Attached files

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________

Form 10-K

(Mark One) | |

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2017 | |

OR | |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO | |

Commission File Number 1-31447

______________________

CenterPoint Energy, Inc.

(Exact name of registrant as specified in its charter)

Texas | 74-0694415 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

1111 Louisiana Houston, Texas 77002 (Address and zip code of principal executive offices) | (713) 207-1111 (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock, $0.01 par value | New York Stock Exchange Chicago Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o | Emerging growth company o |

(Do not check if a smaller reporting company) | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the voting stock held by non-affiliates of CenterPoint Energy, Inc. (CenterPoint Energy) was $11,722,467,012 as of June 30, 2017, using the definition of beneficial ownership contained in Rule 13d-3 promulgated pursuant to the Securities Exchange Act of 1934 and excluding shares held by directors and executive officers. As of February 9, 2018, CenterPoint Energy had 431,048,125 shares of Common Stock outstanding. Excluded from the number of shares of Common Stock outstanding are 166 shares held by CenterPoint Energy as treasury stock.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement relating to the 2018 Annual Meeting of Shareholders of CenterPoint Energy, which will be filed with the Securities and Exchange Commission within 120 days of December 31, 2017, are incorporated by reference in Item 10, Item 11, Item 12, Item 13 and Item 14 of Part III of this Form 10-K.

TABLE OF CONTENTS

PART I | ||||

Page | ||||

Item 1. | Business | |||

Item 1A. | Risk Factors | |||

Item 1B. | Unresolved Staff Comments | |||

Item 2. | Properties | |||

Item 3. | Legal Proceedings | |||

Item 4. | Mine Safety Disclosures | |||

PART II | ||||

Item 5. | Market for Registrants’ Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |||

Item 6. | Selected Financial Data | |||

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |||

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |||

Item 8. | Financial Statements and Supplementary Data | |||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |||

Item 9A. | Controls and Procedures | |||

Item 9B. | Other Information | |||

PART III | ||||

Item 10. | Directors, Executive Officers and Corporate Governance | |||

Item 11. | Executive Compensation | |||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |||

Item 13. | Certain Relationships and Related Transactions, and Director Independence | |||

Item 14. | Principal Accounting Fees and Services | |||

PART IV | ||||

Item 15. | Exhibits and Financial Statement Schedules | |||

Item 16. | Form 10-K Summary | |||

i

GLOSSARY | ||

ADFIT | Accumulated deferred federal income taxes | |

ADMS | Advanced Distribution Management System | |

AEM | Atmos Energy Marketing, LLC, previously a wholly-owned subsidiary of Atmos Energy Holdings, Inc., a wholly-owned subsidiary of Atmos Energy Corporation | |

AFUDC | Allowance for funds used during construction | |

AMAs | Asset Management Agreements | |

AMS | Advanced Metering System | |

AOL | AOL Inc. | |

APSC | Arkansas Public Service Commission | |

ArcLight | ArcLight Capital Partners, LLC | |

ARO | Asset retirement obligation | |

ASC | Accounting Standards Codification | |

ASU | Accounting Standards Update | |

AT&T | AT&T Inc. | |

AT&T Common | AT&T common stock | |

Bcf | Billion cubic feet | |

Btu | British thermal units | |

BDA | Billing Determinant Adjustment, which is a revenue stabilization mechanism used to adjust revenues impacted by declines in natural gas consumption which occurred after the most recent rate case | |

Bond Companies | Wholly-owned, bankruptcy remote entities formed solely for the purpose of purchasing and owning transition or system restoration property through the issuance of Securitization Bonds | |

Brazos Valley Connection | A portion of the Houston region transmission project between Houston Electric’s Zenith substation and the Gibbons Creek substation owned by the Texas Municipal Power Agency | |

CEA | Commodities Exchange Act of 1936 | |

CEIP | CenterPoint Energy Intrastate Pipelines, LLC | |

CenterPoint Energy | CenterPoint Energy, Inc., and its subsidiaries | |

CERC Corp. | CenterPoint Energy Resources Corp. | |

CERC | CERC Corp., together with its subsidiaries | |

CERCLA | Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended | |

CES | CenterPoint Energy Services, Inc., a wholly-owned subsidiary of CERC Corp. | |

CFTC | Commodity Futures Trading Commission | |

Charter Common | Charter Communications, Inc. common stock | |

Charter merger | Merger of Charter Communications, Inc. and Time Warner Cable Inc. | |

CIP | Conservation Improvement Program | |

COLI | Corporate-owned life insurance | |

Continuum | The retail energy services business of Continuum Retail Energy Services, LLC, including its wholly-owned subsidiary Lakeshore Energy Services, LLC and the natural gas wholesale assets of Continuum Energy Services, LLC | |

DCRF | Distribution Cost Recovery Factor | |

Dodd-Frank Act | Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 | |

DOE | U.S. Department of Energy | |

DOT | U.S. Department of Transportation | |

Dth | Dekatherms | |

EBITDA | Earnings before interest, taxes, depreciation and amortization | |

EDIT | Excess deferred income taxes | |

ii

GLOSSARY (cont.) | ||

EECR | Energy Efficiency Cost Recovery | |

EECRF | Energy Efficiency Cost Recovery Factor | |

EGT | Enable Gas Transmission, LLC | |

EIA | U.S. Energy Information Administration | |

Enable | Enable Midstream Partners, LP | |

EPA | Environmental Protection Agency | |

EPAct of 2005 | Energy Policy Act of 2005 | |

ERCOT | Electric Reliability Council of Texas | |

ERCOT ISO | ERCOT Independent System Operator | |

ERISA | Employee Retirement Income Security Act of 1974 | |

ERO | Electric Reliability Organization | |

FASB | Financial Accounting Standards Board | |

FERC | Federal Energy Regulatory Commission | |

Fitch | Fitch, Inc. | |

FRP | Formula Rate Plan | |

Gas Daily | Platts gas daily indices | |

GenOn | GenOn Energy, Inc. | |

GHG | Greenhouse gases | |

GRIP | Gas Reliability Infrastructure Program | |

GWh | Gigawatt-hours | |

Houston Electric | CenterPoint Energy Houston Electric, LLC and its subsidiaries | |

HVAC | Heating, ventilation and air conditioning | |

IBEW | International Brotherhood of Electrical Workers | |

ICA | Interstate Commerce Act of 1887 | |

IG | Intelligent Grid | |

IRS | Internal Revenue Service | |

kV | Kilovolt | |

LIBOR | London Interbank Offered Rate | |

LNG | Liquefied natural gas | |

LPSC | Louisiana Public Service Commission | |

LTIPs | Long-term incentive plans | |

Meredith | Meredith Corporation | |

MGPs | Manufactured gas plants | |

MLP | Master Limited Partnership | |

MMBtu | One million British thermal units | |

MMcf | Million cubic feet | |

Moody’s | Moody’s Investors Service, Inc. | |

MPSC | Mississippi Public Service Commission | |

MPUC | Minnesota Public Utilities Commission | |

MRT | Enable-Mississippi River Transmission, LLC | |

NAV | Net asset value | |

NECA | National Electrical Contractors Association | |

NERC | North American Electric Reliability Corporation | |

NESHAPS | National Emission Standards for Hazardous Air Pollutants | |

NGA | Natural Gas Act of 1938 | |

NGD | Natural gas distribution business | |

NGLs | Natural gas liquids | |

NGPA | Natural Gas Policy Act of 1978 | |

iii

GLOSSARY (cont.) | ||

NGPSA | Natural Gas Pipeline Safety Act of 1968 | |

NRG | NRG Energy, Inc. | |

NYMEX | New York Mercantile Exchange | |

NYSE | New York Stock Exchange | |

OCC | Oklahoma Corporation Commission | |

OGE | OGE Energy Corp. | |

PBRC | Performance Based Rate Change | |

PHMSA | Pipeline and Hazardous Materials Safety Administration | |

PRPs | Potentially responsible parties | |

PUCT | Public Utility Commission of Texas | |

Railroad Commission | Railroad Commission of Texas | |

RCRA | Resource Conservation and Recovery Act of 1976 | |

Reliant Energy | Reliant Energy, Incorporated | |

REP | Retail electric provider | |

RICE MACT | Reciprocating Internal Combustion Engines Maximum Achievable Control Technology | |

