Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 Q417 - Barnes & Noble Education, Inc. | bned-ex322_20170429xq417.htm |

| EX-32.1 - EXHIBIT 32.1 Q417 - Barnes & Noble Education, Inc. | bned-ex321_20170429xq417.htm |

| EX-31.2 - EXHIBIT 31.2 Q417 - Barnes & Noble Education, Inc. | bned-ex312_20170429xq417.htm |

| EX-31.1 - EXHIBIT 31.1 Q417 - Barnes & Noble Education, Inc. | bned-ex311_20170429xq417.htm |

| EX-23.1 - EXHIBIT 23.1 CONSENT - Barnes & Noble Education, Inc. | bned-ex231_20170429xq417.htm |

| EX-21.1 - EXHIBIT 21.1 LIST OF SUBSIDIARIES - Barnes & Noble Education, Inc. | bned-ex211_20170429xq417.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended April 29, 2017

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 1-37499

BARNES & NOBLE EDUCATION, INC.

(Exact Name of Registrant as Specified in Its Charter)

Delaware | 46-0599018 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

120 Mountain View Blvd., Basking Ridge, NJ | 07920 | |

(Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s Telephone Number, Including Area Code: (908) 991-2665

Securities registered pursuant to Section 12(b) of the Act:

Title of Class | Name of Exchange on which registered | |

Common Stock, $0.01 par value per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.(Check one):

Large accelerated filer | ¨ | Accelerated filer | x | ||

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | ||

Emerging Growth Company | ¨ | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting and non-voting stock held by non-affiliates of the registrant was approximately $423 million based upon the closing market price of $9.25 per share of Common Stock on the New York Stock Exchange as of October 29, 2016. As of June 16, 2017, 46,516,890 shares of Common Stock, par value $0.01 per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement for the 2017 Annual Meeting of Shareholders are incorporated by reference into Part III.

BARNES & NOBLE EDUCATION, INC. AND SUBSIDIARIES

INDEX TO FORM 10-K | ||

Page No. | ||

2

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

This annual report on Form 10-K contains certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and information relating to us and our business that are based on the beliefs of our management as well as assumptions made by and information currently available to our management. When used in this communication, the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan,” “will,” “forecasts,” “projections,” and similar expressions, as they relate to us or our management, identify forward-looking statements. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the future events and trends discussed in this Form 10-K may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements.

Such statements reflect our current views with respect to future events, the outcome of which is subject to certain risks, including, among others:

• | general competitive conditions, including actions our competitors may take to grow their businesses; |

• | a decline in college enrollment or decreased funding available for students; |

• | decisions by colleges and universities to outsource their physical and/or online bookstore operations or change the operation of their bookstores; |

• | the general economic environment and consumer spending patterns; |

• | decreased consumer demand for our products, low growth or declining sales; |

• | our ability to continue to successfully integrate the operations of MBS Textbook Exchange, LLC into our Company, while facing competition from not only physical bookstore operations, but also virtual solutions; |

• | the strategic objectives, anticipated synergies, and/or other expected potential benefits of the MBS Textbook Exchange, LLC acquisition may not be fully realized or may take longer than expected; |

• | the integration of MBS Textbook Exchange, LLC’s operations into our own may also increase the risk of our internal controls being found ineffective; |

• | risks associated with operation or performance of MBS Textbook Exchange, LLC’s point-of-sales systems that are sold to college bookstore customers; |

• | implementation of our digital strategy may not result in the expected growth in our digital sales and/or profitability; |

• | risk that digital sales growth does not exceed the rate of investment spend; |

• | the performance of our online, digital and other initiatives, integration of and deployment of, additional products and services, and enhancements to higher education digital products, and the inability to achieve the expected cost savings; |

• | our ability to successfully implement our strategic initiatives including our ability to identify, compete for and execute upon additional acquisitions and strategic investments; |

• | technological changes; |

• | risks associated with counterfeit and piracy of digital and print materials; |

• | our international operations could result in additional risks; |

• | our ability to attract and retain employees; |

• | changes to purchase or rental general terms, payment terms, return policies, the discount or margin on products or other terms with our suppliers; |

• | risks associated with data privacy, information security and intellectual property; |

• | trends and challenges to our business and in the locations in which we have stores; |

• | non-renewal of managed bookstore, physical and/or online store contracts and higher-than-anticipated store closings; |

• | disruptions to our information technology systems, infrastructure and data due to computer malware, viruses, hacking and phishing attacks, resulting in harm to our business and results of operations; |

• | disruption of or interference with third party web service providers and our own proprietary technology; |

• | work stoppages or increases in labor costs; |

3

• | the risk of price reduction or change in format of course materials by publishers, which could negatively impact revenues and margin; |

• | possible increases in shipping rates or interruptions in shipping service; |

• | product shortages, including risks associated with merchandise sourced indirectly from outside the United States; |

• | changes in law or regulation; |

• | enactment of laws which may restrict or prohibit our use of emails or similar marketing activities; |

• | the amount of our indebtedness and ability to comply with covenants applicable to any future debt financing; |

• | our ability to satisfy future capital and liquidity requirements; |

• | our ability to access the credit and capital markets at the times and in the amounts needed and on acceptable terms; |

• | adverse results from litigation, governmental investigations or tax-related proceedings or audits; |

• | changes in accounting standards; and |

• | the other risks and uncertainties detailed in the section titled “Risk Factors” in Part I - Item 1A of this Form 10-K. |

Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results or outcomes may vary materially from those described as anticipated, believed, estimated, expected, intended or planned. Subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements in this paragraph. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise after the date of this Form 10-K.

AVAILABILITY OF INFORMATION

You may read and copy any materials Barnes & Noble Education, Inc. files with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. Copies of such materials also can be obtained free of charge at the SEC’s website, www.sec.gov, or by mail from the Public Reference Room of the SEC, at prescribed rates. Please call the SEC at 1-800-SEC-0330 for further information on the operation of the Public Reference Room. Barnes & Noble Education, Inc.’s SEC filings are also available to the public, free of charge, on its corporate website, www.bned.com, as soon as reasonably practicable after Barnes & Noble Education, Inc. electronically files such material with, or furnishes it to, the SEC. You may also request a copy of any of our filings with the SEC at no cost by writing us at Investor Relations, Barnes & Noble Education, Inc., 120 Mountain View Blvd., Basking Ridge, N.J. 07920. Barnes & Noble Education, Inc.’s common stock is traded on the New York Stock Exchange. Material filed by Barnes & Noble Education, Inc. can be inspected at the offices of the New York Stock Exchange at 20 Broad Street, New York, N.Y. 10005.

4

EXPLANATORY NOTE

On August 2, 2015, we completed the legal separation ("Spin-Off") from Barnes & Noble, Inc., at which time we began to operate as an independent publicly-traded company.

For the results of operations for the 13 weeks ended August 1, 2015 (first quarter of Fiscal 2016), our consolidated financial statements are presented on a stand-alone basis since we were still part of Barnes & Noble, Inc. until the consummation of the Spin-Off on August 2, 2015, and for the results of operations for the 39 weeks ended April 30, 2016, our consolidated financial statements are presented on a consolidated basis as we became a separate consolidated entity. For Fiscal 2017, the results of operations for the entire 52 weeks ended April 29, 2017 reflected in our consolidated financial statements are presented on a consolidated basis.

