Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - SPIRIT REALTY CAPITAL, INC. | a2017q1exhibit322906ceocfo.htm |

| EX-32.1 - EXHIBIT 32.1 - SPIRIT REALTY CAPITAL, INC. | a2017q1exhibit321906ceocfo.htm |

| EX-31.4 - EXHIBIT 31.4 - SPIRIT REALTY CAPITAL, INC. | a2017q1exhibit314302cfosrlp.htm |

| EX-31.3 - EXHIBIT 31.3 - SPIRIT REALTY CAPITAL, INC. | a2017q1exhibit313302ceosrlp.htm |

| EX-31.2 - EXHIBIT 31.2 - SPIRIT REALTY CAPITAL, INC. | a2017q1exhibit312302cfosc.htm |

| EX-31.1 - EXHIBIT 31.1 - SPIRIT REALTY CAPITAL, INC. | a2017q1exhibit311302ceosc.htm |

| EX-10.40 - EXHIBIT 10.40 - SPIRIT REALTY CAPITAL, INC. | a2017q1exhibit1040spiritwe.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2017

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-36004

_______________________________________________

SPIRIT REALTY CAPITAL, INC.

SPIRIT REALTY, L.P.

(Exact name of registrant as specified in its charter)

_______________________________________________

Spirit Realty Capital, Inc. | Maryland | 20-1676382 | ||

Spirit Realty, L.P. | Delaware | 20-1127940 | ||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |||

2727 North Harwood Street, Suite 300, Dallas, Texas 75201 | (972) 476-1900 | |||

(Address of principal executive offices; zip code) | (Registrant’s telephone number, including area code) | |||

(Former name, former address and former fiscal year, if changed since last report)

__________________________________________________________________________

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Spirit Realty Capital, Inc. Yes x No o | Spirit Realty, L.P. Yes o No x |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Spirit Realty Capital, Inc. Yes x No o | Spirit Realty, L.P. Yes x No o |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” or an emerging growth company. See definitions of "large accelerated filer,", "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Spirit Realty Capital, Inc.

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o |

Smaller reporting company o | Emerging growth company o |

Spirit Realty, L.P.

Large accelerated filer o | Accelerated filer o | Non-accelerated filer x |

Smaller reporting company o | Emerging growth company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Spirit Realty Capital, Inc. o | Spirit Realty, L.P. o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Spirit Realty Capital, Inc. Yes o No x | Spirit Realty, L.P. Yes o No x |

As of May 2, 2017, there were 484,008,492 shares of common stock, par value $0.01, of Spirit Realty Capital, Inc. outstanding.

Explanatory Note

This report combines the quarterly reports on Form 10-Q for the three months ended March 31, 2017 of Spirit Realty Capital, Inc., a Maryland corporation, and Spirit Realty, L.P., a Delaware limited partnership. Unless otherwise indicated or unless the context requires otherwise, all references in this report to “we,” “us,” “our,” or the “Company” refer to Spirit Realty Capital, Inc. together with its consolidated subsidiaries, including Spirit Realty, L.P. Unless otherwise indicated or unless the context requires otherwise, all references to the “Operating Partnership” refer to Spirit Realty, L.P. together with its consolidated subsidiaries.

Spirit General OP Holdings, LLC ("OP Holdings") is the sole general partner of the Operating Partnership. The Company is a real estate investment trust, or REIT, and the sole member of OP Holdings, as well as the special limited partner of the Operating Partnership. As sole member of the general partner of our Operating Partnership, our Company has the full, exclusive and complete responsibility for our Operating Partnership’s day-to-day management and control.

We believe combining the quarterly reports on Form 10-Q of our Company and Operating Partnership into a single report results in the following benefits:

• | enhancing investors’ understanding of our Company and Operating Partnership by enabling investors to view the business as a whole, reflective of how management views and operates the business; |

• | eliminating duplicative disclosure and providing a streamlined presentation as a substantial portion of the disclosures apply to both our Company and Operating Partnership; and |

• | creating time and cost efficiencies by preparing one combined report in lieu of two separate reports. |

There are a few differences between our Company and Operating Partnership, which are reflected in the disclosures in this report. We believe it is important to understand these differences in the context of how we operate as an interrelated, consolidated company. Our Company is a REIT, the only material assets of which are the partnership interests in our Operating Partnership. As a result, our Company does not conduct business itself, other than acting as the sole member of the general partner of our Operating Partnership, issuing equity from time to time and guaranteeing certain debt of our Operating Partnership. Our Operating Partnership holds substantially all the assets of our Company. Our Company issued convertible notes and guarantees some of the debt of our Operating Partnership, see footnote 4 to the consolidated financial statements included herein for further discussion. Our Operating Partnership conducts the operations of the business and is structured as a partnership with no publicly traded equity. Except for net proceeds from the issuance of convertible notes and equity issuances by our Company, which are generally contributed to our Operating Partnership in exchange for partnership units of our Operating Partnership, our Operating Partnership generates the capital required by our Company’s business through our Operating Partnership’s operations or our Operating Partnership’s incurrence of indebtedness.

The presentation of stockholders’ equity and partners’ capital are the main areas of difference between the consolidated financial statements of our Company and those of our Operating Partnership. The partnership units in our Operating Partnership are accounted for as partners’ capital in our Operating Partnership’s consolidated financial statements. There are no non-controlling interests in the Company or the Operating Partnership.

To help investors understand the significant differences between our Company and our Operating Partnership, this report presents the consolidated financial statements separately for our Company and our Operating Partnership. All other sections of this report, including “Selected Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Quantitative and Qualitative Disclosures About Market Risk,” are presented together for our Company and our Operating Partnership.

In order to establish that the Chief Executive Officer and the Chief Financial Officer of each entity have made the requisite certifications and that our Company and Operating Partnership are compliant with Rule 13a-15 or Rule 15d-15 of the Securities Exchange Act of 1934, or the Exchange Act, and 18 U.S.C. §1350, this report also includes separate “Item 4. Controls and Procedures” sections and separate Exhibit 31 and 32 certifications for each of our Company and our Operating Partnership.

SPIRIT REALTY CAPITAL, INC.

INDEX

Glossary | |

Item 1. Financial Statements (Unaudited) | |

2

GLOSSARY

Definitions: | |

1031 Exchange | Tax-deferred like-kind exchange of properties held for business or investment purposes, pursuant to Section 1031 of the Code |

2015 Credit Facility | $800.0 million unsecured credit facility pursuant to the Credit Agreement |

2019 Notes | $402.5 million convertible notes of the Corporation due in 2019 |

2021 Notes | $345.0 million convertible notes of the Corporation due in 2021 |

AFFO | Adjusted Funds From Operations |

Amended Incentive Award Plan | Amended and Restated Spirit Realty Capital, Inc. and Spirit Realty, L.P. 2012 Incentive Award Plan |

AOCL | Accumulated Other Comprehensive Loss |

ASC | Accounting Standards Codification |

ASU | Accounting Standards Update |

ATM Program | At the Market equity distribution program, pursuant to which the Corporation may offer and sell registered shares of common stock from time to time |

CMBS | Commercial Mortgage Backed Securities |

Code | Internal Revenue Code of 1986, as amended |

Cole II | Cole Credit Property Trust II, Inc. |

Cole II Merger | Acquisition on July 17, 2013 of Cole II by the Company, in which the Company merged with and into the Cole II legal entity |

Collateral Pools | Pools of collateral assets that are pledged to the indenture trustee for the benefit of the noteholders and secure obligations of issuers under the Spirit Master Funding Program |

Company | The Corporation and its consolidated subsidiaries |

Convertible Notes | The 2019 Notes and 2021 Notes, together |

Corporation | Spirit Realty Capital, Inc., a Maryland corporation |

CPI | Consumer Price Index |

Credit Agreement | 2015 credit facility agreement between the Operating Partnership and certain lenders dated March 31, 2015, as amended or otherwise modified from time to time |

EBITDA | Earnings Before Interest, Taxes, Depreciation and Amortization |

Exchange Act | Securities Exchange Act of 1934, as amended |

FASB | Financial Accounting Standards Board |

FFO | Funds From Operations |

Fitch | Fitch Ratings, Inc. |

GAAP | Generally Accepted Accounting Principles in the United States |

LIBOR | London Interbank Offered Rate |

Master Trust 2013 | The net-lease mortgage securitization trust established in December 2013 under the Spirit Master Funding Program |

Master Trust 2014 | The net-lease mortgage securitization trust established in 2005 and amended and restated in 2014 under the Spirit Master Funding Program |

Master Trust Notes | Master Trust 2013 and Master Trust 2014 notes, together |

Master Trust Release | Proceeds from the sale of assets securing the Master Trust Notes held in restricted accounts until a qualifying substitution is made |

