Attached files

| file | filename |

|---|---|

| 8-K - 8-K 2Q FINANCIAL RESULTS - CATERPILLAR INC | cat_8-kxq2x2017xearningsxr.htm |

Exhibit 99.1

Caterpillar Inc.

2Q 2017 Earnings Release

July 25, 2017

FOR IMMEDIATE RELEASE

Caterpillar Reports Second-Quarter 2017 Results

Delivered Strong Quarter with Higher Sales and Revenues and Profit; Raised Full-Year Outlook

Second Quarter | |||||||

($ in billions except profit per share) | 2017 | 2016 | ● | Second-quarter sales and revenues up $1 billion from a year ago | |||

Sales and Revenues | $11.331 | $10.342 | ● | Profitability across enterprise reflects strong operational performance | |||

Profit Per Share | $1.35 | $0.93 | ● | Delivered strong operating cash flow and increased the quarterly cash dividend | |||

Adjusted Profit Per Share | $1.49 | $1.09 | ● | Raised full-year outlook for 2017 sales and revenues and profit per share | |||

PEORIA, Ill. - Caterpillar Inc. (NYSE: CAT) today announced second-quarter 2017 sales and revenues of $11.3 billion, compared with $10.3 billion in the second quarter of 2016. Second-quarter 2017 profit per share was $1.35, compared with $0.93 per share in the second quarter of 2016. Excluding restructuring costs and a gain on the sale of an equity investment in IronPlanet, second-quarter 2017 adjusted profit per share was $1.49, compared to second-quarter 2016 adjusted profit per share of $1.09.

Caterpillar’s financial position continued to strengthen. Machinery, Energy & Transportation (ME&T) operating cash flow was $2.0 billion during the quarter, and ME&T’s debt-to-capital ratio improved to 38.6 percent, compared with 41.7 percent at the end of the first quarter of 2017. In June, the company announced a quarterly cash dividend increase and ended the quarter with an enterprise cash balance of $10.2 billion.

“Our team delivered an impressive quarter. As demand increased, we continued to control costs and generated higher profit margins,” said Caterpillar CEO Jim Umpleby. “While a number of our end markets remain challenged, construction in China and gas compression in North America were highlights in the quarter. Mining and oil-related activities have come off of recent lows, and we are seeing improving demand for construction in most regions.”

2017 Outlook

As a result of increased demand across many end markets and disciplined cost control, Caterpillar is raising its 2017 outlook. Some risks remain in the outlook, including weakness in the Middle East and Latin America, as well as geopolitical and commodity risk.

In April 2017, Caterpillar provided an outlook range for full-year 2017 sales and revenues of $38 billion to $41 billion with a midpoint of $39.5 billion. The company is raising its full-year 2017 expectations for sales and revenues to a range of $42 billion to $44 billion with a midpoint of $43 billion.

For the full year of 2017, Caterpillar expects profit per share of about $3.50 at the midpoint of the sales and revenues outlook range, or adjusted profit per share of about $5.00. The previous outlook for 2017 profit was about $2.10 per share at the midpoint of the sales and revenues outlook, or adjusted profit per share of about $3.75. The company now expects to incur about $1.2 billion of restructuring costs in 2017. The outlook does not include potential mark-to-market gains or losses related to pension and other postemployment benefit (OPEB) plans.

“Given our performance in the first half of the year and current quotation and ordering activity, we are confident in raising our full-year 2017 outlook,” continued Umpleby. “We remain focused on serving our customers, delivering strong operational performance and executing our ongoing restructuring activities. During the second half of 2017, we anticipate making targeted investments in initiatives that are important to our future competitiveness, including enhanced digital capabilities and accelerating technology updates to our products. We intend to do this without adding to the structural costs we’ve worked so hard to streamline. These investments will prepare us to take advantage of the growth opportunities ahead.”

(more)

2

Notes:

• | Glossary of terms is included on pages 14-15; first occurrence of terms shown in bold italics. |

• | Information on non-GAAP financial measures is included on page 16. |

• | Caterpillar will conduct a teleconference and live webcast, with a slide presentation, beginning at 10 a.m. Central Time on Tuesday, July 25, 2017, to discuss its 2017 second-quarter financial results. The accompanying slides will be available before the webcast on the Caterpillar website at http://www.caterpillar.com/investors/events-and-presentations. |

About Caterpillar:

For more than 90 years, Caterpillar Inc. has been making sustainable progress possible and driving positive change on every continent. Customers turn to Caterpillar to help them develop infrastructure, energy and natural resource assets. With 2016 sales and revenues of $38.537 billion, Caterpillar is the world’s leading manufacturer of construction and mining equipment, diesel and natural gas engines, industrial gas turbines and diesel-electric locomotives. The company principally operates through its three product segments - Construction Industries, Resource Industries and Energy & Transportation - and also provides financing and related services through its Financial Products segment. For more information, visit caterpillar.com. To connect with us on social media, visit caterpillar.com/social-media.

Caterpillar contact: Rachel Potts, 309-675-6892 (Office), 309-573-3444 (Mobile) or Potts_Rachel_A@cat.com

Forward-Looking Statements

Certain statements in this press release relate to future events and expectations and are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Words such as “believe,” “estimate,” “will be,” “will,” “would,” “expect,” “anticipate,” “plan,” “project,” “intend,” “could,” “should” or other similar words or expressions often identify forward-looking statements. All statements other than statements of historical fact are forward-looking statements, including, without limitation, statements regarding our outlook, projections, forecasts or trend descriptions. These statements do not guarantee future performance and speak only as of the date they are made, and we do not undertake to update our forward-looking statements.

Caterpillar’s actual results may differ materially from those described or implied in our forward-looking statements based on a number of factors, including, but not limited to: (i) global and regional economic conditions and economic conditions in the industries we serve; (ii) commodity price changes, material price increases, fluctuations in demand for our products or significant shortages of material; (iii) government monetary or fiscal policies; (iv) political and economic risks, commercial instability and events beyond our control in the countries in which we operate; (v) our ability to develop, produce and market quality products that meet our customers’ needs; (vi) the impact of the highly competitive environment in which we operate on our sales and pricing; (vii) information technology security threats and computer crime; (viii) additional restructuring costs or a failure to realize anticipated savings or benefits from past or future cost reduction actions; (ix) failure to realize all of the anticipated benefits from initiatives to increase our productivity, efficiency and cash flow and to reduce costs; (x) inventory management decisions and sourcing practices of our dealers and our OEM customers; (xi) a failure to realize, or a delay in realizing, all of the anticipated benefits of our acquisitions, joint ventures or divestitures; (xii) union disputes or other employee relations issues; (xiii) adverse effects of unexpected events including natural disasters; (xiv) disruptions or volatility in global financial markets limiting our sources of liquidity or the liquidity of our customers, dealers and suppliers; (xv) failure to maintain our credit ratings and potential resulting increases to our cost of borrowing and adverse effects on our cost of funds, liquidity, competitive position and access to capital markets; (xvi) our Financial Products segment’s risks associated with the financial services industry; (xvii) changes in interest rates or market liquidity conditions; (xviii) an increase in delinquencies, repossessions or net losses of Cat Financial’s customers; (xix) currency fluctuations; (xx) our or Cat Financial’s compliance with financial and other restrictive covenants in debt agreements; (xxi) increased pension plan funding obligations; (xxii) alleged or actual violations of trade or anti-corruption laws and regulations; (xxiii) international trade policies and their impact on demand for our products and our competitive position; (xxiv) additional tax expense or exposure; (xxv) significant legal proceedings, claims, lawsuits or government investigations; (xxvi) new regulations or changes in financial services regulations; (xxvii) compliance with environmental laws and regulations; and (xxviii) other factors described in more detail in Caterpillar’s Forms 10-Q, 10-K and other filings with the Securities and Exchange Commission.

(more)

3

CONSOLIDATED RESULTS

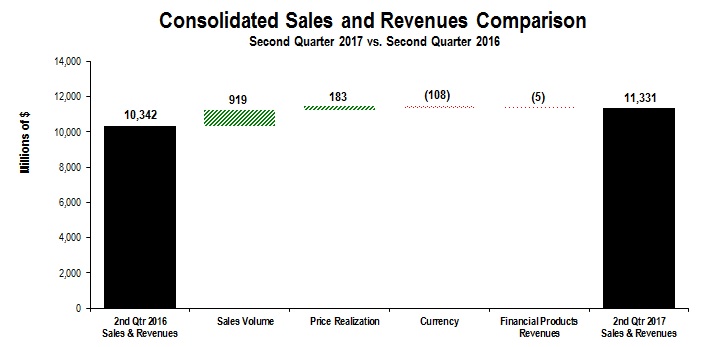

Consolidated Sales and Revenues

The chart above graphically illustrates reasons for the change in Consolidated Sales and Revenues between the second quarter of 2016 (at left) and the second quarter of 2017 (at right). Items favorably impacting sales and revenues appear as upward stair steps with the corresponding dollar amounts above each bar, while items negatively impacting sales and revenues appear as downward stair steps with dollar amounts reflected in parentheses above each bar. Caterpillar management utilizes these charts internally to visually communicate with the company’s board of directors and employees.

