Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - CINTAS CORP | ctas10k2017ex322.htm |

| EX-32.1 - EXHIBIT 32.1 - CINTAS CORP | ctas10k2017ex321.htm |

| EX-31.2 - EXHIBIT 31.2 - CINTAS CORP | ctas10k2017ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - CINTAS CORP | ctas10k2017ex311.htm |

| EX-23 - EXHIBIT 23 - CINTAS CORP | a23-consentofey2017.htm |

| EX-21 - EXHIBIT 21 - CINTAS CORP | a21-subsidiaries2017.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

X | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended May 31, 2017 | |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission File No. 0-11399 | |

CINTAS CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

WASHINGTON | 31-1188630 | |||

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |||

6800 Cintas Boulevard P.O. Box 625737 Cincinnati, Ohio 45262-5737 (Address of Principal Executive Offices) | ||||

(513) 459-1200 (Registrant's telephone number, including area code) | ||||

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock, no par value | The NASDAQ Stock Market LLC (NASDAQ Global Select Market) |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

YES | ü | NO | |||||

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

YES | NO | ü | |||||

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

YES | ü | NO | |||||

Indicate by a check mark whether the Registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files).

YES | ü | NO | |||||

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of the Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to the Form 10-K.

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company", and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer | ü | Accelerated Filer | Non-Accelerated Filer | (Do not check if a smaller reporting company.) | ||

Smaller Reporting Company | Emerging Growth Company | |||||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

YES | NO | ü | |||||

The aggregate market value of the Registrant's Common Stock held by non-affiliates as of November 30, 2016, was $12,034,116,433 based on a closing sale price of $114.60 per share. As of June 30, 2017, 181,027,841 shares of the Registrant's Common Stock were issued and 105,435,865 shares were outstanding.

Documents Incorporated by Reference

Portions of the Registrant's Proxy Statement to be filed with the Commission for its 2017 Annual Meeting of Shareholders are incorporated by reference in Part III of this Form 10-K.

1

Cintas Corporation

Index to Annual Report on Form 10-K

Page | ||

2

Part I

Item 1. Business

Cintas Corporation (Cintas, Company, we, us or our), a Washington corporation, helps more than one million businesses of all types and sizes, primarily in North America, as well as Latin America, Europe and Asia, get Ready™ to open their doors with confidence every day by providing a wide range of products and services that enhance our customers’ image and help keep their facilities and employees clean, safe and looking their best. With products and services including uniforms, floor care, restroom supplies, first aid and safety products, fire extinguishers and testing, and safety and compliance training, Cintas helps customers get Ready for the Workday™. Cintas was founded in 1968 by Richard T. Farmer, currently the Chairman Emeritus of the Board of Directors, when he left his family's industrial laundry business in order to develop uniform programs using an exclusive new fabric. In the early 1970's, Cintas acquired the family industrial laundry business. Over the years, Cintas developed additional products and services that complemented its core uniform business and broadened the scope of products and services available to its customers.

On March 21, 2017, Cintas completed the acquisition of G&K Services, Inc. (G&K) for consideration of approximately $2.1 billion. G&K is now a wholly-owned subsidiary of Cintas that will operate within the Uniform Rental and Facility Services operating segment. To finance the G&K acquisition, Cintas used a combination of new senior notes, a term loan, other borrowings under its existing credit facility and cash on hand. G&K's results of operations are included in Cintas' consolidated financial statements as of and from the date of acquisition.

U.S. Generally Accepted Accounting Principles (U. S. GAAP) requires companies to evaluate their reportable operating segments periodically and when certain events occur. As a result of our evaluation in fiscal 2016, effective June 1, 2015, Cintas realigned its organizational structure and updated its reportable operating segments in light of certain changes in its business including the acquisition of ZEE Medical Inc. (ZEE) in the first quarter of fiscal 2016. Cintas’ updated reportable operating segments are Uniform Rental and Facility Services and First Aid and Safety Services. The Uniform Rental and Facility Services reportable operating segment, which includes G&K, consists of the rental and servicing of uniforms and other garments including flame resistant clothing, mats, mops and shop towels and other ancillary items. In addition to these rental items, restroom cleaning services and supplies, carpet and tile cleaning services and the sale of items from our catalogs to our customers on route are included within this reportable operating segment. The First Aid and Safety Services reportable operating segment, which includes ZEE, consists of first aid and safety products and services. The remainder of Cintas’ business, which consists of Fire Protection Services and its Uniform Direct Sale business, is included in All Other.

At May 31, 2017, Cintas has classified a significant business, referred to as "Discontinued Services", as held for sale. Prior to meeting the held for sale criteria, Discontinued Services was primarily included in All Other. In fiscal 2014, Cintas completed its partnership transaction with the shareholders of Shred-it International Inc. to combine Cintas' shredding business (Shredding) with the shredding business of Shred-it International Inc. (the Shredding Transaction). Pursuant to the Shredding Transaction, the newly formed partnership (the Shred-it Partnership) was owned 42% by Cintas and 58% by the shareholders of Shred-it International Inc. Cintas' investment in the Shred-it Partnership (Shred-it) and the results of Shredding are classified as discontinued operations for all periods presented as a result of selling the investment during fiscal 2016. During fiscal 2015, Cintas sold the storage business (Storage) and, as a result, its operations are also classified as discontinued operations for all periods presented. In accordance with the applicable accounting guidance for the disposal of long-lived assets and discontinued operations, the results of Discontinued Services, Shredding and Storage have been excluded from both continuing operations and operating segment results for all periods presented. Please see Note 16 entitled Discontinued Operations of "Notes to Consolidated Financial Statements" for additional information.

We provide our products and services to over one million businesses of all types, from small service and manufacturing companies to major corporations that employ thousands of people. This diversity in customer base results in no individual customer accounting for greater than one percent of Cintas' total revenue. As a result, the loss of one account would not have a significant financial impact on Cintas.

3

The following table sets forth Cintas' total revenue and the revenue derived from each reportable operating segment and All Other:

Fiscal Year Ended May 31, (in thousands) | 2017 | 2016(1) | 2015(1) | ||||||||

Uniform Rental and Facility Services | $ | 4,202,490 | $ | 3,759,524 | $ | 3,519,199 | |||||

First Aid and Safety Services | 508,233 | 461,783 | 326,593 | ||||||||

All Other | 612,658 | 574,465 | 523,885 | ||||||||

Total Revenue | $ | 5,323,381 | $ | 4,795,772 | $ | 4,369,677 | |||||

(1) | The figures for fiscal 2016 and 2015 reflect the change in classification of Discontinued Services, Shredding and Storage to discontinued operations within the Consolidated Statements of Income. See Note 16 entitled Discontinued Operations of "Notes to Consolidated Financial Statements." |

Additional information regarding each reportable operating segment and All Other is also included in Note 14 entitled Operating Segment Information of "Notes to Consolidated Financial Statements."

The primary markets served by all Cintas businesses are local in nature and highly fragmented. Cintas competes with national, regional and local providers, and the level of competition varies at each of Cintas' local operations. Product, design, price, quality, service and convenience to the customer are the competitive elements in each of our businesses.

Within the Uniform Rental and Facility Services reportable operating segment, Cintas provides its products and services to customers via local delivery routes originating from rental processing plants and branches. Within the First Aid and Safety Services reportable operating segment and All Other, Cintas provides its products and services via its distribution network and local delivery routes or local representatives. In total, Cintas has approximately 11,000 local delivery routes, 528 operational facilities and 11 distribution centers. At May 31, 2017, Cintas employed approximately 42,000 employees, of which approximately 1,700 were represented by labor unions.

Cintas sources finished products from many outside suppliers. In addition, Cintas operates six manufacturing facilities that provide for standard uniform needs. Cintas purchases fabric, used in its manufacturing process, from several suppliers. Cintas is not aware of any circumstances that would hinder its ability to continue obtaining these materials.

