Attached files

| file | filename |

|---|---|

| EX-10.30 - EXHIBIT 10.30 - Research Solutions, Inc. | v474820_ex10-30.htm |

| EX-32.2 - EXHIBIT 32.2 - Research Solutions, Inc. | v474820_ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Research Solutions, Inc. | v474820_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Research Solutions, Inc. | v474820_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - Research Solutions, Inc. | v474820_ex31-1.htm |

| EX-23 - EXHIBIT 23 - Research Solutions, Inc. | v474820_ex23.htm |

| EX-10.34 - EXHIBIT 10.34 - Research Solutions, Inc. | v474820_ex10-34.htm |

| EX-10.33 - EXHIBIT 10.33 - Research Solutions, Inc. | v474820_ex10-33.htm |

| EX-10.32 - EXHIBIT 10.32 - Research Solutions, Inc. | v474820_ex10-32.htm |

| EX-10.31 - EXHIBIT 10.31 - Research Solutions, Inc. | v474820_ex10-31.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: June 30, 2017

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _____________ to _____________

Commission File No. 000-53501

RESEARCH SOLUTIONS, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 11-3797644 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 15821 Ventura Blvd., Suite 165, Encino, California | 91436 |

| (Address of principal executive offices) | (Zip Code) |

(310) 477-0354

(Registrant’s telephone number, including area code)

5435 Balboa Blvd., Suite 202, Encino, California, 91316

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: common stock, par value $0.001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company þ |

| Emerging growth company ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of December 31, 2016, the last business day of the registrant’s most recently completed second fiscal quarter, was $14,204,866 based on the closing price of $1.03 per share as reported on the OTCQB as of that date.

Indicate the number of shares outstanding of each of the issuer’s classes of common stock as of the latest practicable date.

| Title of Class | Number of Shares Outstanding on September 11, 2017 | |

| Common Stock, $0.001 par value | 24,169,792 |

TABLE OF CONTENTS

| 2 |

Cautionary Notice Regarding Forward-Looking Statements

Unless otherwise indicated, (i) the terms “Research Solutions,” “we,” “us” and “our” refer to Research Solutions, Inc., a Nevada corporation, and our two wholly-owned subsidiaries Reprints Desk, Inc., a Delaware corporation (“Reprints Desk”) and Reprints Desk Latin America S. de R.L. de C.V, an entity organized under the laws of Mexico (“Reprints Desk Latin America”), and (ii) the term “common stock” refers to the common stock, par value $0.001 per share, of Research Solutions. The financial information included herein is presented in United States dollars (“US Dollars”), the functional currency of our company. Although the majority of our revenue and costs are in US Dollars, the costs of Reprints Desk Latin America are in Mexican Pesos.

All statements included or incorporated by reference in this Annual Report on Form 10-K, other than statements or characterizations of historical fact, are forward-looking statements. Examples of forward-looking statements include, but are not limited to, statements concerning our accounting estimates; assumptions and judgments; the demand for our products; the competitive nature of and anticipated growth in our industry; and our prospective needs for additional capital. These forward-looking statements are based on our current expectations, estimates, approximations and projections about our industry and business, management’s beliefs, and certain assumptions made by us, all of which are subject to change. Forward-looking statements can often be identified by words such as “anticipates,” “expects,” “intends,” “plans,” “predicts,” “believes,” “seeks,” “estimates,” “may,” “will,” “should,” “would,” “could,” “potential,” “continue,” “ongoing,” and similar expressions, and variations or negatives of these words. These statements are not guarantees of future performance and are subject to risks, uncertainties and assumptions that are difficult to predict. Therefore, our actual results could differ materially and adversely from those expressed in any forward-looking statements as a result of various factors, some of which are listed under “Risk Factors” in Item 1A of this report. These forward-looking statements speak only as of the date of this report. We undertake no obligation to revise or update publicly any forward-looking statement for any reason, except as otherwise required by law.

This Annual Report on Form 10-K also contains estimates and other information concerning our industry, including market size and customer satisfaction ratings, that we obtained from industry publications, surveys and forecasts. This information involves a number of assumptions and limitations, and you are cautioned not to give undue weight to these estimates. Although we believe the information in these industry publications, surveys and forecasts is reliable, we have not independently verified the accuracy or completeness of the information. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors.

Company Overview

Research Solutions was incorporated in the State of Nevada on November 2, 2006, and is a publicly traded holding company with two wholly owned subsidiaries at June 30, 2016: Reprints Desk, Inc., a Delaware corporation and Reprints Desk Latin America S. de R.L. de C.V, an entity organized under the laws of Mexico.

On June 30, 2017, we sold the intangible assets of our Reprints and ePrints business line, but specifically excluding billed accounts receivable and respective liabilities, pursuant to an Asset Purchase Agreement dated June 20, 2017. The aggregate net consideration for the sale is comprised of $450,000 paid on the closing date, and earn-out payments of 45% of gross margin over the 30 month period subsequent to the closing date. We have made a policy election to record the contingent consideration when the consideration is determined to be realizable (each 6-month period ending subsequent to the closing date).

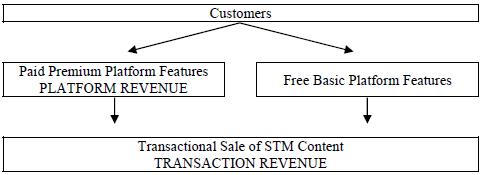

We provide two service offerings to our customers: annual licenses that allow customers to access and utilize certain premium features of our cloud based software-as-a-service (“SaaS”) research intelligence platform (“Platforms”) and the transactional sale of published scientific, technical, and medical (“STM”) content managed, sourced and delivered through the Platform (“Transactions”). Platforms and Transactions are packaged as a single solution that enable life science and other research intensive organizations to speed up research and development activities with faster, single sourced access and management of content and data used throughout the intellectual property development lifecycle.

Platforms

Our cloud-based SaaS research intelligence platform consists of proprietary software and Internet-based interfaces. Legacy functionality allows customers to initiate orders, route orders for the lowest cost acquisition, manage transactions, obtain spend and usage reporting, automate authentication, and connect seamlessly to in-house and third-party software systems. Customers can also enhance the information resources they already own or license and collaborate around bibliographic information.

Additional functionality has recently been added to our Platform in the form of interactive app-like gadgets. An alternative to manual data filtering, identification and extraction, gadgets are designed to gather, augment, and extract data across a variety of formats, including bibliographic citations, tables of contents, RSS feeds, PDF files, XML feeds, and web content. We are rapidly developing new gadgets in order to build an ecosystem of gadgets. Together, these gadgets will provide researchers with an “all in one” toolkit, delivering efficiencies in core research workflows and knowledge creation processes.

| 3 |

Our Platform is deployed as a single, multi-tenant system across our entire customer base. Customers securely access the Platform through online web interfaces and via web service APIs that enable customers to leverage Platform features and functionality from within in-house and third-party software systems. The Platform can also be configured to satisfy a customer’s individual preferences. We leverage our Platform’s efficiencies in scalability, stability and development costs to fuel rapid innovation and competitive advantage.

