Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - ICC Holdings, Inc. | icch-20161231xex32_2.htm |

| EX-32.1 - EX-32.1 - ICC Holdings, Inc. | icch-20161231xex32_1.htm |

| EX-31.2 - EX-31.2 - ICC Holdings, Inc. | icch-20161231xex31_2.htm |

| EX-31.1 - EX-31.1 - ICC Holdings, Inc. | icch-20161231xex31_1.htm |

| EX-23.1 - EX-23.1 - ICC Holdings, Inc. | icch-20161231xex23_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________

FORM 10-K

_______________________________

(Mark One)

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

or

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For transition period from to .

Commission File Number: 333-214081

ICC Holdings, Inc.

(Exact name of registrant as specified in its charter)

_______________________________

|

Pennsylvania

(State or other jurisdiction of

|

|

81-3359409

(I.R.S. Employer

|

|

225 20th Street, Rock Island, Illinois (Address of principal executive offices)

|

|

61201 (Zip Code)

|

(309) 793-1700

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

Common Stock, par value $0.01 per share Title of each class |

|

The NASDAQ Stock Market, LLC Name of exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10‑K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

|

Large accelerated filer ☐ |

Accelerated filer ☐ |

|

|

Non-accelerated filer ☐ (Do not check if a smaller reporting company) |

Smaller reporting company ☒ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of June 30, 2016, the last business day of the Registrant’s most recently completed second fiscal quarter, there was no established public market for the Registrant’s common stock. The Registrant therefore cannot calculate the aggregate market value of its voting and non-voting common equity held by non-affiliates as of such date. The Registrant’s Common Stock began trading on The NASDAQ Stock Market, LLC on March 23,2017.

The number of shares of the registrant’s common stock outstanding as of March 28,2017 was 3,500,000.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the definitive Proxy Statement for our 2017 Annual Meeting of Shareholders which is to be filed within 120 days after the end of the fiscal year ended December 31, 2016, are incorporated by reference into Part III of this Form 10-K, to the extent described in Part III.

|

|

Page |

|

|

PART I |

||

|

Item 1. |

3 | |

|

Item 1A. |

22 | |

|

Item 1B. |

33 | |

|

Item 2. |

33 | |

|

Item 3. |

33 | |

|

Item 3A. |

34 | |

|

Item 4. |

35 | |

|

|

||

|

PART II |

||

|

Item 5. |

Market for Registrant’s Common Equity, Related Stockholder Matters and |

36 |

|

Item 6. |

37 | |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

39 |

|

Item 7A. |

59 | |

|

Item 8. |

61 | |

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

93 |

|

Item 9A. |

93 | |

|

Item 9B. |

93 | |

|

|

||

|

PART III |

||

|

Items 10-14. |

93 | |

|

|

||

|

PART IV |

||

|

Item 15. |

94 | |

|

|

||

| 95 | ||

| 96 | ||

~ 2 ~

Overview

ICC Holdings, Inc. is a Pennsylvania corporation that was organized in 2016. ICC Holdings, Inc. was formed so that it could acquire all of the capital stock of Illinois Casualty Company (ICC) in a mutual-to-stock conversion. Prior to the conversion, ICC Holdings, Inc did not engage in any operations. After the conversion, ICC Holdings, Inc’s primary assets are the outstanding capital stock of ICC, the outstanding membership interests of ICC Realty, LLC and a portion of the net proceeds from the stock offering completed in connection with the mustual-to-stock conversion. As of December 31, 2016, ICC was the ultimate reporting entity and the financial statements herein are for that entity.

As used in this Form 10-K, references to “the Company,” “we,” “us,” and “our” refer to the consolidated group. On a stand-alone basis ICC Holdings, Inc is referred to as the “Parent Company.” The consolidated group consists of the holding company, ICC Holdings, Inc., an operating insurance company, ICC, and ICC’s three wholly-owned subsidiaries, Beverage Insurance Agency, Inc., an inactive insurance agency, Estrella Innovative Solutions, Inc., an outsourcing company, and ICC Realty, LLC, a real estate services and holding company. ICC is an Illinois insurance company.

We are a regional, multi-line property and casualty insurance company focusing exclusively on the food and beverage industry. During 2016, we had $51.0 million in direct written premiums.

We primarily market our products through a network of approximately 140 independent agents in Illinois, Iowa, Indiana, Minnesota, Missouri, Ohio and Wisconsin. ICC has been assigned a “B++” (Good) financial strength rating by A.M. Best Company, Inc. (A.M. Best), which is the fifth highest out of fifteen possible ratings. ICC’s most recent evaluation by A.M. Best occurred on March 28, 2017, when A.M. Best affirmed its Financial Strength Rating (FSR) of “B++” and Issuer Credit Rating (ICR) of “bbb” (Good). The outlook of the FSR is stable, while the outlook of the Long-Term ICR remains positive. A.M. Best also assigned a Long-Term ICR of “bb” to ICC Holdings, Inc. The outlook assigned to the Credit Rating of the Company is positive.

For over 66 years, ICC has specialized in providing customized insurance products and aggressive claims defense for customers exclusively in the food and beverage industry.

ICC was founded as an inter-insurance exchange in 1950 based upon the recognition that establishments serving alcohol require unique insurance protection. Beginning in 1998, we expanded the scope of our product offerings beyond liquor liability to include property, general liability, umbrella, and workers compensation coverage. Our goal was to meet the full range of business insurance needs of our clients in the food and beverage industry.

In 1999, ICC recognized the significant need to automate. Upon determining available commercial software was inadequate to meet our long-term vision, we contracted the development of an integrated platform to handle agency, policy, and vendor management. Introduced in 2001, the first module successfully improved productivity and reporting capabilities. We built on that success by adding document imaging, claims, billing, and risk management modules. As it has grown, our information management system has provided us with a unique and comprehensive ability to automate processes, track and examine risk traits, and monitor claims development. As a result, ICC has constructed and leveraged a multi-variant pricing algorithm that allows us to better segment our business in order to more effectively price to actual exposure.

ICC mutualized in 2004 and began to expand its territory geographically within the Midwest. We are an admitted carrier in nine states: Colorado, Illinois, Iowa, Indiana, Minnesota, Michigan, Missouri, Ohio and Wisconsin. We currently issue policies in seven states, including Ohio where we began writing policies in the third quarter of 2016, and expect to begin writing premium in Michigan as early as 2018. As we expanded our territory and product lines over the last 66 years, we have maintained our focus and commitment to the food and beverage industry. As a result, we have developed unsurpassed expertise in our niche, particularly within the areas of underwriting, loss control, and claims management. ICC continues to leverage that experience into the ongoing development of innovative insurance products and services uniquely tailored to the food and beverage industry.

ICC is subject to examination and comprehensive regulation by the Illinois Department of Insurance. See Item 1. Business — Regulation.

Our executive offices are located at 225 20th Street, Rock Island, Illinois 61201, and our phone number is (309) 793-1700. Our web site address is www.ilcasco.com. Information contained on our website is not incorporated by reference into this Annual Report on Form 10-K and such information should not be considered to be part of this Annual Report on Form 10-K.

