Attached files

| file | filename |

|---|---|

| EX-32 - EX-32 - FreightCar America, Inc. | d357109dex32.htm |

| EX-31.2 - EX-31.2 - FreightCar America, Inc. | d357109dex312.htm |

| EX-31.1 - EX-31.1 - FreightCar America, Inc. | d357109dex311.htm |

| EX-23 - EX-23 - FreightCar America, Inc. | d357109dex23.htm |

| EX-21 - EX-21 - FreightCar America, Inc. | d357109dex21.htm |

| EX-10.27 - EX-10.27 - FreightCar America, Inc. | d357109dex1027.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

or

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 000-51237

FREIGHTCAR AMERICA, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 25-1837219 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| Two North Riverside Plaza, Suite 1300, Chicago, Illinois | 60606 | |

| (Address of principal executive offices) | (Zip Code) | |

(800) 458-2235

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of class |

Name of Each Exchange on Which Registered | |

| Common stock, par value $0.01 per share | Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☐ NO ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☒ NO ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment of this Form 10-K. ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ☒ NO ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.:

| Large accelerated filer | ☐ | Accelerated filer | ☒ | |||

| Non-accelerated filer | ☐ (Do not check if a smaller reporting company) | Smaller reporting company | ☐ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ☐ NO ☒

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant as of June 30, 2016 was $169.0 million, based on the closing price of $14.05 per share on the Nasdaq Global Market.

As of February 24, 2017, there were 12,400,614 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

| Documents | Part of Form 10-K | |

| Portions of the registrant’s definitive Proxy Statement for the 2017 annual meeting of stockholders to be filed pursuant to Regulation 14A within 120 days of the end of the registrant’s fiscal year ended December 31, 2016. | Part III |

Table of Contents

FREIGHTCAR AMERICA, INC.

2

Table of Contents

OVERVIEW

We are a diversified manufacturer of railcars and railcar components. We design and manufacture a broad variety of railcar types for transportation of bulk commodities and containerized freight products primarily in North America, including open top hoppers, covered hoppers, and gondolas along with intermodal and non-intermodal flat cars. We and our predecessors have been manufacturing railcars since 1901. Over the last several years, we have introduced a number of new or redesigned railcar types as we continue to diversify our product portfolio away from coal cars. We believe we are the leading manufacturer of aluminum-bodied railcars including coal cars in North America, based on the number of railcars delivered.

Our railcar manufacturing facilities are located in Cherokee, Alabama (“Shoals”), Danville, Illinois and Roanoke, Virginia. Our Shoals facility is an important part of our long-term growth strategy as we continue to expand our railcar product and service offerings. Our Shoals facility delivered its first railcars during the fourth quarter of 2013 and additional production capacity became operational during the second quarter of 2015. Our Roanoke facility has the capacity to build a variety of railcar types in a cost effective manner and will continue to support our coal car products when market conditions improve. Our Danville facility resumed production in June 2014 after being idled for 14 months and, given the challenged coal market, operations there were again significantly curtailed in 2016. In light of the current cyclical downturn in the railcar industry and the challenged coal market, we will be idling our Danville facility for railcar production effective March 31, 2017.

We lease freight cars through our JAIX Leasing Company subsidiary. Although we continually look for opportunities to package our leased assets for sale to our leasing company partners, these leased assets may not be converted to sales, and may remain revenue producing assets into the foreseeable future. We also refurbish and rebuild railcars and sell forged, cast and fabricated parts for all of the railcars we produce, as well as those manufactured by others.

Our primary customers are railroads, shippers and financial institutions, which represented 45%, 30% and 23%, respectively, of our total sales attributable to each type of customer for the year ended December 31, 2016. In the year ended December 31, 2016, we delivered 5,559 railcars, including 43 coal cars, which compared to 8,980 railcars, including 3,395 coal cars, delivered in the year ended December 31, 2015. Our deliveries for the year ended December 31, 2016 included 227 rebuilt railcars compared to 2,600 rebuilt railcars delivered in 2015. Our total backlog of firm orders for railcars decreased from 9,840 railcars as of December 31, 2015 to 4,259 railcars as of December 31, 2016. Our backlog as of December 31, 2016 includes a variety of railcar types, all of which were orders for non-coal cars. The estimated sales value of our backlog is $419 million as of December 31, 2016.

Our Internet website is www.freightcaramerica.com. We make available, free of charge, on or through our website items related to Corporate governance, including, among other things, our Corporate governance guidelines, charters of various committees of the Board of Directors and our code of business conduct and ethics. Our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, and amendments thereto, are available on our website and on the SEC’s website at www.sec.gov. Any stockholder of our company may also obtain copies of these documents, free of charge, by sending a request in writing to Investor Relations at FreightCar America, Inc., Two North Riverside Plaza, Suite 1300, Chicago, Illinois 60606.

OUR PRODUCTS AND SERVICES

We design and manufacture a broad variety of freight cars including covered hoppers, open top hoppers, gondolas, intermodal and non-intermodal flat cars that transport numerous types of dry bulk and containerized freight products.

In the last five years, we have added 33 new or redesigned products to our portfolio, including various covered hopper car products with cubic capacities from 3,282 cubic foot to 6,250 cubic foot; 52’ and 66’ mill gondolas; coil gondolas; triple hoppers and hybrid aluminum/stainless steel railcars; ore hopper and gondola railcars; ballast hopper cars; aggregate hopper cars (with manual, independent or fully automatic transverse or longitudinal door

3

Table of Contents

systems); intermodal flats (including the 3-unit, 53-foot well cars) and non-intermodal flat cars (including slab, hot slab, ribbon rail and bulkhead flats). Focused product development activity continues in areas where we can leverage our technical knowledge base and capabilities to realize market opportunities.

The types of railcars listed below include the major types of railcars that we are capable of manufacturing; however, some of the types of railcars listed below have not been ordered by any of our customers or manufactured by us in a number of years. We rebuild railcars and sell forged, cast and fabricated parts for all of the railcars we produce, as well as those manufactured by others. Many of our railcars are produced using a patented one-piece center sill, the main longitudinal structural component of the railcar. The one-piece center sill provides a higher carrying capacity, but weighs significantly less than traditional multiple-piece center sills. In addition to railcars designed for use in North America, we have manufactured railcars for export to Latin America and the Middle East. Railroads outside of North America are constructed with a variety of track gauges that are sized differently than in North America, which requires us, in some cases, to alter our manufacturing specifications accordingly.

