Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 EARNINGS RELEASE - KITE REALTY GROUP TRUST | exhibit99_1xq32017.htm |

| 8-K - FORM 8-K Q3 2017 - KITE REALTY GROUP TRUST | form8k_q32017.htm |

Exhibit 99.2 | ||

|

QUARTERLY FINANCIAL SUPPLEMENTAL – SEPTEMBER 30, 2017 |  | |

PAGE NO. | TABLE OF CONTENTS | |

3 | Corporate Profile | |

4 | Contact Information | |

5 | Important Notes Including Non-GAAP Disclosures | |

7 | Consolidated Balance Sheets | |

8 | Consolidated Statements of Operations for the Three and Nine Months Ended September 30, 2017 | |

9 | Funds from Operations for the Three and Nine Months Ended September 30, 2017 | |

10 | Adjusted Funds From Operations and Other Financial Information for the Three and Nine Months Ended September 30, 2017 | |

11 | Market Capitalization as of September 30, 2017 | |

11 | Ratio of Debt to Total Undepreciated Assets as of September 30, 2017 | |

11 | Ratio of Company Share of Net Debt to EBITDA as of September 30, 2017 | |

12 | Same Property Net Operating Income for the Three and Nine Months Ended September 30, 2017 | |

13 | Net Operating Income by Quarter | |

14 | Consolidated Joint Venture Summary as of September 30, 2017 | |

15 | Summary of Outstanding Debt as of September 30, 2017 | |

16 | Maturity Schedule of Outstanding Debt as of September 30, 2017 | |

18 | Unsecured Public Debt Covenants | |

19 | Top 10 Retail Tenants by Total Gross Leasable Area | |

20 | Top 25 Tenants by Annualized Base Rent | |

21 | Retail Leasing Spreads | |

22 | Lease Expirations – Operating Portfolio | |

23 | Lease Expirations – Retail Anchor Tenants | |

24 | Lease Expirations – Retail Shops | |

25 | Lease Expirations – Office Tenants and Other | |

26 | Development Projects Under Construction | |

27 | Under Construction Redevelopment, Reposition, and Repurpose Projects | |

28 | Redevelopment, Reposition, and Repurpose Opportunities | |

29 | 2017 Property Dispositions | |

30 | Geographic Diversification – Annualized Base Rent by Region and State | |

31 | Operating Retail Portfolio Summary Report | |

36 | Operating Office Properties and Other | |

37 | Components of Net Asset Value | |

38 | Earnings Guidance – 2017 | |

p. 2 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

CORPORATE PROFILE | | |

General Description

Kite Realty Group Trust is a full-service, vertically integrated real estate investment trust (REIT) engaged primarily in the ownership and operation, acquisition, development and redevelopment of high-quality neighborhood and community shopping centers in select markets in the United States. As of September 30, 2017, we owned interests in 117 operating and redevelopment properties totaling approximately 23.1 million square feet and two development projects currently under construction.

Our strategy is to maximize the cash flow of our operating properties, successfully complete the construction and lease-up of our redevelopment and development portfolio, and identify additional opportunities to acquire or dispose of properties to further strengthen the Company. New investments are focused in the shopping center sector primarily in markets where we believe we can leverage our existing infrastructure and relationships to generate attractive risk-adjusted returns or otherwise in desirable trade areas. Dispositions are generally designed to increase the quality of our portfolio and to strengthen the Company’s balance sheet.

Company Highlights as of September 30, 2017

# of Properties | Total GLA /NRA1 | Owned GLA /NRA1 | |||||

Operating Retail Properties | 105 | 21,185,634 | 14,965,403 | ||||

Operating Office Properties and Other | 4 | 501,162 | 501,162 | ||||

Redevelopment Properties | 8 | 1,412,060 | 1,303,759 | ||||

Total Operating and Redevelopment Properties | 117 | 23,098,856 | 16,770,324 | ||||

Development Projects | 2 | 553,000 | 31,500 | ||||

Total All Properties | 119 | 23,651,856 | 16,801,824 | ||||

Retail | Office & Other | Total | |||||

Operating Properties – Leased Percentage1 | 94.5% | 98.8% | 94.6% | ||||

States | 20 | ||||||

Stock Listing: New York Stock Exchange symbol: KRG

____________________ | |

1 | Excludes square footage of structures located on land owned by the company and ground leased to tenants. |

p. 3 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

CONTACT INFORMATION | | |

Corporate Office

30 South Meridian Street, Suite 1100

Indianapolis, IN 46204

(888) 577-5600

(317) 577-5600

www.kiterealty.com

Investor Relations Contact: | Analyst Coverage: | Analyst Coverage: | ||

Daniel R. Sink | Robert W. Baird & Co. | DA Davidson | ||

EVP & CFO | Mr. RJ Milligan | Mr. James O. Lykins | ||

Kite Realty Group Trust | (813) 273-8252 | (503) 603-3041 | ||

30 South Meridian Street, Suite 1100 | rjmilligan@rwbaird.com | jlykins@dadco.com | ||

Indianapolis, IN 46204 | ||||

(317) 577-5609 | Bank of America/Merrill Lynch | Hilliard Lyons | ||

dsink@kiterealty.com | Mr. Jeffrey Spector/Mr. Craig Schmidt | Ms. Carol L. Kemple | ||

(646) 855-1363/(646) 855-3640 | (502) 588-1839 | |||

Transfer Agent: | jeff.spector@baml.com | ckemple@hilliard.com | ||

craig.schmidt@baml.com | ||||

Broadridge Financial Solutions | KeyBanc Capital Markets | |||

Ms. Kristen Tartaglione | Barclays | Mr. Jordan Sadler/Mr. Todd Thomas | ||

2 Journal Square, 7th Floor | Mr. Ross Smotrich/Ms. Linda Tsai | (917) 368-2280/(917) 368-2286 | ||

Jersey City, NJ 07306 | (212) 526-2306/(212) 526-9937 | tthomas@keybanccm.com | ||

(201) 714-8094 | ross.smotrich@barclays.com | jsadler@keybanccm.com | ||

linda.tsai@barclays.com | ||||

Stock Specialist: | Raymond James | |||

BTIG | Mr. Paul Puryear/Mr. Collin Mings | |||

GTS | Mr. Michael Gorman | (727) 567-2253/(727) 567-2585 | ||

545 Madison Avenue | (212) 738-6138 | paul.puryear@raymondjames.com | ||

15th Floor | mgorman@btig.com | collin.mings@raymondjames.com | ||

New York, NY 10022 | ||||

(212) 715-2830 | Capital One Securities, Inc. | Sandler O’Neill | ||

Mr. Christopher Lucas | Mr. Alexander Goldfarb | |||

(571) 633-8151 | (212) 466-7937 | |||

christopher.lucas@capitalone.com | agoldfarb@sandleroneill.com | |||

Citigroup Global Markets | Wells Fargo Securities, LLC | |||

Mr. Michael Bilerman/Ms. Christy McElroy | Mr. Jeffrey J. Donnelly, CFA /Ms. Tamara Fique | |||

(212) 816-1383/(212) 816-6981 | (617) 603-4262/(443) 263-6568 | |||

michael.bilerman@citigroup.com | jeff.donnelly@wellsfargo.com | |||

christy.mcelroy@citigroup.com | tamara.fique@wellsfargo.com | |||

p. 4 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

IMPORTANT NOTES INCLUDING NON-GAAP DISCLOSURES | | |

Interim Information

This Quarterly Financial Supplemental contains historical information of Kite Realty Group Trust (“the Company” or “KRG”) and is intended to supplement the Company’s Quarterly Report on Form 10-Q for the quarter ended September 30, 2017 to be filed on or about November 3, 2017, which should be read in conjunction with this supplement. The supplemental information is unaudited, although it reflects all adjustments which, in the opinion of management, are necessary for a fair presentation of operating results for the interim periods.

Forward-Looking Statements

This supplemental information package, together with other statements and information publicly disseminated by us, contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such statements are based on assumptions and expectations that may not be realized and are inherently subject to risks, uncertainties and other factors, many of which cannot be predicted with accuracy and some of which might not even be anticipated. Future events and actual results, performance, transactions or achievements, financial or otherwise, may differ materially from the results, performance, transactions or achievements, financial or otherwise, expressed or implied by the forward-looking statements. Risks, uncertainties and other factors that might cause such differences, some of which could be material, include but are not limited to:

• | national and local economic, business, real estate and other market conditions, particularly in light of low growth in the U.S. economy as well as economic uncertainty caused by fluctuations in the prices of oil and other energy sources; |

• | financing risks, including the availability of, and costs associated with, sources of liquidity; |

• | our ability to refinance, or extend the maturity dates of, our indebtedness; |

• | the level and volatility of interest rates; |

• | the financial stability of tenants, including their ability to pay rent and the risk of tenant bankruptcies; |

• | the competitive environment in which the Company operates; |

• | acquisition, disposition, development and joint venture risks; |

• | property ownership and management risks; |

• | our ability to maintain our status as a real estate investment trust for federal income tax purposes; |

• | potential environmental and other liabilities; |

• | impairment in the value of real estate property the Company owns; |

• | the impact of online retail and the perception that such retail has on the value of shopping center assets; |

• | risks related to the geographical concentration of our properties in Florida, Indiana and Texas; |

• | insurance costs and coverage; |

• | risks associated with cybersecurity attacks and the loss of confidential information and other business disruptions; |

• | other factors affecting the real estate industry generally; and |

• | other risks identified in reports the Company files with the Securities and Exchange Commission (“the SEC”) or in other documents that it publicly disseminates, including, in particular, the section titled “Risk Factors” in our Annual Report on Form |

10-K for the fiscal year ended December 31, 2016, and in our quarterly reports on Form 10-Q.

The Company undertakes no obligation to publicly update or revise these forward-looking statements, whether as a result of new information, future events or otherwise.

Non-GAAP Disclosures

Funds from Operations

Funds from Operations (FFO) is a widely used performance measure for real estate companies and is provided here as a supplemental measure of operating performance. The Company calculates FFO, a non-GAAP financial measure, in accordance with the best practices described in the April 2002 National Policy Bulletin of the National Association of Real Estate Investment Trusts ("NAREIT"). The NAREIT white paper defines FFO as net income (determined in accordance with GAAP), excluding gains (or losses) from sales and impairments of depreciated property, plus depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures.