Sales and Revenues

Total sales and revenues were $11.331 billion in the second quarter of 2017, an increase of $989 million, or 10 percent, compared with $10.342 billion in the second quarter of 2016. The increase was primarily due to higher sales volume, with the largest increase in Construction Industries mostly due to higher end-user demand for construction equipment. Sales volume for Resource Industries increased due to improved end-user demand for aftermarket parts and the favorable impact of changes in dealer inventories. Energy & Transportation’s sales were higher mostly due to increased demand for aftermarket parts for reciprocating engines. Favorable price realization in Construction Industries also contributed to the sales improvement. The unfavorable impact of currency was mostly the result of a weaker euro and British pound. Financial Products’ segment revenues were about flat.

Sales increased in Asia/Pacific, North America and Latin America, and were about flat in EAME. Asia/Pacific sales increased 25 percent primarily due to an increase in construction equipment sales in China resulting from increased infrastructure and residential investment. In North America, sales increased 7 percent due to higher demand for aftermarket parts and construction equipment, partially offset by the unfavorable impact of changes in dealer inventories as dealers decreased inventories more in the second quarter of 2017 than in the second quarter of 2016. Sales increased 20 percent in Latin America primarily due to stabilizing economic conditions in several countries in the region that resulted in improved end-user demand from low levels.

(more)

4

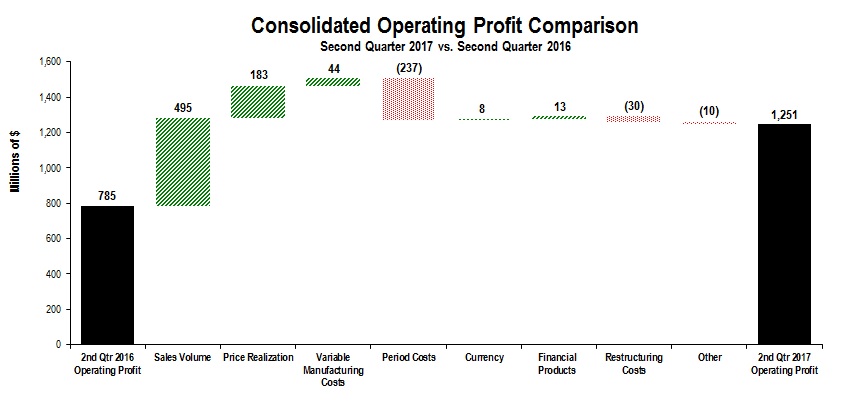

Consolidated Operating Profit

The chart above graphically illustrates reasons for the change in Consolidated Operating Profit between the second quarter of 2016 (at left) and the second quarter of 2017 (at right). Items favorably impacting operating profit appear as upward stair steps with the corresponding dollar amounts above each bar, while items negatively impacting operating profit appear as downward stair steps with dollar amounts reflected in parentheses above each bar. Caterpillar management utilizes these charts internally to visually communicate with the company’s board of directors and employees. The bar entitled Other includes consolidating adjustments and Machinery, Energy & Transportation other operating (income) expenses.

Operating profit for the second quarter of 2017 was $1.251 billion, compared with $785 million in the second quarter of 2016. The increase of $466 million was primarily due to higher sales volume, including a favorable mix of products. Improved price realization and lower variable manufacturing costs were about offset by higher period costs. Price realization was favorable in Construction Industries and about flat in Resource Industries and Energy & Transportation.

Variable manufacturing costs were lower primarily due to the favorable impact from cost absorption, partially offset by higher warranty expense. Cost absorption was favorable as inventory decreased in the second quarter of 2016 and increased in the second quarter of 2017.

Period costs increased primarily due to higher short-term incentive compensation expense, partially offset by the favorable impact of restructuring and cost reduction actions over the past year. These actions primarily impacted depreciation expense and research and development (R&D) expenses.

Restructuring costs of $169 million in the second quarter of 2017 were primarily related to restructuring programs in Resource Industries and Energy & Transportation, compared to $139 million in the second quarter of 2016.

Other Profit/Loss Items

• | Other income/expense in the second quarter of 2017 was income of $29 million, compared with income of $84 million in the second quarter of 2016. The unfavorable change was a result of currency translation and hedging net losses during the second quarter of 2017, primarily due to the euro and British pound. The unfavorable change was partially offset by a pretax gain of $85 million on the sale of Caterpillar’s equity investment in IronPlanet. |

▪ | The provision for income taxes in the second quarter reflects an estimated annual tax rate of 32 percent, which excludes the discrete item discussed in the following paragraph, compared to 25 percent for the second quarter of |

(more)

5

2016. The increase is primarily due to higher non-U.S. restructuring costs in 2017 that are taxed at relatively lower non-U.S. tax rates, along with other changes in the geographic mix of profits from a tax perspective.

In addition, a tax benefit of $10 million was recorded for the settlement of stock-based compensation awards with tax deductions in excess of cumulative U.S. GAAP compensation expense.

Excluding restructuring costs, gain on sale of equity investment and discrete items, the 2017 estimated annual tax rate is expected to be 29 percent.

Global Workforce

Caterpillar worldwide, full-time employment was about 94,800 at the end of the second quarter of 2017, a decrease of about 5,200 full-time employees from the end of the second quarter of 2016, primarily the result of restructuring programs. The flexible workforce increased by about 3,500, primarily due to higher production volumes. In total, the global workforce decreased by about 1,700.

June 30 | ||||||||

2017 | 2016 | Increase / (Decrease) | ||||||

Full-time employment | 94,800 | 100,000 | (5,200 | ) | ||||

Flexible workforce | 16,400 | 12,900 | 3,500 | |||||

Total | 111,200 | 112,900 | (1,700 | ) | ||||

Geographic summary | ||||||||

U.S. workforce | 48,500 | 49,600 | (1,100 | ) | ||||

Non-U.S. workforce | 62,700 | 63,300 | (600 | ) | ||||

Total | 111,200 | 112,900 | (1,700 | ) | ||||

(more)

6

SEGMENT RESULTS

Sales and Revenues by Geographic Region

(Millions of dollars) | Total | % Change | North America | % Change | Latin America | % Change | EAME | % Change | Asia/ Pacific | % Change | |||||||||||||||||||

Second Quarter 2017 | |||||||||||||||||||||||||||||

Construction Industries 1 | $ | 4,930 | 11% | $ | 2,318 | 3% | $ | 364 | 31% | $ | 964 | (5)% | $ | 1,284 | 44% | ||||||||||||||

Resource Industries 2 | 1,759 | 21% | 612 | 14% | 299 | 16% | 396 | 25% | 452 | 32% | |||||||||||||||||||

Energy & Transportation 3 | 3,941 | 5% | 1,982 | 10% | 312 | 13% | 1,079 | 2% | 568 | (6)% | |||||||||||||||||||

All Other Segments 4 | 33 | (20)% | 10 | (29)% | 1 | (50)% | 11 | 22% | 11 | (31)% | |||||||||||||||||||

Corporate Items and Eliminations | (24 | ) | — | (22 | ) | — | (2 | ) | — | ||||||||||||||||||||

Machinery, Energy & Transportation | $ | 10,639 | 10% | $ | 4,900 | 7% | $ | 976 | 20% | $ | 2,448 | 2% | $ | 2,315 | 25% | ||||||||||||||

Financial Products Segment | $ | 776 | 2% | $ | 505 | 7% | $ | 79 | (4)% | $ | 101 | (2)% | $ | 91 | (10)% | ||||||||||||||

Corporate Items and Eliminations | (84 | ) | (51 | ) | (15 | ) | (5 | ) | (13 | ) | |||||||||||||||||||

Financial Products Revenues | $ | 692 | (1)% | $ | 454 | 3% | $ | 64 | (9)% | $ | 96 | (2)% | $ | 78 | (13)% | ||||||||||||||

Consolidated Sales and Revenues | $ | 11,331 | 10% | $ | 5,354 | 7% | $ | 1,040 | 18% | $ | 2,544 | 2% | $ | 2,393 | 23% | ||||||||||||||

Second Quarter 2016 | |||||||||||||||||||||||||||||

Construction Industries 1 | $ | 4,426 | $ | 2,247 | $ | 277 | $ | 1,010 | $ | 892 | |||||||||||||||||||

Resource Industries 2 | 1,457 | 539 | 258 | 317 | 343 | ||||||||||||||||||||||||

Energy & Transportation 3 | 3,750 | 1,809 | 277 | 1,062 | 602 | ||||||||||||||||||||||||

All Other Segments 4 | 41 | 14 | 2 | 9 | 16 | ||||||||||||||||||||||||

Corporate Items and Eliminations | (29 | ) | (25 | ) | — | (2 | ) | (2 | ) | ||||||||||||||||||||

Machinery, Energy & Transportation | $ | 9,645 | $ | 4,584 | $ | 814 | $ | 2,396 | $ | 1,851 | |||||||||||||||||||

Financial Products Segment | $ | 759 | $ | 473 | $ | 82 | $ | 103 | $ | 101 | |||||||||||||||||||

Corporate Items and Eliminations | (62 | ) | (34 | ) | (12 | ) | (5 | ) | (11 | ) | |||||||||||||||||||

Financial Products Revenues | $ | 697 | $ | 439 | $ | 70 | $ | 98 | $ | 90 | |||||||||||||||||||

Consolidated Sales and Revenues | $ | 10,342 | $ | 5,023 | $ | 884 | $ | 2,494 | $ | 1,941 | |||||||||||||||||||

