UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): October 25, 2017

Santander Holdings USA, Inc.

(Exact name of registrant as specified in its charter)

Virginia | 1-16581 | 23-2453088 | ||||

(State or other Jurisdiction of Incorporation) | (Commission File Number) | (IRS Employer Identification No.) | ||||

75 State Street, Boston, Massachusetts | 02109 | |||||

(Address of Principal Executive Offices) | (Zip Code) | |||||

Registrant's telephone number, including area code: (617) 346-7200

N/A |

(Former name or former address if changed since last report.) |

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o |

Item 8.01 Other Events

Introduction

Santander Holdings USA, Inc. (the “Company” or "SHUSA") is a bank holding company ("BHC") in the U.S. with $134.8 billion in assets as of June 30, 2017. Headquartered in Boston, Massachusetts, the Company is the parent company of Santander Bank, National Association (“Santander Bank”), and owns a majority interest (approximately 59%) of Santander Consumer USA Holdings Inc. ("SC"), a specialized consumer finance company focused on vehicle financing and third-party servicing. Through these entities, the Company offers a full range of consumer and commercial banking products and services. SHUSA is a wholly-owned subsidiary of Banco Santander, S.A. (“Santander”). The Company has developed stress testing processes that capture its unique mix of businesses, risks and geographic footprint.

Dodd-Frank Act Mid-Cycle Stress Test Requirements

The Board of Governors of the Federal Reserve System (the “Federal Reserve”) requires BHCs with total consolidated assets of $50 billion or more to conduct an annual mid-cycle stress test under internally-developed baseline, adverse, and severely adverse scenarios, and to publish a summary of the stress test results based on the severely adverse scenario. The results are to reflect a standard set of capital actions over the nine-quarter forecast horizon (“DFAST Capital Actions”).

Forecast Scenario

The Company developed a severely adverse scenario based on previously published Federal Reserve severely adverse scenarios, and benchmarks from the 2008 financial crisis for key macroeconomic variables. Key macroeconomic factors have been modified and tailored to stress the Company’s unique risk profile and strategic plans.

The mid-cycle severely adverse scenario is characterized by a severe global recession, accompanied by a period of heightened corporate financial stress and near-to-zero yields for short-term U.S. Treasury securities, resulting in depressed real estate values and used vehicle values. The impact of the macroeconomic conditions on the Company is further amplified by multiple idiosyncratic events that are non-macro sensitive, including a stress in the auto industry caused by supply-and-demand imbalance that further stresses vehicle values.

The Company’s hypothetical scenario is comparable in severity or more severe than the Federal Reserve’s Comprehensive Capital Analysis and Review 2017 severely adverse scenario. The scenario was designed to test and demonstrate the Company’s ability to withstand an extreme macroeconomic environment paired with non-macro sensitive events and maintain capital ratios well above regulatory minimums.

The table below highlights some of the key macroeconomic trends used for this hypothetical exercise:

Severely Adverse Scenario | ||||||

Average | Worst Quarter | End Point | ||||

Real GDP Growth Rate (QoQ annualized) | (2.0)% | (7.7)% | 3.0% | |||

Unemployment rate | 8.1% | 9.3% | 9.1% | |||

Case-Shiller Home Price Index | 167.1 | 138.4 | 138.4 | |||

3 mo. Treasury | 0.09% | 0.01% | 0.08% | |||

10 yr. Treasury | 1.52% | 1.32% | 1.37% | |||

Commercial Real Estate Price Index | 220.1 | 182.5 | 183.9 | |||

Manheim Used Vehicle Index(1) | 113.5 | 110.2 | 115.5 | |||

(1) Automobile industry supply-and-demand imbalance impact was implemented through management overlays which are not reflected in the Manheim Index presented here.

