Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - W. P. Carey Inc. | wpc2017q48-kerexh991.htm |

| 8-K - 8-K - W. P. Carey Inc. | wpc2017q48-ksupplemental.htm |

Exhibit 99.2

W. P. Carey Inc.

Supplemental Information

Fourth Quarter 2017

Important Disclosures About This Supplemental Package

As used in this supplemental package, the terms “W. P. Carey,” “WPC®,” “we,” “us” and “our” include W. P. Carey Inc., its consolidated subsidiaries and its predecessors, unless otherwise indicated. “CPA® REITs” means Corporate Property Associates 17 – Global Incorporated, or CPA:17 – Global, and Corporate Property Associates 18 – Global Incorporated, or CPA:18 – Global. “CWI® REITs” means Carey Watermark Investors Incorporated, or CWI 1, and Carey Watermark Investors 2 Incorporated, or CWI 2. “Managed REITs” means the CPA REITs and the CWI REITs. “Managed Programs” means the Managed REITs and Carey European Student Housing Fund I, L.P., or CESH I. “CCIF” means Carey Credit Income Fund (now known as Guggenheim Credit Income Fund), which was included in the Managed Programs prior to our resignation as its advisor during the third quarter of 2017. “U.S.” means United States. “AUM” means assets under management.

Important Note Regarding Non-GAAP Financial Measures

This supplemental package includes certain “non-GAAP” supplemental measures that are not defined by generally accepted accounting principles, or GAAP, including funds from operations, or FFO; adjusted funds from operations, or AFFO; earnings before interest, taxes, depreciation and amortization, or EBITDA; adjusted EBITDA; pro rata cash net operating income, or pro rata cash NOI; and normalized pro rata cash NOI. A description of these non-GAAP financial measures and reconciliations to their most directly comparable GAAP measures, as well as a description of other metrics presented, are provided within the Appendix to this supplemental package. FFO is a non-GAAP measure defined by the National Association of Real Estate Investments Trusts, Inc., or NAREIT, an industry trade group.

Amounts may not sum to totals due to rounding.

W. P. Carey Inc.

Supplemental Information – Fourth Quarter 2017

Table of Contents | |

Overview | |

Financial Results | |

Statements of Income – Last Five Quarters | |

FFO and AFFO – Last Five Quarters | |

Balance Sheets and Capitalization | |

Owned Real Estate | |

Investment Activity | |

Investment Management | |

Appendix | |

Adjusted EBITDA – Last Five Quarters | |

W. P. Carey Inc.

Overview – Fourth Quarter 2017

Summary Metrics | |

As of or for the three months ended December 31, 2017.

Financial Results | |||||||||||||||||||

Segment | |||||||||||||||||||

Owned Real Estate | Investment Management | Total | |||||||||||||||||

Revenues, excluding reimbursable costs – consolidated ($'000) | $ | 162,251 | $ | 23,071 | $ | 185,322 | |||||||||||||

Net income attributable to W. P. Carey ($'000) | 54,149 | 21,060 | 75,209 | ||||||||||||||||

Net income attributable to W. P. Carey per diluted share | 0.50 | 0.19 | 0.69 | ||||||||||||||||

Normalized pro rata cash NOI from real estate ($'000) (a) (b) | 165,931 | N/A | 165,931 | ||||||||||||||||

Adjusted EBITDA ($'000) (a) (b) | 157,744 | 32,160 | 189,904 | ||||||||||||||||

AFFO attributable to W. P. Carey ($'000) (a) (b) | 111,336 | 30,726 | 142,062 | ||||||||||||||||

AFFO attributable to W. P. Carey per diluted share (a) (b) | 1.03 | 0.28 | 1.31 | ||||||||||||||||

Distributions declared per share – fourth quarter | 1.01 | ||||||||||||||||||

Distributions declared per share – fourth quarter annualized | 4.04 | ||||||||||||||||||

Dividend yield – annualized, based on quarter end share price of $68.90 | 5.9 | % | |||||||||||||||||

Dividend payout ratio – for the year ended December 31, 2017 (c) | 75.7 | % | |||||||||||||||||

Balance Sheet and Capitalization | |||||||||||||||||||

Equity market capitalization – based on quarter end share price of $68.90 ($'000) | $ | 7,366,968 | |||||||||||||||||

Pro rata net debt ($'000) (d) | 4,150,197 | ||||||||||||||||||

Enterprise value ($'000) | 11,517,165 | ||||||||||||||||||

Total capitalization ($'000) (e) | 11,679,477 | ||||||||||||||||||

Total consolidated debt ($'000) | 4,265,267 | ||||||||||||||||||

Gross assets ($'000) (f) | 8,861,364 | ||||||||||||||||||

Liquidity ($'000) (g) | 1,445,435 | ||||||||||||||||||

Pro rata net debt to enterprise value (b) | 36.0 | % | |||||||||||||||||

Pro rata net debt to adjusted EBITDA (annualized) (a) (b) | 5.5x | ||||||||||||||||||

Total consolidated debt to gross assets | 48.1 | % | |||||||||||||||||

Weighted-average interest rate (b) | 3.4 | % | |||||||||||||||||

Weighted-average debt maturity (years) (b) | 5.4 | ||||||||||||||||||

Moody's Investors Service – corporate rating | Baa2 (stable) | ||||||||||||||||||

Standard & Poor's Ratings Services – issuer rating | BBB (stable) | ||||||||||||||||||

Owned Real Estate Portfolio (Pro Rata) | |||||||||||||||||||

Number of net-leased properties | 887 | ||||||||||||||||||

Number of operating properties | 2 | ||||||||||||||||||

Number of tenants – net-leased properties | 210 | ||||||||||||||||||

ABR from Investment Grade tenants as a % of total ABR – net-leased properties (h) | 27.2 | % | |||||||||||||||||

Net-leased properties – square footage (millions) | 84.9 | ||||||||||||||||||

Occupancy – net-leased properties | 99.8 | % | |||||||||||||||||

Weighted-average lease term (years) | 9.6 | ||||||||||||||||||

Acquisitions and completed capital projects – fourth quarter ($'000) | $ | 32,267 | |||||||||||||||||

Dispositions – fourth quarter ($'000) | 59,067 | ||||||||||||||||||

Managed Programs | CPA:17 – Global | CPA:18 – Global | CWI REITs | CESH I | Total | ||||||||||||||

AUM ($'000) (i) | $ | 5,702,445 | $ | 2,387,349 | $ | 4,880,132 | $ | 155,126 | $ | 13,125,052 | |||||||||

Acquisitions – fourth quarter ($'000) | 52,571 | 94,586 | — | — | 147,157 | ||||||||||||||

Dispositions – fourth quarter ($'000) | — | 64,847 | 85,500 | — | 150,347 | ||||||||||||||

________

| Investing for the long runTM | 1 | |

W. P. Carey Inc.

Overview – Fourth Quarter 2017

(a) | Normalized pro rata cash NOI, Adjusted EBITDA and AFFO are non-GAAP measures. See the Terms and Definitions section in the Appendix for a description of our non-GAAP measures and for details on how certain non-GAAP measures are calculated. |

(b) | Presented on a pro rata basis. See the Terms and Definitions section in the Appendix for a description of pro rata. |

(c) | Represents distributions declared per share divided by AFFO per diluted share on a year-to-date basis. |

(d) | Represents total pro rata debt outstanding less consolidated cash and cash equivalents. See the Terms and Definitions section in the Appendix for a description of pro rata. |

(e) | Represents equity market capitalization plus total pro rata debt outstanding. See the Terms and Definitions section in the Appendix for a description of pro rata. |

(f) | Gross assets represent consolidated total assets before accumulated depreciation on buildings and improvements. Gross assets are net of accumulated amortization on in-place lease and other intangible assets of $423.5 million and above-market rent intangible assets of $276.1 million. |

(g) | Represents availability on our Senior Unsecured Credit Facility plus consolidated cash and cash equivalents. |

(h) | Percentage of portfolio is based on ABR, as of December 31, 2017. Includes tenants or guarantors with investment grade ratings (19.2%) and subsidiaries of non-guarantor parent companies with investment grade ratings (8.0%). Investment grade refers to an entity with a rating of BBB- or higher from Standard & Poor’s Ratings Services or Baa3 or higher from Moody’s Investors Service. See the Terms and Definitions section in the Appendix for a description of ABR. |

(i) | Represents estimated value of real estate assets plus cash and cash equivalents, less distributions payable for the Managed REITs and fair value of investments plus cash for CESH I. |

| | Investing for the long runTM | 2 | |

W. P. Carey Inc.

Overview – Fourth Quarter 2017

Components of Net Asset Value | |

Dollars in thousands, except per share amounts.

Owned Real Estate | Three Months Ended Dec. 31, 2017 | Annualized | |||||||

Normalized pro rata cash NOI (a) (b) | $ | 165,931 | $ | 663,724 | |||||

Investment Management | Three Months Ended Dec. 31, 2017 | Twelve Months Ended Dec. 31, 2017 | |||||||

Adjusted EBITDA (a) (b) (c) | $ | 32,160 | $ | 118,657 | |||||

Selected Components of Adjusted EBITDA: | |||||||||

Asset management revenue (d) | 16,854 | 70,125 | |||||||

Structuring revenue (d) | 6,217 | 34,198 | |||||||

Operating partnership interests in real estate cash flow of Managed REITs (c) (e) | 12,564 | 45,101 | |||||||

Back-end fees and interests associated with the Managed Programs | See the Summary of Back-End Fees for / Interests in the Managed Programs section for details. | ||||||||

Balance Sheet – Selected Information (Consolidated Unless Otherwise Stated) | As of Dec. 31, 2017 | ||||||||

Assets | |||||||||

Book value of real estate excluded from NOI (f) | $ | 40,560 | |||||||

Cash and cash equivalents | 162,312 | ||||||||

Due from affiliates | 105,308 | ||||||||

Other assets, net: | |||||||||

Straight-line rent adjustments | $ | 71,955 | |||||||

Restricted cash, including escrow | 47,364 | ||||||||

Deferred charges | 44,370 | ||||||||

Investment in CCIF (g) | 23,329 | ||||||||

Securities and derivatives | 22,186 | ||||||||

Accounts receivable | 17,770 | ||||||||

Other intangible assets, net | 14,361 | ||||||||

Taxes receivable | 11,137 | ||||||||

Note receivable | 9,971 | ||||||||

Prepaid expenses | 8,137 | ||||||||

Leasehold improvements, furniture and fixtures | 3,859 | ||||||||

Other | 211 | ||||||||

Total other assets, net | $ | 274,650 | |||||||

Liabilities | |||||||||

Total pro rata debt outstanding (b) | $ | 4,312,509 | |||||||

Distributions payable | 109,766 | ||||||||

Deferred income taxes | 67,009 | ||||||||

Accounts payable, accrued expenses and other liabilities: | |||||||||

Accounts payable and accrued expenses | $ | 101,615 | |||||||

Prepaid and deferred rents | 79,483 | ||||||||

Tenant security deposits | 29,050 | ||||||||

Accrued taxes payable | 28,861 | ||||||||

Securities and derivatives | 7,913 | ||||||||

Straight-line rent adjustments | 2,230 | ||||||||

Other | 13,901 | ||||||||

Total accounts payable, accrued expenses and other liabilities | $ | 263,053 | |||||||

| | Investing for the long runTM | 3 | |

W. P. Carey Inc.

Overview – Fourth Quarter 2017

Other | Number of Shares / Units Owned | NAV / Offering Price Per Share | Implied Value | |||||||