1 Does not include inter-segment sales of $29 million and $12 million in second quarter 2017 and 2016, respectively.

2 Does not include inter-segment sales of $77 million and $57 million in second quarter 2017 and 2016, respectively.

3 Does not include inter-segment sales of $827 million and $658 million in second quarter 2017 and 2016, respectively.

4 Does not include inter-segment sales of $105 million and $101 million in second quarter 2017 and 2016, respectively.

Sales and Revenues by Segment

(Millions of dollars) | Second Quarter 2016 | Sales Volume | Price Realization | Currency | Other | Second Quarter 2017 | $ Change | % Change | |||||||||||||||||||||

Construction Industries | $ | 4,426 | $ | 374 | $ | 191 | $ | (61 | ) | $ | — | $ | 4,930 | $ | 504 | 11% | |||||||||||||

Resource Industries | 1,457 | 313 | (7 | ) | (4 | ) | — | 1,759 | 302 | 21% | |||||||||||||||||||

Energy & Transportation | 3,750 | 236 | (3 | ) | (42 | ) | — | 3,941 | 191 | 5% | |||||||||||||||||||

All Other Segments | 41 | (8 | ) | — | — | — | 33 | (8 | ) | (20)% | |||||||||||||||||||

Corporate Items and Eliminations | (29 | ) | 4 | 2 | (1 | ) | — | (24 | ) | 5 | |||||||||||||||||||

Machinery, Energy & Transportation | $ | 9,645 | $ | 919 | $ | 183 | $ | (108 | ) | $ | — | $ | 10,639 | $ | 994 | 10% | |||||||||||||

Financial Products Segment | $ | 759 | $ | — | $ | — | $ | — | $ | 17 | $ | 776 | $ | 17 | 2% | ||||||||||||||

Corporate Items and Eliminations | (62 | ) | — | — | — | (22 | ) | (84 | ) | (22 | ) | ||||||||||||||||||

Financial Products Revenues | $ | 697 | $ | — | $ | — | $ | — | $ | (5 | ) | $ | 692 | $ | (5 | ) | (1)% | ||||||||||||

Consolidated Sales and Revenues | $ | 10,342 | $ | 919 | $ | 183 | $ | (108 | ) | $ | (5 | ) | $ | 11,331 | $ | 989 | 10% | ||||||||||||

(more)

7

Operating Profit (Loss) by Segment

(Millions of dollars) | Second Quarter 2017 | Second Quarter 2016 | $ Change | % Change | ||||||||||

Construction Industries | $ | 901 | $ | 550 | $ | 351 | 64 | % | ||||||

Resource Industries | 97 | (163 | ) | 260 | n/a | |||||||||

Energy & Transportation | 700 | 602 | 98 | 16 | % | |||||||||

All Other Segments | (20 | ) | (14 | ) | (6 | ) | (43 | )% | ||||||

Corporate Items and Eliminations | (526 | ) | (297 | ) | (229 | ) | ||||||||

Machinery, Energy & Transportation | $ | 1,152 | $ | 678 | $ | 474 | 70 | % | ||||||

Financial Products Segment | $ | 191 | $ | 202 | $ | (11 | ) | (5 | )% | |||||

Corporate Items and Eliminations | (5 | ) | (31 | ) | 26 | |||||||||

Financial Products | $ | 186 | $ | 171 | $ | 15 | 9 | % | ||||||

Consolidating Adjustments | (87 | ) | (64 | ) | (23 | ) | ||||||||

Consolidated Operating Profit | $ | 1,251 | $ | 785 | $ | 466 | 59 | % | ||||||

(more)

8

CONSTRUCTION INDUSTRIES

(Millions of dollars) | ||||||||||||||||||

Sales Comparison | ||||||||||||||||||

Second Quarter 2016 | Sales Volume | Price Realization | Currency | Second Quarter 2017 | $ Change | % Change | ||||||||||||

Sales Comparison 1 | $4,426 | $374 | $191 | ($61) | $4,930 | $504 | 11 | % | ||||||||||

Sales by Geographic Region | ||||||||||||||||||

Second Quarter 2017 | Second Quarter 2016 | $ Change | % Change | |||||||||||||||

North America | $2,318 | $2,247 | $71 | 3 | % | |||||||||||||

Latin America | 364 | 277 | 87 | 31 | % | |||||||||||||

EAME | 964 | 1,010 | (46 | ) | (5 | )% | ||||||||||||

Asia/Pacific | 1,284 | 892 | 392 | 44 | % | |||||||||||||

Total 1 | $4,930 | $4,426 | $504 | 11 | % | |||||||||||||

Segment Profit | ||||||||||||||||||

Second Quarter 2017 | Second Quarter 2016 | $ Change | % Change | |||||||||||||||

Segment Profit | $901 | $550 | $351 | 64 | % | |||||||||||||

1 Does not include inter-segment sales of $29 million and $12 million in second quarter 2017 and 2016, respectively.

Construction Industries’ sales were $4.930 billion in the second quarter of 2017, compared with $4.426 billion in the second quarter of 2016. The increase was due to higher sales volume and favorable price realization.

▪ | Sales volume increased primarily due to higher end-user demand for construction equipment in Asia/Pacific and North America, partially offset by the unfavorable impact of changes in dealer inventories. A more significant decrease in North America dealer inventories in the second quarter of 2017 than in the second quarter of 2016 was partially offset by an increase in dealer inventories in Asia/Pacific in the second quarter of 2017. |

▪ | Although market conditions remain competitive, price realization was favorable due to a particularly weak pricing environment in the second quarter of 2016 and previously announced price increases impacting the second quarter of 2017. |

Sales increased in Asia/Pacific and Latin America and were about flat in North America and EAME.

▪ | Sales in Asia/Pacific were higher as a result of an increase in end-user demand, primarily in China, stemming from increased government support for infrastructure and strong residential investment. In addition, changes in dealer inventories in China favorably impacted sales as dealer inventories increased in the second quarter of 2017 and were about flat in the second quarter of 2016. |

▪ | Sales in Latin America were higher due to an increase in end-user demand and the favorable impact of changes in dealer inventories, which increased in the second quarter of 2017 and were about flat in the second quarter of 2016. Although construction activity remained weak across the region, end-user demand increased from low levels due to stabilizing economic conditions in several countries in the region. |

▪ | In North America, an increase in end-user demand and favorable price realization was mostly offset by an unfavorable impact from changes in dealer inventories. End-user demand was higher primarily due to improved residential and non-residential building construction activity, slightly offset by lower sales for infrastructure construction equipment. The |

(more)

9

unfavorable impact of changes in dealer inventories resulted from a more significant decrease in dealer inventories in the second quarter of 2017 than in the second quarter of 2016.

▪ | Sales in EAME were about flat as lower end-user demand and the unfavorable impact of the weaker euro and British pound were mostly offset by favorable price realization. The decline in end-user demand was primarily in Africa/Middle East due to volatile financial and economic conditions, as well as continued tight construction spending in oil-producing countries. |

Construction Industries’ profit was $901 million in the second quarter of 2017, compared with $550 million in the second quarter of 2016. The increase in profit was primarily due to favorable price realization and higher sales volume, including a favorable mix of products. Period costs were about flat as higher short-term incentive compensation expense was mostly offset by the favorable impact of restructuring and cost reduction actions.

RESOURCE INDUSTRIES

(Millions of dollars) | ||||||||||||||||||

Sales Comparison | ||||||||||||||||||

Second Quarter 2016 | Sales Volume | Price Realization | Currency | Second Quarter 2017 | $ Change | % Change | ||||||||||||

Sales Comparison 1 | $1,457 | $313 | ($7) | ($4) | $1,759 | $302 | 21 | % | ||||||||||

Sales by Geographic Region | ||||||||||||||||||

Second Quarter 2017 | Second Quarter 2016 | $ Change | % Change | |||||||||||||||

North America | $612 | $539 | $73 | 14 | % | |||||||||||||

Latin America | 299 | 258 | 41 | 16 | % | |||||||||||||

EAME | 396 | 317 | 79 | 25 | % | |||||||||||||

Asia/Pacific | 452 | 343 | 109 | 32 | % | |||||||||||||

Total 1 | $1,759 | $1,457 | $302 | 21 | % | |||||||||||||

Segment Profit (Loss) | ||||||||||||||||||

Second Quarter 2017 | Second Quarter 2016 | $ Change | % Change | |||||||||||||||

Segment Profit (Loss) | $97 | ($163) | $260 | n/a | ||||||||||||||

1 Does not include inter-segment sales of $77 million and $57 million in second quarter 2017 and 2016, respectively.

Resource Industries’ sales were $1.759 billion in the second quarter of 2017, an increase of $302 million, or 21 percent, from the second quarter of 2016. The increase was primarily due to higher sales volume for aftermarket parts and the favorable impact of changes in dealer inventories. Dealer inventories were about flat in the second quarter of 2017, compared with a decrease in the second quarter of 2016. Dealer deliveries for equipment were about flat. Increases in certain commodity prices over the past year, along with continued commodity consumption, have resulted in increased mining activity, driving the need for maintenance and rebuild activities. The company believes commodity prices need to stabilize at these higher levels to drive stronger activity and longer-term demand for equipment.

Resource Industries’ profit was $97 million in the second quarter of 2017, compared with a loss of $163 million in the second quarter of 2016. The favorable change was due to higher sales volume, including a favorable mix of products, lower period costs and the favorable impact of cost absorption. These items were partially offset by higher warranty expense. Period costs were lower primarily due to the favorable impact of restructuring and cost reduction actions, partially offset by

(more)

10

an increase in short-term incentive compensation expense. The favorable impact of cost absorption was a result of a decrease in inventory in the second quarter of 2016, compared to an increase in inventory in the second quarter of 2017.

