Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - WEST PHARMACEUTICAL SERVICES INC | ex322cfo906certification_2.htm |

| EX-32.1 - EXHIBIT 32.1 - WEST PHARMACEUTICAL SERVICES INC | ex321ceo906certification_2.htm |

| EX-31.2 - EXHIBIT 31.2 - WEST PHARMACEUTICAL SERVICES INC | ex312cfo302certification_2.htm |

| EX-31.1 - EXHIBIT 31.1 - WEST PHARMACEUTICAL SERVICES INC | ex311ceo302certification_2.htm |

| EX-23 - EXHIBIT 23 - WEST PHARMACEUTICAL SERVICES INC | ex23consent_2017.htm |

| EX-21 - EXHIBIT 21 - WEST PHARMACEUTICAL SERVICES INC | ex21listofsubsidiaries_2017.htm |

UNITED STATES |

SECURITIES AND EXCHANGE COMMISSION |

Washington, D.C. 20549 |

FORM 10-K |

(Mark One)

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-8036

WEST PHARMACEUTICAL SERVICES, INC. (Exact name of registrant as specified in its charter) |

Pennsylvania | 23-1210010 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

530 Herman O. West Drive, Exton, PA | 19341-0645 |

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: 610-594-2900

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock, par value $.25 per share | New York Stock Exchange |

Securities registered pursuant to Section 12 (g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | þ | Accelerated filer | o | |

Non-accelerated filer | o | (Do not check if a smaller reporting company) | Smaller reporting company | o |

Emerging growth company | o | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the voting stock held by non-affiliates of the registrant as of June 30, 2017 was approximately $6,994,711,952 based on the closing price as reported on the New York Stock Exchange.

As of January 31, 2018, there were 73,986,496 shares of the registrant's common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Document | Parts Into Which Incorporated |

Proxy Statement for the Annual Meeting of Shareholders to be held May 1, 2018 | Part III |

TABLE OF CONTENTS

Page | ||

BUSINESS | ||

RISK FACTORS | ||

UNRESOLVED STAFF COMMENTS | ||

PROPERTIES | ||

LEGAL PROCEEDINGS | ||

MINE SAFETY DISCLOSURES | ||

MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | ||

SELECTED FINANCIAL DATA | ||

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | ||

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | ||

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | ||

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | ||

CONTROLS AND PROCEDURES | ||

OTHER INFORMATION | ||

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | ||

EXECUTIVE COMPENSATION | ||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | ||

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | ||

PRINCIPAL ACCOUNTING FEES AND SERVICES | ||

EXHIBITS, FINANCIAL STATEMENT SCHEDULES | ||

FORM 10-K SUMMARY | ||

2

PART I

Unless otherwise indicated, or the context otherwise requires, references in this report to “the Company”, “we”, “us”, “our” and “West” refer to West Pharmaceutical Services, Inc. and its majority-owned subsidiaries.

All trademarks and registered trademarks used in this report are our property, either directly or indirectly through our subsidiaries unless noted otherwise. Daikyo Crystal Zenith® (“CZ”) is a registered trademark of Daikyo Seiko, Ltd. (“Daikyo”).

Throughout this report, references to “Notes” refer to the Notes to Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K (“Form 10-K”), unless otherwise indicated.

Information in this Form 10-K is current as of February 26, 2018, unless otherwise specified.

ITEM 1. BUSINESS

General

We are a leading global manufacturer in the design and production of technologically advanced, high-quality, integrated containment and delivery systems for injectable drugs and healthcare products. Our products include a variety of primary packaging, containment solutions, reconstitution and transfer systems, and drug delivery systems, as well as contract manufacturing and analytical lab services. Our customers include the leading biologic, generic, pharmaceutical, diagnostic, and medical device companies in the world. Our top priority is delivering quality products that meet the exact product specifications and quality standards customers require and expect. This focus on quality includes excellence in manufacturing, scientific and technical expertise and management, so we can partner with our customers to deliver safe, effective drug products to patients quickly and efficiently.

The Company was incorporated under the laws of the Commonwealth of Pennsylvania on July 27, 1923.

Business Segments

Our business operations are organized into two reportable segments, Proprietary Products and Contract-Manufactured Products.

Proprietary Products Segment

Our Proprietary Products reportable segment offers proprietary packaging, containment and drug delivery products, along with analytical lab services, to biologic, generic and pharmaceutical drug customers. Our packaging products include stoppers and seals for injectable packaging systems, which are designed to help ensure drug compatibility and stability with active drug products, while also supporting operational efficiency for customers. This product portfolio also includes syringe and cartridge components, including custom solutions for the specific needs of injectable drug applications, as well as administration systems that can enhance the safe delivery of drugs through advanced reconstitution, mixing and transfer technologies. We also provide films, coatings, washing and sterilization processes and services to enhance the quality of packaging components and mitigate the risk of contamination and compatibility issues.

This segment's product portfolio also includes drug containment solutions, including CZ, a cyclic olefin polymer, in the form of vials, syringes and cartridges. These products can provide a high-quality solution to glass incompatibility issues and can stand up to cold storage environments, while reducing the risk of breakage that exists with glass. In addition, we offer a variety of self-injection devices, designed to address the need to provide at-home delivery of injectable therapies. These devices are patient-centric technologies that are easy-to-use and can be combined with connected health technologies that have the potential to increase adherence.

3

Analytical lab services completes the product offerings in the Proprietary Products reportable segment. This group provides specialized testing for drug packaging, devices and administration systems. Offering the combination of primary packaging components, containment solutions, and drug delivery devices, as well as analytical lab services, helps to position us as the leader in the integrated containment and delivery of injectable medicines.

This reportable segment has manufacturing facilities in North and South America, Europe, and Asia Pacific, with affiliated companies in Mexico and Japan. See Item 2, Properties, for additional information on our manufacturing and other sites.

See Note 17, Segment Information, for net sales, operating profit and asset information for Proprietary Products.

Contract-Manufactured Products Segment

Our Contract-Manufactured Products reportable segment serves as a fully integrated business, focused on the design, manufacture, and automated assembly of complex devices, primarily for pharmaceutical, diagnostic, and medical device customers. These products include a variety of custom contract-manufacturing and assembly solutions, which use such technologies as multi-component molding, in-mold labeling, ultrasonic welding and clean room molding and device assembly. We manufacture customer-owned components and devices used in surgical, diagnostic, ophthalmic, injectable, and other drug delivery systems, as well as consumer products.

We have vast expertise in product design and development, including in-house mold design, an engineering center for developmental and prototype tooling, process design and validation and high-speed automated assemblies.

This reportable segment has manufacturing operations in North America and Europe. See Item 2, Properties, for additional information on our manufacturing and other sites.

See Note 17, Segment Information, for net sales, operating profit and asset information for Contract-Manufactured Products.

International

We have significant operations outside of the United States (“U.S.”), which are managed through the same business segments as our U.S. operations – Proprietary Products and Contract-Manufactured Products. Sales outside of the U.S. accounted for 54.1% of consolidated net sales in 2017. For a geographic breakdown of sales, see Note 17, Segment Information. See Item 2, Properties, for additional information on our manufacturing and other sites.

Although the general business processes are similar to the domestic business, international operations are exposed to additional risks. These risks include currency fluctuations relative to the U.S. Dollar (“USD”), multiple tax jurisdictions and, particularly in South America and Israel, political and social issues that could destabilize local markets and affect the demand for our products.