Cintas is subject to various environmental laws and regulations, as are other companies in the uniform rental industry. While environmental compliance is not a material component of its costs, Cintas must incur capital expenditures and associated operating costs, primarily for water treatment and waste removal, on a regular basis. Environmental spending related to water treatment and waste removal was approximately $14 million in fiscal 2017 and approximately $13 million in fiscal 2016. Capital expenditures to limit or monitor hazardous substances totaled approximately $3 million in both fiscal 2017 and fiscal 2016. Cintas does not expect a material change in the cost of environmental compliance and is not aware of any material non-compliance with environmental laws.

Cintas uses its corporate website, www.cintas.com, as a channel for routine distribution of important information, including news releases, analyst presentations and financial information. Cintas files with or furnishes to the SEC Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports, as well as proxy statements and annual reports to shareholders, and, from time to time, other documents. The reports and other documents filed with or furnished to the SEC are available to investors on or through our corporate website free of charge as soon as reasonably practicable after we electronically file them with or furnish them to the SEC. In addition, the public may read and copy any of the materials we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington D.C. 20549. The public may obtain information on the operation of the facilities by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet site located at www.sec.gov that contains reports, proxy and information statements and other information regarding issuers, such as Cintas, that file electronically with the SEC. Cintas' SEC filings can be found on the Investors page of its website at www.cintas-corp.com/company/investor_information/highlights.aspx and its Code of Conduct and Business Ethics can be found on the About Us page of its website at www.cintas-corp.com/company. These documents are available in print to any shareholder who requests a copy by writing or calling Cintas as set forth on the Investor Information page. The content on any website referred to in this Annual Report on Form 10-K is not incorporated by reference into this Form 10-K unless expressly noted.

4

Item 1A. Risk Factors

The statements in this section describe the most significant risks that could materially and adversely affect our business, consolidated financial condition and consolidated results of operation and the trading price of our debt or equity securities.

In addition, this section sets forth statements which constitute our cautionary statements under the Private Securities Litigation Reform Act of 1995.

This Annual Report on Form 10-K contains forward-looking statements. The Private Securities Litigation Reform Act of 1995 provides a safe harbor from civil litigation for forward-looking statements. Forward-looking statements may be identified by words such as “estimates,” “anticipates,” “predicts,” “projects,” “plans,” “expects,” “intends,” “target,” “forecast,” “believes,” “seeks,” “could,” “should,” “may” and “will” or the negative versions thereof and similar words, terms and expressions and by the context in which they are used. Such statements are based upon current expectations of Cintas and speak only as of the date made. You should not place undue reliance on any forward-looking statement. We cannot guarantee that any forward-looking statement will be realized. These statements are subject to various risks, uncertainties, potentially inaccurate assumptions and other factors that could cause actual results to differ from those set forth in or implied by this Annual Report. Factors that might cause such a difference include, but are not limited to, risks inherent with the G&K transaction in the achievement of cost synergies and the timing thereof, including whether the G&K transaction will be accretive and within the expected timeframe; the possibility of greater than anticipated operating costs including energy and fuel costs; lower sales volumes; loss of customers due to outsourcing trends; the performance and costs of integration of acquisitions, including G&K; fluctuations in costs of materials and labor including increased medical costs; costs and possible effects of union organizing activities; failure to comply with government regulations concerning employment discrimination, employee pay and benefits and employee health and safety; the effect on operations of exchange rate fluctuations, tariffs and other political, economic and regulatory risks; uncertainties regarding any existing or newly-discovered expenses and liabilities related to environmental compliance and remediation; the cost, results and ongoing assessment of internal controls for financial reporting required by the Sarbanes-Oxley Act of 2002; costs of our SAP system implementation; disruptions caused by the inaccessibility of computer systems data, including cybersecurity risks; the initiation or outcome of litigation, investigations or other proceedings; higher assumed sourcing or distribution costs of products; the disruption of operations from catastrophic or extraordinary events; the amount and timing of repurchases of our common stock, if any; changes in federal and state tax and labor laws; and the reactions of competitors in terms of price and service. Cintas undertakes no obligation to publicly release any revisions to any forward-looking statements or to otherwise update any forward-looking statements whether as a result of new information or to reflect events, circumstances or any other unanticipated developments arising after the date on which such statements are made, except otherwise as required by law. The risks and uncertainties described herein are not the only ones we may face. Additional risks and uncertainties presently not known to us or that we currently believe to be immaterial may also harm our business.

Negative global economic factors may adversely affect our financial performance.

Negative economic conditions, in North America and our other markets, may adversely affect our financial performance. Higher levels of unemployment, inflation, tax rates and other changes in tax laws and other economic factors could adversely affect the demand for Cintas’ products and services. Increases in labor costs, including the cost to provide employee-partner related healthcare benefits, minimum wages, labor shortages or shortages of skilled labor, regulations regarding the classification of employees and/or their eligibility for overtime wages, higher material costs for items such as fabrics and textiles, the inability to obtain insurance coverage at cost-effective rates, higher interest rates, inflation, higher tax rates and other changes in tax laws and other economic factors could increase our costs of rental uniforms and facility services, cost of other services and selling and administrative expenses. As a result, these factors could adversely affect our sales and consolidated results of operations.

Increased competition could adversely affect our financial performance.

We operate in highly competitive industries and compete with national, regional and local providers. Product, design, price, quality, service and convenience to the customer are the competitive elements in these industries. If existing or future competitors seek to gain or retain market share by reducing prices, Cintas may be required to lower prices, which would hurt its results of operations. Cintas' competitors also generally compete with Cintas for acquisition candidates, which can increase the price for acquisitions and reduce the number of available acquisition candidates. In addition, our customers and prospects may decide to perform certain services in-house instead of outsourcing these services to us. These competitive pressures could adversely affect our sales and consolidated results of operations.

5

An inability to open new, cost effective operating facilities may adversely affect our expansion efforts.

We plan to expand our presence in existing markets and enter new markets. The opening of new operating facilities is necessary to gain the capacity required for this expansion. Our ability to open new operating facilities depends on our ability to identify attractive locations, negotiate leases or real estate purchase agreements on acceptable terms, identify and obtain adequate utility and water sources and comply with environmental regulations, zoning laws and other similar factors. Any inability to effectively identify and manage these items may adversely affect our expansion efforts, and, consequently, adversely affect our financial performance.

Risks associated with our acquisition practice could adversely affect our results of operations.

Historically, a portion of our growth has come from acquisitions. We continue to evaluate opportunities for acquiring businesses that may supplement our internal growth. However, there can be no assurance that we will be able to locate and purchase suitable acquisitions. In addition, the success of any acquisition, including the ability to realize anticipated cost synergies, depends in part on our ability to integrate the acquired company. The process of integrating acquired businesses, including G&K and ZEE, may involve unforeseen difficulties and may require a disproportionate amount of our management's attention and our financial and other resources. If management is not able to effectively manage the integration process, or if any significant business activities are interrupted as a result of the integration process, we may not be able to realize anticipated cost synergies resulting from acquisitions and our business could suffer. Although we conduct due diligence investigations prior to each acquisition, there can be no assurance that we will discover or adequately protect against all material liabilities of an acquired business for which we may be responsible as a successor owner or operator. The failure to identify suitable acquisitions and successfully integrate these acquired businesses, or to discover liabilities associated with such businesses in the diligence process, could adversely affect our consolidated results of operations.

Our indebtedness may limit cash flow available to invest in the ongoing needs of our business.

Our outstanding indebtedness, including indebtedness incurred to consummate the G&K transaction, may have negative consequences on our business, such as requiring us to dedicate a substantial portion of our cash flow from operations to the payment of debt service, reducing the availability of our cash flow to fund working capital, capital expenditures, acquisitions, dividend increases, stock buybacks and other general corporate purposes, as well as increase our vulnerability to adverse economic or industry conditions. In addition, it may limit our ability to obtain additional financing in the future to enable us to react to changes in our business or industry or place us at a competitive disadvantage compared to businesses in our industry that have less debt.

