Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Neff Corp | neff-2016x12x31x16xex322.htm |

| EX-32.1 - EXHIBIT 32.1 - Neff Corp | neff-2016x12x31x16xex321.htm |

| EX-31.2 - EXHIBIT 31.2 - Neff Corp | neff-2016x12x31x16xex312.htm |

| EX-31.1 - EXHIBIT 31.1 - Neff Corp | neff-2016x12x31x16xex311.htm |

| EX-23.1 - EXHIBIT 23.1 - Neff Corp | neff-2016x12x31x16xex231.htm |

| EX-21.1 - EXHIBIT 21.1 - Neff Corp | neff-2016x12x31x16xex211.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2016 |

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____ to ____

Commission File No. 001-36752

Neff Corporation

(Exact name of registrant as specified in its charter)

Delaware | 37-1773826 | |||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||

3750 N.W. 87th Avenue, Suite 400 Miami, FL 33178 |

(Address of principal executive offices) (zip code) |

(305) 513-3350 |

(Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Name of each exchange on which registered

Class A Common Stock, par value $.01 per share New York Stock Exchange

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ¨ | Accelerated filer | ý | |

Non-accelerated filer | ¨ | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ý

As of June 30, 2016, the number of shares of Class A common stock outstanding was 9,025,714. The aggregate market value of common stock held by non-affiliates (defined as other than directors, executive officers and 10 percent beneficial owners) at June 30, 2016 was approximately $97.7 million, calculated by using the closing price of the common stock on such date on the New York Stock Exchange of $10.93.

As of February 23, 2017, the number of shares of Class A common stock outstanding was 8,859,662 and the number of shares of Class B common stock outstanding was 14,951,625.

DOCUMENTS INCORPORATED BY REFERENCE: | |

Related Section | DOCUMENTS |

Part III | Portions of the registrant's definitive proxy statement to be issued in connection with the registrant's 2017 Annual Meeting of Stockholders are incorporated by reference into Part III of this Form 10-K. |

NEFF CORPORATION | ||

TABLE OF CONTENTS | ||

10-K Part and Item No. | Page No. | |

PART I | ||

PART II | ||

PART III | ||

PART IV | ||

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report on Form 10-K contains "forward-looking statements" within the meaning of the federal securities laws. These forward-looking statements include statements regarding industry outlook, our expectations regarding the performance of our business, liquidity, our expected tax rate and benefits and estimated payments under our tax receivable agreement, expected capital expenditures, anticipated future indebtedness or financings and other non-historical statements. We use words such as "could," "may," "might," "will," "expect," "likely," "believe," "continue," "anticipate," "estimate," "intend," "plan," "project" and other similar expressions to identify some but not all forward-looking statements. Forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in the forward-looking statements. Accordingly, any such statements are qualified in their entirety by reference to the information described under the caption "Risk Factors" and elsewhere in this annual report on Form 10-K.

The forward-looking statements contained in this annual report on Form 10-K are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other important factors we believe are appropriate under the circumstances. As you read and consider this annual report on Form 10-K, you should understand that these statements are not guarantees of performance or results. They involve risks, uncertainties (many of which are beyond our control) and assumptions. Although we believe that these forward-looking statements are based on reasonable assumptions, you should be aware that many important factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance anticipated in the forward-looking statements. We believe these important factors include, but are not limited to, those described under the captions "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" in this annual report on Form 10-K.

3

Should one or more of these risks or uncertainties materialize, or should any of these assumptions prove incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements.

Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this annual report on Form 10-K to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances. New important factors that could cause our business not to develop as we expect, emerge from time to time, and it is not possible for us to predict all of them.

4

PART I

Item 1. BUSINESS

Our Company

We are a leading regional equipment rental company in the United States, focused on the fast-growing Sunbelt states. We offer a broad array of equipment rental solutions for our diverse customer base, including infrastructure, non-residential construction, oil and gas and residential construction customers. Our broad fleet of equipment includes earthmoving, material handling, aerial and other rental equipment, which we package together to meet the specific needs of our customers.

Our Branch Network and Fleet

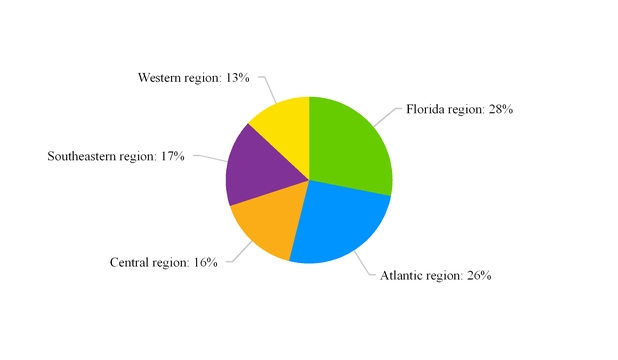

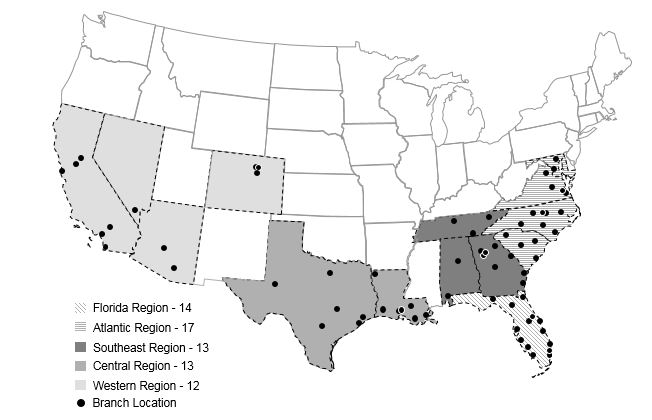

As of December 31, 2016, we operated 69 branches organized into operating clusters in five regions in the United States: Florida, Atlantic, Central, Southeastern and Western. We are strategically located in markets that we believe feature high levels of population growth as well as high levels of construction activity over the near term. We believe that our clustering approach enables us to establish a strong local presence in targeted markets and meet the needs of our customers that have multiple projects within a specific region.

Revenues by Region for the year ended December 31, 2016

5

Our Five Regions

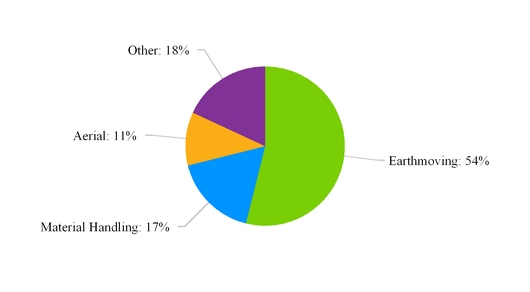

As of December 31, 2016, our rental fleet consisted of approximately 15,000 major units of equipment with an original equipment cost, or OEC, of approximately $824.7 million and an average age of approximately 48 months. Our earthmoving fleet represented approximately 54% of OEC and had an average age of approximately 42 months. We believe that our focus on earthmoving equipment positions us to take advantage of future growth opportunities in our key end-markets.

Rental Fleet by Equipment Category as a Percentage of OEC as of December 31, 2016

6

Segment Reporting

We have one reportable segment. For financial information regarding our reportable segments, refer to our financial statements and notes thereto included in Item 8 of this annual report on Form 10-K and "Management's Discussion and Analysis of Financial Condition and Results of Operations" included in this annual report on Form 10-K.

