Attached files

| file | filename |

|---|---|

| EX-32.1 - EX-32.1 - Heritage Insurance Holdings, Inc. | hrtg-ex321_8.htm |

| EX-31.2 - EX-31.2 - Heritage Insurance Holdings, Inc. | hrtg-ex312_6.htm |

| EX-31.1 - EX-31.1 - Heritage Insurance Holdings, Inc. | hrtg-ex311_9.htm |

| EX-23.1 - EX-23.1 - Heritage Insurance Holdings, Inc. | hrtg-ex231_7.htm |

F7780

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Year Ended December 31, 2016

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period From to

Commission File Number 001-36462

Heritage Insurance Holdings, Inc.

|

Delaware |

|

45-5338504 |

|

(STATE OF INCORPORATION) |

|

(I.R.S. ID) |

2600 McCormick Drive, Suite 300, Clearwater, Florida 33759

(727) 362-7200

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class |

|

|

Name of Each Exchange on Which Registered |

|

Common Stock, par value $0.0001 per share |

|

|

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☒ |

|

|

|

|

|

|

|

|

|

Non-accelerated filer |

|

☐ (Do not check if a smaller reporting company) |

|

Smaller reporting company |

|

☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the Registrant’s common stock held by non-affiliates was $244,038,590 on June 30, 2016, computed on the basis on the closing sale price of the Registrant’s common stock on the New York Stock Exchange on that date.

As of March 1, 2017, the number of shares outstanding of the Registrant’s common stock was 29,740,441.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement for its Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K, provided that if such Proxy Statement is not filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year covered by this Form 10-K, an amendment to this Form 10-K shall be filed no later than the end of such 120-day period.

HERITAGE INSURANCE HOLDINGS, INC.

FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2016

Table of Contents

|

|

|

|

|

Page |

|

|

|

|

||

|

|

|

|||

|

Item 1. |

|

|

1 |

|

|

Item 1A. |

|

|

16 |

|

|

Item 1B. |

|

|

29 |

|

|

Item 2. |

|

|

29 |

|

|

Item 3. |

|

|

29 |

|

|

Item 4. |

|

|

29 |

|

|

|

|

|

|

|

|

|

|

|||

|

Item 5. |

|

|

30 |

|

|

Item 6. |

|

|

31 |

|

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

32 |

|

Item 7A. |

|

|

48 |

|

|

Item 8. |

|

|

50 |

|

|

Item 9. |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

90 |

|

Item 9A. |

|

|

90 |

|

|

Item 9B. |

|

|

91 |

|

|

|

|

|

|

|

|

|

|

|||

|

Item 10. |

|

|

91 |

|

|

Item 11. |

|

|

91 |

|

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

91 |

|

Item 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

|

91 |

|

Item 14. |

|

|

92 |

|

|

|

|

|

|

|

|

|

|

|||

|

Item 15. |

|

|

92 |

|

|

Item 16. |

|

|

94 |

|

|

|

|

|

|

|

|

|

95 |

|||

|

|

|

|

||

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the federal securities laws. These forward-looking statements include, but are not limited to, statements regarding: our core strategy; our growth, results of operations or liquidity; statements concerning projections, predictions, expectations, estimates or forecasts as to our business, financial and operational results and future economic performance; statements of management’s goals and objectives; projections of revenue, earnings, capital structure and other financial items; assumptions underlying statements regarding us and our business; and other similar expressions concerning matters that are not historical facts. These forward-looking statements are subject to risks and uncertainties that could cause actual results and events to differ. A detailed discussion of these and other risks and uncertainties that could cause actual results and events to differ materially from such forward-looking statements is included throughout this filing and particularly in Item 1A: "Risk Factors" and Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” set forth in this Annual Report on Form 10-K. All forward-looking statements included in this document are based on information available to us on the date hereof, and we assume no obligation to revise or publicly release any revision to any such forward-looking statement, except as may otherwise be required by law.

These statements are based on current expectations, estimates and projections about the industry and market in which we operate, and management’s beliefs and assumptions. Without limiting the generality of the foregoing, words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “would,” “estimate,” or “continue” or the negative variations thereof or comparable terminology are intended to identify forward-looking statements. Forward-looking statements are not guarantees of future performance and involve certain known and unknown risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such statements. The risks and uncertainties include, without limitation:

|

|

• |

our limited operating history; |

|

|

• |

the possibility that actual losses may exceed reserves; |

|

|

• |

the concentration of our business in Florida and Hawaii; |

|

|

• |

our exposure to catastrophic events; |

|

|

• |

the fluctuation in our results of operations; |

|

|

• |

increased costs of reinsurance, non-availability of reinsurance, and non-collectability of reinsurance; |

|

|

• |

increased competition, competitive pressures, and market conditions; |

|

|

• |

our failure to accurately price the risks we underwrite; |

|

|

• |

inherent uncertainty of our models and our reliance on such model as a tool to evaluate risk; |

|

|

• |

the failure of our claims department to effectively manage or remediate claims; |

|

|

• |

low renewal rates and failure of such renewals to meet our expectations; |

|

|

• |

our failure to execute our growth strategy; |

|

|

• |

failure of our information technology systems and unsuccessful development and implementation of new technologies; |

|

|

• |

we do not have significant redundancy in our operations; |

|

|

• |

our failure to attract and retain qualified employees and independent agents or our loss of key personnel; |

|

|

• |

our inability to generate investment income; |

|

|

• |

our inability to maintain our financial stability rating; |

|

|

• |

effects of emerging claim and coverage issues relating to legal, judicial, environmental and social conditions; |

|

|

• |

the failure of our risk mitigation strategies or loss limitation methods; and |

|

|

• |

changes in regulations and our failure to meet increased regulatory requirements. |

Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial condition or operating results.

The forward-looking statements speak only as of the date on which they are made, and, except as required by law, we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrences of anticipated events. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in the forward-looking statements. Consequently, you should not place undue reliance on forward-looking statements.

Our Business

Heritage Insurance Holdings, Inc., (“we”, “our”, “us” and “Heritage Insurance”) is a property and casualty insurance holding company that provides personal and commercial residential insurance. We are headquartered in Clearwater, Florida and, through our subsidiaries, Heritage Property & Casualty Insurance Company (“Heritage P&C”) and Zephyr Insurance Company (“Zephyr”), we write personal residential insurance for single-family homeowners and condominium owners, and rental property insurance in the states of Florida, Hawaii, North Carolina and South Carolina. We also provide commercial residential insurance for Florida properties and are also licensed in the states of Alabama, Georgia and Mississippi. We are vertically integrated and control or manage substantially all aspects of insurance underwriting, customer service, actuarial analysis, distribution and claims processing and adjusting. We are led by an experienced senior management team with an average of 30 years of insurance industry experience. We began operations in August 2012, and in December 2012 we began selectively assuming policies from Citizens Property Insurance Corporation (“Citizens”), a Florida state-supported insurer, through participation in a legislatively established “depopulation program” designed to reduce the state’s risk exposure by encouraging private companies to assume insurance policies from Citizens. We also write policies outside the Citizens depopulation program, which we refer to as voluntary policies. At December 31, 2016, approximately 53% of our policies in force were assumed from Citizens. Heritage P&C and Zephyr are currently rated “A” (“Exceptional”) or better by Demotech, Inc. (“Demotech”), a rating agency specializing in evaluating the financial stability of insurers.