Moody's | Moody's Investor Services |

NAREIT | National Association of Real Estate Investment Trusts |

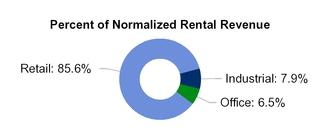

Normalized Rental Revenue | Total rental revenues and earned income from direct financing leases from our owned properties during the final month of the reporting period, adjusted to exclude amounts from properties sold during that period and to include a full month of rental revenues for properties acquired during that period. |

OP Holdings | Spirit General OP Holdings, LLC |

Operating Partnership | Spirit Realty, L.P., a Delaware limited partnership |

3

Definitions: | |

REIT | Real Estate Investment Trust |

S&P | Standard & Poor's Rating Services |

SEC | Securities and Exchange Commission |

Securities Act | Securities Act of 1933, as amended |

Senior Unsecured Notes | $300 million aggregate principal amount of senior notes issued in August 2016 |

Shopko | Specialty Retail Shops Holding Corp. and certain of its affiliates |

Spirit Master Funding Program | The Company's asset-backed securitization program that comprises Master Trust 2013 and Master Trust 2014 |

Term Loan | $420.0 million senior unsecured term facility pursuant to the Term Loan Agreement |

Term Loan Agreement | Term loan agreement between the Operating Partnership and certain lenders dated November 3, 2015, as amended or otherwise modified from time to time |

TSR | Total Shareholder Return |

U.S. | United States |

Unless otherwise indicated or unless the context requires otherwise, all references to "we," "us" or "our" refer to the Corporation and its consolidated subsidiaries, including the Operating Partnership.

4

PART I — FINANCIAL INFORMATION

Item 1. Financial Statements

SPIRIT REALTY CAPITAL, INC.

Consolidated Balance Sheets

(In Thousands, Except Share and Per Share Data)

(Unaudited)

March 31, 2017 | December 31, 2016 | ||||||

Assets | |||||||

Investments: | |||||||

Real estate investments: | |||||||

Land and improvements | $ | 2,665,959 | $ | 2,704,010 | |||

Buildings and improvements | 4,779,465 | 4,775,221 | |||||

Total real estate investments | 7,445,424 | 7,479,231 | |||||

Less: accumulated depreciation | (966,361 | ) | (940,005 | ) | |||

6,479,063 | 6,539,226 | ||||||

Loans receivable, net | 67,880 | 66,578 | |||||

Intangible lease assets, net | 459,799 | 470,276 | |||||

Real estate assets under direct financing leases, net | 27,386 | 36,005 | |||||

Real estate assets held for sale, net | 130,706 | 160,570 | |||||

Net investments | 7,164,834 | 7,272,655 | |||||

Cash and cash equivalents | 9,309 | 10,059 | |||||

Deferred costs and other assets, net | 160,313 | 140,917 | |||||

Goodwill | 254,340 | 254,340 | |||||

Total assets | $ | 7,588,796 | $ | 7,677,971 | |||

Liabilities and stockholders’ equity | |||||||

Liabilities: | |||||||

2015 Credit Facility | $ | 129,000 | $ | 86,000 | |||

Term Loan, net | 418,672 | 418,471 | |||||

Senior Unsecured Notes, net | 295,169 | 295,112 | |||||

Mortgages and notes payable, net | 2,109,117 | 2,162,403 | |||||

Convertible Notes, net | 705,899 | 702,642 | |||||

Total debt, net | 3,657,857 | 3,664,628 | |||||

Intangible lease liabilities, net | 175,261 | 182,320 | |||||

Accounts payable, accrued expenses and other liabilities | 146,836 | 148,915 | |||||

Total liabilities | 3,979,954 | 3,995,863 | |||||

Commitments and contingencies (see Note 7) | |||||||

Stockholders’ equity: | |||||||

Common stock, $0.01 par value, 750,000,000 shares authorized: 484,026,824 and 483,624,120 shares issued and outstanding at March 31, 2017 and December 31, 2016, respectively | 4,840 | 4,836 | |||||

Capital in excess of par value | 5,179,327 | 5,177,086 | |||||

Accumulated deficit | (1,575,325 | ) | (1,499,814 | ) | |||

Accumulated other comprehensive income | — | — | |||||

Total stockholders’ equity | 3,608,842 | 3,682,108 | |||||

Total liabilities and stockholders’ equity | $ | 7,588,796 | $ | 7,677,971 | |||

See accompanying notes.

5

SPIRIT REALTY CAPITAL, INC.

Consolidated Statements of Operations

(In Thousands, Except Share and Per Share Data)

(Unaudited)

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Revenues: | |||||||

Rentals | $ | 159,220 | $ | 161,819 | |||

Interest income on loans receivable | 892 | 1,659 | |||||

Earned income from direct financing leases | 612 | 724 | |||||

Tenant reimbursement income | 3,965 | 3,824 | |||||

Other income | 733 | 331 | |||||

Total revenues | 165,422 | 168,357 | |||||

Expenses: | |||||||

General and administrative | 13,418 | 11,649 | |||||

Restructuring charges | — | 649 | |||||

Property costs | 9,051 | 7,327 | |||||

Real estate acquisition costs | 153 | 57 | |||||

Interest | 46,623 | 53,017 | |||||

Depreciation and amortization | 64,994 | 64,664 | |||||

Impairments | 34,376 | 12,618 | |||||

Total expenses | 168,615 | 149,981 | |||||

(Loss) income before other expense and income tax expense | (3,193 | ) | 18,376 | ||||

Other expense: | |||||||

Loss on debt extinguishment | (30 | ) | (5,341 | ) | |||

Total other expense | (30 | ) | (5,341 | ) | |||

(Loss) income before income tax expense | (3,223 | ) | 13,035 | ||||

Income tax expense | (165 | ) | (81 | ) | |||

(Loss) income before gain on disposition of assets | (3,388 | ) | 12,954 | ||||

Gain on disposition of assets | 16,217 | 10,146 | |||||

Net income attributable to common stockholders | $ | 12,829 | $ | 23,100 | |||

Net income per share attributable to common stockholders—basic | $ | 0.03 | $ | 0.05 | |||

Net income per share attributable to common stockholders—diluted | $ | 0.03 | $ | 0.05 | |||

Weighted average shares of common stock outstanding: | |||||||

Basic | 482,607,198 | 441,365,927 | |||||

Diluted | 482,609,096 | 441,368,407 | |||||

Dividends declared per common share issued | $ | 0.18000 | $ | 0.17500 | |||

See accompanying notes.

6

SPIRIT REALTY CAPITAL, INC.

Consolidated Statements of Comprehensive Income

(In Thousands)

(Unaudited)

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Net income attributable to common stockholders | $ | 12,829 | $ | 23,100 | |||

Other comprehensive income: | |||||||

Change in net unrealized losses on cash flow hedges | — | (856 | ) | ||||

Net cash flow hedge losses reclassified to operations | — | 235 | |||||

Total comprehensive income | $ | 12,829 | $ | 22,479 | |||

See accompanying notes.

7

SPIRIT REALTY CAPITAL, INC.

Consolidated Statement of Stockholders’ Equity

(In Thousands, Except Share Data)

(Unaudited)

Common Stock | ||||||||||||||||||

Shares | Par Value | Capital in Excess of Par Value | Accumulated Deficit | Total Stockholders’ Equity | ||||||||||||||

Balances, December 31, 2016 | 483,624,120 | $ | 4,836 | $ | 5,177,086 | $ | (1,499,814 | ) | $ | 3,682,108 | ||||||||

Net income | — | — | — | 12,829 | 12,829 | |||||||||||||

Dividends declared on common stock | — | — | — | (87,122 | ) | (87,122 | ) | |||||||||||

Tax withholdings related to net stock settlements | (74,882 | ) | (1 | ) | — | (804 | ) | (805 | ) | |||||||||

Stock-based compensation, net | 477,586 | 5 | 2,241 | (414 | ) | 1,832 | ||||||||||||

Balances, March 31, 2017 | 484,026,824 | $ | 4,840 | $ | 5,179,327 | $ | (1,575,325 | ) | $ | 3,608,842 | ||||||||

See accompanying notes.

8

SPIRIT REALTY CAPITAL, INC.

