Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Cheniere Energy Partners, L.P. | exhibit322cqp2017form10q1s.htm |

| EX-32.1 - EXHIBIT 32.1 - Cheniere Energy Partners, L.P. | exhibit321cqp2017form10q1s.htm |

| EX-31.2 - EXHIBIT 31.2 - Cheniere Energy Partners, L.P. | exhibit312cqp2017form10q1s.htm |

| EX-31.1 - EXHIBIT 31.1 - Cheniere Energy Partners, L.P. | exhibit311cqp2017form10q1s.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2017

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Cheniere Energy Partners, L.P.

(Exact name of registrant as specified in its charter)

Delaware | 001-33366 | 20-5913059 |

(State or other jurisdiction of incorporation or organization) | (Commission File Number) | (I.R.S. Employer Identification No.) |

700 Milam Street, Suite 1900 Houston, Texas | 77002 | |

(Address of principal executive offices) | (Zip Code) | |

(713) 375-5000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x | Accelerated filer ¨ | ||||

Non-accelerated filer ¨ | (Do not check if a smaller reporting company) | ||||

Smaller reporting company ¨ | |||||

Emerging growth company ¨ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

As of April 28, 2017, the issuer had 57,109,223 common units, 145,333,334 Class B units and 135,383,831 subordinated units outstanding.

CHENIERE ENERGY PARTNERS, L.P.

TABLE OF CONTENTS

i

DEFINITIONS

As used in this quarterly report, the terms listed below have the following meanings:

Common Industry and Other Terms

Bcf | billion cubic feet | |

Bcf/d | billion cubic feet per day | |

Bcf/yr | billion cubic feet per year | |

Bcfe | billion cubic feet equivalent | |

DOE | U.S. Department of Energy | |

EPC | engineering, procurement and construction | |

FERC | Federal Energy Regulatory Commission | |

FTA countries | countries with which the United States has a free trade agreement providing for national treatment for trade in natural gas | |

GAAP | generally accepted accounting principles in the United States | |

Henry Hub | the final settlement price (in USD per MMBtu) for the New York Mercantile Exchange’s Henry Hub natural gas futures contract for the month in which a relevant cargo’s delivery window is scheduled to begin | |

LIBOR | London Interbank Offered Rate | |

LNG | liquefied natural gas, a product of natural gas that, through a refrigeration process, has been cooled to a liquid state, which occupies a volume that is approximately 1/600th of its gaseous state | |

MMBtu | million British thermal units, an energy unit | |

mtpa | million tonnes per annum | |

non-FTA countries | countries with which the United States does not have a free trade agreement providing for national treatment for trade in natural gas and with which trade is permitted | |

SEC | Securities and Exchange Commission | |

SPA | LNG sale and purchase agreement | |

Train | an industrial facility comprised of a series of refrigerant compressor loops used to cool natural gas into LNG | |

TUA | terminal use agreement | |

1

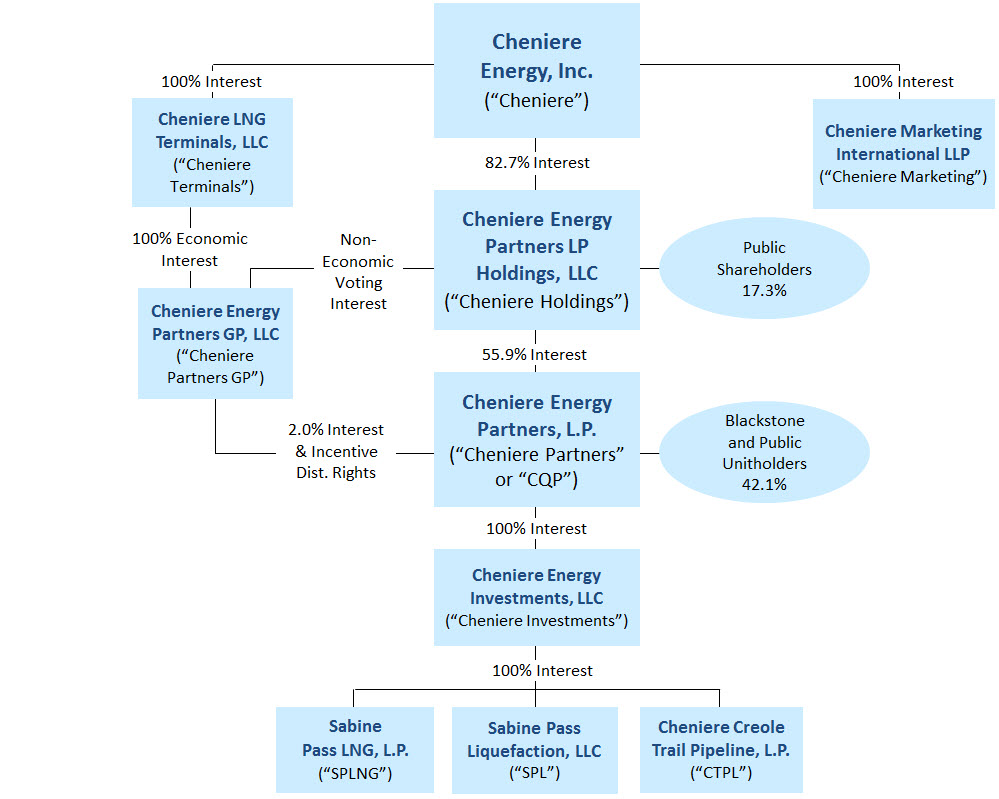

Abbreviated Organizational Structure

The following diagram depicts our abbreviated organizational structure as of March 31, 2017, including our ownership of certain subsidiaries, and the references to these entities used in this quarterly report:

Unless the context requires otherwise, references to “Cheniere Partners,” “the Partnership,” “we,” “us” and “our” refer to Cheniere Energy Partners, L.P. (NYSE MKT: CQP) and its consolidated subsidiaries, including SPLNG, SPL and CTPL.

References to “Blackstone Group” refer to The Blackstone Group, L.P. References to “Blackstone CQP Holdco” refer to Blackstone CQP Holdco LP. References to “Blackstone” refer to Blackstone Group and Blackstone CQP Holdco.

2

PART I. | FINANCIAL INFORMATION |

ITEM 1. | CONSOLIDATED FINANCIAL STATEMENTS |

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(in millions, except unit data)

March 31, | December 31, | |||||||

2017 | 2016 | |||||||

ASSETS | (unaudited) | |||||||

Current assets | ||||||||

Cash and cash equivalents | $ | — | $ | — | ||||

Restricted cash | 756 | 605 | ||||||

Accounts and other receivables | 101 | 90 | ||||||

Accounts receivable—affiliate | 89 | 99 | ||||||

Advances to affiliate | 64 | 38 | ||||||

Inventory | 87 | 97 | ||||||

Other current assets | 30 | 29 | ||||||

Total current assets | 1,127 | 958 | ||||||

Non-current restricted cash | 1,000 | — | ||||||

Property, plant and equipment, net | 14,636 | 14,158 | ||||||

Debt issuance costs, net | 80 | 121 | ||||||

Non-current derivative assets | 44 | 83 | ||||||

Other non-current assets, net | 205 | 222 | ||||||

Total assets | $ | 17,092 | $ | 15,542 | ||||

LIABILITIES AND PARTNERS’ EQUITY | ||||||||

Current liabilities | ||||||||

Accounts payable | $ | 35 | $ | 27 | ||||

Accrued liabilities | 426 | 418 | ||||||

Current debt, net | — | 224 | ||||||

Due to affiliates | 29 | 99 | ||||||

Deferred revenue | 63 | 73 | ||||||

Deferred revenue—affiliate | 20 | 1 | ||||||

Derivative liabilities | 4 | 14 | ||||||

Total current liabilities | 577 | 856 | ||||||

Long-term debt, net | 16,020 | 14,209 | ||||||

Non-current deferred revenue | 4 | 5 | ||||||

Non-current derivative liabilities | 1 | 2 | ||||||

Other non-current liabilities—affiliate | 25 | 27 | ||||||

Partners’ equity | ||||||||

Common unitholders’ interest (57.1 million units issued and outstanding at March 31, 2017 and December 31, 2016) | 50 | 130 | ||||||

Class B unitholders’ interest (145.3 million units issued and outstanding at March 31, 2017 and December 31, 2016) | 297 | 62 | ||||||

Subordinated unitholders’ interest (135.4 million units issued and outstanding at March 31, 2017 and December 31, 2016) | 107 | 240 | ||||||

General partner’s interest (2% interest with 6.9 million units issued and outstanding at March 31, 2017 and December 31, 2016) | 11 | 11 | ||||||