~ 3 ~

Our Business Strategies

We believe that our mission is to deliver expertly crafted insurance products and services for the food and beverage industry. Accordingly, we believe that this focus positions us to write profitable business in both hard insurance markets (where industry capital is constricted, competition is low, and premium rates are rising) and soft insurance markets (where industry capital is rising, competition is high and premium rates are falling). As part of our business process, we have developed our business strategy and focus using the following guiding principles to reflect the essence of who ICC aspires to be:

|

· |

we endeavor to return value to our stakeholders in the form of strong financial performance and sustained surplus growth; |

|

· |

we conduct our business with the highest ethics and unquestionable integrity; |

|

· |

we recognize and reward the commitment of all of our associates who make ICC a success, by challenging our associates, by valuing them and recognizing their contribution, while cultivating a mutually supporting culture; |

|

· |

we believe that an independent agency system is mutually beneficial to both the agent and ICC because of the drive to deliver the highest quality products at competitive prices; |

|

· |

customer service, which is understanding and meeting the needs and expectations of our policyholders and agents, is at the fundamental core of our existence; |

|

· |

we believe we can succeed in the marketplace given our unique understanding of the food and beverage industry, offering customized products and aggressively defending our insureds; |

|

· |

we focus on innovation, which drives our efficiency, quality and effectiveness; |

|

· |

we identify worthy causes to support with our corporate and associate resources and promote good corporate citizenship; and |

|

· |

we strive to improve our products and processes through intelligent investment in talent and technology that meets our exacting needs and those of our customers. |

In order to effectuate our mission and guiding principles, we have identified the following core strategies to achieve our long-term success:

|

· |

design and market commercial property and casualty products customized for the food and beverage industry, through our in-depth knowledge and research of the industry; |

|

· |

pursue deliberate geographic expansion; |

|

· |

Provide and market comprehensive policies with flexible a la carte options; |

|

· |

foster true partnerships with independent agents who have a significant presence in the food and beverage industry and an appreciation for ICC’s commitment and expertise to obtain optimal market share in the food and beverage industry; |

|

· |

leverage business intelligence to maximize performance, increase operational efficiency, and price our products for sustained profitability; |

|

· |

implement an investment strategy that maximizes return within acceptable risk tolerances; |

|

· |

promote a culture of excellence that encourages teamwork and contributes to talent retention and development; and |

|

· |

maintain a robust and comprehensive enterprise risk management program, focused on upside optimization and downside mitigation. |

Competitive Growth Strategies

Technology – We believe that existing and developing technology and information systems are and will continue to impact the insurance industry’s use of risk analysis in the underwriting process, provide tools for reduction of claims, and modernize the claims handling process. As part of our focus, we have internally developed a completely integrated policy management system. This system allows us to leverage loss control data for predictive analytics in both the claims and underwriting areas. For example, in the underwriting area, we create pricing models taking into account the unique characteristics of our customers, with industry-specific variables such as latest hour of close, type and frequency of on-site entertainment, and average alcoholic beverage pricing. We also have achieved better efficiency by moving to a more paperless organization and integrate off-site employees in our claims, underwriting, accounting, loss control and IT development areas. We intend to remain a leader in the industry in utilizing technology and data analysis to price our coverage based on the risk assumed, reduce accidents and provide prompt claims response.

~ 4 ~

Industry Expertise – We have been providing the food and beverage industry with insurance products and services since 1950. By leveraging our experience, we better understand our customers and their needs, which allows us to better price our products and services and defend claims aggressively and economically, using the experience of our in-house Legal Department and an established network of specialized defense attorneys. As a result, we are the endorsed carrier for the Missouri Restaurant Association, the Indiana Restaurant Association, the Illinois Licensed Beverage Association and the Minnesota Licensed Beverage Association. We also provide insurance agents continuing education on industry topics, such as liquor liability, kitchen fire prevention and alcohol server training. For policyholders serving liquor, we provide certified alcohol server training as a value-added service and risk elimination/mitigation tool. Our associates are also regular panel speakers at local and national claims conferences.

Enterprise Risk Management – As part of our effort to grow responsibly, we have put in place a cross-functional, multi-dimensional enterprise risk management program. The program is focused on financial, organization, operational, tactical, market and legal risks and managed at three different levels: the enterprise risk committee of our board of directors, our internal enterprise risk management committee and our internal audit committee. The focus of the enterprise risk committee of our board of directors is on oversight, top tier risk, emerging risks, and risk optimization. The internal enterprise risk committee is comprised of our senior management team, which is focused on conducting a review of all risks attendant to ICC at least annually; rating triaged risks for severity, frequency, and control; completing risk control reports for stress testing, risk tolerance, and mitigation plans; measuring and monitoring risk on an ongoing basis; and tying enterprise risk management to individual performance evaluations and compensation. Our internal audit function focuses on policy and procedure compliance and mitigation plans.

Growth Strategies

While we have established a significant market share in our existing territories, we believe that there is still opportunity for growth within our existing footprint. We will continue to seek out insurance agency partners who have a commitment to our niche and an ability to sell the value represented by our products. Our long-term growth plan also involved expanding geographically into states where we believe current insurance laws provide an attractive market within our niche for our existing products and services. Current state expansion plans include Colorado, Kansas, and Michigan. Additionally, we are currently evaluating expansion into Arizona, Massachusetts, Oregon, Pennsylvania, and Tennessee. We will consider geographic expansion opportunities that allow us to leverage existing agency relationships whose footprints overlap our own. Growth opportunities will always be carefully evaluated with long term profitability at the forefront of the decision making process.

Although we do not have any current plans or intent to expand or grow our business by acquisition, we will consider opportunities that are presented to us. The completion of this offering will supply additional capital needed to support substantially increased premium volume, which we expect to result from the implementation of these growth strategies.

Reaction to Market Cycles

Many insurance companies sporadically target businesses within our niche; however, a relatively small number make a long-term commitment to the niche through changing insurance market cycles. When the insurance market is “hard” and premium growth is achievable in less specialized segments, many carriers exit this niche. Large and diversified insurance carriers have the ability to shift their focus and resources to less challenging areas. When market conditions “soften,” those same carriers often aggressively move back into our niche for premium growth. Because we specialize in the niche, we do not shift resources to other market segments. Therefore, the Company generally maintains pricing stability throughout market cycles by relying on our strong loss control, underwriting, and claims expertise and our customer service commitment. We react to market cycles by adjusting our appetite for risks based on pricing and cycle conditions, but we maintain a consistent commitment to the food and beverage industry. Due to the relatively small number of insurance companies that make a long-term commitment to this niche, the insurance market does not fluctuate to the same extent as the insurance market for the general commercial market.

~ 5 ~

Our Challenges

Our business faces significant challenges that can impede our goal of growing our business while realizing operating profits, including the following:

Estimating Our Loss Reserves.

We maintain loss reserves to cover our estimated ultimate liability for unpaid losses and settlement expenses for reported and unreported claims incurred as of the end of each accounting period. These reserves represent management’s estimates of what the ultimate settlement and administration of claims will cost. Pursuant to applicable insurance regulations, these reserves are reviewed by an independent actuary on at least an annual basis. Setting reserves is inherently uncertain and there can be no assurance that current or future reserves will prove adequate. If our loss reserves are inadequate, it will have an unfavorable impact on our results. See Item 1. Business — Losses and Settlement Expense for a summary of the favorable and unfavorable developments in our loss reserves in the previous 10-year period.

Reliance on Independent Agents.

Our product is distributed through a contracted network of independent insurance agents. Independent agents are typically contracted with a number of insurance carriers. The producers within an agency will determine which product is most appropriate to recommend to their client or prospective client. The agency will select a product based on a variety of factors such as: premium; coverage; service including billing and claims; agency compensation and agency/company relationship. Establishing and maintaining long term financially successful agency relationships is very important to the long term success of a company.

Maintaining Our Financial Strength Ratings.

In March 2017, A.M. Best affirmed ICC’s financial strength rating of “B++” positive outlook. A key to achieving our goal of significant growth in our premiums written, is obtaining an A.M. Best rating of “A-” or better. Increasing our capitalization and maintaining strong operating performance, are significant rating components reviewed by A.M. Best. This is combined with a review of various other rating requirements. If we are not able to increase our rating or if A.M. Best downgrades our rating, it is likely that we will not be able to compete as effectively and our ability to sell insurance policies could decline. As a result, our financial results would be adversely affected. A.M. Best reviews our rating approximately once per year.

Attracting, Developing and Retaining Experienced Personnel.

To sustain our growth as a property and casualty insurance company operating in a specialty niche market, we must continue to attract, develop and retain management, marketing, distribution, underwriting, customer service, and claims personnel with expertise in the products we offer. The loss of key personnel, or our inability to recruit, develop and retain additional qualified personnel, could materially and adversely affect our business, growth and profitability.