Consolidated Statements of Cash Flows

(In Thousands)

(Unaudited)

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Operating activities | |||||||

Net income attributable to common stockholders | $ | 12,829 | $ | 23,100 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 64,994 | 64,664 | |||||

Impairments | 34,376 | 12,618 | |||||

Amortization of deferred financing costs | 2,401 | 2,166 | |||||

Derivative net settlements, amortization and terminations | — | 30 | |||||

Amortization of debt discounts | 3,061 | 760 | |||||

Stock-based compensation expense | 2,246 | 2,305 | |||||

Loss on debt extinguishment | 30 | 5,341 | |||||

Debt extinguishment costs | (544 | ) | (540 | ) | |||

Gains on dispositions of real estate and other assets, net | (16,217 | ) | (10,146 | ) | |||

Non-cash revenue | (6,390 | ) | (6,587 | ) | |||

Other | 1,337 | (14 | ) | ||||

Changes in operating assets and liabilities: | |||||||

Deferred costs and other assets, net | 534 | 95 | |||||

Accounts payable, accrued expenses and other liabilities | (2,398 | ) | (3,085 | ) | |||

Accrued restructuring charges | — | (1,072 | ) | ||||

Net cash provided by operating activities | 96,259 | 89,635 | |||||

Investing activities | |||||||

Acquisitions of real estate | (135,616 | ) | (72,458 | ) | |||

Capitalized real estate expenditures | (13,312 | ) | (3,552 | ) | |||

Investments in loans receivable | (3,000 | ) | — | ||||

Collections of principal on loans receivable and real estate assets under direct financing leases | 1,151 | 2,151 | |||||

Proceeds from dispositions of real estate and other assets | 134,712 | 89,349 | |||||

Transfers of net sales proceeds from restricted accounts pursuant to 1031 Exchanges | — | 39,867 | |||||

Transfers of net sales proceeds to Master Trust Release | (15,984 | ) | (30,578 | ) | |||

Net cash (used in) provided by investing activities | (32,049 | ) | 24,779 | ||||

9

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Financing activities | |||||||

Borrowings under 2015 Credit Facility | 230,200 | 60,000 | |||||

Repayments under 2015 Credit Facility | (187,200 | ) | (36,000 | ) | |||

Repayments under mortgages and notes payable | (19,335 | ) | (96,732 | ) | |||

Borrowings under Term Loan | — | 45,000 | |||||

Repayments under Term Loan | — | (36,000 | ) | ||||

Deferred financing costs | (51 | ) | (125 | ) | |||

Proceeds from issuance of common stock, net of offering costs | — | 13,923 | |||||

Repurchase of shares of common stock | (804 | ) | (738 | ) | |||

Distributions paid | (87,218 | ) | (77,381 | ) | |||

Transfers (from) to reserve/escrow deposits with lenders | (552 | ) | 841 | ||||

Net cash used in financing activities | (64,960 | ) | (127,212 | ) | |||

Net decrease in cash and cash equivalents | (750 | ) | (12,798 | ) | |||

Cash and cash equivalents, beginning of period | 10,059 | 21,790 | |||||

Cash and cash equivalents, end of period | $ | 9,309 | $ | 8,992 | |||

See accompanying notes.

10

SPIRIT REALTY, L.P.

Consolidated Balance Sheets

(In Thousands, Except Share and Per Share Data)

(Unaudited)

March 31, 2017 | December 31, 2016 | ||||||

Assets | |||||||

Investments: | |||||||

Real estate investments: | |||||||

Land and improvements | $ | 2,665,959 | $ | 2,704,010 | |||

Buildings and improvements | 4,779,465 | 4,775,221 | |||||

Total real estate investments | 7,445,424 | 7,479,231 | |||||

Less: accumulated depreciation | (966,361 | ) | (940,005 | ) | |||

6,479,063 | 6,539,226 | ||||||

Loans receivable, net | 67,880 | 66,578 | |||||

Intangible lease assets, net | 459,799 | 470,276 | |||||

Real estate assets under direct financing leases, net | 27,386 | 36,005 | |||||

Real estate assets held for sale, net | 130,706 | 160,570 | |||||

Net investments | 7,164,834 | 7,272,655 | |||||

Cash and cash equivalents | 9,309 | 10,059 | |||||

Deferred costs and other assets, net | 160,313 | 140,917 | |||||

Goodwill | 254,340 | 254,340 | |||||

Total assets | $ | 7,588,796 | $ | 7,677,971 | |||

Liabilities and partners' capital | |||||||

Liabilities: | |||||||

2015 Credit Facility | $ | 129,000 | $ | 86,000 | |||

Term Loan, net | 418,672 | 418,471 | |||||

Senior Unsecured Notes, net | 295,169 | 295,112 | |||||

Mortgages and notes payable, net | 2,109,117 | 2,162,403 | |||||

Notes payable to Spirit Realty Capital, Inc., net | 705,899 | 702,642 | |||||

Total debt, net | 3,657,857 | 3,664,628 | |||||

Intangible lease liabilities, net | 175,261 | 182,320 | |||||

Accounts payable, accrued expenses and other liabilities | 146,836 | 148,915 | |||||

Total liabilities | 3,979,954 | 3,995,863 | |||||

Commitments and contingencies (see Note 7) | |||||||

Partners' capital: | |||||||

Partnership units | |||||||

General partner's capital: 3,988,218 units issued and outstanding as of both March 31, 2017 and December 31, 2016 | 25,957 | 26,586 | |||||

Limited partners' capital: 480,038,606 and 479,635,902 units issued and outstanding as of March 31, 2017 and December 31, 2016, respectively | 3,582,885 | 3,655,522 | |||||

Total partners' capital | 3,608,842 | 3,682,108 | |||||

Total liabilities and partners' capital | 7,588,796 | 7,677,971 | |||||

See accompanying notes.

11

SPIRIT REALTY, L.P.

Consolidated Statements of Operations

(In Thousands, Except Unit and Per Unit Data)

(Unaudited)

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Revenues: | |||||||

Rentals | $ | 159,220 | $ | 161,819 | |||

Interest income on loans receivable | 892 | 1,659 | |||||

Earned income from direct financing leases | 612 | 724 | |||||

Tenant reimbursement income | 3,965 | 3,824 | |||||

Other income | 733 | 331 | |||||

Total revenues | 165,422 | 168,357 | |||||

Expenses: | |||||||

General and administrative | 13,418 | 11,649 | |||||

Restructuring charges | — | 649 | |||||

Property costs | 9,051 | 7,327 | |||||

Real estate acquisition costs | 153 | 57 | |||||

Interest | 46,623 | 53,017 | |||||

Depreciation and amortization | 64,994 | 64,664 | |||||

Impairments | 34,376 | 12,618 | |||||

Total expenses | 168,615 | 149,981 | |||||

(Loss) income before other expense and income tax expense | (3,193 | ) | 18,376 | ||||

Other expense: | |||||||

Loss on debt extinguishment | (30 | ) | (5,341 | ) | |||

Total other expense | (30 | ) | (5,341 | ) | |||

(Loss) income before income tax expense | (3,223 | ) | 13,035 | ||||

Income tax expense | (165 | ) | (81 | ) | |||

(Loss) income before gain on disposition of assets | (3,388 | ) | 12,954 | ||||

Gain on disposition of assets | 16,217 | 10,146 | |||||

Net income | $ | 12,829 | $ | 23,100 | |||

Net income attributable to the general partner | $ | 109 | $ | 196 | |||

Net income attributable to the limited partners | $ | 12,720 | $ | 22,904 | |||

Net income per partnership unit - basic | $ | 0.03 | $ | 0.05 | |||

Net income per partnership unit - diluted | $ | 0.03 | $ | 0.05 | |||

Weighted average partnership units outstanding: | |||||||

Basic | 482,607,198 | 441,365,927 | |||||

Diluted | 482,609,096 | 441,368,407 | |||||

Distributions declared per partnership unit issued | $ | 0.1800 | $ | 0.1750 | |||

See accompanying notes.

12

SPIRIT REALTY, L.P.

Consolidated Statements of Comprehensive Income

(In Thousands)

(Unaudited)

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Net income | $ | 12,829 | $ | 23,100 | |||

Other comprehensive income: | |||||||

Change in net unrealized losses on cash flow hedges | — | (856 | ) | ||||

Net cash flow hedge losses reclassified to operations | — | 235 | |||||

Total comprehensive income | $ | 12,829 | $ | 22,479 | |||

See accompanying notes.

13

SPIRIT REALTY, L.P.

Consolidated Statements of Partners' Capital

(In Thousands, Except Unit Data)

(Unaudited)

General Partner's Capital (1) | Limited Partners' Capital (2) | Total Partnership Capital | ||||||||||||||||

Units | Amount | Units | Amount | |||||||||||||||

Balances, December 31, 2016 | 3,988,218 | $ | 26,586 | 479,635,902 | $ | 3,655,522 | $ | 3,682,108 | ||||||||||

Net income | — | 109 | — | 12,720 | 12,829 | |||||||||||||

Partnership distributions declared | — | (738 | ) | — | (86,384 | ) | (87,122 | ) | ||||||||||

Tax withholdings related to net partnership unit settlements | — | — | (74,882 | ) | (805 | ) | (805 | ) | ||||||||||

Stock-based compensation | — | — | 477,586 | 1,832 | 1,832 | |||||||||||||

Balances, March 31, 2017 | 3,988,218 | $ | 25,957 | 480,038,606 | $ | 3,582,885 | $ | 3,608,842 | ||||||||||

(1) Consists of general partnership interests held by OP Holdings.