ENERGY & TRANSPORTATION

(Millions of dollars) | ||||||||||||||||||

Sales Comparison | ||||||||||||||||||

Second Quarter 2016 | Sales Volume | Price Realization | Currency | Second Quarter 2017 | $ Change | % Change | ||||||||||||

Sales Comparison 1 | $3,750 | $236 | ($3) | ($42) | $3,941 | $191 | 5 | % | ||||||||||

Sales by Geographic Region | ||||||||||||||||||

Second Quarter 2017 | Second Quarter 2016 | $ Change | % Change | |||||||||||||||

North America | $1,982 | $1,809 | $173 | 10 | % | |||||||||||||

Latin America | 312 | 277 | 35 | 13 | % | |||||||||||||

EAME | 1,079 | 1,062 | 17 | 2 | % | |||||||||||||

Asia/Pacific | 568 | 602 | (34 | ) | (6 | )% | ||||||||||||

Total 1 | $3,941 | $3,750 | $191 | 5 | % | |||||||||||||

Segment Profit | ||||||||||||||||||

Second Quarter 2017 | Second Quarter 2016 | $ Change | % Change | |||||||||||||||

Segment Profit | $700 | $602 | $98 | 16 | % | |||||||||||||

1 Does not include inter-segment sales of $827 million and $658 million in second quarter 2017 and 2016, respectively.

Energy & Transportation’s sales were $3.941 billion in the second quarter of 2017, compared with $3.750 billion in the second quarter of 2016. The increase was primarily due to higher sales of aftermarket parts for reciprocating engines.

▪ | Oil and Gas - Sales increased in North America due to higher demand for reciprocating engines used in gas compression as natural gas infrastructure build-out continues and for aftermarket parts as a result of strong rebuild activity in well servicing and gas compression applications. This was partially offset by a decrease in demand for equipment used in production applications in Asia/Pacific. |

▪ | Industrial - Sales were higher in all regions reflecting increased sales for aftermarket parts. |

▪ | Power Generation - Sales were about flat as a slight increase in North America was mostly offset by decreases in other regions. |

▪ | Transportation - Sales decreased in North America as the rail industry continues to have a significant number of idle locomotives. This was partially offset by an increase in sales for rail services as North American rail traffic has increased. Sales declined in marine applications mostly due to lower demand, primarily for offshore vessels. |

Energy & Transportation’s profit was $700 million in the second quarter of 2017, compared with $602 million in the second quarter of 2016. The increase was primarily due to higher sales volume and lower variable manufacturing costs, partially offset by higher period costs. Variable manufacturing costs were favorable primarily due to cost absorption and improved material costs. Cost absorption was favorable as inventory increased in the second quarter of 2017 and was about flat in the second quarter of 2016. The increase in period costs was primarily due to higher short-term incentive compensation expense.

(more)

11

FINANCIAL PRODUCTS SEGMENT

(Millions of dollars) | |||||||||||||||||

Revenues by Geographic Region | |||||||||||||||||

Second Quarter 2017 | Second Quarter 2016 | $ Change | % Change | ||||||||||||||

North America | $505 | $473 | $32 | 7 | % | ||||||||||||

Latin America | 79 | 82 | (3 | ) | (4 | )% | |||||||||||

EAME | 101 | 103 | (2 | ) | (2 | )% | |||||||||||

Asia/Pacific | 91 | 101 | (10 | ) | (10 | )% | |||||||||||

Total | $776 | $759 | $17 | 2 | % | ||||||||||||

Segment Profit | |||||||||||||||||

Second Quarter 2017 | Second Quarter 2016 | $ Change | % Change | ||||||||||||||

Segment Profit | $191 | $202 | ($11) | (5 | )% | ||||||||||||

Financial Products’ revenues were $776 million in the second quarter of 2017, an increase of $17 million, or 2 percent, from the second quarter of 2016. The increase was due to a favorable impact from intercompany lending activity in North America, higher average financing rates in North America and a favorable impact from returned or repossessed equipment in North America. These favorable impacts were partially offset by lower average earning assets in North America and lower average financing rates in Asia/Pacific.

Financial Products’ profit was $191 million in the second quarter of 2017, compared with $202 million in the second quarter of 2016. The decrease was primarily due to the absence of gains on sales of securities at Insurance Services, an increase in SG&A expenses due to higher short-term incentive compensation expense and an unfavorable impact from lower average earning assets. These unfavorable impacts were partially offset by a decrease in the provision for credit losses at Cat Financial, increased intercompany lending activity and a favorable impact from returned or repossessed equipment.

At the end of the second quarter of 2017, past dues at Cat Financial were 2.71 percent, compared with 2.93 percent at the end of the second quarter of 2016. Write-offs, net of recoveries, were $26 million for the second quarter of 2017, compared with $33 million for the second quarter of 2016.

As of June 30, 2017, Cat Financial's allowance for credit losses totaled $338 million, or 1.25 percent of finance receivables, compared with $346 million, or 1.25 percent of finance receivables as of June 30, 2016. The allowance for credit losses at year-end 2016 was $343 million, or 1.29 percent of finance receivables.

Corporate Items and Eliminations

Expense for corporate items and eliminations was $531 million in the second quarter of 2017, an increase of $203 million from the second quarter of 2016. Corporate items and eliminations include: restructuring costs; corporate-level expenses; timing differences, as some expenses are reported in segment profit on a cash basis; retirement benefit costs other than service cost; currency differences for ME&T, as segment profit is reported using annual fixed exchange rates; cost of sales methodology differences as segments use a current cost methodology; and inter-segment eliminations.

The increase in expense from the second quarter of 2016 was primarily due to timing differences, an increase in restructuring costs, higher stock-based compensation expense and other methodology differences.

(more)

12

QUESTIONS AND ANSWERS

Q1: | Can you comment on second-quarter restructuring costs and your 2017 outlook for restructuring costs? |

A: | Restructuring costs of $169 million in the second quarter of 2017 were primarily related to programs in Resource Industries and Energy & Transportation. Second-quarter restructuring costs included a LIFO Inventory Decrement Benefit of $33 million related to the closure of the Gosselies, Belgium, facility. |

We have incurred $921 million of restructuring costs through the first six months of 2017 and expect to incur about $1.2 billion for the full-year 2017, slightly lower than the previous outlook for 2017 restructuring costs of $1.25 billion. We expect costs for the remainder of 2017 to be primarily for previously announced restructuring actions.

Q2: | Can you discuss changes in dealer inventories during the second quarter of 2017? |

A: | Changes in dealer inventories had little impact on sales from the second quarter of 2016 to the second quarter of 2017. Dealer machine and engine inventories decreased about $300 million in the second quarter of 2017, compared to a decrease of about $400 million in the second quarter of 2016. During the first six months of 2017 and 2016, dealer machine and engine inventories decreased about $100 million. |

Q3: | Can you discuss changes to your order backlog by segment? |

A: | At the end of the second quarter of 2017, the order backlog was about $14.8 billion, about flat with the first quarter of 2017. Resource Industries’ order backlog increased about $300 million, Construction Industries’ decreased about $300 million and Energy & Transportation’s was about flat. It is not uncommon for the construction order backlog to decline during the second-quarter selling season. |

Compared with the second quarter of 2016, the order backlog increased about $3.0 billion. The increase was across all segments, most significantly in Construction Industries and Resource Industries.

Q4: | Can you comment on expense related to your 2017 short-term incentive compensation plans? |

A: | Short-term incentive compensation expense is directly related to financial and operational performance, measured against targets set annually. Second-quarter 2017 expense was about $415 million. Second-quarter 2016 expense was about $85 million. |

For 2017, our current outlook includes short-term incentive compensation expense of about $1.3 billion. Our 2017 outlook, issued in January, assumed short-term incentive compensation expense of about $750 million. Full-year 2016 short-term incentive compensation expense was about $250 million, significantly below targeted levels.

Q5: | Can you comment on your balance sheet and cash priorities? |

A: | The ME&T debt-to-capital ratio was 38.6 percent at the end of the second quarter of 2017, compared with 41.7 percent at the end of the first quarter of 2017. Our cash and liquidity positions remain strong with an enterprise cash balance of $10.232 billion as of June 30, 2017. ME&T operating cash flow for the second quarter of 2017 was $2.029 billion, compared with $1.168 billion in the second quarter of 2016. The increase was primarily due to higher profit adjusted for non-cash charges, including short-term incentive compensation expense, in the second quarter of 2017 versus the second quarter of 2016. |

Although our short-term priorities for the use of cash may vary from time to time as business needs and conditions dictate, our long-term cash deployment strategy remains unchanged: maintain a strong financial position in support of our credit rating; provide capital to support growth; appropriately fund employee benefit plans; pay dividends; and repurchase common stock.