Considering the nature of our business as a real estate owner and operator, the Company believes that FFO is helpful to investors in measuring our operational performance because it excludes various items included in net income that do not relate to or are not indicative of our operating performance, such as gains or losses from sales of depreciated property and depreciation and amortization, which can make periodic and peer analyses of operating performance more difficult. For informational purposes, the Company has also provided FFO adjusted for accelerated amortization of debt issuance costs, transaction costs and a severance charge in 2016. The Company believes this supplemental information provides a meaningful measure of our operating performance. The Company believes our presentation of FFO, as adjusted, provides investors with another financial measure that may facilitate comparison of operating performance between periods and among our peer companies. FFO should not be considered as an alternative to net income (determined in accordance with GAAP) as an indicator of our financial performance, is not an alternative to cash flow from operating activities (determined in accordance with GAAP) as a measure of our liquidity, and is not indicative of funds available to satisfy our cash needs, including our ability to make distributions. Our computation of FFO may not be comparable to FFO reported by other REITs that do not define the term in accordance with the current NAREIT definition or that interpret the current NAREIT definition differently than we do. A reconciliation of net income (computed in accordance with GAAP) to FFO is included elsewhere in this Financial Supplement.

p. 5 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

IMPORTANT NOTES INCLUDING NON-GAAP DISCLOSURES (CONTINUED) | | |

Adjusted Funds from Operations

Adjusted Funds From Operations (“AFFO”) is a non-GAAP financial measure of operating performance used by many companies in the REIT industry. AFFO modifies FFO, as adjusted for certain cash and non-cash transactions not included in FFO, as adjusted. AFFO should not be considered an alternative to net income as an indication of the company's performance or as an alternative to cash flow as a measure of liquidity or ability to make distributions. Management considers AFFO a useful supplemental measure of the company’s performance. The Company’s computation of AFFO may differ from the methodology for calculating AFFO used by other REITs, and therefore, may not be comparable to such other REITs. A reconciliation of net income (computed in accordance with GAAP) to AFFO is included elsewhere in this Financial Supplement.

Net Operating Income and Same Property Net Operating Income

The Company uses property net operating income (“NOI”), a non-GAAP financial measure, to evaluate the performance of our properties. The Company defines NOI as income from our real estate, including lease termination fees received from tenants, less our property operating expenses. NOI excludes amortization of capitalized tenant improvement costs and leasing commissions and certain corporate level expenses. The Company believes that NOI is helpful to investors as a measure of our operating performance because it excludes various items included in net income that do not relate to or are not indicative of our operating performance, such as depreciation and amortization, interest expense, and impairment, if any.

The Company also uses same property NOI ("Same Property NOI"), a non-GAAP financial measure, to evaluate the performance of our properties. Same Property NOI excludes properties that have not been owned for the full period presented. It also excludes net gains from outlot sales, straight-line rent revenue, bad debt expense and recoveries, lease termination fees, amortization of lease intangibles and significant prior period expense recoveries and adjustments, if any. The Company believes that Same Property NOI is helpful to investors as a measure of our operating performance because it includes only the NOI of properties that have been owned for the full period presented, which eliminates disparities in net income due to the acquisition or disposition of properties during the particular period presented and thus provides a more consistent metric for the comparison of our properties. The year to date results represent the sum of the individual quarters, as reported.

NOI and Same Property NOI should not, however, be considered as alternatives to net income (calculated in accordance with GAAP) as indicators of our financial performance. Our computation of NOI and Same Property NOI may differ from the methodology used by other REITs, and therefore may not be comparable to such other REITs.

When evaluating the properties that are included in the same property pool, the Company has established specific criteria for determining the inclusion of properties acquired or those recently under development. An acquired property is included in the same property pool when there is a full quarter of operations in both years subsequent to the acquisition date. Development and redevelopment properties are included in the same property pool four full quarters after the properties have been transferred to the operating portfolio. A redevelopment property is first excluded from the same property pool when the execution of a redevelopment plan is likely and the Company begins recapturing space from tenants. For the quarter ended September 30, 2017, the Company excluded eight redevelopment properties and the recently completed Northdale Promenade redevelopment from the same property pool that met these criteria and were owned in both comparable periods.

Earnings Before Interest Expense, Income Tax Expense, Depreciation and Amortization (EBITDA)

The Company defines EBITDA, a non-GAAP financial measure, as net income before depreciation and amortization, interest expense and income tax expense of taxable REIT subsidiary. For informational purposes, the Company has also provided Adjusted EBITDA, which the Company defines as EBITDA less (i) EBITDA from unconsolidated entities, (ii) gains on sales of operating properties or impairment charges, (iii) other income and expense, (iv) noncontrolling interest EBITDA and (v) other non-recurring activity or items impacting comparability from period to period. Annualized Adjusted EBITDA is Adjusted EBITDA for the most recent quarter multiplied by four. Net Debt to Adjusted EBITDA is the Company's share of net debt divided by Annualized Adjusted EBITDA. EBITDA, Adjusted EBITDA, Annualized Adjusted EBITDA and Net Debt to Adjusted EBITDA, as calculated by us, are not comparable to EBITDA and EBITDA-related measures reported by other REITs that do not define EBITDA and EBITDA-related measures exactly as we do. EBITDA, Adjusted EBITDA and Annualized Adjusted EBITDA do not represent cash generated from operating activities in accordance with GAAP, and should not be considered alternatives to net income as an indicator of performance or as alternatives to cash flows from operating activities as an indicator of liquidity.

Considering the nature of our business as a real estate owner and operator, the Company believes that EBITDA, Adjusted EBITDA and the ratio of Net Debt to Adjusted EBITDA are helpful to investors in measuring our operational performance because they exclude various items included in net income that do not relate to or are not indicative of our operating performance, such as gains or losses from sales of depreciated property and depreciation and amortization, which can make periodic and peer analyses of operating performance more difficult. For informational purposes, the Company has also provided Annualized Adjusted EBITDA, adjusted as described above. The Company believes this supplemental information provides a meaningful measure of our operating performance. The Company believes presenting EBITDA and the related measures in this manner allows investors and other interested parties to form a more meaningful assessment of our operating results.

p. 6 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

CONSOLIDATED BALANCE SHEETS (UNAUDITED) | | |

($ in thousands) | ||||||||

September 30, 2017 | December 31, 2016 | |||||||

Assets: | ||||||||

Investment properties, at cost | $ | 3,955,928 | $ | 3,996,065 | ||||

Less: accumulated depreciation | (635,583 | ) | (560,683 | ) | ||||

3,320,345 | 3,435,382 | |||||||

Cash and cash equivalents | 32,465 | 19,874 | ||||||

Tenant and other receivables, including accrued straight-line rent of $30,956 and $28,703 respectively, net of allowance for uncollectible accounts | 53,271 | 53,087 | ||||||

Restricted cash and escrow deposits | 8,878 | 9,037 | ||||||

Deferred costs and intangibles, net | 115,623 | 129,264 | ||||||

Prepaid and other assets | 12,810 | 9,727 | ||||||

Total Assets | $ | 3,543,392 | $ | 3,656,371 | ||||

Liabilities and Shareholders’ Equity: | ||||||||

Mortgage and other indebtedness, net | $ | 1,681,676 | $ | 1,731,074 | ||||

Accounts payable and accrued expenses | 101,574 | 80,664 | ||||||

Deferred revenue and other liabilities | 101,066 | 112,202 | ||||||

Total Liabilities | 1,884,316 | 1,923,940 | ||||||

Commitments and contingencies | ||||||||

Limited Partners’ interests in the Operating Partnership and other redeemable noncontrolling interests | 73,454 | 88,165 | ||||||

Shareholders’ Equity: | ||||||||

Kite Realty Group Trust Shareholders’ Equity: | ||||||||

Common Shares, $.01 par value, 225,000,000 shares authorized, 83,594,068 and 83,545,398 shares issued and outstanding at September 30, 2017 and December 31, 2016, respectively | 836 | 835 | ||||||

Additional paid in capital | 2,068,636 | 2,062,360 | ||||||

Accumulated other comprehensive income (loss) | 1,050 | (316 | ) | |||||

Accumulated deficit | (485,598 | ) | (419,305 | ) | ||||

Total Kite Realty Group Trust Shareholders’ Equity | 1,584,924 | 1,643,574 | ||||||

Noncontrolling Interests | 698 | 692 | ||||||

Total Equity | 1,585,622 | 1,644,266 | ||||||

Total Liabilities and Equity | $ | 3,543,392 | $ | 3,656,371 | ||||

p. 7 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED) | | |

($ in thousands, except per share data) | ||||||||||||||||

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Revenue: | ||||||||||||||||

Minimum rent | $ | 67,585 | $ | 69,518 | $ | 204,926 | $ | 205,436 | ||||||||

Tenant reimbursements | 17,657 | 17,531 | 54,748 | 52,691 | ||||||||||||

Other property related revenue | 1,896 | 2,073 | 10,226 | 7,120 | ||||||||||||

Total revenue | 87,138 | 89,122 | 269,900 | 265,247 | ||||||||||||

Expenses: | ||||||||||||||||

Property operating | 11,859 | 11,916 | 36,950 | 35,454 | ||||||||||||

Real estate taxes | 10,826 | 10,690 | 32,384 | 32,327 | ||||||||||||

General, administrative, and other | 5,431 | 5,081 | 16,389 | 15,228 | ||||||||||||

Transaction costs | — | — | — | 2,771 | ||||||||||||

Impairment charge | — | — | 7,411 | — | ||||||||||||

Depreciation and amortization | 42,793 | 45,543 | 131,333 | 131,625 | ||||||||||||

Total expenses | 70,909 | 73,230 | 224,467 | 217,405 | ||||||||||||

Operating income | 16,229 | 15,892 | 45,433 | 47,842 | ||||||||||||

Interest expense | (16,372 | ) | (17,139 | ) | (49,250 | ) | (47,964 | ) | ||||||||

Income tax benefit (expense) of taxable REIT subsidiary | 33 | (15 | ) | 64 | (763 | ) | ||||||||||

Other expense, net | (94 | ) | — | (314 | ) | (94 | ) | |||||||||

Loss from continuing operations | (204 | ) | (1,262 | ) | (4,067 | ) | (979 | ) | ||||||||

Gains on sales of operating properties | — | — | 15,160 | 194 | ||||||||||||

Net (loss) income | (204 | ) | (1,262 | ) | 11,093 | (785 | ) | |||||||||

Net income attributable to noncontrolling interests | (418 | ) | (420 | ) | (1,528 | ) | (1,391 | ) | ||||||||

Net (loss) income attributable to Kite Realty Group Trust common shareholders | $ | (622 | ) | $ | (1,682 | ) | $ | 9,565 | $ | (2,176 | ) | |||||

(Loss) income per common share - basic | $ | (0.01 | ) | $ | (0.02 | ) | $ | 0.11 | $ | (0.03 | ) | |||||

(Loss) income per common share - diluted | $ | (0.01 | ) | $ | (0.02 | ) | $ | 0.11 | $ | (0.03 | ) | |||||

Weighted average common shares outstanding - basic | 83,594,163 | 83,474,348 | 83,581,847 | 83,399,813 | ||||||||||||

Weighted average common shares outstanding - diluted | 83,594,163 | 83,474,348 | 83,689,590 | 83,399,813 | ||||||||||||

Cash dividends declared per common share | $ | 0.3025 | $ | 0.2875 | $ | 0.9075 | $ | 0.8625 | ||||||||

p. 8 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

FUNDS FROM OPERATIONS1 | | |

($ in thousands, except per share data) | ||||||||||||||||

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Funds From Operations ("FFO") | ||||||||||||||||