ROE | Return on equity | |

RRA | Rate Regulation Adjustment | |

RRI | Reliant Resources, Inc. | |

RSP | Rate Stabilization Plan | |

SEC | Securities and Exchange Commission | |

SESH | Southeast Supply Header, LLC | |

Securitization Bonds | Transition and system restoration bonds | |

Series A Preferred Units | Enable’s 10% Series A Fixed-to-Floating Non-Cumulative Redeemable Perpetual Preferred Units, representing limited partner interests in Enable | |

S&P | Standard & Poor’s Ratings Services, a division of The McGraw-Hill Companies | |

TBD | To be determined | |

TCEH Corp. | Formerly Texas Competitive Electric Holdings Company LLC, predecessor to Vistra Energy Corp. whose major subsidiaries include Luminant and TXU Energy | |

TCJA | Tax reform legislation informally called the Tax Cuts and Jobs Act of 2017 | |

TCOS | Transmission Cost of Service | |

TDU | Transmission and distribution utility | |

Time | Time Inc. | |

Time Common | Time common stock | |

Transition Agreements | Services Agreement, Employee Transition Agreement, Transitional Seconding Agreement and other agreements entered into in connection with the formation of Enable | |

Texas RE | Texas Reliability Entity | |

TW | Time Warner Inc. | |

TW Common | TW common stock | |

TWC | Time Warner Cable Inc. | |

TWC Common | TWC common stock | |

TW Securities | Charter Common, Time Common and TW Common | |

VaR | Value at Risk | |

iv

GLOSSARY (cont.) | ||

Verizon | Verizon Communications, Inc. | |

VIE | Variable interest entity | |

Vistra Energy Corp. | Texas-based energy company focused on the competitive energy and power generation markets | |

ZENS | 2.0% Zero-Premium Exchangeable Subordinated Notes due 2029 | |

2002 Act | Pipeline Safety Improvement Act of 2002 | |

2006 Act | Pipeline Inspection, Protection, Enforcement and Safety Act of 2006 | |

2011 Act | Pipeline Safety, Regulatory Certainty, and Job Creation Act of 2011 | |

2016 Act | Protecting our Infrastructure of Pipelines and Enhancing Safety Act of 2016 | |

v

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

From time to time we make statements concerning our expectations, beliefs, plans, objectives, goals, strategies, future events or performance and underlying assumptions and other statements that are not historical facts. These statements are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Actual results may differ materially from those expressed or implied by these statements. You can generally identify our forward-looking statements by the words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “forecast,” “goal,” “intend,” “may,” “objective,” “plan,” “potential,” “predict,” “projection,” “should,” “target,” “will” or other similar words.

We have based our forward-looking statements on our management’s beliefs and assumptions based on information reasonably available to our management at the time the statements are made. We caution you that assumptions, beliefs, expectations, intentions and projections about future events may and often do vary materially from actual results. Therefore, we cannot assure you that actual results will not differ materially from those expressed or implied by our forward-looking statements.

Some of the factors that could cause actual results to differ from those expressed or implied by our forward-looking statements are described under “Risk Factors” in Item 1A and “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Certain Factors Affecting Future Earnings” and “ — Liquidity and Capital Resources — Other Matters — Other Factors That Could Affect Cash Requirements” in Item 7 of this report, which discussions are incorporated herein by reference.

You should not place undue reliance on forward-looking statements. Each forward-looking statement speaks only as of the date of the particular statement, and we undertake no obligation to update or revise any forward-looking statements.

vi

PART I

Item 1. | Business |

OUR BUSINESS

Overview

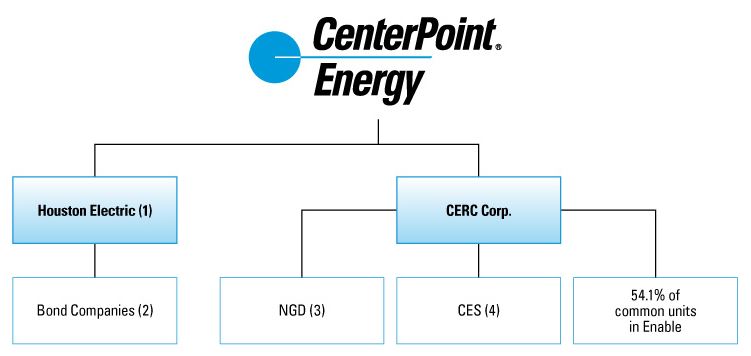

We are a public utility holding company. Our operating subsidiaries own and operate electric transmission and distribution and natural gas distribution facilities, supply natural gas to commercial and industrial customers and electric and natural gas utilities and own interests in Enable as described below. Our simplified corporate structure is shown below:

(1) | Houston Electric engages in the electric transmission and distribution business in the Texas Gulf Coast area that includes the city of Houston. |

(2) | Bond Companies are wholly-owned, bankruptcy remote entities formed solely for the purpose of purchasing and owning transition or system restoration property through the issuance of Securitization Bonds. |

(3) | NGD operates natural gas distribution systems in six states. |

(4) | CES obtains and offers competitive variable and fixed-price physical natural gas supplies and services primarily to commercial and industrial customers and electric and natural gas utilities in 33 states. |

(5) | Represents limited partner interests in Enable, which owns, operates and develops natural gas and crude oil infrastructure assets. For additional information regarding our interest in Enable, see Note 10 to our consolidated financial statements. |

1

Our reportable business segments are Electric Transmission & Distribution, Natural Gas Distribution, Energy Services, Midstream Investments and Other Operations. For a discussion of operating income by segment, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Results of Operations by Business Segment” in Item 7 of Part II of this report. For additional information about the segments, see Note 18 to our consolidated financial statements. From time to time, we consider the acquisition or the disposition of assets or businesses.

Our principal executive offices are located at 1111 Louisiana, Houston, Texas 77002 (telephone number: 713-207-1111).

We make available free of charge on our internet website our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such reports with, or furnish them to, the SEC. Additionally, we make available free of charge on our Internet website:

• | our Code of Ethics for our Chief Executive Officer and Senior Financial Officers; |

• | our Ethics and Compliance Code; |

• | our Corporate Governance Guidelines; and |

• | the charters of the audit, compensation, finance and governance committees of our Board of Directors. |

Any shareholder who so requests may obtain a printed copy of any of these documents from us. Changes in or waivers of our Code of Ethics for our Chief Executive Officer and Senior Financial Officers and waivers of our Ethics and Compliance Code for directors or executive officers will be posted on our Internet website within five business days of such change or waiver and maintained for at least 12 months or timely reported on Item 5.05 of Form 8-K.

Our website address is www.centerpointenergy.com. Investors should also note that we announce material financial information in SEC filings, press releases and public conference calls. Based on guidance from the SEC, we may use the investor relations section of our website to communicate with our investors. It is possible that the financial and other information posted there could be deemed to be material information. Except to the extent explicitly stated herein, documents and information on our website are not incorporated by reference herein.

Electric Transmission & Distribution

Houston Electric is a transmission and distribution electric utility that operates wholly within the state of Texas and is a member of ERCOT. ERCOT serves as the independent system operator and regional reliability coordinator for member electric power systems in most of Texas. The ERCOT market represents approximately 90% of the demand for power in Texas and is one of the nation’s largest power markets. The ERCOT market operates under the reliability standards developed by the NERC, approved by the FERC and monitored and enforced by the Texas RE. The PUCT has primary jurisdiction over the ERCOT market to ensure the adequacy and reliability of electricity supply across the state’s main interconnected power transmission grid. Neither

2

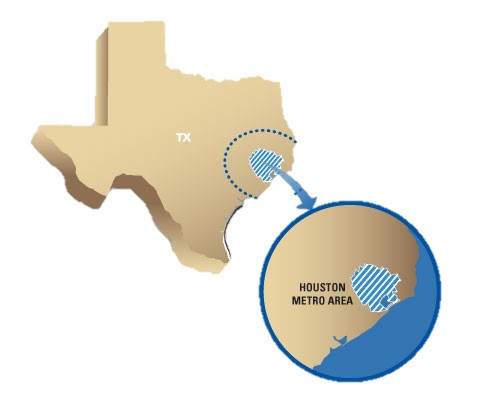

Houston Electric nor any other subsidiary of CenterPoint Energy makes direct retail or wholesale sales of electric energy or owns or operates any electric generating facilities. Houston Electric’s service territory is depicted below:

Electric Transmission

On behalf of REPs, Houston Electric delivers electricity from power plants to substations, from one substation to another and to retail electric customers taking power at or above 69 kV in locations throughout Houston Electric’s certificated service territory. Houston Electric constructs and maintains transmission facilities and provides transmission services under tariffs approved by the PUCT.

