Attached files

| file | filename |

|---|---|

| EX-32 - Kaspien Holdings Inc. | c88078_ex32.htm |

| EX-31.2 - Kaspien Holdings Inc. | c88078_ex31-2.htm |

| EX-31.1 - Kaspien Holdings Inc. | c88078_ex31-1.htm |

| EX-23 - Kaspien Holdings Inc. | c88078_ex23.htm |

| EX-21 - Kaspien Holdings Inc. | c88078_ex21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| FOR THE FISCAL YEAR ENDED JANUARY 28, 2017 | |

| OR | |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT FOR THE TRANSITION PERIOD FROM __________ TO __________ |

COMMISSION FILE NUMBER: 0-14818

TRANS WORLD ENTERTAINMENT CORPORATION

(Exact name of registrant as specified in its charter)

| New York | 14-1541629 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

38 Corporate Circle

Albany, New York 12203

(Address of principal executive offices, including zip code)

(518) 452-1242

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common shares, $0.01 par value per share | NASDAQ Stock Market (Common Shares) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in the Rule 405 of the Securities Act.

Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by a check mark whether the Registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s Knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or an amendment to this Form 10-K. x

Indicate by checkmark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company (as defined in Rule 12b-2 of the Act).

| Large accelerated filer o | Accelerated filer x | Non-accelerated filer o | Small reporting company o |

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | Yes o | No x |

As of July 30, 2016, 30,353,214 shares of the Registrant’s Common Stock were issued and outstanding. The aggregate market value of the voting stock held by non-affiliates of the Registrant, based upon the closing sale price of the Registrant’s Common Stock on July 30, 2016 as reported on the Global tier of The NASDAQ Stock Market, Inc. was $55,505,844, Shares of Common Stock held by the Company’s controlling shareholder, who controlled approximately 48.6% of the outstanding Common Stock, have been excluded for purposes of this computation. Because of such shareholder’s control, shares owned by other officers, directors and 5% shareholders have not been excluded from the computation. As of March 31, 2017, there were 36,115,388 shares of Common Stock issued and outstanding.

| Documents of Which Portions Are Incorporated by Reference |

Parts of the Form 10-K into Which Portion of Documents are Incorporated | |

| Proxy Statement for Trans World Entertainment Corporation’s June 28, 2017 Annual Meeting of Shareholders to be filed on or about May 30, 2017 | III |

| 2 |

PART I

Cautionary Statement for Purposes of the “Safe Harbor” Provisions of the Private Securities Litigation Reform Act of 1995

This document includes forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements relate to analyses and other information that are based on forecasts of future results and estimates of amounts not yet determinable. These statements also relate to the Trans World Entertainment Corporation’s (“the Company’s”) future prospects, developments and business strategies. The statements contained in this document that are not statements of historical fact may include forward-looking statements that involve a number of risks and uncertainties.

We have used the words “anticipate”, “believe”, “could”, “estimate”, “expect”, “intend”, “may”, “plan”, “predict”, “project”, and similar terms and phrases, including references to assumptions, in this document to identify forward-looking statements. These forward-looking statements are made based on management’s expectations and beliefs concerning future events and are subject to uncertainties and factors relating to our operations and business environment, all of which are difficult to predict and many of which are beyond the Company’s control, that could cause actual results to differ materially from those matters expressed in or implied by these forward-looking statements. The following factors are among those that may cause actual results to differ materially from the Company’s forward-looking statements.

· new product introductions;

· accelerated declines in compact disc (“CD”) and home video industry sales;

· highly competitive nature of the retail entertainment business;

· new technology, including digital distribution;

· competitive pricing;

· current economic conditions and changes in mall traffic;

· dependence on key employees, the ability to hire new employees and pay competitive wages;

· the Company’s level of debt and related restrictions and limitations;

· future cash flows;

· availability of real estate;

· vendor terms;

· interest rate fluctuations;

· access to third party digital marketplaces

· adverse publicity;

· product liability claims;

· changes in laws and regulations;

· breach of data security and

· continued growth of e-commerce.

The reader should keep in mind that any forward-looking statement made by us in this document, or elsewhere, pertains only as of the date on which we make it. New risks and uncertainties come up from time-to-time and it’s impossible for us to predict these events or how they may affect us. In light of these risks and uncertainties, you should keep in mind that any forward-looking statements made in this report or elsewhere might not occur.

In addition, the preparation of financial statements in accordance with accounting principles generally accepted in the United States (“GAAP”) requires us to make estimates and assumptions. These estimates and assumptions affect:

| · | the reported amounts and timing of revenue and expenses, |

| · | the reported amounts and classification of assets and liabilities, and |

| · | the disclosure of contingent assets and liabilities. |

Actual results may vary from our estimates and assumptions. These estimates and assumptions are based on historical results, assumptions that we make, as well as assumptions by third parties.

| 3 |

Item 1. BUSINESS

Company Background

Trans World Entertainment Corporation, which, together with its consolidated subsidiaries, is referred to herein as “the Company”, “we”, “us” and “our”, was incorporated in New York in 1972. We own 100% of the outstanding common stock of Record Town, Inc and etailz, Inc. See below for additional information.

Our Reportable Segments

We operate our business in two segments: fye and etailz.

fye Segment

The Company’s fye segment operates retail stores and two e-commerce sites and is one of the largest specialty retailers of entertainment products, including trend, video, music, electronics and related products in the United States.

Stores and Store Concepts

As of January 28, 2017, the Company operated 284 stores totaling approximately 1.6 million square feet in the United States, the District of Columbia and the U.S. Virgin Islands predominantly under the f.y.e. (“For Your Entertainment”) brand.

Mall stores. The Company operated 250 traditional mall-based stores as of January 28, 2017. Mall stores average about 5,200 square feet and carry a full complement of entertainment products, including trend, video, music, electronics, and related products.

During fiscal 2016, the Company opened 14 new and remodeled 10 existing mall stores under a new format which expands the merchandise selection and enhances the presentation of the trend and electronics categories while maintaining a strong presence in the media categories. The new format stores average 4,300 square feet. As of January 28, 2017, the Company operated 34 stores under the new format.

Video only stores. The Company operated 6 video only stores as of January 28, 2017, predominately under the Suncoast Motion Pictures brand. These stores specialize in the sale of video and related product. They average about 2,500 square feet.

Freestanding Stores. The Company operated 28 freestanding stores predominantly under the fye brand. They carry a full complement of entertainment products, including trend, video, music, electronics, and related products and are located in freestanding, strip center and downtown locations. The freestanding stores average approximately 10,300 square feet.

E-Commerce Sites

The Company operates two retail web sites including www.fye.com and www.secondspin.com. fye.com is our flagship site and carries entertainment products, including trend, video, music, electronics and related products. SecondSpin.com is a leading seller of used CDs, DVDs, Blu-Ray and video games online and carries one of the largest catalogs of used media available online.

etailz Segment

On October 17, 2016, the Company acquired all of the issued and outstanding capital stock of etailz, Inc. (“etailz”), an innovative and leading digital marketplace retail expert. etailz uses a data driven approach to digital marketplace retailing utilizing proprietary software and ecommerce insight to identify new distributors and wholesalers, isolate emerging product trends, and optimize price positioning and inventory purchase decisions.

| 4 |

Merchandise Categories

fye Segment

Net sales by merchandise category as a percentage of total net sales for fiscal 2016, 2015 and 2014 were as follows:

| 2016 | 2015 | 2014 | ||||||||||

| Video | 34.1 | % | 39.5 | % | 43.9 | % | ||||||

| Trend | 32.0 | % | 22.2 | 15.2 | ||||||||

| Music | 21.9 | % | 25.1 | 27.0 | ||||||||

| Games | 0.8 | % | 2.4 | 4.3 | ||||||||

| Electronics | 11.2 | % | 10.8 | 9.6 | ||||||||

| Total | 100.0 | % | 100.0 | % | 100.0 | % | ||||||

etailz Segment

etailz generates revenue across a broad array of product lines primarily through the Amazon Marketplace.