Changes in the fuel and energy industry could adversely affect our financial condition and results of operations.

The price of fuel and energy needed to run our vehicles and equipment is unpredictable and fluctuates based on events outside our control, including geopolitical developments, supply and demand for fuel and other energy related products, actions by energy producers, war and unrest in oil producing countries, regional production patterns, limits on refining capacities, natural disasters and environmental concerns. Increases in fuel and energy costs could adversely affect our consolidated financial condition and consolidated results of operations.

Failure to preserve positive labor relationships with our employees could adversely affect our consolidated results of operations.

Following the G&K transaction, more of our labor force is unionized. While we believe that our employee relations are good, we have been and could continue to be the target of a unionization campaign by several unions. These unions have attempted to pressure Cintas into surrendering its employees' rights to a government-supervised election by unilaterally accepting union representation. We will continue to vigorously oppose any unionization campaign and defend our employees' rights to a government-supervised election. Unionization campaigns could be materially disruptive to our business and could adversely affect our consolidated results of operations.

Risks associated with the suppliers from whom our products are sourced could adversely affect our results of operations.

The products we sell are sourced from a wide variety of domestic and international suppliers. Global sourcing of many of the products we sell is an important factor in our financial performance. We require all of our suppliers to comply with applicable laws, including labor and environmental laws, and otherwise be certified as meeting our required supplier standards of conduct. Our ability to find qualified suppliers who meet our standards, and to access products in a timely and efficient manner is a significant challenge, especially with respect to suppliers located and goods sourced outside the United States. Political and economic stability in the countries in which foreign suppliers are located, the financial stability of suppliers, suppliers' failure to meet our supplier standards, labor problems experienced by our suppliers, the availability of raw materials to suppliers, currency exchange rates, transport availability and cost,

6

inflation and other factors relating to the suppliers and the countries in which they are located are beyond our control. In addition, U.S. and foreign trade policies, tariffs and other impositions on imported goods, trade sanctions imposed on certain countries, the limitation on the importation of certain types of goods or of goods containing certain materials from other countries and other factors relating to foreign trade are beyond our control. These and other factors affecting our suppliers and our access to products could adversely affect our consolidated results of operations.

Fluctuations in foreign currency exchange could adversely affect our financial condition and results of operations.

We earn revenue, pay expenses, own assets and incur liabilities in countries using currencies other than the U.S. dollar, including the Canadian dollar, British pound, and the euro. In fiscal years 2017, 2016 and 2015, revenue denominated in currencies other than the U.S. dollar represented less than 10% of our consolidated revenue. Because our consolidated financial statements are presented in U.S. dollars, we must translate revenue, income and expenses, as well as assets and liabilities, into U.S. dollars at exchange rates in effect during or at the end of each reporting period. Therefore, fluctuations in the value of the U.S. dollar against other major currencies, particularly in the event of significant increases in foreign currency revenue, will impact our revenue and operating income and the value of balance sheet items denominated in foreign currencies. This impact could adversely affect our consolidated financial condition and consolidated results of operations.

Failure to comply with federal and state regulations to which we are subject could result in penalties or costs that could adversely affect our results of operations.

Our business is subject to complex and stringent state and federal regulations, including employment laws and regulations, minimum wage requirements, overtime requirements, working condition requirements, citizenship requirements, transportation and other laws and regulations. In particular, we are subject to the regulations promulgated by the U.S. Department of Transportation, or USDOT, and under the Occupational Safety and Health Act of 1970, as amended, or OSHA. We have incurred, and will continue to incur, capital and operating expenditures and other costs in the ordinary course of our business in complying with the USDOT, OSHA and other laws and regulations to which we are subject. Changes in laws, regulations and the related interpretations, including any laws or regulations that may be enacted by the current U.S. presidential administration and Congress, may alter the landscape in which we do business and may affect our costs of doing business. The impact of new laws and regulations cannot be predicted. Compliance with new laws and regulations may increase our operating costs or require significant capital expenditures. Any failure to comply with applicable laws or regulations could result in substantial fines by government authorities, payment of damages to private litigants, or possible revocation of our authority to conduct our operations, which could adversely affect our ability to service customers and our consolidated results of operations.

We are subject to legal proceedings that may adversely affect our financial condition and results of operations.

We are subject to various litigation claims and legal proceeding arising from the ordinary course of our business, including personal injury, customer contract, environmental and employment claims. Certain of these lawsuits or potential future lawsuits, if decided adversely to us or settled by us, may result in liability and expense material to our consolidated financial condition and consolidated results of operations.

Compliance with environmental laws and regulations could result in significant costs that adversely affect our results of operations.

Our operating locations are subject to environmental laws and regulations relating to the protection of the environment and health and safety matters, including those governing discharges of pollutants to the air and water, the management and disposal of hazardous substances and wastes and the clean-up of contaminated sites. The operation of our businesses entails risks under environmental laws and regulations. We could incur significant costs, including clean-up costs, fines and sanctions and claims by third parties for property damage and personal injury, as a result of violations of or liabilities under these laws and regulations. We are currently involved in a limited number of remedial investigations and actions at various locations. While based on information currently known to us, we believe that we maintain adequate reserves with respect to these matters, our liability could exceed forecasted amounts, and the imposition of additional clean-up obligations or the discovery of additional contamination at these or other sites could result in significant additional costs which could adversely affect our results of operations. In addition, potentially significant expenditures could be required to comply with environmental laws and regulations, including requirements that may be adopted or imposed in the future.

7

Under applicable environmental laws, an owner or operator of real estate may be required to pay the costs of removing or remediating hazardous materials located on or emanating from property, whether or not the owner or operator knew of or was responsible for the presence of such hazardous materials. While we regularly engage in environmental due diligence in connection with acquisitions, we can give no assurance that locations that have been acquired or leased have been operated in compliance with environmental laws and regulations during prior periods or that future uses or conditions will not make us liable under these laws or expose us to third-party actions, including tort suits.

We rely extensively on computer systems to process transactions, maintain information and manage our businesses. Disruptions in the availability of computer systems due to implementation of a new system or otherwise, or privacy breaches involving computer systems, could impact our ability to service our customers and adversely affect our sales, results of operations and reputation and expose us to litigation risk.

Our businesses rely on our computer systems to provide customer information, process customer transactions and provide other general information necessary to manage our businesses. We have an active disaster recovery plan in place that is frequently reviewed and tested. However, our computer systems, including the systems inherited from G&K, are subject to damage or interruption due to system conversions, such as our current conversion to SAP enterprise system, power outages, computer or telecommunication failures, catastrophic events such as fires, tornadoes and hurricanes and usage errors by our employees. Although we believe that we have adopted appropriate measures to mitigate potential risks to our technology and our operations from these information technology-related and other potential disruptions, given the unpredictability of the timing, nature and scope of such disruptions, we could potentially be subject to production downtimes, operational delays and interruptions in our ability to provide products and services to our customers. Any disruption caused by the unavailability of our computer systems could adversely affect our sales, could require us to make a significant investment to fix or replace them and, therefore, could adversely affect our consolidated results of operations. In addition, cyber-security attacks are evolving and include, but are not limited to, malicious software, attempts to gain unauthorized access to data and other electronic security breaches that could lead to disruptions in systems, unauthorized release of confidential or otherwise protected information and corruption of data. If the network of security controls, policy enforcement mechanisms and monitoring systems to address these threats to our technology fails, the compromising of confidential or otherwise protected Company, customer, or employee information, destruction or corruption of data, security breaches, or other manipulation or improper use of our systems and networks could result in financial losses from remedial actions, loss of business or potential liability and damage to our reputation.

Failure to achieve and maintain effective internal controls could adversely affect our business and stock price.

