Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - Mylan II B.V. | myl_ex32x2017331-10q.htm |

| EX-31.2 - EXHIBIT 31.2 - Mylan II B.V. | myl_ex312x2017331-10q.htm |

| EX-31.1 - EXHIBIT 31.1 - Mylan II B.V. | myl_ex311x2017331-10q.htm |

| EX-10.7 - EXHIBIT 10.7 - Mylan II B.V. | exhibit107_20170331.htm |

| EX-10.6 - EXHIBIT 10.6 - Mylan II B.V. | exhibit106_20170331.htm |

| EX-10.5 - EXHIBIT 10.5 - Mylan II B.V. | exhibit105_20170331.htm |

| EX-10.4 - EXHIBIT 10.4 - Mylan II B.V. | exhibit104_20170331.htm |

| EX-10.3 - EXHIBIT 10.3 - Mylan II B.V. | exhibit103_20170331.htm |

| EX-10.2 - EXHIBIT 10.2 - Mylan II B.V. | exhibit102_20170331.htm |

| EX-10.1 - EXHIBIT 10.1 - Mylan II B.V. | exhibit101_20170331.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Form 10-Q

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2017

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from_____________to___________

Commission File Number 333-199861

MYLAN N.V.

(Exact name of registrant as specified in its charter)

The Netherlands | 98-1189497 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

Building 4, Trident Place, Mosquito Way, Hatfield, Hertfordshire, AL10 9UL, England

(Address of principal executive offices)

+44 (0) 1707-853-000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | þ | Accelerated filer | ¨ | |||

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Emerging growth company | ¨ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to us the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨ | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

As of May 4, 2017, there were 535,950,491 of the issuer’s €0.01 nominal value ordinary shares outstanding.

MYLAN N.V. AND SUBSIDIARIES

INDEX TO FORM 10-Q

For the Quarterly Period Ended

March 31, 2017

Page | ||

PART I — FINANCIAL INFORMATION | ||

ITEM 1. | Condensed Consolidated Financial Statements (unaudited) | |

ITEM 2. | ||

ITEM 3. | ||

ITEM 4. | ||

PART II — OTHER INFORMATION | ||

ITEM 1. | ||

ITEM 1A. | ||

ITEM 6. | ||

2

PART I — FINANCIAL INFORMATION

MYLAN N.V. AND SUBSIDIARIES

Condensed Consolidated Statements of Operations

(Unaudited; in millions, except per share amounts)

Three Months Ended | |||||||

March 31, | |||||||

2017 | 2016 | ||||||

Revenues: | |||||||

Net sales | $ | 2,687.4 | $ | 2,176.1 | |||

Other revenues | 32.1 | 15.2 | |||||

Total revenues | 2,719.5 | 2,191.3 | |||||

Cost of sales | 1,634.5 | 1,284.3 | |||||

Gross profit | 1,085.0 | 907.0 | |||||

Operating expenses: | |||||||

Research and development | 217.5 | 253.6 | |||||

Selling, general and administrative | 631.3 | 549.3 | |||||

Litigation settlements and other contingencies, net | 9.0 | (1.5 | ) | ||||

Total operating expenses | 857.8 | 801.4 | |||||

Earnings from operations | 227.2 | 105.6 | |||||

Interest expense | 138.2 | 70.3 | |||||

Other expense, net | 17.4 | 16.3 | |||||

Earnings before income taxes | 71.6 | 19.0 | |||||

Income tax provision | 5.2 | 5.1 | |||||

Net earnings | $ | 66.4 | $ | 13.9 | |||

Earnings per ordinary share: | |||||||

Basic | $ | 0.12 | $ | 0.03 | |||

Diluted | $ | 0.12 | $ | 0.03 | |||

Weighted average ordinary shares outstanding: | |||||||

Basic | 534.5 | 489.8 | |||||

Diluted | 536.9 | 509.6 | |||||

See Notes to Condensed Consolidated Financial Statements

3

MYLAN N.V. AND SUBSIDIARIES

Condensed Consolidated Statements of Comprehensive Earnings

(Unaudited; in millions)

Three Months Ended | |||||||

March 31, | |||||||

2017 | 2016 | ||||||

Net earnings | $ | 66.4 | $ | 13.9 | |||

Other comprehensive earnings (loss), before tax: | |||||||

Foreign currency translation adjustment | 434.2 | 502.0 | |||||

Change in unrecognized loss and prior service cost related to defined benefit plans | — | (0.3 | ) | ||||

Net unrecognized gain (loss) on derivatives in cash flow hedging relationships | 32.4 | (49.1 | ) | ||||

Net unrecognized loss on derivatives in net investment hedging relationships | (9.9 | ) | — | ||||

Net unrealized gain on marketable securities | 7.7 | 4.4 | |||||

Other comprehensive earnings, before tax | 464.4 | 457.0 | |||||

Income tax provision (benefit) | 13.7 | (16.8 | ) | ||||

Other comprehensive earnings, net of tax | 450.7 | 473.8 | |||||

Comprehensive earnings | $ | 517.1 | $ | 487.7 | |||

See Notes to Condensed Consolidated Financial Statements

4

MYLAN N.V. AND SUBSIDIARIES

Condensed Consolidated Balance Sheets

(Unaudited; in millions, except share and per share amounts)

March 31, 2017 | December 31, 2016 | ||||||

ASSETS | |||||||

Assets | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 723.8 | $ | 998.8 | |||

Accounts receivable, net | 2,872.0 | 3,310.9 | |||||

Inventories | 2,547.8 | 2,456.4 | |||||

Prepaid expenses and other current assets | 921.9 | 756.4 | |||||

Total current assets | 7,065.5 | 7,522.5 | |||||

Property, plant and equipment, net | 2,338.0 | 2,322.2 | |||||

Intangible assets, net | 14,370.0 | 14,447.8 | |||||

Goodwill | 9,394.1 | 9,231.9 | |||||

Deferred income tax benefit | 564.0 | 633.2 | |||||

Other assets | 541.0 | 568.6 | |||||

Total assets | $ | 34,272.6 | $ | 34,726.2 | |||

LIABILITIES AND EQUITY | |||||||

Liabilities | |||||||

Current liabilities: | |||||||

Trade accounts payable | $ | 1,141.4 | $ | 1,348.1 | |||

Short-term borrowings | 31.0 | 46.4 | |||||

Income taxes payable | 31.0 | 97.7 | |||||

Current portion of long-term debt and other long-term obligations | 294.4 | 290.0 | |||||

Other current liabilities | 3,026.4 | 3,258.5 | |||||

Total current liabilities | 4,524.2 | 5,040.7 | |||||

Long-term debt | 14,700.8 | 15,202.9 | |||||

Deferred income tax liability | 2,019.1 | 2,006.4 | |||||

Other long-term obligations | 1,372.5 | 1,358.6 | |||||

Total liabilities | 22,616.6 | 23,608.6 | |||||

Equity | |||||||

Mylan N.V. shareholders’ equity | |||||||

Ordinary shares — nominal value €0.01 per ordinary share | |||||||

Shares authorized: 1,200,000,000 | |||||||

Shares issued: 537,237,925 and 536,639,291 as of March 31, 2017 and December 31, 2016 | 6.0 | 6.0 | |||||

Additional paid-in capital | 8,522.0 | 8,499.3 | |||||

Retained earnings | 5,008.5 | 4,942.1 | |||||

Accumulated other comprehensive loss | (1,813.0 | ) | (2,263.7 | ) | |||

11,723.5 | 11,183.7 | ||||||

Noncontrolling interest | — | 1.4 | |||||

Less: Treasury stock — at cost | |||||||

Ordinary shares: 1,311,193 as of March 31, 2017 and December 31, 2016 | 67.5 | 67.5 | |||||

Total equity | 11,656.0 | 11,117.6 | |||||

Total liabilities and equity | $ | 34,272.6 | $ | 34,726.2 | |||

See Notes to Condensed Consolidated Financial Statements

5

MYLAN N.V. AND SUBSIDIARIES

Condensed Consolidated Statements of Cash Flows

(Unaudited; in millions)

Three Months Ended | |||||||

March 31, | |||||||

2017 | 2016 | ||||||

Cash flows from operating activities: | |||||||

Net earnings | $ | 66.4 | $ | 13.9 | |||

Adjustments to reconcile net earnings to net cash provided by operating activities: | |||||||