Business Environment

fye Segment

Video and music accounted for approximately 50% of the Company’s net sales in fiscal 2016 versus 65% of sales in fiscal 2015. Physical media sales have suffered from the shift of content to digital distribution, streaming and online retailers (e.g., Amazon) that offer entertainment products at discounted prices and collectively have gained a larger share of the market.

Based primarily on statistical information obtained from Warner Brothers Home Entertainment and Nielsen SoundScan (“SoundScan”); physical video and music represent an approximately $9 billion industry nationwide in 2016.

According to statistics obtained from Warner Brothers Home Entertainment, overall video industry physical retail sales in 2016 were $5.4 billion compared to $6.1 billion in 2015, a decrease of 11%. Industry DVD retail sales decreased 15% in 2016 compared to 2015, while Blu-ray sales decreased 4%.

According to statistical information from SoundScan, the total number of music albums sold, including CD and digital albums, decreased 16% to approximately 194 million units in 2016. Excluding digital albums, in fiscal 2016, album sales decreased 14% from fiscal 2015 to approximately 115 million units.

etailz Segment

The Company’s etailz segment operates as a third party e-commerce market place (“Digital Marketplace”) reseller. Digital marketplaces are e-commerce platforms where online retailers enable third party sellers access to their website and customer base to sell new and used offerings. Digital marketplaces allow consumers to shop from a variety of merchants in one place and have become an integral part of many e-commerce sellers’ businesses, including Amazon.com, Walmart/Jet.com and ebay.

According to the U.S. Census Bureau, total e-commerce sales for 2016 were estimated at $394.9 billion, an increase of 15% from 2015. Total retail sales in 2016 increased 3% from 2015. E-commerce sales in 2016 accounted for 8% of total retail sales as compared to 7% of total retail sales for 2015.

| 5 |

Competition

fye Segment

The specialty entertainment retail industry is intensely competitive and subject to rapid changes in consumer preferences. We compete with mass merchants, consumer electronics stores, lifestyle retailers and online retailers. Our media products are also distributed through other methods such as digital delivery. We also compete with sellers of pre-owned and value media products. Additionally, we compete with other forms of entertainment activities, including casual and mobile games, movies, television, theater, sporting events and family entertainment centers.

We compete with Wal-Mart Stores, Inc. (“Wal-Mart”); Target Corporation (“Target”); Amazon.com, Inc. (“Amazon.com”); and Best Buy Co., Inc. (“Best Buy”), among others.

The Company has diversified its products and taken other measures to position itself competitively within its industry. The Company believes it effectively competes in the following ways:

| ▪ | Diversified product mix: the Company is expanding the range of product offerings in our non-media businesses. As a result, the non media categories contribution to total sales increased to 43% in fiscal 2016 as compared to 33% in fiscal 2015. |

| ▪ | Customer service: the Company offers personalized customer service in its stores guided by a commitment to approach every customer with gratitude, humility and respect; |

| ▪ | Location and convenience: a strength of the Company is its convenient store locations that are often the exclusive retailer in regional shopping centers offering a full complement of entertainment products; |

| ▪ | Marketing: the Company utilizes in-store visual displays, live events and a digital marketing strategy that employs email blasts and social networking. |

etailz Segment

etailz competes with other third-party marketplace sellers using a data driven approach to digital marketplace retailing utilizing proprietary software and ecommerce insight coupled with a direct customer relationship engagement to identify new distributors and wholesalers, isolate emerging product trends, and optimize price positioning and inventory purchase decisions. In the past 12 months, etailz sold over 30,000 SKUs from over 2,000 manufacturers and distributors in numerous product categories, primarily through the Amazon Marketplace.

Seasonality

The Company’s business is seasonal, with its fourth fiscal quarter constituting the Company’s peak selling period and generating substantially all of its’ net income. The fourth fiscal quarter of 2016 was impacted by the inclusion of sales from etailz. In fiscal 2016, fourth quarter revenue for the fye segment accounted for approximately 34% of annual total revenue. Historically, revenue generated during the fourth fiscal quarter for etailz has demonstrated similar seasonality as the fye segment. In anticipation of increased sales activity in the fourth quarter, the Company purchases additional inventory and hires seasonal associates to supplement its core store sales and distribution center staffs. If, for any reason, the Company’s net sales were below seasonal norms during the fourth quarter, the Company’s operating results could be adversely affected. Quarterly sales can also be affected by the timing of new product releases, new store openings or closings and the performance of existing stores.

Advertising

The Company makes use of visual displays including in-store signage and external banners. The Company employs a marketing strategy including email blasts and social networking. Certain vendors from whom the Company purchases merchandise offer advertising allowances, of varying duration and amount, to promote their merchandise.

| 6 |

Suppliers and Purchasing

fye Segment

The Company purchases inventory from approximately 400 suppliers. In fiscal 2016, 48% of purchases were made from ten suppliers including Universal Studio Home Entertainment, AEC - Paramount Video, Buena Vista Home Video, Digital Products International, Bio Domes, Twentieth Century Fox Home Entertainment, Warner/Elektra/Atlantic, Universal Music Group Distribution, Funko LLC, and Warner Home Video. The Company does not have material long-term purchase contracts; rather, it purchases products from its suppliers on an order-by-order basis. Historically, the Company has not experienced difficulty in obtaining satisfactory sources of supply and management believes that it will continue to have access to adequate sources of supply.

etailz segment

In the past 12 months, etailz sold over 30,000 SKUs from over 2,000 manufacturers and distributors in numerous product categories, primarily through the Amazon Marketplace.

Trade Customs and Practices

Under current trade practices with large suppliers, retailers of music and video products are generally entitled to return unsold merchandise they have purchased in exchange for other merchandise carried by the suppliers. The largest music suppliers charge a related merchandise return penalty or return handling fee. Most manufacturers and distributors of video products do not charge a return penalty or handling fee. Under current trade practices with large suppliers, retailers of trend, electronics, video games and related products may receive markdown support from suppliers to help clear discontinued or slow turning merchandise. Merchandise return policies and other trade practices have not changed significantly in recent years. The Company generally adapts its purchasing policies to changes in the policies of its largest suppliers.

As of January 28, 2017, the Company employed approximately 3,000 people, of whom approximately 1,200 were employed on a full-time basis. Others were employed on a part-time basis. The Company hires seasonal sales and distribution center employees during its fourth quarter peak selling season to ensure continued levels of personalized customer service and in-stock position. Assistant store managers, store managers, district managers and regional managers are eligible to receive incentive compensation based on the sales and/or profitability of stores for which they are responsible. Sales support managers are generally eligible to receive incentive compensation based on achieving Company performance targets. None of the Company’s employees are covered by collective bargaining agreements and management believes that the Company enjoys favorable relations with its employees.

Trademarks

The trademarks, for your entertainment (f.y.e.), etailz, Suncoast Motion Pictures and Saturday Matinee are registered with the U.S. Patent and Trademark Office and are owned by the Company. We believe that our rights to these trademarks are adequately protected. We hold no material patents, licenses, franchises or concessions; however, our established trademarks and trade names are essential to maintaining our competitive position in the entertainment retail industry.

