Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - Noble Midstream Partners LP | d417597dex231.htm |

| EX-21.1 - EX-21.1 - Noble Midstream Partners LP | d417597dex211.htm |

| EX-8.1 - EX-8.1 - Noble Midstream Partners LP | d417597dex81.htm |

| EX-5.1 - EX-5.1 - Noble Midstream Partners LP | d417597dex51.htm |

Table of Contents

As filed with the Securities and Exchange Commission on July 14, 2017

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Noble Midstream Partners LP

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 4932 | 47-3011449 | ||

| (State or Other Jurisdiction of | (Primary Standard Industrial | (IRS Employer | ||

| Incorporation or Organization) | Classification Code Number) | Identification No.) |

1001 Noble Energy Way

Houston, Texas 77070

(281) 872-3100

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

John F. Bookout, IV

Chief Financial Officer

1001 Noble Energy Way

Houston, Texas 77070

(281) 872-3100

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

G. Michael O’Leary

George J. Vlahakos

Andrews Kurth Kenyon LLP

600 Travis, Suite 4200

Houston, Texas 77002

(713) 220-4200

Approximate date of commencement of proposed sale to the public:

From time to time after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ (Do not check if a smaller reporting company) | Smaller reporting company | ☐ | |||

| Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities to be Registered | Amount to be Registered(1) |

Proposed Maximum Offering Price per Unit(2)(3) |

Proposed Maximum Aggregate Offering Price(3) |

Amount of Registration Fee | ||||

| Common units representing limited partner interests |

3,525,000 | $45.47 | $160,281,750 | $18,577(4) | ||||

|

| ||||||||

|

| ||||||||

| (1) | Pursuant to Rule 416(a) under the Securities Act of 1933, as amended (the “Securities Act”), the number of common units representing limited partner interests (“common units”) in Noble Midstream Partners LP (the “Partnership”) being registered on behalf of the selling unitholders named in this prospectus shall be adjusted to include any additional common units that may become issuable as a result of any unit distribution, split, combination or similar transaction. |

| (2) | The proposed maximum offering price per common unit will be determined from time to time in connection with, and at the time of, the sale by the holder of such unit. |

| (3) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(c) under the Securities Act, based on the average high and low reported sales prices of the common units on the New York Stock Exchange on July 10, 2017. |

| (4) | Calculated in accordance with Rule 457(o) under the Securities Act. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission becomes effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated July 14, 2017

PROSPECTUS

Noble Midstream Partners LP

3,525,000 Common Units

Representing Limited Partner Interests

This prospectus covers the offer and sale of 3,525,000 common units representing limited partner interests of Noble Midstream Partners LP by the selling unitholders named in this prospectus or in any supplement to this prospectus or any partners, pledgees, donees, transferees or other successors in interest that receive the common units offered by this prospectus from any such selling unitholder (collectively, the “selling unitholders”).

We will not receive any proceeds from the sale of common units owned by the selling unitholders. For a more detailed discussion of the selling unitholders, please read “Selling Unitholders.”

The selling unitholders may offer and sell the common units for their own account from time to time in accordance with the provisions set forth under “Plan of Distribution.” The selling unitholders may offer and sell the common units to or through one or more underwriters, dealers and agents, who may receive compensation in the form of discounts, concessions or commissions, or directly to purchasers, on a continuous or delayed basis. The selling unitholders may offer and sell the common units at various times in amounts, at prices and on terms to be determined by market conditions and other factors at the time of such offerings.

Our common units are listed on the New York Stock Exchange under the symbol “NBLX.” The last reported trading price of our common units on the New York Stock Exchange on July 12, 2017 was $45.10 per unit.

Investing in our common units involves risks. Please read “Risk Factors” beginning on page 7 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Prospectus dated , 2017

Table of Contents

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 5 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 12 | ||||

| 14 | ||||

| PROVISIONS OF OUR PARTNERSHIP AGREEMENT RELATING TO CASH DISTRIBUTIONS |

16 | |||

| 28 | ||||

| 41 | ||||

| 58 | ||||

| 58 |

You should rely only on the information contained or incorporated by reference in this prospectus or any prospectus supplement. Neither we nor any selling unitholder has authorized anyone to provide you with information different from that contained or incorporated by reference in this prospectus or any prospectus supplement. Neither we nor any selling unitholder take responsibility for, nor can we or any selling unitholder provide assurance as to the reliability of, any other information that others may give you. We are not, and the selling unitholders are not, making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of the common units. The information contained in the documents incorporated by reference in this prospectus is accurate only as of the respective dates of those documents. Our business, financial condition, results of operations and prospects may have changed since those dates.

i

Table of Contents

This prospectus is part of a registration statement on Form S-1 that we have filed with the Securities and Exchange Commission (the “SEC”) under the Securities Act of 1933, as amended (the “Securities Act”). This prospectus provides you with a general description of Noble Midstream Partners LP and the common units that are registered hereunder that may be offered by the selling unitholders. This prospectus does not contain all of the information set forth in the registration statement, or the exhibits that are a part of the registration statement, parts of which are omitted as permitted by the rules and regulations of the SEC.

Additional information, including our financial statements and the notes thereto, is incorporated in this prospectus by reference to our reports filed with the SEC. Please read “Where You Can Find More Information” below. You are urged to read this prospectus carefully, including “Risk Factors,” “Cautionary Statement Regarding Forward-Looking Statements,” and the documents incorporated by reference in their entirety before investing in our securities.

Unless the context requires otherwise or unless otherwise noted, all references in this prospectus to “the Partnership,” “we,” “our,” “us” or like terms refer to Noble Midstream Partners LP and its subsidiaries; “Noble” refers to Noble Energy, Inc.; and “our general partner” refers to Noble Midstream GP LLC.

1

Table of Contents

WHERE YOU CAN FIND MORE INFORMATION

We file annual, quarterly and current reports and other information with the SEC. You may read and copy any document we file at the SEC’s public reference room located at 100 F Street, N.E., Washington, DC 20549. Please call the SEC at 1-800-SEC-0330 for further information on the operation of the public reference room. Our SEC filings are also available to the public at the SEC’s web site at www.sec.gov. You may also access the information we file electronically with the SEC through our website at www.nblmidstream.com. We have not incorporated by reference into this prospectus the information included on, or linked from, our website (other than to the extent specified elsewhere herein), and you should not consider it to be a part of this prospectus. You may also inspect reports, proxy statements and other information about Noble Energy, Inc. at the offices of the New York Stock Exchange (“NYSE”), 20 Broad Street, New York, NY 10005.

We “incorporate by reference” information into this prospectus, which means that we disclose important information to you by referring you to another document filed separately with the SEC. The information incorporated by reference is deemed to be part of this prospectus, except for any information superseded by information contained expressly in this prospectus. You should not assume that the information in this prospectus is current as of any date other than the date on the cover page of this prospectus.

