Attached files

| file | filename |

|---|---|

| EX-32.1 - EX-32.1 - SUPREME INDUSTRIES INC | a17-1018_1ex32d1.htm |

| EX-23.1 - EX-23.1 - SUPREME INDUSTRIES INC | a17-1018_1ex23d1.htm |

| EX-31.1 - EX-31.1 - SUPREME INDUSTRIES INC | a17-1018_1ex31d1.htm |

| EX-32.2 - EX-32.2 - SUPREME INDUSTRIES INC | a17-1018_1ex32d2.htm |

| EX-31.2 - EX-31.2 - SUPREME INDUSTRIES INC | a17-1018_1ex31d2.htm |

| EX-21.1 - EX-21.1 - SUPREME INDUSTRIES INC | a17-1018_1ex21d1.htm |

| EX-10.35 - EX-10.35 - SUPREME INDUSTRIES INC | a17-1018_1ex10d35.htm |

| EX-10.34 - EX-10.34 - SUPREME INDUSTRIES INC | a17-1018_1ex10d34.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2016

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

COMMISSION FILE NUMBER: 1-8183

SUPREME INDUSTRIES, INC.

(Exact name of Registrant as specified in its charter)

|

Delaware |

|

75-1670945 |

|

(State or other jurisdiction of incorporation) |

|

(I.R.S. Employer Identification Number) |

|

|

|

|

|

2581 E. Kercher Road |

|

46528 |

|

(Address of principal executive office) |

|

(Zip Code) |

Registrant’s telephone number, including area code: (574) 642-3070

Securities registered pursuant to Section 12(b) of the Exchange Act:

|

Title of each class: |

|

Name of each exchange on which registered: |

|

Class A Common Stock ($.10 Par Value) |

|

NYSE MKT |

Securities registered pursuant to Section 12(g) of the Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o |

|

Accelerated filer x |

|

|

|

|

|

Non-accelerated filer o |

|

Smaller reporting company o |

|

(Do not check if a smaller reporting company) |

|

|

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter, based on the last closing sale price of $12.26 per share for the common stock on the NYSE MKT on such date, was approximately $162,029,129.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock as of the latest practicable date.

|

Class |

|

Outstanding at February 21, 2017 |

|

Class A Common Stock ($.10 Par Value) |

|

15,427,033 shares |

Documents incorporated by reference

Listed below are documents, parts of which are incorporated herein by reference, and the part of this report into which the document is incorporated:

Portions of the Proxy Statement for the 2017 Annual Meeting of Stockholders — Part III

History

Supreme Industries, Inc., a Delaware corporation (the “Company,” “Supreme” or “we”), is one of the nation’s leading manufacturers of specialized commercial vehicles including truck bodies and specialty vehicles. The Company was originally incorporated in 1979.

In January of 1984, Supreme Corporation, the Company’s wholly-owned operating subsidiary, was formed to acquire a company engaged in the business of manufacturing, selling, and repairing specialized truck bodies and related equipment.

General Description of the Company’s Business

The Company has two operating segments — specialized commercial vehicles and fiberglass products. The fiberglass products segment does not meet the quantitative thresholds for separate disclosure. See segment information in Note 1 - Nature of Operations and Accounting Policies of the Notes to Consolidated Financial Statements (Item 8).

Supreme manufactures specialized commercial vehicles that are attached to a truck chassis. The truck chassis, which consists of an engine, drivetrain, a frame with wheels, and in some cases a cab, is manufactured by third parties who are major automotive or truck companies. Such companies typically do not build specialized commercial vehicles.

Supreme offers a wide range of specialized commercial vehicles including truck bodies and specialty vehicles ranging in price from $4,000 to more than $100,000. Supreme’s truck bodies are offered in aluminum, FiberPanel PW, FiberPanel HC, or SignaturePlate. Most of our products are attached to light-duty truck chassis and medium-duty truck chassis. Supreme integrates a wide range of options into its truck bodies including liftgates, cargo-handling equipment, customized doors, special bumpers, ladder racks, and refrigeration equipment. Supreme is primarily a build-to-order operation with very limited production occurring in anticipation of pending orders.

The following is a brief summary of Supreme’s products:

Signature van bodies. Supreme’s Signature van bodies range from 10 to 28 feet in length with exterior walls assembled from one of several material options including pre-painted aluminum, FiberPanel PW, FiberPanel HC, or SignaturePlate. Additional features include molded composite front and side corners, LED marker lights, sealed wiring harnesses, hardwood or pine flooring, and various door configurations to accommodate end-user loading and unloading requirements. This product is adaptable for a diverse range of uses in dry-freight transportation.

Iner-City® cutaway van bodies. An ideal route truck for a variety of commercial applications, the Iner-City bodies are manufactured on cutaway chassis which allow access from the cab to the cargo area. Borrowing many design elements from Supreme’s larger van body, the Iner-City is shorter in length (10 to 18 feet) than a typical van body.

Spartan service bodies. Built on a cutaway chassis out of durable FiberPanel PW, the Spartan service body is a virtual workshop on wheels. In lengths from 10 to 14 feet, the Spartan’s selection of compartments, shelves, doors, and pre-designed options provides job-site protection from the weather while offering a secure lockable workspace.

Spartan cargo vans. Built on a cutaway chassis and constructed of FiberPanel PW, the Spartan cargo van provides the smooth maneuverability of a commercial van with the full-height and spacious cargo area of a truck body. In lengths of 10 to 14 feet and available with a variety of pre-designed options, the Spartan cargo van is a bridge product for those moving up from a traditional cargo van into the truck body category.

Kold King® insulated van bodies. Kold King insulated bodies, in lengths of up to 28 feet, provide versatility and dependability for temperature controlled applications. Flexible for either hand-load or pallet-load requirements, they are ideal for multi-stop distribution of both fresh and frozen products.

Stake bodies. Stake bodies are flatbeds with various configurations of removable sides. The stake body is utilized for a broad range of agricultural and construction industries transportation needs.

Armored SUVs. Supreme’s armored SUV products offer the same outside appearance and interior as a stock model SUV, but with armored protection against hostile fire. These protective vehicles are used both abroad by governmental agencies and for various domestic applications.

Armored trucks and specialty vehicles. Supreme’s armored trucks and specialty vehicles include cash-in-transit vehicles as well as SWAT rapid deployment vehicles, prisoner transport vehicles, and a variety of other security vehicles.

Kold King®, Iner-City®, and Spartan are trade names used by Supreme in its marketing of truck bodies. Kold King®, Iner-City®, FiberPanel® and SignaturePlate® are trademarks registered in the U.S. Patent and Trademark Office.

Manufacturing

Supreme’s manufacturing facilities are located in Goshen and Ligonier, Indiana; Griffin, Georgia; Cleburne, Texas; Moreno Valley, California; and Jonestown, Pennsylvania.

Supreme builds specialized vehicle bodies and installs other equipment on truck chassis, most of which are provided through converter pool agreements or are owned by dealers or end-users. These truck bodies are built on an assembly line from engineered structural components such as floors, roofs, and wall panels. These components are manufactured from Supreme’s proprietary designs and are installed on the truck chassis. Supreme then installs optional equipment and applies any special finishes that the customer has specified. Throughout the manufacturing and installation process, Supreme conducts quality control procedures to ensure that the products meet its customers’ specifications. Supreme’s products are generally produced to firm orders and are designed and engineered by Supreme. Order levels will vary depending upon price, competition, prevailing economic conditions, and other factors.

