Attached files

| file | filename |

|---|---|

| EX-23.8 - EX-23.8 - WARRIOR MET COAL, INC. | d501786dex238.htm |

| EX-23.7 - EX-23.7 - WARRIOR MET COAL, INC. | d501786dex237.htm |

| EX-23.5 - EX-23.5 - WARRIOR MET COAL, INC. | d501786dex235.htm |

| EX-23.4 - EX-23.4 - WARRIOR MET COAL, INC. | d501786dex234.htm |

| EX-23.3 - EX-23.3 - WARRIOR MET COAL, INC. | d501786dex233.htm |

| EX-23.2 - EX-23.2 - WARRIOR MET COAL, INC. | d501786dex232.htm |

| EX-23.1 - EX-23.1 - WARRIOR MET COAL, INC. | d501786dex231.htm |

| EX-10.12 - EX-10.12 - WARRIOR MET COAL, INC. | d501786dex1012.htm |

| EX-10.11 - EX-10.11 - WARRIOR MET COAL, INC. | d501786dex1011.htm |

Table of Contents

As filed with the Securities and Exchange Commission on March 27, 2017

Registration No. 333-216499

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Warrior Met Coal, LLC

to be converted as described herein into a corporation named

Warrior Met Coal, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 1220 | 81-0706839 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

16243 Highway 216

Brookwood, AL 35444

(205) 554-6150

(Address, including zip code and telephone number, including area code, of registrant’s principal executive offices)

Dale W. Boyles

Chief Financial Officer

Warrior Met Coal, LLC

16243 Highway 216

Brookwood, AL 35444

(205) 554-6150

(Name, address, including zip code and telephone number, including area code, of agent for service)

Copies to:

| Rosa Testani Daniel Fisher Shar Ahmed Akin Gump Strauss Hauer & Feld LLP One Bryant Park Bank of America Tower New York, New York 10036 (212) 872-8115 |

Daniel Bursky Andrew Barkan Fried, Frank, Harris, Shriver & Jacobson LLP One New York Plaza New York, New York 10004 (212) 859-8000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement is declared effective.

If any securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended (the “Securities Act”), check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | Accelerated filer | ☐ | ||||

| Non-accelerated filer ☒ | (Do not check if a smaller reporting company) | Smaller reporting company | ☐ |

Table of Contents

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(3) | ||

| Common stock, par value $0.01 per share |

$100,000,000 | $11,590 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) under the Securities Act. |

| (2) | Includes the offering price of common stock that may be purchased by the underwriters upon the exercise of their option to purchase additional shares. |

| (3) | Previously paid in connection with the filing of this Registration Statement on March 7, 2017. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

Warrior Met Coal, LLC, the registrant whose name appears on the cover of this registration statement, is a Delaware limited liability company. Prior to the effectiveness of this registration statement, Warrior Met Coal, LLC will be converted into a Delaware corporation pursuant to a statutory conversion, which we refer to as the “corporate conversion” and be renamed Warrior Met Coal, Inc. as described in the section “Corporate Conversion” of the accompanying prospectus. As a result of the corporate conversion, the members of Warrior Met Coal, LLC will become holders of shares of common stock of Warrior Met Coal, Inc. Except as disclosed in the accompanying prospectus, the audited financial statements and related notes thereto and selected consolidated and combined historical and pro forma financial data and other financial information included in this registration statement are those of Warrior Met Coal, LLC and its subsidiaries and its predecessor and do not give effect to the corporate conversion. Shares of common stock of Warrior Met Coal, Inc. are being offered by the accompanying prospectus.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. The selling stockholders may not sell the securities described herein until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell such securities and it is not soliciting an offer to buy such securities in any state where such offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MARCH 27, 2017

Shares

Warrior Met Coal, Inc.

Common Stock

This is the initial public offering of shares of common stock of Warrior Met Coal, Inc. All of the shares of common stock are being offered by the selling stockholders identified in this prospectus. We will not receive any of the proceeds from the shares of common stock being sold in this offering.

Prior to this offering, there has been no public market for our common stock. We anticipate that the initial public offering price will be between $ and $ per share. We have been approved to list our common stock on the New York Stock Exchange under the symbol “HCC.”

The underwriters may also purchase up to additional shares from the selling stockholders at the initial public offering price, less the underwriting discounts and commissions, within 30 days from the date of this prospectus.

We are an “emerging growth company” as that term is used in the Jumpstart Our Business Startups Act of 2012 and, as such, have elected to comply with certain reduced public company reporting requirements. See “Prospectus Summary—Implications of Being an Emerging Growth Company.”

Investing in our common stock involves risks. See “Risk Factors” on page 20.

| Price to Public |

Underwriting Discounts and Commissions(1) |

Proceeds to Selling Stockholders |

||||||||||

| Per Share |

$ | $ | $ | |||||||||

| Total |

$ | $ | $ | |||||||||

| (1) | See “Underwriting” for additional information regarding underwriting compensation. |

Neither the Securities and Exchange Commission, any state securities commission nor any other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares on or about , 2017.

| Credit Suisse | Citigroup | Morgan Stanley | ||||||

| BMO Capital Markets |

RBC Capital Markets | |||||||

| Apollo Global Securities | Clarksons Platou Securities | KKR | ||||||

The date of this prospectus is , 2017.

Table of Contents

Table of Contents

| 1 | ||||

| 20 | ||||

| 52 | ||||

| 54 | ||||

| 54 | ||||

| 55 | ||||

| 56 | ||||

| 57 | ||||

| SELECTED CONSOLIDATED AND COMBINED HISTORICAL AND PRO FORMA FINANCIAL DATA |

58 | |||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

61 | |||

| 86 | ||||

| 95 | ||||

| 117 | ||||

| 137 | ||||

| 141 | ||||

| 147 | ||||

| 152 | ||||

| 153 | ||||

| MATERIAL U.S. FEDERAL INCOME AND ESTATE TAX CONSEQUENCES FOR NON-U.S. HOLDERS OF OUR COMMON STOCK |

155 | |||

| 159 | ||||

| 168 | ||||

| 168 | ||||

| 168 | ||||

| F-1 | ||||

| A-1 |

You should rely only on the information contained in this prospectus or in any free writing prospectus prepared by us or on behalf of us or to which we have referred you. Neither we, the selling stockholders nor the underwriters have authorized any other person to provide you with information different from that contained in this prospectus and any free writing prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. Neither we, the selling stockholders nor the underwriters are making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of shares of our common stock. The information in any free writing prospectus that we may provide to you in connection with this offering is accurate only as of the date of such free writing prospectus. Our business, financial condition, results of operations and future growth prospects may have changed since those dates.

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. Please read “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.”

Industry and Market Data

The data included in this prospectus regarding the metallurgical (“met”) coal industry, including descriptions of trends in the market, as well as our position within the industry, is based on a variety of sources,

i

Table of Contents

including independent industry publications, government publications and other published independent sources, including Wood Mackenzie, the Energy and Minerals Field Institute and the World Coal Association, none of which are affiliated with us, as well as information obtained from customers, distributors, suppliers, trade and business organizations and publicly available information, as well as our good faith estimates, which have been derived from management’s knowledge and experience in our industry. Although we have not independently verified the accuracy or completeness of the third-party information included in this prospectus, based on management’s knowledge and experience, we believe that the third-party sources are reliable and that the third-party information included in this prospectus or in our estimates is accurate and complete. See “Industry Overview” for additional information regarding the met coal industry.

