Attached files

| file | filename |

|---|---|

| EX-32.2 - Trident Brands Inc | ex32-2.htm |

| EX-32.1 - Trident Brands Inc | ex32-1.htm |

| EX-31.2 - Trident Brands Inc | ex31-2.htm |

| EX-31.1 - Trident Brands Inc | ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

[X] QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE QUARTERLY PERIOD ENDED AUGUST 31, 2017

Commission file number 000-53707

TRIDENT BRANDS INCORPORATED

(Exact name of registrant as specified in its charter)

Nevada

(State or other jurisdiction of incorporation or organization)

200 South Executive Drive, Suite 101

Brookfield, WI 53005

(Address of principal executive offices, including zip code.)

(262) 789-6689

(Telephone number, including area code)

Resident Agents of Nevada

711 S. Carson Street, Suite 4

Carson City, NV 89701

(Name and Address of Agent for Service)

Check whether the issuer (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the last 90 days. YES [X] NO [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES [X] NO [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer, "accelerated filer," "non-accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer [ ]

|

Accelerated filer [ ]

|

|

Non-accelerated filer [ ]

|

Smaller reporting company [X]

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES [ ] NO [X]

The number of the registrant’s common shares outstanding as of October 16, 2017 was 32,311,887.

TRIDENT BRANDS INCORORATED

FORM 10-Q

For the quarterly period ended August 31, 2016

TABLE OF CONTENTS

|

PART I

|

FINANCIAL INFORMATION

|

|

|

Item 1.

|

Financial Statements (Unaudited)

|

7 |

|

Consolidated Balance Sheets as at August 31, 2017 and November 30, 2016

|

8 | |

|

Consolidated Statements of Operations for the three and nine months ended August 31, 2017 and August 31, 2016

|

9 | |

|

Consolidated Statements of Cash Flows for the nine months ended August 31, 2017 and August 31, 2016

|

10 | |

|

Notes to Consolidated Unaudited Financial Statements

|

11 | |

|

Item 2

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

15 |

|

Item 3

|

Quantitative and Qualitative Disclosures about Market Risk

|

21 |

|

Item 4

|

Controls and Procedures

|

21 |

|

PART II

|

OTHER INFORMATION

|

21 |

|

Item 6

|

Exhibits

|

21 |

2

Basis of Presentation

Except where the context otherwise requires, all references in this Quarterly Report on Form 10-Q (“Form 10-Q”) to the “Company”, “we”, “us”, “our”, “Trident” and “Trident Brands” or similar words and phrases are to Trident Brands Incorporated and its subsidiaries, taken together.

In this report, all currency amounts are expressed in thousands of United States (“U.S.”) dollars (“$”), except per share data, unless otherwise stated. Amounts expressed in other than U.S. dollars are noted accordingly. For example, amounts if expressed in Canadian dollars are expressed in thousands of Canadian dollars and preceded by the symbol “Cdn $”.

Forward-Looking Statements

This Form 10-Q contains forward-looking statements which are based on our current expectations and assumptions and involve a number of risks and uncertainties. Generally, forward-looking statements do not relate strictly to historical or current facts and are typically accompanied by words such as “anticipate”, “estimate”, “intend”, “project”, “potential”, “continue”, “believe”, “expect”, “could”, “would”, “should”, “might”, “plan”, “will”, “may”, “predict”, the negatives of such terms, and words and phrases of similar impact and include, but are not limited to references to expected increases in revenues and margins, growth opportunities, the success of new product launches and line extensions, our ability to finance our business, potential strategic investments, business strategies, competitive strengths, goals, references to key markets where we operate and the market for our securities. These forward-looking statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on certain assumptions and analyses we make in light of our experience and our interpretation of current conditions, historical trends and expected future developments, as well as other factors that we believe are appropriate in the circumstance.

Whether actual results and developments will agree with our expectations and predictions is subject to many risks and uncertainties. Accordingly, there are or will be important factors that could cause our actual results to differ materially from our expectations and predictions. We believe these factors include, but are not limited to, the following:

|

·

|

we have a limited operating history with significant losses and expect losses to continue for the foreseeable future;

|

|

·

|

there is doubt about our ability to continue as a going concern due to recurring losses from operations, an accumulated deficit and insufficient cash resources on hand to meet our business objectives, all of which means that we may not be able to continue operations;

|

|

·

|

we could face intense competition, which could result in lower revenues and higher expenditures and could adversely affect our results of operations;

|

|

·

|

we are governed by only three persons serving as directors and officers which may lead to faulty corporate governance;

|

|

·

|

we must attract and maintain key personnel or our business may fail;

|

|

·

|

we may not be able to secure additional financing to meet our future capital needs due to changes in general economic conditions;

|

|

·

|

our business and operating results could be harmed if we fail to manage our growth or change;

|

|

·

|

we have a limited operating history and if we are not successful in growing our business, then we may have to scale back or even cease our ongoing business operations;

|

3

|

·

|

if our intellectual property is not adequately protected, then we may not be able to compete effectively and we may not be profitable;

|

|

·

|

if we are the subject of an intellectual property infringement claim, the cost of participating in any litigation could impact our ability to stay in business;

|

|

·

|

we could lose our competitive advantages if we are not able to protect any of our food and nutritional products and intellectual property rights against infringement, and any related litigation could be time-consuming and costly;

|

|

·

|

if we fail to effectively manage our growth our future business results could be harmed and our managerial and operational resources may be strained;

|

|

·

|

if we fail to effectively manage our growth our future business results could be harmed and our managerial and operational resources may be strained;

|

|

·

|

our services may become obsolete and unmarketable if we are unable to respond adequately to rapidly changing technology and customer demands;

|

|

·

|

our failure to appropriately respond to changing consumer preferences and demand for new products or product enhancements could significantly harm product sales and harm our financial condition and operating results;

|

|

·

|

if we do not introduce new products or make enhancements to adequately meet the changing needs of our customers, some of our products could fail in the marketplace, which could negatively impact our revenues, financial condition and operating results;

|

|

·

|

we are affected by laws and governmental regulations with potential penalties or claims, which could harm our financial condition and operating results;

|

|

·

|

since we rely on independent third parties for the manufacture and supply of certain of our products, if these third parties fail to reliably supply products to us at required levels of quality and which are manufactured in compliance with applicable laws, then our financial condition and operating results would be harmed;