The Company manufactures component parts including fiberglass-reinforced plywood in Ligonier, Indiana, and has extensive metal bending capabilities at all of its locations.

Supreme provides limited warranties against construction defects in its products. These warranties generally provide for the replacement or repair of defective parts or workmanship for periods of up to five years following the date of retail sale.

We purchase raw materials and component parts from a variety of sources. Although we generally do not enter into long-term supply contracts, management believes that we have good relationships with our primary suppliers. In past years prices have fluctuated significantly, but we have experienced no material adverse problems in obtaining adequate supplies of raw materials and component parts to meet the requirements of our production schedules. Management believes that the materials used in the production of our products are available at competitive prices from an adequate number of alternative suppliers. Accordingly, management does not believe that the loss of a single supplier would have a material adverse effect on our business.

Marketing

Supreme sells its products to commercial dealers/distributors, fleet leasing companies, or directly to end-users. Products purchased by a dealer/distributor from Supreme are sold by the dealer/distributor to its own customers.

Supreme’s dealer/distributor network consists of more than 1,000 commercial dealers and a limited number of truck equipment distributors. Management believes that this large network, coupled with Supreme’s geographically-dispersed manufacturing facilities, gives Supreme a marketing advantage over many of its competitors. Supreme generally delivers its products within 4 to 8 weeks after the receipt of orders.

Approximately 75 employees are engaged in direct sales. Supreme engages in direct marketing to target markets and participates in industry and vocational trade shows.

Trademarks

The Company owns and maintains trademarks that are used in marketing specialized products manufactured by Supreme. Management believes that these trademarks have significant customer goodwill. For this reason, management anticipates renewing each trademark discussed above for an additional ten-year period prior to such trademark’s expiration.

Working Capital

The Company had working capital of $58.2 million and $51.9 million at December 31, 2016, and December 26, 2015, respectively. The Company believes that its days sales outstanding, its days inventories on hand and its days payable outstanding are within normal industry levels.

Major Customers

During the year-ended December 31, 2016, one large national fleet leasing customer accounted for approximately 31% of the Company’s consolidated net sales. During the year-ended December 26, 2015, two large national fleet leasing customers accounted for approximately 24% and 11% of the Company’s consolidated net sales. During the year-ended December 27, 2014, one large national fleet leasing customer accounted for approximately 16% of the Company’s consolidated net sales. The Company’s export sales are minimal.

Competitive Conditions

The highly competitive nature of the specialized vehicle industry presents a number of challenges. With only a few national competitors, the Company often competes with smaller, regional companies. As a result of this broad competition, the Company is often faced with competitive pricing pressures. Other competitive factors include quality of product, lead times, geographic proximity to customers, and the ability to manufacture a product customized to customer specifications.

During favorable business cycles, the industry tends to experience an increase in smaller, regional competitors, and then a similar decrease during times of challenging economic pressures. With its national presence and diverse product offerings, the Company believes that it is well positioned to meet the competitive challenges presented.

Governmental Regulation

The Company’s operations are subject to a variety of federal, state, and local environmental and health and safety statutes and regulations including those related to emissions to the air, discharges to water, treatment, storage, and disposal of water, and remediation of contaminated sites. Additionally, the Company’s products are subject to a variety of federal, state, and local safety statutes and regulations. From time to time, the Company has received notices of noncompliance with respect to our operations and products. These notices have typically been resolved by investigating the alleged noncompliance and correcting any noncompliant conditions.

Cyclicality and Seasonality of Business

The Company’s business can be cyclical due to the normal replacement cycle particularly of its truck products (historically approximately seven years) being subject to customers delaying purchases due to adverse changes in economic conditions and other long range factors that can affect the transportation industry. Seasonality arises due to the Company typically participating in bids for large fleet contracts. If successful, the fleet orders generally require shipment of the truck bodies in the first and second quarters. Additionally, our business depends on various factors that are particularly sensitive to general economic conditions and business cycles including: corporate profitability; interest rates; fuel costs; changes in government regulations (i.e. fuel standards); customer preferences; industrial, commercial, and consumer spending patterns; and availability of truck chassis.

Employees

As of December 31, 2016 and December 26, 2015, the Company employed approximately 1,450 and 1,400 employees, respectively, none of whom are represented by a collective bargaining unit. The Company considers its relations with its employees to be favorable.

Backlog

The Company’s backlog of firm orders was $83.4 million at December 31, 2016 compared to $98.1 million at December 26, 2015.

Any investment in our Class A Common Stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below and the other information included in this Form 10-K before purchasing our Class A Common Stock. Although the risks described below are the risks that we believe are material, they are not the only risks relating to our business and our Class A Common Stock. Additional risks and uncertainties, including those that are not yet identified or that we currently believe are immaterial, may also adversely affect our business, financial condition, or results of operations. If any of the events described

below occur, our business and financial results could be materially and adversely affected. The market price of our Class A Common Stock could decline due to any of these risks, perhaps significantly, and you could lose part or all of your investment.

A lack of credit and/or limited financing availability to the Company, its vendors, dealers, or end users could adversely affect our business.

The Company’s liquidity and financial condition could be materially and adversely affected if, under its current bank credit agreement, the Company’s ability to borrow money from its existing lenders to finance its operations is reduced or eliminated. Similar adverse effects may also result if the Company realizes lessened credit availability from trade creditors. Additionally, many of our customers require the availability of financing to facilitate the purchase of our products. As a result, a continuing period of reduced credit availability in the marketplace could have adverse effects on the Company’s business.

Increases in the price and demand for raw materials could lower our margins and profitability.

Supreme generally does not have long-term raw material contracts and is dependent upon suppliers of steel, aluminum, wood products, and fiberglass materials, among others, for its manufacturing operations. Consequently, our ability to produce and deliver our products could be affected by disruptions encountered by our raw material suppliers or freight carriers. Additionally, competitive market conditions may prevent the Company from implementing price increases to offset raw material cost increases. As a result the Company’s gross margin could be adversely affected.

Volatility in the supply of vehicle chassis and other vehicle components could adversely affect our business.

With the exception of some specialty vehicle products, the Company generally does not purchase vehicle chassis for its inventory. The Company accepts shipments of vehicle chassis owned by dealers or end-users for the purpose of installing and/or manufacturing its specialized truck bodies on such chassis. Historically, General Motors Corp. (“GM”) and Ford Motor Company (“Ford”) have been the primary suppliers of chassis. In the event of a disruption in supply from one major supplier, the Company would attempt to use another major supplier, but there can be no assurance that this attempt would be successful. Nevertheless, in the event of chassis supply disruptions, there could be unforeseen consequences that may have a significant adverse effect on the Company’s business operations.

The Company also faces risk relative to finance and storage charges for maintaining an excess supply of consigned chassis from GM and Ford. Under the consigned chassis agreements, if a chassis is not delivered to a customer within a specified time frame, the Company is required to pay finance or storage charges on such chassis.

We compete in the highly competitive specialized vehicle industry which may impact our financial results.

The competitive nature of the specialized vehicle industry creates a number of challenges for the Company. Important factors include product pricing, quality of product, lead times, geographic proximity to customers, and the ability to manufacture a product customized to customer specifications. Specialized vehicles are produced by a number of smaller, regional companies which create product pricing pressures that could adversely impact the Company’s profits. Chassis manufacturers have not generally shown an interest in manufacturing specialized vehicles, including truck bodies, because such manufacturers’ highly-automated assembly line operations do not lend themselves to the efficient production of a wide variety of highly-specialized vehicles with various options and equipment.

