Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - CENTRUS ENERGY CORP | exhibit_32-1x20161231.htm |

| EX-31.2 - EXHIBIT 31.2 - CENTRUS ENERGY CORP | exhibit_31-2x20161231.htm |

| EX-31.1 - EXHIBIT 31.1 - CENTRUS ENERGY CORP | exhibit_31-1x20161231.htm |

| EX-23.1 - EXHIBIT 23.1 - CENTRUS ENERGY CORP | exhibit_23-1x20161231.htm |

| EX-21 - EXHIBIT 21 - CENTRUS ENERGY CORP | exhibit_21x20161231.htm |

| EX-3.2 - EXHIBIT 3.2 - CENTRUS ENERGY CORP | exhibit_3-2x20161231.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2016

Commission file number 1-14287

Centrus Energy Corp.

Delaware | 52-2107911 |

(State of incorporation) | (IRS Employer Identification No.) |

6901 Rockledge Drive, Suite 800, Bethesda, Maryland 20817

(301) 564-3200

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Class A Common Stock, par value $0.10 per share | NYSE MKT LLC |

Rights to purchase Series A Participating Cumulative Preferred Stock, par value $1.00 per share | NYSE MKT LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o. No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o. No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | o | Accelerated filer | o | Non-accelerated filer | o | Smaller reporting company | ý |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ý No o

The aggregate market value of Common Stock held by non-affiliates computed by reference to the price at which the Common Stock was last sold as reported on the New York Stock Exchange as of June 30, 2016, was $17.0 million. As of March 28, 2017, there were 7,563,600 shares of the registrant’s Class A Common Stock and 1,436,400 shares of the registrant’s Class B Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for the 2017 annual meeting of shareholders to be filed subsequent to the date hereof are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

Page | ||

PART I | ||

PART II | ||

PART III | ||

PART IV | ||

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, including Management’s Discussion and Analysis of Financial Condition and Results of Operations in Part II, Item 7, contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934 - that is, statements related to future events. In this context, forward-looking statements may address our expected future business and financial performance, and often contain words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “will”, “should”, “could”, “would” or “may” and other words of similar meaning. Forward-looking statements by their nature address matters that are, to different degrees, uncertain. For Centrus Energy Corp., particular risks and uncertainties that could cause our actual future results to differ materially from those expressed in our forward-looking statements include, risks and uncertainties related to the adoption of fresh start accounting; risks related to our significant long-term liabilities, including material unfunded defined benefit pension plan obligations and postretirement health and life benefit obligations; risks relating to our outstanding 8.0% paid-in-kind (“PIK”) toggle notes (the “PIK Toggle Notes”) maturing in September

2

2019, our 8.25% notes due 2027 (the “8.25% Notes”) and our Series B Senior Preferred Stock (the Series B Preferred Stock), including the potential termination of the guarantee by United States Enrichment Corporation (“Enrichment Corp.”) of the PIK Toggle Notes; risks related to the limited trading markets in our securities; risks related to our ability to maintain the listing of our common stock on the NYSE MKT LLC; risks related to the use of our net operating losses (“NOLs”) and net unrealized built-in losses (“NUBILs”) to offset future taxable income and the use of the rights plan to prevent an “ownership change” as defined in Section 382 of the Internal Revenue Code and our ability to generate taxable income to utilize all or a portion of the NOLs and NUBILs prior to the expiration thereof; the continued impact of the March 2011 earthquake and tsunami in Japan on the nuclear industry and on our business, results of operations and prospects; the impact and potential extended duration of the current supply/demand imbalance in the market for low-enriched uranium (“LEU”); our dependence on others for deliveries of LEU including deliveries from the Russian government entity Joint Stock Company “TENEX” (“TENEX”) under a commercial supply agreement with TENEX (the “Russian Supply Agreement”); risks related to our ability to sell the LEU we procure pursuant to our purchase obligations under our supply agreements including the Russian Supply Agreement; risks relating to our sales order book, including uncertainty concerning customer actions under current contracts and in future contracting due to market conditions and lack of current production capability; risks associated with our reliance on third-party suppliers to provide essential services to us; pricing trends and demand in the uranium and enrichment markets and their impact on our profitability; movement and timing of customer orders; risks related to trade barriers and contract terms that limit our ability to deliver LEU to customers; risks related to actions that may be taken by the U.S. government, the Russian government or other governments that could affect our ability or the ability of our sources of supply to perform under their contract obligations to us, including the imposition of sanctions, restrictions or other requirements; the impact of government regulation including by the U.S. Department of Energy and the U.S. Nuclear Regulatory Commission; uncertainty regarding our ability to commercially deploy competitive enrichment technology; risks and uncertainties regarding funding for the American Centrifuge project and our ability to perform under our agreement with UT-Battelle, LLC, the management and operating contractor for Oak Ridge National Laboratory, for continued research and development of the American Centrifuge technology; the potential for further demobilization or termination of the American Centrifuge project; risks related to the current demobilization of portions of the American Centrifuge project, including risks that the schedule could be delayed and costs could be higher than expected; potential strategic transactions, which could be difficult to implement, disrupt our business or change our business profile significantly; the outcome of legal proceedings and other contingencies (including lawsuits and government investigations or audits); the competitive environment for our products and services; changes in the nuclear energy industry; the impact of financial market conditions on our business, liquidity, prospects, pension assets and insurance facilities; revenue and operating results can fluctuate significantly from quarter to quarter, and in some cases, year to year; and other risks and uncertainties discussed in this and our other filings with the Securities and Exchange Commission.

For a discussion of these risks and uncertainties and other factors that may affect our future results, please see Item 1A, Risk Factors, and the other sections of this Annual Report on Form 10-K. Readers are urged to carefully review and consider the various disclosures made in this report and in our other filings with the Securities and Exchange Commission that attempt to advise interested parties of the risks and factors that may affect our business. We do not undertake to update our forward-looking statements to reflect events or circumstances that may arise after the date of this Annual Report on Form 10-K except as required by law.

3

PART I

Item 1. Business

Overview

Centrus Energy Corp. (“Centrus” or the “Company”) is a trusted supplier of low-enriched uranium (“LEU”) for commercial nuclear power plants. References to “Centrus”, the “Company”, or “we” include Centrus Energy Corp. and its wholly owned subsidiaries as well as the predecessor to Centrus, unless the context otherwise indicates. LEU is a critical component in the production of nuclear fuel for reactors that produce electricity. We supply LEU to both domestic and international utilities for use in nuclear reactors worldwide. We are a leader in the development of advanced uranium enrichment technology and are performing research and demonstration work to support U.S. energy and national security through our contract with UT-Battelle, LLC (“UT-Battelle”), the operator of Oak Ridge National Laboratory (“ORNL”).

As a long-term supplier of LEU to our customers, our goal is to provide value through the reliability and diversity of our supply sources. We provide LEU from multiple sources including our inventory, medium- and long- term supply contracts and spot purchases. Our long-term objective is to resume commercial enrichment production and we are exploring alternative approaches to that end.

We have a contract with UT-Battelle to conduct research and development of our advanced centrifuge technology for the U.S. government. We believe that this technology could play a critical role in meeting our national and energy security needs and achieving our nation’s non-proliferation objectives.