Forecast Approach

The Company considers and evaluates all material risks facing the Company in its capital adequacy and stress testing processes including, but not limited to, the following:

• | Credit risk is the risk of loss arising from a borrower’s or counterparty’s failure to perform on an obligation. Credit risk at the Company is driven by real estate-related lending, large corporate exposures, individual consumer lending and automobile finance exposures. Credit risk is incorporated into our stress results primarily through credit-sensitive macroeconomic models. |

• | Operational risk is the risk of loss resulting from inadequate or failed internal processes, people, or systems, or external events. This risk is incorporated into our stress test results through macroeconomic models, increases in legal reserves and specific adverse events considered in our forecast. |

• | Market risk is the risk to the Company’s financial condition resulting from changes in interest rates or changes in the market value of assets and traded financial instruments, both on-balance sheet and off-balance sheet. Market risk impacts stress results through impairment of consumer assets as well as changes in net interest income and changes in the value of the investment portfolio. |

• | Liquidity risk is the risk arising from an inability to meet obligations as they come due in the normal course of business without causing undue hardship or incurring unacceptable loss. Liquidity risk is incorporated into the stress forecast through limited funding availability, increased cost of funds and credit rating downgrades. |

• | Business risk is the risk of decline in new loan volume originations and thereby the associated income-generating capacity of assets. The stress scenarios are characterized by recessionary environments with reduced economic activity, which results in less demand for loans by consumers and businesses. |

The Company employs various quantitative and qualitative methodologies in its stress tests for balance sheet, income statement, and capital projections. Where practical, the Company utilizes modeling techniques in developing its stress test estimates, including regression-based modeling, transition analytics, business analytics, and other objective, quantitative forecasting methodologies. When models are not used, non-model forecast tools are leveraged to prepare estimates. Forecasting methodologies, management overlays and final stress test results undergo multiple rounds of review and challenge. Additional methodologies employed in developing the stress testing include:

• | Pre-provision Net Revenue (“PPNR”): PPNR forecasting methodology consists of multiple models, calculations and driver-based expert judgment analytical approaches used in conjunction to forecast individual line items for various components of the balance sheet and income statement. Forecasts for term loans and deposit balances as well as forecasts for yields and pricing generally leverage contractual terms for the existing portfolio, while new loans and deposits are forecasted using statistical regression models and expert judgment approaches. Net interest income is calculated based on contractual rates for existing assets and projected interest rates for new volumes applied to forecasted loan and deposit balances. Non-interest income and expense items are forecasted primarily using driver-based analytical approaches utilizing modeled and expert judgment components. |

• | Credit Loss Estimation: For the purposes of capital planning and loss forecasting, the Company has developed loss forecasting models driven by macroeconomic variables across the commercial, retail and automobile portfolios. Credit loss estimations drive changes in reserve levels and ultimately provisions. The forecast for provisions incorporates loss projections and target reserve coverage rates. |

• | Operational Loss Estimation: The Company utilizes statistical approaches to explicitly link operational losses to macroeconomic factors, based on both internal and external loss data and scenario analysis, to identify and evaluate the potential impacts from low-frequency, high-severity loss events linked to the Company’s risk profile. |

• | Capital and Risk-Weighted Assets: The methodologies described above translate identified risks into potential revenue and loss projections, which are aggregated into consolidated net income (loss) estimates over the nine-quarter planning horizon. These estimates then feed the Company’s regulatory capital estimation process. Regulatory capital and risk-weighted asset calculations are based on existing regulatory guidance, including Basel III transition provisions. The resulting regulatory capital ratios are continuously compared to management’s capital target levels, a process which is a key factor in the firm’s capital adequacy framework. |

Summary of Results

The results presented below contain forward-looking projections that represent estimates based on the severely adverse scenario, a hypothetical set of conditions that involve an economic outcome that is more adverse than expected. These estimates are not forecasts of expected losses, revenues, net income or capital ratios.

Under the severely adverse scenario, the most significant drivers of the Company’s regulatory capital ratios and those of Santander Bank are reductions in capital, driven by higher credit losses and lower PPNR, and declines in total assets and risk-weighted assets. For both the Company and Santander Bank, in the severely adverse scenario, capital depletion has a more significant impact on capital ratios than the reduction in assets, resulting in a decline across all capital ratios.