Consolidated net (loss) income | $ | (204 | ) | $ | (1,262 | ) | $ | 11,093 | $ | (785 | ) | |||||

Less: net income attributable to noncontrolling interests in properties | (432 | ) | (461 | ) | (1,302 | ) | (1,383 | ) | ||||||||

Less: gains on sales of operating properties | — | — | (15,160 | ) | (194 | ) | ||||||||||

Add: impairment charge | — | — | 7,411 | — | ||||||||||||

Add: depreciation and amortization of consolidated entities, net of noncontrolling interests | 42,474 | 45,310 | 129,890 | 130,909 | ||||||||||||

FFO of the Operating Partnership1 | 41,838 | 43,587 | 131,932 | 128,547 | ||||||||||||

Less: Limited Partners' interests in FFO | (949 | ) | (918 | ) | (2,995 | ) | (2,708 | ) | ||||||||

FFO attributable to Kite Realty Group Trust common shareholders1 | $ | 40,889 | $ | 42,669 | $ | 128,937 | $ | 125,839 | ||||||||

FFO, as defined by NAREIT, per share of the Operating Partnership - basic | $ | 0.49 | $ | 0.51 | $ | 1.54 | $ | 1.51 | ||||||||

FFO, as defined by NAREIT, per share of the Operating Partnership - diluted | $ | 0.49 | $ | 0.51 | $ | 1.54 | $ | 1.50 | ||||||||

FFO of the Operating Partnership1 | $ | 41,838 | $ | 43,587 | $ | 131,932 | $ | 128,547 | ||||||||

Add: accelerated amortization of debt issuance costs (non-cash) | — | 1,121 | — | 1,121 | ||||||||||||

Add: transaction costs | — | — | — | 2,771 | ||||||||||||

Add: severance charge | — | — | — | 500 | ||||||||||||

FFO, as adjusted, of the Operating Partnership | $ | 41,838 | $ | 44,708 | $ | 131,932 | $ | 132,939 | ||||||||

FFO, as adjusted, per share of the Operating Partnership - basic | $ | 0.49 | $ | 0.52 | $ | 1.54 | $ | 1.56 | ||||||||

FFO, as adjusted, per share of the Operating Partnership - diluted | $ | 0.49 | $ | 0.52 | $ | 1.54 | $ | 1.56 | ||||||||

Weighted average common shares outstanding - basic | 83,594,163 | 83,474,348 | 83,581,847 | 83,399,813 | ||||||||||||

Weighted average common shares outstanding - diluted | 83,708,719 | 83,565,227 | 83,689,590 | 83,488,618 | ||||||||||||

Weighted average common shares and units outstanding - basic | 85,580,993 | 85,417,753 | 85,561,343 | 85,336,859 | ||||||||||||

Weighted average common shares and units outstanding - diluted | 85,695,549 | 85,580,632 | 85,669,087 | 85,425,664 | ||||||||||||

FFO, as defined by NAREIT, per diluted share | ||||||||||||||||

Consolidated net (loss) income | $ | — | $ | (0.01 | ) | $ | 0.13 | $ | (0.01 | ) | ||||||

Less: net income attributable to noncontrolling interests in properties | (0.01 | ) | (0.01 | ) | (0.02 | ) | (0.02 | ) | ||||||||

Less: gains on sales of operating properties | — | — | (0.18 | ) | — | |||||||||||

Add: impairment charge | — | — | 0.09 | — | ||||||||||||

Add: depreciation and amortization of consolidated entities, net of noncontrolling interests | 0.50 | 0.53 | 1.52 | 1.53 | ||||||||||||

FFO, as defined by NAREIT, of the Operating Partnership per diluted share1 | $ | 0.49 | $ | 0.51 | $ | 1.54 | $ | 1.50 | ||||||||

Add: accelerated amortization of debt issuance costs | — | 0.01 | — | 0.01 | ||||||||||||

Add: transaction costs | — | — | — | 0.04 | ||||||||||||

Add: severance charge | — | — | — | 0.01 | ||||||||||||

FFO, as adjusted, of the Operating Partnership per diluted share | $ | 0.49 | $ | 0.52 | $ | 1.54 | $ | 1.56 | ||||||||

____________________ | |

1 | “FFO of the Operating Partnership" measures 100% of the operating performance of the Operating Partnership’s real estate properties. “FFO attributable to Kite Realty Group Trust common shareholders” reflects a reduction for the redeemable noncontrolling weighted average diluted interest in the Operating Partnership. |

p. 9 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

ADJUSTED FUNDS FROM OPERATIONS AND OTHER FINANCIAL INFORMATION | | |

($ in thousands) | ||||||||||||||||

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Reconciliation of FFO, as adjusted, to Adjusted Funds from Operations (AFFO) | ||||||||||||||||

FFO, as adjusted, of the Operating Partnership | $ | 41,838 | $ | 44,708 | $ | 131,932 | $ | 132,939 | ||||||||

Add: | ||||||||||||||||

Depreciation of non-real estate assets | 319 | 233 | 1,450 | 763 | ||||||||||||

Amortization of deferred financing costs | 664 | 992 | 2,014 | 2,624 | ||||||||||||

Non-cash compensation expense | 1,253 | 1,126 | 3,732 | 3,340 | ||||||||||||

Less: | ||||||||||||||||

Straight-line rent | 1,173 | 1,477 | 3,593 | 4,312 | ||||||||||||

Market rent amortization income | 715 | 2,569 | 2,515 | 5,821 | ||||||||||||

Amortization of debt premium | 713 | 880 | 2,200 | 3,008 | ||||||||||||

Other cash and non-cash adjustments1 | — | — | 866 | 3,271 | ||||||||||||

Capital expenditures2: | ||||||||||||||||

Maintenance capital expenditures3 | 983 | 468 | 2,224 | 1,002 | ||||||||||||

Revenue enhancing tenant improvements – retail | 1,825 | 1,930 | 11,554 | 6,132 | ||||||||||||

Revenue enhancing tenant improvements – office | 144 | — | 461 | — | ||||||||||||

External lease commissions | 327 | 486 | 1,426 | 1,455 | ||||||||||||

Total AFFO of the Operating Partnership | $ | 38,194 | $ | 39,249 | $ | 114,289 | $ | 114,665 | ||||||||

Other Financial Information: | ||||||||||||||||

Scheduled debt principal payments | $ | 1,320 | $ | 1,297 | $ | 3,709 | $ | 2,990 | ||||||||

Capitalized interest cost | 787 | 865 | 2,320 | 2,396 | ||||||||||||

Mark to market lease amount in Deferred revenue and other liabilities on consolidated balance sheet | 85,163 | 100,972 | ||||||||||||||

Acreage of undeveloped, vacant land in the operating portfolio4 | 46.9 | |||||||||||||||

September 30, 2017 | December 31, 2016 | |||||||

Investment properties, at cost: | ||||||||

Land, building and improvements4 | $ | 3,838,665 | $ | 3,885,223 | ||||

Furniture, equipment and other | 7,890 | 7,246 | ||||||

Land held for development | 31,142 | 34,171 | ||||||

Construction in progress | 78,231 | 69,425 | ||||||

Total | $ | 3,955,928 | $ | 3,996,065 | ||||

____________________ | |

1 | Reflects a non-cash termination fee for the quarter ended March 31, 2017 and terminated transaction costs and a severance charge for the nine months ended September 30, 2016. |

2 | Excludes landlord work, tenant improvements and leasing commissions relating to development and redevelopment projects. |

3 | A portion of these capital improvements are reimbursed by tenants and are revenue producing. |

4 | Includes undeveloped vacant land with a book value of $21.0 million at September 30, 2017. |

p. 10 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

MARKET CAPITALIZATION AS OF SEPTEMBER 30, 2017 | | |

($ in thousands) | ||||||||||

Percent of Total Equity | Total Market Capitalization | Percent of Total Market Capitalization | ||||||||

Equity Capitalization: | ||||||||||

Total Common Shares Outstanding | 97.7 | % | 83,594,068 | |||||||

Operating Partnership ("OP") Units Outstanding | 2.3 | % | 1,986,830 | |||||||

Combined Common Shares and OP Units | 100.0 | % | 85,580,898 | |||||||

Market Price of Common Shares | $ | 20.25 | ||||||||

Total Equity Capitalization | 1,733,013 | 52 | % | |||||||

Debt Capitalization: | ||||||||||

Company Consolidated Outstanding Debt | 1,681,676 | |||||||||

Plus: Debt Premium and Issuance Costs, net | 1,214 | |||||||||

Less: Partner Share of Consolidated Joint Venture Debt1 | (13,373 | ) | ||||||||

Company Share of Outstanding Debt | 1,669,517 | |||||||||

Less: Cash, Cash Equivalents, and Restricted Cash | (41,343 | ) | ||||||||

Total Net Debt Capitalization | 1,628,174 | 48 | % | |||||||

Total Enterprise Value | $ | 3,361,187 | 100 | % | ||||||

RATIO OF DEBT TO TOTAL UNDEPRECIATED ASSETS AS OF SEPTEMBER 30, 2017 | ||||||||||

Consolidated Undepreciated Real Estate Assets | $ | 3,955,928 | ||||||||

Company Share of Unconsolidated Real Estate Assets2 | 2,500 | |||||||||

3,958,428 | ||||||||||

Total Consolidated Debt | 1,681,676 | |||||||||

Less: Debt Premium and Issuance Costs, net | 1,214 | |||||||||

Less: Cash, Cash Equivalents, and Restricted Cash | (41,343 | ) | ||||||||

$ | 1,641,547 | |||||||||

Ratio of Debt to Total Undepreciated Real Estate Assets | 41.5 | % | ||||||||

RATIO OF COMPANY SHARE OF NET DEBT TO EBITDA AS OF SEPTEMBER 30, 2017 | ||||||||||

Company Share of Consolidated Debt | $ | 1,669,517 | ||||||||

Less: Cash, Cash Equivalents, and Restricted Cash | (41,343 | ) | ||||||||

1,628,174 | ||||||||||

Q3 2017 EBITDA, Annualized: | ||||||||||

- Consolidated EBITDA | $ | 236,088 | ||||||||

- Unconsolidated EBITDA | 137 | |||||||||

- Minority Interest EBITDA1 | (1,728 | ) | 234,497 | |||||||

Ratio of Company Share of Net Debt to EBITDA | 6.9x | |||||||||

____________________ | |||||

1 | See page 14 for details. | ||||

2 | Included in Prepaid and other assets on Consolidated Balance Sheets. | ||||

p. 11 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

SAME PROPERTY NET OPERATING INCOME (NOI) | | |

($ in thousands) | |||||||||||||||||||

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||

2017 | 2016 | % Change | 2017 | 2016 | % Change | ||||||||||||||

Number of properties for the quarter1 | 104 | 104 | |||||||||||||||||

Leased percentage at period end | 94.4 | % | 95.1 | % | 94.4 | % | 95.1 | % | |||||||||||

