Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Hamilton Beach Brands Holding Co | d464680d8k.htm |

Investor Presentation September 2017 Exhibit 99 |

Safe Harbor Statement The following information includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933,

as amended, and Section 21E of the Securities Exchange Act

of 1934, as amended. Any and all statements regarding the Company’s expected future financial position, results of operations, cash flows, business strategy, budgets, projected costs, capital expenditures, products, competitive positions, growth

opportunities, plans, goals and objectives of management

for future operations, as well as statements that include words such as “anticipate,” “if,” “believe,” “plan,” “estimate,” “expect,” “intend,” “may,” “could,” “should,” “will,” and other

similar expressions are forward-looking statements. Such forward-looking statements are inherently uncertain, and readers must recognize that actual results may differ materially from the expectations of the

Company’s management. The Company does not undertake

a duty to update such forward-looking statements. Factors that may cause actual results to differ materially from those in the forward-looking statements include, without limitation, changes in the sales prices, product mix or levels of consumer

purchases of small electric household and specialty

housewares appliances; changes in consumer retail and credit markets, including the increasing volume of transactions made through third-party internet sellers; bankruptcy of or loss of major retail customers or suppliers; changes in costs,

including transportation costs, of sourced products;

delays in delivery of sourced products; changes in or unavailability of quality or cost effective suppliers; exchange rate fluctuations, changes in the import tariffs and monetary and other changes in the regulatory climate in the countries in which Hamilton Beach

Brands buys, operates and/or sells products; product

liability, regulatory actions or other litigation, warranty claims or returns of products; customer acceptance of, changes in costs of, or delays in the development of new products; increased competition, including consolidation within the industry; shift

in consumer shopping patterns, gasoline prices, weather

conditions, the level of consumer confidence and disposable income as a result of economic conditions, unemployment rates or other events or conditions that may adversely affect the level of customer purchases of our products; changes mandated by

federal, state and other regulation, including tax,

health, safety or environmental legislation; decreased levels of consumer visits to brick and mortar stores; increased competition, including through online channels; shift in consumer shopping patterns, gasoline prices, weather conditions, the

level of consumer confidence and disposable income as a

result of economic conditions, unemployment rates or other events or conditions that may adversely affect the number of customers visiting Kitchen Collection ® stores; changes in the sales prices, product mix or levels of consumer purchases of kitchenware and

small electric appliances; changes in costs, including transportation

costs, of inventory; delays in delivery or the unavailability of inventory; customer acceptance of new products; the anticipated impact of the opening of new stores, the ability to renegotiate existing leases and

effectively and efficiently close under-performing

stores; changes in import tariffs and monetary policies and other changes in the regulatory climate in the countries in which Kitchen Collection operates and/or buys and sells products; and other risks identified in the Company’s Registration

Statement on Form S-1 and other filings with the

Securities and Exchange Commission. 1

|

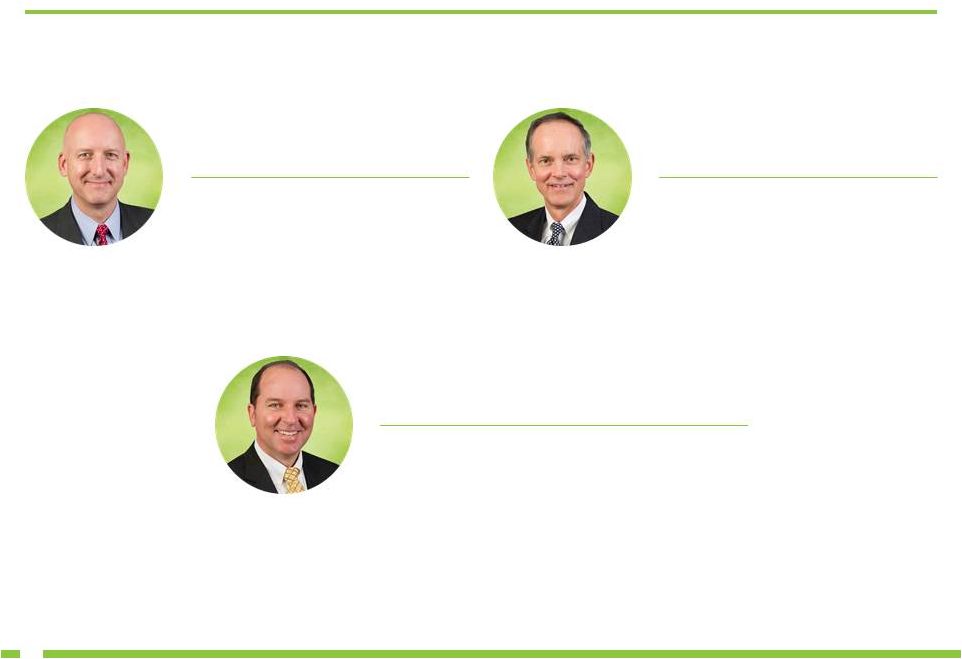

Management Presenters Supported by an executive team with an average of 29 years of experience with Hamilton Beach Brands