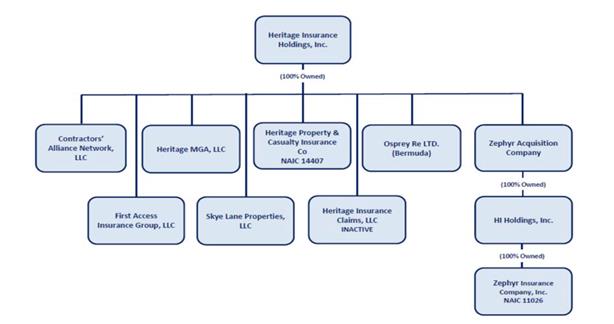

In addition to Heritage P&C, our other subsidiaries include: Heritage Property & Casualty Insurance Company (“Heritage P&C”), which provides personal and commercial residential insurance; Heritage MGA, LLC, the managing general agent that manages substantially all aspects of our Florida insurance subsidiary’s business; Contractors’ Alliance Network, LLC (“CAN”), our vendor network manager for Florida claims which includes BRC Restoration Specialists, Inc. (“BRC”), our provider of restoration, emergency and recovery services; Zephyr Acquisition Company (“ZAC”) and its wholly-owned subsidiary, Zephyr Insurance Company, Inc. (“Zephyr”), our provider for writing insurance policies for residential wind insurance within the State of Hawaii; Skye Lane Properties, LLC, our property management subsidiary; First Access Insurance Group, LLC, our retail agency; Osprey Re Ltd. (“Osprey”), our reinsurance subsidiary that provides a portion of the reinsurance protection purchased by our insurance subsidiaries; and Heritage Insurance Claims, LLC, an inactive subsidiary reserved for future development. The assets of BRC, a building restoration company, were acquired and merged into CAN in 2015. The assets of SVM Restoration Services Inc. (“SVM”), a water mitigation company, were acquired and merged into CAN in 2014.

Our Company

Our company was initially formed as a Florida limited liability company in 2012. On January 1, 2014, we formed a Delaware limited liability company, also named Heritage Insurance Holdings, LLC, and merged with it in order to domicile the Company in

1

Delaware. Effective May 22, 2014, Heritage Insurance Holdings, LLC converted into a Delaware corporation named Heritage Insurance Holdings, Inc.

Our primary products are personal and commercial residential insurance, which at December 31, 2016 were offered in Florida, North Carolina, South Carolina and Hawaii. Our Florida domiciled insurance company, Heritage P&C, is authorized by each of the respective state insurance departments in Florida, North Carolina, South Carolina, George, Alabama and Mississippi. Our Hawaii domiciled insurance company, Zephyr, writes business only in Hawaii and is authorized by the Hawaii Insurance Division. We conduct our operations under one business segment.

As of December 31, 2016, we had 319,676 personal residential policies in force, representing $516.7 million of annualized premium and 3,625 commercial residential policies in force, representing $118.6 million of annualized premium. Approximately 53% of our personal policies and 53% of our commercial policies as of December 31, 2016 were assumed from Citizens. For the years ended December 31, 2016, 2015, and 2014, we had gross premiums written of $626.7 million, $586.1 million and $436.4 million, respectively, and net income of $33.9 million, $92.5 million and $47.1 million, respectively. At December 31, 2016 and 2015, we had total assets of $1 billion and $837.4 million, respectively, and total stockholders’ equity of $358 million and $357 million, respectively.

As of December 31, 2016, Citizens had approximately 456,000 insurance policies, of which approximately 440,000 were personal residential policies and approximately 5,900 were commercial residential policies. We have selectively assumed personal residential policies from Citizens in 27 separate assumption transactions between December 2012 and May 2016. In October 2014 we completed our first commercial residential assumption transaction. During 2016, approximately 11,900 policies were assumed from Citizens. Given the reduced policy count at Citizens resulting from the depopulation program, we do not expect to continue to assume policies from Citizens in the foreseeable future.

Recent Developments

On December 15, 2016, the Company issued $79.5 million in Senior Secured Notes (“Secured Notes”) due 2023 to six accredited investors. Proceeds will be used to participate opportunistically in mergers and acquisitions, to make strategic investments and for general corporate purposes. In connection with the issuance of the Notes, the Company incurred $6.6 million in debt issuance costs. Debt issuance costs are reflected on the consolidated balance sheet as a contra long-term liability, and amortized using the imputed interest method over the life of the underlying debt instrument. For tax purposes, the debt issuance costs are generally amortized over the life of the debt using the straight-line method. See Note 11 — “Note Payable” to our consolidated financial statements under Item 8 of this Annual Report on Form 10-K.

On August 28, 2016 and October 1, 2016, Hurricanes Hermine and Matthew struck Florida. These were the first hurricanes to affect Florida since the 2004/2005 hurricane seasons. The impact to our 2016 net income was $13.4 million. Losses for Hurricanes Matthew and Hermine are estimated to be $18.8 million and $3 million, respectively, before tax. Our reinsurance coverage for the season could exceed $3.1 billion in total with up to $2 billion for a first event. Our Florida retention for our reinsurance coverage is $40 million. Thus, there were no recoveries from reinsurers related to the Hurricanes Hermine and Matthew in 2016.

On March 21, 2016, the Company acquired 100% of the outstanding stock of ZAC and its wholly-owned subsidiary, Zephyr, in exchange for approximately $110.3 million net of cash acquired. Zephyr is a specialty property insurance provider that offers policies for residential customers in Hawaii that cover the peril of windstorm losses caused by a hurricane. This acquisition furthers the Company’s strategic push to diversify business operations and achieve potential reinsurance synergies while expanding growth opportunities outside of Florida. The acquisition provides Heritage with an immediate presence in Hawaii with Zephyr holding approximately 30% of the wind-only market share in the state. The purchase price for the acquisition was approximately $134 million.

On September 14, 2015, the Company announced that the Board of Directors authorized a $20 million share repurchase program through December 31, 2016 under which purchases may be made from time to time in the open market, or through privately negotiated transactions, block transactions or other techniques, as determined by the Company’s management. On May 4, 2016, the Board of Directors authorized an additional stock repurchase of up to $50 million of the Company’s common stock through December 31, 2017. For the year ended December 31, 2016, the Company had purchased through open market or private transactions an aggregate of 1,759,330 shares at a total cost of $25.6 million and had available to purchase under the program $44.4 million.

On March 1, 2016, the Company’s Board of Directors declared a $0.05 per share quarterly cash dividends payable on April 5, 2016, to stockholders of record on March 15, 2016. On May 4, 2016, the Company announced the Board of Directors had declared a second quarter dividend of $0.06 per share to stockholders of record as of June 15, 2016. The dividend was paid on July 1, 2016. On August 1, 2016, the Company announced that its Board of Directors declared a third quarter dividend of $0.06 per common share. The dividend was paid on October 03, 2016. On November 8, 2016, the Company announced that its Board of Directors has declared a quarterly cash dividend on the Company’s common stock of $0.06 per share. The fourth quarter dividend of $0.06 per share was paid on January 4, 2017 to stockholders of record as of December 15, 2016. The declaration and payment of any future dividends will

2

be subject to the discretion of the Board of Directors and will depend on a variety of factors including the Company’s financial condition and results of operations.

In August 2015, the Company announced that it received its Certificate of Authority (“COA”) to write property and casualty insurance in the state of North Carolina, which marked the beginning of the Heritage P&C multi-state expansion. In 2016, Heritage P&C also received its COA in South Carolina, Georgia, Alabama and Mississippi. The Company currently actively writes business in Florida, Hawaii, North Carolina, South Carolina, and in 2017 began writing policies in Georgia.

