Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - Bison Merger Sub I, LLC | fmsa-ex991_37.htm |

| EX-95.1 - EX-95.1 - Bison Merger Sub I, LLC | fmsa-ex951_46.htm |

| EX-32.2 - EX-32.2 - Bison Merger Sub I, LLC | fmsa-ex322_39.htm |

| EX-32.1 - EX-32.1 - Bison Merger Sub I, LLC | fmsa-ex321_38.htm |

| EX-31.2 - EX-31.2 - Bison Merger Sub I, LLC | fmsa-ex312_40.htm |

| EX-31.1 - EX-31.1 - Bison Merger Sub I, LLC | fmsa-ex311_41.htm |

| EX-23.1 - EX-23.1 - Bison Merger Sub I, LLC | fmsa-ex231_42.htm |

| EX-21.1 - EX-21.1 - Bison Merger Sub I, LLC | fmsa-ex211_43.htm |

| EX-10.37 - EX-10.37 - Bison Merger Sub I, LLC | fmsa-ex1037_1106.htm |

| EX-10.31 - EX-10.31 - Bison Merger Sub I, LLC | fmsa-ex1031_1107.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

or

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-36670

FAIRMOUNT SANTROL HOLDINGS INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

34-1831554 |

|

(State or Other Jurisdiction of Incorporation or Organization) |

|

(I.R.S. Employer Identification No.) |

8834 Mayfield Road

Chesterland, Ohio 44026

(Address of Principal Executive Offices) (Zip Code)

(800) 255-7263

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(g) of the Securities Act:

|

Title of each class: |

|

Name of each exchange on which registered: |

|

Common Stock, par value $0.01 per share |

|

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Securities Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file report pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

|

Large accelerated filer |

☐ |

|

Accelerated filer |

☒ |

|

Non-accelerated filer |

☐ |

|

Smaller reporting company |

☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of common stock held by non-affiliates of the registrant computed by reference to the last sales price, $7.71 as reported on the New York Stock Exchange, of such common stock as of the closing of trading on June 30, 2016: $549,912,304

Number of shares of Common Stock outstanding, par value $0.01 per share, as of March 2, 2017: 223,863,231

DOCUMENTS INCORPORATED BY REFERENCE

|

Part III of Form 10-K |

Certain sections of the Proxy Statement for the 2017 Annual Meeting of Stockholders of Fairmount Santrol Holdings Inc. |

Fairmount Santrol Holdings Inc. and Subsidiaries

Annual Report on Form 10-K

For the Fiscal Year Ended December 31, 2016

Table of Contents

|

|

|

|

|

|

Page |

|

|

|

|

|

|

|

|

Part I |

|

|

|

|

|

|

|

Item 1 |

|

|

6 |

|

|

|

Item 1A |

|

|

14 |

|

|

|

Item 1B |

|

|

31 |

|

|

|

Item 2 |

|

|

31 |

|

|

|

Item 3 |

|

|

39 |

|

|

|

Item 4 |

|

|

43 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

Item 5 |

|

|

44 |

|

|

|

Item 6 |

|

|

46 |

|

|

|

Item 7 |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

47 |

|

|

Item 7A |

|

|

64 |

|

|

|

Item 8 |

|

|

65 |

|

|

|

Item 9 |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

102 |

|

|

Item 9A |

|

|

102 |

|

|

|

Item 9B |

|

|

102 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

Item 10 |

|

Directors, Executive Officers, and Corporate Governance |

|

|

|

|

Item 11 |

|

Executive Compensation |

|

|

|

|

Item 12 |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

|

|

|

Item 13 |

|

Certain Relationships and Related Transactions, and Director Independence |

|

|

|

|

Item 14 |

|

Principal Accounting Fees and Services |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

Item 15 |

|

|

105 |

|

|

|

Item 16 |

|

Not Applicable |

|

|

|

|

|

|

|

|

|

|

|

|

|

106 |

||

2

Introduction to Part I, Item 1A and Item 3, and Part II, Item 7

We define various terms to simplify the presentation of information in this Annual Report on Form 10-K (this “Report”). Unless we state otherwise or the context otherwise requires, the terms “we,” “us,” “our,” “Fairmount Santrol,” “our business” and “our company” refer to Fairmount Santrol Holdings Inc. and its consolidated subsidiaries and predecessor companies. We use Adjusted EBITDA herein as a non-GAAP measure of our financial performance. See further discussion of Adjusted EBITDA at Item 7 – Management’s Discussion and Analysis.

FORWARD-LOOKING STATEMENTS

This Report contains forward-looking statements that are subject to risks and uncertainties. All statements other than statements of historical fact included in this Report are forward-looking statements. Forward-looking statements give our current expectations and projections relating to our financial condition, results of operations, plans, objectives, future performance and business. You can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. These statements may include words such as “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “may,” “will,” “should,” “can have,” “likely” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events. For example, all statements we make relating to our estimated and projected costs, expenditures, cash flows, growth rates and financial results, our plans and objectives for future operations, growth or initiatives, strategies or the expected outcome or impact of pending or threatened litigation are forward-looking statements. All forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those that we expected, including:

|

|

• |

the price of oil and gas and the level of activity in the oil and gas industries; |

|

|

• |

the level of cash flows generated to provide adequate liquidity to meet our working capital needs, capital expenditures, and our lease and debt obligations; |

|

|

• |

increasing costs or a lack of dependability or availability of transportation services or infrastructure and geographic shifts in demand; |

|

|

• |

changes to leased terminal arrangements impacting our distribution network and ability to deliver our products to our customers; |

|

|

• |

actions of our competitors, including, but not limited to, their ability to increase production capacity to levels which cause an imbalance in supply and demand resulting in lower market prices; |

|

|

• |

our rights and ability to mine our properties and our renewal or receipt of the required permits and approvals from governmental authorities and other third parties; |

|

|

• |

fluctuations in demand and pricing for raw and coated sand-based proppants or the development of either effective alternative proppants or new processes to replace hydraulic fracturing; |

|

|

• |

continuing pressure on market-based pricing; |

|

|

• |

lower of cost or market inventory adjustments and/or obsolete inventory due to lower proppant demand from the oil and gas industry; |

|

|

• |

our ability to protect our intellectual property rights; |

|

|

• |

our ability to continue to commercialize Propel SSP® proppants; |

|

|

• |

our ability to succeed in competitive markets; |

|

|

• |

loss of, or reduction in, business from our largest customers; |

|

|

• |

our exposure to the credit risk of our customers and any potential material nonpayments, bankruptcies, and/or nonperformance by our customers; |

