Attached files

| file | filename |

|---|---|

| EX-10.10 - SEVERANCE AGREEMENT - Oncolix, Inc. | aepp_ex1010.htm |

| EX-23.1 - CONSENT OF INDEPENDENT - Oncolix, Inc. | aepp_ex231.htm |

| EX-21.1 - LIST OF SUBSIDIARIES - Oncolix, Inc. | aepp_ex211.htm |

| EX-10.12 - FORM OF OPTION AGREEMENT - Oncolix, Inc. | aepp_ex1012.htm |

| EX-10.11 - SEVERANCE AGREEMENT - Oncolix, Inc. | aepp_ex1011.htm |

| EX-5.1 - LEGAL OPINION - Oncolix, Inc. | aepp_ex51.htm |

| EX-4.1 - COMMON STOCK SPECIMEN - Oncolix, Inc. | aepp_ex41.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

| ADVANCED ENVIRONMENTAL PETROLEUM PRODUCERS INC. |

| (Exact name of registrant as specified in its charter) |

| Florida |

| 2834 |

| 46-3046340 |

| (State or other jurisdiction of |

| (Primary Standard Industrial |

| (I. R. S. Employer |

| incorporation or organization) |

| Classification Code Number) |

| Identification Number) |

14405 Walters Road, Suite 780

Houston, Texas 77014

(281) 402-3167

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Michael T. Redman

Chief Executive Officer

14405 Walters Road, Suite 780

Houston, Texas 77014

(281) 402-3167

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copy to:

Thomas C. Pritchard, Esq.

Thomas C. Pritchard, P.C.

800 Bering Dr., Suite 201

Houston, Texas 77057

Tel: (713) 209-2911

Fax: (832) 538-1265

As soon as practicable after this Registration Statement becomes effective

(Approximate date of commencement of proposed sale to the public)

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filed, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filed,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | ¨ | Smaller reporting company | x |

| (Do not check if a smaller reporting company) | Emerging growth company | ¨ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to Be Registered |

| Amount Being Registered (1) |

|

| Proposed Maximum Offering Price Per Share(2) |

|

| Proposed Maximum Aggregate Offering Price |

|

| Amount of Registration Fee |

| ||||

| Shares of Common Stock underlying the Principal Amount of Convertible Notes(3) |

|

| 55,872,837 |

|

| $ | 0.105 |

|

| $ | 5,866,647.89 |

|

| $ | 679.94 |

|

| Common Stock Underlying the Interest of the Convertible Notes(4) |

|

| 5,633,847 |

|

| $ | 0.105 |

|

| $ | 591,553.94 |

|

| $ | 68.56 |

|

| Shares underlying the Principal Amount of Interest of the Convertible Notes in the event of a price decline and concomitant reduction in conversion price(5) |

|

| 6,150,670 |

|

| $ | 0.105 |

|

| $ | 645,820.35 |

|

| $ | 74.85 |

|

| Shares of Common Stock underlying the Warrants(6) |

|

| 59,072,837 |

|

| $ | 0.105 |

|

| $ | 6,202,647.89 |

|

| $ | 718.89 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| TOTAL |

|

| 126,730,191 |

|

|

| -- |

|

| $ | 13,306,670.07 |

|

| $ | 1,542.24 |

|

Shares to Register:

|

| (1) | Pursuant to Rule 416 under the Securities Act of 1933, the Registrant is also registering such additional indeterminate number of shares as may become necessary to adjust the number of shares as a result of a stock split, stock dividend or similar adjustment of its outstanding Common Stock. Registrant is also registering additional shares of Common Stock to be available for issuance based on market fluctuation. |

|

|

|

|

|

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(c) under the Securities Act of 1933, as amended, based on the average high and low prices of the Common Stock as traded on the OTC Pink on August 24, 2017. |

|

|

|

|

|

| (3) | Represents shares of Common Stock issuable by the registrant upon the conversion of the convertible notes in the aggregate original principal amount of $4,190,463 issued to the selling security holders (the “Convertible Notes”) pursuant to the terms of the Convertible Notes dated August 3, 2017. |

|

|

|

|

|

| (4) | Represents shares of Common Stock issuable by the registrant upon the conversion of interest to be accrued pursuant to the terms of the Convertible Notes at a conversion price of $0.075 per share. |

|

|

|

|

|

| (5) | Represents shares of Common Stock as a buffer in the event the monthly redemption payment or interest payment calculations are based on the lower of $0.075 per share and 75% of the average of the five lowest closing bid prices for the twenty consecutive trading days prior to such determination date. |

|

|

|

|

|

| (6) | Represents shares of Common Stock issuable by the registrant upon exercise of Warrants to purchase shares of Common Stock to be issued to the selling security holders (the “Warrants”) upon the terms and conditions set forth in the warrant agreement dated August 3, 2017. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

| 2 |

The information in this prospectus is not complete and may be amended. The selling security holders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION

Prospectus dated August 29, 2017

ADVANCED ENVIRONMENTAL PETROLEUM PRODUCERS INC.

126,730,191 Shares of Common Stock

This prospectus relates to the resale of up to 126,730,191 shares of common stock, par value $0.0001 (“Common Stock”), by certain shareholders (the “selling security holders”). The shares of Common Stock subject to this prospectus include:

|

| (1) | 67,657,354 shares of Common Stock issuable upon conversion of the Convertible Notes with the aggregate principal amounts of $4,190,463 issued to selling security holders (the “Convertible Notes”) pursuant to the Convertible Notes issued August 3, 2017, by and between the Company and selling security holders, and interest to be accrued until maturity. Based upon the current market price of the Company’s Common Stock, the amount of the Company’s Common Stock being registered may be in excess of the number of shares into which the Convertible Notes may currently be converted, however the parties have agreed upon the aggregate number of shares to be registered to account for market fluctuations. |

|

|

|

|

|

| (2) | 59,072,837 shares of Common Stock issuable upon exercise of warrants (“Warrants”) upon the terms and conditions set forth in the Warrant Agreement. |

We will not receive any proceeds from the resale of any of the shares offered hereby,

Our Common Stock is listed for quotation on the OTC Pink quotation systems under the symbol “AEPP.” The market for the Common Stock is limited, sporadic and volatile. The closing price of our Common Stock on August 24, 2017 was $0.11 per share.

We are not selling any of the Common Stock that we are registering. The Common Stock will be sold by the selling security holders as detailed in this prospectus. Such selling security holders may sell the Common Stock at the market price as of the date of sale or a price negotiated in a private sale. Our Common Stock is listed for quotation on the OTC Pink quotation system under the symbol “AEPP.”

This investment involves a high degree of risk. You should purchase shares only if you can afford a complete loss of your investment. You should read this prospectus in its entirety and carefully consider the risk factors beginning on page 9 of this prospectus and the financial data and related notes incorporated by reference before deciding to invest in the shares.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is _______, 2017

| 3 |

|

| 5 |

| |

|

| 5 |

| |

|

| 10 |

| |

|

| 23 |

| |

|

| 24 |

| |

|

| 24 |

| |

|

| 28 |

| |

|

| 30 |

| |

|

| 34 |

| |

| MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

| 49 |

|

|

| 56 |

| |

|

| 56 |

| |

|

| 58 |

| |

|

| 61 |

| |

| DISCLOSURE OF COMMISSION POSITION OF INDEMNIFICATION FOR SECURITIES ACT LIABILITIES |

| 63 |

|

|

| 63 |

| |

|

| 64 |

| |

|

| 64 |

| |

|

| F-1 |

|

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with information that is different. This prospectus is not an offer to sell, nor is it seeking an offer to buy, these securities in any jurisdiction where the offer or sale of these securities is not permitted. You should assume that the information contained in this prospectus is accurate as of the date on the front of this prospectus only. Our business, financial condition, results of operations and prospects may have changed since that date. This prospectus will be updated as required by law.

| 4 |

| Table of Contents |

PROSPECTUS SUMMARY

ADVANCED ENVIRONMENTAL PETROLEUM PRODUCERS INC.