Demand for our products can be adversely impacted by negative economic trends.

Instability in the U.S. economy, negative conditions in the U.S. credit markets, volatility in the industries that our products serve, or adverse changes in the financial condition of our customers could lead to reduced, cancelled, or delayed orders for our products. Our fleet customers traditionally order our products on an annual basis, but the size of fleet orders may be negatively impacted by the negative economic factors listed above or the size of a fleet customer’s previous order. Additionally, negative economic trends may cause our retail customers to choose not to order, cancel orders, or delay ordering, our products. Such occurrences could adversely affect our cash flows and results of operations.

We have potential exposure to environmental and health and safety liabilities which may increase costs and lower profitability.

Our operations are subject to a variety of federal, state, and local environmental and health and safety statutes and regulations, including those relating to emissions to the air, discharges to water, treatment, storage, and disposal of waste, and remediation of contaminated sites. In certain cases, these requirements may limit the productive capacity of our operations.

Certain laws, including the Federal Comprehensive Environmental Response, Compensation, and Liability Act of 1980, as amended, have imposed strict and, under certain circumstances, joint and several liability for costs to remediate contaminated sites upon designated responsible parties including site owners or operators and persons who dispose of wastes at, or transport wastes to, such sites.

From time to time, we have received notices of noncompliance with respect to our operations. These notices have typically been resolved by investigating the alleged noncompliance and correcting any non-compliant conditions. New environmental requirements, more aggressive enforcement of existing ones, or discovery of presently unknown conditions could require material expenditures or result in liabilities which could limit expansion or otherwise have a material adverse effect on our business, financial condition, and operating cash flows.

A product defect claim in excess of our insurance coverage, or for which we have no insurance, or an inability to acquire or maintain insurance at commercially reasonable rates, could have a materially adverse effect upon our business.

We face an inherent risk of exposure to product liability, product recall, and other product defect related claims, if the use of our current or formerly manufactured products result, or are alleged to result, in personal injury and/or property damage, or if a significant number of our products must be recalled, or if a product defect results in the Company having to refund the purchase price of a substantial number of vehicles. If we manufacture a defective product, we may experience material losses and we may incur significant costs to defend product defect claims. We could also incur damages and significant costs in correcting any defects, experience lost sales, and suffer damage to our reputation. We may not have insurance coverage for certain types of claims or our insurance coverage may not be adequate for liabilities we could incur and may not continue to be available on terms acceptable to us.

Our manufacturer’s warranties expose us to potentially significant claims.

We are subject to product warranty claims in the ordinary course of our business. If we manufacture poor quality products or receive defective materials, we may incur unforeseen costs in excess of what we have reserved in our financial statements. These costs could have a material adverse effect on our business and operating cash flows.

We depend on the services of our key executives. Any loss of our key executives could have a material adverse effect on our operations.

Our ability to compete successfully and implement our business strategy depends on the efforts of our senior management personnel. The loss of the services of any one or more of these individuals could have a material adverse effect on our business. We do not maintain key-man life insurance policies on any of our executives. If we were unable to attract qualified personnel to our management, our existing management resources could become strained, which may harm our business and our ability to implement our strategies.

Our relatively low trading volumes may limit our stockholders’ abilities to buy or sell their shares.

Our Class A Common Stock has experienced, and may continue to experience, price volatility and low trading volumes. Overall market conditions, and other risk factors described herein, may cause the market price of our Class A Common Stock to fall. Our high and low sales prices for the twelve month period ended December 31, 2016 were $19.83 and $5.40, respectively. Our Class A Common Stock is listed on the NYSE MKT exchange under the symbol “STS.” However, daily trading volumes for our Class A Common Stock are, and may continue to be, relatively small compared to many other publicly-traded securities. For example, during the twelve month period ended December 31, 2016, our daily trading volume has been as low as 1,000 shares. It may be difficult for you to buy or sell shares in the public market at any given time at prevailing prices, and the price of our Class A Common Stock may, therefore, be volatile.

Our officers and directors own a large percentage of our common stock. They may vote their shares in ways with which you disagree.

As of February 21, 2017, our officers and directors as a group beneficially owned 19.3% of our Class A Common Stock and 95.8% of our Class B Common Stock. As a result, they will continue to be able to exercise significant influence, and in most cases, control, over matters requiring stockholder approval, including the election of directors, changes to our charter documents, and significant corporate transactions. This concentration of ownership makes it unlikely that any other holder or group of holders of our Class A Common Stock will be able to affect the way we are managed or the direction of our business.

Our split classes of stock may make it more difficult or expensive for a third party to acquire the Company which may adversely affect our stock price.

Our outstanding common stock is split into two classes. The Class A Common Stock is listed on the NYSE MKT exchange, and the holders thereof are entitled to elect three members of the Company’s Board of Directors. The majority (95.8%) of the Class B Common Stock is owned or controlled by the Company’s officers and directors and is entitled to elect the remaining seven members of the Company’s Board of Directors. The continuing ability of the holders of our Class B Common Stock to elect a majority of the members of the Company’s Board of Directors will make it difficult for another company to acquire us and for Class A stockholders to receive any related take-over premium (unless the controlling group approves the sale).

Our internal controls provide only reasonable assurance that objectives are met. Failure of one or more of these controls could adversely affect the Company.

While the Company believes that its control systems are effective, there are inherent limitations in all control systems, and misstatements due to error or fraud may occur and not be detected. The Company continues to take action to comply with the internal controls, disclosure controls, and other requirements of the Sarbanes-Oxley Act of 2002. Management, including our Chief Executive Officer and Chief Financial Officer, cannot guarantee that our internal controls and disclosure controls will prevent all possible errors or all fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. In addition, the design of a control system must reflect the fact that there are resource constraints, and the benefit of controls must be relative to their costs. Because of the inherent limitations in all control systems, no system of controls can provide absolute assurance that all control issues and instances of fraud, if any, within the Company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty and that breakdowns can occur because of simple error or mistake. Further, controls can be circumvented by individual acts of some persons, by collusion of two or more persons, or by management override of the controls. The design of any system of controls is also based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions. Over time, a control may be inadequate because of changes in conditions or the degree of compliance with the policies or procedures may deteriorate. Because of inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and not be detected.

We may not have the ability to sell idle facilities.

We currently own facilities which have been idle for a period of time and are currently being marketed for sale (see Item 2. “Properties”). Although management has exercised its best judgment to reflect accurate current market values of these properties in the Company’s financial statements, there cannot be any assurance that these properties can be sold for these values anytime in the near future.

(See other risk factors listed in Item 7 under the caption: “Forward-Looking Statements”).

ITEM 1B. UNRESOLVED STAFF COMMENTS.

Not applicable.