Economic Occupancy percentage2 | 93.5 | % | 92.8 | % | 93.7 | % | 92.9 | % | |||||||||||

Minimum rent | $ | 58,806 | $ | 56,997 | $ | 175,615 | $ | 170,713 | |||||||||||

Tenant recoveries | 16,014 | 15,320 | 49,073 | 46,961 | |||||||||||||||

Other income | 385 | 457 | 839 | 721 | |||||||||||||||

75,205 | 72,774 | 225,527 | 218,395 | ||||||||||||||||

Property operating expenses | (10,136 | ) | (10,041 | ) | (29,883 | ) | (28,956 | ) | |||||||||||

Real estate taxes | (9,820 | ) | (9,413 | ) | (29,808 | ) | (28,923 | ) | |||||||||||

(19,956 | ) | (19,454 | ) | (59,691 | ) | (57,879 | ) | ||||||||||||

Same Property NOI3 | $ | 55,249 | $ | 53,320 | 3.6% | $ | 165,836 | $ | 160,516 | 3.3% | |||||||||

Same Property NOI - excluding the impact of the 3-R initiative4 | 3.9% | 3.9% | |||||||||||||||||

Reconciliation of Same Property NOI to Most Directly Comparable GAAP Measure: | |||||||||||||||||||

Net operating income - same properties | $ | 55,249 | $ | 53,320 | $ | 165,836 | $ | 160,516 | |||||||||||

Net operating income - non-same activity5 | 9,614 | 13,561 | 36,611 | 38,191 | |||||||||||||||

Provision for bad debts - same properties | (410 | ) | (365 | ) | (1,881 | ) | (1,241 | ) | |||||||||||

Other expense, net | (61 | ) | (15 | ) | (250 | ) | (857 | ) | |||||||||||

General, administrative and other | (5,431 | ) | (5,081 | ) | (16,389 | ) | (15,228 | ) | |||||||||||

Transaction costs | — | — | — | (2,771 | ) | ||||||||||||||

Impairment charge | — | — | (7,411 | ) | — | ||||||||||||||

Depreciation and amortization expense | (42,793 | ) | (45,543 | ) | (131,333 | ) | (131,625 | ) | |||||||||||

Interest expense | (16,372 | ) | (17,139 | ) | (49,250 | ) | (47,964 | ) | |||||||||||

Gains on sales of operating properties | — | — | 15,160 | 194 | |||||||||||||||

Net income attributable to noncontrolling interests | (418 | ) | (420 | ) | (1,528 | ) | (1,391 | ) | |||||||||||

Net (loss) income attributable to common shareholders | $ | (622 | ) | $ | (1,682 | ) | $ | 9,565 | $ | (2,176 | ) | ||||||||

____________________ | |

1 | Same Property NOI excludes eight properties in redevelopment, the recently completed Northdale Promenade redevelopment as well as office properties (Thirty South Meridian and Eddy Street Commons). |

2 | Excludes leases that are signed but for which tenants have not yet commenced the payment of cash rent. Calculated as a weighted average based on the timing of cash rent commencement and expiration during the period. |

3 | Same Property NOI excludes net gains from outlot sales, straight-line rent revenue, bad debt expense and recoveries, lease termination fees, amortization of lease intangibles and significant prior period expense recoveries and adjustments, if any. |

4 | See pages 27 and 28 for further detail of the properties included in the 3-R initiative. |

5 | Includes non-cash activity across the portfolio as well as net operating income from properties not included in the same property pool. |

p. 12 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

NET OPERATING INCOME BY QUARTER | | |

($ in thousands) | ||||||||||||||||||||

Three Months Ended | ||||||||||||||||||||

September 30, 2017 | June 30, 2017 | March 31, 2017 | December 31, 2016 | September 30, 2016 | ||||||||||||||||

Revenue: | ||||||||||||||||||||

Minimum rent1 | $ | 67,585 | $ | 68,395 | $ | 68,946 | $ | 68,622 | $ | 69,518 | ||||||||||

Tenant reimbursements | 17,657 | 18,521 | 18,570 | 17,791 | 17,531 | |||||||||||||||

Other property related revenue2 | 1,252 | 5,267 | 1,858 | 1,016 | 1,198 | |||||||||||||||

Overage rent | 82 | 16 | 266 | 904 | 315 | |||||||||||||||

Parking revenue, net3 | 138 | 137 | 81 | 188 | 159 | |||||||||||||||

86,714 | 92,336 | 89,721 | 88,521 | 88,721 | ||||||||||||||||

Expenses: | ||||||||||||||||||||

Property operating - Recoverable4 | 9,533 | 9,386 | 10,376 | 9,986 | 9,599 | |||||||||||||||

Property operating - Non-Recoverable4 | 2,053 | 2,573 | 2,318 | 2,172 | 2,091 | |||||||||||||||

Real estate taxes | 10,675 | 11,095 | 10,198 | 10,469 | 10,515 | |||||||||||||||

22,261 | 23,054 | 22,892 | 22,627 | 22,205 | ||||||||||||||||

Net Operating Income - Properties | 64,453 | 69,282 | 66,829 | 65,894 | 66,516 | |||||||||||||||

Other Expenses: | ||||||||||||||||||||

General, administrative, and other | (5,431 | ) | (5,488 | ) | (5,470 | ) | (5,375 | ) | (5,081 | ) | ||||||||||

Impairment charge | — | — | (7,411 | ) | — | — | ||||||||||||||

(5,431 | ) | (5,488 | ) | (12,881 | ) | (5,375 | ) | (5,081 | ) | |||||||||||

Earnings Before Interest, Taxes, Depreciation and Amortization | 59,022 | 63,794 | 53,948 | 60,519 | 61,435 | |||||||||||||||

Depreciation and amortization | (42,793 | ) | (42,710 | ) | (45,830 | ) | (42,939 | ) | (45,543 | ) | ||||||||||

Interest expense | (16,372 | ) | (16,433 | ) | (16,445 | ) | (17,613 | ) | (17,139 | ) | ||||||||||

Income tax benefit (expense) of taxable REIT subsidiary | 33 | (3 | ) | 33 | (51 | ) | (15 | ) | ||||||||||||

Other expense, net | (94 | ) | (80 | ) | (139 | ) | (75 | ) | — | |||||||||||

(Loss) Income From Continuing Operations | (204 | ) | 4,568 | (8,433 | ) | (159 | ) | (1,262 | ) | |||||||||||

Gains on sales of operating properties | — | 6,290 | 8,870 | 4,059 | — | |||||||||||||||

Net (loss) income | (204 | ) | 10,858 | 437 | 3,900 | (1,262 | ) | |||||||||||||

Less: Net income attributable to noncontrolling interests | (418 | ) | (678 | ) | (432 | ) | (541 | ) | (420 | ) | ||||||||||

Net (loss) income attributable to Kite Realty Group Trust | $ | (622 | ) | $ | 10,180 | $ | 5 | $ | 3,359 | $ | (1,682 | ) | ||||||||

NOI/Revenue | 74.3 | % | 75.0 | % | 74.5 | % | 74.4 | % | 75.0 | % | ||||||||||

Recovery Ratios5 | ||||||||||||||||||||

- Retail Properties | 89.9 | % | 93.1 | % | 92.0 | % | 89.2 | % | 89.4 | % | ||||||||||

- Consolidated | 87.4 | % | 90.4 | % | 90.3 | % | 87.0 | % | 87.2 | % | ||||||||||

____________________ | |

1 | Minimum rent includes $5.0 million in ground lease-related revenue for the three months ended September 30, 2017. |

2 | Other property related revenue for the three months ended September 30, 2017 includes $0.6 million of lease termination income and a $0.4 million gain on the sale of a land parcel. |

3 | Parking revenue, net represents the net operating results of the Eddy Street Parking Garage and the Union Station Parking Garage. In the three months ended September 30, 2017, this amount was calculated as revenue of $499,000 less real estate taxes and property operating expenses of $209,000 and $152,000, respectively. |

4 | Recoverable expenses include total management fee expense (or recurring G&A expense of $1.3 million) allocable to the property operations in the three months ended September 30, 2017, a portion of which is recoverable. Non-recoverable expenses primarily include bad debt provision, ground rent, and professional fees. |

5 | “Recovery Ratio” is computed by dividing tenant reimbursements by the sum of recoverable property operating expense and real estate tax expense. |

p. 13 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

CONSOLIDATED JOINT VENTURE SUMMARY - SEPTEMBER 30, 2017 | | |

($ in thousands)

Ownership | ||||||||||||||

Joint Venture Entity | Location (MSA) | Owned GLA | KRG Ownership % | Current KRG Economic Ownership%1 | ||||||||||

Delray Marketplace | Delray, FL | 260,255 | 50% | 98% | ||||||||||

Pan Am Plaza | Indianapolis, IN | — | 85% | 85% | ||||||||||

Crossing at Killingly Commons | Killingly, CT | 208,929 | 55% | 90% | ||||||||||

Territory Portfolio2 | Las Vegas, NV | 847,690 | 78% | 94% | ||||||||||

Balance Sheet | Current Partner Economic Ownership % | |||||||||||||

Joint Venture Entity | Debt Balance | Partner Share of Debt | Redeemable Noncontrolling Interest | |||||||||||

Delray Marketplace | $ | 56,850 | 2% | $ | 1,138 | $ | — | |||||||

Pan Am Plaza | — | 15% | — | — | ||||||||||

Crossing at Killingly Commons | 33,000 | 10% | 3,300 | 10,070 | ||||||||||

Territory Portfolio2 | 148,940 | 6% | 8,935 | 22,461 | ||||||||||

Total | $ | 238,790 | $ | 13,373 | $ | 32,531 | ||||||||

Income Statement | ||||||||||||||

Joint Venture Entity | Quarterly Minority Interest | Annualized Minority Interest | ||||||||||||

Delray Marketplace | $ | — | $ | — | KRG has an 8% cumulative preferred return | |||||||||

Pan Am Plaza | — | — | Project currently in Land Held For Development | |||||||||||

Crossing at Killingly Commons | 132 | 528 | Partner receives a fixed annual preferred payment of 5.5% on $9.6 million | |||||||||||

Territory Portfolio2 | 300 | 1,200 | Partner receives a fixed annual preferred payment of 4% on $30 million | |||||||||||

Total | $ | 432 | $ | 1,728 | ||||||||||

____________________ | |||||||

1 | Economic ownership % represents the Company's share of cash flow. | ||||||

2 | Joint Venture includes six operating properties located in Las Vegas, Nevada. During the quarter, our partner exercised its option to have the Company redeem a portion of its ownership interest in the joint venture. Our partner has elected to redeem $8.1 million of its interest for cash. The Company can determine the timing of closing, but it must occur before December 27, 2017. | ||||||

p. 14 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

SUMMARY OF OUTSTANDING DEBT AS OF SEPTEMBER 30, 2017 | | |

($ in thousands) | ||||||||||||

TOTAL OUTSTANDING DEBT1 | ||||||||||||

Outstanding Amount | Ratio | Weighted Average Interest Rate | Weighted Average Maturity (in years) | |||||||||