Transactions

Researchers and knowledge workers in life science and other research-intensive organizations generally require single copies of published STM journal articles for use in their research activities. These individuals are our primary users. Our Platform provides our customers with a single source to the universe of published STM content that includes over 70 million existing STM articles and over one million newly published STM articles each year.

Our Platform allows customers to find and download digital versions of STM articles that are critical to their research. Customers submit orders for the articles they need which we source and electronically deliver to them generally in under an hour. This service is generally known in the industry as single article delivery or document delivery. We also obtain the necessary permission licenses from the content publisher or other rights holder so that our customer’s use complies with applicable copyright laws. We have arrangements with hundreds of content publishers that allow us to distribute their content. The majority of these publishers provide us with electronic access to their content, which allows us to electronically deliver single articles to our customers often in a matter of minutes.

Competitive Strengths

We believe that we possess the following competitive strengths:

Services and Technology

We have developed proprietary software, a sophisticated information logistics technology backbone, and Internet-based interfaces that allow customers to initiate orders for STM content, manage these transactions, obtain reporting, automate authentication, improve seamless connectivity to in-house and third-party software systems, and maximize the information resources they already own or license, as well as organize workgroups to collaborate around bibliographic information. Our services alleviate the need for our customers to develop internal systems or contact multiple content publishers in order to obtain the content that is critical to their research.

Our services are highly configurable to meet customers’ needs and provide a personalized yet turnkey solution that covers the full spectrum of customer requirements; from identifying and locating articles, to facilitating copyright compliance, maximizing information resources already owned, monitoring usage, and automating end-user authentication. We continually enhance the performance of our existing proprietary software and systems and develop and implement new technologies that expand the available methods of discovering, obtaining and managing content.

Experienced Management Team

Our management team has well over 100 years of experience satisfying customers across the information services and STM publishing and technology industries. We are led by CEO Peter Derycz, an innovator in the space for more many decades and earning many accolades along the way, including being nominated to the Pharma Voice 100 list of most inspiring people in the Pharmaceutical industry.

Customer Loyalty

The majority of our revenue comes from our loyal base of customers, indicative of our focus on customer satisfaction and quality. Since our inception we have ranked first overall and in every category for every Document Delivery Buyer Survey conducted by industry research and advisory firm Outsell, Inc.: customer satisfaction (depth and breadth of coverage, fair pricing, and ease of doing business) and loyalty (intention to renew or continue service, and willingness to recommend the service to others).

Industry Presence and Established Relationships

We have a well-established presence and a network of contacts with our customers (life science companies, academic institutions, and other research intensive organizations), STM publishing partners, and others in the information services space. We have existing arrangements with hundreds of content publishers that allow us to distribute their content.

Promotion

We employ a segment-focused marketing approach that focuses on traditional buyers such as corporate libraries as well as new types of non-library buyers across a variety of business functions, including those within research and development. In pursuit of growth, we invest in vertical integration and channel relationships to increase the value we provide to customers, extend our promotional reach, and decrease customer acquisition costs. We anticipate growth coming from cross-selling into our existing customer base, penetrating new market verticals, and generating market demand and preference from both existing and new customers. While we place emphasis on the life science market, with a focus on pharmaceutical, biotechnology and medical device customers, we are also penetrating the following markets: academic, aerospace, automotive, electronics, chemicals and food and agriculture.

| 4 |

Growth Strategy

Organic Growth

We seek to grow our customer base through targeted direct and channel promotions of our Platform to potential customers. This strategy for sales and marketing is supported by inbound marketing driven by educational content, innovative technological systems, competitive pricing and high quality service. We are also positioning our sales force to be able to better serve small and medium sized businesses that we consider to be largely underserved today.

In addition, we submit proposals to potential customers in response to requests for proposals, or “Request for Proposals” (RFPs). We are continually improving our operations and technology to ensure that they are capable of delivering proposed solutions and supporting future growth.

Acquisitions and Combinations

From time to time, and as opportunities arise, we may explore strategic acquisitions and combinations, including the acquisition of customer lists, that bring revenue, profitability, growth potential and additional technology, products, services, operations and/or geographic capabilities to our company.

International Expansion

We have expanded internationally through increased sales to companies located abroad, particularly in Europe and Japan. From time to time, and as opportunities arise, we may further expand internationally through partnerships or acquisitions.

Publisher Agreements

We have arrangements with all of the major STM content publishers and most of the smaller STM publishers that allow us to distribute their content, and we regularly advance new business opportunities such as rentals through amendments to existing agreements. In addition, we regularly contact publishers to negotiate additional publisher agreements. A typical publisher agreement would allow us to distribute the publisher’s content according to a negotiated price list, thereby eliminating the need to contact the publisher and obtain the rights for each individual order. The majority of these publishers provide us with electronic access to their content, which allows us to further expedite the delivery of single articles to our customers. In addition, we rely on a small number of content publishers for the majority of our content costs.

Company Services

We generate revenue by providing two service offerings to our customers: annual licenses that allow customers to access and utilize certain premium features of our cloud based SaaS research intelligence platform (“Platforms”) and the transaction sale of STM content managed, sourced and delivered through the Platform (“Transactions”).

Platforms

We charge a subscription fee that allows customers to access and utilize certain premium features of our Platform. Revenue is recognized ratably over the term of the subscription agreement, which is typically one year, provided all other revenue recognition criteria have been met. Billings or payments received in advance of revenue recognition are recorded as deferred revenue.

| 5 |

Transactions

We charge a transactional service fee for the electronic delivery of single articles, and a corresponding copyright fee for the permitted use of the content. We recognize revenue from single article delivery services upon delivery to the customer only when the selling price is fixed or determinable, and collectability is reasonably assured.

Customers and Suppliers

There were no customers that accounted for greater than 10% of our revenue for the years ended June 30, 2017 and 2016.

Approximately 27% and 26% of our content cost for the years ended June 30, 2017 and 2016, respectively, was derived from our two largest suppliers of content. Loss of any or all of these suppliers of content would significantly reduce our revenue, which would have a material adverse effect on our results of operations. We can provide no assurance that these suppliers of content will continue to supply us with content in the future.

Sales and Marketing

To acquire customers, we rely on sales promotion to sell to large enterprise accounts, and marketing communications to more efficiently recruit small-to-medium and geographically-dispersed enterprises. The promotional mix of tactics we utilize includes: educational content, advertising, events, direct response and integrated marketing campaigns, public relations and content publicity, search engine optimization and marketing, thought leadership programs, channel alliances training, and analyst relations. In addition, a portion of our marketing budget is dedicated to research and customer retention, which, we believe, increases total lifetime customer value and generates significant amounts of referrals for new business

Competition

The markets in which we compete are highly competitive. The primary methods of competition in our industry are price, service, technology and niche focus. Competition based on price is often successful in the short-term, but can limit the ability of a supplier to provide adequate service levels. Competition based on service and/or technology requires significant investment in systems and that investment requires time to produce results. Niche operators focus on narrow activities, but cannot aggregate sufficient content, technology and services to satisfy broad customer needs. We believe that many customers and potential customers are less price sensitive if the service levels are high and the technology creates efficiency and/or management information that has not been available previously.

