Attached files

| file | filename |

|---|---|

| EX-32.1 - EX-32.1 - Snap Inc | snap-ex321_6.htm |

| EX-31.2 - EX-31.2 - Snap Inc | snap-ex312_7.htm |

| EX-31.1 - EX-31.1 - Snap Inc | snap-ex311_8.htm |

| EX-23.1 - EX-23.1 - Snap Inc | snap-ex231_721.htm |

| EX-21.1 - EX-21.1 - Snap Inc | snap-ex211_556.htm |

| EX-10.29 - EX-10.29 - Snap Inc | snap-ex1029_720.htm |

| EX-10.28 - EX-10.28 - Snap Inc | snap-ex1028_719.htm |

| EX-10.26 - EX-10.26 - Snap Inc | snap-ex1026_798.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO |

Commission File Number 001-38017

SNAP INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

45-5452795 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer |

|

63 Market Street, Venice, California 90291 |

|

|

(Address of principal executive offices, including zip code) |

|

(310) 399-3339

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Name of each exchange on which registered |

|

|

Class A Common Stock, par value $0.00001 per share |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☐ NO ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☒ NO ☐

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). YES ☒ NO ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☐ |

|

|

|

|

|

|

|

|

|

Non-accelerated filer |

|

☒ (Do not check if a smaller reporting company) |

|

Smaller reporting company |

|

☐ |

|

|

|

|

|

|

|

|

|

|

|

|

|

Emerging growth company |

|

☒ |

If an emerging growth company, indicate by checkmark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant, based on the closing price of the shares of Class A common stock on The New York Stock Exchange on June 30, 2017, was $11,487,095,467.

As of January 31, 2018, the registrant had 887,610,964 shares of Class A common stock, 122,808,708 shares of Class B common stock, and 216,615,870 shares of Class C common stock outstanding.

|

|

|

|

|

Page |

|

|

1 |

|||

|

|

2 |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 1. |

|

|

4 |

|

|

Item 1A. |

|

|

9 |

|

|

Item 1B. |

|

|

36 |

|

|

Item 2. |

|

|

36 |

|

|

Item 3. |

|

|

37 |

|

|

Item 4. |

|

|

37 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 5. |

|

|

37 |

|

|

Item 6. |

|

|

39 |

|

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

42 |

|

Item 7A. |

|

|

62 |

|

|

Item 8. |

|

|

63 |

|

|

Item 9. |

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

|

97 |

|

Item 9A. |

|

|

97 |

|

|

Item 9B. |

|

|

97 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 10. |

|

|

98 |

|

|

Item 11. |

|

|

104 |

|

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

116 |

|

Item 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

|

118 |

|

Item 14. |

|

|

119 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 15. |

|

|

120 |

|

|

|

|

|

123 |

|

i

NOTE REGARDING FORWARD-LOOKING STATEMENTS

The following discussion contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, about us and our industry that involve substantial risks and uncertainties. All statements other than statements of historical facts contained in this Annual Report on Form 10-K, including statements regarding our future results of operations or financial condition, business strategy and plans, and objectives of management for future operations, are forward-looking statements. In some cases, you can identify forward-looking statements because they contain words such as “anticipate,” “believe,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “target,” “will,” or “would” or the negative of these words or other similar terms or expressions.

We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy, and financial needs. These forward-looking statements are subject to known and unknown risks, uncertainties, and assumptions, including risks described in “Risk Factors” and elsewhere in this Annual Report on Form 10-K regarding, among other things:

|

|

• |

our financial performance, including our revenues, cost of revenues, operating expenses, and our ability to attain and sustain profitability; |

|

|

• |

our ability to attract and retain users; |

|

|

• |

our ability to attract and retain advertisers; |

|

|

• |

our ability to compete effectively with existing competitors and new market entrants; |

|

|

• |

our ability to successfully expand in our existing markets and penetrate new markets; |

|

|

• |

our ability to effectively manage our growth and future expenses; |

|

|

• |

our ability to maintain, protect, and enhance our intellectual property; |

|

|

• |

our ability to comply with modified or new laws and regulations applying to our business; |

|

|

• |

our ability to attract and retain qualified employees and key personnel; and |

|

|

• |

future acquisitions of or investments in complementary companies, products, services, or technologies. |

We caution you that the foregoing list may not contain all of the forward-looking statements made in this Annual Report on Form 10-K.

You should not rely on forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this Annual Report on Form 10-K primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition, results of operations, and prospects. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties, and other factors described in “Risk Factors” and elsewhere in this Annual Report on Form 10-K. Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Annual Report on Form 10-K. The results, events, and circumstances reflected in the forward-looking statements may not be achieved or occur, and actual results, events, or circumstances could differ materially from those described in the forward-looking statements.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based on information available to us as of the date of this Annual Report on Form 10-K. And while we believe that information provides a reasonable basis for these statements, that information may be limited or incomplete. Our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all relevant information. These statements are inherently uncertain, and investors are cautioned not to unduly rely on these statements.

1

The forward-looking statements made in this Annual Report on Form 10-K relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this Annual Report on Form 10-K to reflect events or circumstances after the date of this Annual Report on Form 10-K or to reflect new information or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions, or expectations disclosed in our forward-looking statements, and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures, or investments.

Investors and others should note that we may announce material business and financial information to our investors using our investor relations website (investor.snap.com), SEC filings, webcasts, press releases, and conference calls. We use these mediums, including Snapchat and our website, to communicate with our members and the public about our company, our products, and other issues. It is possible that the information that we make available may be deemed to be material information. We therefore encourage investors and others interested in our company to review the information that we make available on our website.

NOTE REGARDING USER METRICS AND OTHER DATA

We define a Daily Active User, or DAU, as a registered Snapchat user who opens the Snapchat application at least once during a defined 24-hour period. We measure average Daily Active Users for a particular quarter by calculating the average Daily Active Users for that quarter. We also break out Daily Active Users by geography because certain markets have a greater revenue opportunity and lower bandwidth costs. We define average revenue per user, or ARPU, as quarterly revenue divided by the average Daily Active Users. For purposes of calculating ARPU, revenue by user geography is apportioned to each region based on our determination of the geographic location in which advertising impressions are delivered, as this approximates revenue based on user activity. This allocation differs from our revenue by geography disclosure in the notes to our consolidated financial statements, where revenue is based on the billing address of the advertising customer. For information concerning these metrics as measured by us, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Unless otherwise stated, statistical information regarding our users and their activities is determined by calculating the daily average of the selected activity for the most recently completed quarter included in this report.

