Attached files

| file | filename |

|---|---|

| EX-32.0 - EXHIBIT 32.0 - ISTAR INC. | star-06302017xex320.htm |

| EX-31.0 - EXHIBIT 31.0 - ISTAR INC. | star-06302017xex310.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________________________________________________________

FORM 10-Q

(Mark One) | |

ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2017 | |

OR | |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to | |

Commission File No. 1-15371

_______________________________________________________________________________

iStar Inc.

(Exact name of registrant as specified in its charter)

Maryland (State or other jurisdiction of incorporation or organization) | 95-6881527 (I.R.S. Employer Identification Number) | |

1114 Avenue of the Americas, 39th Floor | ||

New York, NY (Address of principal executive offices) | 10036 (Zip code) | |

Registrant's telephone number, including area code: (212) 930-9400

_______________________________________________________________________________

Indicate by check mark whether the registrant: (i) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding twelve months (or for such shorter period that the registrant was required to file such reports); and (ii) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o | Emerging growth company o | ||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

As of August 3, 2017, there were 72,190,312 shares, $0.001 par value per share, of iStar Inc. common stock outstanding.

TABLE OF CONTENTS

Page | ||

PART I. CONSOLIDATED FINANCIAL INFORMATION

Item 1. Financial Statements

iStar Inc.

Consolidated Balance Sheets

(In thousands, except per share data)

As of | |||||||

June 30, 2017 (unaudited) | December 31, 2016 | ||||||

ASSETS | |||||||

Real estate | |||||||

Real estate, at cost | $ | 1,710,915 | $ | 1,740,893 | |||

Less: accumulated depreciation | (367,933 | ) | (353,619 | ) | |||

Real estate, net | 1,342,982 | 1,387,274 | |||||

Real estate available and held for sale | 68,045 | 237,531 | |||||

Total real estate | 1,411,027 | 1,624,805 | |||||

Land and development, net | 855,497 | 945,565 | |||||

Loans receivable and other lending investments, net | 1,170,565 | 1,450,439 | |||||

Other investments | 276,821 | 214,406 | |||||

Cash and cash equivalents | 954,279 | 328,744 | |||||

Accrued interest and operating lease income receivable, net | 10,501 | 11,254 | |||||

Deferred operating lease income receivable, net | 88,944 | 88,189 | |||||

Deferred expenses and other assets, net | 147,121 | 162,112 | |||||

Total assets | $ | 4,914,755 | $ | 4,825,514 | |||

LIABILITIES AND EQUITY | |||||||

Liabilities: | |||||||

Accounts payable, accrued expenses and other liabilities | $ | 230,259 | $ | 211,570 | |||

Loan participations payable, net | 107,442 | 159,321 | |||||

Debt obligations, net | 3,368,113 | 3,389,908 | |||||

Total liabilities | 3,705,814 | 3,760,799 | |||||

Commitments and contingencies (refer to Note 11) | — | — | |||||

Redeemable noncontrolling interests (refer to Note 5) | 3,585 | 5,031 | |||||

Equity: | |||||||

iStar Inc. shareholders' equity: | |||||||

Preferred Stock Series D, E, F, G and I, liquidation preference $25.00 per share (refer to Note 13) | 22 | 22 | |||||

Convertible Preferred Stock Series J, liquidation preference $50.00 per share (refer to Note 13) | 4 | 4 | |||||

Common Stock, $0.001 par value, 200,000 shares authorized, 72,190 and 72,042 shares issued and outstanding as of June 30, 2017 and December 31, 2016, respectively | 72 | 72 | |||||

Additional paid-in capital | 3,603,981 | 3,602,172 | |||||

Retained earnings (deficit) | (2,431,123 | ) | (2,581,488 | ) | |||

Accumulated other comprehensive income (loss) (refer to Note 13) | (3,678 | ) | (4,218 | ) | |||

Total iStar Inc. shareholders' equity | 1,169,278 | 1,016,564 | |||||

Noncontrolling interests | 36,078 | 43,120 | |||||

Total equity | 1,205,356 | 1,059,684 | |||||

Total liabilities and equity | $ | 4,914,755 | $ | 4,825,514 | |||

The accompanying notes are an integral part of the consolidated financial statements.

1

iStar Inc.

Consolidated Statements of Operations

(In thousands, except per share data)

(unaudited)

For the Three Months Ended June 30, | For the Six Months Ended June 30, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

Revenues: | |||||||||||||||

Operating lease income | $ | 47,002 | $ | 49,975 | $ | 94,349 | $ | 100,470 | |||||||

Interest income | 28,645 | 34,400 | 57,703 | 67,620 | |||||||||||

Other income | 139,510 | 10,096 | 151,374 | 21,636 | |||||||||||

Land development revenue | 132,710 | 27,888 | 152,760 | 42,835 | |||||||||||

Total revenues | 347,867 | 122,359 | 456,186 | 232,561 | |||||||||||

Costs and expenses: | |||||||||||||||

Interest expense | 48,807 | 56,047 | 99,952 | 113,068 | |||||||||||

Real estate expense | 34,684 | 35,328 | 70,274 | 69,572 | |||||||||||

Land development cost of sales | 122,466 | 17,262 | 138,376 | 28,838 | |||||||||||

Depreciation and amortization | 13,171 | 13,673 | 25,451 | 27,581 | |||||||||||

General and administrative | 27,218 | 19,665 | 52,392 | 42,768 | |||||||||||

(Recovery of) provision for loan losses | (600 | ) | 700 | (5,528 | ) | 2,206 | |||||||||

Impairment of assets | 10,284 | 3,012 | 14,696 | 3,012 | |||||||||||

Other expense | 16,276 | 3,182 | 18,145 | 3,922 | |||||||||||

Total costs and expenses | 272,306 | 148,869 | 413,758 | 290,967 | |||||||||||

Income (loss) before earnings from equity method investments and other items | 75,561 | (26,510 | ) | 42,428 | (58,406 | ) | |||||||||

Loss on early extinguishment of debt, net | (3,315 | ) | (1,457 | ) | (3,525 | ) | (1,582 | ) | |||||||

Earnings from equity method investments | 5,515 | 39,447 | 11,217 | 47,714 | |||||||||||

Income (loss) from continuing operations before income taxes | 77,761 | 11,480 | 50,120 | (12,274 | ) | ||||||||||

Income tax (expense) benefit | (1,644 | ) | 1,190 | (2,251 | ) | 1,604 | |||||||||

Income (loss) from continuing operations | 76,117 | 12,670 | 47,869 | (10,670 | ) | ||||||||||

Income from discontinued operations | 173 | 3,633 | 4,939 | 7,214 | |||||||||||

Gain from discontinued operations | 123,418 | — | 123,418 | — | |||||||||||

Income tax expense from discontinued operations | (4,545 | ) | — | (4,545 | ) | — | |||||||||

Income from sales of real estate(1) | 844 | 43,484 | 8,954 | 53,943 | |||||||||||

Net income | 196,007 | 59,787 | 180,635 | 50,487 | |||||||||||

Net (income) loss attributable to noncontrolling interests | (5,710 | ) | (8,825 | ) | (4,610 | ) | (7,883 | ) | |||||||

Net income attributable to iStar Inc. | 190,297 | 50,962 | 176,025 | 42,604 | |||||||||||

Preferred dividends | (12,830 | ) | (12,830 | ) | (25,660 | ) | (25,660 | ) | |||||||

Net (income) loss allocable to Participating Security holders(2) | — | (20 | ) | — | (11 | ) | |||||||||

Net income allocable to common shareholders | $ | 177,467 | $ | 38,112 | $ | 150,365 | $ | 16,933 | |||||||

Per common share data: | |||||||||||||||

Income attributable to iStar Inc. from continuing operations: | |||||||||||||||

Basic | $ | 0.81 | $ | 0.47 | $ | 0.37 | $ | 0.13 | |||||||

Diluted | $ | 0.69 | $ | 0.34 | $ | 0.35 | $ | 0.13 | |||||||

Net income attributable to iStar Inc.: | |||||||||||||||

Basic | $ | 2.46 | $ | 0.52 | $ | 2.09 | $ | 0.22 | |||||||

Diluted | $ | 2.04 | $ | 0.37 | $ | 1.76 | $ | 0.22 | |||||||

Weighted average number of common shares: | |||||||||||||||

Basic | 72,142 | 73,984 | 72,104 | 75,522 | |||||||||||

Diluted | 88,195 | 118,510 | 88,156 | 75,872 | |||||||||||

_______________________________________________________________________________

(1) | Income from sales of real estate represents gains from sales of real estate that do not qualify as discontinued operations. |

(2) | Participating Security holders are non-employee directors who hold common stock equivalents ("CSEs") and restricted stock awards granted under the Company's Long Term Incentive Plans that are eligible to participate in dividends (refer to Note 14 and Note 15). |

The accompanying notes are an integral part of the consolidated financial statements.

2

iStar Inc.