Statements made by Wood Mackenzie included in this prospectus with respect to our competitive position in 2017 are based upon “Operating Margin” and “Total Cash Cost,” as each such term is defined by Wood Mackenzie. “Operating Margin” is defined by Wood Mackenzie as gross revenue less Total Cash Cost. “Total Cash Cost” is defined by Wood Mackenzie as the sum of the direct cash costs associated with the mining, processing and transport of the marketable product, general and administration overhead costs directly related to mine production and royalty, levies and other indirect taxes (excluding profit related taxes).

Coal Reserve Information

The estimates of our proven and probable reserves as of December 31, 2016 included in this prospectus (i) for our Mine No. 4 and Mine No. 7 were prepared by Marshall Miller & Associates, Inc., an independent mining and geological consulting firm (“Marshall Miller”), (ii) for our Blue Creek Energy Mine (as defined below) were prepared by Norwest Corporation, an independent international mining consulting firm (“Norwest”), and (iii) for our other mining properties described in this prospectus were prepared by McGehee Engineering Corp., an independent mining and geological consulting firm (“McGehee”). The estimates of our proven and probable reserves are based on engineering, economic and geologic data, coal ownership information and current and proposed mine plans. Our proven and probable coal reserves are reported as “recoverable coal reserves,” which is the portion of the coal that could be economically and legally extracted or produced at the time of the reserve determination, taking into account mining recovery and preparation plant yield. These estimates are periodically updated to reflect past coal production, new drilling information and other geologic or mining data. Acquisitions or dispositions of coal properties will also change these estimates. Changes in mining methods may increase or decrease the recovery basis for a coal seam, as will changes in preparation plant processes.

“Reserves” are defined by the Security and Exchange Commission’s (the “SEC”) Industry Guide 7 as that part of a mineral deposit which could be economically and legally extracted or produced at the time of the reserve determination. Industry Guide 7 divides reserves between “proven (measured) reserves” and “probable (indicated) reserves,” which are defined as follows:

| • | “Proven (Measured) Reserves.” Reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well-established. |

| • | “Probable (Indicated) Reserves.” Reserves for which quantity and grade and/or quality are computed from information similar to that used for proven (measured) reserves, but the sites for inspection, sampling, and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven (measured) reserves, is high enough to assume continuity between points of observation. |

Please read “Business—Estimated Recoverable Coal Reserves” for additional information regarding our reserves.

ii

Table of Contents

This summary contains basic information about us and this offering. Because it is a summary, it does not contain all the information that you should consider before investing in our common stock. You should read and carefully consider this entire prospectus before making an investment decision, especially the information presented under the heading “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited combined and consolidated Predecessor and Successor financial statements and the accompanying notes thereto and our unaudited pro forma condensed combined financial statements and the accompanying notes thereto included elsewhere in this prospectus.

Prior to the effectiveness of the registration statement of which this prospectus forms a part, we will complete a corporate conversion pursuant to which Warrior Met Coal, LLC will be converted into a Delaware corporation and be renamed Warrior Met Coal, Inc. as described under “Corporate Conversion.” We refer to this transaction herein as the “corporate conversion.” Except as otherwise indicated or required by the context, all references in this prospectus to the “Company,” “we,” “us,” “our” or “Successor” relate to (1) Warrior Met Coal, LLC, a Delaware limited liability company, and its subsidiaries for periods beginning as of April 1, 2016 and ending immediately before the completion of our corporate conversion, and (2) Warrior Met Coal, Inc., a Delaware corporation, and its subsidiaries for periods beginning with the completion of our corporate conversion and thereafter. References in this prospectus to the “Predecessor” refer to the assets acquired and liabilities assumed by Warrior Met Coal, LLC from Walter Energy, Inc., a Delaware corporation (“Walter Energy”), in the Asset Acquisition on March 31, 2016, as further described below under “—Corporate History and Structure—Walter Energy Restructuring.” The Predecessor periods included in this prospectus begin as of January 1, 2015 and end as of March 31, 2016. References in this prospectus to “selling stockholders” refer to those entities identified as selling stockholders in “Principal and Selling Stockholders.” “Met coal,” “hard coking coal” or “coking coal” as used in this prospectus means metallurgical coal. We have provided definitions for some of the other industry terms used in this prospectus in the “Glossary of Selected Terms” included elsewhere in this prospectus as Appendix A.

Warrior Met Coal, Inc.

Our Business

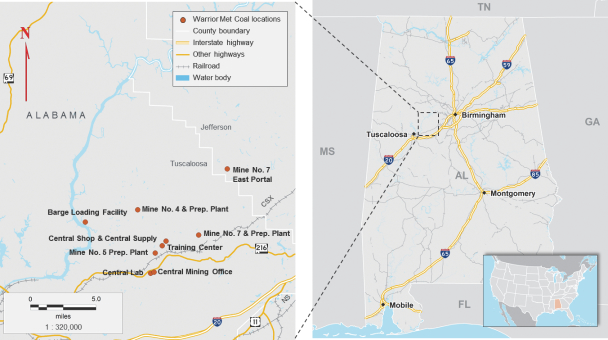

We are a large scale, low-cost U.S.-based producer and exporter of premium met coal operating two highly productive underground mines in Alabama, Mine No. 4 and Mine No. 7, that have an estimated annual production capacity of 7.3 million metric tons of coal. According to Wood Mackenzie, in 2017, we are expected to be the largest seaborne met coal supplier in the Atlantic Basin, and a top ten supplier to the global seaborne met coal market. As of December 31, 2016, based on a reserve report prepared by Marshall Miller, our two operating mines had approximately 107.8 million metric tons of recoverable reserves and, based on a reserve report prepared by Norwest, our undeveloped Blue Creek Energy Mine (as discussed below) contained 103.0 million metric tons of recoverable reserves. The premium hard coking coal (“HCC”) we produce at Mine No. 4 and Mine No. 7 is of a similar quality to coal referred to as the “benchmark HCC” produced in Australia, which is used to set quarterly pricing for the met coal industry.

Our operations are high margin when compared to our competitors. According to Wood Mackenzie, in 2017 our overall operations are expected to be positioned in the first quartile (18th percentile) based on “Operating Margin” as defined by Wood Mackenzie, among mines operated by U.S. seaborne met coal exporters. In addition, according to Wood Mackenzie, in 2017 our overall operations are expected to be positioned in the second quartile (33rd percentile) based on Operating Margin, among all mines operating in the global seaborne met coal market.

1

Table of Contents

We believe our high margin operations relative to our competitors are a direct result of a combination of factors, notably our (1) highly productive mining operations, (2) high-quality coal products, (3) close proximity and efficient access to the Port of Mobile, Alabama and (4) seaborne freight advantage to reaching our primary end markets:

| • | We employ a highly efficient longwall mining method with development support from continuous miners at both of our operating mines. This mining method, together with a redesigned flexible mine plan developed and implemented around the time of the Asset Acquisition (as defined below), new logistics contracts and a new initial Collective Bargaining Agreement (“CBA”) with the United Mine Workers of America (“UMWA”), has enabled us to structurally reduce the operating costs at our Mine No. 4 and Mine No. 7, while also increasing our ability to adjust our cost structure with respect to the HCC benchmark price. We believe the step-down in costs and greater variability in our cost structure relative to Walter Energy equip our operations to endure adverse price environments and generate strong cash flows in favorable price environments. |

| • | Our HCC, mined from the Southern Appalachian portion of the Blue Creek coal seam, is characterized by low sulfur, low-to-medium ash, and low-to-medium volatility. These qualities make our coal ideally suited as a coking coal for the manufacture of steel. As a result of our high quality coal, our realized price has historically been in line with or at a slight discount to the HCC benchmark, which helps drive our high operating margins. |

| • | Our two operating mines are located approximately 300 miles from our export terminal at the Port of Mobile, Alabama, which we believe to be the shortest mine-to-port distance of any U.S.-based met coal producer. Our low cost, flexible and efficient rail and barge network underpins our cost advantage and dependable access to the seaborne markets. Furthermore, in the event of lower coal prices, we have a variable transportation cost structure that results in lower cash requirements. |

| • | We sell our coal to a diversified customer base of blast furnace steel producers, primarily located in Europe and South America. We enjoy a shipping time and distance advantage serving customers throughout the Atlantic Basin relative to competitors located in Australia and Western Canada. |