|

|

·

|

we may incur material product liability claims, which could increase our costs and harm our financial condition and operating results;

|

|

·

|

unless we can generate sufficient cash from operations or raise additional funds, we may not be able to meet our debt obligations;

|

|

·

|

our customers generally are not obligated to continue purchasing products from us;

|

|

·

|

if we do not manage our supply chain effectively, our operating results may be adversely affected;

|

|

·

|

our stock price may be volatile, which may result in losses to our shareholders;

|

|

·

|

our common shares are thinly traded and our shareholders may be unable to sell at or near ask prices, or at all;

|

|

·

|

the market price for our common stock is particularly volatile given our status as a relatively small and developing company, which could lead to wide fluctuations in our share price. Our shareholders may be unable to sell your common stock at or above their purchase price if at all, which may result in substantial losses;

|

4

|

·

|

we do not anticipate paying any cash dividends to our common shareholders and as a result shareholders may only realize a return when the shares are sold;

|

|

·

|

we are listed on the OTCQB quotation system and our common stock is subject to “penny stock” rules which could negatively impact our liquidity and our shareholders’ ability to sell their shares;

|

|

·

|

volatility in our common share price may subject us to securities litigation;

|

|

·

|

the elimination of monetary liability against our directors, officers and employees under Nevada law and the existence of indemnification rights of our directors, officers and employees may result in substantial expenditures by our company and may discourage lawsuits against our directors, officers and employees; and

|

|

·

|

our business is subject to changing regulations related to corporate governance and public disclosure that have increased both our costs and the risk of noncompliance.

|

Consequently all forward-looking statements made herein are qualified by these cautionary statements and there can be no assurance that our actual results or the developments we anticipate will be realized. The foregoing factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this report.

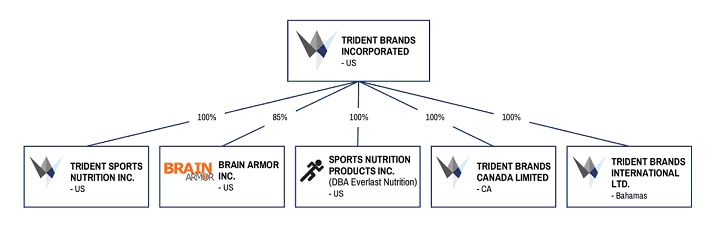

Corporate Legal Structure and Related Matters

Trident Brands Incorporated has five legal subsidiaries, as detailed below.

Trident Sports Nutrition Inc. is 100% owned by Trident Brands and is organized to deliver shelf ready product solutions in the sports nutrition and supplement segment to leading retailers for private label and captive label programs.

Brain Armor Inc. is 85% owned by Trident Brands and is organized to develop, market and sell a portfolio of DHA supplements under the Brain Armor® brand targeted at the cognitive health and performance segment.

Sports Nutrition Product Inc. (DBA Everlast Nutrition) is 100% owned by Trident Brands and holds an exclusive license to market and sell products in the nutritional food and supplement category under the Everlast® brand.

Trident Brands Canada Ltd. is 100% owned by Trident Brands Incorporated and holds various banking facilities, and licenses associated with the manufacturing, importation and sale of natural health and nutrition products in Canada.

Trident Brands International Ltd. is 100% owned by Trident Brands and was organized to handle the company’s international operations and sub-license trademarks and/or products in international markets.

5

The Company’s administrative office is located at 200 South Executive Drive, Suite 101, Brookfield, Wisconsin, 53005 and its fiscal year end is November 30th.

The Company has authorized capital of 300,000,000 common shares with a par value of $0.001 per share. 31,000,000 common shares were issued and outstanding as of August 31, 2017 and 32,311,887 as of October 16, 2017.

6

ITEM 1. FINANCIAL STATEMENTS

The unaudited financial statements for the quarter ended August 31, 2017 immediately follow.

7

TRIDENT BRANDS INCORPORATED

Consolidated Balance Sheets

(Unaudited)

|

As of

|

As of

|

|||||||

|

August 31, 2017

|

November 30, 2016

|

|||||||

|

ASSETS

|

||||||||

|

Current Assets

|

||||||||

|

Cash

|

$

|

4,130,378

|

$

|

1,527,624

|

||||

|

Restricted Cash

|

250,000 | - | ||||||

|

Accounts Receivable

|

661,799

|

53,053

|

||||||

|

Inventory

|

274,367

|

231,221

|

||||||

|

Prepaid

|

210,748

|

67,332

|

||||||

|

Total Current Assets

|

5,527,292

|

1,879,230

|

||||||

|

Fixed Assets-Furniture & Fixtures, net

|

28,029

|

-

|

||||||

|

Intangible Assets - Licenses, net

|

2,200,000

|

2,425,000

|

||||||

|

TOTAL ASSETS

|

$

|

7,755,321

|

$

|

4,304,230

|

||||

|

LIABILITIES & STOCKHOLDERS' DEFICIT

|

||||||||

|

Current Liabilities

|

||||||||

|

Accounts Payable

|

$

|

1,322,818

|

$

|

106,612

|

||||

|

Accrued Liability

|

1,150,958

|

431,178

|

||||||

|

Loan Payable - Third Party, net of discount $0 and $8,812, respectively

|

-

|

191,188

|

||||||

|

Total Current Liabilities

|

2,473,776

|

728,978

|

||||||

|

Convertible Debt, net of discount $2,220,465 and $1,285,836, respectively

|

8,579,535

|

5,114,164

|

||||||

|

Total Liabilities

|

11,053,311

|

5,843,142

|

||||||

|

Stockholders' Deficit

|

||||||||

|

Common stock, $0.001 par value, 300,000,000 shares authorized;

|

||||||||

|

31,000,000 shares issued and outstanding as of August 31, 2017 and November 30, 2016

|

31,000

|

31,000

|

||||||

|

Additional paid-in capital

|

6,922,854

|

5,431,976

|

||||||

|

Non-Controlling Interest in Subsidiary

|

(95,183

|

)

|

(65,786

|

)

|

||||

|

Accumulated Deficit

|

(10,156,661

|

)

|

(6,936,102

|

)

|

||||

|

Total Stockholders' Deficit

|

(3,297,990

|

)

|

(1,538,912

|

)