A | B | A x B | ||||||||

Ownership in Managed Programs: (h) | ||||||||||

CPA:17 – Global (4.2% ownership) | 14,647,412 | $ | 10.11 | (i) | $ | 148,085 | ||||

CPA:18 – Global (2.5% ownership) | 3,616,657 | 8.36 | (j) | 30,235 | ||||||

CWI 1 (2.1% ownership) | 2,920,268 | 10.80 | (k) | 31,539 | ||||||

CWI 2 (1.8% ownership) | 1,560,648 | 10.74 | (l) | 16,761 | ||||||

CESH I (2.4% ownership) | 3,492 | 1,000.00 | (m) | 3,492 | ||||||

$ | 230,112 | |||||||||

________

(a) | Normalized pro rata cash NOI and Adjusted EBITDA are non-GAAP measures. See the Terms and Definitions section in the Appendix for a description of our non-GAAP measures and for details on how they are calculated. |

(b) | Presented on a pro rata basis. See the Terms and Definitions section in the Appendix for a description of pro rata. |

(c) | In connection with our decision to exit non-traded retail fundraising activities, which we announced in June 2017, during the second quarter of 2017 we revised how we view and present our two business segments. As such, equity in earnings of equity method investments in the Managed Programs is now recognized within our Investment Management segment. Earnings from our investment in CCIF continue to be included in our Investment Management segment. Prior periods have been revised to reflect this change. |

(d) | Amounts are gross of fees paid to the respective subadvisors of CWI 1, CWI 2, CPA:18 – Global (for multi-family properties) and CCIF (prior to our resignation as the advisor to CCIF in the third quarter of 2017). |

(e) | We are entitled to receive distributions of our share of earnings up to 10% of the Available Cash of each of the Managed REITs, as defined in their respective operating partnership agreements. Pursuant to the terms of their subadvisory agreements, however, 20% of the distributions of Available Cash we receive from CWI 1 and 25% of the distributions of Available Cash we receive from CWI 2 are paid to their respective subadvisors. Amounts for CWI 1 and CWI 2 are net of fees paid to their respective subadvisors. |

(f) | Represents the value of real estate not included in net operating income, such as vacant assets and in-progress build-to-suit properties. |

(g) | In August 2017, we resigned as the advisor to CCIF, effective as of September 11, 2017. As such, we reclassified our investment in CCIF from Equity investments in the Managed Programs and real estate to Other assets, net in our consolidated balance sheets, since we no longer share decision-making responsibilities with the third-party investment partner. |

(h) | Separate from operating partnership interests and our interests in unconsolidated real estate joint ventures with our affiliate, CPA:17 – Global. |

(i) | The estimated net asset value per share, or NAV, for CPA:17 – Global was determined as of December 31, 2016. We calculated CPA:17 – Global’s NAV by relying in part on an estimate of the fair market value of CPA:17 – Global’s real estate portfolio and debt provided by third parties, adjusted to give effect to the estimated fair value of mortgage loans encumbering its assets (also provided by a third party) as well as other adjustments. |

(j) | We own shares of CPA:18 – Global’s Class A common stock. The quarterly NAV for CPA:18 – Global’s Class A common stock was determined as of September 30, 2017. We calculated the quarterly NAV for CPA:18 – Global’s Class A common stock by relying in part on an estimate of the fair market value of approximately 25% of CPA:18 – Global’s real estate portfolio and debt provided by third parties, adjusted to give effect to the estimated fair value of mortgage loans encumbering its assets (also provided by a third party), as well as other adjustments. |

(k) | The NAV for CWI 1 was based on shares of common stock outstanding at December 31, 2016. We calculated CWI 1’s NAV relying in part on appraisals of the fair market value of CWI 1’s real estate portfolio and mortgage debt provided by third parties. The net amount was then adjusted for estimated disposition costs (including estimates of expenses, commissions and fees payable to us) and CWI 1’s other net assets and liabilities at the same date. |

(l) | We own shares of CWI 2’s Class A common stock. The NAV for CWI 2’s Class A common stock was determined as of December 31, 2016. We calculated the NAV for CWI 2’s Class A common stock by relying in part on an appraisal of the fair market value of CWI 2’s real estate portfolio and estimates of the fair market value of CWI 2’s mortgage debt at December 31, 2016. The net amount was then adjusted for other net assets and liabilities and our interest in disposition proceeds at December 31, 2016. |

(m) | We own limited partnership units of CESH I at its private placement price of $1,000 per share; a NAV for CESH I has not yet been calculated. |

| | Investing for the long runTM | 4 | |

W. P. Carey Inc.

Financial Results

Fourth Quarter 2017

| | Investing for the long runTM | 5 | |

W. P. Carey Inc.

Financial Results – Fourth Quarter 2017

Consolidated Statements of Income – Last Five Quarters | |

In thousands, except share and per share amounts.

Three Months Ended | |||||||||||||||||||

Dec. 31, 2017 | Sep. 30, 2017 | Jun. 30, 2017 | Mar. 31, 2017 | Dec. 31, 2016 | |||||||||||||||

Revenues | |||||||||||||||||||

Owned Real Estate: | |||||||||||||||||||

Lease revenues | $ | 154,826 | $ | 161,511 | $ | 158,255 | $ | 155,781 | $ | 157,105 | |||||||||

Operating property revenues | 6,910 | 8,449 | 8,223 | 6,980 | 7,071 | ||||||||||||||

Reimbursable tenant costs | 5,584 | 5,397 | 5,322 | 5,221 | 6,201 | ||||||||||||||

Lease termination income and other | 515 | 1,227 | 2,247 | 760 | 1,093 | ||||||||||||||

167,835 | 176,584 | 174,047 | 168,742 | 171,470 | |||||||||||||||

Investment Management: | |||||||||||||||||||

Asset management revenue | 16,854 | 17,938 | 17,966 | 17,367 | 16,375 | ||||||||||||||

Structuring revenue | 6,217 | 9,817 | 14,330 | 3,834 | 16,338 | ||||||||||||||

Reimbursable costs from affiliates | 6,055 | 6,211 | 13,479 | 25,700 | 20,061 | ||||||||||||||

Dealer manager fees | — | 105 | 1,000 | 3,325 | 2,623 | ||||||||||||||

Other advisory revenue | — | 99 | 706 | 91 | 1,913 | ||||||||||||||

29,126 | 34,170 | 47,481 | 50,317 | 57,310 | |||||||||||||||

196,961 | 210,754 | 221,528 | 219,059 | 228,780 | |||||||||||||||

Operating Expenses | |||||||||||||||||||

Depreciation and amortization | 64,015 | 64,040 | 62,849 | 62,430 | 62,675 | ||||||||||||||

General and administrative | 17,702 | 17,236 | 17,529 | 18,424 | 24,230 | ||||||||||||||

Reimbursable tenant and affiliate costs | 11,639 | 11,608 | 18,801 | 30,921 | 26,262 | ||||||||||||||

Property expenses, excluding reimbursable tenant costs | 9,560 | 10,556 | 10,530 | 10,110 | 10,956 | ||||||||||||||

Stock-based compensation expense | 4,268 | 4,635 | 3,104 | 6,910 | 3,051 | ||||||||||||||

Impairment charges | 2,769 | — | — | — | 9,433 | ||||||||||||||

Subadvisor fees (a) | 2,002 | 5,206 | 3,672 | 2,720 | 4,131 | ||||||||||||||

Other expenses (b) | (533 | ) | 65 | 1,000 | 73 | 18 | |||||||||||||

Restructuring and other compensation (c) | 289 | 1,356 | 7,718 | — | — | ||||||||||||||

Dealer manager fees and expenses | — | 462 | 2,788 | 3,294 | 3,808 | ||||||||||||||

111,711 | 115,164 | 127,991 | 134,882 | 144,564 | |||||||||||||||

Other Income and Expenses | |||||||||||||||||||

Interest expense | (40,401 | ) | (41,182 | ) | (42,235 | ) | (41,957 | ) | (43,913 | ) | |||||||||

Equity in earnings of equity method investments in the Managed Programs and real estate | 16,930 | 16,318 | 15,728 | 15,774 | 16,476 | ||||||||||||||

Other income and (expenses) | 1,356 | (4,569 | ) | (916 | ) | 516 | (3,731 | ) | |||||||||||

(22,115 | ) | (29,433 | ) | (27,423 | ) | (25,667 | ) | (31,168 | ) | ||||||||||

Income before income taxes and gain on sale of real estate | 63,135 | 66,157 | 66,114 | 58,510 | 53,048 | ||||||||||||||

Benefit from (provision for) income taxes | 192 | (1,760 | ) | (2,448 | ) | 1,305 | (7,826 | ) | |||||||||||

Income before gain on sale of real estate | 63,327 | 64,397 | 63,666 | 59,815 | 45,222 | ||||||||||||||

Gain on sale of real estate, net of tax | 11,146 | 19,257 | 3,465 | 10 | 3,248 | ||||||||||||||

Net Income | 74,473 | 83,654 | 67,131 | 59,825 | 48,470 | ||||||||||||||

Net loss (income) attributable to noncontrolling interests | 736 | (3,376 | ) | (2,813 | ) | (2,341 | ) | (766 | ) | ||||||||||

Net Income Attributable to W. P. Carey | $ | 75,209 | $ | 80,278 | $ | 64,318 | $ | 57,484 | $ | 47,704 | |||||||||

Basic Earnings Per Share | $ | 0.69 | $ | 0.74 | $ | 0.60 | $ | 0.53 | $ | 0.44 | |||||||||

Diluted Earnings Per Share | $ | 0.69 | $ | 0.74 | $ | 0.59 | $ | 0.53 | $ | 0.44 | |||||||||

Weighted-Average Shares Outstanding | |||||||||||||||||||

Basic | 108,041,556 | 108,019,292 | 107,668,218 | 107,562,484 | 107,487,181 | ||||||||||||||

Diluted | 108,208,918 | 108,143,694 | 107,783,204 | 107,764,279 | 107,715,965 | ||||||||||||||

________

(a) | The subadvisors for CWI 1, CWI 2 and CPA:18 – Global earn a percentage of gross fees recorded, which we account for as an expense and which are recorded as Subadvisor fees in our consolidated statements of income. The amounts paid to the subadvisors are the differences between gross and net fees. Pursuant to the terms of the subadvisory agreement we had with the subadvisor in connection with CCIF (prior to our resignation as the advisor to CCIF in the third quarter of 2017), we paid a subadvisory fee equal to 50% of the asset management fees and organization and offering costs paid to us by CCIF. |

(b) | Amount for the three months ended June 30, 2017 is comprised of an accrual for estimated one-time legal settlement expenses. |

(c) | Amounts for the three months ended December 31, 2017, September 30, 2017 and June 30, 2017 represent restructuring expenses resulting from our exit from non-traded retail fundraising activities, which we announced in June 2017. |

| | Investing for the long runTM | 6 | |

W. P. Carey Inc.

Financial Results – Fourth Quarter 2017

Statements of Income, Owned Real Estate – Last Five Quarters | |

In thousands, except share and per share amounts.