Our Business Strengths

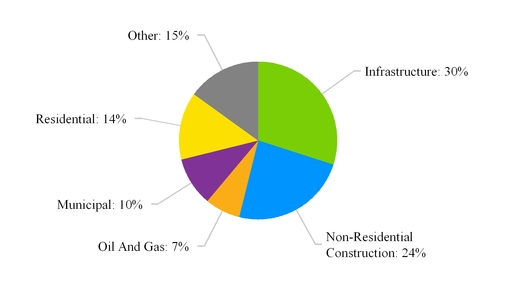

End-Market Growth. For the year ended December 31, 2016, approximately 85% of our rental revenues were derived from five key end-markets: infrastructure, non-residential construction, oil and gas, municipal and residential construction. We believe that our current business is well aligned with these end-markets, and that we will continue to benefit from macroeconomic growth.

Our Rental Revenues by End-Market for the Year Ended December 31, 2016

Prominent Position in Fast-Growing Sunbelt States. 64 of our 69 branches are located in the Sunbelt states of Virginia, North Carolina, South Carolina, Florida, Georgia, Alabama, Tennessee, Louisiana, Texas, Arizona, Nevada and California. Our Sunbelt state locations benefit from favorable climate conditions that facilitate year-round construction activity and reduce seasonality in our business. According to the American Rental Association, construction and industrial equipment rental revenue in the states where we have branch locations is expected to grow approximately 5% annually from 2016 to 2020, compared to an average growth rate of approximately 4% for all other states. By clustering our operations and concentrating our branches in these strategic regional markets, we have established a strong local presence and developed significant brand recognition in those markets.

High-Quality Fleet Focused on Earthmoving Equipment. We offer our customers a broad array of rental equipment with a focus on the earthmoving category. We believe that we are well positioned to benefit from additional penetration in the earthmoving equipment category, which had a penetration rate of approximately 51% in 2016, compared to approximately 92% for the aerial and 84% for the material handling categories, respectively. As of December 31, 2016, we had approximately 5,800 units of earthmoving equipment, accounting for 54% of the OEC of our rental fleet.

Disciplined Sales Culture Drives Strong Customer Relationships. We have a diverse base of customers who we believe value our knowledge and expertise. Our customer base includes large and mid-sized construction firms, municipalities, utilities and industrial users. We serve approximately 15,400 customers annually. For the year ended December 31, 2016, no single customer accounted for more than 1% of our total rental revenues and our ten largest customers accounted for approximately 6% of our total rental revenues, collectively. Our culture is built around the disciplined use of our customer relationship management system, or "CRM system," at every level of our organization, which we believe provides our employees with the tools and information to efficiently provide customized solutions to our existing and potential customers. In addition, our CRM system automatically notifies our sales force of new construction projects within their territories and provides them with the names and contact information of key contractors.

Strong Operating Trends. We have experienced substantial earnings momentum since 2011, driven by the rebound in our end-markets and supported by significant investment in our fleet, which has resulted in an increase in OEC from $471.1 million at December 31, 2011 to $824.7 million at December 31, 2016. In addition, our time utilization, which we define as the daily

7

average OEC of equipment on rent, divided by the OEC of all equipment in the rental fleet during the relevant period, has increased from 65.0% for the year ended December 31, 2011 to 67.1% for the year ended December 31, 2016. We believe that the combination of favorable industry dynamics, significant investments in our fleet and our focus on operating leverage (which has seen our Adjusted EBITDA margin increase from 35.4% for the year ended December 31, 2011 to 48.8% for the year ended December 31, 2016) have driven our Adjusted EBITDA from $86.7 million to $193.8 million over this period. For additional discussion on Adjusted EBITDA and Adjusted EBITDA margin see Management's Discussion and Analysis of Financial Conditions and Results of Operations.

Experienced Management Team. Our senior management team has significant operating experience in the equipment rental industry and has worked together at our company for over a decade. Graham Hood, our Chief Executive Officer, has 39 years of rental industry experience and Mark Irion, our Chief Financial Officer, has 18 years of rental industry experience. Our regional Vice Presidents, with an average of 20 years with our company and 33 years of industry experience, provide us with a stable base of operating management with long-term, local relationships and deep equipment rental industry expertise. This industry expertise, combined with our disciplined sales culture and CRM system, enables our regional management team to respond quickly to changing market conditions.

Our Business Strategy

Focus on Premium Customer Service to Create Strong Customer Relationships. We are committed to providing our customers with premium service. We believe that our customers value our strong regional presence, well established local relationships and full-service branches, which offer 24/7 customer support. Our regional presence is supplemented by a national account focus that allows us to differentiate our brand and product offering to our larger customer accounts. We intend to continue to leverage our national accounts program, our customer service capabilities and our advanced CRM system to retain our existing customers and further penetrate our target customer base.

Emphasis on Active Asset Management. We have invested significantly in both customized technologies and the development of our personnel to ensure that we manage our fleet efficiently. Our equipment clustering strategy allows us to share and deploy equipment among our branches as demand for equipment shifts throughout our branch network. Over time, we have demonstrated our ability to both increase and decrease the age of our fleet in response to changing market conditions. We actively monitor the market environment to determine where investment in fleet assets should be made or when fleet asset divestitures should occur. Our emphasis on active asset management, combined with our rigorous repair and maintenance program, allows us to increase time utilization, extend the useful life of our fleet and also results in higher resale values for our equipment.

Focus on Growing Markets. We believe that our focus on the infrastructure, non-residential construction and residential construction end-markets positions us to benefit from favorable industry and macroeconomic trends. We believe that all of these end-markets are currently experiencing significant growth and will continue to benefit from investment spending driven by the economic recovery in the United States. FMI Construction Outlook predicts that from 2016 through 2020, U.S. infrastructure spending will grow approximately 4.6% annually, U.S. non-residential construction spending will grow 4.7% annually, and U.S. residential construction will grow 3.5% annually. We believe that our focus on these end-markets will position us to achieve significant growth in revenues.

Capitalize on Operating Leverage. We have a highly scalable business model constructed around our network of 69 full-service branch locations. We believe that our current network can support significant additions to our rental fleet without substantial additional investment in infrastructure, personnel or information technology. We intend to capitalize on anticipated growth opportunities primarily by increasing our fleet size within our existing branch network, using our active asset management capabilities to increase time utilization and improve pricing levels and serving customers who value our equipment mix and service capabilities. We regularly evaluate new branch opportunities based on stringent investment return criteria to identify promising new branch locations and will continue to monitor opportunities to expand our strategic branch network.