Set forth below is a brief summary of the properties which are owned or leased by the Company.

|

|

|

Square |

|

Owned or |

|

|

|

|

|

|

Footage |

|

Leased |

|

Operating Segment |

|

|

Manufacturing of Products |

|

|

|

|

|

|

|

|

Goshen, Indiana |

|

540,820 |

|

Owned |

|

Specialized Vehicles |

|

|

Jonestown, Pennsylvania |

|

423,957 |

|

Owned |

|

Specialized Vehicles |

|

|

Griffin, Georgia |

|

190,722 |

|

Owned |

|

Specialized Vehicles |

|

|

Cleburne, Texas |

|

180,785 |

|

Owned |

|

Specialized Vehicles |

|

|

Moreno Valley, California |

|

103,200 |

|

Owned |

|

Specialized Vehicles |

|

|

Moreno Valley, California |

|

13,758 |

|

Leased |

|

Specialized Vehicles |

|

|

|

|

1,453,242 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Manufacturing of Component Parts |

|

|

|

|

|

|

|

|

Ligonier, Indiana |

|

52,142 |

|

Owned |

|

Fiberglass Products |

|

|

|

|

52,142 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Properties for Sale |

|

|

|

|

|

|

|

|

Wilson, North Carolina |

|

113,694 |

|

Owned |

|

Not Applicable |

|

|

Harrisville, Rhode Island |

|

20,000 |

|

Owned |

|

Not Applicable |

|

|

Goshen, Indiana (land only) |

|

— |

|

Owned |

|

Not Applicable |

|

|

|

|

133,694 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Corporate Office Building |

|

|

|

|

|

|

|

|

Goshen, Indiana |

|

26,000 |

|

Owned |

|

Not Applicable |

|

|

|

|

26,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total square footage |

|

1,665,078 |

|

|

|

|

|

In addition, the Company leases approximately 16 acres of land at its Pennsylvania and California locations. The land is used for chassis storage and is leased from unrelated parties.

In an effort to manage its capacity utilization and control its assets, the Company had previously ceased operations at a number of facilities. The North Carolina property and certain Indiana facilities are being marketed for sale or lease and were classified as property, plant, and equipment as of December 31, 2016. The Indiana land and the Rhode Island property were classified as assets held for sale as of December 31, 2016 and are being marketed for sale. The facilities owned or leased by the Company are well maintained, in good condition, and adequate for their intended purposes.

The Company is subject to various investigations, claims, and legal proceedings covering a wide range of matters that arise in the ordinary course of its business activities. Each of these matters is subject to various uncertainties, and it is possible that some of these matters may be resolved unfavorably to the Company. The Company establishes accruals for matters that are probable and reasonably estimable.

On January 3, 2017, an amended complaint was filed against the Company’s subsidiary, Supreme Corporation, in a suit (SVI, Inc. v. Supreme Corporation, Hometown Trolley (a/k/a Double K, Inc.) and Dustin Pence) in the United States District Court, District of Nevada. The amended complaint [followed the original complaint filed on May 16, 2016], from Supreme Corporation’s former trolley distributor, alleges that Supreme Corporation’s sale of its trolley assets to another manufacturer was improper. Claims alleged against Supreme Corporation are as follows: (i) misappropriation of trade secrets; (ii) civil conspiracy/collusion; (iii) tortious interference with contractual relationships; (iv) tortious interference with prospective economic advantage; (v) unjust enrichment; (vi) breach of contract; (vii) breach of the covenant of good faith and fair dealing; (viii) breach of fiduciary duties; (ix) promissory estoppel; (x) declaratory relief establishing a joint venture or partnership; and (xi) cancellation of a trademark registration. The plaintiff alleges that the net present value of the amount lost by the plaintiff is approximately $40,000,000. Supreme Corporation has filed a motion to dismiss which is pending. Due to the inherent risk of litigation, the outcome of this case is uncertain and unpredictable; however, at this time, management believes that the allegations are without merit and is vigorously defending the matter.

On November 4, 2016, a putative class action lawsuit was filed against the Company, Mark Weber (the Company’s Chief Executive Officer) and Matthew W. Long (the Company’s Chief Financial Officer) in the United States District Court for the Central District of California alleging the defendants violated Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and Rule 10b-5 by making material, misleading statements in July 2016 regarding projected backlog. The plaintiff seeks to recover unspecified damages. On February 14, 2017, the court transferred the venue of the case to the Northern District of Indiana upon the joint stipulation of the plaintiff and the defendants. Due to the inherent risk of litigation, the outcome of this case is uncertain and unpredictable; however, at this time, management believes that the allegations are without merit and is vigorously defending the matter.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES.

The Company’s Class A Common Stock is traded on the NYSE MKT exchange (ticker symbol STS). The number of record holders of the Class A Common Stock as of February 21, 2017 was approximately 182. Due to the number of shares held in nominee or street name, it is likely that there are substantially more than 182 beneficial owners of the Company’s Class A Common Stock.

The Company’s Class A Common Stock closed at a price of $18.48 per share on the NYSE MKT exchange on February 21, 2017 on which date there were 15,427,033 shares of Class A Common Stock outstanding. High and low sales prices of the Class A Common Stock for the two-year periods ended December 31, 2016 and December 26, 2015 were:

|

|

|

2016 |

|

2015 |

| ||||||||

|

|

|

High |

|

Low |

|

High |

|

Low |

| ||||

|

1st Quarter |

|

$ |

8.83 |

|

$ |

5.40 |

|

$ |

8.75 |

|

$ |

6.96 |

|

|

2nd Quarter |

|

14.49 |

|

13.94 |

|

8.85 |

|

7.30 |

| ||||

|

3rd Quarter |

|

19.83 |

|

18.65 |

|

8.89 |

|

7.73 |

| ||||

|

4th Quarter |

|

19.34 |

|

11.03 |

|

8.41 |

|

6.76 |

| ||||

All of the 1,656,467 outstanding shares of the Company’s Class B Common Stock were held by a total of 9 persons as of February 21, 2017. There is no established trading market for the Class B Common Stock. The Class B Common Stock is freely convertible on a one-for-one basis into an equal number of shares of Class A Common Stock, and ownership of the Class B Common Stock is deemed to be beneficial ownership of the Class A Common Stock under Rule 13d-3(d) (1) promulgated under the Securities Exchange Act of 1934.

Pursuant to the terms of the Class B Common Stock, 54,371 shares of Class B Common Stock were converted into 54,371 shares of Class A Common Stock during 2016. The shares of Class A Common Stock were issued pursuant to Rule 3(a)(9) of the Securities Act of 1933, as amended.

The Board of Directors approved the following cash dividends on the Company’s outstanding Class A and Class B Common Stock during the years ended December 31, 2016, and December 26, 2015:

|

|

|

|

|

|

|

Cash Dividend |

| |

|

Declaration Date |

|

Record Date |

|

Paid Date |

|

Per Share |

| |

|

March 3, 2015 |

|

March 17, 2015 |

|

March 24, 2015 |

|

$ |

0.025 |

|

|

May 6, 2015 |

|

May 27, 2015 |

|

June 3, 2015 |

|

$ |

0.030 |

|

|

August 5, 2015 |

|

August 24, 2015 |

|

August 31, 2015 |

|

$ |

0.030 |

|

|

November 10, 2015 |

|

December 11, 2015 |

|

January 4, 2016 |

|

$ |

0.300 |

|

|

March 2, 2016 |

|

March 16, 2016 |

|

March 23, 2016 |

|

$ |

0.030 |

|

|

May 25, 2016 |

|

June 9, 2016 |

|

June 16, 2016 |

|

$ |

0.035 |

|

|

August 10, 2016 |

|

August 24, 2016 |

|

August 31, 2016 |

|

$ |

0.035 |

|

|

November 9, 2016 |

|

December 12, 2016 |

|

January 3, 2017 |

|

$ |

0.300 |

|

Future dividend payments will necessarily be subject to business conditions, the Company’s financial position, and requirements for working capital, property, plant and equipment expenditures, and other corporate purposes.