Fixed Rate Debt | $ | 1,588,505 | 94 | % | 4.08 | % | 5.8 | |||||

Variable Rate Debt | 94,385 | 6 | % | 2.73 | % | 4.4 | ||||||

Net Debt Premiums and Issuance Costs, Net | (1,214 | ) | N/A | N/A | N/A | |||||||

Total | $ | 1,681,676 | 100 | % | 4.00 | % | 5.7 | |||||

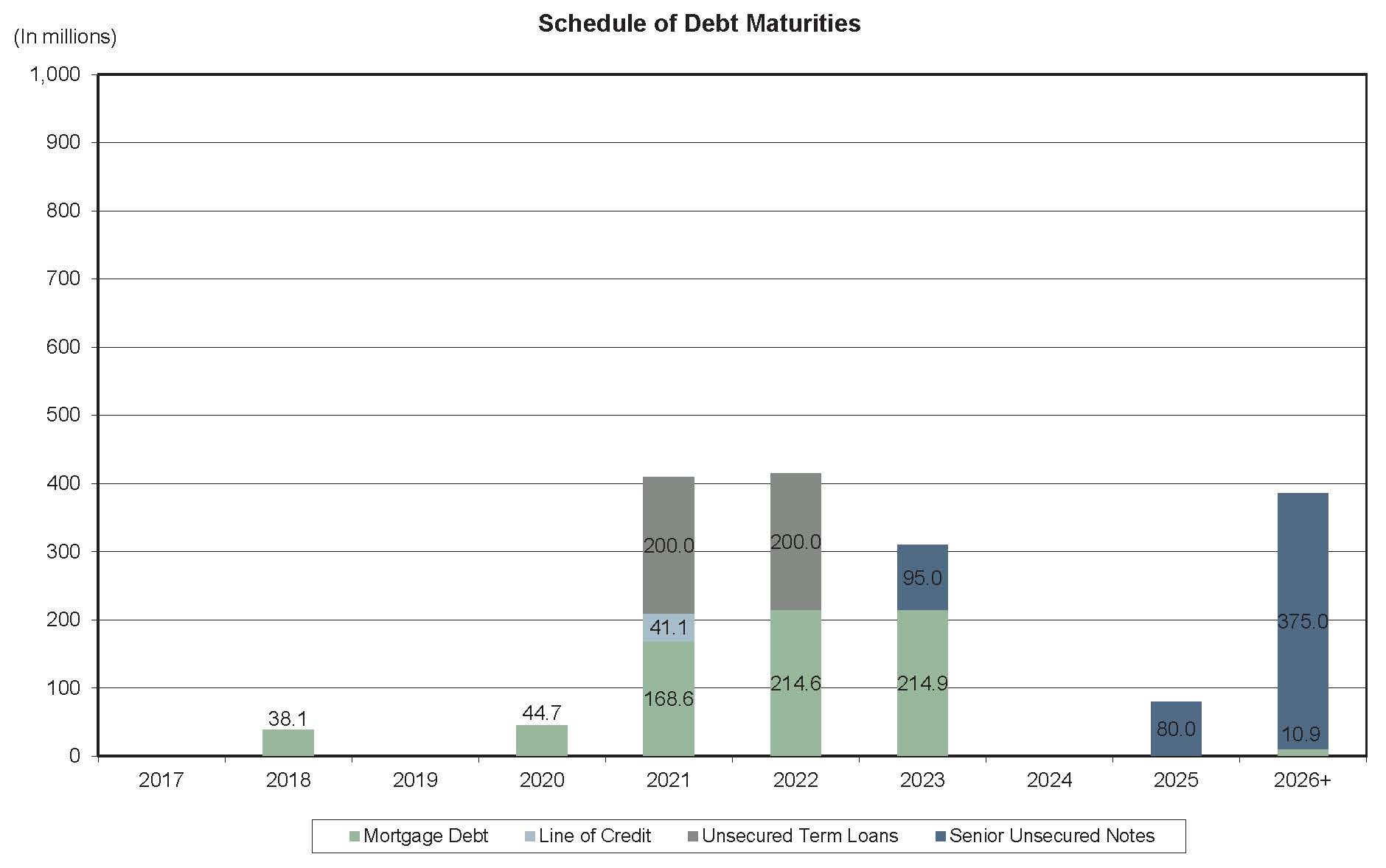

SCHEDULE OF MATURITIES BY YEAR | ||||||||||||||||

Secured Debt | ||||||||||||||||

Scheduled Principal Payments | Term Maturities | Unsecured Debt2 | Total Outstanding Debt | |||||||||||||

2017 | $ | 1,241 | $ | — | $ | — | $ | 1,241 | ||||||||

2018 | 5,635 | 37,584 | — | 43,219 | ||||||||||||

2019 | 5,975 | — | — | 5,975 | ||||||||||||

2020 | 5,920 | 42,339 | — | 48,259 | ||||||||||||

2021 | 4,624 | 159,875 | 241,100 | 405,599 | ||||||||||||

2022 | 1,113 | 205,208 | 200,000 | 406,321 | ||||||||||||

2023 | 806 | 214,940 | 95,000 | 310,746 | ||||||||||||

2024 | 854 | — | — | 854,000 | ||||||||||||

2025 | 904 | — | 80,000 | 80,904 | ||||||||||||

2026 And Beyond | 4,672 | 100 | 375,000 | 379,772 | ||||||||||||

Net Debt Premiums and Issuance Costs, Net | (1,214 | ) | — | — | (1,214 | ) | ||||||||||

Total | $ | 30,530 | $ | 660,046 | $ | 991,100 | $ | 1,681,676 | ||||||||

____________________ | |

1 | Fixed rate debt includes, and variable rate date excludes, the portion of such debt that has been hedged by interest rate derivatives. As of September 30, 2017, $460.5 million in variable rate debt is hedged for a weighted average 2.0 years. |

2 | This presentation reflects the Company's exercise of its option to extend the maturity date by one year to July 28, 2021 for the Company's unsecured credit facility. |

|

____________________ | |

1 | Chart excludes annual principal payments and net premiums on fixed rate debt. |

p. 15 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

MATURITY SCHEDULE OF OUTSTANDING DEBT AS OF SEPTEMBER 30, 2017 | | |

($ in thousands) | |||||||||||||

Property | Lender | Interest Rate1 | Maturity Date | Balance as of June 30, 2017 | % of Total Outstanding | ||||||||

Whitehall Pike | CMBS | 6.71 | % | 7/5/2018 | $ | 4,723 | |||||||

Perimeter Woods | Jackson National Life Insurance | 6.02 | % | 9/1/2018 | 33,330 | ||||||||

2018 Debt Maturities | 38,053 | 2.3 | % | ||||||||||

2019 Debt Maturities | — | — | % | ||||||||||

Fishers Station | Old National Bank | LIBOR + 225 | 1/4/2020 | 6,633 | |||||||||

Lake City Commons/12th Street Plaza/University Town Center II | CMBS | 5.70 | % | 9/1/2020 | 20,700 | ||||||||

Thirty South | Associated Bank | LIBOR + 205 | 12/31/2020 | 17,331 | |||||||||

2020 Debt Maturities | 44,664 | 2.7 | % | ||||||||||

Waxahachie Crossing | CMBS | 5.55 | % | 3/1/2021 | 7,750 | ||||||||

International Speedway Square | CMBS | 5.77 | % | 4/1/2021 | 19,107 | ||||||||

Lima Marketplace | CMBS | 5.80 | % | 4/1/2021 | 8,383 | ||||||||

Bell Oaks Centre | CMBS | 5.59 | % | 4/1/2021 | 6,548 | ||||||||

Northcrest Shopping Center | CMBS | 5.48 | % | 5/1/2021 | 15,780 | ||||||||

University Town Center | CMBS | 5.48 | % | 6/1/2021 | 18,690 | ||||||||

Village at Bay Park | CMBS | 5.58 | % | 6/1/2021 | 9,183 | ||||||||

Silver Springs Pointe | CMBS | 5.03 | % | 7/1/2021 | 8,800 | ||||||||

Lake Mary Plaza | CMBS | 5.10 | % | 7/1/2021 | 5,080 | ||||||||

Unsecured Credit Facility3,4 | KeyBank (Admin. Agent) | LIBOR + 135 | 7/28/2021 | 41,100 | |||||||||

Unsecured Term Loan4 | KeyBank (Admin. Agent) | LIBOR + 130 | 7/28/2021 | 200,000 | |||||||||

Bayport Commons | CMBS | 5.44 | % | 9/1/2021 | 11,963 | ||||||||

Eddy Street Commons | CMBS | 5.44 | % | 9/1/2021 | 23,205 | ||||||||

Four Property Pool Loan | CMBS | 5.44 | % | 9/1/2021 | 34,143 | ||||||||

2021 Debt Maturities | 409,732 | 24.3 | % | ||||||||||

Centre at Panola, Phase I | CMBS | 6.78 | % | 1/1/2022 | 1,747 | ||||||||

Delray Marketplace2 | Bank of America | LIBOR + 160 | 2/5/2022 | 56,850 | |||||||||

Palm Coast Landing | CMBS | 5.00 | % | 3/1/2022 | 22,358 | ||||||||

Bayonne Crossing | CMBS | 4.33 | % | 4/1/2022 | 44,692 | ||||||||

Saxon Crossing | CMBS | 4.65 | % | 7/1/2022 | 11,400 | ||||||||

Merrimack Village Center | CMBS | 4.36 | % | 7/6/2022 | 5,445 | ||||||||

Shops at Moore | CMBS | 4.29 | % | 9/1/2022 | 21,300 | ||||||||

Shops at Julington Creek | CMBS | 4.60 | % | 9/1/2022 | 4,785 | ||||||||

Centre Point Commons | CMBS | 4.34 | % | 10/1/2022 | 14,410 | ||||||||

Unsecured Term Loan4 | KeyBank (Admin. Agent) | LIBOR + 160 | 10/26/2022 | 200,000 | |||||||||

Miramar Square | CMBS | 4.16 | % | 12/1/2022 | 31,625 | ||||||||

2022 Debt Maturities | 414,612 | 24.6 | % | ||||||||||

See footnotes on next page | |||||||||||||

p. 16 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

MATURITY SCHEDULE OF OUTSTANDING DEBT AS OF SEPTEMBER 30, 2017 (CONTINUED) | | |

($ in thousands) | |||||||||||||

Property | Lender | Interest Rate1 | Maturity Date | Balance as of June 30, 2017 | % of Total Outstanding | ||||||||

Centennial Gateway / Eastgate 5 | CMBS | 3.81 | % | 1/1/2023 | $ | 44,385 | |||||||

Crossing at Killingly Commons 5 | Huntington Bank | LIBOR + 170 | 1/1/2023 | 33,000 | |||||||||

