Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - Merchants Bancorp | a2233443zex-23_1.htm |

| EX-10.8 - EX-10.8 - Merchants Bancorp | a2233443zex-10_8.htm |

| EX-5.1 - EX-5.1 - Merchants Bancorp | a2233443zex-5_1.htm |

| EX-2.2 - EX-2.2 - Merchants Bancorp | a2233443zex-2_2.htm |

| EX-1.1 - EX-1.1 - Merchants Bancorp | a2233443zex-1_1.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

Index to Consolidated Financial Statements of Merchants Bancorp

As filed with the Securities and Exchange Commission on October 16, 2017.

Registration No. 333-220623

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

Form S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

MERCHANTS BANCORP

(Exact name of registrant as specified in its charter)

| Indiana | 6022 | 20-5747400 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

11555 North Meridian Street, Suite 400

Carmel, Indiana 46032

(317) 569-7420

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

John F. Macke

Principal Financial Officer

Merchants Bancorp

11555 North Meridian Street, Suite 400

Carmel, Indiana 46032

(317) 569-7420

(Name, address, including zip code and telephone number, including area code, of agent for service)

Copies to:

| Michael J. Messaglia | Frank M. Conner III | |

| Robert J. Wild | Michael P. Reed | |

| Krieg DeVault LLP | Covington & Burling LLP | |

| One Indiana Square, Suite 2800 | One CityCenter | |

| Indianapolis, Indiana 46204 | 850 Tenth Street, NW | |

| (317) 636-4341 | Washington, D.C. 20001 | |

| (202) 662-6000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer" "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o Emerging growth company ý |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. o

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the Registration Statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED OCTOBER 16, 2017

PRELIMINARY PROSPECTUS

5,555,555 Shares

Common Stock

This prospectus relates to the initial public offering of Merchants Bancorp. We are a diversified bank holding company headquartered in Carmel, Indiana.

Prior to this offering, there has been no established public market for our common stock. We anticipate that the public offering price of our common stock will be between $17.00 and $19.00 per share. We have applied to list our common stock on the Nasdaq Capital Market under the trading symbol "MBIN."

Investing in our common stock involves risk. See "Risk Factors" beginning on page 17.

We are an "emerging growth company" under the federal securities laws and will be subject to reduced public company reporting requirements. See "Implications of Being an Emerging Growth Company."

| |

Per Share | Total | |||||

|---|---|---|---|---|---|---|---|

Initial public offering price |

$ | $ | |||||

Underwriting discounts |

|||||||

Proceeds to us, before expenses |

|||||||

We have granted the underwriters an option to purchase up to an additional 833,333 shares from us at the initial public offering price, less the underwriting discounts, within 30 days from the date of this prospectus.

Neither the Securities and Exchange Commission nor any other state securities commission nor any other regulatory authority has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Shares of our common stock are not savings accounts or deposits and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

The underwriters expect to deliver the shares of our common stock against payment in New York, New York, on or about , 2017.

| Sandler O'Neill + Partners, L.P. | Stephens Inc. | Raymond James | ||

SunTrust Robinson Humphrey |

||||

The date of this prospectus is , 2017.

i

You should rely only on the information contained in this prospectus or in any free writing prospectus that we authorize to be delivered to you. We and the underwriters have not authorized anyone to provide you with different or additional information. We and the underwriters are not making an offer of these securities in any jurisdiction where the offer is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

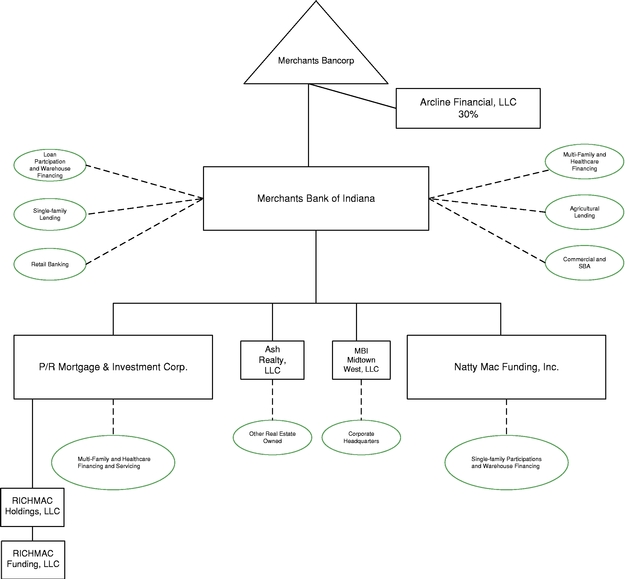

Unless we state otherwise or the context otherwise requires, references in this prospectus to "we," "our," "us" or "the Company" refer to Merchants Bancorp, an Indiana corporation, and our consolidated subsidiaries, references to "Merchants Bank" or the "Bank" refer to our banking subsidiary, Merchants Bank of Indiana, an Indiana state chartered bank, references to "P/RMIC" refer to the Bank's subsidiary, P/R Mortgage and Investment Corp., an Indiana corporation, references to "RICHMAC" refer collectively to P/RMIC's subsidiaries, RICHMAC Holdings, LLC, an Indiana limited liability company and RICHMAC Funding, LLC, a Delaware limited liability company, references to "NMF" refer to the Bank's subsidiary, Natty Mac Funding, Inc., an Indiana corporation, references to "Midtown West" refer to the Bank's subsidiary, MBI Midtown West, LLC, an Indiana limited liability company, and references to "Ash Realty" refer to the Bank's subsidiary, Ash Realty Holdings, LLC.

Within this prospectus, we reference certain market, industry and demographic data and other statistical information. We have obtained this data and information from various independent, third party industry sources and publications. Nothing in the data or information used or derived from third party sources should be construed as advice. Some data and other information are also based on our good faith estimates, which are derived from our review of internal surveys and independent sources. We believe that these external sources and estimates are reliable, but have not independently verified them. Statements as to our market position are based on market data currently available to us. Although we are not aware of any misstatements regarding the economic, employment, industry and other market data presented herein, these estimates involve inherent risks and uncertainties and are based on assumptions that are subject to change.

IMPLICATIONS OF BEING AN EMERGING GROWTH COMPANY

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an "emerging growth company" under the Jumpstart Our Business Startups Act of 2012 (the "JOBS Act"). An emerging growth company may take advantage of reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. As an emerging growth company:

- •

- we may present as few as two years of audited financial statements and two years of related management discussion and analysis of financial

condition and results of operations;

- •

- we are exempt from the requirement to obtain an attestation and report from our auditors on management's assessment of our internal control

over financial reporting under the Sarbanes-Oxley Act of 2002;

- •

- we are permitted to provide less extensive disclosure about our executive compensation arrangements; and

- •

- we are not required to give our shareholders non-binding advisory votes on executive compensation or golden parachute arrangements.

ii

In this prospectus we have elected to take advantage of the reduced disclosure requirements relating to executive compensation and the number of years of financial information presented, and in the future we may take advantage of any or all of these exemptions for so long as we remain an emerging growth company. We will remain an emerging growth company until the earliest of (i) the end of the fiscal year during which we have total annual gross revenues of $1.07 billion or more, (ii) the end of the fiscal year following the fifth anniversary of the completion of this offering, (iii) the date on which we have, during the previous three-year period, issued more than $1.07 billion in non-convertible debt and (iv) the date on which we are deemed to be a "large accelerated filer" under the Securities Exchange Act of 1934, as amended (the "Exchange Act").

In addition to the relief described above, the JOBS Act permits us an extended transition period for complying with new or revised accounting standards affecting public companies. We intend to take advantage of this extended transition period.

iii

This summary highlights selected information contained elsewhere in this prospectus and may not contain all of the information that you should consider before investing in our common stock. Before making an investment decision you should carefully read the entire prospectus, including the sections entitled "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations," together with our consolidated financial statements and the related notes that are included herein.

Our Company Overview

We are a diversified bank holding company headquartered in Carmel, Indiana and registered under the Bank Holding Company Act of 1956, as amended. We currently operate multiple lines of business with a focus on Federal Housing Administration ("FHA") multi-family housing and healthcare facility financing and servicing, mortgage warehouse financing, retail and correspondent residential mortgage banking, agricultural lending and traditional community banking. As of June 30, 2017, we had $3.1 billion in assets, $2.8 billion of deposits and $226.5 million of shareholders' equity.