(more)

13

GLOSSARY OF TERMS

1. | Adjusted Profit Per Share - Profit per share excluding restructuring costs for 2017 and 2016. For 2017, adjusted profit per share also excludes a gain on the sale of an equity investment in IronPlanet recognized in the second quarter. |

2. | All Other Segments - Primarily includes activities such as: the business strategy, product management and development, and manufacturing of filters and fluids, undercarriage, tires and rims, ground engaging tools, fluid transfer products, precision seals, and rubber sealing and connecting components primarily for Cat® products; parts distribution; distribution services responsible for dealer development and administration including a wholly owned dealer in Japan, dealer portfolio management and ensuring the most efficient and effective distribution of machines, engines and parts; digital investments for new customer and dealer solutions that integrate data analytics with state-of-the art digital technologies while transforming the buying experience. |

3. | Consolidating Adjustments - Elimination of transactions between Machinery, Energy & Transportation and Financial Products. |

4. | Construction Industries - A segment primarily responsible for supporting customers using machinery in infrastructure, forestry and building construction applications. Responsibilities include business strategy, product design, product management and development, manufacturing, marketing and sales and product support. The product portfolio includes backhoe loaders, small wheel loaders, small track-type tractors, skid steer loaders, multi-terrain loaders, mini excavators, compact wheel loaders, telehandlers, select work tools, small, medium and large track excavators, wheel excavators, medium wheel loaders, compact track loaders, medium track-type tractors, track-type loaders, motor graders, pipelayers, forestry and paving products and related parts. |

5. | Currency - With respect to sales and revenues, currency represents the translation impact on sales resulting from changes in foreign currency exchange rates versus the U.S. dollar. With respect to operating profit, currency represents the net translation impact on sales and operating costs resulting from changes in foreign currency exchange rates versus the U.S. dollar. Currency includes the impact on sales and operating profit for the Machinery, Energy & Transportation lines of business only excluding restructuring costs; currency impacts on Financial Products’ revenues and operating profit are included in the Financial Products’ portions of the respective analyses. With respect to other income/expense, currency represents the effects of forward and option contracts entered into by the company to reduce the risk of fluctuations in exchange rates (hedging) and the net effect of changes in foreign currency exchange rates on our foreign currency assets and liabilities for consolidated results (translation). |

6. | Debt-to-Capital Ratio - A key measure of Machinery, Energy & Transportation’s financial strength used by management. The metric is defined as Machinery, Energy & Transportation’s short-term borrowings, long-term debt due within one year and long-term debt due after one year (debt) divided by the sum of Machinery, Energy & Transportation’s debt and shareholders’ equity. Debt also includes Machinery, Energy & Transportation’s long-term borrowings from Financial Products. |

7. | EAME - A geographic region including Europe, Africa, the Middle East and the Commonwealth of Independent States (CIS). |

8. | Earning Assets - Assets consisting primarily of total finance receivables net of unearned income, plus equipment on operating leases, less accumulated depreciation at Cat Financial. |

9. | Energy & Transportation - A segment primarily responsible for supporting customers using reciprocating engines, turbines, diesel-electric locomotives and related parts across industries serving power generation, industrial, oil and gas and transportation applications, including marine and rail-related businesses. Responsibilities include business strategy, product design, product management and development, manufacturing, marketing and sales and product support of turbines and turbine-related services, reciprocating engine powered generator sets, integrated systems used in the electric power generation industry, reciprocating engines and integrated systems and solutions for the marine and oil and gas industries; reciprocating engines supplied to the industrial industry as well as Cat machinery; the remanufacturing of Cat engines and components and remanufacturing services for other companies; the business strategy, product design, product management and development, manufacturing, remanufacturing, leasing and service of diesel-electric locomotives and components and other rail-related products and services and product support of on-highway vocational trucks for North America. |

10. | Financial Products Segment - Provides financing alternatives to customers and dealers around the world for Caterpillar products, as well as financing for vehicles, power generation facilities and marine vessels that, in most cases, incorporate Caterpillar products. Financing plans include operating and finance leases, installment sale contracts, working capital loans and wholesale financing plans. The segment also provides insurance and risk management products and services that help customers and dealers manage their business risk. Insurance and risk management products offered include physical damage insurance, inventory protection plans, extended service coverage for machines and engines, and dealer property and casualty insurance. The various forms of financing, insurance and risk management products offered to customers and dealers help support the purchase and lease of our equipment. Financial Products segment profit is determined on a pretax basis and includes other income/expense items. |

(more)

14

11. | Latin America - A geographic region including Central and South American countries and Mexico. |

12. | LIFO Inventory Decrement Benefits - A significant portion of Caterpillar's inventory is valued using the last-in, first-out (LIFO) method. With this method, the cost of inventory is comprised of "layers" at cost levels for years when inventory increases occurred. A LIFO decrement occurs when inventory decreases, depleting layers added in earlier, generally lower cost years. A LIFO decrement benefit represents the impact on operating profit of charging cost of goods sold with prior-year cost levels rather than current period costs. |

13. | Machinery, Energy & Transportation (ME&T) - Represents the aggregate total of Construction Industries, Resource Industries, Energy & Transportation and All Other Segments and related corporate items and eliminations. |

14. | Machinery, Energy & Transportation Other Operating (Income) Expenses - Comprised primarily of gains/losses on disposal of long-lived assets, gains/losses on divestitures and legal settlements and accruals. Restructuring costs classified as other operating expenses on the Results of Operations are presented separately on the Operating Profit Comparison. |

15. | Pension and Other Postemployment Benefit (OPEB) - The company’s defined benefit pension and postretirement benefit plans. |

16. | Period Costs - Includes period manufacturing costs, ME&T selling, general and administrative (SG&A) and research and development (R&D) expenses excluding the impact of currency and exit-related costs that are included in restructuring costs (see definition below). Period manufacturing costs support production but are defined as generally not having a direct relationship to short-term changes in volume. Examples include machinery and equipment repair, depreciation on manufacturing assets, facility support, procurement, factory scheduling, manufacturing planning and operations management. SG&A and R&D costs are not linked to the production of goods or services and include marketing, legal and finance services and the development of new and significant improvements in products or processes. |

17. | Price Realization - The impact of net price changes excluding currency and new product introductions. Price realization includes geographic mix of sales, which is the impact of changes in the relative weighting of sales prices between geographic regions. |

18. | Resource Industries - A segment primarily responsible for supporting customers using machinery in mining, quarry, waste, and material handling applications. Responsibilities include business strategy, product design, product management and development, manufacturing, marketing and sales and product support. The product portfolio includes large track-type tractors, large mining trucks, hard rock vehicles, longwall miners, electric rope shovels, draglines, hydraulic shovels, track and rotary drills, highwall miners, large wheel loaders, off-highway trucks, articulated trucks, wheel tractor scrapers, wheel dozers, landfill compactors, soil compactors, material handlers, continuous miners, scoops and haulers, hardrock continuous mining systems, select work tools, machinery components, electronics and control systems and related parts. In addition to equipment, Resource Industries also develops and sells technology products and services to provide customers fleet management, equipment management analytics and autonomous machine capabilities. Resource Industries also manages areas that provide services to other parts of the company, including integrated manufacturing and research and development. |

19. | Restructuring Costs - Primarily costs for employee separation, long-lived asset impairments and contract terminations. These costs are included in Other Operating (Income) Expenses. Restructuring costs also include other exit-related costs primarily for accelerated depreciation, inventory write-downs, equipment relocation and project management costs and also LIFO inventory decrement benefits from inventory liquidations at closed facilities (primarily included in Cost of goods sold). |

20. | Sales Volume - With respect to sales and revenues, sales volume represents the impact of changes in the quantities sold for Machinery, Energy & Transportation as well as the incremental revenue impact of new product introductions, including emissions-related product updates. With respect to operating profit, sales volume represents the impact of changes in the quantities sold for Machinery, Energy & Transportation combined with product mix as well as the net operating profit impact of new product introductions, including emissions-related product updates. Product mix represents the net operating profit impact of changes in the relative weighting of Machinery, Energy & Transportation sales with respect to total sales. The impact of sales volume on segment profit includes intersegment sales. |

21. | Variable Manufacturing Costs - Represents volume-adjusted costs excluding the impact of currency and restructuring costs (see definition above). Variable manufacturing costs are defined as having a direct relationship with the volume of production. This includes material costs, direct labor and other costs that vary directly with production volume such as freight, power to operate machines and supplies that are consumed in the manufacturing process. |

(more)

15

NON-GAAP FINANCIAL MEASURES

The non-GAAP financial measures Caterpillar uses have no standardized meaning prescribed by U.S. GAAP and therefore are unlikely to be comparable to the calculation of similar measures for other companies. Management does not intend these items to be considered in isolation or substituted for the related GAAP measure.

Adjusted Profit per Share

Caterpillar believes it is important to separately quantify the profit impact of two special items in order for the company’s results to be meaningful to readers. These items consist of restructuring costs, which are incurred in the current year to generate longer-term benefits, and a gain on sale of an equity investment. Caterpillar does not consider these items indicative of earnings from ongoing business activities and believes the non-GAAP measure will provide useful perspective on underlying business results and trends, and a means to assess the company’s period-over-period results.

