Attached files

| file | filename |

|---|---|

| 8-K/A - 8-K/A - HEALTHCARE REALTY TRUST INC | hr-2017630earnings8xka.htm |

2Q | 2017

Supplemental Information

FURNISHED AS OF AUGUST 2, 2017 (UNAUDITED)

Table of Contents

Highlights | ||

The Big Picture | ||

Corporate Information | ||

Balance Sheet Information | ||

Statements of Income Information | ||

FFO, Normalized FFO & FAD | ||

Capital Funding | ||

Debt Metrics | ||

Investment Activity | ||

Portfolio by Market | ||

Square Feet by Health System | ||

Square Feet by Proximity | ||

Lease Maturity, Size and Building Square Feet | ||

Occupancy Information | ||

Same Store Leasing Statistics | ||

Same Store Properties | ||

Reconciliation of NOI | ||

Reconciliation of EBITDA | ||

Components of Net Asset Value | ||

Components of Expected 2017 FFO | ||

Copies of this report may be obtained at www.healthcarerealty.com or by contacting Investor Relations at 615.269.8175 or communications@healthcarerealty.com.

Forward looking statements and risk factors:

This Supplemental Information report contains disclosures that are “forward-looking statements” as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements include all statements that do not relate solely to historical or current facts and can be identified by the use of words and phrases such as “can,” “may,” “payable,” “indicative,” “annualized,” “expect,” “expected,” “future cash or NOI,” “deferred revenue,” “rent increases,” “range of expectations,” "budget," “components of expected 2017 FFO,” and other comparable terms in this report. These forward-looking statements are made as of the date of this report and are not guarantees of future performance. These statements are based on the current plans and expectations of Company management and are subject to a number of unknown risks, uncertainties, assumptions and other factors that could cause actual results to differ materially from those described in this release or implied by such forward-looking statements. Such risks and uncertainties include, among other things, the following: changes in the economy; increases in interest rates; the availability and cost of capital at expected rates; changes to facility-related healthcare regulations; competition for quality assets; negative developments in the operating results or financial condition of the Company's tenants, including, but not limited to, their ability to pay rent and repay loans; the Company's ability to reposition or sell facilities with profitable results; the Company's ability to re-lease space at similar rates as vacancies occur; the Company's ability to renew expiring long-term single-tenant net leases; the Company's ability to timely reinvest proceeds from the sale of assets at similar yields; government regulations affecting tenants' Medicare and Medicaid reimbursement rates and operational requirements; unanticipated difficulties and/or expenditures relating to future acquisitions and developments; changes in rules or practices governing the Company's financial reporting; the Company may be required under purchase options to sell properties and may not be able to reinvest the proceeds from such sales at rates of return equal to the return received on the properties sold; uninsured or underinsured losses related to casualty or liability; the incurrence of impairment charges on its real estate properties or other assets; and other legal and operational matters. Other risks, uncertainties and factors that could cause actual results to differ materially from those projected are detailed under the heading “Risk Factors,” in the Company's Annual Report on Form 10-K filed with the Securities and Exchange Commission (“SEC”) for the year ended December 31, 2016 and other risks described from time to time thereafter in the Company's SEC filings. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

HEALTHCARE REALTY 2 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Highlights

Salient quarterly highlights include:

• | Normalized FFO for the second quarter grew 2.8% year-over-year to $45.3 million. |

• | For the trailing twelve months ended June 30, 2017, same store revenue grew 2.9%, operating expenses increased 1.3%, and same store NOI grew 3.9%: |

◦ | Same store revenue per average occupied square foot increased 2.3%. |

◦ | Average same store occupancy increased to 89.2% from 88.7%. |

• | Four predictive growth measures in the same store multi-tenant portfolio: |

◦ | Contractual rent increases occurring in the quarter averaged 3.0%, and contractual rent increases for leases commencing in the quarter will average 3.3%. |

◦ | Cash leasing spreads were 9.5% on 285,000 square feet renewed: |

• | 0% (<0% spread) |

• | 3% (0-3%) |

• | 35% (3-4%) |

• | 62% (>4%) |

◦ | Tenant retention was 90.3%. |

◦ | The average yield on renewed leases increased 130 basis points. |

• | Leasing activity in the second quarter totaled 472,000 square feet related to 136 leases: |

◦ | 303,000 square feet of renewals |

◦ | 169,000 square feet of new and expansion leases |

• | Acquisitions totaled $67.1 million since the end of the first quarter: |

◦ | In June 2017, the Company purchased a medical office building on Sutter Health's Santa Rosa Regional Hospital campus in the San Francisco market for $26.8 million. The building is 76,000 square feet and 100% leased. |

◦ | Also in June 2017, the Company purchased a medical office building on Trinity Health's Holy Cross Hospital campus in the Washington, DC area for $24.0 million. The building is 62,000 square feet and 100% leased. |

◦ | In July 2017, the Company purchased a medical office building on HCA's West Hills Hospital and Medical Center campus in Los Angeles for $16.3 million. The building is 43,000 square feet, 93% leased, and is immediately adjacent to the West Hills Medical Center MOB that Healthcare Realty acquired in May 2016. |

• | The Company completed the core and shell of a 100,000 square foot medical office building on June 30, 2017. The building represents the Company's third development on CHI's St. Anthony Hospital campus in Denver. The first tenant, a 13,000 square foot surgery center, is expected to take occupancy in August 2017. The balance of the initial leasing, currently 35% of the building, is expected to take occupancy through the first quarter of 2018. |

• | Dispositions totaled $38.2 million for the quarter, including one inpatient rehabilitation facility for $14.5 million and two medical office buildings for $23.7 million. |

• | A dividend of $0.30 per common share was declared, which is equal to 76.9% of normalized FFO per share. |

HEALTHCARE REALTY 3 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Other items of note:

• | Three inpatient rehabilitation facilities were sold for $69.5 million on March 31, 2017 at a cap rate of 7.3%. FFO dilution was approximately $0.01 per share in the second quarter of 2017 as a result of these sales. |

• | Since March 31, 2017, the Company acquired three properties for $67.1 million at an average cap rate of 5.4% and disposed of three properties for $38.2 million at an average cap rate of 6.7%. These six transactions will immediately result in approximately $0.1 million increase in the third quarter NOI over the second quarter, and the full quarter effect beginning in the fourth quarter is expected to be an overall increase in quarterly NOI of $0.3 million. |

• | The Company traditionally experiences an increase in property operating expenses during the third quarter related primarily to seasonal utilities. Over the past three years, third quarter utility expenses have increased by an average of $1.5 million over the second quarter. |

• | In the same store, multi-tenant portfolio, three of the Company's legacy property operating agreements expired during the twelve months ended June 30, 2017; two in September 2016 and one in January 2017. The Company recognized $0.2 million of rental lease guaranty income in the second quarter of 2017 compared to $0.9 million in the second quarter of 2016. The Company's one remaining property operating agreement expires in February 2019. Additional information is available on pages 25 and 26 of the Company's 2016 Form 10-K and page 18 of the Company's second quarter 2017 Form 10-Q. |

• | The Company anticipates a fixed-price purchase option to be exercised on seven properties in Roanoke, Virginia for approximately $45.2 million. The Company recognized approximately $3.1 million of NOI during the six months ended June 30, 2017. The sale of these properties is expected to occur in the first quarter of 2018. Additional information is available on page 26 of the Company's 2016 Form 10-K and page 18 of the Company's second quarter 2017 Form 10-Q. |

HEALTHCARE REALTY 4 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

The Big Picture

Properties | |||

$3.6B | Invested in 197 properties | ||

14.5M SF | Owned in 26 states | ||

10.9M SF | Managed internally | ||

93 | % | Medical office and outpatient | |

85 | % | On/adjacent to hospital campuses | |

3.9 | % | Same store NOI growth (TTM) | |

Capitalization | |||

$5.1B | Enterprise value | ||

$3.9B | Market capitalization | ||

116.5M | Shares outstanding | ||

$0.30 | Quarterly dividend | ||

BBB/Baa | Credit rating | ||

23.6 | % | Net debt to enterprise value | |

4.9x | Net debt to EBITDA | ||

MOB PROXIMITY TO HOSPITAL | ||||

% of SF | ||||

On campus | 68 | % | ||

Adjacent to campus | 17 | % | ||

Total on/adjacent | 85 | % | ||

Anchored | 9 | % | ||

Off campus | 6 | % | ||

Total | 100 | % | ||

HEALTH SYSTEM BY RANK (% of SF) | ||||

MOB/OUTPATIENT | TOTAL | |||

Top 25 | 52 | % | 49 | % |

Top 50 | 69 | % | 67 | % |

Top 75 | 77 | % | 75 | % |

Top 100 | 81 | % | 78 | % |

MSA BY RANK (% of SF) | ||||

MOB/OUTPATIENT | TOTAL | |||

Top 25 | 61 | % | 58 | % |

Top 50 | 84 | % | 80 | % |

Top 75 | 88 | % | 83 | % |

Top 100 | 92 | % | 89 | % |

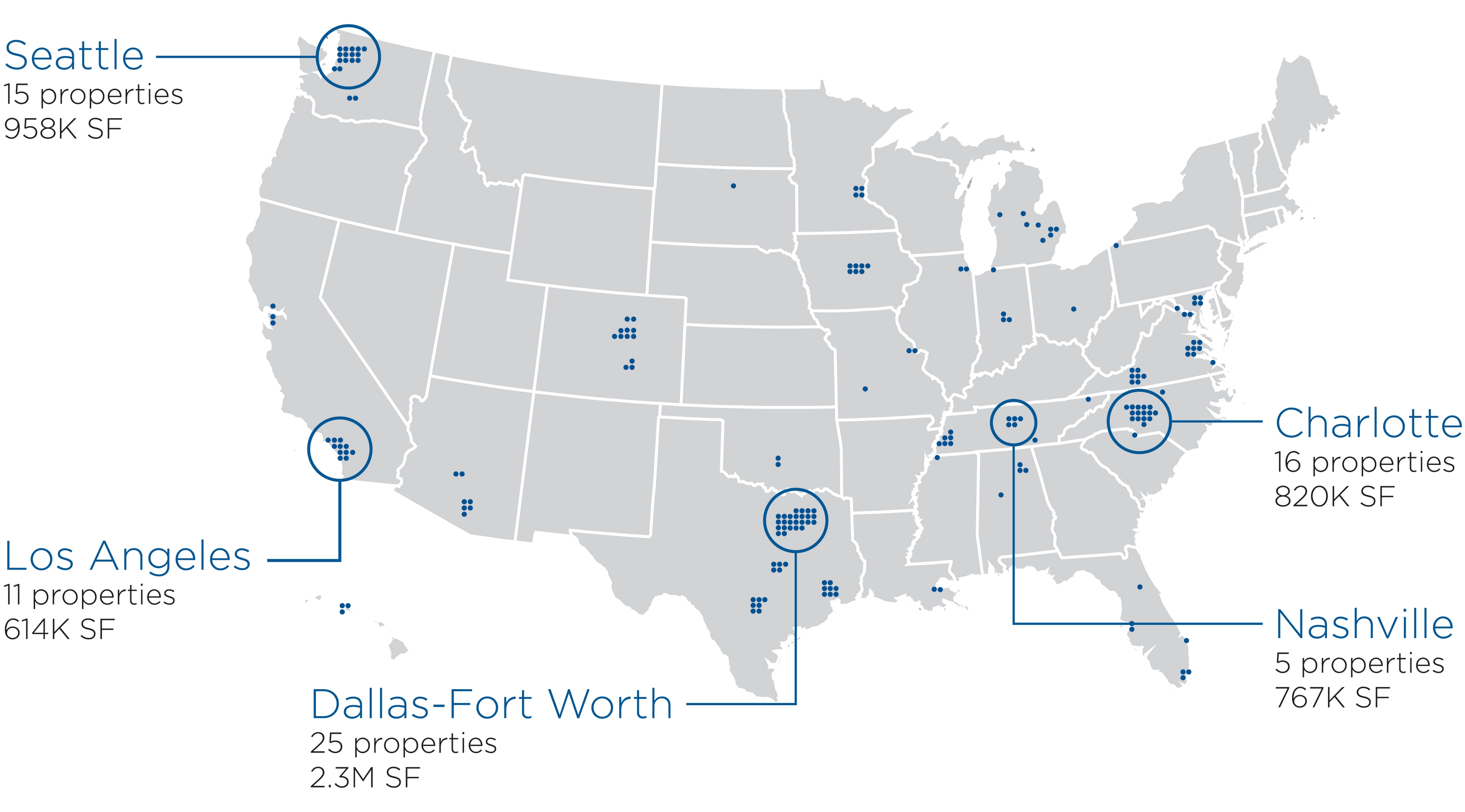

HEALTHCARE REALTY'S TOP MARKETS | ||||

HEALTHCARE REALTY 5 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Corporate Information