We were founded in 1990 as a mortgage banking company, providing financing for multi-family housing and senior living properties. The shared vision of our founders, Michael Petrie and Randall Rogers, was to create a diversified financial services company, which efficiently operates both nationally through mortgage banking and related services and locally through a community bank. We have grown both organically and through acquisitions focused on expanding our services. We have strategically built our business in a way that we believe offers insulation from cyclical economic and credit swings and may provide us with synergies across our lines of business.

Experienced Board and Management Team

Our founders, Michael Petrie and Randall Rogers, each have over 38 years of industry experience. Prior to founding Merchants, Mr. Petrie and Mr. Rogers worked together as Merchants Mortgage Corporation, a company founded by Mr. Rogers, with Mr. Rogers as Chief Executive Officer and Mr. Petrie as Executive Vice President.

In addition to our founders, the other members of our executive management team collectively have, on average, over 27 years of industry experience, each with a diverse and complementary background that is an integral part of our success. Michael Dunlap, the President and Co-Chief Operating Officer of Merchants Bank, has primarily been responsible for establishing our warehouse lending platform and Merchants Mortgage, and previously served in senior management and financial roles for several mortgage companies, including as Chief Financial Officer of National City Mortgage. John Macke, our Chief Financial Officer, previously served as Executive Vice President of Capital Markets and as Chief Financial Officer of Stonegate Mortgage Corporation. Scott Evans, President of Merchants Bank's Lynn Market and Co-Chief Operating Officer, has extensive experience in community banking, including as Vice President of The Farmers State Bank for over 10 years, and is primarily responsible for our Banking segment, including our agriculture lending activities. Michael Dury, the Executive Vice President and Chief Operating Officer of P/RMIC, oversees P/RMIC's strategy and business development for multi-family and healthcare financing activities and since 2010 has originated over $3 billion of multi-family loan volume. For more information on our executive management team, see the "Management" section below in this prospectus. The below table provides a

1

summary of our executive management team and reflects each member's respective current ownership of our common stock as of October 12, 2017.

Name

|

Title | Age | Years in Financial Services |

Years with the Company |

Ownership | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Michael F. Petrie |

Chairman and Chief Executive Officer of Merchants and Merchants Bank | 63 | 38 | 27 | 46.53 | %(1) | |||||||||

Randall D. Rogers |

President and Chief Operating Officer of Merchants, Vice Chairman of Merchants Bank |

71 |

48 |

27 |

44.84 |

%(2) |

|||||||||

Michael J. Dunlap |

President and Co-Chief Operating Officer of Merchants Bank |

51 |

25 |

8 |

* |

||||||||||

John F. Macke |

Chief Financial Officer of Merchants and Merchants Bank |

52 |

25 |

0 |

— |

||||||||||

Michael R. Dury |

Executive Vice President and Chief Operating Officer of P/RMIC |

32 |

10 |

10 |

* |

||||||||||

Scott A. Evans |

Lynn Market President and Co-Chief Operating Officer of Merchants Bank |

52 |

28 |

13 |

* |

||||||||||

Susan D. Kucer |

Indianapolis Market President of Merchants Bank |

62 |

35 |

2 |

— |

||||||||||

Jerry F. Koors |

President of Merchants Mortgage |

53 |

26 |

4 |

* |

||||||||||

Richard L. Belser |

Senior Vice President and Senior Credit Officer of Merchants Bank |

66 |

43 |

10 |

— |

||||||||||

Bill D. Buchanan |

Senior Vice President and Chief Accounting Officer of Merchants and Merchants Bank |

59 |

29 |

3 |

* |

||||||||||

Kevin T. Langford |

Senior Vice President and Chief Administrative Officer of Merchants Bank |

49 |

27 |

1 |

— |

||||||||||

| | | | | | | | | | | | | | | | |

TOTAL |

91.57 |

%(3) |

|||||||||||||

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

AVERAGE |

30.36 |

9.55 |

|||||||||||||

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

- *

- denotes

less than 1%

- (1)

- Includes

38.58% beneficially owned by Mr. Petrie's wife, Jody J. Petrie. See "Security Ownership of Certain Beneficial Owners and Management" for additional

information.

- (2)

- Includes

43.59% beneficially owned by Mr. Rogers' wife, Mary H. Rogers. See "Security Ownership of Certain Beneficial Owners and Management" for additional

information.

- (3)

- Includes 82.17% beneficially owned by Mr. Petrie's or Mr. Rogers' wives as described in (1) and (2) above.

Upon the closing of this offering, Messrs. Petrie and Rogers, together with their families, will hold approximately 73.97% of our outstanding common stock. Therefore, Messrs. Petrie and Rogers, together with their families, will have the ability to control the outcome of matters submitted to our shareholders for approval, including the election or removal of directors and the amendment of our articles of incorporation, along with approval of significant transactions. This control position may conflict with the interests of some or all of our other shareholders. In addition, Messrs. Petrie and Rogers, together with their families, own approximately 24.02% of our outstanding 8% Non-Cumulative, Perpetual Preferred Stock.

Our five non-executive directors are all successful business owners, professionals or senior executives with long-standing ties to their communities. The collective professional background of our

2

directors provides us with valuable insights into the business and banking needs of our customer base. After the completion of this offering, our five non-executive directors and their affiliated entities, collectively, are expected to own approximately 0.15% of our outstanding common stock.

Our Growth

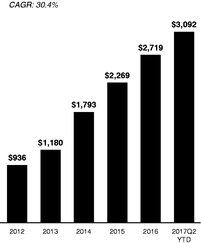

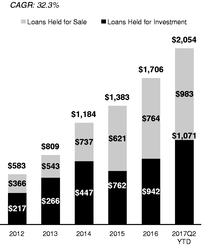

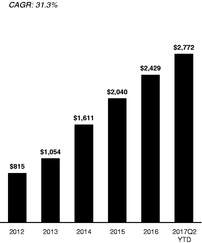

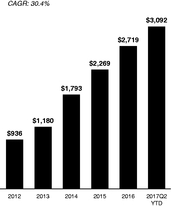

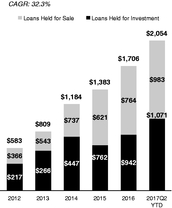

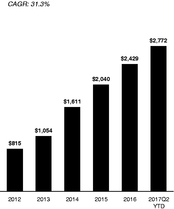

Since our acquisition of Merchants Bank (formerly known as Greensfork Township State Bank), with assets of $6.7 million in March 2002, we have achieved significant growth in many of our key financial performance categories. During this period, we have maintained an acute focus on building profitable and complementary business lines that provide for insulation from cyclical swings and create synergies within our lines of business that give us competitive advantages. Since December 31, 2012, we have seen significant growth in our total assets, total gross loans and total deposits. Between December 31, 2012 and June 30, 2017, our total assets have grown at a compound annual growth rate of 30.4%, from $936 million to $3.1 billion, and we increased total gross loans (including loans held for investment and loans held for sale) at a compound annual growth rate of 32.3%, from $583 million to $2.1 billion. We have funded our growth during this period, in large part, through a substantial increase in deposits, which we have increased from $815 million to $2.8 billion, a compound annual growth rate of 31.3%.