Three Months Ended | |||||||||||||||||||

Dec. 31, 2017 | Sep. 30, 2017 | Jun. 30, 2017 | Mar. 31, 2017 | Dec. 31, 2016 | |||||||||||||||

Revenues | |||||||||||||||||||

Lease revenues | $ | 154,826 | $ | 161,511 | $ | 158,255 | $ | 155,781 | $ | 157,105 | |||||||||

Operating property revenues | 6,910 | 8,449 | 8,223 | 6,980 | 7,071 | ||||||||||||||

Reimbursable tenant costs | 5,584 | 5,397 | 5,322 | 5,221 | 6,201 | ||||||||||||||

Lease termination income and other | 515 | 1,227 | 2,247 | 760 | 1,093 | ||||||||||||||

167,835 | 176,584 | 174,047 | 168,742 | 171,470 | |||||||||||||||

Operating Expenses | |||||||||||||||||||

Depreciation and amortization | 62,951 | 62,970 | 61,989 | 61,522 | 61,717 | ||||||||||||||

General and administrative | 11,691 | 11,234 | 7,803 | 8,274 | 8,938 | ||||||||||||||

Property expenses, excluding reimbursable tenant costs | 9,560 | 10,556 | 10,530 | 10,110 | 10,956 | ||||||||||||||

Reimbursable tenant costs | 5,584 | 5,397 | 5,322 | 5,221 | 6,201 | ||||||||||||||

Impairment charges | 2,769 | — | — | — | 9,433 | ||||||||||||||

Stock-based compensation expense | 2,227 | 1,880 | 899 | 1,954 | 908 | ||||||||||||||

Other expenses (a) | (533 | ) | 65 | 1,000 | 73 | 18 | |||||||||||||

94,249 | 92,102 | 87,543 | 87,154 | 98,171 | |||||||||||||||

Other Income and Expenses | |||||||||||||||||||

Interest expense | (40,401 | ) | (41,182 | ) | (42,235 | ) | (41,957 | ) | (43,913 | ) | |||||||||

Equity in earnings of equity method investments in real estate (b) | 3,535 | 3,740 | 3,721 | 2,072 | 3,343 | ||||||||||||||

Other income and (expenses) | 594 | (4,918 | ) | (1,371 | ) | 40 | (4,016 | ) | |||||||||||

(36,272 | ) | (42,360 | ) | (39,885 | ) | (39,845 | ) | (44,586 | ) | ||||||||||

Income before income taxes and gain on sale of real estate | 37,314 | 42,122 | 46,619 | 41,743 | 28,713 | ||||||||||||||

Benefit from (provision for) income taxes | 4,953 | (1,511 | ) | (3,731 | ) | (1,454 | ) | (3,374 | ) | ||||||||||

Income before gain on sale of real estate | 42,267 | 40,611 | 42,888 | 40,289 | 25,339 | ||||||||||||||

Gain on sale of real estate, net of tax | 11,146 | 19,257 | 3,465 | 10 | 3,248 | ||||||||||||||

Net Income from Owned Real Estate | 53,413 | 59,868 | 46,353 | 40,299 | 28,587 | ||||||||||||||

Net loss (income) attributable to noncontrolling interests | 736 | (3,376 | ) | (2,813 | ) | (2,341 | ) | (766 | ) | ||||||||||

Net Income from Owned Real Estate Attributable to W. P. Carey (b) | $ | 54,149 | $ | 56,492 | $ | 43,540 | $ | 37,958 | $ | 27,821 | |||||||||

Basic Earnings Per Share (b) | $ | 0.50 | $ | 0.52 | $ | 0.41 | $ | 0.35 | $ | 0.26 | |||||||||

Diluted Earnings Per Share (b) | $ | 0.50 | $ | 0.52 | $ | 0.40 | $ | 0.35 | $ | 0.26 | |||||||||

Weighted-Average Shares Outstanding | |||||||||||||||||||

Basic | 108,041,556 | 108,019,292 | 107,668,218 | 107,562,484 | 107,487,181 | ||||||||||||||

Diluted | 108,208,918 | 108,143,694 | 107,783,204 | 107,764,279 | 107,715,965 | ||||||||||||||

________

(a) | Amount for the three months ended June 30, 2017 is comprised of an accrual for estimated one-time legal settlement expenses. |

(b) | In connection with our decision to exit non-traded retail fundraising activities, which we announced in June 2017, during the second quarter of 2017 we revised how we view and present our two business segments. As such, equity in earnings of equity method investments in the Managed Programs is now recognized within our Investment Management segment. Earnings from our investment in CCIF continue to be included in our Investment Management segment. Prior periods have been revised to reflect this change. |

| | Investing for the long runTM | 7 | |

W. P. Carey Inc.

Financial Results – Fourth Quarter 2017

Statements of Income, Investment Management – Last Five Quarters | |

In thousands, except share and per share amounts.

Three Months Ended | |||||||||||||||||||

Dec. 31, 2017 | Sep. 30, 2017 | Jun. 30, 2017 | Mar. 31, 2017 | Dec. 31, 2016 | |||||||||||||||

Revenues | |||||||||||||||||||

Asset management revenue | $ | 16,854 | $ | 17,938 | $ | 17,966 | $ | 17,367 | $ | 16,375 | |||||||||

Structuring revenue | 6,217 | 9,817 | 14,330 | 3,834 | 16,338 | ||||||||||||||

Reimbursable costs from affiliates | 6,055 | 6,211 | 13,479 | 25,700 | 20,061 | ||||||||||||||

Dealer manager fees | — | 105 | 1,000 | 3,325 | 2,623 | ||||||||||||||

Other advisory revenue | — | 99 | 706 | 91 | 1,913 | ||||||||||||||

29,126 | 34,170 | 47,481 | 50,317 | 57,310 | |||||||||||||||

Operating Expenses | |||||||||||||||||||

Reimbursable costs from affiliates | 6,055 | 6,211 | 13,479 | 25,700 | 20,061 | ||||||||||||||

General and administrative | 6,011 | 6,002 | 9,726 | 10,150 | 15,292 | ||||||||||||||

Stock-based compensation expense | 2,041 | 2,755 | 2,205 | 4,956 | 2,143 | ||||||||||||||

Subadvisor fees (a) | 2,002 | 5,206 | 3,672 | 2,720 | 4,131 | ||||||||||||||

Depreciation and amortization | 1,064 | 1,070 | 860 | 908 | 958 | ||||||||||||||

Restructuring and other compensation (b) | 289 | 1,356 | 7,718 | — | — | ||||||||||||||

Dealer manager fees and expenses | — | 462 | 2,788 | 3,294 | 3,808 | ||||||||||||||

17,462 | 23,062 | 40,448 | 47,728 | 46,393 | |||||||||||||||

Other Income and Expenses | |||||||||||||||||||

Equity in earnings of equity method investments in the Managed Programs (c) | 13,395 | 12,578 | 12,007 | 13,702 | 13,133 | ||||||||||||||

Other income and (expenses) | 762 | 349 | 455 | 476 | 285 | ||||||||||||||

14,157 | 12,927 | 12,462 | 14,178 | 13,418 | |||||||||||||||

Income before income taxes | 25,821 | 24,035 | 19,495 | 16,767 | 24,335 | ||||||||||||||

(Provision for) benefit from income taxes | (4,761 | ) | (249 | ) | 1,283 | 2,759 | (4,452 | ) | |||||||||||

Net Income from Investment Management Attributable to W. P. Carey (c) | $ | 21,060 | $ | 23,786 | $ | 20,778 | $ | 19,526 | $ | 19,883 | |||||||||

Basic Earnings Per Share (c) | $ | 0.19 | $ | 0.22 | $ | 0.19 | $ | 0.18 | $ | 0.18 | |||||||||

Diluted Earnings Per Share (c) | $ | 0.19 | $ | 0.22 | $ | 0.19 | $ | 0.18 | $ | 0.18 | |||||||||

Weighted-Average Shares Outstanding | |||||||||||||||||||

Basic | 108,041,556 | 108,019,292 | 107,668,218 | 107,562,484 | 107,487,181 | ||||||||||||||

Diluted | 108,208,918 | 108,143,694 | 107,783,204 | 107,764,279 | 107,715,965 | ||||||||||||||

________

(a) | The subadvisors for CWI 1, CWI 2 and CPA:18 – Global earn a percentage of gross fees recorded, which we account for as an expense and which are recorded as Subadvisor fees in our consolidated statements of income. The amounts paid to the subadvisors are the differences between gross and net fees. Pursuant to the terms of the subadvisory agreement we had with the subadvisor in connection with CCIF (prior to our resignation as the advisor to CCIF in the third quarter of 2017), we paid a subadvisory fee equal to 50% of the asset management fees and organization and offering costs paid to us by CCIF. |

(b) | Amounts for the three months ended December 31, 2017, September 30, 2017 and June 30, 2017 represent restructuring expenses resulting from our exit from non-traded retail fundraising activities, which we announced in June 2017. |

(c) | In connection with our previously announced decision to exit non-traded retail fundraising activities, during the second quarter of 2017 we revised how we view and present our two business segments. As such, equity in earnings of equity method investments in the Managed Programs is now recognized within our Investment Management segment. Earnings from our investment in CCIF continue to be included in our Investment Management segment. Prior periods have been revised to reflect this change. |

| | Investing for the long runTM | 8 | |

W. P. Carey Inc.

Financial Results – Fourth Quarter 2017

FFO and AFFO, Consolidated – Last Five Quarters | |

In thousands, except share and per share amounts.