Our competition includes:

| · | Gadget –Like Toolkit Providers – We consider the rapidly increasing number of companies that are focused on specialized toolkits for researchers as competition. These include: Accelrys, Benchling, ChemAxon, Comsol Multiphysics, Genomenom, Main GCl, Workbench, Molsoft, and SnapGene. | |

| · | Reference Management Applications – We expect to increasingly compete with tools that exist in the marketplace that are used to aid in organizing references, storing personal content assets, and prepare scholarly papers for submission to congresses and journals. | |

| · | Piracy - Perhaps, our most serious competitor. Many entities use content for commercial purposes without complying with applicable copyright laws, and paying the required copyright to the content publisher. As information becomes more readily available, the opportunity for piracy increases. | |

| · | STM Single Article Delivery Vendors and Content Aggregators - Our primary competitors for global, full-service single article delivery services are Copyright Clearance Center, regional interlibrary loan networks throughout the world such as those owned and operated by OCLC, and numerous national libraries located outside of the United States. | |

| · |

Customer In-House Services - While single article delivery services are challenging for our customers to provide in-house, many existing and potential customers manage these services internally. | |

| · | Publisher In-House Capabilities - Some large publishers have developed in-house capabilities to service the content re-use market, however, many of them neglect other content repurposing opportunities and may not be able to aggregate content from other publishers. |

Corporate History and Structure

Research Solutions was incorporated in the State of Nevada on November 2, 2006, and in November 2006 entered into a Share Exchange Agreement with Reprints Desk. At the closing of the transaction contemplated by the Share Exchange Agreement, Research Solutions acquired all of the outstanding shares of Reprints Desk from its stockholders and issued 8,000,003 shares of common stock to the former stockholders of Reprints Desk. Following completion of the exchange transaction, Reprints Desk became a wholly-owned subsidiary of Research Solutions.

| 6 |

On July 24, 2012, we formed Reprints Desk Latin America to provide operational and administrative support services to Reprints Desk.

On March 4, 2013, we consummated a merger with DYSC Subsidiary Corporation, our wholly-owned subsidiary, pursuant to which we, in connection with such merger, amended our Articles of Incorporation to change our name to Research Solutions, Inc. (formerly Derycz Scientific, Inc.).

On June 30, 2017, we sold the intangible assets of our Reprints and ePrints business line, but specifically excluding billed accounts receivable and respective liabilities, pursuant to an Asset Purchase Agreement dated June 20, 2017. The aggregate net consideration for the sale is comprised of $450,000 paid on the closing date, and earn-out payments of 45% of gross margin over the 30 month period subsequent to the closing date. We have made a policy election to record the contingent consideration when the consideration is determined to be realizable (each 6-month period ending subsequent to the closing date).

Employees

As of September 11, 2017, we had 129 full time employees.

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all of the other information in this prospectus, including our consolidated financial statements and related notes, before investing in our common stock. The following summarizes material risks that investors should carefully consider before deciding to buy or maintain an investment in our common stock. Any of the following risks, if they actually occur, would likely harm our business, financial condition and results of operations. As a result, the trading price of our common stock could decline, and investors could lose the money they paid to buy our common stock.

Risks Related to Our Business and Our Industry

We have incurred significant losses, and may be unable to maintain profitability. If we continue to incur losses, we may have to curtail our operations, which may prevent us from successfully operating and expanding our business.

Historically, we have relied upon cash from financing activities to fund substantially all of the cash requirements of our activities and have incurred significant losses and experienced negative cash flow. For our fiscal years ended June 30, 2017 and 2016, we incurred a net loss of $2,293,563 and $497,858, respectively. As of June 30, 2017, we had an accumulated deficit of $17,875,858. We cannot predict if we will be profitable. We may continue to incur losses for an indeterminate period of time and may be unable to sustain profitability. An extended period of losses and negative cash flow may prevent us from successfully operating and expanding our business. We may be unable to sustain or increase our profitability on a quarterly or annual basis.

The loss of our largest customers would significantly reduce our revenue and adversely affect our results of operations.

There were no customers that accounted for greater than 10% of our revenue for the years ended June 30, 2017 and 2016. The loss of our largest customers would significantly reduce our revenue, which would have a material adverse effect on our results of operations. We can provide no assurance that these customers will continue to place orders in the future.

The loss of our largest suppliers of content would significantly reduce our revenue and adversely affect our results of operations.

Approximately 27% and 26% of our content cost for the years ended June 30, 2017 and 2016, respectively, was derived from our two largest suppliers of content. Loss of any or all of these suppliers of content would significantly reduce the attractiveness of our services and our revenue, which would have a material adverse effect on our results of operations. We can provide no assurance that these suppliers of content will continue to supply us with content in the future. Moreover, our arrangements with content providers are non-exclusive. As a result, our content providers can provide the same content to our competitors.

We are exposed to credit risk on our accounts receivable and prepayments to suppliers of content. This risk is heightened during periods when economic conditions worsen.

There were no customers that accounted for greater than 10% of our accounts receivable as of June 30, 2017 and 2016. In addition, we have made prepayments to suppliers of content. While we have procedures to monitor and limit exposure to credit risk on our trade receivables as well as long-term prepayments, there can be no assurance such procedures will effectively limit our credit risk and avoid losses, which could have a material adverse effect on our results of operations.

| 7 |

Our services, technology and industry relationships are key assets and competitive advantages of our company and our business may be affected by how we are perceived in the marketplace.

Our services, technology and industry relationships are key assets that enable us to effectively compete in our industry. Our ability to attract and retain customers is highly dependent upon external perceptions of the quality, efficacy, responsiveness and ease-of-use of our services and business practices, and overall financial condition. Negative perceptions or publicity regarding these matters could damage our reputation with customers and the public, which could make it difficult for us to attract and maintain customers. Adverse developments with respect to our industry may also, by association, negatively impact our reputation. Negative perceptions or publicity could have a material adverse effect on our business and financial results.

Our business performance is dependent upon the effectiveness of our technology investments, the failure of which could materially impact our business and financial results.

We have and will continue to undertake significant investments in our technology infrastructure to continually strengthen our position in research and marketing solutions and improve our existing technology platform. We may fail to effectively invest such amounts, or we may invest significant amounts in technologies that do not ultimately assist us in achieving our strategic goals. We may also fail to maintain our technology infrastructure in a manner that allows us to readily meet our customers’ needs. If we experience any of these or similar failures related to our technology investments, we will not achieve our expected revenue growth, or desired cost savings, and we could experience a significant competitive disadvantage in the marketplace, which could have a material adverse effect on our business and financial results.