Depreciation and amortization | 415.5 | 297.1 | |||||

Share-based compensation expense | 23.1 | 26.5 | |||||

Deferred income tax expense | 35.6 | 38.5 | |||||

Loss from equity method investments | 33.2 | 30.9 | |||||

Other non-cash items | 98.8 | 81.0 | |||||

Litigation settlements and other contingencies, net | 8.9 | 0.3 | |||||

Changes in operating assets and liabilities: | |||||||

Accounts receivable | 286.7 | 83.5 | |||||

Inventories | (105.6 | ) | (222.8 | ) | |||

Trade accounts payable | (242.7 | ) | (57.2 | ) | |||

Income taxes | (175.0 | ) | (84.7 | ) | |||

Other operating assets and liabilities, net | 8.0 | (126.5 | ) | ||||

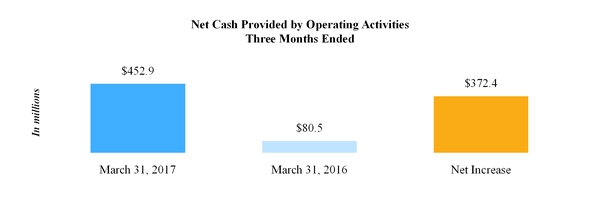

Net cash provided by operating activities | 452.9 | 80.5 | |||||

Cash flows from investing activities: | |||||||

Cash paid for acquisitions, net | (71.6 | ) | — | ||||

Capital expenditures | (58.4 | ) | (51.8 | ) | |||

Proceeds from sale of assets | 31.1 | — | |||||

Change in restricted cash | 12.7 | — | |||||

Purchase of marketable securities | (2.3 | ) | (8.5 | ) | |||

Proceeds from sale of marketable securities | 2.3 | 5.9 | |||||

Payments for product rights and other, net | (77.9 | ) | (105.6 | ) | |||

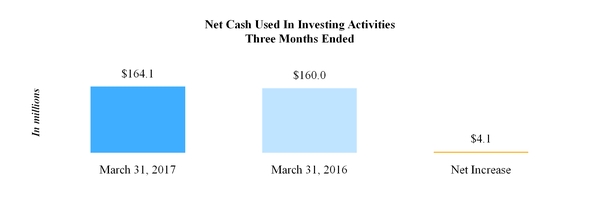

Net cash used in investing activities | (164.1 | ) | (160.0 | ) | |||

Cash flows from financing activities: | |||||||

Payments of long-term debt | (550.0 | ) | — | ||||

Change in short-term borrowings, net | (17.6 | ) | 65.1 | ||||

Taxes paid related to net share settlement of equity awards | (6.1 | ) | (6.9 | ) | |||

Contingent consideration payments | (3.8 | ) | — | ||||

Payments of financing fees | (3.7 | ) | (31.6 | ) | |||

Proceeds from exercise of stock options | 5.0 | 3.6 | |||||

Other items, net | 0.5 | 0.3 | |||||

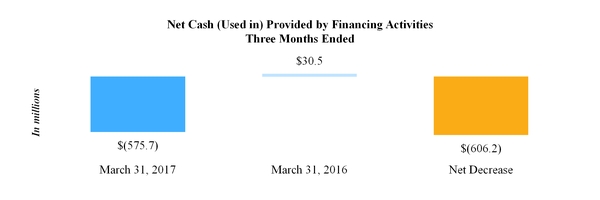

Net cash (used in) provided by financing activities | (575.7 | ) | 30.5 | ||||

Effect on cash of changes in exchange rates | 11.9 | 12.4 | |||||

Net decrease in cash and cash equivalents | (275.0 | ) | (36.6 | ) | |||

Cash and cash equivalents — beginning of period | 998.8 | 1,236.0 | |||||

Cash and cash equivalents — end of period | $ | 723.8 | $ | 1,199.4 | |||

See Notes to Condensed Consolidated Financial Statements

6

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited)

1. | General |

The accompanying unaudited Condensed Consolidated Financial Statements (“interim financial statements”) of Mylan N.V. and subsidiaries (“Mylan” or the “Company”) were prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) and the rules and regulations of the U.S. Securities and Exchange Commission (the “SEC”) for reporting on Form 10-Q; therefore, as permitted under these rules, certain footnotes and other financial information included in audited financial statements were condensed or omitted. The interim financial statements contain all adjustments (consisting of only normal recurring adjustments) necessary to present fairly the interim results of operations, comprehensive earnings, financial position and cash flows for the periods presented.

These interim financial statements should be read in conjunction with the Consolidated Financial Statements and Notes thereto in Mylan N.V.’s Annual Report on Form 10-K for the year ended December 31, 2016, as amended. The December 31, 2016 Condensed Consolidated Balance Sheet was derived from audited financial statements.

The interim results of operations, comprehensive earnings and cash flows for the three months ended March 31, 2017 are not necessarily indicative of the results to be expected for the full fiscal year or any other future period.

2. | Revenue Recognition and Accounts Receivable |

The Company recognizes net sales when title and risk of loss pass to its customers and when provisions for estimates, including discounts, sales allowances, price adjustments, returns, chargebacks and other promotional programs are reasonably determinable.

Accounts receivable are presented net of allowances relating to these provisions. No significant revisions were made to the methodology used in determining these provisions or the nature of the provisions during the three months ended March 31, 2017. Such allowances were $2.14 billion and $2.05 billion at March 31, 2017 and December 31, 2016, respectively. Other current liabilities include $616.5 million and $809.0 million at March 31, 2017 and December 31, 2016, respectively, for certain sales allowances and other adjustments that are settled in cash.

Accounts receivable, net was comprised of the following at March 31, 2017 and December 31, 2016, respectively:

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Trade receivables, net | $ | 2,568.2 | $ | 3,015.4 | |||

Other receivables | 303.8 | 295.5 | |||||

Accounts receivable, net | $ | 2,872.0 | $ | 3,310.9 | |||

Through its wholly owned subsidiary Mylan Pharmaceuticals Inc. (“MPI”), the Company has access to a $400 million accounts receivable securitization facility (the “Receivables Facility”). The receivables underlying any borrowings are included in accounts receivable, net, in the Condensed Consolidated Balance Sheets. There were $854.8 million and $1.13 billion of securitized accounts receivable at March 31, 2017 and December 31, 2016, respectively.

3. | Recent Accounting Pronouncements |

In March 2017, the Financial Accounting Standards Board (the “FASB”) issued Accounting Standards Update 2017-07, Compensation - Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost (“ASU 2017-07”), which requires companies to disaggregate the service cost component from the other components of net benefit cost and disclose the amount of net benefit cost that is included in the income statement or capitalized in assets, by line item. This guidance requires companies to report the service cost component in the same line item(s) as other compensation costs and to report other pension-related costs (which include interest costs, amortization of pension-related costs from prior periods and gains or losses on plan assets) separately and exclude them from the subtotal of operating income. This guidance also allows only the service cost component to be eligible for capitalization when applicable. This guidance is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2017. This guidance should be applied retrospectively for the presentation of the service cost component and the

7

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

other components of net periodic pension cost and net periodic postretirement benefit cost in the income statement and prospectively, on and after the effective date, for the capitalization of the service cost component of net periodic pension cost and net periodic postretirement benefit in assets. The update allows a practical expedient that permits a company to use the amounts disclosed in its pension and other postretirement plan note for the prior comparative periods as the estimation basis for applying the retrospective presentation requirements. The Company is currently assessing the impact of the adoption of this guidance on its consolidated financial statements and disclosures.

In January 2017, the FASB issued Accounting Standards Update 2017-04, Intangibles - Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment (“ASU 2017-04”), which simplifies the subsequent measurement of goodwill by eliminating Step 2 from the goodwill impairment test which previously required measurement of any goodwill impairment loss by comparing the implied fair value of a reporting unit’s goodwill with the carrying amount of that goodwill. Under ASU 2017-04, an entity should perform its annual, or interim, goodwill impairment test by comparing the fair value of a reporting unit with its carrying value and recognize an impairment charge for the amount by which the carrying amount exceeds the reporting unit’s fair value; without exceeding the total amount of goodwill allocated to that reporting unit. This guidance is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2019, with early adoption permitted. The Company has elected to early adopt this guidance as of January 1, 2017 and will apply it on a prospective basis. The adoption did not have a material impact on its condensed consolidated financial statements.

In January 2017, the FASB issued Accounting Standards Update 2017-01, Business Combinations (Topic 805) Clarifying the Definition of a Business (“ASU 2017-01”), which narrows the definition of a business and requires an entity to evaluate if substantially all of the fair value of the gross assets acquired is concentrated in a single identifiable asset or a group of similar identifiable assets, which would not constitute the acquisition of a business. The guidance also requires a business to include at least one substantive process and narrows the definition of outputs. This guidance is effective for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years, with early adoption permitted. The Company has elected to early adopt this guidance as of January 1, 2017 and will apply it on a prospective basis. The adoption did not have a material impact on its condensed consolidated financial statements.