In July 2015, the Company acquired substantially all of the assets of BRC, a Florida based provider of restoration services and emergency and recovery assistance. At closing, Company paid $6 million in cash and 79,850 shares of the Company’s common stock valued at $2 million.

Our Strategy

From our inception until December 31, 2015, a substantial portion of our new business was generated from policies we assumed from Citizens and Sunshine State Insurance Company (“SSIC”). The renewal of these assumed policies, new voluntary business, and renewals of voluntary policies and from our newly acquired Zephyr business comprises our revenue for 2016. We intend to continue to grow profitably by undertaking the following:

Mergers and Acquisitions and/or Making Strategic Investments

We successfully closed strategic acquisitions in each of 2014, 2015 and 2016. This includes the acquisition of substantially all of the assets of SVM and BRC, acquisition of the SSIC policies, and acquisition of the stock of ZAC. The acquisitions of SVM and BRC provided unique claims adjusting and repair resources to better serve our policyholders and better manage loss costs. At December 31, 2016, we had 19,680 SSIC policies in force with an annualized premium of $34.7 million. The acquisition of Zephyr provided an immediate presence in the state of Hawaii with approximately $58 million in annual voluntary premium and a strategic diversification to our platform as well as leveraged reinsurance synergies. We recently closed a private placement of senior secured notes, which provides net proceeds of over $70 million of resources to make strategic investments. These activities demonstrate our commitment and capability to successfully identify, finance, and execute mergers and acquisitions to effectively grow our business.

Expand to New Geographic Markets

Heritage P&C became authorized to write property business in Florida, North Carolina, South Carolina, Georgia, Alabama, and Mississippi and is actively writing in North Carolina and South Carolina. We intend to explore opportunities to enter other states where we can utilize our underwriting and claims expertise to attract and manage profitable business. We believe further increasing our geographic diversification is an important factor in reducing our potential risk of loss from any single catastrophic event, reducing our per policy reinsurance costs and providing an additional arena for future growth beyond our existing market. In addition, through our acquisition of Zephyr we acquired over 70,000 policies in the state of Hawaii. For example, we entered into a marketing agreement with National General Insurance Company and began writing homeowners insurance through their distribution network in early 2016 in the state of North Carolina.

Increase Our Premium in Force in Florida

We have significantly expanded our marketing efforts in Florida. We intend to increase the number of profitable voluntary personal lines policies through expansion of strategic relationships with our independent agent distribution network and other producers of personal lines property insurance in Florida. We currently write commercial residential business in the state of Florida only and we anticipate expansion of our commercial residential business in the state. We may also expand market share through strategic opportunities to acquire profitable business from private insurers. We do not anticipate continuing to assume policies from Citizens.

Optimize Our Reinsurance Program

We will continue to obtain what we believe to be the most appropriate levels and sources of reinsurance. We believe that the significant additional capital entering portions of the reinsurance market provides us with the opportunity to obtain favorable pricing and contract terms and conditions, including multi-year commitments, which comprise a significant portion of our 2016-2017 reinsurance program. For the 2014, 2015 and 2016 hurricane seasons, we entered into fully collateralized multi-year catastrophe reinsurance agreements funded through the issuance of a total of $727.5 million principal amount of catastrophe bonds, and we will continue evaluating such cost-efficient alternatives to traditional reinsurance. Additionally, we will continue to meet certain of our reinsurance needs through the use of our reinsurance subsidiary, Osprey, which helps to manage our reinsurance expense and reduces our reliance on third-party reinsurance.

3

Efficiently Manage Losses and Loss Adjustment Expenses

We are committed to proactively managing our losses and loss adjustment expenses through prudent underwriting performing critical aspects of claims adjusting through our employees, and the use of internal claims adjustment and repair services. In March 2014, we acquired the largest vendor in the CAN network, which we believe has allowed us to expand our in-house mitigation and restoration services. Additionally, the 2015 acquisition of assets of BRC provides us with additional resources and capabilities to perform restoration services in-house, as well as provide construction resources after a catastrophic event. We have additional contracted resources to adjust claims and mitigate losses which were deployed after Hurricanes Hermine and Matthew. The multitude of internal and external resources allowed us to deliver timely service to our policyholders and better manage claims costs

Effectively Manage the Bottom Line

In addition to our proactive efforts to manage losses and loss adjustment expenses, we will continue to be proactive with respect to technology to better serve our agents and policyholders, streamline our processes, manage systems implementation costs, and focus on efficiency.

Our Competitive Strengths

We believe that our growth to date and our ability to capitalize on our future growth prospects are a result of the following competitive strengths of our business:

Experienced Management Team With a Long History in the Residential Property Insurance Market

We have a deep and experienced executive management team led by Bruce Lucas, Chairman and Chief Executive Officer, Richard Widdicombe, President, Steven Martindale, Chief Financial Officer, and Ernesto Garateix, Chief Operating Officer. Our senior management team includes twelve insurance professionals, which averages 30 years of insurance industry experience, has extensive experience in the personal and commercial residential insurance market, particularly in Florida, has built longstanding relationships with key participants in the insurance industry and is supported by a group of highly qualified individuals with industry expertise, including a Chief Actuary with more than 37 years of industry experience.

Strong, Conservative Capital Structure

As of December 31, 2016, we had stockholders’ equity of $358 million. As of December 31, 2016, Heritage P&C and Zephyr had policyholder surplus, as defined by statutory accounting principles, of $200 million and $76 million, respectively. We believe that these levels of surplus places us among the best capitalized insurance companies focusing primarily on the Florida personal residential insurance market and the Hawaii wind-only residential market and is in excess of the minimum capital levels required by our insurance regulators and Demotech for similarly rated in-state insurance companies.

Selective Underwriting and Policy Acquisition Criteria

We believe our proprietary data analytics capabilities and underwriting processes has allowed us to better select the insurance policies we assumed from the Citizens depopulation program, leading to strong profitability and reduced risk. These analytics and underwriting processes also contribute to successful underwriting of our voluntary business. Our data analytics are embedded in the underwriting process and are used for strategic expansion into new product lines and states. We choose to minimize our exposure to or avoid certain types of coverage if we believe there is significant risk of loss, including coverage for sink-hole related losses in high-risk areas.

Unique Claims Servicing Model and Superior Customer Service

We believe that the vertical integration of our claims adjustment, water mitigation, and repair services provides us with a competitive advantage. Through our management of both claims adjusting and repair services, we are generally able to begin the adjustment and mitigation process much earlier than most competitors, thus reducing our loss adjustment expenses and ultimate loss payouts. A significant number of our repair technicians are participating in training and certification programs to become licensed claims adjusters (ten are licensed), allowing us to capture additional efficiencies. We also believe our unique model provides a superior level of customer service for our policyholders, enhancing our reputation and increasing the likelihood that our policyholders will renew their policies with us.

4

Relationships with Highly Rated Reinsurers

We manage our exposure to catastrophic events through, among other things, the purchase of reinsurance. Our relationships with highly rated reinsurers have been developed as a result of our management team’s industry experience and reputation for selective underwriting. Our financial strength, underwriting results and the long-term relationships between our management team and our reinsurance partners help improve the cost-effectiveness of our reinsurance program.

Relationships with Independent Agents and National Underwriters

We have developed relationships with a network of approximately 1,900 independent insurance agents. We believe we have been able to build this network due to our reputation for financial stability, commitment to our markets and integrity in the underwriting and claims process. We have entered into strategic relationships with national insurers and agencies that no longer write substantial personal residential insurance in some of the states in which we do business, which provides us access to their network of agents.