History and Structure

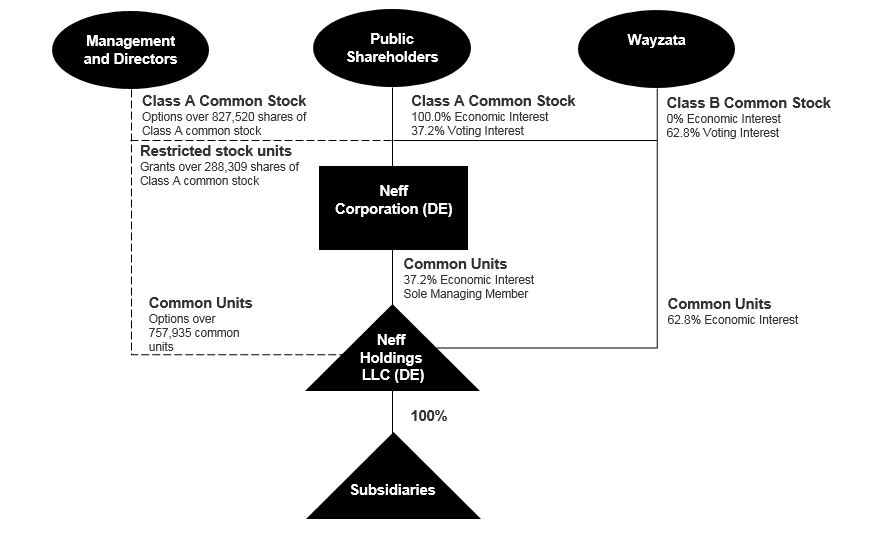

Neff Corporation was formed as a Delaware corporation on August 18, 2014 by Wayzata Opportunities Fund II, L.P. and Wayzata Opportunities Fund Offshore II, L.P., private investment funds (the "Wayzata Funds") managed by Wayzata Investment Partners LLC (and together with the Wayzata Funds, "Wayzata"). On November 26, 2014, Neff Corporation completed an Initial Public Offering (the "IPO") of 10,476,190 shares of Class A common stock in exchange for net proceeds of approximately $146.1 million. A portion of the net proceeds received by Neff Corporation from the IPO were used to purchase 10,476,190 common units in Neff Holdings, which was wholly owned by Wayzata Funds prior to the IPO.

Neff Corporation is the sole managing member of Neff Holdings and as of December 31, 2016, subsequent to common unit repurchases and other equity transactions, owns 8,859,662 common units of Neff Holdings representing approximately 37.2% of the combined voting power of all of Neff Corporation's common stock and through Neff Corporation's ownership of Neff

8

Holdings' common units, indirectly holds approximately 37.2% of the economic interest in the business of Neff Holdings and its subsidiaries. As the sole managing member of Neff Holdings, we control its business and affairs and therefore, we consolidate its financial results within ours. Neff Holdings is a holding company that conducts no operations and, as of the consummation of the IPO, its only material asset is the equity interests of its direct and indirect subsidiaries.

As of December 31, 2016, Wayzata Funds through its ownership of Neff Corporation's Class B common stock, owns 14,951,625 common units of Neff Holdings representing a collective 62.8% of the combined voting power of all of Neff Corporation's common stock and through its ownership of Neff Holdings' common units, holds approximately 62.8% of the economic interest in the business of Neff Holdings and its subsidiaries. Each common unit held by Wayzata Funds or acquired by individuals upon exercise of existing options granted by Neff Holdings will be redeemable, at the election of such member, for, at Neff Corporation's option, newly-issued shares of Class A common stock on a one-for-one basis or a cash payment equal to a volume-weighted average market price of one share of Class A common stock for each common unit redeemed (subject to customary adjustments, including for stock splits, stock dividends and reclassifications) in accordance with the terms of the Neff Holdings LLC Agreement; provided that, at Neff Corporation's election, Neff Corporation may effect a direct exchange of such Class A common stock or such cash for such common units.

The following diagram sets forth our ownership structure and percentages of voting power and common unit ownership, as of December 31, 2016:

Operations

Through our 69 branches, located primarily in the Sunbelt states of Virginia, North Carolina, South Carolina, Florida, Georgia, Alabama, Tennessee, Louisiana, Texas, Arizona, Nevada and California, we generate revenues primarily through the rental of a broad array of construction and industrial equipment, the sale of used and new equipment and the sale of parts, supplies and related merchandise.

Rental Fleet. Our broad fleet of equipment includes earthmoving, material handling, aerial and other rental equipment. As of December 31, 2016, we had over 5,800 units of earthmoving equipment, accounting for 54% of the OEC of our rental fleet. We generate revenue under leases for our rental equipment as well as from fees we charge for the pickup and delivery of equipment, damage waivers and other surcharges.

9

We purchase our equipment from vendors who we believe have reputations for good product quality and support. We identify original equipment manufacturers, or "OEMs" who can supply quality, reliable products and provide value added support services.

As of December 31, 2016, our rental fleet is comprised of the following equipment categories and respective primary OEM suppliers:

Equipment Category | Primary Fleet Equipment | Primary OEM Suppliers | Percentage of OEC | ||||

Earthmoving | Excavators, backhoes, loaders, bulldozers, mini-excavators, trenchers, sweepers and tractors, track loaders and skid steers | Komatsu, John Deere, Kobelco, IHI, Doosan, Bobcat, Link-Belt, Case, Kubota and Takeuchi | 54 | % | |||

Material Handling | Reach forklifts, industrial forklifts and straight-mast forklifts | JLG, Gehl, Genie, JCB, Caterpillar, Case, Doosan, Komatsu, Skytrak and Heli | 17 | % | |||

Aerial | Personnel lifts, electric scissor lifts, dual fuel scissor lifts, articulating boom lifts and straight boom lifts | JLG, Genie and Skyjack | 11 | % | |||

Other Rental Equipment | Compaction and concrete, trucks and trailers, sweepers, air equipment, generators, welders, lighting, pumps and other small equipment and tools | Hamm, International, Wacker, Ford, Bomag, Magnum, EPI, Freightliner, Atlas Copco and Doosan | 18 | % | |||

Rental Revenues. We offer our equipment for rent on a daily, weekly and monthly basis and our customers typically execute written rental agreements, which we account for as leases under generally accepted accounting principles in the United States ("US GAAP"). The majority of our written rental agreements are short-term and do not include specific provisions for early termination. We determine rental rates for each type of equipment based on the cost and expected time utilization of the equipment and adjust rental rates at each location based on demand, length of rental, volume of equipment rented and other competitive considerations.

Equipment Sales. We maintain a regular program of selling used equipment in order to adjust the size and composition of our rental fleet to changing market conditions and to maintain the quality and average age of our rental fleet. We attempt to balance the objective of obtaining acceptable prices from used equipment sales against the recurring revenues obtainable from equipment rentals. Our proactive management of our rental fleet allows us to adjust the rate and timing of new equipment purchases and used equipment sales to improve time utilization rates, take advantage of attractive disposition opportunities and respond to changing economic conditions.

To a much lesser extent, we also generate revenue through the sale of ancillary new equipment.

Parts and Service. We sell complementary parts, supplies, fuel and merchandise to our customers in conjunction with our equipment rental and sales businesses. We maintain an inventory of fuel, maintenance and replacement parts and related products, which are important for timely parts and service support and helps reduce downtime for both our customers and us.

For additional financial information regarding revenues for our rental fleet, equipment sales and parts and service as well as our consolidated net income and total assets, please refer to our financial statements and the notes to the financial statements.

Fleet Management

Our branches are often within close geographic proximity to each other and are all connected through a centralized system which allows any other branch to view rental equipment availability throughout our entire branch network. As a result, we can respond quickly to the needs of our customers and increase the time utilization rates of our equipment, thereby improving profitability and reducing capital expenditures.

We actively monitor fleet purchases to maintain appropriate inventory levels and to manage capital expenditures. At times, we may selectively increase or decrease the age of our fleet in response to changing market conditions. We actively monitor the market environment to determine where investment in fleet assets should be made or when fleet asset divestitures should be made.