The ERCOT ISO is responsible for operating the bulk electric power supply system in the ERCOT market. Houston Electric’s transmission business, along with those of other owners of transmission facilities in Texas, supports the operation of the ERCOT ISO. Houston Electric participates with the ERCOT ISO and other ERCOT utilities to plan, design, obtain regulatory approval for and construct new transmission lines necessary to increase bulk power transfer capability and to remove existing constraints on the ERCOT transmission grid.

Electric Distribution

In ERCOT, end users purchase their electricity directly from certificated REPs. Houston Electric delivers electricity for REPs in its certificated service area by carrying lower-voltage power from the substation to the retail electric customer. Houston Electric’s distribution network receives electricity from the transmission grid through power distribution substations and delivers electricity to end users through distribution feeders. Houston Electric’s operations include construction and maintenance of distribution facilities, metering services, outage response services and call center operations. Houston Electric provides distribution services under tariffs approved by the PUCT. PUCT rules and market protocols govern the commercial operations of distribution companies and other market participants. Rates for these existing services are established pursuant to rate proceedings conducted before municipalities that have original jurisdiction and the PUCT.

Bond Companies

Houston Electric has special purpose subsidiaries consisting of the Bond Companies, which it consolidates. The consolidated special purpose subsidiaries are wholly-owned, bankruptcy remote entities that were formed solely for the purpose of purchasing and owning transition or system restoration property through the issuance of Securitization Bonds, and conducting activities incidental thereto. The Securitization Bonds are repaid through charges imposed on customers in Houston Electric’s service territory. For further discussion of the Securitization Bonds and the outstanding balances as of December 31, 2017 and 2016, see Note 13 to our consolidated financial statements.

Customers

Houston Electric serves nearly all of the Houston/Galveston metropolitan area. At December 31, 2017, Houston Electric’s customers consisted of approximately 68 REPs, which sell electricity to more than 2.4 million metered customers in Houston Electric’s certificated service area, and municipalities, electric cooperatives and other distribution companies located outside Houston Electric’s certificated service area. Each REP is licensed by, and must meet minimum creditworthiness criteria established

3

by, the PUCT. Houston Electric does not have long-term contracts with any of its customers. It operates using a continuous billing cycle, with meter readings being conducted and invoices being distributed to REPs each business day. For information regarding Houston Electric’s major customers, see Note 18 to our consolidated financial statements.

Utility Technology

Houston Electric’s Smart Grid is comprised of the AMS, IG, ADMS and private telecommunications network. Since 2009, Houston Electric has deployed fully operational advanced meters to virtually all of its 2.4 million metered customers, automated 31 substations, installed 872 IG Switching Devices on more than 200 circuits, built a wireless radio frequency mesh telecommunications network across Houston Electric’s 5,000-square mile footprint, and enabled real-time grid monitoring and control, which leverages information from smart meters and field sensors to manage system events through the ADMS. We believe that the Smart Grid is already improving electric distribution service reliability and restoration, enhancing the consumer experience, supporting the growth of renewable energy and helping the environment by reducing carbon emissions.

Competition

There are no other electric transmission and distribution utilities in Houston Electric’s service area. For another provider of transmission and distribution services to provide such services in Houston Electric’s territory, it would be required to obtain a certificate of convenience and necessity from the PUCT and, depending on the location of the facilities, may also be required to obtain franchises from one or more municipalities. We know of no other party intending to enter this business in Houston Electric’s service area at this time. Distributed generation (i.e., power generation located at or near the point of consumption) could result in a reduction of demand for Houston Electric’s distribution services but has not been a significant factor to date.

Seasonality

A significant portion of Houston Electric’s revenues is derived from rates that it collects from each REP based on the amount of electricity it delivers on behalf of that REP. Thus, Houston Electric’s revenues and results of operations are subject to seasonality, weather conditions and other changes in electricity usage, with revenues generally being higher during the warmer months.

Properties

All of Houston Electric’s properties are located in Texas. Its properties consist primarily of high-voltage electric transmission lines and poles, distribution lines, substations, service centers, service wires, telecommunications network and meters. Most of Houston Electric’s transmission and distribution lines have been constructed over lands of others pursuant to easements or along public highways and streets under franchise agreements and as permitted by law.

All real and tangible properties of Houston Electric, subject to certain exclusions, are currently subject to:

• | the lien of a Mortgage and Deed of Trust (the Mortgage) dated November 1, 1944, as supplemented; and |

• | the lien of a General Mortgage (the General Mortgage) dated October 10, 2002, as supplemented, which is junior to the lien of the Mortgage. |

For information related to debt outstanding under the Mortgage and General Mortgage, see Note 13 to our consolidated financial statements.

Electric Lines - Transmission. As of December 31, 2017, Houston Electric owned and operated the following electric transmission lines:

Circuit Miles | ||||||

Operating Voltage | Overhead Lines | Underground Lines | ||||

69 kV | 271 | 2 | ||||

138 kV | 2,198 | 24 | ||||

345 kV | 1,219 | — | ||||

3,688 | 26 | |||||

4

Electric Lines - Distribution. As of December 31, 2017, Houston Electric owned 28,883 pole miles of overhead distribution lines and 24,662 circuit miles of underground distribution lines.

Substations. As of December 31, 2017, Houston Electric owned 235 major substation sites having a total installed rated transformer capacity of 64,924 megavolt amperes.

Service Centers. As of December 31, 2017, Houston Electric operated 14 regional service centers located on a total of 292 acres of land. These service centers consist of office buildings, warehouses and repair facilities that are used in the business of transmitting and distributing electricity.

Franchises

Houston Electric holds non-exclusive franchises from certain incorporated municipalities in its service territory. In exchange for the payment of fees, these franchises give Houston Electric the right to use the streets and public rights-of-way of these municipalities to construct, operate and maintain its transmission and distribution system and to use that system to conduct its electric delivery business and for other purposes that the franchises permit. The terms of the franchises, with various expiration dates, typically range from 20 to 40 years.

