Exhibit 13.01

STATEMENT OF FINANCIAL RESPONSIBILITY AND MANAGEMENT’S REPORT

ON INTERNAL CONTROL OVER FINANCIAL REPORTING

Management’s Statement of Responsibility

The

management of Martin Marietta Materials, Inc. (the “Company” or “Martin Marietta”), is responsible for the consolidated financial statements, the related financial information contained in this 2017 Annual Report and the

establishment and maintenance of adequate internal control over financial reporting. The consolidated balance sheets for Martin Marietta, at December 31, 2017 and 2016, and the related consolidated statements of earnings, comprehensive

earnings, total equity and cash flows for each of the three years in the period ended December 31, 2017, include amounts based on estimates and judgments and have been prepared in accordance with accounting principles generally accepted in the

United States applied on a consistent basis.

A system of internal control over financial reporting is designed to provide reasonable assurance, in

a cost-effective manner, that assets are safeguarded, transactions are executed and recorded in accordance with management’s authorization, accountability for assets is maintained and financial statements are prepared and presented fairly in

accordance with accounting principles generally accepted in the United States. Internal control systems over financial reporting have inherent limitations and may not prevent or detect misstatements. Therefore, even those systems determined to be

effective can provide only reasonable assurance with respect to financial statement preparation and presentation.

The Company operates in an

environment that establishes an appropriate system of internal control over financial reporting and ensures that the system is maintained, assessed and monitored on a periodic basis. This internal control system includes examinations by internal

audit staff and oversight by the Audit Committee of the Board of Directors.

The Company’s management recognizes its responsibility to foster a

strong ethical climate. Management has issued written policy statements that document the Company’s business code of ethics. The importance of ethical behavior is regularly communicated to all employees through the distribution of the Code

of Ethical Business Conduct booklet and through ongoing education and review programs designed to create a strong commitment to ethical business practices.

The Audit Committee of the Board of Directors, which consists of four independent, nonemployee directors, meets periodically and separately with

management, the independent auditors and the internal auditors to review the activities of each. The Audit Committee meets standards established by the Securities and Exchange Commission (SEC) and the New York Stock Exchange as they relate to the

composition and practices of audit committees.

Management’s Report on Internal Control over Financial Reporting

The management of Martin Marietta is responsible for establishing and maintaining adequate control over financial reporting. Management assessed the

effectiveness of the Company’s internal control over financial reporting as of December 31, 2017. In making this assessment, management used the criteria set forth in Internal Control – Integrated Framework issued by the

Committee of Sponsoring Organizations of the Treadway Commission (2013 framework) (COSO). Based on management’s assessment under the 2013 framework, management concluded that the Company’s internal control over financial reporting was

effective as of December 31, 2017.

The 2017 consolidated financial statements and effectiveness of internal control over financial reporting

have been audited by PricewaterhouseCoopers LLP, an independent registered public accounting firm, whose report appears on the following page.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| C. Howard Nye |

|

|

|

James A. J. Nickolas |

| Chairman, President and Chief Executive Officer |

|

|

|

Senior Vice President and Chief Financial Officer |

| February 23, 2018 |

|

|

|

|

Martin

Marietta | Page 7

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To Board of Directors and Shareholders of Martin Marietta Materials, Inc.

Opinions on the Financial Statements and Internal Control over Financial Reporting

We have audited the accompanying consolidated balance sheets of Martin Marietta Materials, Inc. and its subsidiaries as of December 31, 2017 and

2016, and the related consolidated statements of earnings, comprehensive earnings, total equity, and cash flows for each of the two years in the period ended December 31, 2017, including the related notes and schedule of valuation and

qualifying accounts for each of the two years in the period ended December 31, 2017 appearing under Item 15(a)(2) (collectively referred to as the “consolidated financial statements”). We also have audited the Company’s internal

control over financial reporting as of December 31, 2017, based on criteria established in Internal Control - Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO).

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of the

Company as of December 31, 2017 and 2016, and the results of their operations and their cash flows for each of the two years in the period ended December 31, 2017 in conformity with accounting principles generally accepted in the United

States of America. Also in our opinion, the Company maintained, in all material respects, effective internal control over financial reporting as of December 31, 2017, based on criteria established in Internal Control - Integrated

Framework (2013) issued by the COSO.

Basis for Opinions

The Company’s management is responsible for these consolidated financial statements, for maintaining effective internal control over financial

reporting, and for its assessment of the effectiveness of internal control over financial reporting, included in the accompanying Management’s Report on Internal Control over Financial Reporting. Our responsibility is to express opinions on the

Company’s consolidated financial statements and on the Company’s internal control over financial reporting based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States)

(“PCAOB”) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable

assurance about whether the consolidated financial statements are free of material misstatement, whether due to error or fraud, and whether effective internal control over financial reporting was maintained in all material respects.

Our audits of the consolidated financial statements included performing procedures to assess the risks of material misstatement of the consolidated

financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements.

Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. Our audit of internal control over financial

reporting included obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, and testing and evaluating the design and operating effectiveness of internal control based on the

assessed risk. Our audits also included performing such other procedures as we considered necessary in the circumstances. We believe that our audits provide a reasonable basis for our opinions.

Definition and Limitations of Internal Control over Financial Reporting

A company’s internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial

reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company’s internal control over financial reporting includes those policies and procedures that

(i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (ii) provide reasonable assurance that transactions are recorded as

necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors

of the company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any

evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

|

|

|

| Raleigh, North Carolina |

|

/s/ PricewaterhouseCoopers LLP |

| February 23, 2018 |

|

We have served as the Company’s auditor since 2016. |

Martin

Marietta | Page 8

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To Board of Directors and Shareholders of Martin Marietta Materials, Inc.

We have audited the accompanying consolidated statements of earnings, comprehensive earnings, total equity and cash flows of Martin Marietta Materials,

Inc. and consolidated subsidiaries for the year ended December 31, 2015. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our

audit.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards

require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the

financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable

basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the consolidated

results of operations and cash flows of Martin Marietta Materials, Inc. and consolidated subsidiaries for the year ended December 31, 2015, in conformity with U.S. generally accepted accounting principles.