In March 2016, the FASB issued Accounting Standards Update 2016-09, Compensation - Stock Compensation (Topic 718) (“ASU 2016-09”), which simplifies the accounting for share-based compensation payments. The new standard requires all excess tax benefits and tax deficiencies (including tax benefits of dividends on share-based payment awards) to be recognized as income tax expense or benefit on the income statement. The tax effects of exercised or vested awards should be treated as discrete items in the reporting period in which they occur. ASU 2016-09 also addresses the classification of excess tax benefits in the statement of cash flows. As required, the Company applied the provisions of ASU 2016-09 on a prospective basis as of January 1, 2017 and the adoption did not have a material impact on its condensed consolidated financial statements.

In May 2014, the FASB issued Accounting Standards Update 2014-09, Revenue from Contracts with Customers (“ASU 2014-09” updated with “ASU 2015-14”, “ASU 2016-08”, “ASU 2016-10”, “ASU 2016-12” and “ASU 2016-20”), which revises accounting guidance on revenue recognition that will supersede nearly all existing revenue recognition guidance under U.S. GAAP. The core principal of this guidance is that an entity should recognize revenue when it transfers promised goods or services to customers in an amount that reflects the consideration which the entity expects to receive in exchange for those goods or services. This guidance also requires additional disclosure about the nature, amount, timing and uncertainty of revenue and cash flows arising from customer contracts, including significant judgments and changes in judgments and assets recognized from costs incurred to obtain or fulfill a contract. This guidance is effective for fiscal years beginning after December 15, 2017, and for interim periods within those fiscal years, and can be applied using a full retrospective or modified retrospective approach. The Company continues to review specific revenue arrangements, including customer and collaboration contracts, and expects to complete the review in the third quarter of 2017. The Company is still evaluating the adoption method it will elect upon implementation.

4. | Acquisitions and Other Transactions |

Meda AB

On February 10, 2016, the Company issued an offer announcement under the Nasdaq Stockholm’s Takeover Rules and the Swedish Takeover Act (collectively, the “Swedish Takeover Rules”) setting forth a public offer to the shareholders of Meda AB (publ.) (“Meda”) to acquire all of the outstanding shares of Meda (the “Offer”), with an enterprise value, including the net debt of Meda, of approximately Swedish kronor (“SEK” or “kr”) 83.6 billion (based on a SEK/USD exchange rate of 8.4158) or $9.9 billion at announcement. On August 2, 2016, the Company announced that the Offer was accepted by Meda

8

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

shareholders holding an aggregate of approximately 343 million shares, representing approximately 94% of the total number of outstanding Meda shares, as of July 29, 2016, and the Company declared the Offer unconditional. On August 5, 2016, settlement occurred with respect to the Meda shares duly tendered by July 29, 2016 and, as a result, Meda became a controlled subsidiary of the Company. Pursuant to the terms of the Offer, each Meda shareholder that duly tendered Meda shares into the Offer received at settlement (1) in respect of 80% of the number of Meda shares tendered by such shareholder, 165kr in cash per Meda share, and (2) in respect of the remaining 20% of the number of Meda shares tendered by such shareholder, 0.386 of the Company’s ordinary shares per Meda share (subject to treatment of fractional shares as described in the offer document published on June 16, 2016). The non-tendered shares were required to be acquired for cash through a compulsory acquisition proceeding, in accordance with the Swedish Companies Act (Sw. aktiebolagslagen (2005:551)). The compulsory acquisition proceeding price accrued interest as required by the Swedish Companies Act. Meda’s shares were delisted from the Nasdaq Stockholm exchange on August 23, 2016.

On November 1, 2016, the Company made an offer to the remaining Meda shareholders to tender all their Meda shares for cash consideration of 161.31kr per Meda share (the “November Offer”) to provide such remaining shareholders with an opportunity to sell their shares in Meda to the Company in advance of the automatic acquisition of their shares for cash in connection with the compulsory acquisition proceeding. At the end of November 2016, Mylan completed the acquisition of approximately 19 million Meda shares duly tendered for aggregate cash consideration of approximately $330.3 million. In March 2017, the Company received full legal ownership to the remaining non-tendered Meda shares in exchange for a cash payment of approximately $71.6 million, equal to the uncontested portion of the compulsory acquisition price plus statutory interest, and the Company’s arrangement of a customary bank guarantee to secure the payment of any additional cash consideration that may be awarded to the former Meda shareholders in the compulsory acquisition proceeding. The arbitration tribunal conducting the compulsory acquisition proceeding will determine whether to award any such additional cash consideration at the completion of the compulsory acquisition proceeding, which is currently expected to occur in 2017 or 2018. As of March 31, 2017, the Company continues to maintain the bank guarantee as required by Swedish law. The Company does not expect that any additional payments in connection with the compulsory acquisition proceeding would be material to the consolidated financial statements.

On August 5, 2016, the total purchase price was approximately $6.92 billion, net of cash acquired, which includes cash consideration paid of approximately $5.3 billion, the issuance of approximately 26.4 million Mylan N.V. ordinary shares at a fair value of approximately $1.3 billion based on the closing price of the Company’s ordinary shares on August 5, 2016, as reported by the NASDAQ Global Select Stock Market (“NASDAQ”) and an assumed liability of approximately $431.0 million related to the November Offer and the compulsory acquisition proceeding for the non-tendered Meda shares. In accordance with U.S. GAAP, the Company used the acquisition method of accounting to account for this transaction. Under the acquisition method of accounting, the assets acquired and liabilities assumed in the transaction have been recorded at their respective estimated fair values at the acquisition date.

During the three months ended March 31, 2017, adjustments were made to the preliminary purchase price and are reflected as “Measurement Period Adjustments” in the table below. The preliminary allocation of the $6.92 billion purchase price to the assets acquired and liabilities assumed for Meda is as follows:

9

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

(In millions) | Preliminary Purchase Price Allocation as of December 31, 2016 (a) | Measurement Period Adjustments (b) | Preliminary Purchase Price Allocation as of March 31, 2017 (as adjusted) | ||||||||

Current assets (excluding inventories and net of cash acquired) | $ | 482.5 | $ | — | $ | 482.5 | |||||

Inventories | 463.1 | — | 463.1 | ||||||||

Property, plant and equipment | 177.5 | — | 177.5 | ||||||||

Identified intangible assets | 8,060.7 | — | 8,060.7 | ||||||||

Goodwill | 3,676.9 | 1.7 | 3,678.6 | ||||||||

Other assets | 9.5 | — | 9.5 | ||||||||

Total assets acquired | 12,870.2 | 1.7 | 12,871.9 | ||||||||

Current liabilities | (1,105.9 | ) | — | (1,105.9 | ) | ||||||

Long-term debt, including current portion | (2,864.6 | ) | — | (2,864.6 | ) | ||||||

Deferred tax liabilities | (1,613.9 | ) | (1.7 | ) | (1,615.6 | ) | |||||

Pension and other postretirement benefits | (322.3 | ) | — | (322.3 | ) | ||||||

Other noncurrent liabilities | (42.4 | ) | — | (42.4 | ) | ||||||

Net assets acquired | $ | 6,921.1 | $ | — | $ | 6,921.1 | |||||

(a) | As previously reported in the Company’s December 31, 2016 Annual Report on Form 10-K, as amended. |

(b) | The measurement period adjustments were recorded in the first quarter of 2017 and are primarily related to certain income tax adjustments to reflect facts and circumstances that existed as of the acquisition date. |

The preliminary fair value estimates for the assets acquired and liabilities assumed were based upon preliminary calculations, valuations and assumptions that are subject to change as the Company obtains additional information during the measurement period (up to one year from the acquisition date). The primary areas subject to change relate to the finalization of the working capital components and income taxes.

The acquisition of Meda created a more diversified and expansive portfolio of branded and generic medicines along with a strong and growing portfolio of over-the-counter (“OTC”) products. The combined company has a balanced global footprint with significant scale in key geographic markets, particularly the U.S. and Europe. The acquisition of Meda also expanded our presence in emerging markets, which includes countries in Africa, as well as countries throughout Asia and the Middle East, and is complemented by Mylan’s presence in India, Brazil and Africa (including South Africa). The Company recorded a step-up in the fair value of inventory of approximately $107 million at the acquisition date, which was fully amortized as of December 31, 2016.

The identified intangible assets of $8.06 billion are comprised of product rights and licenses that have a weighted average useful life of 20 years. Significant assumptions utilized in the valuation of identified intangible assets were based on company specific information and projections which are not observable in the market and are thus considered Level 3 measurements as defined by U.S. GAAP. The goodwill of $3.68 billion arising from the acquisition consisted largely of the value of the employee workforce and the expected value of products to be developed in the future. The final allocation of goodwill to Mylan’s reportable segments has not been completed; however, the majority of goodwill is expected to be allocated to the Europe segment. None of the goodwill recognized in this transaction is currently expected to be deductible for income tax purposes.

