Attached files

| file | filename |

|---|---|

| EX-31.2 - CHIEF FINANCIAL OFFICER 302 CERTIFICATION - DYNEGY INC. | dyn-2017630xex312.htm |

| EX-32.2 - CHIEF FINANCIAL OFFICER 906 CERTIFICATION - DYNEGY INC. | dyn-2017630xex322.htm |

| EX-32.1 - CHIEF EXECUTIVE OFFICER 906 CERTIFICATION - DYNEGY INC. | dyn-2017630xex321.htm |

| EX-31.1 - CHIEF EXECUTIVE OFFICER 302 CERTIFICATION - DYNEGY INC. | dyn-2017630xex311.htm |

| EX-10.2 - SECOND AMENDMENT TO LETTER OF CREDIT REIMBURSEMENT AGREEMENT - DYNEGY INC. | dyn-2017630xex102.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

ý QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2017

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________

Commission file number: 001-33443

DYNEGY INC.

(Exact name of registrant as specified in its charter)

State of Incorporation | I.R.S. Employer Identification No. | |

Delaware | 20-5653152 | |

601 Travis, Suite 1400 | ||

Houston, Texas | 77002 | |

(Address of principal executive offices) | (Zip Code) | |

(713) 507-6400

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ý | Accelerated filer o | |

Non-accelerated filer o | Smaller reporting company o | |

(Do not check if a smaller reporting company) | Emerging growth company o | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate by check mark whether the registrant filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes x No ¨

Indicate the number of shares outstanding of our class of common stock, as of the latest practicable date: Common stock, $0.01 par value per share, 131,372,747 shares outstanding as of July 13, 2017.

TABLE OF CONTENTS

Page | ||

Item 1. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 1. | ||

Item 1A. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

DEFINITIONS

As used in this Form 10-Q, the abbreviations contained herein have the meanings set forth below.

ATSI | American Transmission Service, Inc. | |

CAA | Clean Air Act | |

CAISO | The California Independent System Operator | |

CDD | Cooling Degree Days | |

COMED | Commonwealth Edison | |

CPUC | California Public Utility Commission | |

CT | Combustion Turbine | |

EBITDA | Earnings Before Interest, Taxes, Depreciation and Amortization | |

EMAAC | Eastern Mid-Atlantic Area Council | |

EPA | Environmental Protection Agency | |

ERCOT | Electric Reliability Council of Texas | |

FCA | Forward Capacity Auction | |

FERC | Federal Energy Regulatory Commission | |

FTR | Financial Transmission Rights | |

HDD | Heating Degree Days | |

IMA | In-market Asset Availability | |

IPH | IPH, LLC | |

ISO | Independent System Operator | |

ISO-NE | Independent System Operator New England | |

kW | Kilowatt | |

LIBOR | London Interbank Offered Rate | |

MAAC | Mid-Atlantic Area Council | |

MISO | Midcontinent Independent System Operator, Inc. | |

MMBtu | One Million British Thermal Units | |

Moody’s | Moody’s Investors Service Inc. | |

MW | Megawatts | |

MWh | Megawatt Hour | |

NYISO | New York Independent System Operator | |

PJM | PJM Interconnection, LLC | |

PPL | PPL Electric Utilities, Corp. | |

PRIDE | Producing Results through Innovation by Dynegy Employees | |

RGGI | Regional Greenhouse Gas Initiative | |

RTO | Regional Transmission Organization | |

S&P | Standard & Poor’s Ratings Services | |

SEC | U.S. Securities and Exchange Commission | |

i

PART I. FINANCIAL INFORMATION

Item 1—FINANCIAL STATEMENTS

DYNEGY INC.

CONSOLIDATED BALANCE SHEETS

(unaudited) (in millions, except share data)

June 30, 2017 | December 31, 2016 | |||||||

ASSETS | ||||||||

Current Assets | ||||||||

Cash and cash equivalents | $ | 447 | $ | 1,776 | ||||

Restricted cash | — | 62 | ||||||

Accounts receivable, net of allowance for doubtful accounts of $1 and $1, respectively | 441 | 386 | ||||||

Inventory | 477 | 445 | ||||||

Assets from risk management activities | 83 | 130 | ||||||

Intangible assets | 23 | 38 | ||||||

Prepayments and other current assets | 119 | 150 | ||||||

Total Current Assets | 1,590 | 2,987 | ||||||

Property, plant and equipment, net | 9,485 | 7,121 | ||||||

Investment in unconsolidated affiliate | 150 | — | ||||||

Restricted cash | — | 2,000 | ||||||

Assets from risk management activities | 46 | 16 | ||||||

Goodwill | 799 | 799 | ||||||

Intangible assets | 58 | 23 | ||||||

Assets held-for-sale | 463 | — | ||||||

Other long-term assets | 168 | 107 | ||||||

Total Assets | $ | 12,759 | $ | 13,053 | ||||

See the notes to consolidated financial statements.

1

DYNEGY INC.

CONSOLIDATED BALANCE SHEETS

(unaudited) (in millions, except share data)

June 30, 2017 | December 31, 2016 | |||||||

LIABILITIES AND EQUITY | ||||||||

Current Liabilities | ||||||||

Accounts payable | $ | 370 | $ | 332 | ||||

Accrued interest | 116 | 81 | ||||||

Intangible liabilities | 25 | 21 | ||||||

Accrued liabilities and other current liabilities | 154 | 133 | ||||||

Liabilities from risk management activities | 73 | 97 | ||||||

Asset retirement obligations | 59 | 51 | ||||||

Debt, current portion, net | 106 | 201 | ||||||

Total Current Liabilities | 903 | 916 | ||||||

Liabilities subject to compromise (Note 18) | — | 832 | ||||||

Debt, long-term portion, net | 9,211 | 8,778 | ||||||

Liabilities from risk management activities | 48 | 43 | ||||||

Asset retirement obligations | 246 | 236 | ||||||

Deferred income taxes | 30 | 5 | ||||||

Intangible liabilities | 41 | 34 | ||||||

Other long-term liabilities | 161 | 170 | ||||||

Total Liabilities | 10,640 | 11,014 | ||||||

Commitments and Contingencies (Note 13) | ||||||||

Stockholders’ Equity | ||||||||

Preferred stock, $0.01 par value, 20,000,000 shares authorized: | ||||||||

Series A 5.375% mandatory convertible preferred stock, $0.01 par value; 4,000,000 shares issued and outstanding, respectively | 400 | 400 | ||||||

Common stock, $0.01 par value, 420,000,000 shares authorized; 142,691,801 shares issued and 131,365,679 shares outstanding at June 30, 2017; 128,626,740 shares issued and 117,300,618 outstanding at December 31, 2016 | 1 | 1 | ||||||

Additional paid-in capital | 3,320 | 3,547 | ||||||

Accumulated other comprehensive income, net of tax | 28 | 21 | ||||||

Accumulated deficit | (1,626 | ) | (1,927 | ) | ||||

Total Dynegy Stockholders’ Equity | 2,123 | 2,042 | ||||||

Noncontrolling interest | (4 | ) | (3 | ) | ||||

Total Equity | 2,119 | 2,039 | ||||||

Total Liabilities and Equity | $ | 12,759 | $ | 13,053 | ||||

See the notes to consolidated financial statements.

2

DYNEGY INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(unaudited) (in millions, except per share data)

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Revenues | $ | 1,164 | $ | 904 | $ | 2,411 | $ | 2,027 | ||||||||

Cost of sales, excluding depreciation expense | (681 | ) | (493 | ) | (1,438 | ) | (1,038 | ) | ||||||||

Gross margin | 483 | 411 | 973 | 989 | ||||||||||||

Operating and maintenance expense | (282 | ) | (256 | ) | (514 | ) | (477 | ) | ||||||||

Depreciation expense | (209 | ) | (160 | ) | (409 | ) | (331 | ) | ||||||||

Impairments | (99 | ) | (645 | ) | (119 | ) | (645 | ) | ||||||||

Loss on sale of assets, net | (29 | ) | — | (29 | ) | — | ||||||||||

General and administrative expense | (42 | ) | (39 | ) | (82 | ) | (76 | ) | ||||||||

Acquisition and integration costs | (7 | ) | 3 | (52 | ) | (1 | ) | |||||||||

Other | 3 | (16 | ) | 1 | (16 | ) | ||||||||||

Operating loss | (182 | ) | (702 | ) | (231 | ) | (557 | ) | ||||||||

Bankruptcy reorganization items (Note 18) | (1 | ) | — | 482 | — | |||||||||||

Earnings from unconsolidated investments | 1 | 1 | — | 3 | ||||||||||||

Interest expense | (159 | ) | (141 | ) | (326 | ) | (283 | ) | ||||||||

Other income and expense, net | 29 | 30 | 46 | 31 | ||||||||||||

Loss before income taxes | (312 | ) | (812 | ) | (29 | ) | (806 | ) | ||||||||

Income tax benefit (expense) (Note 14) | 16 | 9 | 329 | (7 | ) | |||||||||||

Net income (loss) | (296 | ) | (803 | ) | 300 | (813 | ) | |||||||||

Less: Net loss attributable to noncontrolling interest | — | (2 | ) | (1 | ) | (2 | ) | |||||||||

Net income (loss) attributable to Dynegy Inc. | (296 | ) | (801 | ) | 301 | (811 | ) | |||||||||

Less: Dividends on preferred stock | 6 | 6 | 11 | 11 | ||||||||||||

Net income (loss) attributable to Dynegy Inc. common stockholders | $ | (302 | ) | $ | (807 | ) | $ | 290 | $ | (822 | ) | |||||

Earnings (Loss) Per Share (Note 16): | ||||||||||||||||

Basic earnings (loss) per share attributable to Dynegy Inc. common stockholders | $ | (1.96 | ) | $ | (6.73 | ) | $ | 1.91 | $ | (6.97 | ) | |||||

Diluted earnings (loss) per share attributable to Dynegy Inc. common stockholders | $ | (1.96 | ) | $ | (6.73 | ) | $ | 1.76 | $ | (6.97 | ) | |||||

Basic shares outstanding | 154 | 120 | 152 | 118 | ||||||||||||

Diluted shares outstanding | 154 | 120 | 171 | 118 | ||||||||||||

See the notes to consolidated financial statements.