Consolidated Statements of Comprehensive Income (Loss)

(In thousands)

(unaudited)

For the Three Months Ended June 30, | For the Six Months Ended June 30, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

Net income | $ | 196,007 | $ | 59,787 | $ | 180,635 | $ | 50,487 | |||||||

Other comprehensive income (loss): | |||||||||||||||

Reclassification of (gains)/losses on cash flow hedges into earnings upon realization(1) | (313 | ) | 118 | (191 | ) | 375 | |||||||||

Unrealized gains/(losses) on available-for-sale securities | 583 | 446 | 566 | 465 | |||||||||||

Unrealized gains/(losses) on cash flow hedges | (146 | ) | (357 | ) | 394 | (1,319 | ) | ||||||||

Unrealized gains/(losses) on cumulative translation adjustment | 172 | 30 | (229 | ) | (10 | ) | |||||||||

Other comprehensive income (loss) | 296 | 237 | 540 | (489 | ) | ||||||||||

Comprehensive income | 196,303 | 60,024 | 181,175 | 49,998 | |||||||||||

Comprehensive (income) loss attributable to noncontrolling interests | (5,710 | ) | (8,825 | ) | (4,610 | ) | (7,883 | ) | |||||||

Comprehensive income attributable to iStar Inc. | $ | 190,593 | $ | 51,199 | $ | 176,565 | $ | 42,115 | |||||||

_______________________________________________________________________________

(1) | Reclassified to "Interest expense" in the Company's consolidated statements of operations are $30 and $60 for the three and six months ended June 30, 2017, respectively, and $23 and $183 for the three and six months ended June 30, 2016, respectively. Reclassified to "Earnings from equity method investments" in the Company's consolidated statements of operations are $70 and $164 for the three and six months ended June 30, 2017, respectively, and $95 and $192 for the three and six months ended June 30, 2016, respectively. |

The accompanying notes are an integral part of the consolidated financial statements.

3

iStar Inc.

Consolidated Statements of Changes in Equity

For the Six Months Ended June 30, 2017 and 2016

(In thousands)

(unaudited)

iStar Inc. Shareholders' Equity | ||||||||||||||||||||||||||||||||

Preferred Stock(1) | Preferred Stock Series J(1) | Common Stock at Par | Additional Paid-In Capital | Retained Earnings (Deficit) | Accumulated Other Comprehensive Income (Loss) | Noncontrolling Interests | Total Equity | |||||||||||||||||||||||||

Balance as of December 31, 2016 | $ | 22 | $ | 4 | $ | 72 | $ | 3,602,172 | $ | (2,581,488 | ) | $ | (4,218 | ) | $ | 43,120 | $ | 1,059,684 | ||||||||||||||

Dividends declared—preferred | — | — | — | — | (25,660 | ) | — | — | (25,660 | ) | ||||||||||||||||||||||

Issuance of stock/restricted stock unit amortization, net | — | — | — | 1,699 | — | — | — | 1,699 | ||||||||||||||||||||||||

Net income for the period(2) | — | — | — | — | 176,025 | — | 5,946 | 181,971 | ||||||||||||||||||||||||

Change in accumulated other comprehensive income (loss) | — | — | — | — | — | 540 | — | 540 | ||||||||||||||||||||||||

Change in additional paid in capital attributable to redeemable noncontrolling interest | — | — | — | 110 | — | — | — | 110 | ||||||||||||||||||||||||

Distributions to noncontrolling interest | — | — | — | — | — | — | (12,988 | ) | (12,988 | ) | ||||||||||||||||||||||

Balance as of June 30, 2017 | $ | 22 | $ | 4 | $ | 72 | $ | 3,603,981 | $ | (2,431,123 | ) | $ | (3,678 | ) | $ | 36,078 | $ | 1,205,356 | ||||||||||||||

Balance as of December 31, 2015 | $ | 22 | $ | 4 | $ | 81 | $ | 3,689,330 | $ | (2,625,474 | ) | $ | (4,851 | ) | $ | 42,218 | $ | 1,101,330 | ||||||||||||||

Dividends declared—preferred | — | — | — | — | (25,660 | ) | — | — | (25,660 | ) | ||||||||||||||||||||||

Issuance of stock/restricted stock unit amortization, net | — | — | — | 1,371 | — | — | — | 1,371 | ||||||||||||||||||||||||

Net income for the period(2) | — | — | — | — | 42,604 | — | 10,520 | 53,124 | ||||||||||||||||||||||||

Change in accumulated other comprehensive income (loss) | — | — | — | — | — | (489 | ) | — | (489 | ) | ||||||||||||||||||||||

Repurchase of stock | — | — | (9 | ) | (91,826 | ) | — | — | — | (91,835 | ) | |||||||||||||||||||||

Change in additional paid in capital attributable to redeemable noncontrolling interest | — | — | — | 460 | — | — | — | 460 | ||||||||||||||||||||||||

Contributions from noncontrolling interests | — | — | — | — | — | — | 444 | 444 | ||||||||||||||||||||||||

Change in noncontrolling interest(3) | — | — | — | — | — | — | (7,292 | ) | (7,292 | ) | ||||||||||||||||||||||

Balance as of June 30, 2016 | $ | 22 | $ | 4 | $ | 72 | $ | 3,599,335 | $ | (2,608,530 | ) | $ | (5,340 | ) | $ | 45,890 | $ | 1,031,453 | ||||||||||||||

_______________________________________________________________________________

(1) | Refer to Note 13 for details on the Company's Preferred Stock. |

(2) | For the six months ended June 30, 2017 and 2016, net income (loss) shown above excludes $(1,336) and $(2,637) of net loss attributable to redeemable noncontrolling interests. |

(3) | Includes a payment to acquire a noncontrolling interest (refer to Note 5). |

The accompanying notes are an integral part of the consolidated financial statements.

4

iStar Inc.

Consolidated Statements of Cash Flows

(In thousands)

(unaudited)

For the Six Months Ended June 30, | |||||||

2017 | 2016 | ||||||

Cash flows from operating activities: | |||||||

Net income | $ | 180,635 | $ | 50,487 | |||

Adjustments to reconcile net income to cash flows from operating activities: | |||||||

(Recovery of) provision for loan losses | (5,528 | ) | 2,206 | ||||

Impairment of assets | 14,696 | 3,012 | |||||

Depreciation and amortization | 26,352 | 29,182 | |||||

Non-cash expense for stock-based compensation | 9,796 | 6,211 | |||||

Amortization of discounts/premiums and deferred financing costs on debt obligations, net | 6,615 | 8,901 | |||||

Amortization of discounts/premiums on loans, net | (6,978 | ) | (7,237 | ) | |||

Deferred interest on loans, net | (1,290 | ) | 4,631 | ||||

Gain from discontinued operations | (123,418 | ) | — | ||||

Earnings from equity method investments | (11,217 | ) | (47,714 | ) | |||

Distributions from operations of other investments | 35,502 | 31,479 | |||||

Deferred operating lease income | (3,204 | ) | (4,993 | ) | |||

Income from sales of real estate | (9,462 | ) | (53,943 | ) | |||

Land development revenue in excess of cost of sales | (14,384 | ) | (13,997 | ) | |||

Loss on early extinguishment of debt, net | 775 | 1,582 | |||||

Debt discount on repayments of debt obligations | (5,745 | ) | (5,369 | ) | |||

Other operating activities, net | 9,770 | 2,651 | |||||

Changes in assets and liabilities: | |||||||

Changes in accrued interest and operating lease income receivable, net | 2,881 | 4,436 | |||||

Changes in deferred expenses and other assets, net | (6,821 | ) | 1,677 | ||||

Changes in accounts payable, accrued expenses and other liabilities | 3,941 | (13,052 | ) | ||||

Cash flows provided by operating activities | 102,916 | 150 | |||||

Cash flows from investing activities: | |||||||

Originations and fundings of loans receivable, net | (130,701 | ) | (158,262 | ) | |||

Capital expenditures on real estate assets | (16,346 | ) | (35,674 | ) | |||

Capital expenditures on land and development assets | (53,894 | ) | (58,961 | ) | |||

Acquisitions of real estate assets | — | (3,915 | ) | ||||

Repayments of and principal collections on loans receivable and other lending investments, net | 367,028 | 202,014 | |||||

Net proceeds from sales of real estate | 154,291 | 247,956 | |||||

Net proceeds from sales of land and development assets | 146,713 | 33,660 | |||||

Net proceeds from sales of other investments | — | 39,810 | |||||

Distributions from other investments | 11,275 | 8,632 | |||||

Contributions to other investments | (139,139 | ) | (8,283 | ) | |||

Changes in restricted cash held in connection with investing activities | 1,757 | 3,220 | |||||

Other investing activities, net | 5,317 | (5,677 | ) | ||||

Cash flows provided by investing activities | 346,301 | 264,520 | |||||

Cash flows from financing activities: | |||||||

Borrowings from debt obligations | 854,637 | 646,401 | |||||

Repayments and repurchases of debt obligations | (626,492 | ) | (991,184 | ) | |||