Any of the railcar types listed below may be further developed to meet the characteristics of the materials being transported and customer specifications.

| • | VersaFlood Hopper Cars. The VersaFlood™ product series offers versatile design options for transportation of aggregates, sand or minerals. Our VersaFlood™ series open-top hopper railcars include steel, stainless steel or hybrid steel and aluminum-bodied designs equipped with three-pocket (transverse gate) or two-pocket (longitudinal gate) discharge door systems with manual, independent or fully automatic door operation. |

| • | Covered Hopper Cars. Our covered hopper railcar product offerings encompass a wide range of cubic foot (cf) capacity designs for shipping dry bulk commodities of varying densities including: 3,282 cf covered hopper cars for cement, sand and roofing granules; 4,300 cf covered hopper cars for potash or similar commodities; 5,200 cf and 5,400 cf covered hopper cars for grain and other agricultural products; and 5,800 cf and 6,250 cf covered hopper cars for plastic pellets. |

| • | Dynastack Series. Our intermodal doublestack railcar product offerings include a stand-alone 40 foot well car, the DynaStack® articulated, 5-unit, 40 foot and the DynaStack® articulated 3-unit, 53 foot well cars for transportation of international and domestic containers. |

| • | Boxcars. Our high capacity boxcar railcar product offerings, featuring inside length of 50’ and 60’9”, double plug doors, galvanized steel roof panels and nailable steel floors, primarily designed for transporting paper products, paper rolls, lumber and wood products and foodstuffs. |

| • | Aluminum Coal Cars. The BethGon® is the leader in the aluminum-bodied coal gondola railcar segment. Since we introduced the steel BethGon railcar in the late 1970s and the aluminum BethGon railcar in 1986, the BethGon railcar has become the most widely used coal car in North America. Our current BethGon II features lighter weight, higher capacity and increased durability suitable for long-haul coal carrying railcar service. We have received several patents on the features of the BethGon II and continue to explore ways to increase the BethGon II’s capacity and reliability. |

Our aluminum bodied open-top hopper railcar, the AutoFlood™, is a five-pocket coal car equipped with a bottom discharge gate mechanism. We began manufacturing AutoFlood railcars in 1984, and introduced the AutoFlood II and AutoFlood III designs in 1996 and 2002, respectively. Both the AutoFlood II and AutoFlood III designs incorporate the automatic rapid discharge system, the MegaFlo™ door system, a patented mechanism that uses an over-center locking design, enabling the cargo door to close with tension rather than by compression. Further, AutoFlood railcars can be equipped with rotary couplers to permit rotary unloading.

| • | Stainless Steel and Hybrid Stainless Steel/Aluminum Coal Cars. We manufacture a series of stainless steel and hybrid stainless steel and aluminum AutoFlood and BethGon coal cars designed to serve the Eastern railroads. These coal cars are designed to withstand the rigors of Eastern coal transportation service. They offer a unique balance of maximized payload, light weight, efficient unloading and long service life. Our coal car product offerings include aluminum-bodied flat-bottom gondola railcars and steel or stainless steel-bodied triple hopper railcars for coal, metallurgical coke and petroleum coke service. |

4

Table of Contents

| • | Steel Products Cars. Our portfolio of railcar types also includes 52’ and 66’ mill gondola railcars used to transport steel products and scrap; slab, hot slab and coil steel railcars designed specifically for transportation of steel slabs and coil steel products, respectively. |

| • | Other Railcar Types. Our other railcar types include non-intermodal flat railcars and bulkhead flat railcars designed to transport a variety of products, including machinery and equipment, steel and structural steel components (including pipe), wood and forest products and other bulk industrial products; woodchip hopper and gondola railcars designed to haul woodchips and municipal waste or other low-density commodities; and a variety of non-coal carrying open top hopper railcars designed to carry ballast, iron ore, taconite pellets and other bulk commodities; the AVC™ Aluminum Vehicle Carrier design used to transport commercial and light vehicles (automobiles and trucks) from assembly plants and ports to rail distribution centers; and the articulated bulk container railcar designed to carry dense bulk products such as waste products in 20 foot containers. |

MANUFACTURING

We have railcar production facilities in Cherokee, Alabama, Danville, Illinois and Roanoke, Virginia. Our facilities are each certified or approved for certification by the Association of American Railroads (the “AAR”), which sets railcar manufacturing industry standards for quality control. Our Shoals manufacturing facility delivered its first railcars during the fourth quarter of 2013 and provides a solid platform from which to pursue a broad range of non-coal car business including intermodal well cars, non-intermodal flat cars and various open-top hopper, covered hopper and gondola cars. During 2015, we expanded our Shoals facility to add additional production capacity to meet demand for our new types of railcars. On February 27, 2017, we announced that our Danville facility would be idled for railcar production effective March 31, 2017.

Our manufacturing process involves four basic steps: fabrication, assembly, finishing and inspection. Each of our facilities has numerous checkpoints at which we inspect products to maintain quality control, a process that our operations management continuously monitors. In our fabrication processes, we employ standard metal working tools, many of which are computer controlled. Each assembly line typically involves 15 to 20 manufacturing positions, depending on the complexity of the particular railcar design. We use mechanical fastening in the fitting and assembly of our aluminum-bodied railcar parts, while we typically use welding for the assembly of our steel-bodied railcars. For aluminum-bodied railcars, we begin the finishing process by cleaning the railcar’s surface and then applying the decals. In the case of steel-bodied railcars, we begin the finishing process by blasting the surface area of the railcar, painting it and then applying decals. Once we have completed the finishing process, our employees, along with representatives of the customer purchasing the particular railcars, inspect all railcars for adherence to specifications.

CUSTOMERS

We have strong long-term relationships with many large purchasers of railcars. Long-term customer relationships are particularly important in the railcar industry, given the limited number of buyers of railcars.

Our customer base consists mostly of North American railroads, shippers and financial institutions. We believe that our customers’ preference for reliable, high-quality products, the relatively high cost for customers to switch manufacturers, our technological leadership in developing and enhancing innovative products and the competitive pricing of our railcars have helped us maintain our long-standing relationships with our customers.

In 2016, revenue from three customers, CIT Rail, Norfolk Southern Railway Company and ECN Capital Corporation, accounted for approximately 23%, 16% and 15%, respectively, of total revenue. In 2016, sales to our top five customers accounted for approximately 73% of total revenue. In 2015, revenue from three customers, Norfolk Southern Railway Company, CSX Transportation Inc. and CIT Rail, accounted for approximately 22%, 19% and 10%, respectively, of total revenue. In 2015, sales to our top five customers accounted for approximately 64% of total revenue. Our railcar sales to customers outside the United States were $34.0 million and $62.6 million in 2016 and 2015, respectively. Many of our customers do not purchase railcars every year since railcar fleets are not necessarily replenished or augmented every year. The size and frequency of railcar orders often results in a small number of customers representing a significant portion of our sales in a given year.

5

Table of Contents

SALES AND MARKETING

Our direct sales group is organized geographically and consists of regional sales managers and contract administrators, a manager of customer service and support staff. The regional sales managers are responsible for managing customer relationships. Our contract administrators are responsible for preparing proposals and other inside sales activities. Our manager of customer service is responsible for after-sale follow-up and in-field product performance reviews.