3

|

|

• |

changes in U.S. or international political or economic conditions, could adversely impact our operating results; |

|

|

• |

fluctuations in demand for industrial and recreational sand; |

|

|

• |

operating risks that are beyond our control, such as changes in the price and availability of transportation, natural gas or electricity; unusual or unexpected geological formations or pressures; cave-ins, pit wall failures or rock falls; or unanticipated ground, grade or water conditions; |

|

|

• |

our dependence on our Wedron Silica sand-mining facility for a significant portion of our sales, which currently supplies a large majority of our Northern White™ frac sand and a portion of our Industrial & Recreational Products (“I&R”) segment sand sold into our markets; |

|

|

• |

the availability of raw materials to support our manufacturing of coated proppants; |

|

|

• |

diminished access to water; |

|

|

• |

challenges to our title to our mineral properties and water rights; |

|

|

• |

our ability to make capital expenditures to maintain, develop and increase our asset base and our ability to obtain needed capital or financing on satisfactory terms, including financing for existing commitments such as future railcar deliveries; |

|

|

• |

the potential impairment of our property, including our mineral reserves, plant, equipment, goodwill, and intangible assets as a result of market conditions; |

|

|

• |

substantial indebtedness, lease and pension obligations; |

|

|

• |

restrictions imposed by our indebtedness and lease obligations on our current and future operations; |

|

|

• |

the accuracy of our estimates of our mineral reserves and our ability to mine them; |

|

|

• |

substantial costs related to mines, coating facilities, and terminals that have been closed; |

|

|

• |

potential disruption of our operations due to severe weather conditions, such as wind storms, ice storms, tornadoes, electrical storms, and floods, which occur in areas where we operate; |

|

|

• |

a shortage of skilled labor and rising labor costs in the mining industry; |

|

|

• |

increases in the prices of, or interruptions in the supply of, natural gas and electricity, or any other energy sources; |

|

|

• |

our ability to attract and retain key personnel; |

|

|

• |

our ability to maintain satisfactory labor relations; |

|

|

• |

silica-related health issues and corresponding litigation; |

|

|

• |

our ability to maintain effective quality control systems at our mining, processing and production facilities; |

|

|

• |

fluctuations in our sales and results of operations due to seasonality and other factors; |

|

|

• |

interruptions or failures in our information technology systems; |

|

|

• |

failure to comply with the provisions of the Foreign Corrupt Practices Act (“FCPA”); |

|

|

• |

the impact of a terrorist attack or armed conflict; |

|

|

• |

cybersecurity breaches; |

|

|

• |

our failure to maintain adequate internal controls; |

4

|

|

• |

extensive and evolving environmental, mining, health and safety, licensing, reclamation and other regulation (and changes in their enforcement or interpretation); |

|

|

• |

our ability to acquire, maintain or renew financial assurances related to the reclamation and restoration of mining property; and |

|

|

• |

other factors disclosed in the section entitled “Risk Factors” and elsewhere in this Report. |

We derive many of our forward-looking statements from our operating budgets and forecasts, which are based on many detailed assumptions. While we believe that our assumptions are reasonable, we caution that it is very difficult to predict the impact of known factors, and it is impossible for us to anticipate all factors that could affect our actual results. Important factors that could cause actual results to differ materially from our expectations, or cautionary statements, are disclosed under the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Report. All written and oral forward-looking statements attributable to us, or persons acting on our behalf, are expressly qualified in their entirety by these cautionary statements as well as other cautionary statements that are made from time to time in our other SEC filings and public communications. You should evaluate all forward-looking statements made in this Report in the context of these risks and uncertainties.

We caution you that the important factors referenced above may not contain all of the factors that are important to you. In addition, we cannot assure you that we will realize the results or developments we expect or anticipate or, even if substantially realized, that they will result in the consequences or affect us or our operations in the way we expect. The forward-looking statements included in this Report are made only as of the date hereof. We undertake no obligation to update or revise any forward-looking statement as a result of new information, future events or otherwise, except as otherwise required by law.

5

Our Company

Business Overview

We are one of the world’s largest providers of sand-based proppant solutions and for nearly 40 years have been a pioneer in the development of high performance proppants used by Exploration & Production (“E&P”) companies to enhance the productivity of their oil and gas wells. Additionally, for more than 120 years, we and our predecessor companies have provided high quality sand-based products, strong technical leadership and applications knowledge to end users in the I&R markets.

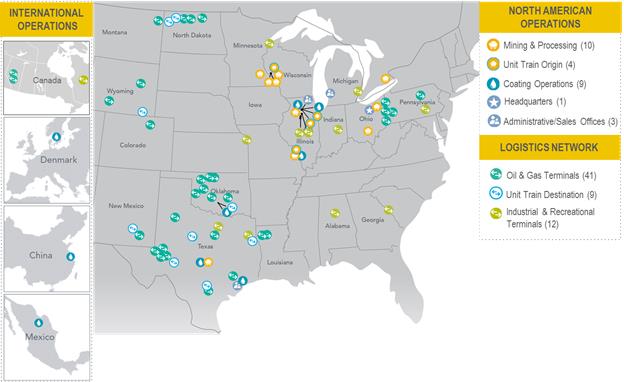

As one of the industry leaders, our asset base at December 31, 2016 included 742 million tons of proven and probable mineral reserves, which we believe is one of the largest reserve bases in the industry. Due to the conditions in the oil and gas markets, we have adjusted our operational footprint to minimize our costs and consolidate into the lowest-cost footprint possible and continue to make cost reductions. As of March 2017, we have 10 sand processing facilities (8 of which are active) with 16.8 million tons of annual sand processing capacity. We re-opened our Menomonie, Wisconsin facility at the end of the third quarter 2016 and restarted our Brewer, Missouri and Maiden Rock, Wisconsin facilities in early 2017, primarily to serve the increased demand in the proppant market. We also have 9 coating facilities (5 of which are active) with 2.3 million tons of annual coating capacity.

As one of the nation’s longest continuously operating mining organizations, we have developed a strong commitment to environmental stewardship and to the three pillars of Sustainable Development: People, Planet and Prosperity. Our strong commitment to safety is reflected in the health and safety of our employees and is illustrated by our achieving a consistently low recordable incident rate among our similarly sized industrial sand competitors as well as one of the lowest rates for all those reporting in the Industrial Mining Association of North America. Since 2011, our employees have demonstrated our commitment to our communities by donating over 76,000 hours of company-paid volunteer hours, as well as significant personal volunteer hours, into the communities in which we live and operate. We are focused on environmental stewardship, and 27 of our facilities now generate zero waste to landfills. Additionally, we executed upon annual initiatives to reduce our carbon emissions and have planted nearly 500,000 trees since 2011 in order to offset our remaining Tier I and Tier 2 emissions. We believe adhering to sustainable development principles is not only the right thing to do, but also results in a higher level of engagement and commitment from our employees, better relationships with our communities and, as a result, a stronger base from which to pursue profitable growth over the long-term. Abiding by these guiding principles, our corporate motto is “Do Good. Do Well.”

Over a period of nearly 40 years, Fairmount Santrol has built a vertically integrated operation that combines mining, sand processing, resin manufacturing and coating operations with a broad logistics network and state-of-the-art research and development capabilities. Our ability to integrate and leverage our asset base to provide comprehensive proppant solutions has allowed us to become a long-term, trusted partner to our customers.