Proceeds from loan participations payable | — | 22,844 | |||||

Preferred dividends paid | (25,660 | ) | (25,660 | ) | |||

Repurchase of stock | — | (90,481 | ) | ||||

Payments for deferred financing costs | (12,243 | ) | (8,003 | ) | |||

Payments for withholding taxes upon vesting of stock-based compensation | (511 | ) | (1,203 | ) | |||

Other financing activities, net | (13,420 | ) | (7,144 | ) | |||

Cash flows provided by (used in) financing activities | 176,311 | (454,430 | ) | ||||

Effect of exchange rate changes on cash | 7 | 22 | |||||

Changes in cash and cash equivalents | 625,535 | (189,738 | ) | ||||

Cash and cash equivalents at beginning of period | 328,744 | 711,101 | |||||

Cash and cash equivalents at end of period | $ | 954,279 | $ | 521,363 | |||

Supplemental disclosure of non-cash investing and financing activity: | |||||||

Fundings and repayments of loan receivables and loan participations, net | $ | (52,406 | ) | $ | 12,267 | ||

Accounts payable for capital expenditures on land and development assets | 2,984 | 5,575 | |||||

Accounts payable for capital expenditures on real estate assets | 1,488 | — | |||||

Receivable from sales of real estate and land parcels | 3,139 | 1,741 | |||||

Developer fee payable | — | 6,438 | |||||

Accruals for repurchase of stock | — | 2,260 | |||||

The accompanying notes are an integral part of the consolidated financial statements.

5

Note 1—Business and Organization

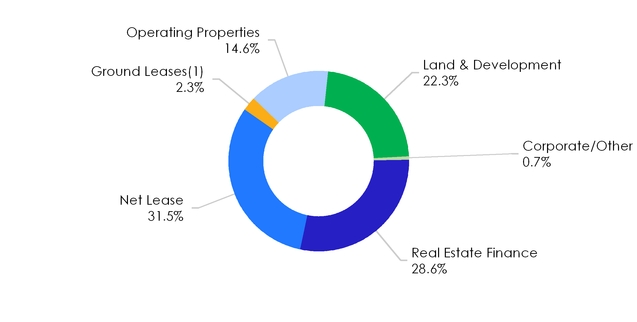

Business—iStar Inc. (the "Company"), doing business as "iStar," finances, invests in and develops real estate and real estate related projects as part of its fully-integrated investment platform. The Company also provides management services for its ground lease and net lease equity method investments (refer to Note 7). The Company has invested more than $35 billion over the past two decades and is structured as a real estate investment trust ("REIT") with a diversified portfolio focused on larger assets located in major metropolitan markets. The Company's primary business segments are real estate finance, net lease, operating properties and land and development (refer to Note 17).

Organization—The Company began its business in 1993 through the management of private investment funds and became publicly traded in 1998. Since that time, the Company has grown through the origination of new investments, as well as through corporate acquisitions.

Note 2—Basis of Presentation and Principles of Consolidation

Basis of Presentation—The accompanying unaudited consolidated financial statements have been prepared in conformity with the instructions to Form 10-Q and Article 10-01 of Regulation S-X for interim financial statements. Accordingly, they do not include all the information and footnotes required by generally accepted accounting principles in the United States of America ("GAAP") for complete financial statements. These unaudited consolidated financial statements and related notes should be read in conjunction with the consolidated financial statements and related notes included in the Company's Annual Report on Form 10-K for the year ended December 31, 2016 (the "2016 Annual Report").

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the dates of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates.

In the opinion of management, the accompanying consolidated financial statements contain all adjustments, consisting of normal recurring adjustments, necessary for a fair statement of the results for the interim periods presented. Such operating results may not be indicative of the expected results for any other interim periods or the entire year. Certain prior year amounts have been reclassified in the Company's consolidated financial statements and the related notes to conform to the current period presentation.

Principles of Consolidation—The consolidated financial statements include the financial statements of the Company, its wholly owned subsidiaries, controlled partnerships and variable interest entities ("VIEs") for which the Company is the primary beneficiary. All significant intercompany balances and transactions have been eliminated in consolidation. The Company's involvement with VIEs affects its financial performance and cash flows primarily through amounts recorded in "Operating lease income," "Interest income," "Earnings from equity method investments," "Real estate expense" and "Interest expense" in the Company's consolidated statements of operations. The Company has not provided financial support to those VIEs that it was not previously contractually required to provide.

Consolidated VIEs—As of June 30, 2017, the Company consolidates VIEs for which it is considered the primary beneficiary. As of June 30, 2017, the total assets of these consolidated VIEs were $326.9 million and total liabilities were $68.9 million. The classifications of these assets are primarily within "Land and development, net" and "Real estate, net" on the Company's consolidated balance sheets. The classifications of liabilities are primarily within "Accounts payable, accrued expenses and other liabilities" and "debt obligations, net" on the Company's consolidated balance sheets. The liabilities of these VIEs are non-recourse to the Company and can only be satisfied from each VIE's respective assets. The Company did not have any unfunded commitments related to consolidated VIEs as of June 30, 2017.

Unconsolidated VIEs—As of June 30, 2017, the Company has investments in VIEs where it is not the primary beneficiary and accordingly the VIEs have not been consolidated in the Company's consolidated financial statements. As of June 30, 2017, the Company's maximum exposure to loss from these investments does not exceed the sum of the $56.6 million carrying value of the investments, which are classified in "Other investments" and "Loans receivable and other lending investments, net" on the Company's consolidated balance sheets, and $53.8 million of related unfunded commitments.

6

Note 3—Summary of Significant Accounting Policies

On January 1, 2017, the Company adopted Accounting Standards Update ("ASU") 2016-09, Compensation—Stock Compensation: Improvements to Employee Share-Based Payment Accounting ("ASU 2016-09") which was issued to simplify several aspects of the accounting for share-based payment transactions, including income tax, classification of awards as either equity or liabilities and classification on the statement of cash flows. The adoption of ASU 2016-09 did not have a material impact on the Company's consolidated financial statements.

As of June 30, 2017, the remainder of the Company's significant accounting policies, which are detailed in the Company's 2016 Annual Report, have not changed materially.

New Accounting Pronouncements—In February 2017, the Financial Accounting Standards Board ("FASB") issued ASU 2017-05, Other Income—Gains and Losses from the Derecognition of Nonfinancial Assets ("ASU 2017-05") to clarify the scope of Subtopic 610-20, Other Income—Gains and Losses from the Derecognition of Nonfinancial Assets, and to add guidance for partial sales of nonfinancial assets. The amendments in ASU 2017-05 simplify GAAP by eliminating several accounting differences between transactions involving assets and transactions involving businesses. The amendments in ASU 2017-05 require an entity to initially measure a retained noncontrolling interest in a nonfinancial asset at fair value consistent with how a retained noncontrolling interest in a business is measured. Also, if an entity transfers ownership interests in a consolidated subsidiary that is within the scope of ASC 610-20 and continues to have a controlling financial interest in that subsidiary, ASU 2017-05 requires the entity to account for the transaction as an equity transaction, which is consistent with how changes in ownership interests in a consolidated subsidiary that is a business are recorded when a parent retains a controlling financial interest in the business. ASU 2017-05 is effective for interim and annual reporting periods beginning after December 15, 2017. Early adoption is permitted beginning January 1, 2017. Management is evaluating the impact of the guidance on the Company's consolidated financial statements and expects to adopt the retrospective approach, which would require the Company to recast revenue and expenses for all prior periods presented in the year of adoption of the new standard. The Company expects that transactions in assets and businesses in which the Company retains an ownership interest, such as the sale of a controlling interest in its GL business (refer to Note 4), will be impacted by this guidance. As a result, under the retrospective approach, in 2018, the Company expects to record an incremental gain of $55.5 million in its consolidated statements of operations for the three and six months ended June 30, 2017, bringing the Company's full gain on the sale of its GL business to approximately $178.9 million.

In January 2017, the FASB issued ASU 2017-01, Business Combinations: Clarifying the Definition of a Business ("ASU 2017-01") to provide a more robust framework to use in determining when a set of assets and activities is a business. The amendments provide more consistency in applying the guidance, reduce the costs of application, and make the definition of a business more operable. The Company's real estate acquisitions have historically been accounted for as a business combination or an asset acquisition. Under ASU 2017-01, certain transactions previously accounted for as business combinations under the existing guidance would be accounted for as asset acquisitions under the new guidance. As a result, the Company expects more transaction costs to be capitalized under real estate acquisitions and less transaction costs to be expensed under business combinations. ASU 2017-01 is effective for interim and annual reporting periods beginning after December 15, 2017. Early application is permitted under certain conditions. Management is evaluating the impact of the guidance on the Company's consolidated financial statements.

