Attached files

| file | filename |

|---|---|

| EX-31.1 - Coda Octopus Group, Inc. | ex31-1.htm |

| EX-32 - Coda Octopus Group, Inc. | ex32.htm |

| EX-14 - Coda Octopus Group, Inc. | ex14.htm |

| EX-10.36 - Coda Octopus Group, Inc. | ex10-36.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended October 31, 2017

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number: 001-38154

CODA OCTOPUS GROUP, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 34-200-8348 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification Number) |

| 7380 W. Sand Lake Road, Suite 500, Orlando, Florida 32819 |

(Address, Including Zip Code of Principal Executive Offices)

(801) 456-8684

(Issuer’s telephone number)

Securities registered under Section 12(b) of the Exchange Act:

COMMON STOCK, $0.001 PAR VALUE PER SHARE

Securities registered under Section 12(g) of the Exchange Act:

NONE

| ● | Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X] |

| ● | Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X] |

| ● | Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ] |

| ● | Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ] |

| ● | Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer or a smaller reporting company. |

| Large accelerated filer [ ] | Accelerated filer [ ] | |

| Non-accelerated filer [ ] | Smaller reporting company [X] |

| ● | Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X] |

| ● | State issuer’s revenues for its most recent fiscal year: $18,025,173 |

| ● | State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of April 30, 2017 representing the last business day of the registrant’s most recently completed second fiscal quarter: approximately $11,898,972. |

| ● | State the number of shares outstanding of each of the issuer’s classes of common equity, as of the latest practicable date: 10,262,273 as of January 29, 2018. |

TABLE OF CONTENTS

| 2 |

FORWARD-LOOKING STATEMENTS

This Form 10-K includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, which we refer to in this annual report as the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, which we refer to in this annual report as the Exchange Act. Forward-looking statements are not statements of historical fact but rather reflect our current expectations, estimates and predictions about future results and events. These statements may use words such as “anticipate,” “believe,” “estimate,” “expect,” “intend,” “predict,” “project” and similar expressions as they relate to us or our management. When we make forward-looking statements, we are basing them on our management’s beliefs and assumptions, using information currently available to us. These forward-looking statements are subject to risks, uncertainties and assumptions, including but not limited to, risks, uncertainties and assumptions discussed in this annual report. Factors that can cause or contribute to these differences include those described under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may vary materially from what we projected. Any forward-looking statement you read in this annual report reflects our current views with respect to future events and is subject to these and other risks, uncertainties and assumptions relating to our operations, results of operations, growth strategy and liquidity. All subsequent written and oral forward-looking statements attributable to us, or individuals acting on our behalf are expressly qualified in their entirety by this paragraph. You should specifically consider the factors identified in this annual report, which would cause actual results to differ before making an investment decision. We are under no duty to update any of the forward-looking statements after the date of this annual report or to conform these statements to actual results.

| 3 |

Overview

Coda Octopus Group, Inc. (“Coda,” “the Company,” or “we”) operates two distinct business segments. Its Products Segments designs and manufactures patented real time 3D sonar solutions and other leading products for subsea applications (“Products Segment” or “Marine Technology Business”). Its Services Segment supplies engineering services to prime defense contractors (“Services Segment” or “Engineering Business”) and focuses primarily on mission critical integrated defense systems that require a high level of reliability and quality controls.

The products sold by our Products Segment are used primarily in the underwater construction market, offshore oil and gas, offshore wind energy industry, complex dredging, port and harbor security, defense, mining both gems and deep sea minerals and marine sciences sectors. Our customers include service providers to major oil and gas companies, law enforcement agencies, government bodies (including maritime and navy organizations), ports, mining companies, defense companies, universities and research institutions.

Our Services Segment supplies engineering services primarily to prime defense contractors. We have been supporting a number of significant defense programs for over 30 years, such as the Raytheon Close in Weapons Program and Northrop Grumman’s Mine Hunting Systems Program and these programs are steadily growing. We also supply, upgrade and maintain proprietary parts to these programs on an ongoing basis. This business model ensures recurring and long tail revenues since we continuously supply parts to these programs.

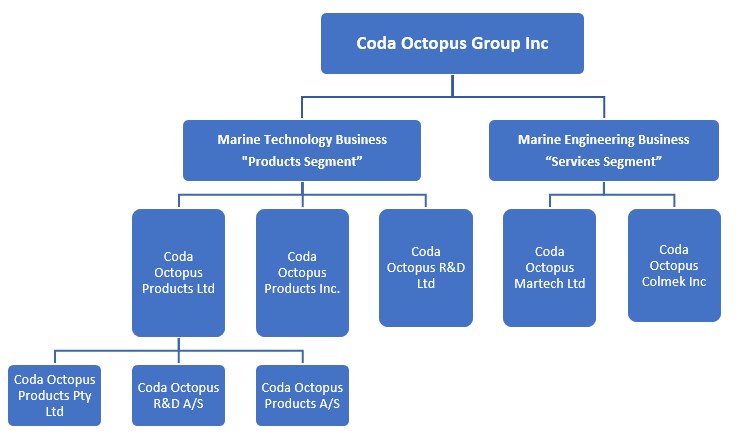

The Products Segment sells its products through our three wholly owned subsidiaries, Coda Octopus Products, Inc. (USA), Coda Octopus Products Limited (United Kingdom), and Coda Octopus Products Pty Limited (Australia) and through our appointed agents globally. The Products Segment also rents its equipment to customers. The Services Segment operates through our wholly owned subsidiaries, Coda Octopus Colmek, Inc. (“Colmek”) based in Salt Lake City, Utah, and Coda Octopus Martech Limited (“Martech”) based in the United Kingdom.

Our corporate structure is as follows:

Corporate History

The Company began as Coda Technologies Limited. This company now operates under the name Coda Octopus Products Limited, a United Kingdom corporation formed in 1994 as a start-up company with its origins as a research group at Herriot-Watt University, Edinburgh, Scotland. Initially, its operations consisted primarily of developing software for subsea mapping and visualization using sidescan sonar (a technology widely used in commercial offshore geophysical survey and naval mine-hunting to detect objects on, and textures of, the surface of the seabed).

| 4 |

In June 2002, we acquired Octopus Marine Systems Ltd, a UK corporation, and changed our name to Coda Octopus Limited. At the time of its acquisition, Octopus Marine Systems was producing geophysical products broadly similar to those of Coda, but targeted at the less sophisticated, easy-to-use, “work-horse” market. The Octopus Marine Systems acquisition led to the introduction of the Motion product (F180® series) into the Products Segment.

In December 2002, Coda Octopus Ltd acquired OmniTech AS, a Norwegian company, which became a wholly owned subsidiary of the Company. This company now operates under the name Coda Octopus R&D AS. OmniTech owned the patents to a “method for producing a 3-D Image” which was acquired under the acquisition. At the time of acquisition, this company had been engaged for over ten years in developing a revolutionary imaging and visualization sonar technology capable of producing real time three-dimensional (“3D”) underwater images for use in subsea activities. Coda Octopus Products Limited (Edinburgh) then developed the visualization software to control and display the images from the real time 3D sonar. This patented technology is now marketed by us under the name “Echoscope®”. This technology is superior to the other imaging sonars in the market as it generates real time 3D images of the underwater environment irrespective of low or zero visibility conditions and, unlike conventional sonars, can image a volume (as opposed to a slice of data) including moving objects subsea. This technology is covered by patents in a number of jurisdictions, including the USA. Currently, a substantial part of our R&D efforts is focused on further innovation and development of this technology. Some of the discriminators of this technology can be found in the table set out in the section below titled “Real Time 3D Sonar”.