We are capable of Class I railroad deliveries to each of North America’s major oil and gas producing basins and also have the flexibility to ship our product via barge, marine terminals and trucks to reach our customers as needed. We operate an integrated logistics platform consisting of 41 proppant distribution terminals and a fleet of approximately 10,000 railcars, which includes 1,195 customer railcars, considering car returns that took place throughout the year and subleases. Our unit train capabilities include four production facilities and nine in-basin terminals, which reduce freight costs and improve cycle times for our railcar fleet. In order to better align our logistics network with customer demand and to reduce costs, we discontinued activity at five transloading terminals in 2016.

Our operations are organized into two segments based on the primary end markets we serve: (i) Proppant Solutions and (ii) Industrial & Recreational Products. Our Proppant Solutions segment predominantly provides sand-based proppants for use in hydraulic fracturing operations throughout the U.S. and Canada, Argentina, Mexico, China, northern Europe and the United Arab Emirates. Our I&R segment provides raw, coated, and custom blended sands to the foundry, building products, glass, turf and landscape and filtration industries primarily in North America. We believe our two market segments are complementary. Our ability to sell to a wide range of customers across

6

multiple end markets allows us to maximize the recovery of our reserve base within our mining operations and to reduce the cyclicality of our earnings.

In 2016, our Proppant Solutions segment sold 6.4 million tons of proppant with revenues of $416.1 million (78% of total company revenues) and gross profit of $26.5 million. This represents an increase of 3%, a decrease of 41%, and a decrease of 85%, respectively, from 2015. Proppants represented approximately 86% and 91% of total company revenues for 2015 and 2014, respectively. For 2016, our I&R segment had sales volume of 2.5 million tons with revenues of $118.9 million and gross profit of $48.8 million, which represents increases of 9% on volume and gross profit, respectively, from 2015. Revenues were relatively flat to 2015.

Corporate History

We were incorporated as a Delaware corporation in 1986. Our predecessor companies began operations over 120 years ago. On October 3, 2014, we completed an Initial Public Offering. We are listed under the ticker symbol “FMSA” on the New York Stock Exchange.

Our corporate headquarters is located at 8834 Mayfield Road, Chesterland, Ohio 44026. Our telephone number is (800) 255-7263. Our company website is www.fairmountsantrol.com. We make available free of charge our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports as soon as reasonably practicable after we file or furnish such reports to the Securities and Exchange Commission (the “SEC”). The information on our website is not incorporated by reference in or considered to be a part of this Annual Report on Form 10-K.

INDUSTRY

Overview

The silica sand industry consists of businesses that are involved in the mining, processing, and sale of silica sand and silica sand-based products. Monocrystalline silica, also referred to as “silica,” “industrial sand and gravel,” “silica sand,” and “quartz sand,” is a term applied to sands and gravels containing a high percentage of silica (also known as silicon dioxide or SiO2) in the form of quartz.

The low relative cost and special properties of monocrystalline silica — chemistry, purity, grain size, color, inertness, hardness, and resistance to high temperatures — make it critical to a variety of industries and end-use markets, including the production of molds and cores for metal castings, glass production, and the manufacturing of building products. In particular, monocrystalline silica is a key input in the hydraulic fracturing techniques used in the development of oil and gas resource basins.

Frac Sand Extraction, Processing, and Distribution

Raw frac sand is a naturally occurring mineral that is mined and processed. While the specific extraction method utilized depends primarily on the geologic conditions, most raw frac sand is mined using conventional open-pit extraction methods. The composition, depth, and chemical purity of the sand also dictate the processing method and equipment utilized. After extraction, raw frac sand is washed with water to remove fine impurities such as clay and organic particles, with additional procedures used when contaminants are not easily removable. The final steps in the production process involve the drying and screening of the raw frac sand according to mesh size.

Most frac sand is shipped in bulk from the processing facility to customers by truck, rail or barge. Because transportation costs may represent a significant portion of the overall delivered product cost, shipping in large quantities, particularly when shipping over long distances, provides a significant cost advantage to the suppliers, which highlights the importance of rail or barge access for low cost delivery. As a result, facility location and logistics capabilities are an important consideration for suppliers and customers. In addition, we believe that, over time, the largest proppant customers would prefer to consolidate their purchases across a smaller group of suppliers with robust logistics capabilities and a broad offering of high performance proppants.

7

Advances in oil and gas extraction techniques, such as horizontal drilling and hydraulic fracturing, have allowed for significantly greater extraction of oil and gas trapped within shale formations. The hydraulic fracturing process consists of pumping fluids down a well at pressures sufficient to create fractures in the targeted hydrocarbon-bearing rock formation in order to increase the flow rate of hydrocarbons from the well. A granular material, called proppant, is suspended and transported in the fluid and fills the fracture, “propping” it open once high-pressure pumping stops. The proppant-filled fracture creates a conductive channel through which the hydrocarbons can flow more freely from the formation into the wellbore and then to the surface. Proppants therefore perform the vital function of promoting the flow, or conductivity, of hydrocarbons over a well’s productive life. In fracturing a well, operators select a proppant that is transportable into the fracture, is compatible with frac and wellbore fluids, permits acceptable cleanup of frac fluids and can resist proppant flowback. In addition, the proppant must be resistant to crushing under the earth’s closure stress and reservoir temperature.

There are three primary types of proppant that are utilized in the hydraulic fracturing process: raw frac sand, coated sand and manufactured ceramic beads. Customers choose among these proppant types based on the geology of the reservoir, expected well pressures, proppant flowback concerns, and product cost. Given the price differences between the various proppant products and well-specific considerations, E&P companies are continually evaluating the optimal mix of lower-cost, lower-conductivity frac sand and higher-cost, higher-conductivity coated sand and ceramics in order to best address the geology of the well and to maximize well productivity and economic returns.

Proppant Industry Demand Trends

Over the past decade, E&P companies increasingly focused on exploiting the vast hydrocarbon reserves contained in North America’s oil and gas reservoirs. Using advanced techniques, such as horizontal drilling and hydraulic fracturing, North American production of oil and gas has grown rapidly as the development of horizontal drilling technologies has evolved. More recently, E&P companies increased their focus on optimizing the use of proppant as a critical component of these efforts to improve well productivity and maximize their returns on invested capital.

This focus on efficiency and profitability led to new development techniques, such as increased use of pad drilling which resulted in a greater number of wells drilled per rig, and incorporated longer lateral lengths and shorter intervals between frac stages, which resulted in more fracturing stages per well. In addition, the amount of proppant used per stage increased dramatically, compounding the increase in total demand for proppant.

As a result of these trends, North American demand for all proppants increased rapidly over the past ten years. This growth was fueled by the continued increase in both wells drilled and proppant used per well. Individual wells were being completed with as much as 20,000 tons of proppant, or 60 to 100 railcars. This represented a significant increase in the usage of proppant per well over just a few years ago and was driven by improved recovery rates for E&P companies at higher levels of proppant intensity.