We incorporate by reference the documents listed below:

| • | our Annual Report on Form 10-K for the fiscal year ended December 31, 2016; |

| • | our Quarterly Report on Form 10-Q for the quarterly period ended March 31, 2017; |

| • | our Current Reports on Form 8-K filed on January 26, 2017, April 7, 2017, June 7, 2017, June 26, 2017 and July 14, 2017; and |

| • | the description of our common units included in our Form 8-A (File No. 001-37640), filed with the SEC on November 17, 2015. |

You can obtain copies of any of these documents without charge upon written or oral request by requesting them in writing or by telephone at:

Noble Midstream Partners LP 1001 Noble Energy Way

Houston, Texas 77070

(281) 872-3100

2

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Some of the information included in or incorporated by reference in this prospectus may contain forward-looking statements. Forward-looking statements are predictive in nature, depend upon or refer to future events or conditions or include the words “believe,” “expect,” “anticipate,” “intend,” “estimate” and other expressions that are predictions of or indicate future events and trends and that do not relate to historical matters. Our forward-looking statements may include statements about our business strategy, our industry, our future profitability, our expected capital expenditures and the impact of such expenditures on our performance, the costs of being a publicly traded partnership and our capital programs.

A forward-looking statement may include a statement of the assumptions or bases underlying the forward-looking statement. While we believe that we have chosen these assumptions or bases in good faith and that they are reasonable, you are cautioned not to place undue reliance on any forward-looking statements. You should also understand that it is not possible to predict or identify all such factors and should not consider the following list to be a complete statement of all potential risks and uncertainties. Factors that could cause our actual results to differ materially from the results contemplated by such forward-looking statements include:

| • | the ability of Noble to meet its drilling and development plans; |

| • | changes in general economic conditions; |

| • | competitive conditions in our industry; |

| • | actions taken by third-party operators, gatherers, processors and transporters; |

| • | the demand for crude oil and natural gas gathering and processing services; |

| • | our ability to successfully implement our business plan; |

| • | our ability to complete internal growth projects on time and on budget; |

| • | the price and availability of debt and equity financing; |

| • | the availability and price of crude oil and natural gas to the consumer compared to the price of alternative and competing fuels; |

| • | competition from the same and alternative energy sources; |

| • | energy efficiency and technology trends; |

| • | operating hazards and other risks incidental to our midstream services; |

| • | natural disasters, weather-related delays, casualty losses and other matters beyond our control; |

| • | interest rates; |

| • | labor relations; |

| • | defaults by Noble under our gathering and processing agreements; |

| • | changes in availability and cost of capital; |

| • | changes in our tax status; |

| • | the effect of existing and future laws and government regulations; and |

| • | the effects of future litigation. |

We caution you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond our control, incident to the gathering and compression business. These risks include, but are not limited to, commodity price volatility, inflation, environmental risks, drilling and completion and other operating risks, regulatory changes, the uncertainty

3

Table of Contents

inherent in projecting future rates of production, cash flow and access to capital, the timing of development expenditures, and the other risks described under “Risk Factors” in this prospectus and in our Annual Report on Form 10-K for the year ended December 31, 2016 and our other reports filed with the SEC.

Should one or more of the risks or uncertainties described in this prospectus or in any document incorporated by reference herein occur, or should underlying assumptions prove incorrect, our actual results and plans could differ materially from those expressed in any forward-looking statements.

All forward-looking statements, expressed or implied, included or incorporated by reference in this prospectus are expressly qualified in their entirety by this cautionary statement.

Except as otherwise required by applicable law, we disclaim any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this prospectus.

4

Table of Contents

This summary provides a brief overview of information contained elsewhere in this prospectus and the documents we incorporate by reference. It does not contain all of the information you should consider before making an investment decision. You should read this entire prospectus and the documents incorporated by reference herein.

Noble Midstream Partners LP

Overview

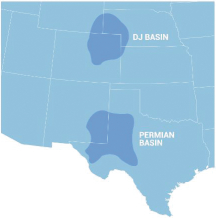

We are a growth-oriented Delaware master limited partnership formed in December 2014 by our parent, Noble, to own, operate, develop and acquire a wide range of domestic midstream infrastructure assets. We currently provide crude oil, natural gas, and water-related midstream services for Noble and third party customers through long-term, fixed-fee contracts. Our current areas of focus are in the Denver-Julesburg (DJ) Basin in Colorado and the Delaware Basin in Texas, where additional midstream assets are currently under construction. The locations of our current areas of focus are shown in the map below:

Noble intends for us to become its primary vehicle for midstream operations in the onshore United States outside of the Marcellus Shale in the northeastern U.S. We have acreage dedications spanning approximately 300,000 acres in the DJ Basin (with over 265,000 dedicated acres from Noble and the remaining dedicated acres from a third party) and approximately 110,000 acres in the Delaware Basin for which we are currently providing, or intend to provide, crude oil, natural gas, and water-related midstream services under long-term, fixed fee contracts.

Risk Factors

An investment in our common units involves risks associated with our business, our partnership structure and the tax characteristics of our common units. Because of our relationship with Noble, adverse developments or announcements concerning Noble could materially adversely affect our business. Please read “Risk Factors” and “Cautionary Statement Regarding Forward-Looking Statements.”

Partnership Information

Our principal executive offices are located at 1001 Noble Energy Way, Houston, Texas 77070, and our telephone number is (281) 872-3100. Our website is located at www.nblmidstream.com.

5

Table of Contents

The Offering

| Common units offered by the selling unitholders |

3,525,000 common units. |

| Units outstanding prior to and after giving effect to this offering |

20,032,586 common units and 15,902,584 subordinated units, for a total of 35,935,170 limited partner units. |

| Use of proceeds |

We will not receive any proceeds from the sale of common units by the selling unitholders. See “Use of Proceeds.” |

| Exchange listing |

Our common units are listed on the New York Stock Exchange (the “NYSE”) under the symbol “NBLX.” |

6

Table of Contents

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. You should carefully consider those risk factors included in our most recent Annual Report on Form 10-K for the year ended December 31, 2016, which are incorporated herein by reference, and those risk factors set forth in any prospectus supplement, together with all of the other information included in this prospectus, any prospectus supplement and the documents we incorporate herein or therein by reference, including the matters addressed under “Cautionary Statement Regarding Forward-Looking Statements,” in evaluating an investment in our common units.

7

Table of Contents

All of the common units covered by this prospectus are being sold by the selling unitholders. See “Selling Unitholders.” We will not receive any proceeds from these sales of our common units.

8

Table of Contents

This prospectus covers the offering for resale of up to an aggregate of 3,525,000 common units that may be offered and sold from time to time by the selling unitholders identified below under this prospectus, subject to any appropriate adjustment as a result of any unit subdivision, split, combination or other reclassification of our common units. The selling unitholders identified below may currently hold or acquire at any time common units in addition to those registered hereby. The selling unitholders acquired the common units pursuant to a common unit purchase agreement with us dated June 20, 2017. On June 26, 2017, we entered into a registration rights agreement with the selling unitholders, which obligated us to prepare and file a registration statement to permit the resale of certain common units held by the selling unitholders from time to time as permitted by Rule 415 promulgated under the Securities Act of 1933, as amended (the “Securities Act”). We are registering the common units described in this prospectus pursuant to this agreement. In addition, the selling unitholders identified below may sell, transfer or otherwise dispose of some or all of their common units in privately negotiated transactions exempt from or not subject to the registration requirements of the Securities Act. Accordingly, we cannot give an estimate as to the number of common units that will be held by the selling unitholders upon completion or termination of this offering.

