Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Meet Group, Inc. | ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Meet Group, Inc. | ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Meet Group, Inc. | ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - Meet Group, Inc. | ex31-1.htm |

| EX-23.1 - EXHIBIT 23.1 - Meet Group, Inc. | ex23-1.htm |

| EX-21.1 - EXHIBIT 21.1 - Meet Group, Inc. | ex21-1.htm |

| EX-10.3 - EXHIBIT 10.3 - Meet Group, Inc. | ex10-3.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

☑ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 31, 2016

Or

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from: to

MeetMe, Inc.

(Exact name of registrant as specified in its charter)

|

Delaware |

001-33105 |

86-0879433 |

|

(State or Other Jurisdiction |

(Commission |

(I.R.S. Employer |

100 Union Square Drive

New Hope, Pennsylvania 18938

(Address of Principal Executive Office) (Zip Code)

(215) 862-1162

(Registrant’s telephone number, including area code)

|

Securities registered pursuant to Section 12(b) of the Act: | ||

|

. |

||

|

Title of each class |

Name of each exchange on which registered | |

|

Common Stock, $0.001 par value |

The NASDAQ Stock Market LLC | |

|

NASDAQ Capital Market | ||

|

Securities registered pursuant to Section 12(g) of the Act: None | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☑ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. ☐ Yes ☑ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☑ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ☑ Yes ☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

☐ |

Accelerated filer |

☑ |

|

Non-accelerated filer |

☐ |

Smaller reporting company |

☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☑ No

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the closing price as of the last business day of the registrant’s most recently completed second fiscal quarter, June 30, 2016, was approximately $259,000,000 based upon the last reported sale price of $5.33 per share on June 30, 2016 on the NASDAQ Capital Market.

The number of shares outstanding of the registrant’s common stock, par value $0.001, as of March 3, 2017, was 59,620,606.

MEETME, INC.

TABLE OF CONTENTS

|

|

|

PART I |

|

Page |

|

|

|

|

|

|

|

Item 1. |

|

Business |

|

1 |

|

|

|

|

|

|

|

Item 1A. |

|

Risk Factors |

|

8 |

|

|

|

|

|

|

|

Item 1B. |

|

Unresolved Staff Comments |

|

25 |

|

|

|

|

|

|

|

Item 2. |

|

Properties |

|

25 |

|

|

|

|

|

|

|

Item 3. |

|

Legal Proceedings |

|

25 |

|

|

|

|

|

|

|

Item 4. |

|

Mine Safety Disclosures |

|

26 |

|

|

|

|

|

|

|

|

|

PART II |

|

|

|

|

|

|

|

|

|

Item 5. |

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

|

27 |

|

|

|

|

|

|

|

Item 6. |

|

Selected Financial Data |

|

30 |

|

|

|

|

|

|

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

31 |

|

|

|

|

|

|

|

Item 7A. |

|

Quantitative and Qualitative Disclosures About Market Risk |

|

45 |

|

|

|

|

|

|

|

Item 8. |

|

Financial Statements and Supplementary Data |

|

45 |

|

|

|

|

|

|

|

Item 9. |

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

|

45 |

|

|

|

|

|

|

|

Item 9A. |

|

Controls and Procedures |

|

45 |

|

|

|

|

|

|

|

Item 9B. |

|

Other Information |

|

46 |

|

|

|

|

|

|

|

|

|

PART III |

|

|

|

|

|

|

|

|

|

Item 10. |

|

Directors, Executive Officers and Corporate Governance |

|

47 |

|

|

|

|

|

|

|

Item 11. |

|

Executive Compensation |

|

50 |

|

|

|

|

|

|

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

74 |

|

|

|

|

|

|

|

Item 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

|

75 |

|

|

|

|

|

|

|

Item 14. |

|

Principal Accountant Fees and Services |

|

77 |

|

|

|

|

|

|

|

|

|

PART IV |

|

|

|

|

|

|

|

|

|

Item 15. |

|

Exhibits, Financial Statement Schedules |

|

78 |

| Item 16. | Form 10-K Summary | 80 | ||

|

Signatures |

|

81 | ||

PART I

ITEM 1. BUSINESS.

COMPANY OVERVIEW

MeetMe, Inc. (the “Company,” “MeetMe,” “us” or “we”) is a fast-growing portfolio of mobile apps that brings together people around the world for new connections. Our mission is to meet the universal need for human connection. We operate location-based social networks for meeting new people on mobile platforms, including on iPhone, Android, iPad and other tablets, and on the web that facilitate interactions among users and encourage users to connect and chat with each other. Given consumer preferences to use more than a single mobile application, we are adopting a brand portfolio strategy, through which we offer products that collectively appeal to the broadest spectrum of consumers. We are consolidating the fragmented mobile meeting sector through strategic acquisitions, leveraging economies and innovation to drive growth. Through this strategy of consolidation, we intend to apply a centralized discipline to learnings, best practices and technologies across our brands in order to increase growth, reduce costs and maximize profitability. On October 3, 2016, the Company completed its acquisition of Skout, Inc. (“Skout”), a leading global mobile network for meeting new people.

MeetMe’s platforms monetize through advertising, in-app purchases, and paid subscriptions. The Company offers online marketing capabilities, which enable marketers to display their advertisements in different formats and in different locations. We offer significant scale to our advertising partners, with hundreds of millions of daily impressions across our active and growing global user base, and sophisticated data science for highly effective hyper-targeting. The Company works with its advertisers to maximize the effectiveness of their campaigns by optimizing advertisement formats and placements.

Just as Facebook has established itself as the social network of friends and family, and LinkedIn as the social network of colleagues and business professionals, MeetMe is creating the social network not of the people you know but of the people you want to know. Nimble and fast-moving, already in more than 100 countries, we are challenging the dominant player in our space, Match Group. Our vision extends beyond dating. We focus on building quality products to satisfy the universal need for human connection among all people, everywhere--not just paying subscribers. We believe meeting new people is a basic human need, especially for users aged 18-34, when so many long-lasting relationships are made. We use advanced technology to engineer serendipitous connections among people who otherwise might never have met — a sort of digital coffeehouse where everyone belongs. Over the years, MeetMe’s apps have originated untold numbers of chats, shares, good friends, dates, romantic relationships – even marriages.

We believe that we have significant growth opportunities as people increasingly use their mobile devices to discover the people around them. Given the importance of establishing connections within a user’s geographic proximity, we believe it is critical to establish a high density of users within the geographic regions we serve. As the MeetMe networks grow and the number of users in a location increases, we believe that users who are seeking to meet new people will incrementally benefit from the quantity of relevant connections.

BUSINESS OVERVIEW

How We Create Value for Users

The Company provides something everyone craves: the magic of human connection. Our innovative apps have advantages the neighborhood pub can’t match. MeetMe is continuously developing new products that improve on serendipity by providing a variety of ways to connect and all are backed by data science that engineers good matches. Our goal is to be the conduit for connecting people to each other for the over 50 million people aged 18-34 in the U.S. and the more than one billion worldwide. We are unashamedly free, monetizing with our industry-leading mobile monetization infrastructure. As a free, ad-supported service, we are fundamentally different from companies with paid memberships like Match Group, Zoosk and Spark Networks.