In addition, the failure to continue to invest in our business could result in a material adverse effect on our future financial results. Such investments may include: executing on, and mitigating risks associated with, new product offerings and entrance into new geographic markets; and ensuring continued compatibility of our new platforms and technologies with our customers’ networks and systems.

We may be subject to intellectual property rights claims by third parties, which are extremely costly to defend, could require us to pay significant damages and could limit our ability to use certain technologies.

Third parties, including our content providers, may assert claims of infringement of intellectual property rights against us or our customers for which we may be liable or have an indemnification obligation. Any claim of infringement by a third party, even those without merit, could cause us to incur substantial costs defending against the claim and could distract our management from our business. Although third parties may offer a license to their content, the terms of any offered license may not be acceptable and the failure to obtain a license or the costs associated with any license could cause our business, results of operations or financial condition to be materially and adversely affected. In addition, our licenses are generally non-exclusive, and therefore our competitors may have access to the same content licensed to us. Furthermore, a successful claimant could secure a judgment or we may agree to a settlement that prevents us from providing certain content or that requires us to pay substantial damages, including treble damages if we are found to have willfully infringed the claimant’s copyrights, royalties or other fees. Any of these events could seriously harm our business, operating results and financial condition.

Our industry is subject to intense competition and rapid technological change, which may result in products or new solutions that are superior to our products or solutions under development. If we are unable to anticipate or keep pace with changes in the marketplace and the direction of technological innovation and customer demands, our products or solutions may become less useful or obsolete and our operating results will suffer.

The industry in which we operate in general is subject to intense and increasing competition and rapidly evolving technologies. Because our products are expected to have long development cycles, we must anticipate changes in the marketplace and the direction of technological innovation and customer demands. To compete successfully, we will need to demonstrate the advantages of our products and solutions.

Our future success will depend in large part on our ability to establish and maintain a competitive position in current and future technologies. Rapid technological development may render our products under development, or any future solutions we may have, and related technologies obsolete. Many of our competitors have or may have greater corporate, financial, operational, sales and marketing resources, and more experience in research and development than we have. We cannot assure you that our competitors will not succeed in developing or marketing technologies or products that are more effective or commercially attractive than our products or that would render our solutions and related technologies obsolete. We may not have or be able to raise or develop the financial resources, technical expertise, or support capabilities to compete successfully in the future. Our success will depend in large part on our ability to maintain a competitive position with our products and solutions.

Increased accessibility of free or relatively inexpensive information sources may reduce demand for our products and services.

In recent years, more public sources of free or relatively inexpensive information have become available, particularly through the Internet, and this trend is expected to continue. For example, some governmental and regulatory agencies have increased the amount of information they make publicly available at no cost. Public sources of free or relatively inexpensive information may reduce demand for our products and services. Our financial results may be adversely affected if our customers choose to use these public sources as a substitute for our products or services.

| 8 |

We depend on the services of Peter Victor Derycz and other key personnel, and may not be able to operate and grow our business effectively if we lose their services or are unable to attract qualified personnel in the future.

Our success depends in part upon the continued service of Peter Victor Derycz, who is our President and Chief Executive Officer. Mr. Derycz is critical to the overall management of our company as well as to the development of our technologies, our culture and our strategic direction and is instrumental in developing and maintaining close ties with our customer base. We also rely heavily on our senior management team because they have substantial experience with our diverse service offerings and business strategies. In addition, we rely on our senior management team to identify internal expansion and external growth opportunities. Our ability to retain senior management and other key personnel is therefore very important to our future success. We have employment agreements with our senior management, but these employment agreements do not ensure that they will not voluntarily terminate their employment with us. In addition, our key personnel are subject to non-solicitation and confidential information restrictions. We do not have key man insurance for any of our current management or other key personnel. The loss of any key personnel would require the remaining key personnel to divert immediate attention to seeking a replacement. Competition for senior management personnel is intense, and fit is important to us. Our inability to find a suitable replacement for any departing executive officer or key employee on a timely basis could adversely affect our ability to operate and grow our business.

We rely on our proprietary software systems, and our websites and online networks, and a disruption, failure or security compromise of these systems would disrupt our business, damage our reputation and adversely affect our revenue and profitability.

Our proprietary software systems are critical to our business because they enable the efficient and timely service of a large number of customer orders. Similarly, we rely on our websites, online networks, and email systems to obtain content and deliver customer orders, and provide timely, relevant and dependable business information to our customers. Therefore, network or system shutdowns caused by events such as computer hacking, sabotage, dissemination of computer viruses, worms and other destructive or disruptive software, denial of service attacks and other malicious activity, as well as loss of service from third parties, power outages, natural disasters and similar events, could affect our ability to store, handle and deliver data and services to our customers. Any such interruption of our operations could negatively impact customer satisfaction and revenue.

Breaches of our data security systems or unintended disclosure of our customer data could result in large expenditures to repair or replace such systems, to remedy any security breaches and to protect us from similar events in the future.

In addition to shutdowns, our systems are subject to risks caused by misappropriation, misuse, leakage, falsification and accidental release or loss of information, including sensitive data maintained in our proprietary software systems and credit card information of our customers. As a result of the increasing awareness concerning the importance of safeguarding information, ongoing attempts to hack and misuse companies’ information, and legislation that continues to be adopted regarding the protection and security of information, information-related costs and risks are increasing.

Disruptions or security compromises of our systems could result in large expenditures to repair or replace such systems, to remedy any security breaches and protect us from similar events in the future. We also could be exposed to negligence claims or other legal proceedings brought by our customers or their clients, and we could incur significant legal expenses and our management’s attention may be diverted from our operations in defending ourselves against and resolving lawsuits or claims. In addition, if we were to suffer damage to our reputation as a result of any system failure or security compromise, our revenue and profitability could be adversely affected.

Our failure to comply with the covenants contained in our loan agreement could result in an event of default that could adversely affect our financial condition and ability to operate our business as planned.

We currently have a line of credit with Silicon Valley Bank, maturing on October 31, 2017, under which there were no outstanding borrowings as of June 30, 2017. Our loan agreement contains, and any agreements to refinance our debt likely will contain, financial and restrictive covenants. While we were in compliance with these covenants as of June 30, 2017, we failed to comply with the tangible net worth covenant in December 2011 and July 2013. On both occasions the parties agreed to amend and reset the minimum tangible net worth required under the covenant. Our failure to comply with these covenants in the future may result in an event of default, which if not cured or waived, could result in the bank preventing us from accessing availability under our line of credit and requiring us to repay any outstanding borrowings. There can be no assurance that we will be able to obtain waivers of future covenant violations or that such waivers will be available on commercially acceptable terms.

In addition, the indebtedness under our loan agreement is secured by a security interest in substantially all of our tangible and intangible assets, and therefore, if we are unable to repay such indebtedness the bank could foreclose on these assets and sell the pledged equity interests, which would adversely affect our ability to operate our business. If any of these were to occur, we may not be able to continue operations as planned, implement our planned growth strategy or react to opportunities for or downturns in our business.