Raleigh, North Carolina

February 23, 2016, except for the recently adopted accounting pronouncements discussed in Note A and the effects of the segment change discussed in

Note O, as to which the date is May 12, 2017

Martin

Marietta | Page 9

|

|

|

| CONSOLIDATED STATEMENTS OF EARNINGS

for years ended December 31 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (add 000, except per share) |

|

2017 |

|

|

|

|

2016 |

|

|

|

|

2015 |

|

| Net Sales |

|

$ |

3,721,428 |

|

|

|

|

$ |

3,576,767 |

|

|

|

|

|

3,268,116 |

|

| Freight and delivery revenues |

|

|

244,166 |

|

|

|

|

|

241,982 |

|

|

|

|

|

271,454 |

|

| Total revenues |

|

|

3,965,594 |

|

|

|

|

|

3,818,749 |

|

|

|

|

|

3,539,570 |

|

| Cost of sales |

|

|

2,749,488 |

|

|

|

|

|

2,665,029 |

|

|

|

|

|

2,541,196 |

|

| Freight and delivery costs |

|

|

244,166 |

|

|

|

|

|

241,982 |

|

|

|

|

|

271,454 |

|

| Total cost of revenues |

|

|

2,993,654 |

|

|

|

|

|

2,907,011 |

|

|

|

|

|

2,812,650 |

|

| Gross Profit |

|

|

971,940 |

|

|

|

|

|

911,738 |

|

|

|

|

|

726,920 |

|

| Selling, general and administrative expenses |

|

|

262,128 |

|

|

|

|

|

241,606 |

|

|

|

|

|

210,754 |

|

| Acquisition-related expenses |

|

|

8,638 |

|

|

|

|

|

909 |

|

|

|

|

|

6,346 |

|

| Other operating expenses and (income), net |

|

|

793 |

|

|

|

|

|

(8,043 |

) |

|

|

|

|

15,653 |

|

| Earnings from Operations |

|

|

700,381 |

|

|

|

|

|

677,266 |

|

|

|

|

|

494,167 |

|

| Interest expense |

|

|

91,487 |

|

|

|

|

|

81,677 |

|

|

|

|

|

76,287 |

|

| Other nonoperating (income) and expenses, net |

|

|

(10,034 |

) |

|

|

|

|

(11,439 |

) |

|

|

|

|

4,079 |

|

| Earnings before income tax (benefit) expense |

|

|

618,928 |

|

|

|

|

|

607,028 |

|

|

|

|

|

413,801 |

|

| Income tax (benefit) expense |

|

|

(94,457 |

) |

|

|

|

|

181,584 |

|

|

|

|

|

124,863 |

|

| Consolidated net earnings |

|

|

713,385 |

|

|

|

|

|

425,444 |

|

|

|

|

|

288,938 |

|

| Less: Net earnings attributable to noncontrolling interests |

|

|

43 |

|

|

|

|

|

58 |

|

|

|

|

|

146 |

|

| Net Earnings Attributable to

Martin Marietta |

|

$ |

713,342 |

|

|

|

|

$ |

425,386 |

|

|

|

|

$ |

288,792 |

|

|

|

|

|

|

|

| Net Earnings Attributable to Martin Marietta Per Common Share (see Note A) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| – Basic attributable to common shareholders |

|

$ |

11.30 |

|

|

|

|

$ |

6.66 |

|

|

|

|

$ |

4.31 |

|

| – Diluted attributable to common shareholders |

|

$ |

11.25 |

|

|

|

|

$ |

6.63 |

|

|

|

|

$ |

4.29 |

|

|

|

|

|

|

|

| Weighted-Average Common Shares Outstanding |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| – Basic |

|

|

62,932 |

|

|

|

|

|

63,610 |

|

|

|

|

|

66,770 |

|

| – Diluted |

|

|

63,217 |

|

|

|

|

|

63,861 |

|

|

|

|

|

67,020 |

|

The notes on pages 15 through 41 are an integral part of these financial statements.

Martin

Marietta | Page 10

|

|

|

| CONSOLIDATED STATEMENTS OF

COMPREHENSIVE EARNINGS for years ended December 31 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (add 000) |

|

2017 |

|

|

|

|

2016 |

|

|

|

|

2015 |

|

| Consolidated Net Earnings |

|

$ |

713,385 |

|

|

|

|

$ |

425,444 |

|

|

|

|

$ |

288,938 |

|

| Other comprehensive (loss) earnings, net of tax: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Defined benefit pension and postretirement plans: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net loss arising during period, net of tax of $(2,625), $(19,734) and $(4,530), respectively |

|

|

(8,052 |

) |

|

|

|

|

(31,620 |

) |

|

|

|

|

(7,101 |

) |

| Amortization of prior service credit, net of tax of $(547), $(617) and $(731), respectively |

|

|

(883 |

) |

|

|

|

|

(992 |

) |

|

|

|

|

(1,149 |

) |

| Amortization of actuarial loss, net of tax of $5,271, $4,437 and $6,551, respectively |

|

|

8,503 |

|

|

|

|

|

7,138 |

|

|

|

|

|

10,299 |

|

| Amount recognized in net periodic pension cost due to settlement, net of tax of $8, $44 and $0,

respectively |

|

|

13 |

|

|

|

|

|

71 |

|

|

|

|

|

– |

|

| Amount recognized in net periodic pension cost due to special plan termination benefits, net of tax of $0,

$293 and $811, respectively |

|

|

– |

|

|

|

|

|

471 |

|

|

|

|

|

1,274 |

|

|

|

|

(419 |

) |

|

|

|

|

(24,932 |

) |

|

|

|

|

3,323 |

|

|

|

|

|

|

|

| Foreign currency translation gain (loss) |

|

|

1,140 |

|

|

|

|

|

(898 |

) |

|

|

|

|

(3,542 |

) |

|

|

|

|

|

|

| Amortization of terminated value of forward starting interest rate swap agreements into interest expense,

net of tax of $571, $541 and $509, respectively |

|

|

872 |

|

|

|

|

|

826 |

|

|

|

|

|

771 |

|

| |

|

|

1,593 |

|

|

|

|

|

(25,004 |

) |

|

|

|

|

552 |

|

| Consolidated comprehensive earnings |

|

|

714,978 |

|

|

|

|

|

400,440 |

|

|

|

|

|

289,490 |

|

| Less: Comprehensive earnings attributable to noncontrolling interests |

|

|

53 |

|

|

|

|

|

119 |

|

|

|

|

|

161 |

|

| Comprehensive Earnings

Attributable to Martin Marietta |

|

$ |

714,925 |

|

|

|

|

$ |

400,321 |

|

|

|

|

$ |

289,329 |

|

The notes on pages 15 through 41 are an integral part of these financial statements.