In November 2016, the FASB issued ASU 2016-18, Statement of Cash Flows: Restricted Cash ("ASU 2016-18") which requires that restricted cash be included with cash and cash equivalents when reconciling beginning and ending cash and cash equivalents on the statement of cash flows. In addition, ASU 2016-18 requires disclosure of what is included in restricted cash. ASU 2016-18 is effective for interim and annual reporting periods beginning after December 15, 2017. Early adoption is permitted. Management does not believe the guidance will have a material impact on the Company's consolidated financial statements.

In August 2016, the FASB issued ASU 2016-15, Statement of Cash Flows: Classification of Certain Cash Receipts and Cash Payments ("ASU 2016-15") which was issued to reduce diversity in practice in how certain cash receipts and cash payments, including debt prepayment or debt extinguishment costs, distributions from equity method investees, and other separately identifiable cash flows, are presented and classified in the statement of cash flows. ASU 2016-15 is effective for interim and annual reporting periods beginning after December 15, 2017. Early adoption is permitted. Management does not believe the guidance will have a material impact on the Company's consolidated financial statements.

In June 2016, the FASB issued ASU 2016-13, Financial Instruments—Credit Losses: Measurement of Credit Losses on Financial Instruments ("ASU 2016-13") which was issued to provide financial statement users with more decision-useful information about the expected credit losses on financial instruments held by a reporting entity. This amendment replaces the

7

incurred loss impairment methodology in current GAAP with a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. The Company currently records a general reserve that covers performing loans and reserves for loan losses are recorded when (i) available information as of each balance sheet date indicates that it is probable a loss has occurred in the portfolio and (ii) the amount of the loss can be reasonably estimated. The formula-based general reserve is derived from estimated principal default probabilities and loss severities applied to groups of loans based upon risk ratings assigned to loans with similar risk characteristics during our quarterly loan portfolio assessment. The Company estimates loss rates based on historical realized losses experienced within its portfolio and take into account current economic conditions affecting the commercial real estate market when establishing appropriate time frames to evaluate loss experience. The Company believes this general reserve component of its total loan loss reserves should minimize the impact of ASU 2016-13. ASU 2016-13 is effective for interim and annual reporting periods beginning after December 15, 2019. Early adoption is permitted for interim and annual reporting periods beginning after December 15, 2018. Management does not believe the guidance will have a material impact on the Company's consolidated financial statements.

In February 2016, the FASB issued ASU 2016-02, Leases ("ASU 2016-02"), which requires the recognition of lease assets and lease liabilities by lessees for those leases classified as operating leases. For operating leases, a lessee will be required to do the following: (i) recognize a right-of-use asset and a lease liability, initially measured at the present value of the lease payments, in the statement of financial position; (ii) recognize a single lease cost, calculated so that the cost of the lease is allocated over the lease term on a generally straight-line basis and (iii) classify all cash payments within operating activities in the statement of cash flows. For operating lease arrangements for which the Company is the lessee, primarily the lease of office space, the Company expects the impact of ASU 2016-02 to be the recognition of a right-of-use asset and lease liability on its consolidated balance sheets. The accounting applied by the Company as a lessor will be largely unchanged from that applied under previous GAAP. However, in certain instances, a new long-term lease of land subsequent to adoption could be classified as a sales-type lease, which could result in the Company derecognizing the underlying asset from its books and recording a profit or loss on sale and the net investment in the lease. ASU 2016-02 is effective for interim and annual reporting periods beginning after December 15, 2018. Early adoption is permitted. Management is evaluating the impact of the guidance on the Company's consolidated financial statements.

In January 2016, the FASB issued ASU 2016-01, Financial Instruments - Overall: Recognition and Measurement of Financial Assets and Financial Liabilities ("ASU 2016-01"), which addresses certain aspects of recognition, measurement, presentation and disclosure of financial instruments. ASU 2016-01 is effective for interim and annual reporting periods beginning after December 15, 2017. Early adoption is not permitted. Management is evaluating the impact of the guidance on the Company's consolidated financial statements.

In May 2014, the FASB issued ASU 2014-09, Revenue from Contracts with Customers ("ASU 2014-09") which supersedes existing industry-specific guidance, including ASC 360-20, Real Estate Sales. The new standard is principles-based and requires more estimates and judgment than current guidance. Certain contracts with customers, including lease contracts and financial instruments and other contractual rights, are not within the scope of the new guidance. Although most of the Company's revenue is operating lease income generated from lease contracts and interest income generated from financial instruments, certain other of the Company's revenue streams will be impacted by the new guidance. The Company currently expects that income from the sale of residential condominiums, land development revenue and other income will be impacted by ASU 2014-09. The Company does not expect income from the sales of net lease or commercial operating properties to be impacted by ASU 2014-09. In August 2015, the FASB issued ASU 2015-14, Revenue from Contracts with Customers - Deferral of the Effective Date, to defer the effective date of ASU 2014-09 by one year. ASU 2014-09 is now effective for interim and annual reporting periods beginning after December 15, 2017. Early adoption is permitted beginning January 1, 2017. Management is evaluating the impact of the guidance on the Company’s consolidated financial statements and expects to adopt the full retrospective approach, which would require the Company to recast revenue and expenses for all prior periods presented in the year of adoption of the new standard.

8

Note 4—Real Estate

The Company's real estate assets were comprised of the following ($ in thousands):

Net Lease(1) | Operating Properties | Total | |||||||||

As of June 30, 2017 | |||||||||||

Land, at cost | $ | 227,231 | $ | 211,057 | $ | 438,288 | |||||

Buildings and improvements, at cost | 950,548 | 322,079 | 1,272,627 | ||||||||

Less: accumulated depreciation | (314,373 | ) | (53,560 | ) | (367,933 | ) | |||||

Real estate, net | 863,406 | 479,576 | 1,342,982 | ||||||||

Real estate available and held for sale (2) | 924 | 67,121 | 68,045 | ||||||||

Total real estate | $ | 864,330 | $ | 546,697 | $ | 1,411,027 | |||||

As of December 31, 2016 | |||||||||||

Land, at cost | $ | 231,506 | $ | 211,054 | $ | 442,560 | |||||

Buildings and improvements, at cost | 987,050 | 311,283 | 1,298,333 | ||||||||

Less: accumulated depreciation | (307,444 | ) | (46,175 | ) | (353,619 | ) | |||||

Real estate, net | 911,112 | 476,162 | 1,387,274 | ||||||||

Real estate available and held for sale (2) | 155,051 | 82,480 | 237,531 | ||||||||

Total real estate | $ | 1,066,163 | $ | 558,642 | $ | 1,624,805 | |||||

_______________________________________________________________________________

(1) | In 2014, the Company partnered with a sovereign wealth fund to form a venture to acquire and develop net lease assets (the "Net Lease Venture") and gave a right of first refusal to the Net Lease Venture on all new net lease investments (refer to Note 7 for more information on the Net Lease Venture). The Company is responsible for sourcing new opportunities and managing the Net Lease Venture and its assets in exchange for a promote and management fee. |

(2) | As of December 31, 2016, net lease includes the Company's ground lease ("GL") assets that were reclassified to "Real estate available and held for sale" (refer to "Dispositions" below). As of December 31, 2016, the carrying value of the Company's GL assets were previously classified as $104.5 million in "Real estate, net," $37.5 million in "Deferred expenses and other assets, net," $8.2 million in "Deferred operating lease income receivable, net" and $3.5 million in "Accrued interest and operating lease income receivable, net" on the Company's consolidated balance sheet. As of June 30, 2017 and December 31, 2016, the Company had $67.1 million and $82.5 million, respectively, of residential properties available for sale in its operating properties portfolio. |

Real Estate Available and Held for Sale—During the six months ended June 30, 2017, the Company transferred one net lease asset with a carrying value of $0.9 million to held for sale due to an executed contract with a third party. During the six months ended June 30, 2016, the Company transferred one net lease asset with a carrying value of $0.7 million and one commercial operating property with a carrying value of $16.1 million to held for sale due to executed contracts with a third parties.

Acquisitions—During the six months ended June 30, 2016, the Company acquired land for $3.9 million and simultaneously entered into a 99 year ground lease with the seller.

Disposition of Ground Lease Business—In April 2017, institutional investors acquired a controlling interest in the Company's GL business through the merger of a Company subsidiary and related transactions (the "Acquisition Transactions"). The Company's GL business was a component of the Company's net lease segment and consisted of 12 properties subject to long-term net leases including seven GLs and one master lease (covering five properties). The acquiring entity was a newly formed unconsolidated entity named Safety, Income and Growth, Inc. ("SAFE"). The carrying value of the Company's GL assets was approximately $161.1 million. Shortly before the Acquisition Transactions, the Company completed the $227.0 million 2017 Secured Financing on its GL assets (refer to Note 10). The Company received all of the proceeds of the 2017 Secured Financing. The Company received an additional $113.0 million of proceeds in the Acquisition Transactions, including $55.5 million that the Company contributed to SAFE in its initial capitalization. As a result of the Acquisition Transactions, the Company deconsolidated the 12 properties and the associated 2017 Secured Financing. The Company accounts for its investment in SAFE as an equity method investment (refer to Note 7). The Company accounted for this transaction as an in substance sale of real estate and recognized a gain of $123.4 million, reflecting the aggregate gain less the fair value of the Company's retained interest in SAFE (refer to Note 2 - Summary of Significant Accounting Policies). The carrying value of the 12 properties is classified in "Real estate available and held for sale" on the Company's consolidated balance sheet as of December 31, 2016 and the gain was recorded in "Gain from discontinued operations" in the Company's consolidated statements of operations.