Effective internal controls are necessary for us to provide reliable financial reports. All internal control systems, no matter how well designed, have inherent limitations. Therefore, even those systems determined to be effective can provide only reasonable assurance with respect to the consolidated financial statement preparation and presentation. While we continue to evaluate our internal controls, including those related to the acquired G&K business, we cannot be certain that these measures will ensure that we implement and maintain adequate controls over our financial processes and reporting in the future. If we fail to maintain the adequacy of our internal controls or if we or our independent registered public accounting firm were to discover material weaknesses in our internal controls, as such standards are modified, supplemented or amended, we may not be able to ensure that we can conclude on an ongoing basis that we have effective internal control over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act of 2002. Failure to achieve and maintain an effective internal control environment could cause us to be unable to produce reliable financial reports or prevent fraud. This may cause investors to lose confidence in our reported financial information, which could have a material adverse effect on our stock price.

We may experience difficulties in attracting and retaining competent personnel in key positions.

We believe that a key component of our success is our corporate culture, which has been imparted by management throughout our corporate organization. This factor, along with our entire operation, depends on our ability to attract and retain key employees. Competitive pressures within and outside our industry may make it more difficult and expensive for us to attract and retain key employees which could adversely affect our businesses.

Unexpected events could disrupt our operations and adversely affect our results of operations.

Unexpected events, including fires or explosions at facilities, natural disasters such as hurricanes and tornadoes, war or terrorist activities, unplanned outages, supply disruptions, failure of equipment or systems or changes in laws and/or regulations impacting our businesses, could adversely affect our consolidated results of operations. These events could result in customer disruption, physical damage to one or more key operating facilities, the temporary closure of one or more key operating facilities or the temporary disruption of information systems.

8

We may recognize impairment charges, which could adversely affect our financial condition and results of operations.

We assess our goodwill and other intangible assets and our long-lived assets for impairment when required by U.S. GAAP. These accounting principles require that we record an impairment charge if circumstances indicate that the asset carrying values exceed their estimated fair values. The estimated fair value of these assets is impacted by general economic conditions in the locations in which we operate. Deterioration in these general economic conditions may result in: declining revenue, which can lead to excess capacity and declining operating cash flow; reductions in management's estimates for future revenue and operating cash flow growth; increases in borrowing rates and other deterioration in factors that impact our weighted average cost of capital; and deteriorating real estate values. If our assessment of goodwill, other intangible assets or long-lived assets indicates an impairment of the carrying value for which we recognize an impairment charge, this may adversely affect our consolidated financial condition and consolidated results of operations.

The effects of credit market volatility and changes in our credit ratings could adversely affect our liquidity and results of operations.

Our operating cash flows, combined with access to the credit markets, provide us with significant discretionary funding capacity. However, deterioration in the global credit markets may limit our ability to access credit markets, which could adversely affect our liquidity and/or increase our cost of borrowing. In addition, credit market deterioration and its actual or perceived effects on our results of operations and financial condition, along with deterioration in general economic conditions, may increase the likelihood that the major independent credit agencies will downgrade our credit ratings, which could increase our cost of borrowing. Increases in our cost of borrowing could adversely affect our consolidated results of operations.

Item 1B. Unresolved Staff Comments

None.

9

Item 2. Properties

Cintas occupies 539 facilities located in 345 cities. Cintas leases 295 of these facilities for various terms ranging from monthly to the year 2032. Cintas expects that it will be able to renew or replace its leases on satisfactory terms. Of the six manufacturing facilities noted below, Cintas controls the operations of one manufacturing facility, but does not own or lease the real estate related to the operation. All remaining facilities are owned. The principal executive office in Cincinnati, Ohio, provides centrally located administrative functions including accounting, finance, marketing and computer system development and support. Cintas operates rental processing plants that house administrative, sales and service personnel and the necessary equipment involved in the cleaning of uniforms and bulk items, such as entrance mats and shop towels. Branch operations provide administrative, sales and service functions. Cintas operates 11 distribution centers and six manufacturing facilities. Cintas also operates first aid and safety and fire protection facilities and direct sales offices. Cintas considers the facilities it operates to be adequate for their intended use. Cintas owns or leases approximately 19,200 vehicles which are used for the route-based services and by the sales and management employee-partners.

The following chart provides additional information concerning Cintas' facilities:

Type of Facility | # of Facilities | ||

Rental Processing Plants | 217 | ||

Rental Branches | 203 | ||

First Aid and Safety Facilities | 53 | ||

All Other Facilities | 49 | ||

Distribution Centers | 11 | (1) | |

Manufacturing Facilities | 6 | ||

Total | 539 | ||

(1) Includes the principal executive office, which is attached to the distribution center in Cincinnati, Ohio.

Rental processing plants, rental branches, distribution centers and manufacturing facilities are used in Cintas' Uniform Rental and Facility Services reportable operating segment. First aid and safety facilities, rental processing plants and distribution centers are used in the First Aid and Safety Services reportable operating segment. Rental processing plants, rental branches, first aid and safety facilities, fire protection facilities, direct sales offices, distribution centers and manufacturing facilities are all utilized by the businesses included in All Other.

Item 3. Legal Proceedings

Cintas is subject to legal proceedings, insurance receipts, legal settlements and claims arising from the ordinary course of its business, including personal injury, customer contract, environmental and employment claims. In the opinion of management, the aggregate liability, if any, with respect to such ordinary course of business actions will not have a material adverse effect on the consolidated financial position, consolidated results of operations or consolidated cash flows of Cintas.

Item 4. Mine Safety Disclosures

Not applicable.

10

Part II

Item 5. Market for Registrant's Common Equity,

Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

Cintas' common stock is traded on the NASDAQ Global Select Market under the symbol "CTAS." The following table provides the high and low sales prices of shares of Cintas' common stock by quarter during the last two fiscal years:

Fiscal 2017 | |||||||

Quarter Ended | High | Low | |||||

May 2017 | $ | 128.85 | $ | 117.21 | |||

February 2017 | 122.21 | 112.96 | |||||

November 2016 | 119.94 | 102.07 | |||||

August 2016 | 117.69 | 91.24 | |||||

Fiscal 2016 | |||||||

Quarter Ended | High | Low | |||||

May 2016 | $ | 95.49 | $ | 84.32 | |||

February 2016 | 93.64 | 80.00 | |||||

November 2015 | 94.35 | 82.71 | |||||

August 2015 | 89.74 | 78.00 | |||||

Holders

At May 31, 2017, there were approximately 2,000 shareholders on record of Cintas' common stock. Cintas believes that this represents approximately 62,000 beneficial owners.

Dividends

Dividends on Cintas' outstanding common stock have been paid annually and amounted to $1.33 per share, $1.05 per share and $1.70 per share in fiscal 2017, 2016 and 2015, respectively. The fiscal 2015 dividend was comprised of an annual cash dividend of $0.85 per share, and an additional $0.85 per share special dividend related to the cash proceeds received from the Shred-it Transaction.

11

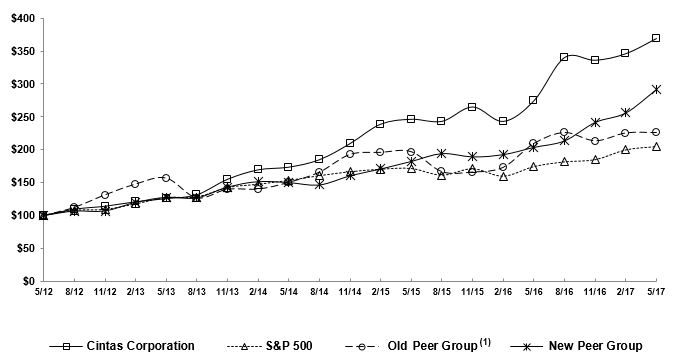

Stock Performance Graph

The following graph summarizes the cumulative return on $100 invested in Cintas' common stock, the S&P 500 Stock Index, the common stocks of a selected peer group of companies Because our products and services are diverse, Cintas does not believe that any single published industry index is appropriate for comparing shareholder return. Therefore, the peer groups used in the performance graph combines publicly traded companies in the business services industry that have similar characteristics as Cintas for each fiscal year, such as route based delivery of products and services. Prior to fiscal 2017, Cintas compared its common stock returns to the following publicly traded companies: G & K Services, Inc., UniFirst Corporation, ABM Industries and Iron Mountain, Inc. (Old Peer Group). In fiscal 2016, Cintas completed the sale of the businesses within the former Document Management Services operating segment. As a result, Cintas made the change to a new peer group (New Peer Group). The companies included in the New Peer Group are UniFirst Corporation, ABM Industries and Rollins, Inc. Rollins, Inc. was added to the New Peer Group because it is a route based provider of products and services with similar characteristics as Cintas.