To complement our highly efficient, low-cost operations, we have the ability to quickly adjust our production levels in response to market conditions. Our mine plan was redesigned and implemented around the time of the Asset Acquisition, allowing us to maximize profitability and operating cash flow. For example, we operated our mines at reduced levels in the early part of 2016 in response to weak met coal market conditions throughout the first nine months of 2016, during which we produced 2.2 million metric tons of met coal. During the fourth quarter of 2016, we commenced ramping up production in response to the increase in the HCC benchmark price, which resulted in us producing 3.1 million metric tons of met coal for the year ended December 31, 2016. During 2013, when the HCC quarterly benchmark price averaged $159 per metric ton, our two operating mines produced a combined 7.3 million metric tons, which we estimate equals our current capacity. We are increasing our production during 2017 and, given our favorable cost structure, generate significantly higher operating cash flow.

For the year ended December 31, 2015 and the nine months ended December 31, 2016, our coal operations:

| • | generated sales of $514.3 million and $276.6 million, respectively; and |

| • | incurred cost of sales of $601.5 million and $244.7 million, respectively. |

Our Competitive Strengths

We believe that we have the following competitive strengths:

Exposure to “pure play,” high quality met coal production. Unlike many other mining companies, substantially all of our revenue is derived from the sale of met coal in the global seaborne markets. All of our

2

Table of Contents

resources are allocated to the mining, transportation and marketing of met coal. The premium HCC we produce at Mine No. 4 and Mine No. 7 is of a similar quality to coal referred to as the “benchmark HCC” produced in Australia, which is used to set quarterly pricing for the met coal industry. Coal from Mine No. 7 is classified as a premium low-volatility HCC and coal from Mine No. 4 is classified as a premium mid-volatility HCC. The combination of low sulfur, low-to-medium ash, low-to-medium volatility, and other characteristics of our coal, as well as our ability to blend them, makes our HCC product an important component within our customers’ overall coking coal requirements. As a result, our realized price has historically been in line with or at a slight discount to the HCC benchmark. Our 2016 average realized price of 99% of the HCC benchmark is in significant contrast to other U.S. met coal producers, which we believe sell a relatively higher proportion of lower rank coals to domestic steel producers and achieved realized prices of approximately 80% to 90% of the HCC benchmark in 2016, based on data from public filings made by such other U.S. met coal producers, as adjusted based on mine-to-port transportation cost estimates from Wood Mackenzie.

Productive longwall mines with low operating costs. We employ a highly efficient longwall mining method with development support from continuous miners at both of our operating mines. This mining method, combined with a redesigned flexible mine plan implemented around the time of the Asset Acquisition allows us to adjust our production levels in response to market conditions to ensure maximum profitability and operating cash flow, throughout coal-pricing cycles. Around the time of the Asset Acquisition, we were able to structurally reduce the operating and logistical costs associated with Mine No. 4 and Mine No. 7. For the nine months ended December 31, 2016, our two operating mines had an average cash cost of sales free-on-board at the Port of Mobile of $82.84 per metric ton, compared to $112.96 per metric ton for the year ended December 31, 2015. Of note, we achieved this 26.7% reduction in cash cost of sales even though we are still in the process of ramping up production at Mine No. 4 and the second longwall within Mine No. 7. See “—Summary Consolidated and Combined Historical and Pro Forma Financial Data—Non-GAAP Financial Measures—Cash Cost of Sales” for the definition of cash cost of sales and a reconciliation of cash cost of sales to our most directly comparable financial measure calculated and presented in accordance with GAAP. These cost reductions were driven in large part by structurally sustainable changes to our overall operations we implemented around the time of the Asset Acquisition, in particular our new flexible mine plan, new initial CBA with the UMWA, and reduced rail, barge and port costs. According to Wood Mackenzie, in 2017, our overall operations are expected to be positioned in the first quartile (18th percentile) based on Operating Margin, among mines operated by U.S. seaborne met coal exporters. In addition, according to Wood Mackenzie, in 2017, our overall operations are expected to be positioned in the second quartile (33rd percentile) based on Operating Margin among all mines operating in the global seaborne met coal market.

Largest seaborne met coal supplier based in the Atlantic Basin with diverse customer base and significant reserve base. According to Wood Mackenzie, in 2017, we are expected to be the largest seaborne supplier of met coal based in the Atlantic Basin. Our location provides us with a significant freight advantage in serving our European and South American customers relative to competitors located in Australia and Western Canada whose coal must be shipped significantly longer distances. This advantage results in a higher margin for our met coal. We have a diverse customer base and have supplied many of our top customers continuously over the last decade. Our ability to serve customers in the Atlantic Basin is supported, as of December 31, 2016, based on a reserve report prepared by Marshall Miller, by approximately 107.8 million metric tons of recoverable coal reserves at our two operating mines. Together, these reserves provide an implied mine life of approximately 15 years at our historical operating rates. We have additional significant embedded growth potential that can be developed at our operating mines and at our undeveloped Blue Creek Energy Mine in a supportive met coal pricing environment. In particular, our undeveloped Blue Creek Energy Mine in Tuscaloosa County, Alabama contains, based on a reserve report prepared by Norwest, an additional 103.0 million metric tons of high-quality met coal recoverable reserves. Management is evaluating the future development of this new mine.

3

Table of Contents

Significant logistical advantage and secure infrastructure access to reach the seaborne market. Our two operating mines are located approximately 300 miles from our export terminal capacity in Mobile, Alabama and have multiple alternative transportation routes to move our coal to port. These alternatives include direct rail access at the mine sites and a wholly owned barge load-out facility, enabling us to utilize the lowest cost option between the two at any given point in time. Around the time of the Asset Acquisition, we successfully negotiated a reduction in rail, barge and port costs. In addition, we have a contract with the Port of Mobile, Alabama, that provides us up to 8.0 million metric tons of annual port capacity through July 2026 for our coal at very competitive rates. The total annual capacity of the McDuffie Coal Terminal at the Port of Mobile, Alabama is approximately 27.2 million metric tons and this coal terminal is presently utilized for all of our coal exports. Our proximity to port contrasts with the approximately 400-mile distances for major Central Appalachian met coal producers to access their nearest port, the Port of Hampton Roads, Virginia. Our proximity to port and the flexibility of our logistics networks underpin our logistical cost advantage compared to other U.S. met coal producers. According to Wood Mackenzie, our operating mines are expected to be in the first quartile (10th percentile) for transportation costs from mine to port in the United States in 2017, contributing to our competitive cost advantage relative to other U.S. exporters who collectively comprise the vast majority of met coal produced in the Atlantic Basin.

Strong leverage to met coal prices with strong operating cash flow generation. Our overall operations have robust operating margins, require modest sustaining capital expenditures and are expected to generate significant operating cash flows in a range of met coal price environments. We acquired our operations in the Asset Acquisition on a debt-free basis and with minimal legacy liabilities and, as a result, we have a strong balance sheet and currently have minimal interest expense. We expect our operating cash flows to benefit from a low effective tax rate, predominantly driven by significant net operating loss carryforwards (“NOLs”) that were acquired in connection with the Asset Acquisition.

