Attached files

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on May 22, 2017

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Ranger Energy Services, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

1389 (Primary Standard Industrial Classification Code Number) |

81-5449572 (IRS Employer Identification No.) |

800 Gessner Street, Suite 1000

Houston, Texas 77024

(713) 935-8900

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Darron M. Anderson

Ranger Energy Services, Inc.

800 Gessner, Suite 1000

Houston, Texas 77024

(713) 935-8900

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

Douglas E. McWilliams Julian J. Seiguer Vinson & Elkins L.L.P. 1001 Fannin, Suite 2500 Houston, Texas 77002 (713) 758-2222 |

William J. Whelan, III Cravath, Swaine & Moore LLP 825 Eighth Avenue New York, New York 10019-7475 (212) 474-1000 |

|

Approximate date of commencement of proposed sale of the securities to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o | Emerging growth company ý |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ý

CALCULATION OF REGISTRATION FEE

|

||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee |

||

|---|---|---|---|---|

Class A common stock, par value $0.01 per share |

$100,000,000 | $11,590 | ||

|

||||

- (1)

- Includes

shares issuable upon exercise of the underwriters' option to purchase additional shares of Class A common stock.

- (2)

- Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities in any state or jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 22, 2017

Shares

Ranger Energy Services, Inc.

Class A Common Stock

We are selling shares of our Class A common stock. Prior to this offering, there has been no public market for our Class A common stock. We anticipate that the initial public offering price for our Class A common stock will be between $ and $ per share. We have applied to list our Class A common stock on the New York Stock Exchange (the "NYSE") under the symbol "RNGR."

The underwriters will have an option to purchase a maximum of additional shares of Class A common stock from us and additional shares of Class A common stock from the selling shareholders named in this prospectus to cover any over-allotment of shares.

We are an "emerging growth company" under federal securities laws and are subject to reduced public company disclosure standards. Please see "Risk Factors" and "Prospectus Summary—Emerging Growth Company Status."

Investing in our Class A common stock involves risks. See "Risk Factors" beginning on page 22.

| |

Price to Public |

Underwriting Discounts and Commissions |

Proceeds to Ranger Energy Services, Inc. (before expenses)(1) |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|

Per Share |

$ | $ | $ | |||||||

Total |

$ | $ | $ | |||||||

- (1)

- See "Underwriting" for information relating to underwriting compensation, including certain expenses of the underwriters to be reimbursed by the Company.

Delivery of the shares of Class A common stock will be made on or about , 2017.

Neither the Securities and Exchange Commission ("SEC") nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| Credit Suisse | Simmons & Company International | Wells Fargo Securities | ||

| Energy Specialists of Piper Jaffray |

Barclays

The date of this prospectus is , 2017.

Neither we, the selling shareholders nor the underwriters have authorized anyone to provide you with information different from that contained in this prospectus and any free writing prospectus we have prepared. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We, the selling shareholders and the underwriters are offering to sell shares of Class A common stock and seeking offers to buy shares of Class A common stock only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of any sale of the Class A common stock. Our business, liquidity position, financial condition, prospects or results of operations may have changed since the date of this prospectus.

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See "Risk Factors" and "Cautionary Note Regarding Forward-Looking Statements."

Dealer Prospectus Delivery Obligation

Until , 2017 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer's obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

i

Presentation of Financial and Operating Data

Unless otherwise indicated, the historical financial and operating information presented in this prospectus is that of Ranger Energy Services, LLC ("Ranger Services") and Torrent Energy Services, LLC ("Torrent Services") on a combined consolidated basis, and these entities on a combined consolidated basis are our predecessor for financial reporting purposes.

Certain amounts and percentages included in this prospectus have been rounded. Accordingly, in certain instances, the sum of the numbers in a column of a table may not exactly equal the total figure for that column.

The market data and certain other statistical information used throughout this prospectus are based on independent industry publications, government publications and other published sources, including industry reports from Coras Oilfield Research ("Coras"), including "Workover Rig Study—Cyclical Downturn Meets A Structural Shift" and "Coras Oilfield Trends—Preparing for the upcoming frac season," Spears and Associates ("Spears"), including "Drilling and Production Outlook—December 2016," "Drilling and Production Outlook—March 2017," "Well Servicing: Market Evaluation Excerpts—December 2016" and "Well Servicing: Market Evaluation—Q1 2017," and data from Qittitut Consulting ("Qittitut"), including its "US Land Drill Out Jobs Market Model—Five-Year History (2012-2016) and One-Year Forecast (2017)," and HPDI/Drillinginfo ("Drillinginfo"), including data available through its online database. Some data are also based on our good faith estimates. Although we believe these third-party sources are reliable as of their respective dates, neither we, the selling shareholders nor the underwriters have independently verified the accuracy or completeness of this information. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section entitled "Risk Factors." These and other factors could cause results to differ materially from those expressed in these publications.

We own or have rights to various trademarks, service marks and trade names that we use in connection with the operation of our business. This prospectus may also contain trademarks, service marks and trade names of third parties, which are the property of their respective owners. Our use or display of third parties' trademarks, service marks, trade names or products in this prospectus is not intended to, and does not imply a relationship with, or endorsement or sponsorship by us. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus may appear without the ®, TM or SM symbols, but the omission of such references is not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable owner of these trademarks, service marks and trade names.

ii

This summary contains basic information about us and the offering. Because it is a summary, it does not contain all the information that you should consider before investing in our Class A common stock. You should read and carefully consider this entire prospectus before making an investment decision, especially the information presented under the heading "Risk Factors," "Cautionary Note Regarding Forward-Looking Statements," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the historical combined consolidated and unaudited pro forma condensed financial statements and the related notes thereto appearing elsewhere in this prospectus.

Except as otherwise indicated or required by the context, all references in this prospectus to the "Company," "we," "us" or "our" relate, prior to the corporate reorganization described in this prospectus, to Ranger Services and Torrent Services on a combined basis (as combined, our "Predecessor," and each, a "Predecessor Company"), and following the corporate reorganization described in this prospectus, to Ranger Energy Services, Inc. ("Ranger Inc.") and its consolidated subsidiaries. References in this prospectus to "Ranger LLC" refer to RNGR Energy Services, LLC, which, following the corporate reorganization described in this prospectus, will own our operating subsidiaries, including Ranger Services and Torrent Services. References in this prospectus to the "Existing Owners" refer to Ranger Energy Holdings, LLC ("Ranger Holdings"), Ranger Energy Holdings II, LLC ("Ranger Holdings II"), Torrent Energy Holdings, LLC ("Torrent Holdings") and Torrent Energy Holdings II, LLC ("Torrent Holdings II"), the entities through which our existing investors, including CSL Capital Management ("CSL"), certain members of our management and other investors, will, following the corporate reorganization described in this prospectus, own their retained interest in us and Ranger LLC. References in this prospectus to "selling shareholders" refer to those persons identified as selling shareholders in "Principal and Selling Shareholders." We have provided definitions for certain of the industry terms used in this prospectus in the "Glossary."

Except as otherwise indicated, all information contained in this prospectus assumes or reflects no exercise of the underwriters' option to purchase additional shares of Class A common stock and excludes shares of Class A common stock reserved for issuance under our long-term incentive plan.

We are one of the largest independent providers of high-specification ("high-spec") well service rigs and associated services in the United States, with a focus on technically demanding unconventional horizontal well completion and production operations. We believe that our fleet of 68 well service rigs is among the newest and most advanced in the industry and, based on our historical rig utilization and feedback from our customers, we believe that we are an operator of choice for U.S. onshore exploration and production ("E&P") companies that require completion and production services at increasing lateral lengths. Our high-spec well service rigs facilitate operations throughout the lifecycle of a well, including (i) well completion support, such as milling out composite plugs used during hydraulic fracturing; (ii) workover, including retrieval and replacement of existing production tubing; (iii) well maintenance, including replacement of downhole artificial lift components; and (iv) decommissioning, such as plugging and abandonment operations. We also provide rental equipment, including well control packages, hydraulic catwalks and other equipment that are often deployed with our well service rigs. In addition, we own and operate a fleet of proprietary, modular natural gas processing equipment that processes rich natural gas streams at the wellhead or central gathering points. We have operations in most of the active oil and natural gas basins in the United States, including the Permian Basin, the Denver-Julesburg Basin, the Bakken Shale and the Eagle Ford Shale.

We have invested in a premier fleet of well service rigs. Our customers, which include many of the leading U.S. onshore E&P operators such as EOG Resources, Inc., Noble Energy, Inc., Oasis

1

Petroleum Inc., PDC Energy Inc. and Statoil ASA, are increasingly utilizing modern horizontal well designs characterized by long lateral lengths that can extend in excess of 12,000 feet. Long lateral length wellbores require increased amounts of completion tubing, which, in turn, require well service rigs with higher operating horsepower ("HP") to pull longer tubing strings from the wellbore. Furthermore, long lateral horizontal wells generally utilize taller stacks of wellhead equipment, which drives demand for well service rigs that have taller mast heights capable of accommodating an elevated work floor. These modern horizontal well designs are ideally serviced by "high-spec" well service rigs with high operating HP (450 HP or greater) and tall mast heights (102 feet or higher) rather than competing coiled tubing units and older or lower-spec well service rigs. As of May 19, 2017, all but one of our well service rigs meets these specifications, and approximately 78% of our well service rigs exceed these specifications with HP ratings of at least 500 HP and mast heights of at least 104 feet, making our fleet particularly well-suited to perform high-margin, horizontal well completion and production operations. The only rig in our fleet that is not high-spec is generally deployed only for plugging and abandonment operations on conventional vertical wells.

The high-spec well service rigs in our existing fleet, a substantial majority of which has been built since 2012, have an average age of approximately four years and feature modern operating components sourced from leading U.S. manufacturers such as National Oilwell Varco, Inc. ("NOV"). In February 2017, to meet expected customer demand, we entered into a purchase agreement (as subsequently amended, the "NOV Purchase Agreement") with NOV, pursuant to which we expect to accept delivery of an additional 27 high-spec well service rigs periodically throughout the remainder of 2017. However, NOV is not obligated pursuant to the NOV Purchase Agreement to deliver such high-spec well service rigs during 2017, and will not face penalties for delayed delivery, regardless of the length or cause of any delay. As a result of the NOV Purchase Agreement, our well service rig fleet will expand to 95 rigs, 94 of which will be high-spec. The following table provides summary information regarding our high-spec well service rig fleet, including the additional rigs that we expect to be delivered during the remainder of 2017. For additional information, please see "Business—Properties and Equipment—Equipment—Well Services."

HP Rating(1)

|

Mast Height | Mast Rating(2) | Manufacturer & Model | Number of High-Spec Rigs |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

600 HP |

112' - 117' | 300,000 - 350,000 lbs | NOV 6-C | 5 | * | ||||||

500 - 550 HP |

104' - 108' | 250,000 - 275,000 lbs | NOV 5-C and equivalent | 69 | ** | ||||||

450 - 475 HP |

102' - 104' | 200,000 - 250,000 lbs | NOV 4-C and equivalent | 20 | *** | ||||||

| | | | | | | | | | | | |

Total |

94 | ||||||||||

- (1)

- Per

manufacturer.

- (2)

- The

mast ratings of our high-spec well service rigs complement their high operating HP and tall mast heights by allowing such rigs to safely support the higher

weights associated with the long tubing strings used in long-lateral well completion operations.

- *

- Includes

four rigs expected to be delivered during the remainder of 2017, two of which we expect to have extended mast heights of 117 feet.

- **

- Includes

17 rigs expected to be delivered during the remainder of 2017.

- ***

- Includes six rigs expected to be delivered during the remainder of 2017.

The composition of our well service rig fleet makes it particularly well-suited to provide both completion-oriented services, the demand for which generally increases along with increased capital spending by E&P operators, and production-oriented services, the demand for which is less influenced, on a comparative basis, by such capital spending. The ability of our well service rigs to accommodate the needs of our E&P customers in a variety of economic conditions has historically allowed us to

2

maintain relatively high rig utilization as compared to our competitors. For example, our rig utilization (as defined in "Management's Discussion and Analysis of Financial Condition and Results of Operations—How We Evaluate Our Operations—Rig Utilization") during 2016 and the first quarter of 2017 was approximately 74% and 81%, respectively, which we believe to be significantly higher than that of our publicly listed competitors in the United States over such periods.

In addition to our core well service rig operations, we offer a suite of complementary services, including wireline, snubbing, fluid management and well service-related equipment rentals. Our rental equipment includes well control packages and hydraulic catwalks, which are typically deployed in conjunction with high-spec well service rigs. These complementary services and equipment are typically procured by the same decision-makers at our customers that procure our well service rigs and are provided by our same field personnel, generating incremental revenues per job while limiting our incremental costs. Our complementary well completion and production services and equipment strategically enhance our operating footprint, create operational efficiencies for our customers and allow us to capture a greater portion of their spending across the lifecycle of a well.

We also provide a range of proprietary, modular equipment for the processing of rich natural gas streams at the wellhead or central gathering points in basins where drilling and completion activity has outpaced the development of permanent processing infrastructure. Our fleet of more than 25 MRUs is modern, reliable and equipped to handle large volumes of natural gas from conventional and unconventional wells while operating across a broad array of oilfield conditions with minimal downtime and maintenance. Our customers rely on our purpose-built MRUs to process natural gas to meet pipeline specifications, extract higher value NGLs, process natural gas to conform to the specifications of fuel gas that can be used at wellsites and facilities, and to reduce the amount of hydrocarbons at the flare tip to control emissions of hazardous VOCs.

We have focused on combining our high-spec rig fleet, complementary well service operations and processing solutions with a highly skilled and experienced workforce, which enables us to consistently and efficiently deliver exceptional service while maintaining high health, safety and environmental standards. We believe that our strong operational performance and safety record provides a strong competitive advantage with current and prospective E&P customers.