Total shareholder return was based on the increase in the price of the common stock and assumed reinvestment of all dividends. Further, total return was weighted according to market capitalization of each company. The companies in the Peer Groups are not the same as those considered by the Compensation Committee of the Board of Directors.

Total Shareholder Returns

Comparison of Five-Year Cumulative Total Return

(1) The Old Peer Group previously included G&K Services, Inc. but has been excluded from the Old Peer Group herein due to our acquisition of G&K Services, Inc. during fiscal 2017.

12

Purchases of Equity Securities by the Issuer and Affiliated Purchases

Period (In millions, except share and per share data) | Total number of shares purchased | Average price paid per share | Total number of shares purchased as part of the publicly announced plan (1) | Maximum approximate dollar value of shares that may yet be purchased under the plan (1) | |||||||||

March 1 - 31, 2017 (2) | 937 | $ | 126.20 | — | $ | 500.0 | |||||||

April 1 - 30, 2017 (3) | 689 | 125.11 | — | 500.0 | |||||||||

May 1 - 31, 2017 (4) | 3,704 | 124.75 | — | 500.0 | |||||||||

Total | 5,330 | $ | 125.05 | — | $ | 500.0 | |||||||

(1) On August 6, 2016, Cintas announced that the Board of Directors authorized a $500.0 million share buyback program, which does not have an expiration date.

(2) During March 2017, Cintas acquired 937 shares of Cintas common stock in satisfaction of employee payroll taxes due on restricted stock awards that vested during the fiscal year. These shares were purchased at an average price of $126.20 per share for a total purchase price of $0.1 million.

(3) During April 2017, Cintas acquired 689 shares of Cintas common stock in satisfaction of employee payroll taxes due on restricted stock awards that vested during the fiscal year. These shares were purchased at an average price of $125.11 per share for a total purchase price of less than $0.1 million.

(4) During May 2017, Cintas acquired 3,704 shares of Cintas common stock in satisfaction of employee payroll taxes due on restricted stock awards that vested during the fiscal year. These shares were purchased at an average price of $124.75 per share for a total purchase price of $0.5 million.

13

Item 6. Selected Financial Data

Five-Year Financial Summary

(In thousands except per share and percentage data) | |||||||||||||||||||||

Fiscal Years Ended May 31, | 2013(1) | 2014(1) | 2015(1) | 2016(1) | 2017(1)(2) | Compound Annual Growth (2013-2017) | |||||||||||||||

Revenue | $ | 3,878,271 | $ | 4,091,204 | $ | 4,369,677 | $ | 4,795,772 | $ | 5,323,381 | 8.2% | ||||||||||

Net Income, Continuing Operations | 300,150 | 330,541 | 402,553 | 448,605 | 457,286 | 11.1% | |||||||||||||||

Net Income, Discontinued Operations | 15,292 | 43,901 | 28,065 | 244,915 | 23,422 | 11.2% | |||||||||||||||

Net Income | $ | 315,442 | $ | 374,442 | $ | 430,618 | $ | 693,520 | $ | 480,708 | 11.1% | ||||||||||

Basic Earnings Per Share: | |||||||||||||||||||||

Continuing Operations | $ | 2.41 | $ | 2.72 | $ | 3.44 | $ | 4.08 | $ | 4.27 | 15.4% | ||||||||||

Discontinued Operations | 0.12 | 0.36 | 0.24 | 2.22 | 0.22 | 16.4% | |||||||||||||||

Basic Earnings Per Share | $ | 2.53 | $ | 3.08 | $ | 3.68 | $ | 6.30 | $ | 4.49 | 15.4% | ||||||||||

Diluted Earnings Per Share: | |||||||||||||||||||||

Continuing Operations | $ | 2.40 | $ | 2.69 | $ | 3.39 | $ | 4.02 | $ | 4.17 | 14.8% | ||||||||||

Discontinued Operations | 0.12 | 0.36 | 0.24 | 2.19 | 0.21 | 15.0% | |||||||||||||||

Diluted Earnings Per Share | $ | 2.52 | $ | 3.05 | $ | 3.63 | $ | 6.21 | $ | 4.38 | 14.8% | ||||||||||

Dividends Per Share | $ | 0.64 | $ | 0.77 | $ | 1.70 | $ | 1.05 | $ | 1.33 | 20.1% | ||||||||||

Total Assets (3) | $ | 4,336,417 | $ | 4,454,457 | $ | 4,185,675 | $ | 4,098,815 | $ | 6,844,057 | 12.1% | ||||||||||

Shareholders' Equity | $ | 2,201,492 | $ | 2,192,858 | $ | 1,932,455 | $ | 1,842,659 | $ | 2,302,793 | 1.1% | ||||||||||

Return on Average Equity (4) | 13.8% | 15.0% | 19.5% | 23.8% | 22.1% | ||||||||||||||||

Long-Term Debt | $ | 1,291,764 | $ | 1,292,482 | $ | 1,293,215 | $ | 1,294,422 | $ 3,133,524(5) | ||||||||||||

(1) | In accordance with the applicable accounting guidance for the disposal of long-lived assets and discontinued operations, the results of our Discontinued Services, Shredding and Storage have been excluded from continuing operations for all periods presented. Please see Note 16 entitled Discontinued Operations of "Notes to Consolidated Financial Statements" for additional information. |

(2) | Includes G&K results of operations from March 21, 2017 through May 31, 2017. Historical periods presented prior to fiscal 2017 do not include G&K and as a result, the information may not be comparable. Please see Note 9 entitled Acquisitions and Divestitures of "Notes to Consolidated Financial Statements" for additional information regarding the G&K acquisition. |

(3) | In accordance with the applicable accounting guidance for simplifying the presentation of debt issuance costs, the debt costs related to recognized debt liabilities have been excluded from Total Assets and reclassified to Long-Term Debt as a direct deduction from the carrying amount of the debt liabilities. The impact of this change in accounting principle on balances previously reported for fiscal 2016, 2015, 2014 and 2013 were reclassifications of $5.6 million, $6.8 million, $8.0 million and $9.2 million, respectively, from other assets to long-term liabilities. |

(4) | Return on average equity is computed as net income from continuing operations divided by the average of shareholders' equity. We believe that disclosure of this non-GAAP financial measure gives management and shareholders a good indication of Cintas' historical performance. |

(5) | Includes issuance of approximately $2.1 billion in debt to fund the G&K acquisition. Please see Note 6 entitled Debt and Derivatives of "Notes to Consolidated Financial Statements" for additional information. |

14

Item 7. Management's Discussion and Analysis

of Financial Condition and Results of Operations

Business Strategy

Cintas helps more than one million businesses of all types and sizes, primarily in North America, as well as Latin America, Europe and Asia, get Ready™ to open their doors with confidence every day by providing a wide range of products and services that enhance our customers’ image and help keep their facilities and employees clean, safe and looking their best. With products and services including uniforms, floor care, restroom supplies, first aid and safety products, fire extinguishers and testing, and safety and compliance training, Cintas helps customers get Ready for the Workday™.