RESEARCH AND DEVELOPMENT

We utilize the latest engineering methods, tools and processes to ensure that new products and processes meet our customers’ requirements and are delivered in a timely manner. We develop and introduce new railcar designs as a result of a combination of customer feedback and close observation of developing market trends. We work closely with our customers to understand their expectations and design railcars that meet their needs. New product designs are tested and validated for compliance with AAR standards prior to introduction. This comprehensive approach provides the criteria and direction that ensure we are developing products that our customers desire and perform as expected. Costs associated with research and development are expensed as incurred and totaled $0.4 million, $0.4 million and $0.3 million for the years ended December 31, 2016, 2015 and 2014, respectively.

BACKLOG

We define backlog as the value of those products or services which our customers have committed in writing to purchase from us or lease from us when built, but which have not yet been recognized as sales. Our contracts may include cancellation clauses under which customers are required, upon cancellation of the contract, to reimburse us for costs incurred in reliance on an order and in some cases, to compensate us for lost profits. However, customer orders may be subject to customer requests for delays in railcar deliveries, inspection rights and other customary industry terms and conditions, which could prevent or delay backlog from being converted into sales.

The following table depicts our reported railcar backlog in number of railcars and estimated future sales value attributable to such backlog, for the periods shown.

| Year Ended December 31, | ||||||||||||

| 2016 | 2015 | 2014 | ||||||||||

| Railcar backlog at start of period |

9,840 | 14,791 | 6,826 | |||||||||

| Railcars delivered |

(5,559 | ) | (8,980 | ) | (7,102 | ) | ||||||

| Net railcar orders (canceled) received |

(22 | ) | 4,029 | 15,067 | ||||||||

|

|

|

|

|

|

|

|||||||

| Railcar backlog at end of period (1) |

4,259 | 9,840 | 14,791 | |||||||||

|

|

|

|

|

|

|

|||||||

| Estimated revenue from backlog at end of period (in thousands) (2) |

$ | 419,381 | $ | 925,977 | $ | 1,268,907 | ||||||

| (1) | Railcar backlog includes 0, 0 and 2,600 rebuilt railcars as of December 31, 2016, 2015 and 2014, respectively. |

| (2) | Estimated revenue from backlog reflects the total revenue attributable to the backlog reported at the end of the period as if such backlog were converted to actual sales. Estimated revenue from backlog does not reflect potential price increases and decreases under customer contracts that provide for variable pricing based on changes in the cost of raw materials. Although we continually look for opportunities to package our leased assets for sale to our leasing company partners, these leased assets may not be converted to sales. |

Although our reported backlog is typically converted to sales within two years, our reported backlog may not be converted to sales in any particular period, if at all, and the actual sales from these contracts may not equal our reported backlog estimates. See Item 1A. “Risk Factors—Risks Related to Our Business—The level of our reported backlog may not necessarily indicate what our future sales will be and our actual sales may fall short of the estimated sales value attributed to our backlog.” In addition, due to the large size of railcar orders and variations in the mix of railcars, the size of our reported backlog at the end of any given period may fluctuate significantly. See Item 1A. “Risk Factors—Risks Related to the Railcar Industry—The variable purchase patterns of our customers and the timing of completion, delivery and customer acceptance of the railcar may cause our revenues and income from operations to vary substantially each quarter, which will result in significant fluctuations in our quarterly results.”

6

Table of Contents

SUPPLIERS AND MATERIALS

The cost of raw materials and components represents a substantial majority of the manufacturing costs of most of our railcar product lines. As a result, the management of raw materials and components purchasing is critical to our profitability. We enjoy generally strong relationships with our suppliers, which helps to ensure access to supplies when railcar demand is high.

Our primary aluminum suppliers are Sapa Extrusions and Constellium N.V. (formerly Alcan Inc.). Aluminum prices generally are fixed at the time a railcar order is accepted, mitigating the effect of future fluctuations in prices. Our primary stainless steel supplier is Crompion International, L.L.C. and our primary carbon steel suppliers are International Truck and Engine Investments Corporation, an affiliate of Navistar, Inc., O’Neal Steel Inc. and Roll Form Group.

Our primary component suppliers include Amsted Industries, Inc., which supplies us with truck components, brake components, couplers and bearings, and Summit Railroad Products, Inc., which supplies us with axles and wheels. Roll Form Group is the sole supplier of our roll-formed center sills, which were used in 73% and 77% of our new railcars produced in 2016 and 2015, respectively. A center sill is the primary structural component of a railcar. In addition, International Truck and Engine Investments Corporation, an affiliate of Navistar, Inc., supplies us with various fabricated parts, components and subassemblies as well as providing truck and wheel and axle assembly services and blast and paint finishing services primarily for our Shoals facility. Other suppliers provide brake systems, castings, bearings, fabrications and various other components. The railcar industry is periodically subject to supply constraints for some of the key railcar components. See Item 1A. “Risk Factors—Risks Related to the Railcar Industry—Limitations on the supply of railcar components could adversely affect our business because they may limit the number of railcars we can manufacture.”

Except as described above, there are usually at least two suppliers for each of our raw materials and specialty components. No single supplier accounted for more than 24% and 16% of our total purchases in 2016 and 2015, respectively. Our top ten suppliers accounted for 67% and 58% of our total purchases in 2016 and 2015, respectively.

COMPETITION

We operate in a highly competitive marketplace especially in periods of low market demand resulting in excess manufacturing capacity. See Item 1A Risk Factors. Competition is based on price, delivery timing, product design, reputation for product quality and customer service and support.

We have four principal competitors in the North American railcar market that primarily manufacture railcars for third-party customers, which are Trinity Industries, Inc., The Greenbrier Companies, Inc., American Railcar Industries, Inc. and National Steel Car Limited.

Competition in the North American market from railcar manufacturers located outside of North America is limited by, among other factors, high shipping costs and familiarity with the North American market.

INTELLECTUAL PROPERTY

We have several U.S. and international patents and pending applications, registered trademarks, copyrights and trade names. Key patents include our one-piece center sill, our hopper railcar with automatic individual door system and our railroad car tub. The protection of our intellectual property is important to our business.

EMPLOYEES

As of December 31, 2016, we had 1,529 employees, of whom 241 were salaried and 1,288 were hourly wage earners, and approximately 537, or 35%, of our employees were members of unions. As of December 31, 2015, we had 1,662 employees, of whom 233 were salaried and 1,429 were hourly wage earners, and approximately 381, or 23%, of our employees were members of unions. See Item 1A. “Risk Factors—Risks Related to Our Business—Labor disputes could disrupt our operations and divert the attention of our management and may have a material adverse effect on our operations and profitability.”

