Attached files

| file | filename |

|---|---|

| EX-32.2 - Immune Therapeutics, Inc. | ex32-2.htm |

| EX-32.1 - Immune Therapeutics, Inc. | ex32-1.htm |

| EX-31.2 - Immune Therapeutics, Inc. | ex31-2.htm |

| EX-31.1 - Immune Therapeutics, Inc. | ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2016

OR

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

For the Transition Period From ____________ to ____________

Commission File Number: 001-34918

IMMUNE THERAPEUTICS, INC.

(Exact name of registrant as specified in its charter)

| Florida | 59-3226705 | |

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) |

37

North Orange Ave, Suite 607,

Orlando, Florida 32801

(Address of principal executive offices)

(888) 613-8802

Registrant’s telephone number, including area code:

None

Securities Registered Pursuant to Section 12(b) of the Act:

Common Stock, par value $0.0001 per share

Securities Registered Pursuant to Section 12(g) of the Act:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter time that the registrant was required to submit and post such files). Yes [ ] No [X]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | [ ] | Accelerated filer | [ ] |

| Non-accelerated filer | [ ] (Do not check if a smaller reporting company) | Smaller reporting company | [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of voting stock held by non-affiliates of the registrant on June 30, 2016, the last business day of the registrant’s most recently completed second quarter, was $31,415,587, based on the last reported sale price of the registrant’s Common Stock on the OTC Markets on that date.

As of March 31, 2017, the registrant had outstanding 273,640,164 shares of common stock, $0.0001 par value per share.

IMMUNE THERAPEUTICS, INC.

2016 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

| 2 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained or incorporated by reference in this Annual Report on Form 10-K are considered forward-looking statements (within the meaning of the Private Securities Litigation Reform Act of 1995) concerning our business, results of operations, economic performance and/or financial condition, based on management’s current expectations, plans, estimates, assumptions and projections. Forward-looking statements are included, for example, in the discussions about:

| ● | strategy; | |

| ● | new product discovery and development; | |

| ● | current or pending clinical trials; | |

| ● | our products’ ability to demonstrate efficacy or an acceptable safety profile; | |

| ● | actions by the FDA and other regulatory authorities; | |

| ● | product manufacturing, including our arrangements with third-party suppliers; | |

| ● | product introduction and sales; | |

| ● | royalties and contract revenues; | |

| ● | expenses and net income; | |

| ● | credit and foreign exchange risk management; | |

| ● | liquidity; | |

| ● | asset and liability risk management; | |

| ● | the outcome of litigation and other proceedings; | |

| ● | intellectual property rights and protection; | |

| ● | economic factors; | |

| ● | competition; and | |

| ● | legal risks. |

Any statements contained in this report that are not statements of historical fact may be deemed forward-looking statements. Forward-looking statements generally are identified by the words “expects,” “anticipates,” “believes,” “intends,” “estimates,” “aims,” “plans,” “may,” “could,” “will,” “will continue,” “seeks,” “should,” “predict,” “potential,” “outlook,” “guidance,” “target,” “forecast,” “probable,” “possible” or the negative of such terms and similar expressions. Forward-looking statements are subject to change and may be affected by risks and uncertainties, most of which are difficult to predict and are generally beyond our control. Forward-looking statements speak only as of the date they are made, and we undertake no obligation to update any forward-looking statement in light of new information or future events, except as required by law, although we intend to continue to meet our ongoing disclosure obligations under the U.S. securities laws and other applicable laws.

We caution you that a number of important factors could cause actual results or outcomes to differ materially from those expressed in, or implied by, the forward-looking statements, and therefore you should not place too much reliance on them. These factors include, among others, those described herein, under “Risk Factors” and elsewhere in this Annual Report and in our other public reports filed with the Securities and Exchange Commission. It is not possible to predict or identify all such factors, and therefore the factors that are noted are not intended to be a complete discussion of all potential risks or uncertainties that may affect forward-looking statements. If these or other risks and uncertainties materialize, or if the assumptions underlying any of the forward-looking statements prove incorrect, our actual performance and future actions may be materially different from those expressed in, or implied by, such forward-looking statements. We can offer no assurance that our estimates or expectations will prove accurate or that we will be able to achieve our strategic and operational goals.

Forward-looking statements are based on information we have when those statements are made or management’s good faith belief as of that time with respect to future events, and are subject to significant risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to:

| ● | our lack of operating history; | |

| ● | our current and future capital requirements and our ability to satisfy our capital needs; | |

| ● | our inability to keep up with industry competition; | |

| ● | interpretations of current laws and the passages of future laws; | |

| ● | acceptance of our business model by investors and our ability to raise capital; | |

| ● | our drug discovery and development activities may not result in products that are approved by the applicable regulatory authorities. Even if our drug candidates do obtain regulatory approval they may never achieve market acceptance or commercial success; | |

| ● | our reliance on key personnel, including our ability to attract and retain scientists; | |

| ● | our reliance on third party manufacturing to supply drugs for clinical trials and sales; | |

| ● | our limited distribution organization with no sales and marketing staff; | |

| ● | our being subject to product liability claims; | |

| ● | our reliance on key personnel, including our ability to attract and retain scientists; | |

| ● | legislation or regulation that may increase the cost of our business or limit our service and product offerings; | |

| ● | risks related to our intellectual property, including our ability to adequately protect intellectual property rights; | |

| ● | risks related to government regulation, including our ability to obtain approvals for the commercialization of some or all of our drug candidates, and ongoing regulatory obligations and continued regulatory review which may result in significant additional expense and subject us to penalties if we fail to comply with applicable regulatory requirements; and | |

| ● | our ability to obtain regulatory approvals in foreign jurisdictions to allow us to market our products internationally. |

Moreover, new risks regularly emerge and it is not possible for our management to predict or articulate all risks we face, nor can we assess the impact of all risks on our business or the extent to which any risk, or combination of risks, may cause actual results to differ from those contained in any forward-looking statements. All forward-looking statements included in this prospectus are based on information available to us on the date of this Annual Report. Except to the extent required by applicable laws or rules, we undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained above and throughout this Annual Report.

| 3 |

JUMPSTART OUR BUSINESS STARTUPS ACT

We qualify as an “emerging growth company” as defined in Section 101 of the Jumpstart our Business Startups Act (“JOBS Act”) as we do not have more than $1,000,000,000 in annual gross revenue and did not have such amount as of December 31, 2016, the last day of our last fiscal year. We are electing to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(1) of the JOBS Act.

As an emerging growth company, we are permitted to, and intend to, rely on exemptions from certain disclosure requirements that are otherwise applicable to public companies. These provisions include, but are not limited to:

| ● | being permitted to present only two years of audited financial statements and only two years of related “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this annual report; | |

| ● | not being requested to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, as amended (“Sarbanes-Oxley Act”); | |

| ● | reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements and registration statements; and | |

| ● | exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. |

We will remain an emerging growth company until the earliest to occur of: (i) our reporting $1 billion or more in annual gross revenues; (ii) the end of fiscal year 2019; (iii) our issuance, in a three year period, of more than $1 billion in non-convertible debt; and (iv) the end of the fiscal year in which the market value of our common stock held by non-affiliates exceeded $700 million on the last business day of our second fiscal quarter.

| 4 |

Company Overview

Immune Therapeutics, Inc. (the “Company”) was initially incorporated in Florida on December 2, 1993 as Resort Clubs International, Inc. (“Resort Clubs”). It was formed to manage and market golf course properties in resort markets throughout the United States. Galliano International Ltd. (“Galliano”) was incorporated in Delaware on May 27, 1998 and began trading in November 1999 through the filing of a 15C-211. On November 10, 2004, Galliano merged with Resort Clubs. Resort Clubs was the surviving corporation. On August 23, 2010, Resort Clubs changed its name to pH Environmental Inc. (“pH Environmental”).

On April 23, 2012, pH Environmental completed a name change to TNI BioTech, Inc., and on April 24, 2012, we executed a share exchange agreement for the acquisition of all of the outstanding shares of TNI BioTech IP, Inc. On September 4, 2014, a majority of our shareholders approved an amendment to our Amended and Restated Articles of Incorporation, as amended, to change our name to Immune Therapeutics, Inc. We filed our name change amendment with the Secretary of State of Florida on October 27, 2014 changing our name to Immune Therapeutics, Inc.