Information concerning the selling unitholders may change from time to time, including by addition of additional selling unitholders, and, if necessary, we will amend or supplement this prospectus accordingly. To our knowledge, none of the selling unitholders has, or has had within the past three years, any position, office or other material relationship with us or any of our predecessors or affiliates, other than its ownership of common units.

We have prepared the table, the paragraph immediately following this paragraph, and the related notes based on information supplied to us by the selling unitholders on or prior to July 5, 2017. We have not sought to verify such information. Additionally, some or all of the selling unitholders may have sold or transferred some or all of the common units listed below in exempt or non-exempt transactions since the date on which the information was provided to us. Other information about the selling unitholders may change over time.

Certain selling unitholders are affiliates of broker-dealers (but are not themselves broker-dealers). Each of these broker-dealer affiliates purchased the securities identified in the table as beneficially owned by it in the ordinary course of business and, at the time of that purchase, had no agreements or understandings, directly or indirectly, with any person to distribute those securities. These broker-dealer affiliates did not receive the securities to be sold in the offering as underwriting compensation.

The selling unitholders, or their partners, pledgees, donees, transferees or other successors in interest that receive the common units offered by this prospectus (each also a selling unitholder for purposes of this prospectus), may sell up to all of the common units shown in the table below under the heading “Offered Hereby” pursuant to this prospectus in one or more transactions from time to time as described below under “Plan of Distribution.” However, the selling unitholders are not obligated to sell any of the common units offered by this prospectus.

| Selling Unitholder |

Beneficially Owned Prior to the Offering |

Offered Hereby |

Beneficially Owned After the Offering* |

As a Percent of Total Outstanding After the Offering |

||||||||||||

| Fidelity Advisor Series I: Fidelity Advisor Small Cap Fund (1) |

647,933 | 252,067 | 395,866 | 1.10 | % | |||||||||||

| Fidelity Advisor Series I: Fidelity Advisor Series Small Cap Fund (1) |

112,700 | 49,623 | 63,077 | * | * | |||||||||||

| VARIABLE INSURANCE PRODUCTS FUND IV: Energy Portfolio (1) |

49,400 | 14,739 | 34,661 | * | * | |||||||||||

| FIDELITY CENTRAL INVESTMENT PORTFOLIOS LLC: Fidelity Energy Central Fund (1) |

146,392 | 45,454 | 100,938 | * | * | |||||||||||

9

Table of Contents

| Selling Unitholder |

Beneficially Owned Prior to the Offering |

Offered Hereby |

Beneficially Owned After the Offering* |

As a Percent of Total Outstanding After the Offering |

||||||||||||

| FIDELITY SELECT PORTFOLIOS: Energy Portfolio (1) |

324,127 | 101,027 | 223,100 | * | * | |||||||||||

| FIDELITY ADVISOR SERIES VII: Fidelity Advisor Energy Fund (1) |

160,787 | 48,372 | 112,415 | * | * | |||||||||||

| FIDELITY SELECT PORTFOLIOS: Natural Resources Portfolio (1) |

131,937 | 43,718 | 88,219 | * | * | |||||||||||

| Goldman Sachs MLP Energy Investment Fund (2) |

985,764 | 285,000 | 700,764 | 1.95 | % | |||||||||||

| TPH Energy Infrastructure Master Fund, LP (3) |

70,513 | 56,933 | 13,580 | * | * | |||||||||||

| TPH MLP Fund, LP (3) |

16,946 | 10,328 | 6,618 | * | * | |||||||||||

| The Board of Regents of the University of Texas System (4) |

342,236 | 227,739 | 114,497 | * | * | |||||||||||

| HITE Hedge LP (5) |

194,250 | 194,250 | — | * | * | |||||||||||

| HITE MLP Advantage LP (5) |

66,600 | 66,600 | — | * | * | |||||||||||

| HITE MLP LP (5) |

133,200 | 133,200 | — | * | * | |||||||||||

| HITE Hedge QP LP (5) |

160,950 | 160,950 | — | * | * | |||||||||||

| Kayne Select Midstream Recovery Fund, L.P. (6) |

18,333 | 18,333 | — | * | * | |||||||||||

| Kayne Anderson Midstream Institutional Fund, L.P. (6) |

314,689 | 48,889 | 265,800 | * | * | |||||||||||

| Orange County Employees Retirement System (6) |

38,133 | 18,333 | 19,800 | * | * | |||||||||||

| Kaiser Foundation Hospitals (6) |

63,067 | 36,667 | 26,400 | * | * | |||||||||||

| Massachusetts Mutual Life Insurance Company (7) |

183,334 | 183,334 | — | * | * | |||||||||||

| MGMP, LP (7) |

61,111 | 61,111 | — | * | * | |||||||||||

| Ascension Alpha Fund, LLC (7) |

115,000 | 110,000 | 5,000 | * | * | |||||||||||

| Ascension Health Master Pension Trust (7) |

76,633 | 73,333 | 3,300 | * | * | |||||||||||

| MTP Energy Master Fund LTD (8) |

245,455 | 245,455 | — | * | * | |||||||||||

| FS Energy Total Return Fund (9) |

24,545 | 24,545 | — | * | * | |||||||||||

| Salient MLP Fund, L.P. (10) |

127,439 | 127,439 | — | * | * | |||||||||||

| Salient MLP Total Return Fund, L.P. (10) |

147,561 | 147,561 | — | * | * | |||||||||||

| Tortoise Direct Opportunities Fund, LP (11) |

504,919 | 504,919 | — | * | * | |||||||||||

| Tortoise Select Opportunity Fund |

14,687 | 14,687 | — | * | * | |||||||||||

| Tortoise MLP & Pipeline Fund |

364,603 | 172,253 | 192,350 | * | * | |||||||||||

| Texas Mutual Insurance Company (12) |

66,262 | 47,761 | 18,501 | * | * | |||||||||||

| Tortoise VIP MLP & Pipeline Portfolio |

692 | 380 | 312 | * | * | |||||||||||

| * | Assumes each selling unitholder sells all of the common units shown under “Offered Hereby.” |

| ** | Represents less than 1%. |

| (1) | These accounts are managed by direct or indirect subsidiaries of FMR LLC. Abigail P. Johnson is a Director, the Vice Chairman, the Chief Executive Officer and the President of FMR LLC. |

Members of the Johnson family, including Abigail P. Johnson, are the predominant owners, directly or through trusts, of Series B voting common shares of FMR LLC, representing 49% of the voting power of FMR LLC. The Johnson family group and all other Series B shareholders have entered into a shareholders’ voting agreement under which all Series B voting common shares will be voted in accordance with the majority vote of Series B voting common shares. Accordingly, through their ownership of voting common shares and the execution of the shareholders’ voting agreement, members of the Johnson family may be deemed, under the Investment Company Act of 1940, to form a controlling group with respect to FMR LLC.