While these metrics are determined based on what we believe to be reasonable estimates of our user base for the applicable period of measurement, there are inherent challenges in measuring how our products are used across large populations globally. For example, there may be individuals who have multiple Snapchat accounts, even though we forbid that in our Terms of Service and implement measures to detect and suppress that behavior. We have not determined the number of such multiple accounts. Our user metrics are also affected by technology on certain mobile devices that automatically runs in the background of our Snapchat application when another phone function is used, and this activity can cause our system to miscount the user metrics associated with such account. Changes in our products, mobile operating systems, or metric tracking system, or the introduction of new products, may impact our ability to accurately determine Daily Active Users or other metrics and we may not determine such inaccuracies promptly. We believe that we don’t capture all data regarding all our Daily Active Users. For example, technical issues may not record data from every user’s application. While we believe this underreporting is generally immaterial, we are unable to precisely determine the level of underreporting and for some periods the underreporting may be material. We continually seek to address these technical issues and improve our accuracy, but given the complexity of the systems involved and the rapidly changing nature of mobile devices and systems, we expect underreporting to continue. We do not adjust our reported metrics to reflect this underreporting.

Some of our demographic data may be incomplete or inaccurate. For example, because users self-report their dates of birth, our age-demographic data may differ from our users’ actual ages. And because users who signed up for Snapchat before June 2013 were not asked to supply their date of birth, we exclude those users and estimate their ages based on a sample of the self-reported ages we do have. If our Daily Active Users provide us with incorrect or incomplete information regarding their age or other attributes, then our estimates may prove inaccurate and fail to meet investor expectations.

2

In the past we have relied on third-party analytics providers to calculate our metrics, but today we rely primarily on our analytics platform that we developed and operate. For example, before June 2015, we used a third party that counted a Daily Active User when the application was opened or a notification was received via the application on any device. We now use an analytics platform that we developed and operate and we count a Daily Active User only when a user opens the application and only once per user per day. We believe this methodology more accurately measures our user engagement. We have multiple pipelines of user data that we use to determine whether a user has opened the application during a particular day, and thus is a Daily Active User. This provides redundancy in the event one pipeline of data were to become unavailable for technical reasons, and also gives us redundant data to help measure how users interact with our application.

Additionally, to align our pre-June 2015 Daily Active Users with this new methodology, we reduced our pre-June 2015 Daily Active Users by 4.8%, the amount by which we estimated the data generated by the third party was overstated. As a result, our metrics may not be comparable to prior periods.

If we fail to maintain an effective analytics platform, our metrics calculations may be inaccurate. We regularly review, have adjusted in the past, and are likely in the future to adjust our processes for calculating our internal metrics to improve their accuracy. As a result of such adjustments, our Daily Active Users or other metrics may not be comparable to those in prior periods. Our measures of Daily Active Users may differ from estimates published by third parties or from similarly titled metrics of our competitors due to differences in methodology or data used.

3

Overview

Snap Inc. is a camera company. We believe that reinventing the camera represents our greatest opportunity to improve the way that people live and communicate. Our products empower people to express themselves, live in the moment, learn about the world, and have fun together.

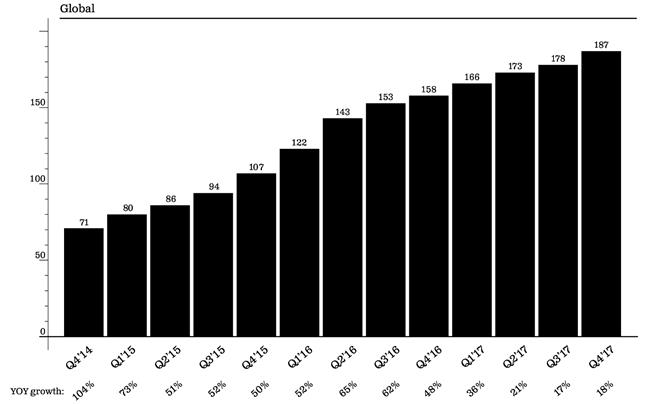

Our flagship product, Snapchat, is a camera application that helps people communicate visually with friends and family through short videos and images called Snaps. Snaps are deleted by default, so there is a lot less pressure to look pretty or perfect when creating and sending images on Snapchat. By reducing the friction typically associated with creating and sharing content, Snapchat has already become one of the most-used cameras in the world. On average, 187 million people use Snapchat daily and create over 3.5 billion Snaps every day. According to InfoTrends, this is more than the total number of photographs taken on average across all phones, tablets, and digital cameras combined (excluding Snapchat) each day in 2017.

In the way that the flashing cursor became the starting point for most products on desktop computers, we believe that the camera screen will be the starting point for most products on smartphones. This is because images created by smartphone cameras contain more context and richer information than other forms of input like text entered on a keyboard. Given the magnitude of this opportunity, we invest heavily and take big risks in an attempt to create innovative and differentiated camera products that are better able to reflect and improve our life experiences.

Our Products

Camera: Snapchat opens directly into the Camera, making it easy to create a Snap and send it to friends. We offer a wide variety of creative tools, created by both us and our community, to make it easy for people to personalize and add context to their Snaps. Over one third of our Daily Active Users play with our augmented reality Lenses every day on average, and anyone can create their own Lens using our Lens Studio. Additionally, we also offer contextually relevant content and creative tools based on things like time, location, and objects.

Friends Page: The first version of our application was a chat service that made it easy to send Snaps back and forth with friends—hence the name “Snapchat.” Interacting with friends on Snapchat now includes creating and watching Stories, chatting with Groups, making voice and video calls, and communicating through a wide range of contextual stickers and Bitmojis. The content and ordering of the Friends page reflects the user’s relationships with their friends and family. This close friend network drives high frequency engagement and results in our community opening our application an average of 25 times per day.

Discover: With so many Snaps created every day around the world, Discover helps surface the most interesting Stories from publishers, creators, and the community, based on a user’s subscriptions and interests. With so much content to explore, our users spend an average of more than 30 minutes every day in our application.

Snap Map: Pinching on the camera screen brings you to a live map of your location, showing nearby friends, popular stories, and a heatmap of recent Snaps posted to Our Story. It’s a great way to see what your friends are doing and explore what is going on around the world.

Memories: Users can choose to save the Snaps they create in a searchable personal collection called Memories. Memories also lets users create Snaps and Stories from their saved Snaps as well as their camera roll.

Spectacles: One of the best ways to create Memories is by using Spectacles, our sunglasses that make Snaps. Spectacles connect seamlessly with Snapchat and capture video from a human perspective.

4

We generate revenue primarily through advertising.