The Company currently operates out of Orlando, Florida. In July 2012, the Company’s focus turned to acquiring patents that would protect and advance the development of new uses of opioid-related immune- therapies, such as low dose naltrexone (“LDN”) and Methionine [Met5]-enkephalin (“MENK”). The Company’s therapies are believed to stimulate and/or regulate the immune system in such a way that they provide the potential to treat a variety of diseases. We believe our therapies may be able to correct abnormalities or deficiencies in the immune system in diseases such as HIV infection, autoimmune disease, immune disorders, or cancer; all of which can lead to disease progression and life-threatening situations when the immune system is not functioning optimally.

In October 2012, the Company formed TNI BioTech International, Ltd., a BVI company in Tortola, British Virgin Islands, which was set up to allow the Company to market and sell LDN in those countries outside the U.S. in which we have been able to obtain approval to sell the Company’s products.

In August 2013, the Company formed its United Kingdom subsidiary, TNI BioTech, LTD (the “UK Subsidiary”). The UK Subsidiary received approval to be considered a micro, small or medium-sized enterprise (“SME”) with the European Medicines Agency (“EMA”) on August 21, 2013. The designation provides the UK Subsidiary with significant discounts when holding meetings or submitting filings to the EMA. On September 19, 2013, the UK Subsidiary submitted a pre-submission package to the EMA regarding Crohn’s Disease. The EMA granted the UK Subsidiary a meeting that took place on September 27, 2013. The UK Subsidiary is eligible to benefit from the provisions for administrative and financial assistance for SMEs set out in Regulation (EC) No 2049/2005. The Company will apply to obtain EMA benefits once funding becomes available.

In December 2013, the Company formed a new subsidiary, Cytocom Inc., to focus on conducting LDN and MENK clinical trials in the United States. In December 2014, the Company finalized the distribution of common stock of Cytocom Inc. to its shareholders. As part of the transaction, the Company retained exclusive rights to all international patents, in-country approvals, formulations, trademarks, manufacturing, marketing, sales, and distributions rights in emerging nations, including Africa, Central America, South America, Russia, India, China, Far East, and The Commonwealth of Independent States (former Soviet Union). The Company will continue to have access to existing clinical data as well as any new data generated by Cytocom Inc. during drug development. On December 8, 2014, the number of Cytocom Inc. shares of common stock that were issued to our shareholders totaled 113,242,522 shares. In connection with the transaction, Cytocom Inc. issued 140,100,000 shares of its common stock to the Company, which gave the Company a 55.3% stake in Cytocom Inc. on that date. In April 2016, the Board of Directors and a majority of shareholders of Cytocom approved a reverse stock split of Cytocom’s outstanding common stock with one new share of stock for each twenty old shares of common stock. Cytocom effectuated and finalized the reverse split in June 2016. At December 31, 2016, the Company’s equity interest had been further reduced to 13%, by subsequent issuances of Cytocom common stock to shareholders in settlement of notes payable.

| 5 |

In March 2014, the Company incorporated Airmed Biopharma Limited, an Irish corporation with an address in Dublin, Ireland, and Airmed Holdings Limited, an Irish company domiciled in Bermuda. The Irish companies were set up to benefit from incentives granted by the Irish government for the establishment of pharmaceutical companies (many of the world’s leading pharmaceutical companies have located in Ireland), and so that the Company could take advantage of Ireland’s status as a member of the European Union and the European Economic Area. An Irish limited liability company enjoys a low corporate income tax rate of 12.5%, one of the lowest in the world. The Irish-domiciled company hopes to qualify for tax incentives for Irish holding/headquartered companies and to benefit from the network of double tax treaties that reduce withholding taxes. TNI BioTech International, Ltd. will manage our international distribution, using product that is manufactured in Ireland and elsewhere.

Today, Immune Therapeutics is focused on the commercialization of affordable non-toxic immunotherapies focused on the activation and rebalancing of the body’s immune system. Stimulating the body’s immune system remains one of the most promising approaches in the treatment of Cancers, HIV, Autoimmune Diseases, inflammatory conditions and other opportunistic infections for chronic often life-threatening diseases through the mobilization of the body’s immune system in Emerging Nations using existing clinical data.

Cytocom Inc, is a clinical-stage pharmaceutical company focused on the development of the first affordable non-toxic immunodulator for the treatment of inflammatory diseases, immune-related disorders, and cancer and is responsible for the development of our patented therapies with the FDA and EMA.

As of this date, neither we nor our collaboration partners are permitted to market our drug candidates in the United States until we receive approval of a New Drug Application from the FDA. Neither we nor our collaboration partners have submitted an application for or received marketing approval for any of our drug candidates. Obtaining approval of an NDA can be a lengthy, expensive and uncertain process.

Some of the Company’s more substantial risks include, but are not limited to, its lack of operating history, its high needs for capital, strict government regulation, risk of law suits from trial participants and otherwise, requirement for drug approvals which may never occur, changes in the industry, failure of the Company’s products to make it through trials, reliance on third parties to conduct trials and manufacture and distribute the Company’s drugs, and fierce competition. All of these factors and more could affect investors’ investments in the Company.

The Company’s technology platform is built surrounding two different immune therapies, IRT-103, low dose naltrexone herein sometimes referred to as “LDN” or “Lodonal™” or IRT-101, herein sometimes referred to as Methionine-Enkephalin or “MENK.” Both therapies have been decades in the making, over forty clinical trials run by institutions such as the Pennsylvania State University Medical School at Hershey, University of Chicago, State University of New York, and Multiple Sclerosis Center at UCSF. When the Company acquired the assets from the either the patent holder or licensee we also acquired the rights to the clinical data, orphan drug designations and IRB. The Company has completed one trial in Nigeria for Lodonal™ and has a second trial underway for cervical cancer in Malawi. The Company has also submitted briefing packaged to the FDA for a phase IIB/III trial for IRT-103 for Crohn’s Disease and is preparing a new briefing package for IRT-103 for pancreatic cancer. In addition to the work in the United States we have been completing pre-clinical and clinical work for IRT-013 with Professor Shan at the School of Immunology in China.

LDN

The Company has branded our Immediate Release Low Dose Naltrexone as IRT-103TM when working with the FDA and EMA and trademarked our product in Africa as LodonalTM. Lodonal™ with an immediate release 4.5mg formulation of Naltrexone is the brand name for our HIV treatment. LDN can be any formulation between .05 and to 10mg and may or may not be immediate release and may be an oral or liquid formulation.

The FDA approved naltrexone HCl in 1984 for the treatment of opioid addiction. The typical daily dosage for opioid addiction is 50mg to 100mg, and 50mg tablets are available commercial. There is no FDA-approved use for naltrexone at any lower dosage then 50mg for the treatment of any other medical conditions or treatments.

| 6 |

Where high dose Naltrexone at 50mg to 100mg and Slow release Naltrexone between .01mg and 10mg and Immediate Release Naltrexone between .01mg and 10mg share commonality” in categories of genes and are considered the same drug the difference in dosing and delivery method (immediate release) difference in the overall response to the immune system. There is a difference in the cell patterns of genes that are altered by the treatment of immediate release naltrexone verses high does naltrexone and slow release low naltrexone between .01mg and 10mg. The differences are important because immediate release naltrexone between .01 and 10mg acts as an immunomodulator.

Since immediate release naltrexone blocks the opiate receptors only for a few hours before it is naturally excreted, what results is a rebound effect; in which both the production and utilization of methionine-enkephalin or opiate growth factor are increased. Once the immediate release naltrexone has been metabolized, the elevated endorphins produced as a result of the rebound effect can now interact with the more sensitive and more-plentiful receptors and assist in regulating cell growth and immunity. There is no rebound effect with either high dose naltrexone or slow release naltrexone and it is the rebound immunomodulatory effect that effects the treatment of treating patients suffering from human immunodeficiency virus (HIV) acquired immune deficiency syndrome (AIDS, autoimmune disease, opportunistic infections, cancer, inflammation, and neurodegenerative diseases

It has been demonstrated in trials that in the presence of LDN, the numbers of T-cells, both CD4+ helper T cells and CD8+ cytotoxic T cells, may increase by more than 300%.