The nuclear industry in general, and the nuclear fuel industry in particular, is in a period of significant change, which could significantly transform the competitive landscape Centrus faces. The nuclear fuel cycle industry remains oversupplied, creating downward pressures on commodity pricing, with uncertainty regarding the timing of industry expansion globally. Changes in the competitive landscape may adversely affect pricing trends, change customer spending patterns, or create uncertainty. To address these changes, we may seek to adjust our cost structure and operations and evaluate opportunities to grow our business organically or through acquisitions and other strategic transactions. We are actively considering, and expect to consider from time to time in the future, potential strategic transactions, which could involve, without limitation, acquisitions and/or dispositions of businesses or assets, joint ventures or investments in businesses, products or technologies. In connection with any such transaction, we may seek additional debt or equity financing, contribute or dispose of assets, assume additional indebtedness, or partner with other parties to consummate a transaction.

Our Business Today

In 2016, Centrus continued to demonstrate why it is a trusted partner to the global nuclear industry. During the year, Centrus’ management team positioned the Company for long-term success with a focus on strengthening our strategic relationships within the nuclear industry, expanding sales to both new and existing customers, and pursuing new business development opportunities.

Our competitive strengths include:

• | Positioned for the long term: Centrus has long-term sales and supply contracts in place that extend well into the next decade, which will provide a stream of revenue for many years and provides a foundation for growth as the global enrichment market recovers. Without the large capital and overhead costs of a production facility, Centrus is positioned to continue to obtain supply at competitive prices from an oversupplied market, which we believe will strengthen our position for the future. |

4

• | Diverse supply portfolio: Centrus’ leadership team is focused on expanding and diversifying our supply base to provide additional value to our customers. For example, Centrus has entered into new agreements with suppliers of enriched uranium, expanding our sources of supply and increasing the number of possible delivery locations for enriched uranium. In late 2015, Centrus also successfully completed a renegotiation with our Russian supplier under our primary supply contract to better align our purchase obligations in light of market conditions generally, our sales order book, and restrictions on the import of Russian LEU and to extend the agreement to at least 2026. In addition, Centrus has acquired or will acquire additional enriched uranium supply from the excess inventories of utility operators of nuclear power plants and from other primary and secondary sources of enriched uranium supply. Together, this portfolio makes Centrus a highly diversified supplier of LEU. |

• | Developing U.S. enrichment technology: Centrus continues to demonstrate its core expertise and world-leading technical, engineering and manufacturing capabilities in Oak Ridge, Tennessee through our contract with the operator of ORNL. Centrus is continuing to advance its U.S. centrifuge technology with a view to deploying a commercial scale enrichment facility over the long term once market conditions recover. We continue to pursue strategic relationships that would capitalize on Centrus’ unique assets, including our operational expertise and our significant technical capabilities. |

We believe that Centrus’ position as a leading provider of enriched uranium and our long-standing global relationships will enable an increase in future market share for the Company. We are well-positioned to capitalize on our heritage, industry-wide relationships, and diversity of supply to provide reliable and competitive sources of enriched uranium. Centrus continues to be valued by our customers as a source of diversity, stability, and competition in the enrichment market. Moreover, our smaller size and lower fixed costs can be advantageous in the current excess capacity market.

For a discussion of the potential risks and uncertainties facing our business, see Item 1A, Risk Factors.

Uranium and Enrichment

LEU consists of two components: separative work units (“SWU”) and uranium. Uranium is a naturally occurring element and is mined from deposits located in Kazakhstan, Canada, Australia, the United States and several other countries. According to the World Nuclear Association, there are adequate measured resources of uranium to fuel nuclear power at current usage rates for about 90 years. In its natural state, uranium is principally comprised of two isotopes: uranium-235 (“U235”) and uranium-238 (“U238”). The concentration of U235 in natural uranium is only 0.711% by weight. Most commercial nuclear power reactors require LEU fuel with a U235 concentration greater than natural uranium and up to 5% by weight. Uranium enrichment is the process by which the concentration of U235 is increased to that level.

SWU is a standard unit of measurement that represents the effort required to transform a given amount of natural uranium into two components: enriched uranium having a higher percentage of U235 and depleted uranium having a lower percentage of U235. The SWU contained in LEU is calculated using an industry standard formula based on the physics of enrichment. The amount of enrichment deemed to be contained in LEU under this formula is commonly referred to as its SWU component and the quantity of natural uranium used in the production of LEU under this formula is referred to as its uranium or “feed” component.

While in some cases customers purchase both the SWU and uranium components of LEU from us, utility customers typically provide uranium to us as part of their enrichment contracts, and in exchange we deliver LEU to these customers and charge for the SWU component. Title to uranium provided by customers generally remains with the customer until delivery of LEU, at which time title to LEU is transferred to the customer and we take title to the uranium.

5

The following outlines the steps for converting natural uranium into LEU fuel, commonly known as the nuclear fuel cycle:

Mining and Milling. Natural, or unenriched, uranium is removed from the earth in the form of ore and then crushed and concentrated.

Conversion. Uranium concentrates (“U3O8”) are combined with fluorine gas to produce uranium hexafluoride (“UF6”), a solid at room temperature and a gas when heated. UF6 is shipped to an enrichment plant.

Enrichment. UF6 is enriched in a process that increases the concentration of the U235 isotope in the UF6 from its natural state of 0.711% up to 5%, which is usable as a fuel for light water commercial nuclear power reactors.

Fuel Fabrication. LEU is then converted to uranium oxide and formed into small ceramic pellets by fabricators. The pellets are loaded into metal tubes that form fuel assemblies, which are shipped to nuclear power plants.

Nuclear Power Plant. The fuel assemblies are loaded into nuclear reactors to create energy from a controlled chain reaction. Nuclear power plants generate approximately 20% of U.S. electricity and 11% of the world’s electricity.

Used Fuel Storage. After the nuclear fuel has been in a reactor for several years, its efficiency is reduced and the assembly is removed from the reactor’s core. The used fuel is warm and radioactive and is kept in a deep pool of water for several years. Many utilities have elected to then move the used fuel into steel or concrete and steel casks for interim storage.

Products and Services

Low-Enriched Uranium

Revenue from our LEU segment is derived primarily from:

• | sales of the SWU component of LEU, |

• | sales of both the SWU and uranium components of LEU, and |

• | sales of natural uranium. |

Revenue for our LEU segment accounted for approximately 88% of our total revenue in 2016. Our customers are primarily domestic and international utilities that operate nuclear power plants. Our agreements with electric utilities are primarily long-term, fixed-commitment contracts under which our customers are obligated to purchase a specified quantity of the SWU component of LEU (or the SWU and uranium components of LEU) from us. Our agreements for natural uranium sales are generally shorter-term, fixed-commitment contracts.

Contract Services

As described below under Advanced Technology, Manufacturing, and Engineering Capability, we perform American Centrifuge engineering and testing activities as a contractor for UT-Battelle, the management and operating contractor of ORNL for the U.S Department of Energy (“DOE”). Revenue and cost of sales for work that we perform as a contractor to UT-Battelle are reported in the contract services segment.