The severely adverse scenario also leads to the following results:

• | Increases in credit losses and provisions that are associated with the more significant portfolios, such as retail mortgage, commercial and industrial, and commercial real estate at Santander Bank and automotive at SC. |

• | Stress impacts on PPNR that are driven by various factors including lower net interest income and fees caused by lower asset balances, net interest margin compression, and higher operational risk losses. Stress impact also includes higher depreciation and impairment expenses on operating lease assets. |

• | The decline in assets at the Company and Santander Bank are largely due to lower commercial loan balances, as well as a reduction in cash, available for sale securities, and operating lease balances. |

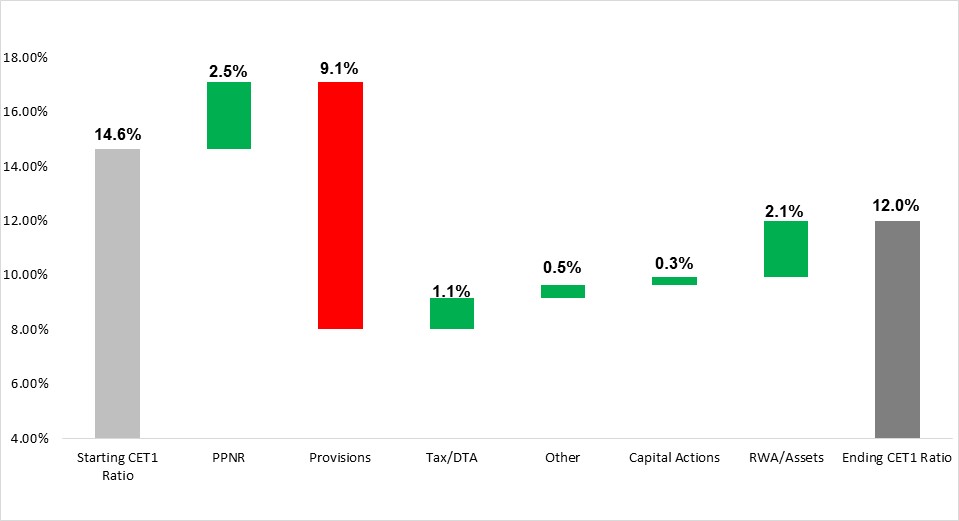

The chart below shows the impact of these changes to SHUSA’s common equity tier 1 (“CET1”) ratio over the nine-quarter forecast horizon. The CET1 ratio decreases approximately 260 basis points from June 30, 2017 to September 30, 2019. The primary driver for this decrease is the $8.7 billion provision expense versus PPNR of $2.4 billion. Risk-weighted assets also decrease by $15 billion during the forecast, which offsets some of the decline on the CET1 ratio.

SHUSA

The estimates below reflect capital ratios for SHUSA under the "DFAST Capital Actions" described previously.

Table 1: SHUSA Actual and Projected Capital Ratios through Q3 2019

Actual Q2 2017 | Severely Adverse | ||||||||

Ending | Minimum | ||||||||

CET1 capital (%) | 14.6 | % | 12.0 | % | 12.0 | % | |||

Tier 1 risk-based capital ratio (%) | 16.3 | % | 13.5 | % | 13.5 | % | |||

Total risk-based capital ratio (%) | 18.1 | % | 15.2 | % | 15.2 | % | |||

Tier 1 leverage ratio (%) | 13.0 | % | 11.1 | % | 11.1 | % | |||

Table 2: SHUSA Actual and Projected Risk-Weighted Assets through Q3 2019

Actual Q2 2017 | Q3 2019 | |||||||

Risk-weighted assets ($bn)1 | $ | 103.2 | $ | 88.4 | ||||

1 Risk-weighted assets are calculated under the transition rules for the Basel III standardized approach.

Table 3: SHUSA Projected Losses, Revenues, and Net Income through Q3 2019

Severely Adverse | |||||||

$bn | % of average assets1 | ||||||

PPNR2 | $ | 2.4 | 1.9 | % | |||

Other revenue | — | ||||||

Less | |||||||

Provisions | 8.7 | ||||||

Realized gains (losses) on securities available-for-sale / held to maturity | — | ||||||