Our Competition

The market for residential property insurance is highly competitive in many of the states in which we do business. We compete to varying degrees with insurers including large national carriers, state-sponsored homeowners’ insurance entities, and single state or regional carriers. We believe Heritage differentiates itself from many competitors with our service levels, financial resources, streamlined processes, and vertical integration which provides loss mitigation and repair services.

Products and Distribution

We market and write personal lines voluntary policies through a network of approximately 1,900 independent agents. We intend to pursue additional voluntary business from agents in our existing independent agent network, expand our independent agent network and seek additional opportunities to use insurer-affiliated agents to offer our personal residential policies in the states in which we are licensed. We had 150,998 voluntary personal residential policies (47.3% of our total policies in force) as of December 31, 2016. Our growth strategy centers on the voluntary market as well as opportunistic acquisitions.

We currently write commercial residential business only in the state of Florida. We market and write commercial residential voluntary policies through a network of approximately 400 independent agents. We intend to pursue additional voluntary business from these agents in our existing independent agent network, expand our independent agent network and seek additional opportunities to increase our commercial residential policies in Florida. We started writing voluntary policies in October 2014. At December 31, 2016, we had 1,714 voluntary policies. The commercial voluntary market is a major component of our corporate growth strategy. At December 31, 2016 and 2015, commercial business represented 18.7% and 19.2%, respectively, of the premium in force.

In order to limit our potential exposure to individual risks and catastrophic events, we purchase significant reinsurance from third party reinsurers. Purchasing reinsurance is an important part of our risk strategy, and premiums paid (or ceded) to reinsurers is one of our largest costs. We have strong relationships with reinsurers which we believe are a result of our management’s industry experience and reputation for selective underwriting and effective claim management. For each of the twelve months beginning June 1, 2015 and 2016, we purchased catastrophe reinsurance from the following sources: (i) the Florida Hurricane Catastrophe Fund, a state-mandated catastrophe fund (“FHCF”), (ii) private reinsurers, all of which were rated “A-” or higher by A.M. Best Company, Inc. (“A.M. Best”) or Standard & Poor’s Financial Services LLC (“S&P”) or were fully collateralized, (iii) sponsorship of multiple catastrophe bonds that provide $728 million of principal limit that can be drawn upon over a three year period, and (iv) our wholly-owned reinsurance subsidiary, Osprey. In addition to purchasing catastrophe reinsurance, we also purchased property risk reinsurance which limits our net exposure in the event of a severe non-catastrophe loss impacting a single location or risk to $1 million. We also utilize facultative reinsurance to supplement our per risk reinsurance program where our capacity needs dictate. See “-Reinsurance – 2016 – 2017 Catastrophe Reinsurance Program”.

Our insurance regulators requires all insurance companies, like us, to have a certain amount of capital reserves and reinsurance coverage in order to cover losses upon the occurrence of a catastrophic event. Our reinsurance programs for each of the twelve months beginning June 1, 2015 and 2016 provides reinsurance in excess of regulatory requirements, which are based on the probable maximum loss that we would incur from an individual catastrophic event estimated to occur once every 100 years based on our portfolio of insured risks. We also purchase reinsurance coverage to protect against the potential for multiple catastrophic events occurring in the same year.

We test the sufficiency of our reinsurance program by subjecting our personal and commercial residential exposures to statistical testing using the AIR U.S. Hurricane Model, which replicates the most severe hurricanes to have occurred historically in states in which we conduct business, individual storms of severity in excess of such historical levels, and the historical calendar years

5

in which the most severe multiple catastrophic events have occurred. For example, the 2004 calendar year, in which four large catastrophic hurricanes made landfall in Florida, is considered to be the worst catastrophic year in Florida’s recorded history. Assuming the reoccurrence of the 2004 calendar year events, the probable after tax net loss to us in 2016, based on the coverage for our 2016-2017 reinsurance program, would be $40.3 million (after tax, net of all reinsurance recoveries and including our retention through Osprey). This loss would have represented 11.3% of our stockholders’ equity at December 31, 2016.

While a significant hurricane has not made landfall in Hawaii since 1992, Hurricane Iniki caused a combined estimated property damage of over $1.8 billion. Assuming the reoccurrence of Hurricane Iniki, the probable after tax net loss to us in 2016, based on the coverage for our 2016-2017 reinsurance program, would be $19.5 million (after tax, net of all reinsurance recoveries and including our retention through Osprey). This loss would have represented 5.4% of our stockholders’ equity at December 31, 2016.

We closely manage all aspects of our claims adjustment process. Claims are initially reviewed by our managers and staff adjusters, who determine the extent of the loss and the resources needed to adjust each claim. In the case of a catastrophic event, we have contracted with multiple large national claims adjusting firms to assist our adjusters with the increased volume of claims and ensure timely responses to our policyholders. In March 2014, we completed the acquisition of the assets and personnel of our main water mitigation services vendor and created our wholly-owned subsidiary, CAN. This acquisition has allowed us to better service our Florida based customers and expand our mitigation and restoration services. We utilize CAN to manage mitigation and restoration services for our customers. CAN primarily handles water damage-related claims, which comprised approximately 48.7% of our losses and loss adjustment expenses through December 31, 2016. We also leverage our 2015 acquisition, BRC, to manage and provide restoration services to CAN customers for all types of claims. BRC has provided services for non-insurance related projects but we expect to shift toward BRC handling only affiliated insurance claims. We believe our approach to claims handling results in a higher level of customer service and reduces our losses and loss adjustment expenses.

Our Market

Nearly 90% of our premium in force is generated from properties located in the State of Florida. According to the U.S. Census Bureau, at July 1, 2016, Florida was the third largest U.S. state with an estimated population of approximately 21 million people. The University of Florida Bureau of Economic and Business Research estimates that Florida is expected to reach a population of approximately 26 million people by 2040, an increase of 30% from 2015. Property ownership and development represent key drivers of the Florida economy.

The states in which we do business are exposed to an increased risk of hurricanes during the entire six months of the Atlantic and Pacific hurricane season, which spans from June 1 through November 30. Florida experienced two hurricanes in 2016. Eight hurricanes in 2004 and 2005, including Hurricanes Charley, Katrina, Rita and Wilma, caused a combined estimated property damage of over $110 billion, a significant portion of which occurred in Florida. While a significant hurricane has not made landfall in Hawaii since 1992, when Hurricane Iniki caused a combined estimated property damage of over $1.8 billion. As a result, personal residential insurance and claims servicing are vitally important to our policyholders.

According to data compiled by the Florida Office of Insurance Regulations (“FLOIR”), which excludes State Farm Florida Insurance Company, Citizens was the largest residential insurance carrier in Florida as of September 30, 2016, with a market share of approximately 9.1% based on total in force direct premiums written for personal and commercial residential insurance. As of the same date, we ranked third in Florida within this market, with a market share of approximately 5.8%. Through December 31, 2015, 100% of our business was generated in Florida and our growth was largely through our depopulation efforts. We assumed approximately 12,000 policies from Citizens in 2016 with the last assumption in May 2016. Assuming further access to capital and reinsurance support, we believe we have the opportunity to significantly expand the size of our voluntary personal and commercial residential insurance business. In 2016, we expanded Heritage P&C’s certificate of authority to write property and casualty insurance in the states of North Carolina, South Carolina, and in Georgia in 2017. Our acquisition of Zephyr adds approximately 70,000 policies to the Company. In recent years, the property and casualty insurance market has experienced a substantial increase in the availability of property catastrophe reinsurance resulting from the increased supply of capital from non-traditional insurance providers, including private capital and hedge funds. This increased capital supply, has reduced the cost of property catastrophe reinsurance, directly benefitting purchasers of this reinsurance, including us.