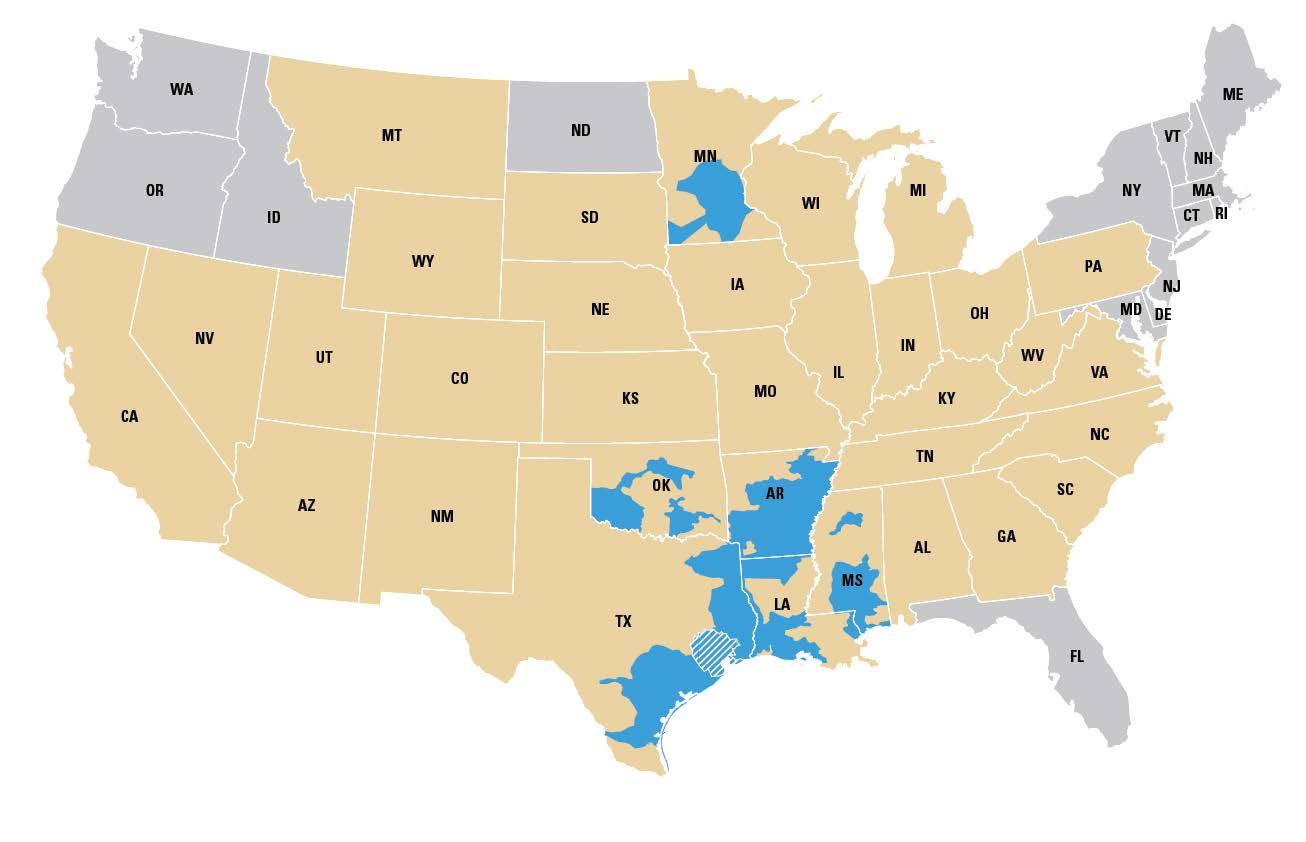

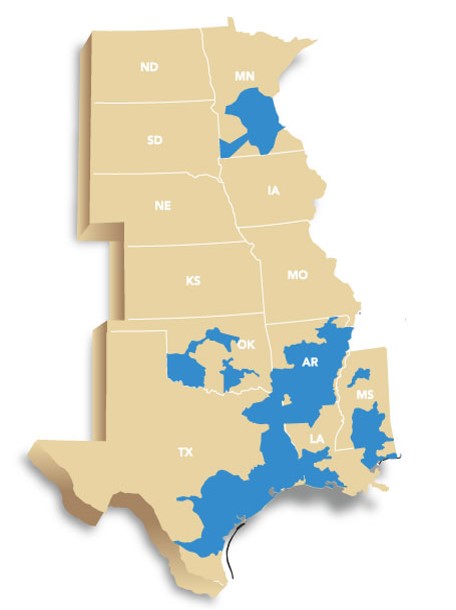

Natural Gas Distribution

CERC Corp.’s NGD engages in regulated intrastate natural gas sales to, and natural gas transportation and storage for, approximately 3.5 million residential, commercial, industrial and transportation customers in Arkansas, Louisiana, Minnesota, Mississippi, Oklahoma and Texas. The largest metropolitan areas served in each state by NGD are Houston, Texas; Minneapolis, Minnesota; Little Rock, Arkansas; Shreveport, Louisiana; Biloxi, Mississippi; and Lawton, Oklahoma. NGD also provides unregulated services in Minnesota consisting of residential appliance repair and maintenance services along with HVAC equipment sales. NGD’s service territory is depicted below:

In 2017, approximately 37% of NGD’s total throughput was to residential customers and approximately 63% was to commercial and industrial and transportation customers. The table below reflects the number of NGD customers by state as of December 31, 2017:

Residential | Commercial/ Industrial | Total Customers | ||||||

Arkansas | 378,429 | 47,965 | 426,394 | |||||

Louisiana | 230,084 | 16,711 | 246,795 | |||||

Minnesota | 788,832 | 70,178 | 859,010 | |||||

Mississippi | 113,752 | 12,567 | 126,319 | |||||

Oklahoma | 89,074 | 10,758 | 99,832 | |||||

Texas | 1,612,969 | 98,472 | 1,711,441 | |||||

Total NGD | 3,213,140 | 256,651 | 3,469,791 | |||||

5

Seasonality

The demand for intrastate natural gas sales to residential customers and natural gas sales and transportation for commercial and industrial customers is seasonal. In 2017, approximately 66% of NGD’s total throughput occurred in the first and fourth quarters. These patterns reflect the higher demand for natural gas for heating purposes during the colder months.

Supply and Transportation. In 2017, NGD purchased virtually all of its natural gas supply pursuant to contracts with remaining terms varying from a few months to four years. Major suppliers in 2017 included the following:

Supplier | Percent of Supply Volumes | |

Tenaska Marketing Ventures | 18.0% | |

Macquarie Energy, LLC | 12.5% | |

BP Energy Company/BP Canada Energy Marketing | 12.1% | |

Kinder Morgan Tejas Pipeline/Kinder Morgan Texas Pipeline | 7.4% | |

CES | 5.4% | |

Mieco, Inc. | 5.0% | |

Spire Marketing, Inc. | 4.9% | |

United Energy Trading, LLC | 4.7% | |

Koch Energy Services, LLC | 4.0% | |

Cargill | 2.8% | |

Numerous other suppliers provided the remaining 23.2% of NGD’s natural gas supply requirements. NGD transports its natural gas supplies through various intrastate and interstate pipelines under contracts with remaining terms, including extensions, varying from one to fifteen years. NGD anticipates that these gas supply and transportation contracts will be renewed or replaced prior to their expiration.

NGD actively engages in commodity price stabilization pursuant to annual gas supply plans presented to and/or filed with each of its state regulatory authorities. These price stabilization activities include use of storage gas and contractually establishing structured prices (e.g., fixed price, costless collars and caps) with our physical gas suppliers. Its gas supply plans generally call for 50–75% of winter supplies to be stabilized in some fashion.

The regulations of the states in which NGD operates allow it to pass through changes in the cost of natural gas, including savings and costs of financial derivatives associated with the index-priced physical supply, to its customers under purchased gas adjustment provisions in its tariffs. Depending upon the jurisdiction, the purchased gas adjustment factors are updated periodically, ranging from monthly to semi-annually. The changes in the cost of gas billed to customers are subject to review by the applicable regulatory bodies.

NGD uses various third-party storage services or owned natural gas storage facilities to meet peak-day requirements and to manage the daily changes in demand due to changes in weather. NGD may also supplement contracted supplies and storage from time to time with stored LNG and propane-air plant production.

NGD owns and operates an underground natural gas storage facility with a capacity of 7.0 Bcf. It has a working capacity of 2.0 Bcf available for use during the heating season and a maximum daily withdrawal rate of 50 MMcf. It also owns eight propane-air plants with a total production rate of 180,000 Dth per day and on-site storage facilities for 12 million gallons of propane (1.0 Bcf natural gas equivalent). It owns a LNG plant facility with a 12 million-gallon LNG storage tank (1.0 Bcf natural gas equivalent) and a production rate of 72,000 Dth per day.

On an ongoing basis, NGD enters into contracts to provide sufficient supplies and pipeline capacity to meet its customer requirements. However, it is possible for limited service disruptions to occur from time to time due to weather conditions, transportation constraints and other events. As a result of these factors, supplies of natural gas may become unavailable from time to time, or prices may increase rapidly in response to temporary supply constraints or other factors.

NGD currently has AMAs associated with its utility distribution service in Arkansas, Louisiana, Mississippi, Oklahoma and Texas. The AMAs have varying terms, the longest of which expires in 2020. Generally, AMAs are contracts between NGD and an asset manager that are intended to transfer the working capital obligation and maximize the utilization of the assets. In these

6

agreements, NGD agrees to release transportation and storage capacity to other parties to manage natural gas storage, supply and delivery arrangements for NGD and to use the released capacity for other purposes when it is not needed for NGD. NGD is compensated by the asset manager through payments made over the life of the agreements based in part on the results of the asset optimization. NGD has an obligation to purchase its winter storage requirements that have been released to the asset manager under these AMAs. NGD has received approval from the state regulatory commissions in Arkansas, Louisiana, Mississippi and Oklahoma to retain a share of the AMA proceeds.

Assets

As of December 31, 2017, NGD owned approximately 75,000 linear miles of natural gas distribution mains, varying in size from one-half inch to 24 inches in diameter. Generally, in each of the cities, towns and rural areas served by NGD, it owns the underground gas mains and service lines, metering and regulating equipment located on customers’ premises and the district regulating equipment necessary for pressure maintenance. With a few exceptions, the measuring stations at which NGD receives gas are owned, operated and maintained by others, and its distribution facilities begin at the outlet of the measuring equipment. These facilities, including odorizing equipment, are usually located on land owned by suppliers.

Competition

NGD competes primarily with alternate energy sources such as electricity and other fuel sources. In some areas, intrastate pipelines, other gas distributors and marketers also compete directly for gas sales to end users. In addition, as a result of federal regulations affecting interstate pipelines, natural gas marketers operating on these pipelines may be able to bypass NGD’s facilities and market and sell and/or transport natural gas directly to commercial and industrial customers.

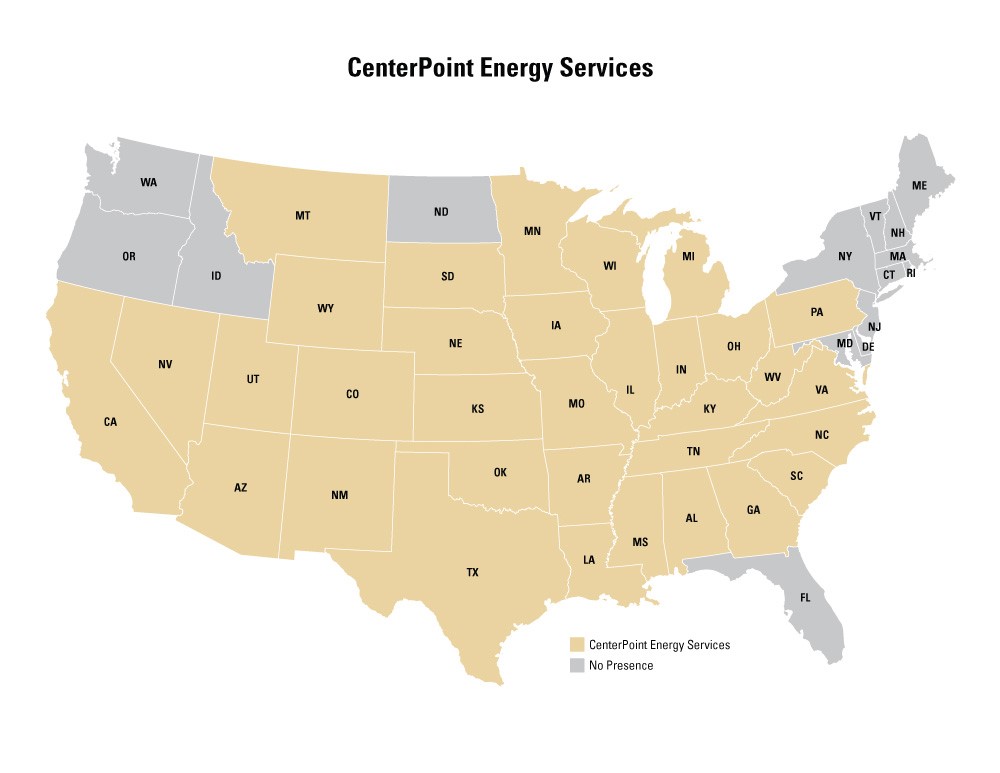

Energy Services

CERC offers competitive variable and fixed-priced physical natural gas supplies primarily to commercial and industrial customers and electric and natural gas utilities through CES and its subsidiary, CEIP. Energy Services’ service territory is depicted below:

In 2017, CES marketed approximately 1,200 Bcf of natural gas, related energy services and transportation to approximately 31,000 customers (including approximately 21 Bcf to affiliates) in 33 states. CES customers vary in size from small commercial customers to large utility companies. Not included in the 2017 customer count are approximately 72,000 natural gas customers that are served under residential and small commercial choice programs invoiced by their host utility. These customers are not included in customer count so as not to distort the significant margin impact from the remaining customer base.

7

In January 2017, CES completed the acquisition of AEM, providing CES with a portfolio of industrial and large commercial customers complementary to CES’s existing customer base and strategically aligned storage and transportation assets. For further information related to this acquisition, see Note 4 to our consolidated financial statements.

CES offers a variety of natural gas management services to gas utilities, large industrial customers, electric generators, smaller commercial and industrial customers, municipalities, educational institutions, government facilities and hospitals. These services include load forecasting, supply acquisition, daily swing volume management, invoice consolidation, storage asset management, firm and interruptible transportation administration and forward price management. CES also offers a portfolio of physical delivery services designed to meet customers’ supply and price risk management needs. These customers are served directly, through interconnects with various interstate and intrastate pipeline companies, and portably, through our mobile energy solutions business.

In addition to offering natural gas management services, CES procures and optimizes transportation and storage assets. CES maintains a portfolio of natural gas supply contracts and firm transportation and storage agreements to meet the natural gas requirements of its customers. CES aggregates supply from various producing regions and offers contracts to buy natural gas with terms ranging from one month to over five years. In addition, CES actively participates in the spot natural gas markets in an effort to balance daily and monthly purchases and sales obligations. Natural gas supply and transportation capabilities are leveraged through contracts for ancillary services including physical storage and other balancing arrangements.

As described above, CES offers its customers a variety of load following services. In providing these services, CES uses its customers’ purchase commitments to forecast and arrange its own supply purchases, storage and transportation services to serve customers’ natural gas requirements. As a result of the variance between this forecast activity and the actual monthly activity, CES will either have too much supply or too little supply relative to its customers’ purchase commitments. These supply imbalances arise each month as customers’ natural gas requirements are scheduled and corresponding natural gas supplies are nominated by CES for delivery to those customers. CES’s processes and risk control environment are designed to measure and value imbalances on a real-time basis to ensure that CES’s exposure to commodity price risk is kept to a minimum. The value assigned to these imbalances is calculated daily and is known as the aggregate VaR.

Our risk control policy, which is overseen by our Risk Oversight Committee, defines authorized and prohibited trading instruments and trading limits. CES is a physical marketer of natural gas and uses a variety of tools, including pipeline and storage capacity, financial instruments and physical commodity purchase contracts, to support its sales. CES optimizes its use of these various tools to minimize its supply costs and does not engage in speculative commodity trading. The VaR limit within which CES currently operates, a $4 million maximum set by the Board of Directors, is consistent with CES’s operational objective of matching its aggregate sales obligations (including the swing associated with load following services) with its supply portfolio in a manner that minimizes its total cost of supply. In 2017, CES’s VaR averaged $0.7 million with a high of $1.8 million.

Assets

As of December 31, 2017, CEIP owned and operated over 200 miles of intrastate pipeline in Louisiana and Texas. In addition, CES leases transportation capacity on various interstate and intrastate pipelines and storage to service its shippers and end users.

Competition

CES competes with regional and national wholesale and retail gas marketers, including the marketing divisions of natural gas producers and utilities. In addition, CES competes with intrastate pipelines for customers and services in its market areas.

Midstream Investments

Our Midstream Investments business segment consists of CERC Corp.’s equity method investment in Enable. Enable is a publicly traded MLP, jointly controlled by CERC Corp. and OGE.

Enable. Enable was formed to own, operate and develop midstream energy infrastructure assets strategically located to serve its customers. Enable’s assets and operations are organized into two reportable segments: (i) gathering and processing and (ii) transportation and storage. Enable’s gathering and processing segment primarily provides natural gas and crude oil gathering and natural gas processing services to its producer customers. Enable’s transportation and storage segment provides interstate and intrastate natural gas pipeline transportation and storage services primarily to its producer, power plant, local distribution company and industrial end-user customers.

Enable’s Gathering and Processing segment. Enable owns and operates substantial natural gas and crude oil gathering and natural gas processing assets in five states. Enable’s gathering and processing operations consist primarily of natural gas gathering

8

and processing assets serving the Anadarko, Arkoma and Ark-La-Tex Basins and crude oil gathering assets serving the Williston Basin. Enable provides a variety of services to the active producers in its operating areas, including gathering, compressing, treating, and processing natural gas, fractionating NGLs, and gathering crude oil and produced water. Enable serves shale and other unconventional plays in the basins in which it operates.

Enable’s gathering and processing systems compete with gatherers and processors of all types and sizes, including those affiliated with various producers, other major pipeline companies and various independent midstream entities. In the process of selling NGLs, Enable competes against other natural gas processors extracting and selling NGLs. Enable’s primary competitors are other midstream companies who are active in the regions where it operates. Competition to gather crude oil and produced water is primarily a function of rates, terms of service, system reliability and construction cycle time. The rates and terms of service of Enable’s crude oil gathering, but not its produced water gathering, are FERC regulated. Enable’s Williston Basin gathering systems compete with other gatherers, including those affiliated with producers and other midstream companies.

Enable’s Transportation and Storage segment. Enable owns and operates interstate and intrastate transportation and storage systems across nine states. Enable’s transportation and storage systems consist primarily of its interstate systems, its intrastate system and its investment in SESH. Enable’s transportation and storage assets transport natural gas from areas of production and interconnected pipelines to power plants, local distribution companies and industrial end users as well as interconnected pipelines for delivery to additional markets. Enable’s transportation and storage assets also provide facilities where natural gas can be stored by customers.

Enable’s interstate pipelines compete with a variety of other interstate and intrastate pipelines across its operating areas. Enable’s intrastate pipeline competes with a variety of interstate and intrastate pipelines in providing transportation and storage services, including several pipelines with which it interconnects. Enable’s management views the principal elements of competition among pipelines as rates and terms, flexibility and reliability of service.

For information related to CERC Corp.’s equity method investment in Enable, see Notes 2(c), 10 and 19 to our consolidated financial statements.

Other Operations

Our Other Operations business segment includes office buildings and other real estate used in our business operations and other corporate operations that support all of our business operations.

REGULATION

We are subject to regulation by various federal, state and local governmental agencies, including the regulations described below.

Federal Energy Regulatory Commission

The FERC has jurisdiction under the NGA and the NGPA, as amended, to regulate the transportation of natural gas in interstate commerce and natural gas sales for resale in interstate commerce that are not first sales. The FERC regulates, among other things, the construction of pipeline and related facilities used in the transportation and storage of natural gas in interstate commerce, including the extension, expansion or abandonment of these facilities. The FERC has authority to prohibit market manipulation in connection with FERC-regulated transactions and to impose significant civil and criminal penalties for statutory violations and violations of the FERC’s rules or orders. Our Energy Services business segment markets natural gas in interstate commerce pursuant to blanket authority granted by the FERC.

Houston Electric is not a “public utility” under the Federal Power Act and, therefore, is not generally regulated by the FERC, although certain of its transactions are subject to limited FERC jurisdiction. The FERC has certain responsibilities with respect to ensuring the reliability of electric transmission service, including transmission facilities owned by Houston Electric and other utilities within ERCOT. The FERC has designated the NERC as the ERO to promulgate standards, under FERC oversight, for all owners, operators and users of the bulk power system (Electric Entities). The ERO and the FERC have authority to (a) impose fines and other sanctions on Electric Entities that fail to comply with approved standards and (b) audit compliance with approved standards. The FERC has approved the delegation by the NERC of authority for reliability in ERCOT to the Texas RE. Houston Electric does not anticipate that the reliability standards proposed by the NERC and approved by the FERC will have a material adverse impact on its operations. To the extent that Houston Electric is required to make additional expenditures to comply with these standards, it is anticipated that Houston Electric will seek to recover those costs through the transmission charges that are imposed on all distribution service providers within ERCOT for electric transmission provided.

9

As a public utility holding company, under the Public Utility Holding Company Act of 2005, we and our consolidated subsidiaries are subject to reporting and accounting requirements and are required to maintain certain books and records and make them available for review by the FERC and state regulatory authorities in certain circumstances.

State and Local Regulation – Electric Transmission & Distribution

Houston Electric conducts its operations pursuant to a certificate of convenience and necessity issued by the PUCT that covers its present service area and facilities. The PUCT and certain municipalities have the authority to set the rates and terms of service provided by Houston Electric under cost-of-service rate regulation. Houston Electric holds non-exclusive franchises from certain incorporated municipalities in its service territory. In exchange for payment of fees, these franchises give Houston Electric the right to use the streets and public rights-of-way of these municipalities to construct, operate and maintain its transmission and distribution system and to use that system to conduct its electric delivery business and for other purposes that the franchises permit. The terms of the franchises, with various expiration dates, typically range from 20 to 40 years.

Houston Electric’s distribution rates charged to REPs for residential customers are primarily based on amounts of energy delivered, whereas distribution rates for a majority of commercial and industrial customers are primarily based on peak demand. All REPs in Houston Electric’s service area pay the same rates and other charges for transmission and distribution services. This regulated delivery charge includes the transmission and distribution rate (which includes municipal franchise fees), a distribution recovery mechanism for recovery of incremental distribution-invested capital above that which is already reflected in the base distribution rate, a nuclear decommissioning charge associated with decommissioning the South Texas nuclear generating facility, an EECR charge, and charges associated with securitization of regulatory assets, stranded costs and restoration costs relating to Hurricane Ike. Transmission rates charged to distribution companies are based on amounts of energy transmitted under “postage stamp” rates that do not vary with the distance the energy is being transmitted. All distribution companies in ERCOT pay Houston Electric the same rates and other charges for transmission services.

For a discussion of certain of Houston Electric’s ongoing regulatory proceedings, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources — Regulatory Matters” in Item 7 of Part II of this report, which discussion is incorporated herein by reference.

State and Local Regulation – Natural Gas Distribution

In almost all communities in which NGD provides natural gas distribution services, it operates under franchises, certificates or licenses obtained from state and local authorities. The original terms of the franchises, with various expiration dates, typically range from 10 to 30 years, although franchises in Arkansas are perpetual. NGD expects to be able to renew expiring franchises. In most cases, franchises to provide natural gas utility services are not exclusive.

Substantially all of NGD is subject to cost-of-service rate regulation by the relevant state public utility commissions and, in Texas, by the Railroad Commission and those municipalities served by NGD that have retained original jurisdiction. In certain of its jurisdictions, NGD has in effect annual rate adjustment mechanisms that provide for changes in rates dependent upon certain changes in invested capital, earned returns on equity or actual margins realized.

For a discussion of certain of NGD’s ongoing regulatory proceedings, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources — Regulatory Matters” in Item 7 of Part II of this report, which discussion is incorporated herein by reference.

Department of Transportation

In December 2006, Congress enacted the 2006 Act, which reauthorized the programs adopted under the 2002 Act. These programs included several requirements related to ensuring pipeline safety, and a requirement to assess the integrity of pipeline transmission facilities in areas of high population concentration.

Pursuant to the 2006 Act, PHMSA, an agency of the DOT, issued regulations, effective February 12, 2010, requiring operators of gas distribution pipelines to develop and implement integrity management programs similar to those required for gas transmission pipelines, but tailored to reflect the differences in distribution pipelines. Operators of natural gas distribution systems were required to write and implement their integrity management programs by August 2, 2011. Our natural gas distribution systems met this deadline.

10

Pursuant to the 2002 Act and the 2006 Act, PHMSA has adopted a number of rules concerning, among other things, distinguishing between gathering lines and transmission facilities, requiring certain design and construction features in new and replaced lines to reduce corrosion and requiring pipeline operators to amend existing written operations and maintenance procedures and operator qualification programs. PHMSA also updated its reporting requirements for natural gas pipelines effective January 1, 2011.

In December 2011, Congress passed the 2011 Act. This act increased the maximum civil penalties for pipeline safety administrative enforcement actions; required the DOT to study and report on the expansion of integrity management requirements and the sufficiency of existing gathering line regulations to ensure safety; required pipeline operators to verify their records on maximum allowable operating pressure; and imposed new emergency response and incident notification requirements. In 2016, the 2016 Act reauthorized PHMSA’s pipeline safety programs through 2019 and provided limited new authority, including the ability to issue emergency orders, to set inspection requirements for certain underwater pipelines and to promulgate minimum safety standards for natural gas storage facilities, as well as to provide increased transparency into the status of as-yet-incomplete PHMSA actions required by the 2011 Act.

We anticipate that compliance with PHMSA’s regulations, performance of the remediation activities by CERC’s natural gas distribution companies and intrastate pipelines and verification of records on maximum allowable operating pressure will continue to require increases in both capital expenditures and operating costs. The level of expenditures will depend upon several factors, including age, location and operating pressures of the facilities. In particular, the cost of compliance with the DOT’s integrity management rules will depend on integrity testing and the repairs found to be necessary by such testing. Changes to the amount of pipe subject to integrity management, whether by expansion of the definition of the type of areas subject to integrity management procedures or of the applicability of such procedures outside of those defined areas, may also affect the costs we incur. Implementation of the 2011 and 2016 Acts by PHMSA may result in other regulations or the reinterpretation of existing regulations that could impact our compliance costs. In addition, we may be subject to the DOT’s enforcement actions and penalties if we fail to comply with pipeline regulations.

Midstream Investments – Rate and Other Regulation

Federal, state, and local regulation may affect certain aspects of Enable’s business.

Interstate Natural Gas Pipeline Regulation

Enable’s interstate pipeline systems—EGT, MRT and SESH—are subject to regulation by the FERC and are considered “natural gas companies” under the NGA. Under the NGA, the rates for service on Enable’s interstate facilities must be just and reasonable and not unduly discriminatory. Rate and tariff changes for these facilities can only be implemented upon approval by the FERC. Enable’s interstate pipelines business operations may be affected by changes in the demand for natural gas, the available supply and relative price of natural gas in the Mid-continent and Gulf Coast natural gas supply regions and general economic conditions.

Market Behavior Rules; Posting and Reporting Requirements

The EPAct of 2005 amended the NGA to add an anti-manipulation provision that makes it unlawful for any entity to engage in prohibited behavior as prescribed in FERC rules, which were subsequently issued in FERC Order No. 670. The EPAct of 2005 also amends the NGA and the NGPA to give the FERC authority to impose civil penalties for violations of these statutes and FERC’s regulations, rules, and orders, of up to $1.2 million per day per violation, subject to periodic adjustment to account for inflation. Should Enable fail to comply with all applicable FERC-administered statutes, rules, regulations and orders, it could be subject to substantial penalties and fines. In addition, the CFTC is directed under the CEA to prevent price manipulations for the commodity and futures markets, including the energy futures markets. Pursuant to the Dodd-Frank Act and other authority, the CFTC has adopted anti-market manipulation regulations that prohibit fraud and price manipulation in the commodity and futures markets. The CFTC also has statutory authority to seek civil penalties of up to the greater of $1.1 million or triple the monetary gain to the violator for violations of the anti-market manipulation sections of the CEA. These maximum penalty levels are also subject to periodic adjustment to account for inflation.

Intrastate Natural Gas Pipeline and Storage Regulation

Intrastate natural gas transportation is largely regulated by the state in which the transportation takes place. However, an intrastate natural gas pipeline system may transport natural gas in interstate commerce provided that the rates, terms, and conditions of such transportation service comply with Section 311 of the NGPA and Part 284 of the FERC’s regulations. Rates for service pursuant to Section 311 of the NGPA are generally subject to review and approval by the FERC at least once every five years.

11

Failure to observe the service limitations applicable to transportation services provided under Section 311, failure to comply with the rates approved by the FERC for Section 311 service, or failure to comply with the terms and conditions of service established in the pipeline’s FERC-approved Statement of Operating Conditions could result in the assertion of federal NGA jurisdiction by the FERC and/or the imposition of administrative, civil and criminal penalties, as described under “—Interstate Natural Gas Pipeline Regulation” above.

Natural Gas Gathering and Processing Regulation

Section 1(b) of the NGA exempts natural gas gathering facilities from the jurisdiction of the FERC. Although the FERC has not made formal determinations with respect to all of the facilities Enable considers to be gathering facilities, Enable believes that its natural gas pipelines meet the traditional tests that the FERC has used to determine that a pipeline is a gathering pipeline and is therefore not subject to FERC jurisdiction. The distinction, however, has been the subject of substantial litigation, and the FERC determines whether facilities are gathering facilities on a case-by-case basis, so the classification and regulation of Enable’s gathering facilities is subject to change based on future determinations.

States may regulate gathering pipelines. State regulation generally includes various safety, environmental and, in some circumstances, anti-discrimination requirements, and in some instances complaint-based rate regulation. Enable’s gathering operations may be subject to ratable take and common purchaser statutes in the states in which they operate.

Enable’s gathering operations could be adversely affected should they be subject in the future to the application of state or federal regulation of rates and services. Enable’s gathering operations could also be subject to additional safety and operational regulations relating to the design, construction, testing, operation, replacement and maintenance of gathering facilities. We cannot predict what effect, if any, such changes might have on Enable’s operations, but the industry could be required to incur additional capital expenditures and increased costs depending on future legislative and regulatory changes.

Crude Oil Gathering Regulation

Enable provides interstate transportation on its crude oil gathering system in North Dakota pursuant to a public tariff in accordance with FERC regulatory requirements. Crude oil gathering pipelines that provide interstate transportation service may be regulated as a common carrier by the FERC under the ICA, the Energy Policy Act of 1992, and the rules and regulations promulgated under those laws. The ICA and FERC regulations require that rates for interstate service pipelines that transport crude oil and refined petroleum products (collectively referred to as “petroleum pipelines”) and certain other liquids, be just and reasonable and non-discriminatory or not conferring any undue preference upon any shipper. FERC regulations also require interstate common carrier petroleum pipelines to file with the FERC and publicly post tariffs stating their interstate transportation rates and terms and conditions of service.

Safety and Health Regulation

Certain of Enable’s facilities are subject to pipeline safety regulations. PHMSA regulates safety requirements in the design, construction, operation and maintenance of jurisdictional natural gas and hazardous liquid pipeline facilities. All natural gas transmission facilities, such as Enable’s interstate natural gas pipelines, are subject to PHMSA’s regulations, but natural gas gathering pipelines are subject only to the extent they are classified as regulated gathering pipelines. In addition, several NGL pipeline facilities and crude oil pipeline facilities are regulated as hazardous liquids pipelines.

Pursuant to various federal statutes, including the NGPSA, the DOT, through PHMSA, regulates pipeline safety and integrity. NGL and crude oil pipelines are subject to regulation by PHMSA under the Hazardous Liquid Pipeline Safety Act which requires PHMSA to develop, prescribe, and enforce minimum federal safety standards for the transportation of hazardous liquids by pipeline, and comparable state statutes with respect to design, installation, testing, construction, operation, replacement and management of pipeline facilities. Should Enable fail to comply with DOT or comparable state regulations, it could be subject to penalties and fines. If future DOT pipeline regulations were to require that Enable expand its integrity management program to currently unregulated pipelines, costs associated with compliance may have a material effect on its operations.

ENVIRONMENTAL MATTERS

Our operations and the operations of Enable are subject to stringent and complex laws and regulations pertaining to the environment. As an owner or operator of natural gas pipelines, distribution systems and storage, electric transmission and distribution systems, and the facilities that support these systems, we must comply with these laws and regulations at the federal, state and local levels. These laws and regulations can restrict or impact our business activities in many ways, including, but not limited to:

12

• | restricting the way we can handle or dispose of wastes; |

• | limiting or prohibiting construction activities in sensitive areas such as wetlands, coastal regions or areas inhabited by endangered species; |

• | requiring remedial action to mitigate environmental conditions caused by our operations or attributable to former operations; |

• | enjoining the operations of facilities with permits issued pursuant to such environmental laws and regulations; and |

• | impacting the demand for our services by directly or indirectly affecting the use or price of natural gas. |

To comply with these requirements, we may need to spend substantial amounts and devote other resources from time to time to, among other activities:

• | construct or acquire new facilities and equipment; |

• | acquire permits for facility operations; |

• | modify, upgrade or replace existing and proposed equipment; and |

• | clean or decommission waste management areas, fuel storage facilities and other locations. |

Failure to comply with these laws and regulations may trigger a variety of administrative, civil and criminal enforcement measures, including the assessment of monetary penalties, the imposition of remedial actions and the issuance of orders enjoining future operations. Certain environmental statutes impose strict, joint and several liability for costs required to assess, clean up and restore sites where hazardous substances have been stored, disposed or released. Moreover, it is not uncommon for neighboring landowners and other third parties to file claims for personal injury and/or property damage allegedly caused by the release of hazardous substances or other waste products into the environment.

The recent trend in environmental regulation has been to place more restrictions and limitations on activities that may impact the environment. There can be no assurance as to the amount or timing of future expenditures for environmental compliance or remediation, and actual future expenditures may be different from the amounts we currently anticipate. We try to anticipate future regulatory requirements that might be imposed and plan accordingly to maintain compliance with changing environmental laws and regulations and to ensure the costs of such compliance are reasonable.

Based on current regulatory requirements and interpretations, we do not believe that compliance with federal, state or local environmental laws and regulations will have a material adverse effect on our business, financial position, results of operations or cash flows. In addition, we believe that our current environmental remediation activities will not materially interrupt or diminish our operational ability. We cannot assure you that future events, such as changes in existing laws, the promulgation of new laws, or the development or discovery of new facts or conditions will not cause us to incur significant costs. The following is a discussion of material current environmental and safety issues, laws and regulations that relate to our operations. We believe that we are in substantial compliance with these environmental laws and regulations.

Global Climate Change

There is increasing attention being paid in the United States and worldwide to the issue of climate change. As a result, from time to time, regulatory agencies have considered the modification of existing laws or regulations or the adoption of new laws or regulations addressing the emissions of GHG on the state, federal, or international level. Some of the proposals would require industrial sources to meet stringent new standards that would require substantial reductions in GHG emissions. CERC’s revenues, operating costs and capital requirements could be adversely affected as a result of any regulatory action that would require installation of new control technologies or a modification of its operations or would have the effect of reducing the consumption of natural gas. Our electric transmission and distribution business, in contrast to some electric utilities, does not generate electricity and thus is not directly exposed to the risk of high capital costs and regulatory uncertainties that face electric utilities that burn fossil fuels to generate electricity. Nevertheless, Houston Electric’s revenues could be adversely affected to the extent any resulting regulatory action has the effect of reducing consumption of electricity by ultimate consumers within its service territory. Likewise, incentives to conserve energy or to use energy sources other than natural gas could result in a decrease in demand for our services. Conversely, regulatory actions that effectively promote the consumption of natural gas because of its lower emissions

13

characteristics would be expected to beneficially affect CERC and its natural gas-related businesses. At this point in time, however, it would be speculative to try to quantify the magnitude of the impacts from possible new regulatory actions related to GHG emissions, either positive or negative, on our businesses.

To the extent climate changes may occur and such climate changes result in warmer temperatures in our service territories, financial results from our and Enable’s businesses could be adversely impacted. For example, CERC’s NGD could be adversely affected through lower natural gas sales and Enable’s natural gas gathering, processing and transportation and crude oil gathering businesses could experience lower revenues. On the other hand, warmer temperatures in our electric service territory may increase our revenues from transmission and distribution through increased demand for electricity for cooling. Another possible result of climate change is more frequent and more severe weather events, such as hurricanes or tornadoes. Since many of our facilities are located along or near the Gulf Coast, increased or more severe hurricanes or tornadoes could increase our costs to repair damaged facilities and restore service to our customers. When we cannot deliver electricity or natural gas to customers, or our customers cannot receive our services, our financial results can be impacted by lost revenues, and we generally must seek approval from regulators to recover restoration costs. To the extent we are unable to recover those costs, or if higher rates resulting from our recovery of such costs result in reduced demand for our services, our future financial results may be adversely impacted.

Air Emissions

Our operations are subject to the federal Clean Air Act and comparable state laws and regulations. These laws and regulations regulate emissions of air pollutants from various industrial sources, including processing plants and compressor stations, and also impose various monitoring and reporting requirements. Such laws and regulations may require pre-approval for the construction or modification of certain projects or facilities expected to produce air emissions or result in the increase of existing air emissions. We may be required to obtain and strictly comply with air permits containing various emissions and operational limitations, or utilize specific emission control technologies to limit emissions. Failure to comply with these requirements could result in monetary penalties, injunctions, conditions or restrictions on operations, and potentially criminal enforcement actions. We may be required to incur certain capital expenditures in the future for air pollution control equipment in connection with obtaining and maintaining operating permits and approvals for air emissions.

The EPA has established new air emission control requirements for natural gas and NGLs production, processing and transportation activities. Under the NESHAPS, the EPA established the RICE MACT rule. Compressors and back up electrical generators used by our Natural Gas Distribution business segment, and back up electrical generators used by our Electric Transmission & Distribution business segment, are substantially compliant with these laws and regulations.

Water Discharges

Our operations are subject to the Federal Water Pollution Control Act of 1972, as amended, also known as the Clean Water Act, and analogous state laws and regulations. These laws and regulations impose detailed requirements and strict controls regarding the discharge of pollutants into waters of the United States. The unpermitted discharge of pollutants, including discharges resulting from a spill or leak incident, is prohibited. The Clean Water Act and regulations implemented thereunder also prohibit discharges of dredged and fill material into wetlands and other waters of the United States unless authorized by an appropriately issued permit. Any unpermitted release of petroleum or other pollutants from our pipelines or facilities could result in fines or penalties as well as significant remedial obligations.

Under the Obama administration, the EPA promulgated a set of rules that included a comprehensive regulatory overhaul of defining “waters of the United States” for the purposes of determining federal jurisdiction. These regulations have the potential to affect many aspects of our water-related regulatory compliance obligations. However, the new rules were challenged in court, and the U.S. Supreme Court has recently held that any challenge to the rules must be brought in the U.S. district courts rather than directly before the U.S. courts of appeals. As a result, the new definition of the “waters of the United States” is likely to be disputed in litigation for years to come. Additionally, the Trump administration has signaled its intent to repeal and replace the Obama-era rules. Thus, the fate and content of the new regulations is currently uncertain, and it is not clear when, and even if, they will be enacted. The potential impact of any new “waters of the United States” regulations on our business, liabilities, compliance obligations or profits and revenues is uncertain at this time.

Hazardous Waste

Our operations generate wastes, including some hazardous wastes, that are subject to the federal RCRA, and comparable state laws, which impose detailed requirements for the handling, storage, treatment, transport and disposal of hazardous and solid waste. RCRA currently exempts many natural gas gathering and field processing wastes from classification as hazardous waste. Specifically, RCRA excludes from the definition of hazardous waste waters produced and other wastes associated with the

14

exploration, development or production of crude oil and natural gas. However, these oil and gas exploration and production wastes are still regulated under state law and the less stringent non-hazardous waste requirements of RCRA. Moreover, ordinary industrial wastes such as paint wastes, waste solvents, laboratory wastes and waste compressor oils may be regulated as hazardous waste. The transportation of natural gas in pipelines may also generate some hazardous wastes that would be subject to RCRA or comparable state law requirements.

Liability for Remediation

CERCLA, also known as “Superfund,” and comparable state laws impose liability, without regard to fault or the legality of the original conduct, on certain classes of persons responsible for the release of “hazardous substances” into the environment. Classes of PRPs include the current and past owners or operators of sites where a hazardous substance was released and companies that disposed or arranged for the disposal of hazardous substances at offsite locations such as landfills. Although petroleum, as well as natural gas, is expressly excluded from CERCLA’s definition of a “hazardous substance,” in the course of our ordinary operations we do, from time to time, generate wastes that may fall within the definition of a “hazardous substance.” CERCLA authorizes the EPA and, in some cases, third parties to take action in response to threats to the public health or the environment and to recover the costs they incur from the responsible classes of persons. Under CERCLA, we could potentially be subject to joint and several liability for the costs of cleaning up and restoring sites where hazardous substances have been released, for damages to natural resources, and for associated response and assessment costs, including for the costs of certain health studies.

Liability for Preexisting Conditions

For information about preexisting environmental matters, please see Note 15(d).

EMPLOYEES

As of December 31, 2017, we had 7,977 full-time employees. The following table sets forth the number of our employees by business segment as of December 31, 2017:

Business Segment | Number | Number Represented by Collective Bargaining Groups | ||||

Electric Transmission & Distribution | 2,816 | 1,452 | ||||

Natural Gas Distribution | 3,316 | 1,200 | ||||

Energy Services | 297 | — | ||||

Other Operations | 1,548 | 127 | ||||

Total | 7,977 | 2,779 | ||||

For information about the status of collective bargaining agreements, see Note 7(f) to our consolidated financial statements.

EXECUTIVE OFFICERS

(as of February 9, 2018)

Name | Age | Title | ||

Milton Carroll | 67 | Executive Chairman | ||

Scott M. Prochazka | 51 | President and Chief Executive Officer and Director | ||

William D. Rogers | 57 | Executive Vice President and Chief Financial Officer | ||

Tracy B. Bridge | 59 | Executive Vice President and President, Electric Division | ||

Scott E. Doyle | 46 | Senior Vice President, Natural Gas Distribution | ||

Joseph J. Vortherms | 57 | Senior Vice President, Energy Services | ||

Dana C. O’Brien | 50 | Senior Vice President and General Counsel | ||

Sue B. Ortenstone | 61 | Senior Vice President and Chief Human Resources Officer | ||

Milton Carroll has served on the Board of Directors of CenterPoint Energy or its predecessors since 1992. He has served as Executive Chairman of CenterPoint Energy since June 2013 and as Chairman from September 2002 until May 2013. Mr. Carroll has served as a director of Halliburton Company since 2006 and Western Gas Holdings, LLC, the general partner of Western Gas Partners, LP, since 2008. He has served as a director of Health Care Service Corporation since 1998 and as its chairman since

15

2002. He previously served as a director of LyondellBasell Industries N.V. from July 2010 to July 2016 as well as LRE GP, LLC, the general partner of LRR Energy, L.P., from November 2011 to January 2014.