Three Months Ended | |||||||||||||||||||

Dec. 31, 2017 | Sep. 30, 2017 | Jun. 30, 2017 | Mar. 31, 2017 | Dec. 31, 2016 | |||||||||||||||

Net income attributable to W. P. Carey | $ | 75,209 | $ | 80,278 | $ | 64,318 | $ | 57,484 | $ | 47,704 | |||||||||

Adjustments: | |||||||||||||||||||

Depreciation and amortization of real property | 62,603 | 62,621 | 61,636 | 61,182 | 61,373 | ||||||||||||||

Gain on sale of real estate, net | (11,146 | ) | (19,257 | ) | (3,465 | ) | (10 | ) | (3,248 | ) | |||||||||

Impairment charges | 2,769 | — | — | — | 9,433 | ||||||||||||||

Proportionate share of adjustments for noncontrolling interests | (2,696 | ) | (2,692 | ) | (2,562 | ) | (2,541 | ) | (3,184 | ) | |||||||||

Proportionate share of adjustments to equity in net income of partially owned entities | 877 | 866 | 833 | 2,717 | 1,059 | ||||||||||||||

Total adjustments | 52,407 | 41,538 | 56,442 | 61,348 | 65,433 | ||||||||||||||

FFO (as defined by NAREIT) Attributable to W. P. Carey (a) | 127,616 | 121,816 | 120,760 | 118,832 | 113,137 | ||||||||||||||

Adjustments: | |||||||||||||||||||

Above- and below-market rent intangible lease amortization, net (b) | 17,922 | 12,459 | 12,323 | 12,491 | 12,653 | ||||||||||||||

Tax benefit – deferred | (10,497 | ) | (1,234 | ) | (1,382 | ) | (5,551 | ) | (2,433 | ) | |||||||||

Stock-based compensation | 4,268 | 4,635 | 3,104 | 6,910 | 3,051 | ||||||||||||||

Other amortization and non-cash items (c) | 2,198 | 6,208 | 6,693 | 2,094 | 5,584 | ||||||||||||||

Amortization of deferred financing costs | 2,043 | 2,184 | 2,542 | 1,400 | 926 | ||||||||||||||

Straight-line and other rent adjustments | (2,002 | ) | (3,212 | ) | (2,965 | ) | (3,500 | ) | (4,953 | ) | |||||||||

Other expenses (d) | (533 | ) | 65 | 1,000 | 73 | 18 | |||||||||||||

Realized (gains) losses on foreign currency | (472 | ) | (449 | ) | (378 | ) | 403 | 1,102 | |||||||||||

Restructuring and other compensation (e) | 289 | 1,356 | 7,718 | — | — | ||||||||||||||

(Gain) loss on extinguishment of debt | (81 | ) | 1,566 | (2,443 | ) | 912 | 224 | ||||||||||||

Proportionate share of adjustments to equity in net income of partially owned entities | 2,884 | 3,064 | 1,978 | 550 | 2,810 | ||||||||||||||

Proportionate share of adjustments for noncontrolling interests | (1,573 | ) | (216 | ) | (513 | ) | (376 | ) | (595 | ) | |||||||||

Total adjustments | 14,446 | 26,426 | 27,677 | 15,406 | 18,387 | ||||||||||||||

AFFO Attributable to W. P. Carey (a) | $ | 142,062 | $ | 148,242 | $ | 148,437 | $ | 134,238 | $ | 131,524 | |||||||||

Summary | |||||||||||||||||||

FFO (as defined by NAREIT) attributable to W. P. Carey (a) | $ | 127,616 | $ | 121,816 | $ | 120,760 | $ | 118,832 | $ | 113,137 | |||||||||

FFO (as defined by NAREIT) attributable to W. P. Carey per diluted share (a) | $ | 1.18 | $ | 1.13 | $ | 1.12 | $ | 1.10 | $ | 1.05 | |||||||||

AFFO attributable to W. P. Carey (a) | $ | 142,062 | $ | 148,242 | $ | 148,437 | $ | 134,238 | $ | 131,524 | |||||||||

AFFO attributable to W. P. Carey per diluted share (a) | $ | 1.31 | $ | 1.37 | $ | 1.38 | $ | 1.25 | $ | 1.22 | |||||||||

Diluted weighted-average shares outstanding | 108,208,918 | 108,143,694 | 107,783,204 | 107,764,279 | 107,715,965 | ||||||||||||||

________

(a) | FFO and AFFO are non-GAAP measures. See the Terms and Definitions section in the Appendix for a description of our non-GAAP measures. |

(b) | Amount for the three months ended December 31, 2017 includes an adjustment of $5.7 million related to accelerated amortization of an above-market rent intangible in connection with a lease restructuring. |

(c) | Represents primarily unrealized gains and losses from foreign exchange and derivatives. |

(d) | Amount for the three months ended June 30, 2017 is comprised of an accrual for estimated one-time legal settlement expenses. |

(e) | Amounts for the three months ended December 31, 2017, September 30, 2017 and June 30, 2017 represent restructuring expenses resulting from our exit from non-traded retail fundraising activities, which we announced in June 2017. |

| | Investing for the long runTM | 9 | |

W. P. Carey Inc.

Financial Results – Fourth Quarter 2017

FFO and AFFO, Owned Real Estate – Last Five Quarters | |

In thousands, except share and per share amounts.

Three Months Ended | |||||||||||||||||||

Dec. 31, 2017 | Sep. 30, 2017 | Jun. 30, 2017 | Mar. 31, 2017 | Dec. 31, 2016 | |||||||||||||||

Net income from Owned Real Estate attributable to W. P. Carey (a) | $ | 54,149 | $ | 56,492 | $ | 43,540 | $ | 37,958 | $ | 27,821 | |||||||||

Adjustments: | |||||||||||||||||||

Depreciation and amortization of real property | 62,603 | 62,621 | 61,636 | 61,182 | 61,373 | ||||||||||||||

Gain on sale of real estate, net | (11,146 | ) | (19,257 | ) | (3,465 | ) | (10 | ) | (3,248 | ) | |||||||||

Impairment charges | 2,769 | — | — | — | 9,433 | ||||||||||||||

Proportionate share of adjustments for noncontrolling interests | (2,696 | ) | (2,692 | ) | (2,562 | ) | (2,541 | ) | (3,184 | ) | |||||||||

Proportionate share of adjustments to equity in net income of partially owned entities | 877 | 866 | 833 | 2,717 | 1,059 | ||||||||||||||

Total adjustments | 52,407 | 41,538 | 56,442 | 61,348 | 65,433 | ||||||||||||||

FFO (as defined by NAREIT) Attributable to W. P. Carey – Owned Real Estate (a) (b) | 106,556 | 98,030 | 99,982 | 99,306 | 93,254 | ||||||||||||||

Adjustments: | |||||||||||||||||||

Above- and below-market rent intangible lease amortization, net (c) | 17,922 | 12,459 | 12,323 | 12,491 | 12,653 | ||||||||||||||

Tax (benefit) expense – deferred | (15,047 | ) | (2,694 | ) | 33 | (2,460 | ) | 2,273 | |||||||||||

Other amortization and non-cash items (d) | 2,260 | 6,808 | 7,038 | 2,009 | 5,698 | ||||||||||||||

Stock-based compensation | 2,227 | 1,880 | 899 | 1,954 | 908 | ||||||||||||||

Amortization of deferred financing costs | 2,043 | 2,184 | 2,542 | 1,400 | 926 | ||||||||||||||

Straight-line and other rent adjustments | (2,002 | ) | (3,212 | ) | (2,965 | ) | (3,500 | ) | (4,953 | ) | |||||||||

Other expenses (e) | (533 | ) | 65 | 1,000 | 73 | 18 | |||||||||||||

Realized (gains) losses on foreign currency | (477 | ) | (454 | ) | (382 | ) | 395 | 1,136 | |||||||||||

(Gain) loss on extinguishment of debt | (81 | ) | 1,566 | (2,443 | ) | 912 | 224 | ||||||||||||

Proportionate share of adjustments to equity in net income of partially owned entities (a) | 41 | (79 | ) | (92 | ) | (434 | ) | (189 | ) | ||||||||||

Proportionate share of adjustments for noncontrolling interests | (1,573 | ) | (216 | ) | (513 | ) | (376 | ) | (595 | ) | |||||||||

Total adjustments | 4,780 | 18,307 | 17,440 | 12,464 | 18,099 | ||||||||||||||

AFFO Attributable to W. P. Carey – Owned Real Estate (a) (b) | $ | 111,336 | $ | 116,337 | $ | 117,422 | $ | 111,770 | $ | 111,353 | |||||||||

Summary | |||||||||||||||||||

FFO (as defined by NAREIT) attributable to W. P. Carey – Owned Real Estate (a) (b) | $ | 106,556 | $ | 98,030 | $ | 99,982 | $ | 99,306 | $ | 93,254 | |||||||||

FFO (as defined by NAREIT) attributable to W. P. Carey per diluted share – Owned Real Estate (a) (b) | $ | 0.99 | $ | 0.91 | $ | 0.93 | $ | 0.92 | $ | 0.87 | |||||||||

AFFO attributable to W. P. Carey – Owned Real Estate (a) (b) | $ | 111,336 | $ | 116,337 | $ | 117,422 | $ | 111,770 | $ | 111,353 | |||||||||

AFFO attributable to W. P. Carey per diluted share – Owned Real Estate (a) (b) | $ | 1.03 | $ | 1.07 | $ | 1.09 | $ | 1.04 | $ | 1.03 | |||||||||

Diluted weighted-average shares outstanding | 108,208,918 | 108,143,694 | 107,783,204 | 107,764,279 | 107,715,965 | ||||||||||||||

________

(a) | In connection with our decision to exit non-traded retail fundraising activities, which we announced in June 2017, during the second quarter of 2017 we revised how we view and present our two business segments. As such, equity in earnings of equity method investments in the Managed Programs is now recognized within our Investment Management segment. Earnings from our investment in CCIF continue to be included in our Investment Management segment. Prior periods have been revised to reflect this change. |

(b) | FFO and AFFO are non-GAAP measures. See the Terms and Definitions section in the Appendix for a description of our non-GAAP measures. |

(c) | Amount for the three months ended December 31, 2017 includes an adjustment of $5.7 million related to accelerated amortization of an above-market rent intangible in connection with a lease restructuring. |

(d) | Represents primarily unrealized gains and losses from foreign exchange and derivatives. |

(e) | Amount for the three months ended June 30, 2017 is comprised of an accrual for estimated one-time legal settlement expenses. |

| | Investing for the long runTM | 10 | |

W. P. Carey Inc.

Financial Results – Fourth Quarter 2017

FFO and AFFO, Investment Management – Last Five Quarters | |

In thousands, except share and per share amounts.

Three Months Ended | |||||||||||||||||||

Dec. 31, 2017 | Sep. 30, 2017 | Jun. 30, 2017 | Mar. 31, 2017 | Dec. 31, 2016 | |||||||||||||||

Net income from Investment Management attributable to W. P. Carey (a) | $ | 21,060 | $ | 23,786 | $ | 20,778 | $ | 19,526 | $ | 19,883 | |||||||||

FFO (as defined by NAREIT) Attributable to W. P. Carey – Investment Management (a) (b) | 21,060 | 23,786 | 20,778 | 19,526 | 19,883 | ||||||||||||||

Adjustments: | |||||||||||||||||||

Tax expense (benefit) – deferred | 4,550 | 1,460 | (1,415 | ) | (3,091 | ) | (4,706 | ) | |||||||||||

Stock-based compensation | 2,041 | 2,755 | 2,205 | 4,956 | 2,143 | ||||||||||||||

Restructuring and other compensation (c) | 289 | 1,356 | 7,718 | — | — | ||||||||||||||

Other amortization and non-cash items (d) | (62 | ) | (600 | ) | (345 | ) | 85 | (114 | ) | ||||||||||

Realized losses (gains) on foreign currency | 5 | 5 | 4 | 8 | (34 | ) | |||||||||||||

Proportionate share of adjustments to equity in net income of partially owned entities (a) | 2,843 | 3,143 | 2,070 | 984 | 2,999 | ||||||||||||||

Total adjustments | 9,666 | 8,119 | 10,237 | 2,942 | 288 | ||||||||||||||

AFFO Attributable to W. P. Carey – Investment Management (a) (b) | $ | 30,726 | $ | 31,905 | $ | 31,015 | $ | 22,468 | $ | 20,171 | |||||||||

Summary | |||||||||||||||||||

FFO (as defined by NAREIT) attributable to W. P. Carey – Investment Management (a) (b) | $ | 21,060 | $ | 23,786 | $ | 20,778 | $ | 19,526 | $ | 19,883 | |||||||||