|

||||

|

TOTAL LIABILITIES & STOCKHOLDERS' DEFICIT

|

$

|

7,755,321

|

$

|

4,304,230

|

||||

See Notes to Unaudited Consolidated Financial Statements

8

TRIDENT BRANDS INCORPORATED

Consolidated Statements of Operations (unaudited)

|

Three Months

|

Three Months

|

Nine Months

|

Nine Months

|

|||||||||||||

|

Ended

|

Ended

|

Ended

|

Ended

|

|||||||||||||

|

August 31, 2017

|

August 31, 2016

|

August 31, 2017

|

August 31, 2016

|

|||||||||||||

|

Revenues

|

$

|

3,277,655

|

$

|

17,028

|

$

|

3,305,644

|

$

|

241,053

|

||||||||

|

Cost of Sales

|

3,117,150

|

9,388

|

3,132,266

|

135,364

|

||||||||||||

|

Gross Profit

|

160,505

|

7,640

|

173,378

|

105,689

|

||||||||||||

|

General, Selling & Administrative Expenses

|

(908,378

|

)

|

(502,659

|

)

|

(2,375,051

|

)

|

(1,755,774

|

)

|

||||||||

|

Loss from Operations

|

(747,873

|

)

|

(495,019

|

)

|

(2,201,673

|

)

|

(1,650,085

|

)

|

||||||||

|

Other Income (Expenses)

|

||||||||||||||||

|

Interest Expense

|

(489,593

|

)

|

(79,269

|

)

|

(1,048,283

|

)

|

(351,353

|

)

|

||||||||

|

Total Other Income (Expenses)

|

(489,593

|

)

|

(79,269

|

)

|

(1,048,283

|

)

|

(351,353

|

)

|

||||||||

|

Net Loss

|

$

|

(1,237,466

|

)

|

$

|

(574,288

|

)

|

$

|

(3,249,956

|

)

|

$

|

(2,001,438

|

)

|

||||

|

Net loss attributable to Trident

|

(1,228,122

|

)

|

(566,582

|

)

|

(3,220,559

|

)

|

(1,990,807

|

)

|

||||||||

|

Net loss attributable to Non-Controlling Interests

|

(9,344

|

)

|

(7,706

|

)

|

(29,397

|

)

|

(10,631

|

)

|

||||||||

|

Loss per share - Basic and diluted

|

$

|

(0.04

|

)

|

$

|

(0.02

|

)

|

$

|

(0.10

|

)

|

$

|

(0.07

|

)

|

||||

|

Weighted average number of common

|

||||||||||||||||

|

shares outstanding - Basic and diluted

|

31,000,000

|

31,000,000

|

31,000,000

|

30,596,364

|

||||||||||||

See Notes to Unaudited Consolidated Financial Statements

9

TRIDENT BRANDS INCORPORATED

Consolidated Statements of Cash Flows (unaudited)

|

Nine Months

|

Nine Months

|

|||||||

|

Ended

|

Ended

|

|||||||

|

August 31, 2017

|

August 31, 2016

|

|||||||

|

CASH FLOWS FROM OPERATING ACTIVITIES

|

||||||||

|

Net loss

|

$

|

(3,249,956

|

)

|

$

|

(2,001,438

|

)

|

||

|

Adjustments to reconcile net loss to net cash used in operating activities:

|

||||||||

|

Amortization of debt discount

|

540,850

|

190,245

|

||||||

|

Amortization of license

|

225,000

|

200,000

|

||||||

|

Stock option expense

|

24,211

|

101,565

|

||||||

|

Changes in operating assets and liabilities:

|

||||||||

|

Accounts Receivable

|

(608,746

|

)

|

(138,763

|

)

|

||||

|

Prepaid expenses

|

(143,416

|

)

|

646

|

|||||

|

Inventory

|

(43,146

|

)

|

(162,418

|

)

|

||||

|

Accounts payable and accrued liabilities

|

1,935,986

|

1,176,761

|

||||||

|

Cash used in operating activities

|

(1,319,217

|

)

|

(633,402

|

)

|

||||

|

CASH FLOWS FROM INVESTING ACTIVITIES

|

||||||||

|

Restricted Cash

|

(250,000 | ) | - | |||||

|

Purchase of Fixed Assets

|

(28,029

|

)

|

-

|

|||||

|

Cash used in investing activities

|

(278,029

|

)

|

-

|

|||||

|

CASH FLOWS FROM FINANCING ACTIVITIES

|

||||||||

|

Proceeds on loan payable - related party

|

-

|

200,000

|

||||||

|

Principal payments on loan payable - third party

|

(200,000

|

)

|

-

|

|||||

|

Proceeds on loan payable - third party

|

-

|

250,000

|

||||||

|

Proceeds on convertible debt

|

4,400,000

|

-

|

||||||

|

Cash provided by financing activities

|

4,200,000

|

450,000

|

||||||

|

Net change in cash

|

2,602,754

|

(183,402

|

)

|

|||||

|

Cash at beginning of period

|

1,527,624

|

187,886

|

||||||

|

Cash at end of period

|

$

|

4,130,378

|

$

|

4,484

|

||||

|

NON-CASH TRANSACTIONS

|

||||||||

|

Beneficial conversion features

|

$

|

1,466,667

|

$

|

-

|

||||

|

Common stock issued for asset acquisition

|

-

|

2,700,000

|

||||||

|

Relative fair value of warrants recorded as debt discount

|

-

|

78,776

|

||||||

|

Supplemental disclosure of cash flow information:

|

||||||||

|

Cash paid for:

|

||||||||

|

Income taxes

|

$

|

-

|

$

|

-

|

||||

|

Interest

|

$

|

20,083

|

$

|

-

|

||||

See Notes to Unaudited Consolidated Financial Statements

10

TRIDENT BRANDS INCORPORATED

Notes to Consolidated Financial Statements

August 31, 2017

(Unaudited)

NOTE 1. ORGANIZATION AND DESCRIPTION OF BUSINESS

Trident Brands Incorporated (f/k/a Sandfield Ventures Corp.) (“we”, “our”, “the Company”) was incorporated under the laws of the State of Nevada on November 5, 2007. The Company was formed to engage in the acquisition, exploration and development of natural resource properties.

The Company is now focused on the development of high growth branded and private label consumer products and ingredients within the nutritional supplement, life sciences and food and beverage categories. The Company is in its early growth stage and has transitioned out of its shell status with the Super-8 filing at the end of August, 2014. Activities to date have focused on capital formation, organizational development and execution of its branded and private label consumer products and ingredients business plan.