We are North America's leading provider of corporate identity uniforms through rental and sales programs, as well as a significant provider of related business services, including entrance mats, restroom cleaning services and supplies, carpet and tile cleaning services, first aid and safety services and fire protection products and services.

Cintas' principal objective is "to exceed customers' expectations in order to maximize the long-term value of Cintas for shareholders and working partners," and it provides the framework and focus for Cintas' business strategy. This strategy is to achieve revenue growth for all of our products and services by increasing our penetration at existing customers and by broadening our customer base to include business segments to which we have not historically served. We will also continue to identify additional product and service opportunities for our current and future customers.

To pursue the strategy of increasing penetration, we have a highly talented and diverse team of service professionals visiting our customers on a regular basis. This frequent contact with our customers enables us to develop close personal relationships. The combination of our distribution system and these strong customer relationships provides a platform from which we launch additional products and services.

We pursue the strategy of broadening our customer base in several ways. Cintas has a national sales organization introducing all of our products and services to prospects in all business segments. Our broad range of products and services allows our sales organization to consider any type of business a prospect. We also broaden our customer base through geographic expansion, especially in our first aid and safety and fire protection businesses. Finally, we evaluate strategic acquisitions as opportunities arise.

Results of Operations

On March 21, 2017, Cintas completed the acquisition of G&K Services, Inc. (G&K) for consideration of approximately $2.1 billion. G&K is now a wholly-owned subsidiary of Cintas that will operate within the Uniform Rental and Facility Services operating segment. To finance the G&K acquisition, Cintas used a combination of new senior notes, a term loan, other borrowings under its existing credit facility and cash on hand. G&K's results of operations are included in Cintas' consolidated financial statements as of and from the date of acquisition.

U. S. GAAP requires companies to evaluate their reportable operating segments periodically and when certain events occur. As a result of our evaluation in fiscal 2016, effective June 1, 2015, Cintas realigned its organizational structure and updated its reportable operating segments in light of certain changes in its business, including the acquisition of ZEE Medical Inc. (ZEE) in the first quarter of fiscal 2016. Cintas’ updated reportable operating segments are Uniform Rental and Facility Services and First Aid and Safety Services. The Uniform Rental and Facility Services reportable operating segment, which includes G&K, consists of the rental and servicing of uniforms and other garments including flame resistant clothing, mats, mops and shop towels and other ancillary items. In addition to these rental items, restroom cleaning services and supplies, carpet and tile cleaning services and the sale of items from our catalogs to our customers on route are included within this reportable operating segment. The First Aid and Safety Services reportable operating segment, which includes ZEE, consists of first aid and safety products and services. The remainder of Cintas’ business, which consists of Fire Protection Services and its Uniform Direct Sale business, is included in All Other. Cintas evaluates operating segment performance based on revenue and income before income taxes. Revenue and income before income taxes for each of these reportable operating segments for the years ended May 31, 2017, 2016 and 2015 are presented in Note 14 entitled Operating Segment Information of "Notes to Consolidated Financial Statements." The Company regularly reviews its operating segments for reporting purposes based on the information its chief operating decision maker regularly reviews for purposes of allocating resources and assessing performance and makes changes when appropriate.

15

At May 31, 2017, Cintas has classified a significant business, referred to as Discontinued Services, as held for sale. Prior to meeting the held for sale criteria, Discontinued Services was primarily included in All Other. In fiscal 2014, Cintas completed its partnership transaction with the shareholders of Shred-it International Inc. to combine Shredding with the shredding business of Shred-it International Inc. Pursuant to the Shredding Transaction, the Shred-it Partnership was owned 42% by Cintas and 58% by the shareholders of Shred-it International Inc. Cintas' investment in Shred-it and the results of Shredding are classified as discontinued operations for all periods presented as a result of selling the investment during fiscal 2016. During fiscal 2015, Cintas sold Storage and, as a result, its operations are also classified as discontinued operations for all periods presented. In accordance with the applicable accounting guidance for the disposal of long-lived assets and discontinued operations, the results of Discontinued Services, Shredding and Storage have been excluded from both continuing operations and operating segment results for all periods presented. Please see Note 16 entitled Discontinued Operations of "Notes to Consolidated Financial Statements" for additional information.

The following table sets forth certain consolidated statements of income data as a percent of revenue by reportable operating segment, All Other and in total for the fiscal years ended May 31:

2017(1) | 2016(1) | 2015(1) | ||||||

Revenue: | ||||||||

Uniform Rental and Facility Services | 79.0 | % | 78.4 | % | 80.5 | % | ||

First Aid and Safety Services | 9.5 | % | 9.6 | % | 7.5 | % | ||

All Other | 11.5 | % | 12.0 | % | 12.0 | % | ||

Total revenue | 100.0 | % | 100.0 | % | 100.0 | % | ||

Cost of sales: | ||||||||

Uniform Rental and Facility Services | 54.9 | % | 55.7 | % | 56.6 | % | ||

First Aid and Safety Services | 54.7 | % | 57.3 | % | 53.4 | % | ||

All Other | 58.3 | % | 58.6 | % | 59.1 | % | ||

Total cost of sales | 55.3 | % | 56.2 | % | 56.6 | % | ||

Gross margin: | ||||||||

Uniform Rental and Facility Services | 45.1 | % | 44.3 | % | 43.4 | % | ||

First Aid and Safety Services | 45.3 | % | 42.7 | % | 46.6 | % | ||

All Other | 41.7 | % | 41.4 | % | 40.9 | % | ||

Total gross margin | 44.7 | % | 43.8 | % | 43.4 | % | ||

Selling and administrative expenses: | ||||||||

Uniform Rental and Facility Services | 27.1 | % | 26.5 | % | 26.2 | % | ||

First Aid and Safety Services | 34.9 | % | 31.9 | % | 32.8 | % | ||

All Other | 34.5 | % | 33.1 | % | 34.3 | % | ||

Total selling and administrative expenses | 28.7 | % | 27.8 | % | 27.7 | % | ||

G&K Services, Inc. transaction and integration expenses | 1.5 | % | — | % | — | % | ||

Gain on sale of stock of an equity method investment | — | % | — | % | 0.5 | % | ||

Interest expense, net | 1.6 | % | 1.3 | % | 1.5 | % | ||

Income from continuing operations before income taxes | 12.9 | % | 14.7 | % | 14.7 | % | ||

(1) | The figures presented reflect the change in classification of Discontinued Services, Shredding and Storage to discontinued operations within the Consolidated Statements of Income. See Note 16 entitled Discontinued Operations of "Notes to Consolidated Financial Statements." |

16

Fiscal 2017 Compared to Fiscal 2016

Fiscal 2017 total revenue was $5.3 billion, an increase of 11.0% over the prior fiscal year. Revenue increased organically by 6.7% as a result of increased sales volume. Organic growth adjusts for the impact of acquisitions, divestitures, workday differences and foreign currency exchange rate fluctuations. Total revenue was positively impacted by 4.8% due to acquisitions, primarily through the acquisition of G&K. Revenue growth was negatively impacted by 0.1% due to foreign currency exchange rate fluctuations and 0.4% due to one less workday in fiscal 2017 compared to fiscal 2016.

Organic growth by quarter is shown in the table below.

Organic Growth | |

First Quarter Ending August 31, 2016 | 6.0% |

Second Quarter Ending November 30, 2016 | 6.0% |

Third Quarter Ending February 28, 2017 | 6.6% |

Fourth Quarter Ending May 31, 2017 | 8.1% |

For the Fiscal Year Ending May 31, 2017 | 6.7% |

Uniform Rental and Facility Services reportable operating segment revenue consists predominantly of revenue derived from the rental of corporate identity uniforms and other garments, including flame resistant clothing, and the rental and/or sale of mats, mops, shop towels, restroom supplies and other rental services. Revenue from the Uniform Rental and Facility Services reportable operating segment increased 11.8% compared to fiscal 2016. The increase resulted from an organic growth increase in revenue of 6.9%. The amount of new business grew, resulting from an increase in the number and productivity of sales representatives. Generally, sales productivity improvements are the result of increased tenure and improved training, which result in a higher number of products and services sold. Revenue growth was negatively impacted by 0.1% due to foreign currency exchange rate fluctuations and 0.4% due to one less workday in fiscal 2017 compared to the same period in the prior fiscal year. Revenue was positively impacted by 5.4% due to acquisitions, primarily G&K.

