Attached files

| file | filename |

|---|---|

| EX-23 - EXHIBIT 23 - CENTERPOINT ENERGY HOUSTON ELECTRIC LLC | cehe_exhibit23x12312017.htm |

| EX-32.2 - EXHIBIT 32.2 - CENTERPOINT ENERGY HOUSTON ELECTRIC LLC | cehe_exhibit322x12312017.htm |

| EX-32.1 - EXHIBIT 32.1 - CENTERPOINT ENERGY HOUSTON ELECTRIC LLC | cehe_exhibit321x12312017.htm |

| EX-31.2 - EXHIBIT 31.2 - CENTERPOINT ENERGY HOUSTON ELECTRIC LLC | cehe_exhibit312x12312017.htm |

| EX-31.1 - EXHIBIT 31.1 - CENTERPOINT ENERGY HOUSTON ELECTRIC LLC | cehe_exhibit311x12312017.htm |

| EX-12 - EXHIBIT 12 - CENTERPOINT ENERGY HOUSTON ELECTRIC LLC | cehe_exhibit12x12312017.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________

Form 10-K

(Mark One) | |

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2017 | |

OR | |

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO | |

Commission file number 1-3187

______________________________

CenterPoint Energy Houston Electric, LLC

(Exact name of registrant as specified in its charter)

Texas | 22-3865106 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

1111 Louisiana | |

Houston, Texas 77002 | (713) 207-1111 |

(Address and zip code of principal executive offices) | (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

9.15% First Mortgage Bonds due 2021 | New York Stock Exchange |

6.95% General Mortgage Bonds due 2033 | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

CenterPoint Energy Houston Electric, LLC meets the conditions set forth in general instruction I(1)(a) and (b) of Form 10-K and is therefore filing this Form 10-K with the reduced disclosure format.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | Non-accelerated filer þ | Smaller reporting company o | Emerging growth company o |

(Do not check if a smaller reporting company) | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the common equity held by non-affiliates as of June 30, 2017: None

TABLE OF CONTENTS

PART I | ||

Page | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | Mine Safety Disclosures | |

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | Exhibits and Financial Statement Schedules | |

Item 16. | Form 10-K Summary | |

i

GLOSSARY | ||

ADFIT | Accumulated deferred federal income taxes | |

ADMS | Advanced Distribution Management System | |

AFUDC | Allowance for funds used during construction | |

AMS | Advanced Metering System | |

ARO | Asset retirement obligation | |

ASC | Accounting Standards Codification | |

ASU | Accounting Standards Update | |

Bond Companies | Bond Company II, Bond Company III, Bond Company IV and Restoration Bond Company, each a wholly-owned, bankruptcy remote entity formed solely for the purpose of purchasing and owning transition or system restoration property through the issuance of Securitization Bonds | |

Bond Company II | CenterPoint Energy Transition Bond Company II, LLC | |

Bond Company III | CenterPoint Energy Transition Bond Company III, LLC | |

Bond Company IV | CenterPoint Energy Transition Bond Company IV, LLC | |

Brazos Valley Connection | A portion of the Houston region transmission project between Houston Electric’s Zenith substation and the Gibbons Creek substation owned by the Texas Municipal Power Agency | |

CenterPoint Energy | CenterPoint Energy, Inc., and its subsidiaries | |

CERC Corp. | CenterPoint Energy Resources Corp. | |

CERC | CERC Corp., together with its subsidiaries | |

CERCLA | Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended | |

CES | CenterPoint Energy Services, Inc. | |

COLI | Corporate-owned life insurance | |

DCRF | Distribution Cost Recovery Factor | |

DOE | U.S. Department of Energy | |

EDIT | Excess deferred income taxes | |

EECR | Energy Efficiency Cost Recovery | |

EECRF | Energy Efficiency Cost Recovery Factor | |

EPA | Environmental Protection Agency | |

ERCOT | Electric Reliability Council of Texas | |

ERCOT ISO | ERCOT Independent System Operator | |

ERO | Electric Reliability Organization | |

FASB | Financial Accounting Standards Board | |

FERC | Federal Energy Regulatory Commission | |

Fitch | Fitch, Inc. | |

GenOn | GenOn Energy, Inc. | |

GHG | Greenhouse gases | |

GWh | Gigawatt-hours | |

Houston Electric | CenterPoint Energy Houston Electric, LLC and its subsidiaries | |

IBEW | International Brotherhood of Electrical Workers | |

IG | Intelligent Grid | |

IRS | Internal Revenue Service | |

kV | Kilovolt | |

LIBOR | London Interbank Offered Rate | |

Moody’s | Moody’s Investors Service, Inc. | |

NAV | Net asset value | |

NECA | National Electrical Contractors Association | |

NERC | North American Electric Reliability Corporation | |

ii

GLOSSARY (cont.) | ||

NRG | NRG Energy, Inc. | |

PRPs | Potentially responsible parties | |

PUCT | Public Utility Commission of Texas | |

RCRA | Resource Conservation and Recovery Act of 1976 | |

Reliant Energy | Reliant Energy, Incorporated | |

REP | Retail electric provider | |

Restoration Bond Company | CenterPoint Energy Restoration Bond Company, LLC | |

RICE MACT | Reciprocating Internal Combustion Engines Maximum Achievable Control Technology | |

RRI | Reliant Resources, Inc. | |

SEC | Securities and Exchange Commission | |

Securitization Bonds | Transition and system restoration bonds | |

S&P | Standard & Poor’s Ratings Services, a division of The McGraw-Hill Companies | |

TBD | To be determined | |

TCEH Corp. | Formerly Texas Competitive Electric Holdings Company LLC, predecessor to Vistra Energy Corp. whose major subsidiaries include Luminant and TXU Energy | |

TCJA | Tax reform legislation informally called the Tax Cuts and Jobs Act of 2017 | |

TCOS | Transmission Cost of Service | |

TDU | Transmission and distribution utility | |

Texas RE | Texas Reliability Entity | |

VIE | Variable interest entity | |

Vistra Energy Corp. | Texas-based energy company focused on the competitive energy and power generation markets | |

iii

We meet the conditions specified in General Instruction I (1)(a) and (b) of Form 10-K and are thereby permitted to use the reduced disclosure format for wholly-owned subsidiaries of reporting companies specified therein. Accordingly, we have omitted from this report the information called for by Item 10 (Directors, Executive Officers and Corporate Governance), Item 11 (Executive Compensation), Item 12 (Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters) and Item 13 (Certain Relationships and Related Transactions, and Director Independence) of Form 10-K. In lieu of the information called for by Item 6 (Selected Financial Data) and Item 7 (Management’s Discussion and Analysis of Financial Condition and Results of Operations) of Form 10-K, we have included, under Item 7, Management’s Narrative Analysis of Results of Operations to explain the reasons for material changes in the amount of revenue and expense items between 2017, 2016 and 2015.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

From time to time we make statements concerning our expectations, beliefs, plans, objectives, goals, strategies, future events or performance and underlying assumptions and other statements that are not historical facts. These statements are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Actual results may differ materially from those expressed or implied by these statements. You can generally identify our forward-looking statements by the words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “forecast,” “goal,” “intend,” “may,” “objective,” “plan,” “potential,” “predict,” “projection,” “should,” “target,” “will” or other similar words.