Centennial Center 5 | CMBS | 3.83 | % | 1/6/2023 | 70,455 | ||||||||

Eastern Beltway 5 | CMBS | 3.83 | % | 1/6/2023 | 34,100 | ||||||||

The Corner | CMBS | 4.10 | % | 3/1/2023 | 14,750 | ||||||||

Chapel Hill | CMBS | 3.78 | % | 4/1/2023 | 18,250 | ||||||||

Senior Unsecured Note | Various | 4.23 | % | 9/10/2023 | 95,000 | ||||||||

2023 Debt Maturities | 309,940 | 18.4 | % | ||||||||||

Senior Unsecured Note | Various | 4.47 | % | 9/10/2025 | 80,000 | ||||||||

Senior Unsecured Note | Various | 4.00 | % | 10/1/2026 | 300,000 | ||||||||

Senior Unsecured Note | Various | 4.57 | % | 9/10/2027 | 75,000 | ||||||||

Rampart Commons | CMBS | 5.73 | % | 6/10/2030 | 10,889 | ||||||||

2024 And Beyond Debt Maturities | 465,889 | 27.7 | % | ||||||||||

NET PREMIUMS ON ACQUIRED DEBT & ISSUANCE COSTS | (1,214 | ) | |||||||||||

TOTAL DEBT PER CONSOLIDATED BALANCE SHEET | $ | 1,681,676 | |||||||||||

____________________ | |

1 | At September 29, 2017, one-month LIBOR was 1.23%. |

2 | Property is held in a joint venture. The loan is guaranteed by Kite Realty Group, LP. See Joint Venture Summary on page 14 for additional detail. |

3 | Assumes Company exercises its option to extend the maturity date by one year |

4 | The Company has 100 unencumbered properties of which 93 are wholly owned and included in the unencumbered property pool of our unsecured facilities. |

5 | Property is held in a joint venture. See Joint Venture Summary on page 14 for additional detail. |

p. 17 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

UNSECURED PUBLIC DEBT COVENANTS | |

September 30, 2017 | Threshold1 | |||||

Total Debt to Undepreciated Assets | 41.0% | <60% | ||||

Secured Debt to Undepreciated Assets | 16.8% | <40% | ||||

Undepreciated Unencumbered Assets to Unsecured Debt | 266.1% | >150% | ||||

Debt Service Coverage | 3.4x | >1.5x | ||||

Senior Unsecured Debt Ratings: | ||||||

Moody's Investors Service | Baa3/Stable | |||||

Standard & Poor's Rating Services | BBB-/Stable | |||||

Liquidity ($ in thousands) | ||||||

Cash and cash equivalents | $ | 32,465 | ||||

Availability under unsecured credit facility | 394,083 | |||||

$ | 426,548 | |||||

____________________ | ||||

1 | For a complete listing of all Debt Covenants related to the Company's Senior Unsecured Notes, as well as definitions of the terms, refer to the Company's filings with the SEC. | |||

p. 18 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

TOP 10 RETAIL TENANTS BY TOTAL GROSS LEASABLE AREA (GLA) | | |

As of September 30, 2017

This table includes the following:

• | Operating retail properties; |

• | Operating office properties; and |

• | Development/Redevelopment property tenants open for business or ground lease tenants who commenced paying rent as of September 30, 2017. |

Tenant | Number of Locations | Total GLA | Number of Leases | Company Owned GLA | Ground Lease GLA | Number of Anchor Owned Locations | Anchor Owned GLA | ||||||||||||||

Wal-Mart Stores, Inc.1 | 15 | 2,578,323 | 6 | 203,742 | 811,956 | 9 | 1,562,625 | ||||||||||||||

Target Corporation | 15 | 2,175,101 | — | — | — | 15 | 2,175,101 | ||||||||||||||

Lowe's Companies, Inc. | 14 | 2,072,666 | 5 | 128,997 | 650,161 | 9 | 1,293,508 | ||||||||||||||

Home Depot Inc. | 6 | 788,167 | 1 | — | 131,858 | 5 | 656,309 | ||||||||||||||

Kohl's Corporation | 9 | 782,386 | 5 | 184,516 | 244,010 | 4 | 353,860 | ||||||||||||||

Publix Super Markets, Inc. | 14 | 670,665 | 14 | 670,665 | — | — | — | ||||||||||||||

The TJX Companies, Inc.2 | 22 | 656,931 | 22 | 656,931 | — | — | — | ||||||||||||||

Ross Stores, Inc. | 18 | 510,707 | 18 | 510,707 | — | — | — | ||||||||||||||

Bed Bath & Beyond, Inc.3 | 19 | 493,719 | 19 | 493,719 | — | — | — | ||||||||||||||

Petsmart, Inc. | 19 | 390,843 | 19 | 390,843 | — | — | — | ||||||||||||||

Total | 151 | 11,119,508 | 109 | 3,240,120 | 1,837,985 | 42 | 6,041,403 | ||||||||||||||

____________________ | |

1 | Includes Sam's Club, which is owned by the same parent company. |

2 | Includes TJ Maxx (13), Home Goods (2) and Marshalls (7), all of which are owned by the same parent company. |

3 | Includes Buy Buy Baby (4), Christmas Tree Shops (1) and Cost Plus (3), all of which are owned by the same parent company. |

p. 19 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

TOP 25 TENANTS BY ANNUALIZED BASE RENT | | |

As of September 30, 2017

($ in thousands, except per square foot data)

This table includes the following:

• | Operating retail properties; |

• | Operating office properties; and |

• | Development/Redevelopment property tenants open for business or ground lease tenants who commenced paying rent as of September 30, 2017. |

Tenant | Number of Stores | Leased GLA/NRA1 | % of Owned GLA/NRA of the Portfolio | Annualized Base Rent2,3 | Annualized Base Rent per Sq. Ft.3 | % of Total Portfolio Annualized Base Rent3 | |||||||||||||

The TJX Companies, Inc.4 | 22 | 656,931 | 2.7 | % | $ | 6,820 | $ | 10.38 | 2.5 | % | |||||||||

Publix Super Markets, Inc. | 14 | 670,665 | 2.7 | % | 6,739 | 10.05 | 2.5 | % | |||||||||||

Petsmart, Inc. | 19 | 390,843 | 1.6 | % | 6,152 | 15.74 | 2.2 | % | |||||||||||

Bed Bath & Beyond, Inc.5 | 19 | 493,719 | 2.0 | % | 6,050 | 12.25 | 2.2 | % | |||||||||||

Ross Stores, Inc. | 18 | 510,707 | 2.1 | % | 5,791 | 11.34 | 2.1 | % | |||||||||||

Lowe's Companies, Inc. | 5 | 128,997 | 0.5 | % | 5,039 | 6.47 | 1.8 | % | |||||||||||

Office Depot (9) / Office Max (6) | 15 | 307,788 | 1.3 | % | 4,242 | 13.78 | 1.6 | % | |||||||||||

Dick's Sporting Goods, Inc.6 | 8 | 390,502 | 1.6 | % | 4,167 | 10.67 | 1.5 | % | |||||||||||

Ascena Retail Group7 | 34 | 206,082 | 0.8 | % | 4,140 | 20.09 | 1.5 | % | |||||||||||

Nordstrom, Inc. | 6 | 197,845 | 0.8 | % | 3,918 | 19.80 | 1.4 | % | |||||||||||

Michaels Stores, Inc. | 14 | 295,066 | 1.2 | % | 3,884 | 13.16 | 1.4 | % | |||||||||||

Wal-Mart Stores, Inc.8 | 6 | 203,742 | 0.8 | % | 3,655 | 3.60 | 1.3 | % | |||||||||||

LA Fitness | 5 | 208,209 | 0.8 | % | 3,447 | 16.56 | 1.3 | % | |||||||||||

Best Buy Co., Inc. | 6 | 213,604 | 0.9 | % | 3,069 | 14.37 | 1.1 | % | |||||||||||

Kohl's Corporation | 5 | 184,516 | 0.8 | % | 2,927 | 6.83 | 1.1 | % | |||||||||||

Toys "R" Us, Inc.9 | 6 | 179,316 | 0.7 | % | 2,924 | 11.82 | 1.1 | % | |||||||||||

Mattress Firm Holdings Corp (18) / Sleepy's (5) | 23 | 105,001 | 0.4 | % | 2,903 | 27.65 | 1.1 | % | |||||||||||

National Amusements | 1 | 80,000 | 0.3 | % | 2,898 | 36.22 | 1.1 | % | |||||||||||

Petco Animal Supplies, Inc. | 12 | 167,455 | 0.7 | % | 2,804 | 16.74 | 1.0 | % | |||||||||||

DSW Inc. | 9 | 175,133 | 0.7 | % | 2,491 | 14.22 | 0.9 | % | |||||||||||

Stein Mart, Inc. | 9 | 307,222 | 1.3 | % | 2,378 | 7.74 | 0.9 | % | |||||||||||

Ulta Beauty, Inc. | 11 | 117,451 | 0.5 | % | 2,317 | 19.73 | 0.8 | % | |||||||||||

Frank Theatres | 2 | 122,224 | 0.5 | % | 2,311 | 18.91 | 0.8 | % | |||||||||||

Walgreens Boots Alliance, Inc. | 4 | 67,212 | 0.3 | % | 2,099 | 31.23 | 0.8 | % | |||||||||||

The Gap, Inc. / Old Navy (9) | 9 | 148,401 | 0.6 | % | 2,079 | 14.01 | 0.8 | % | |||||||||||

TOTAL | 282 | 6,528,631 | 26.6 | % | $ | 95,245 | $ | 11.52 | 34.8 | % | |||||||||

____________________ | |

1 | Excludes the estimated size of the structures located on land owned by the Company and ground leased to tenants. |

2 | Annualized base rent represents the monthly contractual rent for September 30, 2017 for each applicable tenant multiplied by 12. Annualized base rent does not include tenant reimbursements. |

3 | Annualized base rent and percent of total portfolio includes ground lease rent. |

4 | Includes TJ Maxx (13), Marshalls (7) and HomeGoods (2), all of which are owned by the same parent company. |

5 | Includes Bed Bath and Beyond (11), Buy Buy Baby (4) Christmas Tree Shops (1) and Cost Plus (3), all of which are owned by the same parent company. |

6 | Includes Dick's Sporting Goods (7) and Golf Galaxy (1), both of which are owned by the same parent company. |

7 | Includes Ann Taylor (5), Catherine's (2), Dress Barn (11), Lane Bryant (7), Justice Stores (5) and Maurices (4), all of which are owned by the same parent company. |

8 | Includes Sam's Club, which is owned by the same parent company. |

9 | Includes Babies "R" Us (3), and Toys "R" Us/Babies "R" Us combination stores (3), both of which are owned by the same parent company. |

p. 20 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

RETAIL LEASING SPREADS | | |

Comparable Space1,2 | ||||||||||||||||||||||||||||

Category | Total Leases | Total Sq. Ft. | Leases | Sq. Ft. | Prior Rent PSF3 | New Rent PSF4,5 | Cash Rent Spread | TI, LL Work, Lease Commissions PSF6 | ||||||||||||||||||||