Healthcare Realty Trust is a real estate investment trust that integrates owning, managing, financing and developing income-producing real estate properties associated primarily with the delivery of outpatient healthcare services throughout the United States. As of June 30, 2017, the Company had gross investments of approximately $3.6 billion in 197 real estate properties in 26 states totaling approximately 14.5 million square feet. The Company provided leasing and property management services to approximately 10.9 million square feet nationwide.

Corporate Headquarters | |

Healthcare Realty Trust Incorporated | |

3310 West End Avenue, Suite 700 | |

Nashville, Tennessee 37203 | |

Phone: 615.269.8175 | |

Fax: 615.269.8461 | |

E-mail: communications@healthcarerealty.com | |

Website: www.healthcarerealty.com | |

Executive Officers | ||

David R. Emery | Executive Chairman of the Board | |

Todd J. Meredith | President and Chief Executive Officer | |

John M. Bryant, Jr. | Executive Vice President and General Counsel | |

J. Christopher Douglas | Executive Vice President and Chief Financial Officer | |

Robert E. Hull | Executive Vice President - Investments | |

B. Douglas Whitman, II | Executive Vice President - Corporate Finance | |

Board of Directors | ||

David R. Emery | Executive Chairman of the Board, Healthcare Realty Trust Incorporated | |

Nancy H. Agee | President and Chief Executive Officer, Carilion Clinic | |

C. Raymond Fernandez, M.D. | Retired Chief Executive Officer, Piedmont Clinic | |

Peter F. Lyle | Vice President, Medical Management Associates, Inc. | |

Todd Meredith | President and Chief Executive Officer, Healthcare Realty Trust Incorporated | |

Edwin B. Morris III | Managing Director, Morris & Morse Company, Inc. | |

J. Knox Singleton | President and Chief Executive Officer, Inova Health System | |

Bruce D. Sullivan | Retired Audit Partner, Ernst & Young LLP | |

Christann M. Vasquez | President, Dell Seton Medical Center at University of Texas | |

Analyst Coverage | ||||

BMO Capital Markets | J.P. Morgan Securities LLC | Mizuho Securities USA Inc. | ||

BTIG, LLC | Jefferies LLC | Stifel, Nicolaus & Company, Inc. | ||

Cantor Fitzgerald, L.P. | JMP Securities LLC | SunTrust Robinson Humphrey, Inc. | ||

Green Street Advisors, Inc. | Morgan Stanley | Wells Fargo Securities, LLC | ||

J.J.B. Hilliard W.L. Lyons, LLC | KeyBanc Capital Markets Inc. | |||

HEALTHCARE REALTY 6 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Balance Sheet Information

(dollars in thousands, except per share data)

ASSETS | ||||||||||||||||||||

2017 | 2016 | |||||||||||||||||||

Real estate properties: | Q2 | Q1 | Q4 | Q3 | Q2 | |||||||||||||||

Land | $193,072 | $193,101 | $199,672 | $206,647 | $208,386 | |||||||||||||||

Buildings, improvements and lease intangibles | 3,388,734 | 3,327,529 | 3,386,480 | 3,322,293 | 3,235,744 | |||||||||||||||

Personal property | 10,155 | 9,998 | 10,291 | 10,124 | 10,032 | |||||||||||||||

Construction in progress | — | 16,114 | 11,655 | 45,734 | 35,174 | |||||||||||||||

Land held for development | 20,123 | 20,123 | 20,123 | 17,438 | 17,438 | |||||||||||||||

Total real estate properties | 3,612,084 | 3,566,865 | 3,628,221 | 3,602,236 | 3,506,774 | |||||||||||||||

Less accumulated depreciation and amortization | (864,573 | ) | (841,296 | ) | (840,839 | ) | (835,276 | ) | (819,744 | ) | ||||||||||

Total real estate properties, net | 2,747,511 | 2,725,569 | 2,787,382 | 2,766,960 | 2,687,030 | |||||||||||||||

Cash and cash equivalents | 2,033 | 1,478 | 5,409 | 12,649 | 9,026 | |||||||||||||||

Restricted cash | 9,151 | 104,904 | 49,098 | — | — | |||||||||||||||

Assets held for sale and discontinued operations, net | 8,767 | 15,111 | 3,092 | 14,732 | 710 | |||||||||||||||

Other assets, net | 191,036 | 192,174 | 195,666 | 197,380 | 185,298 | |||||||||||||||

Total assets | $2,958,498 | $3,039,236 | $3,040,647 | $2,991,721 | $2,882,064 | |||||||||||||||

LIABILITIES AND STOCKHOLDERS' EQUITY | ||||||||||||||||||||

Liabilities: | ||||||||||||||||||||

Notes and bonds payable | $1,203,146 | $1,278,662 | $1,264,370 | $1,239,062 | $1,414,739 | |||||||||||||||

Accounts payable and accrued liabilities | 62,121 | 62,746 | 78,266 | 71,052 | 70,408 | |||||||||||||||

Liabilities of properties held for sales and discontinued operations | 398 | 93 | 614 | 572 | 17 | |||||||||||||||

Other liabilities | 46,556 | 44,444 | 43,983 | 46,441 | 46,452 | |||||||||||||||

Total liabilities | 1,312,221 | 1,385,945 | 1,387,233 | 1,357,127 | 1,531,616 | |||||||||||||||

Commitments and contingencies | ||||||||||||||||||||

Stockholders' equity: | ||||||||||||||||||||

Preferred stock, $.01 par value; 50,000 shares authorized; none issued and outstanding | — | — | — | — | — | |||||||||||||||

Common stock, $.01 par value; 300,000 shares authorized | 1,165 | 1,165 | 1,164 | 1,160 | 1,067 | |||||||||||||||

Additional paid-in capital | 2,923,519 | 2,920,839 | 2,917,914 | 2,916,816 | 2,609,880 | |||||||||||||||

Accumulated other comprehensive loss | (1,316 | ) | (1,358 | ) | (1,401 | ) | (1,443 | ) | (1,485 | ) | ||||||||||

Cumulative net income attributable to common stockholders | 1,052,326 | 1,027,101 | 995,256 | 942,819 | 930,985 | |||||||||||||||

Cumulative dividends | (2,329,417 | ) | (2,294,456 | ) | (2,259,519 | ) | (2,224,758 | ) | (2,189,999 | ) | ||||||||||

Total stockholders' equity | 1,646,277 | 1,653,291 | 1,653,414 | 1,634,594 | 1,350,448 | |||||||||||||||

Total liabilities and stockholders' equity | $2,958,498 | $3,039,236 | $3,040,647 | $2,991,721 | $2,882,064 | |||||||||||||||

HEALTHCARE REALTY 7 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Statements of Income Information

(dollars in thousands)

2017 | 2016 | 2015 | |||||||||||||||||||||||||||||

Q2 | Q1 | Q4 | Q3 | Q2 | Q1 | Q4 | Q3 | ||||||||||||||||||||||||

Revenues | |||||||||||||||||||||||||||||||

Rental income | $104,869 | $104,088 | $104,736 | $102,534 | $101,472 | $98,740 | $97,466 | $95,383 | |||||||||||||||||||||||

Mortgage interest | — | — | — | — | — | — | — | 29 | |||||||||||||||||||||||

Other operating | 376 | 481 | 573 | 1,125 | 1,170 | 1,281 | 1,116 | 1,313 | |||||||||||||||||||||||

105,245 | 104,569 | 105,309 | 103,659 | 102,642 | 100,021 | 98,582 | 96,725 | ||||||||||||||||||||||||

Expenses | |||||||||||||||||||||||||||||||

Property operating | 38,184 | 37,834 | 37,285 | 37,504 | 36,263 | 35,406 | 36,758 | 35,247 | |||||||||||||||||||||||

General and administrative | 8,005 | 8,694 | 7,622 | 7,859 | 7,756 | 8,072 | 5,975 | 5,852 | |||||||||||||||||||||||

Acquisition and pursuit costs (1) | 785 | 586 | 1,085 | 865 | 373 | 2,174 | 1,241 | 406 | |||||||||||||||||||||||

Depreciation and amortization | 34,823 | 34,452 | 34,022 | 31,985 | 31,290 | 30,393 | 29,575 | 28,957 | |||||||||||||||||||||||

Bad debts, net of recoveries | 105 | 66 | (13 | ) | (47 | ) | 78 | (39 | ) | 9 | (21 | ) | |||||||||||||||||||

81,902 | 81,632 | 80,001 | 78,166 | 75,760 | 76,006 | 73,558 | 70,441 | ||||||||||||||||||||||||

Other Income (Expense) | |||||||||||||||||||||||||||||||

Gain on sales of real estate properties | 16,124 | 23,403 | 41,037 | — | 1 | — | 9,138 | 5,915 | |||||||||||||||||||||||

Interest expense | (14,315 | ) | (14,272 | ) | (13,839 | ) | (13,759 | ) | (14,815 | ) | (14,938 | ) | (14,885 | ) | (15,113 | ) | |||||||||||||||

Pension termination | — | — | — | — | (4 | ) | — | — | — | ||||||||||||||||||||||

Impairment of real estate assets | (5 | ) | (323 | ) | — | — | — | — | (1 | ) | (310 | ) | |||||||||||||||||||

Interest and other income, net | 77 | 113 | 74 | 123 | 93 | 86 | 78 | 72 | |||||||||||||||||||||||

1,881 | 8,921 | 27,272 | (13,636 | ) | (14,725 | ) | (14,852 | ) | (5,670 | ) | (9,436 | ) | |||||||||||||||||||

Income From Continuing Operations | 25,224 | 31,858 | 52,580 | 11,857 | 12,157 | 9,163 | 19,354 | 16,848 | |||||||||||||||||||||||

Discontinued Operations | |||||||||||||||||||||||||||||||

Income (loss) from discontinued operations | — | (18 | ) | (22 | ) | (23 | ) | (19 | ) | (7 | ) | (10 | ) | 61 | |||||||||||||||||

Impairments of real estate assets | — | — | (121 | ) | — | — | — | (686 | ) | — | |||||||||||||||||||||