Total trading and counterparty losses | — | ||||||

Total other losses | — | ||||||

Equals | |||||||

Net income (loss) before taxes, extraordinary items and minority interest 3 | $ | (6.4 | ) | (5.2 | )% | ||

1 Average assets is the nine-quarter average of total assets.

2 PPNR includes losses from operational risk events, mortgage repurchase expenses, and other real estate owned costs.

3 Total may not sum due to rounding of line items.

Table 4: SHUSA Projected Loan Losses by Loan Type Q3 2017 through Q3 2019

Severely Adverse | |||||||

$bn | Portfolio Loss Rates (%)1 | ||||||

Loan losses2 | $ | 8.6 | 11.2 | % | |||

First lien mortgages | 0.2 | 3.5 | % | ||||

Junior liens and home equity lines of credit | 0.2 | 2.6 | % | ||||

Commercial and industrial3 | 0.6 | 4.7 | % | ||||

Commercial real estate | 0.7 | 4.7 | % | ||||

Credit cards | 0.1 | 25.1 | % | ||||

Other consumer4 | 6.6 | 24.5 | % | ||||

Other loans | 0.1 | 1.2 | % | ||||

1 Average loan balances used to calculate portfolio loss rates exclude loans held-for-sale and loans held-for-investment under the fair value option, and are calculated over nine quarters.

2 Total may not sum due to rounding of line items.

3 Commercial and industrial loans include small- and medium-enterprise loans.

4 Other consumer loans include student loans and automobile loans.

Santander Bank

The estimates below reflect capital ratios for Santander Bank under the DFAST Capital Actions described previously.

Table 5: Santander Bank Actual and Projected Capital Ratios through Q3 2019

Actual Q2 2017 | Severely Adverse | ||||||||

Ending | Minimum | ||||||||

CET1 capital (%) | 17.6 | % | 14.9 | % | 14.9 | % | |||

Tier 1 risk-based capital ratio (%) | 17.6 | % | 14.9 | % | 14.9 | % | |||

Total risk-based capital ratio (%) | 18.7 | % | 16.2 | % | 16.2 | % | |||

Tier 1 leverage ratio (%) | 13.4 | % | 12.0 | % | 12.0 | % | |||

Table 6: Santander Bank Actual and Projected Risk-Weighted Assets through Q3 2019

Actual Q2 2017 | Q3 2019 | |||||||

Risk-weighted assets ($bn)1 | $ | 57.7 | $ | 51.2 | ||||

1 Risk-weighted assets are calculated under the transition rules for the Basel III standardized approach.

Cautionary Note Regarding Forward-Looking Information

This Current Report on Form 8-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Any statements about our expectations, beliefs, plans, predictions, forecasts, objectives, assumptions, or future events or performance are not historical facts and may be forward-looking. These statements are often, but not always, made through the use of words or phrases such as “anticipates,” “believes,” “can,” “could,” “may,” “predicts,” “potential,” “should,” “will,” “estimate,” “plans,” “projects,” “continuing,” “ongoing,” “expects,” “intends,” and similar words or phrases. Although the Company believes that the expectations reflected in these forward-looking statements are reasonable, these statements are not guarantees of future performance and involve risks and uncertainties which are subject to change based on various important factors, some of which are beyond the Company’s control. For an additional discussion of these risks, please see Part I, Item 1A entitled “Risk Factors” in the Company’s Annual Report on Form 10-K for 2016.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

Dated: October 25, 2017 | SANTANDER HOLDINGS USA, INC. By:/s/ Madhukar Dayal Name: Madhukar Dayal Title: Chief Financial Officer and Senior Executive Vice President |