`

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The accompanying unaudited interim consolidated financial statements of Trident Brands Incorporated have been prepared in accordance with accounting principles generally accepted in the United States of America and the rules of the Securities and Exchange Commission, and should be read in conjunction with the audited consolidated financial statements and notes thereto contained in Trident’s Form 10-K filed with SEC. In the opinion of management, all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of financial position and the results of operations for the interim periods presented have been reflected herein. The results of operations for interim periods are not necessarily indicative of the results to be expected for the full year. Notes to the consolidated financial statements which would substantially duplicate the disclosure contained in the audited consolidated financial statements for fiscal 2016 as reported in the Form 10-K have been omitted.

Restricted Cash

Restricted cash of $250,000 as of August 31, 2017 represents cash held in a trust account. The funds have been set aside for the acquisition of StreamPak Ltd (see Note 9 regarding subsequent events) and to cover legal and other related costs.

Customer Concentration

The Company has one major customer that accounted for approximately 98% and $3,240,318 of sales for the nine month period ended August 31, 2017 and 97% of the accounts receivable.

Reclassification

Certain amounts in the 2016 consolidated financial statements have been reclassified to conform to the 2017 financial presentation. These reclassifications have no impact on net loss.

NOTE 3. LIQUIDITY

On September 26, 2016, the Company completed a long term financing with a non-US institutional investor, receiving proceeds of $4,100,000 and subsequently $4,400,000 on May 9, 2017 through the issuance of secured convertible promissory notes. The investor has agreed to make additional investments at the Company’s request of up to $1,500,000 ($10,000,000 in the aggregate). As of August 31, 2017, the Company had $4,380,378 in cash and has access to $1,500,000 available from the investor. The Company feels this represents substantial liquid resources (cash & available financing), sufficient to meet the Company’s obligations for the next twelve months.

NOTE 4. WARRANTS AND OPTIONS

The total outstanding stock options as of August 31, 2017 are 2,025,000. The Company uses the Black-Scholes model to value the stock options at $535,021. For the period ended August 31, 2017, the Company expensed $24,211 as compensation expense compared to $101,565 in the previous year. Following are the assumptions used for the shares vested 12, 24 and 36 months from the date of issuance: Discount rate 0.9%, 1.29%, 1.29%; Volatility 68.35%, 67.35%, 65.50%; and Term 3.0, 3.5, 4.0.

The following table represents stock option activity for the period ended August 31, 2017:

11

TRIDENT BRANDS INCORPORATED

Notes to Consolidated Financial Statements

August 31, 2017

(Unaudited)

|

Number of

Options

|

Weighted

Average

Exercise Price

|

Contractual Life

in Years

|

Intrinsic

Value

|

|||||||||||

|

Outstanding - November 30, 2016

|

2,358,333

|

$

|

0.96

|

2.51

|

||||||||||

|

Exercisable - November 30, 2016

|

1,666,667

|

$

|

1.17

|

2.43

|

||||||||||

|

Granted

|

-0-

|

$

|

0.0

|

|||||||||||

|

Exercised or Vested

|

-0-

|

|||||||||||||

|

Cancelled or Expired

|

333,333

|

|||||||||||||

|

Outstanding - August 31, 2017

|

2,025,000

|

$

|

0.96

|

1.68

|

||||||||||

|

Exercisable - August 31, 2017

|

2,025,000

|

$

|

0.96

|

1.68

|

$8,417

|

|||||||||

The total outstanding warrants as of August 31, 2017 are 225,000. The exercise price of the warrants are $1.35 with a term of 3 years and vested immediately. The Company uses the Black-Scholes model to value the warrants. Following are the assumptions used: Discount rate .9%; Volatility 76.25% and 77.30% respectively.

The following table represents warrant activity for the period ended August 31, 2017:

|

Number of

Warrants

|

Weighted

Average

Exercise Price

|

Contractual Life

in Years

|

Intrinsic

Value

|

|||||||||||

|

Outstanding – November 30, 2016

|

225,000

|

$

|

1.35

|

2.21

|

||||||||||

|

Exercisable - November 30, 2016

|

-0-

|

|||||||||||||

|

Granted

|

-0-

|

|||||||||||||

|

Exercised or Vested

|

-0-

|

|||||||||||||

|

Cancelled or Expired

|

-0-

|

|||||||||||||

|

Outstanding – August 31, 2017

|

225,000

|

$

|

1.35

|

1.45

|

$ | 0 | ||||||||

NOTE 5. RELATED PARTY TRANSACTIONS

The Company neither owns nor leases any real or personal property. The Company is paying a director $750 per month rent for use of office space and services.

NOTE 6. LOAN PAYABLE – THIRD PARTY

On February 29, 2016, the Company entered into a Securities Purchase Agreement with CIC whereby the Company received proceeds of $200,000 on March 4, 2016 in return for a $200,000 secured promissory note due 12 months from the issuance date, bearing interest at the rate of 10% per annum, plus 100,000 warrants to purchase common shares of the Company at an exercise price of $1.35 per share for three years from the date of issue. The loan was paid back on March 3, 2017. The remaining debt discount of $8,812 was fully amortized to interest expense during the nine months ended August 31, 2017.

12

TRIDENT BRANDS INCORPORATED

Notes to Consolidated Financial Statements

May 31, 2017

(Unaudited)

NOTE 7. CONVERTIBLE NOTE

On January 29, 2015, the Company entered into a securities purchase agreement with a non-US institutional investor whereby it agreed to sell an aggregate principal amount of $2,300,000 of senior secured convertible debentures, convertible into shares of the company’s common stock.

The Company received $1,800,000 of the funds from the transaction on February 5, 2015. The balance of $500,000 was received on May 14, 2015.

The convertible debentures are convertible into shares of the Company’s common stock at an initial conversion price of $0.71 per share, for an aggregate of up to 3,239,437 shares. The debentures originally accrued interest at 6% per annum. On September 26, 2016 the Company entered into an amendment agreement related to these convertible debentures whereby the applicable interest rate was increased from 6% to 8% and provisions added to allow the investor to transfer, sell or hypothecate the convertible notes subject to applicable securities laws. The maturity date of the notes was also extended through September 30, 2019.