FFO (as defined by NAREIT) attributable to W. P. Carey per diluted share – Investment Management (a) (b) | $ | 0.19 | $ | 0.22 | $ | 0.19 | $ | 0.18 | $ | 0.18 | |||||||||

AFFO attributable to W. P. Carey – Investment Management (a) (b) | $ | 30,726 | $ | 31,905 | $ | 31,015 | $ | 22,468 | $ | 20,171 | |||||||||

AFFO attributable to W. P. Carey per diluted share – Investment Management (a) (b) | $ | 0.28 | $ | 0.30 | $ | 0.29 | $ | 0.21 | $ | 0.19 | |||||||||

Diluted weighted-average shares outstanding | 108,208,918 | 108,143,694 | 107,783,204 | 107,764,279 | 107,715,965 | ||||||||||||||

________

(a) | In connection with our decision to exit non-traded retail fundraising activities, which we announced in June 2017, during the second quarter of 2017 we revised how we view and present our two business segments. As such, equity in earnings of equity method investments in the Managed Programs is now recognized within our Investment Management segment. Earnings from our investment in CCIF continue to be included in our Investment Management segment. Prior periods have been revised to reflect this change. |

(b) | FFO and AFFO are non-GAAP measures. See the Terms and Definitions section in the Appendix for a description of our non-GAAP measures. |

(c) | Amounts for the three months ended December 31, 2017, September 30, 2017 and June 30, 2017 represent restructuring expenses resulting from our previously announced exit from non-traded retail fundraising activities. |

(d) | Represents primarily unrealized gains and losses from foreign exchange. |

| | Investing for the long runTM | 11 | |

W. P. Carey Inc.

Financial Results – Fourth Quarter 2017

Elements of Pro Rata Statement of Income and AFFO Adjustments | |

In thousands. For the three months ended December 31, 2017.

We believe that the table below is useful for investors to help them better understand our business by illustrating the impact of each of our AFFO adjustments on our GAAP statement of income line items. This presentation is not an alternative to the GAAP statement of income, nor is AFFO an alternative to net income as determined by GAAP.

Equity Investments (a) | Noncontrolling Interests (b) | AFFO Adjustments | ||||||||||

Revenues | ||||||||||||

Owned Real Estate: | ||||||||||||

Lease revenues | $ | 4,833 | $ | (3,883 | ) | $ | 13,122 | (c) | ||||

Operating property revenues: | ||||||||||||

Hotel revenues | — | — | — | |||||||||

Reimbursable tenant costs | 24 | (123 | ) | (93 | ) | |||||||

Lease termination income and other | — | (12 | ) | (14 | ) | |||||||

Investment Management: | ||||||||||||

Asset management revenue | — | — | — | |||||||||

Structuring revenue | — | — | — | |||||||||

Reimbursable costs from affiliates | — | — | — | |||||||||

Operating Expenses | ||||||||||||

Depreciation and amortization | 363 | (2,703 | ) | (60,293 | ) | (d) | ||||||

General and administrative | — | (6 | ) | — | ||||||||

Reimbursable tenant and affiliate costs | 23 | (125 | ) | (90 | ) | |||||||

Property expenses, excluding reimbursable tenant costs: | ||||||||||||

Hotel expenses | — | — | — | |||||||||

Non-reimbursable property expenses | 24 | (51 | ) | 22 | (e) | |||||||

Stock-based compensation expense | — | — | (4,268 | ) | (e) | |||||||

Impairment charges | — | — | (2,769 | ) | (e) | |||||||

Subadvisor fees (f) | — | — | — | |||||||||

Other expenses | — | — | 533 | |||||||||

Restructuring and other compensation | — | — | (289 | ) | (g) | |||||||

Other Income and Expenses | ||||||||||||

Interest expense | (531 | ) | 295 | 1,876 | (h) | |||||||

Equity in earnings of equity method investments in the Managed Programs and real estate: | ||||||||||||

Income related to our general partnership interests in the Managed REITs (i) | — | (343 | ) | — | ||||||||

Joint ventures | (3,766 | ) | (1 | ) | 514 | (j) | ||||||

Income related to our ownership in the Managed Programs | — | — | 2,843 | (k) | ||||||||

Other income and (expenses) | (1 | ) | 91 | 1,873 | (l) | |||||||

Benefit from income taxes | (149 | ) | 1,827 | (9,276 | ) | (m) | ||||||

Gain on sale of real estate, net of tax | — | — | (11,146 | ) | ||||||||

Net loss attributable to noncontrolling interests | — | (736 | ) | — | ||||||||

________

(a) | Represents the break-out by line item of amounts recorded in Equity in earnings of equity method investments in the Managed Programs and real estate. |

(b) | Represents the break-out by line item of amounts recorded in Net income attributable to noncontrolling interests. |

(c) | For the three months ended December 31, 2017, represents the reversal of amortization of above- or below-market lease intangibles of $15.4 million (including $5.7 million related to accelerated amortization of an above-market rent intangible in connection with a lease restructuring) and the elimination of non-cash amounts related to straight-line rent and other of $2.3 million. |

(d) | Adjustment is a non-cash adjustment excluding corporate depreciation and amortization. |

(e) | Adjustment to exclude a non-cash item. |

(f) | The subadvisors for CWI 1, CWI 2 and CPA:18 – Global earn a percentage of gross fees recorded, which we account for as an expense and which are recorded as Subadvisor fees in our consolidated statements of income. The amounts paid to the subadvisors are the differences between gross and net fees. |

| | Investing for the long runTM | 12 | |

W. P. Carey Inc.

Financial Results – Fourth Quarter 2017

(g) | Adjustment to exclude restructuring expenses resulting from our exit from non-traded retail fundraising activities. |

(h) | Represents the elimination of non-cash components of interest expense, such as deferred financing costs, debt premiums and discounts. |

(i) | Amount includes 100% of CWI 2 general operating partnership distribution, including $0.4 million paid to subadvisors. |

(j) | Adjustments to include our pro rata share of AFFO adjustments from equity investments. |

(k) | Represents Adjusted MFFO from the Managed Programs in place of our pro rata share of net income from our ownership in the Managed Programs. Adjusted MFFO is defined as MFFO adjusted for deferred taxes and excluding the adjustment for realized gains and losses on hedges. |

(l) | Represents eliminations of gains (losses) related to the extinguishment of debt, foreign currency, unrealized gains (losses) on derivatives and other items. |

(m) | Represents primarily the elimination of deferred taxes. |

| | Investing for the long runTM | 13 | |

W. P. Carey Inc.

Financial Results – Fourth Quarter 2017

Capital Expenditures | |

In thousands. For the three months ended December 31, 2017.

Tenant Improvements and Leasing Costs | |||

Tenant improvements | $ | 644 | |

Leasing costs | 1,731 | ||

Tenant Improvements and Leasing Costs | 2,375 | ||

Maintenance Capital Expenditures | |||

Operating properties | 964 | ||

Net-lease properties | 613 | ||

Maintenance Capital Expenditures | 1,577 | ||

Total: Tenant Improvements and Leasing Costs, and Maintenance Capital Expenditures | $ | 3,952 | |

| | Investing for the long runTM | 14 | |

W. P. Carey Inc.

Balance Sheets and Capitalization

Fourth Quarter 2017

| | Investing for the long runTM | 15 | |

W. P. Carey Inc.

Balance Sheets and Capitalization – Fourth Quarter 2017

Consolidated Balance Sheets | |

In thousands, except share and per share amounts.

Dec. 31, | |||||||

2017 | 2016 | ||||||

Assets | |||||||

Investments in real estate: | |||||||

Land, buildings and improvements (a) | $ | 5,457,265 | $ | 5,285,837 | |||

Net investments in direct financing leases | 721,607 | 684,059 | |||||

In-place lease and other intangible assets | 1,213,976 | 1,172,238 | |||||

Above-market rent intangible assets | 640,480 | 632,383 | |||||

Assets held for sale | — | 26,247 | |||||

Investments in real estate | 8,033,328 | 7,800,764 | |||||

Accumulated depreciation and amortization (b) | (1,329,613 | ) | (1,018,864 | ) | |||

Net investments in real estate | 6,703,715 | 6,781,900 | |||||

Equity investments in the Managed Programs and real estate (c) | 341,457 | 298,893 | |||||

Cash and cash equivalents | 162,312 | 155,482 | |||||

Due from affiliates | 105,308 | 299,610 | |||||

Other assets, net | 274,650 | 282,149 | |||||

Goodwill | 643,960 | 635,920 | |||||

Total assets | $ | 8,231,402 | $ | 8,453,954 | |||

Liabilities and Equity | |||||||

Debt: | |||||||

Unsecured senior notes, net | $ | 2,474,661 | $ | 1,807,200 | |||

Unsecured term loans, net | 388,354 | 249,978 | |||||

Unsecured revolving credit facility | 216,775 | 676,715 | |||||

Non-recourse mortgages, net | 1,185,477 | 1,706,921 | |||||

Debt, net | 4,265,267 | 4,440,814 | |||||

Accounts payable, accrued expenses and other liabilities | 263,053 | 266,917 | |||||

Below-market rent and other intangible liabilities, net | 113,957 | 122,203 | |||||

Deferred income taxes | 67,009 | 90,825 | |||||

Distributions payable | 109,766 | 107,090 | |||||

Total liabilities | 4,819,052 | 5,027,849 | |||||

Redeemable noncontrolling interest | 965 | 965 | |||||

Preferred stock, $0.001 par value, 50,000,000 shares authorized; none issued | — | — | |||||

Common stock, $0.001 par value, 450,000,000 shares authorized; 106,922,616 and 106,294,162 shares, respectively, issued and outstanding | 107 | 106 | |||||

Additional paid-in capital | 4,433,573 | 4,399,961 | |||||

Distributions in excess of accumulated earnings | (1,052,064 | ) | (894,137 | ) | |||

Deferred compensation obligation | 46,656 | 50,222 | |||||

Accumulated other comprehensive loss | (236,011 | ) | (254,485 | ) | |||

Total stockholders' equity | 3,192,261 | 3,301,667 | |||||

Noncontrolling interests | 219,124 | 123,473 | |||||

Total equity | 3,411,385 | 3,425,140 | |||||

Total liabilities and equity | $ | 8,231,402 | $ | 8,453,954 | |||

(a) | Includes $83.0 million and $81.7 million of amounts attributable to operating properties as of December 31, 2017 and 2016, respectively. |

(b) | Includes $630.0 million and $484.4 million of accumulated depreciation on buildings and improvements as of December 31, 2017 and 2016, respectively, and $699.7 million and $534.4 million of accumulated amortization on lease intangibles as of December 31, 2017 and 2016, respectively. |

(c) | Our equity investments in the Managed Programs totaled $201.4 million and $160.8 million as of December 31, 2017 and 2016, respectively. Our equity investments in real estate joint ventures totaled $140.0 million and $138.1 million as of December 31, 2017 and 2016, respectively. |

| | Investing for the long runTM | 16 | |

W. P. Carey Inc.

Balance Sheets and Capitalization – Fourth Quarter 2017

Capitalization | |

In thousands, except share and per share amounts. As of December 31, 2017.