The difference between a subscription-dating site and the MeetMe applications (“apps” or “applications”), is the difference between a singles bar and the neighborhood bar. People feel comfortable using the MeetMe apps to make friends, socialize and chat. In fact, in our internal survey of users conducted in January 2017, 85% of those responding said they preferred to start relationships as friends. We believe this comfort level drives higher engagement and retention.

We believe a dramatic shift is underway in the multi-billion dollar dating industry, and that the industry is anchoring towards free with lowered pricing and dramatic investments in free services by existing players. We believe the subscription model ignores that only a small minority of meeting app users are willing to pay a fee; our model thrives on that fact. We believe the subscription-dating model is ultimately compromised because it leads to significant churn by its nature. We believe churn ultimately reduces daily active users and restricts user density. We believe the density of users within a geographic area is critical to developing a strong meet-new-people service. Ultimately, the network effect in a meet-new-people service comes down to having nearby, highly relevant users to recommend. With no paywalls as a barrier to entry, we believe there are virtually no limits to how many new people we sign up. Every new user provides MeetMe with additional opportunity to engineer great matches — and more engagements to monetize.

The Company has a singular focus on attracting and monetizing the vast majority of its users through superior products. We are not burdened by legacy subscription products, and we believe we are as well positioned as any company to build the global brand for meeting new people. We believe our success will depend in large part, as it does every year, on our ability to continue to execute against an aggressive product pipeline.

More than two million people use our apps, on average, every day to meet new people in their local communities and throughout the world. These daily active users are increasingly choosing to access our apps on their mobile devices, in many cases logging in multiple times per day in order to interact with people they have met on our apps. They are meeting friends, significant others, and potential spouses every day.

Our top priority is to support and grow our dedicated user base by developing innovative ways of bringing people together online. We have historically been able to attract and retain users because we make meeting new people fun and easy. The products we have built for users can be divided into three categories: social networking products, social discovery products, and in-app products available for purchase.

Social Networking Products

Our traditional social networking products support our social discovery mission by enabling users to learn about, communicate with, and organize the people they meet on MeetMe and Skout.

|

● |

Chat: Chat is the most important action happening across our applications. MeetMe and Skout provide a robust chat product for private one-on-one communication between users. MeetMe and Skout users, combined, sent more than 1.5 billion chats per month in the fourth quarter of 2016. Not only is chat the chief thing that our users want to do, it is also by far the most powerful push notification for bringing users back into the apps. As a result, we build the rest of the app around chat. |

|

● |

Profile: A user’s profile represents his or her identity within MeetMe or Skout. Basic demographic information is highlighted, along with a user-generated “About Me” blurb, while activities within social discovery applications, such as Discuss and Buzz, are also featured prominently. Profiles are one of the most popular areas for members to interact with one another. |

|

● |

Friends: Within the Friends section of MeetMe, members interact with the friends they have made on the platform, accept incoming friend requests and browse suggested friends. Skout offers a similar feature called “Favorites.” |

Social Discovery Products

Our social discovery products facilitate interactions among members. They are the key vehicles through which we make it fun and easy to meet new people.

|

● |

Meet: Meet, backed by a data team to try to show users more likely to result in lengthy chat, showcases nearby, relevant members that a member may want to chat with. Meet is the easiest place to go within the apps for MeetMe and Skout members to discover people nearby. |

|

● |

Discuss and Buzz: Discuss and Buzz are location-based stream communication features on MeetMe and Skout, respectively. Unlike the Facebook News Feed, which surfaces content from users’ existing social graphs, Discuss and Buzz surface content from people nearby, thus creating a broader conversation to help users discover new people to meet. Additionally, the Discuss feature on MeetMe offers dozens of topics that users can use to find people who share their interests and make it as easy as possible to start talking with them. |

|

● |

Interested: A Skout-exclusive feature, Interested gives our members a way to meet new people in a Tinder-style queue interface. Users can quickly view potential new friends and matches, choosing on each whether to “favorite” or “skip”. When two users “favorite” one another in Interested, a match is made and the two users can progress to chat. |

In-App Products Available For Purchase

Both MeetMe and Skout feature in-app products called Credits and Points, respectively, which users can buy directly or earn by completing third-party offers, along with several virtual products or “powerups” that users must spend Credits or Points to access or use. Additionally, each app offers a subscription product, MeetMe+ or Skout Premium, that includes an ad-free experience and other benefits.

|

● |

Boost and Feature Me: Like Google’s AdSense, but for people, MeetMe’s Boost and Skout’s Feature Me enable users to purchase placement in some of the most highly trafficked areas of the app, to garner more attention from the community and increase the ability to meet more people faster. |

|

● |

Discuss Spotlight: Discuss Spotlight enables MeetMe users to spend Credits in order to “pin” their post to the top of Discuss for a limited period of time in order to drive more views, likes, and comments for their content. Spotlighted posts are targeted to a given geographic region and age group. |

|

● |

Who Favorited Me: Skout users can spend their Points to unlock the Who Favorited Me? feature. This reveals which other Skout users have favorited them, either in Interested or on their profile, without the typical requirement of a two-sided match — thus allowing paying users to use the product more efficiently to meet new people faster. |

|

● |

Travel: Skout users can spend their Points to virtually travel to other cities and meet new people there, rather than in their current locations. Each city can be unlocked for 24 hours at a time. |

|

● |

MeetMe+: MeetMe+ is a subscription product, available only on our mobile apps, that gives members extra privileges on MeetMe, including additional filtering in Meet, allowances and bonuses of Credits, the ability to see who is viewing your photos, and the ability to suppress mobile advertisements. |

|

● |

Skout Premium: Skout Premium is a subscription product that gives members extra privileges on Skout, including higher priority in the Meet feature, unlimited access to the Travel and Who Favorited Me? features, and the ability to suppress advertisements. |

How We Create Value for Marketers

We believe our large and hyper-engaged youthful audience means significant scale for advertisers and makes MeetMe an attractive publisher for marketers of all sizes. We focus on providing a wide variety of advertising products that drive our users to engage with brands. We offer some of the most cutting-edge, data-driven ad targeting capabilities in mobile, pinpointing hard-to-reach users based on location and demographics. During the fourth quarter of 2016, we served over eight billion ad impressions each month across our web and mobile applications. Our brand and agency advertising business, also known as direct-sold advertising, is generally powered by companies looking for high-impact ad units and brand engagement from our younger demographic. The majority of our advertising inventory is sold through programmatic media buying.

Social Theater

Our Social Theater product enables publishers to offer a value exchange where users can engage with advertisers in exchange for the hosting platform’s virtual currency or products behind a paywall. Social Theater advertising runs not only on MeetMe, where our users can watch videos and otherwise engage with brands in exchange for Credits, but also on social games and applications across other social networks, including Facebook. Social Theater can also be used by marketers to drive video views, application installs, and “likes” and “shares” on Facebook, Twitter, and other social platforms. When a Social Theater campaign is distributed outside of MeetMe on a different platform we consider it “Cross-Platform Revenues.”