Competitive Strengths

Our opportunity for growth is driven by our competitive strengths, which include the following:

Use of Data and Metrics to Improve our Underwriting Results.

Our analysis of data available through both governmental and other industry resources, combined with our internal data, drive our underwriting and pricing decisions. We have developed a multi-variant risk grading system and pricing algorithm that combines both objective and subjective inputs that drive both whether to provide coverage and pricing. This information helps us avoid providing coverage to higher risk insureds while improving our overall risk profile. Every risk we insure is inspected within the first 60 days of policy binding, which permits us to cancel the policy if we determine that the insured is not an acceptable risk or pricing is inadequate. Each inspection consists of an extensive risk profile questionnaire as well as between 25 to 100 pictures of the insured’s place of business. We believe this approach reduces claims frequency.

~ 6 ~

Focus on niche food and beverage business.

We target niche markets within the food and beverage industry that support adequate pricing and believe we are able to adapt to changing market needs ahead of our competitors through our strategic focus. We develop and deliver specialty insurance products priced to meet our customers’ needs and strive to generate consistent underwriting profit. We believe that our extensive experience and expertise specific to underwriting and claims management in the food and beverage industry will allow continued loss ratio improvement in 2017 and going forward. The Company is committed to retaining this underwriting and claim handling expertise as a core competency as the volume of business increases.

Strong market presence with name recognition and long-standing producer relationships.

We have been writing insurance for the food and beverage industry in Illinois since 1950. Approximately 36.9% of current total premium is written in Illinois.

Great care is taken in building the ICC brand in all states of operation and the Company holds significant market share in nearly all states serviced. ICC acknowledges that each state, each agency and each customer is unique. A commitment to quality of product and services is universally important and recognized.

Scalable operations positioned for growth.

We are focused on automation and operating efficiencies across its core functional areas. We have consistently increased premium per full time equivalent employee for five consecutive years and are positioned to continue that trend with current growth plans. We believe we are well-positioned in both terms of personnel and systems to increase written premiums and to expand into new geographic markets with better than industry level profitability using the efficient operating infrastructure we have developed over the last few years.

Experienced management team.

We are managed by an experienced group of executives led by Arron K. Sutherland, our President and Chief Executive Officer. Mr. Sutherland has served in his current position since June 2010, joined ICC in 2006 and has worked in the insurance industry for over 20 years. Michael R. Smith, our Vice President – Chief Financial Officer, has served with ICC since 2011. Mr. Smith has more than 20 years of experience in the financial services industry, including 15 years with insurance organizations. Howard J. Beck, our Vice President – Chief Underwriting Officer, has been with ICC since 2004 and has over 24 years of underwriting experience. Norman D. Schmeichel, our Vice President – Chief Information Officer, has served with ICC since 2002. Mr. Schmeichel has more than 20 years’ experience in information technologies and 14 years’ experience in the insurance industry. Additionally, Julia B. Suiter, our Chief Legal Officer, has served with ICC since 2009 and has over 20 years’ experience in insurance defense and contract law. Rickey Plunkett, our Director of Claims, has served with ICC since 2010 and has over 35 years of experience in the claims field. Kathleen S. Springer, our Director of Human Resources, has served with ICC since 2008 and has over 20 years’ experience in benefits, compensation, and talent acquisition and more than 8 years’ experience in the insurance industry. As a group, our executive officers have on average more than 20 years’ experience in the property and casualty insurance industry.

Products

ICC has specialized in the food and beverage industry since 1950. Our product language is based on Insurance Services Offices (ISO) forms, which is an industry standard, but tailored to the specific needs of our clients. We began by writing liquor liability or dram shop insurance and that remains a prominent line of business today. Commercial property and liability are written in a single policy as a business owners policy (BOP). ICC also writes workers compensation and commercial umbrella policies which are written as complementary lines to the BOP and liquor liability and are not offered on a stand-alone basis. As of December 31, 2016, ICC writes 4,863 BOP policies, 4,683 liquor liability policies, 1,742 worker’s compensation policies and 1,187 commercial umbrella policies. 90.5% of BOP policies and 89.7% of liquor liability policies are for either restaurants or taverns. While we do not currently write commercial auto insurance, we do insure risks associated with the delivery of food or beverage.

Marketing and Distribution

Our commercial insurance product is sold by over 140 independent insurance agents in Illinois, Iowa, Indiana, Minnesota, Missouri, Ohio and Wisconsin. These agencies access multiple insurance companies and are typically established businesses in the communities in which they operate. We view these agents as our primary customers because they are in a position to recommend either our insurance products or those of a competitor to their customers. We consider our relationships with these agencies to be a core strength of the Company.

~ 7 ~

We manage our producers through quarterly business reviews utilizing various internally generated reports. Our quantitative agency review (QAR) measures each agency on a variety of weighted metrics and ranks them from high to low. The measurement is updated on a weekly basis and is available for all company employees’ review.

For the year ended December 31, 2016, only two of our producers were responsible for more than 5% of our direct premiums written and our top 10 producers accounted for approximately 37.5% of direct premiums written.

Our agency partners are supported by our Marketing Department. These representatives also identify and train new agents. We conduct regularly scheduled webinars for agents as well as onsite training on company products and services. These include technical training about our products as well as sales training to effectively market our products. We also offer our agents industry specific training that qualifies for continuing education credit for state insurance license requirements.

Agents are compensated through a fixed base commission with an opportunity for profit sharing depending on the producer’s premiums written and profitability. Agents receive commission as a percentage of premiums (generally 15% for most lines, except worker’s compensation policies which are generally at 7.5%) as their primary compensation from us. We offer a contingent compensation plan as an incentive for producers to place high-quality business with us and to support our loss control efforts. We believe that the contingent compensation paid to our producers is comparable with those offered by other insurance companies and is designed to reward agents for growth and profitability.

Our marketing efforts are also supported by our Claims, Litigation, Billing, Underwriting and Loss Control Departments. As industry specialists, we are able to offer expertise in all interactions with agents and/or policyholders. For example, our claims philosophy is to provide prompt and efficient service and claims processing, resulting in a positive experience for both the agents and policyholders. We take an aggressive, defense-oriented position on third party liability claims which is recognized and appreciated by our policyholders. We believe that these positive experiences result in higher policyholder retention and create new business opportunities for our agents. While we rely on our agents for front line distribution and customer support, underwriting, billing, loss control and claim handling responsibilities are retained by us. Many of our agents have had direct relationships with us for a number of years.

Underwriting, Risk Assessment and Pricing

Our underwriting philosophy is aimed at consistently generating profits through sound risk selection, stringent loss control and pricing discipline. One key element in sound risk selection is our use of risk characteristic metrics. Through 66 years of focused underwriting, we have identified predictive metrics of data that many other insurance companies do not recognize or measure. Use of these metrics allows us to more effectively price risks, thereby improving our profitability and allowing us to compete favorably with other insurance carriers. We also are very active in leveraging our onsite loss control inspections. An example would be the monitoring of kitchen fire suppression systems servicing to reduce kitchen fire losses.

Our philosophy is to understand our industry and be disciplined in our underwriting efforts. We will not compromise profitability for top line growth.

Our competitive strategy in underwriting is:

|

· |

Maximize the use of available information acquired through a wide variety of industry resources. |

|

· |

Allow our internal metrics and rating to establish risk pricing and use sound underwriting judgement for risk selection and pricing modification. |

|

· |

Utilize our risk grading system, which combines both objective and subjective inputs, to quantify desirability of risks and improve our overall risk profile. |

|

· |

Physically inspect every new insured within the first 60 days of policy binding with our in-house loss control representatives. Our inspection consists of an extensive risk profile questionnaire and includes 25 to 100 electronic photos of the insured’s place of business. Inspections that demonstrate that a risk is not desirable is a basis for revoking coverage. |

|

· |

Provide very high-quality service to our agents and insureds by responding quickly and effectively to information requests and policy submissions. Treat our agents as partners and have the same expectation of them. |

Our Underwriting Department works in teams with each agent assigned to one of three teams. We underwrite our accounts by evaluating each risk with consistently applied standards. Each policy undergoes a thorough evaluation process prior to every renewal.