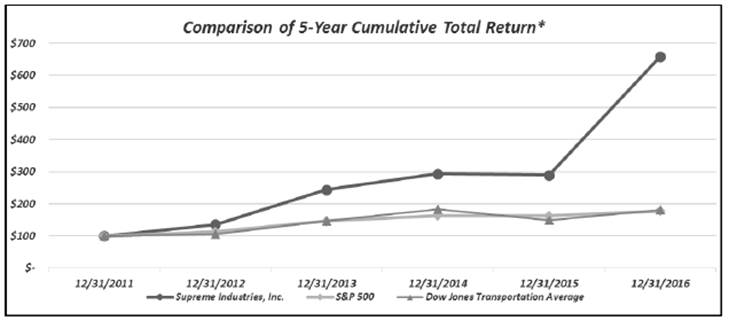

Stock Performance Graph

The following graph compares the cumulative 5-year total return to shareholders of the Company’s common stock relative to the cumulative total return of the S&P 500 Index and the Dow Jones Transportation Average. This graph assumes an initial investment of $100 (with reinvestment of all dividends) to have been made in our Class A Common Stock and the indexes on December 31, 2011 and their relative performance is tracked through December 31, 2016.

|

($) |

|

12/31/2011 |

|

12/31/2012 |

|

12/31/2013 |

|

12/31/2014 |

|

12/31/2015 |

|

12/31/2016 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Supreme Industries, Inc. |

|

100 |

|

136 |

|

244 |

|

294 |

|

290 |

|

658 |

|

|

S&P 500 |

|

100 |

|

113 |

|

147 |

|

164 |

|

162 |

|

178 |

|

|

Dow Jones Transportation Average |

|

100 |

|

106 |

|

147 |

|

182 |

|

150 |

|

180 |

|

* The stock price performance included in this graph is not necessarily indicative of future stock price performance.

ITEM 6. SELECTED FINANCIAL DATA

The following selected financial data has been derived from our consolidated financial statements. The data set forth below should be read in conjunction with Management’s Discussion and Analysis of Financial Condition and Results of Operations and our consolidated financial statements and notes thereto.

All per share data has been adjusted to reflect the five percent (5%) common stock dividend declared and paid during 2013.

|

Consolidated Statement of Continuing Operations Data: |

|

For Fiscal Years Ended |

| |||||||||||||

|

(in millions, except per share amounts) |

|

2016 |

|

2015 |

|

2014 |

|

2013 |

|

2012 |

| |||||

|

Net sales |

|

$ |

299.0 |

|

$ |

278.4 |

|

$ |

236.3 |

|

$ |

246.8 |

|

$ |

239.1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Income from continuing operations |

|

19.0 |

|

12.9 |

|

8.5 |

|

11.2 |

|

12.4 |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Income from continuing operations per share: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Basic earnings per share |

|

1.12 |

|

0.77 |

|

0.52 |

|

0.69 |

|

0.78 |

| |||||

|

Diluted earnings per share |

|

1.11 |

|

0.76 |

|

0.50 |

|

0.68 |

|

0.77 |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Cash dividends paid per common share |

|

.40 |

|

.11 |

|

.025 |

|

— |

|

— |

| |||||

|

Consolidated Balance Sheet Data: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

(in millions) |

|

|

|

|

|

|

|

|

|

|

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Working capital (a) |

|

$ |

58.2 |

|

$ |

51.9 |

|

$ |

43.6 |

|

$ |

36.0 |

|

$ |

36.6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Total assets |

|

134.0 |

|

121.1 |

|

108.9 |

|

110.5 |

|

102.5 |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Total debt |

|

7.5 |

|

8.3 |

|

9.0 |

|

9.7 |

|

14.1 |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Stockholders’ equity |

|

101.7 |

|

88.6 |

|

81.0 |

|

74.1 |

|

67.2 |

| |||||

(a) During the fourth quarter of 2016, the Company reclassified its previously long-term debt to current ($7.5 million at December 31, 2016) as the Credit Agreement is for a period of five years ending on December 19, 2017.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

The following discussion should be read in conjunction with the consolidated financial statements and related notes thereto (see Note 1 “Nature of Operations and Accounting Policies”) located in Item 8 of this document, and pertain to continuing operations unless otherwise noted.

Company Overview

Supreme Industries, Inc., through its wholly-owned subsidiary, Supreme Corporation, is a leading manufacturer of specialized commercial vehicles including truck bodies and specialty vehicles. Established in 1974 and based in Goshen, Indiana, the Company has operations nationwide at seven manufacturing and component locations. In order to serve major geographic markets, these operations are positioned at strategic locations across the continental United States. The Company’s significant brand recognition has a 40-plus-year heritage and offers a complete line of multi-purpose truck bodies. Customers include national rental fleets, national and regional leasing companies, truck dealers and fleet operators. With shipments of more than 20,000 truck bodies annually, the Company offers extensive pool chassis programs with leading light-duty original equipment manufacturers.

Supreme’s extensive truck body product lines include dry-freight, service, refrigerated, and platform/stake bodies. Most of the Company’s products are attached to light-duty and medium-duty truck chassis. Supreme integrates a wide range of options into its truck bodies including liftgates, cargo-handling equipment, customized doors, special bumpers, ladder racks, and refrigeration equipment. Specialty vehicles are designed and customized to move money, dispatch a tactical force, or respond to an emergency to meet many proactive and security needs of its customers.

With a nationwide footprint with seven facilities, the Company’s flexible manufacturing systems support high volume fleets and low volume custom products. Since 2012, the Company has invested more than $25 million in equipment and facilities including building additions, redesigned plant layouts, lean initiatives, and the application of computer-aided design software.

The Company and its product offerings are affected by various risk factors which include, but are not limited to, economic conditions, interest rate fluctuations, volatility in the supply chain of chassis, and the availability of credit and financing to the Company, our vendors, dealers, or end users. The Company’s business is also affected by the availability and costs of certain raw materials that serve as significant components of its product offerings. The Company’s risk factors are disclosed in Item 1A “Risk Factors” of this document.

Results of Operations

Overview

Consolidated net sales for the year ended December 31, 2016 increased 7.4% to $299.0 million, compared with $278.4 million for the year ended December 26, 2015. The sales growth was the result of continued strong demand in both retail and fleet truck body markets when compared with the prior year, which more than offset a decline in sales of specialty vehicles and trolleys.

The sales order backlog at the end of 2016 totaled $83.4 million, down 15.0% compared with $98.1 million at the end of 2015. The decline in backlog was due to lower retail orders received during the fourth quarter of 2016 compared with the fourth quarter of 2015. However, retail orders increased 11% sequentially from the third quarter of 2016.

For the year ended December 31, 2016, gross profit increased by $12.9 million, or 23.8%, to $67.1 million as compared with $54.2 million for the year ended December 26, 2015. Gross margin, as a percentage of net sales improved to 22.4% for the year ended December 31, 2016, as compared with 19.5% for the year ended December 26, 2015. The increase was the result of a favorable product mix including a higher proportion of retail truck sales which typically yield a higher gross margin. Additionally, improved capacity utilization and the fixed nature of certain overhead costs that do not fluctuate with the change in the higher sales volume contributed to the gross margin percentage improvement. The gross margin was negatively impacted by costs and charges associated with a product recall, higher repairs and maintenance due to plant reconfigurations and increased group health insurance costs.