The Mechanism of Action of immediate release LDN is not fully understood at this time, but based on clinical work there are three current theoretical models for how immediate release LDN works in autoimmune disease, inflammatory disease, cancer and HIV/AIDS.

Immediate Release LDN, which is different from either slow or extended release LDN, works by triggering a number of receptors including (1) the opioid and T Cell receptors on immune cells which activate or balance various cells of the immune system, and (2) tolling receptors to shift Th1 (pro-inflammatory) to Th2 (anti-inflammatory) which is critical when dealing with autoimmune and inflammatory disease. (1) Increases the production of cytokines specifically an endorphin referred to as Methionine-enkephaline or OGF.

These compounds then produce pain relief similar to opiates. The body responds to these compounds by inhibition of cell growth, promoting healing, and reducing inflammation, all in an effort to restore homeostasis. IRLDN also causes increase in OGF receptor.

Regulatory applications submitted, if any, to commence clinical trials and the current status of such applications.

Clinical trials under the INDs are anticipated to be conducted in the United States and the EU.

| IND # | Indication | Product Name | Sponsor | Status | ||||

| 34,442 | HIV/AIDS | MENK (IRT-101) | Dr. Ronald Herberman and Dr. Bernard Bihari | Inactive; filed in 1997 (1) | ||||

| 67442 | Crohn’s Disease | Naltrexone HCL (IRT-103) | Dr. Jill Smith | Active; filed May 31, 2003 and filed with the FDA in March, 2013 | ||||

| 50987 | Pancreatic Cancer | MENK (IRT-101) | Dr. Jill Smith | Active; was filed with the FDA in March, 2013 |

| (1) | Currently inactive but will soon be reactivated and transferred to TNIB. |

Immune Therapeutics, Inc. Drug Development Plan

Nigeria

Immune Therapeutics Inc., through its wholly owned subsidiary TNI BioTech Intl., completed a 90-day bridging trial for the treatment of patients with HIV/AIDS in Nigeria. The National Agency for Food and Drug Administration and Control (NAFDAC) approval is based on previous clinical data and the Nigeria Bridging Trial was a single center, open labeled, randomized, bridging study. The trial consisted of a total of one hundred and fifty [150] patients of both genders between the ages of 18-60, each of whom was infected with the human immunodeficiency virus (HIV).

| 7 |

The 90-Day Bridging Trial was undertaken at the State Specialist Hospital in Asubiaro, Osogbo, Osun State, Nigeria and the primary objective of this Bridging Trial was to confirm that LodonalTM has a beneficial effect on the immune system of immune deficient patients and that it is safe. The trial separated the patients into a Control (placebo) Group and a Treatment Group (which was administered LodonalTM). The efficacy of increasing CD4 count [cell/mm3] between Day-1 and Day-90 by at least 25% was set as the criteria for demonstrating beneficial effect on the immune system. Safety was demonstrated through quality of life assessment and vitals both of which were not adversely affected. Treatment Group patients were given a daily dose of 4.5-mg/kg of Lodonal™.

The results yielded an average increase of 44% increase in CD4 count in the Lodonal Treatment Group compared to an 11% increase in the Control Group. Additionally, there were no reported opportunistic infections and no toxicity levels uncovered. Liver function remained normal and there was no negative impact on other systems based on blood results. No sleep disturbance or vivid dreams were present enough to justify trial discontinuation. No appreciable adverse CNS, renal, cardiac, hepatic, musculoskeletal, hematopoietic side effects were present.

NAFDAC has issued approval of Lodonal™as an immune system regulator in the management of HIV patients and the company is now in the process of completing the registration to import the drug into Nigeria.

Malawi

The Company, through its wholly owned subsidiary TNI BioTech International, received permission from the Pharmacy, Medicines and Poisons Board (PMPB) and The College of Medicine; University of Malawi to initiate a clinical trial for a Single Visit Approach to Cervical Cancer Prevention in the Republic of Malawi. The PMPB issued drug approval to import the drug in 2015.

The Malawi Clinical Trial’s primary endpoint includes Safety, Acceptability, and Feasibility of a Single Visit Approach to Cervical Cancer Prevention in patients. (Trial number: VIA-LDN-401 -0 I). The secondary objectives’ is to determine life extension; to improve the immune system of HIV and Cancer positive patients by starting treatment with LDN (“LodonalTM”) and to ensure marked improvement in Clinical benefit based upon parameters that reflect the overall well- being of the patient, including Pain control, performance status, and body weight under the supervision of Dr. Frank Taulo, Dr. Gladys Gadama, Dr. Effie Chipeta as Principal Investigators. The recruitment of study participants, testing and follow up is still on-going. The first evaluation report from the doctors involved is expected by the end of April 2017 as per the study protocol.

The Company intends to initiate a number of additional trials in Africa in the next 6 months, which will include trials as an adjunct to chemotherapy in Kenya and Ghana and HIV/AIDS in Malawi.

FDA and EMA Development Plan for Cytocom, Inc.

After the completion of the spin-off of our subsidiary, Cytocom, Inc., to shareholders, all work with the FDA, EMA or any of the G7 countries will be under the supervision of Cytocom Inc. However, the Company plans to submit all trials and fees on Cytocom Inc.’s behalf until such time as Cytocom, Inc. is sufficiently funded, as all funding is currently being provided through the Company. Nonetheless, the trials will be supervised by Cytocom, Inc. following submission by the Company. At this time the INDs have not been transferred to Cytocom; however they will be transferred before the trials begin. Studies and trials in countries that are not part of the G7 are being conducted directly by the Company.

Our lead product candidate is IRT-103 ™, a first-in-class, proprietary fixed-dose therapy entering Phase 2b clinical trials for the treatment of adult and pediatric Crohn’s disease where we have orphan drug designation. The Company acquired all of the clinical data from Dr. Jill Smith in conjunction with the acquisition of the license. The Company had no direct involvement in the trials.

Crohn’s disease affects over 1.6 million adults in the United States and an estimated 80,000 children. Data from the Phase 2a clinical trial indicate that Lodonal™ was generally well-tolerated therapy that can provide promise for the treatment of Crohn’s disease. The Department of Medicine at The Pennsylvania State University, (PSU) College of Medicine, GI Medicine were responsible for three of the Crohn’s trials that were part of our briefing package to the FDA.

| 8 |

PSU researchers have demonstrated in a mouse model of Crohn’s disease from with dextran sodium sulfate (a chemically induced colitis) that opioid receptor blockade by a low dose of naltrexone resulted in less weight loss, lower disease activity index scores and less histological evidence of inflammation when compared to controls (Matters, GL et al., 2008). Furthermore, the researchers demonstrated that tissue inflammatory cytokine mRNA was reversed to baseline levels in the colons of mice treated with naltrexone.

A Phase 2 trial with low-dose naltrexone was completed on patients with Crohn’s Disease and the objective of the trial was to determine the role of endogenous opioids and opioid antagonists in healing and repair of tissues. Eligible subjects with histologically and endoscopically confirmed active Crohn’s disease activity index (CDAI) score of 220–450 were enrolled in a study using 4.5 mg naltrexone per day. Infliximab was not allowed for a minimum of 8 weeks prior to study initiation. Other therapy for Crohn’s disease that was at a stable dose for 4 weeks prior to enrollment was continued at the same doses. Patients completed the inflammatory bowel disease questionnaire (IBDQ) and the short-form (SF-36) quality of life surveys and CDAI scores were assessed pre-treatment, every 4 weeks while on therapy and 4 weeks after completion of the study. The drug was administered by mouth each evening for a 12-week period. Seventeen patients with a mean CDAI score of 356 °æ 27 were enrolled. CDAI scores decreased significantly (P = 0.01) with LDN, and remained lower than baseline 4 weeks after completing therapy. Eighty-nine percent of patients exhibited a response to therapy and 67% achieved a remission (P < 0.001). Improvement was recorded in both quality of life surveys with LDN compared with baseline. No laboratory abnormalities were noted. The most common side effect was sleep disturbances, occurring in seven patients. The trial concluded that LDN therapy appears effective and safe in subjects with active Crohn’s disease.