Renaissance Topicals Business

On June 15, 2016, the Company completed the acquisition of the non-sterile, topicals-focused business (the “Topicals Business”) of Renaissance Acquisition Holdings, LLC (“Renaissance”) for approximately $1.0 billion in cash at closing, including amounts deposited into escrow for potential contingent payments, subject to customary adjustments. The Topicals Business provided the Company with a complementary portfolio of approximately 25 products, an active pipeline of approximately 25 products, and an established U.S. sales and marketing infrastructure targeting dermatologists. The Topicals Business also provided an integrated manufacturing and development platform. In accordance with U.S. GAAP, the Company

10

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

used the acquisition method of accounting to account for this transaction. Under the acquisition method of accounting, the assets acquired and liabilities assumed in the transaction were recorded at their respective estimated fair values at the acquisition date. The U.S. GAAP purchase price was $972.7 million, which includes estimated contingent consideration of approximately $16 million related to the potential $50 million payment contingent on the achievement of certain 2016 financial targets. The $50 million contingent payment remains in escrow and is classified as restricted cash included in prepaid expenses and other current assets on the Condensed Consolidated Balance Sheets at March 31, 2017 and December 31, 2016.

The preliminary allocation of the $972.7 million purchase price to the assets acquired and liabilities assumed for the Topicals Business is as follows:

(In millions) | |||

Current assets (excluding inventories) | $ | 57.7 | |

Inventories | 74.2 | ||

Property, plant and equipment | 54.8 | ||

Identified intangible assets | 467.0 | ||

In-process research and development | 275.0 | ||

Goodwill | 318.6 | ||

Other assets | 0.1 | ||

Total assets acquired | 1,247.4 | ||

Current liabilities | (74.2 | ) | |

Deferred tax liabilities | (194.6 | ) | |

Other noncurrent liabilities | (5.9 | ) | |

Net assets acquired | $ | 972.7 | |

The preliminary fair value estimates for the assets acquired and liabilities assumed were based upon preliminary calculations, valuations and assumptions that are subject to change as the Company obtains additional information during the measurement period (up to one year from the acquisition date). The primary areas subject to change relate to the finalization of the working capital components and income taxes.

The acquisition of the Topicals Business broadened the Company’s dermatological portfolio. The amount allocated to in-process research and development (“IPR&D”) represents an estimate of the fair value of purchased in-process technology for research projects that, as of the closing date of the acquisition, had not reached technological feasibility and had no alternative future use. The fair value of IPR&D of $275.0 million was based on the excess earnings method, which utilizes forecasts of expected cash inflows (including estimates for ongoing costs) and other contributory charges. A discount rate of 12.5% was utilized to discount net cash inflows to present values. IPR&D is accounted for as an indefinite-lived intangible asset and will be subject to impairment testing until completion or abandonment of the projects. Upon successful completion and launch of each product, the Company will make a determination of the estimated useful life of the individual asset. The acquired IPR&D projects are in various stages of completion and the estimated costs to complete these projects total approximately $59 million, which is expected to be incurred through 2018. There are risks and uncertainties associated with the timely and successful completion of the projects included in IPR&D, and no assurances can be given that the underlying assumptions used to estimate the fair value of IPR&D will not change or the timely completion of each project to commercial success will occur.

The identified intangible assets of $467.0 million are comprised of $454.0 million of product rights and licenses that have a weighted average useful life of 14 years and $13.0 million of contract manufacturing agreements that have a weighted average useful life of five years. Significant assumptions utilized in the valuation of identified intangible assets were based on company specific information and projections which are not observable in the market and are thus considered Level 3 measurements as defined by U.S. GAAP.

The goodwill of $318.6 million arising from the acquisition consisted largely of the value of the employee workforce and the expected value of products to be developed in the future. All of the goodwill was assigned to the North America segment. None of the goodwill recognized in this transaction is currently expected to be deductible for income tax purposes. The acquisition did not have a material impact on a pro forma basis for the three month period ended March 31, 2016.

11

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

Unaudited Pro Forma Financial Results

The following table presents supplemental unaudited pro forma information for the acquisition of Meda, as if it had occurred on January 1, 2015. The unaudited pro forma results reflect certain adjustments related to past operating performance and acquisition accounting adjustments, such as increased amortization expense based on the fair value of assets acquired, the impact of transaction costs and the related income tax effects. The unaudited pro forma results do not include any anticipated synergies which may be achievable, or have been achieved, subsequent to the closing of the Meda transaction. Accordingly, the unaudited pro forma results are not necessarily indicative of the results that actually would have occurred had the acquisitions been completed on the stated dates above, nor are they indicative of the future operating results of Mylan N.V. and its subsidiaries.

Three Months Ended | |||

March 31, | |||

(Unaudited, in millions, except per share amounts) | 2016 | ||

Total revenues | $ | 2,687.7 | |

Net earnings | $ | 10.1 | |

Earnings per ordinary share: | |||

Basic | $ | 0.02 | |

Diluted | $ | 0.02 | |

Weighted average ordinary shares outstanding: | |||

Basic | 518.0 | ||

Diluted | 537.8 | ||

Other Transactions

On March 29, 2017, the Company announced that it had completed its acquisition of the global rights to the Cold-EEZE® brand cold remedy line from ProPhase Labs, Inc. for approximately $50 million in cash. The Company accounted for this transaction as an asset acquisition and the asset is being amortized over a useful life of 15 years. On February 14, 2017, the Company entered into a joint development and marketing agreement for a respiratory product that resulted in approximately $50 million in research and development (“R&D”) expense in the first quarter of 2017.

5. | Share-Based Incentive Plan |

The Company’s shareholders have approved the 2003 Long-Term Incentive Plan (as amended, the “2003 Plan”). Under the 2003 Plan, 55,300,000 ordinary shares are reserved for issuance to key employees, consultants, independent contractors and non-employee directors of the Company through a variety of incentive awards, including: stock options, stock appreciation rights (“SAR”), restricted ordinary shares and units, performance awards (“PSU”), other stock-based awards and short-term cash awards. Stock option awards are granted with an exercise price equal to the fair market value of the ordinary shares underlying the options at the date of the grant, generally become exercisable over periods ranging from three to four years, and generally expire in ten years. Since approval of the 2003 Plan, no further grants of stock options have been made under any other previous plan.

12

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

The following table summarizes stock option and SAR (together, “stock awards”) activity:

Number of Shares Under Stock Awards | Weighted Average Exercise Price per Share | |||||

Outstanding at December 31, 2016 | 7,699,441 | $ | 33.38 | |||

Granted | 706,995 | 45.02 | ||||

Exercised | (242,795 | ) | 21.27 | |||

Forfeited | (161,159 | ) | 50.43 | |||

Outstanding at March 31, 2017 | 8,002,482 | $ | 34.43 | |||

Vested and expected to vest at March 31, 2017 | 7,723,468 | $ | 33.98 | |||

Exercisable at March 31, 2017 | 5,976,527 | $ | 30.24 | |||

As of March 31, 2017, stock awards outstanding, stock awards vested and expected to vest, and stock awards exercisable had average remaining contractual terms of 5.9 years, 5.8 years and 4.9 years, respectively. Also, at March 31, 2017, stock awards outstanding, stock awards vested and expected to vest and stock awards exercisable had aggregate intrinsic values of $73.5 million, $73.4 million and $73.0 million, respectively.

A summary of the status of the Company’s nonvested restricted ordinary shares and restricted stock unit awards, including PSUs (collectively, “restricted stock awards”), as of March 31, 2017 and the changes during the three months ended March 31, 2017 are presented below:

Number of Restricted Stock Awards | Weighted Average Grant-Date Fair Value per Share | |||||

Nonvested at December 31, 2016 | 5,667,830 | $ | 42.46 | |||

Granted | 1,255,062 | 45.17 | ||||

Released | (483,902 | ) | 52.54 | |||

Forfeited | (117,259 | ) | 49.99 | |||

Nonvested at March 31, 2017 | 6,321,731 | $ | 42.09 | |||

As of March 31, 2017, the Company had $181.8 million of total unrecognized compensation expense, net of estimated forfeitures, related to all of its stock-based awards, which will be recognized over the remaining weighted average vesting period of 2.2 years. The total intrinsic value of stock awards exercised and restricted stock units released during the three months ended March 31, 2017 and 2016 was $26.1 million and $40.1 million, respectively.

6. | Pensions and Other Postretirement Benefits |

Defined Benefit Plans

The Company sponsors various defined benefit pension plans in several countries. Benefits provided generally depend on length of service, pay grade and remuneration levels. The Company maintains two fully frozen defined benefit pension plans in the U.S., and employees in the U.S. and Puerto Rico are generally provided retirement benefits through defined contribution plans.