Information Systems

fye segment

The Company’s inventory management systems and point-of-sale technology show daily sales and in-store stock by title by store. The systems use this data to automatically generate replenishment shipments to each store from our distribution centers, enabling each store to carry a merchandise assortment uniquely tailored to its own sales mix and rate of sale. Call lists and reservation system also provide our buying staff with information to determine order size and inventory management for store-by-store inventory allocation.

To support most operations the Company uses a large-scale computing environment with a state-of-the-art storage area network and a wired and wireless corporate network installed at regional headquarters, and a secure virtual private network

| 7 |

to access and provide services to computing assets located in stores, distribution centers and satellite offices, and to the mobile workforce.

An Oracle based point-of-sale system has been enhanced to facilitate trade-in transactions, including automatic lookup of trade-in prices and printing of machine-readable bar codes to facilitate in-store restocking of pre-owned products. In addition, our central database of all pre-owned products allows us to actively manage the pricing and product availability of our pre-owned products across our store base and reallocate our pre-owned products as necessary.

etailz segment

The Company uses a data driven approach to digital marketplace retailing utilizing proprietary software.

Business Combinations

etailz Acquisition

On October 17, 2016, the Company completed the purchase of all of the issued and outstanding shares of etailz, Inc. , an innovative and leading digital marketplace retail expert. etailz is a leading digital marketplace expert retailer, operating both domestically and internationally. They use a data driven approach to digital marketplace retailing utilizing proprietary software and ecommerce insight coupled with a direct customer relationship engagement to identify new distributors and wholesalers, isolate emerging product trends, and optimize price positioning and inventory purchase decisions. The acquisition of etailz is part of our strategy to diversify our business into the fastest growing segment of retail: the Digital Marketplace. The Company plans to access the relationships, operational expertise, and infrastructure built by etailz to help unlock the full potential of etailz and to accelerate our progress towards being the industry leader for digital marketplace sales and expertise.

The Company paid $32.3 million in cash, issued 5.7 million shares of TWMC stock at closing to the shareholders of etailz as consideration for their shares, and paid $4.3 million in cash advances to settle obligations of the selling shareholders. Based on the fair value of $3.56 per share on the acquisition date, the shares had a value of $20.4 million. An earn-out of up to a maximum of $14.6 million will be payable in fiscal 2018 and fiscal 2019 subject to the achievement by etailz of $6 million in operating income in fiscal 2017 and $7.5 million in fiscal 2018 as outlined in the share purchase agreement. In connection with the acquisition, the Company assumed a liability of the selling shareholders for an etailz employee bonus plan, of which $1.9 million was due and payable at closing and funded as part of the cash advances and the remaining $2.3 million will be earned over a two year service period. The acquisition and related costs were funded primarily from the Company’s cash on hand and short term borrowings under its revolving credit facility. The acquisition was accounted for using the purchase method of accounting.

The amount of goodwill represents the excess of the purchase price over the preliminary net identifiable assets acquired and liabilities assumed. Goodwill primarily represents, among other factors, the value of synergies expected to be realized and for the knowledge and expertise of, and established presence in, the digital marketplace, which do not qualify as separate amortizable intangible assets. Goodwill arising from the acquisition of etailz is not deductible for tax purposes.

| 8 |

The acquisition date fair value of the consideration for the above transaction consisted of the following as of October 17, 2016 (in thousands):

| Cash consideration | $ | 36,600 | ||

| Fair value of stock consideration | 20,415 | |||

| Fair value of contingent consideration | 10,381 | |||

| Fair value of indemnification consideration held in escrow | 1,500 | |||

| Fair value of purchase consideration | $ | 68,896 |

The following table summarizes the allocation of the aggregate purchase price to the estimated fair value of the net assets acquired:

| ($ in thousands) | ||||

| October 17, 2016 | ||||

| Assets Acquired | ||||

| Accounts receivable | 1,533 | |||

| Prepaid expenses and other current assets | 5,896 | |||

| Inventory | 14,608 | |||

| Property and equipment, net | 663 | |||

| Other long term-assets | 12 | |||

| Acquired intangible assets: | ||||

| Trade names | 3,200 | |||

| Technology | 6,700 | |||

| Vendor relationships | 19,100 | |||

| Unfavorable lease valuation | (53 | ) | ||

| Goodwill | 39,191 | |||

| Total assets acquired | $ | 90,850 | ||

| Liabilities Assumed | ||||

| Accounts payable | $ | 4,888 | ||

| Debt | 4,729 | |||

| Other current liabilities | 5,349 | |||

| Deferred taxes | 6,988 | |||

| Total liabilities assumed | $ | 21,954 | ||

| Net assets acquired | $ | 68,896 | ||

The results of operations of etailz will be reported in the Company’s etailz segment and has been included in the consolidated results of operations of the Company from the date of acquisition.

Available Information

The Company’s headquarters are located at 38 Corporate Circle, Albany, New York 12203, and its telephone number is (518) 452-1242. The Company’s corporate website address is www.twec.com. The Company makes available, free of charge, its Exchange Act Reports (Forms 10-K, 10-Q, 8-K and any amendments thereto) on its web site as soon as practical after the reports are filed with the Securities and Exchange Commission (“SEC”). The public may read and copy any materials the Company files with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room can be obtained by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. This information can be obtained from the site http://www.sec.gov. The Company’s Common Stock, $0.01 par value, is listed on the NASDAQ National Market under the trading symbol

| 9 |

“TWMC”. The Company’s fiscal year end is the Saturday closest to January 31. The fiscal 2016 (“fiscal 2016”) year ended on January 28, 2017; fiscal 2015 (“fiscal 2015”) year ended on January 30, 2016; and fiscal 2014 (“fiscal 2014”) year ended on January 31, 2015. All fiscal periods presented were 52 weeks.

Item 1A. RISK FACTORS

The following is a discussion of certain factors, which could affect the financial results of the Company.

Risks Related to Our Business and Industry

The Company’s results of operations are affected by the availability of new products.

The Company’s business is affected by the release of “hit” music and video titles, which can create fluctuations in sales. It is not possible to determine the timing of these fluctuations or the future availability of hit titles. The Company is dependent upon the major music and movie producers to continue to produce hit products. To the extent that new hit releases are not available, or not available at prices attractive to consumers, or, if manufacturers fail to introduce or delay the introduction of new products, the Company’s results of operations may be adversely affected.

The Company’s results of operations are affected by the continued declines in the physical video and music industries.

Physical media sales have suffered from the shift of content to digital distribution, streaming and online retailers (e.g., Amazon) that offer entertainment products at discounted prices and collectively have gained a larger share of the market. Physical video and music represent approximately 50% of sales and have been impacted by new distribution channels, including digital distribution, streaming and internet fulfillment. As a result, the Company has had negative comparable store sales for all periods presented.

If we cannot successfully diversify our product mix and implement our business strategy our growth and profitability could be adversely impacted.

Our future results will depend, among other things, on our success in implementing our business strategy. There can be no assurance that we will be successful in implementing our business strategy or that the strategy will be successful in sustaining acceptable levels of sales growth and profitability.

The Company’s results of operations may suffer if the Company does not accurately predict consumer acceptance of new products or distribution technologies or adapt to a shift to multichannel experience.

The entertainment industry is characterized by changing technology, evolving format standards, and new and enhanced product introductions. These characteristics require the Company to respond quickly to technological changes and understand the impact of these changes on customers’ preferences. If the Company is unable to participate in new product or distribution technologies, its results of operations may suffer. Specifically, CD and DVD formats have experienced a continuous decline as digital forms of music and video content have become more prevalent. If the Company does not timely adapt to these changing technologies or sufficiently focus on the other categories, operating results could significantly suffer.