Advertising Products: Our ad products are built on the same foundation that makes our consumer products successful. This means that we can take the things we learn while creating our consumer products and apply them to building innovative and engaging advertising products familiar to our community. Sponsored Lenses take advantage of the reach and scale of our augmented reality platform to create visually engaging 3D experiences. Sponsored Geofilters help users create and send contextual Snaps with their friends, like showing that they are at a particular store or restaurant. Snap Ads and Promoted Stories let advertisers tell their stories the same way our users do, using full screen videos with sound. Attachments allow advertisers to attach additional experiences and actions directly within these ad units, including watching a long-form video, visiting a website, or installing an app.

Campaign Management and Delivery: We are always working to improve the way ads are bought and delivered. We are investing heavily in our programmatic and self-service tools, which provide for automated, sophisticated, and scalable ad buying and campaign management. This helps advertisers increase their return on investment by taking advantage of more refined targeting capabilities, the ability to test and learn with different creatives or campaign attributes in real time, and the pricing dynamics of our auction. Additionally, our delivery framework continues to optimize relevance of ads across the entire platform by determining the best ad to show to any given user based on their real-time and historical attributes and activity. This decreases the number of wasted impressions while improving the effectiveness of the ads that are shown to our community.

Measuring Advertising Effectiveness: We offer a broad range of third-party and first-party solutions to provide analytics on campaign attributes like reach, frequency, demographics, and viewability; changes in perceptions like brand favorability or purchase intent; and lifts in actual behavior like purchases, foot traffic, app installs, and online purchases. We are constantly expanding our capabilities in this area to provide more transparency to advertisers. For example, through our acquisition of Placed, Inc., a location-based measurement services company, we offer omni-channel measurement of store visitation, so that advertisers can measure the performance of their entire budget across all platforms and campaigns as it relates to the more than 90% of retail transactions that still happen offline in the physical world.

Our Strategy

Our strategy is to invest in product innovation and take risks to improve our camera platform. We do this in an effort to drive user engagement, which we can then monetize through advertising. We use the revenue we generate to fund future product innovation to grow our business.

We believe that the best way to compete in a world of widely distributed mobile applications is innovating to create the most engaging products. New mobile software is available to everyone immediately, and usually for free. While not all of our investments will pay off in the long run, we are willing to take risks in an attempt to create the best and most differentiated products on the market.

Due to the nature of our products and business, our ability to succeed in any given country is largely dependent on its mobile infrastructure and its advertising market. These factors influence our product performance, hosting costs, and monetization opportunity in each market.

Visual communication and augmented reality requires intensive processing and generates high bandwidth consumption by our users. As a result, our existing users tend to come from developed countries with high-end mobile devices and high-speed cellular internet. These markets also tend to have cheaper bandwidth costs, meaning that it is less expensive to serve our community in these countries. As we continue to grow in more markets around the world, we are investing heavily in making our service and technology more performant on lower end devices and working with carriers and other infrastructure partners to provide our service at a lower cost to our community.

Substantially all of our revenue comes from advertising, so our ability to generate revenue in a particular country depends on the size of its advertising market. Global advertising spend—especially mobile advertising spend—is extremely concentrated among top markets, and we see a high correlation between markets with significant and developed advertising markets and those that have a deep penetration of high-end mobile devices and high-speed cellular internet access. As such, we benefit greatly from the fact that many of our users are in markets where we have the highest capital efficiency and monetization potential, allowing us to generate revenue and cash flow that we can then invest into future product innovation.

5

Our approach to privacy is simple: Be upfront, offer choices, and never forget that our community comes first.

We built Snapchat as an antidote to the context-less communication that has plagued “social media.” Not so long ago, a conversation among friends would be just that: a private communication in which you knew exactly who you were talking to, what you were talking about, and whether what you were saying was being memorialized for eternity. Somewhere along the way, social media—by prioritizing virality and permanence—sapped conversations of this valuable context and choice. When we began to communicate online, we lost some of what made communication great: spontaneity, emotion, honesty—the full range of human expression that makes us human in the first place.

We don’t think digital communication has to be this way. That’s why choice matters. We build products and services that emphasize the context of a conversation—who, when, what, and where something is being said. If you don’t have the autonomy to shape the context of a conversation, the conversation will simply be shaped by the permanent feeds that homogenize online conversations.

When you read our Privacy Policy, we hope that you’ll notice how much we care about the integrity of personal communication. For starters, we’ve written our Privacy Policy in plain language because we think it’s important that everyone understand exactly how we handle their information. Otherwise, it’s hard to make informed choices about how you communicate. We’ve also created a robust Privacy Center where we show that context and choice are more than talking points. There, we point out the many ways that users can control who sees their Snaps and Stories, we explain how long content will remain on our servers, and much more. You’ll also find there our Transparency Report. We’re proud that we published our first Transparency Report just a few years into the company’s existence, long before most companies take that important step.

We also understand that privacy policies—no matter how ambitious—are only as good as the people and practices behind those policies. When someone trusts us to transmit or store their information, we know we have a responsibility to protect that information and we work hard to keep it secure. New features go through an intense privacy-review process—we debate pros and cons, and we work hard to build products we’re proud of and that we’ll want to use. We use Snapchat constantly, both at work and in our personal lives, and we handle user information with the same care that we want for our family, our friends, and ourselves.

Competition

We compete with other companies in every aspect of our business, particularly with companies that focus on mobile engagement and advertising. Many of these companies, such as Apple, Facebook (including Instagram and WhatsApp), Google (including YouTube), and Twitter, have significantly greater financial and human resources and, in some cases, larger user bases. Given the breadth of our product offerings, we also compete with companies that develop products or otherwise operate in the mobile, camera, communication, media, and advertising industries. Our competitors span from internet technology companies and digital platforms to traditional companies in print, radio, and television sectors to underlying technologies like default smartphone cameras and messaging. Additionally, our competition for engagement varies by region. For instance, we face competition from companies like Kakao, LINE, Naver (including Snow), and Tencent in Asia.

We compete to attract and retain our users’ attention, both in terms of reach and engagement. Since our products and those of our competitors are typically free, we compete based on our brand and the quality and nature of our product offerings rather than on price. As such, we invest heavily in constantly improving and expanding our product lines.

We also compete with other companies to attract and retain partners and advertisers, which depends primarily on our reach and ability to deliver a strong return on investment.