Other revenue, consisting of revenue from the First Aid and Safety Services reportable operating segment and All Other, increased 8.2% compared to fiscal 2016. Revenue increased organically by 6.1% due primarily to improved sales representative productivity. Revenue growth was negatively impacted by 0.1% due to foreign currency exchange rate fluctuations and 0.4% due to one less workday in fiscal 2017 compared to fiscal 2016. Acquisitions positively impacted revenue by 2.6%.

Cost of uniform rental and facility services increased 10.3% compared to fiscal 2016. Cost of uniform rental and facility services consists primarily of production expenses, delivery expenses and the amortization of in service inventory, including uniforms, mats, shop towels and other ancillary items. The cost of uniform rental and facility services increase compared to fiscal 2016 was due to increased Uniform Rental and Facility Services reportable operating segment sales volume from internal growth and the acquired G&K sales volume.

Cost of other consists primarily of cost of goods sold (predominantly first aid and safety products, uniforms and fire protection products), delivery expenses and distribution expenses in the First Aid and Safety Services reportable operating segment and All Other. Cost of other increased 5.6% in fiscal 2017 compared to fiscal 2016. The increase was primarily related to the increased sales volumes in the First Aid and Safety Services reportable operating segment and All Other.

Selling and administrative expenses increased $195.0 million, or 14.6%, compared to fiscal 2016 due primarily to increases in labor and other employee-partner related expenses. As a result of the acquisition of G&K in fiscal 2017, the Company incurred various transaction and integration expenses which relate primarily to asset impairment charges, legal and professional fees, employee termination expenses, the write-off of excess inventory and other miscellaneous expenses. In fiscal 2017, G&K transaction and integration expenses were $79.2 million or 1.5% of total revenue.

Net interest expense (interest expense less interest income) was $86.3 million in fiscal 2017 compared to $63.6 million in fiscal 2016. The increase in net interest expense is primarily due to the additional debt issued to finance the G&K acquisition and $17.1 million of short-term debt financing fees incurred in connection with the acquisition.

17

Income before income taxes was $687.4 million, a decrease of $17.9 million, or 2.5%, compared to fiscal 2016. The decrease in income before income taxes was due to the G&K transaction and integration expenses and the increase in interest expense previously mentioned. These impacts were partially offset by the increase in gross margin.

Cintas' effective tax rate on continuing operations was 33.5% for fiscal 2017 compared to 36.4% in fiscal 2016. The decrease was primarily due to the adoption of Accounting Standard Update (ASU) 2016-09, "Improvements to Employee Share-Based Payment Accounting." The effective tax rate in fiscal 2017 included a benefit of $29.4 million as a result of the adoption of ASU 2016-09. This benefit was partially offset by the election to recognize forfeitures as they occur, which resulted in additional stock compensation expense of $8.3 million when compared to our historical practice of estimating forfeiture for expense purposes. The adoption of ASU 2016-09 also resulted in an increase in the effect of dilutive securities in fiscal 2017 of 0.8 million shares. For fiscal 2017, the net impact on diluted earnings per share from the adoption of ASU 2016-09 was an increase of $0.19 per share over what diluted earnings per share would have been if ASU 2016-09 was not adopted in the current year.

Net income from continuing operations for fiscal 2017 of $457.3 million was a 1.9% increase compared to fiscal 2016. Diluted earnings per share from continuing operations of $4.17 was a 3.7% increase compared to fiscal 2016. Diluted earnings per share from continuing operations increased due to the lower effective tax rate combined with the decrease in weighted average common shares outstanding. The decrease in weighted average common shares outstanding resulted from purchasing 8.8 million shares of common stock under the January 13, 2015 and August 4, 2015 share buyback programs since the beginning of fiscal 2016.

Uniform Rental and Facility Services Reportable Operating Segment

Uniform Rental and Facility Services reportable operating segment revenue increased $443.0 million, or 11.8%, and the cost of uniform rental and facility services increased $214.9 million, or 10.3%, as previously discussed. The reportable operating segment's fiscal 2017 gross margin was 45.1% of revenue compared to 44.3% in fiscal 2016. The 80 basis point improvement was driven by many factors, including new business sold by sales representatives, penetration of additional products and services into existing customers and continuously improving the efficiency of internal processes.

Selling and administrative expenses for the Uniform Rental and Facility Services reportable operating segment increased $143.8 million in fiscal 2017 compared to fiscal 2016. Selling and administrative expense as a percent of revenue for fiscal 2017 was 27.1% compared to 26.5% in fiscal 2016. The increase in selling and administrative expenses for the Uniform Rental and Facility Services reportable operating segment is primarily related to the G&K acquisition.

As a result of the G&K acquisition, the Uniform Rental and Facility Services reportable operating segment incurred $79.2 million of transaction and integration expenses. These expenses consisted of the following: asset impairment charges of $23.3 million, legal and professional fees directly related to the acquisition of $17.4 million, employee termination expenses recognized under ASC Topic 712, "Compensation - Nonretirement Postemployment Benefits" of $31.0 million, write-off of excess inventory of $5.5 million and $2.0 million of other miscellaneous integration expenses.

Income before income taxes increased $5.0 million to $677.1 million for fiscal 2017 compared to fiscal 2016. Income before income taxes as a percent of revenue, at 16.1%, decreased 180 basis points from 17.9% in fiscal 2016. The decrease is primarily due to the G&K transaction and integration expenses mentioned above.

First Aid and Safety Services Reportable Operating Segment

First Aid and Safety Services reportable operating segment revenue increased $46.5 million in fiscal 2017, a 10.1% increase compared to fiscal 2016. Revenue increased organically by 5.9% as a result of increased sales volume. Revenue growth was positively impacted by 4.6% due to acquisitions. One less workday in fiscal 2017 compared to the prior year negatively impacted growth by 0.4%.

Cost of first aid and safety services increased $13.3 million, or 5.0%, in fiscal 2017, due primarily to increased First Aid and Safety Services reportable operating segment volume. Gross margin for the First Aid and Safety Services reportable operating segment is defined as revenue less cost of goods, warehouse expenses, service expenses and training expenses. The gross margin as a percent of revenue was 45.3% for fiscal 2017 compared to 42.7% in fiscal 2016. The increase in gross margin was due to the benefits realized as a result of the integration of ZEE. These benefits included improved delivery efficiencies and improved sourcing of goods.

Selling and administrative expenses for the First Aid and Safety Services reportable operating segment increased by $29.9 million, or 20.3%, in fiscal 2017 compared to fiscal 2016. Selling and administrative expenses as a percent of

18

revenue were 34.9% in fiscal 2017 compared to 31.9% in fiscal 2016. The increase in selling and administrative expenses is primarily the result of the investment in selling resources to grow the acquired ZEE customer base and increases in various employee-partner related expenses.

Income before income taxes was $52.8 million in fiscal 2017, an increase of $3.3 million, or 6.6%, compared to fiscal 2016. Income before income taxes as a percent of revenue, at 10.4%, decreased from 10.7% in fiscal 2016, due primarily to the investment in selling resources mentioned above.

Fiscal 2016 Compared to Fiscal 2015

Fiscal 2016 total revenue was $4.8 billion, an increase of 9.8% over the prior fiscal year. Revenue increased organically by 6.8% as a result of increased sales volume. Organic growth excludes the impact of acquisitions, divestitures, foreign currency exchange rate fluctuations and workday differences. Total revenue was positively impacted by 2.9% due to acquisitions and 0.8% due to two more workdays in fiscal 2016 compared to fiscal 2015. Revenue growth was negatively impacted by 0.7% due to foreign currency exchange rate fluctuations.