Reconciliations of adjusted profit per share to the most directly comparable GAAP measure, diluted profit per share, are as follows:

Machinery, Energy & Transportation

Second Quarter | 2017 Outlook | ||||||

2016 | 2017 | Previous 1 | Current 2 | ||||

Profit per share | $0.93 | $1.35 | $2.10 | $3.50 | |||

Per share restructuring costs 3 | $0.16 | $0.23 | $1.65 | $1.59 | |||

Per share gain on sale of equity investment 4 | - | ($0.09) | - | ($0.09) | |||

Adjusted profit per share | $1.09 | $1.49 | $3.75 | $5.00 | |||

1 2017 Sales and Revenues Outlook in a range of $38-$41 billion (as of April 25, 2017). Profit per share at midpoint. | |||||||

2 2017 Sales and Revenues Outlook in a range of $42-$44 billion. Profit per share at midpoint. | |||||||

3 At estimated annual tax rate based on full-year outlook for per share restructuring costs at statutory tax rates. Second-quarter 2017 and 2017 Outlook at estimated annual rate of 22 percent. 2017 Outlook includes $15 million increase to prior year taxes related to non-U.S. restructuring costs recognized in the first quarter of 2017. Second-quarter 2017 includes a favorable interim adjustment of $0.01 per share resulting from the difference in the estimated annual tax rate for consolidated reporting of 32 percent and the estimated annual tax rate for profit per share excluding restructuring costs, gain on sale of equity investment and discrete items of 29 percent. | |||||||

4 At U.S. statutory tax rate of 35 percent. | |||||||

Caterpillar defines Machinery, Energy & Transportation as it is presented in the supplemental data as Caterpillar Inc. and its subsidiaries with Financial Products accounted for on the equity basis. Machinery, Energy & Transportation information relates to the design, manufacture and marketing of Caterpillar products. Financial Products’ information relates to the financing to customers and dealers for the purchase and lease of Caterpillar and other equipment. The nature of these businesses is different, especially with regard to the financial position and cash flow items. Caterpillar management utilizes this presentation internally to highlight these differences. The company also believes this presentation will assist readers in understanding Caterpillar’s business. Pages 17-25 reconcile Machinery, Energy & Transportation with Financial Products on the equity basis to Caterpillar Inc. consolidated financial information.

Caterpillar's latest financial results and outlook are also available via:

Telephone: 800-228-7717 (Inside the United States and Canada)

858-764-9492 (Outside the United States and Canada)

Internet:

http://www.caterpillar.com/en/investors.html

http://www.caterpillar.com/en/investors/quarterly-results.html (live broadcast/replays of quarterly conference call)

Caterpillar contact: Rachel Potts, 309-675-6892 (Office), 309-573-3444 (Mobile) or Potts_Rachel_A@cat.com

(more)

16

Caterpillar Inc.

Condensed Consolidated Statement of Results of Operations

(Unaudited)

(Dollars in millions except per share data)

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2017 | 2016 | 2017 | 2016 | ||||||||||||

Sales and revenues: | |||||||||||||||

Sales of Machinery, Energy & Transportation | $ | 10,639 | $ | 9,645 | $ | 19,769 | $ | 18,425 | |||||||

Revenues of Financial Products | 692 | 697 | 1,384 | 1,378 | |||||||||||

Total sales and revenues | 11,331 | 10,342 | 21,153 | 19,803 | |||||||||||

Operating costs: | |||||||||||||||

Cost of goods sold | 7,769 | 7,419 | 14,527 | 14,241 | |||||||||||

Selling, general and administrative expenses | 1,289 | 1,123 | 2,334 | 2,211 | |||||||||||

Research and development expenses | 453 | 468 | 871 | 976 | |||||||||||

Interest expense of Financial Products | 162 | 148 | 321 | 300 | |||||||||||

Other operating (income) expenses | 407 | 399 | 1,432 | 796 | |||||||||||

Total operating costs | 10,080 | 9,557 | 19,485 | 18,524 | |||||||||||

Operating profit | 1,251 | 785 | 1,668 | 1,279 | |||||||||||

Interest expense excluding Financial Products | 121 | 130 | 244 | 259 | |||||||||||

Other income (expense) | 29 | 84 | 24 | 84 | |||||||||||

Consolidated profit before taxes | 1,159 | 739 | 1,448 | 1,104 | |||||||||||

Provision (benefit) for income taxes | 361 | 184 | 451 | 276 | |||||||||||

Profit of consolidated companies | 798 | 555 | 997 | 828 | |||||||||||

Equity in profit (loss) of unconsolidated affiliated companies | 5 | (2 | ) | — | (3 | ) | |||||||||

Profit of consolidated and affiliated companies | 803 | 553 | 997 | 825 | |||||||||||

Less: Profit (loss) attributable to noncontrolling interests | 1 | 3 | 3 | 4 | |||||||||||

Profit 1 | $ | 802 | $ | 550 | $ | 994 | $ | 821 | |||||||

Profit per common share | $ | 1.36 | $ | 0.94 | $ | 1.69 | $ | 1.41 | |||||||

Profit per common share — diluted 2 | $ | 1.35 | $ | 0.93 | $ | 1.67 | $ | 1.40 | |||||||

Weighted-average common shares outstanding (millions) | |||||||||||||||

– Basic | 590.2 | 584.1 | 588.8 | 583.4 | |||||||||||

– Diluted 2 | 595.4 | 588.6 | 594.4 | 588.2 | |||||||||||

Cash dividends declared per common share | $ | 1.55 | $ | 1.54 | $ | 1.55 | $ | 1.54 | |||||||

1 | Profit attributable to common shareholders. |

2 | Diluted by assumed exercise of stock-based compensation awards using the treasury stock method. |

(more)

17

Caterpillar Inc.

Condensed Consolidated Statement of Financial Position

(Unaudited)

(Millions of dollars)

June 30, 2017 | December 31, 2016 | ||||||

Assets | |||||||

Current assets: | |||||||

Cash and short-term investments | $ | 10,232 | $ | 7,168 | |||

Receivables – trade and other | 6,675 | 5,981 | |||||

Receivables – finance | 8,920 | 8,522 | |||||

Prepaid expenses and other current assets | 1,776 | 1,682 | |||||

Inventories | 9,388 | 8,614 | |||||

Total current assets | 36,991 | 31,967 | |||||

Property, plant and equipment – net | 14,420 | 15,322 | |||||

Long-term receivables – trade and other | 940 | 1,029 | |||||

Long-term receivables – finance | 13,197 | 13,556 | |||||

Noncurrent deferred and refundable income taxes | 2,866 | 2,790 | |||||

Intangible assets | 2,232 | 2,349 | |||||

Goodwill | 6,142 | 6,020 | |||||

Other assets | 1,722 | 1,671 | |||||

Total assets | $ | 78,510 | $ | 74,704 | |||

Liabilities | |||||||

Current liabilities: | |||||||

Short-term borrowings: | |||||||

Machinery, Energy & Transportation | $ | 5 | $ | 209 | |||

Financial Products | 6,775 | 7,094 | |||||

Accounts payable | 5,778 | 4,614 | |||||

Accrued expenses | 3,211 | 3,003 | |||||

Accrued wages, salaries and employee benefits | 1,986 | 1,296 | |||||

Customer advances | 1,533 | 1,167 | |||||

Dividends payable | 461 | 452 | |||||

Other current liabilities | 1,787 | 1,635 | |||||

Long-term debt due within one year: | |||||||

Machinery, Energy & Transportation | 5 | 507 | |||||

Financial Products | 6,592 | 6,155 | |||||

Total current liabilities | 28,133 | 26,132 | |||||

Long-term debt due after one year: | |||||||

Machinery, Energy & Transportation | 8,815 | 8,436 | |||||

Financial Products | 15,000 | 14,382 | |||||

Liability for postemployment benefits | 9,248 | 9,357 | |||||

Other liabilities | 3,235 | 3,184 | |||||

Total liabilities | 64,431 | 61,491 | |||||

Shareholders’ equity | |||||||

Common stock | 5,316 | 5,277 | |||||

Treasury stock | (17,307 | ) | (17,478 | ) | |||

Profit employed in the business | 27,471 | 27,377 | |||||

Accumulated other comprehensive income (loss) | (1,471 | ) | (2,039 | ) | |||

Noncontrolling interests | 70 | 76 | |||||

Total shareholders’ equity | 14,079 | 13,213 | |||||

Total liabilities and shareholders’ equity | $ | 78,510 | $ | 74,704 | |||

(more)

18

Caterpillar Inc.

Condensed Consolidated Statement of Cash Flow

(Unaudited)

(Millions of dollars)

Six Months Ended June 30, | |||||||

2017 | 2016 | ||||||

Cash flow from operating activities: | |||||||

Profit of consolidated and affiliated companies | $ | 997 | $ | 825 | |||

Adjustments for non-cash items: | |||||||

Depreciation and amortization | 1,430 | 1,494 | |||||

Other | 487 | 368 | |||||

Changes in assets and liabilities, net of acquisitions and divestitures: | |||||||

Receivables – trade and other | (442 | ) | 573 | ||||

Inventories | (688 | ) | 305 | ||||

Accounts payable | 1,113 | 208 | |||||

Accrued expenses | 251 | 1 | |||||

Accrued wages, salaries and employee benefits | 641 | (743 | ) | ||||

Customer advances | 322 | 93 | |||||

Other assets – net | (280 | ) | (127 | ) | |||

Other liabilities – net | 90 | (193 | ) | ||||

Net cash provided by (used for) operating activities | 3,921 | 2,804 | |||||

Cash flow from investing activities: | |||||||

Capital expenditures – excluding equipment leased to others | (371 | ) | (580 | ) | |||

Expenditures for equipment leased to others | (753 | ) | (1,025 | ) | |||

Proceeds from disposals of leased assets and property, plant and equipment | 563 | 383 | |||||

Additions to finance receivables | (5,264 | ) | (4,643 | ) | |||

Collections of finance receivables | 5,508 | 4,466 | |||||

Proceeds from sale of finance receivables | 83 | 42 | |||||

Investments and acquisitions (net of cash acquired) | (21 | ) | (38 | ) | |||

Proceeds from sale of businesses and investments (net of cash sold) | 91 | — | |||||

Proceeds from sale of securities | 187 | 195 | |||||

Investments in securities | (207 | ) | (243 | ) | |||

Other – net | 5 | (14 | ) | ||||

Net cash provided by (used for) investing activities | (179 | ) | (1,457 | ) | |||

Cash flow from financing activities: | |||||||

Dividends paid | (906 | ) | (898 | ) | |||

Distribution to noncontrolling interests | (6 | ) | — | ||||

Common stock issued, including treasury shares reissued | 83 | (47 | ) | ||||

Proceeds from debt issued (original maturities greater than three months) | 4,868 | 2,841 | |||||

Payments on debt (original maturities greater than three months) | (4,225 | ) | (3,331 | ) | |||

Short-term borrowings – net (original maturities three months or less) | (505 | ) | 391 | ||||

Net cash provided by (used for) financing activities | (691 | ) | (1,044 | ) | |||

Effect of exchange rate changes on cash | 13 | 1 | |||||

Increase (decrease) in cash and short-term investments | 3,064 | 304 | |||||

Cash and short-term investments at beginning of period | 7,168 | 6,460 | |||||

Cash and short-term investments at end of period | $ | 10,232 | $ | 6,764 | |||

All short-term investments, which consist primarily of highly liquid investments with original maturities of three months or less, are considered to be cash equivalents. |

(more)

19

Caterpillar Inc.