Finally, we compete to attract and retain highly talented individuals, including software engineers, designers, and product managers. Our headquarters in Venice, California and our other principal offices in the Los Angeles area offer certain advantages, such as lower local recruiting competition from other companies and providing an enticing location to live, as well as certain disadvantages such as the increased need to recruit remotely and requiring employees to relocate to the Los Angeles area. In addition to providing competitive compensation packages, we compete for talent by fostering a culture of working hard to create great products and experiences and allowing our employees to have a direct meaningful contribution to new and exciting projects. We had 3,069 employees as of December 31, 2017.

6

Our research and development efforts focus on product development, advertising technology, and large-scale infrastructure.

Product Development: We work relentlessly and invest heavily to create and improve products for our community and our partners. We develop a wide range of products related to visual communication and storytelling that are powered by a variety of new technologies.

Advertising Technology: We constantly develop and expand our advertising products and technology. In an effort to provide a strong and scalable return on investment to our advertisers, our advertising technology roadmap centers around improving our delivery framework, measurement capabilities, and our self-service buying and creative tools.

Large-scale Infrastructure: We spend considerable resources and investment on the underlying architecture that powers our products, such as optimizing the delivery of billions of videos to hundreds of millions of people around the world every day. We currently partner with providers like Google and Amazon to support the infrastructure for our growing needs. These partnerships have allowed us to scale quickly without upfront infrastructure costs, letting us focus our efforts on product innovation.

Our research and development expenses were $1.5 billion, $183.7 million, and $82.2 million in 2017, 2016, and 2015, respectively. For information about our research and development expenses, see “Management's Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations—Research and Development Expenses” of this Annual Report on Form 10-K.

Seasonality in Our Business

We have historically seen a high degree of seasonality in our business and financial results. Overall brand advertising spend tends to be strongest in the fourth quarter of the calendar year, and we have observed a similar pattern in our historical revenue. We have also experienced seasonality in our user engagement, generally seeing lower engagement during summer months. The rapid growth in our business and user engagement has generally masked these trends to date, and we expect the impact of seasonality to be more pronounced in the future.

Key Customers

No individual customer represented more than 10% of our revenues in 2017, 2016, or 2015.

Intellectual Property

Our success depends in part on our ability to protect our intellectual property and proprietary technologies. To protect our proprietary rights, we rely on a combination of intellectual property rights in the United States and other jurisdictions, including patents, trademarks, copyrights, trade secret laws, license agreements, internal procedures, and contractual provisions. We also enter into confidentiality and invention assignment agreements with our employees and contractors and sign confidentiality agreements with third parties. Our internal controls restrict access to proprietary technology.

As of December 31, 2017, we had 375 issued patents and approximately 514 filed patent applications in the United States and foreign countries relating to our camera platform and other technologies. Our issued patents will expire between 2018 and 2036. We may not be able to obtain protection for our intellectual property, and our existing and future patents, trademarks, and other intellectual property rights may not provide us with competitive advantages or distinguish our products and services from those of our competitors. Our patent applications may not result in the issuance of patents, and any resulting issued patents may have claims narrower than those in our patent applications. Additionally, our current and future patents, trademarks, and other intellectual property rights may be contested, circumvented, or found unenforceable or invalid, and we may not be able to prevent third parties from infringing them. Our internal controls and contractual provisions may not always be effective at preventing unauthorized parties from obtaining our intellectual property and proprietary technologies.

7

We license content, trademarks, technology, and other intellectual property from our partners, and rely on our license agreements with those partners to use the intellectual property. We also enter into licensing agreements with third parties to receive rights to patents and other know-how. Third parties may assert claims related to intellectual property rights against our partners or us.

Other companies and “non-practicing entities” that own patents, copyrights, trademarks, trade secrets, and other intellectual property rights related to the mobile, camera, communication, media, internet, and other technology-related industries frequently enter into litigation based on allegations of infringement, misappropriation, and other violations of intellectual property or other rights. Third parties, including our competitors and non-practicing entities, may make claims from time to time that we have infringed their patents, trademarks, copyrights, trade secrets, or other intellectual property rights. We are party to many agreements under which we are obligated to indemnify our customers, suppliers, and channel partners against such claims. As our business grows and competition increases, we will likely face more claims related to intellectual property and litigation matters. In addition, to the extent that we gain greater visibility and market exposure as a public company, we face a higher risk of being the subject of intellectual property infringement claims from third parties.

Government Regulation

We are subject to many U.S. federal and state and foreign laws and regulations, including those related to privacy, rights of publicity, data protection, content regulation, intellectual property, health and safety, competition, protection of minors, consumer protection, and taxation. These laws and regulations are constantly evolving and may be interpreted, applied, created, or amended in a manner that could harm our business.

In December 2014, the Federal Trade Commission resolved an investigation into some of our early practices by handing down a final order. That order requires, among other things, that we establish a robust privacy program to govern how we treat user data. During the 20-year lifespan of the order, we must complete bi-annual independent privacy audits. In June 2014, we entered into a 10-year assurance of discontinuance with the Attorney General of Maryland implementing similar practices, including measures to prevent minors from creating accounts and providing annual compliance reports. Violating existing or future regulatory orders or consent decrees could subject us to substantial monetary fines and other penalties that could negatively affect our financial condition and results of operations.

Furthermore, foreign data protection, privacy, consumer protection, content regulation, and other laws and regulations are often more restrictive than those in the United States. It is possible that certain governments may seek to block or limit our products or otherwise impose other restrictions that may affect the accessibility or usability of any or all our products for an extended period of time or indefinitely. For example, we have very limited access to the China market, as we have not yet established an operating presence in China to support Snapchat. Access to Google, which currently powers our infrastructure, is restricted in China. Additionally, not all our products are available in all locations, including Spectacles, and may not be due to such laws and regulations. We have a public policy team that monitors legal and regulatory developments in the United States, as well as many foreign countries, and communicates with policymakers and regulators in the United States and internationally.

Corporate Information

We were formed as Future Freshman, LLC, a California limited liability company, in 2010. We changed our name to Toyopa Group, LLC in 2011, incorporated as Snapchat, Inc., a Delaware corporation, in 2012, and changed our name to Snap Inc. in 2016. We completed our initial public offering in March 2017 and our Class A common stock is listed on the NYSE under the symbol “SNAP.”

Our principal executive offices are located at 63 Market Street, Venice, California 90291, and our telephone number is (310) 399-3339. Snap Inc., “Snapchat,” and our other registered and common-law trade names, trademarks, and service marks appearing in this Annual Report on Form 10-K are property of Snap Inc. or our subsidiaries.

Information about Segment and Geographic Revenue

Information about segment and geographic revenue is set forth in Notes 1 and 10 of our Notes to Consolidated Financial Statements included in “Financial Statements and Supplementary Data” of this Annual Report on Form 10-K.

8

Our website address is www.snap.com. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to these reports filed pursuant to Sections 13(a) and 15(d) of the Exchange Act are filed with the U.S. Securities and Exchange Commission, or the SEC. Such reports and other information filed by us with the SEC are available free of charge on our website at investor.snap.com when such reports are available on the SEC’s website. We use our website as a means of disclosing material non-public information and for complying with our disclosure obligations under Regulation FD.

Any person may read and copy any materials filed by us with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Room 1580, Washington, DC 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers, like us, that file electronically with the SEC. The address of that website is www.sec.gov.

Information contained in, or accessible through, of the websites referred to in this Annual Report on Form 10-K are not incorporated into this filing. Further, our references to website addresses are only as inactive textual references.

You should carefully consider the risks and uncertainties described below, together with all the other information in this Annual Report on Form 10-K, including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes. If any of the following risks actually occurs, our business, reputation, financial condition, results of operations, revenue, and future prospects could be seriously harmed. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect our business. Unless otherwise indicated, references to our business being seriously harmed in these risk factors will include harm to our business, reputation, financial condition, results of operations, revenue, and future prospects. In that event, the market price of our Class A common stock could decline, and you could lose part or all of your investment.

Risks Related to Our Business and Industry

Our ecosystem of users, advertisers, and partners depends on the engagement of our user base. We anticipate that the growth rate of our user base will decline over time. If we fail to retain current users or add new users, or if our users engage less with Snapchat, our business would be seriously harmed.

We had 187 million and 158 million Daily Active Users on average in the quarters ended December 31, 2017 and December 31, 2016, respectively, and we view Daily Active Users as a critical measure of our user engagement. Adding, maintaining, and engaging Daily Active Users have been and will continue to be necessary. We anticipate that our Daily Active Users growth rate will decline over time if the size of our active user base increases or we achieve higher market penetration rates. For example, if and when we achieve maximum market penetration rates among younger users in developed markets who use smartphones with iOS operating systems, future growth in Daily Active Users will need to come from older users, developing markets, or users with Android operating systems, which may not be possible or may be more difficult or time consuming for us to achieve. If our Daily Active Users growth rate slows, our financial performance will increasingly depend on our ability to elevate user engagement or increase our monetization of users. If current and potential users do not perceive our products to be fun, engaging, and useful, we may not be able to attract new users, retain existing users, or maintain or increase the frequency and duration of their engagement. In addition, because our products typically require high bandwidth data capabilities, the majority of our users live in countries with high-end mobile device penetration and high bandwidth capacity cellular networks with large coverage areas. We therefore do not expect to experience rapid user growth or engagement in countries with low smartphone penetration even if such countries have well-established and high bandwidth capacity cellular networks. We may also not experience rapid user growth or engagement in countries where, even though smartphone penetration is high, due to the lack of sufficient cellular based data networks, consumers rely heavily on Wi-Fi and may not access our products regularly.

9

Snapchat is free and easy to join, the barrier to entry for new entrants is low, and the switching costs to another platform are also low. Moreover, the majority of our users are 18-34 years old. This demographic may be less brand loyal and more likely to follow trends than other demographics. These factors may lead users to switch to another product, which would negatively affect our user retention, growth, and engagement. Snapchat also may not be able to penetrate other demographics in a meaningful manner. Falling user retention, growth, or engagement could make Snapchat less attractive to advertisers and partners, which may seriously harm our business. In addition, our Daily Active Users may not continue to grow. We measure our Daily Active Users by calculating the daily average of users across the entire quarter. This calculation may mask any individual months within the quarter that are significantly higher or lower than the average. There are many factors that could negatively affect user retention, growth, and engagement, including if:

|

|

• |

users increasingly engage with competing products instead of ours; |

|

|

• |

our competitors have and may continue to mimic our products and therefore harm our user engagement and growth; |

|

|

• |

we fail to introduce new and exciting products and services or those we introduce are poorly received; |

|

|

• |

our products fail to operate effectively on the iOS and Android mobile operating systems; |

|

|

• |

we are unable to continue to develop products that work with a variety of mobile operating systems, networks, and smartphones; |

|

|

• |

we do not provide a compelling user experience because of the decisions we make regarding the type and frequency of advertisements that we display; |

|

|

• |

we are unable to combat spam or other hostile or inappropriate usage on our products; |

|

|

• |

there are changes in user sentiment about the quality or usefulness of our existing products in the short term, long term, or both; |

|

|

• |

there are concerns about the privacy implications, safety, or security of our products; |

|

|

• |

our partners who provide content to Snapchat do not create content that is engaging, useful, or relevant to users; |

|

|

• |

our partners who provide content to Snapchat decide not to renew agreements or devote the resources to create engaging content or do not provide content exclusively to us; |

|

|

• |

advertisers display ads that are untrue, offensive, or otherwise fail to follow our guidelines; |

|

|

• |

there are changes in our products that are mandated by legislation, regulatory authorities, or litigation, including settlements or consent decrees that adversely affect the user experience; |

|

|

• |

there are changes to our Terms of Service that are implemented in connection with the General Data Protection Regulation, or GDPR, in Europe, which may decrease engagement or acceptance by our users; |

|

|

• |

technical or other problems frustrate the user experience, particularly if those problems prevent us from delivering our products in a fast and reliable manner; |

|

|

• |

we fail to provide adequate service to users, advertisers, or partners; |

|

|

• |

we, our partners, or other companies in our industry are the subject of adverse media reports or other negative publicity, some of which may be inaccurate or include confidential information that we are unable to correct or retract; |

|

|

• |

we do not maintain our brand image or our reputation is damaged; or |

|

|

• |

our current or future products reduce user activity on Snapchat by making it easier for our users to interact directly with partners. |

Any decrease to user retention, growth, or engagement could render our products less attractive to users, advertisers, or partners, and would seriously harm our business.

10

Snapchat depends on effectively operating with mobile operating systems, hardware, networks, regulations, and standards that we do not control. Changes in our products or to those operating systems, hardware, networks, regulations, or standards may seriously harm our user retention, growth, and engagement.