Starting in the fourth quarter of 2014 and continuing into mid-2016, the growth rate of global oil supply outpaced that of oil demand. As a result, various operators have cut back on drilling and capital programs, resulting in significantly reduced rig counts. According to Baker Hughes rig count data, United States horizontal land rig counts have fallen from an average of 730 rigs throughout 2015 to an average of 400 rigs in 2016. During 2016, horizontal land rigs in the United States ranged from a low point of 310 rigs in the second quarter to over 530 by the end of the year. This volatility and cyclicality in horizontal rig counts has resulted in market uncertainty and reduced drilling activity and demand for proppants throughout the year. Further, since 2014, average crude oil prices have dropped over $50 per barrel causing E&P companies to seek ways to reduce operating costs, which has further reduced demand for our value-added products such as coated proppants. We believe that the completion of wells that have been drilled and increased proppant usage per well will continue to help partially offset reduced demand for proppants from lower drilling activity in 2016 and beyond. Towards the end of 2016 into early 2017, the price of oil has stabilized and the United States horizontal land rig counts have increased showing potential signs of market stabilization.

8

Proppant Industry Supply Trends

To keep pace with rapidly growing demand, the available supply of proppant increased in 2014 through new entrants and capacity expansions of existing suppliers. Due to the industry factors noted above, there continued to be downward pressure on the selling price of proppants, as well as the closing or idling of industry capacity in 2015 into early 2016. This trend began to reverse in the second half of 2016, where demand and pricing of proppants has begun a gradual recovery and customers are beginning to focus on long-term availability of proppant supply. The effectiveness of additional market supply also will be impacted by the suppliers’ ability to deliver product cost effectively where customers want it. Certain basins, such as the Permian in West Texas and New Mexico, have been particularly active and suppliers of proppant are actively attempting to provide lower-cost sources of supply that can be efficiently delivered to these areas.

Our Proppant Products

We offer proppant products in each of the most common API-specified proppant categories, which we believe address a vast majority of the proppant market. All revenues in our Proppant Solutions segment are derived from these products in each of 2016, 2015, and 2014.

Northern White Frac Sand. Our Northern White frac sand is mined from deposits located in our Illinois, Wisconsin, Missouri, and Minnesota facilities. These reserves are generally characterized by high purity, significant roundness and sphericity, and low turbidity. All of our Northern White raw sand proppant products meet the standards set by the API.

API-Spec Brown Frac Sand. Our API-spec brown sand reserves are located in Texas and marketed under the name Texas Gold® frac sand. Our Texas Gold® frac sand has lower crush resistance than our Northern White frac sand, but it is an effective solution for low pressure wells. These reserves are in close proximity to major oil and gas producing basins in Texas, including the Eagle Ford Shale and the Permian Basin, which provides them with a significant transportation cost advantage relative to API-spec frac sand sourced from more distant locations.

Coated Proppant. We coat a portion of our API-spec produced sand with resin to enhance its performance as a proppant using proprietary resin formulations and coating technologies. Our coated proppants are generally used in higher temperature and higher pressure well environments and are marketed to end users who require increased conductivity in higher pressure wells, high crush resistance, and/or enhanced flow back control in order to enhance the productivity of their wells.

Our coated sand products are sold as both tempered (or pre-cured) and curable (or bonding) products. Curable coated sand bonds down hole as the formation heat causes neighboring coated sand grains to polymerize with one another locking proppant into place. This prevents proppant from flowing back out of the fracture when the oil or natural gas well commences production. For certain resin products, the resin’s chemical properties are triggered by the introduction of an activator into the frac fluid. We formulate, manufacture, and sell activators, which work with the specific chemistry of our resins. Tempered products do not require activation because they are not intended to bond, rather bring additional strength to the proppant.

We manufacture proprietary coatings designed to address the evolving needs of our customers, and have continued to invest in our research and development and technical marketing capabilities to maximize the sales of our coated products. We also coat ceramic product purchased from third-party suppliers. This product is marketed as HyperProp® proppants and has the strength characteristics of ceramic and the flowback performance characteristics of coated sand.

Proprietary Performance Products

Propel SSP®. Our patented Propel SSP® product utilizes a polymer coating applied to a proppant substrate. Upon contact with water, the coating hydrates and swells rapidly to create a hydrogel around the proppant substrate. The hydrogel layer, which is primarily water, is attached to the proppant particle and provides a nearly threefold increase in the hydrostatic radius of the proppant. Test results indicate that the lower specific gravity allows greater volumes of proppant and/or coarser mesh sizes coated with the Propel SSP® product to be carried deep into the fracture,

9

which in turn allow more hydrocarbons to escape into the wellbore. As a result, field trials have shown a variety of benefits, including increased production, decreased use of fluids, and reduced pumping time.

Our Product Delivery

We have established an oil and gas logistics network that we believe is highly responsive to our customers’ needs. One of the most important purchasing criteria of our proppant customers is our ability to deliver the products our customers demand at their desired time and location. We believe we have one of the industry’s largest distribution footprints with 41 active oil and gas distribution terminals. We also have a railcar fleet of approximately 10,000 railcars as of December 31, 2016, providing us the flexibility for delivering product to our locations in-basin when customers require it. We believe we are one of the few proppant producers capable of Class I railroad deliveries to each of North America’s major oil and gas-producing basins. In 2016, we shipped approximately 75% of our North American proppant volume through our terminal network.

The ability to ship proppant through unit trains (a train in which all cars carry the same commodity and are not split up or stored en route) is becoming increasingly important in order to cost-effectively provide the large quantities of product required by evolving well completion methods. We have unit train capabilities at four of our production facilities and nine of our destination terminals and shipped over 330 unit trains of product in 2016. The production unit train capability allows our customers that prefer to purchase the product FOB plant to efficiently ship the proppant to their own facilities.

By the end of the third quarter of 2016, we completed negotiations with certain railcar lessors and paid approximately $9.8 million in fees that resulted in reductions to current railcar operating lease payments, in some cases in exchange for consideration including an extension of the lease terms. In addition, railcar purchase commitments in 2017 and 2018 approximating $49.5 million were cancelled and $136.5 million of purchase commitments were deferred. Please see further detail in Note 18 of our consolidated financial statements in the Annual Report on Form 10-K.

I&R Industry Trends

Demand in the I&R end markets is relatively stable and is primarily influenced by key macroeconomic drivers such as housing starts, light vehicle sales, repair and remodel activity, and industrial production. The economic downturn beginning in 2008 decreased demand in the foundry, building products, and glassmaking end markets, however, the recent economic recovery has significantly increased demand in these same end markets. The primary end markets served by our I&R segment are foundry, building products, sports and recreation, glassmaking, and filtration. All revenues in our I&R segment are derived from the following products in each of 2016, 2015, and 2014.

Our I&R Products

Foundry. We currently supply the foundry industry with multiple grades of high purity, round, angular, and sub-angular sands for molding and core-making applications, with products sold primarily in the U.S., Canada, Mexico, Japan, and China. Foundry sands are characterized by high purity, round and sub-angular sands precisely screened to perform under a variety of metal casting conditions. These factors dictate the refractory level and physical characteristics of the mold and core, which have a significant effect on the quality of the castings produced in the foundry. Our resin binders provide the necessary bonding of molds and cores in casting applications and are designed to improve overall productivity and environment conditions in the workplace.