Government regulations related to the Internet could increase our cost of doing business, affect our ability to grow or may otherwise negatively affect our business.

Governmental agencies and federal and state legislatures have adopted, and may continue to adopt, new laws and regulatory practices in response to the increasing use of the Internet and other online services. These new laws may be related to issues such as online privacy, copyrights, trademarks and service mark, sales taxes, fair business practices, domain name ownership and the requirement that our operating units register to do business as foreign entities or otherwise be licensed to do business in jurisdictions where they have no physical location or other presence. In addition, these new laws, regulations or interpretations relating to doing business through the Internet could increase our costs materially and adversely affect our revenue and results of operations.

| 9 |

We may be adversely affected by changes in legislation and regulation.

Laws relating to communications, data protection, e-commerce, direct marketing and digital advertising and the use of public records have become more prevalent in recent years. Existing and proposed legislation and regulations, including changes in the manner in which such legislation and regulations are interpreted by courts in the United States, Europe and other jurisdictions, may impose limits on our collection and use of certain kinds of information and our ability to communicate such information effectively to our customers. It is difficult to predict in what form laws and regulations will be adopted or how they will be construed by the relevant courts, or the extent to which nay changes might adversely affect us.

Our growth strategy may require significant additional resources, and such additional resources might not be available on terms acceptable to us, if at all, which may in turn hamper our growth and adversely affect our business.

Our growth strategy will require us to significantly expand the capabilities of our administrative and operational resources. We intend to continue to make investments to support our business growth and may require additional funds to respond to business challenges, including the need to develop new technology, improve our operating infrastructure or acquire complementary businesses and technologies. Accordingly, we may need to undertake equity, equity-linked or debt financings to secure additional funds. If we raise additional funds through future issuances of equity or convertible debt securities, our existing stockholders could suffer significant dilution, and any new equity securities we issue could have rights, preferences and privileges superior to those of holders of our common stock. Any debt financing that we secure in the future could involve restrictive covenants relating to our capital raising activities and other financial and operational matters, including the ability to pay dividends. This may make it more difficult for us to obtain additional capital and to pursue business opportunities. We may not be able to obtain additional financing on terms favorable to us, if at all. If we are unable to obtain adequate financing or financing on terms satisfactory to us when we require it, our ability to continue to support our business growth and respond to business challenges could be significantly impaired, and our business may be adversely affected. In addition, our failure to successfully manage our growth could result in our sales not increasing commensurately with our capital investments. If we are unable to successfully manage our growth, we may be unable to achieve our goals.

Acquisitions, joint ventures or similar strategic relationships may disrupt or otherwise have a material adverse effect on our business and financial results.

As part of our strategy, we may explore strategic acquisitions and combinations, including the acquisition of customer lists, or enter into joint ventures or similar strategic relationships. These transactions are subject to the following risks:

| · | Acquisitions, joint ventures or similar relationships may cause a disruption in our ongoing business, distract our management and make it difficult to maintain our standards, controls and procedures; |

| · | We may not be able to integrate successfully the services, content, products and personnel of any such transaction into our operations; |

| · | We may not derive the revenue improvements, cost savings and other intended benefits of any such transaction; and |

| · | There may be risks, exposures and liabilities of acquired entities or other third parties with whom we undertake a transaction, that may arise from such third parties’ activities prior to undertaking a transaction with us. |

Our prior acquisitions have resulted in significant impairment charges and have operated at losses. We can provide no assurance that future acquisitions, joint ventures or strategic relationships will be accretive to our business overall or will result in profitable operations.

We are subject to risks related to our foreign operations which could adversely affect our operations and financial performance.

We have an operational and administrative support organization in Mexico, and sell our services worldwide. Foreign operations are subject to various risks which could have a material adverse effect on those operations or our business as a whole, including: exposure to local economic conditions; exposure to local political conditions; currency exchange rate fluctuations; reliance of local management; and additional potential costs of complying with rules and regulations of foreign jurisdictions. Any adverse consequence resulting from the materialization of the foregoing risks would adversely affect our financial performance and results of operations.

Unfavorable general economic conditions in the United States, Europe, or in other major markets could negatively impact our financial performance.

Unfavorable general economic conditions, such as a recession or economic slowdown in the United States, Europe, Japan, or in one or more of our other major markets, could negatively affect demand for our services and our results of operations. Under difficult economic conditions, businesses may seek to reduce spending on our services, or shift away from our services to in-house alternatives.

| 10 |

Risks Relating to Ownership of Our Common Stock

We cannot predict the extent to which an active public trading market for our common stock will develop or be sustained. If an active public trading market does not develop or cannot be sustained, you may be unable to liquidate your investment in our common stock.

We cannot predict the extent to which an active public market for our common stock will develop or be sustained due to a number of factors, including the fact that we are a small company that is relatively unknown to stock analysts, stock brokers, institutional investors, and others in the investment community that generate or influence sales volume, and that even if we came to the attention of such persons, they tend to be risk-averse and would be reluctant to follow an unproven company such as ours or purchase or recommend the purchase of our shares of common stock until such time as we became more seasoned and viable. As a consequence, there may be periods of several days or more when trading activity in our shares is minimal or non-existent, as compared to a seasoned issuer which has a large and steady volume of trading activity that will generally support continuous sales without an adverse effect on share price. We cannot give you any assurance that an active public trading market for our common stock will develop or be sustained. If such a market cannot be sustained, you may be unable to liquidate your investment in our common stock.

Our common stock may be subject to significant price volatility which may have an adverse effect on your ability to liquidate your investment in our common stock.

The market for our common stock may be characterized by significant price volatility when compared to seasoned issuers, and we expect that our share price will be more volatile than a seasoned issuer for the indefinite future. The potential volatility in our share price is attributable to a number of factors. First, our common shares may be sporadically and/or thinly traded. As a consequence of this lack of liquidity, the trading of relatively small quantities of shares by our stockholders may disproportionately influence the price of those shares in either direction. The price for our shares could, for example, decline precipitously in the event that a large number of our common shares are sold on the market without commensurate demand, as compared to a seasoned issuer that could better absorb those sales without adverse impact on its share price. Secondly, an investment in us is a speculative or “risky” investment due to our lack of meaningful profits to date and uncertainty of future profits. As a consequence of this enhanced risk, more risk-adverse investors may, under the fear of losing all or most of their investment in the event of negative news or lack of progress, be more inclined to sell their shares on the market more quickly and at greater discounts than would be the case with the stock of a seasoned issuer.

We have not paid cash dividends in the past and do not expect to pay cash dividends in the foreseeable future. Any return on your investment may be limited to increases in the market price of our common stock.