(2) Consists of limited partnership interests held by the Corporation and Spirit Notes Partner, LLC.

See accompanying notes.

14

SPIRIT REALTY, L.P.

Consolidated Statements of Cash Flows

(In Thousands)

(Unaudited)

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Operating activities | |||||||

Net income attributable to partners | $ | 12,829 | $ | 23,100 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 64,994 | 64,664 | |||||

Impairments | 34,376 | 12,618 | |||||

Amortization of deferred financing costs | 2,401 | 2,166 | |||||

Derivative net settlements, amortization and terminations | — | 30 | |||||

Amortization of debt discounts | 3,061 | 760 | |||||

Stock-based compensation expense | 2,246 | 2,305 | |||||

Loss on debt extinguishment | 30 | 5,341 | |||||

Debt extinguishment costs | (544 | ) | (540 | ) | |||

Gains on dispositions of real estate and other assets, net | (16,217 | ) | (10,146 | ) | |||

Non-cash revenue | (6,390 | ) | (6,587 | ) | |||

Other | 1,337 | (14 | ) | ||||

Changes in operating assets and liabilities: | |||||||

Deferred costs and other assets, net | 534 | 95 | |||||

Accounts payable, accrued expenses and other liabilities | (2,398 | ) | (3,085 | ) | |||

Accrued restructuring charges | — | (1,072 | ) | ||||

Net cash provided by operating activities | 96,259 | 89,635 | |||||

Investing activities | |||||||

Acquisitions of real estate | (135,616 | ) | (72,458 | ) | |||

Capitalized real estate expenditures | (13,312 | ) | (3,552 | ) | |||

Investments in loans receivable | (3,000 | ) | — | ||||

Collections of principal on loans receivable and real estate assets under direct financing leases | 1,151 | 2,151 | |||||

Proceeds from dispositions of real estate and other assets | 134,712 | 89,349 | |||||

Transfers of net sales proceeds from restricted accounts pursuant to 1031 Exchanges | — | 39,867 | |||||

Transfers of net sales proceeds to Master Trust Release | (15,984 | ) | (30,578 | ) | |||

Net cash (used in) provided by investing activities | (32,049 | ) | 24,779 | ||||

15

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Financing activities | |||||||

Borrowings under 2015 Credit Facility | 230,200 | 60,000 | |||||

Repayments under 2015 Credit Facility | (187,200 | ) | (36,000 | ) | |||

Repayments under mortgages and notes payable | (19,335 | ) | (96,732 | ) | |||

Borrowings under Term Loan | — | 45,000 | |||||

Repayments under Term Loan | — | (36,000 | ) | ||||

Deferred financing costs | (51 | ) | (125 | ) | |||

Proceeds from issuance of common stock, net of offering costs | — | 13,923 | |||||

Repurchase of partnership units | (804 | ) | (738 | ) | |||

Distributions paid | (87,218 | ) | (77,381 | ) | |||

Transfers (from) to reserve/escrow deposits with lenders | (552 | ) | 841 | ||||

Net cash used in financing activities | (64,960 | ) | (127,212 | ) | |||

Net decrease in cash and cash equivalents | (750 | ) | (12,798 | ) | |||

Cash and cash equivalents, beginning of period | 10,059 | 21,790 | |||||

Cash and cash equivalents, end of period | $ | 9,309 | $ | 8,992 | |||

See accompanying notes.

16

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements

March 31, 2017

(Unaudited)

Note 1. Organization

Company Organization and Operations

Spirit Realty Capital, Inc. (the "Corporation" or, with its consolidated subsidiaries, the "Company") operates as a self-administered and self-managed REIT that seeks to generate and deliver sustainable and attractive returns for stockholders by investing primarily in and managing a portfolio of single-tenant, operationally essential real estate throughout the U.S. that is generally leased on a long-term, triple-net basis to tenants operating within predominantly retail, but also office and industrial property types. Single tenant, operationally essential real estate generally refers to free-standing, commercial real estate facilities where tenants conduct activities that are essential to the generation of their sales and profits.The Company began operations through a predecessor legal entity in 2003.

The Company’s operations are generally carried out through Spirit Realty, L.P. (the "Operating Partnership") and its subsidiaries. Spirit General OP Holdings, LLC ("OP Holdings"), one of the Corporation's wholly-owned subsidiaries, is the sole general partner and owns approximately 1.0% of the Operating Partnership. The Corporation and a wholly-owned subsidiary are the only limited partners and together own the remaining 99.0% of the Operating Partnership.

Note 2. Summary of Significant Accounting Policies

Basis of Accounting and Principles of Consolidation

The accompanying consolidated financial statements of the Company and the Operating Partnership have been prepared pursuant to the rules and regulations of the SEC. In the opinion of management, the consolidated financial statements include the normal, recurring adjustments necessary for a fair statement of the information required to be set forth therein. The results for interim periods are not necessarily indicative of the results for the entire year. Certain information and note disclosures, normally included in financial statements prepared in accordance with GAAP, have been condensed or omitted from these statements pursuant to SEC rules and regulations and, accordingly, these financial statements should be read in conjunction with the Company’s audited consolidated financial statements as filed with the SEC in its Annual Report on Form 10-K for the year ended December 31, 2016.

The consolidated financial statements include the accounts of the Corporation and its wholly owned subsidiaries. The consolidated financial statements of the Operating Partnership include the accounts of the Operating Partnership and its wholly-owned subsidiaries. All significant intercompany balances and transactions have been eliminated in consolidation.

All expenses incurred by the Company have been allocated to the Operating Partnership in accordance with the Operating Partnership's first amended and restated agreement of limited partnership, which management determined to be a reasonable method of allocation. Therefore, expenses incurred would not be materially different if the Operating Partnership had operated as an unaffiliated entity.

The Company has formed numerous special purpose entities to acquire and hold real estate encumbered by indebtedness (see Note 4). Each special purpose entity is a separate legal entity and is the sole owner of its assets and responsible for its liabilities. The assets of these special purpose entities are not available to pay, or otherwise satisfy obligations to, the creditors of any affiliate or owner of another entity unless the special purpose entities have expressly agreed and are permitted under their governing documents. At March 31, 2017 and December 31, 2016, net assets totaling $2.87 billion and $2.95 billion, respectively, were held, and net liabilities totaling $2.20 billion and $2.26 billion, respectively, were owed by these special purpose entities and are included in the accompanying consolidated balance sheets.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Although management believes its estimates are reasonable, actual results could differ from those estimates.

17

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

Segment Reporting

The Company views its operations as one segment, which consists of net leasing operations. The Company has no other reportable segments.

Allowance for Doubtful Accounts

The Company reviews its rent and other tenant receivables for collectability on a regular basis, taking into consideration changes in factors such as the tenant’s payment history, the financial condition of the tenant, business conditions in the industry in which the tenant operates, and economic conditions in the area in which the tenant operates. In the event that the collectability of a receivable with respect to any tenant is in doubt, a provision for uncollectible amounts will be established or a direct write-off of the specific receivable will be made. The Company provided for reserves for uncollectible amounts totaling $11.3 million and $6.4 million at March 31, 2017 and December 31, 2016, respectively, against accounts receivable balances of $28.4 million and $25.3 million, respectively. Receivables are recorded within deferred costs and other assets, net in the accompanying consolidated balance sheets. Receivables are written off against the reserves for uncollectible amounts when all possible means of collection have been exhausted.

For deferred rental revenues related to the straight-line method of reporting rental revenue, the collectability review includes management’s estimates of amounts that will not be realized and an assessment of the risks inherent in the portfolio, giving consideration to historical experience and industry default rates for long-term receivables. The Company established a reserve for losses of $4.9 million at March 31, 2017 and $7.7 million at December 31, 2016, against deferred rental revenue receivables of $73.8 million and $71.1 million, respectively. Deferred rental revenue receivables are recorded within deferred costs and other assets, net in the accompanying consolidated balance sheets.

Restricted Cash and Escrow Deposits

Restricted cash and deposits in escrow, classified within deferred costs and other assets, net in the accompanying consolidated balance sheets consisted of the following (in thousands):

March 31, 2017 | December 31, 2016 | ||||||

Collateral deposits (1) | $ | 1,451 | $ | 1,374 | |||

Tenant improvements, repairs, and leasing commissions (2) | 10,277 | 9,739 | |||||

Master Trust Release (3) | 30,395 | 14,412 | |||||

Loan impounds (4) | 653 | 670 | |||||

Other (5) | 598 | 644 | |||||

$ | 43,374 | $ | 26,839 | ||||

(1) Funds held in reserve by lenders which can be applied at their discretion to the repayment of debt (any funds remaining on deposit after the debt is paid in full are released to the borrower).