~ 8 ~

Our underwriting staff of 24 employees has an average of 12 years of insurance industry experience. Howard J. Beck, our Vice President – Chief Underwriting Officer, has been with ICC since 2004 and has over 27 years of insurance experience with 20 years of property and casualty underwriting experience.

We strive to be disciplined in our pricing by pursuing targeted rate changes to continually improve our underwriting profitability while still being able to attract and retain profitable customers. Our pricing reviews involve evaluating our claims experience, loss trends, data acquired from inspections, applications and other data sources to identify characteristics that drive the frequency and severity of our claims. These results drive changes to rates and rating metrics as well as understanding what portions of our business are most profitable.

This knowledge and analysis enables us to price risks accurately, improve account retention, and drive profitable new business.

Claims and Litigation Management

Our claims team supports our underwriting strategy by working to provide a timely, good faith claims handling response to our policyholders. Claims excellence is achieved by timely investigation and handling of claims, settlement of meritorious claims for equitable amounts, maintenance of adequate case reserves, and control of claims loss settlement expenses.

Claims on insurance policies are received directly from the insured or through our independent agents. Our Claims Department supports our producer relationship strategy by working to provide a consistently responsive level of claim service to our policyholders.

Rickey Plunkett, our Director of Claims, supervises a staff of 16 employees with considerable years of experience in processing property and casualty insurance claims. Mr. Plunkett joined ICC in 2010 and has over 30 years of experience in claims management.

Julia B. Suiter, our Chief Legal Officer, supervises a staff of three employees, two of whom are also attorneys. Ms. Suiter joined ICC in 2009 and has been practicing law both in-house and in private practice for 24 years.

Technology

Our technology efforts are focused on supporting our strategy of differentiating ourselves from our competitors through use of data mining, business intelligence solutions, and data analysis to determine profitability of new and existing business and to better price risks that we underwrite.

We have streamlined internal processes to achieve operational efficiencies through the implementation of a policy and claim imaging and workflow system. This system provides online access to electronic copies of policies, quotes, inspections, and any other correspondence enabling our associates to quickly and efficiently underwrite policies and adjust claims as well as respond to our producers’ inquiries.

Since the system integrates all aspects of the policy life cycle, from underwriting to billing to claims, we are able to better automate all internal workflows through electronic routing thus lowering costs and providing better service to our customers. This system allows us to leverage loss control data for predictive analytics in both the claims and underwriting areas. For example, in the underwriting area, we can create pricing models taking into account the unique characteristics of our customers, such as neighborhoods, entertainment on site and average alcoholic beverage pricing.

We have implemented best in class virus or malware protections while still enabling our employees to work from any location. We are tested on a periodic basis to ensure our protections are sufficient.

We have the ability to scale since we are almost entirely a paperless organization. This allows us to integrate off-site employees just as if they are in the office. We intend to remain a leader in the industry by utilizing technology and data analysis to price our coverage based on the risk assumed and to both reduce accidents and provide a prompt response to claims.

As part of our disaster recovery program, we utilize a third party backup system to provide a complete copy of our production systems at an off-site location that is updated on a daily basis. We also have a generator that will allow the home office to operate in the event that power or access to our headquarters is disrupted. We test this disaster recovery plan bi-annually as well as continually expand its capabilities to eliminate business interruption to the best of our ability.

~ 9 ~

Reinsurance

In accordance with insurance industry practice, we reinsure a portion of our exposure and pay to the reinsurers a portion of the premiums received on all policies reinsured. Insurance policies written by us are reinsured with other insurance companies principally to:

|

· |

reduce net liability on individual risks; |

|

· |

mitigate the effect of individual loss occurrences (including catastrophic losses); |

|

· |

stabilize underwriting results; |

|

· |

decrease leverage; and |

|

· |

increase our underwriting capacity. |

Reinsurance can be facultative or treaty. Under facultative reinsurance, each policy or portion of a risk is reinsured individually. Under treaty reinsurance, an agreed-upon portion of a class of business is automatically reinsured. Reinsurance also can be classified as quota share reinsurance, pro rata reinsurance or excess of loss reinsurance. Under quota share reinsurance and pro rata reinsurance, the insurance company issuing the policy cedes a percentage of its insurance liability to the reinsurer in exchange for a like percentage of premiums, less a ceding commission. The company issuing the policy in turn recovers from the reinsurer the reinsurer’s share of all loss and settlement expenses incurred on those risks. Under excess of loss reinsurance, an insurer limits its liability to all or a particular portion of the amount in excess of a predetermined deductible or retention. Regardless of type, reinsurance does not legally discharge the insurance company issuing the policy from primary liability for the full amount due under the reinsured policies. However, the assuming reinsurer is obligated to reimburse the company issuing the policy to the extent of the coverage ceded.

We determine the amount and scope of reinsurance coverage to purchase each year based on a number of factors. These factors include the evaluation of the risks accepted, consultations with reinsurance intermediates and a review of market conditions, including the availability and pricing of reinsurance. A primary factor in the selection of reinsurers from whom we purchase reinsurance is their financial strength. Our reinsurance arrangements are generally renegotiated annually. We expect a 3.1% increase in spend for our 2017 reinsurance contracts. For the year ended December 31, 2016, we ceded to reinsurers $8.1 million of written premiums, compared to $7.8 million of written premiums for the year ended December 31, 2015. Of the $8.1 million spent on 2016 reinsurance premiums, $0.6 was from new contracts. Without the new contracts, 2016 spend would have been $7.5 million, or a decrease of 3.8%.