Underwriting

Our underwriters evaluate and accept only those risks that they believe will enable us to achieve an underwriting profit. In order to achieve underwriting profitability on a consistent basis, we focus on (1) the suitability of the risk to be assumed or written, (2) the adequacy of the premium with regard to the risk to be assumed or written and (3) the geographic distribution of existing policies for our business.

6

All of our personal lines underwriting is performed internally with our experienced staff in Florida and Hawaii. Our underwriters use our proprietary data analytics capabilities, which include a number of automated processes, to analyze a number of risk evaluation factors, including the age, construction, location and value of the residence and the premiums to be received from insuring the residence. New technological advances in computer generated geographical mapping afford us an enhanced perspective as to geographic concentrations of policyholders. When considering the geographic distribution of existing policies, our underwriters may consider the number of other properties we insure within the same region, county, city and zip code. We also consider the cost of reinsurance when assessing the adequacy of the premium with regard to the risk to be assumed or written. The underwriting criteria that we consider will continue to evolve as our business grows and expands.

We also review our expiring policies to determine whether those risks continue to meet our underwriting guidelines. If a given policy no longer meets our underwriting guidelines, we will take appropriate action regarding that policy, including raising premium rates or, to the extent permitted by applicable law and our assumption agreements with Citizens, not offering to renew the policy.

Policy Administration

We have engaged West Point Underwriters, Inc. and Majesco Mastec, providers of web-based software solutions and insurance personnel, to provide us with policy administration services for our business, including processing, billing and policy maintenance. The software is able to adapt to a variety of forms and rates, handle the administration of an increasing number of policies as our Company grows and expands, and provide detailed information about our book of business to our internal underwriters so that they can adjust our underwriting criteria as necessary. The software provides us with daily updates regarding the insurance policies that we have issued. The systems also allow us to provide renewal notices, late payment notices, cancellation notices, endorsements and policies to our policyholders in a timely fashion.

Claims Administration

We closely manage all aspects of the claims process, from processing the initial filing to providing remediation services for Florida claims through our wholly-owned subsidiary, CAN. When a policyholder contacts us to report a claim, members of our claims department create a claim file and aggregate the appropriate supporting documentation. Claims are then reviewed by our managers and staff adjusters, who assess the extent of the loss, including through on-site investigations, and determine the resources needed to adjust each claim. Our claims are generally adjusted by our staff claims professionals, except in the case of a catastrophic event for which we have contracted with several large national claims adjusting firms to assist our adjusters with the increased volume of claims and ensure timely responses to our policyholders. We currently leverage our CAN vendor network to provide repair and remediation services to Florida policyholders; this model could be expanded to other states

We perform or supervise the services rendered to our policyholders at all stages of the claims process, which we believe allows us to reduce cost and provide a high level of customer service to our policyholders. We have in-house resources as well as outsourced vendor relationships for water mitigation and rebuilding after a loss for our Florida policyholders. We have outsourced vendor relationships to provide these services to our policyholders outside of Florida. To encourage our Florida policyholders to allow us to manage their claims from beginning to end, we developed our Platinum Program. Under the Platinum Program, participating customers receive a 10% discount on their claim deductible, and we obtain control over inspection, claims adjusting and repair services, with the repair services being managed by either CAN or one of our contracted vendors. In March 2014, we acquired the largest vendor in the CAN network, which has allowed us to expand our in-house mitigation and restoration services. In August 2015, we acquired BRC to allow us to further expand our restoration services. These resources help to mitigate some of the impact of Assignment of Benefit challenges primarily found in South Florida.

Citizens Assumption Transactions

As of December 31, 2016, we have selectively assumed, net of cancellations, an aggregate of approximately 230,000 policies through participation in the Citizens depopulation program. Citizens generally offers depopulations on a monthly basis. From December 2012 through May 2016, we participated in 27 depopulations. Given the current population of policies written by Citizens, we do not anticipate participating in the depopulation program for the foreseeable future.

In order to be eligible to participate in an assumption transaction, we first apply to FLOIR for approval to assume a specified number of policies. On the effective date of assumption transactions, Citizens transfers to us the unearned premiums for the policies that have not opted out of the assumption transaction. A policyholder may also opt-out during the 30-day period following the effective date of the assumption transaction. If a policyholder opts-out during such period, we return the applicable unearned premiums to Citizens.

Under the terms of our typical assumption agreement with Citizens, we assume all liability and obligation for losses under the assumed policies arising on or after the effective date of the assumption transaction, and we directly service all policyholder claims

7

related to such losses. All terms and conditions of the assumed policies, including coverage and rates, remain unchanged for the remainder of the policy term. Citizens remains liable for all losses under the assumed policies arising prior to the effective date of the assumption transaction and is solely responsible for servicing all policyholder claims related to such losses.

We strive to retain these policies by offering competitive rates and efficient claims handling to our policyholders. In 2016, we renewed approximately 84% and 78% of the personal lines and commercial lines policies we assumed from Citizens, respectively.

Liability For Losses and Loss Adjustment Expenses

Our liability for losses and loss adjustment expenses represents our preliminary estimated lability of (i) claims that have been incurred, but not yet paid (case reserves), (ii) claims that have been incurred but not yet reported to us (“IBNR”), and (iii) loss adjustment expenses (“LAE”) which are intended to cover the ultimate cost of settling claims, including investigation and defense of lawsuits resulting from such claims.

Considerable time can pass between the occurrence of an insured loss, the reporting of the loss and the payment of that loss. Our liability for losses and LAE, which we believe represents the best estimate at a given point in time based on facts, circumstances and historical trends then known, may necessarily be adjusted to reflect additional facts that become available during the loss settlement period. We continually review and adjust our estimated losses as necessary based on industry development trends, evolving claims experience and new information obtained.

For a discussion and summary of the activity in the liability for losses and LAE for the years ended December 31, 2016, 2015 and 2014, see Note 10 — “Reserve for Unpaid Losses” to our consolidated financial statements under Item 8 of this Annual Report on Form 10-K.

Loss Development

Our liability for losses and loss adjustment expenses (“LAE”) represents estimated costs ultimately required to settle all claims for a given period. The following table illustrates development of the estimated liability for losses and LAE as of December 31 for the years 2012 (inception) through 2016 (in thousands):

|

|

|

For the Years Ended December 31, |

|

|||||||||||||||||

|

|

|

2012 |

|

|

2013 |

|

|

2014 |

|

|

2015 |

|

|

2016 |

|

|||||

|

Original liability for losses and LAE1 |

|

$ |

1,243 |

|

|

$ |

19,344 |

|

|

$ |

51,469 |

|

|

$ |

83,722 |

|

|

$ |

140,137 |

|

|

Re-estimated losses and LAE2 as of: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 year later |

|

$ |

798 |

|

|

$ |

19,121 |

|

|

$ |

46,184 |

|

|

$ |

102,512 |

|

|

$ |

— |

|

|

2 years later |

|

$ |

757 |

|

|

$ |

16,846 |

|

|

$ |

46,324 |

|

|

$ |

— |

|

|

$ |

— |

|

|

3 years later |

|

$ |

784 |

|

|

$ |

16,740 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

4 years later |

|

$ |

797 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

Cumulative redundancy (deficiency) 3 |

|

$ |

446 |

|

|

$ |

2,604 |

|

|

$ |

5,145 |

|

|

$ |

(18,790 |

) |

|

$ |

— |

|

|

Cumulative amount of liability paid as of: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 year later |