Our new initial CBA, combined with our flexible rail, port and barge logistics and our royalty structure, results in a highly variable operating cost profile that allows our cash cost of sales to move with changes in the price we realize for our coal. Approximately two-thirds of our cash cost of sales relate to the cost of production at our mines, while the remaining one-third relates to our logistics costs from mine to port as well as royalties. Our logistics costs are structured to reduce cash requirements in lower HCC benchmark price environments and to increase cash requirements within a range with higher HCC benchmark prices. Our royalties are calculated as a percentage of the price we realize and therefore increase or decrease with changes in the HCC benchmark. Our new initial CBA includes a variable element that pays bonus incentives and hourly wage increases tied to HCC benchmark prices. In addition, we can adjust our usage of continuous miner units in response to HCC benchmark pricing. Continuous miner units develop panels for mining by longwall units and operate at a higher cost than longwall units. By running additional continuous miner units in higher met coal price environments, we are able to develop extra panels (also known as “float”) that will enable us to idle continuous miner units in lower met coal price environments, while continuing to run our lower cost longwall units. Our variable cost structure dramatically lowers our cash cost of sales if our realized price falls, while being effectively capped in higher price environments allowing us to generate significant operating cash flow. The following table presents our illustrative run rate cash cost of sales free-on-board at the Port of Mobile:

| HCC benchmark ($ per metric ton) |

$ | 100 | $ | 120 | $ | 150 | $ | 175 | $ | 200 | ||||||||||

| Illustrative cash cost of sales (free-on-board port) ($ per metric ton) |

$ | 80 | $ | 92 | $ | 97 | $ | 101 | $ | 104 |

Dynamic mine plan allows flexibility to quickly adjust production. Our lean organization and dynamic mine plan allow us to quickly ramp up or ramp down production in response to market conditions with minimal one-time costs associated with the change in production levels. During the year ended December 31, 2016, when the HCC benchmark averaged $114.25 per metric ton but had a low of $81 per metric ton in the first quarter of 2016, we produced 3.1 million metric tons of met coal compared to 4.9 million metric tons for the year ended

4

Table of Contents

December 31, 2015, when the HCC benchmark averaged $102.13 per metric ton (with a low of $89 per metric ton in the fourth quarter of 2015). Similarly, in the fourth quarter of 2016, in response to the substantial increase in met coal prices, we rapidly restarted our Mine No. 4 and ramped up production at the second longwall within Mine No. 7 to increase our production rates. Our production in the fourth quarter of 2016 was 0.9 million metric tons, when the HCC benchmark was $200 per metric ton versus 0.6 million metric tons in the fourth quarter of 2015, when the HCC benchmark was $89 per metric ton. On an annual basis, we believe we can ramp up production to 7.3 million metric tons, which was our historical high production level set in 2013.

Highly experienced leadership team with proven commitment to safety and operational excellence. Our Chief Executive Officer (“CEO”), Walter J. Scheller, III, is the former CEO of Walter Energy and has six years of direct experience managing Mine No. 4 and Mine No. 7, and over 30 years of experience in longwall coal mining. Furthermore, following the Asset Acquisition, we hired several key personnel with extensive direct operational experience in met coal longwall mining, including our Chief Operating Officer, Jack Richardson, and our Chairman, Stephen D. Williams. We have a strong record of operating safe mines and are committed to environmental excellence. Our dedication to safety is at the core of all of our overall operations as we work to further reduce workplace incidents by focusing on policy awareness and accident prevention. Our continued emphasis on enhancing our safety performance has resulted in zero fatal incidents as well as non-fatal days lost incidence rates of 3.73 at Mine No. 4 and 3.27 at Mine No. 7 for the year ended December 31, 2016, which are considerably lower than the 2016 national average incident rate for all underground coal mines in the United States of 4.99 non-fatal days lost per site.

Our Business Strategies

Our objective is to increase stockholder value through our continued focus on asset optimization and cost management to drive profitability and cash flow generation. Our key strategies to achieve this objective are described below:

Maximize profitable production. In the year ended December 31, 2016, we produced 3.1 million metric tons of met coal, predominantly from Mine No. 7, as we temporarily idled our Mine No. 4 in early 2016. We have the flexibility in our new initial CBA to increase annual production with relatively modest incremental capital expenditures. We operated at an annual combined production level of 7.3 million metric tons from Mine No. 4 and Mine No. 7 as recently as 2013. Based on our management’s operational experience, we are confident in our ability to produce at or close to this capacity in a safe and efficient manner, and with a comparable cost profile to our current costs, should market conditions warrant.

Maintain and further improve our low-cost operating cost profile. While we have already achieved significant structural cost reductions at our two operating mines around the time of the Asset Acquisition, we see further opportunities to reduce our costs over time. Our new initial CBA with the UMWA has been structured to support these ongoing cost optimization initiatives. For example, in our new initial CBA, we have additional flexibility in our operating days and alternative work schedules that were previously optional and more expensive under the Walter Energy collective bargaining agreement. All contractually guaranteed wage increases and bonus incentives are tied to HCC benchmark prices. Additionally, the new initial CBA enables us to contract out work under certain circumstances. We believe this type of structural incentive provision and workforce flexibility in the new initial CBA is helpful to further align our organization with operational excellence and to increase the proportion of our costs that vary in response to changes in the HCC benchmark price.

Broaden our marketing reach and potentially increase the realized prices we achieve for our coal. We have implemented a strategy to improve both our sales and marketing focus, with a goal of achieving better pricing relative to the HCC benchmark price, which includes: (i) using a combination of benchmark and index pricing with our contract customers; (ii) opportunistic selling into the spot met coal market; and (iii) selected instances of entering into longer term fixed price contracts. Each of these elements is intended to further embed our coal product among a broader group of steel customers. Traditionally, we have predominantly marketed our

5

Table of Contents

coal to European and South American buyers. However, we expect to increase our focus on Asian customers, in particular, Japanese steel mills, some of which have expressed a desire to diversify their supply of premium HCC away from Australian coals. In the near term, our target geographic customer mix is 60% in Europe, 30% in South America and 10% in Asia. We have an arrangement with Xcoal Energy & Resource (“Xcoal”) to serve as Xcoal’s exclusive and strategic partner for exports of low volatility HCC. Under this arrangement, Xcoal takes title to and markets coal that we would historically have sold on the spot market, in an amount of up to 10% of our sales. While the volumes being sold through this arrangement with Xcoal are relatively limited, we are positioned to potentially benefit from Xcoal’s expertise and relationships across all coal that we sell. To that end, we also have an incentive-based arrangement with Xcoal to cover other tonnage, in the event Xcoal is able to offer us a higher realized price relative to the HCC benchmark than we have previously achieved.

Rigorously evaluate our organic and inorganic growth pipeline, including the high-quality Blue Creek Energy Mine. We are continuously analyzing new opportunities to expand our business, but would require any mine openings or asset acquisitions to be highly strategic and additive to our existing high-quality met coal portfolio and result in a strong balance sheet on a pro forma basis. In particular, we own the undeveloped Blue Creek Energy Mine, which, based on a reserve report prepared by Norwest, had 103.0 million metric tons of high quality met coal recoverable reserves as of December 31, 2016. We believe that the Blue Creek Energy Mine is a large block of high quality coal reserves that could support a new longwall operation with a mine life of greater than 30 years. As such, management is evaluating additional leases for this site as well as considering approving additional engineering work to further evaluate this opportunity. Should we decide to develop it in the future, we expect that the Blue Creek Energy Mine would significantly increase our annual production.

Met Coal Industry Overview

Met coal or coking coal is an essential ingredient in the production of steel using blast furnaces. According to Wood Mackenzie, approximately 74.2% of the world’s steel production in 2016, or 1,211 million metric tons, was estimated to be manufactured using blast furnaces. Three major types of met coal are produced globally with varying characteristics: HCC, semi soft coking coal (“SSCC”) and pulverized coal for injection (“PCI”). Unlike SSCC and PCI, HCC currently has no substitutes and must be used in the production of steel by the blast furnace method. Furthermore, the physical properties of individual HCC seams have a significant impact on their suitability and value in use for blast furnace steel production. In particular, HCC that exhibits low volatile matter and limited swell is required for blending with coal containing less desirable qualities.