6

Revenue by Geographic Area, Major Customers and Segment Information

Revenue attributed to domestic and foreign customers, including customers in a foreign country representing 10% or more of total revenue, follows (in millions):

Year Ended December 31, | |||||||

2016 | 2015 | ||||||

United States | $ | 242.8 | $ | 272.8 | |||

Foreign: | |||||||

Japan | 49.1 | 77.8 | |||||

Belgium | * | 55.5 | |||||

Other | 19.4 | 12.1 | |||||

68.5 | 145.4 | ||||||

Total revenue | $ | 311.3 | $ | 418.2 | |||

* less than 10% | |||||||

In 2016, our 10 largest customers represented approximately 90% of total revenue and our four largest customers represented approximately 50% of total revenue. In our LEU segment, revenue from Exelon Corporation, South Carolina Electric & Gas and American Electric Power represented approximately 15%, 12% and 11%, respectively, of total revenue in 2016. In 2015, revenue from Exelon Corporation, Synatom S.A. and Kansai Electric Power Co., Inc. represented approximately 25%, 13%, and 10%, respectively, of total revenue. In our contract services segment, the U.S. government and its contractors represented approximately 12% of total revenue in 2016 and 15% of total revenue in 2015. No other customer represented more than 10% of total revenue in 2016 or 2015. Revenue by segment follows (in millions):

Year Ended December 31, | |||||||

2016 | 2015 | ||||||

LEU segment revenue | $ | 272.8 | $ | 355.4 | |||

Contract services segment revenue | 38.5 | 62.8 | |||||

Total revenue | $ | 311.3 | $ | 418.2 | |||

Reference is made to segment information reported in Note 18 to the consolidated financial statements.

SWU and Uranium Sales Order Book

The SWU component of LEU is typically bought and sold under long-term contracts with deliveries over several years. Our order book of sales under contract (“order book”) extends for more than a decade. As of December 31, 2016, our order book was $1.4 billion compared to $2.3 billion at December 31, 2015. As previously disclosed, some long-term contracts in our order book were established with milestones related to the deployment of the American Centrifuge Plant (“ACP”) in Piketon, Ohio, that permit termination with respect to portions of the contract under limited circumstances. The decline in the order book during 2016 includes $0.7 billion of future sales that were cancelled following customer termination for unmet milestones. We estimate that approximately 5% of our order book as of December 31, 2016, remains at risk due to milestones related to ACP deployment, down from 35% as of December 31, 2015.

We anticipate SWU and uranium revenue from the sales currently under contract in our order book in a range of $175 million to $200 million during 2017.

Most of our contracts provide for fixed purchases of SWU during a given year. Our estimate of the aggregate dollar amount of future SWU and uranium sales is partially based on customers’ estimates of the timing and size of their fuel requirements and other assumptions that are subject to change. For example, depending on the terms of

7

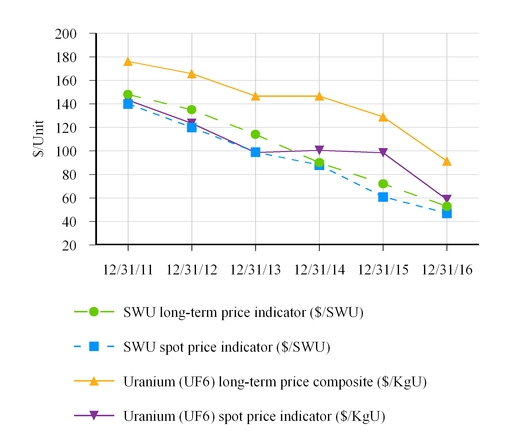

specific contracts, the customer may be able to increase or decrease the quantity delivered within an agreed range. Our order book estimate is also based on our estimates of selling prices, which are subject to change. For example, depending on the terms of specific contracts, prices may be adjusted based on escalation using a general inflation index, published SWU price indicators prevailing at the time of delivery, and other factors, all of which are variable. We use external composite forecasts of future market prices and inflation rates in our pricing estimates. Refer to Item 1A, Risk Factors, for a discussion of risks related to our order book.

Russian Supply Agreement

Our leading supplier of SWU is the Russian government entity Joint Stock Company “TENEX” (“TENEX”). Under a 2011 agreement with TENEX (the “Russian Supply Agreement”), we purchase SWU contained in LEU received from TENEX, and we deliver natural uranium to TENEX for the LEU’s uranium component. In December 2015, we successfully negotiated an amendment to the Russian Supply Agreement to better align our purchase obligations in light of market conditions generally, our sales order book, and restrictions on the import of Russian LEU. The amendment extended the Russian Supply Agreement beyond 2022 and gives us the right to reschedule quantities of SWU into the period 2023-2026, in return for the purchase of additional SWU in those years. Depending on the total purchase obligations rescheduled to 2023-2026, we may defer certain limited quantities beyond 2026.

The LEU that we obtain from TENEX under the Russian Supply Agreement is subject to quotas and other restrictions that could adversely affect our ability to sell the SWU component that we purchase in the United States and other markets. The Russian Supply Agreement only gives us the right to use a portion of this quota, which is less than the amount of Russian LEU that we need to order to meet our SWU purchase obligations to TENEX. We can ask TENEX for additional quota, which they can allocate to us at their discretion. Refer below to Competition and Foreign Trade - Limitations on Imports of LEU from Russia.

We expect that a portion of the Russian LEU that we order during the term of the Russian Supply Agreement will need to be delivered to customers who will use it in foreign reactors. The Russian LEU that we deliver to foreign customers can be delivered either at fabrication facilities in the United States or in foreign countries. The amount of SWU we must purchase from TENEX under the Russian Supply Agreement exceeds our current sales order book and therefore we will need to make new sales to place all the Russian LEU we must order to meet our SWU purchase obligations to TENEX. In addition, due to quotas and other limitations, not all of our delivery obligations under our existing contracts can be met with Russian LEU. We procure LEU from other sources in order to supply the customers who cannot be supplied effectively with Russian LEU or from our existing inventory.

Advanced Technology, Manufacturing, and Engineering Capability

The Company has a long record as a global leader in advanced technology, manufacturing and engineering. Our manufacturing, engineering and testing facilities and our highly-trained workforce are deeply engaged in advancing the next generation of uranium enrichment technology. We are exploring a number of options for returning to domestic production in the future. The economics for commercial deployment of new enrichment capacity are severely challenged by the current supply/demand imbalance in the market for LEU and related downward pressure on market prices for SWU, which are now at historic lows. Market conditions, however, are expected to improve in the long term.

Since September 2015, our government contracts with UT-Battelle have provided for continued engineering and testing work on the American Centrifuge technology at the Company’s facilities in Oak Ridge, Tennessee. In October 2015, DOE issued a report to Congress evaluating a range of possible technologies to restore U.S. domestic uranium enrichment to meet U.S. national security needs through 2041. DOE’s report stated that the American Centrifuge is the “most technically advanced and lowest risk option” for restoring U.S. uranium enrichment capability to meet long-term national security requirements. In September 2016, we entered into a new contract with UT-Battelle valued at approximately $25 million for the period from October 1, 2016, through September 30, 2017. The contract provides for payments for monthly reports of approximately $2.0 million per month and additional

8

aggregate payments of $1.0 million based on completion of certain milestones. The contract is currently being funded incrementally. Funding for the program is provided to UT-Battelle by the federal government which is currently operating under a continuing resolution.