In addition, multichannel retailing is rapidly evolving with the increasing use of computers, tablets, mobile phones and other devices to shop in stores and online and the increased use of social media as a means of interacting with our customers and enhancing their shopping experiences. If we are unable to adapt to the growth of multichannel retailing, and keep pace with the changing expectations of our customers and new developments by our competitors, customer experience could be negatively affected, resulting in a loss of customer confidence and satisfaction, and lost sales, which could adversely affect our reputation and results of operations.

Increased competition from existing retailers, including internet retailers, could adversely affect the Company’s results of operations.

| 10 |

The Company competes with a wide variety of entertainment retailers, including deep-discount retailers, mass merchandisers, consumer electronics outlets, internet retailers and independent operators, some of whom have greater financial and other resources than the Company and frequently sell their product at discounted prices or with added value.

In addition, the Company’s success depends on our ability to positively differentiate ourselves from other retailers. The retail business is highly competitive. In the past, the Company has been able to compete successfully by differentiating our customer shopping experience, by creating an attractive value proposition through a careful combination of price, merchandise assortment, convenience, customer service and marketing efforts. Customer perceptions regarding our stores, our in-stock position and deep assortment of product are also factors in our ability to compete. No single competitive factor is dominant, and actions by our competitors on any of these factors could have an adverse effect on our sales, gross profit and expenses. If we fail to continue to positively differentiate ourselves from our competitors, our results of operations could be adversely affected.

The ability to attract customers to our stores depends heavily on the success of the shopping malls in which many of our stores are located; any decrease in consumer traffic in those malls could adversely affect the Company’s results of operations.

In order to generate customer traffic we depend heavily on locating many of our stores in prominent locations within successful shopping malls. Sales at these stores are derived from the volume of traffic in those malls. Our stores benefit from the ability of a mall’s other tenants to generate consumer traffic in the vicinity of our stores and the continuing popularity of malls as shopping destinations. Our sales volume and mall traffic generally may be adversely affected by, among other things, economic downturns in a particular area, competition from ecommerce retailers, non-mall retailers and other malls, increases in gasoline prices, fluctuations in exchange rates in border or tourism-oriented locations and the closing or decline in popularity of other stores in the malls in which we are located. An uncertain economic outlook could curtail new shopping mall development, decrease shopping mall traffic, reduce the number of hours that shopping mall operators keep their shopping malls open or force them to cease operations entirely. A reduction in mall traffic as a result of these or any other factors could have a material adverse effect on our business, results of operations and financial condition.

The Company’s business is influenced by general economic conditions.

The Company’s performance is subject to general economic conditions and their impact on levels of discretionary consumer spending. General economic conditions impacting discretionary consumer spending include, among others, wages and employment, consumer debt, reductions in net worth, residential real estate and mortgage markets, taxation, fuel and energy prices, interest rates, consumer confidence and other macroeconomic factors.

Consumer purchases of discretionary items, such as our merchandise, generally decline during recessionary periods and other periods where disposable income is adversely affected. A downturn in the economy affects specialty retailers disproportionately, as consumers may prioritize reductions in discretionary spending, which could have a direct impact on purchases of our merchandise and adversely impact our results of operations. In addition, reduced consumer spending may drive us and our competitors to offer additional products at promotional prices, which would have a negative impact on gross profit.

Disruption of global capital and credit markets may have a material adverse effect on the Company’s liquidity and capital resources.

Distress in the financial markets has in the past and can in the future result in extreme volatility in security prices, diminished liquidity and credit availability. There can be no assurance that our liquidity will not be affected by changes in the financial markets and the global economy or that our capital resources will at all times be sufficient to satisfy our liquidity needs.

Because of our floating rate credit facility, we may be adversely affected by interest rate changes.

Our financial position may be affected by fluctuations in interest rates, as our credit facility is subject to floating interest rates. Interest rates are highly sensitive to many factors, including governmental monetary policies, domestic and international economic and political conditions and other factors beyond our control. If we were to borrow against our senior credit facility, a significant increase in interest rates could have an adverse effect on our financial position and results of operations.

| 11 |

Historically, we have experienced declines and we may continue to experience fluctuation in our level of sales, results from operations and operating cash flow.

A variety of factors has historically affected, and will continue to affect, our comparable stores sales results and profit margins. These factors include general regional and national economic conditions; competition; actions taken by our competitors; consumer trends and preferences; new product introductions and changes in our product mix; timing and effectiveness of promotional events and weather. The Company’s comparable store sales may decline further than they did in fiscal 2016. Also, they may vary from quarter to quarter as our business is highly seasonal in nature. Our highest sales and operating income historically occur during the fourth fiscal quarter, which is due in part to the holiday selling season. The fourth quarter generated approximately 34% of our total annual pro forma revenue for fiscal 2016 (as discussed in Note 7 of Notes to the Consolidated Financial Statements in this report). Any decrease in our fourth quarter sales, whether due to a slow holiday selling season, unseasonable weather conditions, economic conditions or otherwise, could have a material adverse effect on our business, financial condition and operating results for the entire fiscal year. There is no assurance that we will achieve positive levels of sales and earnings growth, and any decline in our future growth or performance could have a material adverse effect on our business and results of operations.

Failure to open new stores or renew existing leases in profitable stores may limit our earnings.

Historically, the Company’s growth has come from adding stores. The Company opens new stores if it finds desirable locations and is able to negotiate suitable lease terms for profitability. A lack of new store growth may impact the Company’s ability to increase sales and earnings. During 2016, the Company opened 14 new stores and remodeled 11 under a new format and closed 29 stores with expiring leases. Likewise, the Company regularly renews leases at existing locations if those stores are profitable. Failure to renew these leases may impact the Company’s earnings. See Item 2: Properties, for timing of lease expirations.

A change in one or more of the Company’s vendors’ policies or the Company’s relationship with those vendors could adversely affect the Company’s results of operations.

The Company is dependent on its vendors to supply merchandise in a timely and efficient manner. If a vendor fails to deliver on its commitments, whether due to financial difficulties or other reasons, the Company could experience merchandise shortages that could lead to lost sales.

The majority of the Company’s purchases come from ten major suppliers. As is standard in its industry, the Company does not maintain long-term contracts with its suppliers but instead makes purchases on an order-by-order basis. If the Company fails to maintain customary trade terms or enjoy positive vendor relations, it could have an adverse effect on the Company’s results of operations.

If the Company’s vendors fail to provide marketing and merchandising support at historical levels, the Company’s results of operations could be adversely affected.

The manufacturers of entertainment products have typically provided retailers with significant marketing and merchandising support for their products. As part of this support, the Company receives cooperative advertising and other allowances from these vendors. These allowances enable the Company to actively promote and merchandise the products it sells at its stores and on its websites. If the Company’s vendors fail to provide this support at historical levels, the Company’s results of operations could be negatively impacted.

Parties with whom the Company does business may be subject to insolvency risks or may otherwise become unable or unwilling to perform their obligations to the Company.