Our growth thus far is due primarily to the consistent production and efficiency of P/RMIC and the scalable growth of our warehouse lending line of business. P/RMIC has grown the unpaid principal balance of its servicing portfolio from $2.8 billion as of December 31, 2012 to $6.2 billion as of June 30, 2017, while our warehouse lending funded volumes have grown from $8.3 billion in 2012 to $24.8 billion in 2016. Over the same period of time we have experienced low levels of non-performing assets and charge-offs, driven principally by the nature of our lending business and our focus on originating assets with favorable risk profiles.

| Total Assets ($ in Millions) |

Total Gross Loans ($ in Millions) |

Total Deposits ($ in Millions) |

||

|

|

|

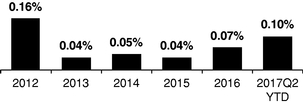

| Nonperforming Assets / Total Assets | Net Charge-offs / Average Loans | |

|

|

3

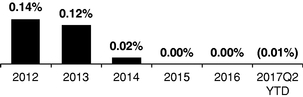

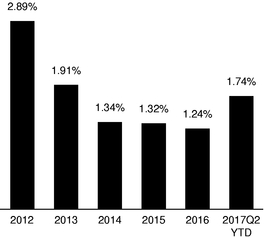

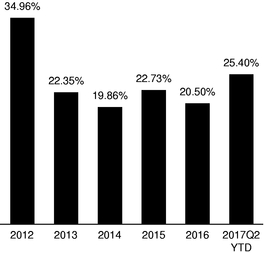

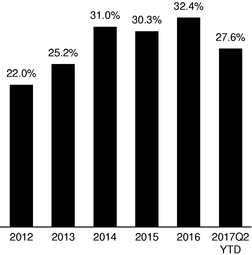

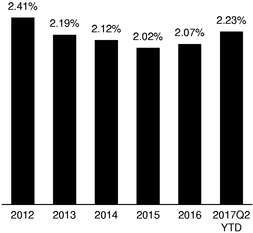

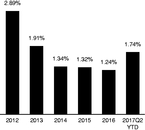

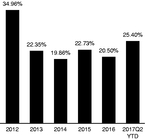

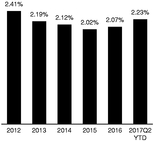

During every period since January 1, 2012, as shown in the chart below, we have maintained a return on average assets above 1.23%, a return on average tangible common equity over 19%, and an efficiency ratio under 33%. We were able to achieve these metrics despite historically earning a lower net interest rate margin than most banks, which is caused by originating low risk, shorter-term assets.

| Return on Average Assets(1) |

Return on Average Tangible Common Equity(1) |

|

|

|

| Efficiency Ratio | Net Interest Margin | |

|

|

- (1)

- In 2014, for federal income tax purposes, we converted from a Subchapter S corporation to a C corporation. The 2012 and 2013 performance metrics reflect adjustments to net income to enhance comparability with subsequent years. Specifically, for 2012 and 2013, we adjusted net income for pro-forma federal and state corporate income tax expenses to which we were subject following our conversion to a C corporation, using an assumed income tax rate of 40%. Net income also was adjusted for 2014 to reverse the charge we recorded for the conversion of deferred tax liabilities in connection with our conversion from a Subchapter S to C corporation. These pro-forma net income metrics are non-GAAP financial measures. Refer to "Non-GAAP Financial Measures" for additional discussion regarding pro-forma net income and a reconciliation of this metric to net income.

4

Our Corporate Structure

We have multiple lines of business and provide various banking and financial services through our subsidiaries as follows:

- •

- Multi-Family Rental Housing

- •

- Healthcare Financing

- •

- Servicing and Subservicing

P/R Mortgage & Investment Corp. (a subsidiary of Merchants Bank)

- •

- Multi-Family Rental Housing

RICHMAC Funding, LLC (a subsidiary of P/RMIC)

- •

- Warehouse Financing and Loan Participations

- •

- Commercial Lending

- •

- Retail Banking

- •

- SBA Small Business Loan Programs

- •

- Agricultural Lending

- •

- Merchants Mortgage

- •

- Single-Family Mortgage Lending

- •

- Correspondent Mortgage Banking

Merchants Bank of Indiana

- •

- Warehouse Financing and Loan Participations

Natty Mac Funding, Inc. (a subsidiary of Merchants Bank)

5

P/RMIC: Multi-Family Rental Housing, Healthcare Financing and Servicing

P/RMIC is primarily engaged in mortgage banking, specializing in originating and servicing loans for multi-family rental housing and healthcare facility financing, particularly for senior living properties.

P/RMIC originated $1.2 billion in loans during 2016 and $906 million during the six months ended June 30, 2017. P/RMIC primarily originates FHA loans that are sold as Government National Mortgage Association ("Ginnie Mae") mortgage backed securities within approximately 30 days. The loans are sold and the mortgage servicing rights are retained. Other originations include bridge and permanent financing that are referred to the Banking segment. These loans eventually become permanent FHA financings by P/RMIC. In addition to the $1.2 billion originated directly by P/RMIC, we also funded loans brought to us by non-affiliated entities. As of June 30, 2017, P/RMIC's servicing portfolio totaled $6.2 billion, which includes both owned and subserviced loans.

We generated approximately $22.6 and $23.0 million, or 41.9% and 27.9%, of net revenue (net interest income plus non-interest income) from our Multi-family Mortgage Banking segment for the six months ended June 30, 2017 and year ended December 31, 2016, respectively.

6

RICHMAC Funding, LLC

In August 2017, P/RMIC acquired RICHMAC Funding, LLC, a national multi-family housing mortgage lender, to complement and expand the products and services offered by P/RMIC.

MERCHANTS BANK

Warehouse Financing and Loan Participations

Merchants Bank started our warehouse lending business in 2009 as a result of dislocation in the market. Merchants Bank currently has warehouse lines of credit and loan participations with some of the largest non-depository financial institutions in the country. As of June 30, 2017, Merchants Bank and NMF had $1.2 billion in loans outstanding from warehouse lines for credit to single and multi-family lenders and loan participations. We generated approximately $17.7 and $35.3 million, or 32.9% and 42.8%, of net revenue (net interest income plus non-interest income) from our Mortgage Warehousing segment for the six months ended June 30, 2017 and year ended December 31, 2016, respectively.

Commercial Lending and Retail Banking

Merchants Bank operates under an Indiana charter and provides full banking services. Merchants Bank has five depository branches located in Carmel, Indianapolis and Lynn, Indiana. Merchants Bank holds loans in its portfolio comprised of multi-family construction and bridge loans referred by P/RMIC, owner occupied commercial real estate loans, commercial & industrial loans, agricultural loans, residential mortgage loans and consumer loans. Merchants Bank receives deposits from customers located primarily in Hamilton, Marion, Randolph and surrounding counties in Indiana and from the escrows generated by the servicing activities of P/RMIC.

SBA Lending

Merchants Bank participates in the Small Business Administration's ("SBA") 7(a) program in order to meet the needs of our small business community, and help diversify our retail revenue stream. We originate and service, as well as sell the guaranteed portion of these loans. As of June 30, 2017, Merchants Bank had originated $4.5 million in SBA 7(a) loans in Marion and Hamilton counties in Central Indiana since our participation in this program.

The SBA's 7(a) program provides up to a 75% guaranty for loans greater than $150,000. For loans $150,000 or less, the program provides up to an 85% guaranty. The maximum 7(a) loan amount is $5 million. The guaranty is conditional and covers a portion of the risk of payment default by the borrower, but not the risk of improper closing and servicing by the lender. As such, prudent underwriting and closing processes are essential to effective utilization of the 7(a) program. We typically sell in the secondary market the SBA-guaranteed portion (generally 75% of the principal balance) of the loans we originate.

Agricultural Lending

Merchants Bank has a division ("MBI-Lynn") located in Lynn, Randolph County, Indiana with its primary business function to provide agricultural loans within its designated Community Reinvestment Act ("CRA") area of Randolph and Wayne counties in Eastern Indiana and nearby Darke County, Ohio. Merchants Bank offers operating lines of credit for crop and livestock production, intermediate term financing to purchase equipment and breeding livestock and long-term financing to purchase agricultural real estate. As of June 30, 2017, of the $66.4 million of agricultural loans in our portfolio, including undisbursed funds of $4.3 million, 48.2% have a Farm Service Agency ("FSA") 90% guarantee. Merchants Bank is approved to sell agricultural loans in the secondary market through the

7

Federal Agricultural Mortgage Corporation ("Farmer Mac") and uses this relationship to manage interest rate risk within the agricultural loan portfolio. As of June 30, 2017, Merchants Bank sold agricultural loans with an aggregate principal balance of $13.5 million to Farmer Mac without recourse. Merchants Bank has written off less than $25 thousand in loan loss in its agricultural loan portfolio since December 31, 2004.

MERCHANTS MORTGAGE: Single Family Mortgage Lending, Correspondent Lending and Servicing

Merchants Mortgage is the branded arm and division of Merchants Bank that is a full service single-family mortgage origination and servicing platform started in February 2013. Merchants Mortgage is both a retail and correspondent mortgage lender. Merchants Mortgage offers agency eligible, jumbo fixed and hybrid adjustable rate mortgages for purchase or refinancing. Other products include construction, bridge and lot financing and home equity lines of credit ("HELOC"), including the All-in-One product, which links a customer's checking account balance to a first lien HELOC. Merchants Mortgage generates revenues from fees charged to borrowers, interest income during the warehouse period, and gain on sale of loan to investors. There are multiple investor outlets, including direct sale capability to Federal National Mortgage Association ("Fannie Mae"), Federal Home Loan Mortgage Corporation ("Freddie Mac"), Federal Home Loan Bank of Indianapolis (the "FHLBI"), and other third-party investors to allow Merchants Mortgage a best execution at sale. Merchants Mortgage also originates loans held for investment and earns interest income over the life of the loan.