7

Table of Contents

REGULATION

The Federal Railroad Administration, or FRA, administers and enforces U.S. federal laws and regulations relating to railroad safety. These regulations govern equipment and safety compliance standards for freight railcars and other rail equipment used in interstate commerce. The AAR promulgates a wide variety of rules and regulations governing safety and design of equipment, relationships among railroads with respect to freight railcars in interchange and other matters. The AAR also certifies freight railcar manufacturers and component manufacturers that provide equipment for use on railroads in the United States as well as providers of railcar repair and maintenance services. New products must generally undergo AAR testing and approval processes. As a result of these regulations, we must maintain certifications with the AAR as a freight railcar manufacturer and products that we sell must meet AAR and FRA standards.

We are also subject to oversight in other jurisdictions by foreign regulatory agencies and to the extent that we expand our business internationally, we will increasingly be subject to the regulations of other non-U.S. jurisdictions.

ENVIRONMENTAL MATTERS

We are subject to comprehensive federal, state, local and international environmental laws and regulations relating to the release or discharge of materials into the environment, the management, use, processing, handling, storage, transport or disposal of hazardous materials, or otherwise relating to the protection of human health and the environment. These laws and regulations not only expose us to liability for our own negligent acts, but also may expose us to liability for the conduct of others or for our actions that were in compliance with all applicable laws at the time these actions were taken. In addition, these laws may require significant expenditures to achieve compliance, and are frequently modified or revised to impose new obligations. Civil and criminal fines and penalties may be imposed for non-compliance with these environmental laws and regulations. Our operations that involve hazardous materials also raise potential risks of liability under the common law.

Environmental operating permits are, or may be, required for our operations under these laws and regulations. These operating permits are subject to modification, renewal and revocation. We regularly monitor and review our operations, procedures and policies for compliance with these laws and regulations. Despite these compliance efforts, risk of environmental liability is inherent in the operation of our businesses, as it is with other companies engaged in similar businesses. We believe that our operations and facilities are in substantial compliance with applicable laws and regulations and that any noncompliance is not likely to have a material adverse effect on our operations or financial condition.

Future events, such as changes in or modified interpretations of existing laws and regulations or enforcement policies, or further investigation or evaluation of the potential health hazards of products or business activities, may give rise to additional compliance and other costs that could have a material adverse effect on our financial condition and operations. In addition, we have in the past conducted investigation and remediation activities at properties that we own to address historic contamination. To date, such costs have not been material. Although we believe we have satisfactorily addressed all known material contamination through our remediation activities, there can be no assurance that these activities have addressed all historic contamination. The discovery of historic contamination or the release of hazardous substances into the environment could require us in the future to incur investigative or remedial costs or other liabilities that could be material or that could interfere with the operation of our business.

In addition to environmental laws, the transportation of commodities by railcar raises potential risks in the event of a derailment or other accident. Generally, liability under existing law in the United States for a derailment or other accident depends on the negligence of the party, such as the railroad, the shipper or the manufacturer of the railcar or its components. However, for the shipment of certain hazardous commodities, strict liability concepts may apply.

8

Table of Contents

The factors described below are the principal risks that could materially adversely affect our operating results and financial condition. Other factors may exist that we do not consider significant based on information that is currently available. In addition, new risks may emerge at any time, and we cannot predict those risks or estimate the extent to which they may affect us.

RISKS RELATED TO THE RAILCAR INDUSTRY

We operate in a highly cyclical industry, and our industry and markets are influenced by factors that are beyond our control, including U.S. and international economic conditions. Such factors could adversely affect demand for our railcar offerings.

Historically, the North American railcar market has been highly cyclical and we expect it to continue to be highly cyclical. During the most recent industry cycle, industry-wide railcar deliveries increased from a low of 16,535 railcars in 2010 to a peak of 82,296 railcars in 2015. During this period, our railcar production increased from approximately 2,229 railcars in 2010 to 8,980 railcars in 2015. Our industry and the markets for which we supply railcars are influenced by factors that are beyond our control, including U.S. and international economic conditions. Downturns in economic conditions could result in lower sales volumes, lower prices for railcars and a loss of profits. The cyclicality of the markets in which we operate may adversely affect our operating results and cash flow. In addition, fluctuations in the demand for our railcars may cause comparisons of our sales and operating results between different fiscal years to be less meaningful as indicators of our future performance.

We operate in a competitive industry and we may be unable to compete successfully against other railcar manufacturers.

We operate in a competitive marketplace especially in periods of low market demand resulting in excess manufacturing capacity and face substantial competition from established competitors in the railcar industry in North America. We have four principal competitors that primarily manufacture railcars for third-party customers. Some of these manufacturers have greater financial and technological resources than us, and they may increase their participation in the railcar segments in which we compete. In addition to price, competition is based on delivery timing, product performance and technological innovation, quality, customer service and other factors. In particular, technological innovation by any of our existing competitors, or new competitors entering any of the markets in which we do business, could put us at a competitive disadvantage and impair our ability to compete successfully against other railcar manufacturers or retain our market share in our established markets. Increased competition for the sales of our railcar products could result in price reductions, reduced margins and loss of market share, which could negatively affect our prospects, business, financial condition and results of operations.

We depend upon a small number of customers that represent a large percentage of our sales. The loss of any single customer, or a reduction in sales to any such customer, could have a material adverse effect on our business, financial condition and results of operations.

Since railcars are typically sold pursuant to large, periodic orders, a limited number of customers typically represent a significant percentage of our railcar sales in any given year. Over the last five years, our top five customers in each year based on sales accounted for, in the aggregate, approximately 58% of our total sales for the five-year period. In 2016, sales to our top three customers accounted for approximately 23%, 16% and 15%, respectively, of our total sales. In 2015, sales to our top three customers accounted for approximately 22%, 19% and 10%, respectively, of our total sales. Although we have long-standing relationships with many of our major customers, the loss of any significant portion of our sales to any major customer, the loss of a single major customer or a material adverse change in the financial condition of any one of our major customers could have a material adverse effect on our business, financial condition and results of operations.

The variable purchase patterns of our customers and the timing of completion, delivery and customer acceptance of orders may cause our revenues and income from operations to vary substantially each quarter, which will result in significant fluctuations in our quarterly results.

Most of our individual customers do not make purchases every year, since they do not need to replace, replenish or increase their railcar fleets on a yearly basis. Many of our customers place orders for products on an as-needed basis, sometimes only once every few years. As a result, the order levels for railcars, the mix of railcar types ordered and

9

Table of Contents

the railcars ordered by any particular customer have varied significantly from quarterly period to quarterly period in the past and may continue to vary significantly in the future. Therefore, our results of operations in any particular quarterly period may be significantly affected by the number of railcars delivered and product mix of railcars delivered in any given quarterly period. Additionally, because we record the sale of a new and rebuilt railcar at the time (1) we complete production, (2) the railcar is accepted by the customer following inspection, (3) the risk for any damage or loss with respect to the railcar passes to the customer, and (4) title to the railcar transfers to the customer, and not when the order is taken, the timing of the completion, delivery and acceptance of significant customer orders will have a considerable effect on fluctuations in our quarterly results. As a result of these quarterly fluctuations, we believe that comparisons of our sales and operating results between quarterly periods may not be meaningful and, as such, these comparisons should not be relied upon as indicators of our future performance.