Global steel production is estimated to be 1,633 million metric tons in 2016, which is a 0.4% increase from 2015 and a 6.0% increase from 2011. Future growth in global steel demand and production will be largely driven by infrastructure investment and urbanization in developing markets, particularly China and India which are expected to account for 50.0% and 5.9% of global steel production in 2016, respectively, according to Wood Mackenzie. Global steel consumption and production will also be impacted by infrastructure improvement in developed countries, in particular the United States. Steel production in the United States was 78.4 million metric tons in 2016, representing a 0.6% decrease from 2015 and an 11.6% decrease from recent peak production in 2012. Approximately 33.4% of 2016 steel production in the United States, or 26.2 million metric tons, was manufactured using blast furnaces. Further, Wood Mackenzie forecasts global steel production to grow from current levels to 1,693 million metric tons in 2020, a 3.7% increase.

Met coal, and in particular HCC, is a scarce commodity with large scale mineable deposits limited to specific geographic regions located in the Eastern United States, Western Canada, Eastern Australia, Russia, China, Mozambique and Mongolia. Collectively, these countries are expected to represent 95.7% of global met coal production in 2016 according to Wood Mackenzie. Global met coal production is estimated to be 1,070 million metric tons in 2016, of which only 597 million metric tons, or 55.8%, was classified as HCC, according to Wood Mackenzie. Of this amount, Wood Mackenzie estimates that 192 million metric tons of HCC

6

Table of Contents

were traded on the seaborne market. Costs of production for met coal are driven by mine fundamentals and input costs such as labor, fuel and local currency. As mines age, mining costs tend to rise, driven by deeper open cut operations with higher strip ratios and greater distance from shafts and ramps to production areas underground. According to Wood Mackenzie, “Total Cash Cost” (as defined by Wood Mackenzie) of met coal production in Australia has risen by an estimated 15% from 2009 to 2017, when measured in local currency. In recent years, many producers responded to low prices by taking action to reduce costs and capital expenditures. As evidenced by recent mine closures, we believe that many producers will be unable to maintain costs at that level due to deferral of investment in aging equipment and infrastructure, and therefore we expect the marginal cost of production to increase over time.

Met coal trades in a global seaborne market and in domestic markets in areas of China and the United States where coal mines are located closer to regional suppliers than ocean ports. According to Wood Mackenzie, seaborne trade of met coal is expected to be 278 million metric tons in 2016. The United States is an important met coal supplier to the seaborne export market, and is the second largest supplier behind Australia. For 2016, Wood Mackenzie estimates these two countries were responsible for 11.7% and 66.6% of global seaborne met coal exports, respectively.

Over the last several years, significant oversupply in the market depressed prices, resulting in mine closures and production curtailments. The United States, with a relatively larger number of high-cost mines, experienced significant contraction in met coal production, from 82.9 million metric tons of production in 2012 to an expected 54.8 million metric tons in 2016, a 33.9% reduction.

Prices for met coal are generally set in the seaborne market, primarily driven by Japanese and Chinese import demand and Australian supply. Chinese import demand depends in part on Chinese steel production and domestic coal production. Of note, China is the largest met coal producer and consumer in the world, consuming over 99% of its 2016 production of 663 million metric tons of met coal domestically. However, due to the lower quality coal that is produced domestically and the distance of Chinese mines relative to the location of coastal steel mills, according to Wood Mackenzie, the Chinese domestic met coal market has a structural need for at least 30 million metric tons of premium benchmark quality HCC. Wood Mackenzie believes that this shortfall will be filled predominantly through the seaborne market, providing sustained demand support in the global seaborne market for premium quality HCC.

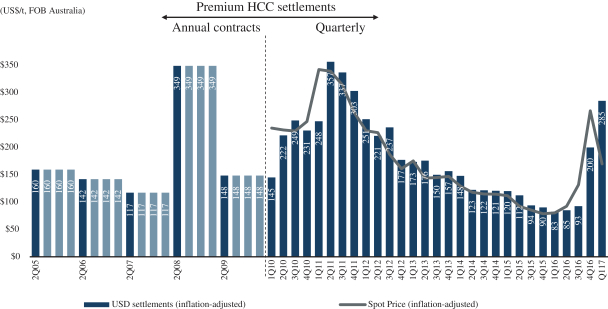

A quarterly benchmark HCC price is set between major Australian suppliers and major Japanese steel mill customers, and that price serves as a reference for most met coal, with adjustments for quality differences; there is also a spot market in which smaller volumes transact. Met coal prices have been highly volatile in the last decade due to seaborne supply disruptions, and more recently Chinese restrictions on domestic coal production. In 2008, benchmark coking coal prices reached $298 per metric ton in response to flooding in Australia’s producing regions, falling to $129 per metric ton in 2009. In 2011, benchmark prices reached $330 per metric ton as a result of flooding in Australia, falling back to $81 per metric ton five years later in early 2016.

In response to lower prices in 2015 and the first nine months of 2016, higher cost producers decreased or discontinued production, and we believe that they have been unable to respond quickly to higher prices due to the significant financial and regulatory burden associated with mine reopening, particularly in the United States. Additionally, Australian and Canadian mines are operating near capacity and would require significant capital investment to materially increase output. The lack of supply response was evident in late 2016, when in response to Chinese policy action, industry consolidation, and flooding in Chinese producing regions, the market saw a significant tightening in the global seaborne supply and demand balance, resulting in a corresponding increase in prices, with prices in the spot market increasing above $300 per metric ton in late 2016 and the first quarter 2017 benchmark contract price being set at $285 per metric ton. As of March 21, 2017, the spot market price was $153.30 per metric ton.

7

Table of Contents

Some of the factors that caused the recent rise in spot market pricing to above $300 per metric ton have eased, resulting in a decline in spot market prices to $153.30 per metric ton as of March 21, 2017. We believe this decline has been driven by (i) the temporary relaxation by the Chinese government of policies that were aimed to reduce domestic coal production and (ii) the resumption of production at Australian mines that had faced supply disruptions. Notwithstanding the recent pullback, spot market prices remain more than approximately 89% higher than the first quarter 2016 benchmark HCC settlement price of $81 per metric ton. The second quarter 2017 benchmark is expected to be set in late March 2017.

Over the long term, price levels between supply shock-induced spikes have been influenced by the marginal cost of production, which we expect to rise in coming years. According to Wood Mackenzie, in 2017, the Total Cash Cost of production for a mine at the 90th percentile of the global seaborne met coal cost curve is expected to be $93.34 per metric ton.

Risk Factors

There are a number of risks that you should understand before making an investment decision regarding this offering. These risks are discussed more fully in the section entitled “Risk Factors” beginning on page 20. These risks include, but are not limited to:

| • | Our business may suffer as a result of a substantial or extended decline in met coal pricing, demand and other factors beyond our control, which could negatively affect our operating results and cash flows. |

| • | Met coal mining involves many hazards and operating risks and is dependent upon many factors and conditions beyond our control, which may cause our profitability and our financial position to decline. |

| • | Significant competition, as well as changes in foreign markets or economics, could harm our sales, profitability and cash flows. |

| • | Extensive environmental, health and safety laws and regulations impose significant costs on our operations and future regulations could increase those costs, limit our ability to produce or adversely affect the demand for our products. |

Recent Developments

On , 2017, our board of managers declared a cash distribution payable to holders of our Class A Units, Class B Units and Class C Units as of , 2017, resulting in distributions to such holders in the aggregate amount of $190.0 million (the “Special Distribution”). The Special Distribution will be funded with available cash on hand and will be paid on , 2017. The Special Distribution will not apply to the shares of common stock to be sold in this offering.

