generates a substantial portion of its revenue from long-term firm contracts for transportation services and is

therefore insulated from competitive factors during the terms of the contracts. When these long-term contracts expire, DECG’s pipeline system faces competitive pressures from similar facilities that serve the South Carolina and southeastern

Georgia area in terms of location, rates, terms of service, and flexibility and reliability of service.

Dominion Energy Questar

Pipeline’s pipeline system generates a substantial portion of its revenue from long-term firm contracts for transportation and storage services and is therefore insulated from competitive factors during the terms of the contracts. When these

long-term contracts expire, Dominion Energy Questar Pipeline’s pipeline system and storage facilities face competitive pressures from similar facilities in the Rocky Mountain region in terms of location, rates, terms of service and availability

and reliability of service.

REGULATION

Dominion Energy Midstream is

subject to regulation by various federal, state and local authorities, including the SEC, FERC, EPA, DOE, DOT and Maryland Commission.

FERC Regulation

The design, construction and operation of interstate natural gas pipelines, LNG terminals (including the Liquefaction Project) and other facilities, the

import and export of LNG, and the transportation of natural gas are all subject to various regulations, including the approval of FERC under Section 3 (for LNG terminals) and Section 7 (for interstate transportation facilities) of the NGA,

as well as the Natural Gas Policy Act of 1978, as amended, to construct and operate the facilities. For the Cove Point LNG Facility, Cove Point is required to maintain authorization from FERC under Section 3 and Section 7 of the NGA. The

design, construction and operation of the Cove Point LNG Facility and its proposed Liquefaction Project, and the import and export of LNG, are highly regulated activities. FERC’s approval under Section 3 and Section 7 of the NGA, as

well as several other material governmental and regulatory approvals and permits, are required for the proposed Liquefaction Project. DECG and Dominion Energy Questar Pipeline are required to maintain authorization from FERC under Section 7 of

the NGA.

Under the NGA, FERC is granted authority to approve, and if necessary, set “just and reasonable rates” for the

transportation, including storage, or sale of natural gas in interstate commerce. In

addition, under the NGA, with respect to the jurisdictional services, we are not permitted to unduly discriminate or grant undue preference as to our rates or the terms and conditions of service.

FERC has the authority to grant certificates allowing construction and operation of facilities used in interstate gas transportation and authorizing the provision of services. Under the NGA, FERC’s jurisdiction generally extends to the

transportation of natural gas in interstate commerce, to the sale in interstate commerce of natural gas for resale for ultimate consumption for domestic, commercial, industrial, or any other use, and to natural gas companies engaged in such

transportation or sale. However, FERC’s jurisdiction does not extend to the production or local distribution of natural gas.

In

general, FERC’s authority to regulate interstate natural gas pipelines and the services that they provide includes:

| |

• |

|

Rates and charges for natural gas transportation and related services; |

| |

• |

|

The certification and construction of new facilities; |

| |

• |

|

The extension and abandonment of services and facilities; |

| |

• |

|

The maintenance of accounts and records; |

| |

• |

|

The acquisition and disposition of facilities; |

| |

• |

|

The initiation and discontinuation of services; and |

In November 2016, pursuant to the terms of a previous settlement, Cove

Point filed a general rate case for its FERC-jurisdictional services, with 23 proposed rates to be effective January 1, 2017. Cove Point proposed an annual

cost-of-service of approximately $140 million. In December 2016, FERC accepted a January 1, 2017 effective date for all proposed rates but five which were

suspended to be effective June 1, 2017. Under the terms of the settlement agreement filed by Cove Point in August 2017 and approved by FERC in November 2017, Cove Point’s rates effective October 2017 result in decreases to annual revenues

and depreciation expense of approximately $17.7 million and $3.0 million, respectively, compared to the rates in effect through December 2016. In addition, to the extent market conditions exist that neither import nor export services

are being sufficiently utilized and LNG cooling quantities are required, the Import Shippers’ responsibility for costs incurred for any LNG cooling quantities received prior to the earlier of operational commencement of the Liquefaction Project

or March 2018 would be reduced to approximately half of such amounts incurred. If the Liquefaction Project has not commenced operations prior to March 2018 and LNG cooling quantities are required, Cove Point is responsible for any costs incurred

until the Liquefaction Project commences operations. Upon operational commencement of the Liquefaction Project, the Import Shippers will have responsibility for costs incurred on certain LNG cooling quantities.

In connection with Dominion Energy’s acquisition of DECG on January 31, 2015, Dominion Energy agreed to a rate moratorium which

precludes DECG from filing a Section 4 NGA general rate case to establish base rates that would have been effective prior to January 1, 2018.