Our ability to sell new railcars may be limited by other factors, including the availability and price of used railcars offered for sale and new or used railcars offered for lease by leasing companies and others.

Our customers may consider alternatives to the purchase of new railcars, including the purchase of used railcars, refurbishment of existing railcars or the lease of new or used railcars. Our competitors may also be able to offer railcar leases at favorable lease rates, negatively impacting our ability to sell new railcars, which may result in price reductions, reduced margins and loss of market share. These additional competitive factors could negatively affect our prospects, business, financial condition and results of operations.

The potential cost volatility of the raw materials that we use to manufacture railcars, especially aluminum and steel, and delivery delays associated with these raw materials may adversely affect our financial condition and results of operations.

The production of railcars and our operations require substantial amounts of steel and aluminum. The cost of steel, aluminum and all other materials (including scrap metal) used in the production of our railcars represents a significant majority of our direct manufacturing costs. Our business is subject to the risk of price increases and periodic delays in the delivery of aluminum, steel and other materials, all of which are beyond our control. Any fluctuations in the price or availability of aluminum or steel, or any other material used in the production of our railcars, may have a material adverse effect on our business, results of operations or financial condition. In addition, if any of our suppliers were unable to continue its business or were to seek bankruptcy relief, the availability or price of the materials we use could be adversely affected. Deliveries of our materials may also fluctuate depending on supply and demand for the material or governmental regulation relating to the material, including regulation relating to the importation of the material.

Limitations on the supply of railcar components could adversely affect our business because they may limit the number of railcars we can manufacture.

We rely upon third-party suppliers for various components for our railcars. In the future, suppliers of railcar components may be unable to meet the short-term or longer-term demand of our industry for certain railcar components. In the event that any of our suppliers of railcar components were to stop or reduce their production, go out of business, refuse to continue their business relationships with us, become subject to work stoppages or ration their supply of components, our business could be disrupted. During periods of high or rapidly increasing railcar demand, we have in the past experienced challenges sourcing certain railcar components to meet our production requirements. In addition, our ability to increase our railcar production to expand our business and/or meet any increase in demand, with new or additional manufacturing capabilities, depends on our ability to obtain an adequate supply of these railcar components. While we believe that we could secure alternative sources for these components, we may incur substantial delays and significant expense in doing so, the quality and reliability of these alternative sources may not be the same and our operating results may be significantly affected. In an effort to secure a supply of components, we have developed foreign sources that require deposits on some occasions. In the event of a material adverse business condition, such deposits may be forfeited. In addition, if one of our competitors entered into a preferred supply arrangement with, or was otherwise favored by, a particular supplier, we would be at a competitive disadvantage, which could negatively affect our operating results. Furthermore, alternative suppliers might charge significantly higher prices for railcar components than we currently pay. Such circumstances could have a material adverse impact on our customer relationships, financial condition and results of operations.

10

Table of Contents

RISKS RELATED TO OUR BUSINESS

Lack of acceptance of our new railcar offerings by our customers could adversely affect our business.

Our growth strategy depends in part on our continued development and sale of new railcar designs and design changes to existing railcars to penetrate railcar markets in which we currently do not compete and to expand or maintain our market share in the railcar markets in which we currently compete. We have dedicated significant resources to the development, manufacturing and marketing of new railcar designs. We typically make decisions to develop and market new railcars and railcars with modified designs without firm indications of customer acceptance. New or modified railcar designs may require customers to alter their existing business methods or threaten to displace existing equipment in which our customers may have a substantial capital investment. Many railcar purchasers prefer to maintain a standardized fleet of railcars and railcar purchasers with established railcar fleets are generally resistant to railcar design changes. Therefore, any new or modified railcar designs that we develop may not gain widespread acceptance in the marketplace and any such products may not be able to compete successfully with existing railcar designs or new railcar designs that may be introduced by our competitors.

The level of our reported backlog may not necessarily indicate what our future sales will be and our actual sales may fall short of the estimated sales value attributed to our backlog.

We define backlog as the sales value of products or services to which our customers have committed in writing to purchase from us or lease from us when built, that have not yet been recognized as revenue. In this annual report on Form 10-K, we have disclosed our backlog, or the number of railcars for which we have purchase orders or firm operating leases for railcars to be built, in various periods and the estimated sales value (in dollars) that would be attributable to this backlog once the backlog is converted to actual sales. We consider backlog to be an indicator of future sales of railcars. However, our reported backlog may not be converted into sales in any particular period, if at all, and the actual sales (including any compensation for lost profits and reimbursement for costs) from such contracts may not equal our reported estimates of backlog value. Customer orders may be subject to cancellation, inspection rights and other customary industry terms, and delivery dates may be subject to delay, thereby extending the date on which we will deliver the associated railcars and realize revenues attributable to such railcar backlog or could prevent the backlog from being converted to sales.

Our warranties may expose us to potentially significant claims, which may damage our reputation and adversely affect our business, financial condition and results of operations.

We generally warrant that new railcars produced by us will be free from defects in material and workmanship under normal use and service identified for a period of up to five years from the time of sale. Accordingly, we may be subject to a risk of product liability or warranty claims in the event that the failure of any of our products results in property damage, personal injury or death, or does not conform to our customers’ specifications. Although we currently maintain product liability insurance coverage, product liability claims, if made, may exceed our insurance coverage limits or insurance may not continue to be available on commercially acceptable terms, if at all. These types of product liability and warranty claims may result in costly product recalls, significant repair costs and damage to our reputation, all of which could adversely affect our results of operations. This risk may increase over the short-term due to our limited warranty claim experience for our new product offerings.

To the extent we expand our sales of products and services internationally, we will increase our exposure to international economic and political risks.

Conducting business outside the United States, for example through our sales to other countries, subjects us to various risks, including changing economic, legal and political conditions, work stoppages, currency fluctuations, terrorist activities directed at U.S. companies, armed conflicts and unexpected changes in the United States and the laws of other countries relating to tariffs, trade restrictions, transportation regulations, foreign investments and taxation. If we fail to obtain and maintain certifications of our railcars and railcar parts in the various countries where we may operate, we may be unable to market and sell our railcars in those countries.

In addition, more stringent rules relating to labor or the environment, adverse tax consequences and price exchange controls could limit our operations and make the distribution of our products internationally more difficult. Furthermore, any material changes in the quotas, regulations or duties on imports imposed by the U.S. government and agencies or on exports by non-U.S. governments and their respective agencies could affect our ability to export the railcars that we manufacture in the United States. The uncertainty of the legal environment could limit our ability to enforce our rights effectively.

11

Table of Contents

Business that we may acquire in the future may fail to perform to expectations or we may be unable to successfully integrate acquired business with our existing business.