GREG

TREPP

President & CEO

21 years with Hamilton Beach Brands

Previously employed with Pepperidge Farm

Inc. and Young & Rubicam

JIM

TAYLOR

Vice President & CFO

34 years with Hamilton Beach Brands

Previously employed with Price Waterhouse

SCOTT

TIDEY

Sr. Vice President, North America Sales & Marketing

24 years with Hamilton Beach Brands

Previously employed with Wyeth Consumer Healthcare

2 |

HBBHC Snapshot Hamilton Beach Brands Holding Company (NYSE: HBB) Hamilton Beach Brands Holding Company (“HBBHC”) is a holding company for two

separate businesses: consumer and commercial small appliances

(“Hamilton Beach Brands” or “HBB”)

and specialty retail (“The Kitchen Collection” or “KC”) Hamilton Beach Brands is a leading global designer, marketer and distributor of

branded small electric household and specialty housewares appliances,

as well as commercial products for restaurants, bars and

hotels The Kitchen Collection is a national specialty

retailer of kitchenware in outlet and traditional malls

throughout the U.S. Headquartered in Glen Allen,

Virginia Approximately 1,400 employees

LTM 6/30/17 revenue – $740.6 million LTM 6/30/17 EBITDA – $50.4 million (1) LTM 6/30/17 net income – $27.2 million 6/30/17 net debt – $48.9 million _____________________ (1) EBITDA is a non-GAAP measure and should not be considered in isolation or as a substitute for GAAP measures. The discussion of

non-GAAP measures and the related reconciliations to

GAAP measures start on page 31. 3

|

Transaction Background and Rationale |

Spin-Off Transaction Summary NACCO Industries, Inc. (“NACCO”) is planning to effect a stock spin-off of Hamilton Beach Brands

Holding Company

Distributing

Company………………........................................................................................NACCO Industries, Inc. (NYSE: NC) Distributed Company…………….............................................................Hamilton Beach

Brands Holding Company (NYSE: HBB) Distributed

Securities………….......………………..……………………………100% of HBBHC Class A and Class B common stock

Distribution

Ratio……………………..…One Class A and one Class B share of HBBHC for every Class A or Class B share of NC HBBHC Total Shares

Outstanding…………...................................................................................................................13.7 million Dividend Policy………………………..................................................................HBBHC

intends

to pay regular quarterly dividends 4 |

Focused Housewares Investment Provides investors with a more focused, single-industry investment option

Improve Flexibility to Pursue Growth

Create greater flexibility to pursue strategic growth opportunities,

such as acquisitions and joint ventures, in the

housewares industry and the potential to use stock to help finance

these growth opportunities Direct Access to Capital

Markets Provide direct access to equity capital markets

and greater access to debt capital markets to fund growth strategies and to establish a capital structure and dividend policy reflecting the business needs and financial position

Recruit, Motivate and Retain Employees

Strengthen the alignment of senior management incentives with the needs

and performance of HBBHC through the use of equity

compensation arrangements, improving the ability to motivate and retain current personnel and attract, retain and motivate additional qualified personnel Management Focus Reinforce management’s focus on serving each market segment and customer need, and on responding flexibly to

changing market conditions and growth markets

Spin-Off Rationale

The spin-off is expected to accomplish important business objectives

for HBBHC 5 |

HBBHC Overview and Strategic Objectives |

Proven Business Model Drives Results Consistent, Market Leading Innovation + + Global Platform #1 Presence in Key Sales Channels + + Trusted, Efficient

and Low-Cost Supply Chain Strong Performance and Return on Capital Iconic Brands + Experienced Management Team + 6 |