Neither FMR LLC nor Abigail P. Johnson has the sole power to vote or direct the voting of the common units owned directly by the various investment companies registered under the Investment Company Act (“Fidelity Funds”) advised by Fidelity Management & Research Company (“FMR Co”), a wholly owned subsidiary of FMR LLC, which power resides with the Fidelity Funds’ Boards of Trustees. Fidelity Management & Research Company carries out the voting of the common units under written guidelines established by the Fidelity Funds’ Boards of Trustees.

| (2) | Goldman Sachs Asset Management (“GSAM”) is the investment manager of the selling unitholder. GSAM exercises sole voting and investment power over the common units offered hereby, subject to the oversight of the trustees of the fund. GSAM is a wholly-owned subsidiary of Goldman Sachs Group, Inc. (“GS Group”), a leading global investment |

10

Table of Contents

| banking, securities and investment management firm. Goldman, Sachs & Co. (“GS&Co.”), a member of FINRA, is also a subsidiary of GS Group and is an investment banking firm that regularly performs services such as acting as financial advisor and serving as principal or agent in the purchase and sale of securities. GS&Co. is affiliated with the following FINRA Members: (a) Goldman Sachs Execution & Clearing, L.P. and (b) Mercer Allied Company, L.P. The Selling Unit Holder, GSAM, GS&Co. and the GS Group and their affiliates disclaim any knowledge of the FINRA relationships, if any, of any other owners of the selling unitholder. |

| (3) | TPH Asset Management LP is the investment manager of the selling unitholder. |

| (4) | The University of Texas/Texas A&M Investment Management Co. is the investment manager of the selling unitholder. TPH Asset Management LP is the investment advisor of the selling unitholder with respect to such sale. |

| (5) | HITE Hedge Capital LP is the managing entity of the selling unitholder. HITE Hedge Capital LLC is the general partner of HITE Hedge Capital LP. James Jampel may be deemed beneficial owner with voting and investment power over the common units held by the selling unitholder. |

| (6) | Kayne Anderson Capital Advisors, LP is the investment manager of the selling unitholder. Ric Kayne may be deemed beneficial owner with voting and investment power over the common units held by the selling unitholder. Mr. Kayne disclaims beneficial ownership of the units reported, except those attributable to him by virtue of his pecuniary interest therein. |

| (7) | KA Fund Advisors, LLC is the investment manager of the selling unitholder. Ric Kayne may be deemed beneficial owner with voting and investment power over the common units held by the selling unitholder. Mr. Kayne disclaims beneficial ownership of the units reported, except those attributable to him by virtue of his pecuniary interest therein. |

| (8) | MTP Energy Management LLC is the investment manager of the selling unitholder. |

| (9) | Magnetar Asset Management LLC is the sub-advisor to the selling unitholder. |

| (10) | Salient Capital Advisors, LLC serves as the selling unitholder’s investment adviser and holds voting and dispositive power with respect to the common units held by the selling unitholder. Gregory A. Reid, John Blaisdell, John Price and Jeremy Radcliffe have control over the selling unitholder as officers of Salient Capital Advisors, LLC. |

| (11) | Tortoise Direct Opportunities GP LLC is the general partner of the selling unitholder. Tortoise Investments, LLC is the sole member of Tortoise Direct Opportunities GP LLC. The Board of Directors of Tortoise Direct Opportunities GP LLC consists of Michelle Kelly, Kyle Krueger and Connie Savage. The Board of Directors of Tortoise Investments, LLC consists of H. Kevin Birzer, Martin Bicknell, Zachary Hamel, Gary Henson, Kenneth Malvey and Terry Matlack and the Executive Committee of Tortoise Investments consists of H. Kevin Birzer, Gary Henson, Michelle Kelly, Edward Russell, Matthew Sallee and Connie Savage. Tortoise Capital Advisors, L.L.C., serves as its Investment Adviser. The Investment Adviser currently has five investment professionals who are primarily responsible for the origination and structuring of the Fund’s portfolio and for voting proxies for securities held by the Fund: Brian A. Kessens, James R. Mick, Stephen Pang, Matthew G.P. Sallee and Robert J. Thummel Jr. |

| (12) | Tortoise Capital Advisors, L.L.C. serves as Investment Advisor to the selling unitholder. Tortoise Investments, LLC is the sole member of Tortoise Capital Advisors, L.L.C. The Board of Directors of Tortoise Investments, LLC consists of H. Kevin Birzer, Martin Bicknell, Zachary Hamel, Gary Henson, Kenneth Malvey and Terry Matlack and the Executive Committee of Tortoise Investments consists of H. Kevin Birzer, Gary Henson, Michelle Kelly, Edward Russell, Matthew Sallee and Connie Savage. Tortoise Capital Advisors, L.L.C. is an investment adviser to Texas Mutual Insurance Company. The Investment Committee of Tortoise Capital Advisors, L.L.C. has voting or dispositive power and is comprised of H. Kevin Birzer, Terry Matlack, Kenneth P. Malvey, Zachary A. Hamel, Brian Kessens, James Mick, Matthew Sallee and Rob Thummel. |

11

Table of Contents

As of the date of this prospectus, we have not been advised by the selling unitholders as to any plan of distribution. Distributions of the common units by the selling unitholders, or by their partners, pledgees, donees (including charitable organizations), transferees or other successors in interest, may from time to time be offered for sale either directly by such individual, or through underwriters, dealers or agents or on any exchange on which the common units may from time to time be traded, in the over-the-counter market, or in independently negotiated transactions or otherwise. The methods by which the common units may be sold include:

| • | privately negotiated transactions; |

| • | underwritten transactions; |

| • | exchange distributions and/or secondary distributions; |

| • | sales in the over-the-counter market; |

| • | ordinary brokerage transactions and transactions in which the broker solicits purchasers; |

| • | broker-dealers may agree with the selling unitholders to sell a specified number of such units at a stipulated price per unit; |

| • | a block trade (which may involve crosses) in which the broker or dealer so engaged will attempt to sell the securities as agent but may position and resell a portion of the block as principal to facilitate the transaction; |

| • | purchases by a broker or dealer as principal and resale by such broker or dealer for its own account pursuant to this prospectus; |

| • | short sales; |

| • | through the writing of options on the units, whether or not the options are listed on an options exchange; |

| • | through the distributions of the units by any selling unitholder to its partners, members or stockholders; |

| • | a combination of any such methods of sale; and |

| • | any other method permitted pursuant to applicable law. |

The selling unitholders may also sell common units pursuant to an exemption from regulation pursuant to Rule 144 under the Securities Act, if available, rather than under this prospectus.

Such transactions may be effected by the selling unitholders at market prices prevailing at the time of sale or at negotiated prices. The selling unitholders may effect such transactions by selling the securities to underwriters or through broker-dealers, and such underwriters or broker-dealers may receive compensation in the form of discounts or commissions from the selling unitholders and may receive commissions from the purchasers of the securities for whom they may act as agent. The selling unitholders may agree to indemnify any underwriter, broker-dealer or agent that participates in transactions involving sales of the common units against certain liabilities, including liabilities arising under the Securities Act. We have agreed to register the common units for sale under the Securities Act and to indemnify the selling unitholders and each person who participates as an underwriter in the offering of the common units against certain civil liabilities, including certain liabilities under the Securities Act.

In connection with sales of the securities under this prospectus, the selling unitholders may enter into hedging transactions with broker-dealers, who may in turn engage in short sales of the securities in the course of hedging the positions they assume. The selling unitholders also may sell securities short and deliver them to close their short positions, or loan or pledge the securities to broker-dealers that in turn may sell them.

12

Table of Contents

The selling unitholders may from time to time pledge or grant a security interest in some or all of the common units owned by them and, if they default in the performance of their secured obligations, the pledgees or secured parties may offer and sell common units from time to time under this prospectus, or under an amendment to this prospectus under Rule 424 or other applicable provision of the Securities Act amending the list of selling unitholders to include the pledgee, transferee or other successors in interest as selling unitholders under this prospectus.