On May 6, 2016, the Company submitted a Defect Information Report to the United States National Highway Traffic Safety Administration (NHTSA) reporting a potential safety defect. Supreme has notified affected customers and directed them to take their vehicle to an approved service center for installation of an appropriate amperage in-line fuse and a warning decal at no charge to the

customer. The Company has estimated its cost for the recall would be no more than $0.5 million which was accrued during the first half of 2016. The balance of the accrual, net of payments and reserve adjustments, was $0.1 million at December 31, 2016.

During the fourth quarter of 2016, the Company consolidated its Rhode Island service center into the Pennsylvania manufacturing campus, which will allow the Company to improve support levels across the East Coast while reducing overhead costs.

Selling, general and administrative expenses increased by $3.2 million, or 9.2%, to $38.5 million for the year ended December 31, 2016 as compared with $35.3 million for the year ended December 26, 2015. The increase was primarily due to higher commission expense on the increased sales volume, higher wages and related costs as the Company added key personnel, annual merit increases and profit-based incentive compensation plans.

The Company recorded income tax expense of $9.4 million at an effective tax rate of 33.1% for the year ended December 31, 2016, compared with $6.3 million at an effective tax rate of 32.9% for the year ended December 26, 2015. The increase in the effective tax rate was due to a change in state apportioned income at different tax rates, additional reserves for uncertain tax positions and a valuation allowance for certain tax credit carryforwards and state net operating losses. Additionally, the rates differ from the federal statutory rate primarily because of varying state income tax rates and permanent federal income tax differences including benefits from a captive insurance company and the domestic manufacturer deduction.

Net income for the year ended December 31, 2016 was $19.0 million, or $1.11 per diluted share, compared with net income of $12.9 million, or $0.76 per diluted share, for the comparable period last year.

On May 11, 2016, the Company entered into an Asset Purchase Agreement for the sale of certain assets of the Company’s trolley business. Trolley products represented less than 2% of the Company’s consolidated net sales in 2016 and 2015. The after-tax impact on consolidated operations for both periods was immaterial. The first stage of the transaction closed on June 30, 2016 and the final stage of the transaction is scheduled to close in the first half of 2017. The Company anticipates no material gain or loss will be recognized on the sale. The sale of the trolley business does not meet the criteria of the Financial Accounting Standards Board (“FASB”) ASU 2014-8 (Reporting Discontinued Operations and Disclosure of Disposals of Components of an Entity) and will not be reported as discontinued operations.

Working capital increased to $58.2 million at December 31, 2016, compared with $51.9 million at December 26, 2015. The Company ended the year with $35.2 million in cash and cash equivalents and $7.2 million in total debt (net of bank amortization fees of $0.3 million). Stockholders’ equity increased to $101.7 million at year end, compared with $88.6 million at December 26, 2015. Supreme invested $3.7 million in facilities and equipment during 2016, compared with $3.9 million in 2015. Net cash provided by operating activities during the year ended December 31, 2016 totaled $29.3 million, compared with $9.8 million in 2015.

As we closed 2016, the Company’s strong performance was primarily the result of focusing resources on several key initiatives including:

· Supplementing our sales team to maximize regional and national account coverage;

· Deployment of lean manufacturing techniques to reduce waste and cycle times;

· Reconfiguration and consolidation of the Indiana manufacturing campus:

· Consolidation of the Rhode Island service center into our Pennsylvania manufacturing plant to improve efficiencies and;

· Divestiture of the trolley product line to focus resources on advancing our work truck strategy.

These initiatives are expected to allow continued growth and help us leverage our existing capacity. Additionally, Supreme’s strong financial position has allowed the Company to invest in growth initiatives while continuing to pay quarterly cash dividends to shareholders. The Board of Directors declared a special cash dividend of $0.265 (26 ½ cents) per common share during the fourth quarter as a means of returning a portion of excess cash flow to shareholders. This was in addition to an increase in the regular quarterly cash dividend of $0.035 (3 ½ cents) per common share announced earlier in the year, and reflects the Board’s assessment of our current financial condition, cash flow and business outlook. Future dividend payments will necessarily be subject to business conditions, the Company’s financial position, and requirements for working capital, property, plant and equipment expenditures, and other corporate purposes.

Comparison of 2016 with 2015

Net sales

Net sales for the year ended December 31, 2016 increased $20.5 million, or 7.4%, to $299.0 million as compared with $278.4 million for the year ended December 26, 2015.

Truck sales increased $23.4 million, or 8.9%, in 2016 due to higher truck sales of both retail and fleet customers. The delivery of high-quality products has allowed the Company to grow at a faster rate than our core industry resulting in top-line growth and improved profitability. Trolley sales decreased $1.2 million, or 22.0%, for the year ended December 31, 2016 when compared with the year ended December 26, 2015. With the divestiture of the trolley product line, the Company will utilize its existing resources to focus on our work truck strategy. Specialty vehicle sales for 2016 decreased $2.1 million, or 29.4%, compared with 2015. Using existing products and capabilities as a foundation and an improved lower cost structure, we continue to look for opportunities to expand product offerings and our customer base for our specialty vehicle product lines. Our fiberglass facility supplies fiberglass-reinforced plywood to Supreme for use in the production of certain truck bodies and also sells to third parties. The fiberglass product sales to third parties increased $0.5 million, or 14.0%, for the year ended December 31, 2016 compared with 2015.

Cost of sales and gross profit

Gross profit increased by $12.9 million, or 23.8%, to $67.1 million for the year ended December 31, 2016 as compared with $54.2 million for the year ended December 26, 2015. Gross margin, as a percentage of net sales improved to 22.4%, for the year ended December 31, 2016 as compared with 19.5% for the year ended December 26, 2015.

Material cost as a percentage of net sales improved by 2.5% for the year ended December 31, 2016 as compared with 2015. The improvement was the result of a favorable product mix as we experienced a higher proportion of retail truck sales which typically yield a higher gross margin. Direct labor as a percentage of net sales remained consistent for the year ended December 31, 2016 as compared with 2015. Manufacturing overhead as a percentage of net sales decreased by 0.4% for the year ended December 31, 2016 as compared with 2015 due to improved capacity utilization and the fixed nature of certain overhead costs that do not fluctuate with the higher sales volume for 2016. The gross margin improvement was negatively impacted by costs and charges associated with a product recall, higher repairs and maintenance due to plant rearrangements and increased group health insurance costs. Increased market demand for certain commodities can result in fluctuating costs of raw materials and other items we utilize in our production processes and, accordingly, the Company closely monitors major commodities to identify any raw material cost movements and attempts to pass them on to customers through price increases.

Delivery expense as a percentage of net sales decreased to 1.7% for the year ended December 31, 2016 as compared with 1.8% at December 26, 2015. The slight decrease was due to changes in both product mix and customer shipment requirements.

Selling, general and administrative expenses

Selling, general and administrative expenses increased by $3.2 million, or 9.2%, to $38.5 million for the year ended December 31, 2016 as compared with $35.3 million for the year ended December 26, 2015.

Selling expenses for the year ended December 31, 2016 increased $1.3 million to $12.1 million as compared with $10.8 million for the year ended December 26, 2015. As a percentage of net sales, selling expenses increased 0.2% for the year ended December 31, 2016 as compared with 2015. The dollar increase was primarily due to higher commission expense on the higher sales volume, higher sales wages and related costs as the Company added sales personnel in key regions, annual merit increases and higher original equipment manufacturing (OEM) marketing expenses.