Description | Shares | Share Price | Market Value | ||||||||||

Equity | |||||||||||||

Common equity | 106,922,616 | $ | 68.90 | $ | 7,366,968 | ||||||||

Preferred equity | — | ||||||||||||

Total Equity Market Capitalization | 7,366,968 | ||||||||||||

Outstanding Balance (a) | |||||||||||||

Pro Rata Debt | |||||||||||||

Non-recourse mortgages | 1,206,661 | ||||||||||||

Unsecured revolving credit facility | 216,775 | ||||||||||||

Unsecured term loans | 389,773 | ||||||||||||

Unsecured senior notes: | |||||||||||||

Due January 20, 2023 | 599,650 | ||||||||||||

Due April 1, 2024 | 500,000 | ||||||||||||

Due July 19, 2024 | 599,650 | ||||||||||||

Due February 1, 2025 | 450,000 | ||||||||||||

Due October 1, 2026 | 350,000 | ||||||||||||

Total Pro Rata Debt | 4,312,509 | ||||||||||||

Total Capitalization | $ | 11,679,477 | |||||||||||

________

(a) | Excludes unamortized deferred financing costs totaling $16.2 million and unamortized discount, net totaling $13.2 million as of December 31, 2017. |

| | Investing for the long runTM | 17 | |

W. P. Carey Inc.

Balance Sheets and Capitalization – Fourth Quarter 2017

Debt Overview | |

Dollars in thousands. Pro rata. As of December 31, 2017.

USD-Denominated | EUR-Denominated | GBP-Denominated | Total | ||||||||||||||||||||||||||||||

Outstanding Balance | |||||||||||||||||||||||||||||||||

Out-standing Balance (in USD) | Weigh-ted -Avg. Interest Rate | Out-standing Balance (in USD) | Weigh-ted -Avg. Interest Rate | Out-standing Balance (in USD) | Weigh-ted Avg. Interest Rate | Amount (a) (b) (in USD) | % of Total | Weigh-ted -Avg. Interest Rate | Weigh-ted -Avg. Maturity (Years) | ||||||||||||||||||||||||

Non-Recourse Debt | |||||||||||||||||||||||||||||||||

Fixed | $ | 774,308 | 5.7 | % | $ | 122,412 | 4.4 | % | $ | 10,739 | 5.6 | % | $ | 907,459 | 21.1 | % | 5.5 | % | 4.5 | ||||||||||||||

Variable: | |||||||||||||||||||||||||||||||||

Floating | 45,492 | 3.2 | % | 119,146 | 0.9 | % | — | — | % | 164,638 | 3.8 | % | 1.6 | % | 0.8 | ||||||||||||||||||

Swapped | 106,865 | 5.0 | % | 9,033 | 6.2 | % | — | — | % | 115,898 | 2.7 | % | 5.1 | % | 2.7 | ||||||||||||||||||

Capped | — | — | % | 18,666 | 3.3 | % | — | — | % | 18,666 | 0.4 | % | 3.3 | % | 3.6 | ||||||||||||||||||

Total Pro Rata Non-Recourse Debt | 926,665 | 5.5 | % | 269,257 | 2.8 | % | 10,739 | 5.6 | % | 1,206,661 | 28.0 | % | 4.9 | % | 3.8 | ||||||||||||||||||

Recourse Debt | |||||||||||||||||||||||||||||||||

Fixed – Unsecured senior notes: | |||||||||||||||||||||||||||||||||

Due January 20, 2023 | — | — | % | 599,650 | 2.0 | % | — | — | % | 599,650 | 13.9 | % | 2.0 | % | 5.1 | ||||||||||||||||||

Due April 1, 2024 | 500,000 | 4.6 | % | — | — | % | — | — | % | 500,000 | 11.6 | % | 4.6 | % | 6.3 | ||||||||||||||||||

Due July 19, 2024 | — | — | % | 599,650 | 2.3 | % | — | — | % | 599,650 | 13.9 | % | 2.3 | % | 6.6 | ||||||||||||||||||

Due February 1, 2025 | 450,000 | 4.0 | % | — | — | % | — | — | % | 450,000 | 10.5 | % | 4.0 | % | 8.8 | ||||||||||||||||||

Due October 1, 2026 | 350,000 | 4.3 | % | — | — | % | — | — | % | 350,000 | 8.1 | % | 4.3 | % | 7.1 | ||||||||||||||||||

Total Unsecured Senior Notes | 1,300,000 | 4.3 | % | 1,199,300 | 2.1 | % | — | — | % | 2,499,300 | 58.0 | % | 3.3 | % | 6.6 | ||||||||||||||||||

Variable: | |||||||||||||||||||||||||||||||||

Unsecured revolving credit facility (due February 22, 2021) (c) | 105,000 | 2.5 | % | 111,775 | 1.0 | % | — | — | % | 216,775 | 5.0 | % | 1.7 | % | 3.1 | ||||||||||||||||||

Unsecured term loans (due February 22, 2022) (d) | — | — | % | 389,773 | 1.1 | % | — | — | % | 389,773 | 9.0 | % | 1.1 | % | 4.1 | ||||||||||||||||||

Total Recourse Debt | 1,405,000 | 4.2 | % | 1,700,848 | 1.8 | % | — | 3,105,848 | 72.0 | % | 2.9 | % | 5.8 | ||||||||||||||||||||

Total Pro Rata Debt Outstanding | $ | 2,331,665 | $ | 1,970,105 | $ | 10,739 | $ | 4,312,509 | 100.0 | % | 3.4 | % | 5.4 | ||||||||||||||||||||

________

(a) | Debt data is presented on a pro rata basis. See the Terms and Definitions section in the Appendix for a description of pro rata. |

(b) | Excludes unamortized deferred financing costs totaling $16.2 million and unamortized discount, net totaling $13.2 million as of December 31, 2017. |

(c) | Based on the applicable currency, we incurred interest at the London Interbank Offered Rate (LIBOR) or Euro Interbank Offered Rate (EURIBOR) plus 1.00% on our Unsecured revolving credit facility. Availability under our Unsecured revolving credit facility was $1.3 billion as of December 31, 2017. |

(d) | We incurred interest at the EURIBOR plus 1.10% on our Unsecured term loans. |

| | Investing for the long runTM | 18 | |

W. P. Carey Inc.

Balance Sheets and Capitalization – Fourth Quarter 2017

Debt Maturity | |

Dollars in thousands. Pro rata. As of December 31, 2017.

Real Estate | Debt | ||||||||||||||||||||

Number of Properties (a) | Weighted- Average Interest Rate | Total Outstanding Balance (b) (c) | Percent of Total Outstanding Balance | ||||||||||||||||||

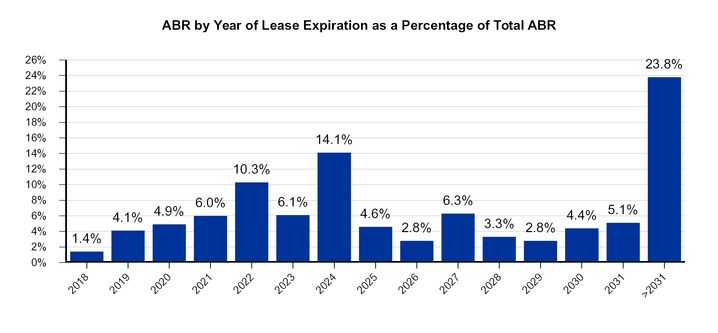

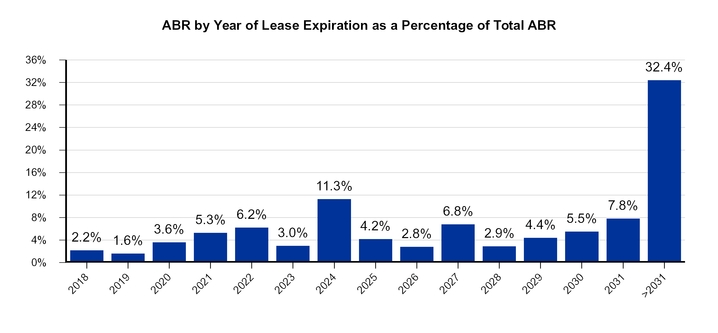

Year of Maturity | ABR (a) | Balloon | |||||||||||||||||||

Non-Recourse Debt | |||||||||||||||||||||

2018 | 29 | $ | 31,494 | 3.1 | % | $ | 198,022 | $ | 199,933 | 4.6 | % | ||||||||||

2019 | 11 | 17,374 | 6.1 | % | 51,450 | 57,208 | 1.3 | % | |||||||||||||

2020 | 22 | 47,412 | 4.8 | % | 222,837 | 252,259 | 5.9 | % | |||||||||||||

2021 | 14 | 25,672 | 5.5 | % | 107,587 | 124,504 | 2.9 | % | |||||||||||||

2022 | 30 | 43,092 | 5.1 | % | 202,421 | 238,335 | 5.5 | % | |||||||||||||

2023 | 25 | 36,362 | 5.2 | % | 91,087 | 135,076 | 3.1 | % | |||||||||||||

2024 | 22 | 20,760 | 5.9 | % | 3,444 | 56,248 | 1.3 | % | |||||||||||||

2025 | 13 | 14,619 | 4.8 | % | 54,052 | 88,962 | 2.1 | % | |||||||||||||

2026 | 7 | 10,086 | 6.6 | % | 18,992 | 43,355 | 1.0 | % | |||||||||||||

2027 | 1 | 2,423 | 5.8 | % | — | 10,781 | 0.3 | % | |||||||||||||

Total Pro Rata Non-Recourse Debt | 174 | $ | 249,294 | 4.9 | % | $ | 949,892 | 1,206,661 | 28.0 | % | |||||||||||

Recourse Debt | |||||||||||||||||||||

Fixed – Unsecured senior notes: | |||||||||||||||||||||

Due January 20, 2023 | 2.0 | % | 599,650 | ||||||||||||||||||

Due April 1, 2024 | 4.6 | % | 500,000 | ||||||||||||||||||

Due July 19, 2024 | 2.3 | % | 599,650 | ||||||||||||||||||

Due February 1, 2025 | 4.0 | % | 450,000 | ||||||||||||||||||

Due October 1, 2026 | 4.3 | % | 350,000 | ||||||||||||||||||

Total Unsecured Senior Notes | 3.3 | % | 2,499,300 | 58.0 | % | ||||||||||||||||

Variable: | |||||||||||||||||||||

Unsecured revolving credit facility (due February 22, 2021) (d) | 1.7 | % | 216,775 | 5.0 | % | ||||||||||||||||

Unsecured term loans (due February 22, 2022) (e) | 1.1 | % | 389,773 | 9.0 | % | ||||||||||||||||

Total Recourse Debt | 2.9 | % | 3,105,848 | 72.0 | % | ||||||||||||||||

Total Pro Rata Debt Outstanding | 3.4 | % | $ | 4,312,509 | 100.0 | % | |||||||||||||||

________

(a) | Represents the number of properties and ABR associated with the debt that is maturing in each respective year. |

(b) | Debt maturity data is presented on a pro rata basis. See the Terms and Definitions section in the Appendix for a description of pro rata. Total outstanding balance includes balloon payments and scheduled amortization for our non-recourse debt. |

(c) | Excludes unamortized deferred financing costs totaling $16.2 million and unamortized discount, net totaling $13.2 million as of December 31, 2017. |

(d) | Based on the applicable currency, we incurred interest at LIBOR or EURIBOR plus 1.00% on our Unsecured revolving credit facility. Availability under our Unsecured revolving credit facility was $1.3 billion as of December 31, 2017. |

(e) | We incurred interest at EURIBOR plus 1.10% on our Unsecured term loans. |

| | Investing for the long runTM | 19 | |

W. P. Carey Inc.

Balance Sheets and Capitalization – Fourth Quarter 2017

Unsecured Senior Notes | |

As of December 31, 2017.