Due to the note being convertible to common shares of the Company, a beneficial conversion feature analysis was performed. The intrinsic value of the conversion feature was $647,888 which was recognized as debt discount. As of August 31, 2017, the full amount of the debt discount has been amortized.

On September 26, 2016, the Company entered into a securities purchase agreement with a non-US institutional investor, pursuant to which, in consideration for proceeds of $4,100,000, the Company issued a secured convertible promissory note in the amount of $4,100,000. Pursuant to the securities purchase agreement, the investor has agreed, from time to time after January 1, 2017, to make additional investments at the Company’s request of up to $5,900,000 ($10,000,000 in the aggregate) in one or more tranches of not less than one tranche during any 60 day period. The funding of any tranche under the agreement (other than the first $4,100,000 which has been funded) is subject to the mutual agreement of the parties as to the use of funds.

On May 9, 2017, the Company received the second tranche of funding with proceeds of $4,400,000 for a total investment by the investor of $8,500,000. Under the terms of the securities purchase agreement, the Company has an additional $1,500,000 of available funding.

The Company intends to use the proceeds of the secured convertible note for general working capital purposes including, without limitation, settlement of accounts payable and repayment of mature loans.

In consideration of each advance made by the investor pursuant to the securities purchase agreement, the Company will issue to the investor a convertible promissory note of equal value, maturing three years after issuance, and bearing interest at the rate of 8% per annum. Each note will be secured in first priority against the present and after acquired assets of the Company, and will be convertible in whole or in part at the option of the holder into common shares of the Company at a conversion price of $0.60 per share, for an aggregate of up to 14,166,667 shares.

Due to the notes being convertible to common shares of the Company, a beneficial conversion feature analysis was performed. The intrinsic value of the conversion feature of the notes amounted to $2,833,334 and was recognized as a debt discount. As of August 31, 2017, $612,869 of the debt discount was amortized of which $532,038 was amortized during the current 9 month period and $80,831 in the prior year. The unamortized discount is $2,220,465.

The Company analyzed the embedded conversion option for derivative accounting consideration under ASC 815-15 “Derivatives and Hedging” and determined that the conversion option should be classified as equity.

13

TRIDENT BRANDS INCORPORATED

Notes to Consolidated Financial Statements

May 31, 2017

(Unaudited)

NOTE 8. INTANGIBLE ASSETS

On January 22, 2015, pursuant to a Deed of Assignment dated effective January 20, 2015, the Company entered into an Emulsion Supply Agreement with Oceans Omega LLC which represents the rights acquired pursuant to the Deed of Assignment. The Emulsion Supply Agreement provides the Company with the non-exclusive right and license (without the right to sublicense) to purchase, market, promote, sell and distribute Oceans Omega LLC’s omega-3 emulsions for use in the development, production, processing, manufacture and sale of food and beverages and exclusive rights to purchase, market, promote, sell and distribute Oceans Omega emulsions for meats, for human or animal consumption. On January 6, 2016 the Company issued 3,000,000 shares to mark the closing of the Deed of Assignment and the Emulsion Supply Agreement, which did not specify the amount of consideration payable by the Company when they were executed on January 20, 2015. The consideration payable was subsequently established by the parties at a market value of $2,700,000 and common shares issued as compensation based on the closing price of the common shares as quoted on the OTC Markets quotation systems on January 6, 2016. The value of the license is being amortized over the remaining contractual life which is 9 years. As of August 31, 2017, the net value of the license was $2,200,000 after amortizing $500,000. Amortization expense for the nine months ended August 31, 2017 and 2016 was $225,000 and $200,000, respectively.

NOTE 9. SUBSEQUENT EVENTS

On September 12, 2017 the Company entered into a note purchase agreement with Fengate Trident LP pursuant to which, in consideration for the issuance of 811,887 of our common shares to Fengate, we purchased outstanding secured convertible promissory notes of Mycell Technologies LLC having an aggregate balance due and payable of $511,141 in principal and $94,526 in interest accrued as at September 12, 2017. The purchased notes, which were originally issued to LPF (MCTECH) Investment Corp. on January 22, 2016, February 5, 2016, and May 19, 2016, bear simple interest on unpaid principal at the rate of ten percent per annum. The outstanding principal and accrued interest is convertible at the option of the note holder into securities of Mycell. We issued the 811,887 common shares to one (1) non-US person (as that term is defined in Regulation S of the Securities Act of 1933), in an offshore transaction relying on Regulation S of the Securities Act of 1933, as amended.

Also on September 12, 2017 we entered into a Share Purchase Agreement dated September 6, 2017 among our wholly owned subsidiary, Trident Brands International Ltd. (“Trident International”), a Bahamas corporation, StreamPak Ltd. (“StreamPak”), an Anguilla corporation, and the sole shareholder of StreamPak, pursuant to which, in consideration for the payment of $125,000 in cash and 500,000 of our common shares, Trident International purchased 100% of the issued and outstanding common shares of StreamPak. As a result of the share purchase StreamPak became a wholly owned subsidiary of Trident International. We issued the 500,000 common shares to one (1) non-US person (as that term is defined in Regulation S of the Securities Act of 1933), in an offshore transaction relying on Regulation S of the Securities Act of 1933, as amended.

14

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONS AND RESULTS OF OPERATIONS

Forward Looking Statements

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) should be read in conjunction with the interim consolidated financial statements, and notes thereto, for the quarter ended August 31, 2017 contained under Item 1 of this Quarterly Report on Form 10-Q (“Form 10-Q”) and in conjunction with the annual consolidated financial statements, and notes thereto, contained in the Annual Report on Form 10-K for the fiscal year ended November 30, 2016 (“Form 10-K”). Unless otherwise indicated herein, the discussion and analysis contained in this MD&A includes information available to October 16, 2017.

Certain statements contained in this MD&A may constitute forward-looking statements as defined under securities laws. Forward-looking statements may relate to our future outlook and anticipated events or results and may include statements regarding our future financial position, business strategy, budgets, litigation, projected costs, capital expenditures, financial results, taxes, plans and objectives. In some cases, forward-looking statements can be identified by terms such as “anticipate”, “estimate”, “intend”, “project”, “potential”, “continue”, “believe”, “expect”, “could”, “would”, “should”, “might”, “plan”, “will”, “may”, “predict”, the negatives of such terms, and other similar expressions concerning matters that are not historical facts. To the extent any forward-looking statements contain future-oriented financial information or financial outlooks, such information is being provided to enable a reader to assess our financial condition, material changes in our financial condition, our results of operations, and our liquidity and capital resources. Readers are cautioned that this information may not be appropriate for any other purpose, including investment decisions.