The Company also sponsors other postretirement benefit plans including plans that provide for postretirement supplemental medical coverage. Benefits from these plans are provided to employees and their spouses and dependents who meet various minimum age and service requirements. In addition, the Company sponsors other plans that provide for life insurance benefits and postretirement medical coverage for certain officers and management employees.

Net Periodic Benefit Cost

Components of net periodic benefit cost for the three months ended March 31, 2017 and 2016 were as follows:

13

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

Pension and Other Postretirement Benefits | |||||||

March 31, | |||||||

(In millions) | 2017 | 2016 | |||||

Service cost | $ | 5.0 | $ | 3.9 | |||

Interest cost | 3.7 | 1.5 | |||||

Expected return on plan assets | (3.5 | ) | (2.0 | ) | |||

Amortization of prior service costs | 0.1 | 0.1 | |||||

Recognized net actuarial losses | 0.2 | 0.2 | |||||

Net periodic benefit cost | $ | 5.5 | $ | 3.7 | |||

The Company is making the minimum mandatory contributions to its U.S. defined benefit pension plans in the 2017 plan year. The Company expects to make total benefit payments of approximately $30.4 million and contributions to pension and other postretirement benefit plans of approximately $30.2 million in 2017.

7. | Balance Sheet Components |

Selected balance sheet components consist of the following:

Inventories

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Raw materials | $ | 833.8 | $ | 783.4 | |||

Work in process | 427.3 | 436.0 | |||||

Finished goods | 1,286.7 | 1,237.0 | |||||

Inventories | $ | 2,547.8 | $ | 2,456.4 | |||

Prepaid and other current assets

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Prepaid expenses | $ | 177.0 | $ | 169.1 | |||

Restricted cash | 135.8 | 148.1 | |||||

Available-for-sale securities | 91.3 | 83.7 | |||||

Fair value of financial instruments | 88.2 | 62.2 | |||||

Trading securities | 30.7 | 29.6 | |||||

Other current assets | 398.9 | 263.7 | |||||

Prepaid expenses and other current assets | $ | 921.9 | $ | 756.4 | |||

Prepaid expenses consist primarily of prepaid rent, insurance and other individually insignificant items.

14

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

Property, plant and equipment, net

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Machinery and equipment | $ | 2,245.3 | $ | 2,227.9 | |||

Buildings and improvements | 1,124.8 | 1,106.5 | |||||

Construction in progress | 330.4 | 328.8 | |||||

Land and improvements | 147.6 | 144.7 | |||||

Gross property, plant and equipment | 3,848.1 | 3,807.9 | |||||

Accumulated depreciation | 1,510.1 | 1,485.7 | |||||

Property, plant and equipment, net | $ | 2,338.0 | $ | 2,322.2 | |||

Other assets

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Equity method investments, clean energy investments | $ | 305.6 | $ | 320.6 | |||

Equity method investments, Sagent Agila | 58.6 | 75.8 | |||||

Other long-term assets | 176.8 | 172.2 | |||||

Other assets | $ | 541.0 | $ | 568.6 | |||

Trade accounts payable

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Trade accounts payable | $ | 749.6 | $ | 939.5 | |||

Other payables | 391.8 | 408.6 | |||||

Trade accounts payable | $ | 1,141.4 | $ | 1,348.1 | |||

Other current liabilities

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Accrued sales allowances | $ | 616.5 | $ | 809.0 | |||

Legal and professional accruals, including litigation accruals | 723.2 | 720.4 | |||||

Payroll and employee benefit plan accruals | 326.8 | 409.8 | |||||

Contingent consideration | 244.8 | 256.9 | |||||

Accrued interest | 130.7 | 41.0 | |||||

Restructuring | 77.2 | 138.6 | |||||

Equity method investments, clean energy investments | 65.3 | 64.7 | |||||

Fair value of financial instruments | 8.5 | 15.3 | |||||

Compulsory acquisition proceeding | — | 70.2 | |||||

Other | 833.4 | 732.6 | |||||

Other current liabilities | $ | 3,026.4 | $ | 3,258.5 | |||

On March 31, 2017, the Company announced that Meridian Medical Technologies (“Meridian”), a Pfizer company that manufactures for the EpiPen® Auto-Injector, expanded a voluntary recall of select lots of EpiPen® Auto-Injector and EpiPen Jr® Auto-Injector to include additional lots distributed in the U.S. and other markets in consultation with the U.S. Food and Drug Administration (“FDA”) (the “EpiPen® Auto-Injector Recall”). This recall was conducted as a result of the receipt of two previously disclosed reports outside of the U.S. of the failure to activate the device due to a potential defect in a supplier component. Both reports were related to the single lot that was previously recalled. The expanded voluntary recall was initiated

15

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

in the U.S. and also extends to additional markets in Europe, Asia, North and South America. The Company is replacing recalled devices at no cost to the consumer. Estimated costs to Mylan related to product recalls are based on a formal campaign soliciting return of the product and are accrued when they are deemed to be probable and can be reasonably estimated. As of March 31, 2017, the Company recorded an accrual with respect to the recall but there can be no assurance that future costs related to the recall will not exceed amounts recorded. In addition, Meridian is contractually obligated to reimburse Mylan for costs related to the EpiPen® Auto-Injector Recall, and the Company has recorded an asset for the recovery of such costs.

In March 2017, the Company completed the compulsory acquisition proceeding and settled the associated liability. The Meda shareholders whose shares were subject to the compulsory acquisition proceeding received cash consideration plus statutory interest for their Meda shares totaling approximately $71.6 million. Refer to Note 4 Acquisitions and Other Transactions for additional information.

Other long-term obligations

(In millions) | March 31, 2017 | December 31, 2016 | |||||

Employee benefit liabilities | $ | 387.1 | $ | 396.7 | |||

Contingent consideration | 321.2 | 307.7 | |||||

Equity method investments, clean energy investments | 288.5 | 302.3 | |||||

Tax contingencies | 240.5 | 239.3 | |||||

Other | 135.2 | 112.6 | |||||

Other long-term obligations | $ | 1,372.5 | $ | 1,358.6 | |||

8. | Equity Method Investments |

The Company has five equity method investments in limited liability companies that own refined coal production plants (the “clean energy investments”), whose activities qualify for income tax credits under Section 45 of the U.S. Internal Revenue Code of 1986, as amended.

Since December 2013, the Company held a 50% interest in Sagent Agila LLC (“Sagent Agila”), which was a joint venture established to develop, manufacture and distribute certain generic injectable products in the U.S. In April 2017, the Company and Sagent Pharmaceuticals Inc. (“Sagent”) finalized an agreement to dissolve the joint venture. Under the terms of the agreement, Mylan received Sagent’s interest in the joint venture in exchange for an approved product right. The assets in the joint venture consisted entirely of product rights for commercialized generic injectables. As a result of this transaction, during the three months ended March 31, 2017, the Company recognized a loss of $5.7 million as a component of net losses from equity method investments. Additionally, during the three months ended March 31, 2017, the Company received a dividend payment of $8.4 million from Sagent Agila, which reduced the carrying value of the equity investment. In the second quarter of 2017, the Company will reclassify its investment in Sagent Agila to product rights and licenses and amortize the amount over the remaining estimated useful lives of the products.

Summarized financial information, in the aggregate, for the Company’s significant equity method investments on a 100% basis for the three months ended March 31, 2017 and 2016 are as follows:

Three Months Ended | |||||||

March 31, | |||||||

(In millions) | 2017 | 2016 | |||||

Total revenues | $ | 122.9 | $ | 144.0 | |||

Gross loss | (2.7 | ) | (0.3 | ) | |||

Operating and non-operating expense | 5.8 | 5.7 | |||||

Net loss | $ | (8.5 | ) | $ | (6.0 | ) | |

The Company’s net losses from the six equity method investments includes amortization expense related to the excess of the cost basis of the Company’s investment to the underlying assets of each individual investee. For the three months ended March 31, 2017 and 2016, the Company recognized net losses from equity method investments of $33.2 million and $30.9

16

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

million, respectively, which was recognized as a component of other expense, net in the Condensed Consolidated Statements of Operations. The Company recognizes the income tax credits and benefits from the clean energy investments as part of its provision for income taxes.

9. | Earnings per Ordinary Share |

Basic earnings per ordinary share is computed by dividing net earnings by the weighted average number of ordinary shares outstanding during the period. Diluted earnings per ordinary share is computed by dividing net earnings by the weighted average number of ordinary shares outstanding during the period increased by the number of additional shares that would have been outstanding related to potentially dilutive securities or instruments, if the impact is dilutive.