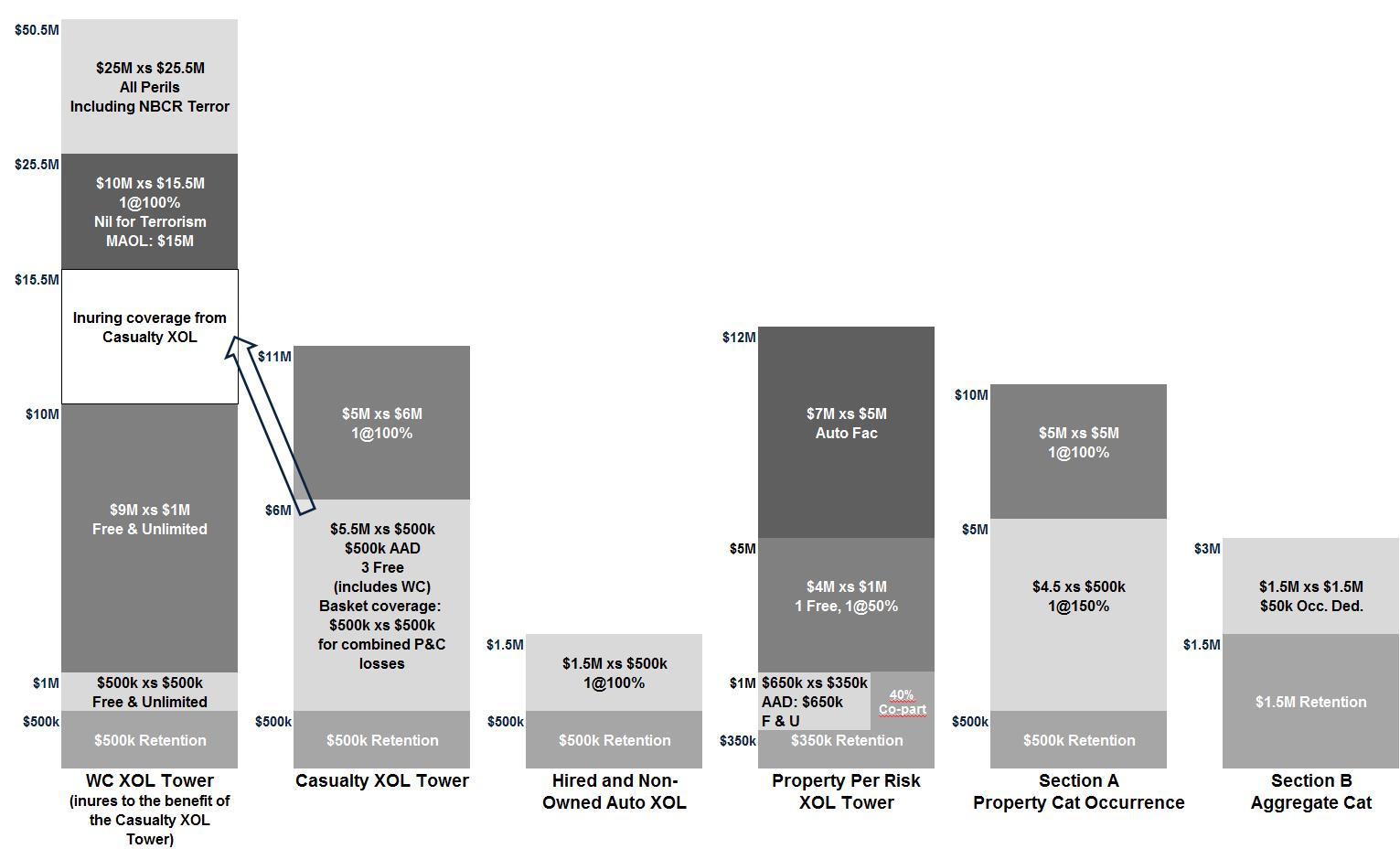

The chart below illustrates the 2017 reinsurance coverage under our excess of loss treaty for individual liability and property risks (with the defined terms listed below the chart):

~ 10 ~

|

|

|

|

|

Term |

|

Meaning |

|

1 @ x% |

|

“1” refers to the number of times that we reinstate the coverage. The number prior to the “%” sign indicates the overall cost to us when reinstating coverage. |

|

|

|

|

|

Aggregate Catastrophe |

|

An aggregate catastrophe treaty is a reinsurance cover designed to help us manage the effects of multiple extreme weather events on our results. |

|

|

|

|

|

Basket Coverage |

|

Excess liability insurance that attaches once retained losses for several lines of coverage (e.g., Workers compensation, Business Owners Liability, or Liquor Liability) reach a certain specified level. If we have one loss occurrence with $500,000 incurred on both a workers compensation claim and a liquor liability claim, this coverage limits our retention to $500,000 and not $500,000 per claim. |

|

|

|

|

|

Casualty |

|

For this chart, this refers to our liquor liability, business owners liability, workers compensation and any umbrella policies. |

|

|

|

|

|

|

|

|

|

Free & Unlimited |

|

This refers to the number and cost of reinstating the reinsurance coverage. With this wording, each separate loss occurrences above the retention will be covered by the treaty. |

|

|

|

|

|

Inures |

|

Our Workers Compensation Reinsurance contracts are first applied to reduce the loss subject to the Casualty XOL contract and are said to inure to the benefit of the Casualty XOL contract. |

|

|

|

|

|

MAOL |

|

This reinsurance sublimit puts a cap on the maximum loss any one life/claimant can contribute to the reinsurance recoverable. |

|

|

|

|

|

Per Risk |

|

Reinsurance in which the reinsurance limit and our loss retention apply “per risk,” rather than per accident, per event, or in the aggregate. |

|

|

|

|

|

Retention |

|

The amount of loss and settlement expense retained by us either per occurrence on casualty losses or per risk on property claims |

|

|

|

|

|

WC |

|

This is short for Workers Compensation. |

|

|

|

|

|

XOL |

|

This is short for Excess of Loss reinsurance coverage. |

|

|

|

|

|

xs |

|

This is short for Excess. For example, our Property per Risk tower has three separate contracts providing coverage. The top layer in that tower provides $7.0 million coverage for each risk with losses in excess of $5.0 million. |

We retain the first $500,000 of workers compensation losses. Losses in excess of the $500,000 are covered under our workers compensation excess of loss program (WC XOL Tower) up to $1.0 million. Losses above the $1.0 million are then covered under the second workers compensation treaty through $10.0 million. Above $10.0 million, losses would fall back to the casualty tower for an additional $5.5 million of coverage per employee. Losses above $15.5 million are covered under a new workers compensation cover that provides $10.0 million in excess of $15.5 million. We purchased a new cover that provideds $25.0 million of coverage in excess of $25.5 million for four direct policies issued by the Company.

Casualty risks (Casualty XOL Tower) (business owners property, liability, liquor liability, umbrella) are covered for $10.5 million in loss above a $500,000 retention for each loss occurrence.

Property per risk excess of loss program (Property Per Risk XOL Tower) provides coverage above our $350,000 retention up to $12.0 million on a treaty basis and facultative for a few risks above that to their full limits.

Property catastrophe reinsurance (Section A Property Cat Occurrence) provides coverage in any one event for $10.0 million of loss in excess of our $500,000 retention.

We also have aggregate catastrophe protection (Section B Aggregate Catastrophe) in the event that catastrophe losses retained by us exceeds $1.5 million in such year. This program allows us to aggregate storms losses where losses exceed $50,000 but fall below the $500,000 occurrence retention.

The insolvency or inability of any reinsurer to meet its obligations to us could have a material adverse effect on our results of operations or financial condition. Our reinsurance providers, the majority of whom are longstanding partners who understand our business, are all carefully selected with the help of our reinsurance broker. We monitor the solvency of reinsurers through regular review of their financial statements and, if available, their A.M. Best ratings. All of our reinsurance partners have at least an “A-” rating from A.M. Best. According to A.M. Best, companies with a rating of “A-” or better “have an excellent ability to meet their ongoing obligations to policyholders.”

~ 11 ~

The following table sets forth the largest amounts of loss and loss expenses recoverable from reinsurers as of December 31, 2016:

|

|

||||||||||

|

|

Losses and Settlement |

|||||||||

|

|

Expense Recoverable |

Percentage of |

||||||||

|

|

On Unpaid Claims |

Total |

A.M. Best |

|||||||

|

Reinsurance Company |

(In thousands) |

Recoverable |

Rating |

|||||||

|

Everest Reinsurance Company |

$ |

3,128 | 25.8% |

A+ |

||||||

|

Partner Reinsurance Company |

2,026 | 16.7% |

A+ |

|||||||

|

Aspen Insurance UK Ltd |

1,973 | 16.3% |

A |

|||||||

|

Hannover Ruckversicherungs |

1,934 | 16.0% |

A+ |

|||||||

|

Toa Reinsurance Company |

1,504 | 12.4% |

A+ |

|||||||

|

Swiss Reinsurance |

1,039 | 8.6% |

A+ |

|||||||

|

Platinum Underwriters |

874 | 7.2% |

A |

|||||||

|

Endurance |

612 | 5.0% |

A |

|||||||

|

Allied World Reinsurance |

588 | 4.9% |

A |

|||||||

|

Lloyd's Syndicate Number 435 |

29 | 0.2% |

A+ |

|||||||

|

All other reinsurers including anticipated subrogation |

(1,592) |

-13.1% |

A- or better |

|||||||

|

Total |

$ |

12,115 | 100.0% | |||||||

Losses and Settlement Expense Reserves

We are required by applicable insurance laws and regulations to maintain reserves for payment of loss and settlement expenses. These reserves are established for both reported claims and for claims incurred but not reported (IBNR), arising from the policies we have issued. The laws and regulations require that provision be made for the ultimate cost of those claims without regard to how long it takes to settle them or the time value of money. The determination of reserves involves actuarial and statistical projections of what we expect to be the cost of the ultimate settlement and administration of such claims. The reserves are set based on facts and circumstances then known, estimates of future trends in claims severity, and other variable factors such as inflation and changing judicial theories of liability.