Gain on sales of real estate properties | — | 5 | — | — | 7 | — | — | 10,571 | |||||||||||||||||||||||

Income (Loss) From Discontinued Operations | — | (13 | ) | (143 | ) | (23 | ) | (12 | ) | (7 | ) | (696 | ) | 10,632 | |||||||||||||||||

Net Income | $25,224 | $31,845 | $52,437 | $11,834 | $12,145 | $9,156 | $18,658 | $27,480 | |||||||||||||||||||||||

(1) | Includes third party and travel costs related to the pursuit of acquisitions and developments. |

HEALTHCARE REALTY 8 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

FFO, Normalized FFO & FAD (1) (2)

(amounts in thousands, except for share data)

2017 | 2016 | 2015 | ||||||||||||||||||||||||||||||

Q2 | Q1 | Q4 | Q3 | Q2 | Q1 | Q4 | Q3 | |||||||||||||||||||||||||

Net Income Attributable to Common Stockholders | $25,224 | $31,845 | $52,437 | $11,834 | $12,145 | $9,156 | $18,658 | $27,480 | ||||||||||||||||||||||||

Gain on sales of real estate properties | (16,124 | ) | (23,408 | ) | (41,037 | ) | — | (8 | ) | — | (9,138 | ) | (16,486 | ) | ||||||||||||||||||

Impairments of real estate assets | 5 | 323 | 121 | — | — | — | 687 | 310 | ||||||||||||||||||||||||

Real estate depreciation and amortization | 35,421 | 35,555 | 34,699 | 32,557 | 31,716 | 30,800 | 29,907 | 29,317 | ||||||||||||||||||||||||

Total adjustments | 19,302 | 12,470 | (6,217 | ) | 32,557 | 31,708 | 30,800 | 21,456 | 13,141 | |||||||||||||||||||||||

Funds from Operations Attributable to Common Stockholders | $44,526 | $44,315 | $46,220 | $44,391 | $43,853 | $39,956 | $40,114 | $40,621 | ||||||||||||||||||||||||

Acquisition and pursuit costs (3)(4) | 785 | 586 | 915 | 649 | 232 | 1,618 | 1,068 | 121 | ||||||||||||||||||||||||

Write-off of deferred financing costs upon amendment of line of credit facility | — | — | — | 81 | — | — | — | — | ||||||||||||||||||||||||

Pension termination | — | — | — | — | 4 | — | — | — | ||||||||||||||||||||||||

Reversal of restricted stock amortization upon director / officer resignation | — | — | — | — | — | — | (40 | ) | — | |||||||||||||||||||||||

Revaluation of awards upon retirement | — | — | — | — | — | 89 | — | — | ||||||||||||||||||||||||

Normalized Funds from Operations Attributable to Common Stockholders | $45,311 | $44,901 | $47,135 | $45,121 | $44,089 | $41,663 | $41,142 | $40,742 | ||||||||||||||||||||||||

Non-real estate depreciation and amortization | 1,539 | 1,355 | 1,339 | 1,386 | 1,360 | 1,390 | 1,341 | 1,312 | ||||||||||||||||||||||||

Provision for bad debt, net | 105 | 66 | (13 | ) | (47 | ) | 78 | (39 | ) | 9 | (21 | ) | ||||||||||||||||||||

Straight-line rent receivable, net | (1,623 | ) | (1,595 | ) | (1,595 | ) | (1,684 | ) | (1,907 | ) | (1,948 | ) | (1,741 | ) | (2,119 | ) | ||||||||||||||||

Stock-based compensation | 2,453 | 2,614 | 1,949 | 1,851 | 1,850 | 1,859 | 1,511 | 1,480 | ||||||||||||||||||||||||

Non-cash items | 2,474 | 2,440 | 1,680 | 1,506 | 1,381 | 1,262 | 1,120 | 652 | ||||||||||||||||||||||||

2nd Generation TI | (3,680 | ) | (5,277 | ) | (7,918 | ) | (6,013 | ) | (5,559 | ) | (4,202 | ) | (3,081 | ) | (3,627 | ) | ||||||||||||||||

Leasing commissions paid | (984 | ) | (1,584 | ) | (1,030 | ) | (1,514 | ) | (1,587 | ) | (1,079 | ) | (1,856 | ) | (1,050 | ) | ||||||||||||||||

Capital additions | (5,667 | ) | (2,520 | ) | (4,283 | ) | (5,088 | ) | (5,653 | ) | (2,098 | ) | (3,918 | ) | (3,402 | ) | ||||||||||||||||

Funds Available for Distribution | $37,454 | $37,960 | $35,584 | $34,012 | $32,671 | $35,546 | $33,407 | $33,315 | ||||||||||||||||||||||||

Funds from Operations per Common Share—Diluted | $0.38 | $0.38 | $0.40 | $0.39 | $0.42 | $0.39 | $0.40 | $0.41 | ||||||||||||||||||||||||

Normalized Funds from Operations Per Common Share—Diluted | $0.39 | $0.39 | $0.41 | $0.39 | $0.42 | $0.41 | $0.41 | $0.41 | ||||||||||||||||||||||||

Funds Available for Distribution Per Common Share - Diluted | $0.32 | $0.33 | $0.31 | $0.30 | $0.31 | $0.35 | $0.33 | $0.33 | ||||||||||||||||||||||||

Weighted Average Common Shares Outstanding - Diluted | 115,674 | 115,507 | 115,408 | 115,052 | 104,770 | 102,165 | 100,474 | 99,997 | ||||||||||||||||||||||||

(1) | Funds from operations (“FFO”) and FFO per share are operating performance measures adopted by the National Association of Real Estate Investment Trusts, Inc. (“NAREIT”). NAREIT defines FFO as the most commonly accepted and reported measure of a REIT’s operating performance equal to “net income (computed in accordance with GAAP), excluding gains (or losses) from sales of property, plus depreciation and amortization (including amortization of leasing commissions), and after adjustments for unconsolidated partnerships and joint ventures.” |

(2) | FFO, Normalized FFO and Funds Available for Distribution ("FAD") do not represent cash generated from operating activities determined in accordance with accounting principles generally accepted in the United States of America and is not necessarily indicative of cash available to fund cash needs. FFO, Normalized FFO and FAD should not be considered alternatives to net income attributable to common stockholders as indicators of the Company's operating performance or as alternatives to cash flow as measures of liquidity. |

(3) | Acquisition and pursuit costs include third party and travel costs related to the pursuit of acquisitions and developments. Beginning in 2017, FFO and FAD are normalized for all acquisition and pursuit costs. Prior to 2017, FFO and FAD were normalized for acquisition and pursuit costs associated with only those acquisitions that closed in the period. These changes were prompted by the Company's adoption of ASU 2017-01 which was effective January 1, 2017. |

(4) | For the first quarter of 2017, acquisition and pursuit costs were reduced by $24 thousand from what was previously reported to remove personnel costs. |

HEALTHCARE REALTY 9 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Capital Funding and Commitments

(dollars in thousands)

ACQUISITION AND RE/DEVELOPMENT FUNDING | |||||||||||||||

2017 | 2016 | ||||||||||||||

Q2 | Q1 | Q4 | Q3 | Q2 | |||||||||||

Acquisitions | $50,786 | $13,513 | $63,775 | $98,290 | $41,615 | ||||||||||

Re/development | 8,940 | 12,159 | 9,567 | 10,939 | 8,542 | ||||||||||

1st generation TI & planned capital expenditures for acquisitions (1) | 1,380 | 1,212 | 4,807 | 4,471 | 5,486 | ||||||||||

MAINTENANCE CAPITAL EXPENDITURES | |||||||||||||||

$ Spent | |||||||||||||||

2nd generation TI | $3,680 | $5,277 | $7,918 | $6,013 | $5,559 | ||||||||||

Leasing commissions paid | 984 | 1,584 | 1,030 | 1,514 | 1,587 | ||||||||||

Capital expenditures | 5,667 | 2,520 | 4,283 | 5,088 | 5,653 | ||||||||||

Total | $10,331 | $9,381 | $13,231 | $12,615 | $12,799 | ||||||||||

% of NOI | |||||||||||||||

2nd generation TI | 5.6 | % | 8.1 | % | 11.9 | % | 9.4 | % | 8.7 | % | |||||

Leasing commissions paid | 1.5 | % | 2.4 | % | 1.6 | % | 2.4 | % | 2.5 | % | |||||

Capital expenditures | 8.7 | % | 3.8 | % | 6.5 | % | 7.9 | % | 8.8 | % | |||||

Total | 15.8 | % | 14.3 | % | 19.9 | % | 19.7 | % | 20.0 | % | |||||

LEASING COMMITMENTS | |||||||||||||||

Renewals | |||||||||||||||

Square feet | 279,738 | 332,527 | 234,641 | 399,263 | 259,936 | ||||||||||

2nd generation TI / square feet / lease year | $2.30 | $1.93 | $1.84 | $0.95 | $1.53 | ||||||||||

Leasing commissions / square feet / lease year | $0.39 | $0.28 | $0.50 | $0.44 | $0.36 | ||||||||||

New leases | |||||||||||||||

Square feet | 134,590 | 73,285 | 82,417 | 119,463 | 140,417 | ||||||||||

2nd generation TI / square feet / lease year | $2.10 | $4.78 | $4.91 | $5.55 | $1.74 | ||||||||||

Leasing commissions / square feet / lease year | $0.47 | $1.10 | $1.36 | $0.94 | $0.30 | ||||||||||

All | |||||||||||||||

Square feet | 414,328 | 405,812 | 317,058 | 518,726 | 400,353 | ||||||||||

2nd generation TI / square feet / lease year | $2.18 | $2.69 | $3.10 | $2.84 | $1.66 | ||||||||||

Leasing commissions / square feet / lease year | $0.44 | $0.50 | $0.85 | $0.65 | $0.32 | ||||||||||

% of annual net rent | 12.8 | % | 15.6 | % | 18.7 | % | 16.6 | % | 11.7 | % | |||||

(1) | Planned capital expenditures for acquisitions include expected near-term fundings that were contemplated as part of the acquisition. |

HEALTHCARE REALTY 10 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Debt Metrics

(dollars in thousands)

SUMMARY OF INDEBTEDNESS | ||||||||||

Q2 2017 Interest Expense | Balance as of 6/30/2017 | Weighted Months to Maturity | Effective Interest Rate | |||||||

Senior Notes due 2021, net of discount | $5,835 | $397,483 | 43 | 5.97 | % | |||||

Senior Notes due 2023, net of discount | 2,393 | 247,499 | 70 | 3.95 | % | |||||

Senior Notes due 2025, net of discount (1) | 2,469 | 247,930 | 94 | 4.08 | % | |||||

Total Senior Notes Outstanding | $10,697 | $892,912 | 64 | 4.89 | % | |||||

Unsecured credit facility due 2020 | 555 | 35,000 | 37 | 2.22 | % | |||||

Unsecured term loan facility due 2019 | 835 | 149,609 | 20 | 2.42 | % | |||||

Mortgage notes payable, net | 1,508 | 125,625 | 76 | 5.06 | % | |||||

Total Outstanding Notes and Bonds Payable | $13,595 | $1,203,146 | 59 | 4.52 | % | |||||