Martin

Marietta | Page 11

|

|

|

| CONSOLIDATED BALANCE SHEETS

at December 31 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Assets (add 000) |

|

2017 |

|

|

|

|

2016 |

|

| Current Assets: |

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents |

|

$ |

1,446,364 |

|

|

|

|

$ |

50,038 |

|

| Accounts receivable, net |

|

|

487,240 |

|

|

|

|

|

457,910 |

|

| Inventories, net |

|

|

600,591 |

|

|

|

|

|

521,624 |

|

| Other current assets |

|

|

96,965 |

|

|

|

|

|

56,813 |

|

| Total Current Assets |

|

|

2,631,160 |

|

|

|

|

|

1,086,385 |

|

|

|

|

|

| Property, plant and equipment, net |

|

|

3,592,813 |

|

|

|

|

|

3,423,395 |

|

| Goodwill |

|

|

2,160,290 |

|

|

|

|

|

2,159,337 |

|

| Operating permits, net |

|

|

439,116 |

|

|

|

|

|

442,202 |

|

| Other intangibles, net |

|

|

67,233 |

|

|

|

|

|

69,110 |

|

| Other noncurrent assets |

|

|

101,899 |

|

|

|

|

|

120,476 |

|

| Total Assets |

|

$ |

8,992,511 |

|

|

|

|

$ |

7,300,905 |

|

|

|

|

|

| Liabilities and Equity (add 000, except parenthetical share

data) |

|

|

|

|

|

|

|

|

|

|

| Current Liabilities: |

|

|

|

|

|

|

|

|

|

|

| Accounts payable |

|

$ |

186,638 |

|

|

|

|

$ |

178,598 |

|

| Accrued salaries, benefits and payroll taxes |

|

|

44,255 |

|

|

|

|

|

47,428 |

|

| Pension and postretirement benefits |

|

|

13,652 |

|

|

|

|

|

9,293 |

|

| Accrued insurance and other taxes |

|

|

64,958 |

|

|

|

|

|

60,093 |

|

| Current maturities of long-term debt |

|

|

299,909 |

|

|

|

|

|

180,036 |

|

| Other current liabilities |

|

|

87,804 |

|

|

|

|

|

71,140 |

|

| Total Current

Liabilities |

|

|

694,216 |

|

|

|

|

|

546,588 |

|

|

|

|

|

| Long-term debt |

|

|

2,727,294 |

|

|

|

|

|

1,506,153 |

|

| Pension, postretirement and postemployment benefits |

|

|

244,043 |

|

|

|

|

|

248,086 |

|

| Deferred income taxes, net |

|

|

410,723 |

|

|

|

|

|

663,019 |

|

| Other noncurrent liabilities |

|

|

233,758 |

|

|

|

|

|

194,469 |

|

| Total Liabilities |

|

|

4,310,034 |

|

|

|

|

|

3,158,315 |

|

|

|

|

|

| Equity: |

|

|

|

|

|

|

|

|

|

|

| Common stock ($0.01 par value; 100,000,000 shares authorized; 62,873,000 and 63,176,000 shares outstanding

at December 31, 2017 and 2016, respectively) |

|

|

628 |

|

|

|

|

|

630 |

|

| Preferred stock ($0.01 par value; 10,000,000 shares authorized; no shares outstanding) |

|

|

– |

|

|

|

|

|

– |

|

| Additional paid-in capital |

|

|

3,368,007 |

|

|

|

|

|

3,334,461 |

|

| Accumulated other comprehensive loss |

|

|

(129,104 |

) |

|

|

|

|

(130,687 |

) |

| Retained earnings |

|

|

1,440,069 |

|

|

|

|

|

935,574 |

|

| Total Shareholders’ Equity |

|

|

4,679,600 |

|

|

|

|

|

4,139,978 |

|

| Noncontrolling interests |

|

|

2,877 |

|

|

|

|

|

2,612 |

|

| Total Equity |

|

|

4,682,477 |

|

|

|

|

|

4,142,590 |

|

| Total Liabilities and

Equity |

|

$ |

8,992,511 |

|

|

|

|

$ |

7,300,905 |

|

The notes on pages 15 through 41 are an integral part of these financial statements.

Martin

Marietta | Page 12

|

|

|

| CONSOLIDATED STATEMENTS OF CASH FLOWS

for years ended December 31 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (add 000) |

|

2017 |

|

|

|

|

2016 |

|

|

|

|

2015 |

|

| Cash Flows from Operating Activities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Consolidated net earnings |

|

$ |

713,385 |

|

|

|

|

$ |

425,444 |

|

|

|

|

$ |

288,938 |

|

| Adjustments to reconcile consolidated net earnings to net cash provided by operating activities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Depreciation, depletion and amortization |

|

|

297,162 |

|

|

|

|

|

285,253 |

|

|

|

|

|

263,587 |

|

| Stock-based compensation expense |

|

|

30,460 |

|

|

|

|

|

20,481 |

|

|

|

|

|

13,589 |

|

| (Gain) Loss on divestitures and sales of assets |

|

|

(19,366 |

) |

|

|

|

|

410 |

|

|

|

|

|

14,093 |

|

| Deferred income taxes, net |

|

|

(239,056 |

) |

|

|

|

|

67,050 |

|

|

|

|

|

85,225 |

|

| Other items, net |

|

|

(13,157 |

) |

|

|

|

|

(17,730 |

) |

|

|

|

|

(5,972 |

) |

| Changes in operating assets and liabilities, net of effects of acquisitions and divestitures: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accounts receivable, net |

|

|

(29,329 |

) |

|

|

|

|

(25,072 |

) |

|

|

|

|

12,309 |

|

| Inventories, net |

|

|

(78,966 |

) |

|

|

|

|

(47,381 |

) |

|

|

|

|

(21,525 |

) |

| Accounts payable |

|

|

(17,874 |

) |

|

|

|

|

(8,116 |

) |

|

|

|

|

(40,053 |

) |

| Other assets and liabilities, net |

|

|

14,619 |

|

|

|

|

|

(11,106 |

) |

|

|

|

|

(29,591 |

) |

| Net Cash Provided by Operating

Activities |

|

|

657,878 |

|

|

|

|

|

689,233 |

|

|

|

|

|

580,600 |

|

|

|

|

|

|

|

| Cash Flows from Investing Activities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Additions to property, plant and equipment |

|

|

(410,325 |

) |

|

|

|

|

(387,267 |

) |

|

|

|

|

(318,232 |

) |

| Acquisitions |

|

|

(12,095 |

) |

|

|

|

|

(178,768 |

) |

|

|

|

|

(43,215 |

) |

| Cash received in acquisition |

|

|

– |

|

|

|

|

|

4,246 |

|

|

|

|

|

63 |

|

| Proceeds from divestitures and sales of assets |

|

|

35,941 |

|

|

|

|

|

6,476 |

|

|

|

|

|

448,122 |

|

| Payment of railcar construction advances |

|

|

(43,594 |

) |

|

|

|

|

(82,910 |

) |

|

|

|

|

(25,234 |

) |

| Reimbursement of railcar construction advances |

|

|

43,594 |

|

|

|

|

|

82,910 |

|

|

|

|

|

25,234 |

|

| Repayments from affiliate |

|

|

– |

|

|

|

|

|

– |

|

|

|

|

|

1,808 |

|

| Net Cash (Used for) Provided By

Investing Activities |

|

|

(386,479 |

) |

|

|

|

|

(555,313 |

) |

|

|

|

|

88,546 |

|

|

|

|

|

|

|

| Cash Flows from Financing Activities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Borrowings of long-term debt |