Estimating the ultimate liability for losses and settlement expense is an inherently uncertain process. Therefore, the reserve for losses and settlement expense does not represent an exact calculation of that liability. Our reserve policy recognizes this uncertainty by maintaining reserves at a level providing for the possibility of adverse development relative to the estimation process. We do not discount our reserves to recognize the time value of money.

When a claim is reported to us, our claims personnel establish a “case reserve” for the estimated amount of the ultimate payment. This estimate reflects an informed judgment based upon general insurance reserving practices and on the experience and knowledge of our claims staff. In estimating the appropriate reserve, our claims staff considers the nature and value of the specific claim, the severity of injury or damage, and the policy provisions relating to the type of loss. Case reserves are adjusted by our claims staff as more information becomes available. It is our policy to resolve each claim as expeditiously as possible.

We maintain IBNR reserves to provide for already incurred claims that have not yet been reported and developments on reported claims. The IBNR reserve is determined by estimating our ultimate net liability for both reported and IBNR claims and then subtracting the case reserves and paid loss and settlement expnse for reported claims.

Each quarter, we compute our estimated ultimate liability using principles and procedures applicable to the lines of business written. However, because the establishment of loss reserves is an inherently uncertain process, we cannot provide assurance that ultimate losses will not exceed the established loss reserves. Adjustments in aggregate reserves, if any, are reflected in the operating results of the period during which such adjustments are made.

~ 12 ~

The following table provides information about open claims, reserves, and paid loss and settlement expense by business line on a direct basis only:

|

|

||||||||||

|

|

As of and for the year ended December 31, 2016 |

|||||||||

|

(In millions, except open claims count) |

Open Claims |

|

Total Reserves1 |

|

Case Reserves |

|

IBNR Reserves |

|

Paid Losses and Settlement Expense |

|

|

Commercial Multi-Peril (non-liability portion) |

147 |

$ 3.84 |

$ 3.95 |

$ (0.11) |

$ 8.33 |

|||||

|

Commercial Multi-Peril (liability portion) |

439 |

22.66 | 12.84 | 9.82 | 7.95 | |||||

|

Workers Compensation |

210 |

8.50 | 4.15 | 4.36 | 3.43 | |||||

|

Other Liability - occurrence |

177 |

17.37 | 6.56 | 10.81 | 5.83 | |||||

|

Grand Total |

973 |

$ 52.37 |

$ 27.49 |

$ 24.88 |

$ 25.54 |

|||||

|

|

||||||||||

| 1 |

Assumed reserves of $0.45 million are excluded from the Total Gross Reserves. Workers Compensation ($0.42 million assumed reserve) and Umbrella Liability ($0.03 million assumed reserve) are the only lines of business that have assumed reserves. |

|||||||||

The following table provides a reconciliation of beginning and ending unpaid losses and settlement expense reserve balances for the years ended December 31, 2016 and 2015, prepared in accordance with GAAP.

|

(In thousands) |

2016 |

2015 |

||||

|

Unpaid losses and settlement expense - beginning of the period: |

||||||

|

Gross |

$ |

61,056 |

$ |

64,617 | ||

|

Less: Ceded |

19,158 | 25,822 | ||||

|

Net |

41,898 | 38,795 | ||||

|

Increase (decrease) in incurred losses and settlement expense: |

||||||

|

Current year |

25,620 | 24,293 | ||||

|

Prior years |

(1,275) | (493) | ||||

|

Total incurred |

24,345 | 23,800 | ||||

|

Deduct: Loss and settlement expense payments for claims incurred: |

||||||

|

Current year |

7,649 | 6,466 | ||||

|

Prior years |

17,892 | 14,231 | ||||

|

Total paid |

25,541 | 20,697 | ||||

|

Net unpaid losses and settlement expense - end of the period |

40,702 | 41,898 | ||||

|

Plus: Reinsurance recoverable on unpaid losses |

12,115 | 19,158 | ||||

|

Gross unpaid losses and settlement expense - end of the period |

$ |

52,817 |

$ |

61,056 | ||

The estimation process for determining the liability for unpaid losses and settlement expense inherently results in adjustments each year for claims incurred (but not paid) in preceding years. Negative amounts reported for claims incurred related to prior years are a result of claims being settled for amounts less than originally estimated (favorable development). Positive amounts reported for claims incurred related to prior years are a result of claims being settled for amounts greater than originally estimated (unfavorable or adverse development).

Reconciliation of Reserve for Loss and Settlement Expenses

The following table shows the development of our reserves for unpaid loss and settlement expense from 2007 through 2016 on a GAAP basis. The top line of the table shows the liabilities at the balance sheet date, including losses incurred but not yet reported. The upper portion of the table shows the cumulative amounts subsequently paid as of successive years with respect to the liability. The lower portion of the table shows the reestimated amount of the previously recorded liability based on experience as of the end of each succeeding year. The estimates change as more information becomes known about the frequency and severity of claims for individual years. The redundancy (deficiency) exists when the reestimated liability for each reporting period is less (greater) than the prior liability estimate. The “cumulative redundancy (deficiency)” depicted in the table, for any particular calendar year, represents the aggregate change in the initial estimates over all subsequent calendar years.

Gross deficiencies and redundancies may be significantly more or less than net deficiencies and redundancies due to the nature and extent of applicable reinsurance.

~ 13 ~

As noted in the table below, since 2007 the Company has consistently selected initial ultimate loss picks that have proven to be redundant over time.

|

|

Year Ended December 31, |

|||||||||||||||||||

|

(In thousands) |

2007 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

||||||||||

|

Liability for unpaid loss and settlement expense, net of reinsurance recoverable |

$ |

33,393 |

$ |

40,040 |

$ |

39,932 |

$ |

37,708 |

$ |

36,204 |

$ |

35,976 |

$ |

36,340 |

$ |

38,795 |

$ |

41,898 |

$ |

40,702 |

|

Cumulative amount of liability paid through: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

One year later |

10,115 | 10,740 | 11,878 | 12,926 | 12,194 | 12,226 | 12,442 | 14,156 | 17,892 | |||||||||||

|

Two years later |

16,146 | 19,865 | 21,240 | 22,003 | 21,128 | 20,870 | 22,678 | 27,092 |

— |

|||||||||||

|

Three years later |

22,419 | 25,914 | 27,712 | 28,749 | 27,235 | 27,520 | 30,071 |

— |

— |

|||||||||||

|

Four years later |

25,498 | 30,217 | 31,840 | 32,561 | 31,167 | 32,086 |

— |

— |

— |

|||||||||||

|

Five years later |

27,696 | 32,210 | 34,044 | 34,429 | 33,183 |

— |

— |

— |

— |

|||||||||||

|

Six years later |

28,720 | 33,544 | 35,179 | 35,563 |

— |

— |

— |

— |

— |

|||||||||||

|

Seven years later |

29,184 | 34,352 | 35,923 |

— |

— |

— |

— |

— |

— |

|||||||||||

|

Eight years later |

29,460 | 34,888 |

— |

— |

— |

— |

— |

— |

— |

|||||||||||

|

Nine years later |

29,791 |

— |

— |

— |

— |

— |

— |

— |

— |

|||||||||||

|

Liability estimated after: |

||||||||||||||||||||

|

One year later |

33,441 | 37,860 | 38,222 | 36,699 | 35,553 | 35,151 | 36,698 | 38,305 | 40,623 | |||||||||||

|

Two years later |

32,242 | 37,709 | 37,212 | 36,840 | 35,763 | 35,545 | 36,210 | 39,813 |

— |

|||||||||||

|

Three years later |

32,156 | 36,205 | 37,239 | 37,170 | 36,083 | 35,418 | 36,914 |

— |

— |

|||||||||||

|

Four years later |

30,950 | 35,857 | 37,099 | 37,211 | 35,544 | 36,215 |

— |

— |

— |

|||||||||||

|

Five years later |

30,654 | 35,349 | 36,689 | 36,627 | 35,377 |

— |

— |

— |

— |

|||||||||||

|

Six years later |

30,194 | 35,111 | 36,445 | 36,645 |

— |

— |

— |

— |

— |

|||||||||||

|

Seven years later |

30,059 | 35,201 | 36,632 |

— |

— |

— |

— |

— |

— |

|||||||||||

|

Eight years later |

30,120 | 35,309 |

— |

— |

— |

— |

— |

— |

— |

|||||||||||

|

Nine years later |

30,118 |

— |

— |

— |

— |

— |

— |

— |

— |

|||||||||||

|

Cumulative total redundancy (deficiency) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross liability - end of year |