Another Phase 2 trial therapy was conducted, entitled, Therapy with the Opioid Antagonist Naltrexone Promotes Mucosal Healing in Active Crohn’s Disease: A Randomized Placebo-Controlled Phase 11 trial at the Department of Medicine, The Pennsylvania State University, College of Medicine, GI Medicine [Smith, JP. et al, 2011]. Aims – A randomized double-blind placebo-controlled study was designed to test the efficacy and safety of an opioid antagonist for 12 weeks in adults with active Crohn’s disease. The phase 2A trial had 3 major endpoints for the study including: 1) Clinical improvement based upon the Crohn’s Disease Activity Index (CDAI) Score, 2) Mucosal healing by colonoscopy, and 3) Safety. The human studies were done with FDA approval under IND 67442. Forty subjects with active Crohn’s disease were enrolled in the study. Randomized patients received daily oral administration of 4.5-mg naltrexone or placebo. Providers and patients were masked to treatment assignment. The primary outcome was the proportion of subjects in each arm with a 70-point decline in Crohn’s Disease Activity Index (CDAI) score. The secondary outcome included mucosal healing based upon colonoscopy appearance and histology. Eighty-eight percent of those treated with naltrexone had at least a 70-point decline in CDAI scores compared to 40% of placebo-treated patients (p = 0.009). After 12 weeks, 78% of subjects treated with naltrexone exhibited an endoscopic response as indicated by a 5-point decline in the Crohn’s disease endoscopy index severity score (CDEIS) from baseline compared to 28% response in placebo-treated controls (p = 0.008). 33% achieved remission with a CDEIS score <6, whereas only 8% of those on placebo, showed the same change. Fatigue was the only side effect reported that was significantly greater in subjects receiving placebo. The study concluded that Naltrexone improves clinical and inflammatory activity of subjects with moderate to severe Crohn’s Disease compared to placebo-treated controls. Strategies to alter the endogenous opioid system provide promise for the treatment of Crohn’s Disease.

A pilot study was completed entitled Safety and Tolerability of Low-dose Naltrexone Therapy in Children With Moderate to Severe Crohn’s Disease trial at the Department of Medicine, The Pennsylvania State University, College of Medicine, GI Medicine Smith, (JP. et al, 2013). The aims of this study were to evaluate the safety and tolerability of an opioid antagonist, naltrexone, in children with moderate to severe Crohn’s disease. The pilot clinical trial was conducted in children with moderate to severe Crohn’s disease. Fourteen subjects with a mean age of 12.3 years (range, 8 to 17 y) were enrolled. Children were randomized to placebo or naltrexone (0.1 mg/kg) orally for 8 weeks followed by open-labeled treatment with 8 additional weeks of naltrexone. Safety and toxicity were monitored by physical examinations and blood chemistries. Clinical activity was assessed by the Pediatric Crohn’s Disease Activity Index (PCDAI) and Quality of life was monitored by the Impact III survey. The results indicated that oral naltrexone was well tolerated without any serious adverse events in children with moderate to severe Crohn’s disease. PCDAI scores decreased from pre-treatment values (34.2Å 3.3) with an 8-week course of naltrexone therapy (21.7Å 3.9) (P=0.005). Twenty-five percent of those treated with naltrexone were considered in remission (score r10) and 67% had improved with mild disease activity (decrease in PCDAI score by at least 10 points) at the end of the study. Systemic and social quality of life improved with naltrexone treatment (P=0.035). The study concluded that naltrexone therapy seems safe with limited toxicity when given to children with Crohn’s disease and may reduce disease activity.

| 9 |

Food And Drug Administration

There are three types of meetings with the FDA: Type A Meeting – is a meeting that is “immediately necessary for an otherwise stalled drug development program to proceed.” This type of meeting refers to meetings to resolve disputes, talk about clinical holds, special protocols. Type B Meetings are identified as (1) pre-IND meetings, (2) certain end of Phase I meetings, (3) end of Phase 2/pre-Phase 3 meetings and (4) pre-NDA/BLA meetings. A type C Meeting is any other kind of meeting.

The Company attended a Type C meeting with the FDA June 26, 2013 with the Division of Gastroenterology and Inborn Errors Products regarding the clinical and regulatory aspects of the proposed Phase IIB/III development program and future 505(b)(2) application for Low Dose Naltrexone (LDN) in the treatment of adults and pediatric patients with Crohn’s Disease. In principal the FDA agreed that a 505(b)(2) application would be an acceptable approach at FDA recommends that sponsors considering the submission of an application through the 505(b)(2) pathway consult FDA’s regulations at 21 CFR 314.54, and the draft guidance for industry Applications Covered by Section 505(b)(2) (October 1999). The Company is planning to submit a request for “breakthrough technology” designation. If this request is granted, what impact could it have on minimizing the Phase 3 study design(s) and the package needed for filing the 505(b)(2) application.

The Company retained the services of Cote Orphan to provide a new briefing package and work with the Division for Breakthrough Therapy Designation is granted to determine the most efficient development program for your product and proposed indication. The Company notes that a 505(b)(2) NDA will need to be submitted with all the same components that a regular NDA requires. The Company hopes to submit our briefing package to the FDA because CDAI was previously been accepted by the FDA for phase 3 trials in CD, FDA has reconsidered the use of the CDAI as a measure of clinical response to therapeutic intervention and we our new trial design endpoint will include endoscopies to show true mescal healing. The Company delayed submitting our new briefing package to the FDA as a number of changes were under consideration at the FDA in connection with 505(2)(b) pathway drug development. The Company has recently begun to make final changes to the briefing package, and expects to present its new briefing package to the FDA before the end of the third quarter 2017, with a meeting shortly thereafter.

Anticipated developmental timelines for Cytocom, Inc.

Guidance meeting held with FDA regarding pediatric and adult studies provided feedback and based on the new submission of a briefing package we anticipate presenting final protocols for both adult and pediatric trial.

| ● | Current development plan includes: |

| ● | Two adult studies planned: |

| ● | Double-blind, randomization, 24-week study of LDN vs. Placebo at 4.5mg |

| ● | Double-blind, randomization 12-week multi-dose study including 4.5mg |

| ● | Both studies will roll-over to an open label |

| ● | Studies to commence Q1 2017 |

| ● | Two pediatric studies |

| ● | Double-blind randomization, 24 week study of LDN vs. Placebo at |

| ● | Both studies will roll-over to open label |

| ● | Studies to commence Q1 of 2017 |

Competitive Advantage

The Company believes many of the same advantages of our therapies apply to both the US market as well as the African market. LodonalTM could provide the first affordable, non-toxic approach for treatment of immune dysfunction, cancer and d chronic inflammatory state.

| 10 |

Some of the Competitive Advantages and Benefits of LodonalTM include the following:

Lower production costs and sales price of treatments

Today the majority of the drugs under development are both more expensive and more toxic. We do not believe this is the right way to move forward. Biologic agents cost between $12,000 and $150,000 a year.

LodonalTM/ IRT-103 can be manufactured and delivered in Emerging Nations for under $.90 cents a day and we estimate a price of $3,600 dollars a year in developed country underwritten to $10 to $15 dollars per month and when not underwritten the company will provide to patients for $30 dollars a month.