(2) Deposits held as additional collateral support by lenders to fund tenant improvements, repairs and leasing commissions incurred to secure a new tenant.

(3) Proceeds from the sale of assets pledged as collateral under the Spirit Master Funding Program, which are held on deposit until a qualifying substitution is made or the funds are applied as prepayment of principal.

(4) Funds held in lender controlled accounts generally used to meet future debt service or certain property operating expenses.

(5) Funds held in lender controlled accounts released after scheduled debt service requirements are met.

Goodwill

Goodwill arises from business combinations and represents the excess of the cost of an acquired entity over the net fair value amounts that were assigned to the identifiable assets acquired and the liabilities assumed. Goodwill is tested for impairment at the reporting unit level on an annual basis and between annual tests if an event occurs or circumstances change that would more likely than not reduce the fair value of the reporting unit below its carrying value.

18

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

Income Taxes

The Company has elected to be taxed as a REIT under the Code. As a REIT, the Company generally will not be subject to federal income tax provided it continues to satisfy certain tests concerning the Company’s sources of income, the nature of its assets, the amounts distributed to its stockholders and the ownership of Company stock. Management believes the Company has qualified and will continue to qualify as a REIT and therefore, no provision has been made for federal income taxes in the accompanying consolidated financial statements. Even if the Company qualifies for taxation as a REIT, it may be subject to state and local income and franchise taxes and to federal income tax and excise tax on its undistributed income.

Franchise taxes are included in general and administrative expenses on the accompanying consolidated statements of operations. Taxable income from non-REIT activities managed through the Company’s taxable REIT subsidiaries are subject to federal, state and local taxes, which are not material.

New Accounting Pronouncements

From time to time, new accounting pronouncements are issued by the FASB or the SEC that are adopted by the Company as of the specified effective date. These new accounting pronouncements entail technical corrections to existing guidance or affect guidance related to specialized industries or entities and therefore will have minimal, if any, impact on the Company's financial position or results of operations upon adoption.

Changes in Accounting Principle

In March 2016, the FASB issued ASU 2016-09, Improvements to Employee Share-Based Payment Accounting, which simplifies many aspects of accounting for share-based payment transactions under ASC Topic 718, Compensation - Stock Compensation, including income tax consequences, classification of awards as either equity or liability, forfeiture rate calculations and classification on the statement of cash flows. The Company adopted this new guidance effective January 1, 2017 and made an accounting policy election to recognize stock-based compensation forfeitures as they occur, whereas previously stock-based compensation forfeitures were estimated and recognized based on historical forfeiture rates. This change in accounting principle has been applied prospectively and the change in accounting principle had no material impact on the financial statements of the Company.

In January 2017, the FASB issued ASU 2017-01, Business Combinations (Topic 805): Clarifying the Definition of a Business, which narrows the definition of a business. The Company early adopted the guidance effective January 1, 2017 and application is on a prospective basis. Under the new guidance, the acquisition of a property with an in-place lease generally will no longer be accounted for as an acquisition of a business, but instead as an asset acquisition, meaning the transaction costs of such an acquisition will now be capitalized instead of expensed. Further, dispositions of properties generally no longer qualify as a disposition of a business and therefore will not generate allocated goodwill when determining gain or loss on sale.

Note 3. Investments

Real Estate Investments

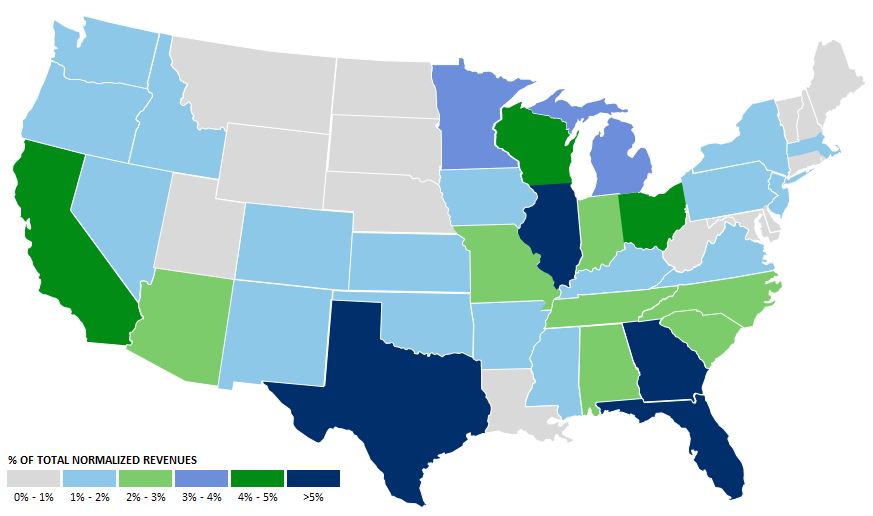

As of March 31, 2017, the Company's gross investment in real estate properties and loans totaled approximately $8.2 billion, representing investments in 2,588 properties, including 74 properties or other related assets securing mortgage loans. The gross investment is comprised of land, buildings, lease intangible assets and lease intangible liabilities, as adjusted for any impairment, and the carrying amount of loans receivable, real estate assets held under direct financing leases and real estate assets held for sale. The portfolio is geographically dispersed throughout 49 states with only one state, Texas, with a real estate investment of 12.6%, accounting for more than 10% of the total dollar amount of the Company’s real estate investment portfolio.

19

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

During the three months ended March 31, 2017, the Company had the following real estate and loan activity, net of accumulated depreciation and amortization:

Number of Properties | Dollar Amount of Investments | |||||||||||||||||||

Owned | Financed | Total | Owned | Financed | Total | |||||||||||||||

(In Thousands) | ||||||||||||||||||||

Gross balance, December 31, 2016 | 2,541 | 74 | 2,615 | $ | 8,181,076 | $ | 66,578 | $ | 8,247,654 | |||||||||||

Acquisitions/improvements (1) | 30 | — | 30 | 148,644 | 3,000 | 151,644 | ||||||||||||||

Dispositions of real estate (2) | (57 | ) | — | (57 | ) | (172,585 | ) | — | (172,585 | ) | ||||||||||

Principal payments and payoffs | — | — | — | — | (1,151 | ) | (1,151 | ) | ||||||||||||

Impairments | — | — | — | (34,376 | ) | — | (34,376 | ) | ||||||||||||

Write-off of gross lease intangibles | — | — | — | (14,467 | ) | — | (14,467 | ) | ||||||||||||

Loan premium amortization and other | — | — | — | (5 | ) | (547 | ) | (552 | ) | |||||||||||

Gross balance, March 31, 2017 | 2,514 | 74 | 2,588 | 8,108,287 | 67,880 | 8,176,167 | ||||||||||||||

Accumulated depreciation and amortization | (1,186,594 | ) | — | (1,186,594 | ) | |||||||||||||||

Net balance, March 31, 2017 | $ | 6,921,693 | $ | 67,880 | $ | 6,989,573 | ||||||||||||||

(1) Includes investments of $12.6 million in revenue producing capitalized expenditures, as well as $0.7 million of non-revenue producing capitalized expenditures as of March 31, 2017.

(2) The total accumulated depreciation and amortization associated with dispositions of real estate was $20.6 million as of March 31, 2017.

Scheduled minimum future contractual rent to be received under the remaining non-cancelable term of the operating leases (including realized rent increases occurring after April 1, 2017) at March 31, 2017 (in thousands):

March 31, 2017 | |||

Remainder of 2017 | $ | 460,417 | |

2018 | 603,955 | ||

2019 | 587,767 | ||

2020 | 569,364 | ||

2021 | 540,081 | ||

Thereafter | 4,127,461 | ||

Total future minimum rentals | $ | 6,889,045 | |

Because lease renewal periods are exercisable at the option of the lessee, the preceding table presents future minimum lease payments due during the initial lease term only. In addition, the future minimum rentals do not include any contingent rentals based on a percentage of the lessees' gross sales or lease escalations based on future changes in the CPI or other stipulated reference rate.