Our Strategy

We believe we are well positioned to pioneer the next category of social networking: social discovery. We are just getting started on our vision of satisfying the universal need for human connection among all people, everywhere. Our strategy for 2017 and beyond is aimed at consolidating the fragmented mobile meeting category, continued growth and engagement of our active user base, and improving the rate at which we monetize our active users, especially on mobile. As we drive toward becoming the dominant global mobile meeting brand, we will seek to strategically acquire synergistic apps that accelerate our scale and density, and immediately contribute to EBITDA.

Key elements of our strategy include:

|

● |

Build Great Products to Acquire, Engage, and Thrill Users: Our core focus is to create innovative social experiences using sophisticated data science that help our users meet new people in their local communities or throughout the world. We plan on continuing to invest in improving our core platform as technology advances and in devising new ways of engineering serendipity as activity increasingly moves online. |

|

● |

Acquire: We think the time is ripe for consolidation in this space and we think we are the ones to do it. The Company is seeking acquisitions that contribute immediately to EBITDA. We operate industry leading margins, and we intend to bring the same superior execution and disciplined focus on results to our target companies. As our portfolio grows, we will realize more economies of scale and cross-promotional opportunities. |

|

● |

Offer Innovative and Engaging Ad Products for Marketers: We consider it critical to continue improving our advertising products to create more value for our marketers, attract new customers, and display targeted advertisements that are more relevant for our users. We pursue these goals through a combination of internal innovation and rapid integration of advertising solutions that have been successful in the marketplace. |

|

● |

Expand Our Reach Internationally: There are over one billion people aged 18-34 worldwide, of which approximately 50 million reside in the U.S., where our traffic has historically been centered. In 2013, we internationalized MeetMe and launched in twelve languages other than English, laying the foundation for significant future growth in other geographies. In 2015, some of our fastest growing audiences were international, including in countries such as Turkey, Italy, and India. |

Operating Metrics

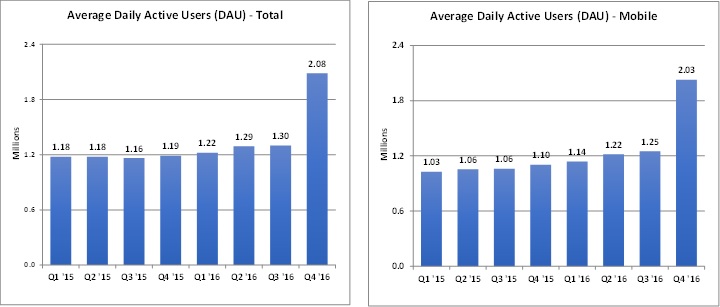

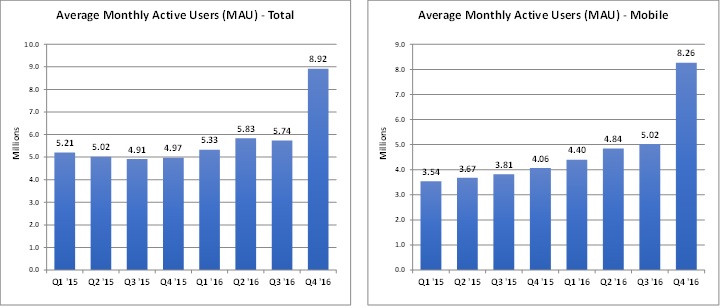

We measure website and application activity in terms of monthly active users (“MAUs”) and daily active users (“DAUs”). We define MAU as a registered user of one of our platforms who has logged in and visited within the last month of measurement. We define DAU as a registered user of one of our platforms who has logged in and visited within the day of measurement. For the quarters ended December 31, 2016, 2015 and 2014, the total Company MAUs were 9.03 million, 4.97 million and 4.98 million, respectively, and total Company DAUs were 2.08 million, 1.19 million and 1.09 million, respectively.

|

Monthly Average for the Quarters Ended December 31, |

||||||||||||

|

2016 |

2015 |

2014 |

||||||||||

|

MAU-MeetMe |

5,675,029 | 4,971,638 | 4,983,122 | |||||||||

|

MAU-Skout |

3,350,274 | — | — | |||||||||

|

MAU-Total |

9,025,303 | 4,971,638 | 4,983,122 | |||||||||

|

For the Quarters ended December 31, |

||||||||||||

|

2016 |

2015 |

2014 |

||||||||||

|

DAU-MeetMe |

1,282,916 | 1,189,290 | 1,088,999 | |||||||||

|

DAU-Skout |

802,071 | — | — | |||||||||

|

DAU-Total |

2,084,987 | 1,189,290 | 1,088,999 | |||||||||

Trends in Our Metrics

In addition to MAUs and DAUs, we measure activity on MeetMe’s properties in terms of average revenue per user (“ARPU”) and average daily revenue per daily active user (“ARPDAU”). We define ARPU as the quarterly average revenue per MAU. We define ARPDAU as the average quarterly revenue per DAU. We define mobile MAU as a user who accessed our sites by a one of our mobile applications or by the mobile optimized version of our website, whether on a mobile phone or tablet during the month of measurement. We define a mobile DAU as a user who accessed our sites by one of our mobile applications or by the mobile optimized version of our website, whether on a mobile phone or tablet during the day of measurement.

In the quarter ended December 31, 2016, MeetMe averaged 5.02 million mobile MAUs and 5.68 million total MAUs on average, as compared to 4.06 million mobile MAUs and 4.97 million total MAUs on average in the quarter ended December 31, 2015, a net increase of 0.96 million or 23.6% for mobile MAUs, and a net increase of 0.71 million or 14.3% for total MeetMe MAUs. In addition, Skout averaged 3.24 million mobile MAUs and 3.35 million total MAUs for the quarter ended December 31, 2016. MeetMe mobile DAUs were 1.25 million in the quarter ended December 31, 2016, a 13.6% increase, from 1.10 million in the quarter ended December 31, 2015. Skout mobile DAUs were 0.78 million in the quarter ended December 31, 2016. For the quarter ended December 31, 2016, MeetMe averaged 1.28 million total DAUs, as compared to 1.19 million total DAUs on average for the quarter ended December 31, 2015, a net increase of approximately 0.09 million total DAUs, or 7.6%. For the quarter ended December 31, 2016, Skout averaged 0.80 million total DAUs.

For the quarter ended December 31, 2016 MeetMe mobile revenue increased by 20% and MeetMe mobile ARPDAU increased by 6% to $20.6 million and $0.180, respectively, for the quarter ended December 31, 2016 from $17.2 million and $0.169, respectively, for the quarter ended December 31, 2015. Our mobile revenue increased by 126% and our mobile ARPDAU by 89% to $17.2 million and $0.169, respectively, for the quarter ended December 31, 2015 from $7.60 million and $0.089, respectively, for the quarter ended December 31, 2014. For the quarter ended December 31, 2016, Skout mobile revenue was $7.2 million, and Skout mobile ARPDAU was $0.102.