Lodonal™ should be able to substantially reduce health care costs for a number of reasons:

| ● | IRT-103 and Lodonal™ can provides a new, non-toxic inexpensive method of medical treatment by mobilizing the natural defenses of one’s own immune system. It can be used as a stand-alone therapy or an adjunct to existing immunosuppressive therapies by reducing the toxic side effects of immunosuppressive drugs. |

| o | Patients who are taking immunosuppressant drugs should see their doctor on a regular basis to monitor the patient for unwanted side effects. |

| ● | Lodonal™ does not require the medical supervision of antiretroviral or immunosuppressive therapies. |

| o | Immunosuppressive drugs are very powerful and can cause such serious side effects as high blood pressure, kidney problems, malignancies and liver disorder. Immunosuppressant drugs lower a person’s resistance to infection and can make infections harder to treat. The drugs can also increase the chance of uncontrolled bleeding. |

| ● | Lodonal™ has no toxic side effects as it is an immunomodulator and activates and re-balances the immune system. |

| o | HIV as a Chronic Disease: For reasons that remain to be elucidated, antiretroviral-treated HIV disease is associated with a new constellation of problems, generally referred to as “non-AIDS morbidity”, and, in the popular press, “premature aging” |

| ● | Health care systems in those regions where most people with HIV reside (e.g., sub-Saharan Africa) were designed to provide acute care only and are ill equipped to provide the chronic care, which is now required to manage HIV. |

| ● | Lodonal as an immunomodulator has a way of helping what is now referred to as “non-AIDS morbidity”, and, in the popular press, “premature aging”. |

| ● | Blocks release of proinflammatory cytokines including Interleukins IL6 and IL12, TNFα, NF-ĸB (nuclear factor kappa light chain enhancer of activated B cells) |

| ● | Modulates T and B lymphocyte production and cause Shift from Th1 (pro-inflammatory) to Th2 (anti-inflammatory) |

| ● | Affects microglia – macrophages/ 1st line of immune defense in CNS; normally quiescent; |

| ● | Cell death, inflammation, infection à Activated microglia à increase in proinflammatory cytokines, excitatory amino acids, and nitric oxide |

| ● | (NO); Increased NFkB à additional proinflammatory cytokines that act on neurons to create pain, fatigue, etc.; Naltrexone suppresses microglial activation; |

| ● | Low dose naltrexone (LDN) enhances maturation of bone marrow dendritic cells (BMDCs) |

| ● | Reduces inducible nitric oxide synthase activity à decreased peroxynitrite formation à glutamate transporters inhibited |

| ● | Excitatory neurotoxicity of glutamate on neuronal cells and oligodendrocytes is prevented |

| ● | Apoptosis of oligodendrocytes reduced |

| ● | Downregulates NFk2, inflammatory cytokines (TNF, IL-1, IL-6) |

| 11 |

| ● | These are all immune system changes associated with aging, which potentially can be improved by Lodonal, which will improve the quality of life for HIV/AIDS patients and reduce the health care burden on the medical system. |

| o | Avoiding contact with people who have infections is also important. In addition, people who are taking or have been taking immunosuppressant drugs should not have such immunizations as smallpox vaccinations without consulting their physician. Because their resistance to infection has been lowered, people taking these drugs might get the disease that the vaccine is designed to prevent. People taking immunosuppressant drugs should avoid contact with anyone who has had a recent dose of oral polio vaccine, as there is a chance that the virus used to make the vaccine could be passed on to them. |

| ● | Lodonal™ has no toxic side effects. |

| ● | LodonalTM does not compromise the immune system. |

| o | Indirect Cost of Immunosuppressive drugs |

| ● | HIV/AIDS still ranks 5th among the 14 diseases, with indirect per person costs ranging from $890 to $2663 in Zaire and from $2425 to $5903 in Tanzania indirect costs are roughly 95% of the total costs which are not covered by donor dollars. |

| ● | The total economic burden of CD was $10.9-15.5 billion in the United States and euro 2.1-16.7 billion of which is approximately 30% to 50% are indirect cost. |

| ● | Lodonal™ has been shown to reduce the number of opportunistic infections with HIV/AIDS |

Lodonal™ can improve compliance. When used correctly, antiretroviral therapy (ART) is effective. However, according to recent studies, ART regimens require 70–90% adherence in order to be effective. Sustaining adherence to ART over the long term requires accurate and consistent monitoring, and this is a particular challenge for countries in sub-Saharan Africa.

| o | Lodonal is a simple, once-daily regimen, which can be taken with or without a food, |

| o | Occasional non-compliance will not affect the overall success therapy. |

| o | Does not require the medical supervision of antiretroviral or immunosuppressive therapies (people will not lose time from work). |

| o | Compliance is further challenged by various social and clinical obstacles, where inadequate suppression of viral replication by ART are resulting due to poor adherence to therapy, low potency of the antiretroviral regimens and viral resistance to antiretroviral medications. |

| o | Estimates suggest that the average rates of non-adherence to antiretroviral therapy range from 50% to 70%. |

| o | Due to lack of compliance, the transmissibility of the antiretroviral resistant viruses from person to person further compounds the problem as a clinical and public health challenge. Which continues to be one of the major problems with treatment around the world. |

Our lead product candidate with the FDA is IRT-103 and is posed to initiate a pivotal phase IIB/III clinical trial for moderate-to-severe adult Crohn’s disease as well for pediatric Crohn’s disease, an orphan indication. We will need to complete both a Phase 2B and Phase 3 clinical trial for both Pediatric and Adult Crohn’s Disease for IRT-103 before we can obtain final approval to market the drug in the U.S. from the FDA.

The Company seeks to benefit patients with chronic and often life-threatening diseases through the stimulation and/or regulation of the body’s immune system. Using our patented immunotherapy, management believes that the Company’s products, technologies and patents will harness the power of the immune system to improve the treatment of cancer, HIV/AIDS, autoimmune diseases, opportunistic infections and inflammatory disorders.

Recent Accomplishments

The Company obtained drug approval from NAFDAC (National Agency for Food and Drug Administration and Control) in April of 2016. In May the Company began the regulatory process with NAFDAC for marketing authorization. There were a number of steps the Company is required to complete before marketing approval will be granted despite the current approval of Lodonal™ as a treatment of immune deficiency by NAFDAC.

| 12 |

The Company is currently completing the regulatory process to begin marketing the drug in Nigeria. Beginning in July of 2016 NAFDAC began requiring a manufacturing site inspection before authorizing the marketing of any new products, including Lodonal™.

On October 3, 2016 the Company received a letter from NAFDAC requesting a site visit of our manufacturing facility as the final step in regulatory marketing approval. Upon completion of the site visit the Company expects to receive marketing approval shortly thereafter.

The Company has been informed that the Nigerian approval allows the company to use the approval to be “fast tracked” for approval in the Economic Community of West African States, a regional group of sixteen countries, of which Nigeria is a member. The countries include Benin, Burkina, Faso, Cote d’Ivoire, Gambia, Ghana, Guinea-Bissau, Liberia, Mali, Nigeria, Senegal, Sierra Leone, and Togo. These countries play a major role in our Africa development strategy, as they are part of the “Test and Treat Program” for West and Central Africa. While the trend in international health funding for HIV/AIDS and ART (Antiretroviral Therapy) and the policies that drive the funding, has been to focus on high-burden countries and HIV ‘hotspots’ in Sub-Saharan Africa, most countries in the region classified by the UN as the West and Central Africa (WCA) region have been neglected. In the WCA region, 76% of those who need antiretroviral therapy – a total of five million people – are still awaiting treatment. The unmet needs in most of these countries are slipping further out of focus and we believe that Lodonal™ could help the people of West and Central Arica.

In September of 2016, the company retained the services of GLOBALMEDLINE SARL in Senegal to assist the drug registration of Lodonal™ in Senegal for HIV/AIDS and Cancer. The filing in Senegal is part of the company’s program to register Lodonal™ throughout the francophone (French-speaking) countries in Africa using our approval in Senegal to fast track the process.

The Company is currently in the process of filing in Kenya, Ghana, Liberia, Mali and Uganda. We will be adding additional countries in 2017.

In September of 2016 the Company signed a consulting agreement with the Honorable Joyce Banda as a member of the Champions for an AIDS Free Generation. His Excellency Festus Mogae, the Former President of the Republic of Botswana, first launched The Champions in 2008. The Champions program works to ensure that all children are born free from HIV in Africa and that all people have access to quality HIV prevention and treatment services.

The Company has been assigned three provisional patent applications: No. 62/296,759, a Method for Inducing a Sustained Immune Response; No. 62/379,272, a Method for Treating and Preventing Protozoan Infection; and No. 62/450,635, Methods and Compositions Useful for Treating Cancer Application. The Company expects to file additional patent applications in the coming months. Our intellectual property portfolio includes biotech assets acquired either through acquisition or exclusive licensing. The Company converted the provisional patent for method for inducing immune response into a US patent, and a PCT application was filed on February 17, 2017 under number PCT/IB2017/000124.

The Company has retained the services Coté Orphan to assist in obtaining FDA and EMEA approvals. Cote Orphan is a boutique, full-service, lab-to-market regulatory group focused on Orphan Drugs. Team Coté is led by Dr. Tim Coté, the former Director of the FDA’s Office of Orphan Products Development (OOPD). Dr. Cote is currently working with the Company to file a briefing package and final protocols for adult and pediatric Crohn’s Disease. The Company expects to finish this process by the end of the second quarter of 2017. The Company has delayed its request for a Type B meeting with the FDA on Crohn’s Disease, as the FDA is in the process of making changes in a number of areas as it applies to both 505(2)(b) pathway development and paediatric trials. The Company is preparing its final submission and expects to have the briefing package ready in the next 90 days.