9

Discontinued Operations—The transactions described above involving the Company's GL business qualified for discontinued operations and the following table summarizes income from discontinued operations for the three and six months ended June 30, 2017 and 2016 ($ in thousands)(1)(2):

For the Three Months Ended June 30, | For the Six Months Ended June 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Revenues | $ | 678 | $ | 4,543 | $ | 6,430 | $ | 8,986 | ||||||||

Expenses | (505 | ) | (910 | ) | (1,491 | ) | (1,772 | ) | ||||||||

Income from discontinued operations | $ | 173 | $ | 3,633 | $ | 4,939 | $ | 7,214 | ||||||||

_______________________________________________________________________________

(1) | The transactions closed on April 14, 2017 and revenues, expenses and income from discontinued operations excludes the period from April 14, 2017 to June 30, 2017. Revenues primarily consisted of operating lease income and expenses primarily consisted of depreciation and amortization and real estate expense. |

(2) | For the six months ended June 30, 2017, cash flows provided by operating activities and cash flows used in investing activities from discontinued operations was $5.7 million and $0.5 million, respectively. For the six months ended June 30, 2016, cash flows provided by operating activities and cash flows used in investing activities from discontinued operations was $9.4 million and $4.6 million, respectively. |

Other Dispositions—During the six months ended June 30, 2017 and 2016, the Company sold residential condominiums for total net proceeds of $17.6 million and $59.2 million, respectively, and recorded income from sales of real estate totaling $2.7 million and $18.8 million, respectively. During the six months ended June 30, 2017 and 2016, the Company sold net lease assets for net proceeds of $19.5 million and $30.2 million, respectively, resulting in gains of $6.2 million and $9.2 million, respectively. During the six months ended June 30, 2016, the Company also sold three commercial operating properties for net proceeds of $158.9 million resulting in gains of $25.9 million. The gains are recorded in "Income from sales of real estate" in the Company's consolidated statements of operations.

Impairments—During the six months ended June 30, 2017, the Company recorded an impairment of $4.4 million on a real estate asset held for sale due to shifting demand in the local condominium market along with a change in the Company's exit strategy. During the six months ended June 30, 2016, the Company recorded an impairment of $3.0 million on a residential operating property resulting from a slowdown in the local condominium real estate market.

Tenant Reimbursements—The Company receives reimbursements from tenants for certain facility operating expenses including common area costs, insurance, utilities and real estate taxes. Tenant expense reimbursements were $5.2 million and $10.7 million for the three and six months ended June 30, 2017, respectively. Tenant expense reimbursements were $5.9 million and $12.1 million for the three and six months ended June 30, 2016, respectively. These amounts are included in "Operating lease income" in the Company's consolidated statements of operations.

Allowance for Doubtful Accounts—As of June 30, 2017 and December 31, 2016, the allowance for doubtful accounts related to real estate tenant receivables was $1.4 million and $1.3 million, respectively, and the allowance for doubtful accounts related to deferred operating lease income was $1.1 million and $1.3 million as of June 30, 2017 and December 31, 2016, respectively. These amounts are included in "Accrued interest and operating lease income receivable, net" and "Deferred operating lease income receivable, net," respectively, on the Company's consolidated balance sheets.

Note 5—Land and Development

The Company's land and development assets were comprised of the following ($ in thousands):

As of | |||||||

June 30, | December 31, | ||||||

2017 | 2016 | ||||||

Land and land development, at cost | $ | 862,774 | $ | 952,051 | |||

Less: accumulated depreciation | (7,277 | ) | (6,486 | ) | |||

Total land and development, net | $ | 855,497 | $ | 945,565 | |||

10

Dispositions—During the six months ended June 30, 2017, the Company sold one land parcel totaling 1,250 acres (see following paragraph) and residential lots and units and recognized land development revenue of $152.8 million from its land and development portfolio. During the six months ended June 30, 2016, the Company sold residential lots and units and recognized land development revenue of $42.8 million from its land and development portfolio. During the six months ended June 30, 2017 and 2016, the Company recognized land development cost of sales of $138.4 million and $28.8 million, respectively, from its land and development portfolio.

In connection with the resolution of litigation involving a dispute over the purchase and sale of approximately 1,250 acres of land in Prince George’s County, Maryland ("Bevard"), during the three and six months ended June 30, 2017, the Company recognized $114.0 million of land development revenue and $106.3 million of land development cost of sales (refer to Note 11). In 2016, the Company acquired an additional 10.7% interest in Bevard for $10.8 million and owns 95.7% of Bevard as of June 30, 2017.

Impairments—During the six months ended June 30, 2017, the Company recorded an impairment of $10.1 million on a land and development asset due to a change in the Company's exit strategy.

Redeemable Noncontrolling Interest—The Company has a majority interest in a strategic venture that provides the third party minority partner an option to redeem its interest at fair value. The Company has reflected the partner's noncontrolling interest in this venture as a component of redeemable noncontrolling interest within its consolidated balance sheets. Changes in fair value are being accreted over the term from the date of issuance of the redemption option to the earliest redemption date using the interest method. As of June 30, 2017 and December 31, 2016, this interest had a carrying value of zero and $1.3 million, respectively. As of June 30, 2017 and December 31, 2016, this interest did not have a redemption value.

Note 6—Loans Receivable and Other Lending Investments, net

The following is a summary of the Company's loans receivable and other lending investments by class ($ in thousands):

As of | |||||||

Type of Investment | June 30, 2017 | December 31, 2016 | |||||

Senior mortgages | $ | 597,335 | $ | 940,738 | |||

Corporate/Partnership loans | 543,589 | 490,389 | |||||

Subordinate mortgages | 22,841 | 24,941 | |||||

Total gross carrying value of loans | 1,163,765 | 1,456,068 | |||||

Reserves for loan losses | (78,789 | ) | (85,545 | ) | |||

Total loans receivable, net | 1,084,976 | 1,370,523 | |||||

Other lending investments—securities | 85,589 | 79,916 | |||||

Total loans receivable and other lending investments, net | $ | 1,170,565 | $ | 1,450,439 | |||

Reserve for Loan Losses—Changes in the Company's reserve for loan losses were as follows ($ in thousands):

For the Three Months Ended June 30, | For the Six Months Ended June 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Reserve for loan losses at beginning of period | $ | 79,389 | $ | 109,671 | $ | 85,545 | $ | 108,165 | ||||||||

(Recovery of) provision for loan losses | (600 | ) | 700 | (5,528 | ) | 2,206 | ||||||||||

Charge-offs | — | — | (1,228 | ) | — | |||||||||||

Reserve for loan losses at end of period | $ | 78,789 | $ | 110,371 | $ | 78,789 | $ | 110,371 | ||||||||

11

The Company's recorded investment in loans (comprised of a loan's carrying value plus accrued interest) and the associated reserve for loan losses were as follows ($ in thousands):

Individually Evaluated for Impairment(1) | Collectively Evaluated for Impairment(2) | Total | |||||||||

As of June 30, 2017 | |||||||||||

Loans | $ | 249,659 | $ | 919,793 | $ | 1,169,452 | |||||

Less: Reserve for loan losses | (60,989 | ) | (17,800 | ) | (78,789 | ) | |||||

Total(3) | $ | 188,670 | $ | 901,993 | $ | 1,090,663 | |||||

As of December 31, 2016 | |||||||||||

Loans | $ | 253,941 | $ | 1,209,062 | $ | 1,463,003 | |||||

Less: Reserve for loan losses | (62,245 | ) | (23,300 | ) | (85,545 | ) | |||||

Total(3) | $ | 191,696 | $ | 1,185,762 | $ | 1,377,458 | |||||

_______________________________________________________________________________

(1) | The carrying value of these loans include unamortized discounts, premiums, deferred fees and costs totaling net discounts of $0.7 million and $0.4 million as of June 30, 2017 and December 31, 2016, respectively. The Company's loans individually evaluated for impairment primarily represent loans on non-accrual status and therefore, the unamortized amounts associated with these loans are not currently being amortized into income. |

(2) | The carrying value of these loans include unamortized discounts, premiums, deferred fees and costs totaling net premiums of $4.5 million and $1.9 million as of June 30, 2017 and December 31, 2016, respectively. |

(3) | The Company's recorded investment in loans as of June 30, 2017 and December 31, 2016 includes accrued interest of $5.7 million and $6.9 million, respectively, which are included in "Accrued interest and operating lease income receivable, net" on the Company's consolidated balance sheets. As of June 30, 2017 and December 31, 2016, the total excludes $85.6 million and $79.9 million, respectively, of securities that are evaluated for impairment under ASC 320. |

Credit Characteristics—As part of the Company's process for monitoring the credit quality of its loans, it performs a quarterly loan portfolio assessment and assigns risk ratings to each of its performing loans. Risk ratings, which range from 1 (lower risk) to 5 (higher risk), are based on judgments which are inherently uncertain and there can be no assurance that actual performance will be similar to current expectation. The Company designates loans as non-performing at such time as: (1) the loan becomes 90 days delinquent; (2) the loan has a maturity default; or (3) management determines it is probable that we will be unable to collect all amounts due according to the contractual terms of the loan. All non-performing loans are placed on non-accrual status and income is only recognized in certain cases upon actual cash receipt.