Interest cost capitalization | (246) | |||||||||

Unsecured credit facility fee and deferred financing costs | 966 | |||||||||

Total Quarterly Consolidated Interest Expense | $14,315 | |||||||||

SELECTED FINANCIAL DEBT COVENANTS (2) | |||||||

Calculation | Requirement | Trailing Twelve Months Ended 6/30/2017 | |||||

Revolving Credit Facility and Term Loan | |||||||

Leverage Ratio | Total Debt / Total Capital | Not greater than 60% | 32.5 | % | |||

Secured Leverage Ratio | Total Secured Debt / Total Capital | Not greater than 30% | 3.4 | % | |||

Unencumbered Leverage Ratio | Unsecured Debt / Unsecured Real Estate | Not greater than 60% | 33.1 | % | |||

Fixed Charge Coverage Ratio | EBITDA / Fixed Charges | Not less than 1.50x | 3.9x | ||||

Unsecured Coverage Ratio | Unsecured EBITDA / Unsecured Interest | Not less than 1.75x | 4.3x | ||||

Construction and Development | CIP / Total Assets | Not greater than 15% | 0.0 | % | |||

Asset Investments | Mortgages & Unimproved Land / Total Assets | Not greater than 20% | 0.7 | % | |||

Senior Notes | |||||||

Incurrence of Total Debt | Total Debt / Total Assets | Not greater than 60% | 31.7 | % | |||

Incurrence of Debt Secured by Any Lien | Secured Debt / Total Assets | Not greater than 40% | 3.3 | % | |||

Maintenance of Total Unsecured Assets | Unencumbered Assets / Unsecured Debt | Not less than 150% | 320.4 | % | |||

Debt Service Coverage | EBITDA / Interest Expense | Not less than 1.5x | 4.3x | ||||

Other | |||||||

Net Debt to adjusted EBITDA (3) | Net debt (debt less cash) / adjusted EBITDA | Not required | 4.9x | ||||

Net Debt to Enterprise Value (4) | Net debt (debt less cash) / Enterprise Value | Not required | 23.6 | % | |||

(1) | The effective interest rate includes the impact of the $1.7 million settlement of a forward-starting interest rate swap that is included in accumulated other comprehensive income on the Company's Condensed Consolidated Balance Sheets. |

(2) | Does not include all financial and non-financial covenants and restrictions that are required by the Company's various debt agreements. |

(3) | Adjusted EBITDA is based on the current quarter results, annualized. See page 21 for a reconciliation of adjusted EBITDA. |

(4) | Based on the closing price of $33.30 on July 31, 2017 and 116,545,032 shares outstanding. |

HEALTHCARE REALTY 11 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Investment Activity

(dollars in thousands)

ACQUISITION/DISPOSITION ACTIVITY | |||||||||||||||||

Location | Property Type (1) | Miles to Campus | Health System Affiliation | Closing | Purchase Price | Square Feet | Leased % | Cap Rate (2) | |||||||||

Acquisitions | |||||||||||||||||

St. Paul, MN (3) | MOB | 0.00 | Fairview Health | 3/6/2017 | $13,513 | 34,608 | 100 | % | 5.9 | % | |||||||

San Francisco, CA | MOB | 0.00 | Sutter Health | 6/12/2017 | 26,786 | 75,649 | 100 | % | 5.3 | % | |||||||

Washington, DC | MOB | 0.00 | Trinity Health | 6/13/2017 | 24,000 | 62,379 | 100 | % | 5.4 | % | |||||||

Los Angeles, CA | MOB | 0.00 | HCA | 7/31/2017 | 16,300 | 42,780 | 93 | % | 5.4 | % | |||||||

2017 Acquisition Activity | $80,599 | 215,416 | 99 | % | 5.5 | % | |||||||||||

Dispositions | |||||||||||||||||

Evansville, IN (3) | OTH | NA | NA | 3/6/2017 | $6,375 | 29,500 | 100 | % | 8.9 | % | |||||||

Columbus, GA | MOB | 0.22 | Columbus Reg | 3/7/2017 | 625 | 12,000 | 0 | % | (6.4 | )% | |||||||

Las Vegas, NV | MOB | 1.38 | NA | 3/30/2017 | 5,500 | 18,147 | 100 | % | 6.7 | % | |||||||

Texas (3 properties) (3) | IRF | NA | NA | 3/31/2017 | 69,500 | 169,722 | 100 | % | 7.3 | % | |||||||

Chicago, IL | MOB | 0.40 | NA | 6/16/2017 | 450 | 5,100 | 0 | % | (9.1 | )% | |||||||

San Antonio, TX (3) | IRF | NA | NA | 6/29/2017 | 14,500 | 39,786 | 100 | % | 7.3 | % | |||||||

Roseburg, OR | MOB | 0.00 | CHI | 6/29/2017 | 23,200 | 62,246 | 100 | % | 6.6 | % | |||||||

2017 Disposition Activity | $120,150 | 336,501 | 95 | % | 7.1 | % | |||||||||||

HISTORICAL INVESTMENT ACTIVITY | ||||||||||||||||||||||||

Acquisitions (4) | Mortgage Funding | Construction Mortgage Funding | Re/Development Funding | Total Investments | Dispositions | |||||||||||||||||||

2013 | $ | 216,956 | $ | — | $ | 58,731 | $ | — | $ | 275,687 | $ | 101,910 | ||||||||||||

2014 | 85,077 | 1,900 | 1,244 | 4,384 | 92,605 | 34,840 | ||||||||||||||||||

2015 | 187,216 | — | — | 27,859 | 215,075 | 157,975 | ||||||||||||||||||

2016 | 241,939 | — | — | 45,343 | 287,282 | 94,683 | ||||||||||||||||||

2017 | 80,599 | — | — | 21,099 | 101,698 | 120,150 | ||||||||||||||||||

Total | $ | 811,787 | $ | 1,900 | $ | 59,975 | $ | 98,685 | $ | 972,347 | $ | 509,558 | ||||||||||||

% of Total | 83.5 | % | 0.2 | % | 6.2 | % | 10.1 | % | 100.0 | % | ||||||||||||||

RE/DEVELOPMENT ACTIVITY | ||||||||||||||||||||

Location | Type (5) | Campus Location | Square Feet | Budget | Amount Funded Q2 2017 | Total Amount Funded Through 6/30/2017 | Estimated Remaining Fundings | Aggregate Leased % | Estimated Completion Date | |||||||||||

Same store redevelopment | ||||||||||||||||||||

Charlotte, NC (6) | Redev | ON | 204,000 | $12,000 | $69 | $304 | $11,696 | 85 | % | Q1 2019 | ||||||||||

Pre-construction activity (7) | ||||||||||||||||||||

Seattle, WA | Dev | ON | 151,000 | 64,120 | 592 | 1,260 | 62,860 | 60 | % | Q1 2019 | ||||||||||

Total Re/development activity | 355,000 | $76,120 | $661 | $1,564 | $74,556 | 74 | % | |||||||||||||

(1) | MOB = Medical Office Building; IRF = Inpatient Rehabilitation Facility; OTH = Other |

(2) | For acquisitions, cap rate represents the forecasted first year NOI / purchase price plus acquisition costs and expected capital additions. For dispositions, cap rate represents the next twelve month forecasted NOI / sales price. |

(3) | Single-tenant net lease property. |

(4) | Net of mortgage notes receivable payoffs upon acquisition. |

(5) | Redev = Redevelopment; Dev = Development |

(6) | Redevelopment project is a 38,000 square foot expansion to an existing medical office building. |

(7) | Includes projects that are in the design phase, but are expected to begin construction once permits and final contracts are executed. |

HEALTHCARE REALTY 12 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Portfolio by Market

(dollars in thousands)

BY MARKET | |||||||||||||||||||||

SQUARE FEET | |||||||||||||||||||||

MOB/OUTPATIENT (92.9%) | INPATIENT (3.7%) | OTHER (3.4%) | |||||||||||||||||||

MSA Rank | Investment(1) | Multi-tenant | Single-tenant Net | Rehab | Surgical | Multi-tenant | Single-tenant Net | Total | % of Total | ||||||||||||

Dallas - Fort Worth, TX | 4 | $472,426 | 2,149,939 | 156,245 | 2,306,184 | 15.9 | % | ||||||||||||||

Seattle - Bellevue, WA | 15 | 405,834 | 890,222 | 67,510 | 957,732 | 6.6 | % | ||||||||||||||

Charlotte, NC | 22 | 167,526 | 820,457 | 820,457 | 5.7 | % | |||||||||||||||

Nashville, TN | 36 | 148,950 | 766,523 | 766,523 | 5.3 | % | |||||||||||||||

Los Angeles, CA | 2 | 163,702 | 551,383 | 63,000 | 614,383 | 4.2 | % | ||||||||||||||

Houston, TX | 5 | 129,275 | 591,027 | 591,027 | 4.1 | % | |||||||||||||||

Richmond, VA | 45 | 145,789 | 548,801 | 548,801 | 3.8 | % | |||||||||||||||

Des Moines, IA | 89 | 133,125 | 233,413 | 146,542 | 152,655 | 532,610 | 3.7 | % | |||||||||||||

Memphis, TN | 42 | 92,625 | 515,876 | 515,876 | 3.6 | % | |||||||||||||||

San Antonio, TX | 24 | 94,346 | 483,811 | 483,811 | 3.3 | % | |||||||||||||||

Denver, CO | 19 | 133,297 | 446,292 | 34,068 | 480,360 | 3.3 | % | ||||||||||||||

Roanoke, VA | 160 | 49,003 | 334,454 | 126,427 | 460,881 | 3.2 | % | ||||||||||||||

Indianapolis, IN | 34 | 74,879 | 382,695 | 382,695 | 2.6 | % | |||||||||||||||

Austin, TX | 31 | 102,143 | 354,481 | 12,880 | 367,361 | 2.5 | % | ||||||||||||||

Washington, DC | 6 | 100,077 | 348,998 | 348,998 | 2.4 | % | |||||||||||||||

Honolulu, HI | 54 | 141,250 | 298,427 | 298,427 | 2.1 | % | |||||||||||||||

San Francisco, CA | 11 | 116,777 | 286,270 | 286,270 | 2.0 | % | |||||||||||||||

Oklahoma City, OK | 41 | 109,110 | 68,860 | 200,000 | 268,860 | 1.9 | % | ||||||||||||||

Miami, FL | 8 | 54,788 | 241,980 | 241,980 | 1.7 | % | |||||||||||||||

Colorado Springs, CO | 79 | 52,189 | 241,224 | 241,224 | 1.7 | % | |||||||||||||||

Chicago, IL | 3 | 56,396 | 238,391 | 238,391 | 1.6 | % | |||||||||||||||

Detroit, MI | 14 | 24,007 | 199,749 | 11,308 | 211,057 | 1.5 | % | ||||||||||||||

Minneapolis, MN | 16 | 61,729 | 172,900 | 34,608 | 207,508 | 1.4 | % | ||||||||||||||

South Bend, IN | 156 | 44,229 | 205,573 | 205,573 | 1.4 | % | |||||||||||||||

Springfield, MO | 113 | 111,293 | 186,000 | 186,000 | 1.3 | % | |||||||||||||||

Other (22 markets) | 401,607 | 1,341,806 | 287,874 | 90,123 | 185,364 | 1,905,167 | 13.2 | % | |||||||||||||

Total | $3,586,372 | 12,379,098 | 1,070,988 | 187,191 | 342,245 | 291,962 | 196,672 | 14,468,156 | 100.0 | % | |||||||||||