The Company recently submitted its application for drug approval in Senegal and Kenya, and expects to have responses from the regulatory authorities by the end of the fourth quarter of 2017.

The Company’s Board has authorized continued discussions with a number of potential partners in Far East as well as discussion with drug development partners in both the US and EU.

| 13 |

MENK

MENK, also herein referred to as IRT-101, opiate growth factor or OGF, and Methionine-enkephalin is a synthetic peptide that activates natural killer (“NK”) cells of the immune system to seek and destroy cancer cells of the immune system to seek and destroy cancer cells. IRT-101 is a small peptide normally made by nerve cells and immune cells.

Further work in the laboratories of Plotnikoff, et al. has shown that daily injection of enkephalins into mice for 1 week resulted in increases in the size and weight of the thymus gland and a concomitant decrease in size and weight of the spleen. These observations led the same workers to study the antitumor action of the enkephalins. Mice carrying L 1210 tl.~mor cells were treated with methionine and leucine enkephalins, and their survival was compared to placebo treated controls.

The survival of the enkephalin-treated mice was longer than that of controls. Such observations in the animal model prompted these and other researchers to evaluate the immune potentiating effects of enkephalins and endorphins in humans. Plotnikoff and his group found that enkephalins and endorphins stimulated active rosettes in humans. Similar results were obtained by Gilman, et al., and Wybran, et al. This work was expanded further to study the effect of enkephalins on an immunosuppressed population of individuals. Lymphocytes from a group of lymphoma patients were treated with the enkephalins in vitro and then evaluated for rosetting with sheep red blood cells (SRBC’s.) It was found that both methionine and leucine enkephalins enhanced the ability of these cells to form T cell rosettes when compared to controls. Methionine enkephalin exhibited this immunopotentiation at a concentration as low as 10-14 mg/ml.

Studies have been undertaken in laboratories to investigate the effects of enkephalins on natural killer (NK) cell activity. The NK cells are a population of cells that can selectively lyse certain tumor cells in vitro without prior sensitization. This is a heterogeneous population of cells present in a variety of animals and humans. It is presently believed that these cells play a major role in protective surveillance against cancer. Anticancer potential of many of the immune activators has been measured by their ability to boost the (NK) defenses of the host. Results to date indicate enkephalins are capable of enhancing NK activity in vitro from normal volunteers and more importantly from cancer patients, some of whom have been heavily pretreated with chemotherapy.

Three separate groups have now reported in vivo clinical findings with the use of methionine enkephalin in patients with AIDS and symptomatic HIV infection. A Low Dose Study (10 micrograms/kg l.V.3 times/wk. for 12 weeks) Zunich and Kirkpatrick administered 10 μg/kg MEK intravenously three times weekly for up to 12 weeks to seven patients with various stages of HIV infection. This trial was conducted prior to the advent of potent antiretroviral therapy. In evaluating cellular immunity, the authors stated that MEK appears to temporarily enhance selected immune responses in patients infected with HIV. However, in this study, the results were neither clinically, nor statistically significant. There were no adverse reactions or evidence of toxicity.

Moderate-High Dose Studies (20, 25, 40, 50, 60, 80, and 100 micrograms/kg 1.V. 1 to 3 times/week for one to 24 months) have also been conducted. The preliminary clinical studies of MEK in symptomatic HIV infection, AIDS and cancer patients (30, 32, 45, 46, 47, 48 and 49) involved individualized treatment schedules with doses ranging up to 100 μg/kg 3x/week and durations extending beyond one year. There were no serious adverse reactions attributed to treatment for any of the patients studied. All reactions were transitory and appear to have been directly related to the infusion.

Eight Kaposi’s Sarcoma Patients were administered MEK (10-100 μg/kg 1-3 x week for 1-24 months). There were no serious adverse reactions attributed to treatment for any of the patients studied.

Symptomatic HIV Infection (Treatment one month up to 24 months, MEK administered at doses of 20-100 μg/kg 1-3x week). In a pilot study in these patients, Dr. J. Wybran in Brussels, Belgium indicated that there may be immunological improvements with MEK treatment. No adverse reactions attributable to MEK treatment were observed.

| 14 |

Asymptomatic HIV+ patients. Four asymptomatic HIV+ patients were treated with methionine enkephalin (60 μg/kg i.v.) once a week for 1-4 months. The monoclonal marker Leu 19 (CD56) for natural killer and killer cells was found to be increased in all four patients (18/24 discrete measures). No adverse reactions to methionine enkephalin were reported. It appears, based on the above data, that a new group of clinically useful immune modulators called enkephalins are emerging. Their in vitro magnitude of potency is at least 106 - 107 greater than that of interferon, interleukins and thymus hormones. Stimulatory effects were observed at concentrations as low as 1012- 10-14 mg/ml (33-37). Such characteristics make endogenous peptides ideal for therapeutic trials. The following additional facts are of interest in this regard: a) Methionine enkephalin stimulates humoral immunity (at low doses) and chemotaxis; b) Methionine enkephalin selectively stimulates production of cytotoxic T cells. Cytotoxic T cells (CD3, CD8) have been reported to inhibit reverse transcriptase of HIV; c) Subacute safety studies in rats and dogs at doses up to 25 mg/kg resulted in no toxicity; d) Human safety studies using doses up to 250 micrograms/kg resulted in no toxicity; e) Enkephalins may in fact be the natural mediators for the endogenous release of both interleukin 2 (32, 44), gamma interferon (32, 44) and IL-12.

Prior clinical studies

Eight (8) Phase I and four (4) Phase II clinical trials completed in cancer and HIV/AIDS between the years 1997-2015.

Notably promising data in HIV/AIDS and Cancer with strong efficacy signals:

123 adults in Phase I/II trials in cancer Between the years 1997-2014

250 adults in Phase I/II for HIV/AIDS Between the years 2000 -2014

Our first acquisition was the patents and intellectual property of Dr. Nicholas P. Plotnikoff and Professor Fengping Shan in 2012. While Dr. Plotnikoff was with Oral Roberts University, he was a member of the team that developed and patented the specific application of MENK as a treatment for cancer, HIV/AIDS, and infectious diseases. All of the clinical data generated by Dr. Plotnikoff has been included in our briefing package to the FDA.

Dr. Nicholas Plotnikoff initiated and completed Phase I and Phase II clinical studies of MENK under Investigational New Drug (“IND”) protocols filed with the U.S. Food and Drug Administration (“FDA”). In these clinical trials, MENK has been shown to reduce the symptoms of early AIDS and AIDS Related Complex (“ARC”), a condition also known as pre-AIDS which includes symptoms such as fever, diarrhea, weight loss, swollen lymph nodes and herpes. In addition to the therapeutic effects of the treatments, trial reports indicated an elevation in mood of the patients treated (Bihari, B., Plotnikoff, N., Freeman, K., Dowling, J., Duguid, C., and Altmann, E., ’‘Methionine Enkephalin in the Treatment of ARC,’’ Seventh Int. Conf. on AIDS, Florence, Italy, 1991).

A double-blind, randomized controlled Phase II study of 46 patients was performed with ARC (Bihari B, Plotnikoff NP. Methionine Enkephalin in the Treatment of AIDS-Related Complex. CRC Press, LLC; Cytokines: Stress and Immunity. 1999; 77-91) that was designed to measure the effect of a regular weekly dosing schedule of MENK at two different dose levels. The study involved randomized assignment to three arms: (i) patients on the first arm received weekly doses of 60µg/kg of MENK (low dose) for 12 weeks; (ii) patients on the second arm received a weekly infusion of 60µg/kg of MENK (low dose) for 2 weeks, followed by 10 weekly doses of MENK at 125µg/kg (high dose); and (iii) the patients on the third arm received a placebo intravenously for 12 weeks.