This acquisition allowed the Company to expand its business activities to include the high-end sonar imaging and hydrographic survey markets. At the inception of the Marine Technology Business our revenues were generated solely from our geophysical software product. We subsequently added our motion sensors product (F180® series) in 2002 and our revenues were split over these two products. With the addition of our real time 3D products, our revenues from our Products Segment are now mainly generated from our real time 3D sonar products including accessories and associated services.

On July 13, 2004, the Company effected a reverse merger pursuant to the terms of a share exchange agreement between The Panda Project, Inc. (“Panda”), a Florida corporation, and a now defunct entity affiliated with Coda Octopus Ltd. (“Coda Parent”). Panda acquired the shares of Coda Octopus Limited, a UK corporation and wholly-owned subsidiary of Coda Parent, in consideration for the issuance of a total of 1,432,143 shares of common stock to Coda Parent and other shareholders of Coda Octopus Limited. The shares issued represented approximately 90.9% of the issued and outstanding shares of Panda. The share exchange was accounted for as a reverse acquisition of Panda by Coda. Subsequently, Panda was reincorporated in Delaware and changed its name to Coda Octopus Group, Inc.

In June 2006, we acquired a UK design and engineering company, Martech Systems (Weymouth) Ltd (“Martech”), which provides bespoke engineering solutions in the fields of electronic data acquisition, transmission and recording. Martech are suppliers to prime defense contractors, among others. Martech changed its name to Coda Octopus Martech Limited in December 2008. This company is part of our Services Segment.

In April 2007, we acquired Colmek (then Miller & Hilton Inc. d/b/a Colmek), a Utah corporation and custom engineering service provider of mission critical integrated systems to defense engineering prime contractors where a high level of reliability and quality is required. Colmek has been supporting a number of defense programs since the early 1990’s. Specifically, it supplies proprietary parts into these programs including providing upgrades to such parts to address either obsolescence issues or advancement in technology. This entity changed its name to Coda Octopus Colmek Inc. in December 2008. This company is part of our Services Segment.

In January 2017, we effectuated a one for fourteen reverse split of our issued and outstanding common stock. Throughout this document, all share numbers have been adjusted for the reverse stock split.

Coda Octopus Group, Inc., is organized under the laws of the State of Delaware as a holding company that conducts its business through subsidiaries, several of which are organized under the laws of foreign jurisdictions, including England, Scotland, Norway, Denmark and Australia. This may have an adverse impact on the ability of U.S. investors to enforce a judgment obtained in U.S. courts against these entities, or to effect service of process on the officers and directors managing the foreign subsidiaries.

| 5 |

Marine Technology Business (“Products Segment”)

Our Marine Technology Business sells and rents proprietary marine products in a number of worldwide market segments including:

| ● | Commercial marine geophysical survey; | |

| ● | Marine and Port Construction | |

| ● | Offshore Energy and Renewables | |

| ● | Defense | |

| ● | Oil & gas | |

| ● | Security and Law Enforcement | |

| ● | Environmental Applications (for example mammal research, natural gas seeps, habitat assessment, and fisheries) | |

| ● | Salvaging and decommissioning applications |

In the commercial marine geophysical survey sector, our products include geophysical data acquisition systems, analysis software and motion detection equipment that are used primarily by survey companies, research institutions and salvage companies.

In the imaging sonar sector, we believe we possess an important and unique patented sonar technology based upon more than 20 years of research and development. This gives us a significant advantage over our competitors in the subsea imaging sonar market sectors. We believe that our real time 3D sonar products are revolutionizing the sonar market, especially in the following areas:

| (A) | Real time three-dimensional visualization; | |

| (B) | Imaging of moving objects (such as blocks, mattresses, subsea structures or installations being placed or landed on the seabed, subsea vehicles, diver support or other objects); | |

| (C) | Imaging of complex subsea structures (imaging a volume as opposed to a slice of data); | |

| (D) | Providing situational awareness in real time to divers in low or zero visibility conditions; | |

| (E) | Real time threat identification and navigation and obstacle avoidance; | |

| (F) | Simultaneous mapping and imaging of moving objects using a single sensor; | |

| (G) | Imaging or visualizing subsea environments in low or zero visibility conditions; and | |

| (H) | Single sensor for multiple applications. |

Our product range includes equipment based on our patented Echoscope® technology and a range of complementary 3D accessories in combination with our proprietary software which also includes patented techniques for rendering and tracking.

Over the years we have significantly advanced our research and development with respect to both hardware and software components of our real time 3D sonar technology and have filed further patents and have increased our market share for imaging sonars. Our third generation of products include the Echoscope® and other derivatives such as CodaOctopus® Underwater Inspection System (UIS), our forward looking sonar, Dimension® and our Echoscope® C500 and more recently our Echoscope® XD variant.

At present we are focusing on developing our fourth generation (“4G”) of real time 3D sonar solutions for various market applications and varying price points. Our 4G products will be aimed at expanding our market share by introducing more applications-focused products. In respect of our 4G of products, we are pursuing a 18-24 months’ roll out plan. In this connection, on January 16, 2018 we launched the first product within our 4G series of real time 3D sonars. This first product is approximately 50% lighter, 40% smaller and requires 30% less power than the 3G generation of products. This product is now marketed under the name of Echoscope4G® Surface and is a shallow water system (for deployments and applications not exceeding 20 meters water depth). We believe this is a significant achievement as it potentially paves the way for more market applications for the technology and potentially increases our market share of imaging sonars.

| 6 |

We believe that the development strategy of our 4G products will help to standardize real time 3D solutions in the subsea market and grow the number of applications for this technology. However, these are complex products and we can give no assurance that we will be successful in realizing commercially viable products or that our goals of increasing our market share will be realized.

We believe that our patented technology is superior in its capability to the current sonars on the market including the multibeam which is the standard technology currently used, as it can generate real time 3D volumetric imaging data of underwater environments (including real time threat identification) and image moving objects in the water column even in the most challenging water conditions. This unique and superior capability provides unparalleled underwater scene awareness in high frame rates similar to cameras. The resultant scene data can be used for multiple tasks simultaneously including object detection and avoidance in true 3D, complex scene mapping and augmented reality 3D workspace imaging combining the real time 3D data with 3D models. This enables real time assessment and decision making. This technology is changing the work flow processes for a number of applications and delivering significant productivity gains and health and safety improvements to our customers, particularly in applications requiring imaging moving objects (either their placement or removal from the sea bed), conducting subsea operations in low or zero visibility conditions and therefore preventing downtime (with the associated costs for such downtime) in these projects and providing real time 3D measurements. Some of our customers are reporting productivity gains of as much as 5000% in block placements for breakwater and other types of projects.

The Echoscope® has a wide range of applications including:

| ● | inspection of harbor walls; | |

| ● | inspection of ship hulls; | |

| ● | inspection of bridge pilings; | |

| ● | block placements (in the context of breakwater construction); | |

| ● | subsea asset placements including landings; | |

| ● | deep sea mineral mining and shallow water gem mining; | |

| ● | cable laying and cable pull in operations in offshore wind energy applications; | |

| ● | inspection of offshore installations such as gas and oil rigs and wind turbines; | |

| ● | Remotely Operated Vehicle (ROV) navigation (obstacle avoidance); | |

| ● | Autonomous Underwater Vehicle (AUV) navigation and target recognition (obstacle avoidance); |

| 7 |

| ● | construction - pipeline touchdown placement and inspection; | |

| ● | bathymetry (measurement of water depth to create 3D terrain models); | |

| ● | managing underwater construction tasks; | |

| ● | underwater intruder detection; | |

| ● | contraband detection; | |

| ● | locating and identifying objects located underwater including mines; | |

| ● | detection and study of individual species in real time 3D (fish, whales etc.); | |

| ● | oil and gas leak detection; | |

| ● | fish school detection and analysis; | |

| ● | diver tracking and guidance; | |

| ● | underwater archaeological and salvage site mapping; | |

| ● | salvaging and decommissioning; | |

| ● | harbor construction – concrete armoring; and | |

| ● | unexploded ordinances survey and intervention. |

The technology enables real time 3D visualization of static scenes or moving objects from either a static location or a dynamically moving platform vessel (Autonomous Underwater Vehicle (“AUV”), Remotely Operated Vehicle (“ROV”)) or a surface vessel. Conventional sonars are capable of producing maps of static scenes only without the ability to image moving objects. A significant part of subsea activities consists of identifying moving objects including whether they may pose a threat.

The Echoscope® technology is protected by patents, including a number of complementary patents such as a patent which covers our visualization methodology and our rendering of real time 3D images. For example, one of our recently awarded patents provides for a new method of using multiple sonar images to produce in real time 3D a highly detailed image with sharply defined edges while intelligently discarding “noise” in the image produced by passing fish or floating debris.

Sales and Marketing

We market the Echoscope® both as a stand-alone sonar device and as a fully integrated system, which we market under the name “CodaOctopus® UIS (Underwater Inspection System)”. This latter system is specifically aimed at the port security market and has been adopted by a significant number of ports in the United States. Since 2015 we built upon our success in selling in excess of 30 Underwater Inspection Systems to ports in the USA by selling a number of systems to an East Asian government agency for use in salvage operations and port and harbor inspection. Our 4G of products which will be smaller, lighter, with less power requirements will present a new opportunity to introduce a new UIS with a lower price point, thus presenting the opportunity to increase the number of ports investing in this equipment.

| 8 |

We also operate a rental model under which we rent our technology with associated services. The equipment is typically supplied with our expert engineers who either train our customers or become the operators of the equipment for our customers for the duration of the project. The rental option represents an increasingly important market and also provides access to the technology to a broader range of end users who typically do not purchase equipment such as large oil companies whose business model is to rent or lease equipment.

We have an internal sales and marketing team which is engaged in marketing and selling this technology; we also have a network of sales agents.

Products

Our products are marketed under the “CodaOctopus®” brand and consist of three main product lines:

Data Acquisition Products includes integrated hardware acquisition devices that feature rich post-processing software for all levels of geophysical survey work, with which we commenced our operations in 1994.

Motion Sensing Products consists of a range of GPS-aided precision attitude and positioning systems and software for all types of marine survey and positioning work.

Real Time 3D Sonar includes our unique and patented real time 3D imaging sonars (Echoscope®) and cutting-edge software (including patented techniques for rendering and tracking algorithms) that we believe is shaping the future of subsea operations both within the commercial and defense sectors.

Real Time 3D Sonar

We believe that our real time 3D imaging sonar technology represents the Company’s most promising area for growth in the medium term. Some of the key differentiators of our technology compared to other imaging sonar technologies on the market are:

| No. | Description of Differentiator | |

| 1. | Real time 3D imaging sonar providing true first-person perspective visualization subsea; | |

| 2. | Real time 3D volumetric images of the underwater environment being imaged; | |

| 3. | Real time 3D volumetric images irrespective of low or zero visibility conditions prevailing at sea; | |

| 4. | Due to the shape of our beams which has width and height capability we can have almost 100% coverage of a subsea object/target with a single pass of the object/target being imaged. Current sonars in the market require multiple passes to be able to create a comprehensive image of the object or target – making this costly and inefficient; | |

| 5. | Real time 3D images of both moving objects and static volumetric scenes in the water. Conventional sonars, such as the multibeam, can only produce static images (mapping); | |

| 6. | No requirement for post-processing images generated by our technology (since it is a real time 3D imaging sonar) thus reducing the costs associated with these activities; | |

| 7. | Real time identification of threats including small target detection and visualizing moving projectiles and their targets in the water column. We can also accurately and repeatedly guide projectiles onto targets; | |

| 8. | Real time automated and manual 3D measurements of subsea objects and targets; | |

| 9. | Crisp and easy to interpret photograph-like images of subsea target thereby deskilling many areas of work in the subsea environment by enabling persons without a hydrographic background to perform subsea tasks (such as law enforcement officers and crane operators); | |

| 10. | Real time image in any orientation including forward looking for obstacle and collision avoidance at sea; |

| 9 |

| 11. | Map complex underwater environments and structures with very high coverage confidence in a fast and efficient manner. Conventional sonars suffer from significant shadows when imaging complex structures; and |

| 12. | Discern with greater degree of confidence real subsea targets versus subsea noise and other moving objects, such as fish, bubbles, gas etc. |

Our current third-generation product line consists of five products within the real time 3D sonar series:

| ● | Echoscope®; | |

| ● | Echoscope® C500 (launched in 2014); | |

| ● | Echoscope® XD (launched in January 2017); | |

| ● | Dimension®(launched in 2013); and | |

| ● | CodaOctopus® Underwater Inspection Systems (“UIS”). |

These products are used either by mounting on a surface vessel, cranes, excavators, underwater vessels such as remotely operated vehicles (ROV) or autonomous underwater vehicles (AUV), mining crawlers and the like.

Echoscope®

This is the first real time 3D sonar we brought to the market. We have variants rated at 300 meters, 600 meters and 3,000 meters which means these systems are fit to operate at this water depth at sea. We have also developed bespoke sonars which operates at 4,000 meters for a prime defense contractor’s autonomous underwater vehicle (“AUV”). The 3G Echoscope weighs 52 pounds and is around 15x11.8x6.3 inches in size. This is sold with software (see section below for various software options).

Due to the current price, size, weight and power requirements to operate the Echoscope, there are a number of applications or markets for which we do not supply this product. However, see section on Fourth Generation (“4G”) of Sonar Products, where these limitations are being addressed.

Dimension®

This product was launched in 2013 and is aimed at the remotely operated underwater vehicle market (“ROV”) for navigation and obstacle avoidance underwater with a wider field of view and is suitable for applications which require safe navigation from one location to the next and real time forward looking 3D imaging of any underwater scene. Based on our patented Echoscope® technology and our Vantage software, we believe that the Dimension® product provides unparalleled real time visualization for subsea vehicle applications. Designed for a wide range of ROVs, the Dimension® sonar is a unique, real time 3D sonar that transforms ROV underwater operations.

Echoscope® C500 (“C500”)

The C500 was launched in 2014 and is based on our patented Echoscope® technology. This sonar device delivers real time 3D sonar capability and is targeted at the ROV and autonomous underwater vehicle (“AUV”) applications.

Echoscope® XD (“XD”)

Many applications require a wide area of view for imaging or visualization subsea. Our standard Echoscope® offers viewing angles of up to 50° x 50°. The XD was launched in 2017, is based on our patented Echoscope® technology and delivers real time 3D sonar capability. This latest product delivers a wider area of view (or, imaging area) – up to 90° x 44°. We believe that this will open the Echoscope® to a number of new applications including bathymetry survey applications. The new capability can also be accessed by users of the current Echoscope® by purchase of an upgrade package.

Software Products

Our Software development capability is an important part of the success we have achieved to date with our real time 3D solutions and forms an important part of our strategy to maintain our lead in designing, manufacturing and selling real time 3D solutions.

Our software products are sold in combination with our real time 3D sonar solutions as a one-time purchase by our customers. During the first 12 months, the customer benefits from our support services. However, after the first year, should the customer need ongoing support services this is purchased as an annual subscription service which entitles the customer to 24x7x365 telephone, email and remote dial in support and minor software upgrades. In addition, where we issue major releases of our software (as opposed to minor releases (maintenance release)), this is a chargeable option for our customers.

| 10 |

The current software packages that we offer with our hardware (real time 3D sonar) are:

| ● | Underwater Survey Explorer” (“USE”); | |

| ● | Vantage; and | |

| ● | Construction Monitoring System (“CMS”). |

These are all Software Packages developed by the Company.

Our software packages are feature rich and includes patented techniques in a number of our modules. In general, our software package contain significant capabilities that are designed to address specific subsea challenges by application particularly in the context of a dynamic subsea setting (as opposed to a static mapping of the seabed as is typical for conventional sonar technology). Some of our unique features include:

| Feature Description | Functionality | |

| Real Time Measurements | important for many types of subsea operations such as block or asset placements or aiding diving operations; | |

| Models + Software Module | allows the user to import existing models and engineering drawings into the real time subsea environment; | |

| Edge Detection Algorithm | allows the user to superimpose an edge to easily identify a subsea target; | |

| Rendering a Noise Free Image | allows for a crisp, clear and high-resolution photo-like image without any processing (which would be required for conventional sonars); and | |

| Tracking Algorithm | Algorithm is used to track known objects within the real time 3D Data. This is currently utilized in our Construction Monitoring Software Package (see below) |

The Echoscope® and Construction Monitoring Software (CMS) have important applications for breakwater construction. Our CMS package has been recently updated to include patented algorithms for tracking and placement of single layer armor blocks used in breakwater construction.

We believe that our technology is becoming the preferred solution for subsea block placements in breakwater solutions because it allows crane operators to visualize in real time the moving blocks and tracking these into their placement position accurately. We believe that our solution has significantly simplified and made safer this area of the workflow process in breakwater construction. It has also increased significantly the lay-rate for blocks being placed with customers reporting up to 5000% increase in productivity.

We are not aware of competing technologies that offer real time 3D visualization and monitoring of subsea construction sites including previously laid blocks. In addition, the feature rich software package (CMS) which allows the complete workflow for breakwater construction to be planned within the software, greatly reduces project risks and timing while improving the quality of the projects. Furthermore, the patented tracking algorithms that have recently been enhanced and strengthened to provide opportunity for additional applications involving placing known objects or structures underwater.

We generate around 87% of our revenues in the Products Segments from our real time 3D sonar products (hardware and software). With the launch of the new products we would anticipate our revenues from this line to increase over time.

Fourth Generation (4G) Real Time 3D Sonar Products

During the last 18 months, we have invested a significant part of our research and development resources on developing our 4G real time 3D solutions for various market applications and varying price points. We expect to roll out this technology over the next 18-24 months.

| 11 |

Echoscope4G® Surface

On January 16, 2018 we launched the first product within our 4G series of real time 3D sonars, the Echoscope4G® Surface. This first product within our 4G range is 50% lighter, 40% smaller and requires 30% less power than our third generation of products. This allows us to compete more effectively against other conventional sonars within this price bracket and applications where size, weight and price are key factors. This product is suitable for shallow water applications only and is now available for customer trials, rental, licensing or outright purchase. Introduction of this product potentially paves the way for more market applications for the technology and potentially increases our market share of imaging sonars. Nevertheless, we can give no assurance that following launch we will be successful with this product.

Data Acquisition

We started our business in 1994 designing and developing the CodaOctopus® GeoSurvey software package. For over two decades, our GeoSurvey has been an industry leading software package on the market for data acquisition and interpretation and provides feature rich solutions and productivity enhancing tools for the most exacting survey requirements. Designed specifically for sidescan and sub-bottom data acquisition, CodaOctopus® GeoSurvey has been purchased by numerous leading survey companies throughout the world. This product range includes:

CodaOctopus® GeoSurvey Acquisition Products

These consist of a range of hardware and software solutions for field acquisition of sidescan sonar and sub-bottom profiler, which includes analogue and digital interfaces compatible with all geophysical survey systems. This is our original product range that includes the following products:

DA4G - 500, Sidescan sonar and sub-bottom profiler simultaneously

DA4G - 1000, Sidescan sonar and sub-bottom profiler separately

DA4G - 2000, Sidescan sonar or sub-bottom profiler

CodaOctopus® GeoSurvey Productivity Suite

This consists of an integrated suite of software that automates the tasks of analyzing, annotating and mosaicing complex data sets, thus ensuring faster and more precise results.

CodaOctopus® Instruments

These consist of simple, solid and robust solutions for sidescan sonar and sub-bottom profilers. Used throughout the world by leading survey companies, navies and academics, CodaOctopus instruments are ideal where minimal training and simple installation and set-up is paramount. Coupled with intuitive but powerful post processing software, the Octopus range meets the requirements of survey applications from the smallest inshore survey, rapid deployment naval reconnaissance to large scale site investigations. This product range comprise our DA4G series of acquisition systems which provide high quality, robust and reliable data acquisition from the latest digital and analogue sidescan sonar and sub-bottom profiler sensors.

DA4G™ is the 4th generation of our successful DA series and is built on twenty years of knowledge, experience and innovation in supplying unparalleled products and service to the worldwide geophysical survey sector. These purpose-built, turn-key, systems incorporate the very latest hardware specifications and are designed and delivered to meet the demanding nature of offshore survey work.

The DA4GTM range consists of a number of options and is backed (like all our products) with global service and support.

We generate around 5% of our revenues from the Products Segments from this range of products. With the launch of the new products we would anticipate our revenues from this line to increase over time.

| 12 |

Motion Sensing Products

Our F180® (and the more recently introduced CodaOctopus F170TM families) have been developed for the marine environment and is based on technology originally developed for the extreme world of motor racing. Modifications and enhancements have resulted in a simple-to-use, off-the-shelf product that brings accurate positioning and motion data into extreme offshore conditions for precision marine survey applications worldwide. Variants within the F180® series include the F190™, exclusively configured for use ‘inland’, e.g. within ports and harbors, and the F185™, with enhanced precision positioning to 2 cm accuracy (<1”). Octopus iHeave, an intelligent software product for dealing with long period ocean swell compensation, is fully integrated within the F180® series.

The F170™ family is designed with ease of use in mind. They are compact, simple to install and produce accurate position and motion data for the marine industry. Two product variants are available: the F170™ and the F175™. The F175™ allows integration of third-party GNSS systems thus enhancing the accuracy of the outputs and improving the robustness of the solution.

Our Motion Sensing Products are sold alone or in conjunction with our real time 3D sonars. We are currently expending a significant amount of our resources in developing the next generation of our motion sensors. Our newly developed suite of products will focus on expanding the market into which we sell these devices, including the AUV market which is an expanding market for our products in general.

We are aiming to launch our fourth-generation of Motion Sensing Products in March 2018. The new hardware motion sensing products will be based on more advanced technology and new software.

We generate around 8% of our revenues from the Products Segments from our Motion Sensing Products. With the launch of the new products we anticipate our revenues from this line to increase over time.

Coda Octopus Products Limited has the requisite accreditation for its business including LRQ accredited to ISO 9001:2008.

Marine Engineering Businesses (“Service Segment”)

Our Marine Engineering Businesses encompass:

| ● | Coda Octopus Colmek, Inc., a company incorporated under the laws of Utah with its principal place of business in Salt Lake City; and | |

| ● | Coda Octopus Martech Limited, a company incorporated under the laws of England & Wales with its principal place of business in Portland, England. |

These two operating entities supply mission critical integrated systems, test equipment, instrumentation and the like primarily to the defense sector where high levels of reliability and quality are essential pre-requisites for securing and maintaining these agreements with their customers. Typically, in the first instance we prototype products for these customers and after going through various acceptance tests, including first article inspection approvals, we are given the production contracts. Many of these production contracts have repeat orders profile which typically follows the life cycle of the defense program that is using the production part.

These arrangements often give us long term preferred/sole supplier status, technology refresh and obsolescence management for such customers and we generally use these long-standing relationships to win more contracts with these customers.

In addition, we are increasingly combining our engineering capabilities with our product offerings. This enables us to offer systems which are complete with installation and support and maximize the utilization of our collective expertise to advance our real time 3D technology.

Coda Octopus Martech Limited (“Martech”)

Martech operates in the specialized niche of bespoke design and manufacturing services mainly to the United Kingdom defense and subsea industries. Its services are provided on a custom sub-contract basis where high quality and high integrity devices are required in small quantities. Martech has the requisite accreditation for its business including LRQ accredited to ISO 9001:2008.

An example of Martech’s design and engineering services is the development of a ruggedized display unit in military vehicles capable of displaying variables such as wind speed, air temperature and humidity independent of the vehicle’s computer.

In late 2010 Martech was awarded a significant contract to design and build two pre-production decontamination units the successors of which have been designated as part of the ground equipment for a major international military aircraft program. The Company has since started production of these units which form part of the standard ground equipment for this military aircraft.

| 13 |

Martech is one of the first suppliers bringing to the market controllers for fire sprinkler systems which periodically test the associated pumps. Sprinkler systems are now required to be introduced in certain larger domestic buildings under UK legislation. Martech is a market leader in this market and in late 2017 was awarded a contract by a leading global pump manufacturer for approximately $650,000.

The Company enjoys pre-approvals to allow it to be short-listed for certain types of government contracts. Much of the more significant business secured by Martech is through the formal government or government contractor tendering process. Government contracts may be terminated at any time at the discretion of the government. If the government does terminate a contract, the Company is allowed to recover the costs incurred up to the date of termination. During the last few years, only one non-material government contract was terminated for convenience.

Martech is a key supplier of various parts to our marine products business and has been assisting in the further development of a number of those products.

Coda Octopus Colmek, Inc. (“Colmek”)

Colmek is a service provider of defense engineering solutions, particularly in the fields of data acquisition, storage, transmission and display. It has grown and diversified since beginning its operations in 1977 and now provides services and products to a wide range of defense, research and exploration organizations in the United States. Colmek has the requisite accreditation for its business including LRQ accredited to ISO 9001:2008.

Colmek designs, manufactures and supports systems that are reliable and effective in multiple military and commercial applications where ruggedness and reliability under extreme operational conditions are paramount and where lives depend on accurate and precise information.

Colmek has long standing relationships with a number of prime defense contractors and has been supporting a number of defense programs for over 30 years including the Close in Weapons Support Program (CIWS) for which it supplies proprietary parts and services and technical refresh programs for these parts. As a result, Colmek has repeat revenues from these long-standing programs. Colmek continues to expand the number of established programs into which it supplies proprietary parts.

In June 2014 Colmek completed the acquisition of the Thermite® which is a rugged visual mission computer line and the Sentiris® AV1 XMC video card for $1,100,000 in cash. Colmek also acquired hardware, Thermite stock, and other intellectual property rights (such as software code and trademarks pertaining to these products).

The Thermite® Product fits within established programs with Department of Defense (“DoD”) prime contractors and benefits from being a single source product under this program. Customers for this item include the US Army, Benchmark, and Endeavor Robotics Defense and Security Division. Since acquiring these two products in 2014, we have received orders in excess of $2,500,000.

Thermite® Rugged Visual Computers

| ● | Rugged, graphics-based PCs designed to perform in the most brutal environmental conditions; | |

| ● | Focus on graphics-based high-performance computing with integrated accelerated video capture capability; | |

| ● | Lightweight, power efficient and conduction-cooled; | |

| ● | Three models, optimized for man-wearable, vehicle, and airborne platforms; and | |

| ● | Programs include dismounted soldier training, mission rehearsal, real time imaging, robotic control, weapon system control, sensor processing and display. |

| 14 |

We are now designing and developing the next generation of the Thermite® and expect to re-engage the existing customer base for this product.

Sentiris® AV1 XMC

| ● | FPGA-based PCI Express Mezzanine Card designed for video and graphics processing applications; and | |

| ● | Targeted platforms include MH-47G helicopters, MH-60M Blackhawk helicopters, MC-130H Combat Talon II and CV-22 Tilt-Rotor aircraft. |

Since acquiring the Sentiris®, we have successfully completed the first article inspection (“FAI”) approval phase and are now in the production phase. We have received orders for approximately $700,000 since completion of the FAI process.

This is expected to be a significant new product as this program is funded and there will be ongoing demand for this product over the life of the program.

Stinger™ family of Rugged Small-Form-Factor PCs

The Stinger 1000 is a unique rugged computer that provides a cost-effective solution for harsh mobile computing environments. Utilizing PC-104 architecture and employing creative ruggedization, Colmek has engineered a stable platform which is easily tailored to any application.

The Stinger 1000 rugged mobile computer is highly customizable, presenting an inspiring assortment of selectable attributes. The stinger mobile computer is engineered to meet military requirements. Colmek has successfully deployed Stinger products on Unmanned Aerial Systems (UAS), and shipboard for satellite-based tracking systems.

RhinoTuff™ family of Rugged Touch Screen Computers

The robust RhinoTuff™ rugged touch screen computer is built exclusively for reliable operation in the world’s harshest environments. It is modular and user-definable affording maximum flexibility. This all-weather, all terrain, all-in-one PC thrives in a field where the average “tough” computer is simply not tough enough, including, mining and construction sites, oil fields, marine environments, and military battlefields.

Rugged Chassis/Enclosures

The chassis and enclosures offered by Coda Octopus Colmek are fully customizable to military/industrial needs. Colmek is a key supplier on high profile programs including Raytheon’s Phalanx Close-In Weapons System (CIWS) and Northrop Grumman’s airborne mine hunting sonar AN/AQS-24. We also offer a variety of enclosures technologies.

Other products offered by Colmek include subsea telemetry & data acquisition systems, rugged workstations, analog-to-digital converters and rugged LCD displays.

Competition

In our Products Segment, we are exposed to the following competitive challenges:

Data Acquisition Products

The sonar equipment industry is fragmented with several companies occupying niche areas, and we face competition from different companies with respect to our different products. In the field of geophysical products, Triton Imaging Inc., a US-based company, now part of the ECA Group (Toulon, France), Chesapeake, a US-based company, and Oceanic Imaging Consultants, Hawaii, USA, dominate the market with an estimated of 25% each of world sales, while we believe that we control approximately 5% of world-wide sales.

| 15 |

Motion Sensing Products

In the field of motion sensing equipment, where our product addresses a small part of the overall market, we believe that we have four principal competitors: TSS (International) Ltd in Watford, England which is focused on the mid-performance segments with about 25% of the world market; Ixsea, a French company which covers all segments, with about 20% of the market; Kongsberg Seatex, a Norwegian company (part of Kongsberg Gruppen) which has products across all segments, with about 15% of the market; and Applanix, a Canadian company, now part of Trimble which has one major product focused on the high end of the market, with about 20% of the market. We believe that our market share in the field of motion sensing equipment is only about 5%. This market is fiercely competitive and with the advancement of technology, there are new entrants to the market such as SBG Systems (a French based manufacturer of motion sensors). Due to the price pressure in this market, we are selling our products more in conjunction with our real time 3D sonars than on a standalone basis.

Real Time 3D Sonar

In the field of Real Time 3D imaging, we are unaware of other companies offering a similar product. The entry into this market is dependent upon specialized marine electronics, acoustic and software development skills. The learning curve, which has resulted in the advancement of our real time 3D sonar device, is the culmination of two decades of research and development into this field. We are aware of a number of high profile and substantial competitors’ real time 3D projects that have failed. Over the last several years there have been lower grade sonars entering the market for 3D imaging. Companies such as Tritech International Ltd., United Kingdom, BlueView Technologies Inc., USA (now a part of Teledyne Technologies Incorporated), and Norbit Group AS Norway are examples, but none of these sonar offerings are directly comparable or competitors in respect of our real time 3D solutions. Specifically, we believe that they do not have the same capabilities as our patented Echoscope® technology in terms of generating real time 3D images of submerged objects and environments in low or zero visibility conditions. However, Teledyne has in the last four years acquired a significant number of subsea companies (examples are Reson and BlueView) along with expertise. Teledyne has much greater resources and liquidity than the Company. We therefore can give no assurance that companies such as these will not enter this market.

We seek to compete on the basis of producing high quality products employing cutting edge technology that is easy to use by operators without specialized skills in sonar technology. We intend to continue our research and development activities to continually improve our products, seek new applications for our existing products and to develop new innovative products.

In our Services Segment, we are exposed to the following competitive challenges:

Marine Engineering Businesses

Through our marine engineering operations, Coda Octopus Colmek, Inc. and Coda Octopus Martech Limited, we are involved in custom engineering for the defense industry in the United States and in the United Kingdom. Martech competes with larger contractors in the defense industry. Typical among these are Ultra Electronics, BAE Systems, and Thales, all of whom are also partners on various projects. In addition, the strongest competitors are often the clients themselves. Because of their size, they often have the option to proceed with a project in-house instead of outsourcing to a sub-contractor like Martech or Colmek.

Intellectual Property

Our product portfolio and technologies are protected by intellectual property rights including trademarks, copyrights and patents. We have a number of fundamental patents including a patent covering the stitching together of acoustic imagery. This covers the real time acoustic image generation element of what we do, and we believe it provides us with a competitive advantage.

Patents

Our patented inventions along with our strategy to enhance these inventions are at the heart of the Company’s strategy for growth and development.

| 16 |

Our patent portfolio consists of the following:

| Patent Number | Description | Expiration Date | ||

| US Patent No. 6,438,071 | Concerns the “Method for Producing a 3-D Image” and is also recorded in the European Patents Register #EP 1097393 B1; Australia #55375/99 and Norway #307014. This patent relates to the method for producing a 3D image of a submerged object, e.g. a shipwreck or the sea bottom. | June 1, 2019 | ||

| US Patent No. 6,532,192 | Concerns “Subsea Positioning System and Apparatus” | July 1, 2019 | ||

| US Patent No. 7,466,628 | Concerns a “Method of constructing mathematical representations of objects from reflected sonar signals.” | August 15, 2026 | ||

| US Patent No. 7,489, 592 | Concerns a “Method of automatically performing a patch test for a sonar system, where data from a plurality of overlapping 3D sonar scans of a surface, as the platform is moved, are used to compensate for biases in mounting the sonar system on the platform”. | January 19, 2027 | ||

| US Patent No. 7,898,902 | Concerns a “method of representation of sonar images” allowing sonar three-dimensional (3D) data to be represented by a two dimensional image. | June 13, 2028 | ||

| US Patent No. 8,059,486 | Concerns a method of rendering volume representation of sonar images. | April 16, 2028 | ||

| US Patent No. 8,854,920 | Concerns a method of volumetric rendering of three dimensional sonar data sets | September 5, 2032 | ||

| US Patent No. 9,019,795 | Method of object tracking using sonar imaging | September 5, 2032 |

Trademarks

We own the following registered trademarks: Coda®, Octopus®, CodaOctopus®, Octopus & Design®, F180®, F180 4G Series®, Echoscope®, Echoscope 4G®, Survey Engine®, Dimension®, DAseries®, CodaOctopus®Vantage; CodaOctopus® UIS; CodaOctopus® USE, Sentiris® and Thermite®.

We also use the following trademarks: F170™, F175™, F190™, UIS™ TEAM™ and TEAM+™. In addition, we have registered a number of internet domain names.

Research and Development

During the fiscal years ended 2016 and 2017 we spent approximately $1 million and $1.4 million, respectively, on mainly developing our real time 3D sonar technology (our Products Segment) and Thermite® refresh (our Services Segment).

Our products are complex and therefore we can give no assurance that we will be successful in the above-stated objective. Furthermore, even following launch we may not succeed. Moreover, we may incur significant research expenditures without realizing viable products.

| 17 |

Government Regulation

Because of the nature of some of our products, they may be subject to United States and other jurisdictions’ export control regimes and may be exported outside these jurisdictions only with the required level of export license or through an export license exception or general export authorization/license.

In addition, as a provider for the US Government, we may be subject to numerous laws and regulations relating to the award, administration and performance of US Government contracts, including the False Claims Act. Non-compliance found by any one agency could result in fines, penalties, debarment, or suspension from receiving additional contracts with all US Government agencies. Given our dependence on US Government business, suspension or debarment could have a material adverse effect on our business and results of operations.

Employees

As of the date hereof, we employ worldwide approximately 110 people, of which 11 hold management positions. A large majority of our employees have a background in science, technology and engineering, with a substantial part being educated to degree and PhD level. None of our employees are employed under a collective agreement and we have not experienced any organized labor difficulties in the past.

Not required for smaller reporting companies.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None.

| 18 |

Orlando, Florida

Our corporate offices are co-located with our subsidiary Coda Octopus Products, Inc. in Orlando where we lease premises on a month to month basis at $1,882 per month.

In addition, Coda Octopus Products, Inc., owns a property which it acquired in February 2016. This property is being used by staff who are assigned or seconded from other parts of our Organization to our Florida Office to assist with R&D projects and/or to provide training or demonstration of our products from time to time.

Salt Lake City, Utah

Coda Octopus Colmek operates from its premises which comprises 16,000 square feet and includes production and R&D Facilities. These premises are owned by Coda Octopus Colmek.

Edinburgh, Scotland

Current Premises

In order to consolidate our activities which were spread over three premises in Edinburgh, on or around January 31, 2017, Coda Octopus Products Ltd acquired a property in Edinburgh, comprising manufacturing facilities, research and development space and offices. The purchase price of the property was the equivalent of $1,512,280 and was paid for in cash. The property is situated in a business park close to Edinburgh Airport and Port Edgar and the Firth of Forth which is ideally located for conducting trials and demonstrations of our products. This new facility has 12,070 square feet of net internal space. This property was reconfigured and upgraded for our specific use and Coda Octopus Products Ltd moved its operation to these new premises on or around May 2017.

Offices which we are actively seeking to sub-let for the remainder of the lease terms.

Our wholly owned United Kingdom subsidiary, Coda Octopus Products Ltd, leases office space comprising 4,099 square feet in Edinburgh, United Kingdom. These premises were used as offices and we are actively seeking to sub-let these premises for the remainder of its term. If we are not successful we will need to pay the rent and other costs associated with these premises up to February 28, 2019 along with any agreed dilapidations. The annual rent is fixed for the duration of the lease at the British Pounds equivalent of $54,130 (the rent is stated in British Pounds and is therefore subject to exchange rate fluctuations).

Production and Repair Services Facilities

The lease for these premises has expired on November 14, 2017 and we are currently negotiating dilapidations with the landlord of these premises. These premises were leased and used by our wholly owned United Kingdom subsidiary, Coda Octopus Products Ltd for production workshop space comprising 2,450 square feet in Edinburgh, United Kingdom. The annual rent was the British Pounds equivalent of $26,950 (the rent was stated in British Pounds and is therefore subject to exchange rate fluctuations).

Perth, Australia

We have a short-term lease for office space comprising 1000 square feet in in Perth, Australia. The lease expires on April 8, 2018. The annual rent is fixed for the duration of the lease at Australian Dollars equivalent of US$11,440. We do not intend to extend this lease upon its expiration.

Portland, Dorset, England

Martech leases premises from Coda Octopus Products Limited. These premises are located in the Marine Center in Portland, Dorset, United Kingdom, are owned by Coda Octopus Products Ltd and comprise 9,890 square feet. The building comprises both office space and manufacturing and testing facilities. The lease, which is for a period of 5 years, provides for an annual rent of the equivalent of $51,000 (the rent increases by 3% annually and is stated in British Pounds and is therefore subject to exchange rate fluctuations). These premises give easy access to marine facilities such as testing vessels etc.

| 19 |

Bergen, Norway

Our wholly owned Norwegian subsidiary, Coda Octopus R&D AS, re-located its facilities on November 30, 2016 and now leases a small facility comprising approximately 300 square feet of office space in a business center. We pay $2,350 on an annual basis (the rent is stated in Norwegian Kroner and is therefore subject to exchange rate variation). This is as a result of the transfer of the production and servicing of the Echoscope® to Edinburgh, UK. The facility now serves as a research and development center for hardware development of our flagship product utilizing our purpose-built laboratories.

All non-US Dollar denominated rents are stated according to prevailing exchange rates as of the date of each respective lease agreement.

From time to time, we may become involved in various lawsuits and legal proceedings which arise in the ordinary course of business. However, litigation is subject to inherent uncertainties, and an adverse result in these or other matters may arise from time to time that may harm our business. We are currently not aware of any such legal proceedings that we believe will have, individually or in the aggregate, a material adverse effect on our business, financial condition or operating results.

ITEM 4. MINE SAFETY DISCLOSURES.

Not Applicable.

| 20 |

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock has been traded on the Nasdaq Capital Market under the symbol “CODA” since July 19, 2017. Prior thereto, it had been quoted on the OTCQX since February 8, 2017 under the symbol COGI, and prior thereto, on the OTC Pink under the symbol CDOC. The following table sets forth the range of high and low bid prices of our common stock as reported and summarized on the Nasdaq, OTCQX or OTC Pink, as applicable, for the periods indicated. These prices are based on inter-dealer bid and asked prices, without markup, markdown, commissions, or adjustments and may not represent actual transactions.

On January 11, 2017, we effected a one for fourteen (1 for 14) reverse stock split of our issued and outstanding common stock. All share prices below have been adjusted retroactively to account for the reverse stock split.

| Year Ended October 31, 2017 | HIGH | LOW | ||||||

| First Quarter | $ | 4.70 | $ | 1.40 | ||||

| Second Quarter | $ | 6.74 | $ | 4.25 | ||||

| Third Quarter | $ | 4.93 | $ | 4.13 | ||||

| Fourth Quarter | $ | 4.98 | $ | 3.91 | ||||

| Year Ended October 31, 2016 | HIGH | LOW | ||||||

| First Quarter | $ | 1.54 | $ | 1.26 | ||||

| Second Quarter | $ | 1.64 | $ | 1.17 | ||||

| Third Quarter | $ | 2.67 | $ | 1.26 | ||||

| Fourth Quarter | $ | 2.14 | $ | 1.68 | ||||

We have not declared or paid any cash dividends on our common stock, and we currently intend to retain future earnings, if any, to finance the expansion of our business, and we do not expect to pay any cash dividends in the foreseeable future. The decision whether to pay cash dividends on our common stock will be made by our board of directors, in their discretion, and will depend on our financial condition, operating results, capital requirements and other factors that the board of directors considers significant.

Recent sales of unregistered securities

None that are required to be disclosed herein.

ITEM 6. SELECTED FINANCIAL DATA

Not applicable.

| 21 |

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OPERATIONS

Forward-Looking Statements

The information herein contains forward-looking statements. All statements other than statements of historical fact made herein are forward looking. In particular, the statements herein regarding industry prospects and future results of operations or financial position are forward-looking statements. These forward-looking statements can be identified by the use of words such as “believes,” “estimates,” “could,” “possibly,” “probably,” anticipates,” “projects,” “expects,” “may,” “will,” or “should” or other variations or similar words. No assurances can be given that the future results anticipated by the forward-looking statements will be achieved. Forward-looking statements reflect management’s current expectations and are inherently uncertain. Our actual results may differ significantly from management’s expectations.

The following discussion and analysis should be read in conjunction with our financial statements, included herewith. This discussion should not be construed to imply that the results discussed herein will necessarily continue into the future, or that any conclusion reached herein will necessarily be indicative of actual operating results in the future. Such discussion represents only the best present assessment of our management.

General Overview

We operate two distinct business segments. Our Products Segment designs and manufactures patented real time 3D sonar solutions and other leading products for subsea applications (“Products Segment”). Our Services Segment supplies engineering services to prime defense contractors (“Services Segment”).

Our products are used primarily in the underwater construction market, offshore oil and gas, offshore wind energy industry, and in the complex dredging, port security, mining and marine sciences sectors. Our customers include service providers to major oil and gas companies, law enforcement agencies, ports, mining companies, defense bodies, research institutes and universities.

Our Services segment supplies engineering services mainly to prime defense contractors such as Raytheon and Northrop Grumman. We have long-standing relationships with prime defense contractors. We support some significant defense programs by supplying and maintaining proprietary parts through obsolescence management programs. These services provide recurring stream of revenues for our Services segment.

Historically, the Products Segment generated approximately 70% of our revenues. However, during the last three fiscal years prior to the 2017 period, the Products Segment has generated around 50% of our overall revenues, with the Services Segment growing at a faster pace. However, during the 2017 period, due to the new US administration’s failure to approve the defense budget, many projected sales did not materialize. As a result, the Services Segment revenues fell from 50% of our overall revenues to 39% in the 2017 with the Products Segment generating 61% of revenues in the 2017 period as compared to 50% in the 2016 period. Although the Products Segment generated 61% of the overall revenues in the 2017 period, it is still adversely affected by the contraction in the oil and gas (O&G) industry. Furthermore, due to the effort by O&G companies to restructure their operations, the climate in which we sell is fiercely competitive thus impacting on revenues and gross margins.

Nevertheless, we believe that our unique and patented real time 3D solutions are a significant advancement on the current technology available in the subsea sonar imaging market due to its real time capability providing real time volumetric data of underwater targets in low or zero visibility conditions and its capability to image moving objects in the subsea environment. Furthermore, because the technology provides real time imaging of the underwater environment, it enhances safety significantly and delivers substantial productivity gains to our customers, thus reducing their costs. In addition, our real time 3D solution is emerging as the preferred solutions for subsea asset placements because of the technology’s unique ability to image moving targets (such as Accropodes™, X-Blocs, Antifers block placements, mattress placements, landing of installations on the seabed and the like). Due to the decline in the price of oil, many O&G companies are seeking cost effective solutions for their operations. We believe that our real time 3D solution has the potential to revolutionize the technology used in underwater operations particularly where real time visualization is required or zero or low visibility conditions prevail. We also believe that with the proliferation of underwater drones our technology has significant application for the imaging sonar defense market (which is worth billions of dollars annually) as it is the only available off the shelf technology that can image moving targets (such as underwater vehicles) in the water.

| 22 |

Since introducing this product, we have made progress in getting our core real time 3D technology, the Echoscope®, adopted by a significant number of ports in the USA (the CodaOctopus® Underwater Inspection System (which integrates our Echoscope, motion sensing product and hydrographic pole) where it is used for port and harbor security. In 2015 we secured the first sale of our Underwater Inspection System to a foreign government body in East Asia and in 2016 we sold two additional full system to this body. We hope to sell additional systems into this government body as part of their technology upgrade program for the next three years.

We have also made progress in expanding the markets (and applications) for our real time 3D sonars. Recently, we have sold a number of systems to mining companies. Increasingly, our customers involved in offshore wind energy and renewables are adopting the technology as the primary tool for scour management, subsea cable installation and associated cable protection tasks.

In addition, in recent years we have started to rent our real time 3D solutions with engineering services. Given the contraction in capital expenditures budget in the O&G market, rentals are increasingly becoming an important part of the composition of the Company’s revenues and these O&G operators are more prepared to utilize operational budgets. Furthermore, our rental offering generally yields a higher gross margin for the Company.

Our business is affected by a number of factors including those set out below:

| A. | The Company’s operations are split between the United States, United Kingdom, Australia and Norway. A large proportion of our revenues (approximately 58%) and costs are incurred outside of the USA with a significant part (50% of our total revenues) of that in the United Kingdom (“UK”). In addition, a significant part of our assets (both current and fixed) are held in British Pounds by our foreign subsidiaries. | |

| B. | On June 23, 2016, the United Kingdom voted to exit the European Union. This resulted in significant currency exchange rate fluctuations and volatility in global stock markets including a sharp fall of the British Pound against the US Dollar. The British government has commenced negotiations to determine the terms of the exit from the European Union (so-called “Brexit”). The United Kingdom’s separation could, among other things, disrupt trade and the free movement of goods, services and people between the United Kingdom and the European Union or other countries as well as create legal and global economic uncertainty. Currencies could remain volatile for the foreseeable future. | |

| C. | Since the Brexit vote, we have suffered adverse currency movements affecting our UK Businesses. In summary, since our reporting currency is the US Dollar, the fall in the British Pound impacts on our revenues, costs and balance sheet valuation. | |

| D. | Given the lack of comparable precedent, the implications of Brexit or how such implications might affect the Company in the medium to long term are unclear. |

Further areas of impact include:

| i. | the price of commodities, in particular O&G. The decline in O&G prices since 2014 with a partial recovery since 2016 has resulted in large scale reductions in capital and operational expenditures, which directly impact on the sales of our products into these and related markets and also our gross margins; | |

| ii. | the allocation of funds to defense procurement by governments in the United States and the United Kingdom; | |

| iii. | volatility of the markets including the currency market; | |

| iv. | approximately 50% of the Company revenues are transacted and generated in British Pounds by the Company’s subsidiaries in the United Kingdom and therefore we have a currency exposure.. The depreciation of the British Pound against major currencies adversely impacts our revenues as a whole which are reported in U.S. Dollars. Furthermore, a large part of our assets is held in British Pounds while the majority of our liabilities (which comprise our senior secured debentures – see Note 8 of the audited Consolidated Financial Statements) are maintained in U.S. Dollars. In the 2017 period as compared to the same 2016 period, we realized a balance sheet gain on our assets due to a slight gain in the British Pound against the US Dollar prevailing at the balance sheet date of October 31, 2017. In fiscal year 2017 compared to the 2016 period, we incurred a loss from the exchange rate translations in respect of our profit and loss account. See Note 2, paragraph n, of the audited Consolidated Financial Statements October 31, 2017 and 2016 regarding our Foreign Currency Translation policy. | |

| v. | global-political uncertainties affecting the markets into which we sell our goods and services; | |

| vi. | global trends which make certain geographical regions more competitive in providing engineering solutions because of lower labor costs (e.g. India and China) are likely to affect our Engineering Businesses in the Group; | |

| vii. | being a small technology company, we are unable to compete for certain specialized electronic engineering skills as our remuneration package is not as competitive as those offered by bigger companies; | |

| viii. | the Company has issued and outstanding a promissory note (See Note 8 of the audited Consolidated Financial Statements October 31, 2017 and 2016). This note is secured by all of the Company’s assets in the USA and is also guaranteed by its overseas subsidiaries; |

| 23 |

| ix. | we lack the financial resources to advance our flagship technology at the commercially appropriate pace required to capture new markets and increase our sales which could facilitate new entrants to the market. For example, Teledyne Technologies Incorporated, a multi-billion company, has recently acquired a number of subsea companies that may speed up their entry into our market; | |

| x | a significant part of our growth strategy is predicated on our patented real time 3D sonar technology. The technology space is inherently uncertain due to the fast pace of innovations and therefore we can give no assurance that we can maintain our leading position in the real time 3D imaging sonar market or that innovations in other areas may not surpass our unique capability that we currently supply to subsea market; and | |

| xi. | the Company has limited external sources of capital available, and as such is reliant upon its ability to sell its products and services to provide sufficient working capital for its operations and obligations. |

Critical Accounting Policies

This discussion and analysis of our financial condition and results of operations is based on our consolidated financial statements that have been prepared under accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements in conformity with US GAAP requires our management to make estimates and assumptions that affect the reported values of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported levels of revenue and expenses during the reporting period. Actual results could materially differ from those estimates.

Below is a discussion of accounting policies that we consider critical to an understanding of our financial condition and operating results and that may require complex judgment in their application or require estimates about matters which are inherently uncertain. A discussion of our significant accounting policies, including further discussion of the accounting policies described below, can be found in Note 2, “Summary of Accounting Policies” of our Consolidated Financial Statements.

Revenue Recognition

Our revenue is derived from sales of underwater technologies and equipment for imaging, mapping, defense and survey applications and from the engineering services which we provide. Revenue is recognized when evidence of a contractual arrangement exists, delivery has occurred or services have been rendered, the contract price is fixed or determinable, and collectability is reasonably assured. No right of return privileges are granted to customers after delivery.

For arrangements with multiple deliverables, we recognize product revenue by allocating the revenue to each deliverable based on the relative fair value of each deliverable, and recognize revenue when equipment is delivered, and for installation and other services as they are performed.

| 24 |

Our contracts sometimes require customer payments in advance of revenue recognition. These amounts are reflected as liabilities and recognized as revenue when the Company has fulfilled its obligations under the respective contracts.

For software license sales for which any services rendered are not considered essential to the functionality of the software, we recognize revenue upon delivery of the software, provided (1) there is evidence of a contractual arrangement for this, (2) collection of our fee is considered probable and (3) the fee is fixed and determinable.