3

DYNEGY INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(unaudited) (in millions)

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||

Net income (loss) | $ | (296 | ) | $ | (803 | ) | $ | 300 | $ | (813 | ) | |||||

Other comprehensive income (loss) before reclassifications: | ||||||||||||||||

Actuarial gain and plan amendment (net of tax of $4, zero, $4, and zero for each respective period) | (4 | ) | — | 11 | — | |||||||||||

Amounts reclassified from accumulated other comprehensive income: | ||||||||||||||||

Amortization of unrecognized prior service credit (net of tax of zero for each respective period) | (2 | ) | (1 | ) | (4 | ) | (2 | ) | ||||||||

Other comprehensive income (loss), net of tax | (6 | ) | (1 | ) | 7 | (2 | ) | |||||||||

Comprehensive income (loss) | (302 | ) | (804 | ) | 307 | (815 | ) | |||||||||

Less: Comprehensive loss attributable to noncontrolling interest | — | (2 | ) | (1 | ) | (2 | ) | |||||||||

Total comprehensive income (loss) attributable to Dynegy Inc. | $ | (302 | ) | $ | (802 | ) | $ | 308 | $ | (813 | ) | |||||

See the notes to consolidated financial statements.

4

DYNEGY INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(unaudited) (in millions)

Six Months Ended June 30, | ||||||||

2017 | 2016 | |||||||

CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

Net income (loss) | $ | 300 | $ | (813 | ) | |||

Adjustments to reconcile net income (loss) to net cash flows from operating activities: | ||||||||

Depreciation expense | 409 | 331 | ||||||

Non-cash interest expense | 32 | 23 | ||||||

Amortization of intangibles | 15 | 13 | ||||||

Risk management activities | (1 | ) | (89 | ) | ||||

Loss on sale of assets, net | 29 | — | ||||||

Earnings from unconsolidated investments | — | (3 | ) | |||||

Deferred income taxes | (329 | ) | 7 | |||||

Impairments | 119 | 645 | ||||||

Change in value of common stock warrants | (15 | ) | (2 | ) | ||||

Bankruptcy reorganization items | (482 | ) | — | |||||

Other | 29 | 18 | ||||||

Changes in working capital: | ||||||||

Accounts receivable, net | (13 | ) | 15 | |||||

Inventory | 76 | 77 | ||||||

Prepayments and other current assets | 44 | 156 | ||||||

Accounts payable and accrued liabilities | 17 | 8 | ||||||

Changes in non-current assets | (1 | ) | (12 | ) | ||||

Changes in non-current liabilities | 1 | 1 | ||||||

Net cash provided by operating activities | 230 | 375 | ||||||

CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

Capital expenditures | (86 | ) | (286 | ) | ||||

Acquisitions, net of cash acquired | (3,263 | ) | — | |||||

Distributions from unconsolidated investments | 2 | 8 | ||||||

Other investing | 1 | 7 | ||||||

Net cash used in investing activities | (3,346 | ) | (271 | ) | ||||

CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

Proceeds from long-term borrowings, net of debt issuance costs | 425 | 2,278 | ||||||

Repayments of borrowings | (331 | ) | (20 | ) | ||||

Proceeds from issuance of equity, net of issuance costs | 150 | 362 | ||||||

Preferred stock dividends paid | (11 | ) | (11 | ) | ||||

Interest rate swap settlement payments | (9 | ) | (9 | ) | ||||

Acquisition of noncontrolling interest | (375 | ) | — | |||||

Payments related to bankruptcy settlement | (123 | ) | — | |||||

Other financing | (1 | ) | (2 | ) | ||||

Net cash provided by (used in) financing activities | (275 | ) | 2,598 | |||||

Net increase (decrease) in cash, cash equivalents and restricted cash | (3,391 | ) | 2,702 | |||||

Cash, cash equivalents and restricted cash, beginning of period | 3,838 | 544 | ||||||

Cash, cash equivalents and restricted cash, end of period | $ | 447 | $ | 3,246 | ||||

See the notes to consolidated financial statements.

5

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

Note 1—Basis of Presentation and Organization

The accompanying unaudited consolidated financial statements have been prepared in accordance with the instructions to interim financial reporting as prescribed by the SEC. The year-end consolidated balance sheet data was derived from audited consolidated financial statements, but does not include all disclosures required by the Generally Accepted Accounting Principles of the United States of America (“GAAP”). The unaudited consolidated financial statements contained in this report include all material adjustments of a normal recurring nature that, in the opinion of management, are necessary for a fair presentation of the results for the interim periods. Certain prior period amounts in our unaudited consolidated financial statements have been reclassified to conform to current year presentation. These interim financial statements should be read together with the consolidated financial statements and notes thereto included in our annual report on Form 10-K for the year ended December 31, 2016, filed with the SEC on February 24, 2017, which we refer to as our “Form 10-K.” Unless the context indicates otherwise, throughout this report, the terms “Dynegy,” “the Company,” “we,” “us,” “our,” and “ours” are used to refer to Dynegy Inc. and its direct and indirect subsidiaries.

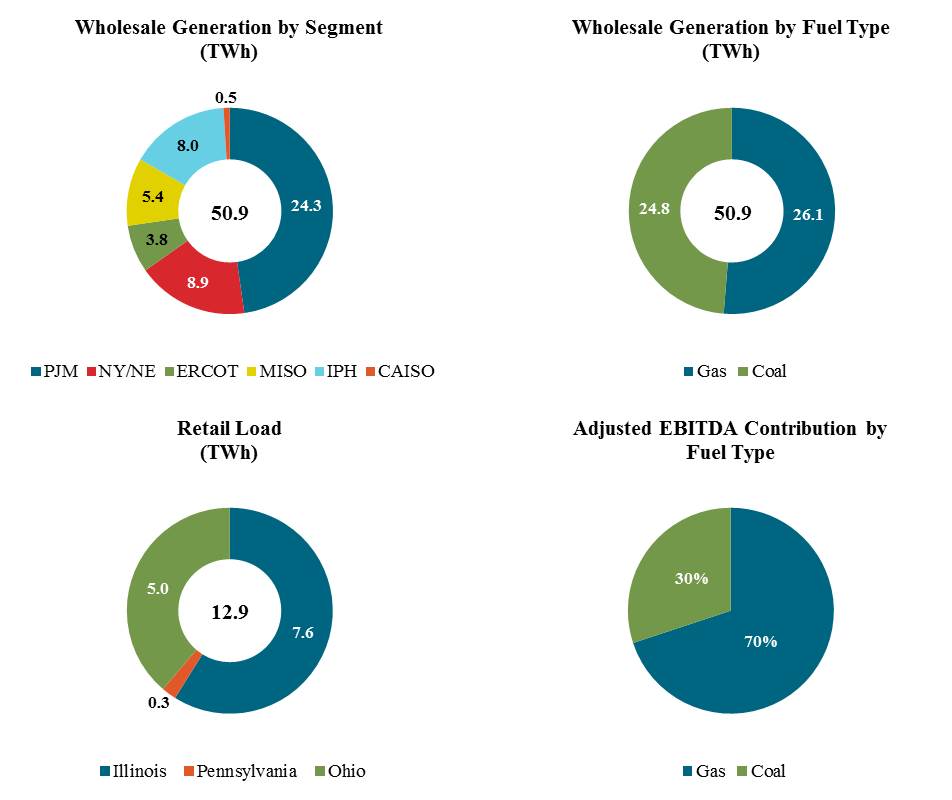

We sell electric energy, capacity and ancillary services primarily on a wholesale basis from our power generation facilities. We also serve residential, municipal, commercial and industrial customers primarily in MISO and PJM through our Homefield Energy and Dynegy Energy Services retail businesses. We report the results of our power generation business as six segments in our unaudited consolidated financial statements: (i) PJM, (ii) ISO-NE/NYISO (“NY/NE”), (iii) ERCOT, (iv) MISO, (v) IPH, and (vi) CAISO. Our consolidated financial results also reflect corporate-level expenses such as general and administrative expense, interest expense, and income tax benefit (expense). All significant intercompany transactions have been eliminated. Please read Note 19—Segment Information for further discussion.