NMF: Warehouse Financing and Loan Participations

Through NMF we engage in loan participations and warehouse financing with Home Point Financial Corporation ("Home Point") and its subsidiaries and correspondent customers. NMF was established as a wholly owned subsidiary of Merchants Bank in 2014. We entered into a Revolving Loan and Subordinated Loan Agreement whereby Home Point invested $30 million in our subordinated debt. In turn, we invested the proceeds into Merchants Bank and then to NMF. NMF provides $300 million of lending capacity to Home Point and its subsidiaries and correspondent customers. We earn net interest income and use Home Point custodial deposits to fund the loans.

MIDTOWN WEST

MBI Midtown owns land upon which we expect to build our new corporate headquarters building in Carmel, Indiana.

ASH REALTY

Ash Realty holds assets acquired through, or in lieu of, loan foreclosures. At June 30, 2017, there were no assets held in Ash Realty.

ARCLINE FINANCIAL, LLC

Merchants owns 30% of Arcline Financial, LLC ("Arcline") and is accounted for using the equity method of accounting. Arcline processes warehouse and correspondent lending transactions, including on behalf of Merchants Bank.

Our Strategic Plan

Our strategic plan focuses on continuing to grow complementary business lines that will provide a diverse and stable revenue platform and create a balance between interest and non-interest income. Our strategic plan reflects our belief that our mortgage business and community banking structure

8

complement one another by creating important operational and revenue synergies. Our strategic plan includes five initiatives:

- •

- maintain and grow complementary and diversified business lines;

- •

- develop deep customer relationships;

- •

- execute prudent acquisitions in strategic areas;

- •

- hire experienced and talented personnel while developing talented personnel from within our organization; and

- •

- maintain a low risk profile through strong enterprise-wide risk management.

We have achieved our recent growth through focused and sustained execution of these initiatives, and we believe that we have an experienced management team in place that will allow us to continue this success.

Our Competitive Strengths

We believe our competitive strengths set us apart from many similarly sized community banks and mortgage banking companies, and include the following key attributes:

Diversified business lines within our mortgage banking business. Our primary business lines within our mortgage banking business are complementary and provide a diverse and stable source of revenue. Our subsidiaries and divisions are integrated and offer opportunities for operational and revenue synergies. For example, Merchants Bank provides short-term lending support for P/RMIC originations in the form of bridge or construction financing. P/RMIC, in turn, deposits custodial escrow servicing accounts at Merchants Bank, which can be invested in securities and pledged to the FHLBI for additional funding capacity. Although we are exposed to the systemic risk in the mortgage market and the economy as a whole, our performance is not directly correlated with mortgage origination volumes. For example, for the year ended December 31, 2016, our mortgage warehouse lending funding volumes increased by 23%, while the mortgage market as a whole increased by 13%. In addition, for the six months ended June 30, 2017 our mortgage warehouse lending volumes increased 4.3% compared to the six months ended June 30, 2016, while the mortgage market as a whole decreased by 4.2% (based on market volumes from Mortgage Bankers Association of America). We largely attribute our ability to succeed under various market conditions to our low efficiency ratio, which is mainly a result of our variable cost operating model, and our balanced presence in single and multi-family finance. In rising rate environments, single family mortgage origination volumes may fall, however this should be offset through increased net interest margin. Additionally, as market interest rates rise, originations for multi-family housing may decrease, but the value of our servicing asset increases due to a lesser expectation of prepayment. In falling rate environments, we may expect to see increased gain on sale income from purchase and refinance originations in both the single and multi-family mortgage markets to offset a potential decrease in the value of our servicing asset due to higher prepayments. Thus, Merchants Mortgage's position in the single-family and P/RMIC's position in multi-family housing sector offers us an alternative against variability in the mortgage industry.

Stable source of non-interest income reduces risks associated with changes in interest rates. Just as we strive to have diversification within our business lines, we also strive to maintain a complementary and diversified revenue model. We believe that this balanced revenue stream approach can help minimize volatility in our earnings through various economic and interest rate cycles. As a result, we do not have an undue reliance on one source of income, such as net interest income, which can be materially affected by changes in interest rates, or non-interest income, which can be materially affected by reductions in mortgage volumes. Historically, P/RMIC earned fees and servicing income (non-interest income) that greatly outweighed the interest income earned by Merchants Bank. We recognize our

9

reliance on this revenue stream and have implemented strategies to augment the revenue. Since 2012, we have increased our portfolio of loans held for investment to balance our income and to reduce our reliance on a single source of income.

| |

For the Six Months Ended June 30, |

For the Year Ended December 31, | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Dollars in thousands) |

2017 | 2016 | 2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||

| |

(unaudited) |

|

|

|

|

|

||||||||||||||||

Net Interest Income |

$ | 29,255 | $ | 23,819 | $ | 53,971 | $ | 42,055 | $ | 30,630 | $ | 25,708 | $ | 20,710 | ||||||||

Non-Interest Income |

24,717 | 9,951 | 28,504 | 27,008 | 20,263 | 27,284 | 36,121 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Revenue |

$ | 53,972 | $ | 33,770 | $ | 82,475 | $ | 69,063 | $ | 50,893 | $ | 52,992 | $ | 56,831 | ||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

Net Interest Income / Revenue |

54 | % | 71 | % | 65 | % | 61 | % | 60 | % | 49 | % | 36 | % | ||||||||

Non-Interest Income / Revenue |

46 | % | 29 | % | 35 | % | 39 | % | 40 | % | 51 | % | 64 | % | ||||||||

Low cost and stable source of funds. Merchants Bank funds its loans, including its participation agreements and warehouse lines of credit, using funds generated primarily from mortgage related custodial deposits. Merchants Bank's cost of total deposits was 0.70% for the six months ended June 30, 2017 and its total cost of funds was 0.98% for the six months ended June 30, 2017. Custodial funds come from Merchants Bank's non-depository financial institution clients, such as servicing related escrow deposits for insurance and property taxes. These deposits are stable because the sources of the deposits have significant borrowing relationships with Merchants Bank that it expects will continue. Merchants Bank may elect not to participate or fund loans in the event these customers decide to remove the deposits, thus we can better manage our assets with our liabilities. Merchants Bank also uses brokered deposits as a source of funding to make up for any funding gap with warehouse volumes or timing of mortgage custodial remittances. These deposits are short term and typically have maturities of up to three months to match the temporarily higher volumes in warehouse volumes and custodial remittances. Further, in the event Merchants Bank's deposits were insufficient to meet its customers' borrowing needs, Merchants Bank has available liquidity through cash reserves and available borrowing capacity of $386.4 million through the FHLBI as of June 30, 2017.

Sophisticated risk management platform. Our largest source of interest income is Merchants Bank's warehouse financing business, which we have structured to minimize risk. Merchants Bank underwrites mortgage companies ("lenders") prior to entering into a warehouse lending agreement. Merchants Bank uses two different arrangements to fund agency eligible, government insured or guaranteed, or jumbo residential mortgage loans secured by mortgages placed on existing one-to-four family dwellings. The majority of our loans are funded under a participation agreement whereby Merchants Bank elects to purchase a participation interest of up to 100% in individual loans and shares proportionately in the interest income until the loan is sold in the secondary market. Merchants Bank also will fund loans under a warehouse line of credit as a secured financing. The warehouse arrangement is secured by a combination of the funded mortgage loans, cash deposits and personal guarantees of the originating lender, and Merchants Bank's initial disbursement of less than 100% of the loan amount. Merchants Bank's risk mitigation procedures include possession of collateral until the loan is sold and Merchants Bank directly receives the proceeds from the secondary market investor. In addition, prior to funding Merchants Bank reviews each loan to confirm its agency eligibility status and uses vendors to further validate loans as well as to hold the collateral securing the loan. Loans typically are sold by lenders to a third-party investor within approximately 20 days of funding, allowing Merchants Bank to minimize its risk that a loan will default prior to sale. The lenders sell most of these loans individually or through government sponsored entities ("GSEs") (i.e., Fannie Mae, Freddie Mac, and Ginnie Mae) mortgage backed securities programs to large financial institutions or to GSEs, as the end investors. This relatively short turnover time is also part of what keeps our balance sheet assets repricing to the current rate environment and helps us manage interest rate risk, as discussed below.