50,207 | 59,039 | 58,295 | 56,012 | 51,432 | 54,623 | 57,334 | 64,618 | 61,054 | 52,817 | ||||||||||

|

Reinsurance recoverable |

16,814 | 18,999 | 18,363 | 18,304 | 15,228 | 18,647 | 20,994 | 25,823 | 19,156 | 12,115 | ||||||||||

|

Net liability - end of year |

33,393 | 40,040 | 39,932 | 37,708 | 36,204 | 35,976 | 36,340 | 38,795 | 41,898 | 40,702 | ||||||||||

|

Gross reestimated liability - latest |

42,847 | 49,792 | 54,228 | 57,315 | 54,278 | 58,018 | 59,072 | 67,392 | 60,573 | |||||||||||

|

Reestimated reinsurance recoverables - latest |

|

12,729 |

|

14,483 |

|

17,596 |

|

20,670 |

|

18,901 |

|

21,803 |

|

22,158 |

|

27,579 |

|

19,950 |

|

|

|

Net reestimated liability - latest |

30,118 | 35,309 | 36,632 | 36,645 | 35,377 | 36,215 | 36,914 | 39,813 | 40,623 | |||||||||||

|

Gross cumulative redundancy (deficiency) |

3,275 | 4,731 | 3,300 | 1,063 | 827 | (239) | (574) | (1,018) | 1,275 | |||||||||||

Investments

Our investments in debt and equity securities are classified as available for sale and are carried at fair value with unrealized gains and losses reflected as a component of equity net of taxes. The goal of our investment activities is to complement and support our overall mission. As such, the investment portfolio’s goal is to maximize after-tax investment income and price appreciation while maintaining the portfolio’s target risk profile.

An important component of our operating results has been the return on invested assets. Our investment objectives are (i) to preserve and grow capital and surplus, in order to improve our competitive position and allow for expansion of insurance operations; (ii) to ensure sufficient cash flow and liquidity to fund expected liability payments and otherwise support our underwriting strategy; (iii) to provide a reasonable and stable level of income; and (iv) to maintain a portfolio which will assist in attaining the highest possible rating from A.M. Best. See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations —Quantitative and Qualitative Information about Market Risk.

In addition to any investments prohibited by the insurance laws and regulations of Illinois and any other applicable states, our investment policy prohibits the following investments and investing activities:

|

· |

short sales; |

|

· |

purchase of securities on margin; |

|

· |

hedge funds; |

~ 14 ~

|

· |

derivatives; |

|

· |

investment in commodities; |

|

· |

mortgage derivatives such as inverse floaters, interest only strips and principal only strips; |

|

· |

options, puts and futures contracts; |

|

· |

private placements; |

|

· |

non-U.S. dollar denominated securities; |

|

· |

any security that would not be in compliance with the regulations of the Illinois Department of Insurance. |

Our board of directors developed our investment policy and reviews the policy periodically. Exceptions to prohibitions discussed above are allowed with express written authority of the board of directors investment committee, but under no circumstance may such exception exceed 5% of our invested assets.

Our investment portfolio is managed by an independent third party firm.

The following table sets forth information concerning our investments in available for sale securities.

|

|

2016 |

2015 |

|||||||||

|

(In thousands) |

Cost or Amortized Cost |

|

Estimated Fair Value |

|

Cost or Amortized Cost |

|

Estimated Fair Value |

||||

|

Fixed maturity securities: |

|||||||||||

|

U.S. treasury |

$ |

1,244 |

$ |

1,241 |

$ |

1,243 |

$ |

1,233 | |||

|

MBS/ABS/CMBS |

19,751 | 19,677 | 17,949 | 18,011 | |||||||

|

Corporate |

27,594 | 28,345 | 29,537 | 29,595 | |||||||

|

Municipal |

14,340 | 14,871 | 15,266 | 16,356 | |||||||

|

Total fixed maturity securities |

62,929 | 64,134 | 63,995 | 65,195 | |||||||

|

Equity securities: |

|||||||||||

|

Common Equity/ETF securities1 |

6,312 | 6,983 | 9,282 | 8,885 | |||||||

|

Preferred Stocks |

2,925 | 2,798 |

— |

— |

|||||||

|

Total equity securities |

9,237 | 9,781 | 9,282 | 8,885 | |||||||

|

Total AFS securities |

$ |

72,166 |

$ |

73,915 |

$ |

73,277 |

$ |

74,080 | |||

|

1 Equity securities consist of exchange traded funds (ETF) |

|||||||||||

The following table summarizes the distribution of our portfolio of fixed maturity investments as a percentage of total estimated fair value based on credit ratings assigned by Standard & Poor’s Corporation (S&P):

|

|

2016 |

2015 |

|||||||||||

|

Rating1 |

|

Estimate Fair Value |

|

Percent of Total2 |

|

Estimate Fair Value |

|

Percent of Total2 |

|||||

|

AAA |

$ |

9,235 | 14.4% |

$ |

6,585 | 10.1% | |||||||

|

AA |

24,820 | 38.7% | 27,447 | 42.1% | |||||||||

|

A |

17,893 | 27.9% | 20,471 | 31.4% | |||||||||

|

BBB |

10,069 | 15.7% | 10,692 | 16.4% | |||||||||

|

BB |

2,116 | 3.3% |

— |

0.0% | |||||||||

|

Total |

$ |

64,134 | 100% |

$ |

65,195 | 100.0% | |||||||

|

|

|||||||||||||

|

1The ratings set forth in this table are based on the ratings assigned by S&P. If S&P’s ratings were unavailable, the equivalent ratings supplied by Moody’s Investor Service, Fitch Investors Service, Inc. or the NAIC were used where available. |

|||||||||||||

|

|

|||||||||||||

|

2Represents percent of fair value for classification as a percent of the total portfolio. |

|||||||||||||

~ 15 ~

The table below sets forth the maturity profile of our debt securities December 31, 2016. Expected maturities could differ from contractual maturities because borrowers may have the right to call or prepay obligations, with or without call or prepayment penalties.

|

(In thousands) |

Amortized Cost |

Estimated Fair Value1 |

|||

|

Less than one year |

$ |

2,518 |

$ 2,526 |

||

|

One through five years |

15,961 | 16,292 | |||

|

Five through ten years |

15,996 | 16,753 | |||

|

Greater than ten years |

8,703 | 8,886 | |||

|

MBS/ABS |

19,751 | 19,677 | |||

|

Total debt securities |

$ |

62,929 |

$ 64,134 |

||

|

|

|||||

|

1Debt securities are carried at fair value in our financials statements |

|||||

At December 31, 2016, the average maturity of our fixed maturity investment portfolio was 6.71 years and the average duration was 4.87 years. As a result, the fair value of our investments may fluctuate significantly in response to changes in interest rates. In addition, we may experience investment losses to the extent our liquidity needs require the disposition of fixed maturity securities in unfavorable interest rate environments.