Forward-looking statements contained in this MD&A are based on certain factors and assumptions regarding expected growth, results of operations, performance, and business prospects and opportunities. While we consider these assumptions to be reasonable, based on information currently available, they may prove to be incorrect. Forward-looking statements are also subject to certain factors, including risks and uncertainties that could cause actual results to differ materially from what we currently expect. These factors are more fully described in the “Risk Factors” section at Item 1A of the Form 10-K.

Forward-looking statements contained in this commentary are based on our current estimates, expectations and projections, which we believe are reasonable as of the date of this report. You should not place undue importance on forward-looking statements and should not rely upon this information as of any other date. Other than as required under securities laws, we do not undertake to update any forward-looking information at any particular time.

All dollar amounts in this MD&A are expressed in thousands of U.S. dollars, except per share amounts, unless otherwise noted.

Business Developments

Effective December 12, 2016 we made the following changes to our officers and directors:

|

·

|

Donald MacPhee resigned as a Director of the Board of Directors, Chair of the Audit Committee and as President and Chief Executive Officer, and was appointed Director of Operations;

|

|

·

|

Anthony Pallante was appointed as Director and Chairman of our Board of Directors, and as Chief Executive Officer;

|

|

·

|

Mark Holcombe resigned as Chairman of the Board of Directors and was appointed as President, Director and Chair of the Compensation Committee.

|

|

·

|

Scott Chapman, our Director and Chair of the Corporate Governance Committee, was also appointed as Chair of the Audit Committee.

|

15

|

·

|

Michael Browne resigned as Corporate Secretary of Trident Brands Incorporated and will continue to serve as Brand Director, Chief Financial Officer, and Treasurer; and

|

|

·

|

Peter Salvo, Controller of the Company was also appointed as Corporate Secretary.

|

On February 15, 2017, we entered into a Letter of Intent (the “LOI”) with The Activation Group, Inc., an integrated marketing and advertising agency incorporated in Ontario, Canada. Pursuant to the LOI, we will seek to enter into a definitive agreement to purchase all the issued and outstanding common shares of The Activation Group in consideration for a purchase price consisting of $200,000 cash, and $800,000 payable in common shares of Trident. The cash consideration is inclusive of a $50,000 deposit paid to The Activation Group upon execution of the LOI, and $150,000 payable upon closing a definitive agreement. Stock payments shall be payable in four $200,000 installments, subject to the achievement of earnings targets. The transaction contemplated by the LOI will be subject to the satisfactory completion of due diligence, and to the negotiation and completion of a definitive agreement among the parties and the shareholders of The Activation Group.

Also, on February 15, 2017, our board of directors appointed Mark Cluett as the Chief Operating Officer at Trident Brands Incorporated, with responsibility for business strategy execution and commercialization.

On September 12, 2017 the Company entered into a note purchase agreement with Fengate Trident LP pursuant to which, in consideration for the issuance of 811,887 of our common shares to Fengate, we purchased outstanding secured convertible promissory notes of Mycell Technologies LLC having an aggregate balance due and payable of $511,141.17 in principal and $94,526.11 in interest accrued as at September 12, 2017. The purchased notes, which were originally issued to LPF (MCTECH) Investment Corp. on January 22, 2016, February 5, 2016, and May 19, 2016, bear simple interest on unpaid principal at the rate of ten percent per annum. The outstanding principal and accrued interest is convertible at the option of the note holder into securities of Mycell. We issued the 811,887 common shares to one (1) non-US person (as that term is defined in Regulation S of the Securities Act of 1933), in an offshore transaction relying on Regulation S of the Securities Act of 1933, as amended.

Also on September 12, 2017 we entered into a Share Purchase Agreement dated September 6, 2017 among our wholly owned subsidiary, Trident Brands International Ltd. (“Trident International”), a Bahamas corporation, StreamPak Ltd. (“StreamPak”), an Anguilla corporation, and the sole shareholder of StreamPak, pursuant to which, in consideration for the payment of $125,000 in cash and 500,000 of our common shares, Trident International purchased 100% of the issued and outstanding common shares of StreamPak. As a result of the share purchase StreamPak became a wholly owned subsidiary of Trident International. We issued the 500,000 common shares to one (1) non-US person (as that term is defined in Regulation S of the Securities Act of 1933), in an offshore transaction relying on Regulation S of the Securities Act of 1933, as amended.

Results of Operations

The following summary of our results of operations should be read in conjunction with our unaudited consolidated financial statements for the three month and nine month periods ended August 31, 2017 and August 31, 2016.

Our operating results for three month periods ended August 31, 2017 and August 31, 2016 are summarized as follows:

16

|

Three Months

Ended

|

Three Months

Ended

|

|||||||

|

August 31, 2017

|

August 31, 2016

|

|||||||

|

Revenues

|

$

|

3,277,655

|

$

|

17,028

|

||||

|

Gross Profit

|

$

|

160,505

|

$

|

7,640

|

||||

|

Operating Expenses

|

$

|

908,378

|

$

|

502,659

|

||||

|

Other Expenses

|

$

|

489,593

|

$

|

79,269

|

||||

|

Net Loss

|

$

|

1,237,466

|

$

|

574,288

|

||||

Revenues and Gross Profits

Revenue increased substantially in the quarter to $3,277,655 versus $17,028 in the prior year. This growth is attributed to a significant contract manufacturing supply agreement with a major retailer, coupled with increased direct sales of Brain Armor® products to professional sports teams and collegiate programs. Gross Profit increased to $160,505 or 4.9% of revenues versus $7,640 or 44.9% of revenues in the prior year as a result of the increase in sales. Management continues to direct operational support and focus toward markets, distribution channels and customers that represent sustainable commercial value. As such, we expect further revenue and profit growth in the remainder of 2017 and 2018. This outlook is supported by expanded retail customer supply agreements and new item listings coupled with further product innovation scheduled for introduction in Q4 2017 and Q1 2018.