|

|

2,408,830 |

|

|

|

|

|

560,000 |

|

|

|

|

|

230,000 |

|

| Repayments of long-term debt |

|

|

(1,065,048 |

) |

|

|

|

|

(449,306 |

) |

|

|

|

|

(244,704 |

) |

| Payments of deferred acquisition consideration |

|

|

(2,774 |

) |

|

|

|

|

– |

|

|

|

|

|

– |

|

| Debt issuance costs |

|

|

(2,204 |

) |

|

|

|

|

(2,300 |

) |

|

|

|

|

– |

|

| Change in bank overdraft |

|

|

– |

|

|

|

|

|

(10,235 |

) |

|

|

|

|

10,052 |

|

| Payments on capital lease obligations |

|

|

(3,543 |

) |

|

|

|

|

(3,364 |

) |

|

|

|

|

(6,616 |

) |

| Dividends paid |

|

|

(108,852 |

) |

|

|

|

|

(105,036 |

) |

|

|

|

|

(107,462 |

) |

| Distributions to owners of noncontrolling interest |

|

|

– |

|

|

|

|

|

(400 |

) |

|

|

|

|

(325 |

) |

| Contributions by noncontrolling interest to joint venture |

|

|

212 |

|

|

|

|

|

44 |

|

|

|

|

|

– |

|

| Repurchase of common stock |

|

|

(99,999 |

) |

|

|

|

|

(259,228 |

) |

|

|

|

|

(519,962 |

) |

| Proceeds from exercise of stock options |

|

|

10,110 |

|

|

|

|

|

27,257 |

|

|

|

|

|

37,230 |

|

| Shares withheld for employees’ income tax obligations |

|

|

(11,805 |

) |

|

|

|

|

(9,723 |

) |

|

|

|

|

(7,601 |

) |

| Net Cash Provided by (Used for)

Financing Activities |

|

|

1,124,927 |

|

|

|

|

|

(252,291 |

) |

|

|

|

|

(609,388 |

) |

| Net Increase (Decrease) in Cash and Cash Equivalents |

|

|

1,396,326 |

|

|

|

|

|

(118,371 |

) |

|

|

|

|

59,758 |

|

| Cash and Cash Equivalents, beginning of year |

|

|

50,038 |

|

|

|

|

|

168,409 |

|

|

|

|

|

108,651 |

|

|

|

|

|

|

|

| Cash and Cash Equivalents, end of year |

|

$ |

1,446,364 |

|

|

|

|

$ |

50,038 |

|

|

|

|

$ |

168,409 |

|

The notes on pages 15 through 41 are an integral part of these financial statements.

Martin

Marietta | Page 13

|

|

|

| CONSOLIDATED STATEMENTS OF TOTAL

EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (add 000, except per share data) |

|

Shares of

Common

Stock |

|

|

Common

Stock |

|

|

Additional

Paid-In

Capital |

|

|

Accumulated

Other

Comprehensive

(Loss) Earnings |

|

|

Retained

Earnings |

|

|

Total

Shareholders’

Equity |

|

|

Non-

controlling

Interests |

|

|

Total

Equity |

|

| Balance at December 31, 2014 |

|

|

67,293 |

|

|

$ |

671 |

|

|

$ |

3,243,619 |

|

|

$ |

(106,159) |

|

|

$ |

1,213,035 |

|

|

$ |

4,351,166 |

|

|

$ |

1,582 |

|

|

$ |

4,352,748 |

|

|

|

|

|

|

|

|

|

|

| Consolidated net earnings |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

288,792 |

|

|

|

288,792 |

|

|

|

146 |

|

|

|

288,938 |

|

| Other comprehensive earnings |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

537 |

|

|

|

– |

|

|

|

537 |

|

|

|

15 |

|

|

|

552 |

|

| Dividends declared ($1.60 per common share) |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

(107,462 |

) |

|

|

(107,462) |

|

|

|

– |

|

|

|

(107,462) |

|

| Issuances of common stock for stock award plans |

|

|

471 |

|

|

|

5 |

|

|

|

30,619 |

|

|

|

– |

|

|

|

– |

|

|

|

30,624 |

|

|

|

– |

|

|

|

30,624 |

|

| Repurchases of common stock |

|

|

(3,285 |

) |

|

|

(33 |

) |

|

|

– |

|

|

|

– |

|

|

|

(519,929 |

) |

|

|

(519,962) |

|

|

|

– |

|

|

|

(519,962) |

|

| Stock-based compensation expense |

|

|

– |

|

|

|

– |

|

|

|

13,589 |

|

|

|

– |

|

|

|

– |

|

|

|

13,589 |

|

|

|

– |

|

|

|

13,589 |

|

| Noncontrolling interest acquired from business combination |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

1,475 |

|

|

|

1,475 |

|

| Purchase of subsidiary shares from noncontrolling interest |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

(325) |

|

|

|

(325) |

|

| Balance at December 31, 2015 |

|

|

64,479 |

|

|

|

643 |

|

|

|

3,287,827 |

|

|

|

(105,622) |

|

|

|

874,436 |

|

|

|

4,057,284 |

|

|

|

2,893 |

|

|

|

4,060,177 |

|

|

|

|

|

|

|

|

|

|

| Consolidated net earnings |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

425,386 |

|

|

|

425,386 |

|

|

|

58 |

|

|

|

425,444 |

|

| Other comprehensive (loss) earnings |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

(25,065) |

|

|

|

– |

|

|

|

(25,065) |

|

|

|

61 |

|

|

|

(25,004 |

) |

| Dividends declared ($1.64 per common share) |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

(105,036 |

) |

|

|

(105,036) |

|

|

|

– |

|

|

|

(105,036 |

) |

| Issuances of common stock for stock award plans |

|

|

285 |

|

|

|

3 |

|

|

|

26,109 |

|

|

|

– |

|

|

|

– |

|

|

|

26,112 |

|

|

|

– |

|

|

|

26,112 |

|

| Repurchases of common stock |

|

|

(1,588 |

) |

|

|

(16) |

|

|

|

– |

|

|

|

– |

|

|

|

(259,212 |

) |

|

|

(259,228) |

|

|

|

– |

|

|

|

(259,228 |

) |

| Stock-based compensation expense |

|

|

– |

|

|

|

– |

|

|

|

20,481 |

|

|

|

– |

|

|

|

– |

|

|

|

20,481 |

|

|

|

– |

|

|

|

20,481 |

|

| Distributions to owners of noncontrolling interest |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