In September 2015, Centrus completed a successful three-year demonstration of the existing American Centrifuge technology at its facility in Piketon, Ohio, with 120 machines linked together in a cascade to simulate industrial operating conditions. On February 19, 2016, we announced our decision to commence with the decontamination and decommissioning (“D&D”) of the Piketon demonstration cascade, and to reduce staffing levels. Refer below to Facility Decontamination and Decommissioning. We lease the Piketon facility from DOE and the current lease term is through June 2019. We have the option to extend the lease term for additional five-year terms. Rent is based on the cost of lease administration and regulatory oversight in Piketon and was approximately $1.5 million for 2016. DOE may terminate for default, including if DOE is able to exercise its remedies with respect to the ACP under our agreement dated June 17, 2002, as amended (the “2002 DOE-USEC Agreement”), or if there is an uncured production shortfall. The lease provides DOE with the right to terminate upon notice and applicable cure period in the event we fail to produce an average of 1 million SWU per year measured over a rolling two year performance period commencing with the two year period starting in April 2011. We are not currently producing SWU. In the event DOE issues a notice under the lease, we would have 180 days to cure or to begin to cure if more than 180 days are reasonably required to cure.

Competition and Foreign Trade

We estimate that the enrichment industry market is currently about 50 million SWU per year. Our global market share is approximately 4 percent. Global LEU suppliers compete in the highly competitive industry primarily in terms of price and secondarily on reliability of supply and customer service. The three largest LEU suppliers comprise an estimated 90 percent of market share combined:

• | Rosatom, a Russian government entity, which sells LEU through its wholly owned subsidiary TENEX; |

• | Urenco, a consortium of companies owned or controlled by the British and Dutch governments and by two German utilities; and |

• | Areva, a company largely owned by the French government. |

The production capacity for Rosatom/TENEX is estimated by the World Nuclear Association (“WNA”) to be approximately 27 million SWU per year. Imports of LEU and other uranium products produced in the Russian Federation are subject to restrictions through 2020 as described below under Limitations on Imports of LEU from Russia.

Urenco reported installed capacity at its European and U.S. enrichment facilities of 18.8 million SWU per year at the end of 2016, down from 19.1 million at the end of 2015. Over the course of 2016, Urenco officials have said that the company is no longer replacing older centrifuge machines that wear out, that it has taken two production halls offline at its Capenhurst site, and that it is no longer expanding enrichment capacity in the current market.

Areva’s gas centrifuge enrichment plant in France began commercial operations in 2011 and more than 95% of the plant’s nominal capacity of 7.5 million SWU was reportedly in service by the end of 2016. Areva has reported that it has suspended planned capacity expansions beyond 7.5 million SWU.

All of our current competitors are owned or controlled, in whole or in part, by foreign governments. These competitors may make business decisions in both domestic and international markets that are influenced by political or economic policy considerations rather than exclusively by commercial considerations.

There are also producers of LEU in China, Japan and Brazil that primarily serve a portion of their respective domestic markets. China is emerging as a growing producer and has begun to supply LEU to international markets. China’s commercial SWU production capacity is estimated to be approximately 7 million SWU per year. Additional capacity is also under construction which may increase capacity up to 12 million SWU per year by 2020.

9

In addition, Global Laser Enrichment, a joint venture of General Electric, Hitachi and Cameco, has an agreement with Silex Systems Limited, an Australian company, to license Silex’s laser enrichment technology.

LEU may also be produced by down-blending government stockpiles of highly enriched uranium. Governments control the timing and availability of highly enriched uranium released for this purpose, and the release of this material to the market could impact market conditions. Given the current oversupplied nuclear fuel market, any additional LEU from down-blended highly enriched uranium released into the market would have a negative effect on prices for LEU.

LEU we supply to foreign customers is exported under the terms of international agreements governing nuclear cooperation between the United States and the country of destination or other entities, such as the European Union or the International Atomic Energy Agency. The LEU supplied to us under the Russian Supply Agreement is subject to the terms of cooperation agreements between the Russian Federation and the country of destination or other entities.

Limitations on Imports of LEU from Russia

Imports into the United States of LEU and other uranium products produced in the Russian Federation, including LEU imported under the Russian Supply Agreement, are subject to quotas imposed under legislation enacted into law in September 2008 and under the 1992 Russian Suspension Agreement, as amended in 2008. These quotas limit the amount of Russian LEU that can be imported into the United States for U.S. consumption. The quotas apply through 2020 and for 2014-2020, are set at an amount equal to approximately 20% of projected annual U.S. consumption of LEU, based on a market report published in 2005 by the World Nuclear Association (“2005 WNA Report”).

As an exception to the quotas on imports of LEU for U.S. consumption, both the Russian Suspension Agreement and the September 2008 legislation permit unlimited imports of Russian LEU for use in initial cores for any new U.S. nuclear reactor.

It is possible that the quotas on imports of Russian LEU could change. Both the Russian Suspension Agreement and the September 2008 legislation permit the Secretary of Commerce to increase the quotas for imports of Russian LEU for consumption in the United States in situations where supply is insufficient to meet U.S. demand for LEU. In addition, both the Russian Suspension Agreement and the September 2008 legislation require the U.S. Department of Commerce (“DOC”) to adjust the quotas in 2016 and 2019 based on changes in projected reactor demand as forecast by the World Nuclear Association. In 2016, the DOC preliminarily determined that the adjustment would increase the quotas, but this increase was challenged by U.S. uranium mining companies, and the DOC has yet to announce the final results of the 2016 adjustment. This adjustment could result in an increase or decrease of the quotas but is not expected to affect deliveries under contracts that were unconditionally approved by the DOC prior to the change.

Aside from the quotas on imports of Russian LEU that will be consumed in the United States, there is a separate quota that applies to deliveries of Russian LEU to foreign customers at U.S. fabrication facilities. This quota generally requires that the LEU be processed and re-exported within a certain period of time. In 2014, the DOC approved our proposal that Japanese customers with existing contracts with our subsidiary be allowed to physically store Russian LEU in the United States pending the restart of nuclear reactors in Japan. Under this approval, Japanese customers who wish to store Russian LEU in the United States pending restart of their reactors can do so under conditions intended to protect the U.S. market while the material is in storage. This material would not have to be re-exported until it is withdrawn from storage.

10

Beginning in February 2017, the Russian Suspension Agreement is subject to two “sunset” reviews being conducted by the DOC and the U.S. International Trade Commission (“ITC”), respectively, that will determine if the Russian Suspension Agreement should be maintained. These “sunset” reviews are required to be conducted every five years. This is the fourth round of “sunset reviews” of the Russian Suspension Agreement. The last round of reviews in 2011-12 concluded that termination of the Russian Suspension Agreement would lead to the continuation or recurrence of dumping of French LEU (a determination made by the DOC), and to the continuation or recurrence of material injury to the U.S. uranium industry (a determination made by the ITC), which resulted in the Russian Suspension Agreement being maintained. Even if the Russian Suspension Agreement were terminated as a result of the “sunset” reviews, the quotas under the September 2008 legislation would remain in place.

At the end of 2020, the Russian Suspension Agreement (and the antidumping order that it suspended), as well as the quotas under the September 2008 legislation, will expire. Accordingly, beginning in 2021, all the quotas on imports of Russian LEU will no longer apply.

Limitations on Imports of LEU from France

The DOC imposed an antidumping order on imports of French LEU in 2002. The order is subject to periodic “sunset reviews” of the antidumping order to determine if it should be revoked. The next review will be held in 2018. Accordingly, at present, we expect that the antidumping order on French LEU will remain in place through at least 2018.