Operating Expenses

Our operating expenses for the three month periods ended August 31, 2017 and August 31, 2016 are summarized below:

|

Three Months

Ended

|

Three Months

Ended

|

|||||||

|

August 31, 2017

|

August 31, 2016

|

|||||||

|

Professional Fees

|

$

|

41,618

|

$

|

11,716

|

||||

|

General & Administrative Expenses

|

$

|

461,330

|

$

|

235,826

|

||||

|

Marketing, Selling & Warehousing Expenses

|

$

|

274,254

|

$

|

142,359

|

||||

|

Management Salary

|

$

|

21,000

|

$

|

12,000

|

||||

|

Director's Fees

|

$

|

21,000

|

$

|

18,000

|

||||

|

Rent

|

$

|

2,926

|

$

|

2,171

|

||||

|

Royalty

|

$

|

86,250

|

$

|

80,587

|

||||

Operating expenses for the three month period ended August 31, 2017 were $908,378 as compared to $502,659 for the comparative period in 2016, an increase of 81%. The increase in our operating expenses was primarily due to increased general and administrative costs as we build out our organization and roll-out our product offering. These costs are expected to continue to increase throughout 2017 as we continue to develop and commercialize our product offerings.

Other Expenses

Other expenses for the three month period ended August 31, 2017 increased to $489,593 versus $79,269 in the comparative period in 2016. The increase was due to an increase in interest expense due to higher debt levels and the impact of certain other items including the beneficial conversion feature related to the convertible note entered into in 2017.

17

Nine Month Periods Ended August 31, 2017 and August 31, 2016

Our operating results for the nine month periods ended August 31, 2017 and August 31, 2016 are summarized as follows:

|

Nine Months

Ended

|

Nine Months

Ended

|

|||||||

|

August 31, 2017

|

August 31, 2016

|

|||||||

|

Revenues

|

$

|

3,305,644

|

$

|

241,053

|

||||

|

Gross Profit

|

$

|

173,378

|

$

|

105,689

|

||||

|

Operating Expenses

|

$

|

2,375,051

|

$

|

1,755,774

|

||||

|

Other Expenses

|

$

|

1,048,283

|

$

|

351,353

|

||||

|

Net Loss

|

$

|

3,249,956

|

$

|

2,001,438

|

||||

Revenues and Gross Profit

Revenue increased substantially for the nine month period ended August 31, 2017 to $3,305,644 versus $241,053 in the prior year. This growth is attributed to a significant contract manufacturing supply agreement with a major retailer, coupled with increased direct sales of Brain Armor® products to professional sports teams and collegiate programs. This translated into a corresponding increase in Gross Profit to $173,378 or 5.2% of revenues versus $105,689 or 43.8% of revenues in the prior year. Management continues to direct operational support and focus toward markets, distribution channels and customers that represent sustainable commercial value. As such, we expect further revenue and profit growth in the remainder of 2017 and 2018. This outlook is supported by expanded retail customer supply agreements and new item listings coupled with further product innovation scheduled for introduction in Q4 2017 and Q1 2018.

Operating Expenses

Our operating expenses for the nine month periods ended August 31, 2017 and August 31, 2016 are summarized below:

|

Nine Months

Ended

|

Nine Months

Ended

|

|||||||

|

August 31, 2017

|

August 31, 2016

|

|||||||

|

Professional Fees

|

$

|

133,796

|

$

|

111,469

|

||||

|

General & Administrative Expenses

|

$

|

1,281,536

|

$

|

767,121

|

||||

|

Marketing, Selling & Warehousing Expenses

|

$

|

569,531

|

$

|

550,954

|

||||

|

Management Salary

|

$

|

63,000

|

$

|

32,500

|

||||

|

Director's Fees

|

$

|

63,000

|

$

|

54,000

|

||||

|

Rent

|

$

|

7,521

|

$

|

6,016

|

||||

|

Royalty

|

$

|

256,667

|

$

|

233,714

|

||||

Operating expenses for the nine month period ended August 31, 2017 were $2,375,051 as compared to $1,755,774 for the comparative period in 2016, an increase of 35.3%. The increase in our operating expenses is primarily due to increased general and administrative costs as we build and roll-out our product offerings. These costs are expected to continue to increase throughout 2017 as we continue to develop and commercialize our product offerings.

18

Other Expenses

Other expenses for the nine month period ended August 31, 2017 increased to $1,048,283 versus $351,353 in the comparative period in 2016. The increase was due to an increase in interest expense due to higher debt levels and the impact of certain other items including the beneficial conversion feature related to the convertible note entered into in 2017.

Balance Sheet Data

The following table provides selected balance sheet as at August 31, 2017 and August 31, 2016.

|

Balance Sheet Data:

|

August 31, 2017

|

August 31, 2016

|

||||||

|

Cash

|

$

|

4,380,378

|

$

|

4,484

|

||||

|

Total assets

|

$

|

7,755,321

|

$

|

3,006,386

|

||||

|

Total liabilities

|

$

|

11,053,311

|

$

|

4,736,704

|

||||

|

Stockholders' (deficit)

|

$

|

(3,297,990

|

)

|

$

|

(1,730,318

|

)

|

||

Total assets and total liabilities increased in the nine month period ended August 31, 2017 versus the corresponding period last year as a result of the receipt of additional financing in September 2016 and May 2017.

Strategic Orientation

Our objective is to provide our shareholders with solid returns through strategic investments across multiple consumer product and food ingredient platforms. The platforms we are focusing on include:

|

·

|

Life science technologies and related products that have applications to a range of consumer products;

|

|

·

|

Nutritional supplements and related consumer goods providing defined benefits to the consumer; and

|

|

·

|

Functional foods and beverages ingredients with defined health and wellness benefits.

|

We are building our business through strategic investments in high growth early stage consumer brands and functional ingredients platforms within segment/sectors which we believe offer long term growth potential. We are focused on three core strategies underpinning our objectives:

|

·

|

To execute our multi-tier brand and innovation strategy to drive revenue;

|

|

·

|

To aggressively manage our asset light business model to drive a low cost platform; and

|

|

·

|

To drive disciplines leading to increased investor awareness and ability to finance and govern growing operations.

|

While we have yet to realize break even cash flows or profitability, we believe we are making progress against our goals and objectives, and expect revenues and margins to increase as we begin commercializing the products within our portfolio. All three of our product platforms show solid potential in the markets where they compete and both our Everlast® and Brain Armor® product lines are now in the market and generating revenues. Our strategy was to first establish listings for these products with non-bricks and mortar accounts, and this has been successful. Brain Armor® has now been listed at a large retail account as well, and we expect listings for Everlast® to follow. The development of Oceans Omega as an ingredient for food and beverage products is ongoing, and given the longer sales cycle for ingredients, we expect to realize revenues later in fiscal 2017 both through external customer product development and also internally via potential line extensions for both the Everlast® and Brain Armor® product lines.