The

Innovation Started Over

110 Years Ago! 7 |

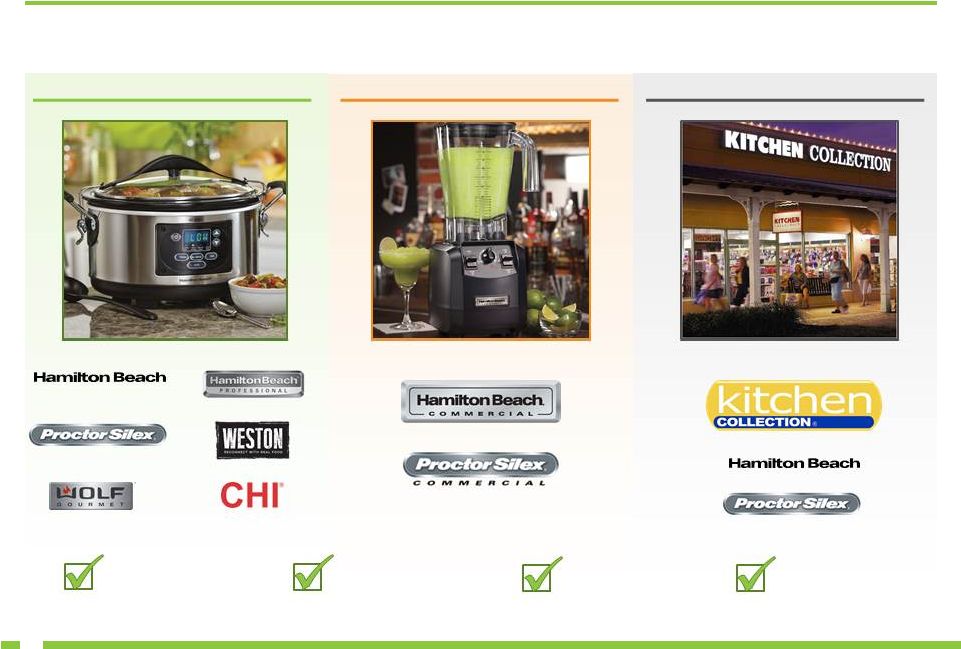

HBBHC is a Collection of Iconic Consumer Product Brands _____________________ (1) Wolf Gourmet ® is a registered trademark of the Sub-Zero Group, Inc. (2) CHI ® is a registered trademark of Farouk Systems, Inc. (1) (2) 8 Trusted Proven Reliable Innovative CONSUMER COMMERCIAL RETAIL |

HBBHC Overview KEY BUSINESS HIGHLIGHTS SALES BY GEOGRAPHY Leading designer, marketer and distributor of branded housewares for retail and

commercial applications

Strong brands with leading market share

Hamilton Beach

®

brand ranked #1 small kitchen appliance brand in U.S.

(based on units)

Strong share in Canada, Mexico and Central America and focused on

growing in other international markets

Strong relationships with leading retail and e-commerce customers

across diverse channels

100+ year track record of innovation and product line

expansion Broad consumer price point segmentation coverage

from good to better to best Multi-layered growth

strategy includes e-commerce leadership, an increase in

premium product offerings, continued international expansion, further

penetration of commercial markets, expansion into adjacent

categories and completion of accretive

acquisitions Highly professional and experienced management

team Strong working capital management and returns on

capital SALES BY

CATEGORY

OPERATING

PROFIT BY CATEGORY 2016 FINANCIAL HIGHLIGHTS 9 United States 84% International 16% Consumer / Commercial 99% Retail 1% Consumer 75% Commercial 6% Retail 19% |

Our Vision To be the leading global supplier of branded small appliances and housewares

Our Mission

Profitable

growth from innovative solutions that improve everyday living Our Values The Customer: Consistently meet or exceed the needs of our internal and external

customers People:

Employ and develop the best Good Thinking: Encourage and cultivate inspired thinking in all areas of our

business Ethics:

Honest,

ethical

behavior

–

always

Quality: Ensuring the quality of our

products and services is our passion Continuous

Improvement: There is always a better way. Change is life Teamwork: We help each other to succeed. We share both successes and failures

Our Environment:

We proactively manage our business in a sustainable, socially

and environmentally responsible manner

Our Core Principles

10 |

11 “Good Thinking” Approach At Hamilton Beach Brands, We Practice “Good Thinking” Excellent Work Environment Consumer Focus Innovation Testing, Testing, Testing Best-in-Class Logistics Trusted, Ethical Work Smart Quality |

Comprehensive Product Portfolio Coffee Makers Kettles Toasters Irons Slow Cookers Hand Mixers Can Openers Blenders Toaster Ovens Meat Grinders Food Processors 12 |

Strong Portfolio of Branded Products TOTAL PRODUCT CATEGORIES OFFERED HBB HAS A TOP 3 BRAND IN 28 KEY HOUSEWARE CATEGORIES 47 40 33 30 28 23 18 16 Cuisinart Oster Black & Decker Breville Kitchen Aid Sunbeam _____________________ Source: NPD point of sales data for the 12-month period ending July, 2017.