On April 15, 2016, in connection with the expiration and settlement of the Company’s equity classified warrants, the Company issued approximately 17.0 million Mylan N.V. ordinary shares. The dilutive impact of the warrants, prior to settlement, is included in the calculation of diluted earnings per ordinary share based upon the average market value of the Company’s ordinary shares during the period as compared to the exercise price. For the three months ended March 31, 2016, 16.7 million warrants were included in the calculation of diluted earnings per ordinary share.

Basic and diluted earnings per ordinary share are calculated as follows:

Three Months Ended | |||||||

March 31, | |||||||

(In millions, except per share amounts) | 2017 | 2016 | |||||

Basic earnings (numerator): | |||||||

Net earnings | $ | 66.4 | $ | 13.9 | |||

Shares (denominator): | |||||||

Weighted average ordinary shares outstanding | 534.5 | 489.8 | |||||

Basic earnings per ordinary share | $ | 0.12 | $ | 0.03 | |||

Diluted earnings (numerator): | |||||||

Net earnings | $ | 66.4 | $ | 13.9 | |||

Shares (denominator): | |||||||

Weighted average ordinary shares outstanding | 534.5 | 489.8 | |||||

Share-based awards and warrants | 2.4 | 19.8 | |||||

Total dilutive shares outstanding | 536.9 | 509.6 | |||||

Diluted earnings per ordinary share | $ | 0.12 | $ | 0.03 | |||

Additional stock awards and restricted stock awards were outstanding during the three months ended March 31, 2017 and 2016, but were not included in the computation of diluted earnings per ordinary share for each respective period because the effect would be anti-dilutive. Excluded shares at March 31, 2017 include certain share-based compensation awards and restricted ordinary shares whose performance conditions had not been fully met. Such excluded shares and anti-dilutive awards represented 4.4 million shares and 6.2 million shares for the three months ended March 31, 2017 and 2016, respectively.

17

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

10. | Goodwill and Intangible Assets |

The changes in the carrying amount of goodwill for the three months ended March 31, 2017 are as follows:

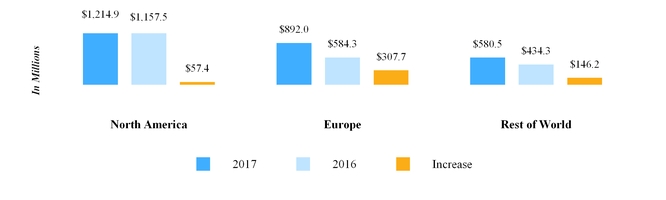

(In millions) | North America Segment | Europe Segment | Rest of World Segment | Total | |||||||||||

Balance at December 31, 2016: | |||||||||||||||

Goodwill | $ | 3,990.4 | $ | 3,859.1 | $ | 1,767.4 | $ | 9,616.9 | |||||||

Accumulated impairment losses | (385.0 | ) | — | — | (385.0 | ) | |||||||||

3,605.4 | 3,859.1 | 1,767.4 | 9,231.9 | ||||||||||||

Reclassifications(1) | (199.0 | ) | 373.2 | (174.2 | ) | — | |||||||||

Measurement period adjustments | — | 1.7 | — | 1.7 | |||||||||||

Divestiture | — | (1.3 | ) | — | (1.3 | ) | |||||||||

Foreign currency translation | 6.6 | 77.7 | 77.5 | 161.8 | |||||||||||

$ | 3,413.0 | $ | 4,310.4 | $ | 1,670.7 | $ | 9,394.1 | ||||||||

Balance at March 31, 2017: | |||||||||||||||

Goodwill | $ | 3,798.0 | $ | 4,310.4 | $ | 1,670.7 | $ | 9,779.1 | |||||||

Accumulated impairment losses | (385.0 | ) | — | — | (385.0 | ) | |||||||||

$ | 3,413.0 | $ | 4,310.4 | $ | 1,670.7 | $ | 9,394.1 | ||||||||

(1) | The reclassifications in the current quarter relate to the allocation of goodwill for the Meda acquisition. |

Intangible assets consist of the following components at March 31, 2017 and December 31, 2016:

(In millions) | Weighted Average Life (Years) | Original Cost | Accumulated Amortization | Net Book Value | |||||||||

March 31, 2017 | |||||||||||||

Amortized intangible assets: | |||||||||||||

Product rights and licenses | 15 | $ | 17,300.9 | $ | 3,986.2 | $ | 13,314.7 | ||||||

Patents and technologies | 20 | 116.6 | 109.6 | 7.0 | |||||||||

Other (1) | 6 | 468.8 | 354.7 | 114.1 | |||||||||

17,886.3 | 4,450.5 | 13,435.8 | |||||||||||

In-process research and development | 934.2 | — | 934.2 | ||||||||||

$ | 18,820.5 | $ | 4,450.5 | $ | 14,370.0 | ||||||||

December 31, 2016 | |||||||||||||

Amortized intangible assets: | |||||||||||||

Product rights and licenses | 15 | $ | 16,968.4 | $ | 3,585.7 | $ | 13,382.7 | ||||||

Patents and technologies | 20 | 116.6 | 108.5 | 8.1 | |||||||||

Other (1) | 6 | 465.9 | 330.0 | 135.9 | |||||||||

17,550.9 | 4,024.2 | 13,526.7 | |||||||||||

In-process research and development | 921.1 | — | 921.1 | ||||||||||

$ | 18,472.0 | $ | 4,024.2 | $ | 14,447.8 | ||||||||

____________

(1) | Other intangible assets consist principally of customer lists, contractual rights and other contracts. |

In December 2011, the Company completed the acquisition of the exclusive worldwide rights to develop, manufacture and commercialize a generic equivalent to GlaxoSmithKline’s Advair® Diskus and Seretide® Diskus incorporating Pfizer

18

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

Inc.’s proprietary dry powder inhaler delivery platform (the “respiratory delivery platform”). The Company accounted for this transaction as a purchase of a business and utilized the acquisition method of accounting. In conjunction with the Company’s Generic Drug User Fee Agreement goal date, on March 28, 2017, the Company received a complete response letter from the FDA regarding its Abbreviated New Drug Application for the respiratory delivery platform. As of March 31, 2017, the Company has an IPR&D asset of $347.2 million and related contingent consideration liability of $436.1 million. The Company performed an analysis and valuation of the IPR&D asset and the fair value of the related contingent consideration liability through the use of a discounted cash flow model. The model contained certain key assumptions including: the expected product launch date, the number of competitors, the timing of competition and a discount factor based on an industry specific weighted average cost of capital. Based on the analysis performed, the Company determined that the IPR&D asset was not impaired at March 31, 2017. Additionally, no significant fair value adjustment was required for the contingent consideration. However, resolution of the matters with the FDA, market conditions and other factors may result in significant changes in the projections and assumptions utilized in the discounted cash flow model, which could lead to material adjustments to the recorded amounts.

Amortization expense, which is classified primarily within cost of sales in the Condensed Consolidated Statements of Operations for the three months ended March 31, 2017 and 2016 totaled:

Three Months Ended | |||||||

March 31, | |||||||

(In millions) | 2017 | 2016 | |||||

Intangible asset amortization expense | $ | 342.4 | $ | 242.3 | |||

Intangible asset amortization expense over the remainder of 2017 and for the years ended December 31, 2018 through 2021 is estimated to be as follows:

(In millions) | |||

2017 | $ | 942 | |

2018 | 1,220 | ||

2019 | 1,130 | ||

2020 | 1,010 | ||

2021 | 936 | ||

11. | Financial Instruments and Risk Management |

The Company is exposed to certain financial risks relating to its ongoing business operations. The primary financial risks that are managed by using derivative instruments are foreign currency risk and interest rate risk.

Foreign Currency Risk Management

In order to manage foreign currency risk, the Company enters into foreign exchange forward contracts to mitigate risk associated with changes in spot exchange rates of mainly non-functional currency denominated assets or liabilities. The foreign exchange forward contracts are measured at fair value and reported as current assets or current liabilities on the Condensed Consolidated Balance Sheets. Any gains or losses on the foreign exchange forward contracts are recognized in earnings in the period incurred in the Condensed Consolidated Statements of Operations.

The Company has also entered into forward contracts to hedge forecasted foreign currency denominated sales from certain international subsidiaries. These contracts are designated as cash flow hedges to manage foreign currency transaction risk and are measured at fair value and reported as current assets or current liabilities on the Condensed Consolidated Balance Sheets. Any changes in fair value are included in earnings or deferred through accumulated other comprehensive earnings (“AOCE”), depending on the nature and effectiveness of the offset. Any ineffectiveness in a cash flow hedging relationship is recognized immediately in earnings in the Condensed Consolidated Statements of Operations.