(400) |

|

|

|

(400 |

) |

| Contribution from owners of noncontrolling interest |

|

|

– |

|

|

|

– |

|

|

|

44 |

|

|

|

– |

|

|

|

– |

|

|

|

44 |

|

|

|

– |

|

|

|

44 |

|

| Balance at December 31, 2016 |

|

|

63,176 |

|

|

|

630 |

|

|

|

3,334,461 |

|

|

|

(130,687) |

|

|

|

935,574 |

|

|

|

4,139,978 |

|

|

|

2,612 |

|

|

|

4,142,590 |

|

|

|

|

|

|

|

|

|

|

| Consolidated net earnings |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

713,342 |

|

|

|

713,342 |

|

|

|

43 |

|

|

|

713,385 |

|

| Other comprehensive earnings |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

1,583 |

|

|

|

– |

|

|

|

1,583 |

|

|

|

10 |

|

|

|

1,593 |

|

| Dividends declared ($1.72 per common share) |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

(108,852 |

) |

|

|

(108,852) |

|

|

|

– |

|

|

|

(108,852 |

) |

| Issuances of common stock for stock award plans |

|

|

155 |

|

|

|

2 |

|

|

|

14,891 |

|

|

|

– |

|

|

|

– |

|

|

|

14,893 |

|

|

|

– |

|

|

|

14,893 |

|

| Shares withheld for employees’ income tax obligations |

|

|

– |

|

|

|

– |

|

|

|

(11,805 |

) |

|

|

– |

|

|

|

– |

|

|

|

(11,805) |

|

|

|

– |

|

|

|

(11,805 |

) |

| Repurchases of common stock |

|

|

(458 |

) |

|

|

(4 |

) |

|

|

– |

|

|

|

– |

|

|

|

(99,995 |

) |

|

|

(99,999) |

|

|

|

– |

|

|

|

(99,999 |

) |

| Stock-based compensation expense |

|

|

– |

|

|

|

– |

|

|

|

30,460 |

|

|

|

– |

|

|

|

– |

|

|

|

30,460 |

|

|

|

– |

|

|

|

30,460 |

|

| Contribution from owners of noncontrolling interest |

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

212 |

|

|

|

212 |

|

| Balance at December 31, 2017 |

|

|

62,873 |

|

|

$ |

628 |

|

|

$ |

3,368,007 |

|

|

$ |

(129,104) |

|

|

$ |

1,440,069 |

|

|

$ |

4,679,600 |

|

|

$ |

2,877 |

|

|

$ |

4,682,477 |

|

The notes on pages 15 through 41 are an integral part of these financial statements.

Martin

Marietta | Page 14

NOTES TO FINANCIAL STATEMENTS

Note A: Accounting Policies

Organization. Martin Marietta Materials, Inc. (the

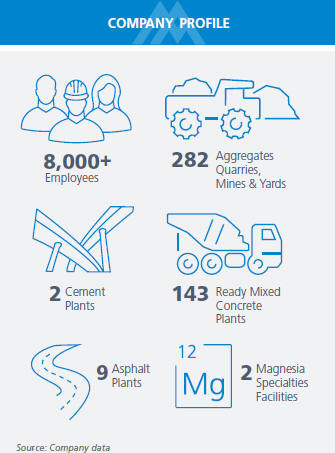

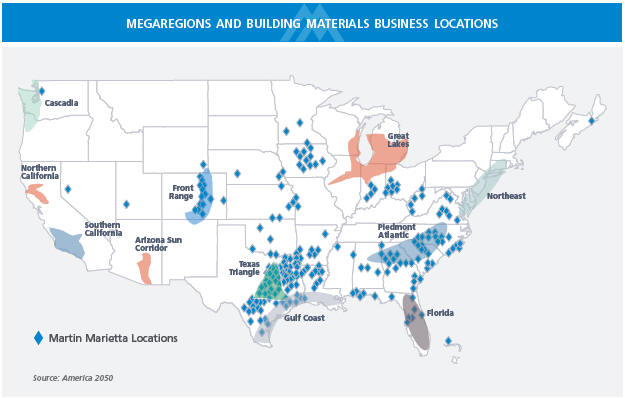

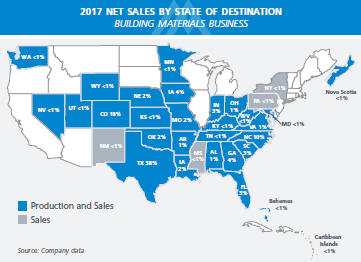

“Company” or “Martin Marietta”) is a natural resource-based building materials company. The Company supplies aggregates (crushed stone, sand and gravel) through its network of 282 quarries, mines and distribution yards to its

customers in 30 states, Canada, the Bahamas and the Caribbean Islands. In the western United States, Martin Marietta also provides cement and downstream products, namely, ready mixed concrete, asphalt and paving services, in markets where the

Company has a leading aggregates position. Specifically, the Company has two cement plants in Texas, five cement distribution facilities and 152 ready mixed concrete and asphalt plants in Texas, Colorado, Louisiana and Arkansas. The Company’s

heavy-side building materials are used in infrastructure, nonresidential and residential construction projects. Aggregates are also used in agricultural, utility and environmental applications and as railroad ballast. The aggregates, cement, ready

mixed concrete and asphalt and paving product lines are reported collectively as the “Building Materials” business. As of December 31, 2017, the Building Materials business contains the following reportable segments: Mid-America Group, Southeast Group and West Group. The Mid-America Group operates in Indiana, Iowa, northern Kansas, Kentucky, Maryland, Minnesota, Missouri, eastern Nebraska,

North Carolina, Ohio, South Carolina, Virginia, Washington and West Virginia. The Southeast Group has operations in Alabama, Florida, Georgia, Tennessee, Nova Scotia and the Bahamas. The West Group operates in Arkansas, Colorado, southern Kansas,

Louisiana, western Nebraska, Nevada, Oklahoma, Texas, Utah and Wyoming. The following states accounted for 74% of the Building Materials business’ 2017 net sales: Texas, Colorado, North Carolina, Iowa and Georgia.

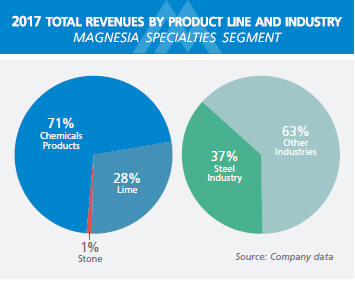

The Company also operates a Magnesia Specialties business, which produces magnesia-based chemical products used in industrial, agricultural and

environmental applications, and dolomitic lime sold primarily to customers in the steel and mining industries. Magnesia Specialties’ production facilities are located in Ohio and Michigan, and products are shipped to customers worldwide.