|

$ |

548 |

|

|

$ |

12,052 |

|

|

$ |

27,265 |

|

|

$ |

65,065 |

|

|

$ |

— |

|

|

2 years later |

|

$ |

627 |

|

|

$ |

13,472 |

|

|

$ |

37,236 |

|

|

$ |

— |

|

|

$ |

— |

|

|

3 years later |

|

$ |

689 |

|

|

$ |

14,946 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

4 years later |

|

$ |

766 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

Gross premiums earned |

|

$ |

6,055 |

|

|

$ |

139,959 |

|

|

$ |

311,514 |

|

|

$ |

524,740 |

|

|

$ |

640,518 |

|

|

(1) |

Represents management’s original best estimated liability of (i) unpaid claims, (ii) incurred but not reported (“IBNR”) and (iii) loss adjustment expenses (“LAE”). |

|

(2) |

Represents the re-estimated liabilities in later years of unpaid claims, IBNR and loss adjustment expenses in the respective years. |

|

(3) |

Represents the difference between the latest re-estimate and the original estimate. A redundancy means the original estimate is higher than the current estimate whereas a deficiency means that the original estimate is lower than the current estimate. |

8

Our business depends upon the use, development and implementation of integrated technology systems. These systems enable us to provide a high level of service to agents and policyholders by processing business efficiently, communicating and sharing data with agents, providing a variety of methods for the payment of premiums and allowing for the accumulation and analysis of information for our management. We believe the availability and use of these technology systems has resulted in improved service to agents and customers, increased efficiencies in processing our multi-state insurance business and lower operating costs.

We also license software from third parties, including West Point Underwriters, Majesco Mastec and AIR Worldwide, Inc. (“AIR”). AIR’s catastrophe modeling software enables us to optimize our insurance portfolio to manage our reinsurance costs. We also own or license other technology systems used by our insurance company affiliates. These technology systems consist primarily of an integrated central processing computer, a series of server-based computer networks, a back-up server and various Internet-based communications systems.

Reinsurance

In order to limit our potential exposure to catastrophic events, we purchase significant reinsurance from third party reinsurers and sponsor catastrophe bonds (Citrus Re). We also purchase property per risk reinsurance and facultative coverage for non-catastrophe related to losses in excess of $1 million. Purchasing reinsurance is an important part of our risk strategy, and premiums paid (or ceded) to reinsurers is one of our largest cost components. Reinsurance involves transferring, or “ceding”, a portion of the risk exposure on policies we write to another insurer, known as a reinsurer. To the extent that our reinsurers are unable to meet the obligations they assume under our reinsurance agreements, we remain liable for the entire insured loss. See in Part I, Item 1A “Risk Factors”. We may not be able to collect reinsurance amounts due to us from the reinsurers with which we have contracted.

Our reinsurance agreements are short-term, prospective contracts. We record an asset, prepaid reinsurance premiums, and a liability, reinsurance payable, for the entire contract amount upon commencement of our new reinsurance agreements. We amortize our reinsurance premiums over the 12-month contract period, which is June 1 through May 31.

In the event that we incur losses and loss adjustment expenses recoverable under our reinsurance program, we record amounts recoverable from our reinsurers on paid losses plus an estimate of amounts recoverable on unpaid losses. The estimate of amounts recoverable on unpaid losses is a function of our liability for unpaid losses associated with the reinsured policies; therefore, the amount changes in conjunction with any changes to our estimate of unpaid losses. As a result, a reasonable possibility exists that an estimated recovery may change significantly in the near term from the amounts included in our consolidated financial statements.

Our insurance regulators requires all insurance companies, like us, to have a certain amount of capital and reinsurance coverage in order to cover losses and loss adjustment expenses upon the occurrence of a catastrophic event. Our 2016-2017 reinsurance program provides reinsurance in excess of our state regulator requirements, which are based on the probable maximum loss that we would incur from an individual catastrophic event estimated to occur once in every 100 years based on our portfolio of insured risks. The nature, severity and location of the event giving rise to such a probable maximum loss differs for each insurer depending on the insurer’s portfolio of insured risks, including, among other things, the geographic concentration of insured value within such portfolio. As a result, a particular catastrophic event could be a one-in-100 year loss event for one insurance company while having a greater or lesser probability of occurrence for another insurance company. We also purchase reinsurance coverage to protect against the potential for multiple catastrophic events occurring in the same year.

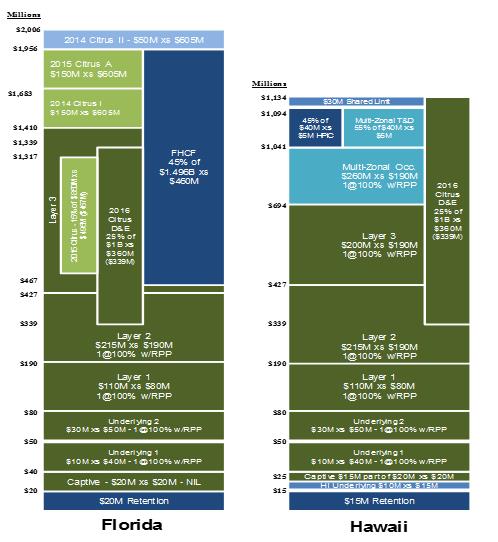

2016 - 2017 Reinsurance Program

The Company placed its reinsurance program for the period from June 1, 2016 through May 31, 2017 during the second quarter of 2016. This reinsurance program incorporates the catastrophe risk of our two insurance subsidiaries, Heritage P&C, a Florida based insurer and Zephyr, a Hawaii based insurer, into one reinsurance structure. The programs are incorporated into one reinsurance structure and are allocated amongst traditional reinsurers, catastrophe bonds issued by Citrus Re Ltd., a Bermuda special purpose insurer formed in 2014 (“Citrus Re”), and the Florida Hurricane Catastrophe Fund (“FHCF”). Coverage is shared by both insurers unless otherwise noted. The 2016-2017 reinsurance program provides, including retention, first event coverage up to $1.9 billion in Florida, first event coverage up to $1.1 billion in Hawaii, and multiple event coverage up to $3 billion.

The reinsurance program, which is segmented into layers of coverage, protects the Company for excess property catastrophe losses and loss adjustment expenses. The Company’s 2016-2017 reinsurance program incorporates the mandatory coverage required by law to be placed with FHCF, which is available only for Florida catastrophe risk. For the 2016 hurricane season, the Company reduced its selected participation percentage in the FHCF from 75% to 45%. The Company also purchased private reinsurance below, alongside and above the FHCF layer, as well as aggregate reinsurance coverage. The following describes the various layers of the Company’s June 1, 2016 to May 31, 2017 reinsurance program.