Ratings

Issuer / Corporate | Unsecured Senior Notes | |||||||

Ratings Agency | Rating | Outlook | Rating | Outlook | ||||

Moody's | Baa2 | Stable | Baa2 | Stable | ||||

Standard & Poor's | BBB | Stable | BBB | Stable | ||||

Unsecured Senior Note Covenants

The following is a summary of the key financial covenants for the Unsecured Senior Notes, along with our estimated calculations of our compliance with those covenants at the end of the period presented. These ratios are not measures of our liquidity or performance and serve only to demonstrate our ability to incur additional debt, as permitted by the covenants for the Unsecured Senior Notes.

Covenant | Metric | Required | As of Dec. 31, 2017 | |||

Limitation on the incurrence of debt | "Total Debt" / "Total Assets" | ≤ 60% | 45.3% | |||

Limitation on the incurrence of secured debt | "Secured Debt" / "Total Assets" | ≤ 40% | 12.5% | |||

Limitation on the incurrence of debt based on consolidated EBITDA to annual debt service charge | "Consolidated EBITDA" / "Annual Debt Service Charge" | ≥ 1.5x | 5.0x | |||

Maintenance of unencumbered asset value | "Unencumbered Assets" / "Total Unsecured Debt" | ≥ 150% | 192.1% | |||

| | Investing for the long runTM | 20 | |

W. P. Carey Inc.

Owned Real Estate

Fourth Quarter 2017

| | Investing for the long runTM | 21 | |

W. P. Carey Inc.

Owned Real Estate – Fourth Quarter 2017

Investment Activity – Capital Investment Projects (a) | |

Dollars in thousands. Pro rata.

Primary Transaction Type | Property Type | Estimated Completion | Estimated New Square Footage | Lease Term (Years) | Funded During Three Months Ended Dec. 31, 2017 | Total Funded Through Dec. 31, 2017 | Maximum Commitment | |||||||||||||||||||||||

Tenant | Location | Remaining | Total | |||||||||||||||||||||||||||

Nord Anglia Education, Inc. (b) | Houston, TX | Build-to-Suit | Education Facility | Q1 2018 | 53,000 | 25 | $ | 7,299 | $ | 16,394 | $ | 4,790 | $ | 21,530 | ||||||||||||||||

Schlage Lock Company LLC (c) | Zawiercie, Poland | Build-to-Suit | Industrial | Q2 2018 | 154,550 | 20 | 3,591 | 4,062 | 6,824 | 10,886 | ||||||||||||||||||||

Hellweg Die Profi-Baumärkte GmbH & Co. KG (c) (d) | Germany | Renovation | Retail | Q2 2018 | N/A | 19 | 969 | 969 | 7,634 | 8,603 | ||||||||||||||||||||

Griffith Foods Group Inc. | Chicago, IL | Renovation | Industrial | Q2 2018 | N/A | 20 | — | — | 3,507 | 3,507 | ||||||||||||||||||||

Ontex BVBA (c) | Radomsko, Poland | Build-to-Suit | Industrial | Q3 2018 | 280,897 | 15 | 1,781 | 1,781 | 13,872 | 15,653 | ||||||||||||||||||||

Nord Anglia Education, Inc. (b) | Windermere, FL | Build-to-Suit | Education Facility | Q3 2018 | 38,000 | 25 | 2,072 | 3,476 | 11,920 | 15,442 | ||||||||||||||||||||

Nord Anglia Education, Inc. (b) | Coconut Creek, FL | Build-to-Suit | Education Facility | Q3 2018 | 130,000 | 25 | 8,979 | 8,979 | 15,742 | 24,810 | ||||||||||||||||||||

Astellas US Holding, Inc. | Westborough, MA | Redevelopment | Laboratory | Q3 2019 | N/A | 18 | — | — | 47,655 | 47,655 | ||||||||||||||||||||

Total | 656,447 | $ | 24,691 | $ | 35,661 | $ | 111,944 | $ | 148,086 | |||||||||||||||||||||

________

(a) | This schedule includes future estimates for which we can give no assurance as to timing or amounts. Completed capital projects are included in the Investment Activity – Acquisitions and Completed Capital Projects section. Funding amounts exclude capitalized construction interest. |

(b) | Interest earned on the funding for these properties is excluded from the remaining commitments. |

(c) | Commitment amounts are based on the foreign exchange rate of the euro at period end. |

(d) | This project relates to a jointly owned investment that we consolidate, and in which our affiliate, CPA:17 – Global, has a 36.52% equity interest. Funding and commitment amounts are presented on a pro rata basis. On a consolidated basis, (i) both the amount funded during the three months ended December 31, 2017 and total amount funded through December 31, 2017 was $1.5 million, (ii) the remaining commitment was $12.1 million and (iii) the total maximum commitment was $13.6 million. |

| | Investing for the long runTM | 22 | |

W. P. Carey Inc.

Owned Real Estate – Fourth Quarter 2017

Investment Activity – Acquisitions and Completed Capital Projects | |

Dollars in thousands. Pro rata. For the year ended December 31, 2017.

Gross Investment Amount | Closing Date / Asset Completion Date | Property Type(s) | Gross Square Footage | ||||||||||

Tenant / Lease Guarantor | Property Location(s) | ||||||||||||

Acquisitions | |||||||||||||

1Q17 (N/A) | |||||||||||||

2Q17 | |||||||||||||

Griffith Foods Group Inc. (a) | Chicago, IL | $ | 6,000 | Jun-17 | Industrial | 84,174 | |||||||

2Q17 Total | 6,000 | 84,174 | |||||||||||

3Q17 (N/A) | |||||||||||||

4Q17 | |||||||||||||

Veritas Technologies LLC | Roseville, MN | 25,846 | Nov-17 | Office | 136,125 | ||||||||

4Q17 Total | 25,846 | 136,125 | |||||||||||

Year-to-Date Total | 31,846 | 220,299 | |||||||||||

Completed Capital Projects | |||||||||||||

1Q17 | |||||||||||||

Carl Leipold GmbH | Windsor, CT | 3,302 | Mar-17 | Industrial | 22,704 | ||||||||

1Q17 Total | 3,302 | 22,704 | |||||||||||

2Q17 | |||||||||||||

Nord Anglia Education, Inc. | Coconut Creek, FL | 17,764 | Apr-17 | Education Facility | 40,000 | ||||||||

Inghams Enterprises Pty. Limited (b) | Monarto, Australia | 15,082 | May-17 | Industrial | 386,705 | ||||||||

Gestamp Automocion, S.L. | McCalla, AL | 21,476 | May-17 | Industrial | 178,000 | ||||||||

2Q17 Total | 54,322 | 604,705 | |||||||||||

3Q17 (N/A) | |||||||||||||

4Q17 | |||||||||||||

Banco Santander, S.A. (b) | Mönchengladbach, Germany | 6,421 | Dec-17 | Parking Garage | N/A | ||||||||

6,421 | |||||||||||||

Year-to-Date Total | 64,045 | 627,409 | |||||||||||

Year-to-Date Total Acquisitions and Completed Capital Projects | $ | 95,891 | 847,708 | ||||||||||

________

(a) | We also committed to fund an additional $3.6 million of building improvements. |

(b) | Amount reflects the applicable exchange rate on the date of the transaction. |

| | Investing for the long runTM | 23 | |

W. P. Carey Inc.

Owned Real Estate – Fourth Quarter 2017

Investment Activity – Dispositions | |

Dollars in thousands. Pro rata. For the year ended December 31, 2017.

Tenant / Lease Guarantor | Property Location(s) | Gross Sale Price | Closing Date | Property Type(s) | Gross Square Footage | ||||||||

1Q17 | |||||||||||||

Vacant (2 properties) (a) (b) | Espoo, Finland | $ | 28,122 | Jan-17 | Office | 466,483 | |||||||

DuraFiber Technologies (a) | Bad Hersfeld, Germany | 24,083 | Jan-17 | Industrial, Office, Warehouse | 858,958 | ||||||||

Vacant (a) | Doncaster, United Kingdom | 626 | Feb-17 | Land | N/A | ||||||||

1Q17 Total | 52,831 | 1,325,441 | |||||||||||

2Q17 | |||||||||||||

Vacant | Houston, TX | 1,375 | May-17 | Warehouse | 25,125 | ||||||||

Vacant | Glendale Heights, IL | 2,125 | May-17 | Office | 35,455 | ||||||||

Bouygues Telecom and Grand-Est International Campus (a) | Illkirch-Graffenstaden, France | 5,150 | May-17 | Office | 72,163 | ||||||||

Pendragon PLC (2 properties) (a) (c) | Doncaster and Newport, United Kingdom | 11,478 | Jun-17 | Retail | 34,429 | ||||||||

2Q17 Total | 20,128 | 167,172 | |||||||||||

3Q17 | |||||||||||||

Bestop, Inc. and Servtech, Inc. (d) | Louisville, CO | 25,560 | Jul-17 | Industrial | 403,871 | ||||||||

IDS Group Ltd. (a) | Shah Alam, Malaysia | 21,351 | Aug-17 | Industrial | 374,751 | ||||||||

Pendragon PLC (a) (c) | Cheltenham, United Kingdom | 4,312 | Aug-17 | Retail | 10,630 | ||||||||

Vacant (a) | Leeds, United Kingdom | 4,379 | Aug-17 | Industrial, Office | 199,618 | ||||||||

Moog, Inc. | Radford, VA | 3,975 | Sep-17 | Industrial | 68,631 | ||||||||

3Q17 Total | 59,577 | 1,057,501 | |||||||||||

4Q17 | |||||||||||||

Vacant | Yakima, WA | 400 | Nov-17 | Warehouse | 11,165 | ||||||||

Actuant Corporation (a) | Kahl, Germany | 18,026 | Dec-17 | Industrial | 305,692 | ||||||||

Vacant | Citrus Heights, CA | 4,000 | Dec-17 | Retail | 89,760 | ||||||||

IDS Group Ltd. (2 properties) (a) | Lam Luk Ka and Bang Pa-in, Thailand | 36,641 | Dec-17 | Warehouse | 772,822 | ||||||||

4Q17 Total | 59,067 | 1,179,439 | |||||||||||

Year-to-Date Total Dispositions | $ | 191,603 | 3,729,553 | ||||||||||

________

(a) | Amount reflects the applicable exchange rate on the date of the transaction. |

(b) | In January 2017, we transferred ownership of these properties and the related non-recourse mortgage loan to the mortgage lender. Amount represents the carrying value of the mortgage loan on date of transfer, less cash held in escrow that was retained by the mortgage lender. |

(c) | Following the disposition of three properties leased to Pendragon PLC during the year ended December 31, 2017, we still own a portfolio of 70 properties leased to that tenant. |

(d) | This multi-tenant property had approximately 197,000 vacant square feet as of the date of disposition. |

| | Investing for the long runTM | 24 | |

W. P. Carey Inc.

Owned Real Estate – Fourth Quarter 2017

Joint Ventures | |

Dollars in thousands. As of December 31, 2017.