The Company's recorded investment in performing loans, presented by class and by credit quality, as indicated by risk rating, was as follows ($ in thousands):

As of June 30, 2017 | As of December 31, 2016 | ||||||||||||

Performing Loans | Weighted Average Risk Ratings | Performing Loans | Weighted Average Risk Ratings | ||||||||||

Senior mortgages | $ | 518,362 | 2.53 | $ | 859,250 | 3.12 | |||||||

Corporate/Partnership loans | 389,550 | 3.03 | 335,677 | 3.09 | |||||||||

Subordinate mortgages | 11,881 | 2.55 | 14,135 | 3.00 | |||||||||

Total | $ | 919,793 | 2.74 | $ | 1,209,062 | 3.11 | |||||||

12

The Company's recorded investment in loans, aged by payment status and presented by class, were as follows ($ in thousands):

Current | Less Than and Equal to 90 Days | Greater Than 90 Days(1) | Total Past Due | Total | |||||||||||||||

As of June 30, 2017 | |||||||||||||||||||

Senior mortgages | $ | 524,362 | $ | — | $ | 76,282 | $ | 76,282 | $ | 600,644 | |||||||||

Corporate/Partnership loans | 389,550 | — | 156,375 | 156,375 | 545,925 | ||||||||||||||

Subordinate mortgages | 22,883 | — | — | — | 22,883 | ||||||||||||||

Total | $ | 936,795 | $ | — | $ | 232,657 | $ | 232,657 | $ | 1,169,452 | |||||||||

As of December 31, 2016 | |||||||||||||||||||

Senior mortgages | $ | 868,505 | $ | — | $ | 76,677 | $ | 76,677 | $ | 945,182 | |||||||||

Corporate/Partnership loans | 335,677 | — | 157,146 | 157,146 | 492,823 | ||||||||||||||

Subordinate mortgages | 24,998 | — | — | — | 24,998 | ||||||||||||||

Total | $ | 1,229,180 | $ | — | $ | 233,823 | $ | 233,823 | $ | 1,463,003 | |||||||||

_______________________________________________________________________________

(1) | As of June 30, 2017, the Company had four loans which were greater than 90 days delinquent and were in various stages of resolution, including legal proceedings, environmental concerns and foreclosure-related proceedings, and ranged from 1.0 to 8.0 years outstanding. As of December 31, 2016, the Company had four loans which were greater than 90 days delinquent and were in various stages of resolution, including legal proceedings, environmental concerns and foreclosure-related proceedings, and ranged from 1.0 to 8.0 years outstanding. |

Impaired Loans—The Company's recorded investment in impaired loans, presented by class, were as follows ($ in thousands)(1):

As of June 30, 2017 | As of December 31, 2016 | ||||||||||||||||||||||

Recorded Investment | Unpaid Principal Balance | Related Allowance | Recorded Investment | Unpaid Principal Balance | Related Allowance | ||||||||||||||||||

With no related allowance recorded: | |||||||||||||||||||||||

Subordinate mortgages | $ | 11,002 | $ | 10,985 | $ | — | $ | 10,862 | $ | 10,846 | $ | — | |||||||||||

Subtotal | 11,002 | 10,985 | — | 10,862 | 10,846 | — | |||||||||||||||||

With an allowance recorded: | |||||||||||||||||||||||

Senior mortgages | 82,282 | 82,390 | (48,518 | ) | 85,933 | 85,780 | (49,774 | ) | |||||||||||||||

Corporate/Partnership loans | 156,375 | 145,849 | (12,471 | ) | 157,146 | 146,783 | (12,471 | ) | |||||||||||||||

Subtotal | 238,657 | 228,239 | (60,989 | ) | 243,079 | 232,563 | (62,245 | ) | |||||||||||||||

Total: | |||||||||||||||||||||||

Senior mortgages | 82,282 | 82,390 | (48,518 | ) | 85,933 | 85,780 | (49,774 | ) | |||||||||||||||

Corporate/Partnership loans | 156,375 | 145,849 | (12,471 | ) | 157,146 | 146,783 | (12,471 | ) | |||||||||||||||

Subordinate mortgages | 11,002 | 10,985 | — | 10,862 | 10,846 | — | |||||||||||||||||

Total | $ | 249,659 | $ | 239,224 | $ | (60,989 | ) | $ | 253,941 | $ | 243,409 | $ | (62,245 | ) | |||||||||

____________________________________________________________

(1) | All of the Company's non-accrual loans are considered impaired and included in the table above. |

13

The Company's average recorded investment in impaired loans and interest income recognized, presented by class, were as follows ($ in thousands):

For the Three Months Ended June 30, | For the Six Months Ended June 30, | ||||||||||||||||||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||||||||||||||||||

Average Recorded Investment | Interest Income Recognized | Average Recorded Investment | Interest Income Recognized | Average Recorded Investment | Interest Income Recognized | Average Recorded Investment | Interest Income Recognized | ||||||||||||||||||||||||

With no related allowance recorded: | |||||||||||||||||||||||||||||||

Senior mortgages | $ | — | $ | — | $ | 9,150 | $ | 111 | $ | — | $ | — | $ | 6,100 | $ | 111 | |||||||||||||||

Subordinate mortgages | 11,023 | — | 5,785 | — | 10,970 | — | 3,857 | — | |||||||||||||||||||||||

Subtotal | 11,023 | — | 14,935 | 111 | 10,970 | — | 9,957 | 111 | |||||||||||||||||||||||

With an allowance recorded: | |||||||||||||||||||||||||||||||

Senior mortgages | 82,368 | — | 126,978 | — | 83,556 | — | 126,903 | — | |||||||||||||||||||||||

Corporate/Partnership loans | 156,839 | — | 5,224 | — | 156,941 | — | 5,396 | — | |||||||||||||||||||||||

Subtotal | 239,207 | — | 132,202 | — | 240,497 | — | 132,299 | — | |||||||||||||||||||||||

Total: | |||||||||||||||||||||||||||||||

Senior mortgages | 82,368 | — | 136,128 | 111 | 83,556 | — | 133,003 | 111 | |||||||||||||||||||||||

Corporate/Partnership loans | 156,839 | — | 5,224 | — | 156,941 | — | 5,396 | — | |||||||||||||||||||||||

Subordinate mortgages | 11,023 | — | 5,785 | — | 10,970 | — | 3,857 | — | |||||||||||||||||||||||

Total | $ | 250,230 | $ | — | $ | 147,137 | $ | 111 | $ | 251,467 | $ | — | $ | 142,256 | $ | 111 | |||||||||||||||

Securities—Other lending investments—securities includes the following ($ in thousands):

Face Value | Amortized Cost Basis | Net Unrealized Gain (Loss) | Estimated Fair Value | Net Carrying Value | |||||||||||||||

As of June 30, 2017 | |||||||||||||||||||

Available-for-Sale Securities | |||||||||||||||||||

Municipal debt securities | $ | 21,230 | $ | 21,230 | $ | 992 | $ | 22,222 | $ | 22,222 | |||||||||

Held-to-Maturity Securities | |||||||||||||||||||

Debt securities | 63,418 | 63,367 | 1,544 | 64,911 | 63,367 | ||||||||||||||

Total | $ | 84,648 | $ | 84,597 | $ | 2,536 | $ | 87,133 | $ | 85,589 | |||||||||

As of December 31, 2016 | |||||||||||||||||||

Available-for-Sale Securities | |||||||||||||||||||

Municipal debt securities | $ | 21,240 | $ | 21,240 | $ | 426 | $ | 21,666 | $ | 21,666 | |||||||||

Held-to-Maturity Securities | |||||||||||||||||||

Debt securities | 58,454 | 58,250 | 2,753 | 61,003 | 58,250 | ||||||||||||||

Total | $ | 79,694 | $ | 79,490 | $ | 3,179 | $ | 82,669 | $ | 79,916 | |||||||||

14

Note 7—Other Investments

The Company's other investments and its proportionate share of earnings from equity method investments were as follows ($ in thousands):