20

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

Loans Receivable

The following table details loans receivable, net of premium and allowance for loan losses (in thousands):

March 31, 2017 | December 31, 2016 | ||||||

Mortgage loans - principal | $ | 54,332 | $ | 55,410 | |||

Mortgage loans - premium, net of amortization | 6,647 | 7,194 | |||||

Mortgages loans, net | 60,979 | 62,604 | |||||

Other note receivables - principal | 7,401 | 4,474 | |||||

Allowance for loan losses | (500 | ) | (500 | ) | |||

Other note receivables | 6,901 | 3,974 | |||||

Total loans receivable, net | $ | 67,880 | $ | 66,578 | |||

The mortgage loans are secured by single-tenant commercial properties and generally have fixed interest rates over the term of the loans. There are four other notes receivable, of which two notes totaling $6.7 million are secured by tenant assets and stock and the remaining two notes are unsecured.

Lease Intangibles, Net

The following table details lease intangible assets and liabilities, net of accumulated amortization (in thousands):

March 31, 2017 | December 31, 2016 | ||||||

In-place leases | $ | 621,372 | $ | 624,723 | |||

Above-market leases | 87,255 | 88,873 | |||||

Less: accumulated amortization | (248,828 | ) | (243,320 | ) | |||

Intangible lease assets, net | $ | 459,799 | $ | 470,276 | |||

Below-market leases | $ | 230,396 | $ | 236,008 | |||

Less: accumulated amortization | (55,135 | ) | (53,688 | ) | |||

Intangible lease liabilities, net | $ | 175,261 | $ | 182,320 | |||

The amounts amortized as a net increase to rental revenue for capitalized above- and below-market leases were $1.8 million and $1.5 million for the three months ended March 31, 2017 and 2016, respectively. The value of in-place leases amortized and included in depreciation and amortization expense was $11.2 million and $11.9 million for the three months ended March 31, 2017 and 2016, respectively.

Real Estate Assets Under Direct Financing Leases

The components of real estate investments held under direct financing leases were as follows (in thousands):

March 31, 2017 | December 31, 2016 | ||||||

Minimum lease payments receivable | $ | 8,837 | $ | 9,456 | |||

Estimated residual value of leased assets | 27,027 | 35,640 | |||||

Unearned income | (8,478 | ) | (9,091 | ) | |||

Real estate assets under direct financing leases, net | $ | 27,386 | $ | 36,005 | |||

21

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

Real Estate Assets Held for Sale

The following table shows the activity in real estate assets held for sale for the three months ended March 31, 2017 (dollars in thousands):

Number of Properties | Carrying Value | |||||

Balance, December 31, 2016 | 44 | $ | 160,570 | |||

Transfers from real estate investments held and used | 27 | 59,015 | ||||

Sales | (12 | ) | (34,619 | ) | ||

Transfers to real estate investments held and used | (6 | ) | (42,644 | ) | ||

Impairments | (11,616 | ) | ||||

Balance, March 31, 2017 | 53 | $ | 130,706 | |||

Impairments

The following table summarizes total impairment losses recognized on the accompanying consolidated statements of operations (in thousands):

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Real estate and intangible asset impairment | $ | 35,220 | $ | 12,630 | |||

Write-off of lease intangibles, net | (844 | ) | 309 | ||||

Loans receivable recovery | — | (324 | ) | ||||

Total impairments from real estate investment net assets | 34,376 | 12,615 | |||||

Other impairment | — | 3 | |||||

Total impairment loss | $ | 34,376 | $ | 12,618 | |||

22

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

Note 4. Debt

The debt of the Company and the Operating Partnership are the same, except for the presentation of the Convertible Notes. The Convertible Notes were issued by the Company. Subsequently, an intercompany note between the Company and the Operating Partnership was executed with terms identical to those of the Convertible Notes. Therefore, in the consolidated balance sheet of the Operating Partnership, the amounts related to the Convertible Notes are reflected as notes payable to Spirit Realty Capital, Inc., net. The Company's debt is summarized below:

Weighted Average Effective Interest Rates (1) | Weighted Average Stated Rates (2) | Weighted Average Maturity (3) | March 31, 2017 | December 31, 2016 | |||||||||||

(in Years) | (In Thousands) | ||||||||||||||

2015 Credit Facility | 4.38 | % | 2.14 | % | 2.0 | $ | 129,000 | $ | 86,000 | ||||||

Term Loan | 2.38 | % | 2.33 | % | 1.6 | 420,000 | 420,000 | ||||||||

Senior Unsecured Notes | 4.69 | % | 4.45 | % | 9.5 | 300,000 | 300,000 | ||||||||

Master Trust Notes | 5.58 | % | 5.03 | % | 6.0 | 1,667,679 | 1,672,706 | ||||||||

CMBS fixed-rate | 5.47 | % | 5.60 | % | 3.9 | 478,687 | 528,427 | ||||||||

Convertible Notes | 5.33 | % | 3.28 | % | 3.0 | 747,500 | 747,500 | ||||||||

Total debt | 5.04 | % | 4.31 | % | 4.8 | 3,742,866 | 3,754,633 | ||||||||

Debt discount, net | (49,923 | ) | (52,894 | ) | |||||||||||

Deferred financing costs, net (4) | (35,086 | ) | (37,111 | ) | |||||||||||

Total debt, net | $ | 3,657,857 | $ | 3,664,628 | |||||||||||

(1) The effective interest rates include amortization of debt discount/premium, amortization of deferred financing costs and credit facility fees, where applicable, calculated for the three months ended March 31, 2017 and based on the average principal balance outstanding during the period.

(2) Represents the weighted average stated interest rate based on the outstanding principal balance as of March 31, 2017.

(3) Represents the weighted average maturity based on the outstanding principal balance as of March 31, 2017.

(4) The Company records deferred financing costs for its 2015 Credit Facility in deferred costs and other assets, net on its consolidated balance sheets.

2015 Credit Facility

On March 31, 2015, the Operating Partnership entered into the Credit Agreement that established a new $600.0 million unsecured credit facility. The 2015 Credit Facility matures on March 31, 2019 (extendable at the Operating Partnership's option to March 31, 2020, subject to satisfaction of certain requirements) and includes an accordion feature to increase the committed facility size up to $1.0 billion, subject to satisfying certain requirements and obtaining additional lender commitments. On April 27, 2016, the Company expanded the borrowing capacity under the 2015 Credit Facility from $600.0 million to $800.0 million by partially exercising the accordion feature under the terms of the Credit Agreement. The 2015 Credit Facility also includes a $50.0 million sub-limit for swing-line loans and up to $60.0 million available for issuances of letters of credit. Swing-line loans and letters of credit reduce availability under the 2015 Credit Facility on a dollar-for-dollar basis. On November 3, 2015, the Company entered into a first amendment to the Credit Agreement. The amendment conforms certain of the terms and covenants to those in the Term Loan Agreement, including limiting the requirement of subsidiary guarantees to material subsidiaries (as defined in the Credit Agreement) meeting certain conditions. At March 31, 2017, there were no subsidiaries meeting this requirement.

Borrowings bear interest at either a specified base rate or LIBOR plus an applicable margin, at the Operating Partnership's option. Per the amendment, the Operating Partnership’s election to change the grid pricing from leverage based to credit rating based pricing initially requires at least two credit ratings of BBB- or better from S&P or Fitch or Baa3 or better from Moody’s. In April 2016, the Corporation received a first time rating of BBB- from Fitch and was upgraded to a BBB- corporate issuer rating by S&P. As a result, the Operating Partnership elected to change the interest rate grid from leverage based pricing to credit rating based pricing in the second quarter of 2016. Under credit rating based pricing, the 2015 Credit Facility bears interest at a rate equal to LIBOR plus 0.875% to 1.55% per annum or a specified base rate plus 0.0% to 0.55% and requires a facility fee in an amount equal to the aggregate revolving credit commitments (whether or not utilized) multiplied by a rate equal to 0.125% to 0.30% per annum, in each case depending

23

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

on the Corporation's credit rating. As of March 31, 2017, the 2015 Credit Facility bore interest at LIBOR plus 1.25% based on the Company's credit rating and incurred a facility fee of 0.25% per annum.

The Operating Partnership may voluntarily prepay the 2015 Credit Facility, in whole or in part, at any time, without premium or penalty, but subject to applicable LIBOR breakage fees, if any. Payment of the 2015 Credit Facility is unconditionally guaranteed by the Corporation and material subsidiaries that meet certain conditions (as defined in the Credit Agreement). The 2015 Credit Facility is full recourse to the Operating Partnership and the aforementioned guarantors.

As a result of entering into the 2015 Credit Facility and expanding the borrowing capacity, the Company incurred costs of $4.8 million. These deferred financing costs are being amortized to interest expense over the remaining initial term of the 2015 Credit Facility. The unamortized deferred financing costs relating to the 2015 Credit Facility were $2.6 million and $2.9 million as of March 31, 2017 and December 31, 2016, respectively, and recorded in deferred costs and other assets, net on the accompanying consolidated balance sheets.