Facility Decontamination and Decommissioning

We produced LEU through May 2013 at the Paducah gaseous diffusion plant (“Paducah GDP”) in Paducah, Kentucky that we had leased from DOE. We then repackaged and transferred our existing inventory to off-site licensed locations under agreements with the operators of those facilities. Our prior enrichment operations generated hazardous, low-level radioactive and mixed wastes. The storage, treatment, and disposal of wastes are regulated by federal and state laws. The treatment and disposal of wastes from our prior operations at the Paducah GDP were completed in 2016. Regarding our past operations at the former Portsmouth GDP in Piketon, Ohio, DOE agreed in 2011 to accept ownership of all nuclear material at the site, some of which required processing for waste disposal. We agreed to pay DOE for costs for disposing of our share of such wastes. Centrus has a recorded liability of $0.2 million as of December 31, 2016, for the processing of remaining waste quantities.

The Portsmouth and Paducah gaseous diffusion plants were operated by agencies of the U.S. government for approximately 40 years prior to the Company’s privatization in 1998. As a result of such operation, there is contamination and other potential environmental liabilities associated with the plants. The USEC Privatization Act and the Company’s former leases for the plants provide that DOE remains responsible for the D&D of the gaseous diffusion plants.

Centrus continues to lease the portion of the DOE facility in Piketon, Ohio, associated with the American Centrifuge advanced technology project. At the conclusion of the lease, Centrus is obligated to return the facility to DOE in a condition that meets NRC requirements and in the same condition as the facility was in when it was leased to Centrus (other than due to normal wear and tear). Centrus must remove all Company-owned capital improvements at the Piketon facility, unless otherwise consented to by DOE, by the conclusion of the lease term. The lease will expire on June 30, 2019, unless it is extended. Effective October 1, 2015, the U.S. government discontinued funding of the American Centrifuge demonstration cascade at Piketon. Centrus began to incur expenditures in the second quarter of 2016 associated with the D&D of the American Centrifuge facilities in Piketon in accordance with the requirements of the NRC and DOE. As of December 31, 2016, Centrus has a recorded liability of $38.6 million on the balance sheet for the estimated fair value of the remaining costs to complete the D&D work. Refer to Note 16, Commitments and Contingencies to the consolidated financial statements for additional information.

11

Employees

A summary of our employees by location follows:

No. of Employees at December 31, | ||||||

Location | 2016 | 2015 | ||||

Piketon, OH | 152 | 255 | ||||

Oak Ridge, TN | 116 | 120 | ||||

Bethesda, MD | 58 | 58 | ||||

Paducah, KY | 12 | 13 | ||||

Total Employees | 338 | 446 | ||||

On March 16, 2017, members the United Steelworkers (“USW”) Local 689 ratified a new collective bargaining agreement for the 41 employees represented by the USW at the advanced technology facility in Piketon. The contract term is through January 19, 2020.

For details concerning ongoing workforce reductions in connection with the conclusion of the federally funded advanced technology demonstration effort in Piketon, Ohio, refer to Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Available Information

Our website is www.centrusenergy.com. We make available on our website, or upon request, without charge, access to our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed with, or furnished to, the Securities and Exchange Commission, pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after such reports are electronically filed with, or furnished to, the Securities and Exchange Commission.

Our code of business conduct provides a brief summary of the standards of conduct that are at the foundation of our business operations. The code of business conduct states that we conduct our business in strict compliance with all applicable laws. Each employee must read the code of business conduct and sign a form stating that he or she has read, understands and agrees to comply with the code of business conduct. A copy of the code of business conduct is available on our website or upon request without charge. We will disclose on the website any amendments to, or waivers from, the code of business conduct that are required to be publicly disclosed.

We also make available on our website or upon request, free of charge, our Board of Directors Governance Guidelines and our Board committee charters.

12

Item 1A. Risk Factors

The following discussion sets forth the material risk factors that could affect Centrus’ financial condition and operations. Readers should not consider any descriptions of such factors to be a complete set of all potential risks that could affect the Company. Below, we describe certain important operational, financial, strategic and legal and compliance risks.

Operational Risks

Operational risks relate to risks arising from systems, processes, people and external events that affect the operation of our business, including supply chain and business disruption and data protection and security, including cyber security.

We are dependent on existing inventory, purchases of Russian LEU and purchases from other suppliers to meet our obligations to customers.

We ceased enrichment at the Paducah GDP at the end of May 2013. The economics, timing and ability of Centrus to commercialize an advanced uranium enrichment centrifuge technology as a replacement for the Paducah GDP are uncertain. As a result, we are dependent on existing inventory, purchases of LEU from TENEX, and purchases from other suppliers to meet our obligations to customers. We are acquiring alternative sources of supply in the market, given the current oversupply. The availability, cost and terms of additional alternative sources of supply are subject to variables that are difficult to predict. A significant delay in, or stoppage or termination of, deliveries of LEU under those supply agreements could adversely affect our ability to make deliveries to customers and would adversely affect revenues and results of operations. A delay, stoppage or termination could occur due to a number of factors, including logistical problems with shipments, commercial or political disputes between the parties or their governments, imposition of sanctions in response to geopolitical events or a failure or inability by either party to meet the terms of such agreements. An interruption of deliveries could adversely impact our business, results of operations, and prospects.

We may be unable to sell all of the LEU purchased under supply agreements including the commercial Russian LEU that is purchased under the Russian Supply Agreement, for prices that cover our purchase costs, which could adversely affect profitability and the viability of our business.

We may not achieve the anticipated benefits from supply agreements we enter into, including the Russian Supply Agreement. The price we are charged for the SWU component of Russian LEU under the Russian Supply Agreement is determined by a formula that combines a mix of market-related price points and other factors, which may result in prices that are not aligned with the prevailing market prices when those market prices are depressed, or declining, as is currently the case. Currently, the price we pay for Russian LEU is above current market prices. The Russian Supply Agreement provides for reexamination of a key element of the pricing formula in later years to account for significant increases or decreases in market prices. We expect this will result in a reduction in the price we would pay in those years, but there can be no assurance that an unexpected change will not occur that could lead to a different result. Other existing or new supply agreements may have pricing mechanisms that may not be aligned with market prices. The pricing mechanisms of our supply agreements may not align with pricing provided in our new or existing sales contracts and could result in sales prices that do not cover our purchase costs and may limit our ability to make new sales at prices that exceed the purchase price we pay for the LEU.

Restrictions on imports or sales of Russian LEU could adversely affect our ability to sell commercial Russian LEU purchased under the Russian Supply Agreement which could adversely affect profitability and the viability of our business.

Our ability to place Russian LEU into existing contracts is subject to U.S. import limitations and, in some cases, the contracts’ terms. Sales of Russian LEU are more challenging than sales of non-Russian material. Some of our customers are unable or unwilling to accept Russian LEU. In addition, we may not achieve the anticipated benefits from the Russian Supply Agreement because of restrictions on U.S. imports of LEU and other uranium products

13

produced in the Russian Federation. For example, imports of LEU under the Russian Supply Agreement are subject to quotas imposed under legislation enacted into law in September 2008 and under the 1992 Russian Suspension Agreement, as amended in 2008. We also dependent upon TENEX to grant us the right to use a portion of these quotas under the terms of the Russian Supply Agreement in order to import Russian LEU for sale in the United States. Further, the U.S. quotas on imports of Russian LEU are subject to periodic review by the Department of Commerce (“DOC”).