Our extensive production experience and technical knowledge of the foundry industry have driven several industry advances. For example, we have developed our Signature Series™ of low smoke, low odor coated sands that provide lower overall emissions while providing a safer and more favorable work environment. Our expertise with coated sands enables us to provide coated sand for molds and cores where exceptional dimensional accuracy and surface finish are required. An example is TruCoat™, which has been engineered to dramatically lower in-plant smoke, odor, and emissions as well as deliver superior performance making TruCoat™ one of the most environmentally sound products on the market.

10

We believe we were the first sand operator to blend sands, which has proven extremely successful for specialty iron and aluminum applications. As foundries continue to utilize higher cost binders to improve the quality of their castings, minimize the use of binders which also reduces overall environmental impact, the industry continues to demand higher quality sands to realize the value of these binders. Our chemists and technicians support these applications with customized products that minimize binder usage, resulting in lower costs to foundries and higher prices for our products.

Glass. We provide a wide variety of high purity, low iron silica sands to the glass market. The glass industry uses industrial sand consumption for the production of windows, electronic display screens, photovoltaic panels, glass bottles, and other glass products.

Building Products. Various grades and types of our sands are used for roofing shingles, asphalt, industrial flooring ballast sand, bridge decking, pipe lining, and tank underlayment. We also work with our customers to blend minerals and chemicals to create colored flooring aggregates, concrete countertops, grout and plaster.

Sports and Recreation. We are a leading supplier of various turf and landscape infill products to contractors, municipalities, nurseries, and mass merchandisers. Our turf-related products are used in multiple major sporting venues, including First Energy Stadium and Progressive Field in Cleveland, Ohio, PNC Park in Pittsburgh, Pennsylvania, and Notre Dame Stadium in Notre Dame, Indiana. In addition, we are a significant supplier of bunker sand, top dressing sands, and all-purpose sands to golf courses and landscape contractors throughout North America. Our sands are also supplied to horse tracks and training facilities. We also provide colored sand to a variety of major retailers for use as play sand and arts and crafts.

Filtration. We provide high-quality industrial sands and gravels in a wide variety of water and wastewater filtration applications. Over the past several years, we increased our focus on the filtration market. Our full range of products are monitored with an active statistical process control program to ensure compliance with all government and customer specifications, including the American Water Works and National Sanitation Foundation standards. Due to our efforts, we have emerged as a leader in sand and gravel products for private, public, and institutional water filtration systems.

Raw Materials

Our products are dependent on the availability of certain raw materials, including natural gas or propane, resins and additives, bagging supplies, and other raw materials. These are readily available from a variety of sources and we are not dependent on any one supplier of raw materials.

Our Customers

Since our inception, we have remained focused on developing and sustaining a loyal, diversified customer base. Currently, we maintain long-term contracts with many of the largest North American oilfield service companies. We believe the strength of our customer base is driven by our collaborative approach to product innovation and development, reputation for high-quality products, and extensive logistics network. Certain of our top customer relationships date back over 30 years. We have approximately 75 customers for our oil and gas proppants and over 830 customers across all our end markets. For the years ended December 31, 2016 and 2015, our top two customers, Halliburton and FTSI, collectively, accounted for approximately 42% and 43%, respectively, of our total sales revenues.

We primarily sell products under supply agreements with terms that vary by contract. Certain of the agreements require the customer to purchase a specified percentage of its proppant requirements from us. Other agreements require the customer to purchase a minimum volume of proppant from us. These minimum volume contracts typically include a “take-or-pay” or “take-or-penalty” provision which triggers certain penalties if the purchased volume does not meet the required minimums. Specific custom orders are generally filled upon request, and backlog is not a material factor.

11

Research and Development and Technical Innovation

We have a history of partnering with our customers to develop innovative solutions to enhance the effectiveness of well completions, from conventional shallow wells to the most complex, multi-stage, horizontal wells. The nature of our vertically integrated model allows us to participate in each phase of proppant manufacturing and delivery and provides us a unique perspective into the current and future needs of our customers. Our technical sales team works closely with market participants to demonstrate the value proposition our proppants offer and stimulate market demand using data indicating enhanced hydrocarbon recoveries.

The table below summarizes some of our most significant product innovations:

|

Innovation |

|

Year |

|

Result |

|

Propel SSP® 350 Products |

|

2016 |

|

Accomplishes the same results as the original SSP technology when faced with brackish, sea, or produced water |

|

CoolSet® Proppants |

|

2014 |

|

Eliminates need for an activator for well temperatures as low as 100°F |

|

TrueSet™ Proppants |

|

2016 |

|

Provides effective flowback control and enhanced production, ideal for downhole temperatures between 150-300°F, does not require an activator, compatible with standard frac fluids and break technologies |

|

PowerProp® Proppants |

|

2010 |

|

Technology that delivers strength and performance characteristics similar to a light-weight ceramic (patent-pending) |

|

Bio-based Binder System |

|

2010 |

|

Technology for use in metal casting industry (patent-pending) |

|

Bio-Balls® Ball Sealers |

|

2006 |

|

Water soluble ball sealers that are environmentally safe and do not require retrieval after treatment |

|

Encapsulated Curable Proppant |

|

1997 |

|

High performance coated proppant used in flow-back control |

|

Dual Coat Technology |

|

1995 |

|

Dual coat curable coated sand for enhanced conductivity and flowback control |

During 2016, 2015, and 2014, we spent $3 million, $5 million, and $6 million, respectively, on research and development.

Propel SSP® products continue to undergo extensive field trials with key customers with successful results (increased productivity and reduced operating costs). Propel SSP® products rely on a hydrogel polymer coating attached to a proppant substrate. When mixed with water, the coating hydrates and swells rapidly to create a hydrogel around the proppant substrate, which provides a nearly threefold increase in the hydrostatic radius of the proppant. Lab results show that the lower specific gravity, while maintaining crush strength, allows greater volumes of proppant and/or coarser mesh sizes coated with Propel SSP® products to be carried deep into the fractures, in turn allowing more hydrocarbons to flow into the wellbore. This technology reduces or eliminates the need for certain frac fluid additives, including friction reducer, guar gum, and crosslinkers, which are used to enhance the transport of proppants into the geologic formation. Extensive field tests have shown the benefits of Propel SSP® products, including increased initial production, reduced fluid usage, and reduced pumping time. Propel SSP® 350 products can now accomplish the same results in hard water.

Competition

There are numerous large and small producers in all sand producing regions of the United States with whom we compete. Our main competitors in the raw frac sand market include Badger Mining Corporation, CARBO Ceramics, Inc., Emerge Energy Services LP, Hi-Crush Partners LP, Preferred Sands LLC, Smart Sand Inc., Unimin Corporation, and U.S. Silica Holdings, Inc. Many new entrants to the raw frac sand market compete on an FOB-plant basis and lack comparable transportation infrastructure to meet customer demands in-basin. Our main competitors in the coated products market include Atlas Resin Proppants LLC, CARBO Ceramics, Momentive Performance Materials Inc., Unimin Corporation, Preferred Sands LLC, and U.S. Silica Holdings, Inc. The most important factors on which we compete in both markets are product quality, performance, sand and proppant characteristics, transportation capabilities, proximity of supply to well site, reliability of supply, and price. Our largest competitors across both markets are U.S. Silica Holdings, Inc., Unimin Corporation, and Badger Mining

12

Corporation (which owns Atlas Resin Proppants LLC). We believe we are uniquely positioned to utilize our scale of raw sand production to supply high-quality substrate for coated products and leverage our transportation infrastructure for reliable delivery in-basin.