On February 2, 2017 (the “Emergence Date”), Illinois Power Generating Company (“Genco”) emerged from bankruptcy. Please read Note 18—Genco Chapter 11 Bankruptcy and Emergence for further discussion.

Note 2—Accounting Policies

The accounting policies followed by the Company are set forth in Note 2—Summary of Significant Accounting Policies in our Form 10-K. The accompanying unaudited consolidated financial statements include our accounts and the accounts of our majority-owned or controlled subsidiaries. Accounting policies for all of our operations are in accordance with GAAP. Except for the adoption of new policies as described below, there have been no significant changes to our accounting policies during the six months ended June 30, 2017.

Use of Estimates. The preparation of unaudited consolidated financial statements in conformity with GAAP requires management to make informed estimates and judgments that affect our reported financial position and results of operations based on currently available information. Actual results could differ materially from our estimates. The results of operations for the interim periods presented in this Form 10-Q are not necessarily indicative of the results to be expected for the full year or any other interim period due to seasonal fluctuations in demand for our energy products and services, changes in commodity prices, timing of maintenance and other expenditures, and other factors.

Accounting Standards Adopted

Statement of Cash Flows. In August 2016, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2016-15-Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments. To reduce current and future diversity in practice, the amendments in this ASU provide guidance for several cash flow classification issues identified where current GAAP is either unclear or does not include specific guidance. We adopted this ASU on January 1, 2017 and applied the amendments on a retrospective basis. The adoption of this ASU affected the classification of prepayments for future planned outage work performed under long-term service agreements. The majority of the cash prepayments required under these agreements will now be reflected as cash outflows from investing activities and the remainder will be classified as cash outflows from operating activities, based on whether they are anticipated to be expensed or capitalized. As a result of the retrospective application of this ASU, we reclassified approximately $62 million of cash prepayments from operating activities to investing activities in our unaudited consolidated statement of cash flows for the six months ended June 30, 2016.

In November 2016, the FASB issued ASU 2016-18-Statement of Cash Flows (Topic 230): Restricted Cash. The amendments in this ASU require that a statement of cash flows explain the change during the period in the total of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents. Therefore, amounts generally

6

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

described as restricted cash and restricted cash equivalents should be included with cash and cash equivalents when reconciling the beginning-of-period and end-of-period total amounts shown on the statement of cash flows. We adopted this ASU as of January 1, 2017 and applied the amendments on a retrospective basis. As a result of the retrospective application of this ASU, changes in restricted cash of $4 million and $2.069 billion previously reflected as cash flows from operating activities and investing activities, respectively, are now reflected in Net increase (decrease) in cash, cash equivalents, and restricted cash in our unaudited consolidated statement of cash flows for the six months ended June 30, 2016. Additionally, restricted cash of $39 million and $2.104 billion are now reflected in the beginning of period and end of period cash, cash equivalents and restricted cash line items, respectively, in our unaudited consolidated statement of cash flows for the six months ended June 30, 2016. Please read Note 7—Cash Flow Information for further discussion.

Compensation. In March 2016, the FASB issued ASU 2016-09-Compensation-Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting. The amendments in this ASU simplify several aspects of the accounting for share-based payment transactions, including the income tax consequences, classification of awards as either equity or liabilities and classification on the statement of cash flows. We adopted this ASU on January 1, 2017 with no material impact on our unaudited consolidated financial statements.

Goodwill. In January 2017, the FASB issued ASU 2017-04-Intangibles-Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment. To simplify the subsequent measure of goodwill, the amendments in this ASU eliminate step two from the goodwill impairment test. An entity will no longer be required to calculate the implied fair value of goodwill by assigning the fair value of a reporting unit to all of its assets and liabilities as if the reporting unit had been acquired in a business combination to determine the impairment of goodwill. The amendments in this ASU will now require goodwill impairment to be measured by the amount by which the carrying value of the reporting unit exceeds its fair value. The guidance in this ASU is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2019. Upon adoption, an entity shall apply the guidance in this ASU prospectively with early adoption permitted for annual goodwill tests performed after January 1, 2017. We adopted this ASU on January 1, 2017 with no material impact on our unaudited consolidated financial statements.

Accounting Standards Not Yet Adopted

Financial Instruments with Down Round Features. In July 2017, the FASB issued ASU 2017-11, Earnings Per Share (Topic 260); Distinguishing Liabilities from Equity (Topic 480); Derivatives and Hedging (Topic 815): Accounting for Certain Financial Instruments with Down Round Features. The amendments of this ASU update the classification analysis of certain equity-linked financial instruments, or embedded features, with down round features, as well as clarify existing disclosure requirements for equity-classified instruments. When determining whether certain financial instruments should be classified as liabilities or equity instruments, a down round feature no longer precludes equity classification when assessing whether the instrument is indexed to an entity’s own stock. The guidance in this ASU is effective for fiscal years beginning after December 15, 2019, and interim periods within fiscal years beginning after December 15, 2020, with early adoption permitted. We are currently evaluating this ASU and any potential impacts the adoption will have on our unaudited consolidated financial statements.

Business Combinations. In January 2017, the FASB issued ASU 2017-01-Business Combinations (Topic 805): Clarifying the Definition of a Business. The amendments in this ASU clarify the definition of a business. The amendments affect all companies and other reporting organizations that must determine whether they have acquired or sold a business. The guidance in this ASU is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2017, with early adoption permitted. We are currently evaluating this ASU and any potential impacts the adoption will have on our unaudited consolidated financial statements.

Pensions. In March 2017, the FASB issued ASU No. 2017-07, Compensation-Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost. The amendments of this ASU require an entity to report the service cost component of net benefit costs in the same line item as other compensation costs arising from services rendered by the related employees during the applicable service period. The other components of net benefit cost are required to be presented separately from the service cost component and below the subtotal of operating income. Additionally, only the service cost component of net benefit costs is eligible for capitalization. The guidance in this ASU is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2017, with early adoption permitted. The adoption of this standard must be applied on a retrospective basis for the amendments concerning income statement presentation and on a prospective basis for the amendments regarding the capitalization of the service cost component. We are currently evaluating this ASU and any potential impacts the adoption will have on our unaudited consolidated financial statements.

7

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

Leases. In February 2016, the FASB issued ASU 2016-02-Leases (Topic 842). The provisions in this ASU will require lessees to recognize lease assets and lease liabilities, for all leases, including operating leases, on the balance sheet. The lease assets recognized in the balance sheet will represent a right-of-use asset, which is an asset that represents the lessee’s right to use, or control the use of, a specified asset for the lease term. The lease liability recognized in the balance sheet will represent the lessee’s obligation to make lease payments arising from a lease, measured based on the present value of the minimum rental payments. Entities may make an accounting policy election to not recognize lease assets or lease liabilities for leases with a term of 12 months or less. The guidance in this ASU is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018, with early adoption permitted. We are currently evaluating this ASU and any potential impacts the adoption will have on our unaudited consolidated financial statements.

Revenue from Contracts with Customers. In May 2014, the FASB issued ASU 2014-09-Revenue from Contracts with Customers (Topic 606). This ASU supersedes current revenue recognition requirements and industry specific guidance and develops a common revenue recognition standard whereby an entity will recognize revenue when it transfers promised goods or services to customers in an amount that reflects the consideration the entity expects to be entitled to in exchange for those goods or services. Additional disclosures will be required to describe the nature, amount, timing, and uncertainty of revenues and cash flows from contracts with customers. The guidance in this ASU and its amendments are effective for interim and annual periods beginning after December 15, 2017, with early adoption permitted for interim and annual periods beginning after December 15, 2016. We have established an implementation team to assess the impact the new accounting standard will have on our financial statements upon adoption and have not currently identified any material changes to the timing of our revenue recognition. We continue to assess the impact of the standard by reviewing our revenue contracts to determine if changes in our recognition policies or controls are necessary. We believe changes to our disclosures will primarily include a regional presentation of our revenues disaggregated by revenue type - energy, capacity, and ancillary services.

Note 3—Acquisitions and Divestitures

Acquisition

ENGIE Acquisition. On February 7, 2017 (the “ENGIE Acquisition Closing Date”), pursuant to the terms of the stock purchase agreement, as amended and restated on June 27, 2016, (the “ENGIE Acquisition Stock Purchase Agreement”), Dynegy acquired approximately 9,017 MW of generation from GDF SUEZ Energy North America, Inc. (“GSENA”) and International Power, S.A. (the “Seller”), including (i) 15 natural gas-fired facilities located in Illinois, Massachusetts, New Jersey, Ohio, Pennsylvania, Texas, Virginia, and West Virginia, (ii) one coal-fired facility in Texas, and (iii) one waste coal-fired facility in Pennsylvania for a base purchase price of approximately $3.3 billion in cash, subject to certain adjustments (the “ENGIE Acquisition”).