In the first quarter of 2017, the Company designated certain Euro borrowings as a hedge of its investment in certain Euro-functional currency subsidiaries in order to manage foreign currency translation risk. The notional amount of the net investment hedges was €1.4 billion and consists of €604 million of the €1.0 billion aggregate principal amount of 2.250% Senior Notes due 2024 (the “2024 Euro Notes”) and €750 million aggregate principal amount of 3.125% Senior Notes due 2028

19

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

(the “2028 Euro Notes”). Borrowings designated as net investment hedges are marked to market using the current spot exchange rate as of the end of the period, with gains and losses included in the foreign currency translation component of AOCE until the sale or substantial liquidation of the underlying net investments. The Company recorded no ineffectiveness from its net investment hedges for the three months ended March 31, 2017. In addition, the Company manages the related foreign exchange risk of the €500 million aggregate principal amount of floating rate Senior Notes due 2018 (the “Floating Rate Euro Notes”), €750 million aggregate principal amount of 1.250% Euro Senior Notes due 2020 (the “2020 Euro Notes”) and the remaining portion of the 2024 Euro Notes through certain Euro denominated financial assets.

Interest Rate Risk Management

The Company enters into interest rate swaps in order to manage interest rate risk associated with the Company’s fixed-rate and floating-rate debt. These derivative instruments are measured at fair value and reported as current assets or current liabilities in the Condensed Consolidated Balance Sheets.

Cash Flow Hedging Relationships

The Company’s interest rate swaps designated as cash flow hedges fix the interest rate on a portion of the Company’s variable-rate debt or hedge part of the Company’s interest rate exposure associated with variability in future cash flows attributable to changes in interest rates. Any changes in fair value are included in earnings or deferred through AOCE, depending on the nature and effectiveness of the offset. Any ineffectiveness in a cash flow hedging relationship is recognized immediately in earnings in the Condensed Consolidated Statements of Operations.

Fair Value Hedging Relationships

The Company’s interest rate swaps designated as fair value hedges convert the fixed rate on a portion of the Company’s fixed-rate senior notes to a variable rate. Any changes in the fair value of these derivative instruments, as well as the offsetting change in fair value of the portion of the fixed-rate debt being hedged, is included in interest expense.

The Company regularly reviews the creditworthiness of its financial counterparties and does not expect to incur a significant loss from the failure of any counterparties to perform under any agreements. The Company is not subject to any obligations to post collateral under derivative instrument contracts. Certain derivative instrument contracts entered into by the Company are governed by master agreements, which contain credit-risk-related contingent features that would allow the counterparties to terminate the contracts early and request immediate payment should the Company trigger an event of default on other specified borrowings. The Company records all derivative instruments on a gross basis in the Condensed Consolidated Balance Sheets. Accordingly, there are no offsetting amounts that net assets against liabilities.

The Effect of Derivative Instruments on the Condensed Consolidated Balance Sheets

Fair Values of Derivative Instruments

Derivatives Designated as Hedging Instruments

Asset Derivatives | |||||||||||

March 31, 2017 | December 31, 2016 | ||||||||||

(In millions) | Balance Sheet Location | Fair Value | Balance Sheet Location | Fair Value | |||||||

Interest rate swaps | Prepaid expenses and other current assets | $ | 23.9 | Prepaid expenses and other current assets | $ | 26.2 | |||||

Foreign currency forward contracts | Prepaid expenses and other current assets | 47.5 | Prepaid expenses and other current assets | 21.9 | |||||||

Total | $ | 71.4 | $ | 48.1 | |||||||

20

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

The Effect of Derivative Instruments on the Condensed Consolidated Balance Sheets

Fair Values of Derivative Instruments

Derivatives Not Designated as Hedging Instruments

Asset Derivatives | |||||||||||

March 31, 2017 | December 31, 2016 | ||||||||||

(In millions) | Balance Sheet Location | Fair Value | Balance Sheet Location | Fair Value | |||||||

Foreign currency forward contracts | Prepaid expenses and other current assets | $ | 16.9 | Prepaid expenses and other current assets | $ | 14.0 | |||||

Total | $ | 16.9 | $ | 14.0 | |||||||

Liability Derivatives | |||||||||||

March 31, 2017 | December 31, 2016 | ||||||||||

(In millions) | Balance Sheet Location | Fair Value | Balance Sheet Location | Fair Value | |||||||

Foreign currency forward contracts | Other current liabilities | $ | 8.5 | Other current liabilities | $ | 15.3 | |||||

Total | $ | 8.5 | $ | 15.3 | |||||||

The Effect of Derivative Instruments on the Condensed Consolidated Statements of Operations

Derivatives in Fair Value Hedging Relationships

Location of (Loss) Gain Recognized in Earnings on Derivatives | Amount of (Loss) Gain Recognized in Earnings on Derivatives | ||||||||

(In millions) | Three Months Ended | ||||||||

March 31, | |||||||||

2017 | 2016 | ||||||||

Interest rate swaps | Interest expense | $ | (2.4 | ) | $ | 29.6 | |||

Total | $ | (2.4 | ) | $ | 29.6 | ||||

Location of Gain (Loss) Recognized in Earnings on Hedged Items | Amount of Gain (Loss) Recognized in Earnings on Hedged Items | ||||||||

(In millions) | Three Months Ended | ||||||||

March 31, | |||||||||

2017 | 2016 | ||||||||

2023 Senior Notes (3.125% coupon) | Interest expense | $ | 2.4 | $ | (29.6 | ) | |||

Total | $ | 2.4 | $ | (29.6 | ) | ||||

The Effect of Derivative Instruments on the Condensed Consolidated Statements of Comprehensive Earnings

Derivatives in Cash Flow Hedging Relationships

Amount of Gain (Loss) Recognized in AOCE (Net of Tax) on Derivative (Effective Portion) | ||||||||

Three Months Ended | ||||||||

March 31, | ||||||||

(In millions) | 2017 | 2016 | ||||||

Foreign currency forward contracts | $ | 14.1 | $ | (4.4 | ) | |||

Interest rate swaps | 0.7 | (35.9 | ) | |||||

Total | $ | 14.8 | $ | (40.3 | ) | |||

21

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

The Effect of Derivative Instruments on the Condensed Consolidated Statements of Comprehensive Earnings

Derivatives in Net Investment Hedging Relationships

Amount of Loss Recognized in AOCE (Net of Tax) on Derivative (Effective Portion) | ||||||||

Three Months Ended | ||||||||

March 31, | ||||||||

(In millions) | 2017 | 2016 | ||||||

Foreign currency borrowings and forward contracts | $ | (9.9 | ) | $ | — | |||

Total | $ | (9.9 | ) | $ | — | |||

The Effect of Derivative Instruments on the Condensed Consolidated Statements of Operations

Derivatives in Cash Flow Hedging Relationships

Location of Loss Reclassified from AOCE into Earnings (Effective Portion) | Amount of (Loss) Gain Reclassified from AOCE into Earnings (Effective Portion) | ||||||||

Three Months Ended | |||||||||

March 31, | |||||||||

(In millions) | 2017 | 2016 | |||||||

Foreign currency forward contracts | Net sales | $ | (5.2 | ) | $ | (10.6 | ) | ||

Interest rate swaps | Interest expense | (1.8 | ) | 0.9 | |||||

Total | $ | (7.0 | ) | $ | (9.7 | ) | |||

Location of (Loss) Gain Excluded from the Assessment of Hedge Effectiveness | Amount of (Loss) Gain Excluded from the Assessment of Hedge Effectiveness | ||||||||

Three Months Ended | |||||||||

March 31, | |||||||||

(In millions) | 2017 | 2016 | |||||||

Foreign currency forward contracts | Other expense, net | $ | (0.8 | ) | $ | 7.3 | |||

Total | $ | (0.8 | ) | $ | 7.3 | ||||

At March 31, 2017, the Company expects that approximately $1 million of pre-tax net losses on cash flow hedges will be reclassified from AOCE into earnings during the next twelve months.

The Effect of Derivative Instruments on the Condensed Consolidated Statements of Operations

Derivatives Not Designated as Hedging Instruments

Location of Loss Recognized in Earnings on Derivatives | Amount of Loss Recognized in Earnings on Derivatives | ||||||||

Three Months Ended | |||||||||

March 31, | |||||||||

(In millions) | 2017 | 2016 | |||||||

Foreign currency option and forward contracts | Other expense, net | $ | (0.3 | ) | $ | (15.0 | ) | ||

Total | $ | (0.3 | ) | $ | (15.0 | ) | |||

Fair Value Measurement

Fair value is based on the price that would be received from the sale of an identical asset or paid to transfer an identical liability in an orderly transaction between market participants at the measurement date. In order to increase consistency and

22

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

comparability in fair value measurements, a fair value hierarchy has been established that prioritizes observable and unobservable inputs used to measure fair value into three broad levels, which are described below:

• | Level 1: Quoted prices (unadjusted) in active markets that are accessible at the measurement date for identical assets or liabilities. The fair value hierarchy gives the highest priority to Level 1 inputs. |

• | Level 2: Observable market-based inputs other than quoted prices in active markets for identical assets or liabilities. |

• | Level 3: Unobservable inputs are used when little or no market data is available. The fair value hierarchy gives the lowest priority to Level 3 inputs. |

In determining fair value, the Company utilizes valuation techniques that maximize the use of observable inputs and minimize the use of unobservable inputs to the extent possible, as well as considers counterparty credit risk in its assessment of fair value.