The Company is a party to contracts, transactions and business relationships with various third parties, including vendors, suppliers, service providers and lenders, pursuant to which such third parties have performance, payment and other obligations to the Company. In some cases, the Company depends upon such third parties to provide essential products, services or other benefits, including with respect to store and distribution center locations, merchandise, advertising, software development and support, logistics, other agreements for goods and services in order to operate the Company’s business in the ordinary course, extensions of credit, credit card accounts and related receivables, and other vital matters. Economic,

| 12 |

industry and market conditions could result in increased risks to the Company associated with the potential financial distress or insolvency of such third parties. If any of these third parties were to become subject to bankruptcy, receivership or similar proceedings, the rights and benefits of the Company in relation to its contracts, transactions and business relationships with such third parties could be terminated, modified in a manner adverse to the Company, or otherwise impaired. The Company cannot make any assurances that it would be able to arrange for alternate or replacement contracts, transactions or business relationships on terms as favorable as the Company’s existing contracts, transactions or business relationships, if at all. Any inability on the part of the Company to do so could negatively affect the Company’s cash flows, financial condition and results of operations.

Breach of data security could harm our business and standing with our customers.

The protection of our customer, employee and business data is critical to us. Our business, like that of most retailers, involves the receipt, storage and transmission of customers’ personal information, consumer preferences and payment card information, as well as confidential information about our employees, our suppliers and our Company. We rely on commercially available systems, software, tools and monitoring to provide security for processing, transmission and storage of all such data, including confidential information. Despite the security measures we have in place, our facilities and systems, and those of our third-party service providers, may be vulnerable to security breaches, acts of vandalism, computer viruses, misplaced or lost data, programming or human errors, or other similar events. Unauthorized parties may attempt to gain access to our systems or information through fraud or other means, including deceiving our employees or third-party service providers. The methods used to obtain unauthorized access, disable or degrade service, or sabotage systems are also constantly changing and evolving, and may be difficult to anticipate or detect. We have implemented and regularly review and update our control systems, processes and procedures to protect against unauthorized access to or use of secured data and to prevent data loss. However, the ever-evolving threats mean we must continually evaluate and adapt our systems and processes, and there is no guarantee that they will be adequate to safeguard against all data security breaches or misuses of data. Any security breach involving the misappropriation, loss or other unauthorized disclosure of customer payment card or personal information or employee personal or confidential information, whether by us or our vendors, could damage our reputation, expose us to risk of litigation and liability, disrupt our operations, harm our business and have an adverse impact upon our net sales and profitability. As the regulatory environment related to information security, data collection and use, and privacy becomes increasingly rigorous, with new and changing requirements applicable to our business, compliance with those requirements could also result in additional costs. Further, if we are unable to comply with the security standards established by banks and the credit card industry, we may be subject to fines, restrictions and expulsion from card acceptance programs, which could adversely affect our retail operations.

Our hardware and software systems are vulnerable to damage, theft or intrusion that could harm our business.

Our success, in particular our ability to successfully manage inventory levels and process customer transactions, largely depends upon the efficient operation of our computer hardware and software systems. We use management information systems to track inventory at the store level and aggregate daily sales information, communicate customer information and process purchasing card transactions, process shipments of goods and report financial information.

Any failure of our computer hardware or software systems that causes an interruption in our operations or a decrease in inventory tracking could result in reduced net sales and profitability. Additionally, if any data intrusion, security breach, misappropriation or theft were to occur, we could incur significant costs in responding to such event, including responding to any resulting claims, litigation or investigations, which could harm our operating results.

Our inability or failure to protect our intellectual property rights, or any claimed infringement by us of third party intellectual rights, could have a negative impact on our operating results.

Our trademarks, service marks, copyrights, patents, trade secrets and other intellectual property, including proprietary software, are valuable assets that are critical to our success. The unauthorized reproduction or other misappropriation of our intellectual property could cause a decline in our revenue. In addition, any infringement or other intellectual property claim made against us could be time-consuming to address, result in costly litigation, cause product delays, require us to enter into royalty or licensing agreements or result in our loss of ownership or use of the intellectual property.

| 13 |

Loss of key personnel or the inability to attract, train and retain qualified employees could adversely affect the Company’s results of operations.

The Company believes that its future prospects depend, to a significant extent, on the services of its executive officers. Our future success will also depend on our ability to attract and retain qualified key personnel. The loss of the services of certain of the Company’s executive officers and other key management personnel could adversely affect the Company’s results of operations.

In addition to our executive officers, the Company’s business is dependent on our ability to attract, train and retain a large number of qualified team members. Many of those team members are employed in entry-level or part-time positions with historically high turnover rates. Our ability to meet our labor needs while controlling our costs is subject to external factors such as unemployment levels, health care costs and changing demographics. If we are unable to attract and retain adequate numbers of qualified team members, our operations, customer service levels and support functions could suffer. Those factors, together with increased wage and benefit costs, could adversely affect our results of operations.

Failure to comply with legal and regulatory requirements could adversely affect the Company’s results of operations.

The Company’s business is subject to a wide array of laws and regulations. Significant legislative changes that impact our relationship with our workforce (none of which is represented by unions) could increase our expenses and adversely affect our operations. Examples of possible legislative changes impacting our relationship with our workforce include changes to an employer’s obligation to recognize collective bargaining units, the process by which collective bargaining units are negotiated or imposed, minimum wage requirements, health care mandates, and changes in overtime regulations

Our policies, procedures and internal controls are designed to comply with all applicable laws and regulations, including those imposed by the Securities and Exchange Commission and the NASDAQ Global Market, as well as applicable employment laws. Additional legal and regulatory requirements increase the complexity of the regulatory environment in which we operate and the related cost of compliance. Failure to comply with such laws and regulations may result in damage to our reputation, financial condition and market price of our stock.

We could be materially and adversely affected if our distribution center is disrupted.

We operate a distribution center in Albany, New York. We ship approximately 78% of our fye segment merchandise inventory through our distribution center. If our distribution center is destroyed or disrupted for any reason, including weather, fire, labor, or other issues we could incur significantly higher costs and longer lead times associated with distributing our products to our stores during the time it takes to reopen or replace the center.

We maintain business interruption insurance to protect us from the costs relating to matters such as a shutdown, but our insurance may not be sufficient, or the insurance proceeds may not be timely paid to us, in the event of a shutdown.

Risks Related to Ownership of Our Common Stock.

The Robert J. Higgins TWMC Trust (the “Trust”) owns approximately 39.5% of the outstanding Common Stock. Therefore, the trustees have significant influence and control over the outcome of any vote of the Company’s Shareholders.

The Robert J. Higgins TWMC Trust owns approximately 39.5% of the outstanding Common Stock and there are no limitations on the Trust acquiring shares in the future. Accordingly, the trustees have significant influence over the election of our directors, the appointment of new management and the approval of actions requiring shareholder approval, such as adopting amendments to our articles of incorporation and approving mergers or sales of all or substantially all of our assets. Such concentration of ownership and substantial voting influence may have the effect of delaying or preventing a change of control, even if a change of control is in the best interest of all shareholders. There may be instances in which the interest of the Trust may conflict or be perceived as being in conflict with the interest of a holder of our securities or the interest of the Company.

| 14 |

The Company’s stock price has experienced and could continue to experience volatility and could decline, resulting in a substantial loss on your investment.

Our stock price has experienced, and could continue to experience in the future, substantial volatility as a result of many factors, including global economic conditions, broad market fluctuations and public perception of the prospects for music and the home video industry. Changes in our comparable store net sales could also affect the price of our Common Stock. Failure to meet market expectations, particularly with respect to comparable store sales, net revenues, operating margins and earnings per share, would likely result in a decline in the market price of our stock.

In addition, an active trading market for our Common Stock may not be sustained, which could affect the ability of our stockholders to sell their shares and could depress the market price of their shares. The stock market has been highly volatile. For example, the closing price of our Common Stock at quarter ends has fluctuated between $1.65 and $4.00 from January 31, 2016 to March 31, 2017. Investors in our Common Stock may experience a decrease in the value of their stock, including decreases unrelated to our operating performance or prospects.