Supplemental Data for Results of Operations

For the Three Months Ended June 30, 2017

(Unaudited)

(Millions of dollars)

Supplemental Consolidating Data | |||||||||||||||||

Consolidated | Machinery, Energy & Transportation 1 | Financial Products | Consolidating Adjustments | ||||||||||||||

Sales and revenues: | |||||||||||||||||

Sales of Machinery, Energy & Transportation | $ | 10,639 | $ | 10,639 | $ | — | $ | — | |||||||||

Revenues of Financial Products | 692 | — | 793 | (101 | ) | 2 | |||||||||||

Total sales and revenues | 11,331 | 10,639 | 793 | (101 | ) | ||||||||||||

Operating costs: | |||||||||||||||||

Cost of goods sold | 7,769 | 7,769 | — | — | |||||||||||||

Selling, general and administrative expenses | 1,289 | 1,154 | 139 | (4 | ) | 3 | |||||||||||

Research and development expenses | 453 | 453 | — | — | |||||||||||||

Interest expense of Financial Products | 162 | — | 167 | (5 | ) | 4 | |||||||||||

Other operating (income) expenses | 407 | 111 | 301 | (5 | ) | 3 | |||||||||||

Total operating costs | 10,080 | 9,487 | 607 | (14 | ) | ||||||||||||

Operating profit | 1,251 | 1,152 | 186 | (87 | ) | ||||||||||||

Interest expense excluding Financial Products | 121 | 146 | — | (25 | ) | 4 | |||||||||||

Other income (expense) | 29 | (35 | ) | 2 | 62 | 5 | |||||||||||

Consolidated profit before taxes | 1,159 | 971 | 188 | — | |||||||||||||

Provision (benefit) for income taxes | 361 | 303 | 58 | — | |||||||||||||

Profit of consolidated companies | 798 | 668 | 130 | — | |||||||||||||

Equity in profit (loss) of unconsolidated affiliated companies | 5 | 5 | — | — | |||||||||||||

Equity in profit of Financial Products’ subsidiaries | — | 129 | — | (129 | ) | 6 | |||||||||||

Profit of consolidated and affiliated companies | 803 | 802 | 130 | (129 | ) | ||||||||||||

Less: Profit (loss) attributable to noncontrolling interests | 1 | — | 1 | — | |||||||||||||

Profit 7 | $ | 802 | $ | 802 | $ | 129 | $ | (129 | ) | ||||||||

1 | Represents Caterpillar Inc. and its subsidiaries with Financial Products accounted for on the equity basis. |

2 | Elimination of Financial Products’ revenues earned from Machinery, Energy & Transportation. |

3 | Elimination of net expenses recorded by Machinery, Energy & Transportation paid to Financial Products. |

4 | Elimination of interest expense recorded between Financial Products and Machinery, Energy & Transportation. |

5 | Elimination of discount recorded by Machinery, Energy & Transportation on receivables sold to Financial Products and of interest earned between Machinery, Energy & Transportation and Financial Products. |

6 | Elimination of Financial Products’ profit due to equity method of accounting. |

7 | Profit attributable to common shareholders. |

(more)

20

Caterpillar Inc.

Supplemental Data for Results of Operations

For the Three Months Ended June 30, 2016

(Unaudited)

(Millions of dollars)

Supplemental Consolidating Data | |||||||||||||||||

Consolidated | Machinery, Energy & Transportation 1 | Financial Products | Consolidating Adjustments | ||||||||||||||

Sales and revenues: | |||||||||||||||||

Sales of Machinery, Energy & Transportation | $ | 9,645 | $ | 9,645 | $ | — | $ | — | |||||||||

Revenues of Financial Products | 697 | — | 778 | (81 | ) | 2 | |||||||||||

Total sales and revenues | 10,342 | 9,645 | 778 | (81 | ) | ||||||||||||

Operating costs: | |||||||||||||||||

Cost of goods sold | 7,419 | 7,419 | — | — | |||||||||||||

Selling, general and administrative expenses | 1,123 | 981 | 147 | (5 | ) | 3 | |||||||||||

Research and development expenses | 468 | 468 | — | — | |||||||||||||

Interest expense of Financial Products | 148 | — | 152 | (4 | ) | 4 | |||||||||||

Other operating (income) expenses | 399 | 99 | 308 | (8 | ) | 3 | |||||||||||

Total operating costs | 9,557 | 8,967 | 607 | (17 | ) | ||||||||||||

Operating profit | 785 | 678 | 171 | (64 | ) | ||||||||||||

Interest expense excluding Financial Products | 130 | 143 | — | (13 | ) | 4 | |||||||||||

Other income (expense) | 84 | 5 | 28 | 51 | 5 | ||||||||||||

Consolidated profit before taxes | 739 | 540 | 199 | — | |||||||||||||

Provision (benefit) for income taxes | 184 | 122 | 62 | — | |||||||||||||

Profit of consolidated companies | 555 | 418 | 137 | — | |||||||||||||

Equity in profit (loss) of unconsolidated affiliated companies | (2 | ) | (2 | ) | — | — | |||||||||||

Equity in profit of Financial Products’ subsidiaries | — | 135 | — | (135 | ) | 6 | |||||||||||

Profit of consolidated and affiliated companies | 553 | 551 | 137 | (135 | ) | ||||||||||||

Less: Profit (loss) attributable to noncontrolling interests | 3 | 1 | 2 | — | |||||||||||||

Profit 7 | $ | 550 | $ | 550 | $ | 135 | $ | (135 | ) | ||||||||

1 | Represents Caterpillar Inc. and its subsidiaries with Financial Products accounted for on the equity basis. |

2 | Elimination of Financial Products’ revenues earned from Machinery, Energy & Transportation. |

3 | Elimination of net expenses recorded by Machinery, Energy & Transportation paid to Financial Products. |

4 | Elimination of interest expense recorded between Financial Products and Machinery, Energy & Transportation. |

5 | Elimination of discount recorded by Machinery, Energy & Transportation on receivables sold to Financial Products and of interest earned between Machinery, Energy & Transportation and Financial Products. |

6 | Elimination of Financial Products’ profit due to equity method of accounting. |

7 | Profit attributable to common shareholders. |

(more)

21

Caterpillar Inc.

Supplemental Data for Results of Operations

For the Six Months Ended June 30, 2017

(Unaudited)

(Millions of dollars)

Supplemental Consolidating Data | |||||||||||||||||

Consolidated | Machinery, Energy & Transportation 1 | Financial Products | Consolidating Adjustments | ||||||||||||||

Sales and revenues: | |||||||||||||||||

Sales of Machinery, Energy & Transportation | $ | 19,769 | $ | 19,769 | $ | — | $ | — | |||||||||

Revenues of Financial Products | 1,384 | — | 1,570 | (186 | ) | 2 | |||||||||||

Total sales and revenues | 21,153 | 19,769 | 1,570 | (186 | ) | ||||||||||||

Operating costs: | |||||||||||||||||

Cost of goods sold | 14,527 | 14,527 | — | — | |||||||||||||

Selling, general and administrative expenses | 2,334 | 2,078 | 265 | (9 | ) | 3 | |||||||||||

Research and development expenses | 871 | 871 | — | — | |||||||||||||

Interest expense of Financial Products | 321 | — | 330 | (9 | ) | 4 | |||||||||||

Other operating (income) expenses | 1,432 | 839 | 603 | (10 | ) | 3 | |||||||||||

Total operating costs | 19,485 | 18,315 | 1,198 | (28 | ) | ||||||||||||

Operating profit | 1,668 | 1,454 | 372 | (158 | ) | ||||||||||||

Interest expense excluding Financial Products | 244 | 290 | — | (46 | ) | 4 | |||||||||||

Other income (expense) | 24 | (88 | ) | — | 112 | 5 | |||||||||||

Consolidated profit before taxes | 1,448 | 1,076 | 372 | — | |||||||||||||

Provision (benefit) for income taxes | 451 | 337 | 114 | — | |||||||||||||

Profit of consolidated companies | 997 | 739 | 258 | — | |||||||||||||

Equity in profit (loss) of unconsolidated affiliated companies | — | — | — | — | |||||||||||||

Equity in profit of Financial Products’ subsidiaries | — | 255 | — | (255 | ) | 6 | |||||||||||

Profit of consolidated and affiliated companies | 997 | 994 | 258 | (255 | ) | ||||||||||||

Less: Profit (loss) attributable to noncontrolling interests | 3 | — | 3 | — | |||||||||||||

Profit 7 | $ | 994 | $ | 994 | $ | 255 | $ | (255 | ) | ||||||||

1 | Represents Caterpillar Inc. and its subsidiaries with Financial Products accounted for on the equity basis. |

2 | Elimination of Financial Products’ revenues earned from Machinery, Energy & Transportation. |

3 | Elimination of net expenses recorded by Machinery, Energy & Transportation paid to Financial Products. |

4 | Elimination of interest expense recorded between Financial Products and Machinery, Energy & Transportation. |

5 | Elimination of discount recorded by Machinery, Energy & Transportation on receivables sold to Financial Products and of interest earned between Machinery, Energy & Transportation and Financial Products. |

6 | Elimination of Financial Products’ profit due to equity method of accounting. |

7 | Profit attributable to common shareholders. |

(more)

22

Caterpillar Inc.