Business Combination Accounting. The ENGIE Acquisition has been accounted for in accordance with ASC 805, Business Combinations, with identifiable assets acquired and liabilities assumed recorded at their estimated fair values on the acquisition date, February 7, 2017. A summary of the various techniques used to fair value the identifiable assets and liabilities, as well as their classification within the fair value hierarchy are listed below.

• | Working capital was valued using available market information (Level 2). |

• | Acquired property, plant and equipment (“PP&E”), excluding those assets classified as held-for-sale, was valued using a discounted cash flow (“DCF”) analysis based upon a debt-free, free cash flow model (Level 3). The DCF model was created for each power generation facility based on its remaining useful life, and: |

◦ | for the years 2017 and 2018, included gross margin forecasts using quoted forward commodity market prices; |

◦ | for the years 2019 through 2026, we used gross margin forecasts based upon commodity and capacity price curves developed internally using forward New York Mercantile Exchange natural gas prices and supply and demand factors; |

◦ | for periods beyond 2026, we assumed a 2.5 percent growth rate. |

We also used management’s forecasts of operations and maintenance expense, general and administrative expense, as well as capital expenditures for the years 2017 through 2021, and for years thereafter assumed a 2.5 percent growth rate. These cash flows were discounted using discount rates of approximately 9 percent to 13 percent for gas-fired, and approximately 13 percent to 14 percent for coal-fired, generation facilities, based upon the plant’s age, efficiency, region, and years until retirement.

• | Acquired PP&E classified as held-for-sale was valued based upon the sale price of the assets (Level 2). |

8

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

• | Acquired derivatives were valued using the methods described in Note 6—Fair Value Measurements (Level 2 or Level 3). |

• | Contracts with terms that were not at current market prices were also valued using a DCF analysis (Level 3). The cash flows generated by the contracts were compared with their cash flows based on current market prices with the resulting difference recorded as either an intangible asset or liability. |

• | Asset retirement obligations (“AROs”) were recorded in accordance with ASC 410, Asset Retirement and Environmental Obligations (Level 3). |

The accounting for the ENGIE Acquisition is not complete because certain information and analysis that may impact our initial valuation is still being obtained or reviewed. Dynegy expects to finalize these amounts during the first quarter of 2018. The significant assets and liabilities for which provisional amounts are recognized are PP&E, deferred income taxes and taxes other than deferred income taxes. Additionally, some taxes have not yet been finalized with the associated taxing jurisdictions, resulting in a potential change to their fair value at acquisition. These changes may also impact the fair value of the acquired PP&E or deferred tax liability. As such, the provisional amounts recognized are subject to revision until our valuation is completed, not to exceed one year from the ENGIE Acquisition Closing Date, and any material adjustments identified that existed as of the acquisition date will be recognized in the period in which they are identified.

The following table summarizes the consideration paid and the provisional fair value amounts recognized for the assets acquired and liabilities assumed related to the ENGIE Acquisition, as of the acquisition date, February 7, 2017:

(amounts in millions) | ||||

Base purchase price | $ | 3,300 | ||

Working capital adjustments and other | (31 | ) | ||

Fair value of total consideration transferred | $ | 3,269 | ||

Cash | $ | 20 | ||

Accounts receivable | 22 | |||

Inventory | 101 | |||

Prepayments and other current assets | 3 | |||

Assets from risk management activities (including current portion of $21 million) | 25 | |||

Property, plant and equipment | 2,756 | |||

Investment in unconsolidated affiliate | 152 | |||

Intangible assets (including current portion of $7 million) | 50 | |||

Assets held-for-sale | 445 | |||

Other long-term assets | 131 | |||

Total assets acquired | 3,705 | |||

Accounts payable | 28 | |||

Liabilities from risk management activities (including current portion of $13 million) | 16 | |||

Asset retirement obligations | 19 | |||

Intangible liabilities (including current portion of $16 million) | 30 | |||

Deferred income taxes, net | 342 | |||

Other long-term liabilities | 1 | |||

Total liabilities assumed | 436 | |||

Net assets acquired | $ | 3,269 | ||

9

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

The following table summarizes certain information related to the ENGIE Acquisition, which is included in our unaudited consolidated statements of operations:

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

(amounts in millions) | 2017 | 2016 | 2017 | 2016 | ||||||||||||

Acquisition costs | $ | 4 | $ | — | $ | 35 | $ | 2 | ||||||||

Revenues | $ | 246 | N/A | $ | 324 | N/A | ||||||||||

Operating income | $ | 20 | N/A | $ | 4 | N/A | ||||||||||

Pro Forma Results. The unaudited pro forma financial results for the six months ended June 30, 2017 and 2016 assume the ENGIE Acquisition occurred on January 1, 2016. The unaudited pro forma financial results may not be indicative of the results that would have occurred had the acquisition been completed as of January 1, 2016, nor are they indicative of future results of operations. The unaudited pro forma financial results for the six months ended June 30, 2017 and 2016 include adjustments of $35 million and $2 million, respectively, for non-recurring acquisition costs attributable to the ENGIE Acquisition.

Six Months Ended June 30, | ||||||||

(amounts in millions) | 2017 | 2016 | ||||||

Revenue | $ | 2,468 | $ | 2,315 | ||||

Net income (loss) | $ | 302 | $ | (948 | ) | |||

Net income (loss) attributable to Dynegy Inc. | $ | 303 | $ | (946 | ) | |||

AER Acquisition. On April 12, 2017, we received approximately $25 million of cash related to the 2013 AER Acquisition. As a result, we have recorded $25 million in Other income and expense, net in our unaudited consolidated statement of operations.

Divestitures

On July 11, 2017, Dynegy completed the sale of its equity ownership interests in two peaking facilities in PJM to LS Power (the “Troy and Armstrong Sale”) for approximately $480 million in cash, plus adjustments for capital expenditures and working capital. The facilities sold were recently acquired in the ENGIE Acquisition and total 1,269 MW. The proceeds are to be allocated to debt reduction.

The Troy and Armstrong facilities are classified as long-term assets held-for-sale as of June 30, 2017 and are presented below, in millions:

Inventory | $ | 11 | ||

Property, plant & equipment | 452 | |||

Assets held-for-sale | $ | 463 | ||

Note 4—Unconsolidated Investments

Equity Method Investments

NELP. In connection with the ENGIE Acquisition, we acquired a 50 percent interest in Northeast Energy, LP (“NELP”), a joint venture with NextEra Energy, Inc., which indirectly owns the Bellingham NEA facility and the Sayreville facility. At June 30, 2017, our equity method investment in NELP included in our unaudited consolidated balance sheets was $150 million. Upon the acquisition, we recognized basis differences in the net assets of approximately $14 million related to PP&E. These basis differences are being amortized over their respective useful lives. Our risk of loss related to our equity method investment is limited to our investment balance.

For the three and six months ended June 30, 2017, we recorded $1 million and less than $1 million in equity earnings, respectively, related to our investment in NELP which is reflected in Earnings from unconsolidated investments in our unaudited consolidated statements of operations. For the six months ended June 30, 2017, we received a distribution of $2 million, all of which was considered to be a return of investment using the cumulative earnings approach and reflected as Distributions from unconsolidated investments in our unaudited consolidated statements of cash flows.

10

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

Elwood. On November 21, 2016, Dynegy sold its 50 percent equity interest in Elwood Energy, LLC, a limited liability company (“Elwood Energy”) and Elwood Expansion LLC, a limited liability company (and together with Elwood Energy “Elwood”), to J-Power USA Development Co. Ltd. for approximately $173 million (the “Elwood Sale”).

For the three and six months ended June 30, 2016, we recorded $1 million and $3 million, respectively, in equity earnings related to our investment in Elwood which is reflected in Earnings from unconsolidated investments in our unaudited consolidated statements of operations. For the six months ended June 30, 2016, we received distributions of $8 million, all of which was considered to be a return of investment using the accumulated earnings approach and reflected as Distributions from unconsolidated investments in our unaudited consolidated statements of cash flows.

Note 5—Risk Management Activities, Derivatives and Financial Instruments

The nature of our business involves commodity market and financial risks. Specifically, we are exposed to commodity price variability related to our power generation business. Our commercial team manages these commodity price risks with financially and physically settled contracts consistent with our commodity risk management policy. Our treasury team manages our interest rate risk.

Our commodity risk management policy gives us the flexibility to sell energy and capacity and purchase fuel through a combination of spot market sales and near-term contractual arrangements (generally over a rolling one- to three-year time frame). Our commodity risk management goal is to protect cash flow in the near-term while keeping the ability to capture value longer-term.

Many of our contractual arrangements are derivative instruments and are accounted for at fair value as part of Revenues in our unaudited consolidated statements of operations. We have other contractual arrangements such as capacity forward sales arrangements, tolling arrangements, fixed price coal purchases, and retail power sales, which do not receive recurring fair value accounting treatment because these arrangements do not meet the definition of a derivative or are designated as “normal purchase, normal sale,” in accordance with ASC 815, Derivatives and Hedging. As a result, the gains and losses with respect to these arrangements are not reflected in the unaudited consolidated statements of operations until the delivery occurs.