10

Minimizing interest rate exposure. We believe that we appropriately minimize the potential for risk in our investment and loan portfolios, including risks associated with an increase in interest rates given the structure and composition of these portfolios. Our securities portfolio consists primarily of callable, government-backed securities with maturities of two years or less, all of which are available for sale. Our loan portfolio is comprised predominantly of variable interest rates or short maturities, which allows the interest rates to change with the market. As of June 30, 2017, 78.7% of Merchants Bank's assets reprice in less than 90 days. In our multi-family financing business, the vast majority of loans are sold into the secondary market with P/RMIC retaining servicing rights. P/RMIC also avoids "locking in" interest rates significantly in advance of loan closings, which further minimizes interest rate risk prior to closing of the loans.

Innovative mortgage warehouse lending platform. We believe that Merchants Bank has an innovative warehouse lending platform that may be considered an industry leader. We have the capability to fully fund electronic mortgages through our E-Note program, one of only seven lenders in the country approved by Freddie Mac to offer this solution. We are highly responsive to our customers' needs by offering mortgage servicing rights ("MSRs") and operating lines of credit selectively to warehouse lending customers. The lines of credit secured by MSR's lead to the potential for additional deposits as the customer increases its servicing portfolio. In addition, customer service is especially important in the warehouse lending business because customers need to be able to rely, with confidence, on a readily accessible, stable source of funds given the timing realities of meeting and honoring mortgage loan closings or purchases. We believe that our mortgage banking expertise and experience, size and low overhead costs permit us to be responsive to customers on a level that many larger banks are unable to match. These factors contribute to Merchants Bank providing warehouse facilities to some of the leading non-depository institutions in the country.

Recent Acquisition

RICHMAC Funding, LLC. We entered into a Member Interests Purchase Agreement dated June 26, 2017, to acquire 100% of the equity interests of RICHMAC Funding, LLC, a Delaware limited liability company. We closed the acquisition on August 15, 2017, and issued 383,271 shares of our common stock in exchange for 100% of the equity interests of RICHMAC. The acquisition is expected to allow P/RMIC through RICHMAC to operate as a Fannie Mae Affordable Lender and a Freddie Mac Targeted Affordable Housing (TAH) Seller/Servicer. In addition, we acquired a Fannie Mae and Freddie Mac servicing portfolio as part of the transaction. The acquisition is expected to provide additional product offerings, such as the Freddie Mac Bridge to Resyndication and the Fannie Mae Tax Exempt Bond Credit Enhancement, to current customers as well as broaden the origination network into attractive markets where we do not currently have a presence. RICHMAC currently operates principally in Minneapolis, Minnesota and New York, New York.

Pending Acquisition

Joy State Bank. On October 31, 2016, we entered into an Agreement and Plan of Merger to acquire Joy State Bank, an Illinois chartered bank located in Joy, Illinois. Since the timing and approval of the transaction was uncertain due to our capital position at September 30, 2016, on December 22, 2016 the Agreement and Plan of Merger was amended and the parties agreed that Michael Petrie and Randall Rogers, two of our directors and executive officers, would acquire Joy State Bank. The acquisition of Joy State Bank by Messrs. Petrie and Rogers received appropriate regulatory approvals and closed on April 3, 2017. On May 8, 2017, we entered into a Stock Purchase Agreement with Messrs. Petrie and Rogers to acquire Joy State Bank. The acquisition is expected to provide access to the Mortgage Partnership Finance (MPF) Program, an attractive program offered through the Federal Home Loan Bank of Chicago which Merchants Bank, as an Indiana chartered state bank, cannot access. We have agreed to pay a purchase price of approximately $5.4 million plus $16,403 for

11

each 30 days after June 30, 2017, prorated to the closing date. The purchase price is equal to the price paid by Messrs. Petrie and Rogers, plus expenses and a cost of funds equal to 3.75%. The acquisition has been approved by the Federal Reserve Bank of Chicago, but remains subject to the approval of the Illinois Department of Financial and Professional Regulation, Division of Banking. We expect to close this acquisition in the first quarter of 2018.

2017 Third Quarter Update

We are currently in the process of preparing our consolidated financial results for the third quarter ended September 30, 2017 and, therefore, our actual results for that period are not yet available and are subject to change. However, based on our expectations, our 2017 third quarter net income will increase over our 2017 first quarter net income of $9.1 million but will be less than our 2017 second quarter net income of $14.8 million. Investors should look at our financial results on an annual basis and not necessarily on a quarterly basis. Our quarterly results tend to exhibit some level of variability, particularly related to non-interest income. Various factors impact our non-interest income resulting in net income being higher or lower from quarter-to-quarter. Our pro-forma return on average assets and pro-forma return on average tangible common equity have ranged from 1.24% to 2.89% and 19.86% to 34.96%, from 2012 through the latest twelve months ended June 30, 2017, respectively, see "Summary Historical Consolidated Data" and "Selected Historical Consolidated Data."

Risks Relating to Our Company

Our ability to implement our strategic plan and the success of our business are subject to numerous risks and uncertainties, which are discussed in the section titled "Risk Factors," beginning on page 17, and include, but are not limited to, the following:

- •

- decreased residential and multi-family mortgage origination, volume and pricing decisions of competitors, and changes in interest rates, may

adversely affect our profitability;

- •

- our mortgage banking profitability could significantly decline if we are not able to originate and resell a high volume of mortgage loans;

- •

- fluctuations in interest rates may reduce net interest income and otherwise negatively impact our financial condition and results of

operations;

- •

- because a significant portion of our loan portfolio is comprised of real estate loans, negative changes in the economy affecting real estate

values and liquidity could impair the value of collateral securing our real estate loans and result in loan and other losses; and

- •

- liquidity risks could affect operations and jeopardize our business, financial condition, and results of operations.

Corporate Information

Our principal executive offices are located at 11555 North Meridian Street, Suite 400, Carmel, Indiana 46032, and our telephone number at that address is (317) 569-7420. Our website address is www.merchantsbankofindiana.com. The information contained on our website is not a part of, or incorporated by reference into, this prospectus.

12

Common stock offered by us |

5,555,555 shares | |

Underwriters' option to purchase additional shares of our common stock |

833,333 shares |

|

Common stock outstanding after completion of this offering |

27,053,222 shares (or 27,886,555 shares if the underwriters exercise in full their option to purchase additional shares of our common stock). |

|

Use of proceeds |

Assuming an initial public offering price of $18.00 per share, which is the midpoint of the offering price range set forth on the cover page of this prospectus, the net proceeds to us from this offering, after deducting underwriting discounts and estimated offering expenses, will be approximately $92.2 million (or approximately $106.3 million if the underwriters exercise their option to purchase additional shares in full). We intend to contribute $86.4 million of the net proceeds that we receive from this offering to Merchants Bank to support balance sheet growth, and to use the remainder for general corporate purposes, which could include future acquisitions and other growth initiatives. We also intend to use approximately $5.8 million to complete the pending acquisition of Joy State Bank. See "Use of Proceeds" and "Business—Pending Acquisition—Joy State Bank." |

|

Dividends |

It has been our policy to pay quarterly dividends to holders of our common stock, and we intend to generally maintain our current dividend levels. Our dividend policy and practice may change in the future, however, and our board of directors may change or eliminate the payment of future dividends at its discretion, without notice to our shareholders. Any future determination to pay dividends to holders of our common stock will depend on our results of operations, financial condition, capital requirements, banking regulations, payment of dividends on our preferred stock, contractual restrictions and any other factors that our board of directors may deem relevant. See "Dividend Policy." |

|

Nasdaq listing |

We have applied to list our common stock on the Nasdaq Capital Market under the trading symbol "MBIN." |

|

Risk factors |

Investing in shares of our common stock involves a high degree of risk. See "Risk Factors" beginning on page 17 for a discussion of certain factors you should consider carefully before deciding to invest. |

13

Directed Share Program |

At our request, the underwriters have reserved for sale, at the initial public offering price, up to 277,777 shares of the common stock being offered by this prospectus, to our directors, officers, employees and other individuals that have a business relationship with us, including current shareholders and customers, and their family members who have expressed an interest in purchasing our common stock in this offering. See "Underwriting." |

Unless otherwise indicated, all information in this prospectus relating to the number of shares of common stock to be outstanding immediately after the completion of this offering is based on 21,497,667 shares outstanding as of October 12, 2017, as adjusted for the 2.5 for 1 stock split that was effective July 6, 2017, and:

- •

- excludes 17,910 shares of unvested restricted stock (as adjusted for the 2.5 for 1 stock split that was effective July 6, 2017); and

- •

- excludes 1,500,000 shares of common stock available for future awards under our 2017 Equity Incentive Plan.