The declaration of dividend payments or the repurchase of our common stock pursuant to our share repurchase program may not continue.

Our dividend policy and share repurchase program may be affected by, among other items, business conditions, changes in our business strategy, our views on potential future capital requirements, the terms of our debt instruments, legal risks, changes in federal income tax law and challenges to our business model. Our dividend policy may change from time to time and we may or may not continue to declare discretionary dividend payments. The Company’s amended credit facility contains certain restrictions related to the payment of cash dividends or share repurchases, including limiting the amount of dividends to $5.0 million annually and not allowing borrowings under the amended facility for the six months before or six months after the dividend payment or repurchase of shares.

Additionally, although we have a share repurchase program authorized by our Board of Directors, we are not obligated to make any purchases under the program and we may discontinue it at any time.

The failure to maintain a minimum closing share price of $1.00 per share of our Common Stock could result in the delisting of our shares on the NASDAQ Global Market, which would harm the market price of the Company’s Common Stock.

In order to retain our listing on the NASDAQ Global Market we are required by NASDAQ to maintain a minimum bid price of $1.00 per share. Our stock price is currently above $1.00 and has been since October 6, 2009. However, in the event that our stock did close below the minimum bid price of $1.00 per share for any 30 consecutive business days, we would regain compliance if our Common Stock closed at or above $1.00 per share for 10 consecutive days during the 180 days immediately following failure to maintain the minimum bid price. If we are unable to do so, our stock could be delisted from the NASDAQ Global Market, transferred to a listing on the NASDAQ Capital Market, or delisted from the NASDAQ markets altogether. The failure to maintain our listing on the NASDAQ Global Market could harm the liquidity of the Company’s Common Stock and could have an adverse effect on the market price of our Common Stock.

Risks Related to the Acquisition of etailz

The integration of etailz, Inc. with existing operations could have an adverse effect on our business.

On October 17, 2016, we acquired all of the issued and outstanding capital stock of etailz Inc. (the “Acquisition”). The acquisition of a business and its integration with existing operations involves a number of financial, managerial and operational challenges that take significant management time and attention. In addition, we have incurred significant expenses and fees in connection with the Acquisition and may incur additional expenses post-closing. Our overall profitability would be adversely affected if our time and expenses associated with businesses we have acquired or may acquire in the future are not matched or exceeded by the revenues that are derived from such acquisition.

In connection with the Acquisition, we are expanding into a new market in which we have limited operating experience.

| 15 |

We have limited experience as a reseller on third-party ecommerce marketplaces. Our entry into this new line of business may subject us to additional risks and uncertainties. If etailz is not successful, it may not produce substantial revenue or profit and our operating results could be adversely affected.

etailz revenue is dependent upon maintaining etailz’s relationship with Amazon and failure to do so, or any restrictions on our ability to offer products on the Amazon Marketplace, could have an adverse impact on our business, financial condition and results of operations.

etailz generates substantially all of its revenue through the Amazon Marketplace. Therefore, we depend in large part on our relationship with Amazon for the continued growth of the etailz segment. In particular, we depend on our ability to offer products on the Amazon Marketplace. We also depend on Amazon for the timely delivery of products to customers. Any adverse change in our relationship with Amazon, including restrictions on the ability to offer products or termination of the relationship, could adversely affect the continued growth of our etailz segment and our financial condition and results of operations.

We may encounter difficulties in fully integrating etailz into our business and may not fully achieve, or achieve within a reasonable time frame, expected strategic objectives and other expected benefits of the Acquisition.

The success of the acquisition of etailz will depend, in part, on our ability to realize the anticipated growth opportunities on a standalone basis and from the integration of etailz with our existing business. There may be substantial difficulties, costs and delays involved in the integration of etailz with our own business, including distracting management from day-to-day operations and potential incompatibility of corporate cultures, and costs and delays in implementing systems and procedures. In addition, the process of integrating the operations of etailz could cause an interruption of, or loss of momentum in, the activities of one or more of our combined businesses and the possible loss of key personnel or vendor partners. Any one or all of these factors may increase our operating costs or lower our anticipated financial performance. Our failure to fully integrate etailz could have an adverse effect on our financial condition and results of operations.

We may record future goodwill impairment charges which could negatively impact our future results of operations and financial condition.

Because we have grown in part through acquisitions, goodwill and other acquired intangible assets represent a substantial portion of our assets. If a determination is made that a significant impairment in value of goodwill, other intangible assets or long-lived assets has occurred, such determination could require us to impair a substantial portion of our assets. Asset impairments could have a material adverse effect on our financial condition and results of operations.

Item 1B. UNRESOLVED SEC COMMENTS

None.

Item 2. PROPERTIES

Retail Stores

As of January 28, 2017, fye segment leased and operated 284 stores some of which have renewal options. The majority of the leases provide for the payment of fixed monthly rent and expenses for maintenance, property taxes and insurance, while others provide for the payment of monthly rent based on a percentage of sales. Certain leases provide for additional rent based on store sales in excess of specified levels. The following table lists the leases due to expire in each of the fiscal years shown as of the fiscal year-end, assuming any renewal options are not exercised:

| Year | No. of Leases | Year | No. of Leases | |||||||||||

| 2017 | 118 | 2021 | 15 | |||||||||||

| 2018 | 60 | 2022 | 26 | |||||||||||

| 2019 | 38 | 2023 and beyond | 13 | |||||||||||

| 2020 | 14 | |||||||||||||

| 16 |

As leases expire, the Company will evaluate the decision to exercise renewal rights or obtain new leases for the same or similar locations based on store profitability.

Corporate Offices and Distribution Center Facilities

As of January 28, 2017, we leased the following office and distribution facilities:

| Square | Owned or | |||||||

| Location | Footage | Leased | Use | |||||

| fye | ||||||||

| Albany, NY | 39,800 | Leased | Office administration | |||||

| Albany, NY | 141,500 | Leased | Distribution center | |||||

| etailz | ||||||||

| Spokane, WA | 8,300 | Leased | Office administration | |||||

| Spokane, WA | 32,000 | Leased | Distribution center | |||||

The Company believes that it has adequate distribution facilities to meet the Company’s current business needs. Shipments from the Albany distribution facility to the Company’s retail stores provide approximately 78% of all merchandise shipment requirements to stores. Stores are serviced by common carriers chosen on the basis of geography and rate considerations. The balance of the stores’ merchandise requirements is satisfied through direct shipments from vendors. The Spokane, WA facility supports the distribution, where required, to outside distribution facilities for sale on third-party marketplace.

Item 3. LEGAL PROCEEDINGS

The Company is subject to various legal proceedings and claims that have arisen in the ordinary course of its business and have not been finally adjudicated. Although there can be no assurance as to the ultimate disposition of these matters, it is management’s opinion, based upon the information available at this time, that the expected outcome of these matters, individually or in the aggregate, will not have a material adverse effect on the results of operations and financial condition of the Company.

Item 4. Mine Safety Disclosures

None.

| 17 |

PART II

Item 5. MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information: The Company’s Common Stock trades on the NASDAQ Global Market under the symbol “TWMC.” As of March 31, 2017, there were 328 shareholders of record. The following table sets forth high and low last reported sale prices for each fiscal quarter during the period from February 1, 2015 through March 31, 2017.

| Closing Sales Prices | ||||||||

| High | Low | |||||||

| 2015 | ||||||||

| 1st Quarter | $ | 4.00 | $ | 3.42 | ||||

| 2nd Quarter | $ | 3.88 | $ | 3.51 | ||||

| 3rd Quarter | $ | 3.94 | $ | 3.50 | ||||

| 4th Quarter | $ | 3.88 | $ | 3.13 | ||||

| 2016 | ||||||||

| 1st Quarter | $ | 4.00 | $ | 3.13 | ||||

| 2nd Quarter | $ | 4.00 | $ | 3.45 | ||||

| 3rd Quarter | $ | 3.92 | $ | 3.40 | ||||

| 4th Quarter | $ | 3.90 | $ | 2.65 | ||||

| 2017 | ||||||||

| 1st Quarter (through March 31, 2017) | $ | 2.90 | $ | 1.65 | ||||

On March 31, 2017, the last reported sale price on the Common

Stock on the NASDAQ National Market was $1.70.