On March 24, 2017, we entered into Amendment No. 2 (the “Second Amendment”) to our Asset-Based Revolving Credit Agreement, dated as of April 1, 2016, by and among the Company and certain of its subsidiaries, as borrowers, the guarantors party thereto, Citibank, N.A., as administrative agent, and the other lenders party thereto (as amended, the “ABL Facility”) to modify certain terms relating to the restricted payment covenant, which provides the Company with improved flexibility to pay dividends, including the Special Distribution.

Corporate History and Structure

Walter Energy Restructuring

Warrior Met Coal, LLC was formed on September 3, 2015 by certain lenders under Walter Energy’s 2011 Credit Agreement, dated as of April 1, 2011 (the “2011 Credit Agreement”), and the noteholders under Walter

8

Table of Contents

Energy’s 9.50% Senior Secured Notes due 2019 (such lenders and noteholders, collectively, “Walter Energy’s First Lien Lenders”) in connection with the acquisition by the Company of certain core assets of Walter Energy and certain of its wholly owned subsidiaries (the “Walter Energy Debtors”) related to their Alabama mining operations. The acquisition was accomplished through a credit bid of the first lien obligations of the Walter Energy Debtors pursuant to section 363 of the U.S. Bankruptcy Code and an order by the Bankruptcy Court (I) Approving the Sale of the Acquired Assets Free and Clear of Claims, Liens, Interests and Encumbrances; (II) Approving the Assumption and Assignment of Certain Executory Contracts and Unexpired Leases; and (III) Granting Related Relief (Case No. 15-02741, Docket No. 1584) (the “Sale Order” and the transactions contemplated thereunder, the “Asset Acquisition”). Prior to the closing of the Asset Acquisition, the Company had no operations and nominal assets. The Asset Acquisition closed on March 31, 2016.

Upon closing of the Asset Acquisition and in exchange for a portion of the outstanding first lien obligations of the Walter Energy Debtors, Walter Energy’s First Lien Lenders were entitled to receive, on a pro rata basis, a distribution of Class A Units in Warrior Met Coal, LLC. As of the date of this prospectus, there continue to be certain unfunded revolving loans under the 2011 Credit Agreement in the form of outstanding undrawn letters of credit arising under the first lien obligations of the Walter Energy Debtors. To the extent such letters of credit are drawn, including following the closing of this offering, the revolving lenders are entitled to an additional distribution of our equity interests. The maximum amount of equity that could be distributed on account of outstanding, but undrawn, letters of credit is less than 0.1% of our outstanding equity before giving effect to this offering.

In connection with the Asset Acquisition, we conducted rights offerings to Walter Energy’s First Lien Lenders and certain qualified unsecured creditors to purchase newly issued Class B Units of Warrior Met Coal, LLC, which diluted the Class A Units on a pro rata basis (the “Rights Offerings”). Proceeds from the Rights Offerings were used to pay certain costs associated with the Asset Acquisition and for general working capital purposes.

The transactions described above are collectively referred to as the “Walter Energy Restructuring.”

Post-IPO Corporate Structure

Prior to the effectiveness of the registration statement of which this prospectus forms a part, we will complete a corporate conversion pursuant to which Warrior Met Coal, LLC will be converted into a Delaware corporation and be renamed Warrior Met Coal, Inc. as described under “Corporate Conversion.”

Upon completion of the corporate conversion and this offering, investment funds managed, advised or sub-advised by Apollo Global Management LLC (“Apollo”) or its affiliates (such funds, the “Apollo Funds”) will own approximately % of our outstanding shares of common stock (or % if the underwriters’ option to acquire additional shares of common stock is exercised in full), investment funds managed, advised or sub-advised by GSO Capital Partners LP (“GSO”) or its affiliates (such funds, the “GSO Funds”) will own approximately % of our outstanding shares of common stock (or % if the underwriters’ option to acquire additional shares of common stock is exercised in full), investment funds managed, advised or sub-advised by KKR & Co. L.L.P. (“KKR”) or its affiliates (such funds, the “KKR Funds”) will own approximately % of our outstanding shares of common stock (or % if the underwriters’ option to acquire additional shares of common stock is exercised in full), and investment funds managed, advised or sub-advised by Franklin Mutual Advisers, LLC (“Franklin Mutual”) or its affiliates (such funds, the “Franklin Funds” and, together with the Apollo Funds, the GSO Funds and the KKR Funds, the “Principal Stockholders”) will own approximately % of our outstanding shares of common stock (or % if the underwriters’ option to acquire additional shares of common stock is exercised in full). In addition, members of our management team will own an approximate aggregate % interest in us.

9

Table of Contents

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenue during its last fiscal year, we qualify as an “emerging growth company” as defined in The Jumpstart our Business Startups Act (the “JOBS Act”). For as long as a company is deemed to be an emerging growth company, it may take advantage of specified reduced reporting and other regulatory requirements that are generally unavailable to other public companies. These provisions include:

| • | the presentation of only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations included in an initial public offering registration statement; |

| • | an exemption to provide less than five years of selected financial data in an initial public offering registration statement; |

| • | an exemption from compliance with any new requirements adopted by the Public Company Accounting Oversight Board (“PCAOB”) requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and the financial statements of the issuer; and |

| • | reduced disclosure about the company’s executive compensation arrangements. |

An emerging growth company is also exempt from Section 404(b) of The Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), which requires that the independent registered public accounting firm shall, in the same report, attest to and report on the assessment on the effectiveness of internal control over financial reporting, and from Sections 14A(a) and (b) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which require stockholder approval of executive compensation and golden parachutes.

In addition, Section 107 of the JOBS Act provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the “Securities Act”), for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies.

We have elected to take advantage of all of the applicable JOBS Act provisions, except that we will elect to opt out of the exemption that allows emerging growth companies to extend the transition period for complying with new or revised financial accounting standards. This election is irrevocable.

Accordingly, the information that we provide you may be different than what you may receive from other public companies in which you hold equity interests.

We may take advantage of these provisions until we are no longer an emerging growth company, which will occur upon the earliest of:

| • | the last day of the fiscal year following the fifth anniversary of this offering; |

| • | the last day of the fiscal year in which we have more than $1 billion in annual revenue; |

| • | the date on which we issue more than $1 billion in non-convertible debt securities over a three-year period; or |

| • | as of the end of any fiscal year in which the market value of our common stock held by non-affiliates exceeded $700 million as of the end of the second quarter of that fiscal year. |

10

Table of Contents

For more information, please see “Risk Factors—For so long as we are an “emerging growth company” we will not be required to comply with certain disclosure requirements that are applicable to other public companies and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common stock less attractive to investors.”

Our Offices

Our principal executive offices are located at 16243 Highway 216, Brookwood, Alabama 35444, and our telephone number at that address is (205) 554-6150. Our website address is www.warriormetcoal.com. Information contained on our website is not incorporated by reference herein and does not constitute part of this prospectus.