Quantitative Disclosures Related to Financial Instruments and Derivatives

As of June 30, 2017, we had net purchases and sales of derivative contracts outstanding in the following quantities:

Contract Type | Quantity | Unit of Measure | Fair Value (1) | ||||||

(dollars and quantities in millions) | Purchases (Sales) | Asset (Liability) | |||||||

Commodity contracts: | |||||||||

Electricity derivatives (2) | (65 | ) | MWh | $ | 40 | ||||

Electricity basis derivatives (3) | (46 | ) | MWh | $ | (9 | ) | |||

Natural gas derivatives (2) | 410 | MMBtu | $ | (17 | ) | ||||

Natural gas basis derivatives | 135 | MMBtu | $ | (15 | ) | ||||

Physical heat rate derivatives | 142/(15) | MMBtu/MWh | $ | (11 | ) | ||||

Emissions derivatives | 14 | Metric Ton | $ | (8 | ) | ||||

Interest rate swaps | 1,965 | U.S. Dollar | $ | (18 | ) | ||||

Common stock warrants (4) | 24 | Warrant | $ | (3 | ) | ||||

__________________________________________

(1) | Includes both asset and liability risk management positions but excludes margin and collateral netting of $46 million. |

(2) | Mainly comprised of swaps and physical forwards. |

(3) | Comprised of FTRs and swaps. |

(4) | Each warrant is convertible into one share of Dynegy common stock. |

11

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

Derivatives on the Balance Sheet. The following tables present the fair value and balance sheet classification of derivatives in our unaudited consolidated balance sheets as of June 30, 2017 and December 31, 2016. As of June 30, 2017 and December 31, 2016, there were no gross amounts available to be offset that were not offset in our unaudited consolidated balance sheets.

June 30, 2017 | |||||||||||||||||||

Gross amounts offset in the balance sheet | |||||||||||||||||||

Contract Type | Balance Sheet Location | Gross Fair Value | Contract Netting | Collateral or Margin Received or Paid | Net Fair Value | ||||||||||||||

(amounts in millions) | |||||||||||||||||||

Derivative assets: | |||||||||||||||||||

Commodity contracts | Assets from risk management activities | $ | 300 | $ | (182 | ) | $ | — | $ | 118 | |||||||||

Interest rate contracts | Assets from risk management activities | 11 | — | — | 11 | ||||||||||||||

Total derivative assets | $ | 311 | $ | (182 | ) | $ | — | $ | 129 | ||||||||||

Derivative liabilities: | |||||||||||||||||||

Commodity contracts | Liabilities from risk management activities | $ | (320 | ) | $ | 182 | $ | 46 | $ | (92 | ) | ||||||||

Interest rate contracts | Liabilities from risk management activities | (29 | ) | — | — | (29 | ) | ||||||||||||

Common stock warrants | Accrued liabilities and other current liabilities and other long-term liabilities | (3 | ) | — | — | (3 | ) | ||||||||||||

Total derivative liabilities | $ | (352 | ) | $ | 182 | $ | 46 | $ | (124 | ) | |||||||||

Total derivatives | $ | (41 | ) | $ | — | $ | 46 | $ | 5 | ||||||||||

December 31, 2016 | |||||||||||||||||||

Gross amounts offset in the balance sheet | |||||||||||||||||||

Contract Type | Balance Sheet Location | Gross Fair Value | Contract Netting | Collateral or Margin Received or Paid | Net Fair Value | ||||||||||||||

(amounts in millions) | |||||||||||||||||||

Derivative assets: | |||||||||||||||||||

Commodity contracts | Assets from risk management activities | $ | 311 | $ | (165 | ) | $ | — | $ | 146 | |||||||||

Total derivative assets | $ | 311 | $ | (165 | ) | $ | — | $ | 146 | ||||||||||

Derivative liabilities: | |||||||||||||||||||

Commodity contracts | Liabilities from risk management activities | $ | (329 | ) | $ | 165 | $ | 54 | $ | (110 | ) | ||||||||

Interest rate contracts | Liabilities from risk management activities | (30 | ) | — | — | (30 | ) | ||||||||||||

Common stock warrants | Accrued liabilities and other current liabilities | (1 | ) | — | — | (1 | ) | ||||||||||||

Total derivative liabilities | $ | (360 | ) | $ | 165 | $ | 54 | $ | (141 | ) | |||||||||

Total derivatives | $ | (49 | ) | $ | — | $ | 54 | $ | 5 | ||||||||||

Certain of our derivative instruments have credit limits that require us to post collateral. The amount of collateral required to be posted is a function of the net liability position of the derivative as well as our established credit limit with the respective counterparty. If our credit rating were to worsen, the counterparties could require us to post additional collateral. The amount of additional collateral that would be required to be posted would vary depending on the extent of change in our credit rating as well as the requirements of the individual counterparty. As of June 30, 2017, the aggregate fair value of all commodity derivative instruments containing credit-risk-related contingent features, in a liability position and not fully collateralized, is $15 million for which we have posted no collateral. Transactions with our clearing brokers are excluded as they are fully collateralized. Our

12

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

remaining derivative instruments do not have credit-related collateral contingencies as they are included within our first-lien collateral program.

The following table summarizes our cash collateral posted as of June 30, 2017 and December 31, 2016, within Prepayments and other current assets in our unaudited consolidated balance sheets and the amount applied against short-term risk management activities:

Location on Balance Sheet | June 30, 2017 | December 31, 2016 | ||||||

(amounts in millions) | ||||||||

Gross collateral posted with counterparties | $ | 80 | $ | 116 | ||||

Less: Collateral netted against risk management liabilities | 46 | 54 | ||||||

Net collateral within Prepayments and other current assets | $ | 34 | $ | 62 | ||||

Impact of Derivatives on the Unaudited Consolidated Statements of Operations

We elect not to designate derivatives related to our power generation business and interest rate instruments as cash flow or fair value hedges. Thus, we account for changes in the fair value of these derivatives within our unaudited consolidated statements of operations.

Our unaudited consolidated statements of operations for the three and six months ended June 30, 2017 and 2016 include the impact of derivative financial instruments as presented below:

Derivatives Not Designated as Hedges | Location of Gain (Loss) Recognized in Income on Derivatives | Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

2017 | 2016 | 2017 | 2016 | |||||||||||||||

(amounts in millions) | ||||||||||||||||||

Commodity contracts | Revenues | $ | 29 | $ | 23 | $ | 213 | $ | 215 | |||||||||

Interest rate contracts | Interest expense | $ | 1 | $ | (4 | ) | $ | 3 | $ | (12 | ) | |||||||

Common stock warrants | Other income and (expense), net | $ | 3 | $ | — | $ | 15 | $ | 1 | |||||||||

Note 6—Fair Value Measurements

We apply the market approach for recurring fair value measurements, employing valuation techniques that maximize the use of observable inputs and minimize the use of unobservable inputs. We have consistently used the same valuation techniques for all periods presented. Please read Note 2—Summary of Significant Accounting Policies—Fair Value Measurements in our Form 10-K for further discussion.

13

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

The following tables set forth, by level within the fair value hierarchy, our financial assets and liabilities that were accounted for at fair value on a recurring basis as of June 30, 2017 and December 31, 2016, and are presented on a gross basis before consideration of amounts netted under master netting agreements and the application of collateral and margin paid:

Fair Value as of June 30, 2017 | ||||||||||||||||

(amounts in millions) | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Assets: | ||||||||||||||||

Assets from commodity risk management activities: | ||||||||||||||||

Electricity derivatives | $ | — | $ | 195 | $ | 15 | $ | 210 | ||||||||

Natural gas derivatives | — | 66 | 9 | 75 | ||||||||||||

Physical heat rate derivatives | — | 13 | — | 13 | ||||||||||||

Emissions derivatives | — | 2 | — | 2 | ||||||||||||

Total assets from commodity risk management activities | — | 276 | 24 | 300 | ||||||||||||

Assets from interest rate contracts | — | 11 | — | 11 | ||||||||||||

Total assets | $ | — | $ | 287 | $ | 24 | $ | 311 | ||||||||

Liabilities: | . | |||||||||||||||

Liabilities from commodity risk management activities: | ||||||||||||||||

Electricity derivatives | $ | — | $ | (163 | ) | $ | (16 | ) | $ | (179 | ) | |||||

Natural gas derivatives | — | (99 | ) | (8 | ) | (107 | ) | |||||||||

Physical heat rate derivatives | — | (22 | ) | (2 | ) | (24 | ) | |||||||||

Emissions derivatives | — | (10 | ) | — | (10 | ) | ||||||||||

Total liabilities from commodity risk management activities | — | (294 | ) | (26 | ) | (320 | ) | |||||||||

Liabilities from interest rate contracts | — | (29 | ) | — | (29 | ) | ||||||||||

Liabilities from outstanding common stock warrants | (3 | ) | — | — | (3 | ) | ||||||||||