LIQUEFACTION PROJECT

In

April 2013, Cove Point filed its application with FERC requesting authorization to construct, modify and operate the Liquefaction Project, as well as enhance the Cove Point Pipeline. In May 2014, FERC staff issued its EA for the Liquefaction

Project.

In the EA, FERC staff addressed a variety of topics related to the proposed construction and development of the Liquefaction Project and its potential impact to the environment, including in the

areas of geology, soils, groundwater, surface waters, wetlands, vegetation, wildlife and aquatic resources, special status species, land use, recreation, socioeconomics, air quality and noise, reliability and safety, and cumulative impacts. In

September 2014, Cove Point received the FERC Order which authorized the construction and operation of the Liquefaction Project. In the FERC Order, FERC concluded that if constructed and operated in accordance with Cove Point’s application and

supplements, and in compliance with the environmental conditions set forth in the FERC Order, the Liquefaction Project would not constitute a major federal action significantly affecting the quality of the human environment. In October 2014, Cove

Point commenced construction of the Liquefaction Project.

Two parties previously separately filed petitions for review of the FERC Order

in the U.S. Court of Appeals for the D.C. Circuit, which petitions were consolidated. In July 2016, the court denied one party’s petition for review of the FERC Order. The court also issued a decision remanding the other party’s

petition for review of the FERC Order to FERC for further explanation of how FERC’s decision that a previous transaction with an existing import shipper was not unduly discriminatory. In September 2017, FERC issued its order on remand from

the U.S. Court of Appeals for the D.C. Circuit, and reaffirmed its rulings in its prior orders that Cove Point did not violate the prohibition against undue discrimination by agreeing to a capacity reduction and early contract termination with the

existing import shipper. In October 2017, the party filed a request for rehearing of the FERC Order on remand. This case is pending.

Energy Policy Act of 2005

The EPACT and FERC’s policies promulgated thereunder contain numerous provisions relevant to the natural gas industry and to interstate

pipelines. Failure to comply with these laws and regulations may result in the assessment of administrative, civil and criminal penalties. Additionally, the EPACT amended Section 3 of the NGA to establish or clarify FERC’s exclusive

authority to approve or deny an application for the siting, construction, expansion or operation of LNG terminals, although except as specifically provided in the EPACT, nothing in the EPACT is intended to affect otherwise applicable law related to

any other federal agency’s authorities or responsibilities related to LNG terminals. The EPACT amended the NGA to, among other things, prohibit market manipulation. In accordance with the EPACT, FERC issued a final rule making it unlawful for

any entity, in connection with the purchase or sale of natural gas or transportation service subject to FERC’s jurisdiction, to defraud, make an untrue statement or omit a material fact or engage in any practice, act or course of business that

operates or would operate as a fraud.

DOE Regulation

Prior to

importing or exporting LNG, Cove Point must receive approvals from the DOE. Cove Point previously received import authority in connection with the construction and operation of the Cove Point LNG Facility and more recently also received authority to

export the commodity.

In October 2011, the DOE granted FTA Authorization for the export of up to 1.0 Bcfe/day of

natural gas to countries that have or will enter into an FTA for trade in natural gas. In September 2013, the DOE also granted Non-FTA Authorization approval for the export of up to 0.77 Bcfe/day of natural

gas to countries that do not have an FTA for trade in natural gas. The FTA Authorization and Non-FTA Authorization have 25- and

20-year terms, respectively. In June 2016, a party filed a petition for review of the DOE’s Non-FTA Authorization approval in the U.S. Court of Appeals for the D.C.

Circuit. In November 2017, the U.S. Court of Appeals for the D.C. Circuit issued an order denying the petition for review.

In July 2017,

Cove Point submitted an application for a temporary operating permit to the Maryland Department of the Environment, as required prior to the date of first production of LNG for commercial purposes of exporting LNG. The permit was received in

December 2017.

DOT Regulation

The Cove Point Pipeline, DECG

and Dominion Energy Questar Pipeline are subject to regulation by the DOT, under the PHMSA, pursuant to which PHMSA has established requirements relating to the design, installation, testing, construction, operation, replacement and management of

pipeline and underground natural gas storage facilities. The NGPSA requires certain pipelines to comply with safety standards in constructing and operating the pipelines and subjects the pipelines to regular inspections.

The PSIA, which is administered by the DOT Office of Pipeline Safety, governs the areas of testing, education, training and communication. The

PSIA requires pipeline companies to perform extensive integrity tests on natural gas transportation pipelines that exist in high population density areas designated as “high consequence areas.” Pipeline companies are required to perform

the integrity tests on a seven-year cycle. The risk ratings are based on numerous factors, including the population density in the geographic regions served by a particular pipeline, as well as the age and condition of the pipeline and its

protective coating. Testing consists of hydrostatic testing, internal electronic testing or direct assessment of the piping. In addition to the pipeline integrity tests, pipeline companies must implement a qualification program to make certain that

employees are properly trained. Pipeline operators also must develop integrity management programs for gas transportation pipelines, which requires pipeline operators to perform ongoing assessments of pipeline integrity; identify and characterize

applicable threats to pipeline segments that could impact a high consequence area; improve data collection, integration and analysis; repair and remediate the pipeline, as necessary; and implement preventive and mitigation actions.