11

Table of Contents

The Offering

Common stock to be sold in this

| offering |

shares ( percent of shares outstanding) |

Total common stock outstanding

| before and after this offering |

shares |

| Over-allotment option |

The underwriters have an option to acquire a maximum of additional shares from the selling stockholders as described in “Underwriting” to cover over-allotments of shares. We will not receive any of the proceeds from the shares of common stock sold pursuant to the over-allotment option. |

| Use of proceeds |

We will not receive any proceeds from the sale of our common stock in this offering. All of the proceeds from this offering will be received by the selling stockholders. See “Use of Proceeds.” |

| Dividend policy |

While we have not made any cash distribution since our inception, our board of managers declared the Special Distribution on , 2017, which is payable to the holders of our Class A Units, Class B Units and Class C Units. The Special Distribution will be made on , 2017 and therefore not apply to the shares of our common stock to be sold in this offering. See “Dividend Policy.” |

After completion of this offering, we may pay cash dividends on our common stock, subject to our compliance with applicable law, and depending on, among other things, our results of operations, financial condition, level of indebtedness, capital requirements, contractual restrictions, restrictions in our debt agreements and in any preferred stock, business prospects and other factors that our board of directors may deem relevant. Our ability to pay dividends on our common stock is limited by covenants in our ABL Facility, and may be further restricted by the terms of any future debt or preferred securities. See “Dividend Policy” and “Description of Certain Indebtedness.”

| NYSE listing symbol |

We have been approved to list our shares of common stock on the New York Stock Exchange (the “NYSE“) under the symbol “HCC.” |

| Risk factors |

You should carefully read and consider the information beginning on page 20 of this prospectus set forth under the heading “Risk Factors” and all other information set forth in this prospectus before deciding to invest in our common stock. |

Unless otherwise indicated, all references to the number and percentage of shares of common stock outstanding and percentage ownership information are based on the shares of common stock to be outstanding following the corporate conversion assuming the following:

| • | the conversion of Warrior Met Coal, LLC from a Delaware limited liability company to a Delaware corporation prior to the effective date of the registration statement of which this prospectus forms a part |

12

Table of Contents

| and, in connection therewith, the automatic conversion of Class B Units of Warrior Met Coal, LLC into Class A Units of Warrior Met Coal, LLC upon termination of the additional capital commitment, as discussed under “Corporate Conversion,” followed by the conversion of the then outstanding Class A Units and Class C Units of Warrior Met Coal, LLC into an aggregate of shares of common stock of Warrior Met Coal, Inc., assuming the corporate conversion occurred on , 2017; |

| • | there is no exercise of the underwriters’ option to purchase up to additional shares of our common stock to cover over-allotments, if any; and |

| • | the number of shares of common stock excludes approximately shares of our common stock reserved for issuance under our equity award plan for our employees and directors. |

13

Table of Contents

Summary Consolidated and Combined Historical and Pro Forma Financial Data

The following tables set forth our summary consolidated and combined historical and pro forma financial data as of and for each of the periods indicated. The summary consolidated historical financial data as of December 31, 2016 and for the nine months ended December 31, 2016 is derived from the audited consolidated financial statements of the Successor included elsewhere in this prospectus. The summary combined historical financial data as of December 31, 2015 and for the three months ended March 31, 2016 and the year ended December 31, 2015 is derived from the audited combined financial statements of our Predecessor included elsewhere in this prospectus. The term “Successor” refers to (1) Warrior Met Coal, LLC and its subsidiaries for periods beginning as of April 1, 2016 and ending immediately before the completion of our corporate conversion and (2) Warrior Met Coal, Inc. and its subsidiaries for periods beginning with the completion of our corporate conversion and thereafter. The term “Predecessor” refers to the assets acquired and liabilities assumed by Warrior Met Coal, LLC from Walter Energy in the Asset Acquisition on March 31, 2016. The Predecessor periods included in this prospectus begin as of January 1, 2015 and end as of March 31, 2016.

The summary unaudited pro forma statement of operations data for the year ended December 31, 2016 is derived from the unaudited pro forma condensed combined statement of operations included elsewhere in this prospectus. The unaudited pro forma condensed combined statement of operations for the year ended December 31, 2016 assumes that the Asset Acquisition, this offering and the Special Distribution (collectively, the “Transactions”) occurred as of January 1, 2015. The summary unaudited pro forma balance sheet data as of December 31, 2016 assumes that the declaration of the Special Distribution occurred as of December 31, 2016. The summary unaudited pro forma financial data is based upon available information and certain assumptions that management believes are factually supportable, are reasonable under the circumstances and are directly related to the Transactions. The summary unaudited pro forma financial data is provided for informational purposes only and does not purport to represent what our results of operations or financial position actually would have been if these transactions had occurred at any other date, and such data does not purport to project our results of operations for any future period.

You should read this summary consolidated and combined historical and pro forma financial data together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Selected Consolidated and Combined Historical and Pro Forma Financial Data,” the unaudited pro forma condensed combined statements of operations and the audited financial statements and related notes thereto included elsewhere in this prospectus. Our historical results are not necessarily indicative of our future results of operations, financial position and cash flows.

14

Table of Contents

| Historical | Pro Forma | |||||||||||||||

| Successor | Predecessor | Predecessor/ Successor |

||||||||||||||

| For the nine months ended December 31, 2016(1) |

For the three months ended March 31, 2016 |

For the year ended December 31, 2015 |

For the year ended December 31, 2016 |

|||||||||||||

| (in thousands, except per unit, per share and per metric ton data) |

||||||||||||||||

| Statements of Operations Data: |

||||||||||||||||

| Revenues: |

||||||||||||||||

| Sales |

$ | 276,560 | $ | 65,154 | $ | 514,334 | $ | 341,714 | ||||||||

| Other revenues |

21,074 | 6,229 | 30,399 | 27,303 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenues |

297,634 | 71,383 | 544,733 | 369,017 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Costs and expenses: |

||||||||||||||||

| Cost of sales (exclusive of items shown separately below) |

244,723 | 72,297 | 601,545 | 315,563 | ||||||||||||

| Cost of other revenues (exclusive of items shown separately below) |

19,367 | 4,698 | 27,442 | 24,065 | ||||||||||||

| Depreciation and depletion |

47,413 | 28,958 | 123,633 | 58,950 | ||||||||||||

| Selling, general and administrative |

20,507 | 9,008 | 38,922 | 29,515 | ||||||||||||

| Other postretirement benefits |

— | 6,160 | 30,899 | — | ||||||||||||

| Restructuring costs |

— | 3,418 | 13,832 | 3,418 | ||||||||||||

| Asset impairment charges |

— | — | 27,986 | — | ||||||||||||

| Transaction and other costs |

13,568 | — | — | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total costs and expenses |

345,578 | 124,539 | 864,259 | 431,511 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating loss |

(47,944 | ) | (53,156 | ) | (319,526 | ) | (62,494 | ) | ||||||||

| Interest expense, net |

(1,711 | ) | (16,562 | ) | (51,077 | ) | (2,243 | ) | ||||||||

| Gain on extinguishment of debt |

— | — | 26,968 | — | ||||||||||||

| Reorganization items, net |

— | 7,920 | (7,735 | ) | — | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss before income taxes |

(49,655 | ) | (61,798 | ) | (351,370 | ) | (64,737 | ) | ||||||||

| Income tax expense (benefit) |

18 | 18 | (40,789 | ) | 36 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss |

$ | (49,673 | ) | $ | (61,816 | ) | $ | (310,581 | ) | $ | (64,773 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss per unit—basic and diluted |