General and administrative expenses for the year ended December 31, 2016 increased $1.9 million to $26.4 million as compared with $24.5 million for the year ended December 26, 2015. As a percentage of net sales, general and administrative expenses remained consistent at 8.8% of the net sales for the years ended December 31, 2016 and December 26, 2015. The dollar increase was mainly the result of profit-based incentive compensation plans, higher salary costs related to adding strategic new hires and annual merit increases.

Other income

For the year ended December 31, 2016, other income was $0.3 million, or 0.1% of net sales, as compared with other income of $0.4 million, or 0.1% of net sales, for the year ended December 26, 2015. Other income consisted of rental income, gain on the sale of assets, and other miscellaneous income received by the Company.

Interest expense

Interest expense was $0.5 million for the year ended December 31, 2016 as compared with $0.1 million for the year ended December 26, 2015. Interest expense includes bank debt and chassis interest on bailment pool chassis offset by interest support received from the chassis manufacturers. Interest expense for the year ended 2016 increased due to higher chassis interest expense as the Company carried elevated levels of bailment pool chassis to meet customer demand. During the year ended December 26, 2015, the Company received interest income from chassis manufacturers which more than offset chassis interest due to demand for pool chassis outpacing the supply. The interest income partially offset the combination of chassis interest expense and interest on bank debt. The effective interest rate on bank borrowings was 3.05% at 2016 year-end, and the Company was in compliance with all provisions of its Credit Agreement.

Income taxes

For the year ended December 31, 2016, the Company recorded income tax expense of $9.4 million at an effective tax rate of 33.1% compared with $6.3 million at an effective tax rate of 32.9% for the year ended December 26, 2015. The increase in the effective tax rate was due to a change in state apportioned income at different tax rates, additional reserves for uncertain tax positions and a valuation allowance for certain tax credit carryforwards and state net operating losses. Additionally, the rates differ from the federal statutory rate primarily because of varying state income tax rates and permanent federal income tax differences including benefits from a captive insurance company and the allowable domestic manufacturer deduction.

Net Income

Reported net income for the year ended December 31, 2016 was $19.0 million, or $1.11 per diluted share, compared with net income of $12.9 million, or $0.76 per diluted share in 2015.

Basic and diluted income (loss) per share

The following table presents basic and diluted income per share and the changes from period to period:

|

|

|

2016 |

|

2015 |

|

Change |

| |||

|

Earnings per share: |

|

|

|

|

|

|

| |||

|

Basic |

|

$ |

1.12 |

|

$ |

0.77 |

|

$ |

0.35 |

|

|

Diluted |

|

$ |

1.11 |

|

$ |

0.76 |

|

$ |

0.35 |

|

Comparison of 2015 with 2014

Net sales

Net sales for the year ended December 26, 2015 increased $42.1 million, or 17.8%, to $278.4 million as compared with $236.3 million for the year ended December 27, 2014.

Truck sales increased $49.6 million, or 23.4%, for the 2015 year due to higher truck sales of both retail and fleet customers. Trolley sales decreased $2.7 million, or 32.7%, for the year ended December 26, 2015 when compared with the year ended December 27, 2014. Specialty vehicle sales for 2015 decreased $6.5 million, or 47.1%, compared with 2014 due to overall lower order volume and the completion of a large US Department of State contract in 2014. Our fiberglass facility supplies fiberglass-reinforced plywood to Supreme for use in the production of certain truck bodies and also sells to third parties. The fiberglass product sales to third parties increased $1.7 million, or 81.6%, for the year ended December 26, 2015 compared with 2014.

Cost of sales and gross profit

Gross profit increased by $10.4 million, or 23.7%, to $54.2 million for the year ended December 26, 2015 as compared with $43.8 million for the year ended December 27, 2014. Gross margin as a percentage of net sales improved by 90 basis points to 19.5%, for the year ended December 26, 2015 as compared with 18.6% for the year ended December 27, 2014.

Material cost as a percentage of net sales increased by 0.8% for the year ended December 26, 2015 as compared with 2014. The increase in the material cost percentage was due in part to a change in product mix with a higher proportion of fleet shipments and liftgate sales which carry a higher material cost percentage. Conversely, the material cost percentage was favorably impacted by decreased prices of steel and aluminum late in the year as well as an increase in supplier discounts. Direct labor as a percentage of net sales improved by 1.4% for the year ended December 26, 2015 as compared with 2014. The decrease was the result of improved

utilization aided by higher production and sale levels and production of large quantities of similar fleet units. Additionally, the first quarter of 2014 was negatively impacted by labor inefficiencies resulting from shortages of light-duty chassis from a major chassis supplier and extreme weather conditions causing inefficiencies in the movement, scheduling and production of truck bodies. Manufacturing overhead as a percentage of net sales increased slightly by 0.1% for the year ended December 26, 2015 as compared with 2014 due to higher wages including annual merit increases, maintenance repairs and group health insurance costs partially offset by improved worker compensation expense in 2015 when compared with 2014.

Delivery expense as a percentage of net sales decreased to 1.8% for the year ended December 26, 2015 as compared with 2.2% at December 27, 2014 due to changes in both product mix and customer shipment requirements.

Selling, general and administrative expenses

Selling, general and administrative expenses increased by $4.0 million, or 12.6%, to $35.3 million for the year ended December 26, 2015 as compared with $31.3 million for the year ended December 27, 2014.

Selling expenses for the year ended December 26, 2015 increased $0.9 million to $10.8 million as compared with $9.9 million for the year ended December 27, 2014. As a percentage of net sales, selling expenses decreased 0.3% for the year ended December 26, 2015 as compared with 2014. The dollar increase was partially due to higher sales compensation and related costs as the Company enhanced its market presence by adding and upgrading sales personnel in key regions and annual merit increases. Additionally, sales commissions increased as a result of the higher sales volume.

General and administrative expenses for the year ended December 26, 2015 increased $3.1 million to $24.5 million as compared with $21.4 million for the year ended December 27, 2014. As a percentage of net sales, general and administrative expenses decreased 0.3% for the year ended December 26, 2015 as compared with 2014. The dollar increase was mainly the result of profit-based incentive plans, higher compensation costs related to annual merit increases and higher group health insurance claims.

Other income

For the year ended December 26, 2015, other income was $0.4 million, or 0.1% of net sales, as compared with other income of $0.5 million, or 0.2% of net sales, for the year ended December 27, 2014. Other income consisted of rental income, gain on the sale of assets, and other miscellaneous income received by the Company.

Interest expense

Interest expense was $0.1 million for the year ended December 26, 2015 as compared with $0.5 million for the year ended December 27, 2014. Interest expense includes bank debt and chassis interest on bailment pool chassis offset by interest support received from the chassis manufacturers. The effective interest rate on bank borrowings was 2.79% at 2015 year-end, and the Company was in compliance with all provisions of its Credit Agreement.

Income taxes

For the year ended December 26, 2015, the Company recorded income tax expense of $6.3 million at an effective tax rate of 32.9% compared with $4.0 million at an effective tax rate of 32.1% for the year ended December 27, 2014. The rates differ from the statutory rate primarily because of varying state income tax rates and permanent federal income tax differences including benefits from a captive insurance company and the allowable domestic manufacturer deduction.

Income from continuing operations

Income from continuing operations for year ended December 26, 2015 was $12.9 million, or $0.76 per diluted share, compared with income from continuing operations of $8.5 million, or $0.50 per diluted share, for the year ended December 27, 2014.