The Russian LEU that we cannot sell for consumption in the United States will have to be sold for consumption by utilities outside the United States. Our ability to sell to those utilities may be limited by policies of foreign governments or regional institutions that seek to restrict the amount of Russian LEU purchased by utilities under their jurisdiction, as well as requirements that Russian LEU imported into the United States to be used to fabricate fuel for foreign customers must be processed and re-exported within a certain period of time. In addition, foreign utilities who take delivery of LEU from us in the United States may be unwilling to cooperate with us in meeting the requirements under U.S. law to permit us to import Russian LEU to deliver to them. Further, geopolitical events, including domestic or international reactions or responses to such events and subsequent government or international actions including the imposition of sanctions, also could impact our ability to purchase, sell or make deliveries of LEU from Russia to customers. An interruption of deliveries under the Russian Supply Agreement could, depending on the length of such an interruption, threaten our ability to fulfill these delivery commitments with adverse effects on our reputation, costs, results of operations, cash flows and long-term viability. Even in the absence of sanctions or other legal restrictions, customers may be unwilling to agree to purchase or amend contracts to permit delivery of the Russian LEU. Accordingly, there is no assurance that we will be successful in our efforts to sell the Russian LEU we are obligated to purchase under the Russian Supply Agreement, in or outside of the United States.

We face risks associated with reliance on third-party suppliers to meet customer commitments.

We rely on third-party suppliers to provide essential services to the Company, such as the storage and management of inventory, transportation and radiation protection. We face the risk that those service providers may not perform on time, with the desired quality or at all for a variety of reasons, many of which are outside our control. Alternative third-party suppliers may not be readily available or may be more costly. As a result of such risks, we may be unable to meet our customer commitments, our costs could be higher than planned, and our relationship with customers could be negatively affected, all of which could adversely affect our business, results of operations, and prospects. Customers place great value in the reliability of their supply of fuel for their reactors. Failure to make a delivery could have an adverse effect on our ability to make new sales and could have an adverse effect on our business, results of operations, and prospects.

Periodically, events or issues arise that may affect the performance of our suppliers. There can be no assurance that the steps we may take to address these events or issues will be successful in minimizing potential impacts to the Company and our customers. Unless adequately addressed, such events or issues could adversely affect our business, results of operations, and prospects.

Dependence on our largest customers could adversely affect us.

In 2016, our 10 largest customers represented approximately 90% of total revenue and our four largest customers represented approximately 50% of total revenue. A reduction in purchases from our largest customers, whether due to their decision not to purchase optional quantities or for other reasons, including a disruption in their operations that reduces their need for LEU from us, could adversely affect our business, results of operations, and prospects.

We are seeing increased price competition as competitors and secondary suppliers lower their prices to sell excess supply created by current market conditions. This has adversely affected our sales efforts. Because price is a significant factor in a customer’s choice of a LEU supplier, when contracts come up for renewal, customers may reduce their purchases from us if we are not able to compete on price, resulting in the loss of new sales contracts. Once lost, customers may be difficult to regain because they typically purchase LEU under long-term contracts. Therefore, given the need to maintain existing customer relationships, particularly with the largest customers, our

14

ability to raise prices to respond to increases in costs or other developments may be limited. In addition, because we have a commitment to acquire Russian LEU under the Russian Supply Agreement, any reduction in purchases by the customers below the level required for us to resell both our inventory and the Russian material could adversely affect our business, results of operations, and prospects.

The dollar amount of the sales order book, as stated at any given time, is not necessarily indicative of future sales revenues and is subject to uncertainty.

Our order book of sales is the estimated aggregate dollar amount of SWU and uranium sales that we expect to recognize as revenue in future periods under existing contracts with customers. There is no assurance that the revenues projected will be realized, or, if realized, will result in profits. Most of our contracts provide for fixed purchases of SWU during a given year. Our estimate of the order book is partially based on customers’ estimates of the timing and size of their fuel requirements and other assumptions that may prove to be inaccurate. The order book is also based on estimates of selling prices, which are subject to change. For example, depending on the terms of specific contracts, prices may be adjusted based on escalation using a general inflation index, published SWU or uranium market price indicators prevailing at the time of delivery, and other factors, all of which are unpredictable, particularly in light of general uncertainty in the nuclear market and the economy generally. We use external composite forecasts of future market prices and inflation rates in our pricing estimates. These forecasts may not be accurate, and therefore estimates of future prices could be overstated. Any inaccuracy in estimates of future prices would add to the imprecision of the order book estimate.

For a variety of reasons, the amounts of SWU and uranium that we will sell in the future under existing contracts, and the timing of customer purchases under those contracts, may differ from estimates. Customers may not purchase as much as we predicted, nor at the times we anticipated, as a result of operational difficulties, changes in fuel requirements or other reasons. Reduced purchases would reduce the revenues we actually receive from contracts included in the order book. Customers could also seek to modify or cancel orders in response to concerns regarding our financial strength or future business prospects. Further, financial and operational issues facing our customers could affect the order book.

The order book includes sales prices that are significantly above current market prices. Customers may seek to limit their obligations under these existing contracts or may be unwilling to continue contracts that have termination rights. Some long-term contracts in our order book were established with milestones related to the ACP that permit termination with respect to portions of the contract under limited circumstances. We estimate that approximately 5% of our order book remains at risk due to milestones related to ACP deployment. From time to time, we have worked with customers to modify contracts that have delivery, scheduling, origin or other terms that may require modifications to address our anticipated supply sources. If we were to initiate such discussions in the future, we

have no assurance that our customers would agree to revise existing contracts or would not seek to exercise contract termination rights or require concessions, which could adversely affect the value of our order book and our prospects.

Failures or security breaches of information technology (“IT”) systems could have an adverse effect on our business.

Our business requires us to use and protect classified, sensitive and other protected information as well as business proprietary information and intellectual property. Our computer networks and other IT systems are designed to protect this information through the use of classified networks and other procedures. A material network breach in the security of the IT systems could include the theft of our business proprietary and intellectual property. To the extent any security breach results in a loss or damage to data, or in inappropriate disclosure of classified or other protected information, it could cause grave damage to the country’s national security and to our business. One of the biggest threats to classified information we protect comes from the insider threat - an employee with legitimate access who engages in misconduct. Transitions in the business, in particular the potential for employee layoffs and other transitions, can increase the risk that an insider with access could steal our intellectual property.

15

Financial Risks

Financial risks relate to our financial condition, capital structure and ability to meet financial obligations and the price, volatility and ownership concentration of our Class A Common Stock.

The Company has significant long-term liabilities.

We continue to have significant long-term liabilities, including the indebtedness under the PIK Toggle Notes, as well as our 8.25% Notes due 2027 (the “8.25% Notes”), which we issued on February 14, 2017. We also still have substantial pension and postretirement health and life benefit obligations and other long-term liabilities. In addition, the terms of the indenture governing our PIK Toggle Notes and the indenture governing our 8.25% Notes will not restrict Centrus or any of its subsidiaries from incurring substantial additional indebtedness in the future.