Product Development Status

| ● | Phase I Trial Pancreatic was completed in 2007 – Department of Medicine, The Pennsylvania State University, College of Medicine, GI Medicine. |

| ● | Dose is 250-300 μg/kg IV weekly. |

| ● | Showed minimal side effects. |

| ● | Determine the maximum tolerated dose standard 3+3 regimen starting at 25 μg/kg. |

| ● | Safety and toxicity of OGF (paresthesia, hypotension at 250μg/kg over 30 min). |

| ● | Compare route of administration (IV vs. SC); solubility issues with sc in low volume. |

| ● | Pharmacokinetic assays; [Met5]-enkephalin by RIA. |

| ● | Examine safety of chronic administration. |

| 15 |

Phase I combination trial OGF & Gemcitabine

| ● | Primary |

Evaluate the safety and toxicity of the combination of OGF biotherapy and gemcitabine chemotherapy in patients with advanced pancreatic cancer / pharmacokinetics. N =20

| ● | Secondary |

Examine the role of OGF given with gemcitabine on, patient survival.

Patients were treatment naïve.

All of the symptoms and possible side effects of MENK/OGF therapy such as nausea, constipation, dry mouth, flushing, diarrhea and abdominal pain thought to be due to the advanced cancer rather than the treatment.

The two side effects thought to be due to the MENK/OGF therapy include the transient paresthesia or tingling at the beginning of the infusion and the hypotension.

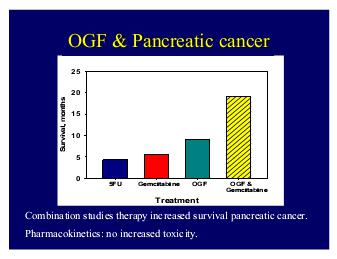

The survival of patients with metastatic pancreatic cancer was increased to almost 9 months compared to standard historical medications used.5 FU only lengthens the survival to 4.5 months and gemcitabine to 5.8 months.

Phase II Trial Pancreatic Cancer

In our larger Phase 2 study when we compared survival of OGF patients to 266 untreated control subjects, the survival was increased. (Department of Medicine, The Pennsylvania State University, College of Medicine, GI Medicine)

| ● | Funded by FDA Orphan Drug Program | |

| ● | Treatment OGF 250mg/kg over 45 min weekly | |

| ● | Open-labeled, untreated controls | |

| ● | Primary endpoint: Survival | |

| ● | Secondary endpoints: efficacy, QOL | |

| ● | 25 OGF-treated subjects & 166 controls | |

| ● | Eligible patients: |

| ● | Unresectable pancreatic cancer | |

| ● | Failed standard therapy | |

| ● | Karnofsky status 50% |

Most importantly, there were no changes in the blood laboratory tests with OGF. Compared to standard chemotherapy that reduces the blood count from bone marrow toxicity, the blood count remained stable with OGF.

| 16 |

One of the most important features of OGF therapy in cancer patients with advanced metastatic disease is the marked improvement in Clinical Benefit. Clinical benefit is based upon parameters that reflect the overall well-being of the patient, including Pain control, performance status, and body weight. 53% of those receiving OGF experienced a clinical benefit compared to patients treated with standard chemotherapy.

The Company is planning to rely on the following available information and historical data to support the initiation of the Phase 3 study and filing of the NDA:

1. Clinical safety data from studies conducted under this IND (50,987 studies NIH# R03

CA80646, NCT00109941, and IRB Protocol No. 26336;

2. Clinical safety data from studies conducted under IND 34,442 (MENK for the treatment of AIDS/ARC and cancer patients and normal healthy volunteers

Toxicology Studies completed by Baxter and Travenol 1984 and 1985

Published literature as summarized in this package (to provide nonclinical pharmacology and additional safety data). To support the NDA filing, we are also planning to conduct the following additional study:

Phase 2b study will run in parallel with the Phase 1 PK and 3 month GLP toxicology studies.

| ● | Population to be studied: Patients on first line therapy with local advanced or metastatic disease |

| ● | The Company is running the GLP toxicology at an FDA approved facility in China and those studies will be completed before the end of Q4 2017. |

| ● | The company anticipates a database of 300 – 600 patients at the time of NDA filing. |

| ● | The FDA stated that a genotoxicity study will not need to be conducted. |

| ● | The MTD has been established previously under this IND in pancreatic cancer patients |

| ● | Due to safety data collected to date and established MTD, TNI BioTech believes that a Phase 1 PK study in healthy volunteers can be run concurrently with a Phase 2 clinical trial in pancreatic cancer patients |

| ● | Doses will not exceed the previously established MTD (250 µg/kg) |

Sponsor, which in this case is the Company, will submit the Phase 2b clinical protocol for FDA review. The FDA confirmed that the Phase 2b study could be conducted as an open-label randomized study with two doses of MENK in combination with nap-paclitaxel + gemcitabine versus nap-paclitaxel + gemcitabine. Exact study design will be determined by the Sponsor, and submitted to the FDA for review.

After completion of the Phase 2b study, the Agency would grant the Sponsor an End-of-Phase 2 meeting.

Hubei Qianjiang and Immune Therapeutics have a signed agreement for the development of MENK and have moved forward on that project since 2014-present.

PK and Toxicology Studies were delayed in 2015 because the China Food and Drug Administration (CFDA) required Chemistry, Manufacturing and Controls to be completed before starting the toxicology study. They have been started and will be completed by the end of 2017.

Hubei Qianjiang signed Pharmaceutical Development Agreement for Formulation Development and CTM Manufacturing of Methionine–Enkephalin for Quinjiang and Immune Therapeutics with China Peptide Company (“CPC”) in Q3 2015

CPC perform analytical, pre-formulation, formulation development, clinical trial manufacturing, release testing and ICH1 stability for Methione- Enkephalin

CPC is among only a handful of companies in the world that can claim both ISO Certification and cGMP licensing. In February 2012, CPC became the first peptide company to successfully pass US FDA inspection outside of US and Europe regions.

CMC and formulations are required for mass production of MENK, which is also required for pivotal trials with the FDA for this work has been ongoing since our meeting with the FDA.

| i. | Qianjiang will provide Cote Orphan the CMC data which is required as part of filing MENK protocols. |

| 17 |

In addition Hubei has completed pre-clinical studies using MENK on various cancers in the lab using mouse models and has shown to be successful in a number of cancers including colon, pancreatic and hepatic. The data will be translated and provided as part of the briefing package for both pancreatic and liver cancer.

The MENK treatment was generally well tolerated with no appreciable toxicity observed. The high dose of MENK increased adaptive cell immunity resulting in increased activity of the body’s immune system (e.g. increased IL-2 receptors, CD56 NK and LAK cells, CD3, CD4 and CD8 cells) and a reduction in the size of lymph nodes. One patient in the high dose group administered by rapid intravenous infusion experienced dizziness, diaphoresis, elevated blood pressure and decreased pulse rate. These signs and symptoms were responded to with supportive measures.

Recently, Professor Fengping Shan and Dr. Plotnikoff have published, in a number of peer-reviewed international journals, that MENK inhibited regulatory T-cells, increasing the functional activities of T cells and NK cells and, thus, is a key to improved cancer therapy. They additionally published results showing that MENK alone or in combination with Interleukin-2 (“IL -2”) or Interferon-γ (“IFN-γ”) can enhance the production of interferon- γ or IL-2 from CD4+T cells, respectively (Shan F, Yanjie Xia, Ning Wang, Jingjuan Meng, Changlong Lu, Yiming Meng, Nicolas P. Plotnikoff. Functional modulation of the pathway between dendritic cells (DCs) and CD4+T cells by the neuropeptide: Methionine enkephalin (MENK). Peptides 32. 2011; 929–937). MENK also appeared to be more potent than IL -2 or IFN-γ, alone (Hua H, Changlong Lu, Weiwei Li, Jingjuan Meng, Danan Wang, Nicolas Plotnikoff, Enhua Wang and Fengping Shan. Comparison of stimulating effect on subpopulations of lymphocytes in human peripheral blood by methionine enkephalin with IL-2 and IFN-γ. Human Vaccines & Immunotherapeutics 8:8, 2012; 1082-1089), two widely known cytokines that have been approved by the FDA for marketing.