See further discussion of our international operations, the risks associated with our international operations, and our attempt to minimize some of these risks in Part I, Item 1A, Risk Factors; Part II, Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations under the caption Financial Condition, Liquidity and Capital Resources; Part II, Item 7A, Quantitative and Qualitative Disclosures About Market Risk; Note 1 under the captions Financial Instruments and Foreign Currency Translation; and Note 9, Derivative Financial Instruments.

Raw Materials

We use three basic raw materials in the manufacture of our products: elastomers, aluminum and plastic. Elastomers include both natural and synthetic materials. We currently have access to adequate supplies of these raw materials to meet our production needs through agreements with suppliers.

4

We employ a supply chain management strategy in our business segments, which involves purchasing from integrated suppliers that control their own sources of supply. Due to regulatory control over our production processes and the cost and time involved in qualifying suppliers, we rely on single-source suppliers for many critical raw materials. We purchase certain raw materials in the open market. This strategy increases the risk that our supply chain may be interrupted in the event of a supplier production or distribution problem. These risks are managed, where possible, by selecting suppliers with multiple manufacturing sites, rigorous quality control systems, surplus inventory levels and other methods of maintaining supply in case of an interruption in production or distribution.

Intellectual Property

Intellectual property, including patents, trade secrets and know-how, is important to our business. We own or license intellectual property rights, including issued patents and pending patent applications in the U.S. and in other countries, that relate to various aspects of our products. Some key value-added and proprietary products and processes are licensed from Daikyo. Our intellectual property rights have been useful in establishing our market position and in the growth of our business, and are expected to continue to be of value in the future.

Seasonality

Although our Proprietary Products business is not inherently seasonal, sales and operating profit in the second half of the year are typically lower than the first half primarily due to scheduled plant shutdowns in conjunction with our customers' production schedules and the year-end impact of holidays on production. This can vary from year-to-year, depending upon customer inventory management programs and customer product launches and other factors.

Our Contract-Manufactured Products business is not inherently seasonal.

Working Capital

We are required to carry significant amounts of inventory to meet customer requirements. In addition, some of our supply agreements require us to purchase inventory in bulk orders, which increases inventory levels but decreases the risk of supply interruption. Levels of inventory are also influenced by the seasonal patterns addressed above. For a more detailed discussion of working capital, please refer to the discussion in Part II, Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations under the caption Financial Condition, Liquidity and Capital Resources.

Marketing

Our Proprietary Products customers include most of the major biologic, generic, and pharmaceutical drug companies in the world, which incorporate our components and other offerings into their products for distribution to the point of care and ultimate end-user - the patient.

Our Contract-Manufactured Products customers include many of the world's largest pharmaceutical, diagnostic, and medical device companies. Contract-Manufactured Products components generally are incorporated into our customers' manufacturing lines for further processing or assembly.

Our products and services are distributed primarily through our own sales force and distribution network, with limited use of contract sales agents and regional distributors.

Our ten largest customers accounted for 37.5% of our consolidated net sales in 2017, but none of these customers individually accounted for more than 10% of net sales. See Note 17, Segment Information, for information on sales by significant product group.

Order Backlog

Order backlog includes firm orders placed by customers for manufacture over a period of time according to their schedule or upon confirmation by the customer. We also have contractual arrangements with a number of our customers. Products covered by these contracts are included in our backlog only as orders are received. Order

5

backlog may be positively or negatively impacted by several factors, including customer ordering patterns and the necessary lead-time to deliver customer orders. Order backlog is one of many measures we use to understand future demand, and should not be considered in isolation to predict future sales growth.

At December 31, 2017 and 2016, the order backlog for Proprietary Products was $377.4 million and $373.3 million, respectively. The increase in backlog reflects the impact of foreign currency, partially offset by the impact of shorter lead-time requirements for customer orders. The majority of the order backlog for Proprietary Products at December 31, 2017 is expected to be filled during 2018.

The majority of Contract-Manufactured Products manufacturing activity is governed by contractual volume expectations, with terms between one and three years, subject to periodic revisions based on customer requirements.

Competition

We compete with several companies across our Proprietary Products product lines. Due to the special nature of our pharmaceutical packaging components and our long-standing participation in the market, competition for these components is based primarily on product design and performance, although total cost is becoming increasingly important as pharmaceutical companies continue with aggressive cost-control programs across their operations.

In addition, there are a number of competitors supplying medical devices and medical device components. We compete in this market on the basis of our reputation for quality and reliability in engineering and project management, as well as our knowledge of, and experience in, compliance with regulatory requirements.

We have specialized knowledge of container closure components, which is integral to developing delivery systems. With our range of proprietary technologies, we compete with new and established companies in the area of drug delivery devices, including suppliers of prefillable syringes, auto-injectors, safety needles and other proprietary systems.

We aim to differentiate ourselves from our competition by being an integrated drug containment and delivery systems global supplier that can provide pre-approval primary packaging support and engineering development, analytical services, regulatory expertise and after-sale technical support. Customers also appreciate the global scope of our manufacturing capability and our ability to produce many products at multiple sites.

Our Contract-Manufactured Products business operates in very competitive markets for its products. The competition varies from smaller regional companies to large global molders. Given the cost pressures they face, many of our customers look off-shore to reduce cost. We aim to differentiate ourselves by leveraging our global capabilities and by employing new technologies such as high-speed automated assembly, insert-molding, multi-shot molding and expertise with multiple-piece closure systems.

Research and Development Activities

We maintain our own research-scale production facilities and laboratories for developing new products, and offer contract engineering design and development services to assist customers with new product development. Our quality control, regulatory and laboratory testing capabilities are used to ensure compliance with applicable manufacturing and regulatory standards for primary and secondary pharmaceutical packaging components and delivery systems. We continue to seek new innovative opportunities for acquisition, licensing, partnering or development of products, services and technologies that serve the injectable drug containment and delivery market. Research and development spending will continue to increase as we pursue innovative strategic platforms in prefillable syringes, injectable containers, advanced injection and safety and administration systems.

Commercial development of our new products and services for medical and pharmaceutical applications commonly requires several years. New products that we develop may require separate approval as medical devices, and products that are intended to be used in the packaging and delivery of pharmaceutical products are subject to both

6

customer acceptance of our products and regulatory approval of the customer's products following our development period.

We spent $39.1 million in 2017, $36.8 million in 2016, and $34.1 million in 2015 on research and development, all of which related to Proprietary Products.

Environmental Regulations

We are subject to various federal, state and local provisions regulating the discharge of materials into the environment or otherwise relating to the protection of the environment. Our compliance with these laws and regulations has not had a material impact on our financial position, results of operations or cash flows. There were no material capital expenditures for environmental control facilities in 2017 and there are no material expenditures planned for such purposes in 2018.

Employees

As of December 31, 2017, we employed approximately 7,500 people in our operations throughout the world, including approximately 7,300 full-time employees.

Available Information

We maintain a website at www.westpharma.com. Our Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available on our website under the Investors - SEC Filings caption as soon as reasonably practical after we electronically file the material with, or furnish it to, the U.S. Securities and Exchange Commission (“SEC”). These filings are also available to the public over the Internet at the SEC's website at www.sec.gov. You may also read and copy any document we file at the SEC's Public Reference Room at 100 F. Street, N.E., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the Public Reference Room.