On February 27, 2017, we acquired MBS Textbook Exchange, LLC ("MBS"). The consolidated financial statements for the 52 weeks ended April 29, 2017 include the financial results of MBS from the acquisition date, February 27, 2017, to April 29, 2017. For additional information on the MBS acquisition, see Form 8-K filed on February 28, 2017 and Form 8K/A pro forma information filed on May 8, 2017.

Additionally, effective with the acquisition of MBS, we determined that we have two reportable segments: Barnes & Noble College Booksellers, LLC ("BNC") and MBS, whereas BNC was previously our only reportable segment prior to the acquisition.

5

PART I

Item 1. BUSINESS

Unless the context otherwise indicates, references to “we,” “us,” “our” and “the Company” refer to Barnes & Noble Education, Inc., a Delaware corporation. References to “Barnes & Noble College” or “BNC” refer to our college bookstore business operated through our subsidiary Barnes & Noble College Booksellers, LLC. References to “MBS” refer to our virtual bookstore and wholesale textbook distribution business operated through our subsidiary MBS Textbook Exchange, LLC, a Delaware corporation.

Our fiscal year is comprised of 52 or 53 weeks, ending on the Saturday closest to the last day of April. “Fiscal 2017” means the 52 weeks ended April 29,2017, “Fiscal 2016” means the 52 weeks ended April 30, 2016, “Fiscal 2015” means the 52 weeks ended May 2, 2015, “Fiscal 2014” means the 53 weeks ended May 3, 2014, and “Fiscal 2013” means the 52 weeks ended April 27, 2013.

Unless otherwise indicated, market and industry information contained in this Form 10-K is based on information provided by the National Association of College Stores ("NACS") and management estimates of market shares.

OVERVIEW

General

Barnes & Noble Education, Inc. (“BNED”) is one of the largest contract operators of physical and virtual bookstores for college and university campuses, and private/parochial K-12 schools, across the United States, and a leading provider of digital education services. Through our Barnes & Noble College (“BNC”) and MBS Textbook Exchange (“MBS”) subsidiaries, we operate 1,481 physical and virtual bookstores and serve more than 6 million students enrolled in higher education institutions and K-12 schools.

Effective with the acquisition of MBS on February 27, 2017, we have determined that we operate two reportable segments: BNC and MBS. See the BNC and MBS segment discussions below.

BNC operates 769 physical campus bookstores, the majority of which also have school-branded e-commerce sites operated by BNC, and BNC also includes our digital operations. Our campus stores are a social and academic hub through which students can access affordable course materials and affinity products, including new and used print and digital textbooks, which are available for sale or rent; emblematic apparel and gifts; trade books; computer products; school and dorm supplies; café offerings; convenience food and beverages; and graduation products. BNC product offerings also include a suite of digital content, software, and services through our LoudCloud platform, such as predictive analytics, a variety of courseware built on a foundation of open educational resources ("OER"), and competency-based learning solutions.

Our MBS subsidiary operates two highly integrated businesses. The MBS Direct business is the largest contract operator of virtual bookstores for college and university campuses, and private/parochial K-12 schools. MBS Direct operates 712 virtual bookstores, offering new and used print and digital textbooks, which are available for sale or rent. Additionally, MBS Direct sells textbooks directly to students through textbooks.comSM, one of the largest e-commerce sites for new and used textbooks. MBS Wholesale is one of the largest textbook wholesalers in the country, providing a comprehensive selection of new and used textbooks at a low cost of supply to more than 3,700 physical bookstores, including BNC’s 769 campus bookstores.

Educational institutions increasingly are outsourcing bookstore operations, investing in data-driven analytical tools, and offering students more affordable options for textbooks and other learning tools. Given these continuing trends, we are well-positioned to capture new market share and partner with an increasing number of schools across the country. As demand for new, improved, and more affordable products and services increase in the rapidly changing education landscape, we are working to evolve our business model and enhance our solutions. We aim to be an even stronger partner for schools and meet customer needs by expanding our physical and virtual bookstore service capabilities, courseware offerings and digital platform services. We believe that our recent strategic actions, including the acquisition of LoudCloud, Promoversity and MBS, and development of courseware, have substantially enhanced our competitive position. We continue to aggressively innovate and collaborate with our partners to provide solutions that extend well beyond course materials sourcing and sales to include new digital services that support successful student outcomes.

Strength of Our Business

We believe our product offerings and services for students, faculty and administrators enable a more personalized learning experience, which improves student success rates and retention. We strive to be the first stop for students, educators and administrators by offering the most comprehensive resources available with our flexible physical and/or virtual bookstore options. The strengths of our business are as follows:

6

• | Large Footprint with Well-Recognized Brand: We operate 1,481 physical and virtual bookstores and serve more than 6 million students enrolled in higher education institutions and K-12 schools. The Barnes & Noble brand is virtually synonymous with bookselling, and we believe it is one of the most widely recognized and respected brands in the United States. Our large Barnes & Noble College footprint, reputation, and credibility in the marketplace not only support our marketing efforts to universities, students and faculty, but are also important for leading publishers who rely on us as one of their primary distribution channels. The addition of MBS’s wholesale and virtual bookstore customers meaningfully expanded our customer base, and MBS Direct’s advanced virtual bookstore capabilities increased our footprint to include higher education institutions and K-12 schools that prefer virtual bookstore solutions, enabling us to offer existing and prospective clients physical, virtual and hybrid bookstore models. |

• | Ability to Meet Students’ Affordability Needs: We are dedicated to providing quality, cost-effective course materials and are constantly seeking new ways to deliver the most affordable and easily accessible materials possible. We offer a comprehensive range of cost-effective options for textbooks (new and used, for rent or for sale), as well as programs that help students to secure the best price, such as our “price match” program. The MBS Wholesale distribution channel, warehousing systems and fulfillment expertise allow us to provide an expanded selection of new and used textbooks. Our digital courseware utilizing open educational resources (“OER”), defined as any type of educational materials that are available to a learning community at little or no cost, is a cost-effective solution for today’s educators, providing course materials at a significantly lower cost to students. |

• | Comprehensive Suite of Course Materials: Our physical bookstores and accompanying e-commerce sites offer new and used print and digital textbooks, which are available to buy or rent. Through our MBS Wholesale business, we have a robust inventory comprised of approximately 300,000 textbook titles in stock and a comprehensive catalog of new and used textbooks and digital course material solutions. We offer alternative forms of educational materials, including digital courseware built on a foundation of OER, so that students and educators have the flexibility to learn and teach in digital and/or print formats. |

• | Well-Established, Deep Relationships with Partners: We have strong partnerships with college and university administrators, as well as with publishers, vendors and suppliers. |

• | Our Barnes & Noble College campus bookstores have an average relationship tenure of 15 years. Our BNC decentralized management structure empowers local teams to make decisions based on the local campus needs and foster collaborative working relationships with our partners. |

• | We have long-term relationships with over 10,000 publishers, who can partner with us to access one of the largest distribution networks of college and K-12 educational materials in the United States. |

• | MBS has developed deep relationships with its wholesale customer base as a result of its substantial inventory of used textbooks, a comprehensive catalog of textbooks, superior service and systems support. MBS Wholesale provides inventory management, hardware and point-of-sale software to approximately 477 college bookstores. |

• | Direct Access to Students and Faculty: We have excellent visibility into the needs of our customers. At our physical campus stores, we serve as social hubs for over 5 million students and their faculty, allowing us to forge deep customer relationships and seamlessly integrate their systems with our technology. For our MBS Direct and Wholesale businesses, we are connected with our customers’ students online and through our proprietary systems. Our multi-channel strategies focus on building close relationships and one-to-one connections with our students, faculty, administrators and alumni, whether in-store, online or mobile. We provide connectivity to our services whether our customers are in the classroom, at the stadium, or at orientation. Our Student Point of View (POV) panel gains insights from more than 8,000 college students, and allows us to adjust our offerings to better meet expressed needs. Through this unique relationship with students, we also operate as a media channel that drives revenue through brands looking to target the college demographic. |

• | Integrated Systems with Our Customers: We are deeply ingrained in the course material adoption processes of our customers. Both BNC and MBC have highly integrated online systems that streamline the adoption process for faculty, enabling them to research, update, approve and submit textbook adoptions online, as well as make informed decisions on adoptions as the application gives real-time information regarding title availability, edition status and price. |

• | Stable, Long-Term Contracts: BNC physical bookstores are operated under management contracts with colleges and universities that are typically for five year terms with renewal options, but can range from one to 15 years, and are typically cancelable by either party without penalty with 90 to 120 days' notice. From Fiscal 2014 through Fiscal 2017, 94% of these contracts were renewed or extended, often before their termination dates. Virtual bookstores offered through MBS Direct operate under a contract with the school as the exclusive seller of course materials. Over the past three years, we have retained more than 95% of our contracts, with the majority of the contracts being automatically renewed as per the contract terms or renewed before their expiration dates without going through a formal bid process. |

7

• | Seasoned Management Team: Both BNC and MBS possess experienced senior management teams with proven track records, and demonstrated expertise in bookstore outsourcing, virtual bookstore operations, wholesale distribution and fulfillment operations, content distribution, marketing and retail operations, and in scaling digital educational and other digital products and services. |

Growth Drivers

The primary factors that we expect will enable us to grow our business are as follows:

• | Increasing Market Share with New Accounts: New store openings are an important driver of growth. In Fiscal 2017, BNC signed 38 new stores for estimated first year annual sales of $118 million. Currently, approximately 52% of college and university affiliated physical bookstores in the United States are operated by their respective institutions. Based on the anticipated continuing trend towards outsourcing in the campus bookstore market, we intend to aggressively pursue these opportunities to grow BNC’s core business. Additionally, our acquisition of MBS expands our addressable market to include K-12 and higher education schools that prefer virtual bookstore solutions. MBS Direct signed 80 new accounts in Fiscal 2017 for $17 million of estimated annual sales. Our ability to offer existing and prospective clients physical, virtual and hybrid bookstore models is a key element of our competitive strategy. We believe that our message of affordability and convenience will continue to gain traction and allow us to capture market share by offering flexible physical and virtual bookstores options, as well as digital solutions. |

• | Scalable and Advanced Digital Solutions: We leverage our digital technology platform to provide product and service offerings designed to address the most pressing issues in higher education, such as affordable and accessible course materials, retention solutions driven by our analytics platform, and products designed to drive and improve student outcomes. Through our LoudCloud platform, we address the growing demand for alternative forms of educational materials and learning tools. By focusing on advanced OER courseware, we plan to continue to enhance and grow our digital content and services in an efficient, low-cost/high-value manner to complement our printed textbook businesses. Additionally, we believe that our predictive analytics solution has strong benefits for higher education institutions, and therefore potentially strong demand characteristics in this emerging space. Our recently announced partnership with Unizin underscores the value proposition of our predictive analytics solutions in helping client institutions improve student success rates and retention. |

• | Expanding Strategic Opportunities through Acquisitions and Partnerships: We intend to pursue strategic relationships with companies that enhance our educational services or distribution platform, or create compelling content offerings. Our acquisitions and partnerships this fiscal year helped us expand into new educational verticals and markets, such as workforce and skills gap training and K-12, but other markets for expansion remain, including international markets. These will continue to be opportunistically evaluated. |

Segments

Effective with the acquisition of MBS on February 27, 2017, we have determined that we operate two reportable segments: BNC and MBS. We identified our segments based on the way our business is managed (focusing on the financial information distributed) and the manner in which our chief operating decision maker allocates resources and assesses financial performance.

BARNES & NOBLE COLLEGE

General

As of April 29, 2017, BNC operates 769 physical campus bookstores, the majority of which also have school-branded e-commerce sites operated by BNC, and BNC also includes our digital operations. During Fiscal 2017, we opened 38 stores with estimated first year annual sales of $118 million, and closed 20 stores, primarily comprised of satellite store locations that we elected to close and we continue to operate the main contract, contracts with low sales volume, as well as those contracts that may have been lost in a competitive bid process. As of June 16, 2017, BNC has signed additional contracts for 23 new physical stores with estimated first year annual sales of $50 million, which we expect to open during our Fiscal 2018.

Contracts

Our BNC stores are typically operated under management agreements with the college or university to be the official university bookstore and the exclusive seller of course materials and supplies, including physical and digital products sold in-store, online or through learning management systems. We offer existing and prospective clients physical, virtual and hybrid bookstore models. Agreements are typically five years with renewal options, but can range from one to 15 years, and are typically cancelable by either party without penalty with 90 to 120 days' notice. We pay the school a percentage of sales for the right to be the official college or university bookstore and the use of the premises; more than half of our agreements do not have any minimum guaranteed amount to be paid to our partners. In addition, we have the non-exclusive right to sell all items typically sold in a college bookstore both in-store and online. We also have the ability to integrate our systems with the university’s systems in order to accept student financial aid, university debit cards and other forms of payment. We obtain student and faculty email lists for direct communication which provide for seamless integration into the university community and potential co-branded marketing opportunities.

8

Over the past four years, we have renewed more than 94% of our agreements, with the majority of the agreements being renewed before their expiration dates and without going through an RFP process.

Customers and Distribution Network

We leverage our BNC physical bookstores, e-commerce sites and digital platform to serve and interact with the key constituents in our business ecosystem and act as a key partner for students, universities and publishers. As of April 29, 2017, we operate 769 physical bookstores nationwide.

The number of BNC college and university bookstores operations located in the United States as of April 29, 2017, is listed below:

STATE | NUMBER OF STORES | STATE | NUMBER OF STORES | STATE | NUMBER OF STORES | |||||

Alabama | 18 | Kentucky | 30 | North Dakota | 1 | |||||

Arizona | 8 | Louisiana | 14 | Ohio | 42 | |||||

Arkansas | 7 | Maryland | 20 | Oklahoma | 5 | |||||

California | 46 | Massachusetts | 29 | Oregon | 5 | |||||

Colorado | 7 | Michigan | 36 | Pennsylvania | 64 | |||||

Connecticut | 14 | Minnesota | 7 | Rhode Island | 3 | |||||

Delaware | 2 | Mississippi | 8 | South Carolina | 20 | |||||

District of Columbia | 6 | Missouri | 9 | South Dakota | 2 | |||||

Florida | 45 | Nebraska | 1 | Tennessee | 13 | |||||

Georgia | 14 | Nevada | 2 | Texas | 65 | |||||

Hawaii | 3 | New Hampshire | 4 | Virginia | 19 | |||||

Illinois | 19 | New Jersey | 22 | Washington | 21 | |||||

Indiana | 14 | New Mexico | 6 | West Virginia | 11 | |||||

Iowa | 5 | New York | 67 | Wisconsin | 6 | |||||

Kansas | 2 | North Carolina | 27 | |||||||

9

Product and Service Offerings

Our campus stores are a social and academic hub through which students can access affordable course materials and affinity products, including new and used print and digital textbooks, which are available for sale or rent; emblematic apparel and gifts; trade books; computer products; school and dorm supplies; café offerings; convenience food and beverages; and graduation products. BNC product offerings also include a suite of digital content, software, and services through our LoudCloud platform, such as learning analytics, a variety of courseware developed utilizing OER, and competency-based learning solutions, which allow students to advance in a course based on their ability to master a skill or competency at their own pace.

BNC’s full suite of product offerings include:

• | Course Material Sales and Rentals: Sales and rentals of print textbooks are a core revenue driver. Our online platform and registration solutions (discussed below) are deeply ingrained in our partner schools’ textbook selection process.We work directly with faculty to ensure the textbooks they have chosen for their courses are available in all required formats before the start of classes. MBS’s wholesale distribution channel enables us to optimize our textbook sourcing, purchasing and liquidation processes, and we are able to more efficiently source and distribute a comprehensive inventory of affordable course materials to customers with the highest and greatest need. On average, MBS Wholesale has approximately 300,000 textbook titles in stock at any given time to support the course offerings of our partner schools. |

• | OER Courseware: In Fall 2016, we launched OER courseware, a turnkey solution for colleges and universities, within our existing physical bookstore footprint and beyond, which offers advanced, affordable learning materials built on a high-quality foundation of OER and enhanced with content such as videos and self-assessments. Our high-quality OER courseware significantly reduces course material costs for students and enables easier implementation for faculty, all with the objective of ultimately improving learning outcomes. Our courseware is delivered digitally on our LoudCloud platform, with analytics integrated into the solution, and companion print versions available to students and educators who prefer the flexibility to learn and teach in either format. Courseware offerings include general education courses, including sociology, psychology and economics, which were piloted in 2016 at institutions such as the Pennsylvania State University, Cuyahoga Community College and West Liberty State College. |

• | eTextbooks: We have partnered with VitalSource, a global leader in building, enhancing and delivering digital content, on our digital reading platform and a broad digital catalog. |

• | General Merchandise: We drive general merchandise sales through both our instore and online channels, including pop up retail locations at major sporting events, throughout the academic year. Our stores feature collegiate and athletic apparel, other custom-branded school spirit products, technology, supplies and convenience items. We continue to see significant year over year growth in our e-commerce sales and in the demand for our True Spirit fan sites, which are dedicated virtual stores that appeal specifically to the alumni and sports fanbase. As of April 29, 2017, we operate 61 True Spirit sites. Additionally, in June 2016, we enhanced our merchandise offering through the acquisition of Promoversity, a custom merchandise supplier and e-commerce storefront solution serving the collegiate bookstore business and its customers. This acquisition provides us with a wide customer base outside of the BNC footprint, as Promoversity’s standalone e-commerce solution can serve any school, corporation or group looking for customized apparel, corporate gifts and novelties, and merchandise. |

• | Cafes and Convenience Stores: We operate 83 customized cafés, featuring Starbucks Coffee®, and 17 stand-alone convenience stores, as well as diverse grab-and-go options including organic, vegan, gluten-free and ethnic fare for students. These offerings increase traffic and time spent in our physical stores. |

• | Brand Partnerships: Through our unique relationship with students, colleges and universities, and our premier position on campus, we operate as a media channel for brands looking to target the college demographic, and derive revenue from these marketing share programs. We create strategic, integrated campaigns which include research, email, social media, display advertising, on-campus events, signage, and sampling. Our client list includes brands like Target, MasterCard, GEICO, Kellogg’s, Verizon, Samsung Pay, and more. |

Platform Services

• | FacultyEnlight®: Used by approximately 310,000 faculty members, FacultyEnlight®, our proprietary online platform enhances content search, discovery and adoption (i.e. textbook selection) by faculty on each campus, enabling them to find and select the course materials that are both relevant to their subject matter and affordable to their students. FacultyEnlight®, which is available to faculty at no cost, also provides us with a communication platform to connect with faculty directly, allowing us to better understand their needs, preferences and challenges when it comes to the textbook adoption process, and deliver our affordability message. |

• | Campus Connect Technologies™: Our Campus Connect Technologies™ platform is customizable technology that delivers a seamless experience, providing students and faculty with the ability to research, find and purchase the most affordable course materials. The platform includes registration integration, learning management system (“LMS”) integration, real-time financial |

10

aid platform, point of sale ("POS") platform and course fee solution. Through our fully integrated purchasing process, students can purchase their course materials in-store or online, or buy them when registering for classes through our Registration Integration solution.

• | LoudCloud platform: Through our LoudCloud platform, we address the growing demand for alternative forms of educational materials and learning tools. LoudCloud is a sophisticated digital platform comprised of learning analytics, LoudSight; advanced OER courseware; and competency learning solutions. |

Our LoudSight predictive analytics solution captures and analyzes key demographic, behavioral and performance metrics from students, allowing educators to identify, monitor and support at-risk student to improve student success. LoudCloud's analytics solution connects disparate systems on campus, builds predictive models based upon data collected by institutions, and presents advisors with a unified view of the factors that drive student success on their campus. By sharing predictive models with institutions, LoudCloud promotes collaboration to ensure advisors and administrators understand what drives student performance. Additionally, LoudSight integrates with campus communication systems, allowing advisors and faculty to easily reach out to students for support in a timely manner. LoudSight has the ability to capture and analyze over 200 parameters across demographic, performance and participation data points. Its powerful predictive engine has the ability to support advisors, faculty and students with real-time alerts and insights into managing and improving student outcomes.

◦ | Through our partnership with Instructure, a leading educational technology company and creator of the Canvas LMS, LoudSight can be fully integrated in Canvas’s platform, providing higher education institutions with actionable insights that provide a comprehensive view of the student journey. Instructure is a leading LMS provider at schools across the country, and we believe the ability to integrate with a school’s Canvas system makes our analytics solution more efficient and effective. |

◦ | We entered into an agreement with Unizin, Ltd. ("Unizin") in May 2017 to provide its 22 member universities with LoudSight. As a result, faculty and advisors will have access to a customized solution that helps educators identify, monitor, and support at-risk students, with the goal of improving student success rates and retention. |

• | Career Now: Our Career Now initiative provides early career preparation for students through personal brand building workshops, faculty resource guides, career prep podcasts and dedicated content through The College Juice, our student blog. We also help build a stronger connection between students and campus resources, including career fairs, mentors, career sponsors and other career services. These career preparatory programs help students achieve their post-graduation goals, which supports our campus partners’ recruitment and retention goals. |

Merchandising and Supply Chain Management

Our purchasing procedures vary by product type (i.e. textbooks, general merchandise or trade books). Purchases are made at the store level based on the relationships our managers have with the faculty, with strategic corporate oversight, while maintaining appropriate inventory levels.

After titles are adopted for an upcoming term, we determine how much inventory we will need to purchase based on several factors, including student enrollment and the previous term’s textbook sales history. We use our automated sourcing systems to determine if our stores have the necessary new or used books on hand and may transfer the inventory to the appropriate store. MBS has historically been one of our largest suppliers of new and used books, and our acquisition of MBS significantly increased our textbook supply at competitive prices. MBS’s broad wholesale distribution channel and warehousing systems also drive inventory efficiencies, allowing us to optimize our textbook sourcing, purchasing and liquidation processes.

After internal sourcing, we purchase books from outside suppliers. As part of our contracts with institutions, we guarantee that we will order textbooks for all courses. Our primary suppliers of new textbooks include Pearson Education, Cengage Learning, McGraw-Hill, MPS, and John Wiley & Sons. Our primary suppliers of used textbooks are students, through returns of previously rented and purchased books. The stores offer a "Cash for Books" program in which students can sell their books back to the store at the end of the semester, typically in December and May. Students typically receive 50% of the price they originally paid for the book if it has been adopted for a future class or the current wholesale price if it has not. Both unsold textbooks and trade books are generally returnable to publishers for full credit. For textbook sales and rentals, we utilize our sophisticated inventory management platforms to manage pricing and inventory across all our stores.

The larger stores feature an expanded selection of trade (general reading) books and use the Barnes & Noble, Inc. Book Master system, a proprietary merchandising system licensed from Barnes & Noble, Inc. Our merchants meet with publishers on a regular basis to identify new titles and trends to support this changing business. In the smaller stores, trade book purchasing is controlled at the store level.

General merchandise vendors and products are initially selected by our merchants using the analytics and insights from our planning and allocation systems. This data is used to establish benchmarks across school type, region and the socio-economics of each of our partner institution’s student base to help local store management team forecast sales and trends. Recommended

11

assortments are provided to the stores, and stores then make selections based on the perceived needs of each campus, reaching back out to the home office merchants with their recommendations on any additional campus specific needs.

Omnichannel Retailer and Customer Marketing Strategies

We operate bookstores in our dynamic, multichannel format virtually and on campuses of state universities, private universities and community colleges of various sizes. Our omnichannel strategies focus on building close relationships and one-to-one connections where our customers need us to be - in-store, online, mobile, at the stadium, at orientation, or wherever they are.

Students, Parents, Alumni

We have flexible research channels that help us stay ahead of the rapidly changing needs and behaviors of our customers, and proactively respond with dynamic solutions. Our Student Point of View (POV) panel gains insights from more than 8,000 college students, and helps us to create the ideal customer experience.

Our marketing efforts are centered around an active digital community of over 6.6 million people, which includes engaged email subscribers and continuous dialogue with customers on our school-customized social media channels, including Facebook, Instagram and Twitter, as well as our student blog, The College Juice. Our exclusive Student POV online panel of over 8,000 students nationwide and our Parent POV online panel of over 2,800 parents help us to better understand their attitudes, values and behaviors. Using a marketing automation platform, we segment students based on demographics and purchasing behavior to ensure our audience receives the most relevant messages and experience. Our dynamic email campaigns educate students on format and affordability options as well as ongoing promotions from game day to graduation.

Through our search engine marketing strategies, BNC has been able to grow online textbook and apparel sales significantly. BNC’S official online bookstores for colleges or universities drove over $438 million of sales in Fiscal 2017. Nationwide, during the current fiscal year, we have built more than 695,000 connections with incoming students and their parents. These efforts have allowed us to maintain and expand market share and cement the college bookstore as the student's first choice for everything they need for academic success.

Promoversity has provided us with the ability to further customize our e-commerce solution to promote our partners’ brands more effectively and drive on-campus merchandise sales. Our True Spirit e-commerce sites for athletic branded merchandise continue to build our partner schools’ brands through alumni and athletics, fostering school spirit and capturing the excitement of collegiate sports. Our ability to support and promote our partner schools’ brands strengthens and deepens our relationships with the administration, faculty, alumni, parents and students. Additionally, our access to alumni through university alumni offices, including over 920,000 alumni with existing customer accounts, allow us to leverage digital marketing strategies on our dedicated fan and alumni e-commerce sites focused on athletic game day and other milestone events for further general merchandise sales growth in school-spirit apparel and related items.

Seasonality

BNC’s business is highly seasonal, with the major portion of sales and operating profit realized during the second and third fiscal quarters, when college students generally purchase and rent textbooks for the upcoming semesters. Revenue from the rental of physical textbooks is deferred and recognized over the rental period commencing at point of sale. Revenue from the rental of digital textbooks is recognized at time of sale. Our fiscal year is comprised of 52 or 53 weeks, ending on the Saturday closest to the last day of April.

MBS TEXTBOOK EXCHANGE

In February 2017, we acquired MBS, the largest contract operator of virtual bookstores for the higher education and private/parochial K-12 school markets, and one of the largest textbook wholesalers in the United States. For additional information, see Item 8. Financial Statements and Supplementary Data - Note 4. Acquisitions and Strategic Agreements.

This acquisition significantly enhances our competitive positioning, increasing our addressable market to include K-12 schools and higher education institutions that need virtual bookstore solutions as an alternative to or in addition to a physical store on campus. The acquisition also increases our addressable market for our digital courseware and analytics solutions, and enables us to generate more value from the textbook marketplace through inventory and procurement synergies.

Our MBS subsidiary operates two highly integrated businesses: MBS Direct and MBS Wholesale. The MBS Direct business is the largest contract operator of virtual bookstores for college and university campuses, and private/parochial K-12 schools, operating 712 virtual bookstores. MBS Direct signed 80 new accounts in Fiscal 2017 with estimated first year annual sales of $17 million, and has signed additional contracts to open 46 new accounts in Fiscal 2018 for estimated first year annual sales of $8 million. MBS Direct offers new and used print and digital textbooks, which are available for sale or rent. Our ability to offer existing and prospective clients physical, virtual and hybrid bookstore models is a key element of our competitive strategy. Additionally, MBS Direct sells textbooks directly to students through textbooks.comSM, one of the largest e-commerce sites for new and used textbooks.

12

MBS Wholesale is one of the largest textbook wholesalers in the country, providing an expanded selection of new and used textbooks at a lower cost of supply. MBS Wholesale business centrally sources and sells new and used textbooks to physical college bookstores, including BNC’s campus bookstores. MBS Wholesale purchases new and used textbooks from bookstore operators, institutional bookstores, book dealers, publishers, other distributors and wholesalers, and students. To secure a steady supply of in-demand used books, MBS Wholesale has a large national sales force to call on college bookstores. MBS Wholesale has deep relationships with clients due to the large inventory of used textbooks, a comprehensive catalog of textbooks, superior service and systems support. The MBS Database Buying Guide has the most complete and accurate source of college textbook information available.

Contracts

Virtual bookstores offered through MBS Direct operate under a contract with the school as the exclusive seller of course materials. Agreements typically have a term that ranges between 3-5 years, with automatic renewal periods. Over the past three years, we have retained more than 95% of our contracts, with the majority of the contracts being automatically renewed as per the contract or renewed before their expiration dates without going through an RFP process.

Customers and Distribution Network

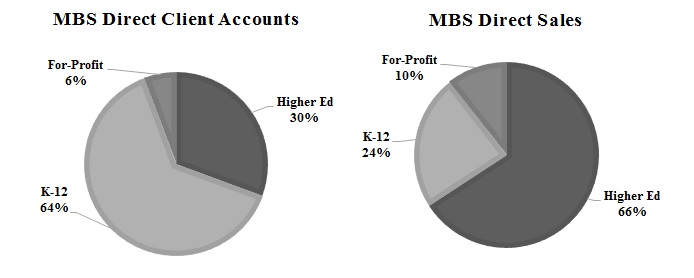

MBS Direct operates 712 virtual bookstores, including 454 virtual stores at K-12 schools. Through contracts with its clients, MBS Direct operates as the institution’s official source of course materials with exclusive rights to booklists and access to online programs that link course materials to the courses offered by the school. MBS Direct utilizes Course Director, a web-based product that allows faculty and/or staff to research, update, approve and submit textbook adoptions online, as well as make informed decisions on adoptions based on real-time information regarding title availability, edition status and price. This real-time information is primarily sourced from the MBS Wholesale used textbook inventory. MBS also operates textbooks.comsm one of the largest e-commerce sites for new and used textbooks. This division is primarily for direct-to-student sales.

13

The number of MBS Direct accounts located in the United States as of April 29, 2017, is listed below:

Number of Stores | Number of Stores | Number of Stores | ||||||||||||||

STATE | K-12 | Higher Ed | STATE | K-12 | Higher Ed | STATE | K-12 | Higher Ed | ||||||||

Alabama | 12 | 3 | Kentucky | 8 | 1 | Ohio | 11 | 12 | ||||||||

Alaska | — | 6 | Louisiana | 14 | 2 | Oklahoma | 3 | 2 | ||||||||

Arizona | 3 | 3 | Maine | 2 | 8 | Oregon | 1 | 9 | ||||||||

Arkansas | 1 | 3 | Maryland | 28 | 7 | Pennsylvania | 13 | 17 | ||||||||

California | 58 | 14 | Massachusetts | 16 | 6 | Rhode Island | 3 | — | ||||||||

Colorado | 7 | — | Michigan | 17 | 8 | South Carolina | 8 | 2 | ||||||||

Connecticut | 14 | 2 | Minnesota | 1 | 6 | South Dakota | — | — | ||||||||

Delaware | 3 | 1 | Mississippi | 2 | — | Tennessee | 4 | 1 | ||||||||

District of Columbia | 5 | — | Missouri | 13 | 16 | Texas | 43 | 9 | ||||||||

Florida | 33 | 12 | Nebraska | 1 | 6 | Utah | 1 | 2 | ||||||||

Georgia | 24 | 12 | Nevada | 3 | — | Vermont | 1 | 2 | ||||||||

Hawaii | 15 | — | New Hampshire | 2 | 4 | Virginia | 26 | 9 | ||||||||

Idaho | — | 2 | New Jersey | 5 | 4 | Washington | 6 | 3 | ||||||||

Illinois | 14 | 16 | New Mexico | — | 3 | West Virginia | — | 5 | ||||||||

Indiana | 3 | 2 | New York | 17 | 8 | Wisconsin | 3 | 1 | ||||||||

Iowa | — | 10 | North Carolina | 9 | 9 | International | — | 1 | ||||||||

Kansas | 1 | 7 | North Dakota | — | 1 | Puerto Rico | — | 1 | ||||||||

Product and Service Offerings

MBS’s full suite of product offerings includes:

• | Virtual Bookstores: MBS Direct services 712 virtual bookstores with a comprehensive e-commerce experience and a broad suite of affordable course materials, including new and used print and digital textbooks, which are available for sale or rent. MBS Direct offers a robust used textbook selection, unique guaranteed buyback program, dynamic pricing, and marketplace offerings. |

• | Wholesale Textbook Distribution: MBS Wholesale centrally sources and sells new and used textbooks to over 3,700 physical college bookstores, including BNED’s 769 campus bookstores. Its large inventory of used textbooks consists of approximately 300,000 textbook titles in stock, and it has a highly automated distribution facility that process more than 13 million textbooks annually. Additionally, MBS Wholesale provides inventory management, hardware and point-of-sale software to approximately 477 college bookstores. |

• | OER Courseware: MBS’s broad base of wholesale and virtual bookstore customers provides us with new sales opportunities for LoudCloud’s digital suite of course materials and platforms as discussed above under the BNC segment discussion. |

• | E-Commerce Site: Through textbooks.comSM, MBS offers new, used and digital textbooks online directly to students. |

• | eTextbooks: MBS has partnered with VitalSource, a global leader with a broad digital catalogue to build, enhance and deliver digital content. |

Platform Services

MBS Direct utilizes Course Director, a web-based product that allows faculty and/or staff to research, update, approve and submit textbook adoptions online, as well as make informed decisions on adoptions as the application gives real-time information regarding title availability, edition status and price. This real-time inventory information is leveraged from the inventory sourced first from MBS Wholesale, primarily for used textbooks. Using the MBS Direct system ensures that the fulfillment order is directed first to MBS Wholesale before other sources of inventory are utilized.

Our MBS Wholesale business also provides inventory management, hardware and point-of-sale software to more than 477 college bookstore customers. MBS provides on-site installation for point-of-sale terminals and servers, and offers technical assistance through user training and our support center facility. The cost savings and ease of deployment ensure clients get the

14

most out of their management systems and create strong customer loyalty. These systems also direct all orders through MBS, giving MBS first rights to fill or refuse the order.

Supply Chain Management

MBS is one of our largest suppliers of used textbooks, as well as new textbooks. An extensive national sales force secures a steady supply of highly-prized used books, which is critical to the success of the MBS Wholesale business. MBS’s broad wholesale distribution channel and warehousing systems also drive inventory efficiencies, allowing us to optimize our textbook sourcing, purchasing and liquidation processes. We can leverage MBS Wholesale’s distribution channel and warehousing systems to more efficiently source and distribute a robust, comprehensive inventory of affordable course materials to customers with the highest and greatest need. Through the proprietary MBS Database Buying Guide, we have access to the best maintained, most accurate, and most complete source of college textbook information available - a key asset that allows us to develop superior supply and demand insights and risk management capabilities.

MBS’s primary suppliers of used textbooks are students, through returns of previously rented and purchased books. MBS also purchases new and used textbooks from BNC, other bookstore operators, institutional bookstores, book dealers, publishers, other distributors and other wholesalers. MBS offers a "Cash for Books" program in which students can sell their books back to the store at the end of the semester, typically in December and May.

Customer Marketing Strategies

Students

MBS student marketing programs promote the retail businesses of MBS Direct and textbooks.comSM. MBS Direct marketing efforts target the student population of contracted schools. We email students frequently throughout the year to promote the online bookstore, offer purchasing incentives and encourage buyback, in addition to other communications. Textbooks.comSM marketing strategies target an online population of students, lifelong learners, parents and general textbook shoppers through a variety of channels including email, search engine marketing, affiliate marketing and display marketing.

School Administrators

To market MBS Direct and Wholesale services, MBS maintains an active contact list of school management and administrators of over 37,000 contacts. We produce and distribute print and digital marketing campaigns to this list several times throughout the year. MBS employs a field sales and marketing force tasked with representing the entire MBS line of products and services to schools across North America.

During the last fiscal year, we have built more than 34,000 connections with current and potential clients through our blog sites and social media presence, and have had over 1.6 million visits to our primary business websites, mbsbooks.com and mbsdirect.net. These efforts have allowed us to capture market share and successfully engage administrators.

Seasonality

MBS’s business is highly seasonal. For MBS’s retail operations (virtual bookstores), a major portion of sales and operating profit are realized during the second and third quarters, when students generally purchase and rent textbooks for the upcoming semesters. For MBS’s wholesale business, a major portion of sales and operating profit is realized during the first, second and third fiscal quarters, as it sells textbooks for retail distribution, which somewhat offsets the decreased first quarter sales attributable to our retail business.

BUSINESS CONDITIONS AND COMPETITION

The market for educational materials is undergoing unprecedented change. Overall spending on education, including tuition, continues to increase dramatically. As tuition and other costs rise, colleges and universities face increasing pressure to attract and retain students and provide them with innovative, affordable educational content and tools that support their educational development.

Current competitive dynamics in the market for distribution of course materials include:

• | A Majority of Traditional Campus Bookstores Have Yet to be Outsourced: Approximately 52% of college and university affiliated bookstores in the United States are operated by their respective institutions. As the delivery of educational materials continues to evolve, driven in large part by the growth of rentals and digital content, and the complexity of modern campus bookstore operations increases, institutions are increasingly outsourcing bookstore operations to third parties such as us, because we can offer a complete set of solutions to students and faculty. We believe that we will benefit from the continuing trend towards outsourcing across the physical and virtual bookstore market. Our expanded capabilities enable us to customize our bookstores to meet customer needs, offering our partners the option of physical, virtual and hybrid bookstore models. |

15

• | Direct Relationship with a Coveted Demographic: Due to the disproportionate impact on trend-setting and early adoption, marketing to college students is important for many brands, as they seek more effective methods to engage with this audience. We work with a number of brands in partnership marketing efforts, often engaging our Student POV panel of more than 8,000 students to learn how a certain brand is perceived on campus. The importance of this demographic provides a significant opportunity to further monetize our direct relationship with more than 6 million students both during and beyond their college years. |

• | Increased Use of Online and Digital Platforms as Companions to Printed Course Materials: Students and faculty can now choose from a wider variety of educational content and tools than ever before, delivered across both print and digital platforms. Students and faculty are increasingly relying on online and digital platforms as a means to discover, consume and share educational content and access affordable non-traditional educational content, including online coursework and supplemental materials. Whereas some companies are creating digital delivery systems that would seek to make traditional textbooks obsolete, others are developing new technologies to complement traditional offerings. Importantly, we have the ability to adjust and grow our digital offering efficiently to complement our printed textbook sales and rental business. |

• | Enrollment Trends: Community college enrollments saw continued declines in 2016, but the overall enrollment trend is expected to be positive over the longer term, and we remain confident in the industry projections of higher education enrollments to reach 22.6 million students by 2026. Technology-enabled education is a key growth area in the higher education industry, with an increasing number of students taking courses away from a traditional campus. According to a Digital Learning Compass report, students taking at least one distance education course comprised 29.7% of all higher education enrollments as of fall 2015. Online degree program enrollments continue to grow, even in the face of declining overall higher education enrollment. Our comprehensive digital offering, particularly with our OER courseware program and analytics capabilities, as well as our virtual bookstore solution, which provides students with the ability to purchase course materials directly through a dedicated e-commerce site, leave us well positioned to capitalize on this trend. |

• | Distribution Network Evolving: The way course materials are distributed and consumed is changing significantly, a trend that is expected to continue. It is clear that significant change in the distribution of course materials is already underway as a result of start-ups promoting free online textbooks and generating revenue from related services, institutions licensing digital materials and providing them to students for a fee, or the surge of textbook rental programs in campus bookstores and online platforms. In addition to the official physical or virtual campus bookstore, course materials are also sold through off-campus bookstores, e-commerce outlets, digital platform companies, publishers’ direct sales to institutions and students, and student-to-student marketplaces. |

The market for course materials, including textbooks and supplemental materials, is intensely competitive and subject to rapid change. We are experiencing growing competition from alternative media and alternative sources of textbooks and course-related materials, such as websites that sell or rent textbooks, eTextbooks, digital content and other merchandise directly to students; online resources, including open educational resources; publishers including Cengage, Pearson and McGraw Hill, bypassing the bookstore distribution channel by selling directly to students and educational institutions; print-on-demand textbooks; textbook rental companies; and student-to-student transactions over the Internet.

In addition to the competition we face from alternative distribution sources, we also have competition from other college bookstore operators and educational content providers, including Akademos, a virtual bookstore and marketplace for academic institutions; Amazon.com, an e-commerce operator and a provider of contract services to colleges and universities; BBA Solutions, a college textbook retailer; bn.com, the e-commerce platform of Barnes & Noble, Inc.; Chegg.com, an online textbook rental company; Civitas Learning, a learning analytics platform; eCampus, an online provider of course materials; Follett Corporation, a contract operator of campus bookstores; IndiCo, an entity created by National Association of College Bookstores (“NACS”); Texas Book Company, bookstore management and operations; and Vital Source Technologies, Inc., a digital course materials provider. We also have competition from providers of eTextbooks, such as Apple iTunes, Blackboard, Google, and Redshelf, and various private textbook rental websites.

In addition, Akademos and Amazon have recently begun to develop relationships with colleges and universities to provide online bookstore solutions which not only competes with our physical bookstore operations but also competes with our subsidiary MBS’ Direct virtual solution. MBS Direct also faces competition from Ambassador Educational Solutions, eCampus, edMap, EdTech, Follett Corporation, Texas Book Company, Tree of Life, and VitalSource Technologies, Inc. MBS Wholesale competes with Amazon, BBA Solutions, Follett, IndiCo, Nebraska Book Company, and Texas Book Company.

Competitors that compete with our general merchandise offerings include Fanatics, Sodexo & Aramark, online retailers, and physical and online office supply stores.

Students often purchase from multiple textbook providers, are highly price sensitive, and can easily shift spending from one provider or format to another. As a consequence, in addition to being competitive in the services we provide to our customers, our textbook business faces significant price competition. Some of our competitors have adopted, and may continue to adopt, aggressive pricing policies and devote substantial resources to marketing, website and systems development.

16

In addition, a variety of business models are being pursued for the provision of print and digital textbooks, some of which may be more profitable or successful than our business model. Furthermore, the market for course materials is diluted from counterfeiting and piracy of digital and print copies or illegal copies of selected chapters made by students or others; user and faculty created content; and sharing or non-purchase of required course materials by students.

TRENDS AND OTHER FACTORS AFFECTING OUR BUSINESS

Current trends and other factors affecting our business include:

• | Overall Economic Environment, College Enrollment and Consumer Spending Patterns: Our business is affected by funding levels at colleges and universities, by changes in enrollments at colleges and universities, and spending on textbooks and general merchandise. The growth of our business depends on our ability to attract new students and to increase the level of engagement by existing students. Historically, increasing enrollment has been a significant driver of sales growth at campus bookstores, a trend that is expected to continue in the long term. According to the National Center for Education Statistics of the U.S. Department of Education ("NCES"), total enrollment in post-secondary degree-granting institutions is expected to increase 9.6%, from 20.6 million in 2012 to 22.6 million in 2026 driven by increased demand for educational services. |

• | Supply Chain and Inventory: Since the demand for used and new textbooks has historically been greater than the available supply, our financial results are highly dependent upon MBS Wholesale’s ability to build its textbook inventory from suppliers in advance of the selling season. |

• | Demand for Digital Offerings: Over the longer-term, we anticipate significant new opportunities for our digital product offerings. Through our LoudCloud platform, we address the growing demand for alternative forms of educational materials and learning tools. Technology-enabled learning is a key growth area in the higher education industry, as a growing number of students are enrolling in online digital courses, and we are ready to meet demand with our virtual bookstore and e-commerce solutions, as well as our OER courseware offering. |

• | New and Existing Bookstore Contracts: We expect awards of new accounts resulting in new physical and virtual store openings will continue to be an important driver of future growth in our business. We are awarded additional contracts for stores as colleges and universities decide to outsource their bookstore, and we also obtain new contracts for stores that were previously operated by competitors. Our virtual bookstore capability expands our addressable market to include schools that cannot or prefer not to have a physical campus bookstore. Sales trends are primarily impacted by new store openings, increasing the students and faculty served, as well as changes in comparable store sales and store closings. Closed stores are primarily comprised of satellite store locations that we elected to close and we continue to operate the main contract, contracts with low sales volume, as well as those contracts that may have been lost in a competitive bid process. During Fiscal 2017, BNC opened 38 stores with estimated first year annual sales of $118 million, and closed 20 stores. As of June 16, 2017, BNC has signed additional contracts for 23 new physical stores with estimated first year annual sales of $50 million, which we expect to open during our Fiscal 2018. MBS Direct has opened 80 virtual bookstores during the 52 weeks ending April 29, 2017, with estimated first year annual sales of $17 million, and has signed additional contracts to open 46 new accounts in Fiscal 2018 for estimated first year annual sales of $8 million. |

• | Campus Bookstore Outsourcing: We continue to see increasing trends towards outsourcing in the campus bookstore market, including virtual bookstores and online marketplace websites. We also continue to see a variety of business models being pursued for the provision of textbooks, course materials and general merchandise. Contract costs, which are included in cost of sales, and primarily consist of the payments we make to the colleges and universities to operate their official bookstores (management service agreement costs), including rent expense, have generally increased as a percentage of sales as a result of increased competition for renewals and new store contracts. |

• | Course Materials Market: In addition to the competition in the services we provide to our customers, our textbook business faces significant price competition. Many students purchase from multiple textbook providers, are highly price sensitive and can easily shift spending from one provider or format to another. Some of our competitors have adopted, and may continue to adopt, aggressive pricing policies and devote substantial resources to marketing, website and systems development. As we expanded our textbook rental offerings, students have been shifting away from higher priced textbook purchases to lower priced rental options, which has resulted in lower textbook sales and increasing rental income. After several years of comparable store sales declines, primarily due to lower textbook unit volume, during the 52 weeks ended May 2, 2015, our comparable store sales trends improved for both textbooks and general merchandise. For the 52 weeks ended April 29, 2017, our comparable store sales declined by 3.0% primarily due to lower community college enrollment and general weakness in the retail environment. |

• | Retail Environment: BNC general merchandise sales, which are subject to short-term fluctuations driven by the broader retail environment, continue to increase over the long term as our product assortments continue to emphasize and reflect the changing consumer trends, and we evolve our presentation concepts and merchandising of products in stores and online. However, lighter store traffic and a continued reluctance by the consumer to make discretionary purchases have created a softer retail |

17

environment. We are confident in our assortment and have received encouraging customer response to our promotional and digital marketing efforts, especially as it relates to web orders. We are encouraged by the growth in our e-commerce sales and expect general merchandise sales to improve as the general retail environment rebounds, but we are taking a cautious approach given the overall uncertainty in the market.

EMPLOYEES

As of April 29, 2017, BNC and MBS had approximately 5,800 and 900 full time and regularly scheduled part-time employees, respectively, or a total of 6,700 full time and regularly scheduled part-time employees. In addition, both BNC and MBS hired approximately 13,000 and 350 additional temporary employees, respectively, during peak periods during Fiscal 2017. Our employees are not represented by unions, with the exception of 25 employees. We believe that our relationship with our employees is good.

EXECUTIVE OFFICERS

The following sets forth information regarding our executive officers, including their positions (ages as of June 16, 2017):

Name | Age | Position | ||

Michael P. Huseby | 62 | Executive Chairman | ||

Max J. Roberts | 64 | Chief Executive Officer | ||

Patrick Maloney | 61 | Executive Vice President and Chief Operating Officer Executive Vice President and President, Barnes & Noble College | ||

William Maloney | 68 | Executive Vice President | ||

Barry Brover | 56 | Chief Financial Officer | ||

Kanuj Malhotra | 50 | Chief Strategy and Development Officer and Chief Operating Officer, Digital Education | ||

Michael C. Miller | 45 | Chief Legal Officer and Vice President of Corporate Affairs | ||

Suzanne E. Andrews | 57 | Vice President, General Counsel, and Corporate Secretary | ||

Jay Chakrapani | 46 | Vice President, Chief Digital Officer | ||

Stephen Culver | 52 | Vice President, Chief Information Officer | ||

Thomas D. Donohue | 47 | Vice President, Treasurer and Investor Relations | ||

Joel Friedman | 66 | Vice President, Chief Merchandising Officer | ||

JoAnn Magill | 63 | Vice President, Chief Human Resources Officer | ||

Lisa Malat | 57 | Vice President, Operations and Chief Marketing Officer | ||

Seema C. Paul | 53 | Vice President, Chief Accounting Officer | ||

Michael P. Huseby, age 62, serves as our Executive Chairman, elected in August 2015, and a director, elected in July 2013. He has served as the Chief Executive Officer and a member of the board of directors of Barnes & Noble, Inc. from January 2014 until the Spin-Off. Previously, Mr. Huseby was appointed Chief Executive Officer of NOOK Media LLC and President of Barnes & Noble, Inc. in July 2013, and Chief Financial Officer of Barnes & Noble, Inc. in March 2012. From 2004 to 2011, Mr. Huseby served as Executive Vice President and Chief Financial Officer of Cablevision Systems Corporation, a leading telecommunications and media company acquired by Altice Group. He served on the Cablevision Systems Corporation Board in 2000 and 2001. Prior to joining Cablevision, Mr. Huseby served as Executive Vice President and Chief Financial Officer of Charter Communications, Inc., then the fourth largest cable operator in the United States. Mr. Huseby served on the Board of Directors of Charter Communications from May 2013 to May 2016. From 1999 to 2002, Mr. Huseby served as Executive Vice President, Finance and Administration, of AT&T Broadband, a provider of cable television services. Since July 2016 to present, Mr. Huseby is a member of the Board of Directors of Commercehub, Inc., serving as the Chair of the Audit Committee and member of the Compensation Committee. In addition, Mr. Huseby spent over 23 years at Arthur Andersen, LLP and Andersen Worldwide, S.C., where he held the position of Global Equity Partner.

Max J. Roberts, age 64, serves as our Chief Executive Officer. Mr. Roberts joined our company in 1996 as President, and has served as Chief Executive Officer, of Barnes & Noble College since August of 2013. Prior to joining Barnes & Noble College in 1996, Mr. Roberts held senior executive positions at Petrie Retail, R.H. Macy & Company and May Department Stores. Mr. Roberts started his professional career at the global public accounting firm of Touche Ross & Company (currently Deloitte).

Patrick Maloney, age 61, serves as our Executive Vice President and Chief Operating Officer. Mr. Maloney is also President of Barnes & Noble College. In this role, he oversees operations at all bookstores nationwide, including bookstore e-commerce, store design and construction, internal operations, learning and development, and book and general merchandising departments. Mr. Maloney began his career at Barnes & Noble in 1974 as a student and assistant manager at SUNY Stony Brook University.

18

William Maloney, age 68, serves as our Executive Vice President. Mr. Maloney has served as Executive Vice President of Barnes & Noble College since 2002. In this role, he oversees campus relations activities, builds partnerships and handles strategic planning and corporate marketing activities. Mr. Maloney began his career at Barnes & Noble in 1971 as a Regional Manager and Operations Director.

Barry Brover, age 56, serves as our Chief Financial Officer. In this role, he oversees all aspects of accounting and finance, including treasury, investor relations, risk management, and tax, as well as provides strategic leadership in areas related to operations and business development. Mr. Brover has served as Chief Financial Officer of Barnes & Noble College since 2006. Mr. Brover joined Barnes & Noble College in 1986 and has held various executive positions with increasing responsibility. Prior to joining Barnes & Noble College, Mr. Brover started his career at KPMG where he earned his CPA.