Total partners’ equity | 465 | 443 | ||||||

Total liabilities and partners’ equity | $ | 17,092 | $ | 15,542 | ||||

3

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(in millions, except per unit data)

(unaudited)

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Revenues | |||||||

LNG revenues | $ | 492 | $ | — | |||

LNG revenues—affiliate | 331 | — | |||||

Regasification revenues | 67 | 65 | |||||

Regasification revenues—affiliate | 1 | 2 | |||||

Total revenues | 891 | 67 | |||||

Operating costs and expenses | |||||||

Cost of sales (excluding depreciation and amortization expense shown separately below) | 513 | 4 | |||||

Operating and maintenance expense | 50 | 18 | |||||

Operating and maintenance expense—affiliate | 18 | 11 | |||||

General and administrative expense | 3 | 3 | |||||

General and administrative expense—affiliate | 22 | 22 | |||||

Depreciation and amortization expense | 66 | 19 | |||||

Total operating costs and expenses | 672 | 77 | |||||

Income (loss) from operations | 219 | (10 | ) | ||||

Other expense | |||||||

Interest expense, net of capitalized interest | (130 | ) | (43 | ) | |||

Loss on early extinguishment of debt | (42 | ) | (1 | ) | |||

Derivative loss, net | — | (21 | ) | ||||

Total other expense | (172 | ) | (65 | ) | |||

Net income (loss) | $ | 47 | $ | (75 | ) | ||

Basic and diluted net loss per common unit | $ | (0.80 | ) | $ | (0.08 | ) | |

Weighted average number of common units outstanding used for basic and diluted net loss per common unit calculation | 57.1 | 57.1 | |||||

The accompanying notes are an integral part of these consolidated financial statements.

4

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF PARTNERS’ EQUITY

(in millions)

(unaudited)

Common Unitholders’ Interest | Class B Unitholders’ Interest | Subordinated Unitholder’s Interest | General Partner’s Interest | Total Partners’ Equity | |||||||||||||||||||||||||||

Units | Amount | Units | Amount | Units | Amount | Units | Amount | ||||||||||||||||||||||||

Balance at December 31, 2016 | 57.1 | $ | 130 | 145.3 | $ | 62 | 135.4 | $ | 240 | 6.9 | $ | 11 | $ | 443 | |||||||||||||||||

Net income | — | 14 | — | — | — | 32 | — | 1 | 47 | ||||||||||||||||||||||

Distributions | — | (24 | ) | — | — | — | — | — | (1 | ) | (25 | ) | |||||||||||||||||||

Amortization of beneficial conversion feature of Class B units | — | (70 | ) | — | 235 | — | (165 | ) | — | — | — | ||||||||||||||||||||

Balance at March 31, 2017 | 57.1 | $ | 50 | 145.3 | $ | 297 | 135.4 | $ | 107 | 6.9 | $ | 11 | $ | 465 | |||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

5

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in millions)

(unaudited)

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Cash flows from operating activities | |||||||

Net income (loss) | $ | 47 | $ | (75 | ) | ||

Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: | |||||||

Depreciation and amortization expense | 66 | 19 | |||||

Amortization of debt issuance costs, deferred commitment fees, premium and discount | 10 | 4 | |||||

Loss on early extinguishment of debt | 42 | 1 | |||||

Total losses on derivatives, net | 39 | 25 | |||||

Net cash used for settlement of derivative instruments | (13 | ) | (3 | ) | |||

Changes in operating assets and liabilities: | |||||||

Accounts and other receivables | (11 | ) | — | ||||

Accounts receivable—affiliate | 59 | 1 | |||||

Advances to affiliate | (41 | ) | (1 | ) | |||

Inventory | 17 | — | |||||

Accounts payable and accrued liabilities | (38 | ) | 34 | ||||

Due to affiliates | (68 | ) | (8 | ) | |||

Deferred revenue | (11 | ) | (1 | ) | |||

Other, net | 1 | (2 | ) | ||||

Other, net—affiliate | 16 | — | |||||

Net cash provided by (used in) operating activities | 115 | (6 | ) | ||||

Cash flows from investing activities | |||||||

Property, plant and equipment, net | (524 | ) | (715 | ) | |||

Other | — | (34 | ) | ||||

Net cash used in investing activities | (524 | ) | (749 | ) | |||

Cash flows from financing activities | |||||||

Proceeds from issuances of debt | 2,314 | 1,235 | |||||

Repayments of debt | (703 | ) | (415 | ) | |||

Debt issuance and deferred financing costs | (26 | ) | (48 | ) | |||

Distributions to owners | (25 | ) | (25 | ) | |||

Net cash provided by financing activities | 1,560 | 747 | |||||

Net increase (decrease) in cash, cash equivalents and restricted cash | 1,151 | (8 | ) | ||||

Cash, cash equivalents and restricted cash—beginning of period | 605 | 434 | |||||

Cash, cash equivalents and restricted cash—end of period | $ | 1,756 | $ | 426 | |||

Balances per Consolidated Balance Sheets:

March 31, | |||||||

2017 | 2016 | ||||||

Cash and cash equivalents | $ | — | $ | 10 | |||

Restricted cash | 756 | 402 | |||||

Non-current restricted cash | 1,000 | 14 | |||||

Total cash, cash equivalents and restricted cash | $ | 1,756 | $ | 426 | |||

The accompanying notes are an integral part of these consolidated financial statements.

6

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

NOTE 1—NATURE OF OPERATIONS AND BASIS OF PRESENTATION

Through SPL, we are developing, constructing and operating natural gas liquefaction facilities (the “Liquefaction Project”) at the Sabine Pass LNG terminal located in Cameron Parish, Louisiana, on the Sabine-Neches Waterway less than four miles from the Gulf Coast. We plan to construct up to six Trains, which are in various stages of development, construction and operations. Trains 1 through 3 have commenced commercial operations, Train 4 is undergoing commissioning, Train 5 is under construction and Train 6 is being commercialized and has all necessary regulatory approvals in place. We also own and operate regasification facilities at the Sabine Pass LNG terminal through SPLNG and own a 94-mile pipeline that interconnects the Sabine Pass LNG terminal with a number of large interstate pipelines (the “Creole Trail Pipeline”) through CTPL.

In the second quarter of 2016, we started production at the Liquefaction Project and began recognizing LNG revenues, which include fees that are received pursuant to our SPAs. During the three months ended March 31, 2017, we received 94% of our net LNG revenues from two SPA customers.

We also recognize regasification revenues, which include LNG regasification capacity reservation fees that are received pursuant to our TUAs and tug services fees that are received by Sabine Pass Tug Services, LLC (“Tug Services”), a wholly owned subsidiary of SPLNG. Substantially all of our regasification revenues are received from our two long-term TUA customers.

Basis of Presentation

The accompanying unaudited Consolidated Financial Statements of Cheniere Partners have been prepared in accordance with GAAP for interim financial information and with Rule 10-01 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements and should be read in conjunction with the Consolidated Financial Statements and accompanying notes included in our annual report on Form 10-K for the year ended December 31, 2016. In our opinion, all adjustments, consisting only of normal recurring adjustments necessary for a fair presentation, have been included. Certain reclassifications have been made to conform prior period information to the current presentation. The reclassifications had no effect on our overall consolidated financial position, results of operations or cash flows.

Results of operations for the three months ended March 31, 2017 are not necessarily indicative of the results of operations that will be realized for the year ending December 31, 2017.

We are not subject to either federal or state income tax, as our partners are taxed individually on their allocable share of our taxable income.

NOTE 2—UNITHOLDERS’ EQUITY

The common units, Class B units and subordinated units represent limited partner interests in us. The holders of the units are entitled to participate in partnership distributions and exercise the rights and privileges available to limited partners under our partnership agreement. Our partnership agreement requires that, within 45 days after the end of each quarter, we distribute all of our available cash (as defined in our partnership agreement). Generally, our available cash is our cash on hand at the end of a quarter less the amount of any reserves established by our general partner. All distributions paid to date have been made from operating surplus as defined in the partnership agreement.

The holders of common units have the right to receive initial quarterly distributions of $0.425 per common unit, plus any arrearages thereon, before any distribution is made to the holders of the subordinated units. The holders of subordinated units will receive distributions only to the extent we have available cash above the initial quarterly distribution requirement for our common unitholders and general partner and certain reserves. Subordinated units will convert into common units on a one-for-one basis when we meet financial tests specified in the partnership agreement. Although common and subordinated unitholders are not obligated to fund losses of the Partnership, their capital accounts, which would be considered in allocating the net assets of the Partnership were it to be liquidated, continue to share in losses.