Throughout this Form 10-K, we incorporate by reference certain information from parts of other documents filed with the SEC and from our Proxy Statement for the 2018 Annual Meeting of Shareholders (“2018 Proxy Statement”), which will be filed with the SEC within 120 days following the end of our 2017 fiscal year. Our 2018 Proxy Statement will be available on our website on or about March 31, 2018, under the caption Investors - Annual Reports & Proxy.

Information about our corporate governance, including our Corporate Governance Principles and Code of Business Conduct, as well as information about our Directors, Board Committees, Committee Charters, and instructions on how to contact the Board, is available on our website under the Investors - Corporate Governance heading. We intend to make any required disclosures regarding any amendments of our Code of Business Conduct or waivers granted to any of our directors or executive officers under the caption Code of Business Conduct on our website. Information relating to the West Pharmaceutical Services Dividend Reinvestment Plan is also available on our website under the Investors - Transfer Agent/Dividend Reinvestment caption.

We will provide any of the foregoing information without charge upon written request to our Corporate Secretary, West Pharmaceutical Services, Inc., 530 Herman O. West Drive, Exton, PA 19341.

ITEM 1A. RISK FACTORS

The statements in this section describe major risks to our business and should be considered carefully. In addition, these statements constitute our cautionary statements under the Private Securities Litigation Reform Act of 1995.

Our disclosure and analysis in this Form 10-K contains some forward-looking statements that are based on management's beliefs and assumptions, current expectations, estimates and forecasts. We also provide forward-

7

looking statements in other materials we release to the public as well as oral forward-looking statements. Such statements give our current expectations or forecasts of future events. They do not relate strictly to historical or current facts. We have attempted, wherever possible, to identify forward-looking statements by using words such as “estimate,” “expect,” “intend,” “believe,” “plan,” “anticipate” and other words and terms of similar meaning. In particular, these include statements relating to future actions, business plans and prospects, new products, future performance or results of current or anticipated products, sales efforts, expenses, interest rates, foreign-exchange rates, economic effects, the outcome of contingencies, such as legal proceedings, and financial results.

Many of the factors that will determine our future results are beyond our ability to control or predict. Achievement of future results is subject to known or unknown risks or uncertainties, including, without limitation, the risks set forth below. Therefore, actual results could differ materially from past results and those expressed or implied in any forward-looking statement. You should bear this in mind as you consider forward-looking statements.

Unless required by applicable securities law, we undertake no obligation to publicly update forward-looking statements, whether as a result of new information, future events or otherwise. We also refer you to further disclosures we make on related subjects in our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K to the SEC.

Our operating results may be adversely affected by unfavorable economic and market conditions.

The current uncertainty in the global economy, including the effects of recession or slow economic growth in the U.S., Europe, and emerging markets in Asia and South America, may negatively affect our operating results. Examples of the effects of these global economic challenges include: our suppliers' and our customers' inability to access the credit markets at commercially reasonable rates; reduction in sales due to customers decreasing their inventories in the near-term or long-term or due to liquidity difficulties; reduction in sales due to shortages of materials we purchase from our suppliers; reduction in research and development efforts and expenditures by our customers; our inability to hedge our currency and raw material risks sufficiently or at commercially reasonable prices; insolvency of suppliers or customers; inflationary pressures on our supplies or our products; and increased expenses due to growing global taxation of corporate profits or revenues, including the impact of the Tax Cuts and Jobs Act (the “2017 Tax Act”). Our operating results in one or more geographic regions may also be affected by uncertain or changing economic conditions within that region. If economic and market conditions in the U.S. or Europe, or in emerging markets, weaken further, we may experience material adverse impacts on our business, financial condition and results of operations.

Our sales and profitability are largely dependent on the sale of drug products delivered by injection and the packaging of drug products. If the products developed by our customers in the future use another delivery system, our sales and profitability could suffer.

Our business depends to a substantial extent on customers' continued sales and development of products that are delivered by injection. If our customers fail to continue to sell, develop and deploy injectable products or we are unable to develop new products that assist in the delivery of drugs by alternative methods, our sales and profitability may suffer.

Changes in foreign currency exchange rates could have a material adverse effect on our business and/or results of operations.

Our business is subject to foreign currency exchange rate fluctuations. Sales outside of the U.S. accounted for 54.1% of our consolidated net sales in 2017 and we anticipate that sales from international operations will continue to represent a significant portion of our total sales in the future. In addition, many of our manufacturing facilities and suppliers are located outside of the U.S. Further, we intend to continue our expansion into emerging and/or faster-growing markets outside of the U.S. in the future. Virtually all of our international sales, assets and related operating costs and expenses are earned, valued or incurred in the currency of the local country, primarily the Euro, the Singapore Dollar (“SGD”), and the Danish Krone. In addition, we are exposed to Japanese Yen (“Yen”), as we maintain a 25% ownership interest in, and we purchase finished goods and other materials from, Daikyo. We are

8

also exposed to currencies in emerging market countries, such as the Chinese Yuan, the Indian Rupee, and various South American currencies. Our consolidated financial statements are presented in USD, and, therefore, we must translate the reported values of our foreign assets, liabilities, revenues and expenses into USD, which can result in significant fluctuations in the amount of those assets, liabilities, revenues or expenses. The exchange rates between these foreign currencies and USD in recent years have fluctuated significantly and may continue to do so in the future. Increases or decreases in the value of USD compared to these foreign currencies may negatively affect the value of these items in our consolidated financial statements, which could have a material adverse effect on our operating results.

In addition to translation risks, we incur currency transaction risk when we or one of our subsidiaries enters into a purchase or sales transaction in a currency other than that entity's local currency. In order to reduce our exposure to fluctuations in certain exchange rates, we have entered, and expect to continue to enter, into hedging arrangements, including the use of financial derivatives. There can be no certainty that we will be able to enter into or maintain hedges of these currency risks, or that our hedges will be effective, which could have a significant effect on our financial condition and operating results.

If we are unable to provide comparative value advantages, timely fulfill customer orders, or resist pricing pressure, we will have to reduce our prices, which may reduce our profit margins.

We compete with several companies across our major product lines. Because of the special nature of these products, competition is based primarily on product design and performance, although total cost is becoming increasingly important as pharmaceutical companies continue with aggressive cost-control programs across their operations. Companies often compete on the basis of price. We aim to differentiate ourselves from our competition by being a “full-service, value-added” global supplier that is able to provide pre-sale compatibility studies, engineering support, and other services and sophisticated post-sale technical support on a global basis. However, we face continued pricing pressure from our customers and competitors. If we are unable to resist or to offset the effects of continued pricing pressure through our value-added services, improved operating efficiencies and reduced expenditures, or if we have to reduce our prices, our sales and profitability may suffer.

Consolidation in the pharmaceutical and healthcare industries could adversely affect our future revenues and operating income.

The pharmaceutical and healthcare industries have experienced a significant amount of consolidation. As a result of this consolidation, competition to provide goods and services to customers has increased. In addition, group purchasing organizations and integrated health delivery networks have served to concentrate purchasing decisions for some customers, which has placed pricing pressure on suppliers. Further consolidation within the industries we serve could exert additional pressure on the prices of our products.

We are subject to regulation by governments around the world, and if these regulations are not complied with, existing and future operations may be curtailed, and we could be subject to liability.