Number of Properties | 168 | 14 | 3 | 2 | 4 | 6 | 197 | ||||||||||||||

Percent of Square Feet | 85.5 | % | 7.4 | % | 1.3 | % | 2.4 | % | 2.0 | % | 1.4 | % | 100.0 | % | |||||||

Investment (1) | $2,992,506 | $262,568 | $45,454 | $208,725 | $56,136 | $20,983 | $3,586,372 | ||||||||||||||

% of Investment | 83.4 | % | 7.3 | % | 1.3 | % | 5.8 | % | 1.6 | % | 0.6 | % | 100.0 | % | |||||||

Multi-tenant | Single-tenant Net | Total | ||||

Number of Properties | 172 | 25 | 197 | |||

Square Feet | 12,671,060 | 1,797,096 | 14,468,156 | |||

Percent of Square Feet | 87.6 | % | 12.4 | % | 100.0 | % |

Investment (1) | $3,048,642 | $537,730 | $3,586,372 | |||

% of Investment | 85.0 | % | 15.0 | % | 100.0 | % |

(1) | Excludes gross assets held for sale, land held for development, construction in progress and corporate property. |

HEALTHCARE REALTY 13 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Square Feet by Health System (1)

MOB SQUARE FEET | ||||||||||||||||||||||

System Rank (3) | Credit Rating | ASSOCIATED (93.7%) (2) | Total MOB SF | % of Total MOB SF | ||||||||||||||||||

Top Health Systems | On | Adjacent (4) | Anchored (5) | Off | ||||||||||||||||||

Baylor Scott & White Health | 20 | AA-/Aa3 | 1,834,256 | 129,879 | 163,188 | — | 2,127,323 | 15.8 | % | |||||||||||||

Ascension Health | 3 | AA+/Aa2 | 1,017,085 | 148,356 | 30,096 | — | 1,195,537 | 8.9 | % | |||||||||||||

Catholic Health Initiatives | 7 | BBB+/Baa1 | 807,182 | 180,125 | 95,486 | — | 1,082,793 | 8.1 | % | |||||||||||||

Carolinas HealthCare System | 31 | --/Aa3 | 353,537 | 98,066 | 313,513 | — | 765,116 | 5.7 | % | |||||||||||||

HCA | 2 | BB/B1 | 389,931 | 177,155 | 157,388 | — | 724,474 | 5.4 | % | |||||||||||||

Tenet Healthcare Corporation | 5 | B/B2 | 570,264 | 67,790 | — | — | 638,054 | 4.7 | % | |||||||||||||

Bon Secours Health System | 61 | A/A2 | 548,801 | — | — | — | 548,801 | 4.1 | % | |||||||||||||

Baptist Memorial Health Care | 109 | A-/-- | 424,306 | — | 39,345 | — | 463,651 | 3.4 | % | |||||||||||||

Indiana University Health | 26 | AA/Aa2 | 280,129 | 102,566 | — | — | 382,695 | 2.8 | % | |||||||||||||

University of Colorado Health | 76 | AA-/Aa3 | 150,291 | 161,099 | 33,850 | — | 345,240 | 2.6 | % | |||||||||||||

Trinity Health | 8 | AA-/Aa3 | 267,952 | 73,331 | — | — | 341,283 | 2.5 | % | |||||||||||||

Providence Health & Services | 9 | AA-/Aa3 | 176,854 | 129,181 | — | — | 306,035 | 2.3 | % | |||||||||||||

University of Washington | 40 | AA+/Aaa | 194,536 | 69,712 | — | — | 264,248 | 2.0 | % | |||||||||||||

Medstar Health | 36 | A/A2 | 241,739 | — | — | — | 241,739 | 1.8 | % | |||||||||||||

Advocate Health Care | 33 | AA+/Aa2 | 142,955 | 95,436 | — | — | 238,391 | 1.8 | % | |||||||||||||

Memorial Hermann | 42 | A+/A1 | — | 206,090 | — | — | 206,090 | 1.5 | % | |||||||||||||

Community Health | 4 | B/B2 | 201,574 | — | — | — | 201,574 | 1.5 | % | |||||||||||||

Mercy (St. Louis) | 35 | AA-/Aa3 | — | — | 200,000 | — | 200,000 | 1.5 | % | |||||||||||||

Overlake Health System | 333 | A/A2 | 191,051 | — | — | — | 191,051 | 1.4 | % | |||||||||||||

Sutter Health | 13 | AA-/Aa3 | 175,591 | — | — | — | 175,591 | 1.3 | % | |||||||||||||

Other credit rated | 1,028,985 | 560,499 | 90,607 | — | 1,680,091 | 12.5 | % | |||||||||||||||

Subtotal - credit rated (6) | 8,997,019 | 2,199,285 | 1,123,473 | — | 12,319,777 | 91.6 | % | |||||||||||||||

Non-credit rated | 136,155 | 144,910 | — | 849,244 | 1,130,309 | 8.4 | % | |||||||||||||||

Total | 9,133,174 | 2,344,195 | 1,123,473 | 849,244 | 13,450,086 | 100.0 | % | |||||||||||||||

% of Total | 67.9 | % | 17.4 | % | 8.4 | % | 6.3 | % | ||||||||||||||

LEASED SQUARE FEET | ||||||||||||||||||||||

LEASED SQUARE FEET | ||||||||||||||||||||||

Top Health Systems | System Rank (3) | Credit Rating | # of Buildings | # of Leases | MOB | Inpatient / Other | Total | % of Total Leased SF | % of Total Revenue | |||||||||||||

Baylor Scott & White Health | 20 | AA-/Aa3 | 20 | 163 | 1,022,630 | 156,245 | 1,178,875 | 9.3 | % | 9.8 | % | |||||||||||

Mercy (St. Louis) | 35 | AA-/Aa3 | 2 | 2 | 200,000 | 186,000 | 386,000 | 3.0 | % | 4.3 | % | |||||||||||

Carolinas HealthCare System | 31 | --/Aa3 | 16 | 78 | 591,504 | — | 591,504 | 4.7 | % | 4.3 | % | |||||||||||

Catholic Health Initiatives | 7 | BBB+/Baa1 | 14 | 69 | 487,170 | — | 487,170 | 3.8 | % | 3.8 | % | |||||||||||

Bon Secours Health System | 61 | A/A2 | 7 | 61 | 264,843 | — | 264,843 | 2.1 | % | 2.2 | % | |||||||||||

HCA | 2 | BB/B1 | 12 | 14 | 404,597 | — | 404,597 | 3.2 | % | 2.1 | % | |||||||||||

Indiana University Health | 26 | AA/Aa2 | 3 | 38 | 255,347 | — | 255,347 | 2.0 | % | 1.9 | % | |||||||||||

Ascension Health | 3 | AA+/Aa2 | 14 | 53 | 312,273 | — | 312,273 | 2.5 | % | 1.8 | % | |||||||||||

Baptist Memorial Health Care | 109 | A-/-- | 6 | 14 | 111,002 | — | 111,002 | 0.9 | % | 1.7 | % | |||||||||||

Tenet Healthcare Corporation | 5 | B/B2 | 10 | 36 | 124,227 | 63,000 | 187,227 | 1.5 | % | 1.6 | % | |||||||||||

Total | 33.0 | % | 33.5 | % | ||||||||||||||||||

(1) | Excludes mortgage notes receivable, construction in progress and assets classified as held for sale. |

(2) | Includes total square feet of buildings located on-campus, adjacent and off-campus/anchored by healthcare systems. |

(3) | Ranked by revenue based on Modern Healthcare's Healthcare Systems Financials Database. |

(4) | The Company defines an adjacent property as being no more than 0.25 miles from a hospital campus. |

(5) | Includes buildings where health systems lease 40% or more of the property. |

(6) | Based on square footage, 91.6% of HR's MOB portfolio is associated with a credit-rated healthcare provider and 79.8% is associated with an investment-grade rated healthcare provider. |

HEALTHCARE REALTY 14 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Square Feet by Proximity (1)(2)

MEDICAL OFFICE BUILDINGS BY LOCATION | ||||||||||||||||||

2017 | 2016 | |||||||||||||||||

Q2 | Q1 | Q4 | Q3 | Q2 | Q1 | |||||||||||||

On campus | 68 | % | 67 | % | 67 | % | 67 | % | 66 | % | 66 | % | ||||||

Adjacent to campus (3) | 17 | % | 18 | % | 18 | % | 18 | % | 18 | % | 18 | % | ||||||

Total on/adjacent | 85 | % | 85 | % | 85 | % | 85 | % | 84 | % | 84 | % | ||||||

Off campus - anchored by hospital system (4) | 9 | % | 9 | % | 9 | % | 8 | % | 9 | % | 9 | % | ||||||

Off campus | 6 | % | 6 | % | 6 | % | 7 | % | 7 | % | 7 | % | ||||||

100 | % | 100 | % | 100 | % | 100 | % | 100 | % | 100 | % | |||||||

MEDICAL OFFICE BUILDINGS BY DISTANCE TO HOSPITAL CAMPUS | |||||||||||||||||

Ground Lease Properties | |||||||||||||||||

Greater than | Less than or equal to | Number of Buildings | Square Feet | % of Total | Cumulative % | Campus Proximity | Square Feet | % of Total | |||||||||

0.00 | 115 | 9,133,174 | 68 | % | 68 | % | On campus | 7,060,583 | 90.6 | % | |||||||

0.00 | 250 yards | 18 | 1,222,987 | 9 | % | 77 | % | Adjacent (3) | 80,525 | 1.0 | % | ||||||

250 yards | 0.25 miles | 19 | 1,121,208 | 8 | % | 85 | % | 120,036 | 1.5 | % | |||||||

0.25 miles | 0.50 | 1 | 124,925 | 1 | % | 86 | % | Off campus | - | — | % | ||||||

0.50 | 1.00 | 3 | 304,993 | 2 | % | 88 | % | - | — | % | |||||||

1.00 | 2.00 | 6 | 590,339 | 4 | % | 92 | % | 319,446 | 4.1 | % | |||||||

2.00 | 5.00 | 10 | 476,633 | 4 | % | 96 | % | 13,818 | 0.2 | % | |||||||

5.00 | 10.00 | 6 | 332,359 | 3 | % | 99 | % | 205,631 | 2.6 | % | |||||||

10.00 | 4 | 143,468 | 1 | % | 100 | % | - | — | % | ||||||||

Total | 182 | 13,450,086 | 100 | % | 7,800,039 | 100.0 | % | ||||||||||

(1) | Excludes mortgage notes receivable, construction in progress and assets classified as held for sale. |

(2) | Proximity to hospital campus includes acute care hospitals with inpatient beds. The Company does not consider inpatient rehab hospitals (IRFs), skilled nursing facilities (SNFs) or long-term acute care hospitals (LTACHs) to be hospital campuses for distance calculations. |

(3) | Beginning in Q1 2016, the Company adopted a definition of an adjacent property as being no more than 0.25 miles from a hospital campus. |

(4) | Includes buildings where health systems lease 40% or more of the property. |

HEALTHCARE REALTY 15 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Lease Maturity, Size and Building Square Feet (1)

(dollars in thousands)

LEASE MATURITY SCHEDULE | ||||||||||||||||||||||||||

MULTI-TENANT | SINGLE-TENANT NET LEASE | TOTAL | ||||||||||||||||||||||||

Number of Leases | Square Feet | % of Square Feet | Number of Leases | Square Feet | % of Square Feet | Number of Leases | Square Feet | % of Total Square Feet | % of Base Revenue (2) | |||||||||||||||||