Our significant long-term liabilities (and other third-party financial obligations) could have important consequences, including:

• | the terms and conditions imposed by the documents governing our indebtedness could make it more difficult for us to satisfy our obligations to lenders and other creditors, resulting in possible defaults on and acceleration of such indebtedness or breaches of such other commitments; |

• | we may be more vulnerable to adverse economic conditions and have less flexibility to plan for, or react to, changes in the nuclear enrichment industry which could place us at a competitive disadvantage compared to industry competitors that have less debt or comparable debt at more favorable interest rates and that, as a result, may be better positioned to withstand economic downturns; |

• | we may find it more difficult to obtain additional financing for future working capital, and other general corporate requirements; and |

• | we will be required to dedicate a substantial portion of our cash resources to payments on the PIK Toggle Notes and 8.25% Notes thereby reducing the availability of our cash to fund our operations, capital expenditures and future business opportunities. |

If we incur substantial additional indebtedness, the foregoing risks would intensify. Additional information concerning the PIK Toggle Notes and 8.25% Notes including the terms and conditions of the PIK Toggle Notes and 8.25% Notes are described in Note 9, Debt, and Note 19, Subsequent Event, of the consolidated financial statements.

The Company has material unfunded defined benefit pension plans obligations and postretirement health and life benefit obligations. These liabilities are anticipated to require material contributions in future periods, which may divert funds from other uses and could adversely impact the Company’s liquidity and prospects.

Centrus and its subsidiary, United States Enrichment Corporation (“Enrichment Corp.”), maintain qualified defined benefit pension plans that are guaranteed by the Pension Benefit Guaranty Corporation (“PBGC”), a wholly owned U.S. government corporation that was created by the Employee Retirement Income Security Act (“ERISA”). Centrus also maintains non-qualified defined benefit pension plans for certain executive officers. Effective August 2013, accrued benefits under the defined benefit pension plans are fixed and no longer increase to reflect changes in compensation or company service. In addition, Enrichment Corp. maintains postretirement health and life benefit plans. The aforementioned pension and health and life benefit plans are closed to new participants. These plans are anticipated to require material cash contributions in the future, which may divert funds from other uses and could adversely impact the Company’s liquidity depending on the timing of any required contributions or payments in relation to the Company’s sources of cash and other payment obligations. See also the Risk Factor, Levels of returns on pension and postretirement benefit plan assets, changes in interest rates and other factors affecting the amounts to be contributed to fund future pension and postretirement benefit liabilities could adversely affect earnings and cash flows in future periods.

16

In addition, we had been engaged in discussions with the PBGC regarding the status of the qualified pension plans, including with respect to potential liability under ERISA Section 4062(e) related to employee reductions resulting from ceasing enrichment operations at the Portsmouth and Paducah GDP facilities. In February 2017, the PBGC confirmed that given changes to ERISA Section 4062(e) enacted by Congress in recent years, the Company is able to waive liability with respect to employee reductions at the Portsmouth and Paducah GDP facilities. In addition, the PBGC stated that it agrees to forbear from future action under ERISA Section 4062(e) related to the American Centrifuge project. In its notification to us, the PBGC cited the positive results of the our exchange offer and consent solicitation described in Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources. However, the PBGC could potentially seek to take action against us in the future.

Levels of returns on pension and postretirement benefit plan assets, changes in interest rates and other factors affecting the amounts to be contributed to fund future pension and postretirement benefit liabilities could adversely affect earnings and cash flows in future periods.

Earnings may be positively or negatively impacted by the amount of expense we record for employee benefit plans. This is particularly true with expense for the pension and postretirement benefit plans. Generally accepted accounting principles in the United States (“U.S. GAAP”) require a company to calculate expense for these plans using actuarial valuations. These valuations are based on assumptions relating to financial markets and other economic conditions. Changes in key economic indicators can result in changes in the assumptions used. The key year-end assumptions used to estimate pension and postretirement benefit expenses for the following year are the discount rate, the expected rate of return on plan assets and healthcare cost trend rates. The rate of return on pension assets and changes in interest rates affect funding requirements for defined benefit pension plans. The IRS and the Pension Protection Act of 2006 regulate the minimum amount we contribute to our pension plans. The amount required to contribute to pension plans can have an adverse effect on our cash flows.

Our revenues and operating results may fluctuate significantly from quarter to quarter and year to year, which could have an adverse effect on our cash flows.

Revenue is recognized at the time LEU or uranium is delivered under the terms of customer contracts. Customer demand is affected by, among other things, electricity markets, reactor operations, maintenance and the timing of refueling outages. Customer payments for the SWU component of LEU typically average roughly $15 million per order. As a result, a relatively small change in the timing of customer orders for LEU due to a change in a customer’s refueling schedule may cause operating results to be substantially above or below expectations, which could have an adverse effect on our cash flows.

Results of operations could be negatively impacted if adverse conditions or changes in circumstances indicate a possible impairment loss related to our intangible assets.

Intangible assets originated from the Company’s reorganization and application of fresh start accounting as of September 30, 2014. The intangible assets represented the fair value adjustment to the assets and liabilities for the Company’s LEU segment. The intangible assets remaining on the Company’s balance sheet relate to our sales order book and customer relationships. The order book intangible asset is amortized to expense as the order book valued at emergence is reduced, principally as a result of deliveries to customers. The customer relationships intangible asset is amortized to expense using the straight-line method over the estimated average useful life of 15 years.

The carrying values of the intangible assets are subject to impairment tests whenever adverse conditions or changes in circumstances indicate a possible impairment loss. If impairment is indicated, the asset carrying value will be reduced to its fair value. Inherent in our fair value determinations are certain judgments and estimates, including projections of future cash flows, the discount rate reflecting the risk inherent in future cash flows, the interpretation of current economic indicators and market valuations, and strategic plans with regard to operations. A

17

change in these underlying assumptions would cause a change in the results of the tests, which could cause the fair value of the intangible asset to be less than its respective carrying amount.

Centrus is dependent on intercompany support from Enrichment Corp.

Substantially all revenue-generating operations of the Company are conducted at our subsidiary, Enrichment Corp. The financing obtained from Enrichment Corp. funds Centrus’ general corporate expenses, including cash interest payments on the PIK Toggle Notes and the 8.25% Notes, which are guaranteed on a limited and subordinated basis by Enrichment Corp. As a wholly owned subsidiary of Centrus, Enrichment Corp. has its own set of creditors and a separate board of directors, including independent directors (the “Enrichment Board”), who are elected by Centrus. Current and future funding and support are conditional and dependent on Enrichment Corp.’s own financial condition and a determination by the Enrichment Board that such funding is in the interest of Enrichment Corp.

There is a limited trading market for our securities and the market price of our securities is subject to volatility.

The price of our Class A Common Stock remains subject to volatility. The market price and level of trading of our Class A Common Stock could be subject to wide fluctuations in response to numerous factors, many of which are beyond our control. These factors include, among other things, our limited trading history, our limited trading volume, the concentration of holdings of our Class A Common Stock, the lack of comparable historical financial information due to our adoption of fresh start accounting, actual or anticipated variations in our operating results and cash flow, the nature and content of our earnings releases, announcements or events that impact our products, customers, competitors or markets, business conditions in our markets and the general state of the securities markets and the market for energy-related stocks, as well as general economic and market conditions and other factors that may affect our future results. The automatic conversion (with limited exceptions) of Class B Common Stock into Class A Common Stock upon the sale of Class B Common Stock could significantly adversely impact the trading price of the Class A Common Stock on the NYSE MKT.