The design, development, manufacturing, marketing and labeling of certain of our products and our customers' products that incorporate our products are subject to regulation by governmental authorities in the U.S., Europe and other countries, including the U.S. Food and Drug Administration (“FDA”) and the European Medicines Agency. Complying with governmental regulation can be costly and can result in required modification or withdrawal of existing products and a substantial delay in the introduction of new products. Failure to comply with applicable regulatory requirements or failure to obtain regulatory approval for a new product could result in expenses and actions that could adversely affect our business and financial performance.

Products incorporating our technologies are subject to regulations and extensive approval or clearance processes, which make the timing and success of new-product commercialization difficult to predict.

The process of obtaining FDA and other required regulatory approvals is expensive and time-consuming. Historically, most medical devices incorporating our technologies have been subject to the FDA's 510(k) marketing

9

approval process, which typically lasts from six to nine months. Supplemental or full pre-market approval reviews require a significantly longer period, delaying commercialization. Pharmaceutical products incorporating our technologies are subject to the FDA's New Drug Application process, which typically takes a number of years to complete. Additionally, biotechnology products incorporating our technologies are subject to the FDA's Biologics License Application process, which also typically takes a number of years to complete. Outside of the U.S., sales of medical devices and pharmaceutical or biotechnology products are subject to international regulatory requirements that vary from country to country. The time required to obtain approval for sale internationally may be longer or shorter than that required for FDA approval.

Changes in the regulation of drug products and devices may increase competitive pressure and adversely affect our business.

An effect of the governmental regulation of our customers' drug products, devices, and manufacturing processes is that compliance with regulations makes it difficult to change components and devices produced by one supplier with those from another supplier, due to the large amount of data and information that customers must generate to demonstrate that the components and devices are equivalent and pose no additional risk to the patient. The regulation of our customers' products that incorporate our components and devices has increased over time. If the applicable regulations were to be modified in a way that reduced the level of data and information needed to prove equivalency for a change from one supplier's components or devices to those made by another, it is likely that the competitive pressure would increase and adversely affect our sales and profitability.

If we are not successful in protecting our intellectual property rights, our ability to compete may be affected.

Our patents, trademarks and other intellectual property are important to our business. We rely on patent, trademark, copyright, trade secret, and other intellectual property laws, as well as nondisclosure and confidentiality agreements and other methods, to protect our proprietary information, technologies and processes. We also have obligations with respect to the non-use and non-disclosure of third party intellectual property. We may need to engage in litigation or similar activities to enforce our intellectual property rights, to protect our trade secrets or to determine the validity and scope of proprietary rights of others. Any such litigation could require us to expend significant resources and divert the efforts and attention of our management and other personnel from our business operations. There can be no assurance that the steps we will take to prevent misappropriation, infringement or other violation of our intellectual property or the intellectual property of others will be successful. In addition, effective patent, copyright, trademark and trade secret protection may be unavailable or limited for some of our intellectual property in some countries. Failure to protect our intellectual property could harm our business and results of operations. In addition, if relevant and effective patent protection is not available or has expired, we may not be able to prevent competitors from independently developing products and services similar or duplicative to ours.

Disruption in our manufacturing facilities could have a material adverse effect on our ability to make and sell products and have a negative impact on our reputation, performance or financial condition.

We have manufacturing sites throughout the world. In some instances, however, the manufacturing of certain product lines is concentrated in one or only a few of our plants. The functioning of our manufacturing and distribution assets and systems could be disrupted for reasons either within or beyond our control, including, without limitation: extreme weather or longer-term climatic changes; natural disasters; pandemic; war; accidental damage; disruption to the supply of material or services; product quality and safety issues; systems failure; workforce actions; or environmental contamination. There is a risk that incident management systems in place may prove inadequate and that any disruption may materially adversely affect our ability to make and sell products and, therefore, materially adversely affect our reputation, performance or financial condition.

The medical technology industry is very competitive and customer demands and/or new products in the marketplace could cause a reduction in demand.

The medical technology industry is subject to rapid technological changes, and we face significant competition across our product lines and in each market in which our products are sold. We face this competition from a wide

10

range of companies, including large medical device companies, some of which have greater financial and marketing resources than we do. We also face competition from firms that are more specialized than we are with respect to particular markets. In some instances, competitors, including pharmaceutical companies, also offer, or are attempting to develop, alternative therapies for diseases that may be delivered via their own, or without, a medical device. The development of new or improved products, processes or technologies by other companies (such as needle-free injection technology) may reduce customer demand for our products or render some of our products or proposed products obsolete or less competitive. In addition, any failure or inability to meet increased customer quality expectations could cause a reduction in demand.

Significant developments in U.S. policies could have a material adverse effect on our business and/or results of operations.

Changes in U.S. social, political, regulatory, and economic conditions, including the impact of the 2017 Tax Act, or in laws and policies governing foreign trade, manufacturing, development, immigration, and investment could have an adverse effect on our financial condition, results of operations and cash flows.

Our international sales and operations are subject to risks and uncertainties that vary by country and which could have a material adverse effect on our business and/or results of operations.

We conduct business in most of the major pharmaceutical markets in the world. Our international operations and our ability to implement our overall business strategy (including our plan to continue expanding into emerging and/or faster-growing markets outside of the U.S.) are subject to risks and uncertainties that can vary by country, and include: transportation delays and interruptions; political and economic instability and disruptions, including the United Kingdom's referendum on withdrawal from the European Union; imposition of duties and tariffs; import and export controls; the risks of divergent business expectations or cultural incompatibility inherent in establishing and maintaining operations in foreign countries; difficulties in staffing and managing multi-national operations; labor strikes and/or disputes; and potentially adverse tax consequences. Limitations on our ability to enforce legal rights and remedies with third parties or our joint venture partners outside of the U.S. could also create exposure. In addition, we may not be able to operate in compliance with foreign laws and regulations, or comply with applicable customs, currency exchange control regulations, transfer pricing regulations or any other laws or regulations to which we may be subject, in the event that these laws or regulations change. Any of these events could have an adverse effect on our international operations in the future by reducing the demand for our products or decreasing the prices at which we can sell our products, or otherwise have an adverse effect on our financial condition, results of operations and cash flows.

Disruptions in the supply of key raw materials could adversely impact our operations.

We generally purchase our raw materials and supplies required for the production of our products in the open market. For reasons of quality assurance, sole source availability or cost effectiveness, many components and raw materials are available and/or purchased only from a single supplier. Due to the stringent regulations and requirements of the FDA and other regulatory authorities regarding the manufacture of our products, we may not be able to quickly establish additional or replacement sources for these components or materials or do so without excessive cost. As a result, a reduction or interruption in supply, or an inability to secure alternative sources of raw materials or components, could have a material adverse effect on our business and/or results of operations.

Raw material and energy prices have a significant impact on our profitability. If raw material and/or energy prices increase, and we cannot pass those price increases on to our customers, our profitability and financial condition may suffer.

We use three basic raw materials in the manufacture of our products: elastomers (which include synthetic and natural material), aluminum and plastic. In addition, our manufacturing facilities consume a wide variety of energy products to fuel, heat and cool our operations. Supply and demand factors, which are beyond our control, generally affect the price of our raw materials and utility costs. If we are unable to pass along increased raw material prices and energy costs to our customers, our profitability, and thus our financial condition, may be adversely affected. The

11

prices of many of these raw materials and utilities are cyclical and volatile. For example, the prices of certain commodities, particularly petroleum-based raw materials, have in the recent past exhibited rapid changes, affecting the cost of synthetic elastomers and plastic. While we generally attempt to pass along increased costs to our customers in the form of sales price increases, historically there has been a time delay between raw material and/or energy price increases and our ability to increase the prices of our products. In some circumstances, we may not be able to increase the prices of our products due to competitive pressure and other factors.

If we are not timely or successful in new-product innovation or the development and commercialization of proprietary multi-component systems, our future revenues and operating income could be adversely affected.

Our growth partly depends on new-product innovation and the development and commercialization of proprietary multi-component systems for injectable drug administration and other healthcare applications. Product development and commercialization is inherently uncertain and is subject to a number of factors outside of our control, including any necessary regulatory approvals and commercial acceptance for the products. The ultimate timing and successful commercialization of new products and systems requires substantial evaluations of the functional, operational, clinical and economic viability of our products. In addition, the timely and adequate availability of filling capacity is essential to both conducting definitive stability trials and the timing of commercialization of customers' products in CZ vials, syringes and cartridges. Delays, interruptions or failures in developing and commercializing new-product innovations or proprietary multi-component systems could adversely affect future revenues and operating income. In addition, adverse conditions may also result in future charges to recognize impairment in the carrying value of our goodwill and other intangible assets, which could have a material adverse effect on our financial results.

We may not succeed in finding and completing acquisition or other strategic transactions, if any, which could have an adverse effect on our business and results of operations.

We have historically engaged in acquisition activity and we may in the future engage in acquisitions or other strategic transactions, such as joint ventures or investments in other entities. We may be unable to identify suitable targets, opportunistic or otherwise, for acquisitions or other strategic transactions in the future. If we identify a suitable candidate, our ability to successfully implement the strategic transaction would depend on a variety of factors including our ability to obtain financing on acceptable terms, and to comply with the restrictions contained in our debt agreements. Strategic transactions involve risks, including those associated with integrating the operations or maintaining the operations as separate (as applicable), financial reporting, disparate technologies and personnel of acquired companies, joint ventures or related companies; managing geographically dispersed operations or other strategic investments; the diversion of management's attention from other business concerns; the inherent risks in entering markets or lines of business in which we have either limited or no direct experience; unknown risks; and the potential loss of key employees, customers and strategic partners of acquired companies, joint ventures or companies in which we may make strategic investments. We may not successfully integrate any businesses or technologies we may acquire or strategically develop in the future and may not achieve anticipated revenue and cost benefits relating to any such strategic transactions. Strategic transactions may be expensive, time consuming and may strain our resources. Strategic transactions may not be accretive to our earnings and may negatively impact our results of operations as a result of, among other things, the incurrence of debt, one-time write-offs of goodwill and amortization expenses of other intangible assets. In addition, strategic transactions that we may pursue could result in dilutive issuances of equity securities.

Product defects could adversely affect the results of our operations.

The design, manufacture and marketing of pharmaceutical packaging and medical devices involve certain inherent risks. Manufacturing or design defects, unanticipated use of our products, or inadequate disclosure of risks relating to the use of our products can lead to injury or other adverse events. These events could lead to recalls or safety alerts relating to our products (either voluntary or required by the FDA or similar governmental authorities in other countries), and could result, in certain cases, in the removal of a product from the market. A recall could result in significant costs, as well as negative publicity and damage to our reputation that could reduce demand for our products. Personal injuries relating to the use of our products can also result in product liability claims being brought against us. In some circumstances, such adverse events could also cause delays in new product approvals.

12

Our operations must comply with environmental statutes and regulations, and any failure to comply could result in extensive costs which would harm our business.

The manufacture of some of our products involves the use, transportation, storage and disposal of hazardous or toxic materials and is subject to various environmental protection and occupational health and safety laws and regulations in the countries in which we operate. This has exposed us in the past, and could expose us in the future, to risks of accidental contamination and events of non-compliance with environmental laws. Any such occurrences could result in regulatory enforcement or personal injury and property damage claims or could lead to a shutdown of some of our operations, which could have an adverse effect on our business and results of operations. We currently incur costs to comply with environmental laws and regulations and these costs may become more significant.

A loss of key personnel or highly skilled employees could disrupt our operations.

Our executive officers are critical to the management and direction of our businesses. Our future success depends, in large part, on our ability to retain these officers and other key employees, including people in technical, marketing, sales and research positions. Competition for experienced employees, particularly for persons with specialized skills, can be intense. Our ability to recruit such talent will depend on a number of factors, including compensation and benefits, work location and work environment. If we cannot effectively recruit and retain qualified executives and employees, our business could be adversely affected. Although we believe that we will be able to attract and retain talented personnel and replace key personnel should the need arise, our inability to do so on a timely basis could disrupt the operations of the unit affected or our overall operations. In addition, because of the complex nature of many of our products and programs, we are generally dependent on an educated and highly skilled engineering staff and workforce. Our operations could be disrupted by a shortage of available skilled employees.

The uncertain effects of potential climate change legislation could lead to significantly increased costs.

If legislation or regulations are enacted or promulgated in the U.S., Europe or Asia or any other jurisdictions in which we do business that limit or reduce allowable greenhouse gas emissions and other emissions, such restrictions could have a significant effect on our operating and financial decisions, including those involving capital expenditures to reduce emissions, and our results of operations. Our manufacturing operations may not be able to operate as planned if we are not able to comply with new legal and regulatory legislation around climate change, or it may become too costly to operate in a profitable manner. Additionally, suppliers' added expenses could be passed on to us in the form of higher prices and we may not be able to pass on such expenses to our customers through price increases.

Healthcare reform may adversely affect our results of operations.

Changes in the U.S. or international healthcare systems, including the Patient Protection and Affordable Care Act (the “PPACA”), could result in reduced demand for our products, as our sales depend, in part, on the extent to which pharmaceutical companies and healthcare providers and facilities are reimbursed by government authorities, private insurers and other third-party payers for the costs of our products. The coverage policies and reimbursement levels of third-party payers, which can vary among public and private sources, may affect which products customers purchase and the prices they are willing to pay for these products in a particular jurisdiction. Legislative or administrative reforms to reimbursement systems in the U.S. (including the possible termination of the PPACA and potential replacement thereafter with a different system) or abroad (for example, those under consideration in France, Germany, Italy and the United Kingdom) could significantly reduce reimbursement for our customers' products, which could in turn reduce the demand for our products.

Moreover, in the coming years, additional changes could be made to global governmental healthcare programs that could significantly impact the success of our products. We will continue to evaluate the PPACA, as amended, the implementation of regulations or guidance related to various provisions of the PPACA by federal agencies, the potential repeal and replacement of the PPACA, as well as trends and changes that may be encouraged by the legislation and other healthcare legislation globally and that may potentially impact our business over time.

13

No assurance can be given that we will continue to pay or declare dividends.

We have historically paid dividends. However, there can be no assurance that we will pay or declare dividends in the future. The actual declaration and payment of future dividends, the amount of any such dividends, and the establishment of record and payment dates, if any, are subject to determination by our Board of Directors each quarter after its review of our then-current strategy, applicable debt covenants and financial performance and position, among other things. Our declaration and payment of future dividends is subject to risks and uncertainties, including: deterioration of our financial performance or position; inability to declare a dividend in compliance with applicable laws or debt covenants; an increase in our cash needs or decrease in available cash; and the business judgment of the Board of Directors that a declaration of a dividend is not in our best interest.

Our results of operations and earnings may not meet guidance or expectations.

We provide public guidance on our expected results of operations for future periods. This guidance is comprised of forward-looking statements subject to risks and uncertainties, including the risks and uncertainties described in this Form 10-K and in our other public filings and public statements, and is based necessarily on assumptions we make at the time we provide such guidance. Our guidance may not always be accurate. If, in the future, our results of operations for a particular period do not meet our guidance or the expectations of investment analysts or if we reduce our guidance for future periods, the market price of our common stock could decline significantly.

We are exposed to credit risk on accounts receivable and certain prepayments made in the normal course of business. This risk is heightened during periods when economic conditions worsen.

A substantial majority of our outstanding trade receivables are not covered by collateral or credit insurance. In addition, we have made prepayments associated with insurance premiums and other advances in the normal course of business. While we have procedures to monitor and limit exposure to credit risk on trade receivables and other current assets, there can be no assurance such procedures will effectively limit our credit risk and avoid losses, which could have a material adverse effect on our financial condition and operating results.

Unauthorized access to our or our customers' information and systems could negatively impact our business.

We may face certain security threats, including threats to the confidentiality, availability and integrity of our data and systems. We maintain an extensive network of technical security controls, policy enforcement mechanisms and monitoring systems in order to address these threats. While these measures are designed to prevent, detect and respond to unauthorized activity in our systems, certain types of attacks could result in financial or information losses and/or reputational harm. If we cannot prevent the unauthorized access, release and/or corruption of our or our customers' confidential, classified or personally identifiable information, our reputation could be damaged, and/or we could face financial losses.

If we fail to comply with our obligations under our distributorship or license agreements with Daikyo, the agreements are terminated early or we are unable to renew these agreements on the same or substantially similar terms, we could lose license rights that are important to our business.

Key value-added and proprietary products and processes are licensed from our affiliate, Daikyo, including but not limited to, CZ, FluroTec® and B2-coating technologies. Our rights to these products and processes are licensed pursuant to agreements that expire in 2027. However, if the agreements are terminated early, our business could be adversely impacted.

ITEM IB. UNRESOLVED STAFF COMMENTS

As of the filing of this Form 10-K, there were no unresolved comments from the Staff of the SEC.

14

ITEM 2. PROPERTIES

Our corporate headquarters are located at 530 Herman O. West Drive, Exton, Pennsylvania. This building also houses our North American sales and marketing, administrative support and customer service functions, as well as laboratories.

The following table summarizes production facilities by segment and geographic region. All facilities shown are owned except where otherwise noted.

Proprietary Products | ||||

Manufacturing: | ||||

North American Operations | European Operations | Asia Pacific Operations | ||

United States | Denmark | China | ||

Clearwater, FL | Horsens | Qingpu | ||

Jersey Shore, PA | England | India | ||

Kearney, NE | St. Austell | Sri City | ||

Kinston, NC | France | Singapore | ||

Lititz, PA | Le Nouvion | Jurong | ||

Scottsdale, AZ (2) | Le Vaudreuil | |||

St. Petersburg, FL (1) | Germany | |||

Eschweiler (1) (2) | ||||

South American Operations | Stolberg | |||

Brazil | Serbia | |||

Sao Paulo | Kovin | |||

Mold-and-Die Tool Shop: | Contract Analytical Laboratory: | |||

North American Operations | European Operations | North American Operations | ||

United States | England | United States | ||

Upper Darby, PA | Bodmin (2) | Exton, PA | ||

Contract-Manufactured Products | ||||

Manufacturing: | ||||

North American Operations | European Operations | |||

United States | Ireland | |||

Frankfort, IN (2) | Dublin (2) | |||

Grand Rapids, MI | ||||

Phoenix, AZ (2) | ||||

Tempe, AZ (2) | ||||

Williamsport, PA | ||||

Puerto Rico | ||||

Cayey | ||||

(1) | This manufacturing facility is also used for research and development activities. |

(2) | This facility is leased in whole or in part. |

Our Proprietary Products reportable segment leases facilities located in Germany, Israel and New Jersey for research and development, as well as other activities. Sales offices in various locations are leased under short-term arrangements.

15

In October 2014, we announced plans to expand our global manufacturing operations to include a new facility in Waterford, Ireland, which will produce packaging components for insulin injector cartridges and other high-value packaging components. The Waterford facility will continue to undergo validation procedures during 2018, with commercial production expected to begin in the second half of 2018.

ITEM 3. LEGAL PROCEEDINGS

None.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

EXECUTIVE OFFICERS OF THE COMPANY

The executive officers of the Company are set forth in this table. Generally, executive officers are elected by the Board of Directors annually at the regular meeting of the Board of Directors following the Annual Meeting of Shareholders. Additionally, executive officers may be elected upon hire or due to a promotion.

Name | Age | Position |

Annette F. Favorite | 53 | Senior Vice President and Chief Human Resources Officer since October 2015. Prior to joining West, she spent more than 25 years at IBM Corporation, an information technology services company, in a number of strategic and global human resources roles. Most recently, she served as Vice President, Global Talent Management. |

William J. Federici | 58 | Senior Vice President and Chief Financial Officer since joining West in August 2003. Acting Treasurer since January 2017. He was National Industry Director for Pharmaceuticals of KPMG LLP (accounting firm) from June 2002 until August 2003 and, prior thereto, an audit partner with Arthur Andersen, LLP. |

Karen A. Flynn | 55 | Senior Vice President and Chief Commercial Officer since January 2016. She was President, Pharmaceutical Packaging Systems from October 2014 to January 2016, President, Pharmaceutical Packaging Systems Americas Region from June 2012 to October 2014, and Vice President, Sales from May 2008 to June 2012. From 2000 to 2008, she worked in Sales Management, most recently as Vice President, Global Accounts, for Catalent (formerly a business segment of Cardinal Health). Prior thereto, she held various positions at West, including Quality, Research and Development, and Sales. |

Eric M. Green | 48 | Chief Executive Officer since April 2015 and President since December 2015. Prior to joining West, he was Executive Vice President and President of the Research Markets business unit at Sigma-Aldrich Corporation, a leading life science and technology company, from 2013 to 2015. From 2009 to 2013, he served as Vice President and Managing Director, International, where he was responsible for Asia Pacific and Latin America, and prior thereto, held various commercial and operational roles. |

Quintin J. Lai | 51 | Vice President, Corporate Development, Strategy and Investor Relations since January 2016. Prior to joining West, he was Vice President of Investor Relations and Corporate Strategy at Sigma-Aldrich Corporation from 2012 to 2015. From 2002 to 2012, he served as Managing Director and Senior Equity Research Analyst of the Life Science Tools and Diagnostic sector at Robert W. Baird & Company. |

Daniel Malone | 56 | Vice President and Corporate Controller since August 2011. He was Vice President of Finance, Pharmaceutical Packaging Systems Americas Region from September 2008 to August 2011 and Director of Financial and Management Reporting from October 1999 to September 2008. |

16

George L. Miller | 63 | Senior Vice President, General Counsel and Corporate Secretary since joining West in November 2015. Previously, he served as Senior Vice President, General Counsel and Corporate Secretary for Sigma-Aldrich Corporation from 2009 to 2015. Prior to working at Sigma-Aldrich, he held senior legal positions with Novartis AG, a global healthcare company. |

David A. Montecalvo | 52 | Senior Vice President, Global Operations and Supply Chain since September 2016. Prior to joining West, he served in a number of senior leadership roles at Medtronic plc, including Vice President, Contract Manufacturing Operations, for the company's Restorative Therapies Group, and Vice President, Business Operations Integration, where he was responsible for directing and leading the global operations integration of Covidien plc into Medtronic. Prior thereto, he held senior operations and product development roles at Urologix, Inc. and LecTec Corporation. |

Eric Resnick | 54 | Vice President and Chief Technology Officer since March 2016. Previously, he served as Vice President and General Manager of Integrated Packaging and Delivery within West's Innovation and Technology Team and President Proprietary Products - Pharmaceutical Delivery Systems from March 2015 until March 2016. He served as Vice President Research and Development and Self-Injection Systems from March 2014 until March 2015, and Vice President and General Manager of West's Contract Manufacturing Delivery Devices division from 2008 until March 2014. Prior thereto, he held various positions of increasing responsibility since joining The Tech Group in 2001. Prior to joining West, he held engineering and operating roles with Eastman Kodak Company and Ortho Clinical Diagnostics. |

17

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is listed on the New York Stock Exchange (“NYSE”) under the symbol “WST.” The following table shows the high and low prices for our common stock as reported by the NYSE, for the periods indicated.

First Quarter | Second Quarter | Third Quarter | Fourth Quarter | Year | ||||||

High | Low | High | Low | High | Low | High | Low | High | Low | |

2017 | $88.30 | $79.06 | $99.91 | $77.97 | $96.81 | $80.02 | $103.36 | $89.77 | $103.36 | $77.97 |

2016 | $69.59 | $53.88 | $77.71 | $68.42 | $84.33 | $71.23 | $86.50 | $70.17 | $86.50 | $53.88 |

As of January 31, 2018, we had 880 shareholders of record, which excludes shareholders whose shares were held by brokerage firms, depositaries and other institutional firms in “street names” for their customers.

Dividends

Our common stock paid a quarterly dividend of $0.12 per share in each of the first three quarters of 2016; $0.13 per share in the fourth quarter of 2016 and each of the first three quarters of 2017; and $0.14 per share in the fourth quarter of 2017.

Issuer Purchases of Equity Securities

The following table shows information with respect to purchases of our common stock made during the three months ended December 31, 2017 by us or any of our “affiliated purchasers” as defined in Rule 10b-18(a)(3) under the Exchange Act:

Period | Total number of shares purchased (1)(2) | Average price paid per share (1)(2) | Total number of shares purchased as part of publicly announced plans or programs (2) | Maximum number (or approximate dollar value) of shares that may yet be purchased under the plans or programs (2) (3) | |||||||||

October 1 – 31, 2017 | — | $ | — | — | 475,000 | ||||||||

November 1 – 30, 2017 | 319,590 | 100.00 | 319,500 | 155,500 | |||||||||

December 1 – 31, 2017 | 155,530 | 99.65 | 155,500 | — | |||||||||

Total | 475,120 | $ | 99.88 | 475,000 | — | ||||||||

(1) | Includes 120 shares purchased on behalf of employees enrolled in the Non-Qualified Deferred Compensation Plan for Designated Employees (Amended and Restated Effective January 1, 2008). Under the plan, Company match contributions are delivered to the plan’s investment administrator, who then purchases shares in the open market and credits the shares to individual plan accounts. |

(2) | In December 2016, we announced a share repurchase program authorizing the repurchase of up to 800,000 shares of our common stock from time to time on the open market or in privately-negotiated transactions as permitted under the Securities Exchange Act of 1934 Rule 10b-18. During the fourth quarter of 2017, we purchased 475,000 shares of our common stock under this program at a cost of $47.5 million, or an average price of $99.88 per share. During the year ended December 31, 2017, we purchased 800,000 shares of our common stock under this program at a cost of $74.4 million, or an average price of $92.96 per share. This share repurchase program expired on December 31, 2017. |

18

(3) | In February 2018, we announced a share repurchase program for calendar-year 2018 authorizing the repurchase of up to 800,000 shares of our common stock from time to time on the open market or in privately-negotiated transactions as permitted under the Securities Exchange Act of 1934 Rule 10b-18. The number of shares to be repurchased and the timing of such transactions will depend on a variety of factors, including market conditions. This share repurchase program is expected to be completed by December 31, 2018. |

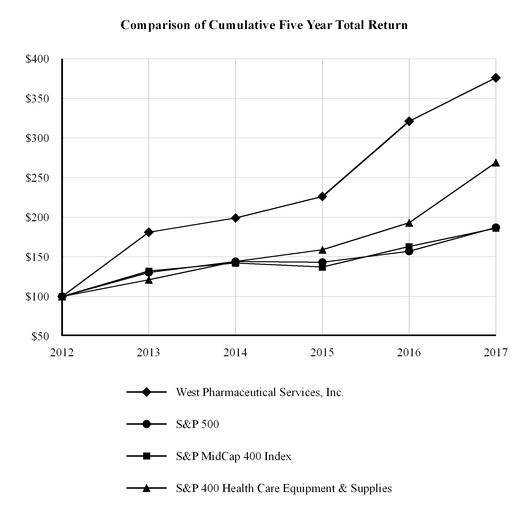

Performance Graph

The following performance graph compares the cumulative total return to holders of our common stock with the cumulative total return of the following Standard & Poor's (“S&P”) indices, for the five years ended December 31, 2017: 500, MidCap 400 Index and 400 Health Care Equipment & Supplies Industry.

Cumulative total return to shareholders is measured by dividing total dividends (assuming dividend reinvestment) plus the per-share price change for the period by the share price at the beginning of the period. The Company's cumulative shareholder return is based on an investment of $100 on December 31, 2012 and is compared to the cumulative total return of the S&P indices mentioned above over the period with a like amount invested.

19

ITEM 6. SELECTED FINANCIAL DATA

FIVE-YEAR SUMMARY

West Pharmaceutical Services, Inc. and Subsidiaries

(in millions, except per share data) | 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||

SUMMARY OF OPERATIONS | |||||||||||||||

Net sales | $ | 1,599.1 | $ | 1,509.1 | $ | 1,399.8 | $ | 1,421.4 | $ | 1,368.4 | |||||

Operating profit | 228.9 | 196.8 | 128.6 | 182.0 | 162.4 | ||||||||||

Net income | 150.7 | 143.6 | 95.6 | 127.1 | 112.3 | ||||||||||

Net income per share: | |||||||||||||||

Basic (1) | $ | 2.04 | $ | 1.96 | $ | 1.33 | $ | 1.79 | $ | 1.61 | |||||

Diluted (2) | 1.99 | 1.91 | 1.30 | 1.75 | 1.57 | ||||||||||

Weighted average common shares outstanding | 73.9 | 73.3 | 72.0 | 70.9 | 69.6 | ||||||||||

Weighted average shares assuming dilution | 75.8 | 75.0 | 73.8 | 72.8 | 71.4 | ||||||||||

Dividends declared per common share | $ | 0.54 | $ | 0.50 | $ | 0.46 | $ | 0.41 | $ | 0.39 | |||||

YEAR-END FINANCIAL POSITION | |||||||||||||||

Cash and cash equivalents | $ | 235.9 | $ | 203.0 | $ | 274.6 | $ | 255.3 | $ | 230.0 | |||||

Working capital | 464.0 | 400.9 | 359.4 | 406.6 | 413.6 | ||||||||||

Total assets | 1,862.8 | 1,716.7 | 1,695.1 | 1,669.7 | 1,670.2 | ||||||||||

Total invested capital: | |||||||||||||||

Total debt | 197.0 | 228.6 | 298.2 | 335.5 | 372.1 | ||||||||||

Total equity | 1,279.9 | 1,117.5 | 1,023.9 | 956.9 | 906.4 | ||||||||||

Total invested capital | $ | 1,476.9 | $ | 1,346.1 | $ | 1,322.1 | $ | 1,292.4 | $ | 1,278.5 | |||||

PERFORMANCE MEASUREMENTS (3) | |||||||||||||||

Gross margin (a) | 32.1 | % | 33.2 | % | 32.6 | % | 31.5 | % | 31.8 | % | |||||

Operating profitability (b) | 14.3 | % | 13.0 | % | 9.2 | % | 12.8 | % | 11.9 | % | |||||

Effective tax rate (4) | 36.4 | % | 28.7 | % | 22.6 | % | 28.0 | % | 27.4 | % | |||||

Return on invested capital (c) | 10.3 | % | 10.5 | % | 7.6 | % | 10.2 | % | 9.8 | % | |||||

Net debt-to-total invested capital (d) | N/A | 2.2 | % | 2.3 | % | 7.7 | % | 13.6 | % | ||||||

Research and development expenses | $ | 39.1 | $ | 36.8 | $ | 34.1 | $ | 37.3 | $ | 37.9 | |||||

Operating cash flow | 263.3 | 219.4 | 212.4 | 182.9 | 220.5 | ||||||||||

Stock price range | $103.36-77.97 | $86.50-53.88 | $64.59-48.66 | $55.29-39.11 | $50.60-27.31 | ||||||||||

(1) Based on weighted average common shares outstanding.

(2) Based on weighted average shares, assuming dilution.

(3) Performance measurements represent indicators commonly used in the financial community. The following performance measures are not in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”) and should not be used as a substitute for the comparable U.S. GAAP financial measures. The non-U.S. GAAP financial measures are included as management uses them in evaluating our results of operations, and believes that this information provides users with a valuable insight into our overall performance and financial position.

(a) Net sales minus cost of goods and services sold, including applicable depreciation and amortization, divided by net sales.

(b) Operating profit divided by net sales.

(c) Operating profit multiplied by one minus the effective tax rate divided by average total invested capital.

(d) Net debt (total debt less cash and cash equivalents) divided by total invested capital less cash and cash equivalents.

20

(4) As a result of the 2017 Tax Act, the federal statutory rate will be reduced from 35.0% to 21.0% effective for tax years beginning after December 31, 2017. Please refer to Note 15, Income Taxes, for further discussion of the 2017 Tax Act.

Factors affecting the comparability of the information reflected in the selected financial data:

▪ | Net income in 2017 included the impact of a discrete tax charge of $48.8 million related to the 2017 Tax Act and the impact of changes in enacted international tax rates on previously-recorded deferred tax asset and liability balances, as well as a tax benefit of $33.1 million associated with our adoption of the guidance issued by the Financial Accounting Standards Board (“FASB”) regarding share-based payment transactions and a charge of $11.1 million related to the deconsolidation of our Venezuelan subsidiary. |

▪ | Net income in 2016 included the impact of restructuring and related charges of $17.4 million (net of $9.0 million in tax), a charge related to the devaluation of the Venezuelan Bolivar of $2.7 million, a pension curtailment gain of $1.3 million (net of $0.8 million in tax), and a discrete tax charge of $1.0 million. |

▪ | Net income in 2015 included the impact of a pension settlement charge of $32.0 million (net of $18.4 million in tax), a charge for executive retirement and related costs of $6.9 million (net of $4.0 million in tax) and a discrete tax charge of $0.8 million. |

▪ | Net income in 2014 included the impact of a charge for license costs associated with acquired in-process research of $0.8 million (net of $0.4 million in tax) and discrete tax charges of $1.8 million. |

▪ | Net income in 2013 included the impact of a loss on extinguishment of debt of $0.2 million and net discrete tax charges of $3.6 million. |

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

OVERVIEW

The following discussion is intended to further the reader's understanding of the consolidated financial condition and results of operations of our Company. It should be read in conjunction with our consolidated financial statements and the accompanying footnotes included in Part II, Item 8 of this Form 10-K. These historical financial statements may not be indicative of our future performance. This Management's Discussion and Analysis of Financial Condition and Results of Operations contains a number of forward-looking statements, all of which are based on our current expectations and could be affected by the uncertainties and risks discussed in Part I, Item 1A of this Form 10-K.

Non-U.S. GAAP Financial Measures

For the purpose of aiding the comparison of our year-over-year results, we may refer to net sales and other financial results excluding the effects of changes in foreign currency exchange rates. The constant-currency amounts are calculated by translating the current year’s functional currency results at the prior-year period’s exchange rate. We may also refer to consolidated operating profit and consolidated operating profit margin excluding the effects of unallocated items. The re-measured results excluding effects from currency translation and excluding the effects of unallocated items are not in conformity with U.S. GAAP and should not be used as a substitute for the comparable U.S. GAAP financial measures. The non-U.S. GAAP financial measures are incorporated into our discussion and analysis as management uses them in evaluating our results of operations, and believes that this information provides users a valuable insight into our results.

21

Our Operations

We are a leading global manufacturer in the design and production of technologically advanced, high-quality, integrated containment and delivery systems for injectable drugs and healthcare products. Our products include a variety of primary packaging, containment solutions, reconstitution and transfer systems, and drug delivery systems, as well as contract manufacturing and analytical lab services. Our customers include the leading biologic, generic, pharmaceutical, diagnostic, and medical device companies in the world. Our top priority is delivering quality products that meet the exact product specifications and quality standards customers require and expect. This focus on quality includes excellence in manufacturing, scientific and technical expertise and management, so we can partner with our customers to deliver safe, effective drug products to patients quickly and efficiently. The Company was incorporated under the laws of the Commonwealth of Pennsylvania on July 27, 1923.

Our business operations are organized into two reportable segments, Proprietary Products and Contract-Manufactured Products. Our Proprietary Products reportable segment offers proprietary packaging, containment and drug delivery products, along with analytical lab services, to biologic, generic and pharmaceutical drug customers. Our Contract-Manufactured Products reportable segment serves as a fully integrated business, focused on the design, manufacture, and automated assembly of complex devices, primarily for pharmaceutical, diagnostic, and medical device customers. We also maintain partnerships to share technologies and market products with affiliates in Japan and Mexico.

2017 Financial Performance Summary

Consolidated net sales increased by $90.0 million, or 6.0%, in 2017, including a favorable foreign currency translation impact of $12.2 million. Excluding foreign currency translation effects, consolidated net sales increased by $77.8 million, or 5.2%.