Because Snapchat is used primarily on mobile devices, the application must remain interoperable with popular mobile operating systems, Android and iOS, and related hardware, including but not limited to mobile-device cameras. The owners of such operating systems, Google and Apple, respectively, each provide consumers with products that compete with ours. Additionally, mobile devices, and mobile-device cameras, are manufactured by a wide array of companies. Those companies have no obligation to test the interoperability of new mobile devices with Snapchat, and may produce new products that are incompatible with or not optimal for Snapchat. We have no control over these operating systems or hardware, and any changes to these systems or hardware that degrade our products’ functionality, or give preferential treatment to competitive products, could seriously harm Snapchat usage on mobile devices. Our competitors that control the operating systems and related hardware our application runs on could make interoperability of our products with those mobile operating systems more difficult or display their competitive offerings more prominently than ours. We plan to continue to introduce new products regularly and have experienced that it takes time to optimize such products to function with these operating systems and hardware, impacting the popularity of such products, and we expect this trend to continue.

The majority of our user engagement is on smartphones with iOS operating systems. As a result, although our products work with Android mobile devices, we historically prioritized development of our products to operate with iOS operating systems rather than smartphones with Android operating systems. To continue growth in user engagement, we have and will continue to prioritize improving our products’ operability on smartphones with Android operating systems. If we are unable to improve operability of our products on smartphones with Android operating systems, and those smartphones become more popular and fewer people use smartphones with iOS operating systems, our business could be seriously harmed.

Moreover, our products require high-bandwidth data capabilities. If the costs of data usage increase or access to cellular networks is limited, our user retention, growth, and engagement may be seriously harmed. Additionally, to deliver high-quality video and other content over mobile cellular networks, our products must work well with a range of mobile technologies, systems, networks, regulations, and standards that we do not control. In particular, any future changes to the iOS or Android operating systems may impact the accessibility, speed, functionality, and other performance aspects of our products, which issues are likely to occur in the future from time to time. In addition, the adoption of any laws or regulations that adversely affect the growth, popularity, or use of the internet, including laws governing internet neutrality, could decrease the demand for our products and increase our cost of doing business. For example, in December 2017, the Federal Communications Commission, or FCC, voted to repeal the “open internet rules,” which prohibit mobile providers in the United States from impeding access to most content, or otherwise unfairly discriminating against content providers like us and also prohibit mobile providers from entering into arrangements with specific content providers for faster or better access over their data networks. While the FCC’s repeal of these net neutrality regulations has not yet taken effect, the future impact of such repeal and any challenges to the repeal remains uncertain and our business could be seriously harmed. The European Union similarly requires equal access to internet content. Additionally, as part of its Digital Single Market initiative, the European Union may impose network security, disability access, or 911-like obligations on “over-the-top” services such as those provided by us, which could increase our costs. If the FCC’s repeal of the open internet rules are allowed to take effect or the European Union modifies these open internet rules, mobile and internet providers may be able to limit our users’ ability to access Snapchat or make Snapchat a less attractive alternative to our competitors’ applications. Were that to happen, our business would be seriously harmed.

We may not successfully cultivate relationships with key industry participants or develop products that operate effectively with these technologies, systems, networks, regulations, or standards. If it becomes more difficult for our users to access and use Snapchat on their mobile devices, if our users choose not to access or use Snapchat on their mobile devices, or if our users choose to use mobile products that do not offer access to Snapchat, our user retention, growth, and engagement could be seriously harmed.

We rely on Google Cloud for the vast majority of our computing, storage, bandwidth, and other services. Any disruption of or interference with our use of the Google Cloud operation would negatively affect our operations and seriously harm our business.

Google provides a distributed computing infrastructure platform for business operations, or what is commonly referred to as a “cloud” computing service, and we currently run the vast majority of our computing on Google Cloud.

11

Any transition of the cloud services currently provided by Google Cloud to another cloud provider would be difficult to implement and will cause us to incur significant time and expense. We have committed to spend $2.0 billion with Google Cloud over five years (beginning January 2017) and have built our software and computer systems to use computing, storage capabilities, bandwidth, and other services provided by Google, some of which do not have an alternative in the market. Given this, any significant disruption of or interference with our use of Google Cloud would negatively impact our operations and our business would be seriously harmed. If our users or partners are not able to access Snapchat through Google Cloud or encounter difficulties in doing so, we may lose users, partners, or advertising revenue. The level of service provided by Google Cloud or similar providers may also impact the usage of and our users’, advertisers’, and partners’ satisfaction with Snapchat and could seriously harm our business and reputation. If Google Cloud or similar providers experience interruptions in service regularly or for a prolonged basis, or other similar issues, our business would be seriously harmed. Hosting costs also have and will continue to increase as our user base and user engagement grows and may seriously harm our business if we are unable to grow our revenues faster than the cost of utilizing the services of Google or similar providers.

In addition, Google may take actions beyond our control that could seriously harm our business, including:

|

|

• |

discontinuing or limiting our access to its Google Cloud platform; |

|

|

• |

increasing pricing terms; |

|

|

• |

terminating or seeking to terminate our contractual relationship altogether; |

|

|

• |

establishing more favorable relationships or pricing terms with one or more of our competitors; and |

|

|

• |

modifying or interpreting its terms of service or other policies in a manner that impacts our ability to run our business and operations. |

Google has broad discretion to change and interpret its terms of service and other policies with respect to us, and those actions may be unfavorable to us. Google may also alter how we are able to process data on the Google Cloud platform. If Google makes changes or interpretations that are unfavorable to us, our business would be seriously harmed.

We generate substantially all of our revenue from advertising. The failure to attract new advertisers, the loss of advertisers, or a reduction in how much they spend could seriously harm our business.

Substantially all of our revenue is generated from third parties advertising on Snapchat, a trend that we expect to continue. For the years ended December 31, 2017 and 2016, advertising revenue accounted for 97% and 96% of total revenue, respectively. Although we have and continue to try to establish longer-term advertising commitments with advertisers, most advertisers do not have long-term advertising commitments with us, and our efforts to establish long-term commitments may not succeed.