The selling unitholders and any underwriters, dealers or agents that participate in distribution of the securities may be deemed to be underwriters, and any profit on sale of the securities by them and any discounts, commissions or concessions received by any underwriter, dealer or agent may be deemed to be underwriting discounts and commissions under the Securities Act.

There can be no assurances that the selling unitholders will sell any or all of the securities offered under this prospectus.

13

Table of Contents

DESCRIPTION OF OUR COMMON UNITS

Our Common Units

Our common units represent limited partner interests in us. The holders of common units, along with the holders of subordinated units, are entitled to participate in partnership distributions and to exercise the rights and privileges provided to limited partners under our partnership agreement. Please read “Provisions of Our Partnership Agreement Relating to Cash Distributions.” For a description of the rights and privileges of limited partners under our partnership agreement, including voting rights, please read “Our Partnership Agreement.”

Our common units are listed on the NYSE under the symbol “NBLX.” The intraday high and low sales prices of our common units for the period starting January 1, 2017 and ending March 31, 2017 were a high of $53.29 and a low of $35.56.

Transfer Agent and Registrar

Duties

Wells Fargo Shareowner Services serves as the transfer agent and registrar for our common units. We pay all fees charged by the transfer agent for transfers of common units, except for the following that must be paid by our unitholders:

| • | surety bond premiums to replace lost or stolen certificates, or to cover taxes and other governmental charges in connection therewith; |

| • | special charges for services requested by a holder of a common unit; and |

| • | other similar fees or charges. |

Unless our general partner determines otherwise in respect of some or all of any classes of our partnership interests, our partnership interests will be evidenced by book-entry notation on our partnership register and not by physical certificates.

There is no charge to our unitholders for disbursements of our cash distributions. We will indemnify the transfer agent, its agents and each of their respective stockholders, directors, officers and employees against all claims and losses that may arise out of acts performed or omitted for its activities in that capacity, except for any liability due to any gross negligence or intentional misconduct of the indemnified person or entity.

Resignation or Removal

The transfer agent may resign, by notice to us, or be removed by us. The resignation or removal of the transfer agent will become effective upon our appointment of a successor transfer agent and registrar and its acceptance of the appointment. If a successor has not been appointed or has not accepted its appointment within 30 days after notice of the resignation or removal, our general partner may act as the transfer agent and registrar until a successor is appointed.

Transfer of Common Units

By transfer of common units in accordance with our partnership agreement, each transferee of common units shall be admitted as a limited partner with respect to the common units transferred when such transfer and admission are reflected in our books and records. Each transferee:

| • | represents that the transferee has the capacity, power and authority to become bound by our partnership agreement; |

14

Table of Contents

| • | automatically agrees to be bound by the terms and conditions of, and is deemed to have executed, our partnership agreement; and |

| • | gives the consents, waivers and approvals contained in our partnership agreement, such as the approval of all transactions and agreements entered into in connection with our formation and our initial public offering (“IPO”). |

A transferee will become a substituted limited partner of our partnership for the transferred common units automatically upon the recording of the transfer on our books and records. Our general partner will cause any transfers to be recorded on our books and records from time to time as necessary to accurately reflect the transfers but no less frequently than quarterly.

We may, at our discretion, treat the nominee holder of a common unit as the absolute owner. In that case, the beneficial holder’s rights are limited solely to those that it has against the nominee holder as a result of any agreement between the beneficial owner and the nominee holder.

Common units are securities and are transferable according to the laws governing the transfer of securities. In addition to other rights acquired upon transfer, the transferor gives the transferee the right to become a substituted limited partner in our partnership for the transferred common units.

Until a common unit has been transferred on our books, we and the transfer agent may treat the record holder of the common unit as the absolute owner for all purposes, except as otherwise required by law or securities exchange regulations.

15

Table of Contents

PROVISIONS OF OUR PARTNERSHIP AGREEMENT RELATING TO CASH DISTRIBUTIONS

Set forth below is a summary of the significant provisions of our partnership agreement that relate to cash distributions.

Distributions of Available Cash

General

Our partnership agreement requires that, within 45 days after the end of each quarter, we distribute all of our available cash to unitholders of record on the applicable record date.

Definition of Available Cash

Available cash generally means, for any quarter, all cash and cash equivalents on hand at the end of that quarter:

| • | less, the amount of cash reserves established by our general partner to: |

| • | provide for the proper conduct of our business (including reserves for our future capital expenditures, future acquisitions and for anticipated future credit needs); |

| • | comply with applicable law or any loan agreement, security agreement, mortgage, debt instrument or other agreement or obligation to which we or any of our subsidiaries is a party or by which we or such subsidiary is bound or we or such subsidiary’s assets are subject; or |

| • | provide funds for distributions to our unitholders and to our general partner for any one or more of the next four quarters (provided that our general partner may not establish cash reserves for distributions pursuant to this bullet point if the effect of such reserves will prevent us from distributing the minimum quarterly distribution on all common units and any cumulative arrearages on such common units for the current quarter); |

| • | plus, if our general partner so determines, all or any portion of the cash on hand on the date of determination of available cash for the quarter resulting from working capital borrowings made subsequent to the end of such quarter. |

The purpose and effect of the last bullet point above is to allow our general partner, if it so decides, to use cash from working capital borrowings made after the end of the quarter but on or before the date of determination of available cash for that quarter to pay distributions to unitholders. Under our partnership agreement, working capital borrowings are generally borrowings incurred under a credit facility, commercial paper facility or similar financing arrangement that are used solely for working capital purposes or to pay distributions to our partners and with the intent of the borrower to repay such borrowings within twelve months with funds other than from additional working capital borrowings.

Intent to Distribute the Minimum Quarterly Distribution

Under our current cash distribution policy, we intend to make a minimum quarterly distribution to the holders of our common units and subordinated units of $.3750 per unit, or $1.5000 per unit on an annualized basis, to the extent we have sufficient available cash after the establishment of cash reserves and the payment of costs and expenses, including reimbursements of expenses to our general partner. However, there is no guarantee that we will pay the minimum quarterly distribution on our units in any quarter. The amount of distributions paid under our cash distribution policy and the decision to make any distribution is determined by our general partner, taking into consideration the terms of our partnership agreement.

16

Table of Contents

General Partner Interest

Our general partner owns a non-economic general partner interest in us, which does not entitle it to receive cash distributions. However, our general partner may in the future own common units or other equity securities in us that will entitle it to receive distributions.

Incentive Distribution Rights

Noble currently holds incentive distribution rights that entitle it to receive increasing percentages, up to a maximum of 50%, of the available cash we distribute from operating surplus (as defined below) in excess of $0.4313 per unit per quarter. The maximum distribution of 50% does not include any distributions that Noble or its affiliates may receive on common units or subordinated units that it owns.

Operating Surplus and Capital Surplus

General

All cash distributed to unitholders is characterized as either being paid from “operating surplus” or “capital surplus.” We treat distributions of available cash from operating surplus differently than distributions of available cash from capital surplus.