In the quarter ended December 31, 2016, MeetMe earned an average of $0.25 ARPU on the web and $4.11 in ARPU in our mobile applications, as compared to $0.87 in web ARPU and $4.22 in mobile ARPU for the quarter ended December 31, 2015. In the quarter ended December 31, 2016, MeetMe earned an average of $0.039 in web ARPDAU and $0.180 in mobile ARPDAU, as compared to $0.106 in web ARPDAU and $0.169 in mobile ARPDAU for the quarter ended December 31, 2015. Skout mobile ARPU was $2.21 and mobile ARPDAU was $0.102 for the quarter ended December 31, 2016.

PRODUCT DEVELOPMENT

We are continually developing new products, as well as optimizing our existing platform and feature set in order to meet the evolving needs of our user base and advertising partners.

We develop most of our software internally. We will, however, purchase technology and license intellectual property rights where it is strategically important, operationally compatible, or economically advantageous. For instance, we partner with third parties to further our internationalization efforts as we look to bring additional languages into our existing platforms. We are not materially dependent upon licenses and other agreements with third parties relating to product development.

Our technology team of 73 people consists of our product development and engineering team, our database administration team, our quality assurance team and our network system operators. These teams are responsible for feature enhancements and general maintenance across all of our platforms. Our technology team is headquartered in New Hope, Pennsylvania with an additional office in San Francisco, California.

SALES AND MARKETING

Historically, we have grown our user base in large part through organic, viral channels. By encouraging members to invite their friends to join MeetMe and to share their activity across other external platforms, including Facebook and Twitter, and by providing members with easy-to-use tools, we believe we have successfully grown our user base while minimizing marketing costs. We focus primarily on creating a truly differentiated experience and compelling value proposition for new users in our markets and developing the technologies needed to facilitate their word-of-mouth marketing on our behalf in order to attract and retain new members.

Our paid customer acquisition strategy continues to focus on both acquiring users in new geographies where the active user base on the Company’s mobile apps had previously been small in comparison to our user base in the U.S. and Canada. We spent $12.1 million, $3.3 million and $2.0 million on paid direct user acquisition in 2016, 2015 and 2014, or 15.9%, 5.9% and 4.5% of our total revenue, respectively. Of the $12.1 million spent in 2016, $10.2 million was spent on user acquisition for MeetMe and $1.9 million was spent on user acquisition for Skout. As mobile ARPU has increased over the last few years, we believe it has made sense to increase our marketing spend. We plan to increase the overall Company spend rate in 2017 to approximately 20% of revenue.

SALES AND OPERATIONS

Our advertising sales and operations team is comprised of 11 full-time employees in the U.S. and covers major brand agencies, direct response and cost-per-action engagement advertisers, advertising networks, and mobile agencies. Our advertising operations are headquartered in New Hope, Pennsylvania, with additional offices in New York, New York, Los Angeles, California and San Francisco, California.

Our operations and member services team consists of 22 full-time employees, 6 part-time employees, and 52 contractors split between Delhi and Bangalore, India and Cavite, Philippines. This team is responsible for reviewing images and other user-generated content, investigating and responding to member abuse reports, and providing general customer support.

INTELLECTUAL PROPERTY

Our intellectual property includes trademarks related to our brands, products, and services, copyrights in software and creative content, trade secrets, domain names, and other intellectual property rights and licenses of various kinds. We seek to protect our intellectual property through copyright, trade secret, trademark and other laws of the U.S. and other countries, and through contractual provisions.

We consider the MeetMe, Skout and Social Theater trademarks and our related trademarks to be valuable to the Company, and we have registered these trademarks in the U.S. and other countries throughout the world and aggressively seek to protect them.

COMPETITION

We believe we are challenging the dominant player in the dating space, Match Group, but we are not limited to dating. We operate at the forefront of a nascent segment (social discovery) of a broader sector that is still being defined (social networking). As such, we face significant competition in every aspect of our business, both from established companies whose products help users meet new people, or are evolving to do so, and from smaller but well-funded startups that can quickly gain attention and compete with us for users. Examples of services that compete with us for users and advertiser interest include, but are not limited to:

|

● |

Mobile applications and websites whose primary focus is to help users meet new people in their geographical area, including Badoo, Twoo, and Meetup. |

|

● |

Social networking mobile applications and websites with a focus on dating, which is a subset of the opportunity around meeting new people, such as Zoosk, Match, Happn, PlentyOfFish, OkCupid, and Tinder. |

|

● |

Broader social networks that currently offer or may evolve to offer services aimed at helping users meet new people in their area, such as Facebook, Twitter, and LinkedIn. |

|

● |

Interest-based communities that help users connect with like-minded people online, including Pinterest, Reddit, Tumblr, and Quora, as well as vertical communities such as Goodreads, Last.fm, and Fitocracy. |

|

● |

Significant competition for Social Theater comes from publishers including TrueX, Unruly Media, SuperSonic Advertising, Jun Group, and Genesis Media. |

As we introduce new products, and as other companies introduce new products and services, we expect to become subject to additional competition. Additional information regarding certain risks related to our competition is included in Part I, Item 1A—Risk Factors of this report.

In addition to other online dating and social networking brands, we compete indirectly with offline dating services, such as matchmakers.

EMPLOYEES

As of December 31, 2016, we employed 124 full-time and 7 part-time employees in the U.S. Our future success is substantially dependent on the performance of our senior management and key technical personnel, as well as our continuing ability to attract, maintain the caliber of, and retain highly qualified technical and managerial personnel. Additional information regarding certain risks related to our employees is included in Part I, Item 1A—Risk Factors of this report and is incorporated herein by reference.

GOVERNMENT REGULATION

In the U.S., advertising and promotional information presented to visitors on our mobile applications and website and our other marketing activities are subject to federal and state consumer protection laws that regulate unfair and deceptive practices. There are a variety of state and federal restrictions on the marketing activities conducted by email, or over the Internet, including U.S. federal and state privacy laws and the Telephone Consumer Protection Act of 1991, or the TCPA, the Controlling the Assault of Non-Solicited Pornography and Marketing Act of 2001, or the CAN-SPAM Act. We may also be subject to laws in the various other countries in which we operate. The rules and regulations are complex and may be subject to different interpretations by courts or other governmental authorities. We may unintentionally violate such laws, such laws may be modified, and new laws may be enacted in the future. Any such developments (or developments stemming from enactment or modification of other laws) or the failure to anticipate accurately the application or interpretation of these laws could create liability to us, result in adverse publicity, and negatively affect our businesses. Additional information regarding certain risks related to government regulations is included in Part I, Item 1A—Risk Factors of this report.

CORPORATE HISTORY

MeetMe was incorporated in Nevada in June 1997, and merged with Insider Guides, Inc., doing business as myYearbook.com, on November 10, 2011. On December 6, 2011, the Company changed its legal domicile to Delaware. Effective June 1, 2012, the Company changed its name from Quepasa Corporation to MeetMe, Inc. and completed the transition of its website to meetme.com in the fourth quarter of 2012. On October 3, 2016, MeetMe acquired 100% of the issued and outstanding shares of common stock of Skout. The Company owns and operates the MeetMe and Skout mobile applications, and meetme.com and skout.com.