We provide transportation of our rental equipment to and from the customer's location and our payroll expenses reflect the cost of providing such transportation. Once our drivers have delivered rental equipment to the customer, the customer takes

10

complete control of operating the equipment. All customers are expected to provide insurance coverage of the rental equipment under their control during the period of utilization of such rental equipment.

Customers

Our large customer base, which included approximately 15,400 customers for the year ended December 31, 2016, is diversified among various industries, including infrastructure, non-residential construction, oil and gas, municipal and residential construction. In particular within these industries, we serve industrial and civil construction, manufacturing, public utilities, offshore oil exploration and drilling, refineries and petrochemical facilities, municipalities, golf course construction, shipping and the military. We target mid-sized, regional and local construction companies that value customer service. Our customer base includes both large Fortune 500 companies who have elected to outsource some of their equipment needs and small construction contractors, subcontractors and machine operators whose equipment needs are job-based. Our top ten customers accounted for approximately 6% of our total rental revenues for the year ended December 31, 2016 collectively, and no single customer accounted for more than 1% of our total rental revenues for the year ended December 31, 2016.

We largely conduct our business on account with customers who are screened through a credit application process. Credit account customers are our core customers, accounting for approximately 98% of our total revenues for the year ended December 31, 2016.

Sales and Marketing

We maintain a strong sales and marketing orientation throughout our organization, which we believe helps us to increase our customer base and better understand and serve our customers. Managers develop relationships with local customers and assist them in planning their equipment rental requirements. They are also responsible for managing the mix of equipment at their locations, keeping current on local construction activity and monitoring competitors in their respective markets. To stay informed about their local markets, salespeople track rental opportunities and construction projects in the area through Equipment Data Reports, F.W. Dodge Reports, PEC (Planning, Engineering and Construction) Reports and local contacts.

Our national accounts are serviced by a core team of dedicated managers to provide continuity and customized solutions to our national account customers.

Our sales training program emphasizes customer service and focuses on sales generation.

Management Information Systems

In addition to our CRM system, we have developed customized management information systems, capable of monitoring our branch operations and sales force productivity on a real-time basis, which management believes can support our current and future needs. These systems link all of our rental locations and allow management to track customer and sales information, as well as the location, rental status and maintenance history of every major piece of equipment in the rental fleet. By using these systems, branch managers can search our entire rental fleet for needed equipment, quickly determine the closest location of such equipment and arrange for delivery of equipment to the customer's work site.

Employees

As of December 31, 2016, we had approximately 1,160 full-time employees. None of our employees are represented by a union or covered by a collective bargaining agreement. We believe we have satisfactory relations with our employees.

Our sales force is divided into salaried sales coordinators and field sales professionals. Our sales professionals receive monthly sales commissions based on rental revenue and a percentage of the gross profit from the sale of used and new equipment.

Seasonality and Cyclicality

Our Sunbelt locations benefit from favorable climate conditions that facilitate year round construction activity and reduce seasonality in our business. Our operating results are subject to annual and seasonal fluctuations resulting from a variety of factors, including:

• | the seasonality of rental activity by our customers, with lower activity levels during the winter; |

• | the cyclicality of the construction industry; |

• | the number of our significant competitors and the competitive supply of rental equipment; |

• | general economic conditions; and |

11

• | the price of oil and other commodities and other general economic trends impacting the industries in which our customers and end users operate. |

In addition, our operating results may be affected by severe weather events and seismic conditions (such as hurricanes, tornadoes, flooding and earthquakes) in the regions we serve. Severe weather events can result in short-term reductions in construction activity levels, but after these periods of reduced construction activity, repair and reconstruction efforts have historically resulted in periods of increased demand for rental equipment.

Competition

The equipment industry is highly fragmented and we believe that competition tends to be based on geographic proximity and availability of products. While the competitive landscape also includes small, independent businesses with only a few rental locations, we believe that we mostly compete against regional competitors which operate in one or more states, public companies and equipment vendors and dealers who both sell and rent equipment directly to customers. Some of these competitors include United Rentals, Herc Rentals, Ahern Rentals, H&E Equipment Services, CAT Rental, Sunstate Equipment and Sunbelt Rentals.

We believe that, in general, large companies may enjoy competitive advantages compared to smaller operators, including greater purchasing power, a lower cost of capital, the ability to provide customers with a broader range of equipment and services, and greater flexibility to transfer equipment among locations in response to customer demand. See "Risk Factors—Risks Relating to Our Business—The equipment rental industry is highly competitive, and competitive pressures could lead to a decrease in our market share or in rental rates and our ability to sell equipment at favorable prices."

Environmental and Safety Regulations

We and our facilities and operations are subject to comprehensive and frequently changing federal, state and local environmental and safety and health requirements, including those relating to discharges of substances to the air, water and land, the handling, storage, transport, use and disposal of hazardous materials and wastes and the cleanup of properties affected by pollutants. In connection with our vehicle and equipment fueling and maintenance, repair and washing operations, we use regulated substances such as petroleum products and solvents and we generate small quantities of regulated waste such as used oil, radiator fluid and spent solvents. All of our properties currently have above ground and/or underground storage tanks and oil-water separators (or equivalent wastewater collection/treatment systems). Although we have made, and will continue to make capital expenditures to comply with environmental requirements, we do not anticipate that compliance with such requirements will have a material adverse effect on our business or financial condition or competitive position. However, in the future, new or more stringent laws or regulations could be adopted. Accordingly, we cannot assure you that we will not have to make significant capital or other expenditures in the future in order to comply with applicable laws and regulations or that we will be able to remain in compliance at all times.

Most, but not all, of our current properties have been the subject of an environmental site assessment conducted with the goal of identifying conditions that may cause us to incur costs under applicable environmental laws. In addition, all but one of our properties are leased and certain of our lease agreements provide that the site owner has responsibility for the preexisting environmental contamination at the property and that we are liable for contamination caused by us or that occurs during the term of the lease. However, given the nature of our operations and the historical operations conducted at these properties, and inherent limits on the information from the environmental site assessments mentioned above, we cannot be sure that all potential instances of contamination have been identified, that our operations have not caused contamination or that our landlords will be able or willing to hold us harmless for preexisting contamination at the relevant sites. Future events, such as changes in laws or policies, the discovery of previously unknown contamination, or the failure of another party to honor an obligation it may have to indemnify us for remediation costs or liabilities, may give rise to remediation costs which may be material. See "Risk Factors—Risks Relating to Our Business—We are subject to numerous environmental and health and safety laws and regulations that may result in our incurring liabilities, which could have a material adverse effect on our operating performance."

Other Information

We maintain a website with the address www.neffrental.com. We are not including the information contained in our website as part of, or incorporating it by reference into, this annual report on Form 10-K. We make available, free of charge through our website, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to these reports as soon as reasonably practicable after we electronically file these materials with, or otherwise furnish them to, the Securities and Exchange Commission (the “SEC”).

12

Item 1A. RISK FACTORS

Neff Corporation and its consolidated subsidiaries, including Neff Holdings and Neff Holdings' subsidiaries, Neff LLC and Neff Rental LLC, (collectively, the "Company," "we," "our" or "us") face significant risks and uncertainties. Certain important factors may have a material adverse effect on our business, financial condition, results of operations or cash flows. Accordingly, in evaluating our business, you should carefully consider the following discussion of risk factors in addition to other information contained in or incorporated by reference into this annual report on Form 10-K and our other public filings with the SEC.