Operating Surplus

We define operating surplus as:

| • | $45.0 million (as described below); plus |

| • | all of our cash receipts after the closing of our IPO, excluding cash from interim capital transactions (as defined below) and the termination of hedge contracts, provided that cash receipts from the termination of a commodity hedge or interest rate hedge prior to its scheduled settlement or termination date shall be included in operating surplus in equal quarterly installments over the remaining scheduled life of such commodity hedge or interest rate hedge; plus |

| • | working capital borrowings made after the end of a quarter but on or before the date of determination of operating surplus for that quarter; plus |

| • | cash distributions (including incremental distributions on incentive distribution rights) paid in respect of equity issued, other than equity issued in our IPO, to finance all or a portion of expansion capital expenditures in respect of the period from the date that we enter into a binding obligation to commence the construction, development, replacement, improvement or expansion of a capital asset and ending on the earlier to occur of the date the capital asset commences commercial service and the date that it is abandoned or disposed of; less |

| • | all of our operating expenditures (as defined below) after the closing of our IPO; less |

| • | the amount of cash reserves established by our general partner to provide funds for future operating expenditures; less |

| • | all working capital borrowings not repaid within twelve months after having been incurred, or repaid within such twelve-month period with the proceeds of additional working capital borrowings; less |

| • | any cash loss realized on disposition of an investment capital expenditure (which is a capital expenditure other than a maintenance capital expenditure or an expansion capital expenditure). |

As described above, operating surplus does not reflect actual cash on hand that is available for distribution to our unitholders and is not limited to cash generated by operations. For example, it includes a provision that will enable us, if we choose, to distribute as operating surplus up to $45.0 million of cash we receive in the future

17

Table of Contents

from non-operating sources such as asset sales, issuances of securities and long-term borrowings that would otherwise be distributed as capital surplus. In addition, the effect of including, as described above, certain cash distributions on equity interests in operating surplus is to increase operating surplus by the amount of any such cash distributions. As a result, we may also distribute as operating surplus up to the amount of any such cash that we receive from non-operating sources.

The proceeds of working capital borrowings increase operating surplus and repayments of working capital borrowings are generally operating expenditures (as described below) and thus reduce operating surplus when repayments are made. However, if working capital borrowings, which increase operating surplus, are not repaid during the twelve-month period following the borrowing, they will be deemed repaid at the end of such period, thus decreasing operating surplus at such time. When such working capital borrowings are in fact repaid, they will not be treated as a further reduction in operating surplus because operating surplus will have been previously reduced by the deemed repayment.

We define interim capital transactions as (i) borrowings, refinancings or refundings of indebtedness (other than working capital borrowings and items purchased on open account or for a deferred purchase price in the ordinary course of business) and sales of debt securities, (ii) issuances of equity securities, (iii) sales or other dispositions of assets, other than sales or other dispositions of inventory, accounts receivable and other assets in the ordinary course of business and sales or other dispositions of assets as part of normal asset retirements or replacements and (iv) capital contributions received.

We define operating expenditures as all of our cash expenditures, including, but not limited to, taxes, reimbursements of expenses of our general partner and its affiliates, officer, director and employee compensation, debt service payments, payments made in the ordinary course of business under interest rate hedge contracts and commodity hedge contracts (provided that payments made in connection with the termination of any interest rate hedge contract or commodity hedge contract prior to its scheduled settlement or termination date will be included in operating expenditures in equal quarterly installments over the remaining scheduled life of such interest rate hedge contract or commodity hedge contract and amounts paid in connection with the initial purchase of an interest rate hedge contract or a commodity hedge contract will be amortized over the life of such interest rate hedge contract or commodity hedge contract), estimated maintenance capital expenditures (as discussed in further detail below), and repayment of working capital borrowings; provided, however, that operating expenditures do not include:

| • | repayments of working capital borrowings where such borrowings have previously been deemed to have been repaid (as described above); |

| • | payments (including prepayments and prepayment penalties) of principal of and premium on indebtedness other than working capital borrowings; |

| • | actual maintenance capital expenditures; |

| • | expansion capital expenditures; |

| • | investment capital expenditures; |

| • | payment of transaction expenses (including taxes) relating to interim capital transactions; |

| • | distributions to our partners; or |

| • | repurchases of partnership interests (excluding repurchases we make to satisfy obligations under employee benefit plans). |

Capital Surplus

Capital surplus is defined in our partnership agreement as any distribution of available cash in excess of our cumulative operating surplus. Accordingly, except as described above, capital surplus would generally be generated by:

| • | borrowings other than working capital borrowings; |

18

Table of Contents

| • | sales of our equity and debt securities; |

| • | sales or other dispositions of assets, other than inventory, accounts receivable and other assets sold in the ordinary course of business or as part of ordinary course retirement or replacement of assets; and |

| • | capital contributions received. |

Characterization of Cash Distributions

All available cash distributed by us on any date from any source is treated as distributed from operating surplus until the sum of all available cash distributed by us since the closing of our IPO equals the operating surplus from the closing of our IPO through the end of the quarter immediately preceding that distribution. We anticipate that distributions from operating surplus generally will not represent a return of capital. However, operating surplus, as defined in our partnership agreement, includes certain components, including a $45.0 million cash basket, that represent non-operating sources of cash. Consequently, it is possible that all or a portion of specific distributions from operating surplus may represent a return of capital. Any available cash distributed by us in excess of our cumulative operating surplus is deemed to be capital surplus under our partnership agreement. Our partnership agreement treats a distribution of capital surplus as the repayment of the initial unit price from our IPO and as a return of capital. We do not anticipate that we will make any distributions from capital surplus.

Capital Expenditures

For purposes of determining operating surplus, maintenance capital expenditures are those capital expenditures required to maintain our long-term operating capacity and/or operating income, and expansion capital expenditures are those capital expenditures that we expect will expand our operating capacity or operating income over the long term. Examples of maintenance capital expenditures include capital expenditures associated with the replacement of equipment and well connections, or the construction, development or acquisition of other facilities, to replace expected reductions in hydrocarbons available for gathering, treating, transporting or otherwise handled by our facilities (which we refer to as operating capacity). Maintenance capital expenditures will also include interest (and related fees) on debt incurred and distributions on equity issued to finance all or any portion of the construction or development of a replacement asset that is paid in respect of the period that begins when we enter into a binding obligation to commence constructing or developing a replacement asset and ending on the earlier to occur of the date that any such replacement asset commences commercial service or the date that it is abandoned or disposed of. Capital expenditures made solely for investment purposes are not considered maintenance capital expenditures.

Because our maintenance capital expenditures can be irregular, the amount of our actual maintenance capital expenditures may differ substantially from period to period, which could cause similar fluctuations in the amounts of operating surplus, adjusted operating surplus and cash available for distribution to our unitholders if we subtracted actual maintenance capital expenditures from operating surplus.

Our partnership agreement requires that an estimate of the average quarterly maintenance capital expenditures necessary to maintain our operating capacity or operating income over the long term be subtracted from operating surplus each quarter as opposed to the actual amounts spent. The amount of estimated maintenance capital expenditures deducted from operating surplus for those periods is subject to review and change by our general partner at least once a year, provided that any change is approved by our special committee. The estimate is made at least annually and whenever an event occurs that is likely to result in a material adjustment to the amount of our maintenance capital expenditures, such as a major acquisition or the introduction of new governmental regulations that will impact our business. For purposes of calculating operating surplus, any adjustment to this estimate will be prospective only.