Equity in Earnings | |||||||||||||||||||||||

Carrying Value as of | For the Three Months Ended June 30, | For the Six Months Ended June 30, | |||||||||||||||||||||

June 30, 2017 | December 31, 2016 | 2017 | 2016 | 2017 | 2016 | ||||||||||||||||||

Real estate equity investments | |||||||||||||||||||||||

iStar Net Lease I LLC ("Net Lease Venture") | $ | 128,997 | $ | 92,669 | $ | 1,032 | $ | 944 | $ | 2,013 | $ | 1,890 | |||||||||||

Safety, Income and Growth, Inc. ("SAFE")(1) | 50,287 | — | 48 | — | 48 | — | |||||||||||||||||

Marina Palms, LLC ("Marina Palms") | 7,191 | 35,185 | 1,183 | 5,180 | 4,300 | 13,401 | |||||||||||||||||

Other real estate equity investments(2) | 63,107 | 53,202 | 2,892 | 28,600 | 4,249 | 26,898 | |||||||||||||||||

Subtotal | 249,582 | 181,056 | 5,155 | 34,724 | 10,610 | 42,189 | |||||||||||||||||

Other strategic investments(3) | 27,239 | 33,350 | 360 | 4,723 | 607 | 5,525 | |||||||||||||||||

Total | $ | 276,821 | $ | 214,406 | $ | 5,515 | $ | 39,447 | $ | 11,217 | $ | 47,714 | |||||||||||

_______________________________________________________________________________

(1) | Equity in earnings is for the period from April 14, 2017 to June 30, 2017. |

(2) | In June 2016, a majority-owned consolidated subsidiary of the Company sold its interest in a real estate equity method investment for net proceeds of $39.8 million and recognized a gain of $31.5 million, of which $10.1 million of the gain was attributable to the noncontrolling interest. |

(3) | In conjunction with the sale of the Company's interests in Oak Hill Advisors, L.P. in 2011, the Company retained a share of the carried interest related to various funds. During the three and six months ended June 30, 2016, the Company recognized $0.5 million and $3.7 million, respectively, of carried interest income. |

Net Lease Venture—In February 2014, the Company partnered with a sovereign wealth fund to form an unconsolidated entity in which the Company has an equity interest of approximately 51.9%. The partners plan to contribute up to an aggregate $500 million of equity to acquire and develop net lease assets over time. The Company is responsible for sourcing new opportunities and managing the venture and its assets in exchange for a promote and management fee. Several of the Company's senior executives whose time is substantially devoted to the Net Lease Venture own a total of 0.6% equity ownership in the venture via co-investment. These senior executives are also entitled to an amount equal to 50% of any promote payment received based on the 47.5% partner's interest. During the six months ended June 30, 2017, the Net Lease Venture acquired industrial properties for $59.0 million. During the six months ended June 30, 2017, the Company sold a net lease asset for proceeds of $6.2 million, which approximated its carrying value, to the Net Lease Venture and derecognized the associated $18.9 million financing.

As of June 30, 2017 and December 31, 2016, the venture's carrying value of total assets was $626.5 million and $511.3 million, respectively. During the three and six months ended June 30, 2017, the Company recorded management fees of $0.5 million and $0.9 million, respectively, and $0.4 million and $0.8 million for the three and six months ended June 30, 2016, respectively, from the Net Lease Venture which are included in "Other income" in the Company's consolidated statements of operations. This entity is not a VIE and the Company does not have controlling interest due to the substantive participating rights of its partner.

Safety, Income and Growth, Inc.—The Company along with two institutional investors capitalized SIGI Acquisition, Inc. ("SIGI") on April 14, 2017. The Company contributed $55.5 million for an initial 49% noncontrolling interest in SIGI and the two institutional investors contributed an aggregate $57.5 million for an initial 51% controlling interest in SIGI. A wholly-owned subsidiary of the Company that held the Company's GL business and assets merged with and into SIGI on April 14, 2017 with SIGI surviving the merger and being renamed Safety, Income and Growth, Inc. ("SAFE"). Through this merger and related transactions, the institutional investors acquired a controlling interest in the Company's GL business. The Company's carrying value of the GL assets was approximately $161.1 million. Shortly before the Acquisition Transactions, the Company completed the $227.0 million 2017 Secured Financing on its GL assets (refer to Note 10). The Company received all of the proceeds of the 2017 Secured Financing. The Company received an additional $113.0 million of proceeds in the Acquisition Transactions, including $55.5 million that the Company contributed to SAFE in its initial capitalization. As a result of the Acquisition Transactions, the

15

Company deconsolidated the 12 properties and the associated 2017 Secured Financing. The Company accounted for this transaction as an in substance sale of real estate and recognized a gain of $123.4 million, reflecting the aggregate gain less the fair value of the Company's retained interest in SAFE. The carrying value of the 12 properties are classified in "Real estate available and held for sale" on the Company's consolidated balance sheet as of December 31, 2016 and the gain was recorded in "Gain from discontinued operations" in the Company's consolidated statements of operations.

On June 27, 2017, SAFE completed its initial public offering (the "Offering") raising $205.0 million in gross proceeds and concurrently completed a $45.0 million private placement to the Company. In addition, the Company paid $16.6 million in organization and offering costs of the up to $25.0 million in organization and offering costs it has agreed to pay in connection with the Offering and concurrent private placement through June 30, 2017, including commissions payable to the underwriters and other offering expenses. The Company expensed the portion of offering costs that was attributable to other investors in "Other expense" in the Company's consolidated statements of operations and capitalized the portion of offering costs attributable to the Company's ownership interest in "Other investments" on the Company's consolidated balance sheets. As of June 30, 2017, the Company owned approximately 28% of SAFE's common stock outstanding.

A wholly-owned subsidiary of the Company is the external manager of SAFE and is entitled to a management fee, payable solely in shares of SAFE's common stock, equal to the sum of 1.0% of SAFE's total equity up to $2.5 billion and 0.75% of SAFE's total equity in excess of $2.5 billion. The Company is not entitled to receive any performance or incentive compensation. The Company is also entitled to receive expense reimbursements, payable solely in shares of SAFE's common stock, for its personnel that perform certain legal, accounting, due diligence tasks and other services that third-party professionals or outside consultants otherwise would perform. The Company has agreed to waive both the management fee and certain of the expense reimbursements through June 30, 2018.

Marina Palms—As of June 30, 2017, the Company owned a 47.5% equity interest in Marina Palms, a 468 unit, two tower residential condominium development in North Miami Beach, Florida. The 234 unit north tower has one unit remaining for sale as of June 30, 2017. The 234 unit south tower is 84% sold or pre-sold (based on unit count) as of June 30, 2017. This entity is not a VIE and the Company does not have controlling interest due to shared control of the entity with its partner. As of June 30, 2017 and December 31, 2016, the venture's carrying value of total assets was $52.7 million and $201.8 million, respectively.

Other real estate equity investments—As of June 30, 2017, the Company's other real estate equity investments included equity interests in real estate ventures ranging from 20% to 85%, comprised of investments of $7.9 million in operating properties and $55.2 million in land assets. As of December 31, 2016, the Company's other real estate equity investments included $3.6 million in operating properties and $49.6 million in land assets.

In December 2016, the Company sold a land and development asset to a newly formed unconsolidated entity in which the Company owns a 50.0% equity interest. This entity is a VIE and the Company does not have a controlling interest due to shared control of the entity with its partner. The Company and its partner both made $7.0 million contributions to the venture and the Company provided financing to the entity in the form of a $27.0 million senior loan commitment, which had a carrying value of $23.6 million and $22.7 million as of June 30, 2017 and December 31, 2016, respectively, and is included in "Loans receivable and other lending investments, net" on the Company's consolidated balance sheets. During the three and six months ended June 30, 2017, the Company recorded $0.5 million and $0.9 million of interest income, respectively, on the senior loan.

Other strategic investments—As of June 30, 2017, the Company also had smaller investments in real estate related funds and other strategic investments in several other entities that were accounted for under the equity method or cost method. As of June 30, 2017 and December 31, 2016, the carrying value of the Company's cost method investments was $0.9 million and $1.4 million, respectively.

16

Summarized investee financial information—The following table presents the investee level summarized financial information of the Company's equity method investments, which were significant subsidiaries for the six months ended June 30, 2017 and 2016 ($ in thousands):

Revenues | Expenses | Net Income Attributable to Parent Entities | |||||||||

For the Six Months Ended June 30, 2017 | |||||||||||

Marina Palms | $ | 31,847 | $ | (19,771 | ) | $ | 12,076 | ||||

For the Six Months Ended June 30, 2016 | |||||||||||

Marina Palms | $ | 87,494 | $ | (47,764 | ) | $ | 39,730 | ||||

Note 8—Other Assets and Other Liabilities

Deferred expenses and other assets, net, consist of the following items ($ in thousands):

As of | |||||||

June 30, 2017 | December 31, 2016 | ||||||

Intangible assets, net(1) | $ | 20,452 | $ | 30,727 | |||

Other receivables(2) | 56,851 | 52,820 | |||||

Other assets | 29,449 | 34,351 | |||||

Restricted cash | 23,380 | 25,883 | |||||

Leasing costs, net(3) | 11,367 | 11,802 | |||||

Corporate furniture, fixtures and equipment, net(4) | 5,133 | 5,691 | |||||

Deferred financing fees, net | 489 | 838 | |||||

Deferred expenses and other assets, net | $ | 147,121 | $ | 162,112 | |||

_______________________________________________________________________________

(1) | Intangible assets, net includes above market and in-place lease assets and lease incentives related to the acquisition of real estate assets. Accumulated amortization on intangible assets, net was $33.5 million and $31.9 million as of June 30, 2017 and December 31, 2016, respectively. The amortization of above market leases and lease incentive assets decreased operating lease income in the Company's consolidated statements of operations by $0.8 million and $1.6 million for the three and six months ended June 30, 2017, respectively, and $1.1 million and $2.2 million for the three and six months ended June 30, 2016, respectively. These intangible lease assets are amortized over the term of the lease. The amortization expense for in-place leases was $0.7 million and $1.2 million for the three and six months ended June 30, 2017, respectively, and $0.6 million and $1.1 million for the three and six months ended June 30, 2016, respectively. These amounts are included in "Depreciation and amortization" in the Company's consolidated statements of operations. |

(2) | As of June 30, 2017 and December 31, 2016, included $26.0 million of receivables related to the construction and development of an amphitheater. |

(3) | Accumulated amortization of leasing costs was $7.0 million and $6.7 million as of June 30, 2017 and December 31, 2016, respectively. |

(4) | Accumulated depreciation on corporate furniture, fixtures and equipment was $9.8 million and $9.0 million as of June 30, 2017 and December 31, 2016, respectively. |

17

Accounts payable, accrued expenses and other liabilities consist of the following items ($ in thousands):

As of | |||||||

June 30, 2017 | December 31, 2016 | ||||||

Other liabilities(1) | $ | 81,526 | $ | 75,993 | |||

Accrued expenses(2) | 84,174 | 72,693 | |||||

Accrued interest payable | 56,716 | 54,033 | |||||

Intangible liabilities, net(3) | 7,843 | 8,851 | |||||

Accounts payable, accrued expenses and other liabilities | $ | 230,259 | $ | 211,570 | |||

_______________________________________________________________________________

(1) | As of June 30, 2017 and December 31, 2016, other liabilities includes $24.0 million related to profit sharing arrangements with developers for certain properties sold. As of June 30, 2017 and December 31, 2016, includes $1.5 million and $1.2 million, respectively, associated with "Real estate available and held for sale" on the Company's consolidated balance sheets. As of June 30, 2017 and December 31, 2016, other liabilities also includes $7.3 million and $8.5 million, respectively, related to tax increment financing bonds which were issued by government entities to fund development within two of the Company's land projects. The amount represents tax assessments associated with each project, which will decrease as the Company sells units. |

(2) | As of June 30, 2017 and December 31, 2016, accrued expenses includes $2.5 million and $1.7 million, respectively, associated with "Real estate available and held for sale" on the Company's consolidated balance sheets. |

(3) | Intangible liabilities, net includes below market lease liabilities related to the acquisition of real estate assets. Accumulated amortization on below market lease liabilities was $7.5 million and $6.4 million as of June 30, 2017 and December 31, 2016, respectively. The amortization of below market leases increased operating lease income in the Company's consolidated statements of operations by $0.8 million and $1.0 million for the three and six months ended June 30, 2017, respectively, and $0.3 million and $0.6 million for the three and six months ended June 30, 2016, respectively. |

Deferred tax assets and liabilities of the Company's taxable REIT subsidiaries were as follows ($ in thousands):

As of | |||||||

June 30, 2017 | December 31, 2016 | ||||||

Deferred tax assets (liabilities) | $ | 82,219 | $ | 66,498 | |||

Valuation allowance | (82,219 | ) | (66,498 | ) | |||

Net deferred tax assets (liabilities) | $ | — | $ | — | |||

Note 9—Loan Participations Payable, net

The Company's loan participations payable, net were as follows ($ in thousands):

Carrying Value as of | ||||||||

June 30, 2017 | December 31, 2016 | |||||||

Loan participations payable(1) | $ | 107,844 | $ | 160,251 | ||||

Debt discounts and deferred financing costs, net | (402 | ) | (930 | ) | ||||

Total loan participations payable, net | $ | 107,442 | $ | 159,321 | ||||

_______________________________________________________________________________

(1) | As of June 30, 2017, the Company had two loan participations payable with a weighted average interest rate of 6.2%. As of December 31, 2016, the Company had three loan participations payable with a weighted average interest rate of 4.8%. |

Loan participations represent transfers of financial assets that did not meet the sales criteria established under ASC Topic 860 and are accounted for as loan participations payable, net. As of June 30, 2017 and December 31, 2016, the corresponding loan receivable balances were $107.1 million and $159.1 million, respectively, and are included in "Loans receivable and other lending investments, net" on the Company's consolidated balance sheets. The principal and interest due on these loan participations payable are paid from cash flows of the corresponding loans receivable, which serve as collateral for the participations.

18

Note 10—Debt Obligations, net

The Company's debt obligations were as follows ($ in thousands):

Carrying Value as of | Stated Interest Rates | Scheduled Maturity Date | ||||||||||

June 30, 2017 | December 31, 2016 | |||||||||||

Secured credit facilities and mortgages: | ||||||||||||

2015 $250 Million Secured Revolving Credit Facility | $ | — | $ | — | LIBOR + 2.75% | (1) | March 2018 | |||||

2016 Senior Secured Credit Facility | 498,750 | 498,648 | LIBOR + 3.75% | (2) | July 2020 | |||||||

Mortgages collateralized by net lease assets | 225,624 | 249,987 | 4.851% - 7.26% | (3) | Various through 2032 | |||||||

Total secured credit facilities and mortgages | 724,374 | 748,635 | ||||||||||

Unsecured notes: | ||||||||||||

5.85% senior notes | — | 99,722 | 5.85 | % | March 2017 | |||||||

9.00% senior notes | — | 275,000 | 9.00 | % | June 2017 | |||||||

4.00% senior notes(4) | 550,000 | 550,000 | 4.00 | % | November 2017 | |||||||

7.125% senior notes | 300,000 | 300,000 | 7.125 | % | February 2018 | |||||||

4.875% senior notes(5) | 300,000 | 300,000 | 4.875 | % | July 2018 | |||||||

5.00% senior notes(6) | 770,000 | 770,000 | 5.00 | % | July 2019 | |||||||

6.50% senior notes(7) | 275,000 | 275,000 | 6.50 | % | July 2021 | |||||||

6.00% senior notes(8) | 375,000 | — | 6.00 | % | April 2022 | |||||||

Total unsecured notes | 2,570,000 | 2,569,722 | ||||||||||

Other debt obligations: | ||||||||||||

Trust preferred securities | 100,000 | 100,000 | LIBOR + 1.50% | October 2035 | ||||||||

Total debt obligations | 3,394,374 | 3,418,357 | ||||||||||

Debt discounts and deferred financing costs, net | (26,261 | ) | (28,449 | ) | ||||||||

Total debt obligations, net(9) | $ | 3,368,113 | $ | 3,389,908 | ||||||||

_______________________________________________________________________________

(1) | The loan bears interest at the Company's election of either (i) a base rate, which is the greater of (a) prime, (b) federal funds plus 0.5% or (c) LIBOR plus 1.0% and subject to a margin ranging from 1.25% to 1.75%, or (ii) LIBOR subject to a margin ranging from 2.25% to 2.75%. At maturity, the Company may convert outstanding borrowings to a one year term loan which matures in quarterly installments through March 2019. |

(2) | The loan bears interest at the Company's election of either (i) a base rate, which is the greater of (a) prime, (b) federal funds plus 0.5% or (c) LIBOR plus 1.0% and subject to a margin of 2.75% or (ii) LIBOR subject to a margin of 3.75% with a minimum LIBOR rate of 1.0%. |

(3) | As of June 30, 2017 and December 31, 2016, includes a loan with a floating rate of LIBOR plus 2.0%. As of June 30, 2017, the weighted average interest rate of these loans is 5.2%. |

(4) | The Company can prepay these senior notes without penalty beginning August 1, 2017. |

(5) | The Company can prepay these senior notes without penalty beginning January 1, 2018. |

(6) | The Company can prepay these senior notes without penalty beginning July 1, 2018. |

(7) | The Company can prepay these senior notes without penalty beginning July 1, 2020. |

(8) | The Company can prepay these senior notes without penalty beginning April 1, 2021. |

(9) | The Company capitalized interest relating to development activities of $2.0 million and $4.0 million during the three and six months ended June 30, 2017, respectively, and $1.4 million and $2.8 million during the three and six months ended June 30, 2016, respectively. |

19