Risks Relating to Our Business

The equipment rental industry is highly cyclical. Decreases in construction or industrial activities could materially adversely affect our revenues and operating results by decreasing the demand for our equipment or the rental rates or prices we can charge.

The equipment rental industry is highly cyclical and its revenues are closely tied to general economic conditions and to conditions in the non-residential construction industry in particular. Our products and services are used primarily in non-residential construction and oil and gas end-markets and, to a lesser extent, in industrial activity and residential construction end-markets. These are cyclical businesses that are sensitive to changes in general economic conditions. Weakness in our end-markets, such as a decline in non-residential construction, oil and gas end-markets or industrial activity, have led, and may in the future lead, to a decrease in the demand for our equipment or the rental rates or prices we can charge. For example, in 2009 and 2010, there were significant decreases in non-residential construction activity compared to prior periods, which materially adversely affected our results for those periods. Recently, we have observed a significant slowdown in activity in the oil and gas industry, which has materially adversely affected our rentals to participants in this industry. Factors that may cause weakness in our end-markets include:

• | weakness in the economy, decreases in the market value of real estate or the onset of a new recession; |

• | slowdowns in residential construction and/or non-residential construction in the geographic regions in which we operate; |

• | continued decline and/or volatility in oil and gas prices as well as slowdowns in the oil and gas industry in the geographic regions in which we operate; |

• | reductions in spending levels by customers; |

• | unfavorable credit markets affecting end-user access to capital; |

• | adverse changes in the federal and local government infrastructure spending; |

• | an increase in the cost of construction materials; |

• | adverse weather conditions which may affect a particular region; |

• | oversupply of available commercial real estate in the markets we serve; |

• | increases in interest rates; and |

• | terrorism or hostilities involving the United States. |

Future declines in non-residential construction and industrial activity could materially adversely affect our operating results by decreasing our revenues and gross profit margins. Because of our focus on the earthmoving equipment category, which represented approximately 54% of our OEC as of December 31, 2016, any such declines may affect us more than our competitors.

In addition, the cyclicality of our industry makes it more difficult for us to forecast trends. Uncertainty regarding future product demand could cause us to maintain excess equipment inventory and increase our equipment inventory costs. Alternatively, during periods of increased demand, we may not have enough rental equipment to satisfy demand, which could result in a loss of market share.

Our substantial indebtedness could materially adversely affect our business, financial condition, results of operations and cash flows.

We have a significant amount of indebtedness. As of December 31, 2016, we had total indebtedness of approximately $702.1 million (of which $475.7 million consisted of borrowings under our second lien credit agreement (the "Second Lien Loan")

13

and $226.4 million consisted of borrowings under our Revolving Credit Facility (as defined below)). As of December 31, 2016, we had borrowing capacity under our senior secured revolving credit facility (the "Revolving Credit Facility"), net of approximately $4.1 million in outstanding letters of credit, of $223.0 million, subject to certain conditions. In addition, subject to certain conditions, our Second Lien Loan can be increased by an additional $75.0 million under an uncommitted incremental facility. Under the terms of the agreements governing our indebtedness, we may be able to incur substantial indebtedness in the future.

Our substantial indebtedness could have important consequences to you. For example, it could:

• | make it more difficult for us to satisfy our obligations with respect to our indebtedness or refinance our indebtedness as they become due; |

• | increase our vulnerability to general adverse economic and industry conditions; |

• | require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures, strategic growth efforts and other general corporate purposes; |

• | decrease our profitability or cash flow; |

• | limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

• | limit our ability to attract acquisition candidates or to complete future acquisitions; |

• | place us at a competitive disadvantage compared to our competitors who have less indebtedness; and |

• | limit our ability to obtain additional financing for working capital, capital expenditures, acquisitions or general corporate purposes. |

In addition, the agreements governing our indebtedness contain restrictive covenants that limit our ability to engage in activities that may be in our long-term best interests. Our failure to comply with those covenants could result in an event of default which, if not cured or waived, could result in the acceleration of all of our indebtedness. In the past, we have had to seek waivers and amendments to certain covenants from our lenders which we obtained. There can be no assurance that we will not be required to seek waivers and amendments in the future or that, if sought, our lenders would grant such waivers or amendments.

To service our indebtedness, we will require a significant amount of cash. Our ability to generate cash depends on many factors beyond our control and any failure to meet our debt service obligations could harm our business, financial condition and results of operations.

As a result of our significant indebtedness, we have substantial debt service requirements. Our ability to satisfy our debt service requirements and to meet our other capital and liquidity needs will depend on our ability to generate sufficient cash flow. Our ability to generate sufficient cash flow to satisfy our debt service requirements is subject to numerous factors, many of which are beyond our control, such as general economic conditions and changes in our industry. Also, we are dependent on the ability of our subsidiaries to distribute their operating cash flow to the borrower under our indebtedness to satisfy our debt service requirements. If our subsidiaries are restricted from distributing cash, whether by reason of contractual limitations, legal restrictions or otherwise, we may not be able to cause such cash to be distributed.

We cannot assure you that our business will generate sufficient cash flow from operations or that future borrowings will be available to us under our Revolving Credit Facility in an amount sufficient to enable us to pay our indebtedness or to fund our other liquidity needs. We may need to refinance all or a portion of our indebtedness on or before maturity. Our ability to refinance our indebtedness will depend on the capital markets and our financial condition at such time. Any refinancing of our indebtedness could be at high interest rates and may require us to comply with more onerous covenants, which could further restrict our business operations. We cannot assure you that we will be able to refinance any of our indebtedness, including our Revolving Credit Facility and the Second Lien Loan, on commercially reasonable terms or at all. Our inability to refinance our indebtedness or to do so upon attractive terms could materially and adversely affect our business, results of operations, financial condition, cash flows and make us vulnerable to adverse industry and general economic conditions.

Without a refinancing, we could be forced to implement alternative actions, including to reduce or delay capital expenditures, limit our growth, seek additional capital, or sell assets to make up for any shortfall in our payment obligations under unfavorable circumstances. The Revolving Credit Facility and the documentation governing the Second Lien Loan limit our ability to sell assets and also restrict the use of proceeds from such a sale. Moreover, the Revolving Credit Facility is secured on a first-priority basis by substantially all of our assets and the Second Lien Loan and the guarantees are secured on a second-priority basis

14

by substantially the same assets. We may not be able to sell assets quickly enough or for sufficient amounts to enable us to meet our obligations.

Variable rate indebtedness subjects us to interest rate risk, which could cause our debt service obligations to increase significantly.

Borrowings under our Revolving Credit Facility and the Second Lien Loan are at variable rates of interest and expose us to interest rate risk. While we have generally not entered into hedging arrangements in the ordinary course of our business, in March 2015, we did enter into an interest rate swap in the notional amount of $200.0 million to hedge the variable rate on a portion of the Revolving Credit Facility for the period between April 8, 2015 and April 8, 2020. Since our hedging arrangements only cover a portion of our indebtedness, our results of operations are still sensitive to movements in interest rates. There are many economic factors outside our control that have in the past and may, in the future, impact rates of interest including publicly announced indices that underlie the interest obligations related to a certain portion of our debt. Factors that impact interest rates include governmental monetary policies, inflation, recession, changes in unemployment, the money supply, international disorder and instability in domestic and foreign financial markets. If interest rates increase, our debt service obligations on the variable rate indebtedness would increase even though the amount borrowed remained the same.