Financial assets and liabilities carried at fair value are classified in the tables below in one of the three categories described above:

March 31, 2017 | |||||||||||||||

(In millions) | Level 1 | Level 2 | Level 3 | Total | |||||||||||

Recurring fair value measurements | |||||||||||||||

Financial Assets | |||||||||||||||

Cash equivalents: | |||||||||||||||

Money market funds | $ | 275.8 | $ | — | $ | — | $ | 275.8 | |||||||

Total cash equivalents | 275.8 | — | — | 275.8 | |||||||||||

Trading securities: | |||||||||||||||

Equity securities — exchange traded funds | 30.7 | — | — | 30.7 | |||||||||||

Total trading securities | 30.7 | — | — | 30.7 | |||||||||||

Available-for-sale fixed income investments: | |||||||||||||||

Corporate bonds | — | 18.3 | — | 18.3 | |||||||||||

U.S. Treasuries | — | 6.0 | — | 6.0 | |||||||||||

Agency mortgage-backed securities | — | 3.8 | — | 3.8 | |||||||||||

Asset backed securities | — | 1.6 | — | 1.6 | |||||||||||

Other | — | 2.2 | — | 2.2 | |||||||||||

Total available-for-sale fixed income investments | — | 31.9 | — | 31.9 | |||||||||||

Available-for-sale equity securities: | |||||||||||||||

Marketable securities | 59.4 | — | — | 59.4 | |||||||||||

Total available-for-sale equity securities | 59.4 | — | — | 59.4 | |||||||||||

Foreign exchange derivative assets | — | 64.4 | — | 64.4 | |||||||||||

Interest rate swap derivative assets | — | 23.9 | — | 23.9 | |||||||||||

Total assets at recurring fair value measurement | $ | 365.9 | $ | 120.2 | $ | — | $ | 486.1 | |||||||

Financial Liabilities | |||||||||||||||

Foreign exchange derivative liabilities | $ | — | $ | 8.5 | $ | — | $ | 8.5 | |||||||

Contingent consideration | — | — | 566.0 | 566.0 | |||||||||||

Total liabilities at recurring fair value measurement | $ | — | $ | 8.5 | $ | 566.0 | $ | 574.5 | |||||||

23

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

December 31, 2016 | |||||||||||||||

(In millions) | Level 1 | Level 2 | Level 3 | Total | |||||||||||

Recurring fair value measurements | |||||||||||||||

Financial Assets | |||||||||||||||

Cash equivalents: | |||||||||||||||

Money market funds | $ | 433.7 | $ | — | $ | — | $ | 433.7 | |||||||

Total cash equivalents | 433.7 | — | — | 433.7 | |||||||||||

Trading securities: | |||||||||||||||

Equity securities — exchange traded funds | 29.6 | — | — | 29.6 | |||||||||||

Total trading securities | 29.6 | — | — | 29.6 | |||||||||||

Available-for-sale fixed income investments: | |||||||||||||||

Corporate bonds | — | 17.5 | — | 17.5 | |||||||||||

U.S. Treasuries | — | 6.0 | — | 6.0 | |||||||||||

Agency mortgage-backed securities | — | 4.0 | — | 4.0 | |||||||||||

Asset backed securities | — | 1.6 | — | 1.6 | |||||||||||

Other | — | 2.3 | — | 2.3 | |||||||||||

Total available-for-sale fixed income investments | — | 31.4 | — | 31.4 | |||||||||||

Available-for-sale equity securities: | |||||||||||||||

Marketable securities | 52.3 | — | — | 52.3 | |||||||||||

Total available-for-sale equity securities | 52.3 | — | — | 52.3 | |||||||||||

Foreign exchange derivative assets | — | 35.9 | — | 35.9 | |||||||||||

Interest rate swap derivative assets | — | 26.2 | — | 26.2 | |||||||||||

Total assets at recurring fair value measurement | $ | 515.6 | $ | 93.5 | $ | — | $ | 609.1 | |||||||

Financial Liabilities | |||||||||||||||

Foreign exchange derivative liabilities | $ | — | $ | 15.3 | $ | — | $ | 15.3 | |||||||

Contingent consideration | — | — | 564.6 | 564.6 | |||||||||||

Total liabilities at recurring fair value measurement | $ | — | $ | 15.3 | $ | 564.6 | $ | 579.9 | |||||||

For financial assets and liabilities that utilize Level 2 inputs, the Company utilizes both direct and indirect observable price quotes, including the LIBOR yield curve, foreign exchange forward prices and bank price quotes. Below is a summary of valuation techniques for Level 1 and Level 2 financial assets and liabilities:

• | Cash equivalents — valued at observable net asset value prices. |

• | Trading securities — valued at the active quoted market price from broker or dealer quotations or transparent pricing sources at the reporting date. |

• | Available-for-sale fixed income investments — valued at the quoted market price from broker or dealer quotations or transparent pricing sources at the reporting date. |

• | Available-for-sale equity securities — valued using quoted stock prices from public exchanges at the reporting date. |

• | Interest rate swap derivative assets and liabilities — valued using the LIBOR/EURIBOR yield curves at the reporting date. Counterparties to these contracts are highly rated financial institutions. |

• | Foreign exchange derivative assets and liabilities — valued using quoted forward foreign exchange prices and spot rates at the reporting date. Counterparties to these contracts are highly rated financial institutions. |

24

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

Contingent Consideration

The fair value measurement of contingent consideration is determined using Level 3 inputs. The Company’s contingent consideration represents a component of the total purchase consideration for the respiratory delivery platform, the acquisition of Agila Specialties (“Agila”), the acquisition of certain female healthcare businesses from Famy Care Limited (such businesses “Jai Pharma Limited”), the acquisition of the Topicals Business and certain other acquisitions. The measurement is calculated using unobservable inputs based on the Company’s own assumptions. For the respiratory delivery platform, Jai Pharma Limited, the Topicals Business and certain other acquisitions, significant unobservable inputs in the valuation include the probability and timing of future development and commercial milestones and future profit sharing payments. When valuing the contingent consideration related to the respiratory delivery platform and Jai Pharma Limited, the value of the obligations are derived from a probability assessment based on expectations of when certain milestones or profit share payments occur which are discounted using a market rate of return. At March 31, 2017 and December 31, 2016, discount rates ranging from 0.9% to 10.0% were utilized in the valuations. Significant changes in unobservable inputs could result in material changes to the contingent consideration liability.

A rollforward of the activity in the Company’s fair value of contingent consideration from December 31, 2016 to March 31, 2017 is as follows:

(In millions) | Current Portion (1) | Long-Term Portion (2) | Total Contingent Consideration | ||||||||

Balance at December 31, 2016 | $ | 256.9 | $ | 307.7 | $ | 564.6 | |||||

Payments | (16.1 | ) | (0.2 | ) | (16.3 | ) | |||||

Accretion | — | 7.8 | 7.8 | ||||||||

Fair value loss(3) | 4.0 | 5.9 | 9.9 | ||||||||

Balance at March 31, 2017 | $ | 244.8 | $ | 321.2 | $ | 566.0 | |||||

(1) | Included in other current liabilities on the Condensed Consolidated Balance Sheets. |

(2) | Included in other long-term obligations on the Condensed Consolidated Balance Sheets. |

(3) | Included in litigation settlements and other contingencies, net in the Condensed Consolidated Statements of Operations. |

2017 Changes to Contingent Consideration: During the three months ended March 31, 2017, the Company recorded a fair value loss of $9.9 million related to Jai Pharma Limited contingent consideration. In addition, the Company made payments of approximately $12.5 million related to the settlement reached with Strides Arcolab Limited in November 2016.

Although the Company has not elected the fair value option for other financial assets and liabilities, any future transacted financial asset or liability will be evaluated for the fair value election.

25

MYLAN N.V. AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements (Unaudited) - Continued

12. | Debt |

Long-Term Debt

A summary of long-term debt is as follows:

____________

(In millions) | Coupon | March 31, 2017 | December 31, 2016 | |||||||

Current portion of long-term debt: | ||||||||||

Meda Bank Loans (a) | $ | 222.9 | $ | 219.6 | ||||||

Other | 4.3 | 3.7 | ||||||||

Current portion of long-term debt | $ | 227.2 | $ | 223.3 | ||||||