Our executive offices and principal facilities are located at 100 Union Square Drive, New Hope, Pennsylvania, 18938. Our telephone number is (215) 862-1162. Our corporate website is www.meetmecorp.com. Investors can obtain copies of our SEC filings from our corporate website free of charge, as well as from the SEC website, www.sec.gov. The information contained on our corporate website and the SEC website is not incorporated herein.

AVAILABLE INFORMATION

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to reports filed or furnished pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, are available free of charge on our Investor Relations website at www.meetmecorp.com/investors/sec-filings/ as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The SEC maintains a website that contains these filings at www.sec.gov. The information posted on our corporate website and the SEC website is not incorporated herein.

ITEM 1A. RISK FACTORS.

Investing in our common stock involves a high degree of risk. You should consider carefully the risks and uncertainties described below, together with all of the other information in this report, including the consolidated financial statements and the related notes included elsewhere in this report, before deciding whether to invest in shares of our common stock. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material may also become important factors that adversely affect our business. If any of the following risks actually occurs, our business, financial condition, results of operations, and future prospects could be materially and adversely affected. In that event, the market price of our common stock could decline, and you could lose part or all of your investment.

Risks Related to Our Business

If we cannot increase our daily and monthly active users and increase their engagement on MeetMe and Skout, our future operating results may decline.

We offer applications that are free to use, with only a small percentage of our users paying for virtual goods. Our financial performance has been and will continue to be significantly determined by our success in adding, retaining, and engaging active users. We must continue to add new members to our user base and retain existing members by offering new and engaging features and products in order to attract advertising investment and generate revenue from the sale of in-app products. The challenges we face include, among other things, our ability to:

|

● |

attract new users and retain existing users at a consistent rate; |

|

● |

increase engagement by existing users; |

|

● |

monetize our user base; |

|

● |

anticipate changes in the social networking and social discovery industry; |

|

● |

launch new products and release enhancements that become popular; |

|

● |

develop and maintain a scalable, high-performance technology infrastructure that can efficiently and reliably handle increased member usage, fast load times and the deployment of new features and applications; |

|

● |

process, store and use data in compliance with governmental regulation and other legal obligations related to privacy; |

|

● |

compete with other companies that are currently in, or may in the future enter, the social networking or social discovery industry; |

|

● |

hire, integrate and retain world class talent; and, |

|

● |

expand our business internationally and with respect to mobile devices. |

If we fail to retain existing users or add new users, or if our users decrease their level of engagement, our revenue, financial results, and business may be significantly harmed.

The size of our user base and our users’ level of engagement are critical to our success. Our financial performance is significantly affected by our success in adding, retaining, and engaging active users. If people do not perceive our products to be useful, reliable, and trustworthy, we may not be able to attract or retain users or otherwise maintain or increase the frequency and duration of their engagement. A number of other social networking companies that achieved early popularity have since seen their active user bases or levels of engagement decline, in some cases precipitously. There is no guarantee that we will not experience a similar erosion of our active user base or engagement levels. A decrease in user retention, growth, or engagement could render us less attractive to advertisers, which may have a material and adverse impact on our revenue, business, financial condition, and results of operations. Any number of factors could potentially negatively affect user retention, growth, and engagement, including if we fail to:

|

● |

introduce new and improved products that are favorably received; |

|

● |

identify and respond to emerging technological trends in the market; |

|

● |

provide a compelling user experience with the decisions we make with respect to the frequency, prominence, and size of advertising and other commercial content we display; |

|

● |

continue to develop features for mobile devices that users find engaging, that work with a variety of mobile operating systems and networks, and that achieve a high level of market acceptance; |

|

● |

acquire or license leading technologies; |

|

● |

avoid technical or other problems that prevent us from delivering our services in a rapid and reliable manner or otherwise affect the user experience; or |

|

● |

provide adequate customer service to users or advertisers. |

If we are unable to maintain and increase our user base and user engagement, our revenue, financial results, and future growth potential could be adversely affected.

We believe the number of our registered users is higher than the number of actual users.

We believe the number of our registered users is higher than the number of actual users because some members may have multiple registrations, other members may have died or may have become incapacitated, and others may have registered under fictitious names. Members also terminate their memberships and delete their profiles. Given the challenges inherent in identifying these accounts, we do not have a reliable system to accurately identify the number of our active members.

If our users do not interact with each other or our viral marketing strategy fails, our ability to attract new users may suffer and our revenue may decrease.

The majority of our users do not visit MeetMe and Skout frequently and spend a limited amount of time when they do visit. The majority of our page views are generated by a minority of our users. If we are unable to encourage our users to interact more frequently and to increase the amount of user generated content they provide, our ability to attract new users and our financial results may suffer. In addition, part of our success depends on our users interacting with our products and contributing to our viral advertising platform (Social Theater). If our Social Theater platform is unsuccessful and our users do not participate in Social Theater campaigns, our operating results could suffer.

We generate the majority of our revenue from advertising, and in particular, digital advertising. If we incur a loss of advertisers, or a reduction in spending by advertisers, our revenue could substantially decline, resulting in significant operating losses and negatively impacting our cash flows.

We generate most of our revenue from parties advertising on our platform, and, in particular, those advertisers in the digital advertising market. The digital advertising market, while growing, is still relatively new and remains somewhat unproven. Factors such as the lack of standard metrics in the digital advertising market may lead to varying and inconsistent ad rates and potentially demands for rebates.

As is common in the industry, our advertisers typically do not have long-term advertising commitments with us. Many of our advertisers spend only a relatively small portion of their overall advertising budget with us. Advertisers will not continue to do business with us, or they will reduce the prices they are willing to pay to advertise with us, if we do not deliver advertising and other commercial content in an effective manner, or if they do not believe that their investment in advertising with us will generate a competitive return relative to other alternatives. Our advertising revenue could be adversely affected by a number of other factors, including:

|

● |

decreases in user engagement, including time spent on MeetMe; |

|

● |

product changes or inventory management decisions we may make that reduce the size, frequency, or relative prominence of advertising and other commercial content that we display; |

|

● |

our inability to increase the rate at which our users “click through” on the ads we display; |

|

● |

our inability to improve our analytics and measurement solutions that demonstrate the value of our advertising and other commercial content; |

|

● |

loss of advertising market share to our competitors; |

|

● |

adverse legal developments relating to advertising, including legislative and regulatory developments and developments in litigation; |

|

● |

adverse media reports or other negative publicity involving us or other companies in our industry; |

|

● |

objections to the content of our apps and websites; |

|

● |

changes in the way online advertising is priced; |

|

● |

changes in the digital advertising market, including the introduction of standard metrics; |

|

● |

the impact of new technologies that could block or obscure the display of our advertising and other commercial content; and |

|

● |

the impact of macroeconomic conditions and conditions in the advertising industry, and, in particular, the digital advertising industry, in general. |

The occurrence of any of these or other factors could result in a reduction in demand for our advertising and other commercial content, which could reduce the prices we receive for our advertising and other commercial content, or cause advertisers to stop advertising with us altogether. In turn, we could incur a substantial decline in revenue, increased operating losses, and a negative impact on cash flows.