We have never paid cash dividends on our common stock and do not anticipate paying cash dividends on our common stock in the foreseeable future. In addition, our Loan and Security Agreement with Silicon Valley Bank prohibits us from paying cash dividends. The payment of dividends on our common stock will depend on our earnings, financial condition and other business and economic factors affecting us at such time as the board of directors may consider relevant. If we do not pay dividends, our common stock may be less valuable because a return on your investment might only occur if the market price of our common stock appreciates.

Voting power of a significant percentage of our common stock is held by our president and chief executive officer, and his brother-in-law, who together are able to exert significant influence over the outcome of matters to be voted on by our stockholders.

As of September 11, 2017, Peter Victor Derycz, our President and Chief Executive Officer, had voting power equal to approximately 16% of votes eligible to be cast at a meeting of our stockholders. Paul Kessler, the brother-in-law of Mr. Derycz, exercises investment and voting control over the shares held by Bristol Investment Fund, Ltd., and had, as of September 11, 2017, voting power equal to approximately 20% of votes eligible to be cast at a meeting of our stockholders. As a result of their significant ownership interests, Mr. Derycz and Mr. Kessler together currently have the ability to exert significant influence over the election of directors, and other matters submitted to a vote of all of our stockholders. They may also have interests that differ from yours and may vote in a manner that is adverse to your interests. This concentration of ownership may have the effect of deterring, delaying or preventing a change of control of our company, could deprive our stockholders of an opportunity to receive a premium for their common stock as part of a sale of our company and might ultimately affect the market price of our common stock.

The exercise of outstanding options and warrants to purchase our common stock could substantially dilute your investment.

Under the terms of our outstanding options and warrants to purchase our common stock issued to employees and others, the holders are given an opportunity to profit from a rise in the market price of our common stock that, upon the exercise of the options and/or warrants, could result in dilution in the interests of our other stockholders.

The market price of our common stock and the value of your investment could substantially decline if our warrants or options are exercised and our common stock is issued and resold into the market, or if a perception exists that a substantial number of shares will be issued upon exercise of our warrants and option and then resold into the market.

If the exercise prices of our warrants or options are lower than the price at which you made your investment, immediate dilution of the value of your investment will occur. In addition, sales of a substantial number of shares of common stock issued upon exercise of our warrants and options, or even the perception that such sales could occur, could adversely affect the market price of our common stock. You could, therefore, experience a substantial decline in the value of your investment as a result of both the actual and potential exercise of our warrants or options.

| 11 |

Because we are subject to the “Penny Stock” rules, the level of trading activity in our common stock may be reduced.

Our common stock is currently quoted on the OTCQB tier of the OTC Markets Group Inc., under the symbol “RSSS.” On September 11, 2017, the last reported sale price of our common stock on the OTCQB was $1.02. As a result, our common stock constitutes a “Penny Stock.” Broker-dealer practices in connection with transactions in Penny Stocks are regulated by rules adopted by the Securities and Exchange Commission, or SEC. Penny Stocks are generally equity securities with a price per share of less than $5.00 (other than securities registered on certain national exchanges). The Penny Stock rules require a broker-dealer, prior to a transaction in Penny Stocks not exempt from the rules, to deliver a standardized risk disclosure document that provides information about Penny Stocks and the nature and level of risks in the Penny Stock market. The broker-dealer must also provide the customer with current bid and offer quotations for the Penny Stock, the compensation of the broker-dealer and the salesperson in the transaction, and monthly accounting statements showing the market value of each Penny Stock held in the customer’s account. In addition, the broker-dealer must make a special written determination that the Penny Stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction. These requirements may have the effect of reducing the level of trading activity in a Penny Stock, such as our common stock, and investors in our common stock may find it difficult to sell their shares.

Because our common stock is not currently listed on a national securities exchange, you may find it difficult to dispose of or obtain quotations for our common stock.

Our common stock is quoted on the OTCQB under the symbol “RSSS.” Because our stock is quoted on the OTCQB rather than on a national securities exchange, you may find it difficult to either dispose of, or to obtain quotations as to the price of, our common stock.

Failure to achieve and maintain effective internal controls in accordance with Section 404 of the Sarbanes-Oxley Act of 2002 could result in a restatement of our financial statements, cause investors to lose confidence in our financial statements and our company and have a material adverse effect on our business and stock price.

We produce our financial statements in accordance with accounting principles generally accepted in the United States, or GAAP. Effective internal controls are necessary for us to provide reliable financial reports to help mitigate the risk of fraud and to operate successfully as a publicly traded company. As a public company, we are required to document and test our internal control procedures in order to satisfy the requirements of Section 404 of the Sarbanes-Oxley Act of 2002, or Section 404. Further, Section 404 requires annual management assessments of the effectiveness of our internal controls over financial reporting.

Testing and maintaining internal controls can divert our management’s attention from other matters that are important to our business. We may not be able to conclude on an ongoing basis that we have effective internal controls over financial reporting in accordance with Section 404. If we are unable to conclude that we have effective internal controls over financial reporting, investors could lose confidence in our reported financial information and our company, which could result in a decline in the market price of our common stock, and cause us to fail to meet our reporting obligations in the future, which in turn could impact our ability to raise additional financing if needed in the future.

Our board of directors has broad discretion to issue additional securities.

We are entitled under our certificate of incorporation to issue up to 100,000,000 shares of common stock and 20,000,000 shares of “blank check” preferred stock, although these amounts may change in the future subject to stockholder approval. Shares of our blank check preferred stock provide our board of directors’ broad authority to determine voting, dividend, conversion, and other rights. As of June 30, 2017 we had issued and outstanding 23,883,145 shares of common stock and we had 7,276,470 shares of common stock reserved for future grants under our equity compensation plans and for issuances upon the exercise or conversion of currently outstanding options, warrants and convertible securities. As of June 30, 2017, we had no shares of preferred stock issued and outstanding. Accordingly, as of June 30, 2017, we could issue up to 68,840,385 additional shares of common stock and 20,000,000 additional shares of “blank check” preferred stock. Any additional stock issuances could be made at a price that reflects a discount or premium to the then-current market price of our common stock. In addition, in order to raise capital, we may need to issue securities that are convertible into or exchangeable for a significant amount of our common stock. Our board may generally issue those common and preferred shares, or convertible securities to purchase those shares, without further approval by our stockholders. Any preferred shares we may issue could have such rights, preferences, privileges and restrictions as may be designated from time-to-time by our board, including preferential dividend rights, voting rights, conversion rights, redemption rights and liquidation provisions. We may also issue additional securities to our directors, officers, employees and consultants as compensatory grants in connection with their services, both in the form of stand-alone grants or under our stock incentive plans. The issuance of additional securities may cause substantial dilution to our stockholders.

Our articles of incorporation, bylaws and Nevada law have anti-takeover provisions that could discourage, delay or prevent a change in control, which may cause our stock price to decline.