Discontinued operations

The Company decided to discontinue its shuttle bus operations on December 31, 2013 and on February 28, 2014, the Company entered into an agreement for the sale of certain assets of those operations. Accordingly, the Company classified the results as discontinued operations. For the year ended December 27, 2014, the after-tax loss from discontinued operations was $1.6 million. There was no financial impact of these operations on the 2015 results.

Net Income

Reported net income for the year ended December 26, 2015 was $12.9 million, or $0.76 per diluted share, compared with net income of $6.9 million, or $0.41 per diluted share in 2014.

Basic and diluted income (loss) per share

The following table presents basic and diluted income (loss) per share and the changes from period to period:

|

|

|

2015 |

|

2014 |

|

Change |

| |||

|

Basic income (loss) per share: |

|

|

|

|

|

|

| |||

|

Income from continuing operations |

|

$ |

0.77 |

|

$ |

0.52 |

|

$ |

0.25 |

|

|

Loss from discontinued operations |

|

— |

|

(0.10 |

) |

0.10 |

| |||

|

Net income per basic share |

|

$ |

0.77 |

|

$ |

0.42 |

|

$ |

0.35 |

|

|

|

|

|

|

|

|

|

| |||

|

Diluted income (loss) per share: |

|

|

|

|

|

|

| |||

|

Income from continuing operations |

|

$ |

0.76 |

|

$ |

0.50 |

|

$ |

0.26 |

|

|

Loss from discontinued operations |

|

— |

|

(0.09 |

) |

0.09 |

| |||

|

Net income per diluted share |

|

$ |

0.76 |

|

$ |

0.41 |

|

$ |

0.35 |

|

Liquidity and Capital Resources

Cash Flows

The Company’s primary sources of liquidity have been cash flows from operating activities and borrowings under its Credit Agreement. Principal uses of cash have been to support working capital needs, fund capital expenditures, pay cash dividends, and meet debt service requirements.

Operating activities

Cash flows from operations represent the net income earned in the reported periods adjusted for non-cash charges and changes in operating assets and liabilities. Net cash from operating activities totaled $29.3 million for the year ended December 31, 2016 as compared with $9.8 million for the year ended December 26, 2015. Net income was $19.0 million in 2016 compared with $12.9 million in 2015. Changes in operating assets and liabilities were impacted by a $4.9 million decrease in accounts receivable due to lower sales in the fourth quarter of 2016 as compared with the same period in 2015. Inventories decreased $0.7 million due to a lower year-over-year sales order backlog. These increases in cash from operating activities were partially offset by a $1.1 million decrease in trade accounts payable due to the lower inventories.

Net cash from operating activities totaled $9.8 million for the year ended December 26, 2015 as compared with $9.5 million for the year ended December 27, 2014. Net income was $12.9 million in 2015 compared with $6.9 million in 2014. Changes in operating assets and liabilities were impacted by a $7.1 million increase in accounts receivable due to increased sales, and a $2.3 million increase in inventories caused by the year-over-year increase in sales order backlog. Despite the increase in inventories, trade accounts payable decreased by $1.0 million as a result of the acceleration of vendor payments to take advantage of discount payment terms. These uses of cash flow were partially offset by a $1.0 million return of cash deposits from the Company’s former workers compensation insurance carrier as a result of lower collateral requirements associated with having fewer and lower open claims.

Investing activities

Cash used by investing activities was $3.7 million for the year ended December 31, 2016 as compared with $2.1 million for the year ended December 26, 2015. During 2016, the Company’s capital expenditures totaled $3.7 million which predominantly related to property and plant improvements.

Cash used by investing activities was $2.1 million for the year ended December 26, 2015 as compared with $1.1 million for the year ended December 27, 2014. During 2015, the Company’s capital expenditures totaled $3.9 million and included facilities and equipment to enhance manufacturing efficiencies. Investing activities in 2015 provided cash of $1.0 million resulting from the routine sale of investments by the Company’s captive insurance subsidiary. Additionally, the Company received $0.9 million from the sale of two smaller facilities including a facility in Missouri, which was being leased to an unrelated party, and an idle facility in Indiana.

Financing activities

Financing activities used $7.7 million of cash for the year ended December 31, 2016 as compared with cash used of $2.0 million for the year ended December 26, 2015. During 2016, the Company used $6.8 million to pay cash dividends to its shareholders, and used $0.8 million to make scheduled quarterly principal payments on its outstanding term loan.

Financing activities used $2.0 million of cash for the year ended December 26, 2015 as compared with cash used of $0.7 million for the year ended December 27, 2014. During 2015, the Company used $1.8 million to pay cash dividends to its shareholders, and used $0.7 million to make scheduled quarterly principal payments on its outstanding term loan. These payments were partially offset by $0.6 million received from the exercise of stock options.

Capital Resources

On December 19, 2012, the Company entered into an Amended and Restated Credit Agreement (the “Credit Agreement”) with Wells Fargo Bank, National Association (“Wells Fargo”). Under the terms of the Credit Agreement, Wells Fargo agreed to provide to the Company a credit facility of up to $45.0 million consisting of a revolving credit facility, a term loan facility, and a letter of credit facility. The Credit Agreement is for a period of five years ending on December 19, 2017. The Company had unused credit capacity of $35.0 million at December 31, 2016. Interest on outstanding borrowings under the Credit Agreement is based on Wells Fargo’s prime rate or LIBOR depending on the pricing option selected and the Company’s leverage ratio (as defined in the Credit Agreement) resulting in an effective interest rate of 3.05% at December 31, 2016. Pursuant to the Credit Agreement, the financial covenants include a consolidated total leverage ratio, a consolidated fixed charge coverage ratio, and a limitation on annual capital expenditures. As of December 31, 2016 and December 26, 2015, the Company was in compliance with all three financial covenants. On August 27, 2014, the Company entered into an amendment of the Credit Agreement. The amendment changed the cash dividend limit from a percentage of consolidated net income for the immediately preceding fiscal quarter to a flat per fiscal quarter limit of $0.03 per share of capital stock then issued and outstanding. On November 19, 2015, the Company entered into an amendment of the Credit Agreement. The amendment permitted the Company to issue a special dividend of up to $6.5 million on or about January 4, 2016 and changed the cash dividend limit from a flat per fiscal quarter limit of $0.03 per share of capital stock then issued and outstanding to an amount paid in any fiscal quarter not to exceed an amount equal to 50% of the consolidated net income for the immediately preceding fiscal quarter. On November 16, 2016, the Company entered into an amendment of the Credit Agreement. The amendment permitted the Company to issue a special dividend of up to $6.5 million on or about January 2, 2017.

Revolving Credit Facility

The revolving credit facility provides for borrowings of up to $35.0 million. The revolving credit facility bears interest at (i) LIBOR plus a margin which varies from 1.50% to 2.50% based upon a leverage ratio of total indebtedness to trailing four quarter EBITDA or (ii) the higher of (a) the prime rate and (b) the federal funds rate plus 0.50% plus a margin which varies from 0.50% to 1.50% based upon the debt to EBITDA leverage ratio. The revolving credit facility also requires a quarterly commitment fee ranging from 0.20% to 0.50% per annum depending on the Company’s financial ratios and based upon the average daily unused portion. As of December 31, 2016, and December 26, 2015, there were no borrowings against the revolving credit facility.

Term Loan Facility