Due to increased demand for sand based proppants in the years leading up to the end of 2014, there had been an increase in the number of frac sand producers. Moreover, as a result of this increased demand, existing frac sand producers have added to or expanded their frac sand production capacity, thereby increasing competition. Demand for sand-based proppants is closely linked to proppant consumption patterns for the completion of oil and natural gas wells in North America. These consumption patterns in a particular basin are influenced by numerous factors, including the price of hydrocarbons, the drilling rig count, and hydraulic fracturing activity levels, including the number of stages completed and the amount of proppant used per stage. Further, these consumption patterns are also influenced by the location, quality, selling price and availability of sand-based proppants and other types of proppants such as ceramic proppant. Selling prices for sand-based proppants vary by basin and are determined based on supply and demand dynamics within each basin.

As a result of increasing global supply of oil, the demand for proppant has decreased since the end of 2014 and through 2016, resulting in proppant oversupply and downward pressure on proppant selling prices. This caused some proppant producers to exit the market and others, including us, to adjust operations and minimize costs. Towards the end of 2016 into early 2017, the price of oil has stabilized and the United States horizontal land rig counts have increased showing potential signs of market stabilization.

Competitors in the I&R markets include some of our larger proppant competitors such as Unimin Corporation and U.S. Silica Holdings, Inc. but also typically include smaller, local or regional producers of sand and gravel.

Employees

As of December 31, 2016, we employed a workforce of 744 employees. We believe our culture of “People, Planet and Prosperity” has enabled us to achieve a long-tenured workforce and good relations with our workforce.

We maintain an active dialogue with employees and provide salaried and hourly employees a comprehensive benefits package including medical, life, and accident insurance, incentive bonus programs, a 401(k) plan with an employer match and discretionary employer contribution, as well as educational assistance. Certain employees are also eligible for stock-based compensation programs that are designed to encourage long-term performance aligned with Company objectives.

As of December 31, 2016, approximately 138 of our domestic employees are parties to collective bargaining contracts. We believe we have strong relationships with and maintain an active dialogue with union representatives. We have historically been able to successfully extend and renegotiate collective bargaining agreements as they expire.

Seasonality

Our business is affected to some extent by seasonal fluctuations in weather that impact our production levels and our customers’ business needs. For example, our proppant sales levels are lower in the first and fourth quarters due to lower market demand as adverse weather tends to slow oil and gas operations to varying degrees depending on the severity of the weather. Our inability to mine and process frac sand year round at our surface mines in northern states results in a seasonal build-up of inventory as we excavate excess sand to build a stockpile that will feed our drying facilities during the winter months. Additionally, in the second and third quarters, we sell more sand to our customers in the I&R end markets due to the seasonal rise in demand driven by more favorable weather conditions.

Intellectual Property

Our intellectual property consists primarily of patents, trade secrets, know-how, trademarks, including our name Fairmount Santrol™ and products, including, but not limited to PowerProp®, Propel SSP®, HyperProp®, and CoolSet®. We hold numerous U.S. and foreign-granted patents that are still in force as well as many U.S. and

13

foreign patent applications that are still pending. We own patents in most of our major, differentiated proppant product lines. We have not granted any third-party rights with respect to our patents. The majority of our patents have an expiration date after 2025. In early 2016, we received a patent on certain of the Propel SSP® proppant technology and have additional patents pending. With respect to trade secrets and know-how, our extensive experience with a variety of different products enables us to offer our customers a wide range of proppants for their particular application.

An investment in our securities involves significant risks. You should carefully consider the risks described below, together with the financial and other information contained in this Report, as well as the information discussed under the section entitled, “Management's Discussion and Analysis of Financial Conditions and Results of Operations” in evaluating us, our business and your investment in us. If any of the following risks actually occurs, our business, financial condition, results of operations, cash flows, and prospects could be materially and adversely affected. As a result, the trading price of our common stock could decline and you could lose all or part of your investment in our common stock.

Risks Related to Our Business

Our business and financial performance depend on the level of activity in the oil and gas industries.

Approximately 78% of our revenues for the year ended December 31, 2016 were derived from sales to companies in the oil and gas industry. As a result, our operations are materially dependent on the levels of activity in oil and gas exploration, development, and production. More specifically, the demand for the proppants we produce is closely related to the number of oil and gas wells completed in geological formations where sand-based proppants are used in fracturing activities. These activity levels are affected by both short- and long-term trends in oil and gas prices, among other factors.

In recent years, oil and gas prices and, therefore, the level of exploration, development, and production activity, have experienced significant fluctuations. Worldwide economic, political, and military events, including war, terrorist activity, events in the Middle East, and initiatives by the Organization of the Petroleum Exporting Countries (“OPEC”) and other large non-OPEC producers have contributed, and are likely to continue to contribute, to price and volume volatility. In 2016, OPEC producers reached an agreement to limit production through May 2017, which contributed to an increase in global oil and gas prices. However, this limit is voluntary and political and other issues may create varying degrees of adherence to this limitation, which could cause volatility and price fluctuations in the demand for oil and gas.

Despite the pricing rebound in the latter half of 2016, prices were still not at sustainable levels and remain subject to volatility. A return to a reduction in oil and gas prices would generally depress the level of oil and gas exploration, development, production, and well completion activity and may result in a corresponding decline in the demand for the proppants we produce. Such a decline would have a material adverse effect on our business, results of operations, and financial condition, and we may not be able to meet our debt obligations. The commercial development of economically-viable alternative energy sources could have a similar effect. In addition, certain U.S. federal income tax deductions currently available with respect to oil and gas exploration and development, including the repeal of the percentage depletion allowance for oil and gas properties, may be eliminated as a result of proposed legislation. Any future decreases in the rate at which oil and gas reserves are discovered or developed, whether due to the passage of legislation, increased governmental regulation leading to limitations, or prohibitions on exploration and drilling activity, including hydraulic fracturing, or other factors, could have a material adverse effect on our business and financial condition, even in a stronger oil and natural gas price environment.

Our substantial indebtedness could adversely affect our financial flexibility and our competitive position.