We believe the demand for our services will continue to increase as a result of a number of favorable industry trends. Demand for oilfield services is primarily driven by the level of drilling, completion and production activity by E&P companies, which, in turn, depends largely on the current and anticipated profitability of developing oil and natural gas reserves. Crude oil prices have increased from their lows of $26.21 per barrel ("Bbl") in early 2016 to $49.33 per Bbl at the end of April 2017 (based on the Cushing West Texas Intermediate Spot Oil Price ("WTI")), but remain approximately 54% lower than a high of $107.26 per Bbl in June 2014. Natural gas prices have increased from their lows of $1.64 per million British Thermal Units ("MMBtu") in early 2016 to $3.17 per MMBtu at the end of April 2017 (based on the Henry Hub Natural Gas Spot Price), but remain approximately 61% lower than a high of $8.15 per MMBtu in February 2014. Drilling and completion activity by E&P companies has increased along with increased commodity prices. Although our cost of services has also historically risen along with increased commodity prices and may rise faster than increases in our revenues, we believe that we will benefit from the increased demand for our services that we expect would result from increased commodity prices. Additionally, we believe there are long term fundamental demand trends that will continue to benefit us, including:

- •

- Increasing complexity of well completion operations, including longer laterals and a greater number of frac stages per well;

- •

- Increasing percentage of rigs that are drilling horizontal wells;

3

- •

- Increasing percentage of total production attributable to older horizontal wells;

- •

- Shift towards liquids-rich development that is reliant on artificial lift technologies and associated well maintenance and workover operations;

- •

- Sizable inventory of DUC wells requiring completion; and

- •

- Increasing customer focus on well-capitalized, safe and efficient service providers that can meet or exceed their health, safety and environmental requirements.

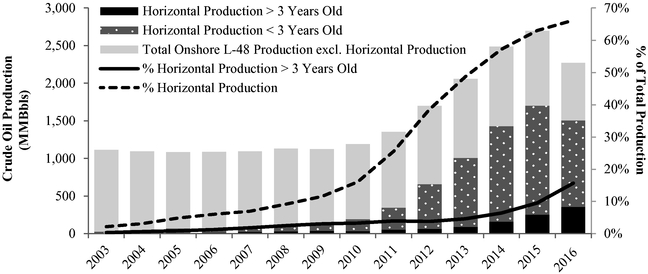

Historically, the well services market in the United States has primarily been driven by well maintenance and workover operations on conventional, vertical wells. However, Coras estimates that more than 100,000 new horizontal shale wells have been brought online over the last decade, driven by a structural shift towards unconventional resource development. According to data from the Energy Information Administration and Drillinginfo, the contribution of horizontal wells to total onshore U.S. crude oil production has increased rapidly over the last five years, representing approximately 66% of such production from the lower 48 states in 2016 as compared to approximately 39% in 2012. Further, the contribution to total onshore U.S. crude oil production of horizontal wells completed more than three years ago, which are typically the most likely to require workover and maintenance services, represented approximately 16% of such production in the lower 48 states in 2016, or approximately four times greater than that in 2012. In addition, according to Spears, a total of approximately 66,900 new horizontal wells are expected to be drilled in the United States from 2017 to 2021. Going forward, unconventional horizontal wells are expected to drive the demand for high-spec well service rigs both for completion of new wells and for maintenance and workover operations to sustain production on the increasing population of existing wells. To the extent that the oil and natural gas industry recovers from the recent prolonged decline in activity, we expect that demand for our higher-margin, completion-oriented services will grow at a faster rate in the near-term than that for our production-oriented services.

In addition to the demand trends cited above, we believe pricing for our services will be further enhanced as a result of the following supply factors:

- •

- Limited existing base of high-spec well service rigs;

- •

- Aging of existing well services equipment given the limited investment since the industry downturn in late 2014;

- •

- Limited number of manufacturers capable of building high-spec well service rigs; and

- •

- Lesser reliability of alternative techniques, including coiled tubing, for high-complexity well completions.

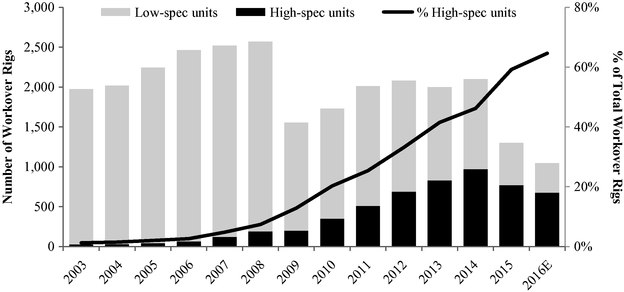

According to Coras, the vast majority of well service rigs in the United States are poorly suited for unconventional, long-lateral horizontal well applications. Coras classifies well service rigs with capacities of 450 HP or more and mast heights of 102 feet or higher as high-spec well service rigs that are ideally suited to service unconventional horizontal wells. According to Coras, the U.S. oil and natural gas industry is expected to require 1,000 to 1,500 of such ideally suited high-spec well service rigs over the next three years, as compared to an estimated total industry fleet of 770 as of February 28, 2017.

Moreover, alternative techniques for well completion, such as the deployment of coiled tubing units for drill-out operations, have increasingly become less common as wellbore lateral lengths have continued to increase beyond the point where coiled tubing can reliably be deployed for well completion. Based on discussions with our E&P customers, we believe that coiled tubing units generally begin to decrease in effectiveness at lateral lengths in excess of 8,000 feet. Spears estimates that in 2016, wells with lateral lengths in excess of 8,000 feet accounted for approximately 98% of the horizontal wells drilled in the Bakken Shale, approximately 50% of the horizontal wells drilled in the

4

Permian Basin and approximately 42% of the horizontal wells drilled in the Rocky Mountains region, including the Denver-Julesburg Basin. Increased lateral lengths in these and other basins are generally prompting operators to shift from using coiled tubing units to more reliable high-spec well service rigs. For example, according to Qittitut, approximately 45% of horizontal well completion drill-outs in 2016 were completed with well service rigs, as compared to approximately 25% in 2012.

As a result of the supply and demand trends listed above, we expect to benefit from enhanced pricing for our services and continued industry-leading utilization. We believe that increased demand for our services as a result of commodity price trends and the increasing complexity of well completion operations, along with the limited supply of high-spec well service rigs and the relative unreliability of alternative well servicing techniques, present a unique market opportunity for our high-spec well service rig operations and related services.

We believe that the following strengths will position us to achieve our primary business objective of creating value for our shareholders:

Leading Provider of High-Spec Well Service Rigs and Associated Services

We have invested in a premier fleet of well service rigs designed to efficiently execute technically challenging horizontal well completion programs as well as production-oriented well maintenance, workover and decommissioning operations. In February 2017, we entered into the NOV Purchase Agreement, pursuant to which we expect to accept delivery of an additional 27 high-spec well service rigs periodically throughout the remainder of 2017. As a result of the NOV Purchase Agreement, our total well service rig fleet will expand to 95 rigs, 94 of which will be high-spec. Based on Coras data, this makes us one of the largest independent providers of high-spec well service rigs and associated services in the United States. Further, we believe that our fleet of high-spec well service rigs is among the youngest fleet of well service rigs in the industry and is therefore more reliable and better suited to perform work on long lateral horizontal wells than the older fleets of many of our competitors. Additionally, our large and increasingly uniform fleet of high-spec well service rigs facilitates consistency in maintenance, training, in-field performance and service quality to customers. As horizontal well complexity continues to increase, we expect our customers will increasingly rely on high-spec well service rigs to perform both completion and production services. Consequently, we expect demand growth for our fleet of well service rigs to outpace that for many of our competitors' fleets.

Balanced Exposure to Completion and Production Activity

The composition of our well service rig fleet makes it particularly well-suited to provide both completion-oriented and production-oriented services. Accordingly, we benefit from increased exposure to high-margin unconventional well completion support operations during periods of increased completion activity while maintaining stable growth through workover, well maintenance and decommissioning operations on the growing base of producing wells. The ability of our well service rigs to accommodate the needs of our E&P customers in a variety of economic conditions has historically allowed us to maintain relatively high well service rig utilization as compared to our competitors. For example, our rig utilization during 2016 and the first quarter of 2017 was approximately 74% and 81%, respectively, which we believe to be significantly higher than that of our publicly listed competitors in the United States over such periods. Going forward, we believe that our balanced exposure to completion and production activity will continue to result in relatively high well service rig utilization as compared to our competitors.

5

Proprietary Natural Gas and NGL Processing Solutions

We have developed a premium offering that includes proprietary designs on modern processing equipment, including modular MRUs that process natural gas at the wellhead or central gathering points to meet pipeline specifications, extract higher value NGLs, provide fuel gas for wellsites and facilities and reduce emissions at the flare tip. To facilitate the processing of rich natural gas streams in basins where drilling and completion activity has outpaced the development of permanent processing infrastructure, we typically enter into six- to twelve-month rental agreements with customers for our full-service, turnkey solutions, providing us with relatively stable cash flows as compared to the shorter-term agreements often used for similar equipment and services. Our modular units provide flexibility across a broad range of project requirements and operating environments, and are designed to allow for quick mobilization to minimize downtime and increase utilization, particularly in conjunction with the operational support provided by our expert field personnel. We expect our advanced technology and high-quality service to continue to drive market penetration across the multiple basins in which we operate.

Deep Relationships with Blue-Chip E&P Customers across Multiple Basins

We are headquartered in Houston, Texas, and have an extensive operating footprint in key unconventional energy plays, including the Permian Basin, the Denver-Julesburg Basin, the Eagle Ford Shale and the Bakken Shale, which are among the most prolific unconventional resource plays in the United States. Our relationships with our broad customer base, which includes EOG Resources, Inc., Noble Energy, Inc., Oasis Petroleum Inc., PDC Energy Inc. and Statoil ASA, enabled us during the recent downturn to maintain higher utilization and stronger financial results than many of our competitors. Our track record of consistently providing high-quality, safe and reliable service has allowed us to develop long-term customer partnerships, which we believe makes us the service provider of choice for many of our customers. For example, in 2014, we entered into a five-year take-or-pay contract (the "EOG Contract") with EOG Resources, Inc. for three well service rigs, which was increased in 2015 to six well service rigs, operating in the Eagle Ford Shale in South Texas. Pursuant to the EOG Contract, EOG Resources, Inc. is generally obligated, with respect to each contracted well service rig, to utilize such well service rig for an average annual minimum of 2,750 hours at a stated rate based on our costs and other adjustments plus a mark-up that is subject to adjustment in certain circumstances based on market conditions and other factors. Further, during 2016, we worked for 148 distinct customers, including 33 publicly traded companies, with no customer accounting for more than 20% of our annual revenues. As our customers increase their drilling and completion activity, we expect to continue to leverage our current relationships to expand our geographic footprint and to facilitate continued growth in the basins in which we currently operate.

Strong Balance Sheet Enables Strategic Deployment of Capital

We believe our balance sheet strength has allowed us to continue to invest in our equipment and meet working capital requirements required for a fast growing business, while also providing flexibility to opportunistically pursue expansion opportunities. We believe that larger E&P operators prefer well-capitalized service providers that are better positioned to meet service requirements and financial obligations. Many of our primary competitors have high levels of total debt or recently emerged from bankruptcy during which they significantly reduced their capital and maintenance expenditures. By contrast, after giving effect to this offering and the use of proceeds therefrom, we expect to have no outstanding debt, $ million of borrowing capacity under a senior secured revolving credit facility that we intend to enter into in connection with the closing of this offering (our "Credit Facility") and approximately $ million of cash on the balance sheet (based on our cash balance as of March 31, 2017), providing us with ample liquidity to support strategic investments to continue to grow our business and enhance market share.

6

Experienced Management Team Reinforces Dedication to Safety and Reliability

The members of our management team are seasoned operating, financial and administrative executives with extensive experience in and knowledge of the oilfield services industry. Our senior executives have a strong track record in establishing oilfield service companies and growing them organically and through strategic acquisitions. Our management team is led by our President and Chief Executive Officer, Darron M. Anderson, who has more than 26 years of oil and natural gas experience and a track record of leadership in the oilfield services industry. Each member of our management team possesses significant leadership and operational experience with long tenures in the industry and respective careers at leading companies. We believe that the commitment of our management team to building and supporting a strong company culture has driven our consistent track record of reliability and safety. During 2016, our Total Recordable Incident Rates ("TRIR") in our Well Services and Processing Solutions segments were 0.72 and 0.00, respectively. Our history of safe operations enables us to qualify for projects with industry leading E&P customers that have stringent safety requirements.

We believe that we will be able to achieve our primary business objective of creating value for our shareholders by executing on the following strategies:

Capitalize on the Expected Increase in Demand for High-Spec Well Service Rigs

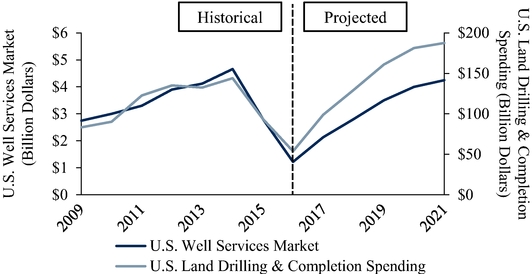

As a leading owner and operator of modern high-spec well service rigs with an operating footprint and customer relationships in the most active unconventional oil and natural gas basins in the United States, we believe that our company is well positioned to capitalize efficiently on a recovery in unconventional completion and production activity and the resulting demand for high-spec well service rigs. Further, we expect that the relatively high current inventory of DUC wells will drive demand growth for horizontal well completion services that will outpace the growth in the U.S. onshore drilling rig count. Industry reports by Spears forecast that the U.S. onshore market for completion equipment and services is expected to grow at a compound annual growth rate of 26% through 2021, primarily driven by unconventional horizontal wells. We intend to leverage our high quality assets to strategically target higher-margin, horizontal completions-oriented work that typically exceeds the capabilities of coiled tubing and older, lower specification well service rigs. Unconventional oil wells in particular typically require frequent intervention as a result of relatively high utilization of downhole tools and equipment. As the growing base of unconventional producing wells ages, we expect E&P operators to increasingly deploy well service programs in order to increase and sustain production. We are well positioned to provide these services throughout the life of the well to meet this demand, including through well completion support services, workover operations and well maintenance, which should result in stable growth, increased asset utilization, enhanced profitability and relatively limited cyclicality.

Grow Our Fleet of High-Spec Well Service Rigs, Modular MRUs and Associated Equipment

We have invested in a fleet of high-spec well service rigs through a combination of purchasing new-build rigs from leading U.S. manufacturers and by acquiring and integrating assets from other companies. As a result of the NOV Purchase Agreement, we expect to accept delivery of an additional 27 high-spec rigs periodically throughout the remainder of 2017. Further, in connection with our continued investment in high-spec well service rigs capable of meeting the most challenging horizontal well demands, we intend to accelerate our utilization of innovative technology systems allowing for the immediate collection and analysis of rig performance data. This data will allow us to operate among the highest levels of efficiency while assisting our customers in developing best well servicing practices.

We have also invested in differentiated and proprietary assets in our equipment rentals business, including our modern, reliable fleet of modular MRUs. We expect to leverage our strong balance sheet

7

and continue to strategically deploy additional capital to invest in high-spec well service rigs, purpose-built MRUs and complementary rental equipment to service our customers' well completion, production and processing operations.

Develop and Expand Relationships with Existing and New Customers

We serve well-capitalized customers that we believe will be critical to the long-term development of conventional and unconventional domestic onshore resources in the United States. We intend to continue developing long-term relationships with our customer base of leading E&P operators that value safe and reliable operations and have the financial stability and flexibility to weather most industry cycles. We believe that our strong track record of performance combined with our fleet of high-spec well service rigs will allow us to both develop new customer relationships and expand our existing customer relationships through cross-selling opportunities with respect to our complementary equipment and services. Furthermore, many of our customers have established operations throughout the United States, which we intend to leverage as opportunities for us to enter new geographic regions as well as further strengthen our presence in the regions where we currently operate.

Maintain a Conservative Balance Sheet to Pursue Organic and External Growth Opportunities

We intend to maintain a conservative approach to managing our balance sheet to preserve operational and strategic flexibility. We actively manage our liquidity by monitoring cash flow, capital spending and debt capacity. For example, as of March 31, 2017, we had only approximately $22.5 million of total combined consolidated long-term debt, all of which, as well as the additional $3.5 million incurred under the Ranger Bridge Loan (as defined herein) in April and May 2017, has been or will be repaid prior to or in connection with the consummation of this offering. Our focus on maintaining a strong balance sheet has enabled us to execute our strategy through industry volatility and commodity price cycles. We expect to fund the expansion of our high-spec well service rig fleet and continue to grow our operations with the proceeds from this offering, cash flow from operations, availability under our Credit Facility and capital markets offerings when appropriate.

Reinforce Strong Company Culture through Employee Retention and Dedication to Safety

We believe that our technically skilled personnel enable us to provide consistently reliable services while maintaining an excellent safety record that surpasses industry averages and meets the expectations of our leading E&P customers. By reinforcing our strong company culture, fostering a dedication to safety through the maintenance of stringent employee screening and training and providing opportunities to work with modern equipment and leading technologies, we expect to continue to experience relatively low turnover of our highly skilled workforce and attract additional talent to continue to deliver exceptional service to our customers.

We believe that our strong growth has been augmented by our relationship with CSL, our equity sponsor. We believe that we will continue to benefit from CSL's investment experience in the oilfield services sector, its expertise in effecting transactions and its support for our near-term and long-term strategic initiatives.

CSL is an SEC-registered private equity firm founded in early 2008 and headquartered in Houston, Texas, that invests in energy services companies and entrepreneurs with a focus on oilfield services opportunities. Since its inception, CSL has raised in excess of $1.4 billion in equity capital and commitments across various investment vehicles, including startups, growth equity, recapitalizations and restructurings in energy services, consumables and equipment. The CSL team has deep sector expertise in the energy industry and takes a hands-on approach to investments, relying on organic growth and

8

strategic thinking to generate investment success. CSL's investors include financial institutions, endowments, foundations, family offices and high net worth individuals.

Upon completion of this offering, the Existing Owners will initially own shares of Class A common stock, Ranger Units and shares of Class B common stock, representing approximately % of the voting power of our capital stock. CSL holds a majority of the voting interests in each of the Existing Owners.

For more information on CSL and the ownership of our common stock by our principal and selling shareholders, including the Existing Owners, see "Corporate Reorganization" and "Principal and Selling Shareholders."

Our History and Corporate Reorganization

Ranger Services was, through Ranger Holdings, formed by CSL in June 2014 as a provider of high-spec well service rigs and associated services. Torrent Services was, through Torrent Holdings, acquired by CSL in September 2014 as a provider of proprietary, modular equipment for the processing of natural gas. In June 2016, CSL indirectly acquired substantially all of the assets of Magna Energy Services, LLC ("Magna"), a provider of well services and wireline services, which it contributed to Ranger Services in September 2016. In October 2016, Ranger Services acquired substantially all of the assets of Bayou Workover Services, LLC ("Bayou"), an owner and operator of high-spec well service rigs. The historical combined consolidated financial information of our Predecessor included in this prospectus presents the historical financial information of the Predecessor Companies, including, as applicable, the results of operations of Magna and Bayou for periods subsequent to their respective acquisitions.

Ranger Inc. was incorporated as a Delaware corporation in February 2017. Following this offering and the corporate reorganization described below, Ranger Inc. will be a holding company, the sole material assets of which will consist of membership interests in Ranger LLC. Ranger LLC will own all of the outstanding equity interests in Ranger Services and Torrent Services, the subsidiaries through which it will operate its assets. After the consummation of the corporate reorganization described below, Ranger Inc. will be the sole managing member of Ranger LLC, will be responsible for all operational, management and administrative decisions relating to Ranger LLC's business and will consolidate the financial results of Ranger LLC and its subsidiaries.

In connection with this offering, the Existing Owners will effect a series of restructuring transactions, as a result of which (a) Ranger Holdings II and Torrent Holdings II will contribute certain of the equity interests in the Predecessor Companies to Ranger LLC in exchange for an aggregate of shares of Class A common stock, (b) Ranger Holdings and Torrent Holdings will contribute the remaining membership interests in the Predecessor Companies to Ranger LLC in exchange for units in Ranger LLC ("Ranger Units"), (c) Ranger Inc. will issue and contribute shares of its Class B common stock and all of the net proceeds received by it in this offering to Ranger LLC in exchange for Ranger Units and (d) Ranger LLC will distribute to each of Ranger Holdings and Torrent Holdings one share of Class B common stock for each Ranger Unit such Existing Owner holds. To the extent the underwriters' option to purchase additional shares is exercised in full or in part, Ranger Inc. will contribute the net proceeds received by it therefrom to Ranger LLC in exchange for an additional number of Ranger Units equal to the number of shares of Class A common stock issued by it pursuant to the underwriters' option. Ranger LLC will use such net proceeds to purchase from Ranger Holdings and Torrent Holdings an aggregate number of Ranger Units equal to the number of shares of Class A common stock issued by Ranger Inc. pursuant to the underwriters' option.

After giving effect to these transactions and the offering contemplated by this prospectus, Ranger Inc. will own an approximate % interest in Ranger LLC (or % if the underwriters'

9

option to purchase additional shares is exercised in full) and the Existing Owners will own an approximate % interest in Ranger LLC (or % if the underwriters' option to purchase additional shares is exercised in full). Please see "Principal and Selling Shareholders" and "Use of Proceeds."

Each share of Class B common stock has no economic rights but entitles its holder to one vote on all matters to be voted on by shareholders generally. Holders of Class A common stock and Class B common stock will vote together as a single class on all matters presented to our shareholders for their vote or approval, except as otherwise required by applicable law or by our amended and restated certificate of incorporation. We do not intend to list our Class B common stock on any exchange.

Following this offering, under the Amended and Restated Limited Liability Company Agreement of Ranger LLC (the "Ranger LLC Agreement"), each holder (a "Ranger Unit Holder") of Ranger Units will, subject to certain limitations, have the right (the "Redemption Right") to cause Ranger LLC to acquire all or a portion of its Ranger Units (along with a corresponding number of shares of our Class B common stock) for, at Ranger LLC's election, (i) shares of our Class A common stock at a redemption ratio of one share of Class A common stock for each Ranger Unit redeemed, subject to conversion rate adjustments for stock splits, stock dividends, reclassification and other similar transactions, or (ii) cash in an amount equal to the Cash Election Value (as defined herein) of such Class A common stock. We will determine whether to issue shares of Class A common stock or cash in an amount equal to the Cash Election Value based on facts in existence at the time of the decision, which we expect would include the trading prices for the Class A common stock at the time relative to the cash purchase price for the Ranger Units, the availability of other sources of liquidity (such as an issuance of preferred stock) to acquire the Ranger Units and alternative uses for such cash. Alternatively, upon the exercise of the Redemption Right, Ranger Inc. (instead of Ranger LLC) will have the right (the "Call Right") to, for administrative convenience, acquire each tendered Ranger Unit directly from the redeeming Ranger Unit Holder for, at its election, (x) one share of Class A common stock or (y) cash in an amount equal to the value of a share of Class A common stock, based on a volume-weighted average price. In addition, upon a change of control of us, we have the right to require each Ranger Unit Holder (other than us) to exercise its Redemption Right with respect to some or all of such unitholder's Ranger Units. In connection with any redemption of Ranger Units pursuant to the Redemption Right or our Call Right, the corresponding number of shares of Class B common stock will be cancelled. See "Certain Relationships and Related Party Transactions—Ranger LLC Agreement."

Our acquisition (or deemed acquisition for U.S. federal income tax purposes) of Ranger Units pursuant to an exercise of the Redemption Right or the Call Right is expected to result in adjustments to the tax basis of the tangible and intangible assets of Ranger LLC, and such adjustments will be allocated to us. These adjustments would not have been available to us absent our acquisition or deemed acquisition of Ranger Units and are expected to reduce the amount of cash tax that we would otherwise be required to pay in the future.

In connection with the closing of this offering, we will enter into a Tax Receivable Agreement (the "Tax Receivable Agreement") with certain of the Ranger Unit Holders and their permitted transferees (each such person, a "TRA Holder" and, together, the "TRA Holders"). The Tax Receivable Agreement will generally provide for the payment by Ranger Inc. to each TRA Holder of 85% of the net cash savings, if any, in U.S. federal, state and local income tax and franchise tax that Ranger Inc. actually realizes (computed using the estimated impact of state and local taxes) or is deemed to realize in certain circumstances in periods after this offering as a result of (i) certain increases in tax basis that occur as a result of Ranger Inc.'s acquisition (or deemed acquisition for U.S. federal income tax purposes) of all or a portion of such TRA Holder's Ranger Units in connection with this offering or pursuant to the exercise of the Redemption Right or the Call Right and (ii) imputed interest deemed to be paid by Ranger Inc. as a result of, and additional tax basis arising from, any payments

10

Ranger Inc. makes under the Tax Receivable Agreement. Ranger Inc. will retain the benefit of the remaining 15% of these cash savings.

Payments will generally be made under the Tax Receivable Agreement as we realize actual cash tax savings in periods after this offering from the tax benefits covered by the Tax Receivable Agreement. However, if we experience a change of control (as defined under the Tax Receivable Agreement, which includes certain mergers, asset sales and other forms of business combinations) or the Tax Receivable Agreement terminates early (at our election or as a result of our breach), we would be required to make a substantial, immediate lump-sum payment, and such payment may be significantly in advance of, and may materially exceed, the actual realization, if any, of the future tax benefits to which the payment relates. Ranger Inc. is a holding company and accordingly will be dependent upon distributions from Ranger LLC to make payments under the Tax Receivable Agreement. It is expected that payments will continue to be made under the Tax Receivable Agreement for more than 20 to 25 years. For additional information regarding the Tax Receivable Agreement, see "Risk Factors—Risks Related to Our Corporate Reorganization and Resulting Structure" and "Certain Relationships and Related Party Transactions—Tax Receivable Agreement."

The Existing Owners will have the right, under certain circumstances, to cause us to register the offer and resale of their shares of Class A common stock. See "Certain Relationships and Related Party Transactions—Registration Rights Agreement."

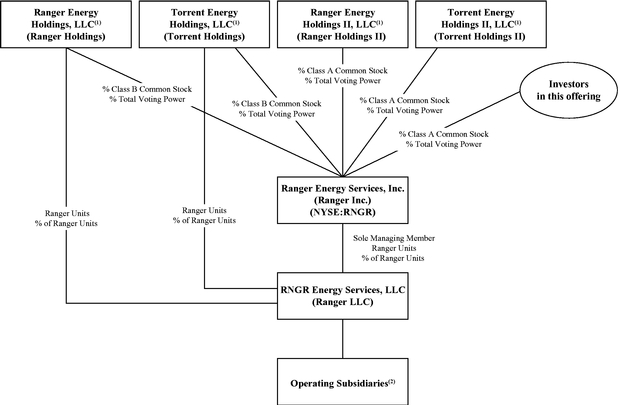

The following diagram indicates our simplified ownership structure immediately following this offering and the transactions related thereto (assuming that the underwriters' option to purchase additional shares is not exercised):

- (1)

- CSL,

certain members of our management and other investors own all of the equity interests in the Existing Owners, and CSL holds a majority of the voting interests

in each of the Existing Owners.

- (2)

- Includes Ranger Services and Torrent Services.

11

Investing in our Class A common stock involves risks. You should read carefully the section of this prospectus entitled "Risk Factors" for an explanation of these risks before investing in our Class A common stock. In particular, the following considerations may offset our competitive strengths or have a negative effect on our strategy or operating activities, which could cause a decrease in the price of our Class A common stock and a loss of all or part of your investment.

- •

- Our business depends on domestic capital spending by the oil and natural gas industry, and reductions in such capital spending could have a

material adverse effect on our business, liquidity position, financial condition, prospects and results of operations.

- •

- The volatility of oil and natural gas prices may adversely affect the demand for our services and negatively impact our results of operations.

- •

- Our operations are subject to inherent risks, some of which are beyond our control. These risks may be self-insured, or may not be fully

covered under our insurance policies.

- •

- Reliance upon a few large customers may adversely affect our revenues and operating results.

- •

- We face intense competition that may cause us to lose market share and could negatively affect our ability to market our services and expand

our operations.

- •

- We currently rely on a limited number of third-party manufacturers to build the new high-spec well service rigs that we purchase, and such

reliance exposes us to risks including price and timing of delivery.

- •

- Our operating history may not be sufficient for investors to evaluate our business and prospects.

- •

- The growth of our business through acquisitions may expose us to various risks, including those relating to difficulties in identifying

suitable, accretive acquisition opportunities and integrating businesses, assets and personnel, as well as difficulties in obtaining financing for targeted acquisitions and the potential for increased

leverage or debt service requirements.

- •

- We will incur significant capital expenditures for new equipment as we grow our operations and may be required to incur further capital

expenditures as a result of advancements in oilfield services technologies.

- •

- Increases in the scope or pace of midstream infrastructure development, or decreased federal or state regulation of natural gas pipelines,

could decrease demand for our services.

- •

- We may be unable to employ or retain a sufficient number of skilled and experienced workers.

- •

- Delays or restrictions in obtaining permits by us for our operations or by our customers for their operations could impair our business.

- •

- Federal, state and local legislative and regulatory initiatives relating to induced seismicity could result in operating restrictions or delays

in the drilling and completion of oil and natural gas wells that may reduce demand for our services and could have a material adverse effect on our business, liquidity position, financial condition,

prospects and results of operations.

- •

- Changes in transportation regulations may increase our costs and negatively impact our results of operations.

- •

- We are subject to environmental and occupational health and safety laws and regulations that may expose us to significant costs and

liabilities.

- •

- Ranger Services has had difficulty maintaining compliance with the covenants and ratios required under the Ranger Line of Credit and Ranger Note (each as defined herein). We may

12

- •

- We rely on a few key employees whose absence or loss could adversely affect our business.

- •

- We have identified a material weakness in our internal control over financial reporting and may identify additional material weaknesses in the

future or otherwise fail to maintain an effective system of internal controls, which may result in material misstatements of our financial statements or cause us to fail to meet our periodic reporting

obligations.

- •

- CSL has the ability to direct the voting of a majority of our voting stock, and its interests may conflict with those of our other

shareholders.

- •

- We expect to be a "controlled company" within the meaning of NYSE rules and, as a result, will qualify for and intend to rely on exemptions

from certain corporate governance requirements.

- •

- We are a holding company. Our sole material asset after completion of this offering will be our equity interest in Ranger LLC, and we will be accordingly dependent upon distributions from Ranger LLC to pay taxes, make payments under the Tax Receivable Agreement and cover our corporate and other overhead expenses.

have similar difficulties with the new Credit Facility that we expect to enter into in connection with the consummation of this offering. Failure to maintain compliance with these financial covenants or ratios could adversely affect our business, financial condition, results of operations and cash flows.

Emerging Growth Company Status

We are an "emerging growth company" within the meaning of the Jumpstart Our Business Startups Act (the "JOBS Act"). For as long as we are an emerging growth company, we will not be required to comply with certain requirements that are applicable to other public companies that are not "emerging growth companies" within the meaning of the JOBS Act, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 ("Sarbanes-Oxley") and the reduced disclosure obligations regarding executive compensation in our periodic reports. In addition, Section 107 of the JOBS Act provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the "Securities Act"), for complying with new or revised accounting standards. We have irrevocably opted out of the extended transition period and, as a result, we will adopt new or revised accounting standards on the relevant dates on which adoption of such standards is required for other public companies. We have elected to adopt certain of the reduced disclosure requirements available to emerging growth companies. For a description of the qualifications and other requirements applicable to emerging growth companies and certain elections that we have made due to our status as an emerging growth company, see "Risk Factors—Related to this Offering and Our Class A Common Stock—For as long as we are an emerging growth company, we will not be required to comply with certain reporting requirements, including those relating to accounting standards and disclosure about our executive compensation, that apply to other public companies."

Because CSL, through its interests in the Existing Owners, will initially hold approximately % of the voting power of our capital stock following the completion of this offering, we expect to be a controlled company as of the completion of the offering under Sarbanes-Oxley and NYSE rules. A controlled company does not need its board of directors to have a majority of independent directors or to form an independent compensation or nominating and corporate governance committee. As a controlled company, we will remain subject to rules of Sarbanes-Oxley and the NYSE that require us to have an audit committee composed entirely of independent directors. Under these rules, we must have

13

at least one independent director on our audit committee by the date our Class A common stock is listed on the NYSE, at least two independent directors on our audit committee within 90 days of the listing date, and at least three independent directors on our audit committee within one year of the listing date. We expect to have independent directors upon the closing of this offering.

If at any time we cease to be a controlled company, we will take all action necessary to comply with Sarbanes-Oxley and NYSE rules, including by appointing a majority of independent directors to our board of directors and ensuring we have a compensation committee and a nominating and corporate governance committee, each composed entirely of independent directors, subject to a permitted "phase-in" period.

Initially, our board of directors will consist of a single class of directors each serving one-year terms. After CSL and its affiliates no longer collectively hold more than 50% of the voting power of our common stock, our board of directors will be divided into three classes of directors, with each class as equal in number as possible, serving staggered three-year terms, and such directors will be removable only for "cause." See "Management—Status as a Controlled Company."

Our principal executive offices are located at 800 Gessner Street, Suite 1000, Houston, Texas 77024, and our telephone number at that address is (713) 935-8900. Our website address is www.rangerenergy.com. Information contained on our website does not constitute part of this prospectus.

14

Class A common stock offered by us |

shares ( shares if the underwriters' option to purchase additional shares is exercised in full). | |

Class A common stock offered by the selling shareholders |

shares if the underwriters' option to purchase additional shares is exercised in full. |

|

Class A common stock to be outstanding immediately after completion of this offering |

shares ( shares if the underwriters' option to purchase additional shares is exercised in full). |

|

Class B common stock to be outstanding immediately after completion of this offering |

shares ( shares if the underwriters' option to purchase additional shares is exercised in full), or one share for each Ranger Unit held by the Existing Owners immediately following this offering. Class B shares are non-economic. When a Ranger Unit is redeemed for a share of Class A common stock, a corresponding share of Class B common stock will be cancelled. |

|

Voting power of Class A common stock after giving effect to this offering |

% (or % if the underwriters' option to purchase additional shares is exercised in full). The voting power of our Class A common stock would be 100% if all outstanding Ranger Units held by the Ranger Unit Holders were redeemed (along with a corresponding number of shares of our Class B common stock) for newly issued shares of Class A common stock on a one-for-one basis. |

|

Voting power of Class B common stock after giving effect to this offering |

% (or % if the underwriters' option to purchase additional shares is exercised in full). The voting power of our Class B common stock would be 0% if all outstanding Ranger Units held by the Ranger Unit Holders were redeemed (along with a corresponding number of shares of our Class B common stock) for newly issued shares of Class A common stock on a one-for-one basis. |

|

Voting rights |

Each share of our Class A common stock entitles its holder to one vote on all matters to be voted on by shareholders generally. Each share of our Class B common stock entitles its holder to one vote on all matters to be voted on by shareholders generally. Holders of our Class A common stock and Class B common stock vote together as a single class on all matters presented to our shareholders for their vote or approval, except as otherwise required by applicable law or by our amended and restated certificate of incorporation. See "Description of Capital Stock." |

15

Use of proceeds |

We expect to receive approximately $ million of net proceeds from the sale of Class A common stock, after deducting underwriting discounts and estimated offering expenses payable by us (assuming the midpoint of the price range set forth on the cover page of this prospectus). Each $1.00 increase (decrease) in the public offering price would increase (decrease) our net proceeds by approximately $ million. | |

|

We intend to contribute all of the net proceeds received by us in this offering to Ranger LLC in exchange for Ranger Units. Ranger LLC will use approximately $29.1 million of the net proceeds to fully repay amounts outstanding under the Ranger Line of Credit, the Ranger Note and the Ranger Bridge Loan (including the make-whole premium thereon), and approximately $38.6 million of the net proceeds to acquire high-spec well service rigs, including pursuant to the NOV Purchase Agreement. Ranger LLC will use the remaining net proceeds for general corporate purposes, including funding potential future acquisitions and other capital expenditures. | |

|

To the extent the underwriters' option to purchase additional shares is exercised in full or in part, Ranger Inc. will contribute the net proceeds received by it therefrom to Ranger LLC in exchange for an additional number of Ranger Units equal to the number of shares of Class A common stock issued by it pursuant to the underwriters' option. Ranger LLC will use such net proceeds to purchase from Ranger Holdings and Torrent Holdings an aggregate number of Ranger Units equal to the number of shares of Class A common stock issued by Ranger Inc. pursuant to the underwriters' option. We will not receive any proceeds from the sale of shares by the selling shareholders. Please see "Use of Proceeds." | |

Dividend policy |

We currently anticipate that we will retain all future earnings, if any, to finance the growth and development of our business. We do not intend to pay cash dividends in the foreseeable future. Please see "Dividend Policy." |