19

Table of Contents

The use of estimated maintenance capital expenditures in calculating operating surplus will have the following effects:

| • | it will reduce the risk that maintenance capital expenditures in any one quarter will be large enough to render operating surplus less than the initial quarterly distribution to be paid on all the units for the quarter and subsequent quarters; |

| • | it will increase our ability to distribute as operating surplus cash we receive from non-operating sources; and |

| • | it will be more difficult for us to raise our distribution above the minimum quarterly distribution and pay incentive distributions on the incentive distribution rights. |

Expansion capital expenditures are cash expenditures to construct new midstream infrastructure and those expenditures incurred in order to extend the useful lives of our assets, reduce costs, increase revenues or increase system throughput or capacity from current levels, including well connections that increase existing system throughput. Examples of expansion capital expenditures include the construction, development or acquisition of additional gathering pipelines and centralized gathering facilities, in each case to the extent such capital expenditures are expected to expand our operating capacity, operating income or revenue. In the future, if we make acquisitions that increase system throughput or capacity, the associated capital expenditures may also be considered expansion capital expenditures.

Capital expenditures that are made in part for maintenance capital purposes and in part for expansion capital purposes are allocated as maintenance capital expenditures or expansion capital expenditures by our general partner.

Subordinated Units and Subordination Period

General

Our partnership agreement provides that, during the subordination period (which we define below), the common units have the right to receive distributions of available cash from operating surplus each quarter in an amount equal to $0.3750 per unit, which amount is defined in our partnership agreement as the minimum quarterly distribution, plus any arrearages in the payment of the minimum quarterly distribution on the common units from prior quarters, before any distributions of available cash from operating surplus may be made on the subordinated units. Subordinated units are deemed “subordinated” because for a period of time, referred to as the “subordination period,” the subordinated units are not entitled to receive any distributions until the common units have received the minimum quarterly distribution plus any arrearages in the payment of the minimum quarterly distribution on the common units from prior quarters. Furthermore, no arrearages will accrue or be payable on the subordinated units. The practical effect of the subordinated units is to increase the likelihood that, during the subordination period, there will be available cash to be distributed on the common units.

Subordination Period

The subordination period began on the closing date of our IPO and, except as described below, will extend until the first business day following the distribution of available cash in respect of any quarter beginning after September 31, 2019 that each of the following tests are met:

| • | distributions of available cash from operating surplus on each of the outstanding common units and subordinated units equaled or exceeded $1.5000 (the annualized minimum quarterly distribution), for each of the three consecutive, non-overlapping four-quarter periods immediately preceding that date; |

| • | the adjusted operating surplus (as defined below) generated during each of the three consecutive, non-overlapping four-quarter periods immediately preceding that date equaled or exceeded the sum of |

20

Table of Contents

| $1.5000 (the annualized minimum quarterly distribution) on all of the outstanding common units and subordinated units during those periods on a fully diluted basis; and |

| • | there are no arrearages in payment of the minimum quarterly distribution on the common units. |

Early Termination of the Subordination Period

Notwithstanding the foregoing, the subordination period will automatically terminate on the first business day following the distribution of available cash in respect of any quarter, beginning with the quarter ending September 30, 2017, that each of the following tests are met:

| • | distributions of available cash from operating surplus on each of the outstanding common units and subordinated units equaled or exceeded $2.2500 (150% of the annualized minimum quarterly distribution), for the four-quarter period immediately preceding that date; |

| • | the adjusted operating surplus (as defined below) generated during the four-quarter period immediately preceding that date equaled or exceeded the sum of (i) $2.2500 (150% of the annualized minimum quarterly distribution) on all of the outstanding common units and subordinated units during that period on a fully diluted basis and (ii) the corresponding distributions on the incentive distribution rights; and |

| • | there are no arrearages in payment of the minimum quarterly distribution on the common units. |

Expiration of the Subordination Period

When the subordination period ends, each outstanding subordinated unit will convert into one common unit and will thereafter participate pro rata with the other common units in distributions of available cash.

Adjusted Operating Surplus

Adjusted operating surplus is intended to reflect the cash generated from operations during a particular period and therefore excludes net drawdowns of reserves of cash established in prior periods. Adjusted operating surplus for a period consists of:

| • | operating surplus generated with respect to that period (excluding any amounts attributable to the item described in the first bullet under the caption “—Operating Surplus and Capital Surplus—Operating Surplus” above); less |

| • | any net increase in working capital borrowings with respect to that period; less |

| • | any net decrease in cash reserves for operating expenditures with respect to that period not relating to an operating expenditure made with respect to that period; plus |

| • | any net decrease in working capital borrowings with respect to that period; plus |

| • | any net decrease made in subsequent periods to cash reserves for operating expenditures initially established with respect to that period to the extent such decrease results in a reduction in adjusted operating surplus in subsequent periods; plus |

| • | any net increase in cash reserves for operating expenditures with respect to that period required by any debt instrument for the repayment of principal, interest or premium. |

Distributions of Available Cash from Operating Surplus During the Subordination Period

We will make distributions of available cash from operating surplus for any quarter during the subordination period in the following manner:

| • | first, 100% to the common unitholders, pro rata, until we distribute for each outstanding common unit an amount equal to the minimum quarterly distribution for that quarter; |

21

Table of Contents

| • | second, 100% to the common unitholders, pro rata, until we distribute for each outstanding common unit an amount equal to any arrearages in payment of the minimum quarterly distribution on the common units for any prior quarters during the subordination period; |

| • | third, 100% to the subordinated unitholders, pro rata, until we distribute for each outstanding subordinated unit an amount equal to the minimum quarterly distribution for that quarter; and |

| • | thereafter, in the manner described in “—Incentive Distribution Rights” below. |

The preceding discussion is based on the assumptions that we do not issue additional classes of equity securities.

Distributions of Available Cash from Operating Surplus After the Subordination Period

We will make distributions of available cash from operating surplus for any quarter after the subordination period in the following manner:

| • | first, 100% to all common unitholders, pro rata, until we distribute for each outstanding common unit an amount equal to the minimum quarterly distribution for that quarter; and |

| • | thereafter, in the manner described in “—Incentive Distribution Rights” below. |

The preceding discussion is based on the assumptions that we do not issue additional classes of equity securities.

Incentive Distribution Rights

Incentive distribution rights represent the right to receive an increasing percentage (15%, 25% and 50%) of quarterly distributions of available cash from operating surplus after the minimum quarterly distribution and the target distribution levels have been achieved. Noble holds the incentive distribution rights, but may transfer these rights separately from its ownership of the general partner.