9

|

|

event strikes Hawaii, the Company has a primary retention of the first $30 million of losses and loss adjustment expenses, of which Osprey is responsible for $15 million. If a second catastrophic event strikes Florida, Heritage P&C’s primary retention decreases to $15 million and the remainder of the losses are ceded to third parties. If a second event strikes Hawaii, Zephyr’s primary retention decreases to $5 million. In the second event only for a loss exceeding $190 million, there is an additional Company co-participation of 5.4% subject to a maximum co-participation of $11.6 million. Heritage P&C and Zephyr each have a $5 million primary retention for events beyond the second catastrophic event. Osprey has no primary retention beyond the first catastrophic event in Florida or Hawaii. Additionally, Osprey is responsible for payment of up to $5.3 million of reinstatement premium, depending on the amount of losses incurred. |

|

|

• |

Shared Layers above retention and below FHCF. Immediately above the retention, the Company has purchased $374 million of reinsurance from third party reinsurers. Through the payment of a reinstatement premium, the Company is able to reinstate the full amount of this reinsurance one time. To the extent that $374 million or a portion thereof is exhausted in a first catastrophic event, the Company has purchased reinstatement premium protection insurance to pay the required premium necessary for the reinstatement of this coverage. |

|

|

• |

FHCF Layer. The Company’s FHCF program provides coverage for Florida events only and includes an estimated maximum provisional limit of 45% of $1.5 billion, in excess of its retention of $460 million. The limit and retention of the FHCF coverage is subject to upward or downward adjustment based on, among other things, submitted exposures to FHCF by all participants. The Company has purchased coverage alongside from third party reinsurers and through reinsurance agreements with Citrus Re. To the extent the FHCF coverage is adjusted, this private reinsurance with third party reinsurers and Citrus Re will adjust to fill in any gaps in coverage up to the reinsurers’ aggregate limits for this layer. The FHCF coverage cannot be reinstated once exhausted, but it does provide coverage for multiple events. |

|

|

• |

Layers alongside the FHCF. The Florida reinsurance program includes third party layers alongside the FHCF. These include 2015 C and 2015 B series catastrophe bonds, which cover Florida only for the 2016 season, and 2016 D and 2016 E catastrophe bond series issued by Citrus Re, which total $377.5 million of coverage, as discussed below, as well as a traditional reinsurance layer providing $200 million of coverage. Through a reinstatement, the Company is able to reinstate the full amount of the $200 million of reinsurance one time. These 2016 catastrophe bonds and the traditional reinsurance layer provide coverage for both Florida and Hawaii catastrophe losses. |

|

|

• |

2016 Class D and E Notes: During February 2016, Heritage P&C and Zephyr entered into two catastrophe reinsurance agreements with Citrus Re. The agreements provide for three years of coverage from catastrophic losses caused by named storms, including hurricanes, beginning on June 1, 2016. Heritage P&C and Zephyr pay a periodic premium to Citrus Re during this three-year risk period. Citrus Re issued an aggregate of $250 million of principal-at-risk variable notes due February 2019 to fund the reinsurance trust account and its obligations to Heritage P&C and Zephyr under the reinsurance agreements. The Class D notes provide $150 million of coverage and the Class E notes provide $100 million of coverage. The Class D and Class E notes provide reinsurance coverage for a sliver of the catastrophe coverage that had previously been provided by the FHCF. The limit of coverage is fully collateralized by a reinsurance trust account for the benefit of Heritage P&C and Zephyr. The maturity date of the notes may be extended up to two additional years to satisfy claims for catastrophic events occurring during the three-year term of the reinsurance agreements. |

10

Layers above the FHCF - Florida program

|

|

• |

2015 Class A Notes: During April 2015, Heritage P&C entered into catastrophe reinsurance agreements with Citrus Re. The 2015 notes do not provide coverage for Zephyr for the 2016 hurricane season. The agreements provide for three years of coverage from catastrophic losses caused by named storms, including hurricanes, beginning on June 1, 2015. Heritage P&C pays a periodic premium to Citrus Re during this three-year risk period. Citrus Re issued principal-at-risk variable notes due April 2018 to fund the reinsurance trust account and its obligations to Heritage P&C under the reinsurance agreements. The Class A notes provide $150 million of coverage for a layer above the FHCF. The limit of coverage is fully collateralized by a reinsurance trust account for the benefit of Heritage P&C. The maturity date of the notes may be extended up to two additional years to satisfy claims for catastrophic events occurring during the three-year term of the reinsurance agreements. |

|

|

• |

2014 Class A Notes: Coverage immediately below and above the 2015 Class A notes is provided by the 2014 reinsurance agreements entered into with Citrus Re. The first contract with Citrus Re provides $150 million of coverage immediately below 2015 Class A, and the second contract provides an additional $50 million of coverage which sits immediately above 2015 Class A. During April 2014, Heritage P&C entered into two catastrophe reinsurance agreements with Citrus Re. The 2014 notes do not provide coverage for Zephyr for the 2016 hurricane season. The agreements provide for three years of coverage from catastrophe losses caused by certain named storms, including hurricanes, beginning on June 1, 2014. The limit of coverage of $200 million is fully collateralized by a reinsurance trust account for the benefit of Heritage P&C. Heritage P&C pays a periodic premium to Citrus Re during this three-year risk period. Citrus Re issued $200 million of principal-at-risk variable notes due April 2017 to fund the reinsurance trust account and its obligations to Heritage P&C under the reinsurance agreements. The maturity date of the notes may be extended up to two additional years to satisfy claims for catastrophic events occurring during the three-year term of the reinsurance agreements. |

|

|

• |

Multi-Zonal Layers – The Company purchased additional layers which provide coverage for Florida for a second event and both first and second event coverage for Hawaii. The first event coverage for Hawaii is a counterpart to the Florida-only catastrophe bond layers and FHCF layer. There is a total of $282 million of reinsurance coverage purchased on this basis, with $260 million having a prepaid reinstatement. The multi-zonal occurrence layer provides first and second event coverage of $260 million for Hawaii and second event coverage of $260 million for Florida. A top and drop multi-zonal layer provides first and subsequent event coverage of $22 million for Hawaii and second or subsequent event coverage of $22 million for Florida. |

|

|

• |

Aggregate Coverage. In addition to what is described above, much of the reinsurance is structured in a way to provide aggregate coverage. $682 million of limit is structured on this basis. To the extent that this coverage is not fully exhausted in the first catastrophic event, it provides coverage commencing at its reduced retention for second and subsequent events where underlying coverage has been previously exhausted. $460 million has a reinstatement, which is prepaid. |

For a first catastrophic event striking Florida, our reinsurance program provides coverage for $2 billion of losses and loss adjustment expenses, including our retention, and we are responsible for all losses and loss adjustment expenses in excess of such amount. For a first catastrophic event striking Hawaii, our reinsurance program provides coverage for $1.1 billion of losses and loss adjustment expenses, including our retention, and we are responsible for all losses and loss adjustment expenses in excess of such amount. For subsequent catastrophic events, our total available coverage depends on the magnitude of the first event, as we may have coverage remaining from layers that were not previously fully exhausted. $860 million of limit purchased in 2016 includes a reinstatement, with $825 million being prepaid. In total, we have purchased $3.1 billion of potential reinsurance coverage, including our retention, for multiple catastrophic events. Our ability to access this coverage, however, will be subject to the severity and frequency of such events. Hurricane losses in North Carolina and South Carolina would be covered under the Florida program with

11

the exception of the FHCF and the series 2014 and 2015 CAT bonds. Management deemed this reinsurance protection to be sufficient given the level of catastrophe exposure in 2016 for North Carolina and South Carolina.