Dividend Policy: The Company did not pay cash dividends in fiscal 2016 and fiscal 2015. The declaration and payment of any dividends is at the sole discretion of the board of directors and is not guaranteed. The Company’s amended credit facility contains certain restrictions related to the payment of cash dividends, including limiting the amount of dividends to $5.0 million annually and not allowing borrowings under the amended facility for the six months before or six months after the dividend payment.

| 18 |

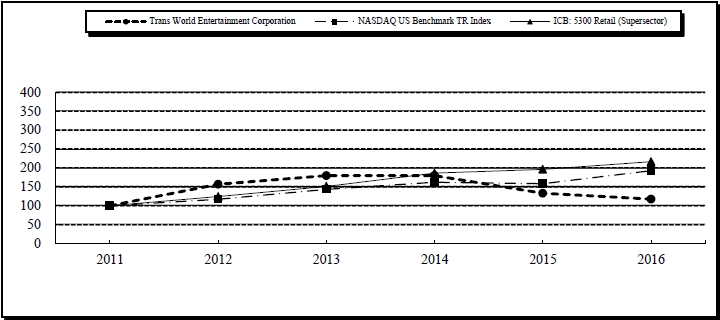

Five-Year Performance Graph

The following line graph reflects a comparison of the cumulative total return of the Company’s Common Stock from January 28, 2012 through January 28, 2017 with the NASDAQ US Benchmark TR Index and with ICB: 5300 Retail (Supersector) index. Because none of the Company’s leading competitors has been an independent publicly traded company over the period, the Company has elected to compare shareholder returns with the published index of retail companies compiled by NASDAQ. All values assume a $100 investment on January 29, 2011, and that all dividends were reinvested.

| Fiscal Years | |||||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | ||||||||||||||||||

| Trans World Entertainment Corporation | 100 | 157 | 179 | 180 | 133 | 117 | |||||||||||||||||

| NASDAQ US Benchmark TR Index | 100 | 117 | 143 | 162 | 158 | 193 | |||||||||||||||||

| ICB: 5300 Retail (Supersector) | 100 | 124 | 151 | 186 | 196 | 217 | |||||||||||||||||

Issuer Purchases of Equity Securities During the Quarter Ended January 28, 2017

The Board of Directors authorized a $22 million share repurchase program in August 2013. The timing of share repurchases under the repurchase program depends upon marketplace conditions and other factors, and the program remains subject to the discretion of the Board of Directors.

During the 3 months period ended January 28, 2017, the Company did not repurchase any shares under the share repurchase program.

The Company’s amended credit facility contains certain restrictions related to share repurchases, including limiting the amount of repurchases to $5.0 million annually and not allowing borrowings under the amended facility for the six months before or six months after the share repurchase transaction.

Item 6. SELECTED CONSOLIDATED FINANCIAL DATA

The following table sets forth selected Statements of Income and Balance Sheet data for the five fiscal years ended January 28, 2017 and is derived from the Company’s audited Consolidated Financial Statements. The fiscal year ended February 2, 2013 consisted of 53 weeks while all the other fiscal years of the Company presented consisted of 52 weeks. This information should be read in conjunction with the Company’s audited Consolidated Financial Statements and related notes and other financial information included herein, including Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

| 19 |

| Fiscal Year Ended | ||||||||||||||||||||

| January 28, | January 30, | January 31, | February 1, | February 2, | ||||||||||||||||

| (in thousands, except per share data) | 2017 (1) | 2016 | 2015 | 2014 | 2013 | |||||||||||||||

| STATEMENT OF INCOME DATA: | ||||||||||||||||||||

| Net sales | $ | 348,672 | $ | 334,661 | $ | 358,490 | $ | 393,659 | $ | 458,544 | ||||||||||

| Other revenue (2) | 4,798 | 4,843 | 4,773 | 4,326 | 4,437 | |||||||||||||||

| Total revenue | 353,470 | 339,504 | 363,263 | 397,985 | 462,981 | |||||||||||||||

| Cost of sales | 218,811 | 204,089 | 222,572 | 245,755 | 286,422 | |||||||||||||||

| Gross profit | 134,659 | 135,415 | 140,691 | 152,230 | 176,559 | |||||||||||||||

| Selling, general and administrative expenses | 139,691 | 130,845 | 136,916 | 141,855 | 163,009 | |||||||||||||||

| Gain on sale of asset | (1,164 | ) | — | — | — | (22,750 | ) | |||||||||||||

| Income (loss) from operations | (3,868 | ) | 4,570 | 3,775 | 10,375 | 36,300 | ||||||||||||||

| Interest expense | 775 | 1,860 | 1,951 | 2,010 | 2,384 | |||||||||||||||

| Other income | (1,081 | ) | (160 | ) | (70 | ) | (80 | ) | (66 | ) | ||||||||||

| Income (loss) before income taxes | (3,562 | ) | 2,870 | 1,894 | 8,445 | 33,982 | ||||||||||||||

| Income tax expense (benefit) | (6,773 | ) | 181 | 116 | 168 | 248 | ||||||||||||||

| Net income | $ | 3,211 | $ | 2,689 | $ | 1,778 | $ | 8,277 | $ | 33,734 | ||||||||||

| Basic earnings per share | $ | 0.10 | $ | 0.09 | $ | 0.06 | $ | 0.25 | $ | 1.07 | ||||||||||

| Weighted average number of shares outstanding - basic | 32,162 | 31,167 | 31,744 | 32,584 | 31,577 | |||||||||||||||

| Diluted earnings per share | $ | 0.10 | $ | 0.09 | $ | 0.06 | $ | 0.25 | $ | 1.06 | ||||||||||

| Weighted average number of shares – diluted | 32,321 | 31,323 | 31,897 | 32,862 | 31,878 | |||||||||||||||

| Cash dividend paid per share | — | — | $ | 0.50 | — | $ | 0.47 | |||||||||||||

| Fiscal Year Ended | ||||||||||||||||||||

| January 28, | January 30, | January 31, | February 1, | February 2, | ||||||||||||||||

| 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||

| (in thousands, except store count data) | ||||||||||||||||||||

| BALANCE SHEET DATA (at the end of the period): | ||||||||||||||||||||

| Total assets | $ | 307,810 | $ | 271,605 | $ | 280,009 | $ | 311,591 | $ | 314,414 | ||||||||||

| Current portion of long-term debt and capital lease obligations | — | — | 938 | 1,066 | 936 | |||||||||||||||

| Long-term obligations | — | — | — | 938 | 2,004 | |||||||||||||||

| Shareholders’ equity | $ | 197,936 | $ | 175,268 | $ | 171,740 | $ | 190,970 | $ | 179,934 | ||||||||||

| OPERATING DATA: | ||||||||||||||||||||

| Store count (open at end of period): | ||||||||||||||||||||

| Mall stores | 256 | 267 | 270 | 293 | 304 | |||||||||||||||

| Freestanding stores | 28 | 32 | 40 | 46 | 54 | |||||||||||||||

| Total stores | 284 | 299 | 310 | 339 | 358 | |||||||||||||||

| Comparable store sales decreases(2) | (4 | %) | (1 | %) | (1 | %) | (5 | %) | (1 | %) | ||||||||||