The terms of our Revolving Credit Facility and the Second Lien Loan may restrict our current and future operations, particularly our ability to respond to changes in our business or to take certain actions.

Our Revolving Credit Facility and the documentation governing the Second Lien Loan contain, and the terms of any future indebtedness of ours would likely contain, a number of restrictive covenants that will impose significant operating and other restrictions on us. These restrictions will affect, and in many respects will limit or prohibit, among other things, our ability to:

• | incur additional indebtedness; |

• | pay dividends and make distributions; |

• | issue stock of subsidiaries; |

• | make certain investments, acquisitions or capital expenditures; |

• | repurchase stock; |

• | create liens; |

• | enter into affiliate transactions; |

• | enter into sale-leaseback transactions; |

• | merge or consolidate; and |

• | transfer and sell assets. |

In addition, our Revolving Credit Facility includes other more restrictive covenants and limits us from prepaying our other indebtedness, including the Second Lien Loan, while borrowings under the Revolving Credit Facility are outstanding.

The operating and financial restrictions and covenants in our existing debt agreements and any future financing agreements may adversely affect our ability to finance future operations or capital needs or to engage in other business activities. In addition, a failure to comply with the covenants contained in the credit agreements governing our Revolving Credit Facility or the Second Lien Loan could result in an event of default under the applicable facility which, if not cured or waived, could have a material adverse effect on our business, financial condition and results of operations. If we default under our Revolving Credit Facility or the Second Lien Loan, the lenders thereunder:

• | will not be required to lend any additional amounts to us; |

• | could elect to declare all of our outstanding borrowings, together with accrued and unpaid interest and fees, to be immediately due and payable; and |

• | could effectively require us to apply all of our available cash to repay these borrowings even if they do not accelerate the borrowings. |

Any of these actions under one of our credit facilities could result in an event of default under the other facility or a future debt facility.

15

If the indebtedness under our Revolving Credit Facility or the Second Lien Loan were to be accelerated, there can be no assurance that our assets would be sufficient to repay such indebtedness in full and we could be forced into bankruptcy or liquidation.

If we are unable to obtain additional capital as required, we may be unable to fund the capital outlays required for the success of our business, including those relating to purchasing equipment, opening new rental locations, making acquisitions and refinancing existing indebtedness.

Our business has significant capital requirements. Our ability to remain competitive, sustain our growth and expand our operations through start-up locations and acquisitions largely depends on our access to capital. If the cash that we generate from our business, together with cash on hand and borrowings under our Revolving Credit Facility, to the extent available, is not sufficient to meet our capital needs and implement our growth strategy, we will require additional financing. However, we may not succeed in obtaining additional financing on terms that are satisfactory to us or at all. In addition, our ability to obtain additional financing will be restricted by the terms of our Revolving Credit Facility and by the terms of the Second Lien Loan. If we are unable to obtain sufficient additional capital in the future, we may be unable to fund the capital outlays required for the success and growth of our business, including those relating to purchasing equipment, opening new rental locations and completing acquisitions. Any additional indebtedness that we do incur will make us more vulnerable to economic downturns and may limit our ability to withstand competitive pressures.

Past economic downturns have had, and future economic downturns could have, a material adverse impact on our business.

Economic downturns in the areas we do business adversely affect us as our end-markets are in the highly cyclical construction area. A slowdown in the economic recovery or worsening of economic conditions, in particular with respect to U.S. construction and industrial activities, could have a material adverse effect on our overall business, results of operations and financial condition in a number of ways, including the following:

• | a decrease in expected levels of infrastructure spending, including lower than expected government funding for economic stimulus projects; |

• | a decrease in expected levels of capital projects; |

• | a lack of availability of credit or an increase in interest rates due to deterioration or volatility of the banking system or financial markets; |

• | a delay or inability to pay for equipment rentals or fulfill other terms of rental agreements by customers; |

• | a delay or decrease in equipment rentals by existing or potential customers; and |

• | an increase in our equipment inventory costs. |

Our revenues and operating results will fluctuate, which could affect the volatility of the trading of our Class A common stock.

Our revenues and operating results fluctuate from quarter to quarter due to various factors, including:

• | changes in rental rates or changes in demand for our equipment due to economic conditions, competition, weather or other factors; |

• | seasonal rental and purchasing patterns of our customers, with rental and purchasing activity tending to be lower in the winter due to weather and the holiday season; |

• | the cyclical nature of the businesses of our construction customers; |

• | the timing of capital expenditures for rental fleet expansion; |

• | changes in the cost and availability of equipment we purchase, including changes in manufacturer incentive programs; |

• | changes in corporate spending for plants and facilities or changes in government spending for infrastructure projects; |

• | severe weather and seismic conditions temporarily affecting the regions we serve (such as hurricanes, tornadoes, flooding and earthquakes) or the suppliers that supply us with equipment; |

16

• | cost fluctuations, including fuel costs and other raw material costs (such as the price of steel); |

• | other cost fluctuations, such as costs for employee related compensation and healthcare benefits; |

• | potential enactment of new legislation affecting our operations, rental equipment or labor relations; |

• | the timing and cost of opening new rental or customer repair center locations or acquiring new locations; and |

• | our effectiveness in integrating new or acquired rental or customer repair center locations and branch locations, in integrating acquisitions with existing operations, or in achieving the anticipated benefits of such integrations, expansions and acquisitions. |

Any of these factors could increase the volatility, or materially adversely affect, the trading price of our Class A common stock.

The equipment rental industry is highly competitive, and competitive pressures could lead to a decrease in our market share or in rental rates and our ability to sell equipment at favorable prices.

The equipment rental industry is highly fragmented and very competitive. Our competitors include:

• | a few large national companies, including public companies and divisions of public companies; |

• | several regional competitors that operate in multiple states; |

• | thousands of small, independent businesses with only one or a few rental locations; and |

• | hundreds of equipment manufacturers and dealers that both sell and rent equipment directly to customers. |

Some of our competitors are significantly larger than we are and have greater financial and marketing resources than we have. In addition, some of our competitors have a more diversified offering than us. Some of our competitors also have greater technical resources, longer operating histories, lower cost structures and better relationships with equipment manufacturers than we have. In addition, certain of our competitors are more geographically diverse than we are and have greater name recognition among customers than we do. As a result, our competitors that have the advantages identified above may be able to provide their products and services at lower costs or may be able to capture a greater market share. We may in the future encounter increased competition in the equipment rental market, equipment sales market or in the equipment repair and services market from existing competitors or from new market entrants.

We believe that rental rates, fleet size and quality are the primary competitive factors in the equipment rental industry. From time to time, we or our competitors may attempt to compete aggressively by lowering rental rates or prices. Competitive pressures could materially adversely affect our revenues and operating results by decreasing our market share or depressing the rental rates. To the extent we lower rental rates or increase our fleet in order to retain or increase market share, our operating margins would be adversely impacted. In addition, we may not be able to match a larger competitor's price reductions or fleet investment because of its greater financial resources, all of which could adversely impact our operating results through a combination of a decrease in our market share and revenues.

We are exposed to various risks relating to legal proceedings or claims that could materially adversely affect our operating results. The nature of our business exposes us to various liability claims which may exceed the level of our insurance coverage and thereby not fully protect us, or not be covered by our insurance at all, and this could have a material adverse effect on our operating performance.