The general partner interest is entitled to at least 2% of all distributions made by us. In addition, the general partner holds incentive distribution rights (“IDRs”), which allow the general partner to receive a higher percentage of quarterly distributions of

7

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

available cash from operating surplus after the initial quarterly distributions have been achieved and as additional target levels are met. The higher percentages range from 15% to 50%.

During 2012, Blackstone CQP Holdco and Cheniere completed their purchases of a new class of equity interests representing limited partner interests in us (“Class B units”) for total consideration of $1.5 billion and $500 million, respectively. Proceeds from the financings were used to fund a portion of the costs of developing, constructing and placing into service the first two Trains of the Liquefaction Project. In May 2013, Cheniere purchased an additional 12.0 million Class B units for consideration of $180 million in connection with our acquisition of CTPL and Cheniere Pipeline GP Interests, LLC. In 2013, Cheniere formed Cheniere Holdings to hold its limited partner interests in us. The Class B units are subject to conversion, mandatorily or at the option of the Class B unitholders under specified circumstances, into a number of common units based on the then-applicable conversion value of the Class B units. The Class B units are not entitled to cash distributions except in the event of our liquidation or a merger, consolidation or other combination of us with another person or the sale of all or substantially all of our assets. On a quarterly basis beginning on the date of the initial purchase date of the Class B units, the conversion value of the Class B units increases at a compounded rate of 3.5% per quarter, subject to additional upward adjustment for certain equity and debt financings. The accreted conversion ratio of the Class B units owned by Cheniere Holdings and Blackstone CQP Holdco was 1.97 and 1.92, respectively, as of March 31, 2017. Since Train 3 of the Liquefaction Project achieved substantial completion in March 2017, the Class B units will mandatorily convert into common units on the first business day following the record date of our first distribution with respect to the quarter ended June 30, 2017 if not voluntarily converted by Blackstone CQP Holdco earlier.

NOTE 3—RESTRICTED CASH

Restricted cash consists of funds that are contractually restricted as to usage or withdrawal and have been presented separately from cash and cash equivalents on our Consolidated Balance Sheets. As of March 31, 2017 and December 31, 2016, restricted cash consisted of the following (in millions):

March 31, | December 31, | |||||||

2017 | 2016 | |||||||

Current restricted cash | ||||||||

Liquefaction Project | $ | 531 | $ | 358 | ||||

CQP and cash held by guarantor subsidiaries | 225 | 247 | ||||||

Total current restricted cash | $ | 756 | $ | 605 | ||||

Non-current restricted cash | ||||||||

Liquefaction Project | $ | 1,000 | $ | — | ||||

NOTE 4—ACCOUNTS AND OTHER RECEIVABLES

As of March 31, 2017 and December 31, 2016, accounts and other receivables consisted of the following (in millions):

March 31, | December 31, | |||||||

2017 | 2016 | |||||||

SPL trade receivable | $ | 92 | $ | 88 | ||||

Other accounts receivable | 9 | 2 | ||||||

Total accounts and other receivables | $ | 101 | $ | 90 | ||||

Pursuant to the accounts agreement entered into with the collateral trustee for the benefit of SPL’s debt holders, SPL is required to deposit all cash received into reserve accounts controlled by the collateral trustee. The usage or withdrawal of such cash is restricted to the payment of liabilities related to the Liquefaction Project and other restricted payments. As of March 31, 2017 and December 31, 2016, substantially all of our trade receivable balance was from two SPA customers.

8

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 5—INVENTORY

As of March 31, 2017 and December 31, 2016, inventory consisted of the following (in millions):

March 31, | December 31, | |||||||

2017 | 2016 | |||||||

Natural gas | $ | 19 | $ | 15 | ||||

LNG | 22 | 45 | ||||||

Materials and other | 46 | 37 | ||||||

Total inventory | $ | 87 | $ | 97 | ||||

NOTE 6—PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment, net consists of LNG terminal costs and fixed assets, as follows (in millions):

March 31, | December 31, | |||||||

2017 | 2016 | |||||||

LNG terminal costs | ||||||||

LNG terminal | $ | 10,420 | $ | 7,976 | ||||

LNG terminal construction-in-process | 4,826 | 6,728 | ||||||

Accumulated depreciation | (616 | ) | (553 | ) | ||||

Total LNG terminal costs, net | 14,630 | 14,151 | ||||||

Fixed assets | ||||||||

Fixed assets | 20 | 20 | ||||||

Accumulated depreciation | (14 | ) | (13 | ) | ||||

Total fixed assets, net | 6 | 7 | ||||||

Property, plant and equipment, net | $ | 14,636 | $ | 14,158 | ||||

Depreciation expense during the three months ended March 31, 2017 and 2016 was $64 million and $18 million, respectively.

During the three months ended March 31, 2017 and 2016, we realized offsets to LNG terminal costs of $124 million and $14 million, respectively, that were related to the sale of commissioning cargoes because these amounts were earned prior to the start of commercial operations, during the testing phase for the construction of the Liquefaction Project.

NOTE 7—DERIVATIVE INSTRUMENTS

We have entered into the following derivative instruments that are reported at fair value:

• | interest rate swaps to hedge the exposure to volatility in a portion of the floating-rate interest payments under certain of our credit facilities (“Interest Rate Derivatives”) and |

• | commodity derivatives consisting of natural gas supply contracts for the commissioning and operation of the Liquefaction Project (“Physical Liquefaction Supply Derivatives”) and associated economic hedges (collectively, the “Liquefaction Supply Derivatives”). |

None of our derivative instruments are designated as cash flow hedging instruments, and changes in fair value are recorded within our Consolidated Statements of Operations.

9

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The following table (in millions) shows the fair value of our derivative instruments that are required to be measured at fair value on a recurring basis as of March 31, 2017 and December 31, 2016, which are classified as other current assets, non-current derivative assets, derivative liabilities or non-current derivative liabilities in our Consolidated Balance Sheets.

Fair Value Measurements as of | |||||||||||||||||||||||||||||||

March 31, 2017 | December 31, 2016 | ||||||||||||||||||||||||||||||

Quoted Prices in Active Markets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | Quoted Prices in Active Markets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | ||||||||||||||||||||||||

SPL Interest Rate Derivatives liability | $ | — | $ | — | $ | — | $ | — | $ | — | $ | (6 | ) | $ | — | $ | (6 | ) | |||||||||||||

CQP Interest Rate Derivatives asset | — | 16 | — | 16 | — | 13 | — | 13 | |||||||||||||||||||||||

Liquefaction Supply Derivatives asset (liability) | (2 | ) | — | 41 | 39 | (4 | ) | (2 | ) | 79 | 73 | ||||||||||||||||||||

There have been no changes to our evaluation of and accounting for our derivative positions designated as Level 1 during the three months ended March 31, 2017. See Note 8—Derivative Instruments of our Notes to Consolidated Financial Statements in our annual report on Form 10-K for the year ended December 31, 2016 for additional information.

We value our Interest Rate Derivatives using valuations based on the initial trade prices. Using an income-based approach, subsequent valuations are based on observable inputs to the valuation model including interest rate curves, risk adjusted discount rates, credit spreads and other relevant data.

The fair value of our Physical Liquefaction Supply Derivatives is predominantly driven by market commodity basis prices and our assessment of the associated conditions precedent, including evaluating whether the respective market is available as pipeline infrastructure is developed. Upon the completion and placement into service of relevant pipeline infrastructure to accommodate marketable physical gas flow, we recognize a gain or loss based on the fair value of the respective natural gas supply contracts as of the reporting date.

The fair value of substantially all of our Physical Liquefaction Supply Derivatives is developed through the use of internal models which are impacted by inputs that are unobservable in the marketplace. As a result, the fair value of our Physical Liquefaction Supply Derivatives is designated as Level 3 within the valuation hierarchy. The curves used to generate the fair value of our Physical Liquefaction Supply Derivatives are based on basis adjustments applied to forward curves for a liquid trading point. In addition, there may be observable liquid market basis information in the near term, but terms of a particular Physical Liquefaction Supply Derivatives contract may exceed the period for which such information is available, resulting in a Level 3 classification. In these instances, the fair value of the contract incorporates extrapolation assumptions made in the determination of the market basis price for future delivery periods in which applicable commodity basis prices were either not observable or lacked corroborative market data. Internal fair value models include conditions precedent to the respective long-term natural gas supply contracts. As of March 31, 2017 and December 31, 2016, some of our Physical Liquefaction Supply Derivatives existed within markets for which the pipeline infrastructure is under development to accommodate marketable physical gas flow.