We have terminated agreements with our former advertising partner and may not be able to collect amounts due.

On June 2, 2015, we terminated two agreements with Beanstock relating to our advertising inventory on web and mobile: the Web Agreement and the Mobile Agreement. We terminated both agreements for non-payment, and in the third quarter of 2015, we wrote-off the accounts receivable balance under the agreements of $5.7 million as uncollectible. We have filed suit against Beanstock and its guarantor, Adaptive Medias, Inc., and we intend to pursue all available remedies to collect amounts due to us, including liquidated damages under the Mobile Agreement. We cannot guarantee if, when or how much outstanding will be paid to us. We also do not know the amount of time and effort that will be required from management to collect these amounts. On January 20, 2016, the Company received notice from the United States Bankruptcy Court, District of Delaware, that a Chapter 7 bankruptcy case against Beanstock had been filed on October 7, 2015. Both of the state court actions have been stayed by the courts as a result of the bankruptcy filing against Beanstock. For a description of the litigation, see Part I, Item 3—Legal Proceedings.

We fill our advertising inventory internally, without the use an external advertising partner as in the past, and if we fail to maintain and expand our base of advertisers, our revenue and our business could be harmed.

Our ability to grow our business depends in part on our ability to maintain and expand our advertiser base. To do so, we must ensure that existing and prospective advertisers know that our advertising products offer a material benefit and can generate a competitive return relative to other alternatives, including online, mobile and traditional advertising platforms. Advertisers may not continue to do business with us, or they may reduce the prices they are willing to pay to advertise with us, if we do not deliver ads in an effective manner, or if they do not believe that their investment in advertising with us will generate competitive returns. Our ability to do so depends on factors including:

|

● |

Competitiveness of Our Products. We must deliver ads in an effective manner and provide accurate analytics and measurement solutions that demonstrate the value of our advertising products compared to those of our competitors. Similarly, if the pricing of our advertising products does not compare favorably to those of our competitors, advertisers may reduce their advertising with us or choose not to advertise with us at all. |

|

● |

Traffic Quality. The success of our advertising program depends on delivering positive results to our advertising customers. Low-quality or invalid traffic, such as robots, spiders and the mechanical automation of clicking, may be detrimental to our relationships with advertisers and could adversely affect our advertising pricing and revenue. If we fail to detect and prevent click fraud or other invalid clicks on ads, the affected advertisers may experience or perceive a reduced return on their investments, which could lead to dissatisfaction with our products, refusals to pay, refund demands or withdrawal of future business. |

|

● |

Perception of Our Platform. Our ability to compete effectively for advertiser budgets depends on our reputation and perceptions regarding our platform. |

|

● |

Macroeconomic Conditions. Adverse macroeconomic conditions can have a negative impact on the demand for advertising, particularly with respect to online advertising products. Advertisers may have limited advertising budgets and may view online advertising as lower priority than offline advertising. |

As is typical in our industry, our advertisers generally do not have long-term obligations to purchase our products. Their decisions to renew depend on the degree of satisfaction with our products as well as a number of factors that are outside of our control. As a result, we may experience attrition in our advertisers in the ordinary course of business resulting from several factors, including losses to competitors or declining advertising budgets. The occurrence of any of these or other factors could result in a reduction in demand for our ads, which may reduce the prices we receive for our ads, either of which would negatively affect our revenue and operating results.

If we cannot effectively monetize our mobile products, we may not be able to successfully grow our business.

The shift of our audience from web to mobile may be disruptive to our business and operating results. As our users shift from web to mobile access, web page views have decreased. Decreasing web traffic contributes to declining web revenue. Our business faces the challenge of ramping up mobile monetization to offset declining web revenues as users continue to increase their mobile access. The transition in our user access could impact revenue in the short-term and medium-term as mobile monetization continues to mature slowly. Accordingly, as users increasingly access our mobile products as a substitute for using personal computers, if personal computer usage continues to be phased out by the popularity of smart phones and tablets, and if we are unable to successfully implement monetization strategies for our mobile users, our revenue and financial results could be negatively affected.

Because we face significant competition from other social networks and companies with greater resources, we may not be able to compete effectively.

We face significant competition from other companies that seek to connect members online. Our competitors are other companies providing portal and online community services, such as Facebook, Google, Badoo, PlentyOfFish, and OkCupid. Many of our competitors have greater resources, more established reputations, a broader range of content and products and services, longer operating histories, and more established relationships with their users than we do. They can use their experience and resources against us in a variety of competitive ways, including developing ways to attract and maintain users. These factors may allow our competitors to respond more effectively than us to new or emerging technologies and changes in market requirements. Our competitors may develop products, features, or services that are similar to ours or that achieve greater market acceptance, may undertake more far-reaching and successful efforts at developing new services or marketing campaigns, or may adopt more aggressive pricing policies. Some of our competitors may enjoy better competitive positions in certain geographical regions or within certain user demographics that we currently serve or may serve in the future. These advantages could enable these competitors to offer products that are more appealing to users and potential users than our products or to respond more quickly and/or cost-effectively than us to new or changing opportunities. In addition, within the industry generally, costs for users to switch between products are low, and users have a propensity to try new approaches to connecting with people. As a result, new products, entrants and business models are likely to continue to emerge. It is possible that a new product could gain rapid scale at the expense of existing brands through harnessing a new technology or distribution channel, creating a new approach to connecting people or some other means.

We believe that our ability to compete effectively depends upon many factors both within and beyond our control, including:

|

● |

the usefulness, ease of use, performance, and reliability of our services compared to our competitors; |

|

● |

the size and composition of our user base; |

|

● |

the engagement of our users with our services; |

|

● |

the timing and market acceptance of services, including developments and enhancements to our or our competitors’ services; |

|

● |

our ability to monetize our services; |

|

● |

the frequency, size, and relative prominence of the advertising and other commercial content displayed by us or our competitors; |

|

● |

customer service and support efforts; |

|

● |

marketing and selling efforts; |

|

● |

changes mandated by legislation, regulatory authorities, or litigation, including settlements and consent decrees, some of which may have a disproportionate effect on us; |

|

● |

acquisitions or consolidation within our industry, which may result in more formidable competitors; |

|

● |

our ability to attract, retain, and motivate talented employees, particularly software engineers; |

|

● |

our ability to cost-effectively manage and grow our operations; and |

|

● |

our reputation and brand strength relative to our competitors. |

If we are not able to effectively compete, our user base and level of user engagement may decrease, which could make us less attractive to advertisers and materially and adversely affect our revenue and results of operations.

Because we face competition from traditional media companies, we may not be included in the advertising budgets of large advertisers, which could harm our operating results.

Major brand and network advertising drives most of our revenue. We rely primarily on cost per thousand (“CPM”) advertising, where the price for advertising is based on the number of users who view it. In addition to mobile application developers and Internet companies, we face competition from companies that offer traditional media advertising opportunities. Most large advertisers have set advertising budgets, a portion of which is allocated to Internet and mobile advertising. We expect that large advertisers will continue to increase their advertising efforts on the Internet and mobile devices. If we fail to convince these companies to spend a portion of their advertising budgets on social media and specifically with us, however, our operating results could be harmed.

An increasing number of individuals are using devices other than personal computers to access the Internet. If versions of our applications developed for these devices do not gain widespread adoption, or do not function as intended, our business could be adversely affected.

The number of people who access the Internet through devices other than personal computers, including smart phones, cell phones and handheld tablets, has increased dramatically in the past few years and is projected to continue to increase. We have launched a mobile application for Android smart phones, iPhones and iPads. We are dependent on interoperability with popular mobile operating systems that we do not control, such as Android and iOS, and any changes in such systems that degrade our platform’s functionality or give preferential treatment to competitive services could adversely affect our mobile application usage. Each device manufacturer or platform provider may establish unique or restrictive terms and conditions for developers on such devices or platforms, and our applications may not work well or be viewable on these devices as a result.

We rely on the Apple App Store and the Google Play Store to distribute our mobile applications. Our business will suffer if we are unable to maintain a good relationship with Apple and Google, if their terms and conditions or pricing change to our detriment, if we violate, or either company believes that we have violated, its terms and conditions, or if either of these platforms are unavailable for a prolonged period of time.

The Apple App Store and the Google Play Store are our primary distribution, marketing, promotion and payment platforms for our apps. Any deterioration in our relationship with Google or Apple would harm our business and adversely affect the value of our stock.

We are subject to these platforms’ standard terms and conditions for application developers, which govern the promotion, distribution and operation of applications. These platforms have policies governing, for example, use of user data, personal and sensitive information, and advertising IDs, as well as ones relating to advertising (including deceptive, disruptive and inappropriate ads) and interference with application and device functionality. If we violate, or if a platform provider believes we have violated, these terms and conditions, the particular platform provider may discontinue or limit our access to that platform, which could prevent us from satisfying our contractual obligations to our mobile customers. Our business could also be harmed if a platform provider modifies its current terms of service or other policies, including fees, in a manner adverse to us.

We also rely on the continued operation and availability of these third-party platforms. In the past, platforms have been unavailable for short periods of time. On more than one occasion, for example, Apple has rejected our applications because of user generated content and other concerns. In response we devoted additional resources to image review, and changed some of our content allowance policies. If this recurs on a prolonged or frequent basis, or other similar issues arise that impact users’ ability to download or use our mobile event applications, we may owe some of our customers rebates, which would increase our expenses and lower our gross margins. Our revenue, operating results or brands could also suffer harm. Furthermore, any material change or deterioration in our relationship with these platform providers could harm our business.

Furthermore, if Google or Apple loses its market position or otherwise falls out of favor with users, we would need to identify alternative channels for marketing, promoting and distributing our apps, which would consume substantial resources and may not be effective. In addition, Google and Apple have broad discretion to change their terms of service and other policies with respect to us and other developers, and those changes may be unfavorable to us.

If the Apple “App Store” or “Google Play” changes its search and rating algorithms, it could affect our ability to acquire new mobile members.

Our iPhone and Android applications rank near the top of the “Free Social” categories and near the top of many key search terms. However, Apple and Google have changed their rating and search algorithms in the past without notice. Future changes to the rating and search algorithms by Apple or Google could impact our rating and search results, leading to a drop in new mobile application downloads, which could cause our business and operating results to suffer.

If we are unable to continue to develop successful applications for mobile platforms and standalone mobile applications, our growth prospects could suffer.

We have offered applications for mobile platforms since May 2010. We expect to continue to devote substantial resources to the development of mobile applications, but there can be no assurances that we will continue to succeed in developing applications that appeal to users or advertisers. We may encounter difficulty in attracting leading advertisers to our mobile applications. We may also face challenges working with wireless carriers, mobile platform providers and other mobile communications partners. Finally, we may face challenges converting mobile users into users that pay for in-app products. These and other uncertainties make it difficult to know whether we will continue to succeed in developing commercially viable applications for mobile platforms. If we do not succeed in doing so, our growth prospects could suffer.

If we cannot address technological change in our industry in a timely fashion and develop new services, our future results of operations could be adversely affected.

The Internet and electronic commerce industries are characterized by:

|

● |

rapidly changing technology; |

|

● |

evolving industry standards and practices that could render our platform and proprietary technology obsolete; |

|

● |

changes in consumer tastes and demands; and |

|

● |

frequent introductions of new services or products that embody new technologies. |

Our future performance will depend, in part, on our ability to develop, license or acquire leading technologies and program formats, enhance our existing services, and respond to technological advances and consumer tastes and emerging industry standards and practices on a timely and cost-effective basis. Developing mobile and website technology involves significant technical and business risks. We may not be able to successfully use new technologies or adapt our platforms and technology to emerging industry standards. We may not be able to remain competitive or sustain growth if we do not adapt to changing market conditions or customer requirements.

Because we plan to continue expanding our operations abroad where we have limited operating experience, we may be subject to increased business, economic and regulatory risks that could affect our financial results.

We plan to continue the international expansion of our business operations. We may enter new international markets where we have limited or no experience in marketing, selling, and deploying our products. If we fail to deploy or manage our operations in international markets successfully, our business could suffer. In addition, we are subject to a variety of risks inherent in doing business internationally, including:

|

● |

political, social, or economic instability; |

|

● |

risks related to the legal and regulatory environment in foreign jurisdictions, including with respect to privacy, and changes in laws, regulatory requirements, and enforcement; |

|

● |

burdens of complying with a variety of foreign laws; |

|

● |

potential damage to our brands and reputation due to our compliance with local laws, including potential censorship or requirements to provide user information to local authorities, and/or potential penalties for failing to comply with such local laws; |

|

● |

lack of familiarity with local customs; |

|

● |

fluctuations in currency exchange rates; |

|

● |

higher levels of credit risk and payment fraud; |

|

● |

reduced protection for intellectual property rights in some countries; |

|

● |

difficulties in staffing and managing global operations and the increased travel, infrastructure; and |

|

● |

compliance with the United States Foreign Corrupt Practices Act and similar laws in other jurisdictions. |

If we are unable to expand internationally and manage the complexity of our global operations successfully, our financial results could be adversely affected.

If we are unable to implement payment gateways to our users, our results of operations could be adversely affected.

We conduct our business in countries outside of the U.S. and depend on payment gateways that are not as well developed as those in the U.S., where most people have credit cards or bank debit cards to use in paying for virtual goods, products, and services. Users in some countries in which we operate do not always have access to credit and debit cards and other payment methods common in the U.S. If we are unable to implement payment gateways that provide our members with the ability to pay for goods, products and services easily, our future results could be adversely affected. Additionally, our inability to collect and receive payments from these other sources could have an adverse effect on our business and results of operations.

Because we rely on Facebook as a distribution, marketing, and promotion platform, if our relationship with Facebook changes or if Facebook loses market share, our business could be adversely affected.

Facebook is an important distribution, marketing and promotion platform for our content and applications. We generate a number of our new users through the Facebook platform and we expect to continue to do so for the foreseeable future. As such, we are subject to Facebook’s standard terms and conditions for Facebook Connect and for application developers, which govern the promotion, distribution and operation of applications on the Facebook platform.

Our ability to acquire new members and provide services to our existing members could be harmed if:

|

● |

Facebook discontinues or limits access to its platform by us and other application developers; |

|

● |

Facebook modifies its terms of service or other policies, including changing how the personal information of its users is made available to application developers on the Facebook platform or shared by users; |

|

● |

Facebook develops its own competitive offerings; or |

|

● |

Facebook disallows our advertising in its platforms. |

We have benefited from Facebook’s strong brand recognition and large user base. If Facebook loses its market position or otherwise falls out of favor with users, we would need to identify alternative channels for marketing, promoting and distributing our content and applications, which could consume substantial resources and may not be effective. In addition, Facebook has broad discretion to change its terms of service and other policies with respect to us and other developers, and any such changes could be unfavorable. Facebook may also change its fee structure or add fees associated with access to and use of the Facebook platform.

Because our business is subject to complex and evolving U.S. and foreign laws and regulations regarding privacy, data protection, and other matters, we could be subject to claims, changes to our business practices, increased cost of operations, or declines in user growth or engagement, or otherwise sustain harm to our business.

We are subject to a variety of laws and regulations in the U.S. and abroad that involve matters central to our business, including user privacy, rights of publicity, data protection, intellectual property, electronic contracts and other communications, competition, protection of minors, consumer protection, taxation, and online payment services. Foreign data protection, privacy, and other laws and regulations are often more restrictive than those in the U.S. U.S. federal, state and foreign laws and regulations are constantly evolving and can be subject to significant change. The application and interpretation of these laws and regulations are often uncertain, particularly in the new and rapidly evolving industry in which we operate. In addition, federal, state and foreign legislative or regulatory bodies may enact new or additional laws and regulations concerning data privacy and retention issues which could adversely impact our business. The interpretation and application of privacy, data protection and data retention laws and regulations are currently unsettled in the U.S. and internationally. These laws may be interpreted and applied inconsistently from country to country and inconsistently with our current data protection policies and practices. Complying with these varying state to state or international requirements could cause us to incur substantial costs or require us to change our business practices in a manner adverse to our business.

We are also subject to laws and regulations that dictate whether, how, and under what circumstances we can transfer, process and/or receive transnational data that is critical to our operations, including data relating to users, customers, or partners outside the U.S., and those laws and regulations are uncertain and subject to change. For example, in October 2015, the European Court of Justice invalidated the European Commission's 2000 Safe Harbour Decision as a legitimate basis on which companies could rely for the transfer of data from the European Union to the U.S.

Proposed legislation and regulations could also significantly affect our business. There currently are a number of proposals pending before federal, state, and foreign legislative and regulatory bodies, including a data protection regulation that is pending final approval by the European legislature that may include operational requirements for companies that receive or process personal data that are different than those currently in place in the European Union, and that will include significant penalties for non-compliance. Similarly, there are a number of legislative proposals in the U.S., at both the federal and state level, that could impose new obligations in areas affecting our business.

We use email, push notifications, and text message campaigns to drive user engagement. Disruptions in, restrictions on, and certain legal risks associated with the sending or receipt of emails, push notifications, or text messages or a decrease in user willingness to receive emails, push notifications, and text messages could adversely affect our revenues and business.

We use email, push notifications, and text message campaigns to drive user engagement. We send a large volume of emails, push notifications, and text messages to users notifying them of a variety of activities on our platform, such as new connections. We also rely on the use of email, push notifications, and text messages as a part of our registration and validation processes. Because of the importance of email, push notifications, and text messages to our business, if we are unable to successfully deliver emails, push notifications, or text messages to our users or if users consistently decline to open our emails, push notifications, or text messages, our business could be adversely affected.

We also face a risk that service providers or email applications may block bulk message transmissions or otherwise experience technical difficulties that result in our inability to successfully deliver emails, push notifications, or text messages to our users. Third parties may also block our emails as spam, impose restrictions on our emails, push notifications, or text messages, or start to charge for the delivery of emails through their email systems. In addition, changes in how webmail applications organize and prioritize email may reduce the number of users opening our emails. For example, Google’s Gmail service has a feature that organizes incoming emails into categories (for example, primary, social and promotions). Such categorization or similar inbox organizational features may result in our emails being delivered in a less prominent location in a user’s inbox or viewed as “spam” by our users and could reduce the likelihood of that user opening our emails.

Email communications may subject us to potential risks, such as liabilities or claims resulting from unsolicited email or spamming, lost or misdirected messages, security breaches, illegal or fraudulent use of email or personal information or interruptions or delays in email service. For example, in the U.S., the CAN-SPAM Act establishes certain requirements for the distribution of “commercial” email messages and provides for penalties for transmission of commercial email messages that are intended to deceive the recipient as to source or content. In addition, some countries and states have passed laws regulating commercial email practices that are, in some cases, significantly more punitive and difficult to comply with than the CAN-SPAM Act.

Push notifications and text messages may subject us to potential risks, including liabilities or claims relating to consumer protection laws. For example, the Telephone Consumer Protection Act of 1991, or the TCPA, restricts telemarketing and the use of automatic SMS text messages without proper consent. The Federal Trade Commission, or the FTC, has guidelines that impose responsibilities on companies with respect to communications with consumers, such as text messages, and impose fines and liability for failure to comply with rules with respect to advertising or marketing practices it may deem misleading or deceptive. Furthermore, a number of states and countries have enacted statutes that address telemarketing through SMS text messages. Restrictions on marketing through text messages are enforced in the U.S. by the FTC, the Federal Communications Commission, state agencies and through the availability of statutory damages and class action lawsuits for violations of the TCPA or similar laws. The scope and interpretation of the laws that are or may be applicable to our use of push notifications and text messages are continuously evolving and developing. If we do not comply with these laws or regulations, are named in a lawsuit involving these laws or regulations, or if we become liable under these laws or regulations, we could be harmed, and we could be forced to implement new marketing methods, which could be costly or ineffective.

Without the ability to deliver emails, push notifications, and text messages to our users we may have limited means of maintaining contact and inducing them to use our platform. Due to the importance of email, push notifications, and text messages to our business, any disruptions or restrictions on the distribution or receipt of emails, push notifications, or text messages or increase in the associated costs could have a material adverse effect on our business and operating results.

Technologies have been developed that can block the display of our ads, which could adversely affect our financial results.

We generate substantially all of our revenue from advertising, and technologies have been developed, and will likely continue to be developed, that can block the display of our ads on our website and our mobile applications. These technologies could have had an adverse effect on our financial results and, if such technologies continue to proliferate, in particular with respect to mobile platforms, our future financial results may be harmed.

A failure in or breach of our operational or security systems or infrastructure, or those of third parties with which we do business, including as a result of cyber-attacks, could disrupt our businesses, result in the disclosure or misuse of confidential or proprietary information, damage our reputation, increase our costs and cause losses.