New Leases - Q3, 2017 | 39 | 92,089 | 18 | 44,091 | $ | 23.58 | $ | 28.04 | 18.9 | % | $ | 49.06 | ||||||||||||||||

New Leases - Q2, 2017 | 51 | 164,214 | 23 | 71,828 | $ | 21.52 | $ | 25.27 | 17.4 | % | $ | 58.67 | ||||||||||||||||

New Leases - Q1, 20177 | 32 | 109,513 | 15 | 74,122 | $ | 10.20 | $ | 14.85 | 45.5 | % | $ | 34.37 | ||||||||||||||||

New Leases - Q4, 2016 | 49 | 218,329 | 25 | 137,028 | $ | 14.84 | $ | 18.74 | 26.3 | % | $ | 52.03 | ||||||||||||||||

Renewals - Q3, 2017 | 47 | 340,725 | 47 | 340,725 | $ | 16.40 | $ | 17.99 | 9.7 | % | $ | 1.63 | ||||||||||||||||

Renewals - Q2, 2017 | 45 | 460,103 | 45 | 460,103 | $ | 14.07 | $ | 15.20 | 8.0 | % | $ | 2.42 | ||||||||||||||||

Renewals - Q1, 20178 | 48 | 399,851 | 48 | 399,851 | $ | 16.13 | $ | 16.89 | 4.7 | % | $ | 2.34 | ||||||||||||||||

Renewals - Q4, 2016 | 43 | 352,761 | 43 | 352,761 | $ | 13.98 | $ | 14.75 | 5.5 | % | $ | 1.11 | ||||||||||||||||

Total - Q3, 20179 | 86 | 432,814 | 65 | 384,816 | $ | 17.22 | $ | 19.14 | 11.1 | % | $ | 7.06 | ||||||||||||||||

Total - Q2, 2017 | 96 | 624,317 | 68 | 531,931 | $ | 15.08 | $ | 16.56 | 9.8 | % | $ | 10.02 | ||||||||||||||||

Total - Q1, 20178 | 80 | 509,364 | 63 | 473,973 | $ | 15.20 | $ | 16.57 | 9.0 | % | $ | 7.34 | ||||||||||||||||

Total - Q4, 2016 | 92 | 571,090 | 68 | 489,789 | $ | 14.22 | $ | 15.87 | 11.5 | % | $ | 15.36 | ||||||||||||||||

________________ | |

1 | Comparable space leases on this report are included for retail properties only. Leases at our two office properties, Thirty South Meridian and Eddy Street, are included in the totals and ground leases are excluded. |

2 | Comparable leases represent those leases signed for which there was a former tenant within the last 12 months. |

3 | Prior rent represents minimum rent, if any, paid by the prior tenant in the final 12 months of the term. |

4 | All amounts reported at lease execution. |

5 | Contractual rent represents contractual minimum rent per square foot for the first 12 months of the lease. |

6 | Includes redevelopment costs for tenant specific landlord work and tenant allowances provided to tenants at properties in the 3-R pipeline. |

7 | Cash rent spread on comparable new leases for Q1, 2017, excluding one anchor lease, was 14.3%. |

8 | Cash renewal spread on comparable leases for Q1, 2017, excluding one strategic anchor renewal, was 5.5%. The aggregate spread excluding the one anchor renewal was 10.3%. |

9 | The aggregate spread on a straight-line basis over the contractual life of the lease to the comparable lease was 17.0% for Q3, 2017, 13.9% for Q2, 2017 and 13.7% for Q1, 2017. |

p. 21 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

LEASE EXPIRATIONS – OPERATING PORTFOLIO | | |

As of September 30, 2017

($ in thousands, except per square foot data)

This table includes the following:

• | Operating retail properties; |

• | Operating office properties; and |

• | Development/Redevelopment property tenants open for business or ground lease tenants who commenced paying rent as of September 30, 2017. |

Number of Expiring Leases1 | Expiring GLA/NRA2 | % of Total GLA/NRA Expiring | Expiring Annualized Base Rent3 | % of Total Annualized Base Rent | Expiring Annualized Base Rent per Sq. Ft. | Expiring Ground Lease Revenue | ||||||||||||||||||

2017 | 44 | 178,949 | 1.2 | % | $ | 3,527 | 1.4 | % | $ | 19.71 | $ | — | ||||||||||||

2018 | 260 | 1,362,250 | 8.8 | % | 24,115 | 9.6 | % | 17.70 | 234 | |||||||||||||||

2019 | 256 | 1,698,997 | 11.0 | % | 25,329 | 10.1 | % | 14.91 | 653 | |||||||||||||||

2020 | 253 | 2,077,957 | 13.5 | % | 28,659 | 11.4 | % | 13.79 | 1,592 | |||||||||||||||

2021 | 299 | 1,763,875 | 11.4 | % | 29,563 | 11.8 | % | 16.76 | 911 | |||||||||||||||

2022 | 297 | 2,132,844 | 13.8 | % | 35,810 | 14.3 | % | 16.79 | 1,217 | |||||||||||||||

2023 | 176 | 1,496,195 | 9.8 | % | 23,569 | 9.4 | % | 15.75 | 1,813 | |||||||||||||||

2024 | 99 | 946,120 | 6.1 | % | 18,910 | 7.5 | % | 19.99 | 288 | |||||||||||||||

2025 | 80 | 744,548 | 4.8 | % | 12,987 | 5.2 | % | 17.44 | 806 | |||||||||||||||

2026 | 80 | 767,131 | 5.0 | % | 11,259 | 4.5 | % | 14.68 | 1,320 | |||||||||||||||

Beyond | 151 | 2,244,623 | 14.5 | % | 37,458 | 14.9 | % | 16.69 | 11,012 | |||||||||||||||

1,995 | 15,413,489 | 100.0 | % | $ | 251,187 | 100.0 | % | $ | 16.30 | $ | 19,846 | |||||||||||||

____________________ | |

1 | Lease expiration table reflects rents in place as of September 30, 2017 and does not include option periods; 2017 expirations include 13 month-to-month tenants. This column also excludes ground leases. |

2 | Expiring GLA excludes estimated square footage attributable to non-owned structures on land owned by the Company and ground leased to tenants. |

3 | Annualized base rent represents the monthly contractual rent for September 2017 for each applicable tenant multiplied by 12. Excludes tenant reimbursements and ground lease revenue. |

p. 22 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

LEASE EXPIRATIONS – RETAIL ANCHOR TENANTS1 | | |

As of September 30, 2017

($ in thousands, except per square foot data)

This table includes the following:

• | Operating retail properties; and |

• | Development/Redevelopment property tenants open for business or ground lease tenants who commenced paying rent as of September 30, 2017. |

Number of Expiring Leases2 | Expiring GLA/NRA3 | % of Total GLA/NRA Expiring | Expiring Annualized Base Rent4 | % of Total Annualized Base Rent | Expiring Annualized Base Rent per Sq. Ft. | Expiring Ground Lease Revenue | ||||||||||||||||||

2017 | — | — | — | % | $ | — | — | % | $ | — | $ | — | ||||||||||||

2018 | 33 | 815,526 | 5.3 | % | 9,884 | 3.9 | % | 12.12 | — | |||||||||||||||

2019 | 34 | 1,105,131 | 7.2 | % | 10,693 | 4.3 | % | 9.68 | — | |||||||||||||||

2020 | 39 | 1,543,517 | 10.0 | % | 15,698 | 6.2 | % | 10.17 | 1,111 | |||||||||||||||

2021 | 42 | 1,091,651 | 7.1 | % | 12,688 | 5.1 | % | 11.62 | 318 | |||||||||||||||

2022 | 53 | 1,434,297 | 9.3 | % | 18,099 | 7.2 | % | 12.62 | 745 | |||||||||||||||

2023 | 34 | 901,424 | 5.9 | % | 11,123 | 4.4 | % | 12.34 | 1,454 | |||||||||||||||

2024 | 21 | 655,301 | 4.3 | % | 11,950 | 4.8 | % | 18.24 | — | |||||||||||||||

2025 | 19 | 485,641 | 3.2 | % | 6,728 | 2.7 | % | 13.85 | 381 | |||||||||||||||

2026 | 16 | 512,101 | 3.3 | % | 4,972 | 2.0 | % | 9.71 | 750 | |||||||||||||||

Beyond | 55 | 1,886,231 | 12.2 | % | 27,938 | 11.1 | % | 14.81 | 6,373 | |||||||||||||||

346 | 10,430,820 | 67.7 | % | $ | 129,773 | 51.7 | % | $ | 12.44 | $ | 11,131 | |||||||||||||

____________________ | |

1 | Retail anchor tenants are defined as tenants that occupy 10,000 square feet or more. |

2 | Lease expiration table reflects rents in place as of September 30, 2017 and does not include option periods. |

3 | Expiring GLA excludes square footage for non-owned ground lease structures on land we own and ground leased to tenants. |

4 | Annualized base rent represents the monthly contractual rent for September 2017 for each applicable tenant multiplied by 12. Excludes tenant reimbursements and ground lease revenue. |

p. 23 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

LEASE EXPIRATIONS – RETAIL SHOPS | | |

As of September 30, 2017

($ in thousands, except per square foot data)

This table includes the following:

• | Operating retail properties; and |

• | Development/Redevelopment property tenants open for business as of September 30, 2017. |

Number of Expiring Leases1 | Expiring GLA/NRA2 | % of Total GLA/NRA Expiring | Expiring Annualized Base Rent3 | % of Total Annualized Base Rent | Expiring Annualized Base Rent per Sq. Ft. | Expiring Ground Lease Revenue | |||||||||||||||

2017 | 42 | 96,432 | 0.6% | $ | 2,050 | 0.8% | $ | 21.25 | $ | — | |||||||||||

2018 | 225 | 532,870 | 3.4% | 13,949 | 5.6% | 26.18 | 234 | ||||||||||||||

2019 | 221 | 588,613 | 3.8% | 14,535 | 5.8% | 24.69 | 653 | ||||||||||||||

2020 | 212 | 521,129 | 3.4% | 12,705 | 5.1% | 24.38 | 481 | ||||||||||||||

2021 | 254 | 663,225 | 4.3% | 16,647 | 6.6% | 25.10 | 593 | ||||||||||||||

2022 | 239 | 633,527 | 4.1% | 16,450 | 6.5% | 25.97 | 473 | ||||||||||||||

2023 | 136 | 439,423 | 2.9% | 10,877 | 4.3% | 24.75 | 359 | ||||||||||||||

2024 | 75 | 216,593 | 1.4% | 5,759 | 2.3% | 26.59 | 288 | ||||||||||||||

2025 | 57 | 172,228 | 1.1% | 4,841 | 1.9% | 28.11 | 425 | ||||||||||||||

2026 | 64 | 255,030 | 1.7% | 6,287 | 2.5% | 24.65 | 570 | ||||||||||||||

Beyond | 95 | 349,238 | 2.2% | 9,250 | 3.7% | 26.48 | 4,639 | ||||||||||||||

1,620 | 4,468,308 | 28.8% | $ | 113,349 | 45.1% | $ | 25.37 | $ | 8,715 | ||||||||||||