This summary highlights selected information about the Company and this offering. This summary is not complete and does not contain all of the information that may be important to you. You should read carefully the entire prospectus, including “Risk Factors” and the other information contained or incorporated by reference in this prospectus before making an investment decision. Unless otherwise indicated or the context otherwise requires: (i) “we,” “us,” “our,” or “Company” refer to Advanced Environmental Petroleum Producers Inc. and its wholly-owned subsidiary, Oncolix, Inc. (“Oncolix”) and (ii) in certain instances we refer to AEPP to describe AEPP’s operations or financial statements prior to the Merger (as described below) and Oncolix to describe Oncolix’s operations or financial statements prior to the Merger.

This prospectus contains certain “forward-looking statements” within the meaning of the federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which statements involve substantial risks and uncertainties. In some cases, it is possible to identify forward-looking statements because they contain words such as “anticipates,” believes,” “contemplates,” “continue,” “could,” “estimates,” “expects,” “future,” “intends,” “likely,” “may,” “plans,” “potential,” “predicts,” “projects,” “seek,” “should,” “target” or “will,” or the negative of these words or other similar terms or expressions that concern our expectations, strategy, plans or intentions. Many factors could cause our actual operations or results to differ materially from the operations and results anticipated in forward-looking statements. These factors include, but are not limited to, those set forth under “Risk Factors” commencing on page 10.

· the early stage of development of our product candidate Prolanta™; · the timing, cost or results of our clinical trials; · our need for substantial additional funds and uncertainties regarding our ability to raise such funds on acceptable terms, if at all; · our ability to make arrangements to repay indebtedness, and the possible loss of assets or our ability to operate if we are unable to do so on acceptable terms; · uncertainties relating to patent and intellectual property matters; and · our dependence on third parties, including our contract manufacturer, clinical research organizations, and consultants.

Company

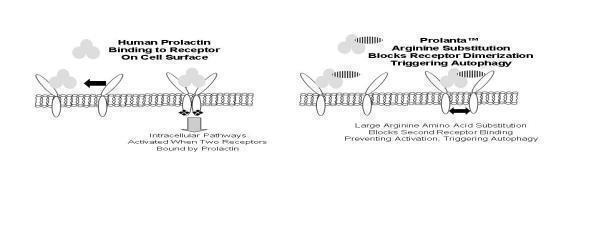

We are a clinical-stage biopharmaceutical company developing medical therapies for the treatment of cancer. We currently own issued or pending patent applications related to the use of Prolanta™, a recombinant protein analogue of human prolactin that is designed to bind to the prolactin receptor on human cells. There is substantial scientific evidence that prolactin is associated with various cancers, including ovarian, breast, uterine and prostate. We and our collaborators have conducted animal studies that indicate that our drug Prolanta™ may be effective in treating breast and ovarian cancers, either as a stand-alone therapy or in combination with other drugs, by blocking the effect of human prolactin. ProlantaTM may also affect the cellular mechanisms that assist cancer cells to develop resistance to chemotherapy.

Our initial focus is the development, clinical testing and commercialization of Prolanta™ for the treatment of ovarian cancer. The US Food and Drug Administration (“FDA”) has provided us with clearance to commence a Phase 1clinical trial of Prolanta™ in the treatment of ovarian cancer, and we have dosed three subjects in the first phase of this clinical trial. We chose ovarian cancer as the first human application of Prolanta™ because of the significant unmet medical need as well as favorable regulatory status. Because of the size of the US market, the FDA has granted Prolanta™ status as an Orphan Drug, providing potential tax benefits and market exclusivity. We intend to apply for Orphan designation in the European Union and in Japan.

If Prolanta™ is found to be safe and well tolerated in the Phase 1 study, we will seek regulatory clearance to conduct additional clinical trials in larger numbers of ovarian cancer patients to establish efficacy. We expect that at least two clinical studies will be required, and possibly more, to establish the efficacy and safety of Prolanta™ in sufficient numbers of ovarian cancer patients in order to seek approval to market Prolanta™ for this cancer. The design of these studies will be finalized after the completion of the Phase 1 study and after consultation with the FDA, but we currently believe we will first evaluate the use of Prolanta™ in combination with other chemotherapy drugs such as platinum-based drugs and taxanes. There is preclinical and laboratory evidence that Prolanta™ may be synergistic with these other therapies, allowing a broader market opportunity. We intend to seek a distribution partner to market Prolanta™, but may develop our own sales force in the event we cannot make suitable arrangements.

| 5 |

| Table of Contents |

Depending on the availability of resources, we also intend to evaluate Prolanta™ for the treatment of other cancers. These studies may be performed in collaboration with larger pharmaceutical companies, either through licenses or joint ventures. Our scientific collaborators have demonstrated in animal models the efficacy of Prolanta™ in treating breast cancer, and we intend to engage academic collaborators to develop data for the treatment of other cancer types.

We may also consider in-licensing or acquiring other drug candidates, preferably in oncology. We operate with a small staff of employees and key consultants and have utilized contractors for certain operations. We do not intend to develop the infrastructure or acquire the facilities necessary to manufacture Prolanta™, and instead we plan to utilize contract manufacturers. We also plan to utilize contract research organizations to assist us in conducting clinical trials. We intend to employ additional administrative and clinical personnel as necessary to conduct our clinical trials and commercialize Prolanta™.

Recent Developments

Acquisition of Oncolix

On August 3, 2017, the Company closed its agreement and plan of merger whereby AEPP Merger Sub, Inc., a wholly-owned subsidiary of the Company (“Merger Sub”) merged with and into Oncolix, and Oncolix became a wholly-owned subsidiary of the Company (“Merger”). Pursuant to the terms of the Merger, a total of 71,770,200 shares of Company Common Stock were issued to the former common stock holders of Oncolix and 62,138,680 shares of Company Series A Preferred Stock were issued to the former series A preferred stock holders of Oncolix. Each share of Series A Preferred Stock issued by the Company is convertible into one share of Company Common Stock, has voting rights, a liquidation preference, and other customary rights and preferences. As a result of the Merger, the shares of Company Common Stock owned by Oncolix were cancelled. In addition, pursuant to the Merger, all outstanding options and warrants to acquire Oncolix common stock and Series A Preferred Stock were converted into the right to acquire or convert into Company Common Stock or Company Series A Preferred Stock.

Post-Merger a warrant to purchase Series A Preferred Stock was exercised resulting in an additional amount of 899,604 shares of Series A Preferred Stock being issued. As of August 28, 2017, there are 103,536,703 shares of Company Common Stock issued and outstanding and 63,038,284 shares of Series A Preferred Stock issued and outstanding that are convertible into 63,038,284 shares of Company Common Stock.

The Merger was treated as a reverse acquisition of AEPP, a public shell company, for financial accounting and reporting purposes. As such, Oncolix is treated as the acquirer for accounting and financial reporting purposes while AEPP is treated as the acquired entity for accounting and financial reporting purposes. Further, as a result, the financial statements for periods prior to the Merger that will be reflected in this filing and the Company’s future financial statements filed with the United States Securities and Exchange Commission (“SEC”) will be those of Oncolix, and the Company’s assets, liabilities and results of operations for periods after the Merger, including this filing, will be the consolidated assets, liabilities and results of operations of AEPP and Oncolix.

Debt and Warrant Financing

On August 3, 2017, AEPP and Oncolix entered into agreements with investors in connection with a $4,190,463 convertible debt and warrant financing (the “Units”). Such investment was effected through the issuance and sale of Units of Convertible Notes and Warrants for (i) $2,000,000 in cash for Convertible Notes in the principal amount of $2,352,941 and Warrants to acquire 31,372,547 shares of AEPP Common Stock (the “Cash Offering”) and (ii) (A) the exchange of outstanding secured indebtedness in the amount of $1,561,894 and warrants to acquire 17,608,280 shares of AEPP Common Stock (formerly Oncolix warrants prior to being assumed by AEPP in the Merger) issued by Oncolix to existing noteholders (“Existing Investors”), for (B) the issuance and sale of Units of Convertible Notes issued by the Company in the aggregate principal amount of $1,837,522 and Warrants to acquire 24,500,290 shares of Company Common Stock (the “Exchange Offering” and collectively with the Cash Offering, referred to as the “Unit Offering). The investors in the Unit Offering are collectively referred to as “Purchasers”. In addition, Warrants to acquire an additional 3,200,000 shares of Company Common Stock are held by a Purchaser and included in Warrants herein.

The Unit Offering is documented with the Purchasers pursuant to the following: (i) a Securities Purchase Agreement, dated August 3, 2017, by and among AEPP, Purchasers and Oncolix (the “Purchase Agreement”); (ii) 10% Senior Secured Convertible Notes of AEPP issued in favor of the Purchasers (the “Convertible Notes”); (iii) a Registration Rights Agreement, dated August 3, 2017, by and between AEPP and the Purchasers (the “Registration Rights Agreement”); (iv) a Security Agreement, dated August 3, 2017, by and among AEPP, Oncolix and Purchasers (the “Security Agreement”); (v) an IP Security Agreement, dated August 3, 2017, by and among AEPP, Oncolix and the collateral agent of the Unit Offering (the “IP Security Agreement”); (vi) five-year warrants to purchase AEPP Common Stock dated August 3, 2017, issued by AEPP to the Purchasers (“Warrants”); (vii) a Lock-Up Agreement, dated August 3, 2017, by and among AEPP, Oncolix and certain existing equity holders (the “Lock-Up Agreement”); and (viii) a Subsidiary Guarantee, dated August 3, 2017, by and between Oncolix and Purchasers (the “Guarantee” and collectively with the Purchase Agreement, Convertible Notes, Registration Rights Agreement, Security Agreement, IP Security Agreement, Warrants and Lock-Up Agreement, the “Transaction Documents”), pursuant to which AEPP issued and sold the Convertible Notes and the Warrants to the Purchasers pursuant to the Transaction Documents.

| 6 |

| Table of Contents |

Convertible Notes

Pursuant to the Purchase Agreement, the Company issued Convertible Notes to the Purchasers in an aggregate principal amount of $4,190,463 for a purchase price of $3,561,894, consisting of gross cash proceeds of $2,000,000 and the exchange of existing convertible debt and related accrued interest of Oncolix totaling $1,561,894. The Convertible Notes were issued at a 15% discount.

The Convertible Notes bear interest at a rate of 10% per annum, payable quarterly on November 1, 2017, February 1, 2018, and May 1, 2018 and thereafter, on a monthly basis until maturity. The interest is payable in cash or, at the option of the Company, subject to compliance with Equity Conditions (as defined below), in fully tradable Company Common Stock at the lesser of the then conversion price or a 25% discount to the average of the five lowest closing bid prices for the twenty trading days prior to the interest payment date. The final maturity of the Convertible Notes is November 1, 2018, but commencing on May 1, 2018 and on the first day of each month thereafter until maturity, we are required to redeem an amount of the Convertible Notes equal to 1/7th of the original principal amount, plus 10% of such monthly redemption amount as a bonus. The principal payments shall be made in cash or, subject to the satisfaction of Equity Conditions, in our Common Stock valued at the lesser of the then conversion price or a 25% discount to the average of the five lowest closing bid prices for the twenty trading days prior to the amortization date.

The Convertible Notes are convertible at the option of the Purchasers at a conversion price equal to the lesser of (i) $0.075 per share of our Common Stock, (ii) 75% of the 10-day average closing bid price of our Common Stock for the period prior to the filing of a registration statement as described below (subject to a floor of $0.0375 per share), and (iii) 75% of the 10-day average closing bid price of our Common Stock for the 10-day period prior to the effective date of the registration statement (subject to a floor of $0.0375 per share). The Convertible Notes contain customary anti-dilution protection, including full-ratchet anti-dilution adjustments in the event of certain dilutive issuances (that adjust both conversion price and share amounts to be issued upon conversion).

In the event of a closing of an $8 million financing in connection with a change in listing of our Common Stock to Nasdaq or the NYSE, the Convertible Notes shall be subject to mandatory conversion into our Common Stock at a 30% discount to the offering price.

We shall be required to offer to prepay in cash the aggregate principal amount of the Convertible Notes at 120% of the principal amount thereof plus any unpaid accrued interest to the date of repayment, at maturity, on the sale of substantially all of our assets, upon a change of control, upon a qualified offering, or upon a “fundamental transaction” (tender offer, reclassification, sale of substantially all assets and merger); in such an event, the Purchasers shall have the right to convert the Convertible Notes prior to the date of any such prepayment.

The Convertible Notes contain standard negative covenants customary for transactions of this type. The events of default are also customary for transactions of this type, including default in timely payment of principal or interest, failure to observe or perform any covenant or agreement contained in the Convertible Note and Transaction Documents (including the Registration Rights Agreement), the commencement of bankruptcy or insolvency proceedings, failure to timely deliver conversion shares underlying the Convertible Notes, failure to timely file Exchange Act filings, and failure to satisfy certain Equity Conditions.

Equity Conditions mean, during the period in question, (a) the Company shall have duly honored all conversions and redemptions of the Convertible Notes, (b) we shall have complied with all conversion and other provisions of the Convertible Notes and shall have paid all liquidated damages and other amounts owing in respect of this Convertible Note, (c)(A) there is an effective registration statement pursuant to which the holder is permitted to utilize the prospectus thereunder to resell at least the number of shares of Common Stock issuable pursuant to the Transaction Documents at such time or (B) all of the underlying shares may be resold pursuant to Rule 144 without volume or manner-of-sale restrictions or current public information requirements, (d) our Common Stock is trading on a trading market, (e) there is a sufficient number of authorized but unissued and otherwise unreserved shares of our Common Stock for the issuance of five times all of the shares issuable pursuant to the Convertible Notes and Warrants, (f) there is no existing event of default or no existing event which, with the passage of time or the giving of notice, would constitute an event of default, (g) the issuance of the shares in question would not violate the beneficial ownership limitations in the Transaction Documents, (h) there has been no public announcement of a pending or proposed fundamental transaction or change of control transaction that has not been consummated, (i) the holder is not in possession of any information provided by the Company that constitutes, or may constitute, material non-public information, (j) our Common Stock is DWAC eligible and not subject to a DTC “chill;” and (k) for each trading day in a period of 10 consecutive trading days prior to the applicable date in question (A) the daily dollar trading volume for our Common Stock on the principal trading market exceeds $75,000 per trading day and (B) the weighted average stock price for our Common Stock on the principal trading market is above 50% of the closing stock price on August 3, 2017 (as adjusted for all stock splits stock dividends, stock combinations, reclassifications and other transactions).

We have the right at any time to redeem all, but not less than all, of the total outstanding amount of principal amount then remaining under the Convertible Notes at a price equal to 120% of such principal amount.

| 7 |

| Table of Contents |

Warrants

In connection with the Purchase Agreement, the Company issued the Purchasers five-year Warrants to purchase an aggregate of 55,872,837 shares of our Common Stock at a purchase price of $0.09 per share, exercisable for cash or on a cashless basis. In addition, in connection with the debt converted in the Exchange Offering, one Purchaser was issued five-year Warrants to acquire 3,200,000 shares of our Common Stock at a purchase price of $0.0825 per share, exercisable for cash or on a cashless basis. The Warrants contain customary anti-dilution provisions, including full-ratchet anti-dilution adjustments in the event of certain dilutive issuances (that adjust both exercise price and share amounts to be issued upon exercise).

Security Agreements and Guarantee

In connection with the issuance of the Convertible Notes, the Company and its wholly-owned subsidiary Oncolix, pledged substantially all of their assets as security and collateral for the Convertible Notes, including all intellectual property of Oncolix and the shares of capital stock of Oncolix owned by the Company. Additionally, Oncolix guaranteed the obligations of the Convertible Notes.

Registration Rights Agreement

In connection with the execution of the Purchase Agreement, the Company and the Purchasers also entered into the Registration Rights Agreement. Pursuant to the Registration Rights Agreement, the Company has agreed to file an initial registration statement (“Initial Registration Statement”) with the SEC to register the resale of all shares of Common Stock issuable under conversion of the Convertible Notes and upon exercise of the Warrants and any securities issued or then issuable upon any stock split, dividend or other distribution, recapitalization or similar event with respect to the foregoing (the “Registrable Shares”) on or prior to September 2, 2017, and have it declared effective at the earlier of (i) the 90th calendar day after August 3, 2017 (120th calendar day after August 3, 2017 in the event that the registration statement is subject to review by the SEC) and (ii) the 5th business day after the date the Company is notified by the SEC that the registration statement will not be reviewed or will not be subject to further review.

The Company also agreed to file additional registration statements to cover all of the Registrable Securities that are not covered by the Initial Registration Statement on or prior to 30 days following the date the Company first knows that such additional registration statement is required to be filed (the “Additional Registration Statements”) and have it declared effective no later than the earlier of (i) the 60th calendar day following the date the Company first knows that it is required to file such Additional Registration Statement and (ii) the 5th business day after the date the Company is notified by the SEC that the registration statement will not be reviewed or will not be subject to further review. If (i) the Initial Registration Statement is not declared effective on or before the 90th calendar day following the date of the Purchase Agreement (120th day in the event of a SEC review), (ii) any Additional Registration Statement is not declared effective on or before its effectiveness deadline, or (iii) any registration statement is declared effective by the SEC but shall thereafter cease to be effective for a period of time of 10 consecutive calendar days but not more than an aggregate of 15 calendar days in any one 12-month period (each such event, a “Non-Registration Event”), then the Company shall deliver to the Purchasers, as liquidated damages, an amount equal to ten percent of the outstanding principal amount of the Convertible Notes then held by the Purchasers for the first 30 days (or part thereof) and after such 30 days, an additional 10% of the outstanding principal amount of the Convertible Notes for a subsequent 30-day period (or part thereof); provided that the maximum amount of liquidated damages shall not exceed 18% of the aggregate outstanding principal amount of the Convertible Notes. The Company may pay the liquidated damages in cash or through the issuance of shares of Common Stock (valued at 75% of the average of the five lowest closing bid prices for the twenty consecutive trading days prior to the Non-Registration Event) provided the Equity Conditions are met. In addition, if there is not an effective registration statement covering all the Registrable Securities and the Company elects to register the issuance or resale of other Company securities, the Company is required to include such Registrable Securities in such registration statement filed with the SEC.

The Company also agreed, among other things, to indemnify the Purchasers from certain liabilities and fees and expenses of the Purchasers incident to the Company’s obligations under the Registration Rights Agreement, including certain liabilities under the Securities Act. The Purchasers have agreed to indemnify and hold harmless the Company and each of its directors, officers and persons who control the Company against certain liabilities that may be based upon written information furnished by the Purchasers to the Company for inclusion in a registration statement pursuant to the Registration Rights Agreement, including certain liabilities under the Securities Act.

| 8 |

| Table of Contents |

Other Terms

The Purchase Agreement contains customary representations, warranties and covenants by, among and for the benefit of the parties. Additionally, the Purchase Agreement provides for (i) liquidated damages in the event of the failure to timely (A) deliver our Common Stock upon conversion of the Notes or issuance of shares upon exercise of Warrants and (B) remove restrictive legends, (ii) a right to participate in future financings, (iii) a most-favored nation’s right with respect to future financings, and (iv) certain “down-round” protection. The Purchase Agreement also provides for indemnification of the Purchasers and its affiliates in the event that the Purchasers incur losses, liabilities, obligations, claims, contingencies, damages, costs and expenses related to the Company’s breach of any of its representations, warranties or covenants under the Purchase Agreement.

The officers and directors of the Company, Michael T. Redman and J. Donald Payne, as well as GHC Research Development Corporation (“GHC”), agreed for a period of fifteen months from August 3, 2017, not to sell, assign or otherwise transfer any of their shares of our Common Stock or our Series A Preferred Stock.

At no time will the Purchasers be entitled to convert any portion of the Convertible Notes or exercise any portion of the Warrants, to the extent that after such conversion and/or exercise, the Purchasers (together with their affiliates) would beneficially own more than 4.99% of the outstanding shares of our Common Stock as of such date, which limit may be increased to 9.99% at the election of the Purchasers but no greater than 9.99%.

Risk Factors

Investing in our Common Stock involves risks that include the speculative nature of the biopharmaceutical business, competition, need for additional capital and other material factors. You should read carefully the section of this prospectus entitled “Risk Factors” beginning on page 10 for an explanation of these risks before investing in our Common Stock. In particular, the following considerations may offset our competitive strengths or have a negative effect on our strategy or operating activities, which could cause a decrease in the price of our Common Stock and a loss of all or part of your investment:

· Our business is difficult to evaluate because of our limited operating history; · We have incurred net losses from inception and expect to continue to incur net losses; · We have no product revenue and don’t expect product revenue in the near future; · We need to raise capital to continue to fund working capital obligations; · The terms of our Convertible Notes may adversely affect our ability to raise additional capital; · The biopharmaceutical industry is intensely competitive; · Regulations that govern the biopharmaceutical industry are significant; · Our intellectual property rights may be challenged; · The selling security holders’ ability to sell a significant percentage of our Common Stock from time to time under this prospectus may have an adverse effect on the public market of our Common Stock; and · We may be unable to repay or redeem the non-converted portion of the Convertible Notes when due.

About This Offering

| Common Stock offered by selling security holder |

| 126,730,191 shares(1) beneficially held by the selling security holders. The selling security holders may from time to time sell some, all or none of the shares of Common Stock pursuant to which this prospectus is a part. |

|

|

|

|

| Shares outstanding prior to the offering |

| 103,536,703 shares of Company Common Stock and 63,038,284 shares of Series A Preferred Stock convertible into 63,038,284 shares of Company Common Stock, aggregating 166,574,987 voting capital stock issued and outstanding as of August 28, 2017. In addition, the selling security holders must convert indebtedness or exercise Warrants for the 126,730,191 shares beneficially held in order to sell the shares of Common Stock offered hereby. |

|

|

|

|

| Shares to be outstanding after the offering |

| 230,266,894 shares of Company Common Stock and 63,038,284 shares of Series A Preferred Stock convertible into 63,038,284 shares of Company Common Stock, aggregating 293,305,178 voting capital stock issued and outstanding as of August 28, 2017(2) |

|

|

|

|

| Use of proceeds |

| The selling security holder will receive all of the proceeds from the sale of shares of our Common Stock. We will not receive any proceeds from the sale of the Common Stock. |

|

|

|

|

| Risk Factors |

| The securities offered hereby involve a high degree of risk. See “Risk Factors.” |

|

|

| |

| Stock symbol |

| AEPP |

| 9 |

| Table of Contents |

__________

(1) The shares of Common Stock are comprised of the following: (i) with respect to the shares underlying the Convertible Notes, (A) 55,872,837 shares of Common Stock issuable upon conversion of the principal amount of $4,190,463 based on a conversion price of $0.075 per share pursuant to the monthly redemption payment schedule assuming timely payment and no default either in principal or interest payment obligations, (B) 5,633,847 shares of Common Stock issuable as payment of interest in lieu of cash, assuming timely payment of all interest obligations and no default either in principal or interest payment obligations, based on an interest conversion rate of $0.75 per share, and (C) 6,150,670 shares of Common Stock as a buffer in the event the monthly redemption payment or interest payment calculations are based on the lower of $0.075 per share and 75% of the average of the five lowest closing bid prices for the twenty consecutive trading days prior to such determination date; and (ii) 59,072,837 shares of Common Stock underlying the Warrants. (2) Assuming all shares offered hereby are issued upon conversion of the Convertible Notes and exercise of the Warrants as of the date of the prospectus.

Corporate Address

Our executive offices are located at 14405 Walters Road, Suite 780, Houston, Texas 77014, and our telephone number is (281) 402-3167.

This investment has a high degree of risk. Before you invest you should carefully consider the risks and uncertainties described below and the other information in this prospectus. If any of the following risks actually occur, our business, operating results and financial condition could be harmed and the value of our stock could go down. This means you could lose all or a part of your investment.

Risks Related to Our Financial Position and Capital Needs

We have incurred net losses since our inception and anticipate that we will continue to incur net losses for the foreseeable future.

Investment in biopharmaceutical product development is highly speculative because it entails substantial upfront capital expenditures and significant risk that any potential product candidate will fail to demonstrate adequate efficacy or an acceptable safety profile, gain regulatory approval or be commercially viable. We are a clinical stage biopharmaceutical company with limited operating history. We have not completed our Phase I clinical trials and no assurances can be given that when, if ever, we will be able to. As a result we have not yet demonstrated an ability to complete clinical trials, obtain regulatory approvals, manufacture a commercial-scale drug or arrange for a third party to do so on our behalf, or conduct sales and marketing activities necessary for successful commercialization. We may encounter unforeseen expenses, difficulties, complications, delays and other known and unknown difficulties in achieving our business objectives. We have no product approved for commercial sale and have not generated any product revenues to date, and we continue to incur significant research and development and other expenses related to our ongoing operations and clinical development of Prolanta™. As a result, we are not and have never been profitable and have incurred losses in each period since our commencement of operations in 2007. We will need to raise substantial additional capital to fund operations and the failure to obtain capital may cause us to curtail or cease operations.

For the year ended December 31, 2016, we reported a net loss of $1.4 million; and as of December 31, 2016, we had an accumulated deficit of $19.0 million. For the six months ended June 30, 2017, we reported a net loss of $1.3 million; and as of June 30, 2017, we had an accumulated deficit of $20.3 million. We expect to continue to incur significant losses for the foreseeable future, and we expect these losses to increase as we continue our research and development of, and seek regulatory approvals for, Prolanta™. We may also encounter unforeseen expenses, difficulties, complications, delays and other unknown factors that may adversely affect our business. The size of our future net losses will depend, in part, on the rate of future growth of our expenses and our ability to generate revenues, if any. Our prior losses and expected future losses have had and will continue to have an adverse effect on our stockholders’ equity and working capital.

We currently have no source of product revenue and may never achieve or maintain profitability.

Our ability to generate product revenue and become profitable depends upon our ability to successfully commercialize our sole product, Prolanta™. We do not anticipate generating revenue from the sale of Prolanta™ for the foreseeable future. Our ability to generate future product revenue also depends on a number of additional factors, including, but not limited to, our ability to:

· successfully complete the research and clinical development of, and receive regulatory approval for, Prolanta™;

| 10 |

| Table of Contents |

· launch, commercialize and achieve market acceptance of Prolanta™, and if launched independently, successfully establish a sales, marketing and distribution infrastructure; · continue to build a portfolio of product candidates through the acquisition or in-license of products, product candidates or technologies; · initiate preclinical and clinical trials for any additional product candidates that we may pursue in the future; · establish and maintain supplier and manufacturing relationships with third parties, and ensure adequate and legally compliant manufacturing of bulk drug substances and drug products to maintain that supply; · obtain coverage and adequate product reimbursement from third-party payors, including government payors; · establish, maintain, expand and protect our intellectual property rights; and · attract, hire and retain additional qualified personnel.

In addition, because of the numerous risks and uncertainties associated with drug development, we are unable to predict the timing or amount of increased expenses, and if or when we will achieve or maintain profitability. In addition, our expenses could increase beyond expectations if we decide to or are required by the FDA or foreign regulatory authorities to perform studies or trials in addition to those that we currently anticipate. Even if we complete the development and regulatory processes described above, we anticipate incurring significant costs associated with launching and commercializing Prolanta™. We will need to raise substantial additional capital to fund operations and the failure to obtain capital may cause us to curtail or cease operations.

Even if we generate revenues from the sale of Prolanta™, we may not become profitable and may need to obtain additional funding to continue operations or acquire additional products that will require additional funding to develop them. If we fail to become profitable or do not sustain profitability on a continuing basis, then we may be unable to continue our operations at planned levels and be forced to reduce our operations or curtail operations.

We have limited cash on hand, and we will need substantial additional funding and if we are unable to raise additional capital when needed, we would be forced to delay, reduce or eliminate our clinical trials and curtail operations.

The Company believes that it has sufficient cash on hand to fund its operations through calendar 2017, and into early 2018. The exact duration that our liquidity will be sufficient to fund operations depends upon many factors, some of which are outside the control of the Company, and is difficult to predict. We expect our research and development expenses to increase in connection with our ongoing activities relating to Prolanta™, particularly as we focus on and proceed with our clinical trials for our Prolanta™ product. In addition, our expenses could increase beyond current expectations if applicable regulatory authorities, including the FDA, require that we perform studies in addition to those that we currently anticipate, assuming we successfully complete our Phase I clinical trials, commence and complete our proposed Phase II clinical trials. We currently estimate that we require approximately $2 million to complete the Phase I clinical trial, depending on the cost and availability of drug supplies. We will still need substantial additional capital in the future in order to complete the clinical trials and obtain regulatory approval of Prolanta™. Accordingly, we will need to raise additional capital to fund future operations and we expect to finance future cash needs through best-efforts public or private equity offerings, debt financings or corporate collaboration and licensing arrangements. Such funding may not be available on favorable terms, if at all. Failure to raise additional capital could cause us to curtail or cease operations and result in the loss of your investment in our Common Stock.

If adequate funds are not available, we may be required to delay, reduce the scope of, or eliminate one or more of our research or development programs or our commercialization efforts. To the extent that we raise additional funds by issuing equity securities, our stockholders may experience additional significant dilution, and debt financing, if available, may involve restrictive covenants. To the extent that we raise additional funds through collaboration and licensing arrangements, it may be necessary to relinquish some rights to our technologies or our product candidates or to grant licenses on terms that may not be favorable to us. We may seek to access the public or private capital markets whenever conditions are favorable, even if we do not have an immediate need for additional capital at that time.

Our forecast of the period of time through which our current capital will be adequate to support our operations is a forward-looking statement and involves risks and uncertainties, and actual results could vary as a result of a number of factors. We have based this estimate on assumptions that may prove to be wrong, and we could utilize our available capital resources sooner than we currently expect.

The terms of the Convertible Notes will restrict our operating flexibility.

Pursuant to the Purchase Agreement, the Company issued Convertible Notes to the Purchasers in an aggregate principal amount of $4,190,463 at a 15% discount. The Convertible Notes bear interest at a rate of 10% per annum, payable quarterly on November 1, 2017, February 1, 2018, and May 1, 2018 and thereafter, on a monthly basis until maturity. The interest is payable in cash or, at our option, subject to compliance with the Equity Conditions, in fully tradable Common Stock at the lesser of the then conversion price or a 25% discount to the average of the five lowest closing bid prices for the twenty trading days prior to the interest payment date. The final maturity of the Convertible Notes is November 1, 2018, but commencing on May 1, 2018 and on the first day of each month thereafter until maturity, we are required to redeem an amount of the Convertible Notes equal to 1/7th of the original principal amount, plus 10% of such monthly redemption amount. The principal payments shall be made in cash or, subject to the satisfaction of Equity Conditions, in our Common Stock valued at the lesser of the then conversion price or a 25% discount to the average of the five lowest closing bid prices for the twenty trading days prior to the amortization date. Accordingly, in the event that the Company issues shares of its Common Stock to pay principal and/or interest on the Convertible Notes, such payment through the issuance of shares of Common Stock may be dilutive to the Company. Moreover, satisfaction of the Equity Conditions may be difficult; therefore investors should assume that the Company will be required to utilize cash for its payment obligations pursuant to the Convertible Notes. The Company will need to raise additional capital to fund principal and interest obligations of the Convertible Notes and there is no assurance that it will be successful in this endeavor. Failure to raise additional capital could cause a default in the Convertible Notes and result in a foreclosure by the Convertible Note holders on substantially all of our assets.

| 11 |

| Table of Contents |

The Convertible Notes are convertible at the option of the Purchasers at a conversion price equal to the lesser of (i) $0.075 per share of Common Stock, (ii) 75% of the 10-day average closing bid price of our Common Stock for the period prior to the filing of a registration statement as described below (subject to a floor of $0.0375 per share), and (iii) 75% of the 10-day average closing bid price of our Common Stock for the 10-day period prior to the effective date of the registration statement (subject to a floor of $0.0375 per share). The Convertible Notes contain customary anti-dilution protection, including full-ratchet anti-dilution adjustments in the event of certain dilutive issuances (that adjust both conversion price and share amounts to be issued upon conversion). Accordingly, the conversion price of the Convertible Notes is subject to future market prices of the Company Common Stock (of which the Company has no control) as well as the price of future Common Stock issuances (either in connection with any potential financings or in lieu of cash for services to be rendered) which could result in the conversion price being further adjusted to a price lower than the floor of $0.0375 per share with additional shares being issued upon conversion per the anti-dilution provisions. These provisions may make it more difficult and more expensive for us to raise capital in the future and may result in further dilution to shareholders.

In the event of a closing of an $8 million financing in connection with a change in listing of our Common Stock to Nasdaq or the NYSE, the Convertible Notes shall be subject to mandatory conversion into our Common Stock at a 30% discount to the offering price. There can be no assurance that the Company will be able to satisfy initial listing requirements of the Nasdaq or NYSE. We shall be required to offer to prepay in cash the aggregate principal amount of the Convertible Notes at 120% of the principal amount thereof plus any unpaid accrued interest to the date of repayment, at maturity, on the sale of substantially all of our assets, upon a change of control, upon a qualified offering, or upon a “fundamental transaction”; in such an event, the Purchasers shall have the right to convert the Convertible Notes prior to the date of any such prepayment.

The Convertible Notes contain standard negative covenants customary for transactions of this type. These negative covenants may preclude or restrict the ability of the Company to effect future debt and convertible debt financings without the prior approval of holders of the majority principal amount of the Convertible Notes. The events of default are also customary for transactions of this type, including default in timely payment of principal or interest, failure to observe or perform any covenant or agreement contained in the Convertible Note and Transaction Documents, the commencement of bankruptcy or insolvency proceedings, failure to timely deliver conversion shares underlying the Convertible Notes, failure to timely file Exchange Act filings, and failure to satisfy certain Equity Conditions. In the event that the Company triggers one of these event of default provisions, the holders of the Convertible Notes have the ability to foreclose on substantially all of the assets of the Company which would result in the cessation of our operations.

Equity Conditions mean, during the period in question, (a) we shall have duly honored all conversions and redemptions of the Convertible Notes, (b) we shall have complied with all conversion and other provisions of the Convertible Notes and shall have paid all liquidated damages and other amounts owing in respect of this Convertible Note, (c)(A) there is an effective registration statement pursuant to which the holder is permitted to utilize the prospectus thereunder to resell at least the number of shares of Common Stock issuable pursuant to the Transaction Documents at such time or (B) all of the underlying shares may be resold pursuant to Rule 144 without volume or manner-of-sale restrictions or current public information requirements, (d) our Common Stock is trading on a trading market, (e) there is a sufficient number of authorized but unissued and otherwise unreserved shares of AEPP Common Stock for the issuance of five times all of the shares issuable pursuant to the Convertible Notes and Warrants, (f) there is no existing event of default or no existing event which, with the passage of time or the giving of notice, would constitute an event of default, (g) the issuance of the shares in question would not violate the beneficial ownership limitations in the Transaction Documents, (h) there has been no public announcement of a pending or proposed fundamental transaction or change of control transaction that has not been consummated, (i) the holder is not in possession of any information provided by the Company that constitutes, or may constitute, material non-public information, (j) our Common Stock is DWAC eligible and not subject to a DTC “chill;” and (k) for each trading day in a period of 10 consecutive trading days prior to the applicable date in question (A) the daily dollar trading volume for our Common Stock on the principal trading market exceeds $75,000 per trading day and (B) the weighted average stock price for our Common Stock on the principal trading market is above 50% of the closing stock price on August 3, 2017 (as adjusted for all stock splits stock dividends, stock combinations, reclassifications and other transactions). The satisfaction of the Equity Conditions may be difficult to meet as many of these conditions involve events outside of the Company’s control. The failure to meet these Equity Conditions precludes the Company’s ability to utilize its shares of Common Stock to satisfy payment obligations pursuant to the Convertible Notes.

We have the right at any time to redeem all, but not less than all, of the total outstanding amount of principal amount then remaining under the Convertible Notes at a price equal to 120% of such principal amount.

| 12 |

| Table of Contents |

Terms of our existing $4,190,463 senior debt and warrants may impact our ability to obtain additional financing.

The Convertible Notes are senior secured obligations of the Company. The terms of the Convertible Notes preclude the Company from obtaining any additional debt senior to or pari passu with the Convertible Notes. Additionally, the Convertible Notes are secured by substantially all of our assets and guaranteed by Oncolix. In the event of our default with respect to the Convertible Notes, the holders have the right to foreclose on substantially all of our assets which likely would result in us ceasing operations. The terms of the Convertible Notes may adversely affect the Company’s ability to obtain additional debt or equity financing to fund additional working capital needs, including the payment obligations of the Convertible Notes.

Registration Rights Agreement will affect future capital raises.

The Registration Rights Agreement entered into in connection with the issuance of the Convertible Notes requires the Company to register the resale of all the underlying shares of our Common Stock issuable upon conversion of the Convertible Notes and exercise of the Warrants. The Company has filed this registration statement, and intends to use its best efforts to file any additional registration statements, to register the resale of these underlying shares under the Securities Act as soon as practical. The availability of these shares for sale in the public markets will likely have a depressive effect on any market price of our Common Stock. The Registration Rights Agreement contains liquidated damage provisions in the event that the Company fails to timely comply with the registration requirements therein. Additionally, the registration obligations may adversely impact our ability to issue additional equity or convertible debt securities to fund additional working capital needs, including the payment obligations of the Convertible Notes.

Our ability to use our net operating loss carryforwards and certain other tax attributes may be limited.

We have incurred substantial losses during our history. We do not expect to become profitable in the near future, and we may never achieve profitability. Unused losses generally are available to be carried forward to offset future taxable income, if any, until such unused losses expire. Under Sections 382 and 383 of the Internal Revenue Code of 1986, as amended, if a corporation undergoes an “ownership change,” generally defined as a greater than 50% change (by value) in its equity ownership over a three-year period, the corporation’s ability to use its pre-change net operating loss carryforwards, or NOLs, and other pre-change tax attributes (such as research tax credits) to offset its post-change taxable income or taxes may be limited. Our largest stockholder, GHC, is considering a reorganization that would limit our ability to utilize certain tax attributes. As a result, our ability to use our pre-change NOLs to offset U.S. federal taxable income may be subject to limitations, which could potentially result in increased future tax liability to us.

The current economic climate and legislative and regulatory changes in the U.S. and internationally creates uncertainties for the Company.

The uncertain economic climate in the U.S. and internationally may, therefore, have a material adverse effect on the healthcare industry in general and the Company in particular. In addition, proposed healthcare legislation in the United States, and the uncertainty of its future regulatory framework, may have a substantial impact on the Company and its operations. The Company cannot predict at this time what the potential impact may be or whether the effects on the Company will be positive or negative. If the Company suffers adverse effects it could cause the Company to fail to meet, or face delays in meeting, its marketing and sales objectives. Any such failures or delays will create additional financial uncertainties and difficulties for the Company.

We face significant competition from other pharmaceutical and biotechnology companies and they or others may also discover, develop or commercialize products before or more successfully than we do.

The development and commercialization of a drug candidate is highly competitive. We face competition with respect to our current product candidate, and will face competition with respect to any product candidates that we may seek to develop or commercialize in the future, from major pharmaceutical companies, specialty pharmaceutical companies, and biotechnology companies worldwide. We have competitors many of which have substantially greater name recognition, commercial infrastructure and financial, technical and personnel resources than we have. Established competitors may invest heavily to quickly discover and develop products that could make our products obsolete or uneconomical. Any new product that competes with an approved product may need to demonstrate compelling advantages in efficacy, cost, convenience, tolerability and safety to be commercially successful. Other competitive factors, including generic competition, could force us to lower prices or could result in reduced sales. In addition, new products developed by others could emerge as competitors to our products. If we are not able to compete effectively against our current and future competitors, our business will not grow and our financial condition and operations will suffer.

| 13 |

| Table of Contents |

There can be no assurance that Prolanta™ will successfully complete its Phase 1 and later stage clinical trials.

There can be no assurance that we will be able to successfully complete such Phase 1 clinical trials or if so, that we will obtain regulatory approval for our later stage clinical trials and/or successfully complete such later stage clinical trials and/or obtain all required regulatory approvals. Moreover, no assurances can be given we will be able to commercialize Prolanta™ or that we will ever generate sustained revenue or achieve profitability. Our ability to operate profitably in the future will depend upon, among other items, our ability to (i) successfully complete all required clinical trials for Prolanta™, (ii) obtain regulatory approval from the FDA or other regulatory agencies for Prolanta™, (iii) scale up our business and operational structure, (iv) commercialize and market Prolanta™, and (v) successfully gain market acceptance of Prolanta™. There can be no assurance that we will successfully achieve any of the foregoing. Our prospects must be considered in light of the numerous risks, expenses, delays and difficulties frequently encountered in the intensely competitive and high risk markets in which Prolanta™ is intended to compete. If we are unable to develop and commercialize Prolanta™, we will not achieve profitability. Even if we do achieve profitability, we may not be able to sustain or increase profitability.

We will need substantial additional funding and if we are unable to raise capital when needed, we would be forced to delay, reduce or eliminate our product development and commercialization plans.

We expect our research and development expenses to increase in connection with our ongoing activities. In addition, our expenses could increase beyond expectations if applicable regulatory authorities, including the FDA, require that we perform studies in addition to those that we currently anticipate, in which case the timing of any potential product approval may be delayed. We will still need substantial additional capital in the future in order to complete the development and commercialization of Prolanta™. Until we can generate a sufficient amount of product revenue, if ever, we expect to finance future cash needs through public or private equity offerings, debt financings or corporate collaboration and licensing arrangements. Such funding, if needed, may not be available on favorable terms, if at all. Failure to obtain additional capital could cause us to curtail or cease operations.

If adequate funds are not available, we may be required to delay, reduce the scope of, or eliminate one or more of our research or development programs or our commercialization efforts. To the extent that we raise additional funds by issuing equity securities, our stockholders may experience additional significant dilution, and debt financing, if available, may involve restrictive covenants. To the extent that we raise additional funds through collaboration and licensing arrangements, it may be necessary to relinquish some rights to our technologies or our product candidates or to grant licenses on terms that may not be favorable to us.

We contract with a third party for the manufacture of Prolanta™ for clinical trials and we expect to continue to do so in connection with the commercialization of Prolanta™ and for clinical trials and commercialization of any other product candidates that we develop. Any failure by the Manufacturer to produce acceptable supplies for us or to comply with FDA or comparable foreign regulations may delay or impair our ability to initiate or complete our clinical trials, obtain regulatory approvals to market, or sell any resulting product.

We do not currently have nor do we plan to build the internal infrastructure or capability to manufacture Prolanta™ or any future product candidates for use in the conduct of our clinical trials or for commercial supply. We currently rely on a third-party contract manufacturer to manufacture clinical supplies of Prolanta™. We expect to rely upon this manufacturer or another contract manufacturer to manufacture clinical trial supplies and commercial quantities of Prolanta™ if and when we receive approval for marketing by applicable regulatory authorities. Our contract manufacturer subcontracts to other third-party manufacturers certain aspects of the manufacturing of Prolanta™, including the filling of vials and the lyophilization (freeze-drying) of the final drug product.

Reliance on a contract manufacturer to manufacture Prolanta™ entails risks, including:

· manufacturing delays if the contract manufacturer gives greater priority to the supply of other products over Prolanta™; · manufacturing delays or increased costs if the contract manufacturer does not satisfactorily perform according to the terms of any agreement between us; · the failure of the contract manufacturer to comply with applicable regulatory requirements; · the possible misappropriation of our proprietary information, including our trade secrets and know-how.

| 14 |

| Table of Contents |

We are currently conducting a Phase I clinical trial of Prolanta™ for the treatment of ovarian cancer. The first of three dosing groups has been completed, and we must obtain additional supplies of Prolanta™ to complete this and future clinical trials. We will seek these drug supplies from our contract manufacturer. We also intend to pursue alternative sources of manufacturing to evaluate the feasibility and cost of other suppliers.

In the event we develop or acquire additional product candidates, we expect to make similar arrangements with a other third-party contract manufacturers for such product candidates, and these arrangements will entail similar risks.

If we are unable to make satisfactory arrangements with contract manufacturers, we may be required to alter our plans and we may have to establish our own manufacturing capabilities. This would require substantial additional funds, personnel and other resources to build, lease or operate any manufacturing facility.

Third-party manufacturers are required to comply with Current Good Manufacturing Practices (“cGMPs”) and similar regulatory requirements outside the United States. Facilities used by our contract manufacturer must be approved by the FDA before potential approval of Prolanta™. Similar regulations apply for use or sale in foreign countries. We do not control the manufacturing process and are completely dependent on contract manufacturers for compliance with the applicable regulatory requirements for the manufacture of Prolanta™. If a contract manufacturer cannot successfully manufacture material that conforms to the strict regulatory requirements of the FDA and any applicable foreign regulatory authority, they will not be able to secure the applicable approval for their manufacturing facilities. If these facilities are not approved for commercial manufacture, we may need to find alternative manufacturing facilities, which could result in delays in obtaining approval for the applicable product candidate as well as substantial additional expense.

In addition, contract manufacturers are subject to ongoing periodic unannounced inspections by the FDA and corresponding state and foreign agencies for compliance with cGMPs and similar regulatory requirements. Failure by contract manufacturers to comply with applicable cGMPs or other regulatory requirements could result in sanctions being imposed on us, including fines, injunctions, civil penalties, delays, suspensions or withdrawals of approvals, operating restrictions, interruptions in supply and criminal prosecutions, any of which could significantly and adversely affect supplies of our Prolanta™ and have a material adverse impact on our business, financial condition and results of operations.

Our current and anticipated future dependence upon others for the manufacture of Prolanta™ and any other product candidate that we develop may adversely affect our future profit margins and our ability to commercialize any products that receive marketing approval on a timely and competitive basis.

If clinical trials of Prolanta™ or of any future product candidate that we advance to clinical trials fail to demonstrate safety and efficacy to the satisfaction of the FDA or comparable foreign regulatory authorities or do not otherwise produce favorable results, we may incur additional costs or experience delays in completing, or ultimately be unable to complete, the development and commercialization of Prolanta™ or any other product candidate.

We are not permitted to commercialize, market, promote, or sell Prolanta™ in the United States without obtaining marketing approval from the FDA or in other countries without obtaining approvals from comparable foreign regulatory authorities, such as the EMA, and we may never receive such approvals. We must complete extensive clinical trials to demonstrate the safety and efficacy of Prolanta™ in humans before we will be able to obtain these approvals. Clinical testing is expensive, difficult to design and implement, can take many years to complete and is inherently uncertain as to outcome. We have not previously submitted an NDA to the FDA or similar drug approval filings to comparable foreign regulatory authorities for Prolanta™.

The clinical development of Prolanta™ and any other product candidates is susceptible to the risk of failure inherent at any stage of drug development, including failure to achieve efficacy in a trial or across a broad population of patients, the occurrence of severe adverse events, failure to comply with protocols or applicable regulatory requirements, and determination by the FDA or any comparable foreign regulatory authority that a drug product is not approvable. The outcome of preclinical studies and any early clinical trial may not be predictive of the success of later clinical trials, and interim results of a clinical trial do not necessarily predict final results. For example, although Prolanta™ demonstrated an acceptable safety profile and efficacy in preclinical studies, we may nonetheless fail to demonstrate the safety or tolerability of Prolanta™ in our Phase 1 clinical trial, and may fail to demonstrate efficacy in any of our clinical trials.

In addition, preclinical and clinical data are often susceptible to varying interpretations and analyses. Many companies that believed their product candidates performed satisfactorily in preclinical studies and clinical trials have nonetheless failed to obtain marketing approval for the product candidates. Even if we believe that the results of our clinical trials warrant marketing approval, the FDA or comparable foreign regulatory authorities may disagree and may not grant marketing approval of our product candidates.

| 15 |

| Table of Contents |

In some instances, there can be significant variability in safety and/or efficacy results between different trials of the same product candidate due to numerous factors, including changes in trial procedures set forth in protocols, differences in the size and type of the patient populations, adherence to the dosing regimen and other trial protocols and the rate of dropout among clinical trial participants. We cannot assure you that any of the clinical trials that we may conduct will demonstrate consistent or adequate efficacy and safety to obtain regulatory approval to market our product candidates.

We may experience numerous unforeseen events during, or as a result of, clinical trials that could delay or prevent us from obtaining regulatory approval for Prolanta™, including:

· clinical trials of our product candidates may produce unfavorable or inconclusive results; · we may decide, or regulators may require us, to conduct additional clinical trials or abandon product development programs; · the number of patients required for clinical trials may be larger than we anticipate, enrollment in these clinical trials may be slower than we anticipate or participants may drop out of these clinical trials at a higher rate than we anticipate; · our third-party contractors, including the manufacturer for Prolanta™ or the CROs conducting clinical trials on our behalf, may fail to comply with regulatory requirements or meet their contractual obligations to us in a timely manner, or at all; · regulators or institutional review boards may not authorize us or our investigators to commence a clinical trial or conduct a clinical trial at a prospective trial site; · we may have delays in reaching or fail to reach agreement on acceptable clinical trial contracts or clinical trial protocols with prospective trial sites; · we may have to suspend or terminate clinical trials of Prolanta™ for various reasons, including lack of capital, a finding that the participants are being exposed to unacceptable health risks, undesirable side effects or other unexpected characteristics of our product candidate; · regulators or institutional review boards may require that we or our investigators suspend or terminate clinical research for various reasons, including noncompliance with regulatory requirements or a finding that the participants are being exposed to unacceptable health risks, undesirable side effects or other unexpected characteristics of the product candidate; · the FDA or comparable foreign regulatory authorities may fail to approve the manufacturing processes or facilities of our third-party manufacturer; · the supply or quality of Prolanta™ or other materials necessary to conduct clinical trials may be insufficient or inadequate; and · the approval policies or regulations of the FDA or comparable foreign regulatory authorities may significantly change in a manner rendering our clinical data insufficient for approval

If we are required to conduct additional clinical trials or other testing of Prolanta™ beyond the trials and testing that we contemplate, if we are unable to successfully complete clinical trials of Prolanta™ or other testing, if the results of these trials or tests are unfavorable or are only modestly favorable or if there are safety concerns associated with Prolanta™, we may:

· be delayed in obtaining marketing approval for Prolanta™; · not obtain marketing approval at all; · obtain approval for indications or patient populations that are not as broad as intended or desired; obtain approval with labeling that includes significant use or distribution restrictions or significant safety warnings, including boxed warnings; · be subject to additional post-marketing testing or other requirements; · remove the product from the market after obtaining marketing approval; or · curtail operations.