In placing our 2016-2017 reinsurance program, we sought to capitalize on favorable reinsurance pricing and mitigate uncertainty surrounding the future cost of our reinsurance by negotiating multi-year arrangements. The $727.5 million of aggregate coverage we have purchased from Citrus Re Ltd, which includes the 2014 Class A & B notes, the 2015 Class A, B, and C notes, and the 2016 Class D & E notes extends $200 million until May of 2017, $277.5 million for another two-year period and $250 million for a three-year period. To the extent coverage is all or partially exhausted before the end of three years, it cannot be reinstated. In the aggregate, multi-year coverage from Citrus Re Ltd accounts for approximately 42% of our purchases of private reinsurance for the 2016 hurricane season. The terms of each of the multi-year coverage arrangements described above are subject to adjustment depending on, among other things, the size and composition of our portfolio of insured risks in future periods.

Assuming the reoccurrence of Hurricane Andrew, which is considered to be the most catastrophic single event in Florida’s recorded history, the probable maximum net loss to us in 2016, assuming the reinsurance coverage described above, would be $24.8 million (after tax, net of all reinsurance recoveries and including our retention through Osprey). This loss would have represented 6.9% of our stockholders’ equity at December 31, 2016. We estimate that, based on our portfolio of insured risks as of August 31, 2016, Hurricane Andrew would have represented a catastrophic event likely to occur approximately once every 49 years and would have exhausted approximately 56.6% of our first event expected reinsurance coverage.

For the twelve months ending May 31, 2017, we purchased reinsurance from the following sources: (i) FHCF, (ii) Citrus Re Ltd, (iii) 23 third-party private reinsurers, all of which were rated “A-” or higher by A.M. Best or S&P and (iv) our wholly-owned reinsurance subsidiary, Osprey. Allianz Global Corporate & Specialty SE provides approximately 38% of our third-party reinsurance program, including Citrus Re catastrophe bonds. The chart below lists our third-party reinsurers with A.M. Best and S&P ratings:

12

|

AM Best |

S&P |

|

|

Aeolus Re Ltd |

Fully Collateralized |

|

|

American Standard Insurance Company of Wisconsin |

A |

NR |

|

Amlin AG (Bermuda Branch) |

A |

A |

|

Aquilo/CatCo |

Fronted by AM Best "A+" Paper |

|

|

Aspen Re |

A |

A |

|

Axis Specialty Limited |

A+ |

A+ |

|

Chubb Tempest1 |

A++ |

AA |

|

Cincinnati Re |

A+ |

A+ |

|

Citrus Re |

Fully Collateralized |

|

|

Coriolis Capital (obo Horseshoe Re) |

Fully Collateralized |

|

|

DaVinci Re |

A |

AA- |

|

Everest Reinsurance Company |

A+ |

A+ |

|

Fermat Capital Management, LLC |

Fully Collateralized |

|

|

Fidelis Insurance Bermuda Limited |

A- |

NR |

|

General Insurance Corporation of India |

A- |

NR |

|

Hannover Re (Bermuda) Ltd |

A+ |

AA- |

|

Hiscox Insurance Co (Bermuda) Limited |

A |

A |

|

Insurance Company of the West |

A- |

NR |

|

ILS Capital |

Fully Collateralized |

|

|

Lancashire Insurance Company Limited |

A |

A- |

|

Lloyd's |

A |

A |

|

Markel Bermuda Limited |

A |

A |

|

Nephila Capital Ltd |

Fully Collateralized |

|

|

New India |

A- |

NR |

|

Odyssey Reinsurance Company |

A |

A- |

|

Osprey Re |

Fully Collateralized |

|

|

Partner Reinsurance Co Ltd |

A |

A+ |

|

Pillar Capital |

Fully Collateralized |

|

|

Qatar Reinsurance Company Limited |

A |

A |

|

Renaissance Reinsurance Limited |

A+ |

AA- |

|

Satec |

Fronted by AM Best "A+" Paper |

|

|

Securis |

Fully Collateralized |

|

|

Swiss Reinsurance America Corporation |

A+ |

AA- |

|

Taiping Reinsurance Co, Ltd. |

A |

A |

|

Tokio Millennium Re AG |

A++ |

A+ |

|

Transatlantic Reinsurance Company |

A |

A+ |

|

XL Catlin |

A |

A+ |

Investments

Our investments are managed by seven third-party asset managers. We have designed our investment policy to provide a balance between current yield, conservation of capital and the liquidity requirements of our operations. As such, our investable assets are primarily held in cash and bonds with relatively short durations. Our investment policy sets guidelines that provide for a well-diversified investment portfolio that is compliant with Florida and Hawaii statutes that emphasizes quality and preservation of capital. The policy limits investments in common and preferred stocks to 15% of each of our insurance company affiliates’ admitted assets, with no more than 10% in either class. Our bond portfolio must have a minimum weighted average portfolio quality of A, with only $1 million invested in below investment grade bonds. No more than 2% of admitted assets can be invested in any one issuer, excluding government-related securities. Investments in commercial mortgages cannot exceed 10% of admitted assets. Prohibited investments include short sales and margin purchases, oil, gas, mineral or other types of leases, speculative uses of futures and options, unrated corporate securities, non-US denominated securities, convertible securities high risk CMO instruments, repurchase agreements, securities lending transactions and speculative foreign currency valuation transactions. Our investment policy, which may change from time to time, is approved by our Investment Committee and is reviewed on a regular basis in order to ensure that our investment policy evolves in response to changes in the financial market. See Note 3 to our consolidated financial statements for the year ended December 31, 2016 included elsewhere in this Annual Report.

As of December 31, 2016, we held $105.8 million in cash and cash equivalents and $603 million in securities, which were comprised of $571 million in bonds, $14.5 million in preferred stocks and $17.5 million in common stock.

Government Regulation

The insurance industry is extensively regulated. Our insurance company subsidiaries are subject to the laws and regulations of the states in which they do business. The insurance regulatory statutes and rules provide for regulation of virtually all aspects of the business of insurance companies. The states in which we conduct business, like many states, have adopted several model laws and

13

regulations as promulgated by the NAIC. State statutes and administrative rules generally require each insurance company that is part of a holding company group to register with the department of insurance in its state of domicile and to furnish information concerning the operations of the companies within the holding company system which may materially affect the operations, management or financial condition of the insurers within the group. As part of its registration, each insurance company must identify material agreements, relationships and transactions with affiliates, including without limitation loans, investments, asset transfers, transactions outside of the ordinary course of business, certain management, service, and cost sharing agreements, reinsurance transactions, dividends and consolidated tax allocation agreements. In some instances, individual state insurance laws and regulations are even more stringent that those promulgated by the NAIC or other states.

We are subject to regulations administered by a department of insurance in each state in which we do business. These regulations relate to, among other things:

|

|

• |

the content and timing of required notices and other policyholder information; |

|

|

• |

the amount of premiums the insurer may assume or write in relation to its surplus (writing ratios); |

|

|

• |

the amount and nature of reinsurance a company is required to purchase; |

|

|

• |

participation in guaranty funds and other statutorily created markets or organizations; |

|

|

• |

business operations and claims practices; |

|

|

• |

approval of policy forms and premium rates; |

|

|

• |

standards of solvency, including risk-based capital measurements; |

|

|

• |

licensing of insurers and their products; |

|

|

• |

restrictions on the nature, quality and concentration of investments; |

|

|

• |

restrictions on the ability of insurance company subsidiaries to pay dividends to insurance holding companies; |

|

|

• |

restrictions on transactions between insurance companies and their affiliates; |

|

|

• |

restrictions on the size of risks insurable under a single policy; |

|

|

• |

requiring deposits for the benefit of policyholders; |

|

|

• |

requiring certain methods of accounting; |

|

|

• |

periodic examinations of our operations and finances; |

|

|

• |

the form and content of records of financial condition required to be filed; and |

|

|

• |

requiring reserves. |