Use of Estimates. The preparation of the

Company’s consolidated financial statements in conformity with accounting principles generally accepted in the United States (U.S. GAAP) requires management to make certain estimates and assumptions about future events. These estimates and the

underlying assumptions affect the amounts of assets and liabilities reported, disclosures about contingent assets and liabilities and reported amounts of

revenues and expenses. Such estimates include the valuation of accounts receivable, inventories, goodwill, intangible assets and other long-lived assets and assumptions used in the calculation of

income tax (benefit) expense, retirement and other postemployment benefits, and the allocation of the purchase price to the fair values of assets acquired and liabilities assumed as part of business combinations. These estimates and assumptions are

based on management’s judgment. Management evaluates estimates and assumptions on an ongoing basis using historical experience and other factors, including the current economic environment, and adjusts such estimates and assumptions when facts

and circumstances dictate. Changes in credit, equity and energy markets and changes in construction activity increase the uncertainty inherent in certain estimates and assumptions. As future events and their effects cannot be determined with

precision, actual results could differ significantly from estimates. Changes in estimates, including those resulting from continuing changes in the economic environment, are reflected in the consolidated financial statements for the period in which

the change in estimate occurs.

Basis of Consolidation. The consolidated financial statements include the accounts of the Company and its wholly-owned and majority-owned subsidiaries. Partially-owned affiliates are either consolidated or accounted for at cost or as equity

investments, depending on the level of ownership interest or the Company’s ability to exercise control over the affiliates’ operations. Intercompany balances and transactions have been eliminated in consolidation.

Revenue Recognition. Total revenues include sales

of materials and services provided to customers, net of discounts or allowances, if any, and include freight and delivery costs billed to customers. Revenues for product sales are recognized when risks associated with ownership have passed to

unaffiliated customers. Typically, this occurs when finished products are shipped. Revenues derived from the paving business are recognized using the

percentage-of-completion method under the revenue-cost approach. Under the revenue-cost approach, recognized contract revenue equals the total estimated contract revenue

multiplied by the percentage of completion. Recognized costs equal the total estimated contract cost multiplied by the percentage of completion. The percentage of completion is determined by costs incurred to date as a percentage of total costs

estimated for the project.

Freight and Delivery Costs. Freight and delivery costs represent pass-through transportation costs incurred and paid

Martin

Marietta | Page 15

NOTES TO FINANCIAL STATEMENTS (continued)

by the Company to third-party carriers to deliver products to customers. These costs are then billed to

the customers.

Cash and Cash Equivalents.

Cash equivalents are comprised of highly-liquid instruments with original maturities of three months or less from the date of purchase. The Company manages its cash and cash equivalents to ensure short-term operating cash needs are met and excess

funds are managed efficiently. When operating cash is not sufficient to meet current needs, the Company borrows money under its existing credit facilities. The Company utilizes excess cash to either pay down credit facility borrowings or invest in

money market funds, money market demand deposit accounts or offshore time deposit accounts. Money market demand deposits and offshore time deposit accounts are exposed to bank solvency risk.

Customer Receivables. Customer receivables are

stated at cost. The Company does not typically charge interest on customer accounts receivables. The Company records an allowance for doubtful accounts, which includes a provision for probable losses based on historical write offs and a specific

reserve for accounts deemed at risk. The Company writes off customer receivables as bad debt expense when it becomes probable based upon customer facts and circumstances that such amounts will not be collected.

Inventories Valuation. Inventories are stated at

the lower of cost or net realizable value. Costs for finished products and in process inventories are determined by the first-in, first-out method. Carrying value for

expendable parts and supplies are determined by the weighted-average cost method. The Company records an allowance for finished product inventories based on an analysis of inventory on hand in excess of historical sales for a twelve-month period or

five-year average and future demand. The Company also establishes an allowance for expendable parts over five years old and supplies over one year old.

Post-production stripping costs, which represent costs of removing overburden and waste materials to access mineral deposits, are a component of

inventory production costs and recognized in cost of sales in the same period as the revenue from the sale of the inventory.

Property, Plant and Equipment. Property, plant and equipment are stated at cost.

The estimated service lives for property, plant and equipment are as follows:

|

|

|

| Class of Assets |

|

Range of Service Lives |

| Buildings |

|

5 to 20 years |

| Machinery & Equipment |

|

2 to 20 years |

| Land Improvements |

|

5 to 60 years |

The Company begins capitalizing quarry development costs at a point when reserves are determined to be proven or

probable, economically mineable and when demand supports investment in the market. Capitalization of these costs ceases when production commences. Capitalized quarry development costs are classified as land improvements and depreciated over the life

of the reserves.

The Company reviews relevant facts and circumstances to determine whether to capitalize or expense

pre-production stripping costs when additional pits are developed at an existing quarry. If the additional pit operates in a separate and distinct area of the quarry, these costs are capitalized as quarry

development costs and depreciated over the life of the uncovered reserves. Additionally, a separate asset retirement obligation is created for additional pits when the liability is incurred. Once a pit enters the production phase, all

post-production stripping costs are charged to inventory production costs as incurred.

Mineral reserves and mineral interests acquired in

connection with a business combination are valued using an income approach over the life of the reserves.

Depreciation is computed based on

estimated service lives, principally using the straight-line method. Depletion of mineral reserves is calculated based on proven and probable reserves using the

units-of-production method on a quarry-by-quarry basis.

Property, plant and equipment are reviewed for impairment whenever facts and circumstances indicate that the carrying amount of an asset group may not

be recoverable. An impairment loss is recognized if expected future undiscounted cash flows over the estimated remaining service life of the related asset are less than the asset’s carrying value.

Repair and Maintenance Costs. Repair and

maintenance costs that do not substantially extend the life of the Company’s plant and equipment are expensed as incurred.

Goodwill and Intangible Assets. Goodwill represents the excess purchase price paid for acquired businesses over

Martin

Marietta | Page 16

NOTES TO FINANCIAL STATEMENTS (continued)

the estimated fair value of identifiable assets and liabilities. Other intangibles represent amounts

assigned principally to contractual agreements and are amortized ratably over periods based on related contractual terms.