Organic growth by quarter is shown in the table below.

Organic Growth | |

First Quarter Ending August 31, 2015 | 6.9% |

Second Quarter Ending November 30, 2015 | 6.6% |

Third Quarter Ending February 28, 2016 | 7.1% |

Fourth Quarter Ending May 31, 2016 | 6.8% |

For the Fiscal Year Ending May 31, 2016 | 6.8% |

Uniform Rental and Facility Services reportable operating segment revenue consists predominantly of revenue derived from the rental of corporate identity uniforms and other garments, including flame resistant clothing, and the rental and/or sale of mats, mops, shop towels, restroom supplies and other rental services. Revenue from the Uniform Rental and Facility Services reportable operating segment increased 6.8% compared to fiscal 2015. The increase resulted from an organic growth increase in revenue of 6.5%. The amount of new business grew, resulting from an increase in the number and productivity of sales representatives. Generally, sales productivity improvements are the result of increased tenure and improved training, which result in a higher number of products and services sold. Revenue was positively impacted by 0.3% due to acquisitions, 0.8% due to two more workdays in fiscal 2016 compared to 2015 and negatively impacted by 0.8% due to foreign currency exchange rate fluctuations.

Other revenue, consisting of revenue from the First Aid and Safety Services reportable operating segment and All Other, increased 21.8% compared to fiscal 2015. The increase primarily resulted from an organic growth increase of 8.3%, which was largely due to improved sales representative productivity. Revenue in fiscal 2016 was negatively impacted by 0.5% due to foreign currency exchange rate fluctuations. Acquisitions positively impacted the growth rate by 13.0%, and two more workdays in fiscal 2016 contributed an additional 1.0%.

Cost of uniform rental and facility services increased 5.0% compared to fiscal 2015. Cost of uniform rental and facility services consists primarily of production expenses, delivery expenses and the amortization of in service inventory, including uniforms, mats, shop towels and other ancillary items. The increase in the cost of uniform rental and facility services compared to fiscal 2015 was due to increased Uniform Rental and Facility Services reportable operating segment sales volume.

Cost of other increased 24.3% compared to fiscal 2015. Cost of other consists primarily of cost of goods sold (predominantly first aid and safety products, uniforms and fire protection products), delivery expenses and distribution expenses in the First Aid and Safety Services reportable operating segment and All Other. The increase from fiscal 2015 was primarily due to increased First Aid and Safety Services reportable operating segment sales volume.

Selling and administrative expenses increased $123.1 million, or 10.2%, compared to fiscal 2015 due primarily to increases in labor and other employee-partner related expenses.

During fiscal 2015, Cintas sold stock in an equity method investment. In conjunction with the sale of the equity method investment, the Company received a cash dividend. The sale resulted in the recording of a gain of $21.7 million in fiscal 2015.

19

Operating income of $768.9 million in fiscal 2016 increased $85.3 million, or 12.5%, compared to fiscal 2015.

Net interest expense (interest expense less interest income) was $63.6 million in fiscal 2016 compared to $64.8 million in fiscal 2015. The decrease in net interest expense is primarily due to the capitalization of $1.1 million of interest in fiscal year 2016 versus $0.6 million of interest capitalized in fiscal 2015.

Income before income taxes was $705.3 million, an increase of $64.8 million, or 10.1%, compared to fiscal 2015. The increase in income before income taxes was primarily due to revenue growing at a faster rate than expenses.

Cintas' effective tax rate in fiscal 2016 was 36.4%, which was comparable to the effective tax rate of 37.2% in fiscal 2015. See Note 8 entitled Income Taxes of "Notes to Consolidated Financial Statements" for more information on income taxes.

Net income from continuing operations for fiscal 2016 of $448.6 million was a 11.4% increase compared to fiscal 2015. Diluted earnings per share from continuing operations of $4.02 was a 18.6% increase compared to fiscal 2015. The increase in diluted earnings per share is higher than the increase in net income due to a decrease in weighted average common stock outstanding as a result of Cintas purchasing 8.7 million shares of common stock under the January 13, 2015 share buyback program since the beginning of fiscal 2016.

Uniform Rental and Facility Services Reportable Operating Segment

Uniform Rental and Facility Services reportable operating segment revenue increased $240.3 million, or 6.8%, and the cost of uniform rental and facility services increased $100.2 million, or 5.0%. Revenue in fiscal 2016 was negatively affected by 0.8% due to foreign currency exchange rate changes compared to fiscal 2015 and positively affected by 0.3% due to acquisitions and 0.8% due to two more workdays in fiscal 2016 compared to 2015. The reportable operating segment's fiscal 2016 gross margin was 44.3% of revenue compared to 43.4% in fiscal 2015. The increase in gross margin as a percent of revenue over fiscal 2015 was due to new business sold by sales representatives, penetration of additional products and services into existing customers, and continuously improving the efficiency of internal processes. In addition, lower energy-related expenses increased gross margin 50 basis points.

Selling and administrative expenses for the Uniform Rental and Facility Services reportable operating segment increased $72.0 million in fiscal 2016 compared to fiscal 2015 primarily due to increases in labor and other employee-partner related expenses. Selling and administrative expense as a percent of revenue for fiscal 2016 was 26.5% compared to 26.2% in fiscal 2015.

Income before income taxes increased $68.1 million to $672.1 million for fiscal 2016 compared to fiscal 2015. Income before income taxes as a percent of revenue, at 17.9%, increased from 17.2% in fiscal 2015. This increase is primarily due to the increase in gross margin.

First Aid and Safety Services Reportable Operating Segment

First Aid and Safety Services reportable operating segment revenue increased $135.2 million in fiscal 2016, a 41.4% increase compared to fiscal 2015. Revenue increased organically by 9.7% as a result of increased sales volume. Revenue growth was positively impacted by 1.1% due to two more workdays in fiscal 2016 compared to fiscal 2015. The remaining 30.6% increase in growth represents growth derived through acquisitions, primarily the ZEE acquisition.

Cost of first aid and safety services increased $90.5 million, or 51.9%, in fiscal 2016, due primarily to increased First Aid and Safety Services reportable operating segment volume. Gross margin for the First Aid and Safety Services reportable operating segment is defined as revenue less cost of goods, warehouse expenses, service expenses and training expenses. The gross margin as a percent of revenue was 42.7% for fiscal 2016 compared to 46.6% in fiscal 2015. ZEE integration costs and the lower efficiency of the acquired ZEE routes were primarily responsible for the decrease in gross margin.

Selling and administrative expenses increased by $40.3 million, or 37.6%, in fiscal 2016 compared to fiscal 2015 primarily due to an increase in labor and other employee-partner related expenses and costs associated with the integration of ZEE. Selling and administrative expenses as a percent of revenue, at 31.9%, decreased from 32.8% in fiscal 2015.

Income before income taxes was $49.5 million in fiscal 2016, an increase of $4.4 million, or 9.7%, compared to fiscal 2015. Income before income taxes as a percent of revenue, at 10.7%, decreased from 13.8% in fiscal 2015, due to the decrease in gross margin discussed above.

20

Liquidity and Capital Resources

The following is a summary of our cash flows and cash, cash equivalents and marketable securities as of and for the fiscal years ending May 31:

(In thousands) | 2017 | 2016 | |||||

Net cash provided by operating activities | $ | 763,887 | $ | 465,845 | |||

Net cash (used in) provided by investing activities | $ | (2,310,349 | ) | $ | 128,381 | ||

Net cash provided by (used in) financing activities | $ | 1,578,502 | $ | (866,724 | ) | ||

Cash and cash equivalents at the end of the period | $ | 169,266 | $ | 139,357 | |||