16

Redemption rights of Ranger Unit Holders |

Following this offering, under the Ranger LLC Agreement, each Ranger Unit Holder will, subject to certain limitations, have the right, pursuant to the Redemption Right, to cause Ranger LLC to acquire all or a portion of its Ranger Units (along with a corresponding number of shares of our Class B common stock) for, at Ranger LLC's election, (i) shares of our Class A common stock at a redemption ratio of one share of Class A common stock for each Ranger Unit redeemed, subject to conversion rate adjustments for stock splits, stock dividends, reclassification and other similar transactions, or (ii) cash in an amount equal to the Cash Election Value of such Class A common stock. Alternatively, upon the exercise of the Redemption Right, Ranger Inc. (instead of Ranger LLC) will have the right, pursuant to the Call Right, to acquire each tendered Ranger Unit directly from the redeeming Ranger Unit Holder for, at its election, (x) one share of Class A common stock or (y) cash in an amount equal to the value of a share of Class A common stock, based on a volume-weighted average price. In addition, upon a change of control of us, we have the right to require each Ranger Unit Holder (other than us) to exercise its Redemption Right with respect to some or all of such unitholder's Ranger Units. In connection with any redemption of Ranger Units pursuant to the Redemption Right or our Call Right, the corresponding number of shares of Class B common stock will be cancelled. Please see "Certain Relationships and Related Party Transactions—Ranger LLC Agreement." | |

Tax Receivable Agreement |

Our acquisition (or deemed acquisition for U.S. federal income tax purposes) of Ranger Units pursuant to an exercise of the Redemption Right or the Call Right is expected to result in adjustments to the tax basis of the tangible and intangible assets of Ranger LLC, and such adjustments will be allocated to us. These adjustments would not have been available to use absent our acquisition or deemed acquisition of Ranger Units and are expected to reduce the amount of cash tax that we would otherwise be required to pay in the future. In connection with the closing of this offering, we will enter into a Tax Receivable Agreement with the TRA Holders that will generally provide for the payment by us to each TRA Holder of 85% of the net cash savings, if any, in U.S. federal, state and local income tax and franchise tax that we actually realize or are deemed to realize in certain circumstances in periods after this offering as a result of certain tax basis increases and certain tax benefits attributable to imputed interest. We will retain the benefit of the remaining 15% of these cash savings. See "Risk Factors—Risks Related to Our Corporate Reorganization and Resulting Structure" and "Certain Relationships and Related Party Transactions—Tax Receivable Agreement." |

17

Directed share program |

The underwriters have reserved for sale at the initial public offering price up to % of the Class A common stock being offered by this prospectus for sale to our employees, executive officers, directors, business associates and related persons who have expressed an interest in purchasing Class A common stock in this offering. We do not know if these persons will choose to purchase all or any portion of those reserved shares, but any purchases they do make will reduce the number of shares available to the general public. See "Underwriting." | |

Listing symbol |

We have applied to list our Class A common stock on the NYSE under the symbol "RNGR." | |

Risk factors |

You should carefully read and consider the information set forth under the heading "Risk Factors" and all other information set forth in this prospectus before deciding to invest in our Class A common stock. |

18

Summary Historical Combined Consolidated and Unaudited Pro Forma Condensed Financial and Operating Data

Ranger Inc. was formed in February 2017 and does not have historical financial results. The following table shows summary historical combined consolidated financial information of our Predecessor and summary unaudited pro forma condensed financial data for the periods and as of the dates indicated. The summary historical combined consolidated financial information at December 31, 2015 and 2016, and for the years then ended, was derived from the historical audited combined consolidated financial statements of our Predecessor included elsewhere in this prospectus. The summary historical unaudited condensed combined consolidated financial information at March 31, 2017, and for the three months ended March 31, 2016 and 2017, was derived from the historical unaudited condensed combined consolidated financial statements of our Predecessor included elsewhere in this prospectus.

The summary unaudited pro forma condensed statement of operations for the year ended December 31, 2016 has been prepared to give pro forma effect to (i) the acquisitions of Magna and Bayou (each as defined herein), (ii) the transactions described under "Corporate Reorganization" and (iii) this offering and the use of proceeds therefrom, as if each had been completed as of January 1, 2016. The summary unaudited pro forma condensed statement of operations and balance sheet for the three months ended March 31, 2017 have been prepared to give pro forma effect to (i) the transactions described under "Corporate Reorganization" and (ii) this offering and the use of proceeds therefrom, as if each had been completed on January 1, 2016, in the case of the unaudited pro forma condensed statement of operations data, and March 31, 2017, in the case of the unaudited pro forma condensed balance sheet data. This information is subject to and gives effect to the assumptions and adjustments described in the notes accompanying the unaudited pro forma condensed financial statements included elsewhere in this prospectus. The summary unaudited pro forma condensed financial data are presented for informational purposes only and should not be considered indicative of actual results of operations that would have been achieved had the applicable transactions been consummated on the dates indicated, and do not purport to be indicative of results of operations for any future period. The following table should be read together with "Use of Proceeds," "Selected Historical Combined Consolidated and Unaudited Pro Forma Condensed Financial and Operating Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations," "Corporate Reorganization" and the financial statements and related notes included elsewhere in this prospectus.

19

| |

Predecessor | Pro Forma Ranger Energy Services, Inc. |

|||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Year Ended December 31, |

Three Months Ended March 31, |

|

Three Months Ended March 31, 2017 |

|||||||||||||||

| |

Year Ended December 31, 2016 |

||||||||||||||||||

| |

2015 | 2016 | 2016 | 2017 | |||||||||||||||

| |

|

|

(unaudited) |

(unaudited) |

|||||||||||||||

| |

|

(dollars in millions, except share, per share and operational amounts) |

|

||||||||||||||||

Statements of Operations Data: |

|||||||||||||||||||

Revenues: |

|||||||||||||||||||

Well Services |

$ | 9.7 | $ | 46.3 | $ | 3.6 | $ | 27.3 | $ | $ | |||||||||

Processing Solutions |

11.5 | 6.5 | 1.2 | 1.8 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total revenues |

21.2 | 52.8 | 4.8 | 29.1 | |||||||||||||||

Operating expenses: |

|||||||||||||||||||

Cost of services (excluding depreciation and amortization shown separately): |

|||||||||||||||||||

Well Services |

8.2 | 36.7 | 2.9 | 23.2 | |||||||||||||||

Processing Solutions |

7.9 | 2.6 | 0.6 | 0.7 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total cost of services |

16.1 | 39.3 | 3.5 | 23.9 | |||||||||||||||

General and administrative |

7.8 | 11.4 | 1.7 | 7.3 | |||||||||||||||

Depreciation and amortization |

2.1 | 6.6 | 0.9 | 3.6 | |||||||||||||||

Impairment of goodwill |

1.6 | — | — | — | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total operating expenses |

27.6 | 57.3 | 6.1 | 34.8 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Operating loss |

(6.4 | ) | (4.5 | ) | (1.3 | ) | (5.7 | ) | |||||||||||

Interest expense, net |

(0.3 | ) | (0.5 | ) | (0.1 | ) | (0.5 | ) | |||||||||||

| | | | | | | | | | | | | | | | | | | | |

Loss before income taxes |

(6.7 | ) | (5.0 | ) | (1.4 | ) | (6.2 | ) | |||||||||||

Income tax provision(1) |

— | — | — | — | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Net loss |

$ | (6.7 | ) | $ | (5.0 | ) | $ | (1.4 | ) | $ | (6.2 | ) | $ | $ | |||||

| | | | | | | | | | | | | | | | | | | | |