Attached files

| file | filename |

|---|---|

| 8-K - 8-K - WhiteHorse Finance, Inc. | tv483287_8k.htm |

Exhibit 99.1

Investor Presentation January 2018 WhiteHorse Finance, Inc. NASDAQ: WHF (Common Stock) NASDAQ: WHFBL (6.50% Senior Notes due 2020)

1 References in this presentation to “WHF”, “we”, “us”, “our” and “the Company” refer to WhiteHorse Finance, Inc. This presentation and the information and views included herein do not constitute investment advice, or a recommendation or a n o ffer to enter into any transaction with the Company or any of its affiliates. Investors are advised to consider carefully the Company’s investment objectives, ris ks, charges and expenses before investing in the Company’s securities. A prospectus supplement dated June 27, 2017 and an accompanying prospectus dated June 15, 2017 (together, the “Prospectus”), and a quarterly report on Form 10 - Q for the quarter ended September 30, 2017, which have been filed with the Securities and Exchange Commission (“SEC”), contain this and other information about the Company and should be read carefully before investing in the Company’s sec urities. The information in the Prospectus and this presentation is not complete and may be changed. The Prospectus and this presentation are not offers to sell the Company’s securities and are not soliciting an offer to buy the Company’s securities in any jurisdiction where such offer or sale is not permitted. A shelf registration statement relating to the Company’s securities is on file with and has been declared effective by the SE C. A public offering of the Company’s securities may be made only by means of a prospectus and a related prospectus supplement, copies of which may be obtained by wri ting the Company at 1450 Brickell Avenue, 31st Floor, Miami, FL 33131, Attention: Investor Relations, or by calling (305) 381 - 6999; copies may also be obtained by visiting EDGAR on the SEC’s website at http://www.sec.gov . Forward Looking Statements Some of the statements in this presentation constitute forward - looking statements, which relate to future events or the Company’s fut ure performance or financial condition. The forward - looking statements contained in this presentation involve risks and uncertainties, including statements as to: the Company’s future operating results; changes in political, economic or industry conditions, the interest rate environment or conditions affecti ng the financial and capital markets, which could result in changes to the value of the Company’s assets; the Company’s business prospects and the prospects of its pr ospective portfolio companies; the impact of investments that the Company expects to make; the impact of increased competition; the Company’s contractual ar ran gements and relationships with third parties; the dependence of the Company’s future success on the general economy and its impact on the industries in wh ich the Company invests; the ability of the Company’s prospective portfolio companies to achieve their objectives; the relative and absolute performance o f t he Company’s investment adviser; the Company’s expected financings and investments; the adequacy of the Company’s cash resources and working capital; the timi ng of cash flows, if any, from the operations of the Company’s prospective portfolio companies; and the impact of future acquisitions and divestitures. Such forward - looking statements may include statements preceded by, followed by or that otherwise include the words “may,” “migh t,” “will,” “intend,” “should,” “could,” “can,” “would,” “expect,” “believe,” “estimate,” “anticipate,” “predict,” “potential,” “plan” or similar words. The Company has based the forward - looking statements included in this presentation on information available to us on the date of this presentation, and the Company assumes no obligation to update any such forward - looking statements. Actual results could differ materially from those implied or expressed in the Company’s forward - looking statements for any reason, and future results could differ materially from historical performance. Al though the Company undertakes no obligation to revise or update any forward - looking statements, whether as a result of new information, future events or other wise, you are advised to consult any additional disclosures that are made directly to you or through reports that the Company in the future may file with the Sec urities and Exchange Commission, including annual reports on Form 10 - K, quarterly reports on Form 10 - Q and current reports on Form 8 - K. For a further discussion of factors that could cause the Company’s future results to differ materially from any forward - looking statements, see the section entitled “Risk Factors” in th e annual report on Form 10 - K, the Prospectus and the quarterly report on Form 10 - Q for the quarter ended September 30, 2017. Important Information and Forward Looking Statements

2 WhiteHorse Finance Snapshot Company / Ticker: WhiteHorse Finance, Inc. / NASDAQ: WHF (“WhiteHorse Finance” or the “Company”) : Current Share Price: $13.36 (1) : Market Cap: $274.3M (1 ) : Price / NAV: 0.96x (1 )(2) Portfolio Fair Value: $435.3MM (2 ) : Current Dividend Yield: 10.6% ( 1) ; consistent quarterly dividends of $0.355 per share since 2012 IPO: (1) As of January 3, 2018 (2) Based on NAV per share of $13.92 as of September 30, 2017 External Manager: Affiliate of H.I.G. Capital, LLC (“H.I.G. Capital” or “H.I.G.”)