Total liabilities | $ | (3 | ) | $ | (323 | ) | $ | (26 | ) | $ | (352 | ) | ||||

Fair Value as of December 31, 2016 | ||||||||||||||||

(amounts in millions) | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Assets: | ||||||||||||||||

Assets from commodity risk management activities: | ||||||||||||||||

Electricity derivatives | $ | — | $ | 118 | $ | 20 | $ | 138 | ||||||||

Natural gas derivatives | — | 169 | 4 | 173 | ||||||||||||

Total assets from commodity risk management activities | $ | — | $ | 287 | $ | 24 | $ | 311 | ||||||||

Liabilities: | ||||||||||||||||

Liabilities from commodity risk management activities: | ||||||||||||||||

Electricity derivatives | $ | — | $ | (245 | ) | $ | (12 | ) | $ | (257 | ) | |||||

Natural gas derivatives | — | (52 | ) | (10 | ) | (62 | ) | |||||||||

Emissions derivatives | — | (10 | ) | — | (10 | ) | ||||||||||

Total liabilities from commodity risk management activities | — | (307 | ) | (22 | ) | (329 | ) | |||||||||

Liabilities from interest rate contracts | — | (30 | ) | — | (30 | ) | ||||||||||

Liabilities from outstanding common stock warrants | (1 | ) | — | — | (1 | ) | ||||||||||

Total liabilities | $ | (1 | ) | $ | (337 | ) | $ | (22 | ) | $ | (360 | ) | ||||

Level 3 Valuation Methods. The electricity derivatives classified within Level 3 include financial swaps executed in illiquid trading locations or on long dated contracts, capacity contracts and FTRs. The curves used to generate the fair value of the financial swaps are based on basis adjustments applied to forward curves for liquid trading points, while the curves for the capacity deals are based upon auction results in the marketplace, which are infrequently executed. The forward market price of FTRs is derived using historical congestion patterns within the marketplace and heat rate derivative valuations are derived using

14

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

a discounted cash flow model, which uses modeled forward natural gas and power prices. The natural gas derivatives classified within Level 3 include financial swaps, basis swaps, and physical purchases executed in illiquid trading locations or on long dated contracts.

Sensitivity to Changes in Significant Unobservable Inputs for Level 3 Valuations. The significant unobservable inputs used in the fair value measurement of our commodity instruments categorized within Level 3 of the fair value hierarchy include estimates of forward congestion, power price spreads, and natural gas pricing, and the difference between our plant locational prices to liquid hub prices. Power price spreads, and natural gas pricing, and the difference between our plant locational prices to liquid hub prices are generally based on observable markets where available, or derived from historical prices and forward market prices from similar observable markets when not available. Increases in the price of the spread on a buy or sell position in isolation would result in a higher/lower fair value measurement. The significant unobservable inputs used in the valuation of Dynegy’s contracts classified as Level 3 as of June 30, 2017 are as follows:

Transaction Type | Quantity | Unit of Measure | Net Fair Value | Valuation Technique | Significant Unobservable Input | Significant Unobservable Input Range | |||||||||

(dollars in millions) | |||||||||||||||

Electricity derivatives: | |||||||||||||||

Forward contracts—power (1) | (12 | ) | Million MWh | $ | 3 | Basis spread + liquid location | Basis spread | $4.25 - $6.25 | |||||||

FTRs | (40 | ) | Million MWh | $ | (4 | ) | Historical congestion | Forward price | $0 - $6.00 | ||||||

Physical heat rate derivatives | 23/(3) | Million MMBtu/Million MWh | $ | (2 | ) | Discounted Cash Flow | Forward price | $2.40 - $3.30 / $25 - $31 | |||||||

Natural gas derivatives (1) | 103 | Million MMBtu | $ | 1 | Illiquid location fixed price | Forward price | $2.50 - $3.10 | ||||||||

__________________________________________

(1) | Represents forward financial and physical transactions at illiquid pricing locations and long-dated contracts. |

The following tables set forth a reconciliation of changes in the fair value of financial instruments classified as Level 3 in the fair value hierarchy:

Three Months Ended June 30, 2017 | ||||||||||||||||

(amounts in millions) | Electricity Derivatives | Natural Gas Derivatives | Heat Rate Derivatives | Total | ||||||||||||

Balance at March 31, 2017 | $ | (17 | ) | $ | (2 | ) | $ | — | $ | (19 | ) | |||||

Total gains (losses) included in earnings | 7 | 3 | (2 | ) | 8 | |||||||||||

Settlements (1) | 9 | — | — | 9 | ||||||||||||

Balance at June 30, 2017 | $ | (1 | ) | $ | 1 | $ | (2 | ) | $ | (2 | ) | |||||

Unrealized gains (losses) relating to instruments held as of June 30, 2017 | $ | 7 | $ | 3 | $ | (2 | ) | $ | 8 | |||||||

Six Months Ended June 30, 2017 | ||||||||||||||||

(amounts in millions) | Electricity Derivatives | Natural Gas Derivatives | Heat Rate Derivatives | Total | ||||||||||||

Balance at December 31, 2016 | $ | 8 | $ | (6 | ) | $ | — | $ | 2 | |||||||

Acquired derivatives | 1 | — | — | 1 | ||||||||||||

Total gains (losses) included in earnings | (22 | ) | 13 | (2 | ) | (11 | ) | |||||||||

Settlements (1) | 12 | (6 | ) | — | 6 | |||||||||||

Balance at June 30, 2017 | $ | (1 | ) | $ | 1 | $ | (2 | ) | $ | (2 | ) | |||||

Unrealized gains (losses) relating to instruments held as of June 30, 2017 | $ | (22 | ) | $ | 13 | $ | (2 | ) | $ | (11 | ) | |||||

15

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

Three Months Ended June 30, 2016 | ||||||||||||||||

(amounts in millions) | Electricity Derivatives | Natural Gas Derivatives | Coal Derivatives | Total | ||||||||||||

Balance at March 31, 2016 | $ | (17 | ) | $ | (18 | ) | $ | 1 | $ | (34 | ) | |||||

Total gains (losses) included in earnings | (12 | ) | — | — | (12 | ) | ||||||||||

Settlements (1) | 5 | 3 | — | 8 | ||||||||||||

Balance at June 30, 2016 | $ | (24 | ) | $ | (15 | ) | $ | 1 | $ | (38 | ) | |||||

Unrealized gains (losses) relating to instruments held as of June 30, 2016 | $ | (12 | ) | $ | — | $ | — | $ | (12 | ) | ||||||

Six Months Ended June 30, 2016 | ||||||||||||||||

(amounts in millions) | Electricity Derivatives | Natural Gas Derivatives | Coal Derivatives | Total | ||||||||||||

Balance at December 31, 2015 | $ | (18 | ) | $ | (32 | ) | $ | 2 | $ | (48 | ) | |||||

Total gains (losses) included in earnings | (5 | ) | 3 | — | (2 | ) | ||||||||||

Settlements (1) | (1 | ) | 14 | (1 | ) | 12 | ||||||||||

Balance at June 30, 2016 | $ | (24 | ) | $ | (15 | ) | $ | 1 | $ | (38 | ) | |||||

Unrealized gains (losses) relating to instruments held as of June 30, 2016 | $ | (5 | ) | $ | 3 | $ | — | $ | (2 | ) | ||||||

(1) | For purposes of these tables, we define settlements as the beginning of period fair value of contracts that settled during the period. |

Gains and losses recognized for Level 3 recurring items are included in Revenues in our unaudited consolidated statements of operations for commodity derivatives. We believe an analysis of commodity instruments classified as Level 3 should be undertaken with the understanding that these items generally serve as economic hedges of our power generation portfolio. We did not have any material transfers between Level 1, Level 2 and Level 3 for the three and six months ended June 30, 2017 and 2016.

Nonfinancial Assets and Liabilities. Nonfinancial assets and liabilities that are measured at fair value on a nonrecurring basis are classified in their entirety based on the lowest level of input that is significant to the fair value measurement. Our assessment of the significance of a particular input to the fair value measurement requires judgment and may affect the valuation of such assets and liabilities and their placement within the fair value hierarchy.

During the three and six months ended June 30, 2017 and 2016, we recorded impairment charges related to certain of our facilities using a discounted cash flow model classified as Level 3 within the fair value hierarchy. See Note 9—Property, Plant and Equipment for further discussion. During the six months ended June 30, 2017, we fair valued the ENGIE Acquisition and our acquisition of additional joint ownership interest in the Zimmer facility. See Note 3—Acquisitions and Divestitures for further discussion of the fair value hierarchy classifications of valuations of acquired identifiable assets and liabilities and Note 10—Joint Ownership of Generating Facilities for further discussion of the acquisition of additional joint ownership interest in the Zimmer facility.

16

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

Fair Value of Financial Instruments. The following table discloses the fair value of financial instruments which are not recognized at fair value in our unaudited consolidated balance sheets. Unless otherwise noted, the fair value of debt as reflected in the table has been calculated based on the average of certain available broker quotes as of June 30, 2017 and December 31, 2016, respectively.