Except as otherwise indicated, all information in this prospectus:

- •

- assumes an initial public offering of $18.00 per share, which is the midpoint of the price range set forth on the cover page of this

prospectus;

- •

- assumes no exercise by the underwriters of their option to purchase additional shares of our common stock; and

- •

- assumes that all shares reserved under the Directed Share Program are purchased.

14

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

The following table sets forth our summary historical consolidated financial data as of the dates and for the periods shown. The summary balance sheet data as of December 31, 2016 and 2015 and the summary income statement data for the years ended December 31, 2016 and 2015 have been derived from our audited consolidated financial statements included elsewhere in this prospectus. We have derived the summary historical consolidated financial data as of and for the years ended December 31, 2014, 2013 and 2012 from our audited financial statements not included in this prospectus. The summary consolidated financial data as of June 30, 2017 and for the six months ended June 30, 2017 and 2016 is derived from our unaudited interim consolidated financial statements included elsewhere in this prospectus and includes all normal and recurring adjustments that we consider necessary for a fair presentation. Operating results for the six months ended June 30, 2017 are not necessarily indicative of the results that may be expected for the year ending December 31, 2017.

You should read the following financial data in conjunction with the other information contained in this prospectus, including "Selected Historical Consolidated Financial Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and in the consolidated financial statements and related notes included elsewhere in this prospectus.

| |

At or for the Six Months Ended June 30, |

At or for the Year Ended December 31, | |

||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Dollars in thousands, except per share data) |

2017 | 2016 | 2016 | 2015 | 2014 | 2013 | 2012 | |

|||||||||||||||

| |

(unaudited) |

|

|

|

|

|

|

||||||||||||||||

Balance Sheet Data |

|||||||||||||||||||||||

Total Assets |

$ | 3,091,500 | $ | 2,506,974 | $ | 2,718,512 | $ | 2,269,442 | $ | 1,793,008 | $ | 1,179,791 | $ | 936,172 | |||||||||

Loans held for investment |

1,070,866 | 872,292 | 941,796 | 762,212 | 447,614 | 266,092 | 217,073 | ||||||||||||||||

Allowance for loan losses |

(6,865 | ) | (5,902 | ) | (6,250 | ) | (5,422 | ) | (4,458 | ) | (3,295 | ) | (2,854 | ) | |||||||||

Loans held for sale |

983,420 | 818,404 | 764,503 | 620,583 | 736,667 | 542,571 | 365,444 | ||||||||||||||||

Deposits |

2,771,501 | 2,247,621 | 2,428,621 | 2,039,520 | 1,610,719 | 1,054,304 | 815,418 | ||||||||||||||||

Total liabilities |

2,864,987 | 2,329,701 | 2,512,224 | 2,121,242 | 1,682,872 | 1,060,976 | 841,864 | ||||||||||||||||

Total shareholder's equity |

226,513 | 177,273 | 206,288 | 148,200 | 110,137 | 118,814 | 94,308 | ||||||||||||||||

Tangible common equity |

184,409 | 148,226 | 164,184 | 137,677 | 109,614 | 118,291 | 93,785 | ||||||||||||||||

Income Statement Data |

|

||||||||||||||||||||||

Interest Income |

$ | 41,471 | $ | 32,421 | $ | 72,939 | $ | 56,345 | $ | 39,554 | $ | 31,659 | $ | 25,764 | |||||||||

Interest Expense |

12,216 | 8,602 | 18,968 | 14,290 | 8,924 | 5,951 | 5,054 | ||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | |

Net interest income |

29,255 | 23,819 | 53,971 | 42,055 | 30,630 | 25,708 | 20,710 | ||||||||||||||||

Provision for loan losses |

480 | 480 | 960 | 960 | 1,215 | 720 | 1,270 | ||||||||||||||||

Noninterest income |

24,717 | 9,951 | 28,504 | 27,008 | 20,263 | 27,284 | 36,121 | ||||||||||||||||

Noninterest expense |

14,902 | 12,163 | 26,720 | 20,922 | 15,796 | 13,328 | 12,504 | ||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | |

Income before taxes |

38,590 | 21,127 | 54,795 | 47,181 | 33,882 | 38,944 | 43,057 | ||||||||||||||||

Provision for income taxes |

14,702 | 8,353 | 21,668 | 18,798 | 30,079 | — | — | ||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | |

Net income, as previously reported |

23,888 | 12,774 | 33,127 | 28,383 | 3,803 | 38,944 | 43,057 | ||||||||||||||||

Non-GAAP Reconciliation: |

|||||||||||||||||||||||

Pro-forma adjustments: |

|||||||||||||||||||||||

Add back of tax effect of S Corp to C Corp conversion |

— | — | — | — | 16,431 | (1) | — | — | |||||||||||||||

Less provision for income taxes |

— | — | — | — | — | 15,578 | (2) | 17,223 | (2) | ||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | |

Pro-forma net income |

23,888 | 12,774 | 33,127 | 28,383 | 20,234 | 23,366 | 25,834 | ||||||||||||||||

Preferred stock dividends |

1,665 | 407 | 2,002 | — | — | — | — | ||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | |

Pro-forma net income available to common shareholders |

$ | 22,223 | $ | 12,367 | $ | 31,125 | $ | 28,383 | $ | 20,234 | $ | 23,366 | $ | 25,834 | |||||||||

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Credit Quality Data |

|

||||||||||||||||||||||

Nonperforming loans |

$ | 3,219 | $ | 2,195 | $ | 1,887 | $ | 887 | $ | 815 | $ | 490 | $ | 1,451 | |||||||||

15

| |

At or for the Six Months Ended June 30, |

At or for the Year Ended December 31, | |

||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Dollars in thousands, except per share data) |

2017 | 2016 | 2016 | 2015 | 2014 | 2013 | 2012 | |

|||||||||||||||

| |

(unaudited) |

|

|

|

|

|

|

||||||||||||||||

Nonperforming loans to total loans |

0.30 | % | 0.25 | % | 0.20 | % | 0.12 | % | 0.18 | % | 0.18 | % | 0.67 | % | |||||||||

Nonperforming assets |

$ | 3,219 | $ | 2,195 | $ | 1,887 | $ | 887 | $ | 815 | $ | 490 | $ | 1,451 | |||||||||

Nonperforming assets to total assets |

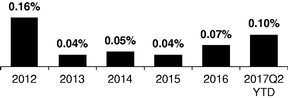

0.10 | % | 0.09 | % | 0.07 | % | 0.04 | % | 0.05 | % | 0.04 | % | 0.16 | % | |||||||||

Allowance for loan losses to total loans |

0.64 | % | 0.68 | % | 0.66 | % | 0.71 | % | 1.00 | % | 1.24 | % | 1.31 | % | |||||||||

Allowance for loan losses to nonperforming loans |

213.26 | % | 268.88 | % | 331.21 | % | 611.27 | % | 546.99 | % | 672.45 | % | 196.69 | % | |||||||||

Net charge-offs/(recoveries) to average loans |

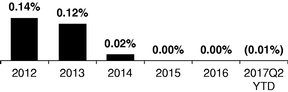

(0.01 | )% | — | — | — | 0.02 | % | 0.12 | % | 0.14 | % | ||||||||||||

Per Share Data (Common Stock) |

|

||||||||||||||||||||||

Basic and diluted earnings per share |

|||||||||||||||||||||||

As reported |

$ | 1.05 | $ | 0.59 | $ | 1.47 | $ | 1.35 | $ | 0.19 | $ | 1.95 | $ | 2.15 | |||||||||