The Cove Point Pipeline, DECG and Dominion Energy Questar Pipeline are subject to the Pipeline Safety, Regulatory Certainty, and Jobs Creation

Act of 2011, which regulates safety requirements in the design, construction, operation and maintenance of interstate natural gas transmission and underground storage facilities. Our underground natural gas storage facilities are subject to DOT

regulation through PHMSA, which oversees the safety, security, monitoring and compliance of such facilities.

State Regulation

The Maryland Commission regulates electricity suppliers, fees for pilotage services to vessels, construction of generating stations and

certain common carriers engaged in the transportation for hire of persons in the state of Maryland. See Note 19 to the Consolidated Financial Statements for additional information.

Worker Health and Safety

Dominion Energy Midstream is subject to a

number of federal and state laws and regulations, including OSHA, and comparable state statutes, whose purpose is to protect the health and safety of workers. Dominion Energy Midstream has an internal safety, health and security program designed to

monitor and enforce compliance with worker safety requirements and routinely reviews and considers improvements in its programs. Cove Point is also subject to the U.S. Coast Guard’s Maritime Security Standards for Facilities, which are designed

to regulate the security of certain maritime facilities. Dominion Energy Midstream believes that it is in material compliance with all applicable laws and regulations related to worker health and safety. Notwithstanding these preventative measures,

incidents may occur, including those outside of Dominion Energy Midstream’s control.

ENVIRONMENTAL

REGULATION

General

Dominion Energy

Midstream’s operations are subject to stringent, comprehensive and evolving federal, regional, state and local laws and regulations governing environmental protection. These laws and regulations may, among other things, require the acquisition

of permits or other approvals to conduct regulated activities, restrict the amounts and types of substances that may be released into the environment, limit operational capacity of the facilities, require the installation of environmental controls,

limit or prohibit construction activities in sensitive areas such as wetlands or areas inhabited by endangered or threatened species and impose substantial liabilities for pollution resulting from operations. The cost of complying with applicable

environmental laws, regulations and rules is expected to be material. Failure to comply with these laws and regulations may also result in the assessment of administrative, civil and criminal penalties, the imposition of investigatory and remedial

obligations and the issuance of orders enjoining some or all of Dominion Energy Midstream’s operations in affected areas.

Dominion

Energy Midstream has applied for or obtained the necessary environmental permits for the construction and operation of its facilities. Many of these permits are subject to reissuance and continuing review. Additional information related to Dominion

Energy Midstream’s environmental compliance matters, including current and planned capital expenditures relating to environmental compliance, can be found in Future Issues and Other Matters in Item 7. MD&A.

Air Emissions

The regulation of air emissions under the CAA and

comparable state laws and regulations restrict the emission of air pollutants from many sources and also impose various monitoring and reporting requirements. The CAA new source review regulations require us to obtain

pre-approval for the construction or modification of certain projects or facilities expected to produce or significantly increase air emissions, obtain and strictly comply

with stringent air permit requirements or install and operate specific equipment or technologies to control emissions. Obtaining necessary air permits has the potential to delay the development

of our projects.

The regulation of air emissions under the CAA requires that we obtain various construction and operating permits,

including Title V air permits, and incur capital expenditures for the installation of certain air pollution control devices at our facilities. We have taken and expect to continue to take certain measures to comply with various regulations specific

to our operations, such as National Emission Standards for Hazardous Air Pollutants, New Source Performance Standards, new source review and federal and state regulatory measures imposed to meet national ambient air quality standards. We have

incurred, and expect to continue to incur, substantial capital expenditures to maintain compliance with these and other air emission regulations that have been promulgated or may be promulgated or revised in the future.

Global Climate Change

The national and international attention in

recent years on GHG emissions and their relationship to climate change has resulted in federal, regional and state legislative and regulatory action in this area. Dominion Energy Midstream supports national climate change legislation that would

provide a consistent, economy-wide approach to addressing this issue and is currently taking action to protect the environment and address climate change while meeting the future needs of its customers. Dominion Energy Midstream’s CEO and its

management are responsible for compliance with the laws and regulations governing environmental matters, including climate change.

In

response to findings that emissions of GHGs present an endangerment to public health and the environment, the EPA adopted regulations under existing provisions of the CAA in April 2010, that require a reduction in emissions of GHGs from motor

vehicles. These rules took effect in January 2011 and established GHG emissions as regulated pollutants under the CAA. In June 2014, the U.S. Supreme Court ruled that the EPA lacked the authority under the CAA to require PSD or Title V permits for

stationary sources based solely on GHG emissions. However, the Court upheld the EPA’s ability to require best available control technology for GHG for sources that are otherwise subject to PSD or Title V permitting for conventional pollutants.

In August 2016, the EPA issued a draft rule proposing to reaffirm that a GHG source’s obligation to obtain a PSD or Title V permit for GHG’s is triggered only if such permitting requirements are first triggered by non-GHG, or conventional, pollutants that are regulated by the new source review program, and to set a significant emissions rate at 75,000 tons per year of

CO2 equivalent emissions under which a source would not be required to apply best available control technology for its GHG emissions. Due to uncertainty regarding what additional actions states

may take to amend their existing regulations and what action the EPA ultimately takes to address the court ruling under a new rulemaking, we cannot predict the impact to the financial statements at this time.

In January 2015, as part of its Climate Action Plan, the EPA announced plans to reduce methane emissions from the oil and gas sector including

natural gas processing and transmission sources. In July 2015, the EPA announced the next generation of its

voluntary Natural Gas Star Program. The program covers the entire natural gas sector from production to distribution, with more emphasis on transparency and increased reporting for both annual

emissions and reductions achieved through implementation measures. DECG joined the EPA’s voluntary Natural Gas Star Program in July 2016 and submitted an implementation plan in September 2016.

Maryland, along with eight other Northeast states, has implemented regulations requiring reductions in CO2 emissions through the RGGI, a cap and trade program covering CO2 emissions from electric generating units in the Northeast. The CPCN

required that the Liquefaction Project submit a Climate Action Plan to the Maryland Department of the Environment and gain approval of the plan. The Dominion Energy Cove Point Liquefaction Facility Climate Action Plan was approved in November 2017.

Additionally, by not connecting to the larger grid, the Liquefaction Project generating station is exempt from purchasing RGGI carbon emission allowances. Furthermore, the CPCN requires Cove Point to make payments over time totaling approximately

$48 million to the SEIF and Maryland low income energy assistance programs.

GHG EMISSIONS

Dominion Energy began tracking and reporting GHG emissions at the Cove Point LNG Facility in 2010 under the EPA’s GHG Reporting Program and voluntarily

tracked such emissions prior to 2010. A comprehensive methane leak survey is conducted each year in accordance with the EPA rule to detect leaks and to quantify leaks from compressor units.

Annual GHG emissions at the Cove Point LNG Facility have remained fairly constant from 2011 to 2016, ranging from 141,250 to 183,800 metric

tons of CO2 equivalent. Approximately 95% of these emissions are CO2 emissions from combustion sources, such as compressor engines and

heaters. Only 5% of the annual Cove Point GHG emissions comes from methane emissions. Compared to other fossil fuels, natural gas has a much lower carbon emission rate with an ample regional supply, promoting energy and economic security. In 2016,

annual GHG emissions from Dominion Energy Midstream’s facilities, including the Cove Point LNG Facility, five compressor stations and pipeline blowdown emissions between compressor stations in South Carolina and two compressor stations in

Virginia were approximately 285,600 metric tons of CO2 equivalent emissions. The 2016 GHG emissions above do not include Dominion Energy Questar Pipeline, which became part of Dominion Energy

Midstream in December 2016.

Water

The CWA is a comprehensive

program requiring a broad range of regulatory tools including a permit program with strong enforcement mechanisms to authorize and regulate discharges to surface waters. Dominion Energy Midstream must comply with applicable aspects of the CWA

programs at its operating facilities. Dominion Energy Midstream has applied for or obtained the necessary environmental permits for the operation of its facilities.

The CWA and analogous state laws impose restrictions and strict controls regarding the discharge of effluent into surface waters. Pursuant to

these laws, permits must be obtained to

discharge into state waters or waters of the U.S. Any such discharge into regulated waters must be performed in accordance with the terms of the permit issued by the EPA or the analogous state

agency. Spill prevention, control and countermeasure requirements under federal and state law require appropriate containment berms and similar structures to help prevent the accidental release of petroleum into the environment. In addition, the CWA

and analogous state laws require individual permits or coverage under general permits for discharges of storm water runoff from certain types of activities. Stormwater related to construction activities is also regulated under the CWA and by state

and local stormwater management and erosion and sediment control laws.

From time to time, Dominion Energy Midstream’s projects and

operations may potentially impact tidal and non-tidal wetlands. In these instances, Dominion Energy Midstream must obtain authorization from the appropriate federal, state and local agencies prior to impacting

a subject wetland. The authorizing agency may impose significant direct or indirect mitigation costs to compensate for regulated impacts to wetlands. The approval timeframe may also be extended and potentially affect project schedules resulting in a