While no individual customer accounts for more than 10% of our revenue, many of our advertisers only recently started working with us and spend a relatively small portion of their overall advertising budget with us. In addition, advertisers may view some of our products as experimental and unproven. Advertisers will not continue to do business with us if we do not deliver advertisements in an effective manner, or if they do not believe that their investment in advertising with us will generate a competitive return relative to other alternatives. Moreover, we rely heavily on our ability to collect and disclose data and metrics to and for our advertisers to attract new advertisers and retain existing advertisers. Any restriction, whether by law, regulation, policy, or other reason, on our ability to collect and disclose data which our advertisers find useful would impede our ability to attract and retain advertisers. Our advertising revenue could be seriously harmed by many other factors, including:

|

|

• |

a decrease in the number of Daily Active Users on Snapchat; |

|

|

• |

a decrease in the amount of time spent on Snapchat or decreases in usage of our Creative Tools, Chat Service, or Storytelling Platform; |

|

|

• |

our inability to create new products that sustain or increase the value of our advertisements; |

|

|

• |

changes in our user demographics that make us less attractive to advertisers; |

|

|

• |

lack of ad creative availability by our advertising partners; |

|

|

• |

our partners who provide content to us may not renew agreements or devote the resources to create engaging content or do not provide content exclusively to us; |

12

|

|

• |

decreases in the perceived quantity, quality, usefulness, or relevance of the content provided by our users or partners; |

|

|

• |

changes in our analytics and measurement solutions that demonstrate the value of our advertisements and other commercial content; |

|

|

• |

competitive developments or advertiser perception of the value of our products that change the rates we can charge for advertising or the volume of advertising on Snapchat; |

|

|

• |

product changes or advertising inventory management decisions we may make that change the type, size, or frequency of advertisements displayed on Snapchat or the method used by advertisers to purchase advertisements; |

|

|

• |

adverse legal developments relating to advertising, including changes mandated by legislation, regulation, or litigation; |

|

|

• |

adverse media reports or other negative publicity involving us, our founders, our partners, or other companies in our industry; |

|

|

• |

advertiser or user perception that content published by us, our users, or our partners is objectionable; |

|

|

• |

the degree to which users skip advertisements and therefore diminish the value of those advertisements to advertisers; |

|

|

• |

changes in the way advertising is priced or its effectiveness is measured; |

|

|

• |

our inability to measure the effectiveness of our advertising or target the appropriate audience for advertisements; |

|

|

• |

our inability to collect and disclose data that new and existing advertisers may find useful; |

|

|

• |

difficulty and frustration from advertisers who may need to reformat or change their advertisements to comply with our guidelines; and |

|

|

• |

the macroeconomic climate and the status of the advertising industry in general. |

These and other factors could reduce demand for our advertising products, which may lower the prices we receive, or cause advertisers to stop advertising with us altogether. Either of these would seriously harm our business.

Our two co-founders have control over all stockholder decisions because they control a substantial majority of our voting stock.

As a result of the Class C common stock that they hold, Evan Spiegel, our co-founder and Chief Executive Officer, and Robert Murphy, our co-founder and Chief Technology Officer, are able to exercise voting rights with respect to an aggregate of 216,615,870 shares of Class C common stock, which represents approximately 94.6% of the voting power of our outstanding capital stock as of December 31, 2017. In addition, Mr. Spiegel was granted an RSU for 37,447,817 shares of Class C common stock on the closing of our initial public offering, or IPO. This RSU award vested immediately on the closing of our IPO in March 2017 and such shares are delivered to our CEO in quarterly installments over three years beginning in November 2017, following which Mr. Spiegel alone may be able to exercise voting control over our outstanding capital stock. The Class A common stock has no voting rights, the Class B common stock is entitled to one vote per share, and the Class C common stock is entitled to ten votes per share. As a result, Mr. Spiegel and Mr. Murphy, and potentially either one of them alone, have the ability to control the outcome of all matters submitted to our stockholders for approval, including the election, removal, and replacement of directors and any merger, consolidation, or sale of all or substantially all of our assets. If Mr. Spiegel’s or Mr. Murphy’s employment with us is terminated, they will continue to have the ability to exercise the same significant voting power and potentially control the outcome of all matters submitted to our stockholders for approval. Either of our co-founders’ shares of Class C common stock will automatically convert into Class B common stock, on a one-to-one basis, nine months following his death or on the date on which the number of outstanding shares of Class C common stock held by such holder represents less than 30% of the Class C common stock held by such holder on the closing of our IPO, or 32,383,178 shares of Class C common stock. Should either of our co-founders’ Class C common stock be converted to Class B common stock, the remaining co-founder will be able to exercise voting control over our outstanding capital stock.

13

In addition, in October 2016, we issued a dividend of one share of non-voting Class A common stock to all our equity holders, which will prolong our co-founders’ voting control. As a result of such dividend, our co-founders will be able to liquidate their holdings of non-voting Class A common stock without diminishing their voting control. In the future, our board of directors may, from time to time, decide to issue special or regular stock dividends in the form of Class A common stock, and if we do so, our co-founders’ control could be further prolonged. This concentrated control could delay, defer, or prevent a change of control, merger, consolidation, or sale of all or substantially all of our assets that our other stockholders support. Conversely, this concentrated control could allow our co-founders to consummate such a transaction that our other stockholders do not support. In addition, our co-founders may make long-term strategic investment decisions and take risks that may not be successful and may seriously harm our business.

As our CEO, Mr. Spiegel has control over our day-to-day management and the implementation of major strategic investments of our company, subject to authorization and oversight by our board of directors. As board members and officers, Mr. Spiegel and Mr. Murphy owe a fiduciary duty to our stockholders and must act in good faith in a manner they reasonably believe to be in the best interests of our stockholders. As stockholders, even controlling stockholders, Mr. Spiegel and Mr. Murphy are entitled to vote their shares, and shares over which they have voting control, in their own interests, which may not always be in the interests of our stockholders generally. We have not elected to take advantage of the “controlled company” exemption to the corporate governance rules for New York Stock Exchange, or NYSE, listed companies. Moreover, Mr. Spiegel and Mr. Murphy have entered into a proxy agreement under which each has granted a voting proxy with respect to all shares of our Class B common stock and Class C common stock that each may beneficially own from time to time or have voting control over. The proxy would become effective on either founder’s death or disability. Mr. Spiegel and Mr. Murphy have each initially designated the other as their respective proxies. Accordingly, on the death or incapacity of either Mr. Spiegel or Mr. Murphy, the other could individually control nearly all of the voting power of our outstanding capital stock.

If we do not develop successful new products or improve existing ones, our business will suffer. We also invest in new lines of business that could fail to attract or retain users or generate revenue.

Our ability to engage, retain, and increase our user base and to increase our revenue will depend heavily on our ability to successfully create new products, both independently and together with third parties. We may introduce significant changes to our existing products or develop and introduce new and unproven products and services, including technologies with which we have little or no prior development or operating experience. These new products and updates may fail to increase the engagement of our users, advertisers, or partners, and may even result in short-term or long-term decreases in such engagement by disrupting existing user, advertiser, or partner behavior, or by introducing performance and quality issues. For example, in 2017, we transitioned most of our Snap Ads sales to a programmatic model, which decreased average advertising prices. Additionally, we introduced a major redesign of the Snapchat application in December 2017 that rolled out more broadly in February 2018, which has received negative attention in the press and in app store reviews. The short- and long-term impact of any major change, like our recent redesign, is particularly difficult to predict. If new or enhanced products fail to engage our users, advertisers, or partners, we may fail to attract or retain users or to generate sufficient revenue, operating margin, or other value to justify our investments, any of which may seriously harm our business in the short term, long term, or both. Additionally, we frequently launch new products and the products that we launch may have technical issues that diminish the performance of our application. These performance issues or issues that we encounter in the future could impact our user engagement.