The Company’s

reporting units, which represent the level at which goodwill is tested for impairment, are based on the geographic segments of the Building Materials business. Goodwill is assigned to the respective reporting unit(s) based on the location of

acquisitions at the time of consummation. Goodwill is tested for impairment by comparing the reporting unit’s fair value to its carrying value, which represents Step 1 of a two-step approach. However,

prior to Step 1, the Company may perform an optional qualitative assessment and evaluate macroeconomic conditions, industry and market conditions, cost factors, overall financial performance and other business or reporting unit-specific events. If

the Company concludes it is more-likely-than-not (i.e., a likelihood of more than 50%) that a reporting unit’s fair value is higher than its carrying value, the Company does not perform any further

goodwill impairment testing for that reporting unit. Otherwise, it proceeds to Step 1 of its goodwill impairment analysis. The Company may bypass the qualitative assessment for any reporting unit in any period and proceed directly with the

quantitative calculation in Step 1. If the reporting unit’s fair value exceeds its carrying value, no further calculation is necessary. A reporting unit with a carrying value in excess of its fair value constitutes a Step 1 failure and may lead

to an impairment charge.

The carrying values of goodwill and other indefinite-lived intangible assets are reviewed annually, as of October 1,

for impairment. An interim review is performed between annual tests if facts and circumstances indicate potential impairment. The carrying value of other amortizable intangibles is reviewed if facts and circumstances indicate potential impairment.

If a review indicates the carrying value is impaired, a charge is recorded.

Retirement Plans

and Postretirement Benefits. The Company sponsors defined benefit retirement plans and also provides other postretirement benefits. The Company recognizes the funded status, defined as the difference

between the fair value of plan assets and the benefit obligation, of its pension plans and other postretirement benefits as an asset or liability on the consolidated balance sheets. Actuarial gains or losses that arise during the year are

not recognized as net periodic benefit cost in the same year, but rather are recognized as a component of accumulated other comprehensive earnings or loss. Those amounts are amortized over the

participants’ average remaining service period and recognized as a component of net periodic benefit cost. The amount amortized is determined using a corridor approach and represents the excess over 10% of the greater of the projected benefit

obligation or pension plan assets.

Stock-Based Compensation. The Company has stock-based compensation plans for employees and its Board of Directors. The Company recognizes all forms of stock-based awards that vest, including stock options, as compensation expense. The compensation

expense is the fair value of the awards at the measurement date and is recognized over the requisite service period.

The fair value of

restricted stock awards, incentive compensation stock awards and Board of Directors’ fees paid in the form of common stock are based on the closing price of the Company’s common stock on the awards’ respective grant dates. The fair

value of performance stock awards is determined by a Monte Carlo simulation methodology.

In 2017 and 2016, the Company did not issue any stock

options. For stock options issued prior to 2016, the Company used the accelerated expense recognition method. The accelerated recognition method requires stock options that vest ratably to be divided into tranches. The expense for each tranche is

allocated to its particular vesting period.

The Company uses the lattice valuation model to determine the fair value of stock option awards. The

lattice valuation model takes into account employees’ exercise patterns based on changes in the Company’s stock price and other variables. The period of time for which options are expected to be outstanding is a derived output of the

lattice valuation model and includes the following considerations: vesting period of the award, expected volatility of the underlying stock and employees’ ages.

Key assumptions used in determining the fair value of the stock options awarded in 2015 were:

|

|

|

|

|

| Risk-free interest rate |

|

|

2.20% |

|

| Dividend yield |

|

|

1.20% |

|

| Volatility factor |

|

|

36.10% |

|

| Expected term |

|

|

8.5 years |

|

Martin

Marietta | Page 17

NOTES TO FINANCIAL STATEMENTS (continued)

Based on these assumptions, the weighted-average fair value of each stock option granted in 2015 was

$57.71.

The risk-free interest rate reflects the interest rate on zero-coupon U.S. government bonds,

available at the time each option was granted, having a remaining life approximately equal to the option’s expected life. The dividend yield represents the dividend rate expected to be paid over the option’s expected life. The

Company’s volatility factor measures the amount by which its stock price is expected to fluctuate during the expected life of the option and is based on historical stock price changes. Forfeitures are required to be estimated at the time of

grant and revised, if necessary, in subsequent periods if actual forfeitures differ from those estimates. The Company estimates forfeitures and will ultimately recognize compensation cost only for those stock-based awards that vest.

Environmental Matters. The Company records a

liability for an asset retirement obligation at fair value in the period in which it is incurred. The asset retirement obligation is recorded at the acquisition date of a long-lived tangible asset if the fair value can be reasonably estimated. A

corresponding amount is capitalized as part of the asset’s carrying amount. The fair value is affected by management’s assumptions regarding the scope of the work required, inflation rates and quarry closure dates.

Further, the Company records an accrual for other environmental remediation liabilities in the period in which it is probable that a liability has been

incurred and the appropriate amounts can be estimated reasonably. Such accruals are adjusted as further information develops or circumstances change. Generally, these costs are not discounted to their present value or offset for potential insurance

or other claims or potential gains from future alternative uses for a site.

Income

Taxes. Deferred income taxes, net, on the consolidated balance sheets reflect the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting

purposes and the amounts used for income tax purposes, net of valuation allowances. The effect on deferred income tax assets and liabilities attributable to changes in enacted tax rates are charged or credited to income tax expense or benefit in the

period of enactment.

Uncertain Tax Positions. The Company recognizes a tax benefit when it is more-likely-than-not, based on the technical merits, that a tax position would be sustained upon examination by a taxing authority.

The amount to be recognized is measured as the largest amount of tax benefit that is greater than 50%

likely of being realized upon ultimate settlement with a taxing authority that has full knowledge of all relevant information. The Company’s unrecognized tax benefits are recorded in other

liabilities on the consolidated balance sheets or as an offset to the deferred tax asset for tax carryforwards where available.

The Company

records interest accrued in relation to unrecognized tax benefits as income tax expense. Penalties, if incurred, are recorded as operating expenses in the consolidated statements of earnings.

Sales Taxes. Sales taxes collected from customers

are recorded as liabilities until remitted to taxing authorities and therefore are not reflected in the consolidated statements of earnings.

Start-Up Costs. Noncapital start-up costs for new facilities and products are charged to operations as incurred.

Warranties. The Company’s construction

contracts contain warranty provisions covering defects in materials, design or workmanship that generally run from nine months to one year after project completion. Due to the nature of its projects, including contract owner inspections of the work

both during construction and prior to acceptance, the Company has not experienced material warranty costs for these short-term warranties and therefore does not believe an accrual for these costs is necessary. The ready mixed concrete product line

carries a longer warranty period, for which the Company has accrued an estimate of warranty cost based on experience with the type of work and any known risks relative to the projects. These costs were not material to the Company’s consolidated

results of operations for the years ended December 31, 2017, 2016 and 2015.