Air purifiers

Electric knives

Ice shavers Rice cookers Blenders Espresso makers Iced tea makers Roaster ovens Bread makers Food choppers Irons Sandwich makers Burners, single and double Food processors Jar openers Single serve blenders Can openers Food steamers Juice extractors Skillets Citrus juicers Garment steamers Kettles Slow cookers Coffee grinders Griddles Kitchen systems Soda machines Coffee makers, traditional drip Grills, indoor Meat grinders / mincers Stand mixers Coffee makers, single serve Grills / griddles Microwave ovens Toaster ovens Compact refrigerators Hand blenders Odor eliminators Toasters Crepe makers Hand mixers Pizza ovens Vacuum sealers Deep fryers Hand / stand mixers Popcorn poppers Waffle makers Specialty drink makers Ice cream makers Quesadilla makers _____________________ Source: NPD for the 12-month period ending August, 2017.

13 |

Consistent Innovation in New Product Development 53 37 49 51 70 58 59 58 50 67 80 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E HBB aggregates data from 25,000+ consumers annually to introduce new, research-driven products

HBB generated more than 30% of its revenue in the last

3 years from products that are less than 3 years old

_____________________

(1) Excludes product introductions from The Kitchen Collection and gadget introductions from Weston. PRODUCT PLATFORM INTRODUCTIONS (1) SELECT 2017 PRODUCT INTRODUCTIONS Weston Pro ® Series Dehydrator Hamilton Beach ® MultiBlend Quiet Blender Proctor Silex ® Panini Press & Compact Grill Hamilton Beach ® Commercial Quantum Blender HBB protects its innovations through a robust patent renewal process 14 |

SPECIALTY RETAILERS DEPARTMENT STORES WAREHOUSE CLUBS MASS MARKET RETAILERS E-COMMERCE RETAILERS Broad Customer Base Across Diverse Channels E-Commerce 28% Other 72% 2017E U.S. SALES BY CHANNEL HBB Believes it Has the #1 Unit Share of Small Kitchen Appliances at the Top 2 U.S. E-Commerce Retailers HBB Has a Diverse Base of 2,500+ Customers GROCERY STORES INDEPENDENT RETAILERS 1,000+ Customer Accounts 2016 SALES BY CUSTOMER SPORT RETAILERS 15 Costco Sam’s Club PRICESMART Bodega Aurrera Family Dollar Grupo Exito Walmart TARGET JET JD.COM Wayfair TMALL.COM Amazon KOHL’S Liverpool BED BATH & BEYOND El Palacio de Hierro BEST BUY Macy’s Bemol Harrods FAST SHOP Sur la table WILLIAMS-SONOMA Academy SPORT + OUTDOORS Kroger Wakefern FOOD CORP H.E.B Cabela’s DICK’S Customer 1 Customer 2 Customer 3 Customer 4 Customer 5 Customer 6 Customer 7 Customer 8 Customer 9 Customer 10 Other 32% 10% 5% 4% 3% 2% 2% 2% 2% 1% Other 37% |

Global Infrastructure to Support HBB Objectives Picton, Ontario Distribution Center Strategically located footprint to efficiently serve customers globally

Markham, Ontario

Canada Sales and

Administration

Headquarters

Bentonville,

Arkansas Sales Office Richmond, Virginia Corporate Headquarters Sales & Marketing Engineering Southern Pines, North Carolina Service Center for Customer Returns; Catalog Distribution Center; Parts Distribution Center Mexico City, Mexico Mexico Sales and Administrative Headquarters Tultitlan, Mexico Distribution Center Jundiai, Sao Paulo, Brazil Distribution Center Sao Paulo, Brazil Brazil Sales and Administrative Headquarters Geel, Belgium Distribution Center Shanghai, China Sales Office, Engineering, Quality Assurance Shanghai, China Distribution Center Shenzhen, China Engineering, Quality Assurance, Operations Distribution Sales Corporate HQ Sales and Administrative HQ Miami, Florida Sales Office Olive Branch, Mississippi Distribution Office Seattle, Washington Sales Office Minneapolis, Minnesota Sales Office 16 |

Market Backdrop Summary CONSUMER KITCHEN APPLIANCE MARKET BY GEOGRAPHY (1) ~$71 B ~$39 B ~$23 B ~$30 B CHANNEL OVERVIEW 2017E U.S. HOUSEWARES SALES BY CHANNEL _____________________ (1) Marketline. (2) NPD. 17 (2) Asia-Pacific 43% Europe 24% United States 14% ROW 19% E-Commerce 25% Other 75% INDUSTRY GEOGRAPHIC FOOTPRINT |

Tangible Growth Opportunities to Generate Attractive Returns E-Commerce leadership Premium Product Offerings Adjacent Categories Strategic Acquisitions International Market Penetration Commercial Product Line Expansion Long-Term HBB Objectives (excludes KC): Sales: Operating Profit Margin: $750M – $1B 9% – 10% 18 |