2017 | 343 | 1,162,031 | 10.7 | % | 5 | 334,454 | 18.6 | % | 348 | 1,496,485 | 11.8 | % | 11.2 | % | ||||||||||||

2018 | 456 | 1,541,496 | 14.2 | % | — | — | — | % | 456 | 1,541,496 | 12.2 | % | 12.0 | % | ||||||||||||

2019 | 495 | 2,053,238 | 18.9 | % | 8 | 342,305 | 19.0 | % | 503 | 2,395,543 | 18.9 | % | 18.4 | % | ||||||||||||

2020 | 369 | 1,447,225 | 13.3 | % | 1 | 83,318 | 4.7 | % | 370 | 1,530,543 | 12.0 | % | 11.9 | % | ||||||||||||

2021 | 297 | 1,105,381 | 10.2 | % | — | — | — | % | 297 | 1,105,381 | 8.7 | % | 8.7 | % | ||||||||||||

2022 | 188 | 820,813 | 7.4 | % | 1 | 58,285 | 3.2 | % | 189 | 879,098 | 6.9 | % | 7.0 | % | ||||||||||||

2023 | 140 | 747,757 | 6.9 | % | — | — | — | % | 140 | 747,757 | 5.9 | % | 6.1 | % | ||||||||||||

2024 | 129 | 736,327 | 6.8 | % | — | — | — | % | 129 | 736,327 | 5.8 | % | 5.3 | % | ||||||||||||

2025 | 62 | 489,606 | 4.5 | % | 2 | 91,561 | 5.1 | % | 64 | 581,167 | 4.6 | % | 3.9 | % | ||||||||||||

2026 | 61 | 209,875 | 1.9 | % | — | — | — | % | 61 | 209,875 | 1.7 | % | 1.7 | % | ||||||||||||

Thereafter | 90 | 566,669 | 5.2 | % | 8 | 887,173 | 49.4 | % | 98 | 1,453,842 | 11.5 | % | 13.8 | % | ||||||||||||

Total leased | 2,630 | 10,880,418 | 85.9 | % | 25 | 1,797,096 | 100.0 | % | 2,655 | 12,677,514 | 87.6 | % | 100.0 | % | ||||||||||||

Total building | 12,671,060 | 100.0 | % | 1,797,096 | 100.0 | % | 14,468,156 | 100.0 | % | |||||||||||||||||

BY LEASE SIZE | ||||||

NUMBER OF LEASES | ||||||

Square Feet | Multi-Tenant Properties (3) | Single-Tenant Net Lease Properties | ||||

0 - 2,500 | 1,398 | — | ||||

2,501 - 5,000 | 649 | — | ||||

5,001 - 7,500 | 213 | 1 | ||||

7,501 - 10,000 | 120 | — | ||||

10,001 + | 250 | 24 | ||||

Total Leases | 2,630 | 25 | ||||

BY BUILDING SQUARE FEET | |||||||||

Size Range by Square Feet | % of Total | Total Square Footage | Average Square Feet | Number of Properties | |||||

>100,000 | 44.2 | % | 6,395,112 | 148,724 | 43 | ||||

<100,000 and >75,000 | 24.4 | % | 3,528,743 | 86,067 | 41 | ||||

<75,000 and >50,000 | 16.5 | % | 2,390,775 | 62,915 | 38 | ||||

<50,000 | 14.9 | % | 2,153,526 | 28,714 | 75 | ||||

Total | 100.0 | % | 14,468,156 | 73,442 | 197 | ||||

(1) | Excludes mortgage notes receivable, land held for development, construction in progress, corporate property and assets classified as held for sale. |

(2) | Represents the current annualized minimum rents on in-place leases, excluding the impact of potential lease renewals and sponsor support payments under financial support arrangements and straight-line rent. |

(3) | The average lease size in the multi-tenant properties is 4,137 square feet. |

HEALTHCARE REALTY 16 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Historical Occupancy (1)

(dollars in thousands)

2017 | 2016 | ||||||||||||||

Q2 | Q1 | Q4 | Q3 | Q2 | |||||||||||

Same store properties | |||||||||||||||

Multi-tenant | |||||||||||||||

Investment | $2,492,031 | $2,493,309 | $2,438,564 | $2,300,520 | $2,284,072 | ||||||||||

Number of properties | 137 | 138 | 139 | 136 | 135 | ||||||||||

Total building square feet | 10,764,672 | 10,801,498 | 10,690,819 | 10,288,750 | 10,252,590 | ||||||||||

% occupied | 88.0 | % | 87.7 | % | 87.3 | % | 87.8 | % | 87.8 | % | |||||

Single-tenant | |||||||||||||||

Investment | $524,444 | $524,268 | $617,908 | $677,171 | $673,865 | ||||||||||

Number of properties | 24 | 24 | 30 | 34 | 34 | ||||||||||

Total building square feet | 1,762,488 | 1,762,488 | 2,080,227 | 2,284,747 | 2,284,747 | ||||||||||

% occupied | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | |||||

Total same store properties | |||||||||||||||

Investment | $3,016,475 | $3,017,577 | $3,056,472 | $2,977,691 | $2,957,937 | ||||||||||

Number of properties | 161 | 162 | 169 | 170 | 169 | ||||||||||

Total building square feet | 12,527,160 | 12,563,986 | 12,771,046 | 12,573,497 | 12,537,337 | ||||||||||

% occupied | 89.7 | % | 89.4 | % | 89.3 | % | 90.0 | % | 90.0 | % | |||||

Acquisitions (2) | |||||||||||||||

Investment | $445,164 | $405,975 | $431,859 | $402,267 | $331,992 | ||||||||||

Number of properties | 19 | 18 | 18 | 15 | 15 | ||||||||||

Total building square feet | 1,113,659 | 1,011,189 | 1,087,260 | 1,003,876 | 921,069 | ||||||||||

% occupied | 94.0 | % | 93.0 | % | 94.4 | % | 95.0 | % | 95.0 | % | |||||

Development Completions (3) | |||||||||||||||

Investment | $26,967 | $5,353 | $5,353 | $5,057 | $4,817 | ||||||||||

Number of properties | 2 | 1 | 1 | 1 | 1 | ||||||||||

Total building square feet | 112,837 | 12,880 | 12,880 | 12,880 | 12,958 | ||||||||||

% occupied | 11.4 | % | 100.0 | % | 100.0 | % | 100.0 | % | 15.2 | % | |||||

% leased | 42.4 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | |||||

Reposition (4) | |||||||||||||||

Investment | $97,766 | $96,134 | $97,176 | $148,489 | $153,878 | ||||||||||

Number of properties | 15 | 14 | 14 | 16 | 17 | ||||||||||

Total building square feet | 714,500 | 704,362 | 709,462 | 951,568 | 995,472 | ||||||||||

% occupied | 53.5 | % | 52.5 | % | 52.8 | % | 59.3 | % | 57.0 | % | |||||

Total | |||||||||||||||

Investment | $3,586,372 | $3,525,039 | $3,590,860 | $3,533,504 | $3,448,624 | ||||||||||

Number of properties | 197 | 195 | 202 | 202 | 202 | ||||||||||

Total building square feet | 14,468,156 | 14,292,417 | 14,580,648 | 14,541,821 | 14,466,836 | ||||||||||

% occupied | 87.6 | % | 87.8 | % | 87.9 | % | 88.4 | % | 88.0 | % | |||||

(1) | Excludes mortgage notes receivable, land held for development, construction in progress, corporate property and assets classified as held for sale. |

(2) | Acquisition include properties acquired within the last 8 quarters of the period presented and are excluded from same store. |

(3) | Development completions consist of two properties, with the core and shell of one property reaching completion in June 2017 that is 35% leased and 0% occupied as of June 30, 2017. |

(4) | Reposition includes properties that meet any of the Company-defined criteria: properties having less than 60% occupancy that is expected to last at least two quarters; properties that experience a loss of occupancy over 30% in a single quarter; properties with negative net operating income that is expected to last at least two quarters; or condemnation. |

HEALTHCARE REALTY 17 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Occupancy Reconciliation

(dollars in thousands)

SEQUENTIAL | |||||||||||||||||

PORTFOLIO | SAME STORE | ||||||||||||||||

Occupied Square Feet | Total Square Feet | Occupancy | Occupied Square Feet | Total Square Feet | Occupancy | ||||||||||||

March 31, 2017 | 12,554,019 | 14,292,417 | 87.8 | % | 11,230,870 | 12,563,986 | 89.4 | % | |||||||||

Portfolio Activity | |||||||||||||||||

Acquisitions | 138,028 | 138,028 | 100.0 | % | NA | NA | NA | ||||||||||

Re/Development completions | — | 99,957 | — | % | — | — | — | % | |||||||||

Dispositions (2) | (62,246 | ) | (62,246 | ) | 100.0 | % | (62,246 | ) | (62,246 | ) | 100.0 | % | |||||

Reclassifications to same store: | |||||||||||||||||

Acquisitions | NA | NA | NA | 33,148 | 35,558 | 93.2 | % | ||||||||||

Development completions | NA | NA | NA | — | — | — | % | ||||||||||

Reposition | NA | NA | NA | (7,493 | ) | (10,138 | ) | 73.9 | % | ||||||||

Subtotal | 12,629,801 | 14,468,156 | 87.3 | % | 11,194,279 | 12,527,160 | 89.4 | % | |||||||||

Leasing Activity | |||||||||||||||||

New leases/expansions | 169,064 | NA | NA | 148,957 | NA | NA | |||||||||||

Move-outs/contractions | (121,351 | ) | NA | NA | (107,255 | ) | NA | NA | |||||||||

Net Absorption | 47,713 | NA | NA | 41,702 | NA | NA | |||||||||||

June 30, 2017 | 12,677,514 | 14,468,156 | 87.6 | % | 11,235,981 | 12,527,160 | 89.7 | % | |||||||||

YEAR-OVER-YEAR | |||||||||||||||||

PORTFOLIO | SAME STORE | ||||||||||||||||

Occupied Square Feet | Total Square Feet | Occupancy | Occupied Square Feet | Total Square Feet | Occupancy | ||||||||||||

June 30, 2016 | 12,727,048 | 14,466,758 | 88.0 | % | 11,282,401 | 12,537,337 | 90.0 | % | |||||||||

Portfolio Activity | |||||||||||||||||

Acquisitions | 555,910 | 576,286 | 96.5 | % | NA | NA | NA | ||||||||||

Re/Development completions (1) | — | 149,046 | — | % | — | 49,089 | — | % | |||||||||

Dispositions (2) | (715,923 | ) | (723,934 | ) | 98.9 | % | (715,923 | ) | (718,834 | ) | 99.6 | % | |||||

Reclassifications to same store: | |||||||||||||||||

Acquisitions | NA | NA | NA | 371,558 | 383,696 | 96.8 | % | ||||||||||

Development completions | NA | NA | NA | — | — | — | % | ||||||||||

Reposition | NA | NA | NA | 191,763 | 275,872 | 69.5 | % | ||||||||||

Subtotal | 12,567,035 | 14,468,156 | 86.9 | % | 11,129,799 | 12,527,160 | 88.8 | % | |||||||||

Leasing Activity | |||||||||||||||||

New leases/expansions | 604,071 | NA | NA | 513,499 | NA | NA | |||||||||||

Move-outs/contractions | (493,592 | ) | NA | NA | (407,317 | ) | NA | NA | |||||||||