The following table includes quantitative information for the unobservable inputs for our Level 3 Physical Liquefaction Supply Derivatives as of March 31, 2017:

Net Fair Value Asset (in millions) | Valuation Technique | Significant Unobservable Input | Significant Unobservable Inputs Range | |||||

Physical Liquefaction Supply Derivatives | $41 | Income Approach | Basis Spread | $(0.345) - $0.081 | ||||

10

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The following table (in millions) shows the changes in the fair value of our Level 3 Physical Liquefaction Supply Derivatives during the three months ended March 31, 2017 and 2016:

Three Months Ended March 31, | ||||||||

2017 | 2016 | |||||||

Balance, beginning of period | $ | 79 | $ | 32 | ||||

Realized and mark-to-market losses: | ||||||||

Included in cost of sales (1) | (41 | ) | (2 | ) | ||||

Purchases and settlements: | ||||||||

Purchases | 4 | — | ||||||

Settlements (1) | (1 | ) | — | |||||

Balance, end of period | $ | 41 | $ | 30 | ||||

Change in unrealized gains relating to instruments still held at end of period | $ | (41 | ) | $ | (2 | ) | ||

(1) | Does not include the decrease in fair value of $1 million related to the realized gains capitalized during the three months ended March 31, 2016. |

Derivative assets and liabilities arising from our derivative contracts with the same counterparty are reported on a net basis, as all counterparty derivative contracts provide for net settlement. The use of derivative instruments exposes us to counterparty credit risk, or the risk that a counterparty will be unable to meet its commitments in instances when our derivative instruments are in an asset position. Our derivative instruments are subject to contractual provisions which provide for the unconditional right of set-off for all derivative assets and liabilities with a given counterparty in the event of default.

Interest Rate Derivatives

SPL had entered into interest rate swaps (“SPL Interest Rate Derivatives”) to protect against volatility of future cash flows and hedge a portion of the variable interest payments on the credit facilities it entered into in June 2015 (the “2015 SPL Credit Facilities”). In March 2017, SPL settled the SPL Interest Rate Derivatives and recognized a derivative loss of $7 million in conjunction with the termination of approximately $1.6 billion of commitments under the 2015 SPL Credit Facilities, as discussed in Note 10—Debt.

During the three months ended March 31, 2017 there were no changes to the terms of our interest rate swaps (“CQP Interest Rate Derivatives”) entered into to hedge a portion of the variable interest payments on the credit facilities we entered into in February 2016 (the “2016 CQP Credit Facilities”). See Note 8—Derivative Instruments of our Notes to Consolidated Financial Statements in our annual report on Form 10-K for the year ended December 31, 2016 for additional information.

As of March 31, 2017, we had the following Interest Rate Derivatives outstanding:

Initial Notional Amount | Maximum Notional Amount | Effective Date | Maturity Date | Weighted Average Fixed Interest Rate Paid | Variable Interest Rate Received | |||||||

CQP Interest Rate Derivatives | $225 million | $1.3 billion | March 22, 2016 | February 29, 2020 | 1.19% | One-month LIBOR | ||||||

11

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The following table (in millions) shows the fair value and location of our Interest Rate Derivatives on our Consolidated Balance Sheets:

March 31, 2017 | December 31, 2016 | |||||||||||||||||||||||

SPL Interest Rate Derivatives | CQP Interest Rate Derivatives | Total | SPL Interest Rate Derivatives | CQP Interest Rate Derivatives | Total | |||||||||||||||||||

Balance Sheet Location | ||||||||||||||||||||||||

Non-current derivative assets | $ | — | $ | 16 | $ | 16 | $ | — | $ | 16 | $ | 16 | ||||||||||||

Derivative liabilities | — | — | — | (4 | ) | (3 | ) | (7 | ) | |||||||||||||||

Non-current derivative liabilities | — | — | — | (2 | ) | — | (2 | ) | ||||||||||||||||

Total derivative liabilities | — | — | — | (6 | ) | (3 | ) | (9 | ) | |||||||||||||||

Derivative asset (liability), net | $ | — | $ | 16 | $ | 16 | $ | (6 | ) | $ | 13 | $ | 7 | |||||||||||

The following table (in millions) shows the changes in the fair value and settlements of our Interest Rate Derivatives recorded in derivative loss, net on our Consolidated Statements of Operations during the three months ended March 31, 2017 and 2016:

Three Months Ended March 31, | ||||||||

2017 | 2016 | |||||||

SPL Interest Rate Derivatives loss | $ | (2 | ) | $ | (11 | ) | ||

CQP Interest Rate Derivatives gain (loss) | 2 | (10 | ) | |||||

Liquefaction Supply Derivatives

The following table (in millions) shows the fair value and location of our Liquefaction Supply Derivatives on our Consolidated Balance Sheets:

Fair Value Measurements as of (1) | |||||||||

Balance Sheet Location | March 31, 2017 | December 31, 2016 | |||||||

Liquefaction Supply Derivatives | Other current assets | $ | 16 | $ | 13 | ||||

Liquefaction Supply Derivatives | Non-current derivative assets | 28 | 67 | ||||||

Liquefaction Supply Derivatives | Derivative liabilities | (4 | ) | (7 | ) | ||||

Liquefaction Supply Derivatives | Non-current derivative liabilities | (1 | ) | — | |||||

(1) | Does not include collateral of $5 million and $6 million deposited for such contracts, which is included in other current assets in our Consolidated Balance Sheets as of March 31, 2017 and December 31, 2016, respectively. |

SPL had secured up to approximately 2,051 million MMBtu and 1,994 million MMBtu of natural gas feedstock through natural gas supply contracts as of March 31, 2017 and December 31, 2016, respectively. The notional natural gas position of our Liquefaction Supply Derivatives was approximately 1,214 million MMBtu and 1,117 million MMBtu as of March 31, 2017 and December 31, 2016, respectively.

The following table (in millions) shows the changes in the fair value, settlements and location of our Liquefaction Supply Derivatives recorded on our Consolidated Statements of Operations during the three months ended March 31, 2017 and 2016:

Three Months Ended March 31, | |||||||||

Statement of Operations Location (1) | 2017 | 2016 | |||||||

Liquefaction Supply Derivatives loss (2) | Cost of sales | $ | 39 | $ | 4 | ||||

(1) | Fair value fluctuations associated with commodity derivative activities are classified and presented consistently with the item economically hedged and the nature and intent of the derivative instrument. |

(2) | Does not include the realized value associated with derivative instruments that settle through physical delivery. |

12

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Balance Sheet Presentation

Our derivative instruments are presented on a net basis on our Consolidated Balance Sheets as described above. The following table (in millions) shows the fair value of our derivatives outstanding on a gross and net basis:

Gross Amounts Recognized | Gross Amounts Offset in the Consolidated Balance Sheets | Net Amounts Presented in the Consolidated Balance Sheets | ||||||||||

Offsetting Derivative Assets (Liabilities) | ||||||||||||

As of March 31, 2017 | ||||||||||||

CQP Interest Rate Derivatives | $ | 17 | $ | (1 | ) | $ | 16 | |||||

Liquefaction Supply Derivatives | 48 | (4 | ) | 44 | ||||||||

Liquefaction Supply Derivatives | 2 | (7 | ) | (5 | ) | |||||||

As of December 31, 2016 | ||||||||||||

SPL Interest Rate Derivatives | $ | (6 | ) | $ | — | $ | (6 | ) | ||||

CQP Interest Rate Derivatives | 16 | — | 16 | |||||||||

CQP Interest Rate Derivatives | (3 | ) | — | (3 | ) | |||||||

Liquefaction Supply Derivatives | 82 | (2 | ) | 80 | ||||||||

Liquefaction Supply Derivatives | (11 | ) | 4 | (7 | ) | |||||||

NOTE 8—OTHER NON-CURRENT ASSETS

As of March 31, 2017 and December 31, 2016, other non-current assets consisted of the following (in millions):

March 31, | December 31, | |||||||

2017 | 2016 | |||||||

Advances made under EPC and non-EPC contracts | $ | 20 | $ | 23 | ||||

Advances made to municipalities for water system enhancements | 95 | 95 | ||||||

Advances and other asset conveyances to third parties to support LNG terminals | 30 | 31 | ||||||

Tax-related payments and receivables | 25 | 28 | ||||||

Information technology service assets | 26 | 27 | ||||||

Other | 9 | 18 | ||||||

Total other non-current assets, net | $ | 205 | $ | 222 | ||||

NOTE 9—ACCRUED LIABILITIES

As of March 31, 2017 and December 31, 2016, accrued liabilities consisted of the following (in millions):