Plotnikoff & Shan History

| ● | 1983 Baxter takes license Conducts sub-chronic multiple dose pathology and toxicology studies |

| ● | Beginning 1984 Open Label clinical studies started in cancer and AIDs patients |

| ● | 1989 NIH AID’s Committee recommends Methionine-enkephalin for inclusion in AIDs clinical trials (low priority). Methionine-enkephalin discovered to activate LAK cells which destroy AIDs virus |

| ● | 1990-1995 Double Blind placebo controlled study in HIV patients begun at C.R.L in New York |

| ● | 1995-2000 Open Label Tulsa, Belgium, Denver and New York |

| ● | 2012-2014 Open Label 1Department of Cord Blood Bank, Shengjing Hospital; China Medical University; Heping District, Shenyang, PR China; Department of dermatology; No.1hospital; China Medical University; Heping District, Shenyang, PR China; Department of Immunology; School of Basic Medical Science; China Medical University; Heping District, Shenyang, PR China and TNI Bio. Tech. Inc.; Orlando, FL USA |

| ● | In 1984 Nicholas P Plotnikoff and Gerald C miller and Joseph Wybran (etc) initiated a trial in 14 healthy volunteers and 8 cancer patients the Clinical pharmacology of methionine-enkephalin was studied in normal volunteers at doses of 1, 10, 50, 100, 150, 200, and 250 pg/kg. Immunologically, increases in total lymphocytes, B lymphocytes, active rosette-forming cells, T lymphocytes (OKTl 1), T-helper lymphocytes (OKT4), and T-suppressor lymphocytes (OKT8) were seen after infusion with methionine-enkephalin. In addition, increased mitogen-stimulated blastogenesis with PHA, Con A, and pokeweed were also seen with methionine-enkephalin treatment. No material changes were seen in EKG, blood pressure, heart rate, respiratory rate, temperature, or neurologic reflexes of normal volunteers receiving methionine enkephalin in doses of 1 to 200 pg/kg. |

Our human (in vivo) studies have demonstrated that methionine-enkephalin is an activator of T-cell subsets, NK cells, and potentiator of blastogenesis in the presence of PHA, Con A, pokeweed, or Staph A. All of the clinical pharmacologic variables were normal, including EKG, heart rate, blood pressure, respiration, temperature, and neurologic reflexes, as well as urinalysis and SMAC 26. Transient side effects such as vasodilation and/or gastrointestinal cramps were seen only at high doses (100, 150, 200, and 250 pg/kg). Thus, in this study, methionine-enkephalin, a natural hormone, was administered without significant adverse effect in a dose range of 1 to 250 pg/kg (by intravenous infusion).

| 18 |

In our studies in cancer patients with Kaposi’s sarcoma (due to AIDS), melanoma, lung cancer, and hypernephroma increases in T-cell subsets were also observed. Increased levels of blastogenesis with the mitogens PHA, Con A, and pokeweed were also observed. An increased expression of interleukin-2 receptors was also observed, while Wybran reported increased blood levels of interleukin-2 in patients receiving methionine-enkephalin. In addition, Wybran et al. 28 have reported that methionine enkephalin elevates T-cell subset numbers in pre-AIDS or ARC patients. Methionine enkephalin may well be useful as an immunomodulator in the treatment of patient in the early stages of their illness and/or following surgery, radiation, or chemotherapy treatment.

Cancer Patients

Methionine-enkephalin was administrated to seven patients with lung cancer. These patients were newly diagnosed and had not yet received prior treatment such as surgery, chemotherapy, radiotherapy, or immunotherapy. Immunologic tests were performed before Methionine-enkephalin injection, and 2 hours, 24 hours, 6 days after Methionine-enkephalin perfusion. The results can be summarized as follows: in four patients active T-cells were increased in the blood; in five patients the percentage of OKTlO increased in the blood; and in seven the cells with the Leu 11 phenotype increased (to more than twice the initial value in four of these patients). More interestingly, NK activity increased in five of seven patients (by more than 100 in three of them, in whom NK activity increased from 30 to 60, 7 to 15%, and 18 to 36%).

Once again, the absence of subjective or objective side effects should be stressed in this single-injection study.

ARC Patients

Seven patients with AIDS-related complex received Methionine-enkephalin three times a week intravenously for a minimum of 21 days; the concentrations varied from 20 to 100 pg/kg at each injection. Some patients have already been treated for 130 days. The immunologic results can be summarized as follows after 21 days of treatment: increase in the numbers of blood OKT3 and OKT4 lymphocytes, no increase in the absolute count of lymphocytes, borderline increase in NK activity (p < 0.10), and increase in IL-2 production as well as in PHA response. The most striking result is the enhancement of the PHA response. Some patients were treated for a longer period of time and one patient has shown a remarkable immunologic and clinical course. This 32-year-old Caucasian homosexual male had a prior history of an 11-kg weight loss, night sweats, recurrent scrota infections, and lymphadenopathy for a period of 2 years. Testing of his immunologic status showed a reduced OKT4 percentage (20%) and count 336/mm3), low NK activity (22%), low ILL-2 production (0.5 units), and low PHA response (147,000 cpm). He was started on Methionine-enkephalin and followed immunologically as well as clinically. At day 130, his OKT4 percentage is 38% and the OKT4 count 730/mm3. The NK activity has increased to 43% and the IL-2 production is also normalized to 2.1 units. Finally, his PHA response has presently reached 414,000 cpm. Clinically, this patient has no more scrota1 infections, he has gained 8 kg, the night sweats have disappeared, and the lymph nodes have completely regressed within 3 months. In summary, this patient shows an almost complete immunologic nonspecific functional reconstitution, except with respect to the OKT4 subset. Clinically, he is in complete remission. All the data indicate that Methionine-enkephalin can enhance some immunologic functions in ARC patients, and preliminary data suggest some therapeutic beneficial effect in some patients. These results have to be confirmed in larger series in double-blind randomized trials.

AIDS Patients

One AIDS patient received a single injection of 20 pg/kg of Methionine-enkephalin and his PHA response increased from 4300 cpm to 14,000 cpm! Another AIDS patient with Kaposi’s Sarcoma is now receiving chronic treatment with Methionine-enkephalin. His lesions have remained stable for 4 months. More interestingly, an AIDS patient (with Hodgkin’s lymphoma, Toxoplasma cerebral abscess, atypical mycobacteria) was diagnosed as having Kaposi’s Sarcoma lesions (biopsy-proven). He was started on Methionine-enkephalin treatment 1 month after the Kaposi’s Sarcoma lesions appeared, and after 4 weeks of treatment these lesions have flattened and are in the process of disappearing (as determined by biopsy). In the case, Methionine-enkephalin administration was associated with the regression of the Kaposi’s Sarcoma.

Clinical Studies finished with 178 patients in Tulsa, Brussels the Belgium Medical School, New York SUNY, Denver Colorado Medical School and Chicago to increase number of cytotoxic cells CD4, CD8 and NK Cells in AIDS and Cancer patients. The studies demonstrated that Methionine-enkephalin is an effective and potent immunomodulator in HIV/AIDS patients. Methionine-enkephalin exhibited a dose response between the dose of 10, 20, 50 and 100 micrograms/kg in terms of increasing number of CD3, CD4, CD8 and NK cells in these patients (average increase of 50%). Higher doses of Methionine-enkephalin (150, 200, 250 and 300 micrograms/kg) exhibited a plateau effect. No toxicity was seen in these patients. Methionine-enkephalin increases the number of cytotoxic cells (subsets CD4, CD8 and NK) that are known to specifically destroy HIV. This “antiviral” effect was recorded by marked reduction of p24 both in vitro and in vivo.

| 19 |

A phase II clinical study under IND was completed. The study, was a double-blind and placebo controlled, involved randomized assignment to three arms receiving a weekly intravenous infusion of 60mpg/km (low Dose) or receiving a weekly infusion of 125 micrograms/kg and the third receiving a placebo infusion of normal saline. Twenty subjects completed 12 weeks of the trial, twenty-six patients completed 8 weeks, and 33 patients completed 4 weeks. Eligibility for this clinical study included a positive HIV serology, CD4 level between 200 and 500.

Substantial differences from baseline were observed (at eight weeks in patients receiving 125 micrograms/km) for the following parameters: CD4, DC8, DC35, CD38, CD56, NK, PHA, PWM and CMV. The most important findings of the study were the increase in CD4 (T helper cells) and CD56 (cytotoxic cells NK-K-LAK). There were no serious adverse reactions.