Pro-forma |

$ | 1.05 | $ | 0.59 | $ | 1.47 | $ | 1.35 | $ | 1.01 | (3) | $ | 1.17 | (3) | $ | 1.29 | (3) | ||||||

Dividends declared |

$ | 0.10 | $ | 0.10 | $ | 0.20 | $ | 0.20 | $ | 0.95 | $ | 0.72 | $ | 0.44 | |||||||||

Book value |

|||||||||||||||||||||||

As reported |

$ | 8.76 | $ | 7.05 | $ | 7.80 | $ | 6.55 | $ | 5.32 | $ | 5.94 | $ | 4.72 | |||||||||

Pro-forma |

$ | 8.76 | $ | 7.05 | $ | 7.80 | $ | 6.55 | $ | 6.11 | (4) | $ | 5.16 | (5) | $ | 3.85 | (5) | ||||||

Tangible book value |

|||||||||||||||||||||||

As reported |

$ | 8.73 | $ | 7.02 | $ | 7.78 | $ | 6.52 | $ | 5.29 | $ | 5.92 | $ | 4.69 | |||||||||

Pro-forma |

$ | 8.73 | $ | 7.02 | $ | 7.78 | $ | 6.52 | $ | 6.09 | (4) | $ | 5.14 | (5) | $ | 3.83 | (5) | ||||||

Weighted average shares outstanding |

|||||||||||||||||||||||

Basic |

21,114,400 | 21,111,200 | 21,111,208 | 21,075,475 | 20,017,400 | 20,000,000 | 20,000,000 | ||||||||||||||||

Diluted |

21,119,411 | 21,112,283 | 21,113,435 | 21,075,475 | 20,017,400 | 20,000,000 | 20,000,000 | ||||||||||||||||

Shares outstanding at period end |

21,114,400 | 21,111,200 | 21,111,200 | 21,111,200 | 20,703,700 | 20,000,000 | 20,000,000 | ||||||||||||||||

Performance Metrics |

|

||||||||||||||||||||||

Return on average assets |

|||||||||||||||||||||||

As reported |

1.74 | % | 1.05 | % | 1.24 | % | 1.32 | % | 0.25 | % | 3.18 | % | 4.81 | % | |||||||||

Pro-forma |

1.74 | % | 1.05 | % | 1.24 | % | 1.32 | % | 1.34% | (4) | 1.91% | (5) | 2.89% | (5) | |||||||||

Return on average equity |

|||||||||||||||||||||||

As reported |

22.00 | % | 16.52 | % | 18.68 | % | 22.62 | % | 3.71 | % | 37.07 | % | 57.86 | % | |||||||||

Pro-forma |

22.00 | % | 16.52 | % | 18.68 | % | 22.62 | % | 19.76% | (4) | 22.24% | (5) | 34.71% | (5) | |||||||||

Return on average tangible common equity |

|||||||||||||||||||||||

As reported |

25.40 | % | 17.18 | % | 20.50 | % | 22.73 | % | 3.73 | % | 37.25 | % | 58.27 | % | |||||||||

Pro-forma |

25.40 | % | 17.18 | % | 20.50 | % | 22.73 | % | 19.86% | (4) | 22.35% | (5) | 34.96% | (5) | |||||||||

Net interest margin |

2.23 | % | 2.03 | % | 2.07 | % | 2.02 | % | 2.12 | % | 2.19 | % | 2.41 | % | |||||||||

Efficiency ratio |

27.61 | % | 36.02 | % | 32.40 | % | 30.29 | % | 31.04 | % | 25.15 | % | 22.00 | % | |||||||||

Loans and loans held for sale to deposits |

74.12 | % | 75.22 | % | 70.26 | % | 67.80 | % | 73.52 | % | 76.70 | % | 71.44 | % | |||||||||

Capital Ratios—Merchants Bancorp |

|

||||||||||||||||||||||

Tangible common equity to tangible assets |

6.0 | % | 5.9 | % | 6.0 | % | 6.1 | % | 6.1 | % | 10.0 | 10.0 | |||||||||||

Common equity Tier 1 capital to risk-weighted assets |

7.4 | % | 7.4 | % | 8.1 | % | 8.5 | % | N/A | N/A | N/A | ||||||||||||

Tier 1 leverage ratio |

7.4 | % | 6.5 | % | 6.6 | % | 6.1 | % | 6.1 | % | 8.4 | % | 8.0 | % | |||||||||

Tier 1 capital to risk weighted assets |

9.3 | % | 8.9 | % | 10.3 | % | 9.2 | % | 7.7 | % | 11.9 | % | 18.0 | % | |||||||||

Total capital to risk-weighted assets |

9.6 | % | 9.2 | % | 10.6 | % | 9.6 | % | 8.1 | % | 12.2 | % | 18.0 | % | |||||||||

Regulatory Capital Ratios—Merchants Bank Only |

|

||||||||||||||||||||||

Tier 1 common capital to risk-weighted assets |

11.7 | % | 12.0 | % | 13.2 | % | 12.9 | % | N/A | — | — | ||||||||||||

Tier 1 leverage ratio |

9.3 | % | 8.7 | % | 8.4 | % | 8.5 | % | 8.7 | % | 8.4 | % | 8.0 | % | |||||||||

Tier 1 capital to risk-weighted assets |

11.7 | % | 12.0 | % | 13.2 | % | 12.9 | % | 11.0 | % | 11.9 | % | 18.0 | % | |||||||||

Total capital to risk-weighted assets |

12.0 | % | 12.4 | % | 13.5 | % | 13.3 | % | 11.3 | % | 12.2 | % | 18.0 | % | |||||||||

- (1)

- Represents

the recognition of deferred tax liabilities recorded upon conversion from a Subchapter S corporation to a regular C corporation.

- (2)

- Represents

the pro-forma effects of income taxes using a 40% income tax rate, as we were a Subchapter S corporation in years prior to 2014.

- (3)

- Represents

basic and diluted earnings per share calculated on pro-forma net income.

- (4)

- Represents

pro-forma performance metrics calculated on net income as adjusted for the effects of the deferred tax liabilities recorded in connection with the

conversion from Subchapter S to C corporation.

- (5)

- Represents pro-forma performance metrics calculated on net income as adjusted for the effects of income taxes included calculated using a 40% income tax rate for years previously reported as a Subchapter S corporation.

16

Investing in our common stock involves a high degree of risk. Before you decide to invest, you should carefully consider the risks described below, together with all other information included in this prospectus. Any of the following risks, as well as risks that we do not know or currently deem immaterial, could have a material adverse effect on our business, financial condition, results of operations and growth prospects. As a result, the trading price of our common stock could decline and you could experience a partial or complete loss of your investment. Further, to the extent that any of the information in this prospectus constitutes forward-looking statements, the risk factors below also are cautionary statements identifying important factors that could cause actual results to differ materially from those expressed in any forward-looking statements made by us or on our behalf. See "Cautionary Note Regarding Forward-Looking Statements" beginning on page 38.

Risks Related to Our Business

Decreased residential and multi-family mortgage origination, volume and pricing decisions of competitors, and changes in interest rates, may adversely affect our profitability.

We currently operate a residential and multi-family mortgage origination, warehouse financing, and servicing business. Changes in interest rates and pricing decisions by our loan competitors may adversely affect demand for our mortgage loan products, the revenue realized on the sale of loans, revenues received from servicing such loans and the valuation of our mortgage servicing rights.

Our mortgage banking profitability could significantly decline if we are not able to originate and resell a high volume of mortgage loans.

Mortgage production, especially refinancing activity, declines in rising interest rate environments. Interest rates have been historically low over the last few years and this environment likely will not continue indefinitely. Moreover, when interest rates increase further, there can be no assurance that our mortgage production will continue at current levels. Because we sell a substantial portion of the mortgage loans we originate and purchase, the profitability of our mortgage banking business also depends in large part on our ability to aggregate a high volume of loans and sell them at a gain in the secondary market. Thus, in addition to our dependence on the interest rate environment, we are dependent upon (i) the existence of an active secondary market and (ii) our ability to profitably sell loans or securities into that market. If our level of mortgage production declines, the profitability will depend upon our ability to reduce our costs commensurate with the reduction of revenue from our mortgage operations.

In addition, our ability to sell mortgage loans readily is dependent upon our ability to remain eligible for the programs offered by GSEs and other institutional and non-institutional investors. Any significant impairment of our eligibility with any of the GSEs could materially and adversely affect our operations. Further, the criteria for loans to be accepted under such programs may be changed from time to time by the sponsoring entity, which could result in a lower volume of corresponding loan originations. The profitability of participating in specific programs may vary depending on a number of factors, including our administrative costs of originating and purchasing qualifying loans and our costs of meeting such criteria.

The ability for us and our warehouse financing customers to originate and sell residential mortgage loans readily is dependent upon the availability of an active secondary market for single-family mortgage loans, which in turn depends in part upon the continuation of programs currently offered by GSEs and other institutional and non-institutional investors. These entities account for a substantial portion of the secondary market in residential mortgage loans. Because the largest participants in the secondary market are Fannie Mae and Freddie Mac, GSEs whose activities are governed by federal law, any future changes in laws that significantly affect the activity of these GSEs could, in turn,

17

adversely affect our operations. In September 2008, Fannie Mae and Freddie Mac were placed into conservatorship by the U.S. government. The federal government has for many years considered proposals to reform Fannie Mae and Freddie Mac, but the results of any such reform, and their impact on us, are difficult to predict. To date, no reform proposal has been enacted.

Fluctuations in interest rates may reduce net interest income and otherwise negatively impact our financial condition and results of operations.

Net interest income is the difference between the amounts received by us on our interest-earning assets and the interest paid by us on our interest-bearing liabilities. When interest rates rise, the rate of interest we pay on our liabilities, such as deposits, rises more quickly than the rate of interest that we receive on our interest-bearing assets, such as loans, which may cause our profits to decrease. The impact on earnings is more adverse when short-term interest rates increase more than long-term interest rates or when long-term interest rates decrease more than short-term interest rates, leading to similar yields between short-term and long-term rates. Many factors impact interest rates, including governmental monetary policies, inflation, recession, changes in unemployment, the money supply and international economic weaknesses and disorder and instability in domestic and foreign financial markets.

Interest rate increases often result in larger payment requirements for our borrowers, which increases the potential for default. At the same time, the marketability of the underlying property may be adversely affected by any reduced demand resulting from higher interest rates. In a declining interest rate environment, there may be an increase in prepayments on loans as borrowers refinance their mortgages and other indebtedness at lower rates.

Our mortgage servicing rights assets typically have a ten year call protection, but as interest rates decrease, the potential for prepayment increases and the fair market value of our mortgage servicing rights assets may decrease. Our ability to mitigate this decrease in value is largely dependent on our ability to be the refinancier and retain servicing rights. While we have previously been successful in our servicing retention, we may not be able to achieve the same level of retention in the future.

Changes in interest rates also can affect the value of loans, securities and other assets. An increase in interest rates that adversely affects the ability of borrowers to pay the principal or interest on loans may lead to an increase in nonperforming assets and a reduction of income recognized, which could have a material adverse effect on our results of operations and cash flows. Further, when we place a loan on nonaccrual status, we reverse any accrued but unpaid interest receivable, which decreases interest income. Subsequently, we continue to have a cost to fund the loan, which is reflected as interest expense, without any interest income to offset the associated funding expense. Thus, an increase in the amount of nonperforming assets would have an adverse impact on net interest income.

Rising interest rates will result in a decline in value of the fixed-rate debt securities we hold in our investment securities portfolio. The unrealized losses resulting from holding these securities would be recognized in other comprehensive income (loss) and reduce total shareholders' equity. Unrealized losses do not negatively impact our regulatory capital ratios; however, tangible common equity and the associated ratios would be reduced. If debt securities in an unrealized loss position are sold, such losses become realized and will reduce our regulatory capital ratios.

If short-term interest rates remain at their historically low levels for a prolonged period, and assuming longer term interest rates fall further, we could experience net interest margin compression as our interest earning assets would continue to reprice downward while our interest-bearing liability rates could fail to decline in tandem. This would have a material adverse effect on our net interest income and our results of operations.

18

Because a significant portion of our loan portfolio is comprised of real estate loans, negative changes in the economy affecting real estate values and liquidity could impair the value of collateral securing our real estate loans and result in loan and other losses.

At June 30, 2017, approximately 81.4% of our loan portfolio was comprised of loans with real estate as a primary or secondary component of collateral. As a result, adverse developments affecting real estate values in our market areas could increase the credit risk associated with our real estate loan portfolio. The market value of real estate can fluctuate significantly in a short period of time as a result of market conditions in the area in which the real estate is located. Adverse changes affecting real estate values and the liquidity of real estate in one or more of our markets could increase the credit risk associated with our loan portfolio, significantly impair the value of property pledged as collateral on loans and affect our ability to sell the collateral upon foreclosure without a loss or additional losses, which could result in losses that would adversely affect profitability. Such declines and losses would have a material adverse impact on our business, results of operations and growth prospects. In addition, if hazardous or toxic substances are found on properties pledged as collateral, the value of the real estate could be impaired. If we foreclose on and take title to such properties, we may be liable for remediation costs, as well as for personal injury and property damage. Environmental laws may require us to incur substantial expenses to address unknown liabilities and may materially reduce the affected property's value or limit our ability to use or sell the affected property.

Liquidity risks could affect operations and jeopardize our business, financial condition, and results of operations.

Liquidity is essential to our business. An inability to raise funds through deposits, borrowings, the sale of loans and/or investment securities and from other sources could have a substantial negative effect on our liquidity. A source of our funds consists of our customer deposits, including escrow deposits held in connection with our multi-family mortgage servicing business. These deposits are subject to potentially dramatic fluctuations in availability or price due to certain factors that may be outside of our control, such as a loss of confidence by customers in us or the banking sector generally, customer perceptions of our financial health and general reputation, increasing competitive pressures from other financial services firms for consumer or corporate customer deposits, changes in interest rates and returns on other investment classes. If customers move money out of bank deposits and into other investments, we could lose a relatively low cost source of funds, which would require us to seek wholesale funding alternatives in order to continue to grow, thereby increasing our funding costs and reducing our net interest income and net income.

As of June 30, 2017, $819.7 million, or 29.6% of our total deposits, were concentrated in three large mortgage non-depository financial institutions. These concentration levels expose us to the risk that one of these depositors will experience financial difficulties, withdraw its deposits, or otherwise lose the ability to generate custodial funds due to business or regulatory realities. However, two of these institutions also have warehouse funding arrangements, providing us the opportunity to mitigate this risk by electing not to participate or fund an institution's loans in the event such institution removes its deposits. Nonetheless, failure to effectively manage this risk and subsequent reduction in the deposits of our significant customers could have a material impact on our ability to fund lending commitments or increase cost of funds, thereby decreasing our revenues.

Additional liquidity is provided by brokered deposits and our ability to borrow from the FHLBI. As of June 30, 2017 brokered deposits were $687.3 million, or 24.8% of our total deposits. Brokered deposits may be more rate sensitive than other sources of funding. In the future, those depositors may not replace their brokered deposits with us as they mature, or we may have to pay a higher rate of interest to keep those deposits or to replace them with other deposits or other sources of funds. Not being able to maintain or replace those deposits as they mature would adversely affect our liquidity. Additionally, if the Bank does not maintain its well-capitalized position, it may not accept or renew any

19

brokered deposits without a waiver granted by the FDIC. We also may borrow from third-party lenders from time to time. Our access to funding sources in amounts adequate to finance or capitalize our activities or on terms that are acceptable to us could be impaired by factors that affect us directly or the financial services industry or economy in general, such as disruptions in the financial markets or negative views and expectations about the prospects for the financial services industry.

Additionally, as a bank holding company we are dependent on dividends from our subsidiaries as our primary source of income. Our subsidiaries are subject to certain legal and regulatory limitations on their ability to pay us dividends. Any reduction or limitation on our subsidiaries abilities to pay us dividends could have a material adverse effect on our liquidity and in particular, affect our ability to repay our borrowings.

Any decline in available funding, including a decrease in brokered deposits, could adversely impact our ability to continue to implement our strategic plan, including our ability to originate loans, fund warehouse financing commitments, meet our expenses, declare and pay dividends to our shareholders or to fulfill obligations such as repaying our borrowings or meeting deposit withdrawal demands, any of which could have a material adverse impact on our liquidity, business, financial condition and results of operations.