19

Liquidity and Capital Resources

Our cash balance at August 31, 2017 was $4,380,378. Management believes the current funds available to the Company will be sufficient to fund our operations for the next twelve months.

On January 29, 2015, we entered into a securities purchase agreement with a non-US institutional investor whereby we agreed to sell an aggregate principal amount of $2,300,000 of senior secured convertible debentures, convertible into shares of the company’s common stock. We received $1,800,000 of the funds from the transaction on February 5, 2015 and the balance of $500,000 on May 14, 2015. On September 26, 2016, we entered into a Convertible Promissory Note Amendment Agreement with this investor whereby we agreed to extend the maturity date and amend the interest payable on the senior secured convertible debentures, whereby we extended the term of the notes through September 30, 2019 and interest rate was increased from 6% per annum to 8% per annum. The convertible debentures are convertible into shares of the Company’s common stock at an initial conversion price of $0.71 per share for an aggregate of up to 3,239,437 shares.

On September 26, 2016, we entered into a Securities Purchase Agreement with a non-US institutional investor pursuant to which, in consideration for proceeds of $4,100,000, we issued a secured convertible promissory note in the amount of $4,100,000. Pursuant to the Securities Purchase Agreement, the investor has agreed, from time to time after January 1, 2017, to make additional investments at our request of up to $5,900,000 ($10,000,000 in the aggregate) in one or more tranches of not less than one tranche during any 60 day period. The funding of any tranche under the agreement (other than the first $4,100,000 which has been funded) is subject to the mutual agreement of the parties as to the use of funds. The parties have agreed to negotiate in good faith to pre-approve use of funds within 120 days following September 26, 2016. On May 9, 2017, the Company received the second tranche of funding with proceeds of $4,400,000 for a total investment by the investor of $8,500,000. Under the terms of the securities purchase agreement, the Company has an additional $1,500,000 of available funding. We intend to use the proceeds of the secured convertible note for general working capital purposes including, without limitation, settlement of accounts payable and repayment of mature loans. In consideration of each advance made by the investor pursuant to the Securities Purchase Agreement, we will issue to the investor a convertible promissory note of equal value, maturing three years after issuance, and bearing interest at the rate of 8% per annum. Each note will be secured in first priority against the present and after acquired assets of the Company, and will be convertible in whole or in part at the option of the holder into common shares of the Company at a conversion price per share of $0.60, equal to a 25% discount to the 10 day average closing price of the Company’s common stock for the period immediately preceding the issuance of the applicable note. Due to the notes being convertible to the Company common shares, a beneficial conversion feature analysis was performed. The intrinsic value of the conversion feature was $1,366,667 and $1,466,667 respectively and which was recognized as debt discount. As of August 31, 2017, $612,869 of debt discount was amortized of which $532,038 was amortized during the current nine month period and $80,831 in the prior year. The unamortized discount is $2,220,465.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that is material to investors.

Contractual Obligations

Except for the transactions noted in Business Developments, there have been no material changes outside the normal course of business in our contractual obligations since January 3, 2015.

Critical Accounting Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities, related revenues and expenses, and disclosure of gain and loss contingencies at the date of the financial statements. The estimates and assumptions made require us to exercise our judgment and are based on historical experience and various other factors that we believe to be reasonable under the circumstances. We continually evaluate the information that forms the basis of our estimates and assumptions as our business and the business environment generally changes. The use of estimates is pervasive throughout our financial statements. There have been no material changes to the critical accounting estimates disclosed under the heading “Critical Accounting Estimates” in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, of the Form 10-K.

20

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

As a smaller reporting company we are not required to provide this information.

ITEM 4. CONTROLS AND PROCEDURES

Evaluation of Disclosure Controls and Procedures

Under the supervision and with the participation of our management, including our principal executive officer and the principal financial officer, we have conducted an evaluation of the effectiveness of the design and operation of our disclosure controls and procedures, as defined in Rules 13a-15(e) and 15d-15(e) under the Securities and Exchange Act of 1934, as of the end of the period covered by this report. Based on this evaluation, our principal executive officer and principal financial officer concluded as of the evaluation date that our disclosure controls and procedures were not effective such that the material information required to be included in our Securities and Exchange Commission reports is accumulated and communicated to our management, including our principal executive and financial officer, recorded, processed, summarized and reported within the time periods specified in SEC rules and forms relating to our company, particularly during the period when this report was being prepared.

Changes in Internal Controls Over Financial Reporting

Our management, with the participation of our principal executive officer and principal financial officer have concluded that there have been no changes in our internal control over financial reporting that occurred during the last fiscal quarter ended August 31, 2017 that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

PART II. OTHER INFORMATION

ITEM 6. EXHIBITS

The following exhibits are included with this quarterly filing:

|

Exhibit No.

|

Description

|

|

|

3.1

|

Articles of Incorporation*

|

|

|

3.2

|

Bylaws*

|

|

|

31.1

|

Sec. 302 Certification of Chief Executive Officer

|

|

|

31.2

|

Sec. 302 Certification of Chief Financial Officer

|

|

|

32.1

|

Sec. 906 Certification of Chief Executive Officer

|

|

|

32.2

|

Sec. 906 Certification of Chief Financial Officer

|

|

|

101

|

Interactive data files pursuant to Rule 405 of Regulation S-T.

|

| * |

Document is incorporated by reference and can be found in its entirety in our Registration Statement on Form SB-2, SEC File Number 333-148710, at the Securities and Exchange Commission website at www.sec.gov.

|

21

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

|

October 16, 2017

|

Trident Brands Incorporated

|

|

|

/s/ Anthony Pallante

|

||

|

By: Anthony Pallante

|

||

|

(Chief Executive Officer & Chair of the Board)

|

||

|

/s/ Mike Browne

|

||

|

By: Mike Browne

|

||

|

(Chief Financial Officer)

|

||

|

/s/ Mark Holcombe

|

||

|

By: Mark Holcombe

|

||

|

(President & Director)

|

||

|

/s/ Scott Chapman

|

||

|

By: Scott Chapman

|

||

|

(Director)

|

||

22