Because our products created new ways of communicating, they have often required users to learn new behaviors to use our products, or to use our products repeatedly to receive the most benefit. These new behaviors, such as swiping and tapping in the Snapchat application, are not always intuitive to users. This can create a lag in adoption of new products and new user additions related to new products. To date, this has not hindered our user growth or engagement, but that may be the result of a large portion of our user base being in a younger demographic and more willing to invest the time to learn to use our products most effectively. To the extent that future users, including those in older demographics, are less willing to invest the time to learn to use our products, and if we are unable to make our products easier to learn to use, our user growth or engagement could be affected, and our business could be harmed. We may develop new products that increase user engagement and costs without increasing revenue. For example, we introduced Memories in 2016, our cloud storage service for Snaps, which increases our storage costs.

In addition, we have invested and expect to continue to invest in new lines of business, new products, and other initiatives to generate revenue. The launch of Spectacles in late 2016, which has not and may not generate significant revenue for us, is a good example. We do not have significant experience with hardware products, and we have incurred Spectacles inventory-related charges and may incur increased costs in connection with the development, sale, and marketing of hardware

14

products. There is no guarantee that investing in new lines of business, new products, and other initiatives will succeed. If we do not successfully develop new approaches to monetization or meet the expectations of our users or partners, we may not be able to maintain or grow our revenue as anticipated or recover any associated development costs, and our business could be seriously harmed.

Our business is highly competitive. We face significant competition that we anticipate will continue to intensify. If we are not able to maintain or improve our market share, our business could suffer.

We face significant competition in almost every aspect of our business both domestically and internationally. This includes larger, more established companies such as Apple, Facebook (including Instagram and WhatsApp), Google (including YouTube), Twitter, Kakao, LINE, Naver (including Snow), and Tencent, which provide their users with a variety of products, services, content, and online advertising offerings, and smaller companies that offer products and services that may compete with specific Snapchat features. For example, Instagram, a subsidiary of Facebook, introduced a “stories” feature that largely mimics our Stories feature and may be directly competitive. We may also lose users to small companies that offer products and services that compete with specific Snapchat features because of the low cost for our users to switch to a different product or service. Moreover, in emerging international markets, where mobile devices often lack large storage capabilities, we may compete with other applications for the limited space available on a user’s mobile device. We also face competition from traditional and online media businesses for advertising budgets. We compete broadly with the social media offerings of Apple, Facebook, Google, and Twitter, and with other, largely regional, social media platforms that have strong positions in particular countries. As we introduce new products, as our existing products evolve, or as other companies introduce new products and services, we may become subject to additional competition. For example, in late 2016, we launched Spectacles, our first hardware product. While we view Spectacles as an extension of Snapchat, adding hardware products and services to our product portfolio subjects us to additional competition and new competitors.

Many of our current and potential competitors have significantly greater resources and broader global recognition and occupy stronger competitive positions in certain markets than we do. These factors may allow our competitors to respond to new or emerging technologies and changes in market requirements better than we can. Our competitors may also develop products, features, or services that are similar to ours or that achieve greater market acceptance. These products, features, and services may undertake more far-reaching and successful product development efforts or marketing campaigns, or may adopt more aggressive pricing policies. In addition, advertisers may use information that our users share through Snapchat to develop or work with competitors to develop products or features that compete with us. Certain competitors, including Apple, Facebook, and Google, could use strong or dominant positions in one or more markets to gain competitive advantages against us in areas where we operate, including by:

|

|

• |

integrating competing social media platforms or features into products they control such as search engines, web browsers, or mobile device operating systems; |

|

|

• |

making acquisitions for similar or complementary products or services; or |

|

|

• |

impeding Snapchat’s accessibility and usability by modifying existing hardware and software on which the Snapchat application operates. |

As a result, our competitors may acquire and engage users at the expense of our user growth or engagement, which may seriously harm our business.

We believe that our ability to compete effectively depends on many factors, many of which are beyond our control, including:

|

|

• |

the usefulness, novelty, performance, and reliability of our products compared to our competitors; |

|

|

• |

the number and demographics of our Daily Active Users; |

|

|

• |

the timing and market acceptance of our products, including developments and enhancements of our competitors’ products; |

|

|

• |

our ability to monetize our products; |

|

|

• |

the effectiveness of our advertising and sales teams; |

|

|

• |

the effectiveness of our advertising products; |

|

|

• |

our ability to establish and maintain advertisers’ and partners’ interest in using Snapchat; |

15

|

|

• |

the frequency, relative prominence, and type of advertisements displayed on our application or by our competitors; |

|

|

• |

the effectiveness of our customer service and support efforts; |

|

|

• |

the effectiveness of our marketing activities; |

|

|

• |

changes as a result of legislation, regulatory authorities, or litigation, including settlements and consent decrees, some of which may have a disproportionate effect on us; |

|

|

• |

acquisitions or consolidation within our industry; |

|

|

• |

our ability to attract, retain, and motivate talented employees, particularly engineers and sales personnel; |

|

|

• |

our ability to successfully acquire and integrate companies and assets; |

|

|

• |

our ability to cost-effectively manage and scale our rapidly growing operations; and |

|

|

• |

our reputation and brand strength relative to our competitors. |

If we cannot effectively compete, our user engagement may decrease, which could make us less attractive to users, advertisers, and partners and seriously harm our business.

We have incurred operating losses in the past, expect to incur operating losses in the future, and may never achieve or maintain profitability.

We began commercial operations in 2011 and for all of our history we have experienced net losses and negative cash flows from operations. As of December 31, 2017, we had an accumulated deficit of $4.7 billion and for the year ended December 31, 2017, we experienced a net loss of $3.4 billion. We expect our operating expenses to increase in the future as we expand our operations. If our revenue does not grow at a greater rate than our expenses, we will not be able to achieve and maintain profitability. We may incur significant losses in the future for many reasons, including without limitation the other risks and uncertainties described in this report. Additionally, we may encounter unforeseen expenses, operating delays, or other unknown factors that may result in losses in future periods. If our expenses exceed our revenue, our business may be seriously harmed and we may never achieve or maintain profitability.

The loss of one or more of our key personnel, or our failure to attract and retain other highly qualified personnel in the future, could seriously harm our business.