We use quoted values and other data provided by independent pricing services as inputs in our process for determining fair values of our investments. The pricing services cover substantially all of the securities in our portfolio for which publicly quoted values are not available. The pricing services’ evaluations represent an exit price, a good faith opinion as to what a buyer in the marketplace would pay for a security in a current sale. The pricing is based on observable inputs either directly or indirectly, such as quoted prices in markets that are active, quoted prices for similar securities at the measurement date, or other inputs that are observable.

Our independent third party investment manager provides us with pricing information that they obtain from independent pricing services, to determine the fair value of our fixed maturity securities. After performing a detailed review of the information obtained from the pricing service, limited adjustments may be made by the manager to the values provided.

Our average cash and invested assets, net investment income and return on average cash and invested assets for the years ended December 31, 2016 and 2015 were as follows:

|

(In thousands) |

2016 |

2015 |

||||||

|

Average cash and invested assets |

$ |

78,660 |

$ |

74,869 | ||||

|

Net investment income |

1,968 | 1,333 | ||||||

|

Return on average cash and invested assets |

2.5% | 1.8% | ||||||

A.M. Best Rating

A.M. Best Company, Inc. (“A.M. Best”) rates insurance companies based on factors of concern to policyholders. A.M. Best currently assigns a “B++” (Good) rating to ICC. This rating is the fifth highest out of 15 rating classifications. The latest rating evaluation by A.M. Best occurred on February 23, 2016. According to the A.M. Best guidelines, companies rated “B++” are considered by A.M. Best to have “a good ability to meet their ongoing insurance obligations.” The rating evaluates the claims paying ability of a company, and is not a recommendation on the merits of an investment in our common stock.

In evaluating a company’s financial and operating performance, A.M. Best reviews:

|

· |

the company’s profitability, leverage and liquidity; |

|

· |

its book of business; |

|

· |

the adequacy and soundness of its reinsurance; |

|

· |

the quality and estimated fair value of its assets; |

|

· |

the adequacy of its reserves and surplus; |

|

· |

its capital structure; |

|

· |

the experience and competence of its management; and |

|

· |

its marketing presence. |

~ 16 ~

In its ratings report on ICC, A.M. Best stated that ICC’s rating reflected ICC’s improved operating results and risk-adjusted capitalization over the past five years, the ability of current management to continue to improve rates and grow premium while maintaining a slow growing policy count, ICC’s combined ratios trending in a positive direction with results under 100% for 2014, 2015, and 2016, traction gained with respect to expense initiatives, strength in loss reserves with redundancies on both an accident and calendar year basis and strong underwriting expertise and a long-standing position within the food and beverage industry in the Midwest. These factors were somewhat offset by ICC’s overall weak operating return measures. Although underwriting results are improving, the past five years have fluctuated. A.M. Best has affirmed ICC’s outlook as positive.

Competition

Given our exclusive focus on providing insurance products and services for the food and beverage industry, the market conditions for our business and, accordingly, our competition, varies geographically based upon the states in which we operate and also by the segment of the food and beverage industry (e.g., bars versus fine dining). In the most competitive states in which we operate (Illinois, Indiana and Wisconsin), our primary competitors are insurance companies with products targeting the food and beverage industry, such as Society Mutual Insurance Company in all three states, as well as Badger Mutual Insurance Company, Wilson Mutual Insurance Company and West Bend Mutual Insurance Company in Wisconsin. In other jurisdictions, such as Iowa and Minnesota, we compete with both the carriers with products identified above (such as Badger Mutual Insurance Company, Wilson Mutual Insurance Company and Founders Insurance Company) and excess and surplus line insurance companies (such as Scottsdale Insurance Company and Lloyd’s of London). In other jurisdictions, like Missouri, our primary competitors are larger regional and national insurance companies without a focus on the food and beverage industry (such as Allied Insurance Company, Auto-Owners Insurance Company and Travelers Insurance Company) and excess and surplus line insurance companies (such as EverGuard Insurance Services, Inc. and Lloyd’s of London). When evaluating the franchise and fine dining segment of the food and beverage industry, we compete with national insurance carriers, such as Allied Insurance Company, Travelers Insurance Company and The Hartford Insurance Company.

Despite significant competition, we believe we continue to maintain strong market share.

|

|

Number of Eating and Drinking Places in 2015 |

Number of Locations Insured by ICC at December 31, 2016 |

Approximate Market Share (%) |

||

|

Illinois |

27,189 |

2,736 |

10.1% |

||

|

Iowa |

6,129 |

1,296 |

21.1% |

||

|

Indiana |

11,620 |

593 |

5.1% |

||

|

Michigan1 |

16,110 |

N/A |

N/A |

||

|

Minnesota |

9,709 |

922 |

9.5% |

||

|

Missouri |

10,903 |

1,030 |

9.4% |

||

|

Ohio2 |

22,023 |

31 |

0.1% |

||

|

Wisconsin |

12,170 |

262 |

2.2% |

||

|

Total |

115,853 |

6,870 |

5.9% |

||

|

Total (w/o MI) |

99,743 |

6,870 |

6.9% |

||

|

|

|||||

|

Source: National Restaurant Association; ICC |

|||||

|

|

|||||

|

1We expect to begin writing premium in Michigan as early as 2018 |

|||||

|

|

|||||

|

2We began accepting business in Ohio in August 2016 |

|||||

Employees

As of December 31, 2016, we had 91 full-time equivalent employees. None of these employees are covered by a collective bargaining agreement, and we believe that our employee relations are good.

~ 17 ~

Regulation

General

We are subject to extensive regulation, particularly at the state level. The method, extent and substance of such regulation varies by state, but generally has its source in statutes and regulations that establish standards and requirements for conducting the business of insurance and that delegate regulatory authority to state insurance regulatory agencies. In general, such regulation is intended for the protection of those who purchase or use insurance products, not the companies that write the policies. These laws and regulations have a significant impact on our business and relate to a wide variety of matters including accounting methods, agent and company licensure, claims procedures, corporate governance, examinations, investing practices, policy forms, pricing, trade practices, reserve adequacy and underwriting standards.

State insurance laws and regulations require ICC to file financial statements with state insurance departments everywhere it does business, and the operations of ICC and its accounts are subject to examination by those departments at any time. ICC prepares statutory financial statements in accordance with accounting practices and procedures prescribed or permitted by these departments.

Premium rate regulation varies greatly among jurisdictions and lines of insurance. In most states in which our subsidiaries write insurance, premium rates for the various lines of insurance are subject to either prior approval or limited review upon implementation. States require rates for property-casualty insurance that are adequate, not excessive, and not unfairly discriminatory.

Many jurisdictions have laws and regulations that limit an insurer’s ability to withdraw from a particular market. For example, states may limit an insurer’s ability to cancel or non-renew policies. Laws and regulations that limit cancellation and non-renewal may restrict our ability to exit unprofitable marketplaces in a timely manner.

Examinations

Examinations are conducted by the Illinois Department of Insurance every three to five years. The Illinois Department of Insurance’s last examination of ICC was in February 2012 covering the period from 2007-2011. The examination did not result in any adjustments to our financial position. In addition, there were no substantive qualitative matters indicated in the examination report that had a material adverse impact on our operations.

NAIC Risk-Based Capital Requirements

In addition to state-imposed insurance laws and regulations, the NAIC has adopted risk-based capital requirements that require insurance companies to calculate and report information under a risk-based formula. These risk-based capital requirements attempt to measure statutory capital and surplus needs based on the risks in a company’s mix of products and investment portfolio. Under the formula, a company first determines its “authorized control level” risk-based capital. This authorized control level takes into account (i) the risk with respect to the insurer’s assets; (ii) the risk of adverse insurance experience with respect to the insurer’s liabilities and obligations, (iii) the interest rate risk with respect to the insurer’s business; and (iv) all other business risks and such other relevant risks as are set forth in the risk-based capital instructions. A company’s “total adjusted capital” is the sum of statutory capital and surplus and such other items as the risk-based capital instructions may provide. The formula is designed to allow state insurance regulators to identify weakly capitalized companies.