Although our indebtedness has been significantly reduced in 2016, it continues to be substantial and increases the risk that we may be unable to generate cash sufficient to pay amounts due in respect of our indebtedness, or refinance that indebtedness on favorable terms. As of December 31, 2016, we had approximately $843.0 million of

14

outstanding long-term debt due in September 2019. Our indebtedness could have other important consequences and significant effects on our business. For example, it could:

|

|

• |

increase our vulnerability to adverse changes in general economic, industry and competitive conditions; |

|

|

• |

require us to dedicate a substantial portion of our cash flow from operations to make payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures and other general corporate purposes; |

|

|

• |

limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

|

|

• |

restrict us from exploiting business opportunities; |

|

|

• |

make it more difficult to satisfy our financial obligations, including payments on our indebtedness; |

|

|

• |

place us at a disadvantage compared to our competitors that have less debt; and |

|

|

• |

limit our ability to borrow additional funds for working capital, capital expenditures, railcar or other future purchase commitments, acquisitions, debt service requirements, execution of our business strategy, or other general corporate purposes. |

Increasing logistics costs, a lack of dependability or availability of transportation services or infrastructure, and geographic shifts in demand could have a material adverse effect on our business.

Transportation and handling costs are a significant component of the total delivered cost of our products. In many instances, transportation costs can represent 70% to 80% of the delivered cost of frac sand. The high relative cost of transportation could favor suppliers located in close proximity to the customer. In addition, as we continue to expand our sand-based proppant production, we will need increased investment in transportation infrastructure, including terminals and railcars. We contract with truck, rail, ship, and barge services to move sand-based proppants from our production facilities to distribution terminals. Labor disputes, derailments, adverse weather conditions or other environmental events, increased railcar congestion, and other changes to rail freight systems could interrupt or limit available transportation services or result in a significant increase in transportation service rates. Increased costs resulting from these types of events that we are not able to pass on to our customers could impair our ability to deliver our products economically to our customers or to expand our markets. Accordingly, because we are so dependent on rail infrastructure, if there are disruptions of the rail transportation services utilized by us or our customers, and we or our customers are unable to find alternative transportation providers to transport our products, our business and results of operations could be adversely affected. Further, declining volumes could result in additional railcar over-capacity, which would lead to railcar storage fees while, at the same time, we would continue to incur lease costs for those railcars in storage.

A portion of our distribution infrastructure is located in or near oil and gas producing areas. A shift in demand away from areas where we have significant distribution infrastructure or relocation of our customers’ businesses to areas farther from our plants or distribution infrastructure could have a material adverse effect on our business, financial condition, and results of operations.

Our operations are dependent on timely securing and maintaining various permits and approvals from governmental authorities and other third parties.

We hold numerous governmental, environmental, mining and other permits, water rights and approvals authorizing operations at each of our facilities. A decision by a governmental agency or other third party to deny or delay issuing a new or renewed permit or approval, or to revoke or substantially modify an existing permit or approval, could have a material adverse effect on our ability to continue operations at the affected facility. Furthermore, state and local governments could impose a moratorium on mining operations in certain areas. Expansion of our existing operations is also predicated on securing the necessary environmental or other permits, including air permits for our coated manufacturing, and water rights or approvals, which we may not receive in a timely manner or at all. In addition, our facilities are located near existing and proposed third-party industrial operations that could affect our ability to fully extract, or the manner in which we extract, the mineral reserves to which we have mining rights.

15

We may be adversely affected by decreased or shifted demand for sand-based proppants or the development of either effective alternative proppants or new processes to replace hydraulic fracturing.

Frac sand and coated sand are proppants used in the completion and re-completion of oil and gas wells through the process of hydraulic fracturing. A significant shift in demand from sand-based proppants to other proppants, or a shift in demand from higher-margin sand-based proppants to lower-margin sand-based proppants, could have a material adverse effect on our business, financial condition, and results of operations. The development and use of new technology for effective alternative proppants, or the development of new processes to replace hydraulic fracturing altogether, could also cause a decline in demand for the sand-based proppants we produce and could have a material adverse effect on our business, financial condition, and results of operations.

Our proppant sales are subject to fluctuations in market pricing.

Substantially all of our supply agreements involving the sale of sand-based proppants have market-based pricing mechanisms. Accordingly, in periods with decreasing prices, our results of operations may be lower than if our agreements had fixed prices. In periods with increasing prices, our agreements permit us to increase prices; however, our customers may elect to cease purchasing our sand-based proppants if they do not agree with our price increases or are able to find alternative, cheaper sources of supply. Furthermore, certain volume-based supply agreements may influence the ability to fully capture current market pricings. These pricing provisions may result in significant variability in our results of operations and cash flows from period to period.

Changes in supply and demand dynamics could also impact market pricing for proppants. A number of existing frac sand providers and new market entrants have recently announced reserve acquisitions, processing capacity expansions and greenfield projects. In periods where sources of supply of raw frac sand exceed market demand, market prices for frac sand may decline and our results of operations and cash flows may continue to decline, be volatile, or otherwise be adversely affected.

We may not be able to complete greenfield development or expansion projects or, if we do, we may not realize the expected benefits.

Any greenfield development or expansion project requires us to spend substantial capital and obtain numerous state and local permits. A decision by any governmental agency not to issue a required permit or substantial delays in the permitting process could prevent us from pursuing the development or expansion project. In addition, if the demand for our products declines during the period we experience delays in raising capital or completing the permitting process, we may not realize the expected benefits from our greenfield facility or expansion project. Furthermore, our new or modified facilities may not operate at designed capacity or may cost more to operate than we expect. The inability to complete greenfield development or expansion projects or to complete them on a timely basis and in turn grow our business could adversely affect our business and results of operations.

We rely upon trade secrets, contractual restrictions and patents to protect our proprietary rights. Failure to protect our intellectual property rights may undermine our competitive position, and protecting our rights or defending against third-party allegations of infringement may be costly.

Our commercial success depends on our proprietary information and technologies, know-how and other intellectual property. Because of the technical nature of our business, we rely on patents, trade secrets, trademarks, and contractual restrictions to protect our intellectual property rights, particularly with respect to our coated products. The measures we take to protect our trade secrets and other intellectual property rights may be insufficient. Failure to protect, monitor, and control the use of our existing intellectual property rights could cause us to lose our competitive advantage and incur significant expenses. It is possible that our competitors or others could independently develop the same or similar technologies or otherwise obtain access to our unpatented technologies. In such case, our trade secrets would not prevent third parties from competing with us. As a result, our results of operations may be adversely affected. Furthermore, third parties or our employees may infringe or misappropriate our proprietary technologies or other intellectual property rights, which could also harm our business and results of operations. Policing unauthorized use of intellectual property rights can be difficult and expensive, and adequate remedies may not be available.

16

In addition, third parties may claim that our products infringe or otherwise violate their patents or other proprietary rights and seek corresponding damages or injunctive relief. Defending ourselves against such claims, with or without merit, could be time-consuming and result in costly litigation. An adverse outcome in any such litigation could subject us to significant liability to third parties (potentially including treble damages) or temporary or permanent injunctions prohibiting the manufacture or sale of our products, the use of our technologies or the conduct of our business. Any adverse outcome could also require us to seek licenses from third parties (which may not be available on acceptable terms, or at all) or to make substantial one-time or ongoing royalty payments. Protracted litigation could also result in our customers or potential customers deferring or limiting their purchase or use of our products until resolution of such litigation. In addition, we may not have insurance coverage in connection with such litigation and may have to bear all costs arising from any such litigation to the extent we are unable to recover them from other parties. Any of these outcomes could have a material adverse effect on our business, financial condition and results of operations.