Our articles of incorporation, bylaws and Nevada law contain provisions which could make it more difficult for a third party to acquire us, even if closing such a transaction would be beneficial to our stockholders. We are currently authorized to issue up to 20,000,000 shares of “blank check” preferred stock. This preferred stock may be issued in one or more series, the terms of which may be determined at the time of issuance by our board of directors without further action by stockholders. The terms of any series of preferred stock may include voting rights (including the right to vote as a series on particular matters), preferences as to dividend, liquidation, conversion and redemption rights and sinking fund provisions. No shares of our preferred stock are currently outstanding. The issuance of any preferred stock could materially adversely affect the rights of the holders of our common stock, and therefore, reduce the value of our common stock. In particular, specific rights granted to future holders of preferred stock could be used to restrict our ability to merge with, or sell our assets to, a third party and thereby preserve control by current management.

| 12 |

Provisions of our articles of incorporation, bylaws and Nevada law also could have the effect of discouraging potential acquisition proposals or making a tender offer or delaying or preventing a change in control, including changes a stockholder might consider favorable. Such provisions may also prevent or frustrate attempts by our stockholders to replace or remove our management. In particular, our articles of incorporation, our bylaws and Nevada law, as applicable, among other things, provide our board of directors with the ability to alter our bylaws without stockholder approval, and provide that vacancies on our board of directors may be filled by a majority of directors in office, although less than a quorum.

We may become subject to Nevada’s control share acquisition laws (Nevada Revised Statutes 78.378 -78.3793), which prohibit an acquirer, under certain circumstances, from voting shares of a corporation’s stock after crossing specific threshold ownership percentages, unless the acquirer obtains the approval of the issuing corporation’s stockholders. We are also subject to Nevada’s Combination with Interested Stockholders Statute (Nevada Revised Statutes 78.411 -78.444) which prohibits an interested stockholder from entering into a “combination” with the corporation, unless certain conditions are met. These provisions are expected to discourage certain types of coercive takeover practices and inadequate takeover bids and to encourage persons seeking to acquire control of our company to first negotiate with our board of directors. These provisions may delay or prevent someone from acquiring or merging with us, which may cause the market price of our common stock to decline.

Item 1B. Unresolved Staff Comments

Not applicable.

Our executive offices are located at 15821 Ventura Blvd., Suite 165, Encino, California. We lease approximately 3,765 square feet of office space for approximately $10,500 per month from an unrelated third party. The lease expires on January 31, 2021.

Reprints Desk Latin America S. de R.L. de C.V, rents on a month to month basis approximately 280 square meters of office space in Monterrey, Mexico, for approximately $1,200 (22,000 Mexican Pesos) per month.

We believe that our existing facilities are sufficient to meet our present and anticipated needs for the foreseeable future.

We are involved in legal proceedings in the ordinary course of our business. Although our management cannot predict the ultimate outcome of these legal proceedings with certainty, it believes that the ultimate resolution of our legal proceedings, including any amounts we may be required to pay, will not have a material effect on our consolidated financial statements.

Item 4. Mine Safety Disclosures

Not applicable.

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information and Approximate Number of Holders of Common Stock

Our common stock is quoted on the OTCQB under the symbol "RSSS." The following table sets forth, for the periods indicated, the reported high and low bid quotations for our common stock as reported on the OTCQB. The bid prices reflect inter-dealer quotations, do not include retail markups, markdowns, or commissions, and do not necessarily reflect actual transactions

| High Bid | Low Bid | |||||||

| Year Ended June 30, 2017: | ||||||||

| First Quarter (July 1 – September 30) | $ | 1.17 | $ | 0.89 | ||||

| Second Quarter (October 1 – December 31) | $ | 1.04 | $ | 0.75 | ||||

| Third Quarter (January 1 – March 31) | $ | 1.20 | $ | 1.00 | ||||

| Fourth Quarter (April 1 – June 30) | $ | 1.04 | $ | 0.66 | ||||

| Year Ended June 30, 2016: | ||||||||

| First Quarter (July 1 – September 30) | $ | 1.05 | $ | 0.70 | ||||

| Second Quarter (October 1 – December 31) | $ | 0.89 | $ | 0.55 | ||||

| Third Quarter (January 1 – March 31) | $ | 0.88 | $ | 0.49 | ||||

| Fourth Quarter (April 1 – June 30) | $ | 1.20 | $ | 0.84 | ||||

As of September 11, 2017, we had a total of 24,169,792 shares of our common stock outstanding and the closing sales price was $1.02 per share on the OTCQB. According to the records of our transfer agent, we had 39 record holders of our common stock as of September 11, 2017. Because brokers and other institutions hold shares on behalf of stockholders, we are unable to estimate the total number of stockholders represented by these record holders.

| 13 |

Dividends

We have never declared or paid dividends on our common stock. In addition, our Loan and Security Agreement with Silicon Valley Bank prohibits us from paying cash dividends. We currently intend to retain all available funds and any future earnings for use in the operation of our business and do not anticipate paying any dividends on our common stock in the foreseeable future, if at all. Any future determination to declare dividends will be made at the discretion of our board of directors and will depend on our financial condition, operating results, capital requirements, general business conditions and other factors that our board of directors may deem relevant.

Common Stock Repurchases

On March 10, 2015, the Compensation Committee of our Board of Directors authorized the repurchase, over a 12-month period on the last day of each trading window and otherwise in accordance with our insider trading policies, of up to $139,181 of outstanding common stock (at prices no greater than $1.60 per share) from our employees to satisfy their tax obligations in connection with the vesting of stock incentive awards. The actual number of shares repurchased will be determined by applicable employees in their discretion, and will depend on their evaluation of market conditions and other factors.

On May 24, 2016, the Compensation Committee of our Board of Directors authorized the repurchase, over a 12-month period on the last day of each trading window and otherwise in accordance with our insider trading policies, of up to $100,000 of outstanding common stock (at prices no greater than $1.60 per share) from our employees to satisfy their tax obligations in connection with the vesting of stock incentive awards. The actual number of shares repurchased will be determined by applicable employees in their discretion, and will depend on their evaluation of market conditions and other factors.

On February 16, 2017, the Compensation Committee of our Board of Directors authorized the repurchase, over a 12-month period on the last day of each trading window and otherwise in accordance with our insider trading policies, of up to $300,000 of outstanding common stock (at prices no greater than $2.00 per share) from our employees to satisfy their tax obligations in connection with the vesting of stock incentive awards. The actual number of shares repurchased will be determined by applicable employees in their discretion, and will depend on their evaluation of market conditions and other factors.

During the years ended June 30, 2017 and 2016, we repurchased 195,958 and 46,898 shares of our common stock under the repurchase plan at an average price of approximately $1.02 and $0.80 per share, respectively, for an aggregate amount of $199,323 and $37,747, respectively. As of June 30, 2017, $175,050 remains under the current authorization to repurchase our outstanding common stock from our employees.

Shares repurchased are retired and deducted from common stock for par value and from additional paid in capital for the excess over par value. Direct costs incurred to acquire the shares are included in the total cost of the shares.