Our PIK Toggle Notes, the 8.25% Notes and the Series B Preferred Stock are not listed on any securities exchange. No assurance can be given as to the liquidity of the trading market for the PIK Toggle Notes, the 8.25% Notes or the Series B Preferred Stock. The PIK Toggle Notes, the 8.25% Notes and the Series B Preferred Stock may be traded only infrequently in transactions arranged through brokers or otherwise, and reliable market quotations for the PIK Toggle Notes, the 8.25% Notes and the Series B Preferred Stock may not be available. In addition, the trading prices of the PIK Toggle Notes, the 8.25% Notes and the Series B Preferred Stock will depend on many factors, including prevailing interest rates, the limited trading volume of the PIK Toggle Notes, the 8.25% Notes and the Series B Preferred Stock, and the other factors discussed above with respect to the Class A Common Stock. Our Class B stockholders may make decisions regarding their investment in the Company based upon factors that are unrelated to the Company’s performance.

A small number of Class A stockholders may exert significant influence over the direction of the Company.

As of December 31, 2016, based solely on amounts reported in Schedule 13D and 13G filings with the SEC, two principal stockholders (those stockholders with beneficial ownership of more than 10% of our Class A Common Stock) collectively beneficially own approximately 36.3% of our Class A Common Stock. As a result, these stockholders may be able to exert significant influence over all matters requiring stockholder approval, including the election of directors and approval of significant corporate transactions, such as a merger of the Company or sale of substantially all of the Company’s assets. These stockholders may have interests that differ from and may vote in a way adverse to other holders of Class A Common Stock. This concentration of ownership may make it more difficult for other stockholders to effect substantial changes in the Company and may also have the effect of delaying, preventing or expediting, as the case may be, a change in control of the Company.

18

Our ability to utilize our net operating loss carryforwards to offset future taxable income may be limited.

Our ability to fully utilize our existing net operating losses (“NOLs”) or net unrealized built-in losses could be limited or eliminated in the event (i) we undergo an “ownership change” as described under Section 382 of the Code, (ii) we do not reach profitability or are only marginally profitable, or (iii) there are changes in federal laws and regulations. An “ownership change” is generally defined as a greater than 50% change in equity ownership by value over a rolling three-year period. Past or future ownership changes, some of which may be beyond our control, as well as differences and fluctuations in the value of our equity securities may adversely affect our ability to utilize our NOLs and could reduce our flexibility to raise capital in future equity financings or other transactions, or we may determine to pursue transactions even if they would result in an ownership change and impair our ability to use our NOLs. In addition, the Section 382 Rights Agreement we have adopted with respect to our common stock and the transfer restrictions in the Series B Preferred Stock contain limitations on transferability intended to prevent the possibility of experiencing an “ownership change,” but we cannot assure you that these measures will be effective or we may determine to pursue transactions even if they would result in an ownership change and impair our ability to use our NOLs. In addition, any changes to tax rules and regulations or the interpretation of tax rules and regulations could negatively impact our ability to recognize any potential benefits from our NOLs or net unrealized built-in losses.

We have identified a material weakness in our internal control over financial reporting which could, if not remediated, result in material misstatements in our financial statements.

In connection with management's evaluation of the effectiveness of our internal control over financial reporting as of December 31, 2016, we determined that we did not design and maintain effective controls at an appropriate level of precision over the review of the spreadsheets used in the calculation of the decontamination and decommissioning (“D&D”) obligation and the cost estimates supporting the calculation. This resulted in a material adjustment in the fourth quarter D&D obligation balance, which was recorded prior to the issuance of our consolidated financial statements as of and for the year ended December 31, 2016. For additional discussion see Part II, Item 9A, Controls and Procedures.

We are developing a plan of remediation to strengthen our overall internal control over accounting for our D&D obligation. If our remediation efforts are insufficient to address the identified material weakness or if additional material weaknesses in internal controls are discovered in the future, we may be unable to timely and accurately record, process, summarize and report our financial results. The occurrence of or failure to remediate a material weakness may adversely affect our reputation and business and the market price of shares of our common stock.

Strategic Risks

Strategic risks relate to the Company’s future business plans and strategies, including the risks associated with: the global macro-environment in which we operate; the demand for our products and services, competitive threats and technology innovation.

Our future prospects are tied directly to the nuclear energy industry worldwide.

Potential events that could affect either nuclear reactors under current or future contracts with us or the nuclear industry as a whole, include:

• | accidents, terrorism or other incidents at nuclear facilities or involving shipments of nuclear materials; |

• | regulatory actions or changes in regulations by nuclear regulatory bodies; |

• | decisions by agencies, courts or other bodies that limit our ability to seek relief under applicable trade laws to offset unfair competition or pricing by foreign competitors; |

• | disruptions in other areas of the nuclear fuel cycle, such as uranium supplies or conversion; |

• | civic opposition to, or changes in government policies regarding, nuclear operations; |

19

• | business decisions concerning reactors or reactor operations; |

• | the need for generating capacity; or |

• | consolidation within the electric power industry. |

These events could adversely affect us to the extent they result in a reduction or elimination of customers’ contractual requirements to purchase from us, the suspension or reduction of nuclear reactor operations, the reduction of supplies of raw materials, lower demand, burdensome regulation, disruptions of shipments or production, increased competition from third parties, increased operational costs or difficulties or increased liability for actual or threatened property damage or personal injury.

Our results of operations could be significantly affected by market prices of uranium which are cyclical and subject to substantial price fluctuations.

Our earnings and operating cash flow are and will be particularly sensitive to the long and short term changes in the market price of uranium. Among other factors, these prices affect the value of our inventories.

Market prices are affected by numerous factors beyond our control. Such factors include, among others: demand for nuclear power; political and economic conditions in uranium producing and consuming countries; public and political response to a nuclear incident; reprocessing of used reactor fuel, the re-enrichment of depleted uranium tails and the enricher practice of underfeeding; sales of excess civilian and military inventories (including from the dismantling of nuclear weapons; the premature decommissioning of nuclear power plants; and from the build-up of Japanese utility uranium inventories as a result of the Fukushima incident) by governments and industry participants; uranium supply, including the supply from other secondary sources; and production levels and costs of production. Other factors relating to the price of uranium include: levels of supply and demand for a broad range of industrial products; substitution of new or different products in critical applications for our existing products; expectations with respect to the rate of inflation; the relative strength of the U.S. dollar and of certain other currencies; interest rates; global or regional political or economic crises; regional and global economic conditions; and sales of uranium by holders in response to such factors.

The continued excess supply of LEU in the market could adversely affect our business, results of operations and prospects.

Approximately 60 reactors in Japan and Germany were taken off-line following the March 2011 earthquake and tsunami that caused irreparable damage to four reactors in Fukushima, Japan. The events at Fukushima and its aftermath have negatively affected the balance of supply and demand. This impact could continue to grow depending on the length and severity of delays or cancellations of deliveries. The longer that this demand is reduced or absent from the market, the greater the cumulative impact on the market. Market prices for our products are at their lowest levels in more than a decade and this trend could continue or worsen. Suppliers whose deliveries are cancelled or delayed due to shutdown reactors or delays in reactor refuelings have excess supply available to sell in the market. This has adversely affected our success in selling LEU. The events have created significant uncertainty and our business, results of operations, and prospects have been and in the future could be adversely affected.