The development and marketing of Propel SSP® products may prove to be unsuccessful.

The technology supporting Propel SSP® products is still being proven through field trials. Although the results of field trials have been encouraging, and one customer in particular is using Propel SSP® products on a commercial basis in all of its wells, additional testing ultimately may demonstrate that the product is ineffective or not commercially viable. A return to or a prolonged decline in the oil and gas market may make the adoption of higher-value products, such as Propel SSP® products, more difficult. Additionally, competitive products could be developed and marketed. A failure to capitalize on Propel SSP® products in commercial application would result in a significant unrecouped investment and the failure to realize certain anticipated benefits, each of which could have a material adverse effect on our business, financial condition, and results of operations. For more information on Propel SSP® products, please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Acquisitions.”

Our future performance will depend on our ability to succeed in competitive markets, and on our ability to appropriately react to potential fluctuations in demand for and supply of sand-based proppants.

We operate in a highly competitive market that is characterized by several large, national producers and a larger number of small, regional or local producers. Competition in the industry is based on price, consistency and quality of product, site location, distribution capability, customer service, reliability of supply, breadth of product offering, and technical support. In the proppant business, we compete with producers such as Badger Mining Corporation, CARBO Ceramics Inc., Emerge Energy Services LP, Hi-Crush Partners, LP, Momentive Performance Materials Inc., Preferred Sands LLC, Smart Sand Inc., Unimin Corporation, and U.S. Silica Holdings, Inc. Certain of our large competitors may have greater financial and other resources than we do, may develop technology superior to ours or may have production facilities that are located closer to key customers than ours.

We also compete with smaller, regional or local producers. In recent years there has been an increase in the number of small producers servicing the sand-based proppants market which could result in increased competition and pricing pressure in certain market conditions. In addition, oil and gas exploration and production companies and other providers of hydraulic fracturing services could acquire their own sand reserves, expand their existing sand-based proppant production capacity or otherwise fulfill their own proppant requirements and existing or new sand-based proppant producers could add to or expand their sand-based proppants production capacity, which could increase competition in the proppant industry. We may not be able to compete successfully against either our larger or smaller competitors in the future, and competition could have a material adverse effect on our business, financial condition and results of operations.

A large portion of our sales is generated by a limited number of customers, and the loss of, or a significant reduction in purchases by, our largest customers could adversely affect our operations.

For the year ended December 31, 2016 and 2015, our top two proppant customers, Halliburton and FTSI, collectively accounted for approximately 42% and 43% of our sales, respectively. These customers may not continue to purchase the same levels of our sand-based proppants in the future due to a variety of reasons. Over the course of our relationships, we have sold proppant to Halliburton and FTSI on a purchase order basis and pursuant to supply agreements. We currently have supply agreements with both customers that contain customary

17

termination provisions for bankruptcy related events and uncured breaches of the applicable agreement. If any of our major customers substantially reduces or altogether ceases purchasing our sand-based proppants and we are not able to generate replacement sales of sand-based proppants into the market, our business, financial condition, and results of operations could be adversely affected for a short-term period until such time as we generate replacement sales in the market.

We are exposed to the credit risk of our customers, and any material nonpayment or nonperformance by our customers could adversely affect our financial results.

We are subject to the risk of loss resulting from nonpayment or nonperformance by our customers, many of whose operations are concentrated solely in the global oilfield services industry which, as described above, is subject to volatility and therefore credit risk. Our credit procedures and policies may not be adequate to fully reduce customer credit risk. If we fail to adequately assess the creditworthiness of existing or future customers or unanticipated deterioration in their creditworthiness, any resulting increase in nonpayment or nonperformance by them and our inability to re-market or otherwise use the production could have a material adverse effect on our business, financial condition, and results of operations.

The demand for industrial and recreational sand fluctuates, which could adversely affect our results of operations.

A portion of our sales are to customers in industries that have historically been cyclical, such as glassmaking, building products and foundry. During periods of economic slowdown, our customers often reduce their production rates and also reduce capital expenditures and defer or cancel pending projects. Such developments occur even among customers that are not experiencing financial difficulties.

Demand in many of the end markets for industrial and recreational sand is driven by the construction and automotive industries. For example, the flat glass market depends on the automotive and commercial and residential construction and remodeling markets. The market for industrial sand used to manufacture building products is driven primarily by demand in the construction markets. The demand for foundry silica substantially depends on the rate of automobile, light truck and heavy equipment production. Other factors influencing the demand for industrial and recreational sand include (i) the substitution of plastic or other materials for glass, (ii) competition from offshore producers of glass products, (iii) changes in demand for our products due to technological innovations, and (iv) prices, availability, and other factors relating to our products.

We cannot predict or control the factors that affect demand for our products. Negative developments in the above factors, among others, could cause the demand for industrial and recreational sand to decline, which could adversely affect our business, financial condition, results of operations, cash flows, and prospects.

Our operations are subject to operating risks that are often beyond our control and could adversely affect production levels and costs, and such risks may not be covered by insurance.

Our mining, processing and production facilities are subject to risks normally encountered in the proppant and industrial and recreational sand industries. These risks include:

|

|

• |

changes in the price and availability of transportation; |

|

|

• |

changes in the price and availability of natural gas or electricity; |

|

|

• |

unusual or unexpected geological formations or pressures; |

|

|

• |

cave-ins, pit wall failures, or rock falls, particularly in underground mines; |

|

|

• |

unanticipated ground, grade, or water conditions; |

|

|

• |

extreme seasonal weather conditions; |

|

|

• |

hazardous or catastrophic weather conditions or events, including flooding, tornadoes, and hurricanes, and the physical impacts of climate change; |

18

|

|

• |

industrial accidents; |

|

|

• |

changes in laws and regulations (or the interpretation thereof) or increased public scrutiny related to the mining and the drilling and well completion industries, silica dust exposure or the environment; |

|

|

• |

inability to acquire or maintain necessary permits or mining or water rights; |

|

|

• |

restrictions on blasting and mining operations, including potential moratoriums on mining as result of local activism or complaints; |

|

|

• |

inability to obtain necessary production equipment or replacement parts; |

|

|

• |

reduction in the amount of water available for processing; |

|

|

• |

labor disputes; |

|

|

• |

cybersecurity breaches; |

|

|

• |

late delivery of supplies; |

|

|

• |

fires, explosions, or other accidents; and |

|

|

• |

facility shutdowns in response to environmental regulatory actions |

Any of these risks could result in damage to, or destruction of, our mining properties or production facilities, personal injury, environmental damage, delays in mining or processing, losses, or possible legal liability. Any prolonged downtime or shutdowns at our mining properties or production facilities could have a material adverse effect on us.

Not all of these risks are reasonably insurable, and our insurance coverage contains limits, deductibles, exclusions, and endorsements. Our insurance coverage may not be sufficient to meet our needs in the event of loss and any such loss may have a material adverse effect on us.

A significant portion of our sales is generated at our Wedron Silica facility. Any adverse developments at this plant could have a material adverse effect on our business, financial condition, and results of operations.