June 30, 2017 | December 31, 2016 | |||||||||||||||||

(amounts in millions) | Fair Value Hierarchy | Carrying Amount | Fair Value | Carrying Amount | Fair Value | |||||||||||||

Dynegy Inc.: | ||||||||||||||||||

Tranche C-1 Term Loan, due 2024 (1) | Level 2 | $ | (2,129 | ) | $ | (2,213 | ) | $ | (1,994 | ) | $ | (2,025 | ) | |||||

Tranche B-2 Term Loan, due 2020 (1) | Level 2 | $ | — | $ | — | $ | (219 | ) | $ | (225 | ) | |||||||

Revolving Facility (1) | Level 2 | $ | (300 | ) | $ | (300 | ) | $ | — | $ | — | |||||||

6.75% Senior Notes, due 2019 (1) | Level 2 | $ | (2,085 | ) | $ | (2,163 | ) | $ | (2,083 | ) | $ | (2,137 | ) | |||||

7.375% Senior Notes, due 2022 (1) | Level 2 | $ | (1,733 | ) | $ | (1,735 | ) | $ | (1,731 | ) | $ | (1,665 | ) | |||||

5.875% Senior Notes, due 2023 (1) | Level 2 | $ | (493 | ) | $ | (463 | ) | $ | (492 | ) | $ | (431 | ) | |||||

7.625% Senior Notes, due 2024 (1) | Level 2 | $ | (1,236 | ) | $ | (1,213 | ) | $ | (1,237 | ) | $ | (1,156 | ) | |||||

8.034% Senior Notes, due 2024 (1) | Level 2 | $ | (184 | ) | $ | (175 | ) | $ | — | $ | — | |||||||

8.00% Senior Notes, due 2025 (1) | Level 2 | $ | (738 | ) | $ | (729 | ) | $ | (738 | ) | $ | (703 | ) | |||||

7.00% Amortizing Notes, due 2019 (TEUs) (1) | Level 2 | $ | (58 | ) | $ | (68 | ) | $ | (78 | ) | $ | (90 | ) | |||||

Forward capacity agreement (1) | Level 3 | $ | (210 | ) | $ | (210 | ) | $ | (205 | ) | $ | (205 | ) | |||||

Inventory financing agreements | Level 3 | $ | (48 | ) | $ | (48 | ) | $ | (129 | ) | $ | (127 | ) | |||||

Equipment financing agreements (1) | Level 3 | $ | (103 | ) | $ | (103 | ) | $ | (73 | ) | $ | (73 | ) | |||||

Genco: | ||||||||||||||||||

Liabilities subject to compromise (2) | Level 3 | $ | — | $ | — | $ | (825 | ) | $ | (366 | ) | |||||||

__________________________________________

(1) | Carrying amounts include unamortized discounts and debt issuance costs. Please read Note 12—Debt for further discussion. |

(2) | Carrying amounts represent the Genco senior notes that were classified as liabilities subject to compromise as of December 31, 2016. The fair value of the senior notes was equal to the Genco Plan consideration and is a Level 3 valuation due to a lack of observable inputs that make up the consideration. Please read Note 22—Genco Chapter 11 Bankruptcy in our Form 10-K for further details. |

Note 7—Cash Flow Information

The supplemental disclosures of our non-cash investing and financing information are as follows:

Six Months Ended June 30, | ||||||||

(amounts in millions) | 2017 | 2016 | ||||||

Change in capital expenditures included in accounts payable | $ | 28 | $ | (3 | ) | |||

Change in capital expenditures pursuant to an equipment financing agreement | $ | 27 | $ | 4 | ||||

Issuance of 2017 Warrants | $ | 17 | $ | — | ||||

Issuance of senior notes related to the Genco restructuring | $ | 185 | $ | — | ||||

Non-cash working capital adjustment to purchase price of the ENGIE acquisition | $ | 14 | $ | — | ||||

Sale of interest in Conesville facility | $ | (57 | ) | $ | — | |||

Acquisition of interest in Zimmer facility | $ | 27 | $ | — | ||||

17

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

The following table provides a reconciliation of cash, cash equivalents and restricted cash reported within our unaudited consolidated balance sheets that sum to the total of the same such amounts shown in our unaudited consolidated statements of cash flows:

(amounts in millions) | June 30, 2017 | June 30, 2016 | ||||||

Cash and cash equivalents | $ | 447 | $ | 1,142 | ||||

Restricted cash included in current assets (1) | — | 104 | ||||||

Restricted cash included in long-term assets (2) | — | 2,000 | ||||||

Total cash, cash equivalents and restricted cash | $ | 447 | $ | 3,246 | ||||

__________________________________________

(1) | Includes $70 million placed in escrow for the issuance of the Tranche C Term Loan ($50 million of pre-funded interest and $20 million of pre-funded original issue discount) and $34 million related to collateral. |

(2) | Relates to amounts placed into escrow for the issuance of the Tranche C Term Loan. |

Note 8—Inventory

A summary of our inventories is as follows:

(amounts in millions) | June 30, 2017 | December 31, 2016 | ||||||

Materials and supplies | $ | 254 | $ | 182 | ||||

Coal | 192 | 238 | ||||||

Fuel oil | 13 | 17 | ||||||

Natural gas | 15 | — | ||||||

Emissions allowances (1) | 3 | 8 | ||||||

Total | $ | 477 | $ | 445 | ||||

__________________________________________

(1) | At June 30, 2017 and December 31, 2016, a portion of this inventory was held as collateral by one of our counterparties as part of an inventory financing agreement. Please read Note 12—Debt—Emissions Repurchase Agreements for further discussion. |

Note 9—Property, Plant and Equipment

A summary of our property, plant and equipment is as follows:

(amounts in millions) | June 30, 2017 | December 31, 2016 | ||||||

Power generation | $ | 10,065 | $ | 7,537 | ||||

Buildings and improvements | 1,137 | 944 | ||||||

Office and other equipment | 117 | 98 | ||||||

Property, plant and equipment | 11,319 | 8,579 | ||||||

Accumulated depreciation | (1,834 | ) | (1,458 | ) | ||||

Property, plant and equipment, net | $ | 9,485 | $ | 7,121 | ||||

18

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

Impairments

For the three and six months ended June 30, 2017 and 2016, we recognized the following impairments in our unaudited consolidated statements of operations (amounts in millions):

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||

Facility | Fair Value | 2017 | 2016 | 2017 | 2016 | |||||||||||||||

Baldwin (1) | $ | 97 | $ | — | $ | 645 | $ | — | $ | 645 | ||||||||||

Killen (2) | $ | — | — | — | 20 | — | ||||||||||||||

Hennepin (1) | $ | 16 | 10 | — | 10 | — | ||||||||||||||

Havana (1) | $ | 37 | 89 | — | 89 | — | ||||||||||||||

Total | $ | 99 | $ | 645 | $ | 119 | $ | 645 | ||||||||||||

_________________________________________

(1) | Units failed to recover their basic operating costs in the MISO capacity auctions. |

(2) | In first quarter 2017, Dayton Power and Light Co., the partner and operator of Killen, announced the shutdown of the Killen generation facility by June 2018. |

As a result of our impairment analysis on our coal facilities in MISO, we decreased the estimated useful lives of certain of the facilities.

Retirements

The Brayton Point facility officially retired on June 1, 2017. During the three and six months ended June 30, 2017, we recognized $5 million of severance costs, which were classified within Operating and maintenance expense in our unaudited consolidated statement of operations.

Note 10—Joint Ownership of Generating Facilities

We hold ownership interests in certain jointly owned generating facilities. We are entitled to the proportional share of the generating capacity and the output of each unit equal to our ownership interests. We pay our share of capital expenditures, fuel inventory purchases, and operating expenses, except in certain instances where agreements have been executed to limit certain joint owners’ maximum exposure to additional costs. Our share of revenues and operating costs of the jointly owned generating facilities is included within the corresponding financial statement line items in our unaudited consolidated statements of operations.

The following tables present the ownership interests of the jointly owned facilities as of June 30, 2017 and December 31, 2016 included in our unaudited consolidated balance sheets. Each facility is co-owned with one or more other generation companies.

June 30, 2017 | |||||||||||||||||||

(dollars in millions) | Ownership Interest | Property, Plant and Equipment | Accumulated Depreciation | Construction Work in Progress | Total | ||||||||||||||

Miami Fort | 64.0 | % | $ | 209 | $ | (50 | ) | $ | 4 | $ | 163 | ||||||||

Stuart (1)(2) | 39.0 | % | $ | — | $ | — | $ | 2 | $ | 2 | |||||||||

Zimmer | 71.9 | % | $ | 125 | $ | (33 | ) | $ | 8 | $ | 100 | ||||||||

Killen (1)(2) | 33.0 | % | $ | — | $ | — | $ | — | $ | — | |||||||||

December 31, 2016 | |||||||||||||||||||

(dollars in millions) | Ownership Interest | Property, Plant and Equipment | Accumulated Depreciation | Construction Work in Progress | Total | ||||||||||||||

Miami Fort | 64.0 | % | $ | 207 | $ | (39 | ) | $ | 4 | $ | 172 | ||||||||

Stuart (1) | 39.0 | % | $ | — | $ | — | $ | 4 | $ | 4 | |||||||||

Conesville (1) | 40.0 | % | $ | 61 | $ | (3 | ) | $ | 6 | $ | 64 | ||||||||

Zimmer | 46.5 | % | $ | 115 | $ | (25 | ) | $ | 6 | $ | 96 | ||||||||

Killen (1) | 33.0 | % | $ | 19 | $ | (2 | ) | $ | 3 | $ | 20 | ||||||||

__________________________________________

(1) | Facilities not operated by Dynegy. |

19

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

(2) | Stuart Unit 1 is scheduled to be retired in the third quarter of 2017, with remaining Stuart and Killen units scheduled to be retired by mid-2018. |

On May 12, 2017, the joint owners received approval to retire the units at Stuart Station and Killen effective June 1, 2018. On July 19, 2017, Stuart Unit 1 received approval from PJM to retire early effective September 30, 2017.