3 H.I.G. WhiteHorse Highlights Leading Lower Middle Market Position ▪ H.I.G. brings over 20 years of experience and ~$ 24Bn of capital committed (1) primarily across a number of synergistic lower middle market strategies Unique Deal Sourcing Infrastructure ▪ Robust direct origination platform has enabled the Company to deploy ~$845MM since December 2012 IPO Deep Credit Expertise ▪ H.I.G.’s senior management team has collectively invested in more than 1,000 loans Compelling Market Opportunity ▪ Structural inefficiencies in the lower middle market provide an opportunity to generate attractive risk - adjusted returns Attractive Portfolio ▪ Diversified ~$435MM portfolio principally composed of senior secured loans with an attractive yield Note: As of September 30, 2017 (1) Based on total capital commitments managed by H.I.G. Capital and affiliates Large and Experienced Team with Substantial Resources ▪ Access to H.I.G. Capital’s resources and expertise, including an investment team of over 350 professionals with 25 business development resources and dedicated team of over 25 Whitehorse Direct Lending professionals

▪ Consistent, robust deal flow generated through H.I.G.’s proprietary sourcing network - Proprietary deal sourcing consisting of sponsored and non - sponsored opportunities - Experienced team able to underwrite more complex non - sponsored opportunities ▪ Over 2,000 opportunities reviewed and approximately $1B invested since December 2012 IPO ▪ Over 25 Whitehorse deal professionals dedicated to sourcing and underwriting for WHF plus 25 person business development team seeks opportunities from H.I.G .’s proprietary database of over 20,000 contacts ▪ Deals being sourced by more than 350 Investment Professionals across H.I.G.’s platform Proprietary Deal Sourcing Network 4 WhiteHorse Finance Overview Investment Strategy ▪ Generate attractive risk - adjusted returns primarily by originating and investing in senior secured loans to performing lower middle market companies ▪ Opportunistically invest at other levels of a company’s capital structure where the investment presents an opportunity to achieve an attractive risk - adjusted return Secure Investment Portfolio ▪ 100% of all WHF loans were senior secured loans as of 9/30/2017 ▪ Portfolio has significant downside protection with meaningful value coverage ▪ Loans diligently structured with tight covenants and broad lender rights Note: As of September 30, 2017 unless otherwise noted

Note: As of September 30, 2017 (1) Based on total capital commitments managed by H.I.G. Capital and affiliates 5 H.I.G. Capital Overview ▪ Leading global alternative asset manager focused on the lower middle market , defined as companies with $50MM to $350MM of enterprise value − Founded in 1993; ~$ 24Bn of capital under management (1) ▪ Differentiated, value - added strategy and deep experience in the lower middle market segment of the market have resulted in what we believe is a superior track record ▪ Broad investment capabilities across sectors, capital structures, and investment styles, with a focus on smaller, complex situations ▪ Investment activities include: − Leveraged Buyouts − Credit − Growth Capital − Real Estate ▪ Over ~350 investment professionals located in eighteen offices across North America, South America and Europe ▪ “Institutionalized” management structure and processes with strong financial staff, controls, legal, compliance, IT support, and risk management procedures in place Investment Approach Global Footprint Miami New York Boston Chicago San Francisco Dallas Rio de Janeiro London Madrid Milan Hamburg Paris Atlanta