March 31, | December 31, | |||||||

2017 | 2016 | |||||||

Interest costs and related debt fees | $ | 147 | $ | 205 | ||||

Sabine Pass LNG terminal and related pipeline costs | 275 | 211 | ||||||

Other accrued liabilities | 4 | 2 | ||||||

Total accrued liabilities | $ | 426 | $ | 418 | ||||

13

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 10—DEBT

As of March 31, 2017 and December 31, 2016, our debt consisted of the following (in millions):

March 31, | December 31, | |||||||

2017 | 2016 | |||||||

Long-term debt: | ||||||||

SPL | ||||||||

5.625% Senior Secured Notes due 2021 (“2021 SPL Senior Notes”), net of unamortized premium of $7 and $7 | $ | 2,007 | $ | 2,007 | ||||

6.25% Senior Secured Notes due 2022 (“2022 SPL Senior Notes”) | 1,000 | 1,000 | ||||||

5.625% Senior Secured Notes due 2023 (“2023 SPL Senior Notes”), net of unamortized premium of $5 and $6 | 1,505 | 1,506 | ||||||

5.75% Senior Secured Notes due 2024 (“2024 SPL Senior Notes”) | 2,000 | 2,000 | ||||||

5.625% Senior Secured Notes due 2025 (“2025 SPL Senior Notes”) | 2,000 | 2,000 | ||||||

5.875% Senior Secured Notes due 2026 (“2026 SPL Senior Notes”) | 1,500 | 1,500 | ||||||

5.00% Senior Secured Notes due 2027 (“2027 SPL Senior Notes”) | 1,500 | 1,500 | ||||||

4.200% Senior Secured Notes due 2028 (“2028 SPL Senior Notes”), net of unamortized discount of $1 and zero | 1,349 | — | ||||||

5.00% Senior Secured Notes due 2037 (“2037 SPL Senior Notes”) | 800 | — | ||||||

2015 SPL Credit Facilities | — | 314 | ||||||

Cheniere Partners | ||||||||

2016 CQP Credit Facilities | 2,560 | 2,560 | ||||||

Unamortized debt issuance costs | (201 | ) | (178 | ) | ||||

Total long-term debt, net | 16,020 | 14,209 | ||||||

Current debt: | ||||||||

$1.2 billion SPL Working Capital Facility (“SPL Working Capital Facility”) | — | 224 | ||||||

Total debt, net | $ | 16,020 | $ | 14,433 | ||||

2017 Debt Issuances and Redemptions

Senior Notes

In February 2017, SPL issued an aggregate principal amount of $800 million of the 2037 SPL Senior Notes on a private placement basis in reliance on the exemption from registration provided for under Section 4(a)(2) of the Securities Act of 1933, as amended. In March 2017, SPL issued an aggregate principal amount of $1.35 billion, before discount, of the 2028 SPL Senior Notes. Net proceeds of the offerings of the 2037 SPL Senior Notes and the 2028 SPL Senior Notes were $789 million and $1.33 billion, respectively, after deducting the initial purchasers’ commissions (for the 2028 SPL Senior Notes) and estimated fees and expenses. The net proceeds of the 2037 SPL Senior Notes were used to repay the then outstanding borrowings of $369 million under the 2015 SPL Credit Facilities and, along with the net proceeds of the 2028 SPL Senior Notes, the remainder is being used to pay a portion of the capital costs in connection with the construction of Trains 1 through 5 of the Liquefaction Project in lieu of the terminated portion of the commitments under the 2015 SPL Credit Facilities.

In connection with the issuance of the 2037 SPL Senior Notes and the 2028 SPL Senior Notes, SPL terminated the remaining available balance of $1.6 billion under the 2015 SPL Credit Facilities, resulting in a write-off of debt issuance costs associated with the 2015 SPL Credit Facilities of $42 million during the three months ended March 31, 2017.

The 2037 SPL Senior Notes and the 2028 SPL Senior Notes accrue interest at fixed rates of 5.00% and 4.200%, respectively, and interest is payable semi-annually in arrears. The terms of the 2037 SPL Senior Notes are governed by an indenture which contains customary terms and events of default and certain covenants that, among other things, limit SPL’s ability and the ability of SPL’s restricted subsidiaries to incur additional indebtedness or issue preferred stock, make certain investments or pay dividends or distributions on capital stock or subordinated indebtedness or purchase, redeem or retire capital stock, sell or transfer assets, including capital stock of SPL’s restricted subsidiaries, restrict dividends or other payments by restricted subsidiaries, incur liens, enter into transactions with affiliates, dissolve, liquidate, consolidate, merge, sell or lease all or substantially all of SPL’s assets

14

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

and enter into certain LNG sales contracts. The 2028 SPL Senior Notes are governed by the same common indenture as the other senior notes, which also contains customary terms and events of default, covenants and redemption terms.

At any time prior to six months before the respective dates of maturity of the 2037 SPL Senior Notes and the 2028 SPL Senior Notes, SPL may redeem all or part of such notes at a redemption price equal to the “optional redemption” price for the 2037 SPL Senior Notes or the “make-whole” price for the 2028 SPL Senior Notes, as set forth in the respective indentures governing the notes, plus accrued and unpaid interest, if any, to the date of redemption. SPL may also, at any time within six months of the respective maturity dates for the 2037 SPL Senior Notes and the 2028 SPL Senior Notes, redeem all or part of such notes at a redemption price equal to 100% of the principal amount of such notes to be redeemed, plus accrued and unpaid interest, if any, to the date of redemption.

In connection with the issuance of the 2028 SPL Senior Notes, SPL entered into a registration rights agreement (the “SPL Registration Rights Agreement”). Under the terms of the SPL Registration Rights Agreement, SPL has agreed, and any future guarantors will agree, to use commercially reasonable efforts to file with the SEC and cause to become effective a registration statement relating to an offer to exchange any and all of the 2028 SPL Senior Notes for a like aggregate principal amount of debt securities of SPL with terms identical in all material respects to the 2028 SPL Senior Notes sought to be exchanged (other than with respect to restrictions on transfer or to any increase in annual interest rate), within 360 days after March 6, 2017. Under specified circumstances, SPL has also agreed, and any future guarantors will also agree, to use commercially reasonable efforts to cause to become effective a shelf registration statement relating to resales of the 2028 SPL Senior Notes. SPL will be obligated to pay additional interest on the 2028 SPL Senior Notes if it fails to comply with its obligation to register them within the specified time period.

Credit Facilities

Below is a summary (in millions) of our credit facilities outstanding as of March 31, 2017:

SPL Working Capital Facility | 2016 CQP Credit Facilities | |||||||

Original facility size | $ | 1,200 | $ | 2,800 | ||||

Outstanding balance | — | 2,560 | ||||||

Letters of credit issued | 377 | 50 | ||||||

Available commitment | $ | 823 | $ | 190 | ||||

Interest rate | LIBOR plus 1.75% or base rate plus 0.75% | LIBOR plus 2.25% or base rate plus 1.25% (1) | ||||||

Maturity date | December 31, 2020, with various terms for underlying loans | February 25, 2020, with principals due quarterly commencing on February 19, 2019 | ||||||

(1) | There is a 0.50% step-up for both LIBOR and base rate loans beginning on February 25, 2019. |

Interest Expense

Total interest expense consisted of the following (in millions):

Three Months Ended March 31, | ||||||||

2017 | 2016 | |||||||

Total interest cost | $ | 211 | $ | 192 | ||||

Capitalized interest | (81 | ) | (149 | ) | ||||

Total interest expense, net | $ | 130 | $ | 43 | ||||

15

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Fair Value Disclosures

The following table (in millions) shows the carrying amount and estimated fair value of our debt:

March 31, 2017 | December 31, 2016 | |||||||||||||||

Carrying Amount | Estimated Fair Value | Carrying Amount | Estimated Fair Value | |||||||||||||

Senior notes, net of premium or discount (1) | $ | 12,861 | $ | 13,807 | $ | 11,513 | $ | 12,309 | ||||||||

2037 SPL Senior Notes (2) | 800 | 826 | — | — | ||||||||||||

Credit facilities (3) | 2,560 | 2,560 | 3,098 | 3,098 | ||||||||||||

(1) | Includes 2021 SPL Senior Notes, 2022 SPL Senior Notes, 2023 SPL Senior Notes, 2024 SPL Senior Notes, 2025 SPL Senior Notes, 2026 SPL Senior Notes, 2027 SPL Senior Notes and 2028 SPL Senior Notes. The Level 2 estimated fair value was based on quotes obtained from broker-dealers or market makers of these senior notes and other similar instruments. |