On May 9, 2017, Dynegy finalized the sale of its 40 percent ownership interest in Conesville to American Electric Power (“AEP”) in exchange for AEP’s 25.4 percent ownership interest in Zimmer. As a result, Dynegy now owns 71.9 percent of the Zimmer facility and no longer has an ownership interest in the Conesville facility. No cash was exchanged in the transaction and no additional debt was incurred by either party. AEP returned a previously issued letter of credit totaling $58 million to Dynegy. The acquisition of the additional interest in Zimmer has been accounted for as a business combination using similar fair value methodologies as described in Note 3—Acquisitions and Divestitures. The fair value of the additional Zimmer interest is $27 million and was allocated $14 million to Property, plant and equipment, $14 million to Inventory and $1 million to ARO liability in our unaudited consolidated balance sheets. As a result of the Conesville sale, we recognized a loss of $30 million for the three and six months ended June 30, 2017, representing the difference between the $57 million book value of our transferred interest in Conesville and the $27 million fair value of the acquired interest in Zimmer.

On April 21, 2017, Dynegy reached an agreement with AES Ohio Generation, LLC and The Dayton Power and Light Company (collectively, “AES”) under which Dynegy will purchase AES’ 28.1 percent interest in Zimmer and 36 percent interest in Miami Fort for $50 million in cash and the assumption of certain liabilities, subject to customary adjustments. The transaction is expected to close in the second half of 2017.

Note 11—Intangible Assets and Liabilities

The following table summarizes the components of our intangible assets and liabilities as of June 30, 2017 and December 31, 2016:

June 30, 2017 | December 31, 2016 | |||||||||||||||||||||||

(amounts in millions) | Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | ||||||||||||||||||

Intangible Assets: | ||||||||||||||||||||||||

Electricity contracts | $ | 281 | $ | (219 | ) | $ | 62 | $ | 260 | $ | (206 | ) | $ | 54 | ||||||||||

Gas transport contracts | 29 | (10 | ) | 19 | 13 | (6 | ) | 7 | ||||||||||||||||

Total intangible assets | $ | 310 | $ | (229 | ) | $ | 81 | $ | 273 | $ | (212 | ) | $ | 61 | ||||||||||

Intangible Liabilities: | ||||||||||||||||||||||||

Electricity contracts | $ | (24 | ) | $ | 14 | $ | (10 | ) | $ | (28 | ) | $ | 26 | $ | (2 | ) | ||||||||

Coal contracts | (35 | ) | 33 | (2 | ) | (49 | ) | 42 | (7 | ) | ||||||||||||||

Coal transport contracts | (86 | ) | 78 | (8 | ) | (86 | ) | 73 | (13 | ) | ||||||||||||||

Gas transport contracts | (60 | ) | 15 | (45 | ) | (41 | ) | 8 | (33 | ) | ||||||||||||||

Gas storage contracts | (2 | ) | 1 | (1 | ) | — | — | — | ||||||||||||||||

Total intangible liabilities | $ | (207 | ) | $ | 141 | $ | (66 | ) | $ | (204 | ) | $ | 149 | $ | (55 | ) | ||||||||

Intangible assets and liabilities, net | $ | 103 | $ | (88 | ) | $ | 15 | $ | 69 | $ | (63 | ) | $ | 6 | ||||||||||

20

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

The following table presents our amortization expense (revenue) of intangible assets and liabilities for the three and six months ended June 30, 2017 and 2016:

Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

(amounts in millions) | 2017 | 2016 | 2017 | 2016 | ||||||||||||

Electricity contracts, net (1) | $ | 9 | $ | 17 | $ | 24 | $ | 33 | ||||||||

Coal contracts, net (2) | (1 | ) | (11 | ) | (3 | ) | (23 | ) | ||||||||

Coal transport contracts, net (2) | (2 | ) | (7 | ) | (5 | ) | (14 | ) | ||||||||

Gas transport contracts, net (2) | (2 | ) | — | (1 | ) | 17 | ||||||||||

Total | $ | 4 | $ | (1 | ) | $ | 15 | $ | 13 | |||||||

__________________________________________

(1) | The amortization of these contracts is recognized in Revenues or Cost of sales in our unaudited consolidated statements of operations. |

(2) | The amortization of these contracts is recognized in Cost of sales in our unaudited consolidated statements of operations. |

The following table summarizes the components of our contract based intangible assets and liabilities recorded in connection with the ENGIE Acquisition in February 2017:

(amounts in millions/months) | Gross Carrying Amount | Weighted-Average Amortization Period | ||||

Intangible Assets: | ||||||

Electricity contracts | $ | 34 | 39 | |||

Gas transport contracts | 16 | 47 | ||||

Total intangible assets | $ | 50 | 41 | |||

Intangible Liabilities: | ||||||

Electricity contracts | $ | (11 | ) | 32 | ||

Gas contracts | — | 1 | ||||

Gas transport contracts | (17 | ) | 35 | |||

Gas storage contracts | (2 | ) | 13 | |||

Total intangible liabilities | $ | (30 | ) | 33 | ||

Total intangible assets and liabilities, net | $ | 20 | ||||

Amortization expense (revenue), net related to intangible assets and liabilities recorded in connection with the ENGIE Acquisition for the next five years as of June 30, 2017 is as follows: 2017—$(5) million, 2018—$8 million, 2019—$17 million, 2020—$4 million and 2021—$(1) million.

21

DYNEGY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

For the Interim Periods Ended June 30, 2017 and 2016

Note 12—Debt

A summary of our long-term debt is as follows:

(amounts in millions) | June 30, 2017 | December 31, 2016 | ||||||

Secured Obligations: | ||||||||

Tranche C-1 Term Loan, due 2024 (1) | $ | 2,218 | $ | 2,000 | ||||

Tranche B-2 Term Loan, due 2020 | — | 224 | ||||||

Revolving Facility | 300 | — | ||||||

Forward Capacity Agreements | 230 | 219 | ||||||

Inventory Financing Agreements | 48 | 129 | ||||||

Subtotal secured obligations | 2,796 | 2,572 | ||||||

Unsecured Obligations: | ||||||||

7.00% Amortizing Notes, due 2019 (TEUs) | 60 | 80 | ||||||

6.75% Senior Notes, due 2019 | 2,100 | 2,100 | ||||||

7.375% Senior Notes, due 2022 | 1,750 | 1,750 | ||||||

5.875% Senior Notes, due 2023 | 500 | 500 | ||||||

7.625% Senior Notes, due 2024 | 1,250 | 1,250 | ||||||

8.034% Senior Notes, due 2024 (2) | 184 | — | ||||||

8.00% Senior Notes, due 2025 | 750 | 750 | ||||||

Equipment Financing Agreements | 131 | 97 | ||||||

Subtotal unsecured obligations | 6,725 | 6,527 | ||||||

Total debt obligations | 9,521 | 9,099 | ||||||

Unamortized debt discounts and issuance costs | (204 | ) | (120 | ) | ||||

9,317 | 8,979 | |||||||

Less: Current maturities, including unamortized debt discounts and issuance costs, net | 106 | 201 | ||||||

Total long-term debt | $ | 9,211 | $ | 8,778 | ||||

__________________________________________

(1) | At December 31, 2016, the $2.0 billion Tranche C Term Loan was held by Dynegy Finance IV. Upon the close of the ENGIE Acquisition, this debt obligation became Dynegy Inc.’s secured obligation. |

(2) | On the Genco Emergence Date, we issued $182 million of 8.034 percent seven-year unsecured senior notes due 2024 and on April 18, 2017, we issued an additional $3 million of such notes. See Note 18—Genco Chapter 11 Bankruptcy and Emergence for further discussion. |

Credit Agreement

As of June 30, 2017, we had a $3.769 billion credit agreement, as amended, that consisted of (i) a $2.224 billion seven-year senior secured term loan facility (the “Tranche C-1 Term Loan”) and (ii) $1.545 billion in senior secured revolving credit facilities (the “Revolving Facility,” and collectively with the Tranche C-1 Term Loan the “Credit Agreement”). During the six months ended June 30, 2017, we made the following changes to the Credit Agreement: