Attached files

| file | filename |

|---|---|

| EX-23.1 - EXHIBIT 23.1 - NanoVibronix, Inc. | s106597_23-1.htm |

As filed with the Securities and Exchange Commission on June 21, 2017

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

NanoVibronix, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 3842 | 01-0801232 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

9 Derech Hashalom Street

Nesher, Israel 36651

(914) 233-3004

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Brian Murphy

Chief Executive Officer

NanoVibronix, Inc.

9 Derech Hashalom Street

Nesher, Israel 36651

(914) 233-3004

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

| Rick A. Werner, Esq. | Ralph V. De Martino |

| Haynes and Boone, LLP | Cavas S. Pavri |

| 30 Rockefeller Plaza, 26th Floor | Schiff Hardin LLP |

| New York, New York 10112 | 901 K Street NW Suite 700 |

| Tel. (212) 659-7300 | Washington, D.C. 20001 |

| Fax (212) 884-8234 | Telephone: (202) 778-6400 |

| Facsimile: (202) 778-6460 |

Approximate date of commencement of proposed

sale to the public: As soon as practicable after the effective

date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

(Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ |

| Non-accelerated filer ¨ | Smaller reporting company x |

| (Do not check if a smaller reporting company) | |

| Emerging growth company x |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ¨

| Title of Each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price (1)(2) | Amount of Registration Fee (3) | ||||||

| Common Stock, $0.001 par value per share | $ | $ | ||||||

| Series D Convertible Preferred Stock, $0.001 par value per share | $ | $ | ||||||

| Common Stock, $0.001 par value per share, issuable upon the conversion of the Series D Convertible Preferred Stock | – | (4) | ||||||

| Representative’s Warrant | ||||||||

| Warrants to purchase shares of Common Stock included in Representative’s Warrant (6) | – | (5) | ||||||

Common Stock, $0.001 par value per share, underlying Representative’s Warrant (6) | $ | 562,500 | $ | 65.19 | ||||

| Total | $ | 9,562,500 | $ | 1,108.29 | ||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes shares that the underwriter has the option to purchase to cover over-allotments, if any. |

| (3) | Pursuant to Rule 416 under the Securities Act of 1933, as amended, this registration statement also covers any additional securities that may be offered or issued in connection with any stock split, stock dividend or similar transaction. |

| (4) | No registration fee required pursuant to Rule 457(i) under the Securities Act. |

| (5) | No registration fee required pursuant to Rule 457(g) under the Securities Act. |

| (6) | Represents a representative warrant to purchase up to 5% of the number of shares of common stock underlying the securities sold in this offering (including the number of shares of common stock issuable upon conversion of the Series D Convertible Preferred Stock but excluding any shares of common stock underlying the warrants issued in this offering) at an exercise price equal to 125% of the public offering price per security issued in the offering. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | DATED June 21, 2017 |

![]()

NanoVibronix, Inc.

Up to $ of Common Stock and Series D Convertible Preferred Stock |

| ( Shares of Common Stock Underlying the Series D Convertible Preferred Stock) |

We are offering shares of our common stock. We are also offering to those purchasers, if any, whose purchase of our common stock in this offering would otherwise result in such purchaser, together with its affiliates and certain related parties, beneficially owning more than 4.99% of our outstanding common stock immediately following the consummation of this offering, the opportunity, in lieu of purchasing common stock, to purchase Series D Convertible Preferred Stock (the “Preferred Stock”). For each share of Preferred Stock purchased in this offering in lieu of common stock, we will reduce the number of shares of common stock being sold in the offering by 1. Pursuant to this prospectus, we are also offering the shares of common stock issuable upon conversion of the Preferred Stock.

Each share of Preferred Stock is convertible into one share of our common stock (subject to adjustment as provided in the related designation of preferences) at any time at the option of the holder, provided that the holder will be prohibited from converting Preferred Stock into shares of our common stock if, as a result of such conversion, the holder, together with its affiliates, would own more than 4.99% of the total number of shares of our common stock then issued and outstanding. However, any holder may increase such percentage to any other percentage not in excess of 9.99%, provided that any increase in such percentage shall not be effective until 61 days after such notice to us. The shares of Preferred Stock will otherwise have the preferences, rights and limitations described under “Description of Our Securities- Description of the Securities We Are Offering by this Prospectus - Series D Convertible Preferred Stock” beginning on page 85 of this prospectus.

Our common stock is quoted on the OTCQB over-the-counter marketplace under the symbol “NAOV.” As of June 20, 2017, the last reported sale price of our common stock as reported on the OTCQB over-the-counter marketplace was $5.85 per share. We have applied to list our shares of common stock on The NASDAQ Capital Market under the symbol “NAOV.” We do not intend to apply for any listing of the Preferred Stock on The NASDAQ Capital Market or any other securities exchange or nationally recognized trading system, and we do not expect that the Preferred Stock will be quoted on the OTCQB over-the-counter marketplace. There is no established public trading market for the Preferred Stock, and we do not expect a market to develop.

Investing in our securities (and the common stock underlying such securities) involves a high degree of risk. See “Risk Factors” beginning on page 9 of this prospectus before making a decision to purchase our securities.

We are an “emerging growth company” as defined in the Jumpstart our Business Startups Act of 2012, or JOBS Act and, as such, have elected to comply with certain reduced public company reporting requirements.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share

of Common Stock | Per Share

of Preferred Stock | Total | ||||||||||

| Public offering price | $ | $ | $ | |||||||||

| Underwriting discounts and commissions (1) | $ | $ | $ | |||||||||

| Proceeds, before expenses, to us | $ | $ | $ | |||||||||

| (1) | The underwriters will receive compensation in addition to the underwriting discounts and commissions. See “Underwriting” beginning on page 93 of this prospectus for a description of the compensation payable to the underwriters. |

We have granted the underwriter an option, exercisable one or more times in whole or in part, to purchase up to additional shares of common stock and/or additional shares of Preferred Stock from us at the public offering price, less the underwriting discounts and commissions, for 45 days after the date of this prospectus to cover over-allotments, if any.

The underwriter expects to deliver the shares of common stock and Preferred Stock against payment in New York, New York on or about , 2017.

Dawson James Securities, Inc.

The date of this prospectus is , 2017

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus. We have not authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offer to sell these securities in any jurisdiction where offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

Unless otherwise indicated, information contained in this prospectus concerning our industry and the markets in which we operate, including our general expectations and market position, market opportunity and market share, is based on information from our own management estimates and research, as well as from industry and general publications and research, surveys and studies conducted by third parties. Management estimates are derived from publicly available information, our knowledge of our industry and assumptions based on such information and knowledge, which we believe to be reasonable. Our management estimates have not been verified by any independent source, and we have not independently verified any third-party information. In addition, assumptions and estimates of our and our industry’s future performance are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors.” These and other factors could cause our future performance to differ materially from our assumptions and estimates. See “Cautionary Note Regarding Forward-Looking Statements.”

This prospectus contains references to our trademarks and service marks and to those belonging to other entities. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

i

This summary highlights selected information contained in greater detail elsewhere in this prospectus. This summary may not contain all of the information that you should consider before investing in the common stock or the Preferred Stock. You should read this entire prospectus carefully, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our historical financial statements and related notes included elsewhere in this prospectus before making an investment decision. In this prospectus, unless the context requires otherwise, all references to “we,” “our” and “us” refer to NanoVibronix, Inc., a publicly traded Delaware corporation and its consolidated subsidiaries.

Overview

We are a medical device company focusing on noninvasive biological response-activating devices that target biofilm prevention, wound healing and pain therapy and can be administered at home, without the assistance of medical professionals. Our products, which are in various stages of clinical and market development, currently consist of:

| · | WoundShieldTM, a patch-based therapeutic ultrasound device intended to facilitate tissue regeneration and wound healing by using ultrasound to increase local capillary perfusion and tissue oxygenation; |

| · | PainShieldTM, a patch-based therapeutic ultrasound technology to treat pain, muscle spasm and joint contractures by delivering a localized ultrasound effect to treat pain and induce soft tissue healing in a targeted area; and |

| · | UroShieldTM, an ultrasound-based product that is designed to prevent bacterial colonization and biofilm in urinary catheters, increase antibiotic efficacy and decrease pain and discomfort associated with urinary catheter use. |

Each of our PainShield, UroShield, and WoundShield products employs a small, disposable transducer that transmits low frequency, low intensity ultrasound acoustic waves that seek to repair and regenerate tissue, musculoskeletal and vascular structures and increase antibiotic efficacy. Through their size, effectiveness and ease of use, these products are intended to eliminate the need for technicians and medical personnel to manually administer ultrasound treatment through large transducers, thereby promoting patient independence and enabling more cost-effective home-based care.

PainShield is currently cleared for marketing in the United States by the U.S. Food and Drug Administration and all three of our products have CE Mark approval in the European Union, a Canadian medical device license and a certificate allowing us to sell PainShield, UroShield and WoundShield in Israel. We are able to sell PainShield, UroShield and WoundShield in India and Ecuador based on our CE Mark. We have consummated sales of PainShield and UroShield in the relevant markets, although to date sales have been minimal; WoundShield has not generated any revenue to date. We generally apply, through our distributor, for approval in a particular country for a particular product only when we have a distributor in place with respect to such product.

In the United States, PainShield requires a prescription from a licensed healthcare practitioner. If U.S. Food and Drug Administration clearance is obtained, we anticipate that WoundShield and UroShield will require a prescription from a licensed healthcare practitioner in the United States. We anticipate that UroShield will be sold directly to health care facilities and therefore will not require a prescription for these venues. However in other countries in which we sell PainShield and UroShield, and in which we may sell WoundShield although we do not have any sales to date, such products are eligible for sale without a prescription.

| 1 |

In addition to the need to obtain regulatory approvals, we anticipate that sales volumes and prices of our WoundShield and PainShield products will depend in large part on the availability of insurance coverage and reimbursement for at-home use from third party payers. Third party payers include governmental programs such as Medicare and Medicaid in the United States, private insurance plans and workers’ compensation plans. We do not currently have reimbursement codes use of WoundShield in any of the markets in which we have regulatory authority to sell WoundShield. Of the markets in which we have regulatory authority to sell PainShield, we have reimbursement codes in the United States (i.e., Current Procedural Terminology codes or “CPT codes”) for clinical use only, but do not have such reimbursement codes for at-home use of the product, although the product is marketed and sold for such use. With respect to UroShield, which may be used in a clinical and home setting, we do not currently have reimbursement codes in any of the markets in which we have regulatory authority to sell UroShield, although the product is marketed and sold for clinical and at-home use. We anticipate that we will begin to seek reimbursement codes for use of our products in the markets in which we have regulatory authority to sell such products, however, there is no guarantee that we will be successful in obtaining such codes quickly, or at all.

We are currently conducting a double blind clinical trial for UroShield in the United States in order to obtain 510(k) clearance from the U.S. Food and Drug Administration. In addition, we are currently ramping up our marketing efforts in North America with respect to PainShield. We anticipate that these efforts will include recruiting indirect sales personnel and representatives, making in-office calls to physicians and attending trade shows and conferences. We have also identified a market for PainShield in the professional sports industry, where in some cases reimbursement may be available from sports alumni organizations or, more likely, self-pay. In order to pursue this market, we are exhibiting at sports trainers meetings, pursuing alumni associations, advertising in their media, and negotiating with a sports trainer focused sales organization. The PainShield device is offered for sale to practitioners with a provider rental program which was implemented in January 2017. The PainShield product was also modified and enhanced through various accessories for use within the equine community. This market is currently being pursued through prominent equine clinicians and independent sales representatives. We believe there is an attractive opportunity in this segment due to the lack of an expectation for reimbursement and the opportunity to sell at a premium price point.

Ultrasound Technology and Our Products

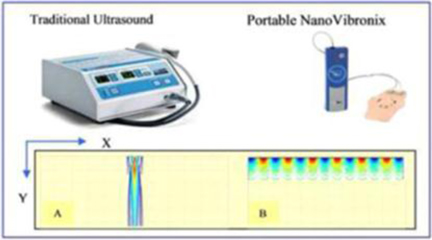

As noted above, our primary products are based on the use of low frequency ultrasound, which delivers energy through mechanical vibrations in the form of sound waves. Ultrasound has long been used in physical therapy, physical medicine, rehabilitation and sports medicine.

Our proprietary technology consists of a small, thin (1 millimeter) transducer that is capable of transmitting ultrasonic acoustic waves onto treatment surfaces with a radius of up to 10 centimeters beyond the transducer. This technology allows us to treat wounds by implanting our transducers into a small, portable self-adhering acoustic patch, thereby eliminating the need for technicians and medical personnel to manually administer ultrasound therapy, which should reduce the cost of therapy. Moreover, we believe that, based upon the body of evidence, the delivery of ultrasound through our portable devices is equal to or more effective than existing competitive products, as our technology is better positioned to target the affected areas of the body.

While there are currently a number of products on the market that treat pain through ultrasound therapy, we believe that our products differentiate themselves because they are portable, without the requirement to be plugged into an outlet and they have a frequency of 100kHz (in contrast to other devices, which have a frequency of 1MHz), which means our products do not produce heat that can damage tissue. Our products can therefore (i) be self-administered by the patient without the need to be moved about the treated area by the patient or a clinician, (ii) be applied for a significantly longer period without the risk of tissue damage and (iii) do not require the use of gel. We are aware of one competitive product with similar ultrasound technology, the SAM® Sport4 by a company called Zetroz Systems LLC, aka Zetroz, Inc. However, it is our belief that this product does not generate surface acoustic waves as our products do, the treatment area is generally limited to that of the transducer’s diameter, the use of transmission gel is still required and the transducer thickness is significantly greater than ours (approximately 1.5cm). The device only provides a battery life of 4 hours and is continuous therapy versus intermittent therapy. We are also aware of a small clinical study, for which results were reported in August 2013, in which the SAM® Sport4 showed positive results in the treatment of venous ulcers, a type of chronic wound.

Micro Vibrations Technology and Our Products

It is well established that increasing blood flow to the wound and peri-wound area helps accelerate the healing of ischemic wounds. Micro-vibrations applied on the skin tissue increase local blood flow and oxygen delivery to the wound area and stimulate angiogenesis and growth factors that are helpful for the wound healing process. Vibration therapy has been found to stimulate blood flow due to mechanical stresses of endothelial cells resulting in increased production of nitric oxide and vasodilation, as well as increase soft tissue and skin circulation. In addition, micro vibrations induce skin surface nerve axon reflex and type IIa muscle fibers contraction rates, resulting in vasodilation.

| 2 |

Urinary catheter usage is associated with pain and discomfort caused by the friction between the catheter surface and the urethral tissue. Generally, this friction is treated by applying lubricating gels and low friction catheter coatings. These methods are effective for a short term during the catheter insertion as the lubricating gel is quickly absorbed into the surrounding tissue and loses its effect and the catheter coatings lose their lubricity within a few days, as the coating is covered by a thin film of mucous.

Our UroShield product provides vibrations along the surface of the urinary catheter that is in contact with urethral tissue. We believe that these vibrations create a continuous acoustic lubrication effect along the surface of the indwelling catheter that is in contact with the surrounding tissue, thus reducing catheter-tissue contact time, which may lessen trauma from urethra abrasion and adhesion.

Markets for Our Products

We believe our products compete and/or will compete in the markets described below:

| · | Wound-Healing Devices Market. Our WoundShield product is aimed at the market for wound-healing devices. The global wound care device market totaled approximately $24 billion in 2015 and it is expected to grow at a compound annual growth rate (“CAGR”) of 6.7% during 2016-2022 (as reported by P&S Global Research in January 2017). |

| · | Pain Market. Our PainShield product is aimed at the pain treatment market. Pain is one of the most common conditions that hinders quality of life of a vast patient population. According to Bonica’s Management of Pain (2001), a work considered current in the industry based on available industry data, and Landro L, “New Ways to Treat Pain: Tricking the Brain, Blocking the Nerves in Patients When all Else Has Failed,” Wall Street Journal, May 11, 2010, approximately 25% of the U.S. population, 75 million people, suffer from chronic pain. |

| · | Catheter Market. Our UroShield product is complementary to products in the catheter market. Approximately 25% of patients who are admitted to a hospital will have an indwelling catheter at some point during their stay and 7% of nursing home residents are managed by long term catheterization . In the United States there are 25 million Foley catheters sold annually and there are 75 million catheters sold elsewhere, yielding a total global Foley catheter market of 100 million units worldwide. |

Risks Associated with Our Business

Our ability to operate our business and achieve our goals and strategies is subject to numerous risks as discussed more fully in the section titled “Risk Factors,” including, without limitation:

| · | our ability to continue as a going concern; | |

| · | the timing of clinical studies and eventual U.S. Food and Drug Administration approval of WoundShield™ and UroShieldTM; |

| · | regulatory actions that could adversely affect the price of or demand for our approved products; |

| · | favorable or unfavorable decisions about our products from government regulators, insurance companies or other third-party payers; |

| · | protection of our intellectual property portfolio; |

| · | intense competition in our industry, with competitors having substantially greater financial, technological, research and development, regulatory and clinical, manufacturing, marketing and sales, distribution and personnel resources than we do; |

| 3 |

| · | our ability to recruit and retain qualified regulatory and research and development personnel; |

| · | unforeseen changes in healthcare reimbursement for any of our approved products, the loss of such reimbursement or the inability to obtain such reimbursement for use of our products at home, as well as in a clinical setting; |

| · | insufficient or inadequate reimbursement by governmental and other third party payers for our products; | |

| · | lack of financial resources to adequately support our operations; |

| · | difficulties in maintaining commercial scale manufacturing capacity and capability; |

| · | our ability to generate internal growth; |

| · | our failure to comply with regulatory guidelines; |

| · | uncertainty in industry demand and patient wellness behavior; |

| · | loss or retirement of key executives and qualified personnel;

| |

| · | general economic conditions and market conditions in the medical device industry; |

| · | future sales of large blocks of our common stock, which may adversely impact our stock price; and |

| · | depth of the trading market in our common stock. |

Conversion of Convertible Promissory Notes Upon Completion of this Offering

Since March 1, 2017, we have completed a series of bridge financings pursuant to which we have received aggregate proceeds of $1,030,000 in exchange for convertible promissory notes in the aggregate principal amount of $1,030,000, and seven-year warrants to purchase an aggregate of 412,000 shares of common stock at an exercise price of $5.90 per share.

The notes issued in the bridge financings discussed above are collectively referred to in this prospectus as the “2017 Notes,” and the seven-year warrants issued in such bridge financings are collectively referred to in this prospectus as the “2017 Warrants.”

The principal amount and all accrued but unpaid interest on each 2017 Note will become due and payable on the earlier of the (i) 5-year anniversary of the date of issuance, or (ii) the date we complete an equity financing pursuant to which we issue and sell shares of capital stock resulting in aggregate proceeds of at least $2,000,000 (a “Qualified Financing”). The 2017 Notes bear interest at a rate of 6% per annum. Upon consummation of a Qualified Financing, the holders of the 2017 Notes may elect to have the outstanding principal and accrued but unpaid interest thereon repaid in cash or converted into shares of the same class and series of equity securities sold in such Qualified Financing at a price per share equal to the lesser of: (a) 80% of the price per share at which such securities are sold in such Qualified Financing and (b) $5.90 per share, as such amount may be adjusted for any stock split, stock dividend, reclassification or similar events affecting our capital stock. In the absence of a Qualified Financing, on the maturity date, the holders of our 2017 Notes may elect to have the outstanding principal and accrued but unpaid interest thereon repaid in cash or converted into common stock. To the extent that the conversion of our 2017 Notes causes any holder thereof to beneficially own more than 9.99% of our common stock, such holder may elect to receive shares of our Series C Convertible Preferred Stock (the “Series C Preferred Stock”) in lieu of common stock or common stock equivalents. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Recent Events.”

| 4 |

We expect this offering to constitute a Qualified Financing under the 2017 Notes, and therefore, upon closing of this offering, the holders of the 2017 Notes, instead of being repaid in cash, may elect to convert the outstanding principal amount and all accrued but unpaid interest on such holder’s 2017 Notes into shares of common stock, or Preferred Stock in lieu of common stock, at a conversion price equal to the lesser of 80% of the public offering price or $5.90. As of June 20, 2017, the aggregate outstanding principal amount of the 2017 Notes and accrued but unpaid interest thereon was approximately $1,039,486. If all holders of the 2017 Notes elect to convert the outstanding principal and accrued but unpaid interest on their 2017 Notes into shares of common stock, based on the outstanding principal amount and all accrued but unpaid interest on the 2017 Notes as of June 20, 2017, at 80% of the assumed offering price of $5.85 per share of common stock, which is the last reported sales price of our common stock as of June 20, 2017, we will be required to issue an aggregate of 222,112 shares of common stock or Preferred Stock to the holders of the 2017 Notes.

Corporate Information

We were organized as a Delaware corporation on October 20, 2003. Our principal executive offices are located at 9 Derech Hashalom Street, Nesher, Israel 36651. Our telephone number is (914) 233-3004. Our website address is www.nanovibronix.com. Information accessed through our website is not incorporated into this prospectus and is not a part of this prospectus.

| 5 |

The Offering

| Issuer | NanoVibronix, Inc. | |

| Common stock offered by us in this offering | shares of our common stock, par value $0.001 per share. | |

| Preferred Stock offered by us | We are also offering to those purchasers, if any, whose purchase of common stock in this offering would otherwise result in such purchaser, together with its affiliates and certain related parties, beneficially owning more than 4.99% of our outstanding common stock immediately following the consummation of this offering, the opportunity, in lieu of purchasing common stock, to purchase up to shares of Preferred Stock. This prospectus also relates to the offering of shares of common stock issuable upon conversion of the Preferred Stock. | |

| Conversion | Each share of Preferred Stock is convertible into one share of our common stock (subject to adjustment as provided in the related designation of preferences) at any time at the option of the holder, provided that the holder will be prohibited from converting Preferred Stock into shares of our common stock if, as a result of such conversion, the holder, together with its affiliates, would own more than 4.99% of the total number of shares of our common stock then issued and outstanding. However, any holder may increase such percentage to any other percentage not in excess of 9.99%, provided that any increase in such percentage shall not be effective until 61 days after such notice to us. | |

| Liquidation rights | In the event of our liquidation, dissolution, or winding up, holders of our Preferred Stock will be entitled to receive the amount of cash, securities or other property to which such holder would be entitled to receive with respect to such shares of Preferred Stock if such shares had been converted to common stock immediately prior to such event (without giving effect for such purposes to any beneficial ownership limitation), subject to the preferential rights of holders of any class or series of our capital stock specifically ranking by its terms senior to the Preferred Stock as to distributions of assets upon such event, whether voluntarily or involuntarily. | |

| Voting Rights | The holders of the Preferred Stock have no voting rights, except as required by law. Any amendment to our certificate of incorporation, bylaws or certificate of designation that adversely affects the powers, preferences and rights of the Preferred Stock requires the approval of the holders of a majority of the shares of Preferred Stock then outstanding. |

| 6 |

| Dividends | The holders of our Preferred Stock are entitled to receive dividends on shares of Preferred Stock equal (on an as-if-converted-to-common-stock basis, without giving effect for such purposes to any beneficial ownership limitation) to and in the same form as dividends actually paid on shares of the common stock when such dividends are specifically declared by our board of directors. | |

| Common stock outstanding immediately before this offering | 2,632,710 shares | |

| Common stock outstanding immediately after this offering | shares or shares if the underwriter exercises its over-allotment option in full.(1) | |

Over-allotment option to be offered by us:

|

We have granted the underwriter the right to purchase up to additional shares of common stock and/or Preferred Stock from us at the public offering price less the underwriting discounts and commissions within 45 days from the date of this prospectus to cover over-allotments. See “Underwriting” for additional information regarding the over-allotment option. | |

| Use of proceeds | We estimate that our net proceeds from this offering will be approximately $ , or approximately $ if the underwriter exercises its over-allotment option in full, after deducting the underwriting discount and estimated offering expenses payable by us. | |

| We currently expect to use the net proceeds from this offering: (i) to cover expenses related to listing our shares on The NASDAQ Capital Market; (ii) to expand our sales leadership and field level sales resources; (iii) for research and development; (iv) to implement our Surface Acoustic Wave platform to other applications; (v) to pursue complimentary acquisitions; (vi) to pay any holders of the 2017 Notes that elect to be repaid in cash; and (vii) for general working capital. Any balance of the net proceeds will be used for general corporate purposes. See “Use of Proceeds.” | ||

| Dividend policy | We have not declared or paid any cash or other dividends on our common stock or preferred stock, and we do not expect to declare or pay any cash or other dividends in the foreseeable future. See “Dividend Policy.” | |

| Risk factors | You should carefully read and consider the information beginning on page 9 of this prospectus set forth under the heading “Risk Factors” and all other information set forth in this prospectus before deciding to invest in our securities. | |

| OTCQB symbol for common stock: | NAOV. |

| 7 |

| Proposed Symbol and listing: | We have applied to list our shares of common stock on The NASDAQ Capital Market under the symbol “NAOV.” We do not intend to apply for any listing of the Preferred Stock on The NASDAQ Capital Market or any other securities exchange or nationally recognized trading system, and we do not expect that the Preferred Stock will be quoted on the OTCQB over-the-counter marketplace. There is no established public trading market for the Preferred Stock, and we do not expect a market to develop. |

| (1) | Assumes only shares of common stock are sold in this offering. For each share of Preferred Stock purchased in this offering in lieu of common stock, we will reduce the number of shares of common stock being sold in the offering by 1. |

The number of shares to be outstanding immediately before and immediately after this offering is based on 2,632,710 shares of our common stock and 1,951,261 shares of Series C Preferred Stock outstanding as of June 19, 2017, and excludes as of that date:

| · | 331,293 shares of common stock issuable upon the exercise of warrants with an exercise price of $1.39 per share;

| |

| · | 563,910 shares of common stock issuable upon the exercise of warrants with an exercise price of $2.66 per share;

| |

| · | 61,000 shares of common stock issuable upon the exercise of warrants with an exercise price of $2.57 per share; |

| · | 420,000 shares of common stock issuable upon the exercise of warrants with an exercise price of $3.00 per share; |

| · | 420,000 shares of common stock issuable upon the exercise of warrants with an exercise price of $6.00 per share;

| |

| · | 412,000 shares of common stock issuable upon the exercise of 2017 Warrants with an exercise price of $5.90 per share; |

| · | 1,951,261 shares of common stock issuable upon conversion of the currently outstanding Series C Preferred Stock; | |

| · | additional shares of common stock that maybe issued, upon exercise, to the holders of certain warrants to purchase an aggregate of 563,910 shares of common stock, pursuant to a full ratchet anti-dilution price protection in such warrants (See “Description of Securities—Warrants”); and

| |

| · | 1,237,434 shares of common stock issuable upon the exercise of currently outstanding options with exercise prices ranging from $0.07 to $120.75 and having a weighted average exercise price of $3.87. |

Unless otherwise stated, all information contained in this prospectus assumes:

| · | no investor purchased Preferred Stock in lieu of common stock sold in this offering; and |

| · | no exercise of the over-allotment option granted to the underwriter. |

| 8 |

An investment in our securities involves a high degree of risk. Before deciding whether to invest in our securities, you should consider carefully the risks described below, together with other information in this prospectus, and in any free writing prospectus that we have authorized for use in connection with this offering. If any of these risks actually occur, our business, financial condition, results of operations or cash flow could be seriously harmed. This could cause the trading price of our common stock to decline, resulting in a loss of all or part of your investment. The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties not presently known to us, or that we currently see as immaterial, may also harm our business. Please also read carefully the section below entitled “Cautionary Note Regarding Forward-Looking Statements.”

Risks Related to Our Business

We have a history of losses and we expect to continue to incur losses and may not achieve or maintain profitability.

For the three months ended March 31, 2017, we had a net loss of $877,000, with revenues of $52,000. For the fiscal year ended December 31, 2016, we had a net loss of $2,831,000, with revenues of $229,000. As of March 31, 2017, we had an accumulated deficit of $24,294,000 and a total stockholders’ deficit of $2,803,000. We expect to incur losses for at least the next year, as we continue to incur expenses related to seeking U.S. Food and Drug Administration approval for UroShield and WoundShield, and market acceptance of PainShield, which will require costly clinical trials and research, further product development and professional fees associated with regulatory compliance. Even if we succeed in commercializing our new products, we may not be able to generate sufficient revenues to cover our expenses and achieve profitability or be able to maintain profitability.

The report of our independent registered public accounting firm contains an explanatory paragraph as to our ability to continue as a going concern, which could prevent us from obtaining new financing on reasonable terms or at all.

Because we have had recurring losses and negative cash flows from operating activities, substantial doubt exists regarding our ability to remain in operation at the same level we are currently performing. Further, the report of Kost Forer Gabbay & Kasierer, a member firm of Ernst & Young Global, our independent registered public accounting firm, with respect to our financial statements at December 31, 2016 and 2015 and for the two years ended December 31, 2016, includes an explanatory paragraph as to our potential inability to continue as a going concern. This may adversely affect our ability to obtain new financing on reasonable terms or at all.

If we are unable to raise additional capital, our clinical trials and product development will be limited and our long-term viability will be threatened; however, if we do raise additional capital, your percentage ownership as a stockholder could decrease and constraints could be placed on the operations of our business.

We have experienced negative operating cash flows since our inception and have funded our operations primarily from proceeds of the sale of our securities, with only limited revenue being generated from our product sales. In order to fully realize our business objectives, we will need to raise additional capital following the completion of this offering. We will seek to raise such additional funds through equity or debt financings, or strategic alliances with third parties, either alone or in combination with equity financings. These financings could result in substantial dilution to the holders of our common stock, or require contractual or other restrictions on our operations or on alternatives that may be available to us. If we raise additional funds by issuing debt securities, these debt securities could impose significant restrictions on our operations through the imposition of restrictive covenants and requiring us to pledge assets in order to secure repayment. In addition, if we raise funds through the sale of equity, we may issue equity securities with rights superior to our common stock, including voting rights, rights to proceeds upon our liquidation or sale, rights to dividends and rights to appoint board members. Any such required financing may not be available in amounts or on terms acceptable to us, and the failure to procure such required financing could have a material adverse effect on our business, financial condition and results of operations, or threaten our ability to continue as a going concern.

| 9 |

A variety of factors could impact the timing and amount of any required financings, including, without limitation:

| · | unforeseen developments during our clinical trials; | |

| · | delays in our receipt of required regulatory approvals; | |

| · | delayed market acceptance of our products; | |

| · | unanticipated expenditures in our acquisition and defense of intellectual property rights, and/or the loss of those rights; | |

| · | the failure to develop strategic alliances for the marketing of some of our product candidates; | |

| · | unforeseen changes in healthcare reimbursement for any of our approved products; | |

| · | lack of financial resources to adequately support our operations; | |

| · | difficulties in maintaining commercial scale manufacturing capacity and capability; | |

| · | unanticipated difficulties in operating in international markets; | |

| · | unanticipated financial resources needed to respond to technological changes and increased competition; | |

| · | unforeseen problems in attracting and retaining qualified personnel; | |

| · | enactment of new legislation or administrative regulations; | |

| · | the application to our business of new regulatory interpretations; | |

| · | claims that might be brought in excess of our insurance coverage; | |

| · | the failure to comply with regulatory guidelines; and | |

| · | the uncertainty in industry demand. |

In addition, although we have no present commitments or understandings to do so, we may seek to expand our operations and product lines through acquisitions or joint ventures. Any acquisition or joint venture would likely increase our capital requirements.

If we fail to obtain an adequate level of reimbursement for our approved products by third party payers, there may be no commercially viable markets for our approved products or the markets may be much smaller than expected.

The availability and levels of reimbursement by governmental and other third party payers affect the market for our approved products. The efficacy, safety, performance and cost-effectiveness of our product and product candidates, and of any competing products, will determine the availability and level of reimbursement. Reimbursement and healthcare payment systems vary significantly by country, and include both government sponsored healthcare and private insurance. To obtain reimbursement or pricing approval in some countries, we may be required to produce clinical data, which may involve one or more clinical trials, that compares the cost-effectiveness of our approved products to other available therapies. We may not obtain reimbursement or pricing approvals in markets we seek to enter in a timely manner, if at all. Our failure to receive reimbursement or pricing approvals in target markets would negatively impact market acceptance of our products in these jurisdictions, placing us at a material cost disadvantage to our competitors.

Even if we obtain reimbursement approvals for our products, we believe that, in the future, reimbursement for any of our products or product candidates may be subject to increased restrictions both in the United States and in international markets. Future legislation, regulation or policies of third party payers that limit reimbursement may adversely affect the demand for our products currently under development and our ability to sell our products on a profitable basis. In addition, third party payers continually attempt to contain or reduce the costs of healthcare by challenging the prices charged for healthcare products and services.

In the United States, specifically, health care providers, such as hospitals and clinics, and individual patients, generally rely on third-party payers. Third-party reimbursement is dependent upon decisions by the Centers for Medicare and Medicaid Services, contracted Medicare carriers or intermediaries, individual managed care organizations, private insurers, other governmental health programs and other payers of health care costs. Failure to receive or maintain favorable coding, coverage and reimbursement determinations for our products by these organizations could discourage medical practitioners from using or prescribing our products due to their costs. In addition, with recent federal and state government initiatives directed at lowering the total cost of health care, the U.S. Congress and state legislatures will likely continue to focus on health care reform including the reform of the Medicare and Medicaid programs, and on the cost of medical products and services, which could limit reimbursement. Additionally, third-party payers are increasingly challenging the prices charged for medical products and services, and imposing conditions on payment. We may be unable to sell our products on a profitable basis if third-party payers deny coverage, provide low reimbursement rates or reduce their current levels of reimbursement.

| 10 |

The medical device and therapeutic product industries are highly competitive and subject to rapid technological change. If our competitors are better able to develop and market products that are safer and more effective than any products we may develop, our commercial opportunities will be reduced or eliminated.

Our success depends, in part, upon our ability to maintain a competitive position in the development of technologies and products. We face competition from established medical device companies, such as Neurometrix Inc., Zetrox, Kinetic Concepts, Inc. and Smith & Nephew plc, manufacturers of certain portable ultrasound devices capable of self-administered use, as well as from academic institutions, government agencies, and private and public research institutions in the United States and abroad. Most, if not all, of our principal competitors have significantly greater financial resources and expertise than we do in research and development, manufacturing, pre-clinical testing, conducting clinical trials, obtaining regulatory approvals, marketing approved products, protecting and defending their intellectual property rights and designing around the intellectual property rights of others. Other small or early-stage companies may also prove to be significant competitors, particularly through collaborative arrangements, or mergers with, or acquisitions by, large and established companies, or through the development of novel products and technologies.

The industry in which we operate has undergone, and we expect it to continue to undergo, rapid and significant technological change, and we expect competition to intensify as technological advances are made. Our competitors may be able to respond to changes in technology or the marketplace faster than us. Our competitors may develop and commercialize medical devices that are safer or more effective or are less expensive than any products that we may develop. We also compete with our competitors in recruiting and retaining qualified scientific and management personnel, in establishing clinical trial sites and patient registration for clinical trials, and in acquiring technologies complementary to our programs or advantageous to our business. Given our small size and lack of resources, we are often at a disadvantage with our competitors in all of these areas, which could limit or eliminate our commercial opportunities.

We face the risk of product liability claims and may not be able to obtain insurance.

Our business exposes us to the risk of product liability claims that are inherent in the development of medical devices and products. If the use of one or more of our products harms people, we may be subject to costly and damaging product liability claims brought against us by clinical trial participants, consumers, health care providers, pharmaceutical companies or others selling our products. We currently carry clinical trial and product liability insurance for the products we sell. However, we cannot predict all of the possible harms or side effects that may result and, therefore, the amount of insurance coverage we hold may not be adequate to cover all liabilities we might incur. We intend to expand our insurance coverage to include the sale of additional commercial products as we obtain marketing approval for our product candidates in development and as our sales expand, but we may be unable to obtain commercially reasonable product liability insurance for such products. If we are unable to obtain insurance at an acceptable cost or otherwise protect against potential product liability claims and we continue to make sales, or if our coverages turns out to be insufficient, we may be exposed to significant liabilities, which may materially and adversely affect our business and financial position. If we are sued for any injury allegedly caused by our products and do not have sufficient insurance coverage, our liability could exceed our total assets and our ability to pay the liability. A product liability claim or series of claims brought against us would decrease our cash and could reduce our value or marketability.

Our product candidates may not be developed or commercialized successfully.

Our product candidates are based on a technology that has not been used previously in the manner we propose and must compete with more established treatments currently accepted as the standards of care. Market acceptance of our products will largely depend on our ability to demonstrate their relative safety, efficacy, cost-effectiveness and ease of use.

| 11 |

We are subject to the risks that:

| · | the U.S. Food and Drug Administration or a foreign regulatory authority finds our product candidates ineffective or unsafe; | |

| · | we do not receive necessary regulatory approvals; | |

| · | the regulatory review and approval process may take much longer than anticipated, requiring additional time, effort and expense to respond to regulatory comments and/or directives; | |

| · | we are unable to get our product candidates in commercial quantities at reasonable costs; and | |

| · | the patient and physician community does not accept our product candidates. |

In addition, our product development program may be curtailed, redirected, eliminated or delayed at any time for many reasons, including:

| · | adverse or ambiguous results; | |

| · | undesirable side effects that delay or extend the trials; | |

| · | the inability to locate, recruit, qualify and retain a sufficient number of clinical investigators or patients for our trials; and | |

| · | regulatory delays or other regulatory actions. |

Additionally, we currently have limited experience in marketing or selling our products, and we have a limited marketing and sales staff and distribution capabilities. Developing a marketing and sales force is time-consuming and will involve the investment of significant amounts of financial and management resources, and could delay the launch of new products or expansion of existing product sales. In addition, we compete with many companies that currently have extensive and well-funded marketing and sales operations. If we fail to establish successful marketing and sales capabilities or fail to enter into successful marketing arrangements with third parties, our ability to generate revenues will suffer.

Furthermore, even if we enter into marketing and distributing arrangements with third parties, we may have limited or no control over the sales, marketing and distribution activities of these third parties, and these third parties may not be successful or effective in selling and marketing our products. If we fail to create successful and effective marketing and distribution channels, our ability to generate revenue and achieve our anticipated growth could be adversely affected. If these distributors experience financial or other difficulties, sales of our products could be reduced, and our business, financial condition and results of operations could be harmed.

We cannot predict whether we will successfully develop and commercialize our product candidates. If we fail to do so, we will not be able to generate substantial revenues, if any.

The loss of our key management would likely hinder our ability to execute our business plan.

As a small company with eight full-time employees and four contract employees, our success depends on the continuing contributions of our management team and qualified personnel and on our ability to attract and retain highly qualified personnel. We face intense competition in our hiring efforts from other medical device companies, as well as from universities and nonprofit research organizations, and we may have to pay higher salaries to attract and retain qualified personnel. We are also at a disadvantage in recruiting and retaining key personnel as our small size and limited resources may be viewed as providing a less stable environment, with fewer opportunities than would be the case at one of our larger competitors. The loss of one or more of these individuals, or our inability to attract additional qualified personnel, could substantially impair our ability to implement our business plan.

| 12 |

Our failure to protect our intellectual property rights could diminish the value of our solutions, weaken our competitive position and reduce our revenue.

We regard the protection of our intellectual property, which includes patents and patent applications, trade secrets, trademarks and domain names, as critical to our success. We strive to protect our intellectual property rights by relying on federal, state and common law rights, as well as contractual restrictions. We enter into confidentiality and invention assignment agreements with our employees, consultants and contractors, and confidentiality agreements with parties with whom we conduct business in order to limit access to, and disclosure and use of, our proprietary information. However, these contractual arrangements and the other steps we have taken to protect our intellectual property may not prevent the misappropriation of our proprietary information or deter independent development of similar technologies by others.

We have obtained patents and we have patent applications pending in both the United States and foreign jurisdictions. There can be no assurance that our patent applications will be approved, that any patents issued will adequately protect our intellectual property, or that these patents will not be challenged by third parties or found to be invalid or unenforceable. We have also obtained trademark registration in the United States and in foreign jurisdictions. Effective trade secret, trademark and patent protection is expensive to develop and maintain, both in terms of initial and ongoing registration requirements and the costs of defending our rights. We may be required to protect our intellectual property in an increasing number of jurisdictions, a process that is expensive and may not be successful or which we may not pursue in every location. We may, over time, increase our investment in protecting our intellectual property through additional patent filings that could be expensive and time-consuming.

Monitoring unauthorized use of our intellectual property is difficult and costly. Our efforts to protect our proprietary rights may not be adequate to prevent misappropriation of our intellectual property. We may not be able to detect unauthorized use of, or take appropriate steps to enforce, our intellectual property rights. Further, our competitors may independently develop technologies that are similar to ours but which avoid the scope of our intellectual property rights. Further, the laws in the United States and elsewhere change rapidly, and any future changes could adversely affect us and our intellectual property. Our failure to meaningfully protect our intellectual property could result in competitors offering solutions that incorporate our most technologically advanced features, which could seriously reduce demand for our products. In addition, we may in the future need to initiate infringement claims or litigation. Litigation, whether we are a plaintiff or a defendant, can be expensive, time-consuming and may divert the efforts of our technical staff and managerial personnel, which could harm our business, whether or not the litigation results in a determination that is unfavorable to us. In addition, litigation is inherently uncertain, and thus we may not be able to stop our competitors from infringing our intellectual property rights.

We could incur substantial costs and disruption to our business as a result of any dispute related to, or claim of infringement of another party’s intellectual property rights, which could harm our business and operating results.

In recent years, there has been significant litigation in the United States over patents and other intellectual property rights. From time to time, we may face allegations that we or customers who use our products have infringed the trademarks, copyrights, patents and other intellectual property rights of third parties, including allegations made by our competitors or by non-practicing entities, or that we or our customers have misappropriated the intellectual property rights of such third parties. We cannot predict whether assertions of third party intellectual property rights or claims arising from these assertions will substantially harm our business and operating results. If we are forced to defend any infringement or misappropriation claims or attacks on the validity of our intellectual property rights, whether they are with or without merit or are ultimately determined in our favor, we may face costly litigation and diversion of technical and management personnel. Most of our competitors have substantially greater resources than we do and are able to sustain the cost of complex intellectual property litigation to a greater extent and for longer periods of time than we could. Furthermore, an adverse outcome of a dispute may require us, among other things: to pay damages, potentially including treble damages and attorneys’ fees, if we are found to have willfully infringed a party’s patent or other intellectual property rights; to cease making, licensing or using products that are alleged to incorporate or make use of the intellectual property of others; to expend additional development resources to redesign our products; and to enter into potentially unfavorable royalty or license agreements in order to obtain the rights to use necessary technologies. Royalty or licensing agreements, if required, may be unavailable on terms acceptable to us, or at all. In any event, we may need to license intellectual property which would require us to pay royalties or make one-time payments. Even if these matters do not result in litigation or are resolved in our favor or without significant cash settlements, the time and resources necessary to resolve them could harm our business, operating results, financial condition and reputation.

| 13 |

Risks Related to the Regulation of Our Products

We are subject to extensive governmental regulation, including the requirement of U.S. Food and Drug Administration approval or clearance, before our product candidates may be marketed.

The process of obtaining U.S. Food and Drug Administration approval is lengthy, expensive and uncertain, and we cannot be sure that our additional product candidates will be approved in a timely fashion, or at all. If the U.S. Food and Drug Administration does not approve or clear our product candidates in a timely fashion, or at all, our business and financial condition would likely be adversely affected.

Both before and after approval or clearance of our product candidates, we, our product candidates, our suppliers and our contract manufacturers are subject to extensive regulation by governmental authorities in the United States and other countries. Failure to comply with applicable requirements could result in, among other things, any of the following actions:

| · | FDA issuance of Form 483 or Warning Letters, which may be made public and may lead to further regulatory or enforcement actions, or similar letters by other regulatory authorities; | |

| · | fines and other monetary penalties; | |

| · | unanticipated expenditures; | |

| · | delays in U.S. Food and Drug Administration approval and clearance, or U.S. Food and Drug Administration refusal to approve or clear a product candidate; | |

| · | product recall or seizure; | |

| · | interruption of manufacturing or clinical trials; | |

| · | operating restrictions; | |

| · | injunction or other restrictions imposed on our operations, including closing our facilities or our contract manufacturers’ facilities; or | |

| · | criminal prosecutions. |

In addition to the approval and clearance requirements, numerous other regulatory requirements apply, both before and after approval or clearance, to us, our products and product candidates, and our suppliers and contract manufacturers. These include requirements related to the following:

| · | testing and quality control; | |

| · | manufacturing; | |

| · | quality assurance | |

| · | labeling; | |

| · | advertising; | |

| · | promotion; | |

| · | distribution; | |

| · | export; | |

| · | reporting to the U.S. Food and Drug Administration certain adverse experiences associated with the use of the products; and | |

| · | obtaining additional approvals or clearances for certain modifications to the products or their labeling or claims. |

We are also subject to inspection by the U.S. Food and Drug Administration to determine our compliance with regulatory requirements, as are our suppliers and contract manufacturers, and we cannot be sure that the U.S. Food and Drug Administration will not identify compliance issues that may disrupt production or distribution, or require substantial resources to correct.

The U.S. Food and Drug Administration’s requirements may change and additional government regulations may be promulgated that could affect us, our product candidates, and our suppliers and contract manufacturers. We cannot predict the likelihood, nature or extent of government regulation that may arise from future legislation or administrative action. There can be no assurance that we will not be required to incur significant costs to comply with such laws and regulations in the future, or that such laws or regulations will not have a material adverse effect upon our business.

| 14 |

Failure to obtain regulatory approval in foreign jurisdictions will prevent us from marketing our products abroad.

International sales of our products and any of our product candidates that we commercialize are subject to the regulatory requirements of each country in which the products are sold. Accordingly, the introduction of our product candidates in markets outside the United States where we do not already possess regulatory approval will be subject to regulatory approvals in those jurisdictions. The regulatory review process varies from country to country. Many countries impose product standards, packaging and labeling requirements, and import restrictions on medical devices. In addition, each country has its own tariff regulations, duties and tax requirements, as well as reimbursement and healthcare payment systems. The approval by foreign government authorities is unpredictable and uncertain, and can be expensive. We may be required to perform additional pre-clinical, clinical or post-approval studies even if U.S. Food and Drug Administration approval has been obtained. Our ability to market our approved products could be substantially limited due to delays in receipt of, or failure to receive, the necessary approvals or clearances.

We are uncertain regarding the success of our clinical trials for our products in development.

We believe that all of our products in development, which consist of LungShield and RenooSkin, will require clinical trials to determine their safety and efficacy by regulatory bodies in their target markets, including the U.S. Food and Drug Administration and various foreign regulators. There can be no assurance that we will be able to successfully complete the U.S. and foreign regulatory approval processes for products in development. In addition, there can be no assurance that we will not encounter additional problems that will cause us to delay, suspend or terminate our clinical trials. In addition, we cannot make any assurance that clinical trials will be deemed sufficient in size and scope to satisfy regulatory approval requirements, or, if completed, will ultimately demonstrate our products to be safe and efficacious.

The adoption of health policy changes and health care reform in the United States may adversely affect our business and financial results.

On March 23, 2010, President Obama signed into law major health care reform legislation under the Patient Protection and Affordable Care Act of 2010, commonly referred to as the Affordable Care Act, which was modified on March 30, 2010, by the enactment of the Health Care and Education Reconciliation Act of 2010. The Affordable Care Act contains numerous regulations regarding the payment for and provision of health care, including provisions aimed at improving quality, extending health care coverage to tens of millions of individuals, enhancing remedies for fraud and abuse, adding transparency requirements and conditions to reimbursement, and decreasing health care costs. The Affordable Care Act also includes significant provisions that encourage state and federal law enforcement agencies to increase activities related to preventing, detecting and prosecuting those who commit fraud, waste and abuse in federal healthcare programs, including Medicare, Medicaid and Tricare. This legislation is one of the most comprehensive and significant reforms ever experienced by the United States health care industry and has significantly changed the way health care is financed by both governmental and private insurers. Extending health care coverage to those who previously lacked coverage will likely result in substantial cost to the United States federal government, which may force additional changes to the health care system in the United States. Much of the funding for expanded health care coverage may be sought through cost savings. While some of these savings may come from realizing greater efficiencies in delivering care, improving the effectiveness of preventive care and enhancing the overall quality of care, much of the cost savings may come from reducing the cost of health care and increased enforcement activities. The cost of health care could be reduced by decreasing the level of reimbursement for medical services or products (including products we may sell or market), or by restricting coverage of medical services or products. A reduction in the use of or reimbursement for products we may sell in the United States could materially adversely affect our business and results of operations.

| 15 |

Some of the provisions of the Affordable Care Act have not yet been fully implemented and the effect of the legislation is difficult to predict. The Affordable Care Act continues to be implemented through regulation and government activity, and is subject to possible additional implementing regulations and interpretive guidelines. Further, the Affordable Care Act has been subject to judicial and Congressional challenges, and legislative initiatives to modify, limit, or repeal the Affordable Care Act continue. It remains to be seen, however, precisely what new health care reform legislation will be enacted, if any, and what impact it will have on the availability of health care and containing or lowering the cost of health care. The manner in which the Affordable Care Act continues to evolve could materially affect the extent to which and the amount at which health care products and services are reimbursed by government programs such as Medicare, Medicaid and Tricare. We cannot predict all impacts the Affordable Care Act or other health care reform legislation may have on our products, but it may result in our products being chosen less frequently or the pricing being substantially lowered.

In addition, other health care reform proposals have emerged at the federal and state levels, including those aimed at reducing health care costs and increasing transparency. We cannot predict the effect these newly enacted laws or any future legislation or regulation will have on us. However, the implementation of new legislation and regulation may lower reimbursements for our products, increase our compliance and other costs, and adversely affect our business.

We cannot predict what additional healthcare reform initiatives may be adopted in the future or how federal and state legislative and regulatory developments are likely to evolve, but we expect ongoing initiatives in the United States to increase pressure on pricing for health care products and services. Such reforms could have an adverse effect on the pricing and market for our products.

If we fail to comply with the U.S. federal and state fraud and abuse and other health care laws and regulations, we could be subject to criminal and civil penalties and exclusion from the Medicare and Medicaid programs, which would have a material adverse effect on our business and results of operations.

All of our financial relationships with health care providers and others who provide products or services to federal health care program beneficiaries are potentially governed by the federal and state fraud and abuse laws, and other health care laws and regulations may be or become applicable to our business and operations and expose us to risk. For example:

· The federal Anti-Kickback Statute, which prohibits the offer, payment, solicitation or receipt of any form of remuneration in return for referring, ordering, leasing, purchasing or arranging for, or recommending the ordering, purchasing or leasing of, items or services payable by Medicare, Medicaid or any other federal health care program.

· Federal false claims laws and civil monetary penalty laws, including the False Claims Act, that prohibit, among other things, individuals or entities from knowingly presenting, or causing to be presented, claims for payment from Medicare, Medicaid or other government health care programs that are false or fraudulent, or making a false statement to avoid, decrease or conceal an obligation to pay money to the federal government.

· The federal Health Insurance Portability and Accountability Act of 1996, or HIPAA, which prohibits knowingly and willfully executing, or attempting to execute, a scheme to defraud any healthcare benefit program or obtain, by means of false or fraudulent pretenses, representations, or promises, any of the money or property owned by, or under the custody or control of, any health care benefit program, and for knowingly and willfully falsifying, concealing or covering up a material fact or making any materially false statements in connection with the delivery of or payment for health care benefits, items or services.

· HIPAA, as amended by the Health Information Technology for Economic and Clinical Health Act of 2009, and its implementing regulations, which also impose obligations and requirements on health care providers, health plans, and healthcare clearinghouses as well as their respective business associates that perform certain services for them that involve the use or disclosure of individually identifiable health information, with respect to safeguarding the privacy and security of certain individually identifiable health information.

| 16 |

· The federal transparency requirements under the Affordable Care Act, including the provision commonly referred to as the Physician Payments Sunshine Act, which requires certain manufacturers of drugs, devices, biologics and medical supplies that are reimbursable under Medicare, Medicaid or Children’s Health Insurance Program to report annually to Centers for Medicare and Medicaid Services, or CMS, information related to payments and other transfers of value to physicians and teaching hospitals, and ownership and investment interests held by physicians and their immediate family members.

· Analogous state and foreign laws and regulations, such as state anti-kickback and false claims laws, which may be broader in scope and apply to referrals and items or services reimbursed by both governmental and non-governmental third-party payers, including private insurers, many of which differ from each other in significant ways and often are not preempted by federal law, thus complicating compliance efforts.

Because of the breadth of these laws and the narrowness of the statutory exceptions and safe harbors available, it is possible that some of our business activities could be subject to challenge under one or more of such laws. In addition, recent health care reform legislation has strengthened these laws. Efforts to ensure that our business arrangements with third parties and our operations are compliant with applicable health care laws and regulations will involve the expenditure of appropriate, and possibly significant, resources. If we are found to be in violation of any current or future statutes or regulations involving applicable fraud and abuse or other health care laws and regulations, we may be subject to significant civil, criminal and administrative penalties, damages, fines, disgorgement, imprisonment, exclusion from government funded health care programs, such as Medicare and Medicaid, contractual damages, reputational harm, diminished profits and future earnings, which could have a material adverse effect on our business, results of operations and financial condition. If any physicians or other health care providers or entities with whom we expect to do business are found to not be in compliance with applicable laws, they may be subject to criminal, civil or administrative sanctions, including exclusions from government funded health care programs, which could adversely affect our ability to operate our business and our results of operations.

Risks Related to our Operations in Israel

We conduct our operations in Israel and therefore our results may be adversely affected by political, economic and military instability in Israel and its region.