$ | (13.15 | ) | |||||||||||||

| Weighted average units outstanding—basic and diluted |

3,777 | |||||||||||||||

| Supplemental pro forma net loss per share—basic and diluted(2) |

$ | |||||||||||||||

| Supplemental pro forma weighted average shares outstanding—basic and diluted(2) |

||||||||||||||||

| Statements of Cash Flow Data: |

||||||||||||||||

| Cash provided by (used in): |

||||||||||||||||

| Operating activities |

$ | (9,187 | ) | $ | (40,698 | ) | $ | (131,818 | ) | |||||||

| Investing activities |

$ | (30,884 | ) | $ | (5,422 | ) | $ | (64,249 | ) | |||||||

| Financing activities |

$ | 192,727 | $ | (6,240 | ) | $ | (147,145 | ) | ||||||||

| Other Financial Data: |

||||||||||||||||

| Depreciation and depletion |

$ | 47,413 | $ | 28,958 | $ | 123,633 | $ | 58,950 | ||||||||

| Capital expenditures(3) |

$ | 11,531 | $ | 5,422 | $ | 64,971 | ||||||||||

| Adjusted EBITDA(4) |

$ | 50,089 | $ | (9,048 | ) | $ | (145,805 | ) | $ | 48,428 | ||||||

| Sales Data: |

||||||||||||||||

| Metric tons sold |

2,391 | 777 | 5,121 | 3,168 | ||||||||||||

| Average selling price per metric ton |

$ | 115.67 | $ | 83.85 | $ | 100.44 | $ | 107.86 | ||||||||

| Cash cost of sales (free-on-board port) per metric ton(5) |

$ | 82.84 | $ | 69.74 | $ | 112.96 | $ | 79.17 | ||||||||

15

Table of Contents

| Pro Forma(6) | Historical | |||||||||||

| Successor | Successor | Predecessor | ||||||||||

| December 31, 2016 |

December 31, 2016 |

December 31, 2015 |

||||||||||

| (in thousands) | ||||||||||||

| Balance Sheet Data: |

||||||||||||

| Cash and cash equivalents |

$ | 150,045 | $ | 150,045 | $ | 79,762 | ||||||

| Working capital(7) |

$ | 36,137 | $ | 226,137 | $ | 129,558 | ||||||

| Mineral interests, net |

$ | 143,231 | $ | 143,231 | $ | 5,295 | ||||||

| Property, plant and equipment, net |

$ | 496,959 | $ | 496,959 | $ | 567,594 | ||||||

| Total assets |

$ | 947,631 | $ | 947,631 | $ | 802,137 | ||||||

| Long-term debt(8) |

$ | 3,725 | $ | 3,725 | $ | — | ||||||

| Total liabilities not subject to compromise |

$ | 384,664 | $ | 194,664 | $ | 126,720 | ||||||

| Total members’ equity and parent net investment |

$ | 562,967 | $ | 752,967 | $ | (820,861 | ) | |||||

| (1) | For the three months ended December 31, 2016, (i) the average HCC quarterly benchmark price per metric ton was $200.00, (ii) our average realized price per metric ton was $169.47, (iii) metric tons sold were 0.9 million, (iv) our revenues were $153.5 million, (v) our Adjusted EBITDA, a non-GAAP financial measure, was $51.3 million, (vi) our cash cost of sales, a non-GAAP financial measure, per metric ton were $88.41 and (vii) our capital expenditures were $3.1 million. For a definition of Adjusted EBITDA and a reconciliation to our most directly comparable financial measure calculated and presented in accordance with GAAP, please read “—Non-GAAP Financial Measures—Adjusted EBITDA.” For a definition of cash cost of sales and a reconciliation to our most directly comparable financial measure calculated and presented in accordance with GAAP, please read “—Non-GAAP Financial Measures—Cash Cost of Sales.” |

| (2) | We present certain per share data on a supplemental pro forma basis to the extent that the proceeds from this offering will be deemed to be used to fund the Special Distribution of $190.0 million. For further information on the supplemental pro forma per share data, see Note 26 to our audited financial statements included elsewhere in this prospectus. |

| (3) | Capital expenditures consist of the purchases of property, plant and equipment. |

| (4) | Adjusted EBITDA is a non-GAAP financial measure. For a definition of Adjusted EBITDA and a reconciliation to our most directly comparable financial measure calculated and presented in accordance with GAAP, please read “—Non-GAAP Financial Measures—Adjusted EBITDA.” |

| (5) | Cash cost of sales is a non-GAAP financial measure. For a definition of cash cost of sales and a reconciliation to our most directly comparable financial measure calculated and presented in accordance with GAAP, please read “—Non-GAAP Financial Measures—Cash Cost of Sales.” |

| (6) | Reflects the declaration of the Special Distribution. See Note 26 to our audited financial statements appearing elsewhere in this prospectus for information regarding this unaudited pro forma balance sheet data. |

| (7) | Working capital consists of current assets less current liabilities. |

| (8) | Represents a security agreement and the long-term portion of a promissory note assumed in the Asset Acquisition. The agreement was entered into for the purchase of underground mining equipment. The promissory note matures on March 31, 2019, has a fixed interest rate of 4.00% per annum and is secured by the underground mining equipment it was used to purchase. |

Non-GAAP Financial Measures

Cash Cost of Sales

Cash cost of sales is based on reported cost of sales and includes items such as freight, royalties, manpower, fuel and other similar production and sales cost items, and may be adjusted for other items that, pursuant to accounting principles generally accepted in the United States (“GAAP”), are classified in the Statements of Operations as costs other than cost of sales, but relate directly to the costs incurred to produce met coal and sell it free-on-board at the Port of Mobile. Our cash cost of sales per metric ton is calculated as cash cost of sales divided by the metric tons sold.

16

Table of Contents

Cash costs of sales is a financial measure that is not calculated in conformity with GAAP and should be considered supplemental to, and not as a substitute or superior to, financial measures calculated in conformity with GAAP. We believe that this non-GAAP financial measure provides additional insight into our operating performance, and reflects how management analyzes our operating performance and compares that performance against other companies on a consistent basis for purposes of business decision making by excluding the impact of certain items that management does not believe are indicative of our core operating performance. We believe that cash costs of sales presents a useful measure of our controllable costs and our operational results by including all costs incurred to produce met coal and sell it free-on-board at the Port of Mobile. Period-to-period comparisons of cash cost of sales are intended to help our management identify and assess additional trends potentially impacting our Company that may not be shown solely by period-to-period comparisons of cost of sales. In addition, we believe that cash costs of sales is a useful measure as some investors and analysts use it to compare us against other companies. However, cash cost of sales may not be comparable to similarly titled measures used by other entities.

The following table presents a reconciliation of cost of sales to cash costs of sales (in thousands):

| Historical | Pro Forma | |||||||||||||||

| Successor | Predecessor | Predecessor/ Successor |

||||||||||||||

| For the nine months ended December 31, 2016(3) |

For the three months ended March 31, 2016 |

For the year ended December 31, 2015 |

For the year ended December 31, 2016 |

|||||||||||||

| Cost of sales |

$ | 244,723 | $ | 72,297 | $ | 601,545 | $ | 315,563 | ||||||||

| Mine No. 4 idle costs(1) |

(8,726 | ) | (10,173 | ) | — | (18,899 | ) | |||||||||

| VEBA contribution(2) |

(25,000 | ) | — | — | (25,000 | ) | ||||||||||

| Other (operating overhead, etc.) |

(12,922 | ) | (7,936 | ) | (23,077 | ) | (20,858 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Cash cost of sales |

$ | 198,075 | $ | 54,188 | $ | 578,468 | $ | 250,806 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Represents idle costs incurred, such as electricity, insurance and maintenance labor. This mine was idled in early 2016. |

| (2) | We entered into a new initial CBA with the UMWA pursuant to which we agreed to contribute $25.0 million to a Voluntary Employees’ Beneficiary Association (“VEBA”) trust formed and administered by the UMWA. |

| (3) | The following table presents a reconciliation of cost of sales to cash cost of sales for the three months ended December 31, 2016 (in thousands): |

| Successor | ||||

| For the three months ended December 31, 2016 |

||||

| Cost of sales |

$ | 85,960 | ||

| Other (operating overhead, etc.) |

(9,474 | ) | ||

|

|

|

|||

| Cash cost of sales |

$ | 76,486 | ||

|

|

|

|||

Adjusted EBITDA