As of March 31, 2017, $129.0 million was outstanding, no letters of credit were issued and $671.0 million of borrowing capacity was available under the 2015 Credit Facility. The Operating Partnership's ability to borrow under the 2015 Credit Facility is subject to ongoing compliance with a number of customary financial covenants and other customary affirmative and negative covenants. As of March 31, 2017, the Corporation and the Operating Partnership were in compliance with these financial covenants.

Term Loan

On November 3, 2015, the Company entered into a Term Loan Agreement among the Operating Partnership, as borrower, the Company as guarantor and the lenders that are parties thereto. The Term Loan Agreement provides for a $325.0 million senior unsecured term facility that has an initial maturity date of November 2, 2018, which may be extended at the Company's option pursuant to two one-year extension options, subject to the satisfaction of certain conditions and payment of an extension fee. In addition, an accordion feature allows the facility to be increased up to $600.0 million, subject to obtaining additional lender commitments. During the fourth quarter of 2015 and 2016, the Company exercised the accordion feature under the Credit Agreement and increased the term facility borrowing capacity from $325.0 million to $370.0 million and $420.0 million, respectively.

The Term Loan Agreement provides that borrowings bear interest at either LIBOR plus 1.35% to 1.80% per annum or a specified base rate plus 0.35% to 0.80% per annum, at the Operating Partnership's option. In each case, the applicable margin is determined based upon the Corporation’s leverage ratio. If the Corporation obtains at least two credit ratings on its senior unsecured long-term indebtedness of BBB- from S&P or Fitch or Baa3 from Moody's, the Operating Partnership may make an irrevocable election to have the margin based upon the Corporation's credit ratings. In April 2016, the Corporation received a first time rating of BBB- from Fitch and was upgraded to a BBB- corporate issuer rating by S&P. As a result, the Operating Partnership elected to change the interest rate grid from leverage based pricing to credit rating based pricing in the second quarter of 2016. Under credit rating based pricing, borrowings bear interest at either LIBOR plus 0.90% to 1.75% per annum or a specified base rate plus 0.0% to 0.75% per annum, in each case depending on the Corporation’s credit ratings. As of March 31, 2017, the Term Loan bore interest at LIBOR plus 1.35% based on the Company's credit rating.

The Operating Partnership may voluntarily prepay the Term Loan, in whole or in part, at any time, without premium or penalty, but subject to applicable LIBOR breakage fees. Borrowings may be repaid without premium or penalty, and may be re-borrowed within 30 days up to the then available loan commitment and subject to occurrence limitations within any twelve-month period. Payment of the Term Loan is unconditionally guaranteed by the Corporation and, under certain circumstances, by one or more material subsidiaries (as defined in the Term Loan Agreement) of the Corporation. The obligations of the Corporation and any guarantor under the Term Loan are full recourse to the Corporation and each guarantor.

As a result of entering into the Term Loan, the Company incurred origination costs of $2.4 million. These deferred financing costs are being amortized to interest expense over the remaining initial term of the Term Loan. As of March 31, 2017 and December 31, 2016, the unamortized deferred financing costs relating to the Term Loan were $1.3 million

24

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

and $1.5 million, respectively, and recorded net against the principal balance of the Term Loan on the accompanying consolidated balance sheets.

As of March 31, 2017, the Term Loan was fully drawn. The Operating Partnership's ability to borrow under the Term Loan is subject to ongoing compliance with a number of customary financial covenants and other customary affirmative and negative covenants. The Corporation has unconditionally guaranteed all obligations of the Operating Partnership under the Term Loan Agreement. As of March 31, 2017, the Corporation and the Operating Partnership were in compliance with these financial covenants.

Senior Unsecured Notes

On August 18, 2016, the Operating Partnership completed a private placement of $300.0 million aggregate principal amount of senior notes, which are guaranteed by the Corporation. The Senior Unsecured Notes were issued at 99.378% of their principal amount, resulting in net proceeds of $296.2 million, after deducting transaction fees and expenses. The Senior Unsecured Notes accrue interest at a rate of 4.45% per year, payable on March 15 and September 15 of each year, until the maturity date of September 15, 2026. The Company has agreed to file with the SEC and cause to become effective a registration statement pursuant to which the Company will offer to exchange the Senior Unsecured Notes for substantially similar registered notes.

The Senior Unsecured Notes are redeemable in whole at any time or in part from time to time, at the Operating Partnership’s option, at a redemption price equal to the sum of: an amount equal to 100% of the principal amount of the Senior Unsecured Notes to be redeemed plus accrued and unpaid interest and liquidated damages, if any, up to, but not including, the redemption date; and a make-whole premium calculated in accordance with the indenture. Notwithstanding the foregoing, if any of the Senior Unsecured Notes are redeemed on or after June 15, 2026 (three months prior to the maturity date of the Senior Unsecured Notes), the redemption price will not include a make-whole premium.

In connection with the offering, the Operating Partnership incurred $3.2 million in deferred financing costs. This amount is being amortized to interest expense over the life of the Senior Unsecured Notes. As of March 31, 2017 and December 31, 2016, the unamortized deferred financing costs relating to the Senior Unsecured Notes were $3.1 million, respectively, and recorded net against the Senior Unsecured Notes principal balance on the accompanying consolidated balance sheets.

In connection with the issuance of the Senior Unsecured Notes, the Corporation and Operating Partnership are subject to ongoing compliance with a number of customary financial covenants and other customary affirmative and negative covenants. As of March 31, 2017, the Corporation and the Operating Partnership were in compliance with these financial covenants.

Master Trust Notes

The Company has access to an asset-backed securitization platform, the Spirit Master Funding Program, to raise capital through the issuance of non-recourse net-lease mortgage notes collateralized by commercial real estate, net-leases and mortgage loans. The Spirit Master Funding Program consists of two separate securitization trusts, Master Trust 2013 and Master Trust 2014, each of which have one or multiple bankruptcy-remote, special purpose entities as issuers or co-issuers of the notes. Each issuer is an indirect wholly-owned special purpose entity of the Corporation.

25

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

The Master Trust Notes are summarized below:

Stated Rates (1) | Maturity | March 31, 2017 | December 31, 2016 | ||||||||||

(in Years) | (in Thousands) | ||||||||||||

Series 2014-1 Class A1 | 5.1 | % | 3.2 | $ | 51,036 | $ | 53,919 | ||||||

Series 2014-1 Class A2 | 5.4 | % | 3.3 | 253,300 | 253,300 | ||||||||

Series 2014-2 | 5.8 | % | 4.0 | 225,404 | 226,283 | ||||||||

Series 2014-3 | 5.7 | % | 5.0 | 311,701 | 311,820 | ||||||||

Series 2014-4 Class A1 | 3.5 | % | 2.8 | 150,000 | 150,000 | ||||||||

Series 2014-4 Class A2 | 4.6 | % | 12.8 | 360,000 | 360,000 | ||||||||

Total Master Trust 2014 notes | 5.1 | % | 6.3 | 1,351,441 | 1,355,322 | ||||||||

Series 2013-1 Class A | 3.9 | % | 1.7 | 125,000 | 125,000 | ||||||||

Series 2013-2 Class A | 5.3 | % | 6.7 | 191,238 | 192,384 | ||||||||

Total Master Trust 2013 notes | 4.7 | % | 4.7 | 316,238 | 317,384 | ||||||||

Total Master Trust notes | 1,667,679 | 1,672,706 | |||||||||||

Debt discount, net | (17,737 | ) | (18,787 | ) | |||||||||

Deferred financing costs, net | (15,607 | ) | (16,376 | ) | |||||||||

Total Master Trust Notes, net | $ | 1,634,335 | $ | 1,637,543 | |||||||||

(1) Represents the individual series stated interest rate as of March 31, 2017 and the weighted average stated rate of the total Master Trust Notes, based on the collective series outstanding principal balances as of March 31, 2017.

As of March 31, 2017, the Master Trust 2014 notes were secured by 847 owned and financed properties issued by five indirect wholly-owned subsidiaries of the Corporation. The notes issued under Master Trust 2014 are cross-collateralized by the assets of all issuers within this trust. As of March 31, 2017, the Master Trust 2013 notes were secured by 304 owned and financed properties issued by a single indirect wholly-owned subsidiary of the Corporation.

CMBS

As of March 31, 2017, indirect wholly-owned special purpose entity subsidiaries of the Corporation were borrowers under 19 fixed-rate non-recourse loans, excluding two loans in default, which have been securitized into CMBS and are secured by the borrowers' respective leased properties and related assets. The stated interest rates of the loans as of March 31, 2017, excluding the defaulted loans, ranged from 3.90% to 6.52% with a weighted average stated interest rate of 5.34%. As of March 31, 2017, these fixed-rate loans were secured by 123 properties. As of March 31, 2017 and December 31, 2016, the unamortized deferred financing costs associated with these fixed-rate loans were $4.5 million and $4.7 million, respectively, and recorded net against the principal balance of the mortgages and notes payable on the accompanying consolidated balance sheets. The deferred financing costs are being amortized to interest expense over the term of the respective loans.