9% 14% 14% 17% 21% 28% 2012 2013 2014 2015 2016 2017E RECENT ONLINE REVIEWS Success in Growing E-Commerce Channel GLOBAL E-COMMERCE FOOTPRINT Online sales of housewares is the fastest growing segment and is

expected to account for 25% of U.S. industry sales in 2017

Consumers are more discriminating of products due to their ability to

research products online

Consumers are increasingly focused on reviews which take into

account brand reputation, product performance and

safety These habits play into HBB’s favor given the

positive information available on HBB’s products

online E-commerce rewards brands, innovation and

product quality above and beyond traditional

brick-and-mortar retail and HBB is leveraging its

strengths in these areas to execute its online growth

strategy Continue to drive sales and capture market share

with the top global online retailers

Deliver best-in-class communication and promotional strategies

to drive conversion

Excel in direct fulfillment business model

Expand brands into new categories to drive incremental

sales Consistently identify / evaluate new online

participants to ensure maximum channel

presence HBB

U.S. E-COMMERCE SALES (2012 – 2017E) _____________________ Source: Intelligent Eye, which compiled reviews from amazon.com, walmart.com and target.com during 2016.

HBB’s U.S. E-Commerce Sales are Expected to

Exceed the U.S. Industry Average of 25% in 2017

19 Brand 2016 Average Star Total Reviews 4.1 189,137 4.1 21,536 Cuisinart 4.0 35,725 Oster 4.0 87,787 Mr. Coffee 3.9 28,244 Magic Bullet 3.9 4,106 Black & Decker 3.8 59,870 Rowenta 3.8 6,212 Delonghi 3.8 9,760 Bella 3.7 9,322 |

Multi-Initiative Marketing Strategy HBB delivers 3 billion+ impressions annually through its marketing strategy

Advertising

Online E-mail Everyday

Good Thinking Blog

Facebook

Pinterest

Twitter

Instagram

YouTube

500,000+ followers

1,500+ subscribers

17,000+ followers

8,000+ followers

20 |

Premium Product Market Opportunity Well-positioned to grow in the premium market Leverage brand strength, engineering, design capabilities and commercial expertise to expand premium product offering

Expansion of Hamilton Beach

®

Professional and Weston

®

brand product lines

Robust

roadmap

of new product introductions from Wolf Gourmet ® through multi-year agreement with Sub-Zero Group, Inc. Wolf is a premium brand with a reputation of innovation and quality designed to create the ultimate cooking

experience Introduction

of CHI ® –branded garment care line, through multi-year licensing deal with Farouk Systems, Inc. CHI is a high-quality hair products brand with products that reflect education, the environment and innovation

Expand placements and share in the “Only-the-Best”

high-end market with strong brands and product lines

21 ® |

Expand internationally in the emerging Asia and Latin America markets and continue to expand in Canada and Mexico Target to increase international sales by concentrating on key growth markets, including China and Brazil o Flexible entry model includes establishing a local team and then working through distributors or directly with retailers or e-commerce partners o Also an opportunity to grow with existing customers as they expand into new markets Invest in resources to identify local consumer needs / preferences through consumer research / feedback and introduce new products for specific markets Leverage strength of brands and innovative products to expand in new geographies Commercial division has been present in global markets for decades providing a strong platform to build upon Selective licensing of HBB brands with high-quality partners

in eight countries

International Market Opportunity

_____________________

(1) Source: Marketline.

CONSUMER

KITCHEN

APPLIANCE

MARKET BY

GEOGRAPHY

(1) Significant expansion opportunity for international growth 2016 HBBHC GEOGRAPHIC SALES MIX $70.5 B $39.0 B $23.0 B $30.4 B 22 United States 84% International 16% Asia-Pacific 43% Europe 24% United States 14% ROW 19% |

Commercial Market Opportunity Opportunity to accelerate growth in the $18 billion global commercial market (1) Food service markets benefitting from changing demographics and shift to healthier food options

Increase in onsite food preparation driving demand for commercial

appliances Company’s commercial brand reputation for

performance, reliability and differentiated products driving growth Investing to understand customers’ unmet needs for unique solutions to build a competitive advantage

Opportunity to accelerate growth through the introduction of new

product capabilities and categories Continuing to build

distribution capabilities and investing resources to establish presence in international food service market Increasing penetration of products at global and regional chains Commercial grade, innovative features, strong performance and heavy-duty durability Dependable value, commercially rated, strong performance and durability _____________________ (1) Company estimate. 23 |

Expand into New Small Appliance and Adjacent Categories Pursuing opportunities to grow outside of the small kitchen appliance category