| Total square footage in operation (Year end) | 1,593 | 1,730 | 1,799 | 2,030 | 2,209 | |||||||||||||||

| Total square footage in operation (Average) | 1,669 | 1,793 | 1,940 | 2,134 | 2,362 | |||||||||||||||

| 1. | In 2016, we acquired the outstanding stock of etailz, Inc., which included $40.2 million in revenue, $9.9 million in gross profit, and $9.2 million in selling, general, and administrative expenses. The total above includes operational results from October 17, 2016 to January 28, 2017. |

| 2. | Other revenue is comprised of third-party commission income and management fees. Prior fiscal years were reformatted to include this immaterial adjustment. |

| 3. | A store is included in comparable store sales calculations at the beginning of its thirteenth full month of operation. Stores relocated, expanded or downsized are excluded from comparable store sales if the change in square footage is greater than 20% until the thirteenth full month following relocation, expansion or downsizing. Closed stores that were open for at least thirteen months are included in comparable store sales through the month immediately preceding the month of closing. |

| 20 |

Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Overview

Management’s Discussion and Analysis of Financial Condition and Results of Operations provide information that the Company’s management believes necessary to achieve an understanding of its financial condition and results of operations. To the extent that such analysis contains statements which are not of a historical nature, such statements are forward-looking statements, which involve risks and uncertainties. These risks include, but are not limited to, changes in the competitive environment for the Company’s merchandise, including the entry or exit of non-traditional retailers of the Company’s merchandise to or from its markets; releases by the music, video, and video game industries of an increased or decreased number of “hit releases”; general economic factors in markets where the Company’s merchandise is sold; and other factors including, but not limited to: cost of goods, consumer disposable income, consumer debt levels and buying patterns, consumer credit availability, interest rates, customer preferences, unemployment, labor costs, inflation, fuel and energy prices, weather patterns, climate change, catastrophic events, competitive pressures and insurance costs. discussed in the Company’s filings with the Securities and Exchange Commission. The following discussion and analysis of the Company’s financial condition and results of operations should be read in conjunction with “Item 6: Selected Consolidated Financial Data” and the Consolidated Financial Statements and related notes included elsewhere in this report.

During October 2016, the Company acquired all of the issued and outstanding capital stock of etailz, Inc. , an innovative and leading digital marketplace retail expert. See Note 7 to the Consolidated Financial Statements for additional information. Subsequent to this acquisition, reportable segments consist of fye and etailz. The etailz acquisition represents a significant step forward in the Company’s reinvention. The Company believes the rapid growth of marketplace sales will continue and is clear evidence of the explosive long-term trends underway in retailing. fye’s progress onboarding digital and marketing talent, accelerated through the etailz acquisition, will enable the Company to continue to build upon its credibility with fans of entertainment and pop culture. As of January 28, 2017, the Company operated 284 stores totaling approximately 1.6 million square feet in the United States, the District of Columbia and the U.S. Virgin Islands.

fye Segment

The U.S. entertainment retailing industry is a mature industry and continues to experience declines. Physical Video and Music represent approximately 50% of sales and both categories have been impacted by new distribution channels, including digital distribution and internet fulfillment. As a result, the Company has had negative comparable store sales for the past five years. To mitigate or lessen the impact these changes have had, the Company has focused on the following areas in an effort to improve its business:

Evolve the fye Brand Customer Experience.

The Company is evolving the fye brand experience by diversifying its merchandise assortment and enhancing its merchandise presentation as it continues its strategy towards becoming the most compelling entertainment and pop culture centric engagement in the marketplace. In addition, the Company offers personalized customer service in its stores guided by a commitment to approach every customer with gratitude, humility and respect.

Store Portfolio Evaluation

The Company’s real estate strategy is to maintain a core group of profitable locations, while evaluating opportunities for new locations in new and existing malls. During fiscal 2016, the Company opened 14 new and remodeled 10 existing fye stores under a new format which expands the merchandise selection and enhances the presentation of the trend and electronics categories while maintaining a strong presence in the media categories. As of January 28, 2017, the Company operated 34 stores under the new format.

| 21 |

During fiscal 2016 and fiscal 2015, the Company closed 29 and 19 stores, respectively. The Company closes stores when minimum operating thresholds are not achieved or upon lease expiration when either renewal is not available or management determines that renewal is not in the Company’s best interest. The Company has signed short-term lease agreements for desirable locations, which enables us to negotiate rents that are responsive to the then-current sales environment. We will continue to close stores that do not meet our profitability goals, a process which could result in asset impairments and store closure costs. Continued reduction in the number of stores would lower total sales.

The Company believes that there is near-term opportunity for improving the productivity of existing stores. The environment in which our stores operate is intensely competitive and includes Internet-based retailers and mass merchants. We believe a specialty retailer that can differentiate itself by offering a distinctive assortment and customer experience, and that can operate efficiently, will be better positioned to maintain or grow market share. Therefore, we remain dedicated to enhancing our merchandise assortment through introducing additional product lines, improving the operational efficiency of our stores and offering our customers a rewarding shopping experience guided by an approach to engage every customer with gratitude, humility and respect.

Expanding Customer Base

To strengthen customer loyalty, the Company offers its customers the option of signing up for a Backstage Pass card which provides an additional 10% discount off of everyday selling prices on nearly all products in addition to other value added benefits members receive through the program in exchange for a membership fee. The Company also co-sponsors events in many of its stores to provide various segments of its customers an opportunity to experience entertainment and shop for unique and exclusive products based on their particular interests.

etailz Segment

On October 17, 2016, the Company acquired all of the issued and outstanding capital stock of etailz, Inc., an innovative and leading digital marketplace retail expert. etailz uses a data driven approach to digital marketplace retailing utilizing proprietary software and ecommerce insight coupled with a direct customer relationship engagement to identify new distributors and wholesalers, isolate emerging product trends, and optimize price positioning and inventory purchase decisions. The etailz acquisition represents a significant step forward in Company’s reinvention. The Company believes the rapid growth of marketplace sales will continue and is clear evidence of the explosive long-term trends underway in retailing. fye’s progress onboarding digital and marketing talent, accelerated through the etailz acquisition, will enable the Company to continue to build upon its credibility with fans of entertainment and pop culture.

Key Performance Indicators

Management monitors a number of key performance indicators to evaluate its performance, including:

Net Sales and Comparable Store Net Sales: The Company measures the rate of comparable store net sales change. A store is included in comparable store net sales calculations at the beginning of its thirteenth full month of operation. Stores relocated, expanded or downsized are excluded from comparable store sales if the change in square footage is greater than 20% until the thirteenth full month following relocation, expansion or downsizing. Closed stores that were open for at least thirteen months are included in comparable store sales through the month immediately preceding the month of closing. The Company further analyzes net sales by store format and by product category.

Cost of Sales and Gross Profit: Gross profit is calculated based on the cost of product in relation to its retail selling value. Changes in gross profit are impacted primarily by net sales levels, mix of products sold, vendor discounts and allowances, shrinkage, obsolescence and distribution costs. Distribution expenses include those costs associated with receiving, inspecting and warehousing merchandise and costs associated with product returns to vendors.

Selling, General and Administrative (“SG&A”) Expenses: Included in SG&A expenses are payroll and related costs, occupancy charges, general operating and overhead expenses and depreciation charges (excluding those related to

| 22 |