Consolidated Comprehensive Earnings and Accumulated Other Comprehensive Loss. Consolidated comprehensive earnings for the Company consist of consolidated net earnings, adjustments for the funded status of pension and postretirement benefit plans, foreign currency translation adjustments and the

amortization of the value of terminated forward starting interest rate swap agreements into interest expense, and are presented in the Company’s consolidated statements of comprehensive earnings.

Accumulated other comprehensive loss consists of unrecognized gains and losses related to the funded status of the pension and postretirement benefit

plans, foreign currency translation and the unamortized value of terminated forward starting interest rate swap agreements, and is presented on the Company’s consolidated balance sheets.

Martin

Marietta | Page 18

NOTES TO FINANCIAL STATEMENTS (continued)

The components of the changes in accumulated other comprehensive loss and related cumulative

noncurrent deferred tax assets are as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| years ended December 31 (add 000)

|

|

Pension and

Postretirement Benefit Plans

|

|

|

Foreign

Currency |

|

|

Unamortized

Value of Terminated

Forward Starting Interest

Rate Swap |

|

|

Total |

|

| |

|

|

| |

|

|

2017 |

|

| |

|

| Accumulated other comprehensive loss at beginning of period |

|

|

|

$ |

(128,373) |

|

|

$ |

(1,162 |

) |

|

$ |

(1,152) |

|

|

$ |

(130,687) |

|

|

|

|

|

|

|

|

| Other comprehensive (loss) earnings before reclassifications, net of tax |

|

|

|

|

(8,062) |

|

|

|

1,140 |

|

|

|

– |

|

|

|

(6,922) |

|

| Amounts reclassified from accumulated other comprehensive loss, net of tax |

|

|

|

|

7,633 |

|

|

|

– |

|

|

|

872 |

|

|

|

8,505 |

|

|

|

|

|

|

|

|

| Other comprehensive (loss) earnings, net of tax |

|

|

|

|

(429) |

|

|

|

1,140 |

|

|

|

872 |

|

|

|

1,583 |

|

|

|

|

|

|

|

|

| Accumulated other comprehensive loss at end of period |

|

|

|

$ |

(128,802) |

|

|

$ |

(22 |

) |

|

$ |

(280) |

|

|

$ |

(129,104) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cumulative noncurrent deferred tax assets at end of period |

|

|

|

$ |

79,938 |

|

|

$ |

– |

|

|

$ |

178 |

|

|

$ |

80,116 |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

2016 |

|

| |

|

| Accumulated other comprehensive loss at beginning of period |

|

|

|

$ |

(103,380) |

|

|

$ |

(264 |

) |

|

$ |

(1,978) |

|

|

$ |

(105,622) |

|

|

|

|

|

|

|

|

| Other comprehensive loss before reclassifications, net of tax |

|

|

|

|

(31,678) |

|

|

|

(898 |

) |

|

|

– |

|

|

|

(32,576) |

|

| Amounts reclassified from accumulated other comprehensive loss, net of tax |

|

|

|

|

6,685 |

|

|

|

– |

|

|

|

826 |

|

|

|

7,511 |

|

|

|

|

|

|

|

|

| Other comprehensive (loss) earnings, net of tax |

|

|

|

|

(24,993) |

|

|

|

(898 |

) |

|

|

826 |

|

|

|

(25,065) |

|

|

|

|

|

|

|

|

| Accumulated other comprehensive loss at end of period |

|

|

|

$ |

(128,373) |

|

|

$ |

(1,162 |

) |

|

$ |

(1,152) |

|

|

$ |

(130,687) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cumulative noncurrent deferred tax assets at end of period |

|

|

|

$ |

82,044 |

|

|

$ |

– |

|

|

$ |

749 |

|

|

$ |

82,793 |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

2015 |

|

| |

|

| Accumulated other comprehensive (loss) earnings at beginning of period |

|

|

|

$ |

(106,688) |

|

|

$ |

3,278 |

|

|

$ |

(2,749) |

|

|

$ |

(106,159) |

|

|

|

|

|

|

|

|

| Other comprehensive loss before reclassifications, net of tax |

|

|

|

|

(7,116) |

|

|

|

(3,542 |

) |

|

|

– |

|

|

|

(10,658) |

|

| Amounts reclassified from accumulated other comprehensive loss, net of tax |

|

|

|

|

10,424 |

|

|

|

– |

|

|

|

771 |

|

|

|

11,195 |

|

|

|

|

|

|

|

|

| Other comprehensive earnings (loss), net of tax |

|

|

|

|

3,308 |

|

|

|

(3,542 |

) |

|

|

771 |

|

|

|

537 |

|

|

|

|

|

|

|

|

| Accumulated other comprehensive loss at end of period |

|

|

|

$ |

(103,380) |

|

|

$ |

(264 |

) |

|

$ |

(1,978) |

|

|

$ |

(105,622) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cumulative noncurrent deferred tax assets at end of period |

|

|

|

$ |

66,467 |

|

|

$ |

– |

|

|

$ |

1,290 |

|

|

$ |

67,757 |

|

|

|

|

|

|

|

|

Reclassifications out of accumulated other comprehensive loss are as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| years ended December 31

(add 000) |

|

2017 |

|

|

2016 |

|

|

2015 |

|

|

Affected line items in the

consolidated statements of earnings |

| Pension and postretirement benefit plans |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Special plan termination benefit |

|

$ |

– |

|

|

$ |

764 |

|

|

$ |

2,085 |

|

|

|

| Settlement charge |

|

|

21 |

|

|

|

115 |

|

|

|

– |

|

|

|

| Amortization of: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Prior service credit |

|

|

(1,430 |

) |

|

|

(1,609 |

) |

|

|

(1,880 |

) |

|

|

| Actuarial loss |

|

|

13,774 |

|

|

|

11,575 |

|

|

|

16,850 |

|

|

|

|

|

|

12,365 |

|

|

|

10,845 |

|

|

|

17,055 |

|

|

Other nonoperating (income) and expenses, net |

| Tax effect |

|

|

(4,732 |

) |

|

|

(4,160 |

) |

|

|

(6,631 |

) |

|

Income tax (benefit) expense |

| Total |

|

$ |

7,633 |

|

|

$ |

6,685 |

|

|

$ |

10,424 |

|

|

|

|

|

|

|

|

| Unamortized value of terminated forward starting interest rate swap |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Additional interest expense |

|

$ |

1,443 |

|

|

$ |

1,367 |

|

|

$ |

1,280 |

|

|

Interest expense |

| Tax effect |

|

|

(571 |

) |

|

|

(541 |

) |

|

|

(509 |

) |

|

Income tax (benefit) expense |

| Total |

|

$ |

872 |

|

|

$ |

826 |

|

|

$ |

771 |

|

|

|

Martin

Marietta | Page 19

NOTES TO FINANCIAL STATEMENTS (continued)