(2) | The Level 3 estimated fair value was calculated based on inputs that are observable in the market or that could be derived from, or corroborated with, observable market data, including our stock price and interest rates based on debt issued by parties with comparable credit ratings to us and inputs that are not observable in the market. |

(3) | Includes 2015 SPL Credit Facilities, SPL Working Capital Facility and 2016 CQP Credit Facilities. The Level 3 estimated fair value approximates the principal amount because the interest rates are variable and reflective of market rates and the debt may be repaid, in full or in part, at any time without penalty. |

NOTE 11—RELATED PARTY TRANSACTIONS

Below is a summary (in millions) of our related party transactions as reported on our Consolidated Statements of Operations for the three months ended March 31, 2017 and 2016:

Three Months Ended March 31, | ||||||||

2017 | 2016 | |||||||

LNG revenues—affiliate | ||||||||

Cheniere Marketing SPA and Cheniere Marketing Master SPA | $ | 331 | $ | — | ||||

Regasification revenues—affiliate | ||||||||

Contracts for Sale and Purchase of Natural Gas and LNG | — | 1 | ||||||

Tug Boat Lease Sharing Agreement | 1 | 1 | ||||||

Total regasification revenues—affiliate | 1 | 2 | ||||||

Operating and maintenance expense—affiliate | ||||||||

Contracts for Sale and Purchase of Natural Gas and LNG | — | 1 | ||||||

Services Agreements | 18 | 10 | ||||||

Total operating and maintenance expense—affiliate | 18 | 11 | ||||||

General and administrative expense—affiliate | ||||||||

Services Agreements | 22 | 22 | ||||||

LNG Terminal Capacity Agreements

Terminal Use Agreements

SPL obtained approximately 2.0 Bcf/d of regasification capacity under a TUA with SPLNG as a result of an assignment in July 2012 by Cheniere Investments of its rights, title and interest under its TUA with SPLNG. SPL is obligated to make monthly capacity payments to SPLNG aggregating approximately $250 million per year (the “TUA Fees”), continuing until at least 20 years after SPL delivers its first commercial cargo at the Liquefaction Project.

16

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

In connection with this TUA, SPL is required to pay for a portion of the cost (primarily LNG inventory) to maintain the cryogenic readiness of the regasification facilities at the Sabine Pass LNG terminal, which is recorded as operating and maintenance expense on our Consolidated Statements of Operations.

Cheniere Investments, SPL and SPLNG entered into the terminal use rights assignment and agreement (the “TURA”) pursuant to which Cheniere Investments has the right to use SPL’s reserved capacity under the TUA and has the obligation to pay the TUA Fees required by the TUA to SPLNG. However, the revenue earned by SPLNG from the TUA Fees and the loss incurred by Cheniere Investments under the TURA are eliminated upon consolidation of our Financial Statements. We have guaranteed the obligations of SPL under its TUA and the obligations of Cheniere Investments under the TURA.

In an effort to utilize Cheniere Investments’ reserved capacity under the TURA during construction of the Liquefaction Project, Cheniere Marketing has entered into an amended and restated variable capacity rights agreement with Cheniere Investments (the “Amended and Restated VCRA”) pursuant to which Cheniere Marketing is obligated to pay Cheniere Investments 80% of the expected gross margin of each cargo of LNG that Cheniere Marketing arranges for delivery to the Sabine Pass LNG terminal. Cheniere Investments recorded no revenues—affiliate from Cheniere Marketing during the three months ended March 31, 2017 and 2016, respectively, related to the Amended and Restated VCRA.

Cheniere Marketing SPA

Cheniere Marketing has entered into an SPA with SPL to purchase, at Cheniere Marketing’s option, any LNG produced by SPL in excess of that required for other customers at a price of 115% of Henry Hub plus $3.00 per MMBtu of LNG.

Cheniere Marketing Master SPA

SPL has entered into an agreement with Cheniere Marketing that allows the parties to sell and purchase LNG with each other by executing and delivering confirmations under this agreement.

Commissioning Confirmation

Under the Cheniere Marketing Master SPA, SPL has executed a confirmation with Cheniere Marketing that obligates Cheniere Marketing in certain circumstances to buy LNG cargoes produced during the periods while Bechtel Oil, Gas and Chemicals, Inc. has control of, and is commissioning, the first four Trains of the Liquefaction Project.

Pre-commercial LNG Marketing Agreement

SPL has entered into an agreement with Cheniere Marketing that authorizes Cheniere Marketing to act on SPL’s behalf to market and sell certain quantities of pre-commercial LNG that has not been accepted by BG Gulf Coast LNG, LLC, one of SPL’s SPA customers. SPL pays a fee to Cheniere Marketing for marketing and transportation, which is based on volume sold under this agreement.

Services Agreements

As of March 31, 2017 and December 31, 2016, we had $64 million and $38 million of advances to affiliates, respectively, under the services agreements described below. The non-reimbursement amounts incurred under the services agreements described below are recorded in general and administrative expense—affiliate.

Cheniere Partners Services Agreement

We have entered into a services agreement with Cheniere Terminals, a wholly owned subsidiary of Cheniere, pursuant to which Cheniere Terminals is entitled to a quarterly non-accountable overhead reimbursement charge of $3 million (adjusted for inflation) for the provision of various general and administrative services for our benefit. In addition, Cheniere Terminals is entitled to reimbursement for all audit, tax, legal and finance fees incurred by Cheniere Terminals that are necessary to perform the services under the agreement.

17

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Cheniere Investments Information Technology Services Agreement

Cheniere Investments has entered into an information technology services agreement with Cheniere, pursuant to which Cheniere Investments’ subsidiaries receive certain information technology services. On a quarterly basis, the various entities receiving the benefit are invoiced by Cheniere according to the cost allocation percentages set forth in the agreement. In addition, Cheniere is entitled to reimbursement for all costs incurred by Cheniere that are necessary to perform the services under the agreement.

SPLNG O&M Agreement

SPLNG has entered into a long-term operation and maintenance agreement (the “SPLNG O&M Agreement”) with Cheniere Investments pursuant to which SPLNG receives all necessary services required to operate and maintain the Sabine Pass LNG receiving terminal. SPLNG pays a fixed monthly fee of $130,000 (indexed for inflation) under the SPLNG O&M Agreement and the cost of a bonus equal to 50% of the salary component of labor costs in certain circumstances to be agreed upon between SPLNG and Cheniere Investments at the beginning of each operating year. In addition, SPLNG is required to reimburse Cheniere Investments for its operating expenses, which consist primarily of labor expenses. Cheniere Investments provides the services required under the SPLNG O&M Agreement pursuant to a secondment agreement with a wholly owned subsidiary of Cheniere. All payments received by Cheniere Investments under the SPLNG O&M Agreement are required to be remitted to such subsidiary.

SPLNG MSA

SPLNG has entered into a long-term management services agreement (the “SPLNG MSA”) with Cheniere Terminals, pursuant to which Cheniere Terminals manages the operation of the Sabine Pass LNG receiving terminal, excluding those matters provided for under the SPLNG O&M Agreement. SPLNG pays a monthly fixed fee of $520,000 (indexed for inflation) under the SPLNG MSA.

SPL O&M Agreement

SPL has entered into an operation and maintenance agreement (the “SPL O&M Agreement”) with Cheniere Investments pursuant to which SPL receives all of the necessary services required to construct, operate and maintain the Liquefaction Project. Before the Liquefaction Project is operational, the services to be provided include, among other services, obtaining governmental approvals on behalf of SPL, preparing an operating plan for certain periods, obtaining insurance, preparing staffing plans and preparing status reports. After the Liquefaction Project is operational, the services include all necessary services required to operate and maintain the Liquefaction Project. Before the Liquefaction Project is operational, in addition to reimbursement of operating expenses, SPL is required to pay a monthly fee equal to 0.6% of the capital expenditures incurred in the previous month. After substantial completion of each Train, for services performed while the Liquefaction Project is operational, SPL will pay, in addition to the reimbursement of operating expenses, a fixed monthly fee of $83,333 (indexed for inflation) for services with respect to such Train. Cheniere Investments provides the services required under the SPL O&M Agreement pursuant to a secondment agreement with a wholly owned subsidiary of Cheniere. All payments received by Cheniere Investments under the SPL O&M Agreement are required to be remitted to such subsidiary.

SPL MSA

SPL has entered into a management services agreement (the “SPL MSA”) with Cheniere Terminals pursuant to which Cheniere Terminals manages the construction and operation of the Liquefaction Project, excluding those matters provided for under the SPL O&M Agreement. The services include, among other services, exercising the day-to-day management of SPL’s affairs and business, managing SPL’s regulatory matters, managing bank and brokerage accounts and financial books and records of SPL’s business and operations, entering into financial derivatives on SPL’s behalf and providing contract administration services for all contracts associated with the Liquefaction Project. Under the SPL MSA, SPL pays a monthly fee equal to 2.4% of the capital expenditures incurred in the previous month. After substantial completion of each Train, SPL will pay a fixed monthly fee of $541,667 (indexed for inflation) for services with respect to such Train.