We are a party to lawsuits in the normal course of our business. Litigation in general can be expensive, lengthy and disruptive to normal business operations. Moreover, the results of complex legal proceedings are difficult to predict. Responding to lawsuits brought against us, or legal actions that we may initiate, can often be expensive and time consuming. Unfavorable outcomes from these claims and/or lawsuits could materially adversely affect our business, results of operations and financial condition, and we could incur substantial monetary liability and/or be required to change our business practices.

Our business exposes us to claims for personal injury, death or property damage resulting from the use of the equipment we rent, sell, service or repair and from injuries caused in motor vehicle accidents in which our personnel are involved and other employee related matters. Additionally, we could be subject to potential litigation associated with compliance with various laws and governmental regulations at the federal, state or local levels, such as those relating to the protection of persons with disabilities, employment, health, safety, security and other regulations under which we operate.

17

We carry comprehensive insurance, subject to deductibles, at levels we believe are sufficient to cover existing and future claims made during the respective policy periods. However, we may be exposed to multiple claims, including workers compensation claims, that do not exceed our deductibles, and, as a result, we could incur significant out-of-pocket costs that could materially adversely affect our business, financial condition and results of operations. In addition, the cost of such insurance policies may increase significantly upon renewal of those policies as a result of general rate increases for the type of insurance we carry as well as our historical experience and experience in our industry. Our existing or future claims may exceed the coverage level of our insurance, and such insurance may not continue to be available on economically reasonable terms, or at all. If we are required to pay significantly higher premiums for insurance, are not able to maintain insurance coverage at affordable rates or if we must pay amounts in excess of claims covered by our insurance, we could experience higher costs that could materially adversely affect our business, financial condition, results of operations and cash flows. In addition, we may be subject to various legal proceedings and claims, such as claims for punitive damages or damages arising from intentional misconduct, either asserted or unasserted, that may not be covered by our insurance. Any such claims, whether with or without merit, could be time consuming and expensive to defend and could divert management's attention and resources.

We depend on key personnel whom we may not be able to retain.

Our operations are managed by a small number of key executive officers, and our future performance depends on the continued contributions of those management personnel. A loss of one or more of these key people could harm our business and prevent us from implementing our business strategy. We do not maintain "key man" life insurance on the lives of any members of our senior management. We have existing employment agreements with certain key executives. However, each of the employment agreements is of limited duration. We cannot assure you that these executives will remain employed with us for the full term of their agreements or that the term of their agreements will be extended beyond the current term.

The success of our operations also depends in part on our ability to attract, hire, train and retain qualified managerial, sales and marketing personnel. Competition for these types of personnel is high. We may be unsuccessful in attracting and retaining the personnel we require to conduct our operations successfully and, in such an event, our business could be materially adversely affected.

We may recognize significantly higher maintenance costs in connection with increases in the weighted average age of our rental fleet.

As our fleet of rental equipment ages, the cost of maintaining such equipment, if not replaced, will likely increase. We manage the average age of different types of equipment according to the expected wear and tear that a specific type of equipment is expected to experience over its useful life. As of December 31, 2016, the average age of our rental equipment fleet was approximately 48 months. As of December 31, 2016, approximately 54% (based on OEC) of our rental fleet consisted of earthmoving equipment, which generally has higher maintenance costs than similar-sized aerial or material handling equipment. It is possible that we may allow the average age of our rental equipment fleet to increase, which would require an increase in the amounts we invest in maintenance, parts and repair. We cannot assure you that costs of maintenance, parts or repair will not materially increase in the future. Any material increase in such costs could have a material adverse effect on our business, financial condition and results of operations.

We are subject to numerous environmental and health and safety laws and regulations that may result in our incurring liabilities, which could have a material adverse effect on our operating performance.

Our facilities and operations are subject to comprehensive and frequently changing federal, state and local laws and regulations relating to environmental protection and health and safety. These laws and regulations govern, among other things, the discharge of substances into the air, water and land, the handling, storage, transport, use and disposal of hazardous materials and wastes and the cleanup of properties affected by pollutants. If we violate environmental laws or regulations, we may be required to implement corrective actions and could be subject to civil or criminal fines or penalties or other sanctions. Although expenses related to environmental compliance have not been material to date, we cannot assure you that we will not have to make significant capital or operating expenditures in the future in order to comply with applicable laws and regulations or that we will comply with applicable environmental laws at all times. Such violations or liability could have a material adverse effect on our business, financial condition and results of operations.

Environmental laws also impose obligations and liability for the investigation and cleanup of properties affected by hazardous substance spills or releases. These liabilities are often joint and several (which could result in an entity paying for more than its fair share), and may be imposed on the parties generating or disposing of such substances or on the owner or operator of affected property, often without regard to whether the owner or operator knew of, or was responsible for, the presence of hazardous substances. We may also have liability for past contamination as successors-in-interest for companies which were acquired or where there was a merger. Accordingly, we may become liable, either contractually or by operation of law, for investigation, remediation, monitoring and other costs even if the contaminated property is not presently owned or operated by us, or if the

18

contamination was caused by third parties during or prior to our ownership or operation of the property. Contamination and exposure to hazardous substances can also result in claims for damages, including personal injury, property damage, and natural resources damage claims.

All of our properties currently have above ground and/or underground storage tanks and oil-water separators (or equivalent wastewater collection/treatment systems). Given the nature of our operations (which involve the use of diesel and other petroleum products, solvents and other hazardous substances) for fueling, washing and maintaining our rental equipment and vehicles, and the historical operations at some of our properties, we may incur material costs associated with soil or groundwater contamination. Future events, such as changes in existing laws or policies or their enforcement, or the discovery of currently unknown contamination, may give rise to remediation liabilities or other claims or costs that may be material.

Various U.S. and international authorities continue to consider legislation and regulations related to greenhouse gas emissions. Should legislation or regulations be adopted imposing significant limitations on greenhouse gas emissions or costs on entities deemed to be responsible for such emissions, demand for our services could be affected, our costs could increase, and our business, financial condition and results of operations could be materially adversely affected.

We are dependent on our relationships with our key equipment manufacturers and the termination of one or more of our relationships with any of these key equipment manufacturers or their inability to fulfill the terms of their agreements with us could have a material adverse effect on our business.

We purchase most of our rental and sales equipment from a limited number of OEMs. For example, as of December 31, 2016, equipment from JLG Industries, Komatsu, John Deere and Kobelco represented approximately 14.4%, 10.9%, 8.1% and 7.9%, respectively, of our total OEC. Termination of one or more of our relationships with any of these or other major suppliers or insolvency, financial difficulties or other factors may result in our equipment manufacturers not being able to fulfill the terms of their agreement with us or may force our suppliers to seek to renegotiate existing contracts with us. Although we believe we have alternative sources of supply for the equipment we need, termination of our relationship with any of our key suppliers could have a material adverse effect on our business, financial condition and results of operations if we were unable to obtain adequate equipment for rental and sale from other sources in a timely manner, on favorable terms or at all. Because our major suppliers also sell equipment to our competitors, our relationships with our suppliers do not provide us any particular competitive advantage.

Our rental fleet is subject to residual value risk upon disposition.