As of March 31, 2017, certain borrowers were in default under the loan agreements relating to two separate CMBS fixed-rate loans, where four properties securing the respective loans were no longer generating sufficient revenue to pay the scheduled debt service. The default interest rate on these loans was between 9.85% and 10.62%. Each defaulted borrower is a bankruptcy remote special purpose entity and the sole owner of the collateral securing the loan obligations. As of March 31, 2017, the aggregate principal balance under the defaulted loans was $27.2 million, which includes $10.1 million of interest capitalized to the principal balance.

26

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

Convertible Notes

In May 2014, the Corporation issued $402.5 million aggregate principal amount of 2.875% convertible notes due in 2019 and $345.0 million aggregate principal amount of 3.75% convertible notes due in 2021. Interest on the Convertible Notes is payable semiannually in arrears on May 15 and November 15 of each year. The 2019 Notes will mature on May 15, 2019 and the 2021 Notes will mature on May 15, 2021.

The Convertible Notes are convertible only during certain periods and, subject to certain circumstances, into cash, shares of the Corporation's common stock, or a combination thereof. The initial conversion rate applicable to each series is 76.3636 per $1,000 principal note (equivalent to an initial conversion price of $13.10 per share of common stock, representing a 22.5% premium above the public offering price of the common stock offered concurrently at the time the Convertible Notes were issued). The conversion rate is subject to adjustment for certain anti-dilution events, including special distributions and regular quarterly cash dividends exceeding $0.16625 per share. As of March 31, 2017, the conversion rate was 76.9167 per $1,000 principal note. Earlier conversion may be triggered if shares of the Corporation's common stock trades higher than the established thresholds, if the Convertible Notes trade below established thresholds, or certain corporate events occur.

In connection with the issuance of the Convertible Notes, the Company recorded a discount of $56.7 million, which represents the estimated value of the embedded conversion feature for each of the Convertible Notes. The discount is being amortized to interest expense using the effective interest method over the term of each of the 2019 Notes and 2021 Notes. As of March 31, 2017 and December 31, 2016, the unamortized discount was $31.0 million and $33.5 million, respectively. The discount is shown net against the aggregate outstanding principal balance of the Convertible Notes on the accompanying consolidated balance sheets. The equity component of the conversion feature is recorded in capital in excess of par value in the accompanying consolidated balance sheets, net of financing transaction costs.

In connection with the offering, the Company also incurred $19.6 million in deferred financing costs. This amount has been allocated on a pro-rata basis to each of the Convertible Notes and is being amortized to interest expense over the term of each note. As of March 31, 2017 and December 31, 2016, the unamortized deferred financing costs relating to the Convertible Notes were $10.6 million and $11.4 million, respectively, and recorded net against the Convertible Notes principal balance on the accompanying consolidated balance sheets.

Debt Extinguishment

During the three months ended March 31, 2017, the Company extinguished a total of $49.2 million aggregate principal amount of senior mortgage indebtedness with a weighted average contractual interest rate of 5.69%. As a result of these transactions, the Company recognized a de minimis net loss. The payment of premium is included in debt extinguishment costs within operating activities in the consolidated statement of cash flows.

During the three months ended March 31, 2016, the Company extinguished a total of $103.8 million aggregate principal amount of senior mortgage indebtedness with a weighted average contractual interest rate of 6.72%. As a result of these transactions, the Company recognized a net loss on debt extinguishment of approximately $5.3 million.

27

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

Debt Maturities

As of March 31, 2017, scheduled debt maturities of the Company’s 2015 Credit Facility, Term Loan, Senior Unsecured Notes, Master Trust Notes, CMBS and Convertible Notes, including balloon payments, are as follows (in thousands):

Scheduled Principal | Balloon Payment | Total | |||||||||

Remainder of 2017 (1) | $ | 19,984 | $ | 139,295 | $ | 159,279 | |||||

2018 (2) | 42,115 | 602,779 | 644,894 | ||||||||

2019 | 44,325 | 541,500 | 585,825 | ||||||||

2020 | 39,096 | 413,206 | 452,302 | ||||||||

2021 | 30,658 | 554,753 | 585,411 | ||||||||

Thereafter | 219,135 | 1,096,020 | 1,315,155 | ||||||||

Total | $ | 395,313 | $ | 3,347,553 | $ | 3,742,866 | |||||

(1) The balloon payment balance in 2017 includes $27.2 million, including $10.1 million of capitalized interest, for the acceleration of principal payable following an event of default under two non-recourse CMBS loans with a stated maturity in 2017.

(2) 2018 includes $420 million unsecured Term Loan that is extendible at borrower's option pursuant to two one-year extension options.

Interest Expense

The following table is a summary of the components of interest expense related to the Company's borrowings (in thousands):

Three Months Ended March 31, | |||||||

2017 | 2016 | ||||||

Interest expense – 2015 Credit Facility (1) | $ | 1,232 | $ | 457 | |||

Interest expense – Term Loan | 2,246 | 1,747 | |||||

Interest expense – Senior Unsecured Notes | 3,338 | — | |||||

Interest expense – mortgages and notes payable | 28,218 | 41,730 | |||||

Interest expense – Convertible Notes (2) | 6,127 | 6,127 | |||||

Non-cash interest expense: | |||||||

Amortization of deferred financing costs | 2,401 | 2,166 | |||||

Amortization of net losses related to interest rate swaps | — | 30 | |||||

Amortization of debt discount, net | 3,061 | 760 | |||||

Total interest expense | $ | 46,623 | $ | 53,017 | |||

(1) Includes facility fees of approximately $0.6 million and $0.4 million for the three months ended March 31, 2017 and 2016, respectively.

(2) Included in interest expense on the Operating Partnership's consolidated statements of operations are amounts paid to the Corporation by the Operating Partnership related to the notes payable to Spirit Realty Capital, Inc.

Note 5. Derivative and Hedging Activities

The Company uses interest rate derivative contracts to manage its exposure to changes in interest rates on its variable rate debt. These derivatives are considered cash flow hedges and are recorded on a gross basis at fair value. Assessments of hedge effectiveness are performed quarterly using regression analysis and the measurement of hedge ineffectiveness is based on the hypothetical derivative method. The effective portion of changes in fair value are recorded in AOCL and subsequently reclassified to earnings when the hedged transactions affect earnings. The ineffective portion is recorded immediately in earnings in general and administrative expenses. The Company does not enter into derivatives contracts for speculative or trading purposes.

The Company is exposed to credit risk in the event of non-performance by its derivative counterparties. The Company evaluates counterparty credit risk through monitoring the creditworthiness of counterparties, which includes review of

28

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

Notes to Consolidated Financial Statements - (continued)

March 31, 2017

(Unaudited)

debt ratings and financial performance. To mitigate its credit risk, the Company enters into agreements with counterparties it considers credit-worthy, such as large financial institutions with favorable credit ratings.

The Company has terminated all existing derivative contracts as of June 30, 2016 and has not entered into any new derivative contracts as of March 31, 2017.

The following tables provide information about the amounts recorded in AOCL, as well as the loss recorded in operations, when reclassified out of AOCL or recognized in earnings immediately, for the three months ended March 31, 2016 (in thousands):

Amount of Gain or (Loss) Recognized in AOCL on Derivative (Effective Portion) | ||||

Derivatives in Cash Flow Hedging Relationships | Three Months Ended March 31, 2016 | |||

Interest rate swaps | $ | (856 | ) | |

Amount of Loss Reclassified from AOCL into Operations (Effective Portion) | ||||

Location of Loss Reclassified from AOCL into Operations | Three Months Ended March 31, 2016 | |||

Interest expense | $ | (235 | ) | |

Amount of Loss Recognized in Operations on Derivative (Ineffective Portion) | ||||

Location of Loss Recognized in Operations on Derivatives | Three Months Ended March 31, 2016 | |||

General and administrative expense | $ | — | ||

Note 6. Stockholders’ Equity and Partners' Capital

Issuance of Common Stock

During the three months ended March 31, 2017, portions of awards of restricted common stock and performance share awards granted to certain of the Company's officers and other employees vested. The vesting of these awards, granted pursuant to the Amended Incentive Award Plan, resulted in federal and state income tax liabilities for the recipients. As permitted by the terms of the Amended Incentive Award Plan and the award grants, certain executive officers and employees elected to surrender 0.1 million shares of common stock valued at $0.8 million, solely to pay the associated statutory tax withholdings during the three months ended March 31, 2017.

ATM Program