18

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

CTPL O&M Agreement

CTPL has entered into an amended long-term operation and maintenance agreement (the “CTPL O&M Agreement”) with Cheniere Investments pursuant to which CTPL receives all necessary services required to operate and maintain the Creole Trail Pipeline. CTPL is required to reimburse the counterparty for its operating expenses, which consist primarily of labor expenses. Cheniere Investments provides the services required under the CTPL O&M Agreement pursuant to a secondment agreement with a wholly owned subsidiary of Cheniere. All payments received by Cheniere Investments under the CTPL O&M Agreement are required to be remitted to such subsidiary.

CTPL MSA

CTPL has entered into a management services agreement (the “CTPL MSA”) with Cheniere Terminals pursuant to which Cheniere Terminals manages the modification and operation of the Creole Trail Pipeline, excluding those matters provided for under the CTPL O&M Agreement. The services include, among other services, exercising the day-to-day management of CTPL’s affairs and business, managing CTPL’s regulatory matters, managing bank and brokerage accounts and financial books and records of CTPL’s business and operations and providing contract administration services for all contracts associated with the pipeline facilities. Under the CTPL MSA, CTPL pays a monthly fee equal to 3.0% of the capital expenditures to enable bi-directional natural gas flow on the Creole Trail Pipeline incurred in the previous month.

Agreement to Fund SPLNG’s Cooperative Endeavor Agreements (“CEAs”)

SPLNG has executed CEAs with various Cameron Parish, Louisiana taxing authorities that allowed them to collect certain annual property tax payments from SPLNG from 2007 through 2016. This ten-year initiative represented an aggregate commitment of $25 million in order to aid in their reconstruction efforts following Hurricane Rita, which SPLNG fulfilled in the first quarter of 2016. In exchange for SPLNG’s advance payments of annual ad valorem taxes, Cameron Parish will grant SPLNG a dollar-for-dollar credit against future ad valorem taxes to be levied against the Sabine Pass LNG terminal starting in 2019. Beginning in September 2007, SPLNG entered into various agreements with Cheniere Marketing, pursuant to which Cheniere Marketing would pay SPLNG additional TUA revenues equal to any and all amounts payable by SPLNG to the Cameron Parish taxing authorities under the CEAs. In exchange for such amounts received as TUA revenues from Cheniere Marketing, SPLNG will make payments to Cheniere Marketing equal to, and in the year the Cameron Parish dollar-for-dollar credit is applied against, ad valorem tax levied on our LNG terminal.

On a consolidated basis, these advance tax payments were recorded to other non-current assets, and payments from Cheniere Marketing that SPLNG utilized to make the ad valorem tax payments were recorded as a long-term obligation. As of both March 31, 2017 and December 31, 2016, we had $25 million of both other non-current assets resulting from SPLNG’s ad valorem tax payments and non-current liabilities—affiliate resulting from these payments received from Cheniere Marketing.

Contracts for Sale and Purchase of Natural Gas and LNG

SPLNG is able to sell and purchase natural gas and LNG under agreements with Cheniere Marketing. Under these agreements, SPLNG purchases natural gas or LNG from Cheniere Marketing at a sales price equal to the actual purchase price paid by Cheniere Marketing to suppliers of the natural gas or LNG, plus any third-party costs incurred by Cheniere Marketing with respect to the receipt, purchase and delivery of natural gas or LNG to the Sabine Pass LNG terminal.

Tug Boat Lease Sharing Agreement

In connection with its tug boat lease, Tug Services entered into a tug sharing agreement with a wholly owned subsidiary of Cheniere to provide its LNG cargo vessels with tug boat and marine services at the Sabine Pass LNG terminal.

LNG Terminal Export Agreement

SPLNG and Cheniere Marketing have entered into an LNG Terminal Export Agreement that provides Cheniere Marketing the ability to export LNG from the Sabine Pass LNG terminal. SPLNG did not record any revenues associated with this agreement during the three months ended March 31, 2017 and 2016.

19

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

State Tax Sharing Agreements

SPLNG has entered into a state tax sharing agreement with Cheniere. Under this agreement, Cheniere has agreed to prepare and file all state and local tax returns which SPLNG and Cheniere are required to file on a combined basis and to timely pay the combined state and local tax liability. If Cheniere, in its sole discretion, demands payment, SPLNG will pay to Cheniere an amount equal to the state and local tax that SPLNG would be required to pay if its state and local tax liability were calculated on a separate company basis. There have been no state and local taxes paid by Cheniere for which Cheniere could have demanded payment from SPLNG under this agreement; therefore, Cheniere has not demanded any such payments from SPLNG. The agreement is effective for tax returns due on or after January 1, 2008.

SPL has entered into a state tax sharing agreement with Cheniere. Under this agreement, Cheniere has agreed to prepare and file all state and local tax returns which SPL and Cheniere are required to file on a combined basis and to timely pay the combined state and local tax liability. If Cheniere, in its sole discretion, demands payment, SPL will pay to Cheniere an amount equal to the state and local tax that SPL would be required to pay if SPL’s state and local tax liability were calculated on a separate company basis. There have been no state and local taxes paid by Cheniere for which Cheniere could have demanded payment from SPL under this agreement; therefore, Cheniere has not demanded any such payments from SPL. The agreement is effective for tax returns due on or after August 2012.

CTPL has entered into a state tax sharing agreement with Cheniere. Under this agreement, Cheniere has agreed to prepare and file all state and local tax returns which CTPL and Cheniere are required to file on a combined basis and to timely pay the combined state and local tax liability. If Cheniere, in its sole discretion, demands payment, CTPL will pay to Cheniere an amount equal to the state and local tax that CTPL would be required to pay if CTPL’s state and local tax liability were calculated on a separate company basis. There have been no state and local taxes paid by Cheniere for which Cheniere could have demanded payment from CTPL under this agreement; therefore, Cheniere has not demanded any such payments from CTPL. The agreement is effective for tax returns due on or after May 2013.

NOTE 12—NET LOSS PER COMMON UNIT

Net loss per common unit for a given period is based on the distributions that will be made to the unitholders with respect to the period plus an allocation of undistributed net loss based on provisions of the partnership agreement, divided by the weighted average number of common units outstanding. Distributions paid by us are presented on the Consolidated Statement of Partners’ Equity. On April 21, 2017, we declared a $0.425 distribution per common unit and the related distribution to our general partner to be paid on May 15, 2017 to unitholders of record as of May 2, 2017 for the period from January 1, 2017 to March 31, 2017.

The two-class method dictates that net income (loss) for a period be reduced by the amount of available cash that will be distributed with respect to that period and that any residual amount representing undistributed net income be allocated to common unitholders and other participating unitholders to the extent that each unit may share in net income as if all of the net income for the period had been distributed in accordance with the partnership agreement. Undistributed income is allocated to participating securities based on the distribution waterfall for available cash specified in the partnership agreement. Undistributed losses (including those resulting from distributions in excess of net income) are allocated to common units and other participating securities on a pro rata basis based on provisions of the partnership agreement. Historical income (loss) attributable to a company that was purchased from an entity under common control is allocated to the predecessor owner in accordance with the terms of the partnership agreement. Distributions are treated as distributed earnings in the computation of earnings per common unit even though cash distributions are not necessarily derived from current or prior period earnings.

The Class B units were issued at a discount to the market price of the common units into which they are convertible. This discount, totaling $2,130 million, represents a beneficial conversion feature and is reflected as an increase in common and subordinated unitholders’ equity and a decrease in Class B unitholders’ equity to reflect the fair value of the Class B units at issuance on our Consolidated Statement of Partners’ Equity. The beneficial conversion feature is considered a dividend that will be distributed ratably with respect to any Class B unit from its issuance date through its conversion date, resulting in an increase in Class B unitholders’ equity and a decrease in common and subordinated unitholders’ equity. We amortize the beneficial conversion feature through the mandatory conversion date of August 2017 for Cheniere Holdings’ and Blackstone CQP Holdco’s Class B units. We are amortizing using the effective yield method with a weighted average effective yield of 888.7% per year and 966.1% per year for Cheniere Holdings’ and Blackstone CQP Holdco’s Class B units, respectively. The impact of the beneficial conversion feature is also included in earnings per unit for the three months ended March 31, 2017 and 2016.