The market value of any given piece of rental equipment could be less than its depreciated value at the time it is sold. The market value of used rental equipment depends on several factors, including:

• | the market price for new equipment of a like kind; |

• | wear and tear on the equipment relative to its age; |

• | the age of the equipment at the time it is sold; |

• | the time of year that it is sold (generally prices are higher during the peak construction season for any given area); |

• | worldwide and domestic supply of and demand for used equipment; |

• | inventory levels at OEMs; and |

• | general economic conditions. |

We include in income from operations the difference between the sales price and the depreciated value of an item of equipment sold. Changes in our assumptions regarding depreciation could change our depreciation expense, as well as the gain or loss realized upon disposal of equipment. If prices we are able to obtain for our used rental equipment decline or fall below our projections or if we sell our equipment in lesser quantities as a result of the above or other factors, our operating results may be materially adversely affected.

The cost of new equipment we use in our rental fleet may increase, which may cause us to spend significantly more for replacement equipment, and in some cases we may not be able to procure equipment at all due to supplier constraints.

We operate in a capital intensive business. Price increases could materially adversely affect our business, financial condition and results of operations.

While we can manage the size and aging of our fleet generally over time, eventually we must retire older equipment and either allow our fleet to shrink or replace the older equipment in our fleet with newer models. We anticipate that we will need to

19

purchase additional equipment in 2017 in order to supplement our current fleet. We may be at a competitive disadvantage if the average age of our fleet increases compared to the age of our competitors' fleets.

In some cases, we may not be able to procure replacement equipment on a timely basis to the extent that manufacturers for the equipment we need are not able to produce sufficient inventory on schedules that meet our timing demands. If demand for new equipment increases significantly, manufacturers may not be able to meet customer orders on a timely basis. As a result, we at times may experience long lead times for certain types of new equipment and we cannot assure you that we will be able to acquire the types or sufficient numbers of the equipment we need to replace older equipment as quickly as we would like. Consequently, we may have to age our fleet longer than we would consider optimal or shrink our fleet, either of which could restrict our ability to grow our business.

Trends in oil and gas prices could adversely affect the level of exploration, development and production activity of certain of our customers and the demand for our services and products.

Demand for our services and products is sensitive to the level of exploration, development and production activity of, and the corresponding capital spending by, oil and gas companies, including national oil companies, regional exploration and production providers, and related service providers. The level of exploration, development and production activity is directly affected by trends in oil and gas prices, which historically have been volatile and are likely to continue to be volatile.

Prices for oil and gas are subject to large fluctuations in response to relatively minor changes in the supply of and demand for oil and gas, market uncertainty, and a variety of other economic factors that are beyond our control. Factors affecting the prices of oil and gas include:

• | the level of supply and demand for oil and gas; |

• | governmental regulations, including the policies of governments regarding the exploration for, and production and development of, oil and gas reserves; |

• | weather conditions and natural disasters; |

• | worldwide political, military and economic conditions; |

• | the level of oil production by non-Organization of the Petroleum Exporting Countries ("OPEC") countries and the available excess production capacity within OPEC; |

• | oil refining capacity and shifts in customer preferences toward fuel efficiency and the use of gas; |

• | the cost of producing and delivering oil and gas; and |

• | potential acceleration of the development of alternative fuels. |

Any prolonged reduction in oil and gas prices will depress the immediate levels of exploration, development and production activity, which could have an adverse effect on our business, results of operations and financial condition. Even the perception of longer-term lower oil and gas prices by oil and gas companies and related service providers can similarly reduce or defer major expenditures by these companies and service providers given the long-term nature of many large scale development projects.

Disruptions in or threats to the security of our information technology and customer relationship management systems could materially adversely affect our operating results by limiting our capacity to effectively monitor and control our operations.

Our information technology systems facilitate our ability to monitor and control our operations to adjust to changing market conditions, including management of our rental fleet. Our CRM system allows our sales force to access comprehensive information about customer activity relating to specific accounts to assist their sales efforts. The effectiveness of our sales force depends upon the continuous availability and reliability of our CRM system. Consequently, any disruptions in our information technology or customer relationship management systems or the failure of these systems, including our redundant systems, to operate as expected could, depending on the magnitude of the problem, impair our ability to effectively monitor and control our existing operations and improve our future sales efforts, and thereby materially adversely affect our operating results.

Additionally, we collect and store data in the ordinary course of our business that is sensitive to our company and our customers. Operating our information technology systems and networks in a manner that maintains this data in a secure manner is critical to our business. Potential security threats, including cybersecurity attacks to gain unauthorized access to our systems, networks and data are increasing in frequency and sophistication and have impacted a number of companies, including companies much larger than us. While we actively manage information technology security risks within our control, we cannot assure you that such actions will be sufficient to prevent or mitigate all potential risks to our systems, networks and data. If we were to

20

experience a material cybersecurity attack, such attack may materially adversely affect our operating results, and may result in reputational damage, litigation with third parties, and increased cybersecurity protection and remediation costs.

Potential acquisitions and expansions into new markets may result in significant transaction expenses and expose us to risks associated with entering new markets and integrating new or acquired operations.

We may encounter risks associated with entering new markets in which we have limited or no experience. Startup rental locations, in particular, require significant capital expenditures and may initially have a negative impact on our short-term cash flow, net income and results of operations. New startup locations may not become profitable when projected or ever. Acquisitions may impose significant strains on our management, operating systems and financial resources and could experience unanticipated integration issues. The pursuit and integration of acquisitions will require substantial attention from our senior management, which will limit the amount of time they have available to devote to our existing operations. Our ability to realize the expected benefits from any future acquisitions depends in large part on our ability to integrate and consolidate the new operations with our existing operations in a timely and effective manner. Future acquisitions also could result in the incurrence of substantial amounts of indebtedness and contingent liabilities (including potentially environmental, employee benefits and safety and health liabilities), accumulation of goodwill that may become impaired, and an increase in amortization expenses related to intangible assets. Any significant diversion of management's attention from our existing operations, the loss of key employees or customers of any acquired business, any major difficulties encountered in the opening of startup locations or the integration of acquired operations or any associated increases in indebtedness, liabilities or expenses could have a material adverse effect on our business, financial condition and results of operations, which could decrease our cash flows and make it more difficult for us to make payments on our indebtedness.

We have operations throughout the United States, which exposes us to multiple state and local regulations. Changes in applicable law, regulations or requirements, or our material failure to comply with any of them, can increase our costs and have other negative impacts on our business.

Our 69 branch locations are located in 14 states and we must comply with many different state and local regulations. These laws and requirements address multiple aspects of our operations, such as worker safety, consumer rights, privacy, employee benefits and more, and can often have different requirements in different jurisdictions. Changes in these requirements, or any material failure by our branches to comply with them, can increase our costs, affect our reputation, limit our business, consume management time and attention and otherwise impact our operations in adverse ways.

If we determine that our goodwill has become impaired, we may incur impairment charges, which would negatively impact our operating results.

At December 31, 2016, we had $60.6 million of goodwill on our consolidated balance sheet. Goodwill represents the excess of cost over the fair value of identifiable net assets of businesses acquired. We assess potential impairment of our goodwill at least annually. Impairment may result from significant changes in the manner of use of the acquired assets, negative industry or economic trends and/or significant underperformance relative to historic or projected operating results. A material impairment charge may occur in a future period. Such a charge could materially adversely affect our financial condition and results of operations.

Labor disputes could disrupt our ability to serve our customers and/or lead to higher labor costs.