Net Absorption | 110,479 | NA | NA | 106,182 | NA | NA | |||||||||||

June 30, 2017 | 12,677,514 | 14,468,156 | 87.6 | % | 11,235,981 | 12,527,160 | 89.7 | % | |||||||||

(1) | Includes the completion of 70,000 square feet vertical expansion that was completed in the fourth quarter of 2016. The net increase to total square feet was 49,089 due to a portion of the original building that was demolished to begin construction of the expansion. |

(2) | Includes properties reclassified as held for sale. |

HEALTHCARE REALTY 18 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Same Store Leasing Statistics (1)

2017 | 2016 | 2015 | ||||||||||||||||

Q2 | Q1 | Q4 | Q3 | Q2 | Q1 | Q4 | Q3 | |||||||||||

Contractual rent increases occurring in the quarter | ||||||||||||||||||

Multi-tenant properties | 3.0 | % | 2.9 | % | 2.9 | % | 2.8 | % | 2.9 | % | 2.9 | % | 3.0 | % | 2.9 | % | ||

Single-tenant net lease properties | 2.3 | % | 2.1 | % | 2.5 | % | 1.7 | % | 2.2 | % | 1.0 | % | 1.6 | % | 2.6 | % | ||

Total | 2.8 | % | 2.8 | % | 2.9 | % | 2.5 | % | 2.7 | % | 2.5 | % | 2.8 | % | 2.8 | % | ||

Multi-tenant renewals | ||||||||||||||||||

Cash leasing spreads | 9.5 | % | 4.5 | % | 3.9 | % | 4.3 | % | 6.3 | % | 7.2 | % | 3.7 | % | 2.1 | % | ||

Tenant retention rate | 90.3 | % | 79.2 | % | 88.5 | % | 90.1 | % | 81.2 | % | 87.2 | % | 91.2 | % | 82.4 | % | ||

As of 6/30/2017 | |||||

Multi-tenant | Single-tenant Net Lease | ||||

Leased Square Feet | 9,473,493 | 1,762,488 | |||

Contractual Rental Rate Increases by Type | |||||

Annual increase | |||||

CPI | 1.8 | % | 60.3 | % | |

Fixed | 84.8 | % | 22.8 | % | |

Non-annual increase | |||||

CPI | 2.1 | % | 3.3 | % | |

Fixed | 4.0 | % | 13.6 | % | |

No increase | |||||

Term < 1 year | 4.5 | % | — | % | |

Term > 1 year | 2.8 | % | — | % | |

Tenant Type | |||||

Hospital | 45.8 | % | 79.1 | % | |

Physician and other | 54.2 | % | 20.9 | % | |

Lease Structure | |||||

Gross | 15.1 | % | — | % | |

Modified gross | 28.7 | % | — | % | |

Net | 56.2 | % | 100.0 | % | |

Ownership Type | |||||

Ground lease | 62.5 | % | 10.3 | % | |

Fee simple | 37.5 | % | 89.7 | % | |

(1) | Excludes recently acquired or disposed properties, mortgage notes receivable, construction in progress, land held for development, corporate property, reposition properties and assets classified as held for sale. |

HEALTHCARE REALTY 19 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Same Store Properties

(dollars in thousands)

QUARTERLY (1) | ||||||||||||||||||||||||

Q2 2017 | Q1 2017 | Q4 2016 | Q3 2016 | Q2 2016 | Q1 2016 | Q4 2015 | Q3 2015 | |||||||||||||||||

Multi-tenant | ||||||||||||||||||||||||

Revenues | $77,662 | $76,288 | $75,579 | $76,265 | $75,155 | $74,125 | $73,648 | $72,636 | ||||||||||||||||

Expenses | 31,760 | 31,457 | 31,451 | 32,634 | 31,070 | 30,579 | 32,609 | 31,393 | ||||||||||||||||

NOI | $45,902 | $44,831 | $44,128 | $43,631 | $44,085 | $43,546 | $41,039 | $41,243 | ||||||||||||||||

Occupancy | 88.0 | % | 87.6 | % | 87.3 | % | 87.3 | % | 87.0 | % | 87.0 | % | 87.0 | % | 86.5 | % | ||||||||

Number of properties | 137 | 137 | 137 | 137 | 137 | 137 | 137 | 137 | ||||||||||||||||

Single-tenant net lease | ||||||||||||||||||||||||

Revenues | $12,613 | $13,001 | $12,655 | $12,924 | $12,802 | $12,836 | $12,837 | $12,782 | ||||||||||||||||

Expenses | 362 | 430 | 404 | 373 | 343 | 401 | 439 | 370 | ||||||||||||||||

NOI | $12,251 | $12,571 | $12,251 | $12,551 | $12,459 | $12,435 | $12,398 | $12,412 | ||||||||||||||||

Occupancy | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||

Number of properties | 24 | 24 | 24 | 24 | 24 | 24 | 24 | 24 | ||||||||||||||||

Total | ||||||||||||||||||||||||

Revenues | $90,275 | $89,289 | $88,234 | $89,189 | $87,957 | $86,961 | $86,485 | $85,418 | ||||||||||||||||

Expenses | 32,122 | 31,887 | 31,855 | 33,007 | 31,413 | 30,980 | 33,048 | 31,763 | ||||||||||||||||

Same Store NOI | $58,153 | $57,402 | $56,379 | $56,182 | $56,544 | $55,981 | $53,437 | $53,655 | ||||||||||||||||

Occupancy | 89.7 | % | 89.4 | % | 89.1 | % | 89.1 | % | 88.8 | % | 88.9 | % | 88.8 | % | 88.4 | % | ||||||||

Number of properties | 161 | 161 | 161 | 161 | 161 | 161 | 161 | 161 | ||||||||||||||||

% NOI year-over-year growth | 2.8 | % | 2.5 | % | 5.5 | % | 4.7 | % | ||||||||||||||||

TRAILING TWELVE MONTHS (1) | |||||||||

Twelve Months Ended June 30, | |||||||||

2017 | 2016 | % Change | |||||||

Multi-tenant | |||||||||

Revenues | $305,794 | $295,564 | 3.5 | % | |||||

Expenses | $127,302 | $125,651 | 1.3 | % | |||||

NOI | $178,492 | $169,913 | 5.0 | % | |||||

Revenue per average occupied square foot | $32.48 | $31.61 | 2.8 | % | |||||

Average occupancy | 87.5 | % | 86.9 | % | |||||

Number of properties | 137 | 137 | |||||||

Single-tenant net lease | |||||||||

Revenues | $51,193 | $51,257 | (0.1 | %) | |||||

Expenses | $1,569 | $1,553 | 1.0 | % | |||||

NOI | $49,624 | $49,704 | (0.2 | %) | |||||

Revenue per average occupied square foot | $29.05 | $29.09 | (0.1 | %) | |||||

Average occupancy | 100.0 | % | 100.0 | % | |||||

Number of properties | 24 | 24 | |||||||

Total | |||||||||

Revenues | $356,987 | $346,821 | 2.9 | % | |||||

Expenses | $128,871 | $127,204 | 1.3 | % | |||||

Same Store NOI | $228,116 | $219,617 | 3.9 | % | |||||

Revenue per average occupied square foot | $31.94 | $31.21 | 2.3 | % | |||||

Average occupancy | 89.2 | % | 88.7 | % | |||||

Number of Properties | 161 | 161 | |||||||

(1) | Excludes recently acquired or disposed properties, mortgage notes receivable, development completions, construction in progress, land held for development, corporate property, reposition properties and assets classified as held for sale. |

HEALTHCARE REALTY 20 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Reconciliation of NOI

(dollars in thousands)

BOTTOM UP RECONCILIATION | ||||||||||||||||||||||||||||||||

Q2 2017 | Q1 2017 | Q4 2016 | Q3 2016 | Q2 2016 | Q1 2016 | Q4 2015 | Q3 2015 | |||||||||||||||||||||||||

Net income | $25,224 | $31,845 | $52,437 | $11,834 | $12,145 | $9,156 | $18,658 | $27,480 | ||||||||||||||||||||||||

Loss (income) from discontinued operations | — | 13 | 143 | 23 | 12 | 7 | 696 | (10,632 | ) | |||||||||||||||||||||||

Income from continuing operations | 25,224 | 31,858 | 52,580 | 11,857 | 12,157 | 9,163 | 19,354 | 16,848 | ||||||||||||||||||||||||

Other income (expense) | (1,881 | ) | (8,921 | ) | (27,272 | ) | 13,636 | 14,725 | 14,852 | 5,670 | 9,436 | |||||||||||||||||||||

General and administrative expense | 8,005 | 8,694 | 7,622 | 7,859 | 7,756 | 8,072 | 5,975 | 5,852 | ||||||||||||||||||||||||

Depreciation and amortization expense | 34,823 | 34,452 | 34,022 | 31,985 | 31,290 | 30,393 | 29,575 | 28,957 | ||||||||||||||||||||||||

Other expenses (1) | 2,204 | 1,979 | 2,431 | 1,488 | 1,696 | 3,351 | 2,375 | 1,503 | ||||||||||||||||||||||||

Straight-line rent revenue | (1,783 | ) | (1,751 | ) | (1,754 | ) | (1,223 | ) | (2,091 | ) | (2,132 | ) | (1,929 | ) | (2,309 | ) | ||||||||||||||||

Other revenue (2) | (1,211 | ) | (794 | ) | (1,228 | ) | (1,422 | ) | (1,465 | ) | (1,417 | ) | (1,432 | ) | (1,413 | ) | ||||||||||||||||

NOI | $65,381 | $65,517 | $66,401 | $64,180 | $64,068 | $62,282 | $59,588 | $58,874 | ||||||||||||||||||||||||

Acquisitions / Development completions | (5,996 | ) | (5,389 | ) | (5,406 | ) | (3,100 | ) | (2,672 | ) | (1,513 | ) | (1,142 | ) | (147 | ) | ||||||||||||||||

Reposition | (712 | ) | (687 | ) | (570 | ) | (360 | ) | (274 | ) | (238 | ) | (393 | ) | (278 | ) | ||||||||||||||||

Dispositions / other | (520 | ) | (2,039 | ) | (4,046 | ) | (4,538 | ) | (4,578 | ) | (4,550 | ) | (4,616 | ) | (4,794 | ) | ||||||||||||||||

Same store NOI | $58,153 | $57,402 | $56,379 | $56,182 | $56,544 | $55,981 | $53,437 | $53,655 | ||||||||||||||||||||||||

TOP DOWN RECONCILIATION | ||||||||||||||||||||||||||||||||

Q2 2017 | Q1 2017 | Q4 2016 | Q3 2016 | Q2 2016 | Q1 2016 | Q4 2015 | Q3 2015 | |||||||||||||||||||||||||

Property operating | $90,360 | $88,067 | $87,362 | $85,264 | $83,283 | $80,501 | $79,466 | $76,960 | ||||||||||||||||||||||||

Single-tenant net lease | 12,726 | 14,270 | 15,620 | 16,047 | 16,098 | 16,107 | 16,071 | 16,114 | ||||||||||||||||||||||||

Straight-line rent revenue | 1,783 | 1,751 | 1,754 | 1,223 | 2,091 | 2,132 | 1,929 | 2,309 | ||||||||||||||||||||||||

Rental income | 104,869 | 104,088 | 104,736 | 102,534 | 101,472 | 98,740 | 97,466 | 95,383 | ||||||||||||||||||||||||

Property lease guaranty income | 153 | 225 | 354 | 817 | 885 | 1,002 | 851 | 999 | ||||||||||||||||||||||||