20

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Based on the capital structure as of March 31, 2017, the anticipated impact to the capital accounts in connection with the amortization of the beneficial conversion feature is as follows in 2017 (in millions):

Common Units | Class B Units | Subordinated Units | ||

$(594) | $2,004 | $(1,410) | ||

Under our partnership agreement, the IDRs participate in net income (loss) only to the extent of the amount of cash distributions actually declared, thereby excluding the IDRs from participating in undistributed net income (loss). We did not allocate earnings or losses to IDR holders for the purpose of the two-class method earnings per unit calculation for any of the periods presented. The following table (in millions, except per unit data) provides a reconciliation of net income (loss) and the allocation of net income (loss) to the common units, the subordinated units and the general partner units for purposes of computing net loss per unit.

Limited Partner Units | ||||||||||||||||||||

Total | Common Units | Class B Units | Subordinated Units | General Partner Units | ||||||||||||||||

Three Months Ended March 31, 2017 | ||||||||||||||||||||

Net income | $ | 47 | ||||||||||||||||||

Declared distributions | 25 | 24 | — | — | 1 | |||||||||||||||

Amortization of beneficial conversion feature of Class B units | — | (70 | ) | 235 | (165 | ) | — | |||||||||||||

Assumed allocation of undistributed net income | $ | 22 | — | — | 22 | — | ||||||||||||||

Assumed allocation of net income (loss) | $ | (46 | ) | $ | 235 | $ | (143 | ) | $ | 1 | ||||||||||

Weighted average units outstanding | 57.1 | 145.3 | 135.4 | |||||||||||||||||

Net loss per unit | $ | (0.80 | ) | $ | (1.06 | ) | ||||||||||||||

Three Months Ended March 31, 2016 | ||||||||||||||||||||

Net loss | $ | (75 | ) | |||||||||||||||||

Declared distributions | 25 | 24 | — | — | 1 | |||||||||||||||

Assumed allocation of undistributed net loss | $ | (100 | ) | (29 | ) | — | (69 | ) | (2 | ) | ||||||||||

Assumed allocation of net loss | $ | (5 | ) | $ | — | $ | (69 | ) | $ | (1 | ) | |||||||||

Weighted average units outstanding | 57.1 | 145.3 | 135.4 | |||||||||||||||||

Net loss per unit | $ | (0.08 | ) | $ | (0.51 | ) | ||||||||||||||

NOTE 13—SUPPLEMENTAL CASH FLOW INFORMATION

The following table (in millions) provides supplemental disclosure of cash flow information:

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Cash paid during the period for interest, net of amounts capitalized | $ | 175 | $ | 24 | |||

The balance in property, plant and equipment, net funded with accounts payable and accrued liabilities (including affiliate) was $316 million and $307 million as of March 31, 2017 and 2016, respectively.

21

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 14—RECENT ACCOUNTING STANDARDS

The following table provides a brief description of recent accounting standards that had not been adopted by the Partnership as of March 31, 2017:

Standard | Description | Expected Date of Adoption | Effect on our Consolidated Financial Statements or Other Significant Matters | |||

ASU 2014-09, Revenue from Contracts with Customers (Topic 606), and subsequent amendments thereto | This standard provides a single, comprehensive revenue recognition model which replaces and supersedes most existing revenue recognition guidance and requires an entity to recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The standard requires that the costs to obtain and fulfill contracts with customers should be recognized as assets and amortized to match the pattern of transfer of goods or services to the customer if expected to be recoverable. The standard also requires enhanced disclosures. This guidance may be adopted either retrospectively to each prior reporting period presented subject to allowable practical expedients (“full retrospective approach”) or as a cumulative-effect adjustment as of the date of adoption (“modified retrospective approach”). | January 1, 2018 | We continue to evaluate the effect of this standard on our Consolidated Financial Statements. Preliminarily, we plan to adopt this standard using the full retrospective approach and we do not currently anticipate that the adoption will have a material impact upon our revenues. The Financial Accounting Standards Board has issued and may issue in the future amendments and interpretive guidance which may cause our evaluation to change. Furthermore, we routinely enter into new contracts and we cannot predict with certainty whether the accounting for any future contract under the new standard would result in a significant change from existing guidance. Because this assessment is preliminary and the accounting for revenue recognition is subject to significant judgment, this conclusion could change as we finalize our assessment. We have not yet determined the impact that recognizing fulfillment costs as assets will have on our Consolidated Financial Statements. | |||

ASU 2016-02, Leases (Topic 842) | This standard requires a lessee to recognize leases on its balance sheet by recording a lease liability representing the obligation to make future lease payments and a right-of-use asset representing the right to use the underlying asset for the lease term. A lessee is permitted to make an election not to recognize lease assets and liabilities for leases with a term of 12 months or less. The standard also modifies the definition of a lease and requires expanded disclosures. This guidance may be early adopted, and must be adopted using a modified retrospective approach with certain available practical expedients. | January 1, 2019 | We continue to evaluate the effect of this standard on our Consolidated Financial Statements. Preliminarily, we anticipate a material impact from the requirement to recognize all leases upon our Consolidated Balance Sheets. Because this assessment is preliminary and the accounting for leases is subject to significant judgment, this conclusion could change as we finalize our assessment. We have not yet determined the impact of the adoption of this standard upon our results of operations or cash flows, whether we will elect to early adopt this standard or which, if any, practical expedients we will elect upon transition. | |||

ASU 2016-16, Income Taxes (Topic 740): Intra-Entity Transfers of Assets Other Than Inventory | This standard requires the immediate recognition of the tax consequences of intercompany asset transfers other than inventory. This guidance may be early adopted, but only at the beginning of an annual period, and must be adopted using a modified retrospective approach. | January 1, 2018 | We are currently evaluating the impact of the provisions of this guidance on our Consolidated Financial Statements and related disclosures. | |||

22

CHENIERE ENERGY PARTNERS, L.P. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Additionally, the following table provides a brief description of a recent accounting standard that was adopted by the Partnership during the reporting period:

Standard | Description | Date of Adoption | Effect on our Consolidated Financial Statements or Other Significant Matters | |||

ASU 2015-11, Inventory (Topic 330): Simplifying the Measurement of Inventory | This standard requires inventory to be measured at the lower of cost and net realizable value. Net realizable value is the estimated selling prices in the ordinary course of business, less reasonably predictable costs of completion, disposal and transportation. This guidance may be early adopted and must be adopted prospectively. | January 1, 2017 | The adoption of this guidance did not have a material impact on our Consolidated Financial Statements or related disclosures. | |||

23

ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Information Regarding Forward-Looking Statements

This quarterly report contains certain statements that are, or may be deemed to be, “forward-looking statements.” All statements, other than statements of historical or present facts or conditions, included herein or incorporated herein by reference are “forward-looking statements.” Included among “forward-looking statements” are, among other things:

• | statements regarding our ability to pay distributions to our unitholders; |

• | statements regarding our expected receipt of cash distributions from SPLNG, SPL or CTPL; |

• | statements that we expect to commence or complete construction of our proposed LNG terminals, liquefaction facilities, pipeline facilities or other projects, or any expansions thereof, by certain dates, or at all; |

• | statements regarding future levels of domestic and international natural gas production, supply or consumption or future levels of LNG imports into or exports from North America and other countries worldwide or purchases of natural gas, regardless of the source of such information, or the transportation or other infrastructure or demand for and prices related to natural gas, LNG or other hydrocarbon products; |

• | statements regarding any financing transactions or arrangements, or our ability to enter into such transactions; |

• | statements relating to the construction of our Trains, including statements concerning the engagement of any EPC contractor or other contractor and the anticipated terms and provisions of any agreement with any such EPC or other contractor, and anticipated costs related thereto; |

• | statements regarding any SPA or other agreement to be entered into or performed substantially in the future, including any revenues anticipated to be received and the anticipated timing thereof, and statements regarding the amounts of total LNG regasification, natural gas liquefaction or storage capacities that are, or may become, subject to contracts; |

• | statements regarding counterparties to our commercial contracts, construction contracts and other contracts; |

• | statements regarding our planned development and construction of additional Trains, including the financing of such Trains; |

• | statements that our Trains, when completed, will have certain characteristics, including amounts of liquefaction capacities; |

• | statements regarding our business strategy, our strengths, our business and operation plans or any other plans, forecasts, projections, or objectives, including anticipated revenues, capital expenditures, maintenance and operating costs and cash flows, any or all of which are subject to change; |

• | statements regarding legislative, governmental, regulatory, administrative or other public body actions, approvals, requirements, permits, applications, filings, investigations, proceedings or decisions; and |

• | any other statements that relate to non-historical or future information. |