Supplemental Data for Results of Operations

For the Six Months Ended June 30, 2016

(Unaudited)

(Millions of dollars)

Supplemental Consolidating Data | |||||||||||||||||

Consolidated | Machinery, Energy & Transportation 1 | Financial Products | Consolidating Adjustments | ||||||||||||||

Sales and revenues: | |||||||||||||||||

Sales of Machinery, Energy & Transportation | $ | 18,425 | $ | 18,425 | $ | — | $ | — | |||||||||

Revenues of Financial Products | 1,378 | — | 1,537 | (159 | ) | 2 | |||||||||||

Total sales and revenues | 19,803 | 18,425 | 1,537 | (159 | ) | ||||||||||||

Operating costs: | |||||||||||||||||

Cost of goods sold | 14,241 | 14,241 | — | — | |||||||||||||

Selling, general and administrative expenses | 2,211 | 1,936 | 286 | (11 | ) | 3 | |||||||||||

Research and development expenses | 976 | 976 | — | — | |||||||||||||

Interest expense of Financial Products | 300 | — | 307 | (7 | ) | 4 | |||||||||||

Other operating (income) expenses | 796 | 204 | 606 | (14 | ) | 3 | |||||||||||

Total operating costs | 18,524 | 17,357 | 1,199 | (32 | ) | ||||||||||||

Operating profit | 1,279 | 1,068 | 338 | (127 | ) | ||||||||||||

Interest expense excluding Financial Products | 259 | 283 | — | (24 | ) | 4 | |||||||||||

Other income (expense) | 84 | (47 | ) | 28 | 103 | 5 | |||||||||||

Consolidated profit before taxes | 1,104 | 738 | 366 | — | |||||||||||||

Provision (benefit) for income taxes | 276 | 162 | 114 | — | |||||||||||||

Profit of consolidated companies | 828 | 576 | 252 | — | |||||||||||||

Equity in profit (loss) of unconsolidated affiliated companies | (3 | ) | (3 | ) | — | — | |||||||||||

Equity in profit of Financial Products’ subsidiaries | — | 249 | — | (249 | ) | 6 | |||||||||||

Profit of consolidated and affiliated companies | 825 | 822 | 252 | (249 | ) | ||||||||||||

Less: Profit (loss) attributable to noncontrolling interests | 4 | 1 | 3 | — | |||||||||||||

Profit 7 | $ | 821 | $ | 821 | $ | 249 | $ | (249 | ) | ||||||||

1 | Represents Caterpillar Inc. and its subsidiaries with Financial Products accounted for on the equity basis. |

2 | Elimination of Financial Products’ revenues earned from Machinery, Energy & Transportation. |

3 | Elimination of net expenses recorded by Machinery, Energy & Transportation paid to Financial Products. |

4 | Elimination of interest expense recorded between Financial Products and Machinery, Energy & Transportation. |

5 | Elimination of discount recorded by Machinery, Energy & Transportation on receivables sold to Financial Products and of interest earned between Machinery, Energy & Transportation and Financial Products. |

6 | Elimination of Financial Products’ profit due to equity method of accounting. |

7 | Profit attributable to common shareholders. |

(more)

23

Caterpillar Inc.

Supplemental Data for Cash Flow

For the Six Months Ended June 30, 2017

(Unaudited)

(Millions of dollars)

Supplemental Consolidating Data | ||||||||||||||||

Consolidated | Machinery, Energy & Transportation 1 | Financial Products | Consolidating Adjustments | |||||||||||||

Cash flow from operating activities: | ||||||||||||||||

Profit of consolidated and affiliated companies | $ | 997 | $ | 994 | $ | 258 | $ | (255 | ) | 2 | ||||||

Adjustments for non-cash items: | ||||||||||||||||

Depreciation and amortization | 1,430 | 998 | 432 | — | ||||||||||||

Undistributed profit of Financial Products | — | (255 | ) | — | 255 | 3 | ||||||||||

Other | 487 | 453 | (87 | ) | 121 | 4 | ||||||||||

Changes in assets and liabilities, net of acquisitions and divestitures: | ||||||||||||||||

Receivables - trade and other | (442 | ) | (54 | ) | 63 | (451 | ) | 4, 5 | ||||||||

Inventories | (688 | ) | (688 | ) | — | — | ||||||||||

Accounts payable | 1,113 | 1,145 | (52 | ) | 20 | 4 | ||||||||||

Accrued expenses | 251 | 234 | 17 | — | ||||||||||||

Accrued wages, salaries and employee benefits | 641 | 634 | 7 | — | ||||||||||||

Customer advances | 322 | 322 | — | — | ||||||||||||

Other assets – net | (280 | ) | (152 | ) | (48 | ) | (80 | ) | 4 | |||||||

Other liabilities – net | 90 | (78 | ) | 88 | 80 | 4 | ||||||||||

Net cash provided by (used for) operating activities | 3,921 | 3,553 | 678 | (310 | ) | |||||||||||

Cash flow from investing activities: | ||||||||||||||||

Capital expenditures - excluding equipment leased to others | (371 | ) | (367 | ) | (4 | ) | — | |||||||||

Expenditures for equipment leased to others | (753 | ) | (12 | ) | (749 | ) | 8 | 4 | ||||||||

Proceeds from disposals of leased assets and property, plant and equipment | 563 | 87 | 481 | (5 | ) | 4 | ||||||||||

Additions to finance receivables | (5,264 | ) | — | (6,240 | ) | 976 | 5 | |||||||||

Collections of finance receivables | 5,508 | — | 6,602 | (1,094 | ) | 5 | ||||||||||

Net intercompany purchased receivables | — | — | (425 | ) | 425 | 5 | ||||||||||

Proceeds from sale of finance receivables | 83 | — | 83 | — | ||||||||||||

Net intercompany borrowings | — | 44 | (1,500 | ) | 1,456 | 6 | ||||||||||

Investments and acquisitions (net of cash acquired) | (21 | ) | (21 | ) | — | — | ||||||||||

Proceeds from sale of businesses and investments (net of cash sold) | 91 | 91 | — | — | ||||||||||||

Proceeds from sale of securities | 187 | 9 | 178 | — | ||||||||||||

Investments in securities | (207 | ) | (11 | ) | (196 | ) | — | |||||||||

Other – net | 5 | (25 | ) | 30 | — | |||||||||||

Net cash provided by (used for) investing activities | (179 | ) | (205 | ) | (1,740 | ) | 1,766 | |||||||||

Cash flow from financing activities: | ||||||||||||||||

Dividends paid | (906 | ) | (906 | ) | — | — | ||||||||||

Distribution to noncontrolling interests | (6 | ) | (6 | ) | — | — | ||||||||||

Common stock issued, including treasury shares reissued | 83 | 83 | — | — | ||||||||||||

Net intercompany borrowings | — | 1,500 | (44 | ) | (1,456 | ) | 6 | |||||||||

Proceeds from debt issued (original maturities greater than three months) | 4,868 | 361 | 4,507 | — | ||||||||||||

Payments on debt (original maturities greater than three months) | (4,225 | ) | (505 | ) | (3,720 | ) | — | |||||||||

Short-term borrowings – net (original maturities three months or less) | (505 | ) | (200 | ) | (305 | ) | — | |||||||||

Net cash provided by (used for) financing activities | (691 | ) | 327 | 438 | (1,456 | ) | ||||||||||

Effect of exchange rate changes on cash | 13 | (6 | ) | 19 | — | |||||||||||

Increase (decrease) in cash and short-term investments | 3,064 | 3,669 | (605 | ) | — | |||||||||||

Cash and short-term investments at beginning of period | 7,168 | 5,257 | 1,911 | — | ||||||||||||

Cash and short-term investments at end of period | $ | 10,232 | $ | 8,926 | $ | 1,306 | $ | — | ||||||||

1 | Represents Caterpillar Inc. and its subsidiaries with Financial Products accounted for on the equity basis. |

2 | Elimination of Financial Products’ profit after tax due to equity method of accounting. |

3 | Elimination of non-cash adjustment for the undistributed earnings from Financial Products. |

4 | Elimination of non-cash adjustments and changes in assets and liabilities related to consolidated reporting. |

5 | Reclassification of Financial Products’ cash flow activity from investing to operating for receivables that arose from the sale of inventory. |

6 | Elimination of net proceeds and payments to/from Machinery, Energy & Transportation and Financial Products. |

(more)

24

Caterpillar Inc.

Supplemental Data for Cash Flow

For the Six Months Ended June 30, 2016

(Unaudited)

(Millions of dollars)

Supplemental Consolidating Data | ||||||||||||||||