Exclude straight-line rent revenue | (1,783 | ) | (1,751 | ) | (1,754 | ) | (1,223 | ) | (2,091 | ) | (2,132 | ) | (1,929 | ) | (2,309 | ) | ||||||||||||||||

Exclude other revenue (3) | (988 | ) | (538 | ) | (1,009 | ) | (1,114 | ) | (1,180 | ) | (1,138 | ) | (1,167 | ) | (1,070 | ) | ||||||||||||||||

Revenue | 102,251 | 102,024 | 102,327 | 101,014 | 99,086 | 96,472 | 95,221 | 93,003 | ||||||||||||||||||||||||

Property operating expense | (38,184 | ) | (37,834 | ) | (37,285 | ) | (37,504 | ) | (36,263 | ) | (35,406 | ) | (36,758 | ) | (35,247 | ) | ||||||||||||||||

Exclude other expenses (4) | 1,314 | 1,327 | 1,359 | 670 | 1,245 | 1,216 | 1,125 | 1,118 | ||||||||||||||||||||||||

NOI | $65,381 | $65,517 | $66,401 | $64,180 | $64,068 | $62,282 | $59,588 | $58,874 | ||||||||||||||||||||||||

Acquisitions / Development completions | (5,996 | ) | (5,389 | ) | (5,406 | ) | (3,100 | ) | (2,672 | ) | (1,513 | ) | (1,142 | ) | (147 | ) | ||||||||||||||||

Reposition | (712 | ) | (687 | ) | (570 | ) | (360 | ) | (274 | ) | (238 | ) | (393 | ) | (278 | ) | ||||||||||||||||

Dispositions / other | (520 | ) | (2,039 | ) | (4,046 | ) | (4,538 | ) | (4,578 | ) | (4,550 | ) | (4,616 | ) | (4,794 | ) | ||||||||||||||||

Same store NOI | $58,153 | $57,402 | $56,379 | $56,182 | $56,544 | $55,981 | $53,437 | $53,655 | ||||||||||||||||||||||||

TRAILING TWELVE MONTHS NOI | |||||||||||

Twelve Months Ended June 30, | |||||||||||

2017 | 2016 | % Change | |||||||||

Same store NOI | $228,116 | $219,617 | 3.9 | % | |||||||

Reposition | 2,329 | 1,183 | 96.9 | % | |||||||

Subtotal | $230,445 | $220,800 | 4.4 | % | |||||||

Acquisitions / Development completions | 19,891 | 5,474 | 263.4 | % | |||||||

Dispositions / other | 11,143 | 18,538 | (39.9 | %) | |||||||

NOI | $261,479 | $244,812 | 6.8 | % | |||||||

(1) | Includes acquisition and development expense, bad debt, above and below market ground lease intangible amortization, leasing commission amortization, and ground lease straight-line rent. |

(2) | Includes interest and other income, mortgage interest income, above and below market lease intangibles, lease inducements, lease terminations and TI amortization. |

(3) | Includes above and below market lease intangibles, lease inducements, lease terminations and TI amortization. |

(4) | Includes above and below market ground lease intangible amortization, leasing commission amortization, and ground lease straight-line rent. |

HEALTHCARE REALTY 21 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Reconciliation of EBITDA

(dollars in thousands)

EBITDA | ||||||||||||||||||||

Q2 2017 | Q1 2017 | Q4 2016 | Q3 2016 | Trailing Twelve Months | ||||||||||||||||

Net income | $25,224 | $31,845 | $52,437 | $11,834 | $121,340 | |||||||||||||||

Interest expense | 14,315 | 14,272 | 13,839 | 13,759 | 56,185 | |||||||||||||||

Depreciation and amortization | 34,823 | 34,452 | 34,022 | 31,985 | 135,282 | |||||||||||||||

EBITDA | $74,362 | $80,569 | $100,298 | $57,578 | $312,807 | |||||||||||||||

Acquisition and development expense | 785 | 586 | 1,085 | 865 | 3,321 | |||||||||||||||

Gain on sales of real estate properties | (16,124 | ) | (23,408 | ) | (41,037 | ) | — | (80,569 | ) | |||||||||||

Impairments on real estate assets | 5 | 323 | 121 | — | 449 | |||||||||||||||

Debt Covenant EBITDA | $59,028 | $58,070 | $60,467 | $58,443 | $236,008 | |||||||||||||||

Timing impact of acquisitions and dispositions (1) | (90 | ) | (1,260 | ) | (901 | ) | 1,283 | (968 | ) | |||||||||||

Stock based compensation | 2,453 | 2,614 | 1,949 | 1,851 | 8,867 | |||||||||||||||

Adjusted EBITDA | $61,391 | $59,424 | $61,515 | $61,577 | $243,907 | |||||||||||||||

(1) | Adjusted to reflect quarterly EBITDA from properties acquired or disposed in the quarter. |

HEALTHCARE REALTY 22 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Components of Net Asset Value

(dollars in thousands)

Q2 2017 | |||||||||||||||||||||||||||

Asset Type | Same Store NOI(1) | Acquisitions/Development Completions NOI (2) | Reposition NOI(3) | Timing Adjustments(4) | Adjusted NOI | Annualized Adjusted NOI | % of Adjusted NOI | ||||||||||||||||||||

MOB / Outpatient | $50,502 | $5,996 | $719 | $1,278 | $58,495 | $233,980 | 88.2 | % | |||||||||||||||||||

Inpatient rehab | 1,422 | — | — | — | 1,422 | 5,688 | 2.1 | % | |||||||||||||||||||

Inpatient surgical | 4,490 | — | — | — | 4,490 | 17,960 | 6.8 | % | |||||||||||||||||||

Other | 1,739 | 106 | 84 | — | 1,929 | 7,716 | 2.9 | % | |||||||||||||||||||

Total NOI | $58,153 | $6,102 | $803 | $1,278 | $66,336 | $265,344 | 100.0 | % | |||||||||||||||||||

TOTAL SHARES OUTSTANDING (AS OF JULY 31, 2017) 116,545,032

DEVELOPMENT PROPERTIES | ||||

Land held for development | $20,123 | |||

Unstabilized development (5) | 21,614 | |||

Subtotal | $41,737 | |||

OTHER ASSETS | ||||

Assets held for sale(6) | $8,699 | |||

Reposition properties (net book value)(3) | 3,702 | |||

Cash and other assets(7) | 71,694 | |||

Subtotal | $84,095 | |||

DEBT | ||||

Unsecured credit facility | $35,000 | |||

Unsecured term loan | 150,000 | |||

Senior notes | 900,000 | |||

Mortgage notes payable | 124,758 | |||

Other liabilities(8) | 70,791 | |||

Subtotal | $1,280,549 | |||

(1) | See Same Store Properties schedule on page 20 for details on same store NOI. |

(2) | Adjusted to reflect quarterly NOI from properties acquired or developments completed during the full eight quarter period that are not included in same store NOI. |

(3) | Reposition properties includes 15 properties which comprise 714,500 square feet. The NOI table above includes 12 of these properties comprising 563,265 square feet that have generated positive NOI totaling approximately $0.8 million. The remaining 3 properties, comprising 151,235 square feet, have generated negative NOI of approximately $0.1 million and are reflected at a net book value of $3.7 million in the table above. |

(4) | Timing adjustments related to current quarter acquisitions and the difference between leased and occupied square feet on previous re/developments. |

(5) | Unstabilized development includes one property that was completed on June 30, 2017 and tenants have not yet begun taking occupancy. |

(6) | Assets held for sale includes one real estate property that is excluded from same store NOI and reflects net book value or the contractual purchase price, if applicable. |

(7) | Includes cash of $2.0 million, restricted cash of $9.2 million, and prepaid assets of $60.5 million that are expected to generate future cash or NOI and assets that are currently causing non-cash reductions to NOI. |

(8) | Includes only liabilities that are expected to reduce future cash or NOI and that are currently producing non-cash benefits to NOI. Included are accounts payable and accrued liabilities of $62.3 million, security deposits of $6.4 million and deferred operating expense reimbursements of $2.1 million. Also, excludes deferred revenue of $34.8 million. |

HEALTHCARE REALTY 23 | 2Q 2017 SUPPLEMENTAL INFORMATION | |

Components of Expected 2017 FFO

(dollars in thousands, except per square foot data)

SAME STORE QUARTERLY RANGE OF EXPECTATIONS | ||||||||

Low | High | |||||||

Occupancy | ||||||||

Multi-Tenant | 87.5 | % | 89.0 | % | ||||

Single-Tenant Net Lease | 95.0 | % | 100.0 | % | ||||

TTM Revenue per Occupied Square Foot (1) | ||||||||

Multi-Tenant | $31.00 | $33.00 | ||||||

Single-Tenant Net Lease | $28.50 | $29.50 | ||||||

Multi-Tenant TTM NOI Margin (1) | 57.0 | % | 59.0 | % | ||||

Multi-Tenant Contractual Rent Increases by Type (% of SF) | ||||||||

Annual Increase | 80.0 | % | 90.0 | % | ||||

Non-annual Increase | 5.0 | % | 7.0 | % | ||||

No Increase (term < 1 year) | 4.0 | % | 6.0 | % | ||||

No Increase (term > 1 year) | 2.0 | % | 4.0 | % | ||||

Contractual Increases Occurring in the Quarter | ||||||||

Multi-Tenant | 2.8 | % | 3.0 | % | ||||

Single-Tenant Net Lease | 1.0 | % | 3.0 | % | ||||

Multi-Tenant Cash Leasing Spreads | 3.0 | % | 6.0 | % | ||||

Multi-Tenant Lease Retention Rate | 75.0 | % | 90.0 | % | ||||

TTM NOI Growth (1) | ||||||||

Multi-Tenant (2) | 4.5 | % | 6.0 | % | ||||

Single-Tenant Net Lease | (0.5 | %) | 1.0 | % | ||||

ANNUAL RANGE OF EXPECTATIONS | ||||||||

Low | High | |||||||

Normalized G&A (3) | $33,000 | $35,000 | ||||||

Funding Activity | ||||||||

Acquisitions | $175,000 | $225,000 | ||||||

Dispositions | (120,000) | (125,000) | ||||||

Re/Development | 25,000 | 40,000 | ||||||

1st Generation TI and Planned Capital Expenditures for Acquisitions | 9,000 | 12,000 | ||||||

2nd Generation Tenant Improvements | 20,000 | 25,000 | ||||||

Leasing Commissions | 4,000 | 7,000 | ||||||

Capital Expenditures | 11,000 | 22,000 | ||||||

Cash Yield | ||||||||

Acquisitions | 5.25 | % | 6.00 | % | ||||

Dispositions | 7.00 | % | 7.25 | % | ||||

Re/development (stabilized) | 6.75 | % | 8.00 | % | ||||

Leverage (Debt/Cap) | 32.0 | % | 35.0 | % | ||||

Net Debt to Adjusted EBITDA | 5.0x | 5.5x | ||||||

(1) | TTM = Trailing Twelve Months |

(2) | Long-term same store NOI Growth, excluding changes in occupancy, is expected to range between 2% and 4%. |

(3) | Normalized G&A excludes acquisition expenses and includes amortization of non-cash share-based compensation awards of $8.5 million inclusive of $4.3 million related to 2016 performance and transition awards. |

HEALTHCARE REALTY 24 | 2Q 2017 SUPPLEMENTAL INFORMATION | |