We have based our forward-looking statements on our management’s beliefs and assumptions based on information reasonably available to our management at the time the statements are made. We caution you that assumptions, beliefs, expectations, intentions and projections about future events may and often do vary materially from actual results. Therefore, we cannot assure you that actual results will not differ materially from those expressed or implied by our forward-looking statements.

Some of the factors that could cause actual results to differ from those expressed or implied by our forward-looking statements are described under “Risk Factors” in Item 1A and “Management’s Narrative Analysis of Results of Operations — Certain Factors Affecting Future Earnings” in Item 7 of this report, which discussions are incorporated herein by reference.

You should not place undue reliance on forward-looking statements. Each forward-looking statement speaks only as of the date of the particular statement, and we undertake no obligation to update or revise any forward-looking statements.

iv

PART I

Item 1. | Business |

OUR BUSINESS

Overview

We are an indirect, wholly-owned subsidiary of CenterPoint Energy, a public utility holding company. We provide electric transmission and distribution services to REPs serving more than 2.4 million metered customers in the Texas Gulf Coast area that includes the city of Houston. We consist of a single reportable business segment: Electric Transmission & Distribution.

Our principal executive offices are located at 1111 Louisiana, Houston, Texas 77002 (telephone number: 713-207-1111).

We make available free of charge on our parent company’s Internet website our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such reports with, or furnish them to, the SEC. Our parent company’s website address is www.centerpointenergy.com. Investors should also note that we announce material financial information in SEC filings, press releases and public conference calls. Based on guidance from the SEC, we may use the investor relations section of our parent’s website to communicate with our investors. It is possible that the financial and other information posted there could be deemed material information. Except to the extent explicitly stated herein, documents and information on our parent company’s website are not incorporated by reference herein.

Electric Transmission & Distribution

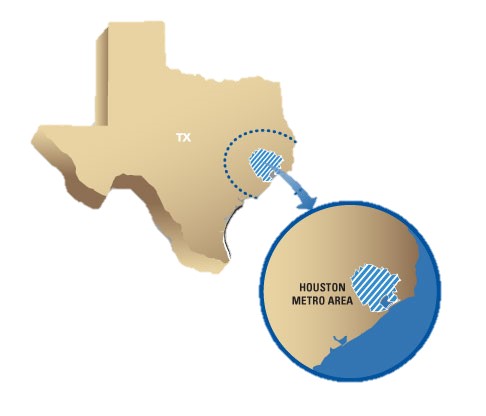

We are a transmission and distribution electric utility that operates wholly within the state of Texas and is a member of ERCOT. ERCOT serves as the independent system operator and regional reliability coordinator for member electric power systems in most of Texas. The ERCOT market represents approximately 90% of the demand for power in Texas and is one of the nation’s largest power markets. The ERCOT market operates under the reliability standards developed by the NERC, approved by the FERC and monitored and enforced by the Texas RE. The PUCT has primary jurisdiction over the ERCOT market to ensure the adequacy and reliability of electricity supply across the state’s main interconnected power transmission grid. Neither we nor any other subsidiary of CenterPoint Energy makes direct retail or wholesale sales of electric energy or owns or operates any electric generating facilities. Our service territory is depicted below:

Electric Transmission

On behalf of REPs, we deliver electricity from power plants to substations, from one substation to another and to retail electric customers taking power at or above 69 kV in locations throughout our certificated service territory. We construct and maintain transmission facilities and provide transmission services under tariffs approved by the PUCT.

1

The ERCOT ISO is responsible for operating the bulk electric power supply system in the ERCOT market. Our transmission business, along with those of other owners of transmission facilities in Texas, supports the operation of the ERCOT ISO. We participate with the ERCOT ISO and other ERCOT utilities to plan, design, obtain regulatory approval for and construct new transmission lines necessary to increase bulk power transfer capability and to remove existing constraints on the ERCOT transmission grid.

Electric Distribution

In ERCOT, end users purchase their electricity directly from certificated REPs. We deliver electricity for REPs in our certificated service area by carrying lower-voltage power from the substation to the retail electric customer. Our distribution network receives electricity from the transmission grid through power distribution substations and delivers electricity to end users through distribution feeders. Our operations include construction and maintenance of distribution facilities, metering services, outage response services and call center operations. We provide distribution services under tariffs approved by the PUCT. PUCT rules and market protocols govern the commercial operations of distribution companies and other market participants. Rates for these existing services are established pursuant to rate proceedings conducted before municipalities that have original jurisdiction and the PUCT.

Bond Companies

We have special purpose subsidiaries consisting of the Bond Companies, which we consolidate in our consolidated financial statements. The consolidated special purpose subsidiaries are wholly-owned, bankruptcy remote entities that were formed solely for the purpose of purchasing and owning transition or system restoration property through the issuance of Securitization Bonds, and conducting activities incidental thereto. The Securitization Bonds are repaid through charges imposed on customers in our service territory. For further discussion of the Securitization Bonds and the outstanding balances as of December 31, 2017 and 2016, see Note 8 to our consolidated financial statements.

Customers

We serve nearly all of the Houston/Galveston metropolitan area. At December 31, 2017, our customers consisted of approximately 68 REPs, which sell electricity to more than 2.4 million metered customers in our certificated service area, and municipalities, electric cooperatives and other distribution companies located outside our certificated service area. Each REP is licensed by, and must meet minimum creditworthiness criteria established by, the PUCT. We do not have long-term contracts with any of our customers. We operate using a continuous billing cycle, with meter readings being conducted and invoices being distributed to REPs each business day. For information regarding our major customers, see Note 7 to our consolidated financial statements.

Utility Technology

Our Smart Grid is comprised of the AMS, IG, ADMS and private telecommunications network. Since 2009, we have deployed fully operational advanced meters to virtually all of our 2.4 million metered customers, automated 31 substations, installed 872 IG Switching Devices on more than 200 circuits, built a wireless radio frequency mesh telecommunications network across our 5,000-square mile footprint, and enabled real-time grid monitoring and control, which leverages information from smart meters and field sensors to manage system events through the ADMS. We believe that the Smart Grid is already improving electric distribution service reliability and restoration, enhancing the consumer experience, supporting the growth of renewable energy and helping the environment by reducing carbon emissions.

Competition

There are no other electric transmission and distribution utilities in our service area. For another provider of transmission and distribution services to provide such services in our territory, it would be required to obtain a certificate of convenience and necessity from the PUCT and, depending on the location of the facilities, may also be required to obtain franchises from one or more municipalities. We know of no other party intending to enter this business in our service area at this time. Distributed generation (i.e., power generation located at or near the point of consumption) could result in a reduction of demand for our distribution services but has not been a significant factor to date.

Seasonality

A significant portion of our revenues is derived from rates that we collect from each REP based on the amount of electricity we deliver on behalf of that REP. Thus, our revenues and results of operations are subject to seasonality, weather conditions and other changes in electricity usage, with revenues generally being higher during the warmer months.

2

Properties

All of our properties are located in Texas. Our properties consist primarily of high-voltage electric transmission lines and poles, distribution lines, substations, service centers, service wires, telecommunications network and meters. Most of our transmission and distribution lines have been constructed over lands of others pursuant to easements or along public highways and streets under franchise agreements and as permitted by law.

All of our real and tangible properties, subject to certain exclusions, are currently subject to:

• | the lien of a Mortgage and Deed of Trust (the Mortgage) dated November 1, 1944, as supplemented; and |

• | the lien of a General Mortgage (the General Mortgage) dated October 10, 2002, as supplemented, which is junior to the lien of the Mortgage. |

For information related to debt outstanding under the Mortgage and General Mortgage, see Note 8 to our consolidated financial statements.

Electric Lines - Transmission. As of December 31, 2017, we owned and operated the following electric transmission lines:

Circuit Miles | ||||||

Operating Voltage | Overhead Lines | Underground Lines | ||||

69 kV | 271 | 2 | ||||

138 kV | 2,198 | 24 | ||||

345 kV | 1,219 | — | ||||

3,688 | 26 | |||||

Electric Lines - Distribution. As of December 31, 2017, we owned 28,883 pole miles of overhead distribution lines and 24,662 circuit miles of underground distribution lines.

Substations. As of December 31, 2017, we owned 235 major substation sites having a total installed rated transformer capacity of 64,924 megavolt amperes.

Service Centers. As of December 31, 2017, we operated 14 regional service centers located on a total of 292 acres of land. These service centers consist of office buildings, warehouses and repair facilities that are used in the business of transmitting and distributing electricity.

Franchises

We hold non-exclusive franchises from certain incorporated municipalities in our service territory. In exchange for the payment of fees, these franchises give us the right to use the streets and public rights-of-way of these municipalities to construct, operate and maintain our transmission and distribution system and to use that system to conduct our electric delivery business and for other purposes that the franchises permit. The terms of the franchises, with various expiration dates, typically range from 20 to 40 years.

REGULATION

We are subject to regulation by various federal, state and local governmental agencies, including the regulations described below.

Federal Energy Regulatory Commission

We are not a “public utility” under the Federal Power Act and, therefore, are not generally regulated by the FERC, although certain of our transactions are subject to limited FERC jurisdiction. The FERC has certain responsibilities with respect to ensuring the reliability of electric transmission service, including transmission facilities owned by us and other utilities within ERCOT. The FERC has designated the NERC as the ERO to promulgate standards, under FERC oversight, for all owners, operators and users of the bulk power system (Electric Entities). The ERO and the FERC have authority to (a) impose fines and other sanctions on Electric Entities that fail to comply with approved standards and (b) audit compliance with approved standards. The FERC has approved the delegation by the NERC of authority for reliability in ERCOT to the Texas RE. We do not anticipate that the reliability standards

3

proposed by the NERC and approved by the FERC will have a material adverse impact on our operations. To the extent that we are required to make additional expenditures to comply with these standards, it is anticipated that we will seek to recover those costs through the transmission charges that are imposed on all distribution service providers within ERCOT for electric transmission provided.

As a public utility holding company, under the Public Utility Holding Company Act of 2005, CenterPoint Energy is subject to reporting and accounting requirements and is required to maintain certain books and records and make them available for review by the FERC and state regulatory authorities in certain circumstances.

State and Local Regulation

We conduct our operations pursuant to a certificate of convenience and necessity issued by the PUCT that covers our present service area and facilities. The PUCT and certain municipalities have the authority to set the rates and terms of service provided by us under cost-of-service rate regulation. We hold non-exclusive franchises from certain incorporated municipalities in our service territory. In exchange for payment of fees, these franchises give us the right to use the streets and public rights-of-way of these municipalities to construct, operate and maintain our transmission and distribution system and to use that system to conduct our electric delivery business and for other purposes that the franchises permit. The terms of the franchises, with various expiration dates, typically range from 20 to 40 years.

Our distribution rates charged to REPs for residential customers are primarily based on amounts of energy delivered, whereas distribution rates for a majority of commercial and industrial customers are primarily based on peak demand. All REPs in our service area pay the same rates and other charges for transmission and distribution services. This regulated delivery charge includes the transmission and distribution rate (which includes municipal franchise fees), a distribution recovery mechanism for recovery of incremental distribution-invested capital above that which is already reflected in the base distribution rate, a nuclear decommissioning charge associated with decommissioning the South Texas nuclear generating facility, an EECR charge, and charges associated with securitization of regulatory assets, stranded costs and restoration costs relating to Hurricane Ike. Transmission rates charged to distribution companies are based on amounts of energy transmitted under “postage stamp” rates that do not vary with the distance the energy is being transmitted. All distribution companies in ERCOT pay us the same rates and other charges for transmission services.

For a discussion of certain of our ongoing regulatory proceedings, see “Management’s Narrative Analysis of Results of Operations — Liquidity and Capital Resources — Regulatory Matters” in Item 7 of this report, which discussion is incorporated herein by reference.

ENVIRONMENTAL MATTERS

Our operations are subject to stringent and complex laws and regulations pertaining to the environment. As an owner or operator of electric transmission and distribution systems, and the facilities that support these systems, we must comply with these laws and regulations at the federal, state and local levels. These laws and regulations can restrict or impact our business activities in many ways, including, but not limited to:

• | restricting the way we can handle or dispose of wastes; |

• | limiting or prohibiting construction activities in sensitive areas such as wetlands, coastal regions or areas inhabited by endangered species; |

• | requiring remedial action to mitigate environmental conditions caused by our operations or attributable to former operations; and |

• | enjoining the operations of facilities with permits issued pursuant to such environmental laws and regulations. |

To comply with these requirements, we may need to spend substantial amounts and devote other resources from time to time to, among other activities:

• | construct or acquire new facilities and equipment; |

• | acquire permits for facility operations; |

4

• | modify, upgrade or replace existing and proposed equipment; and |

• | clean or decommission waste management areas, fuel storage facilities and other locations. |

Failure to comply with these laws and regulations may trigger a variety of administrative, civil and criminal enforcement measures, including the assessment of monetary penalties, the imposition of remedial actions and the issuance of orders enjoining future operations. Certain environmental statutes impose strict, joint and several liability for costs required to assess, clean up and restore sites where hazardous substances have been stored, disposed or released. Moreover, it is not uncommon for neighboring landowners and other third parties to file claims for personal injury and/or property damage allegedly caused by the release of hazardous substances or other waste products into the environment.

The recent trend in environmental regulation has been to place more restrictions and limitations on activities that may impact the environment. There can be no assurance as to the amount or timing of future expenditures for environmental compliance or remediation, and actual future expenditures may be different from the amounts we currently anticipate. We try to anticipate future regulatory requirements that might be imposed and plan accordingly to maintain compliance with changing environmental laws and regulations and to ensure the costs of such compliance are reasonable.

Based on current regulatory requirements and interpretations, we do not believe that compliance with federal, state or local environmental laws and regulations will have a material adverse effect on our business, financial position, results of operations or cash flows. In addition, we believe that our current environmental remediation activities will not materially interrupt or diminish our operational ability. We cannot assure you that future events, such as changes in existing laws, the promulgation of new laws, or the development or discovery of new facts or conditions will not cause us to incur significant costs. The following is a discussion of material current environmental and safety issues, laws and regulations that relate to our operations. We believe that we are in substantial compliance with these environmental laws and regulations.

Global Climate Change

There is increasing attention being paid in the United States and worldwide to the issue of climate change. As a result, from time to time, regulatory agencies have considered the modification of existing laws or regulations or the adoption of new laws or regulations addressing the emissions of GHG on the state, federal, or international level. Some of the proposals would require industrial sources to meet stringent new standards that would require substantial reductions in GHG emissions. We, in contrast to some electric utilities, do not generate electricity and thus are not directly exposed to the risk of high capital costs and regulatory uncertainties that face electric utilities that burn fossil fuels to generate electricity. Nevertheless, our revenues could be adversely affected to the extent any resulting regulatory action has the effect of reducing consumption of electricity by ultimate consumers within our service territory. Likewise, incentives to conserve energy or to use other energy sources could result in a decrease in demand for our services. At this point in time, however, it would be speculative to try to quantify the magnitude of the impacts from possible new regulatory actions related to GHG emissions, either positive or negative, on our business.

To the extent climate changes may occur, financial results from our business could be impacted. Warmer temperatures in our service territory may increase our revenues from transmission and distribution through increased demand for electricity for cooling. Another possible result of climate change is more frequent and more severe weather events, such as hurricanes or tornadoes. Since many of our facilities are located along or near the Gulf Coast, increased or more severe hurricanes or tornadoes could increase our costs to repair damaged facilities and restore service to our customers. When we cannot deliver electricity to customers, or our customers cannot receive our services, our financial results can be impacted by lost revenues, and we generally must seek approval from regulators to recover restoration costs. To the extent we are unable to recover those costs, or if higher rates resulting from our recovery of such costs result in reduced demand for our services, our future financial results may be adversely impacted.

Air Emissions

Our operations are subject to the federal Clean Air Act and comparable state laws and regulations. These laws and regulations regulate emissions of air pollutants from various industrial sources and also impose various monitoring and reporting requirements. Such laws and regulations may require pre-approval for the construction or modification of certain projects or facilities expected to produce air emissions or result in the increase of existing air emissions. We may be required to obtain and strictly comply with air permits containing various emissions and operational limitations, or utilize specific emission control technologies to limit emissions. Failure to comply with these requirements could result in monetary penalties, injunctions, conditions or restrictions on operations, and potentially criminal enforcement actions. We may be required to incur certain capital expenditures in the future for air pollution control equipment in connection with obtaining and maintaining operating permits and approvals for air emissions. Under the National

5

Emission Standards for Hazardous Air Pollutants, the EPA established the RICE MACT rule. Back up electrical generators we use are substantially compliant with these laws and regulations.

Water Discharges

Our operations are subject to the Federal Water Pollution Control Act of 1972, as amended, also known as the Clean Water Act, and analogous state laws and regulations. These laws and regulations impose detailed requirements and strict controls regarding the discharge of pollutants into waters of the United States. The unpermitted discharge of pollutants, including discharges resulting from a spill or leak incident, is prohibited. The Clean Water Act and regulations implemented thereunder also prohibit discharges of dredged and fill material into wetlands and other waters of the United States unless authorized by an appropriately issued permit. Any unpermitted release of petroleum or other pollutants from our facilities could result in fines or penalties as well as significant remedial obligations.

Under the Obama administration, the EPA promulgated a set of rules that included a comprehensive regulatory overhaul of defining “waters of the United States” for the purposes of determining federal jurisdiction. These regulations have the potential to affect many aspects of our water-related regulatory compliance obligations. However, the new rules were challenged in court, and the U.S. Supreme Court has recently held that any challenge to the rules must be brought in the U.S. district courts rather than directly before the U.S. courts of appeals. As a result, the new definition of the “waters of the United States” is likely to be disputed in litigation for years to come. Additionally, the Trump administration has signaled its intent to repeal and replace the Obama-era rules. Thus, the fate and content of the new regulations is currently uncertain, and it is not clear when, and even if, they will be enacted. The potential impact of any new “waters of the United States” regulations on our business, liabilities, compliance obligations or profits and revenues is uncertain at this time.

Hazardous Waste

Our operations generate wastes, including some hazardous wastes, that are subject to the federal RCRA, and comparable state laws, which impose detailed requirements for the handling, storage, treatment, transport and disposal of hazardous and solid waste. Ordinary industrial wastes such as paint wastes, waste solvents and laboratory wastes may be regulated as hazardous waste.

Liability for Remediation

CERCLA, also known as “Superfund,” and comparable state laws impose liability, without regard to fault or the legality of the original conduct, on certain classes of persons responsible for the release of “hazardous substances” into the environment. Classes of PRPs include the current and past owners or operators of sites where a hazardous substance was released and companies that disposed or arranged for the disposal of hazardous substances at offsite locations such as landfills. In the course of our ordinary operations we do, from time to time, generate wastes that may fall within the definition of a “hazardous substance.” CERCLA authorizes the EPA and, in some cases, third parties to take action in response to threats to the public health or the environment and to recover the costs they incur from the responsible classes of persons. Under CERCLA, we could potentially be subject to joint and several liability for the costs of cleaning up and restoring sites where hazardous substances have been released, for damages to natural resources, and for associated response and assessment costs, including for the costs of certain health studies.

Liability for Preexisting Conditions

For information about preexisting environmental matters, please see Note 10(b) to our consolidated financial statements.

EMPLOYEES

As of December 31, 2017, we had 2,816 full-time employees, of which approximately 52% were subject to a collective bargaining agreement. The collective bargaining agreement with the IBEW Local 66 will expire in May of 2020. This agreement was last negotiated in 2016.

6

Item 1A. | Risk Factors |

The following, along with any additional legal proceedings identified or incorporated by reference in Item 3 of this report, summarizes the principal risk factors associated with our business. However, additional risks and uncertainties either not presently known or not currently believed by management to be material may also adversely affect our business.

Risk Factors Associated with Our Consolidated Financial Condition

We are an indirect, wholly-owned subsidiary of CenterPoint Energy. CenterPoint Energy can exercise substantial control over our dividend policy and business and operations and could do so in a manner that is adverse to our interests.

We are managed by officers and employees of CenterPoint Energy. Our management will make determinations with respect to the following:

• | our payment of dividends; |

• | our financings and our capital raising activities; |

• | mergers or other business combinations; and |

• | our acquisition or disposition of assets. |

Other than the financial covenant contained in our credit facility (described under “Management’s Narrative Analysis of Results of Operations—Liquidity and Capital Resources” in Item 7 of Part II of this report), which could have the practical effect of limiting the payment of dividends under certain circumstances, there are no contractual restrictions on our ability to pay dividends to CenterPoint Energy. Our management could decide to increase our dividends to CenterPoint Energy to support its cash needs. This could adversely affect our liquidity. However, under our credit facility, our ability to pay dividends is restricted by a covenant that debt, excluding Securitization Bonds, as a percentage of total capitalization may not exceed 65%.

If we are unable to arrange future financings on acceptable terms, our ability to refinance existing indebtedness could be limited.

As of December 31, 2017, we had $4.8 billion of outstanding indebtedness on a consolidated basis, which includes $1.9 billion of non-recourse Securitization Bonds. As of December 31, 2017, principal repayments through 2020 are limited to scheduled principal repayments of approximately $1.1 billion on Securitization Bonds, for which dedicated revenue streams exist. Our future financing activities may be significantly affected by, among other things:

• | general economic and capital market conditions; |

• | credit availability from financial institutions and other lenders; |

• | investor confidence in us and CenterPoint Energy and the markets in which we operate; |

• | maintenance of acceptable credit ratings by us and CenterPoint Energy; |

• | market expectations regarding our and CenterPoint Energy’s future earnings and cash flows; |

• | our and CenterPoint Energy’s ability to access capital markets on reasonable terms; |

• | our exposure to GenOn (formerly known as RRI Energy, Inc., Reliant Energy and RRI), a wholly-owned subsidiary of NRG and currently the subject of bankruptcy proceedings, in connection with certain indemnification obligations; and |

• | provisions of relevant tax and securities laws. |

As of December 31, 2017, we had approximately $2.9 billion aggregate principal amount of general mortgage bonds outstanding under the General Mortgage, including approximately $118 million held in trust to secure pollution control bonds for which CenterPoint Energy is obligated. Additionally, as of December 31, 2017, we had approximately $102 million aggregate principal amount of first mortgage bonds outstanding under the Mortgage. We may issue additional general mortgage bonds on the basis of

7

retired bonds, 70% of property additions or cash deposited with the trustee. Approximately $4.2 billion of additional first mortgage bonds and general mortgage bonds in the aggregate could be issued on the basis of retired bonds and 70% of property additions as of December 31, 2017. We have contractually agreed that we will not issue additional first mortgage bonds, subject to certain exceptions.

Our current credit ratings are discussed in “Management’s Narrative Analysis of Results of Operations — Liquidity and Capital Resources — Impact on Liquidity of a Downgrade in Credit Ratings” in Item 7 of Part II of this report. These credit ratings may not remain in effect for any given period of time and one or more of these ratings may be lowered or withdrawn entirely by a rating agency. We note that these credit ratings are not recommendations to buy, sell or hold our securities. Each rating should be evaluated independently of any other rating. Any future reduction or withdrawal of one or more of our credit ratings could have a material adverse impact on our ability to access capital on acceptable terms.

The creditworthiness and liquidity of our parent company and our affiliates could affect our creditworthiness and liquidity.

Our credit ratings and liquidity may be impacted by the creditworthiness and liquidity of our parent company and our affiliates. As of December 31, 2017, CenterPoint Energy and its subsidiaries other than us have approximately $50 million principal amount of debt required to be paid through 2020. If CenterPoint Energy were to experience a deterioration in its creditworthiness or liquidity, our creditworthiness and liquidity could be adversely affected. In addition, CenterPoint Energy or its other subsidiaries or affiliates may from time to time acquire or dispose of assets or businesses or enter into joint ventures or other transactions that could adversely impact the credit capacity, credit ratings or liquidity of CenterPoint Energy or its other subsidiaries or affiliates, which, as a result, could adversely impact our credit ratings and liquidity. Also, from time to time we and other affiliates invest in or borrow funds from the money pool maintained by CenterPoint Energy. If CenterPoint Energy or the affiliates that borrow our invested funds were to experience a deterioration in their creditworthiness or liquidity, our creditworthiness, liquidity and the repayment of notes receivable from CenterPoint Energy and our affiliates under the money pool could be adversely impacted.

Risk Factors Affecting Our Business

Rate regulation of our business may delay or deny our ability to earn an expected return and fully recover our costs.

Our rates are regulated by certain municipalities and the PUCT based on an analysis of our invested capital, our expenses and other factors in a test year in comprehensive base rate proceedings (i.e., general rate cases) subject to periodic review and adjustment. Each of these rate proceedings is subject to third-party intervention and appeal, and the timing of a general base rate proceeding may be out of our control. The rates that we are allowed to charge may not match our costs at any given time, which is referred to as “regulatory lag.”

Though several interim rate adjustment mechanisms have been implemented to reduce the effects of regulatory lag, these adjustment mechanisms are subject to the applicable regulatory body’s approval and are subject to limitations that may reduce our ability to adjust rates. For example, the DCRF mechanism adjusts an electric utility’s rates for increases in net distribution-invested capital (e.g., distribution plant and intangible plant and communication equipment) since its last comprehensive base rate proceeding, but we may only make a DCRF filing once per calendar year. The TCOS mechanism allows a transmission service provider to update its wholesale transmission rates to reflect changes in transmission-related invested capital, but is only available twice per calendar year.

We can make no assurance that filings for such mechanisms will result in favorable adjustments to rates. Notwithstanding the application of the rate mechanisms discussed above, the regulatory process by which rates are determined is subject to change as a result of the legislative process or rulemaking, as the case may be, and may not always be available or result in rates that will produce recovery of our costs or enable us to earn an expected return. In addition, changes to the interim adjustment mechanisms could result in an increase in regulatory lag or otherwise impact our ability to recover our costs in a timely manner. To the extent the regulatory process does not allow us to make a full and timely recovery of appropriate costs, our results of operations, financial condition and cash flows could be adversely affected.

Disruptions at power generation facilities owned by third parties could interrupt our sales of transmission and distribution services.

We transmit and distribute to customers of REPs electric power that the REPs obtain from power generation facilities owned by third parties. We do not own or operate any power generation facilities. If power generation is disrupted or if power generation capacity is inadequate, our sales of transmission and distribution services may be diminished or interrupted, and our results of operations, financial condition and cash flows could be adversely affected.

8

Our revenues and results of operations are seasonal.

A significant portion of our revenues is derived from rates that we collect from each REP based on the amount of electricity we deliver on behalf of such REP. Thus, our revenues and results of operations are subject to seasonality, weather conditions and other changes in electricity usage, with revenues generally being higher during the warmer months. Unusually mild weather in the warmer months could diminish our results of operations and harm our financial condition. Conversely, extreme warm weather conditions could increase our results of operations in a manner that would not likely be annually recurring.

We could be subject to higher costs and fines or other sanctions as a result of mandatory reliability standards.

The FERC has jurisdiction with respect to ensuring the reliability of electric transmission service, including transmission facilities owned by us and other utilities within ERCOT. The FERC has designated the NERC as the ERO to promulgate standards, under FERC oversight, for all owners, operators and users of the bulk power system. The FERC has approved the delegation by the NERC of authority for reliability in ERCOT to the Texas RE, a Texas non-profit corporation. Compliance with the mandatory reliability standards may subject us to higher operating costs and may result in increased capital expenditures. In addition, if we were to be found to be in noncompliance with applicable mandatory reliability standards, we could be subject to sanctions, including substantial monetary penalties.

A substantial portion of our receivables is concentrated in a small number of REPs and any delay or default in such payments could adversely affect our cash flows, financial condition and results of operations.

Our receivables from the distribution of electricity are collected from REPs that supply the electricity we distribute to their customers. As of December 31, 2017, we did business with approximately 68 REPs. Adverse economic conditions, structural problems in the market served by ERCOT or financial difficulties of one or more REPs could impair the ability of these REPs to pay for our services or could cause them to delay such payments. We depend on these REPs to remit payments on a timely basis. Applicable regulatory provisions require that customers be shifted to another REP or a provider of last resort if a REP cannot make timely payments. Applicable PUCT regulations significantly limit the extent to which we can apply normal commercial terms or otherwise seek credit protection from firms desiring to provide retail electric service in our service territory, and we thus remain at risk for payments related to services provided prior to the shift to another REP or the provider of last resort. A significant portion of our billed receivables from REPs are from affiliates of NRG and Vistra Energy Corp., formerly known as TCEH Corp. Our aggregate billed receivables balance from REPs as of December 31, 2017 was $215 million. Approximately 34% and 12% of this amount was owed by affiliates of NRG and Vistra Energy Corp., respectively. Any delay or default in payment by REPs could adversely affect our cash flows, financial condition and results of operations. If an REP were unable to meet its obligations, it could consider, among various options, restructuring under the bankruptcy laws, in which event such REP might seek to avoid honoring its obligations, and claims might be made by creditors involving payments we had received from such REP.

The AMS deployed throughout our service territory may experience unexpected problems with respect to the timely receipt of accurate metering data.

We have deployed an AMS throughout our service territory, which integrates equipment and computer software from various vendors to eliminate the need for physical meter readings to be taken at consumers’ premises, such as monthly readings for billing purposes and special readings associated with a customer’s change in REPs or the connection or disconnection of electric service. Unanticipated difficulties could be encountered during the operation of the AMS, including failures or inadequacy of equipment or software, difficulties in integrating the various components of the AMS, changes in technology, cyber-security issues and factors outside our control, which could result in delayed or inaccurate metering data that might lead to delays or inaccuracies in the calculation and imposition of delivery or other charges, which could have a material adverse effect on our results of operations, financial condition and cash flows.

Other Risk Factors Affecting Our Business

We are subject to operational and financial risks and liabilities arising from environmental laws and regulations.

Our operations are subject to stringent and complex laws and regulations pertaining to the environment. As an owner or operator of electric transmission and distribution systems, and the facilities that support these systems, we must comply with these laws and regulations at the federal, state and local levels. These laws and regulations can restrict or impact our business activities in many ways, such as:

• | restricting the way we can handle or dispose of wastes; |

9

• | limiting or prohibiting construction activities in sensitive areas such as wetlands, coastal regions, or areas inhabited by endangered species; |

• | requiring remedial action to mitigate environmental conditions caused by our operations, or attributable to former operations; and |

• | enjoining the operations of facilities with permits issued pursuant to such environmental laws and regulations. |

To comply with these requirements, we may need to spend substantial amounts and devote other resources from time to time to:

• | construct or acquire new facilities and equipment; |

• | acquire permits for facility operations; |

• | modify or replace existing and proposed equipment; and |

• | clean or decommission waste management areas, fuel storage facilities and other locations. |

Failure to comply with these laws and regulations may trigger a variety of administrative, civil and criminal enforcement measures, including the assessment of monetary penalties, the imposition of remedial actions, and the issuance of orders enjoining future operations. Certain environmental statutes impose strict joint and several liability for costs required to clean and restore sites where hazardous substances have been stored, disposed or released. Moreover, it is not uncommon for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by the release of hazardous substances or other waste products into the environment.

The recent trend in environmental regulation has been to place more restrictions and limitations on activities that may impact the environment, and thus there can be no assurance as to the amount or timing of future expenditures for environmental compliance or remediation, and actual future expenditures may be greater than the amounts we currently anticipate.

Our insurance coverage may not be sufficient. Insufficient insurance coverage and increased insurance costs could adversely impact our results of operations, financial condition and cash flows.

We currently have general liability and property insurance in place to cover certain of our facilities in amounts that we consider appropriate. Such policies are subject to certain limits and deductibles and do not include business interruption coverage. Insurance coverage may not be available in the future at current costs or on commercially reasonable terms, and the insurance proceeds received for any loss of, or any damage to, any of our facilities may not be sufficient to restore the loss or damage without negative impact on our results of operations, financial condition and cash flows.

In common with other companies in our line of business that serve coastal regions, we do not have insurance covering our transmission and distribution system, other than substations, because we believe it to be cost prohibitive and believe insurance capacity to be limited. In the future, we may not be able to recover the costs incurred in restoring our transmission and distribution properties following hurricanes or other disasters through issuance of storm restoration bonds or a change in our regulated rates or otherwise, or any such recovery may not be timely granted. Therefore, we may not be able to restore any loss of, or damage to, any of our transmission and distribution properties without negative impact on our results of operations, financial condition and cash flows.

We and CenterPoint Energy could incur liabilities associated with businesses and assets that we have transferred to others.

Under some circumstances, we and CenterPoint Energy could incur liabilities associated with assets and businesses we, CenterPoint Energy and CERC no longer own. These assets and businesses were previously owned by Reliant Energy, our predecessor, directly or through subsidiaries and include:

• | merchant energy, energy trading and REP businesses transferred to RRI or its subsidiaries in connection with the organization and capitalization of RRI prior to its initial public offering in 2001 and now owned by affiliates of NRG; and |

10

• | Texas electric generating facilities transferred to a subsidiary of Texas Genco in 2002, later sold to a third party and now owned by an affiliate of NRG. |

In connection with the organization and capitalization of RRI (now GenOn) and Texas Genco (now an affiliate of NRG), those companies and/or their subsidiaries assumed liabilities associated with various assets and businesses transferred to them and agreed to certain indemnity agreements of CenterPoint Energy entities. Such indemnities have applied in cases such as the litigation arising out of sales of natural gas in California and other markets (the last remaining case involving CenterPoint Energy is now on appeal, following the district court’s summary judgment in favor of CES, a subsidiary of CERC Corp.) and various asbestos and other environmental matters that arise from time to time. In June 2017, GenOn and various affiliates filed for protection under Chapter 11 of the U.S. Bankruptcy Code. In December 2017, GenOn received court approval of a restructuring plan and is expected to emerge from Chapter 11 in mid-2018. CenterPoint Energy, CERC and CES submitted proofs of claim in the bankruptcy proceedings to protect CenterPoint Energy’s indemnity rights. If any of the indemnifying entities were unable to meet their indemnity obligations or satisfy a liability that has been assumed in the gas market manipulation litigation, we, CenterPoint Energy or CERC could incur liability and be responsible for satisfying the liability.

In connection with our sale of Texas Genco, the separation agreement was amended to provide that Texas Genco would no longer be liable for, and we would assume and agree to indemnify Texas Genco against, liabilities that Texas Genco originally assumed in connection with its organization to the extent, and only to the extent, that such liabilities are covered by certain insurance policies held by us, and in certain of the asbestos lawsuits we have agreed to continue to defend such claims to the extent they are covered by insurance maintained by us, subject to reimbursement of the costs of such defense by an NRG affiliate.

Cyber-attacks, physical security breaches, acts of terrorism or other disruptions could adversely impact our reputation, results of operations, financial condition and/or cash flows.

We are subject to cyber and physical security risks related to adversaries attacking information technology systems, network infrastructure, technology and facilities used to conduct almost all of our business, which includes (i) managing operations and other business processes and (ii) protecting sensitive information maintained in the normal course of business. For example, the operation of our electric transmission and distribution system is dependent on not only physical interconnection of our facilities but also on communications among the various components of our system. This reliance on information and communication between and among those components has increased since deployment of smart meters and the intelligent grid. Disruption of those communications, whether caused by physical disruption such as storms or other natural disasters, by failure of equipment or technology or by manmade events, such as cyber-attacks or acts of terrorism, may disrupt our ability to conduct operations and control assets.

Cyber-attacks and unauthorized access could also result in the loss, or unauthorized use, of confidential, proprietary or critical infrastructure data or security breaches of other information technology systems that could disrupt operations and critical business functions, adversely affect reputation, increase costs and subject us to possible legal claims and liability. Further, third parties, including vendors, suppliers and contractors, who perform certain services for us or administer and maintain our sensitive information, could also be targets of cyber-attacks and unauthorized access. We are not fully insured against all cyber-security risks, any of which could adversely affect our reputation and could have a material adverse effect on our results of operations, financial condition and cash flows.

In addition, distribution and transmission facilities may be targets of terrorist activities that could disrupt our ability to conduct our business. In January 2017, the DOE’s Quadrennial Energy Review reported that cyber threats to the electricity system are increasing in sophistication, magnitude and frequency. Any such disruptions could result in significant costs to repair damaged facilities and implement increased security measures, which could have a material adverse effect on our results of operations, financial condition and/or cash flows.

Failure to maintain the security of personally identifiable information could adversely affect us.

In connection with our business we collect and retain personally identifiable information (e.g., information of our customers, suppliers and employees), and there is an expectation that we will adequately protect that information. The U.S. regulatory environment surrounding information security and privacy is increasingly demanding. A significant theft, loss or fraudulent use of the personally identifiable information we maintain, or of our data, by cyber-crime or otherwise could adversely impact our reputation and could result in significant costs, fines and litigation.

11

Our results of operations, financial condition and cash flows may be adversely affected if we are unable to successfully operate our facilities or perform certain corporate functions.

Our performance depends on the successful operation of our facilities. Operating these facilities involves many risks, including:

• | operator error or failure of equipment or processes, including failure to follow appropriate safety protocols; |

• | the handling of hazardous equipment or materials that could result in serious personal injury, loss of life and environmental and property damage; |

• | operating limitations that may be imposed by environmental or other regulatory requirements; |

• | labor disputes; |

• | information technology or financial system failures, including those due to the implementation and integration of new technology, that impair our information technology infrastructure, reporting systems or disrupt normal business operations; |

• | information technology failure that affects our ability to access customer information or causes us to lose confidential or proprietary data that materially and adversely affects our reputation or exposes us to legal claims; and |

• | catastrophic events such as fires, earthquakes, explosions, leaks, floods, droughts, hurricanes, terrorism, pandemic health events or other similar occurrences, which may require participation in mutual assistance efforts by us or other utilities to assist in power restoration efforts. |

Such events may result in a decrease or elimination of revenue from our facilities, an increase in the cost of operating our facilities or delays in cash collections, any of which could have a material adverse effect on our results of operations, financial condition and/or cash flows.

Our success depends upon our ability to attract, effectively transition, motivate and retain key employees and identify and develop talent to succeed senior management.

We depend on our senior executive officers and other key personnel. Our success depends on our ability to attract, effectively transition and retain key personnel. The inability to recruit and retain or effectively transition key personnel or the unexpected loss of key personnel may adversely affect our operations. In addition, because of the reliance on our management team, our future success depends in part on our ability to identify and develop talent to succeed senior management. The retention of key personnel and appropriate senior management succession planning will continue to be critically important to the successful implementation of our strategies.

Failure to attract and retain an appropriately qualified workforce could adversely impact our results of operations.

Our business is dependent on our ability to recruit, retain, and motivate employees. Certain circumstances, such as an aging workforce without appropriate replacements, a mismatch of existing skillsets to future needs, or the unavailability of contract resources may lead to operating challenges such as a lack of resources, loss of knowledge or a lengthy time period associated with skill development. Our costs, including costs to replace employees, productivity costs and safety costs, may rise. Failure to hire and adequately train replacement employees, including the transfer of significant internal historical knowledge and expertise to the new employees, or the future availability and cost of contract labor may adversely affect the ability to manage and operate our business. If we are unable to successfully attract and retain an appropriately qualified workforce, our results of operations could be negatively affected.

Climate change legislation and regulatory initiatives could result in increased operating costs and reduced demand for our services.

Regulatory agencies have from time to time considered adopting legislation, including modification of existing laws and regulations, to reduce GHGs, and there continues to be a wide-ranging policy and regulatory debate, both nationally and internationally, regarding the potential impact of GHGs and possible means for their regulation. Efforts have been made and continue to be made in the international community toward the adoption of international treaties or protocols that would address global climate change issues.

12

Following a finding by the EPA that certain GHGs represent an endangerment to human health, the EPA adopted two sets of rules regulating GHG emissions under the Clean Air Act, one that requires a reduction in emissions of GHGs from motor vehicles and another that regulates emissions of GHGs from certain large stationary sources. The EPA has also expanded its existing GHG emissions reporting requirements. These permitting and reporting requirements could lead to further regulation of GHGs by the EPA. Our electric transmission and distribution business, in contrast to some electric utilities, does not generate electricity and thus is not directly exposed to the risk of high capital costs and regulatory uncertainties that face electric utilities that burn fossil fuels to generate electricity. Nevertheless, our revenues could be adversely affected to the extent any resulting regulatory action has the effect of reducing consumption of electricity by ultimate consumers within our service territory. Likewise, incentives to conserve energy or use other energy sources could result in a decrease in demand for our services.

Climate changes could result in more frequent and more severe weather events which could adversely affect the results of operations of our business.

If climate changes occur, financial results from our business could be impacted. Another possible result of climate change is more frequent and more severe weather events, such as hurricanes or tornadoes. Since our facilities are located along or near the Gulf Coast, increased or more severe hurricanes or tornadoes could increase our costs to repair damaged facilities and restore service to our customers. When we cannot deliver electricity to customers or our customers cannot receive our services, our financial results can be impacted by lost revenues, and we generally must seek approval from regulators to recover restoration costs. To the extent we are unable to recover those costs, or if higher rates resulting from our recovery of such costs result in reduced demand for our services, our future financial results may be adversely impacted.

We are uncertain how the PUCT and local municipalities may require us to respond to the effects of the recent comprehensive tax reform legislation, and these regulatory requirements may adversely affect our results of operations, financial condition and cash flows.

On December 22, 2017, President Trump signed into law comprehensive tax reform legislation informally called the Tax Cuts and Jobs Act, or TCJA, which resulted in significant changes to federal tax laws effective January 1, 2018, including, but not limited to, a reduction in the corporate income tax rate.

Our federal income tax expense is included in the rates approved by the PUCT and local municipalities and charged to consumers. When we have general rate cases and other periodic rate adjustments, we expect the lower corporate tax expense resulting from the TCJA (which includes determining the treatment of EDIT), along with other increases and decreases in our revenue requirements, to be incorporated into our future rates. Nevertheless, regulators may require us to respond to the TCJA in other ways, including through faster recoveries of reductions in federal income tax expense, accounting orders to reflect a liability to return to customers in future rate proceedings, accelerated returns to consumers of previously collected deferred federal income taxes, increased funding of infrastructure upgrades, or offsets of future rate increases. The effect on us of any potential return of tax savings resulting from the TCJA to consumers may differ depending on how each regulatory body requires us to return such savings.

On January 25, 2018, the PUCT issued an accounting order in Project No. 47945 directing electric utilities, including us, to record as a regulatory liability (1) the difference between revenues collected under existing rates and revenues that would have been collected had the existing rates been set using the recently approved federal income tax rates and (2) the balance of EDIT that now exists because of the reduction in federal income tax rates. On February 13, 2018, we and other likely parties to a future rate case announced a settlement that requires us to make (i) a TCOS filing by February 20, 2018 to reflect the change in the federal income tax rate for our transmission rate base through July 31, 2017 and account for certain EDIT (and such filing was timely submitted), (ii) a DCRF filing in April 2018 to reflect the change in the federal income tax rate for our distribution rate base through December 31, 2017 and (iii) a full rate case filing by April 30, 2019. The settlement was presented to the PUCT during its open meeting on February 15, 2018. In response to the settlement, the PUCT did not proceed with a prior proposal to require us to file a rate case in the summer of 2018. The PUCT also amended its prior accounting order to remove the requirement that utilities include carrying costs in the new regulatory liability.

We can provide no assurances on how any regulatory body will ultimately require us to act. As such, we are currently unable to determine the impact of these potential regulatory actions in response to the enactment of the TCJA, which may adversely affect our results of operations, financial condition and cash flows.

In addition, the TCJA also includes a variety of other changes, such as a limitation on the tax deductibility of interest expense and acceleration of business asset expensing, among others. Several provisions of the TCJA are not generally applicable to the public utility industry, including the limitation on the tax deductibility of interest expense and the acceleration of business asset expensing.

13

We continue to assess the impact that the TCJA may have on our future results of operations, financial condition and cash flows, which impact may adversely affect our future results of operations, financial condition and cash flows.

Aging infrastructure may lead to increased costs and disruptions in operations that could negatively impact our financial results.

We have risks associated with aging infrastructure assets. The age of certain of our assets may result in a need for replacement, or higher level of maintenance costs as a result of our risk based federal and state compliant integrity management programs. Failure to achieve timely recovery of these expenses could adversely impact revenues and could result in increased capital expenditures or expenses.

The operation of our facilities depends on good labor relations with our employees.

We have entered into and have in place a collective bargaining agreement with a labor union. In 2016, we entered into a renegotiated collective bargaining agreement with the IBEW Local 66, which is scheduled to expire in 2020. Any failure to reach an agreement on a new labor contract or to negotiate this labor contract might result in strikes, boycotts or other labor disruptions. These potential labor disruptions could have a material adverse effect on our business, results of operations and/or cash flows. Labor disruptions, strikes or significant negotiated wage and benefit increases, whether due to union activities, employee turnover or otherwise, could have a material adverse effect on our business, results of operations and/or cash flows.

Our business will continue to have to adapt to technological change and may not be successful or may have to incur significant expenditures to adapt to technological change.

We operate a business that requires sophisticated data collection, processing systems, software and other technology. Some of the technologies supporting the industries we serve are changing rapidly and increasing in complexity. New technologies will emerge or grow that may be superior to, or may not be compatible with, some of our existing technologies, and may require us to make significant expenditures so that we can continue to provide cost-effective and reliable methods of energy delivery. Among such technological advances are distributed generation resources (e.g., private solar), energy storage devices and more energy-efficient buildings and products designed to reduce consumption. As these technologies become a more cost-competitive option over time, whether through cost effectiveness or government incentives and subsidies, certain customers may choose to meet their own energy needs and subsequently decrease usage of our systems and services.

Our future success will depend, in part, on our ability to anticipate and adapt to these technological changes in a cost-effective manner and to offer, on a timely basis, reliable services that meet customer demands and evolving industry standards. If we fail to adapt successfully to any technological change or obsolescence, fail to obtain access to important technologies or incur significant expenditures in adapting to technological change, or if implemented technology does not operate as anticipated, our business, operating results, financial condition and cash flows could be materially and adversely affected.

Our potential business strategies, including, merger and acquisition activities, may not be completed or perform as expected.

From time to time, we have made and may continue to make acquisitions of businesses and assets, including the formation of joint ventures. However, suitable acquisition candidates may not continue to be available on terms and conditions we find acceptable, or the expected benefits of completed acquisitions may not be realized fully or at all, or may not be realized in the anticipated timeframe.

Any completed or future acquisitions involve substantial risks, including the following:

• | acquired businesses or assets may not produce revenues, earnings or cash flow at anticipated levels; |

• | acquired businesses or assets could have environmental, permitting or other problems for which contractual protections prove inadequate; |

• | we may assume liabilities that were not disclosed to us, that exceed our estimates, or for which our rights to indemnification from the seller are limited; |

• | we may be unable to integrate acquired businesses successfully and realize anticipated economic, operational and other benefits in a timely manner, which could result in substantial costs and delays or other operational, technical or financial problems; and |

14

• | acquisitions, or the pursuit of acquisitions, could disrupt ongoing businesses, distract management, divert resources and make it difficult to maintain current business standards, controls and procedures. |

We are involved in numerous legal proceedings, the outcome of which are uncertain, and resolutions adverse to us could negatively affect our financial results.

We are subject to numerous legal proceedings, the most significant of which are summarized in Note 10 of our consolidated financial statements. Litigation is subject to many uncertainties, and we cannot predict the outcome of all matters with assurance. Final resolution of these matters may require additional expenditures over an extended period of time that may be in excess of established insurance or reserves and may have a material adverse effect on our financial results.

We are exposed to risks related to reduction in energy consumption due to factors including unfavorable economic conditions in our service territory, energy efficiency initiatives and use of alternative technologies.

Our business is affected by reduction in energy consumption due to factors including economic climate in our service territory, energy efficiency initiatives and use of alternative technologies, which could impact our ability to grow our customer base and our rate of growth. Declines in demand for electricity as a result of economic downturns in our regulated electric service territory will reduce overall sales and lessen cash flows, especially as industrial customers reduce production and, therefore, consumption of electricity. Although we are subject to regulated allowable rates of return and recovery of certain costs under periodic adjustment clauses, overall declines in electricity sold as a result of economic downturn or recession could reduce revenues and cash flows, thereby diminishing results of operations. Additionally, prolonged economic downturns that negatively impact our results of operations and cash flows could result in future material impairment charges to write-down the carrying value of certain assets, including goodwill, to their respective fair values.