The following table summarizes repurchases of our common stock on a monthly basis:

| Period | Total Number of Shares Purchased1 | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||||||

| September 2015 | 1,848 | $ | 0.95 | - | - | |||||||||||

| December 2015 | 27,450 | $ | 0.67 | - | - | |||||||||||

| June 2016 | 17,600 | $ | 1.00 | - | - | |||||||||||

| Year ended June 30, 2016 | 46,898 | $ | 0.80 | - | - | |||||||||||

| September 2016 | 25,508 | $ | 1.04 | - | - | |||||||||||

| December 2016 | 54,200 | $ | 1.03 | - | - | |||||||||||

| March 2017 | 7,250 | $ | 1.10 | - | $ | 292,025 | ||||||||||

| June 2017 | 109,000 | $ | 1.00 | - | $ | 175,050 | ||||||||||

| Year ended June 30, 2017 | 195,958 | $ | 1.02 | - | $ | 175,050 | ||||||||||

1 Consists of shares of common stock purchased from employees to satisfy tax obligations in connection with the vesting of stock incentive awards.

| 14 |

Equity Compensation Plan Information

Information relating to compensation plans under which our equity securities are authorized for issuance is set forth in Item 12 of this report under “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.”

Item 6. Selected Financial Data

Not required.

| 15 |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Cautionary Notice Regarding Forward-Looking Statements

The following discussion and analysis of our financial condition and results of operations for the years ended June 30, 2017 and 2016 should be read in conjunction with our consolidated financial statements and related notes to those financial statements that are included elsewhere in this report. Our discussion includes forward-looking statements based upon current expectations that involve risks and uncertainties, such as our plans, objectives, expectations and intentions. Actual results and the timing of events could differ materially from those anticipated in these forward-looking statements as a result of a number of factors, including those set forth under “Risk Factors” and elsewhere in this report.

We use words such as “anticipate,” “estimate,” “plan,” “project,” “continuing,” “ongoing,” “expect,” “believe,” “intend,” “may,” “will,” “should,” “could,” and similar expressions to identify forward-looking statements. All forward-looking statements included in this report are based on information available to us on the date hereof and, except as required by law, we assume no obligation to update any such forward-looking statements.

Overview

Research Solutions was incorporated in the State of Nevada on November 2, 2006, and is a publicly traded holding company with two wholly owned subsidiaries at June 30, 2016: Reprints Desk, Inc., a Delaware corporation and Reprints Desk Latin America S. de R.L. de C.V, an entity organized under the laws of Mexico.

On June 30, 2017, we sold the intangible assets of our Reprints and ePrints business line, but specifically excluding billed accounts receivable and respective liabilities, pursuant to an Asset Purchase Agreement dated June 20, 2017. The aggregate net consideration for the sale is comprised of $450,000 paid on the closing date, and earn-out payments of 45% of gross margin over the 30 month period subsequent to the closing date. We have made a policy election to record the contingent consideration when the consideration is determined to be realizable (each 6-month period ending subsequent to the closing date).

We provide two service offerings to our customers: annual licenses that allow customers to access and utilize certain premium features of our cloud based software-as-a-service (“SaaS”) research intelligence platform (“Platforms”) and the transactional sale of published scientific, technical, and medical (“STM”) content managed, sourced and delivered through the Platform (“Transactions”). Platforms and Transactions are packaged as a single solution that enable life science and other research intensive organizations to speed up research and development activities with faster, single sourced access and management of content and data used throughout the intellectual property development lifecycle.

Platforms

Our cloud-based SaaS research intelligence platform consists of proprietary software and Internet-based interfaces. Legacy functionality allows customers to initiate orders, route orders for the lowest cost acquisition, manage transactions, obtain spend and usage reporting, automate authentication, and connect seamlessly to in-house and third-party software systems. Customers can also enhance the information resources they already own or license and collaborate around bibliographic information.

Additional functionality has recently been added to our Platform in the form of interactive app-like gadgets. An alternative to manual data filtering, identification and extraction, gadgets are designed to gather, augment, and extract data across a variety of formats, including bibliographic citations, tables of contents, RSS feeds, PDF files, XML feeds, and web content. We are rapidly developing new gadgets in order to build an ecosystem of gadgets. Together, these gadgets will provide researchers with an “all in one” toolkit, delivering efficiencies in core research workflows and knowledge creation processes.

Our Platform is deployed as a single, multi-tenant system across our entire customer base. Customers securely access the Platform through online web interfaces and via web service APIs that enable customers to leverage Platform features and functionality from within in-house and third-party software systems. The Platform can also be configured to satisfy a customer’s individual preferences. We leverage our Platform’s efficiencies in scalability, stability and development costs to fuel rapid innovation and competitive advantage.

Transactions

Researchers and knowledge workers in life science and other research-intensive organizations generally require single copies of published STM journal articles for use in their research activities. These individuals are our primary users. Our Platform provides our customers with a single source to the universe of published STM content that includes over 70 million existing STM articles and over one million newly published STM articles each year.

Our Platform allows customers to find and download digital versions of STM articles that are critical to their research. Customers submit orders for the articles they need which we source and electronically deliver to them generally in under an hour. This service is generally known in the industry as single article delivery or document delivery. We also obtain the necessary permission licenses from the content publisher or other rights holder so that our customer’s use complies with applicable copyright laws. We have arrangements with hundreds of content publishers that allow us to distribute their content. The majority of these publishers provide us with electronic access to their content, which allows us to electronically deliver single articles to our customers often in a matter of minutes.

| 16 |

Critical Accounting Policies and Estimates

The preparation of our consolidated financial statements in conformity with accounting principles generally accepted in the United States, or GAAP, requires us to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenue and expenses, and related disclosure of contingent assets and liabilities. When making these estimates and assumptions, we consider our historical experience, our knowledge of economic and market factors and various other factors that we believe to be reasonable under the circumstances. Actual results may differ under different estimates and assumptions.

The accounting estimates and assumptions discussed in this section are those that we consider to be the most critical to an understanding of our financial statements because they inherently involve significant judgments and uncertainties.

Revenue Recognition

Our policy is to recognize revenue when services have been performed, risk of loss and title to the product transfers to the customer, the selling price is fixed or determinable, and collectability is reasonably assured. We generate revenue by providing two service offerings to our customers: annual licenses that allow customers to access and utilize certain premium features of our cloud based SaaS research intelligence platform (“Platforms”) and the transaction sale of STM content managed, sourced and delivered through the Platform (“Transactions”).

Platforms

We charge a subscription fee that allows customers to access and utilize certain premium features of our Platform. Revenue is recognized ratably over the term of the subscription agreement, which is typically one year, provided all other revenue recognition criteria have been met. Billings or payments received in advance of revenue recognition are recorded as deferred revenue.

Transactions

We charge a transactional service fee for the electronic delivery of single articles, and a corresponding copyright fee for the permitted use of the content. We recognize revenue from single article delivery services upon delivery to the customer only when the selling price is fixed or determinable, and collectability is reasonably assured.

Stock-Based Compensation