Significant opportunity to expand outside the small kitchen appliances

category Leverage existing infrastructure and channels to

introduce adjacent products E-commerce channel enhances

ability to successfully add new products Introducing new

products in both consumer and commercial markets Compact

Refrigerators

Coffee Airpots

Kitchen Scales

Commercial

Chamber Sealers

Buffet Servers

24 |

Acquisition Growth Strategy Large, global housewares market that is highly fragmented Competitive market position that gives HBB potential to increase share / enter new product categories Opportunity in current consumer space, new consumer categories or commercial Strong brand and / or channel presence International presence / focus with differentiated customer base E-commerce expands acquisition opportunities, as the platform

makes it easier to present new products

Accelerate growth and margins

Highly-accretive when layered into current business

model Meet or exceed return on capital targets

“We are thrilled to welcome the Weston team and their

consumers and vendors to the Hamilton Beach Brands

family. Through the combination of the highly talented

Weston organization along with our own dedicated

employees, we believe we can achieve significant

opportunities for future growth and profitability in line with our

strategic initiatives”

Product expansion opportunity within existing product categories and beyond

HBB’s small kitchen and commercial appliance

business ATTRACTIVE MARKETS

TARGET PROFILE

VALUE CREATION

HBBHC will be a more attractive acquirer as its own entity

Value Drivers for HBB

Incremental access to new consumer

markets such as outdoor enthusiast

and farm-to-table and also retail

channels such as sporting goods

Expands distribution capabilities for

existing HBB brands

25 - Greg Trepp December 2014 |

The Kitchen Collection Strategy 209 stores as of June 30, 2017 strategically located primarily in outlet malls across the U.S.

Meet the challenge of a difficult environment and evolve aggressively in

a constructive manner, focusing on the outlet mall

segment Outlet malls have a sustainable presence and

Kitchen Collection is the leading housewares player in

outlet malls Optimize store portfolio with stores in

strong outlet malls in well-positioned locations and

exit stores that do not generate acceptable returns

Average lease duration expected to be 12 months or less for

two-thirds of stores by the end of 2018

Substantial progress has already been made and in a manner that has

minimized financial impact on the business

Focus on comparable store sales growth through:

Enhancing customers’ store experience through improved customer

interactions to generate greater average sales

transaction size Working to enhance sales volume and

profitability by improving closure rates through

continued refinement of product offerings, merchandise mix and store displays and appearances Continued focus on gross margin, profit and cash flow improvement areas

Emphasis on increasing sales of higher-margin products

Maintain inventory efficiency and store inventory controls

Ongoing merchandising improvements through use of highly analytical

merchandising skills and disciplined operating

controls 26 |

Consolidated Financial Overview |

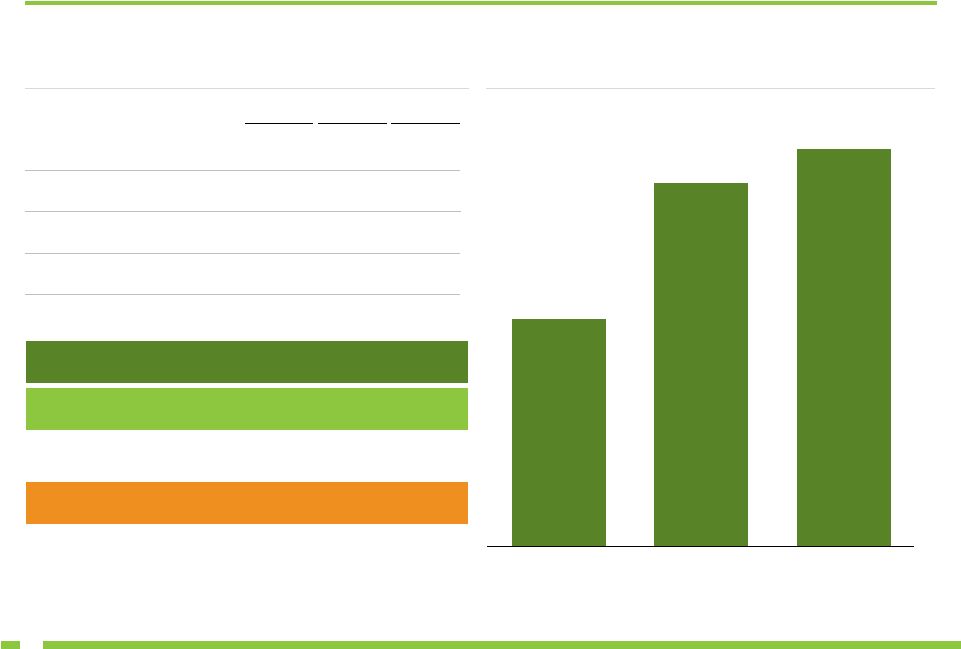

REVENUE Historical Financial Highlights ($ in millions) $621.0 $605.2 $604.1 2015 2016 LTM June 2017 EBITDA (1) $38.0 $46.9 $49.0 2015 2016 LTM June 2017 $151.0 $144.4 $139.9 2015 2016 LTM June 2017 $1.6 $1.9 $1.3 2015 2016 LTM June 2017 _____________________ (1) Excludes potential incremental standalone costs. EBITDA is a non-GAAP measure and should not be considered in isolation or as a