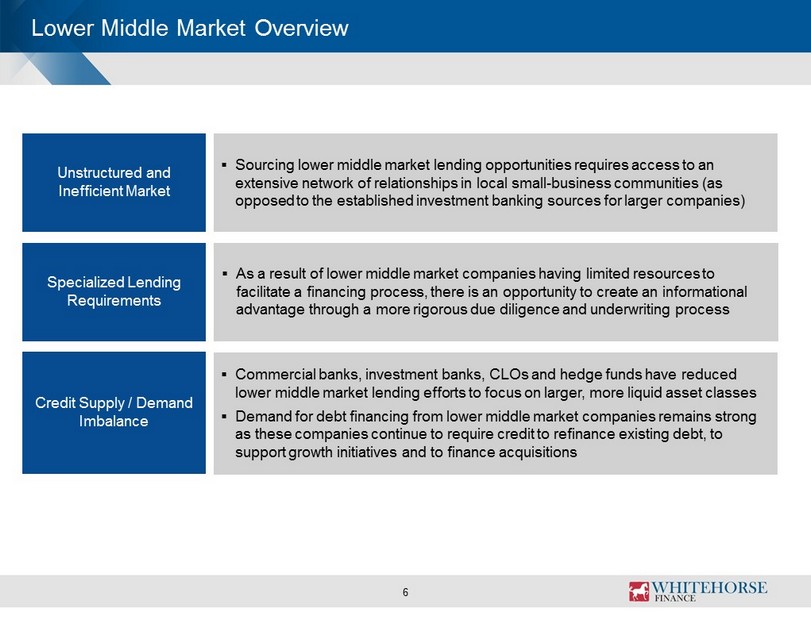

6 Lower Middle Market Overview Unstructured and Inefficient Market ▪ Sourcing lower middle market lending opportunities requires access to an extensive network of relationships in local small - business communities (as opposed to the established investment banking sources for larger companies) Specialized Lending Requirements ▪ As a result of lower middle market companies having limited resources to facilitate a financing process, there is an opportunity to create an informational advantage through a more rigorous due diligence and underwriting process Credit Supply / Demand Imbalance ▪ C ommercial banks, investment banks, CLOs and hedge funds have reduced lower middle market lending efforts to focus on larger, more liquid asset classes ▪ Demand for debt financing from lower middle market companies remains strong as these companies continue to require credit to refinance existing debt, to support growth initiatives and to finance acquisitions

7 Self - Originated Lower Middle Market Broadly Syndicated Market Value Add for Investors ▪ Proprietary deals with limited competition, resulting in above market risk - return dynamics ▪ Larger, more liquid investments; competition among a large number of participants often drives down yields Number of Lenders ▪ Sole or club lender in most transactions ▪ Large number of lenders in syndicated transactions; less influence over process Due Diligence ▪ Direct access to management allows for more thorough diligence process to create potential informational advantages ▪ Limited access to management and owners/ sponsors at underwriting stage Terms/ Credit Metrics ▪ Moderate leverage levels, favorable lender terms ▪ Market process and equity sponsor influence often lead to more borrower - friendly terms Financial Covenants ▪ Control over documentation, resulting in tight operational and financial covenants ▪ Documentation controlled by agent; competitive market dynamics can result in less stringent covenant packages Monitoring ▪ Lead monitoring process, able to take quick action if any issues arise ▪ Often limited to predetermined compliance package; access to company controlled by the agent Compelling Lower Middle Market Lending Opportunities ▪ With access to H.I.G. Capital’s extensive sourcing network, the Company is able to capitalize on attractive self - originated lower middle market transactions as compared to the broadly syndicated market Directly originated loans to lower middle market companies typically generate more attractive risk - adjusted returns relative to larger, broadly syndicated credits

8 WhiteHorse Finance Portfolio Investment Characteristics As of September 30, 2017; based on fair value of investments; numbers may not foot due to rounding Loan Composition 100% of WHF loans are senior secured 99.95% of floating loans have LIBOR floors Highly diversified portfolio by sector with significant downside protection Mitigates non - credit (interest rate and reinvestment) risks Investments by Type Investments by Sector Fixed Rate vs. Floating Rate

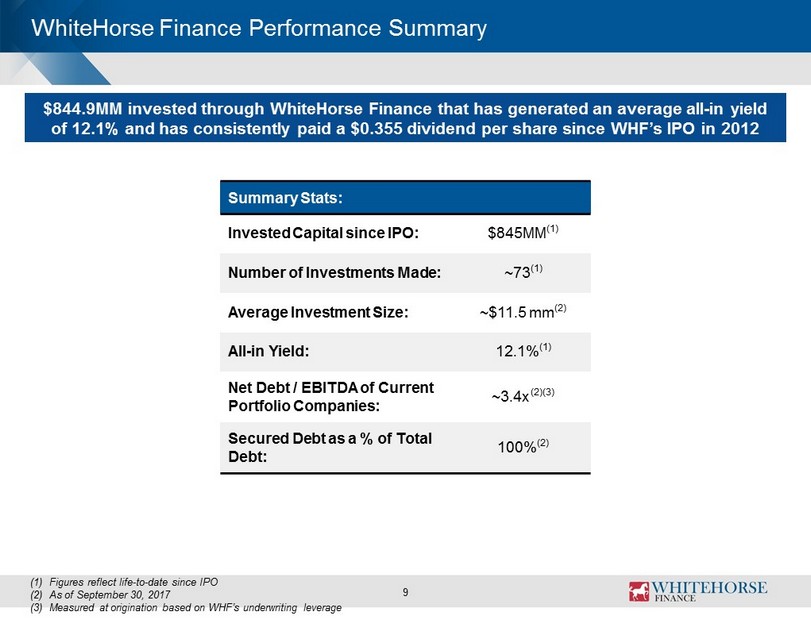

WhiteHorse Finance Performance Summary Summary Stats: Invested Capital since IPO: $845MM (1) Number of Investments Made: ~73 (1) Average Investment Size: ~$ 11.5 mm (2) All - in Yield : 12.1% (1) Net Debt / EBITDA of Current Portfolio Companies: ~ 3.4x (2)(3) Secured Debt as a % of Total Debt : 100% (2) $844.9MM invested through WhiteHorse Finance that has generated an average all - in yield of 12.1% and has consistently paid a $0.355 dividend per share since WHF’s IPO in 2012 (1) Figures reflect life - to - date since IPO (2) As of September 30, 2017 (3) Measured at origination based on WHF’s underwriting leverage 9

WhiteHorse Differentiated Deal Flow As a result of its proprietary sourcing network, we believe the WhiteHorse Finance portfolio has generated higher yields at lower portfolio company leverage than the broader middle market All - in Yield of Invested Capital (1) Leverage Multiple of Invested Capital (2) » Compared to the broader middle market, the WhiteHorse Finance portfolio has produced an average all - in yield of 12.1% and an average portfolio company leverage multiple of 3.2x since 2013 10 (1) Source : S&P LCD data for senior secured loans for middle market companies (2) Measured at time of WHF’s underwriting of portfolio company leverage 4.9x Avg. 3.2x Avg.

Origination Pipeline Funnel (1) Dedicated origination resources provide wide - ranging access to proprietary opportunities in the lower middle market Opportunities Reviewed Initial Due Diligence Term Sheets Delivered Closed Transactions 11 246 2,979 39 959 (1) Origination Pipeline figures reflect 2014 through September 2017

Rigorous Credit Process Institutionalized processes for evaluating, monitoring and, if necessary, working out credits Fundamental Analysis » Structured approach to deal evaluation » Assesses industry, company, management, and macro factors » Emphasizes cash flow and downside protection Investment Committee » Broad market experience investing and managing structured credit with experience across cycles » Access to H.I.G. Capital’s global knowledge platform to leverage insight across industry, geography, and transaction type » Conservative view on credit risk driven by prior workout and bankruptcy experience » Weekly investment committee meetings include entire credit team, require group consensus, and are structured to provide detailed feedback to counterparties separate from a buy/pass decision Technical Analysis » Assess return potential from rate, fee, upside participation » Focus on structural protections including covenants, call protection, security, priority, and inter - creditor rights » Leverage past experience with issuers, management teams, and sponsors Portfolio Construction & Monitoring » Portfolio construction and ongoing risk management to mitigate risk and enhance investment returns » Top - down assessment of portfolio diversification and risk exposure (industry, issuer, geography, and credit type) » Multi - layered monitoring and active manager dialogue to stay current on issuer activities » Four formal investment committee reviews annually on existing portfolio with watch list credits reviewed more frequently 12

13 Appendix

14 Historical Quarterly Operating Highlights (USD amounts in millions, except per share data) (1) (3)

15 Historical Quarterly Balance Sheet Highlights (USD amounts in millions, except per share data)

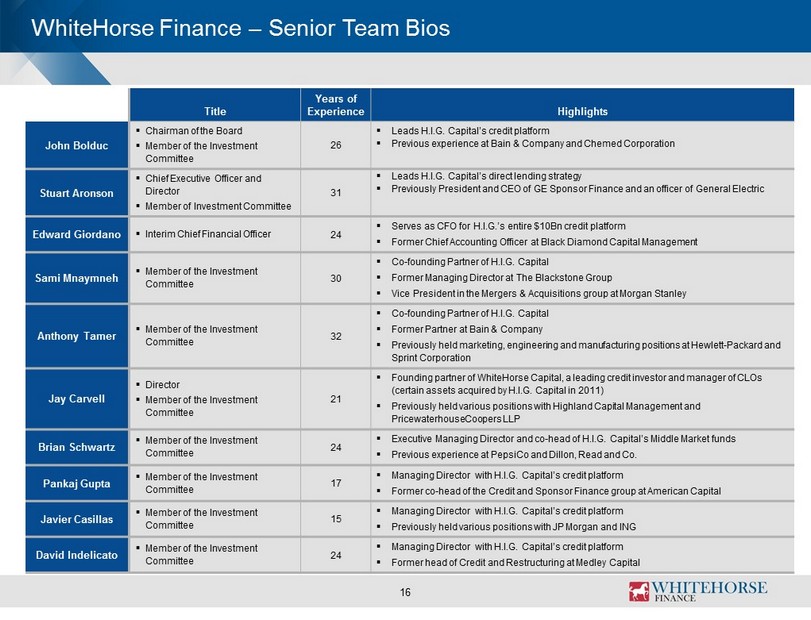

16 WhiteHorse Finance – Senior Team Bios Title Years of Experience Highlights John Bolduc ▪ Chairman of the Board ▪ Member of the Investment Committee 26 ▪ Leads H.I.G. Capital’s c redit platform ▪ Previous experience at Bain & Company and Chemed Corporation Stuart Aronson ▪ Chief Executive Officer and Director ▪ Member of Investment Committee 31 ▪ Leads H.I.G. Capital’s direct lending strategy ▪ Previously President and CEO of GE Sponsor Finance and an officer of General Electric Edward Giordano ▪ Interim Chief Financial Officer 24 ▪ Serves as CFO for H.I.G.’s entire $10Bn credit platform ▪ Former Chief Accounting Officer at Black Diamond Capital Management Sami Mnaymneh ▪ Member of the Investment Committee 30 ▪ Co - founding Partner of H.I.G. Capital ▪ Former Managing Director at The Blackstone Group ▪ Vice President in the Mergers & Acquisitions group at Morgan Stanley Anthony Tamer ▪ Member of the Investment Committee 32 ▪ Co - founding Partner of H.I.G. Capital ▪ Former Partner at Bain & Company ▪ Previously held marketing, engineering and manufacturing positions at Hewlett - Packard and Sprint Corporation Jay Carvell ▪ Director ▪ Member of the Investment Committee 21 ▪ Founding partner of WhiteHorse Capital, a leading credit investor and manager of CLOs (certain assets acquired by H.I.G. Capital in 2011) ▪ Previously held various positions with Highland Capital Management and PricewaterhouseCoopers LLP Brian Schwartz ▪ Member of the Investment Committee 24 ▪ Executive Managing Director and co - head of H.I.G. Capital’s Middle Market funds ▪ Previous experience at PepsiCo and Dillon, Read and Co. Pankaj Gupta ▪ Member of the Investment Committee 17 ▪ Managing Director with H.I.G. Capital’s credit platform ▪ Former co - head of the Credit and Sponsor Finance group at American Capital Javier Casillas ▪ Member of the Investment Committee 15 ▪ Managing Director with H.I.G. Capital’s credit platform ▪ Previously held various positions with JP Morgan and ING David Indelicato ▪ Member of the Investment Committee 24 ▪ Managing Director with H.I.G. Capital’s credit platform ▪ Former head of Credit and Restructuring at Medley Capital