Joint Venture or JV (Principal Tenant) | JV Partnership | Consolidated | Pro Rata (a) | |||||||||||||||||

Partner | WPC % | Debt Outstanding (b) | ABR | Debt Outstanding (c) | ABR | |||||||||||||||

Unconsolidated Joint Ventures (Equity Method Investments) (d) | ||||||||||||||||||||

Wanbishi Archives Co. Ltd. (e) | CPA:17 – Global | 3.00% | $ | — | $ | 2,710 | $ | — | $ | 81 | ||||||||||

Jumbo Logistiek Vastgoed B.V. (e) | CPA:17 – Global | 15.00% | 76,518 | 14,742 | 11,478 | 2,211 | ||||||||||||||

ALSO Actebis GmbH (e) | CPA:17 – Global | 30.00% | — | 3,988 | — | 1,196 | ||||||||||||||

Wagon Automotive GmbH (e) | CPA:17 – Global | 33.33% | — | 3,448 | — | 1,149 | ||||||||||||||

Frontier Spinning Mills, Inc. | CPA:17 – Global | 40.00% | — | 5,237 | — | 2,095 | ||||||||||||||

The New York Times Company | CPA:17 – Global | 45.00% | 101,093 | 27,247 | 45,492 | 12,261 | ||||||||||||||

Total Unconsolidated Joint Ventures | 177,611 | 57,372 | 56,970 | 18,993 | ||||||||||||||||

Consolidated Joint Ventures | ||||||||||||||||||||

Berry Global Inc. (f) | CPA:17 – Global | 50.00% | 23,396 | 7,426 | 11,698 | 3,713 | ||||||||||||||

Tesco Global Aruhazak Zrt. (e) | CPA:17 – Global | 51.00% | 36,599 | 6,932 | 18,665 | 3,535 | ||||||||||||||

Dick’s Sporting Goods, Inc. (f) | CPA:17 – Global | 55.10% | 18,936 | 3,559 | 10,434 | 1,961 | ||||||||||||||

Hellweg Die Profi-Baumärkte GmbH & Co. KG (e) (f) | CPA:17 – Global | 63.48% | — | 33,387 | — | 21,194 | ||||||||||||||

Eroski Sociedad Cooperativa (e) | CPA:17 – Global | 70.00% | — | 2,510 | — | 1,757 | ||||||||||||||

U-Haul Moving Partners, Inc. and Mercury Partners, LP | CPA:17 – Global | 88.46% | — | 36,008 | — | 31,853 | ||||||||||||||

McCoy-Rockford, Inc. | Third party | 90.00% | 3,433 | 857 | 3,089 | 771 | ||||||||||||||

Total Consolidated Joint Ventures | 82,364 | 90,679 | 43,886 | 64,784 | ||||||||||||||||

Total Unconsolidated and Consolidated Joint Ventures | $ | 259,975 | $ | 148,051 | $ | 100,856 | $ | 83,777 | ||||||||||||

________

(a) | See the Terms and Definitions section in the Appendix for a description of pro rata. |

(b) | Excludes unamortized deferred financing costs totaling $0.7 million and unamortized premium, net totaling $0.3 million as of December 31, 2017. |

(c) | Excludes unamortized deferred financing costs totaling $0.2 million and unamortized premium, net totaling $0.1 million as of December 31, 2017. |

(d) | Excludes a preferred equity position in a jointly owned investment, Beach House JV, LLC, which did not have debt outstanding or ABR as of December 31, 2017. |

(e) | Amounts are based on the applicable exchange rate at the end of the period. |

(f) | Excludes certain properties leased to the tenants that we consolidate and in which we have a 100% ownership interest. |

| | Investing for the long runTM | 25 | |

W. P. Carey Inc.

Owned Real Estate – Fourth Quarter 2017

Top Ten Tenants | |

Dollars in thousands. Pro rata. As of December 31, 2017.

Tenant / Lease Guarantor | Property Type | Tenant Industry | Location | Number of Properties | ABR | ABR Percent | Weighted-Average Lease Term (Years) | ||||||||||||

Hellweg Die Profi-Baumärkte GmbH & Co. KG (a) | Retail | Retail Stores | Germany | 53 | $ | 36,375 | 5.3 | % | 16.2 | ||||||||||

U-Haul Moving Partners Inc. and Mercury Partners, LP | Self Storage | Cargo Transportation, Consumer Services | United States | 78 | 31,853 | 4.7 | % | 6.3 | |||||||||||

State of Andalucia (a) | Office | Sovereign and Public Finance | Spain | 70 | 29,163 | 4.3 | % | 17.0 | |||||||||||

Pendragon PLC (a) | Retail | Retail Stores, Consumer Services | United Kingdom | 70 | 22,266 | 3.3 | % | 12.3 | |||||||||||

Marriott Corporation | Hotel | Hotel, Gaming and Leisure | United States | 18 | 20,065 | 2.9 | % | 5.9 | |||||||||||

Forterra Building Products (a) (b) | Industrial | Construction and Building | United States and Canada | 49 | 17,496 | 2.6 | % | 18.3 | |||||||||||

OBI Group (a) | Office, Retail | Retail Stores | Poland | 18 | 16,565 | 2.4 | % | 6.4 | |||||||||||

True Value Company | Warehouse | Retail Stores | United States | 7 | 15,680 | 2.3 | % | 5.0 | |||||||||||

UTI Holdings, Inc. | Education Facility | Consumer Services | United States | 5 | 14,484 | 2.1 | % | 4.2 | |||||||||||

ABC Group Inc. (c) | Industrial, Office, Warehouse | Automotive | Canada, Mexico and United States | 14 | 14,110 | 2.1 | % | 18.9 | |||||||||||

Total (d) | 382 | $ | 218,057 | 32.0 | % | 11.5 | |||||||||||||

________

(a) | ABR amounts are subject to fluctuations in foreign currency exchange rates. |

(b) | Of the 49 properties leased to Forterra Building Products, 44 are located in the United States and five are located in Canada. |

(c) | Of the 14 properties leased to ABC Group Inc., six are located in Canada, four are located in Mexico and four are located in the United States, subject to three master leases all denominated in U.S. dollars. |

(d) | See the Terms and Definitions section in the Appendix for a description of pro rata. |

| | Investing for the long runTM | 26 | |

W. P. Carey Inc.

Owned Real Estate – Fourth Quarter 2017

Diversification by Property Type | |

In thousands, except percentages. Pro rata. As of December 31, 2017.

Total Net-Lease Portfolio | Unencumbered Net-Lease Portfolio (a) | ||||||||||||||||||||||||||

Property Type | ABR | ABR Percent | Square Footage (b) | Sq. ft. Percent | ABR | ABR Percent | Square Footage (b) | Sq. ft. Percent | |||||||||||||||||||

U.S. | |||||||||||||||||||||||||||

Industrial | $ | 139,580 | 20.5 | % | 27,867 | 32.8 | % | $ | 76,969 | 17.8 | % | 16,650 | 29.6 | % | |||||||||||||

Office | 105,566 | 15.5 | % | 6,419 | 7.6 | % | 44,597 | 10.3 | % | 3,095 | 5.5 | % | |||||||||||||||

Retail | 28,051 | 4.1 | % | 2,121 | 2.5 | % | 15,974 | 3.7 | % | 1,260 | 2.3 | % | |||||||||||||||

Warehouse | 74,641 | 11.0 | % | 14,859 | 17.5 | % | 38,206 | 8.9 | % | 7,779 | 13.8 | % | |||||||||||||||

Self Storage | 31,853 | 4.7 | % | 3,535 | 4.2 | % | 31,853 | 7.4 | % | 3,535 | 6.3 | % | |||||||||||||||

Other (c) | 68,638 | 10.1 | % | 4,344 | 5.1 | % | 31,498 | 7.3 | % | 1,872 | 3.3 | % | |||||||||||||||

U.S. Total | 448,329 | 65.9 | % | 59,145 | 69.7 | % | 239,097 | 55.4 | % | 34,191 | 60.8 | % | |||||||||||||||

International | |||||||||||||||||||||||||||

Industrial | 62,774 | 9.2 | % | 10,451 | 12.3 | % | 61,328 | 14.2 | % | 10,269 | 18.3 | % | |||||||||||||||

Office | 64,718 | 9.5 | % | 4,715 | 5.5 | % | 51,241 | 11.9 | % | 4,119 | 7.3 | % | |||||||||||||||

Retail | 84,493 | 12.4 | % | 7,569 | 8.9 | % | 68,095 | 15.8 | % | 5,762 | 10.3 | % | |||||||||||||||

Warehouse | 20,358 | 3.0 | % | 3,019 | 3.6 | % | 11,617 | 2.7 | % | 1,867 | 3.3 | % | |||||||||||||||

Self Storage | — | — | % | — | — | % | — | — | % | — | — | % | |||||||||||||||

Other | — | — | % | — | — | % | — | — | % | — | — | % | |||||||||||||||

International Total | 232,343 | 34.1 | % | 25,754 | 30.3 | % | 192,281 | 44.6 | % | 22,017 | 39.2 | % | |||||||||||||||

Total | |||||||||||||||||||||||||||

Industrial | 202,354 | 29.7 | % | 38,318 | 45.1 | % | 138,297 | 32.0 | % | 26,919 | 47.9 | % | |||||||||||||||

Office | 170,284 | 25.0 | % | 11,134 | 13.1 | % | 95,838 | 22.2 | % | 7,214 | 12.8 | % | |||||||||||||||

Retail | 112,544 | 16.5 | % | 9,690 | 11.4 | % | 84,069 | 19.5 | % | 7,022 | 12.6 | % | |||||||||||||||

Warehouse | 94,999 | 14.0 | % | 17,878 | 21.1 | % | 49,823 | 11.6 | % | 9,646 | 17.1 | % | |||||||||||||||

Self Storage | 31,853 | 4.7 | % | 3,535 | 4.2 | % | 31,853 | 7.4 | % | 3,535 | 6.3 | % | |||||||||||||||

Other (c) | 68,638 | 10.1 | % | 4,344 | 5.1 | % | 31,498 | 7.3 | % | 1,872 | 3.3 | % | |||||||||||||||

Total (d) | $ | 680,672 | 100.0 | % | 84,899 | 100.0 | % | $ | 431,378 | 100.0 | % | 56,208 | 100.0 | % | |||||||||||||

________

(a) | Represents properties unencumbered by non-recourse mortgage debt. |

(b) | Includes square footage for vacant properties. |

(c) | Includes ABR from tenants with the following property types: education facility, hotel, theater, fitness facility and net-lease student housing. |

(d) | See the Terms and Definitions section in the Appendix for a description of pro rata. |

| | Investing for the long runTM | 27 | |

W. P. Carey Inc.

Owned Real Estate – Fourth Quarter 2017

Diversification by Tenant Industry | |

In thousands, except percentages. Pro rata. As of December 31, 2017.