substitute for GAAP measures. The discussion of non-GAAP measures and the related reconciliations to GAAP measures start on page 31. (2) HBBHC financials net of eliminations. ($ in millions) $767.9 $745.4 $740.6 2015 2016 LTM June 2017 $40.3 $48.8 $50.4 2015 2016 LTM June 2017 % of Revenue:

6.1%

7.7% 8.1% % of Revenue:

1.1%

1.3% 0.9% % of Revenue:

5.2%

6.5% 6.8% (2) 27 |

2015 2016 June 2017 Net Income $19.7 $26.2 $27.2 EBITDA 40.3 48.8 50.4 Cash and Cash Equivalents 16.8 11.3 5.3 Consolidated Debt 58.4 38.7 54.3 Net Debt 41.6 27.4 49.0 Consolidated Debt / EBITDA 1.4x 0.8x 1.1x Net Debt / EBITDA 1.0x 0.6x 1.0x Consolidated Equity $82.8 $65.1 $63.0 Debt to Total Capitalization 41.4% 37.3% 46.3% Capital Structure and Return on Capital FLEXIBLE CAPITAL STRUCTURE (HBBHC) 19.1% 30.5% 33.4% 2015 2016 LTM June 2017 ATTRACTIVE ROTCE (HBB) _____________________ (1) Net Income and EBITDA represent last twelve months as of June 2017.

(2) Leverage doesn’t reflect impact from planned dividend. (3) EBITDA, Debt to Total Capitalization and ROTCE are non-GAAP measures and should not be considered in isolation or as a

substitute for GAAP measures. The discussion of non-GAAP measures and the related reconciliations to GAAP measures start on page 31. Prior to the spin, HBBHC intends to distribute a $35 million dividend to NACCO,

an acceleration of a previously planned dividend expected to be paid in

Q4 2017 (1)

(3) (2) (2) (3) 28 (3) |

Company Outlook KC OUTLOOK HBB OUTLOOK U.S. and Canadian consumer markets for small appliances during H2 2017

expected to be comparable to H2 2016, as sales continue to shift from

in- store channels to online

HBB will continue to focus on strengthening its market position with new

products across various categories and brands; H2 2017

sales and net income are expected to be higher than levels

seen in H2 2016 Longer term, HBB will continue to focus on

improving return on sales through scale derived from

market growth and strategic initiatives along with

leveraging KC’s infrastructure for future operations

Declining consumer traffic to physical retail locations and reduced

in-store transactions are reducing KC’s target

consumers’ spending on housewares in mall

locations Given the market backdrop, KC expects financial

performance to decline during H2 2017 compared to H2

2016 Going forward, KC will aggressively manage its store

portfolio with a focus on a defined profitable product

line at more favorable mall locations; the Company

believes its small core store portfolio is well positioned to take advantage of a market turnaround 29 HBBHC expects to incur up to $2.5 million of spin-related costs in Q3 2017 |

Key Investment Highlights 30 Strong Core Business Model Leading Global Market Share in Branded Housewares Strong Cash Flows and ROTCE Global Sourcing and Distribution Platform Broad Customer Base Comprehensive Product Offering Experienced Management Team Iconic Brands Known Globally Leading Provider to the Growing E-Commerce Market Multi-Layered Growth Strategy Increase in Premium Product Offerings Continued International Expansion Further Penetration of Commercial Markets Expansion into Adjacent Markets Complete Accretive Acquisitions Business Growth will Drive Further Economies of Scale E-Commerce Leadership |

Appendix |

Non-GAAP Disclosure EBITDA is defined as net income before income taxes plus interest expense, interest income and depreciation and amortization expense; Debt to Total Capitalization is defined as consolidated debt divided by consolidated debt plus consolidated equity; Net debt is defined as total debt less cash and cash equivalents; and Return on capital employed is defined as net income before interest expense, after tax divided by LTM average capital employed. LTM average capital employed is defined as LTM average equity plus LTM average debt less LTM average cash. 31 This presentation contains non-GAAP financial measures. Included in this presentation are reconciliations of these

non-GAAP financial measures to the most directly

comparable financial measures calculated in accordance with U.S. generally accepted accounting principles ("GAAP"). EBITDA is a measure of net income (loss) that differs from financial results measured in

accordance with GAAP.