If for any quarter:

| • | we have distributed available cash from operating surplus to the common unitholders and subordinated unitholders in an amount equal to the minimum quarterly distribution; and |

| • | we have distributed available cash from operating surplus on outstanding common units in an amount necessary to eliminate any cumulative arrearages in payment of the minimum quarterly distribution; |

then, we will distribute any additional available cash from operating surplus for that quarter among the unitholders and the holders of the incentive distribution rights in the following manner:

| • | first, 100% to all unitholders, pro rata, until each unitholder receives a total of $0.4313 per unit for that quarter (the “first target distribution”); |

| • | second, 85% to all unitholders, pro rata, and 15% to the holders of our incentive distribution rights, until each unitholder receives a total of $0.4688 per unit for that quarter (the “second target distribution”); |

| • | third, 75% to all unitholders, pro rata, and 25% to the holders of our incentive distribution rights, until each unitholder receives a total of $0.5625 per unit for that quarter (the “third target distribution”); and |

| • | thereafter, 50% to all unitholders, pro rata, and 50% to the holders of our incentive distribution rights. |

Percentage Allocations of Available Cash from Operating Surplus

The following table illustrates the percentage allocations of available cash from operating surplus between the unitholders and our general partner based on the specified target distribution levels. The amounts set forth

22

Table of Contents

under “Marginal Percentage Interest in Distributions” are the percentage interests of Noble, as holder of our incentive distribution rights, and the unitholders in any available cash from operating surplus we distribute up to and including the corresponding amount in the column “Total Quarterly Distribution Per Unit Target Amount.” The percentage interests shown for our unitholders Noble for the minimum quarterly distribution are also applicable to quarterly distribution amounts that are less than the minimum quarterly distribution. The percentage interests set forth below assume that Noble has not transferred its incentive distribution rights and that there are no arrearages on common units.

| Total Quarterly Distribution per Unit |

Marginal Percentage Interest in Distributions |

|||||||||||||||

| Unitholders | IDR Holders | |||||||||||||||

| Minimum Quarterly Distribution |

$0.3750 | 100.0 | % | 0.0 | % | |||||||||||

| First Target Distribution |

above $0.3750 | up to $0.4313 | 100.0 | % | 0.0 | % | ||||||||||

| Second Target Distribution |

above $0.4313 | up to $0.4688 | 85.0 | % | 15.0 | % | ||||||||||

| Third Target Distribution |

above $0.4688 | up to $0.5625 | 75.0 | % | 25.0 | % | ||||||||||

| Thereafter |

above $0.5625 | 50.0 | % | 50.0 | % | |||||||||||

Noble’s Right to Reset Incentive Distribution Levels

Noble, as the initial holder of all our incentive distribution rights, has the right under our partnership agreement, subject to certain conditions, to elect to relinquish the right to receive incentive distribution payments based on the initial target distribution levels and to reset, at higher levels, the minimum quarterly distribution amount and target distribution levels upon which the incentive distribution payments to our general partner would be set. If Noble transfers all or a portion of the incentive distribution rights in the future, then the holder or holders of a majority of our incentive distribution rights will be entitled to exercise this right. The following discussion assumes that Noble holds all of the incentive distribution rights at the time that a reset election is made. Noble’s right to reset the minimum quarterly distribution amount and the target distribution levels upon which the incentive distributions payable to Noble are based may be exercised, without approval of our unitholders or the conflicts committee, at any time when there are no subordinated units outstanding, we have made cash distributions to the holders of the incentive distribution rights at the highest level of incentive distributions for each of the four consecutive fiscal quarters immediately preceding such time and the amount of each such distribution did not exceed adjusted operating surplus for such quarter. If Noble and its affiliates are not the holders of a majority of the incentive distribution rights at the time an election is made to reset the minimum quarterly distribution amount and the target distribution levels, then the proposed reset will be subject to the prior written concurrence of the general partner that the conditions described above have been satisfied. The reset minimum quarterly distribution amount and target distribution levels will be higher than the minimum quarterly distribution amount and the target distribution levels prior to the reset such that the holder of the incentive distribution rights will not receive any incentive distributions under the reset target distribution levels until cash distributions per unit following this event increase as described below. We anticipate that Noble would exercise this reset right in order to facilitate acquisitions or internal growth projects that would otherwise not be sufficiently accretive to cash distributions per common unit, taking into account the existing levels of incentive distribution payments being made.

In connection with the resetting of the minimum quarterly distribution amount and the target distribution levels and the corresponding relinquishment by Noble of incentive distribution payments based on the target distributions prior to the reset, Noble will be entitled to receive a number of newly issued common units based on a predetermined formula described below that takes into account the “cash parity” value of the average cash distributions related to the incentive distribution rights received by Noble for the two quarters immediately preceding the reset event as compared to the average cash distributions per common unit during that two-quarter period.

23

Table of Contents

The number of common units that Noble (or the then-holder of the incentive distribution rights, if other than our general partner) would be entitled to receive from us in connection with a resetting of the minimum quarterly distribution amount and the target distribution levels then in effect would be equal to the quotient determined by dividing (x) the average aggregate amount of cash distributions received by Noble or such holder in respect of its incentive distribution rights during the two consecutive fiscal quarters ended immediately prior to the date of such reset election by (y) the average of the aggregate amount of cash distributed per common unit during each of these two quarters.

Following a reset election, the minimum quarterly distribution amount will be reset to an amount equal to the average cash distribution amount per common unit for the two fiscal quarters immediately preceding the reset election (which amount we refer to as the “reset minimum quarterly distribution”) and the target distribution levels will be reset to be correspondingly higher such that we would distribute all of our available cash from operating surplus for each quarter thereafter as follows:

| • | first, 100% to all unitholders, pro rata, until each unitholder receives an amount equal to 115% of the reset minimum quarterly distribution for that quarter; |

| • | second, 85% to all unitholders, pro rata, and 15% to the holders of our incentive distribution rights, until each unitholder receives an amount per unit equal to 125% of the reset minimum quarterly distribution for the quarter; |

| • | third, 75% to all unitholders, pro rata, and 25% to the holders of our incentive distribution rights, until each unitholder receives an amount per unit equal to 150% of the reset minimum quarterly distribution for the quarter; and |

| • | thereafter, 50% to all unitholders, pro rata, and 50% to the holders of our incentive distribution rights. |

Noble will be entitled to cause the minimum quarterly distribution amount and the target distribution levels to be reset on more than one occasion, provided that it may not make a reset election except at a time when it has received incentive distributions for the immediately preceding four consecutive fiscal quarters based on the highest level of incentive distributions that it is entitled to receive under our partnership agreement.

Distributions from Capital Surplus

How Distributions from Capital Surplus will be Made

We will make distributions of available cash from capital surplus, if any, in the following manner:

| • | first, 100% to all unitholders, pro rata, until we distribute for each common unit that was issued in our IPO, an amount of available cash from capital surplus equal to the initial public offering price in our IPO; |

| • | second, 100% to all unitholders, pro rata, until we distribute for each common unit, an amount of available cash from capital surplus equal to any unpaid arrearages in payment of the minimum quarterly distribution on the outstanding common units; and |

| • | thereafter, as if they were from operating surplus. |

Effect of a Distribution from Capital Surplus

Our partnership agreement treats a distribution of capital surplus as the repayment of the initial unit price from our IPO, which is a return of capital. The initial public offering price less any distributions of capital surplus per unit and any distributions of cash in connection with dissolution and liquidation is referred to as the “unrecovered initial unit price.” Each time a distribution of capital surplus is made, the minimum quarterly distribution and the target distribution levels will be reduced in the same proportion as the corresponding reduction in the unrecovered initial unit price. Because distributions of capital surplus will reduce the minimum

24

Table of Contents

quarterly distribution after any of these distributions are made, the effects of distributions of capital surplus may make it easier for Noble to receive incentive distributions and for the subordinated units to convert into common units. However, any distribution of capital surplus before the unrecovered initial unit price is reduced to zero cannot be applied to the payment of the minimum quarterly distribution or any arrearages.