____________________ | |

1 | Lease expiration table reflects rents in place as of September 30, 2017, and does not include option periods; 2017 expirations include 13 month-to-month tenants. This column also excludes ground leases. |

2 | Expiring GLA excludes estimated square footage attributable to non-owned structures on land we own and ground leased to tenants. |

3 | Annualized base rent represents the monthly contractual rent for September 2017 for each applicable tenant multiplied by 12. Excludes tenant reimbursements and ground lease revenue. |

p. 24 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

LEASE EXPIRATIONS – OFFICE TENANTS AND OTHER | | |

As of September 30, 2017

($ in thousands, except per square foot data)

Number of Expiring Leases1 | Expiring GLA/NRA2 | % of Total GLA/NRA Expiring | Expiring Annualized Base Rent3 | % of Total Annualized Base Rent | Expiring Annualized Base Rent per Sq. Ft. | ||||||||||||

2017 | 2 | 82,517 | 0.5% | $ | 1,477 | 0.6% | $ | 17.90 | |||||||||

2018 | 2 | 13,854 | 0.1% | 282 | 0.1% | 20.38 | |||||||||||

2019 | 1 | 5,253 | 0.0% | 101 | 0.0% | 19.25 | |||||||||||

2020 | 2 | 13,311 | 0.1% | 256 | 0.1% | 19.25 | |||||||||||

2021 | 3 | 8,999 | 0.1% | 228 | 0.1% | 25.38 | |||||||||||

2022 | 5 | 65,020 | 0.4% | 1,261 | 0.5% | 19.39 | |||||||||||

2023 | 6 | 155,348 | 1.0% | 1,569 | 0.6% | 10.10 | |||||||||||

2024 | 3 | 74,226 | 0.5% | 1,201 | 0.5% | 16.19 | |||||||||||

2025 | 4 | 86,679 | 0.6% | 1,418 | 0.6% | 16.36 | |||||||||||

2026 | — | — | 0.0% | — | 0.0% | — | |||||||||||

Beyond | 1 | 9,154 | 0.1% | 270 | 0.1% | 29.50 | |||||||||||

29 | 514,361 | 3.5% | $ | 8,065 | 3.2% | $ | 15.68 | ||||||||||

____________________ | |

1 | Lease expiration table reflects rents in place as of September 30, 2017 and does not include option periods. This column also excludes ground leases. |

2 | Lease expiration table reflects rents in place as of September 30, 2017 and does not include option periods. This column also excludes ground leases. |

3 | Annualized base rent represents the monthly contractual rent for September 2017 for each applicable tenant multiplied by 12. Excludes tenant reimbursements. |

p. 25 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

DEVELOPMENT PROJECTS UNDER CONSTRUCTION | | |

As of September 30, 2017

($ in thousands)

Project | Company Ownership % | MSA | Projected Stabilization Date1 | Projected Owned GLA2 | Projected Total GLA3 | Percent of Owned GLA Occupied4 | Percent of Owned GLA Pre-Leased/ Committed | Total Estimated Project Cost | Cost Incurred as of September 30, 2017 | Major Tenants and Non-owned Anchors | |||||||||

Holly Springs Towne Center, NC - Phase II Expansion | 100% | Raleigh | Mid 2018 | 23,000 | 23,000 | — | % | 100.0 | % | $ | 2,700 | $ | 1,555 | O2 Fitness | |||||

Eddy Street Commons at Notre Dame, IN - Phase II 5 | 100% | South Bend | Q4 2020 | 8,500 | 530,000 | — | % | — | % | $ | 8,447 | $ | 501 | Ground lease with multi-family developer on 450 units; 8,500 square feet of owned retail. | |||||

Total | 31,500 | 553,000 | — | % | 73.0 | % | $ | 11,147 | $ | 2,056 | |||||||||

Projected Annualized Development / Redevelopment Cash NOI Summary | |||

Remaining Under Construction Development / Redevelopment Cash NOI | $ | 6,020 | |

Remaining Transitional Development / Redevelopment Cash NOI | 2,151 | ||

Total Remaining Annual Cash NOI | $ | 8,171 | |

Summary of Construction In Progress on Consolidated Balance Sheet: | |||

Under Construction Development / Redevelopment CIP | $ | 18,402 | |

Transitional Development / Redevelopment CIP | 9,513 | ||

Lake Lofts at Deerwood - Jacksonville, FL | 20,405 | ||

Holly Springs Towne Center - Phase III | 5,771 | ||

Eddy Street Hotel 6 | 8,966 | ||

Various tenant improvements and small projects | 15,174 | ||

Construction In Progress on Consolidated Balance Sheet | $ | 78,231 | |

____________________ | ||||||||||

1 | Stabilization date represents near completion of project construction and substantial occupancy of the property. | |||||||||

2 | Projected Owned GLA represents gross leasable area we project we will own. It excludes square footage that we project will be attributable to non-owned outlot structures on land owned by us and expected to be ground leased to tenants. It also excludes non-owned anchor space. | |||||||||

3 | Projected Total GLA includes Projected Owned GLA, projected square footage attributable to non-owned outlot structures on land that we own, and non-owned anchor space that currently exists or is under construction. | |||||||||

4 | Includes tenants that have taken possession of their space or have begun paying rent. | |||||||||

5 | Total estimated cost of all components of Eddy Street Phase II equals $89.2 million. This consists of KRG estimated project cost ($8.4 million), Tax Increment Financing ($16.1 million), and residential apartments and townhomes to be ground subleased to unrelated third party ($64.7 million). | |||||||||

6 | The Company began construction of a hotel at Eddy Street Commons at the University of Notre Dame. Projected cost is $40 million, net of Tax Increment Financing of $6.0 million, and the Company is in negotiations to form and retain a minority interest in an unconsolidated joint venture to complete and own the hotel. | |||||||||

p. 26 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

UNDER CONSTRUCTION REDEVELOPMENT, REPOSITION, AND REPURPOSE PROJECTS | |

($ in thousands) | ||||||

Property | Location (MSA) | Description | Projected ROI | Projected Cost | Percentage of Cost Spent | Est. Stabilized Period |

Bolton Plaza, Phase II | Jacksonville | Replacing existing vacant shop space with Marshalls and a ground lease with Aldi; additionally undergoing center upgrades. | 9.5% - 10.5% | $5,000 - $5,500 | 96% | 2H 2017 |

Burnt Store Promenade* | Punta Gorda | New building construction of Publix into 45,000 square foot space. New 20 year lease and center upgrades. | 10.5% - 11.5% | $9,000 - $10,000 | 83% | 1H 2018 |

Centennial Center A | Las Vegas | Reposition of 2 retail buildings totaling 14,000 square feet, as well as Panera Bread outlot. Scope including addition of traffic signal and other significant building/site enhancements. | 10.0% - 11.0% | $4,000 - $5,000 | 38% | 2H 2018 |

City Center* | White Plains | Reactivating street-level retail components and enhancing overall shopping experience within multilevel project. | 6.5% - 7.0% | $17,000 - $17,500 | 87% | 1H 2018 |

Fishers Station* | Indianapolis | Demolition, expansion, and replacement of previous anchor with a Kroger ground lease. Center upgrades and new shop space. | 9.5% - 10.5% | $10,500 - $11,500 | 73% | 2H 2018 |

Portofino Shopping Center, Phase II | Houston | Demolition and expansion of existing vacant space to accommodate Nordstrom Rack; rightsizing of existing Old Navy, and relocation of shop tenants. | 8.0% - 8.5% | $6,500 - $7,000 | 64% | 2H 2018 |

Rampart Commons* | Las Vegas | Relocating, re-tenanting, and renegotiating leases as a part of new development plan. Upgrades to building façades and hardscape throughout the center. | 7.0% - 7.5% | $16,000 - $17,000 | 19% | 2H 2018 |

Trussville Promenade1 | Birmingham | Replacing existing vacant small shops with 22,000 square foot junior anchor. | 6.5% - 7.5% | $4,500 - $5,500 | 74% | 2H 2017 |

UNDER CONSTRUCTION REDEVELOPMENT, REPOSITION, REPURPOSE TOTALS | 8.0% - 9.0% | $72,500 - $79,000 | 65% | |||

____________________ | |

1 | Refers to Trussville I |

* | Asterisk represents assets removed from the operating portfolio. |

p. 27 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

REDEVELOPMENT, REPOSITION, AND REPURPOSE OPPORTUNITIES | | |

($ in thousands) | ||

REDEVELOPMENT | Location (MSA) | Description |

Beechwood Promenade* | Athens | Remerchandising opportunity across vacant shop space via new fitness facility, fast casual dining, and other shops; also considering self storage opportunities. |

Courthouse Shadows* | Naples | Recapture of natural lease expiration; demolition of the site to add mixed use format and outparcel development. |

Hamilton Crossing Centre* | Indianapolis | Recapture of lease expiration; substantially enhancing merchandising mix and replacing available anchor tenant. |

Targeted Return | 9.5% - 10.5% | |

Expected Cost | $25,000 - $35,000 | |

REPOSITION1 | Location (MSA) | Description |

Centennial Center B | Las Vegas | General building enhancements to 5 remaining outparcels. Addition of two restaurants to anchor the small shop building. |

Targeted Return | 9.5% - 10.5% | |

Expected Cost | $5,000 - $6,000 | |

REPURPOSE | Location (MSA) | Description |

The Corner* | Indianapolis | Creation of a mixed use (retail and multi-family) development replacing an unanchored small shop center. |

Targeted Return | 9.0% - 9.5% | |

Expected Cost | $15,000 - $20,000 | |

Total Targeted Return | 9.0% - 11.0% | |

Total Expected Cost | $45,000 - $61,000 | |

____________________ | |

1 | Reposition refers to less substantial asset enhancements based on internal costs. |

* | Asterisk represents assets removed from the operating portfolio. |

Note: | These opportunities are merely potential at this time and are subject to various contingencies, many of which are beyond the Company's control. Targeted return is based upon our current expectations of capital expenditures, budgets, anticipated leases and certain other factors relating to such opportunities. The actual return on these investments may not meet our expectations. |

p. 28 | Kite Realty Group Trust Supplemental Financial and Operating Statistics –9/30/17 |

2017 PROPERTY DISPOSITIONS | | |

($ in thousands)

DISPOSITIONS

Property Name | MSA | Date Sold | Sales Price | |||

Cove Center | Stuart, FL | 3/31/2017 | ||||

Clay Marketplace | Birmingham, AL | 5/25/2017 | ||||

The Shops at Village Walk | Fort Myers, FL | 5/25/2017 | ||||