EBITDA, debt to total capitalization, net debt and return on capital

employed in this presentation are provided

solely

as supplemental non-GAAP disclosures of operating results. Management believes these non-GAAP financial measures assist investors in understanding the results of operations of Hamilton Beach Brands Holding Company and its

subsidiaries. In addition, management evaluates

results using these non-GAAP financial measures.

Hamilton

Beach

Brands

Holding

Company

defines

non-GAAP

measures

as follows: For reconciliations from GAAP measurements to non-GAAP measurements see pages 32 and 33. |

Non-GAAP EBITDA Reconciliation ($ in millions) Note: EBITDA is provided solely as a supplemental disclosure. EBITDA does not represent net income, as defined by U.S. GAAP and

should not be considered as a substitute for net income,

or as an indicator of operating performance. The Company defines EBITDA as income (loss) before income tax provision, plus net interest expense and depreciation and amortization expense. EBITDA is not a measurement under U.S. GAAP and is not necessarily comparable with

similarly titled measures of other companies.

32 Calculation of EBITDA Net income $19.7 $26.2 $27.2 Income tax provision 12.3 15.0 15.6 Interest expense 2.0 1.4 1.5 Interest income 0.0 0.0 (0.0) Depreciation and amortization expense 6.3 6.2 6.1 EBITDA $40.3 $48.8 $50.4 Calculation of EBITDA Net loss ($0.4) ($0.3) ($0.6) Income tax provision 0.4 0.5 0.3 Interest expense 0.1 0.2 0.2 Interest income 0.0 0.0 0.0 Depreciation and amortization expense 1.5 1.5 1.4 EBITDA $1.6 $1.9 $1.3 Year Ended December 31, 2015 2016 LTM June 2017 Calculation of EBITDA Net income $19.7 $26.6 $27.8 Income tax provision 11.8 14.5 15.3 Interest expense 1.8 1.1 1.2 Interest income (0.1) 0.0 (0.0) Depreciation and amortization expense 4.8 4.7 4.7 EBITDA $38.0 $46.9 $49.0 |

Capitalization and ROTCE Reconciliation ($ in millions) CAPITALIZATION (HBBHC) ROTCE (HBB) (1) _____________________ (1) Return on capital employed is provided solely as a supplemental disclosure with respect to income generation because management

believes it provides useful information with respect to earnings in a form that is comparable to the Company’s cost of capital employed, which includes both equity and debt securities, net of cash. Return on

capital employed is a non-GAAP measure and should not be considered in isolation or as a substitute for a GAAP measure. (2) Tax rate of 38% represents the Company’s target marginal tax rate.

(2) (2) (2) 33 2015 2016 June 2017 Consolidated Debt $58.4 $38.7 $54.3 Plus: Consolidated Equity 82.8 65.1 63.0 Total Capitalization $141.2 $103.8 $117.3 Debt to Total Capitalization 41.4% 37.3% 46.3% 2015 Average Equity (12/31/2014 and each of 2015's quarter ends) $51.5 Average Debt (12/31/2014 and each of 2015's quarter ends) 58.9 Average Cash (12/31/2014 and each of 2015's quarter ends) (1.4) Total 2015 average capital employed $109.0 2015 Net Income, as reported 19.7 Plus: 2015 Interest expense, net 1.8 Less: Income taxes on 2015 interest expense at 38% (0.7) Actual return on capital employed = actual net income before interest expense, net, after tax

20.8 Actual return on capital employed percentage 19.1% 2016 Average Equity (12/31/2015 and each of 2016's quarter ends) $52.0 Average Debt (12/31/2015 and each of 2016's quarter ends) 40.2 Average Cash (12/31/2015 and each of 2016's quarter ends) (2.6) Total 2016 average capital employed $89.5 2016 Net Income, as reported 26.6 Plus: 2016 Interest expense, net 1.2 Less: Income taxes on 2016 interest expense at 38% (0.5) Actual return on capital employed = actual net income before interest expense, net, after tax

27.3 Actual return on capital employed percentage 30.5% Trailing 12 Months, June 2017 Average Equity (6/30/17, 3/31/17, 12/31/16, 9/30/16, 6/30/16) $50.4 Average Debt (6/30/17, 3/31/17, 12/31/16, 9/30/16, 6/30/16) 39.1 Average Cash (6/30/17, 3/31/17, 12/31/16, 9/30/16, 6/30/16) (4.2) Total Trailing 12 months average capital employed $85.3 Trailing 12 Months Net Income, as reported 27.8 Plus: Trailing 12 months Interest expense, net 1.2 Less: Income taxes on Trailing 12 months interest expense at 38%

(0.5)

Actual return on capital employed = actual net income before interest

expense, net, after tax 28.5

Actual return on capital employed percentage

33.4% |