We may engage in future acquisitions, which in each case could materially affect our business, operating results, and financial condition. However, we may not be able to find suitable acquisition candidates, and we may not be able to complete such acquisitions on favorable terms, if at all. Future acquisitions may not strengthen our competitive position or achieve our desired goals and may disrupt our ongoing operations, divert management from day-to-day responsibilities, increase our expenses and reduce our cash available for operations and other uses. There can be no assurance that we will be able to effectively manage the integration of businesses we may acquire in the future, or be able to retain and motivate key personnel from those businesses.

If we lose key personnel, our operations and ability to manage the day-to-day aspects of our business may be adversely affected.

We believe our success depends to a significant degree upon the continued contributions of our executive officers and key employees, both individually and as a group. Our future performance will substantially depend on our ability to retain and motivate them. If we lose key personnel or are unable to recruit qualified personnel, our ability to manage the day-to-day aspects of our business may be adversely affected.

The loss of the services of one or more members of our senior management team could have a material adverse effect on our business, financial condition and results of operations. Because our senior management team has many years of experience in the railcar industry and other manufacturing and capital equipment industries, it could be difficult to replace any of them without adversely affecting our business operations. Our future success will also depend in part upon our continuing ability to attract and retain highly qualified personnel. We do not currently maintain “key person” life insurance.

Shortages of skilled labor may adversely impact our operations.

We depend on skilled labor in the manufacture of railcars. Some of our facilities are located in areas

where demand for skilled laborers often exceeds supply. Shortages of some types of skilled laborers may restrict our ability to maintain or increase production rates and could cause our labor costs to increase.

Labor disputes could disrupt our operations and divert the attention of our management and may have a material adverse effect on our operations and profitability.

As of December 31, 2016, we had a collective bargaining agreement with a union representing approximately 26% of our total active labor force that expires on March 31, 2017 and a collective bargaining agreement with a union representing approximately 10% of our total active labor force that expires on October 31, 2018. Disputes with the unions representing our employees could result in strikes or other labor protests which could disrupt our operations and divert the attention of management from operating our business. If we were to experience a strike or work stoppage, it could be difficult for us to find a sufficient number of employees with the necessary skills to replace these employees. Any such labor disputes could have a material adverse effect on our financial condition, results of operations or cash flows.

We rely upon a single supplier to supply us with all of our roll-formed center sills for our railcars, and any disruption of our relationship with this supplier could adversely affect our business.

We rely upon a single supplier to manufacture all of our roll-formed center sills for our railcars, which are based upon our proprietary and patented process. A center sill is the primary longitudinal structural component of a railcar, which helps the railcar withstand the weight of the cargo and the force of being pulled during transport. Our center sill is formed into its final shape without heating by passing steel plate through a series of rollers. Of the new railcars that we produced in 2016 and 2015, 73% and 77%, respectively, were manufactured using this roll-formed center sill. Although we have a good relationship with our supplier and have not experienced any significant delays, manufacturing shortages or failures to meet our quality requirements and production specifications in the past, our supplier could stop production of our roll-formed center sills, go out of business, refuse to continue its business relationship with us or become subject to work stoppages. While we believe that we could secure alternative

12

Table of Contents

manufacturing sources, our present supplier is currently the only manufacturer of our roll-formed center sills for our railcars. We may incur substantial delays and significant expense in finding an alternative source, our results of operations may be significantly affected and the quality and reliability of these alternative sources may not be the same. Moreover, alternative suppliers might charge significantly higher prices for our roll-formed center sills than we currently pay.

Equipment failures, delays in deliveries or extensive damage to our facilities could lead to production or service curtailments or shutdowns.

We have railcar production facilities in Cherokee, Alabama, Danville, Illinois and Roanoke, Virginia. An interruption in railcar production capabilities at these facilities, as a result of equipment failure or other factors, could reduce or prevent our production of railcars. A halt of production at any of our manufacturing facilities could severely affect delivery times to our customers. Any significant delay in deliveries to our customers could result in the termination of contracts, cause us to lose future sales and negatively affect our reputation among our customers and in the railcar industry and our results of operations. Our facilities are also subject to the risk of catastrophic loss due to unanticipated events, such as fires, explosions, floods or weather conditions. We may experience plant shutdowns or periods of reduced production as a result of equipment failures, delays in deliveries or extensive damage to any of our facilities, which could have a material adverse effect on our business, results of operations or financial condition.

The Company may be unable to renew its lease arrangements at its manufacturing facilities at commercially acceptable terms

Two of our manufacturing facilities are leased from third parties. As each lease expires, we may be unable to negotiate renewals on commercially acceptable terms. Failure to renew our leases at commercially acceptable terms could have a potential adverse impact on our operations.

We might fail to adequately protect our intellectual property, which may result in our loss of market share, or third parties might assert that our intellectual property infringes on their intellectual property, which would be costly to defend and divert the attention of our management.

The protection of our intellectual property is important to our business. We rely on a combination of trademarks, copyrights, patents and trade secrets to protect our intellectual property. However, these protections might be inadequate. For example, we have patents for portions of our railcar designs that are important to our market leadership in the coal car segment. Our pending or future trademark, copyright and patent applications might not be approved or, if allowed, might not be sufficiently broad. Conversely, third parties might assert that our technologies or other intellectual property infringe on their proprietary rights. In either case, litigation may result, which could result in substantial costs and diversion of our management team’s efforts. Regardless of whether we are ultimately successful in any litigation, such litigation could adversely affect our business, results of operations and financial condition.

Our information technology and other systems are subject to cybersecurity risk, including the misappropriation of customer information and other breaches of information security. Security breaches and other disruptions could compromise our information, expose us to liability and harm our reputation and business.

In the ordinary course of our business, we collect and store sensitive data on our networks, including intellectual property, our proprietary business information and that of our customers, suppliers and business partners and personally identifiable information and other personal information of our customers and employees. While we continually work to safeguard our systems and to mitigate potential security risks, our information and processes are exposed to increasing global information security threats and more sophisticated and targeted computer crime, which may result in our data being subject to a security breach, a system failure, a computer virus, malicious software or unauthorized or fraudulent use by our employees or other third parties. Any compromise of our data security and access to or public disclosure or loss of personal or confidential business information could result in legal claims or proceedings with third parties, liability or regulatory penalties under the laws that protect the privacy of personal information, disruption of our operations, damage to our reputation, loss of business or remediation costs, any of which could have a material adverse effect on our prospects, business, financial condition and results of operations.

13

Table of Contents

We are subject to risks with respect to changes in U.S. tax law and rates.

As a result of recent changes in the U.S. government, tax reform may be enacted in the near future. These changes could include a reduction in the U.S. corporate tax rate, elimination of certain deductions and a border tax adjustment. We cannot predict whether or not any of these tax reform proposals will ultimately be adopted and, until the details of each proposal have been developed and reviewed, we cannot determine the impact of the proposed legislation on our tax expense. However, any changes could have a significant impact on the Company’s business and financial results depending upon the final legislation.

We are subject to a variety of environmental laws and regulations and the cost of complying with environmental requirements or any failure by us to comply with such requirements may have a material adverse effect on our business, financial condition and results of operations.

We are subject to a variety of federal, state and local environmental laws and regulations, including those governing air quality and the handling, disposal and remediation of waste products, fuel products and hazardous substances. Although we believe that we are in material compliance with all of the various regulations and permits applicable to our business, we may not at all times be in compliance with such requirements. The cost of complying with environmental requirements may also increase substantially in future years. If we violate or fail to comply with these regulations, we could be fined or otherwise sanctioned by regulators. In addition, these requirements are complex, change frequently and may become more stringent over time, which could have a material adverse effect on our business. We have in the past conducted investigation and remediation activities at properties that we own to address historic contamination. However, there can be no assurance that these remediation activities have addressed all historic contamination. Environmental liabilities that we incur, including those relating to the off-site disposal of our wastes, if not covered by adequate insurance or indemnification, will increase our costs and have a negative impact on our profitability.

The agreement governing our revolving credit facility contains various covenants that, among other things, limit our discretion in operating our business and provide for certain minimum financial requirements.

The agreement governing our revolving credit facility contains various covenants that, among other things, limit our management’s discretion by restricting our ability to incur additional debt, enter into certain transactions with affiliates, make investments and other restricted payments and create liens. Our failure to comply with these financial covenants and other covenants under our revolving credit facility could lead to an event of default under the agreement governing any other indebtedness that we may have outstanding at the time, permitting the lenders to accelerate all borrowings under such agreement and to foreclose on any collateral. In addition, any such events may make it more difficult or costly for us to borrow additional funds in the future. Our failure to raise capital if and when needed could have a material adverse effect on our results of operations and financial condition.

The market price of our securities may fluctuate significantly, which may make it difficult for stockholders to sell shares of our common stock when desired or at attractive prices.

Since our initial public offering in April 2005 until December 31, 2016, the trading price of our common stock ranged from a low of $10.87 per share to a high of $78.34 per share. The price for our common stock may fluctuate in response to a number of events and factors, such as quarterly variations in operating results and our reported backlog, the cyclical nature of the railcar market, announcements of new products by us or our competitors, changes in financial estimates and recommendations by securities analysts, the operating and stock price performance of other companies that investors may deem comparable to us, and news reports relating to trends in our markets or general economic conditions. Additionally, volatility or a lack of positive performance in our stock price may adversely affect our ability to retain key employees, all of whom have been granted stock options or other stock awards.

14

Table of Contents

Item 1B. Unresolved Staff Comments.

None.

The following table presents information on our leased and owned operating properties as of December 31, 2016:

| Use |

Location |

Size |

Leased or |

Lease Expiration Date | ||||

| Corporate headquarters | Chicago, Illinois | 15,540 square feet | Leased | March 31, 2022 | ||||

| Railcar assembly and component manufacturing | Danville, Illinois | 308,665 square feet on 36.5 acres of land | Owned | — | ||||

| Railcar assembly and component manufacturing | Roanoke, Virginia | 383,709 square feet on 15.5 acres of land | Leased | December 31, 2024 | ||||

| Railcar assembly and component manufacturing | Cherokee, Alabama | 772,828 square feet | Leased | December 31, 2021 | ||||

| Administrative | Johnstown, Pennsylvania | 29,500 square feet on 1.02 acres of land | Owned | — | ||||

| Parts warehouse | Johnstown, Pennsylvania | 86,000 square feet | Leased | December 31, 2023 | ||||

The information in response to this item is included in Note 17, Risks and Contingencies, to our Consolidated Financial Statements included in Part II, Item 8 of this Form 10-K

Item 4. Mine Safety Disclosures.

Not applicable

15

Table of Contents

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock has been quoted on the Nasdaq Global Market under the symbol “RAIL” since April 6, 2005. As of February 7, 2017, there were approximately 91 holders of record of our common stock, which does not include persons whose shares of common stock are held by a bank, brokerage house or clearing agency. The following table sets forth quarterly high and low closing prices of our common stock since January 1, 2015, as reported on the Nasdaq Global Market.

| Common Stock Price | Dividend | |||||||||||

| High | Low | Declared | ||||||||||

| 2016 |

||||||||||||

| Fourth Quarter |

$ | 15.35 | $ | 10.90 | $ | 0.09 | ||||||

| Third Quarter |

$ | 15.42 | $ | 13.47 | $ | 0.09 | ||||||

| Second Quarter |

$ | 17.64 | $ | 13.09 | $ | 0.09 | ||||||

| First Quarter |

$ | 19.83 | $ | 14.87 | $ | 0.09 | ||||||

| 2015 |

||||||||||||

| Fourth Quarter |

$ | 24.48 | $ | 16.93 | $ | 0.09 | ||||||

| Third Quarter |

$ | 22.94 | $ | 16.99 | $ | 0.09 | ||||||

| Second Quarter |

$ | 31.59 | $ | 20.88 | $ | 0.09 | ||||||

| First Quarter |

$ | 31.78 | $ | 22.67 | $ | 0.09 | ||||||

Dividend Policy

The declaration and payment of future dividends will be at the discretion of our board of directors and will depend on, among other things, general economic and business conditions, our strategic plans, our financial results, contractual and legal restrictions on the payment of dividends by us and our subsidiaries and such other factors as our board of directors considers to be relevant. The ability of our board of directors to declare a dividend on our common stock is limited by Delaware law. On February 6, 2017, our board of directors declared a cash dividend of $0.09 per share of our common stock, payable on February 22, 2017, to shareholders of record at the close of business on February 16, 2017.

16

Table of Contents

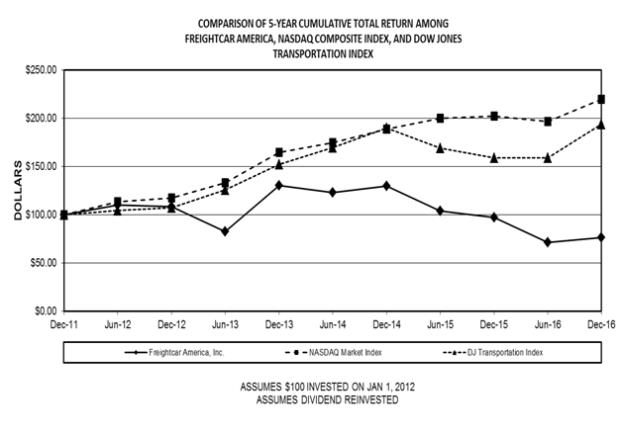

Performance Graph

The following performance graph and related information shall not be deemed “soliciting material” or to be “filed” with the Securities and Exchange Commission, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended, except to the extent that the Company specifically incorporates it by reference into such filing.

The following graph illustrates the cumulative total stockholder return on our common stock during the period from January 1, 2012 through December 31, 2016 and compares it with the cumulative total return on the NASDAQ Composite Index and DJ Transportation Index. The comparison assumes $100 was invested on January 1, 2012 in our common stock and in each of the foregoing indices and assumes reinvestment of dividends, if any. The performance shown is not necessarily indicative of future performance.

| Dec 31, | Jun 30, | Dec 31, | Jun 30, | Dec 31, | Jun 30, | Dec 31, | Jun 30, | Dec 31, | Jun 30, | Dec 31, | ||||||||||||||||||||||||||||||||||

| 2011 | 2012 | 2012 | 2013 | 2013 | 2014 | 2014 | 2015 | 2015 | 2016 | 2016 | ||||||||||||||||||||||||||||||||||

| FreightCar America, Inc. |

100.00 | 110.21 | 108.24 | 82.52 | 130.06 | 122.97 | 129.74 | 103.67 | 97.25 | 71.12 | 76.49 | |||||||||||||||||||||||||||||||||

| NASDAQ Market Index |

100.00 | 113.28 | 117.45 | 133.23 | 164.57 | 174.75 | 188.84 | 199.97 | 201.98 | 196.62 | 219.89 | |||||||||||||||||||||||||||||||||

| DJ Transportation Index |

100.00 | 104.62 | 107.49 | 125.90 | 151.96 | 169.54 | 190.07 | 169.33 | 158.82 | 158.97 | 193.53 | |||||||||||||||||||||||||||||||||

17

Table of Contents

Item 6. Selected Financial Data.

The selected financial data presented for each of the years in the five-year period ended December 31, 2016 was derived from our audited consolidated financial statements and other operational information reported on Form 10-K. The selected financial data should be read in conjunction with Management’s Discussion and Analysis of Financial Condition and Results of Operations and the Consolidated Financial Statements and Notes thereto included in Item 7 and Item 8, respectively, of this annual report on Form 10-K. (in thousands, except for share and per share data and railcar amounts)

| Year Ended December 31, | ||||||||||||||||||||

| Statements of Operations Data | 2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||

| Revenues |

$ | 523,731 | $ | 772,854 | $ | 598,518 | $ | 290,393 | $ | 677,449 | ||||||||||

| Gross profit |

40,179 | 82,661 | 42,343 | 13,225 | 64,986 | |||||||||||||||

| Selling, general and administrative expense |

36,376 | 41,663 | 35,317 | 27,464 | 32,736 | |||||||||||||||

| Gain on sale of railcars available for lease |

— | (1,187 | ) | (1,403 | ) | (604 | ) | (989 | ) | |||||||||||

| Gain on sale of railcar repair and maintenance services business and facility |

— | (4,578 | ) | (1,078 | ) | — | — | |||||||||||||

| Gain on settlement of postretirement benefit obligation, net of plaintiffs’ attorneys’ fees |

(14,306 | ) | — | — | — | — | ||||||||||||||

| Restructuring and impairment charges |

2,261 | — | — | 10,452 | — | |||||||||||||||

| Net income (loss)(1)(2)(3)(4)(5) |

$ | 12,324 | $ | 31,805 | $ | 5,904 | $ | (19,295 | ) | $ | 19,095 | |||||||||

| Weighted average common shares outstanding—basic |

12,262,275 | 12,175,955 | 12,001,587 | 11,954,238 | 11,932,926 | |||||||||||||||

| Weighted average common shares outstanding—diluted |

12,262,275 | 12,217,755 | 12,103,520 | 11,954,238 | 11,969,337 | |||||||||||||||

| Per share data: |

||||||||||||||||||||

| Net income (loss) per common share —basic |

$ | 1.00 | $ | 2.59 | $ | 0.49 | $ | (1.61 | ) | $ | 1.60 | |||||||||

| Net income (loss) per common share —diluted |

$ | 1.00 | $ | 2.58 | $ | 0.49 | $ | (1.61 | ) | $ | 1.60 | |||||||||

| Dividends declared per common share |

$ | 0.36 | $ | 0.36 | $ | 0.24 | $ | 0.24 | $ | 0.24 | ||||||||||

| Other financial and operating data: |

||||||||||||||||||||

| Investment in property, plant and equipment and railcars on operating leases |

$ | 13,846 | $ | 16,699 | $ | 11,802 | $ | 17,317 | $ | 9,088 | ||||||||||

| Railcars delivered |

5,559 | 8,980 | 7,102 | 3,821 | 8,325 | |||||||||||||||

| Net railcar (cancellations) orders |

(22 | ) | 4,029 | 15,067 | 7,766 | 2,903 | ||||||||||||||

| Railcar backlog at period end |

4,259 | 9,840 | 14,791 | 6,826 | 2,881 | |||||||||||||||

| Estimated revenue from backlog at period end |

$ | 419,381 | $ | 925,977 | $ | 1,268,907 | $ | 492,018 | $ | 197,597 | ||||||||||

| Balance sheet data (at period end): |

||||||||||||||||||||

| Cash and cash equivalents |

$ | 92,750 | $ | 83,068 | $ | 113,532 | $ | 145,506 | $ | 98,509 | ||||||||||

| Restricted cash and restricted certificates of deposit |

5,970 | 6,896 | 6,015 | 7,780 | 14,700 | |||||||||||||||

| Marketable securities |

— | 26,951 | 47,961 | 38,988 | 41,978 | |||||||||||||||

| Total assets |

339,255 | 406,904 | 385,252 | 417,719 | 388,565 | |||||||||||||||

| Total debt, including capital leases |

— | — | — | — | — | |||||||||||||||

| Total stockholders’ equity |

256,914 | 235,111 | 198,695 | 202,535 | 211,331 | |||||||||||||||

| (1) | For the year ended December 31, 2016, we recorded a pre-tax gain on a settlement of a postretirement benefit plan obligation, net of plaintiffs’ attorneys’ fees of $14.3 million. |

| (2) | For the year ended December 31, 2016, we recorded pre-tax restructuring and impairment charges of $2.3 million. See Note 7 to our consolidated financial statements. |

| (3) | For the year ended December 31, 2015, we recorded a pre-tax gain on the sale of our railcar repair and maintenance services business of $4.6 million. |

| (4) | For the year ended December 31, 2014, we recorded a pre-tax gain on the sale of our closed railcar repair and maintenance facility of $1.1 million. |

| (5) | For the year ended December 31, 2013, we recorded pre-tax impairment charges to write down assets at our idled Danville manufacturing facility of $7.6 million, impairment charges to write down assets at our closed Clinton, Indiana maintenance and repair shop of $1.6 million, other charges related to the closure of our Clinton maintenance and repair shop of $303,000 and Corporate severance charges of $1.6 million. |

18

Table of Contents

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

OVERVIEW

You should read the following discussion in conjunction with our consolidated financial statements and related notes included elsewhere in this annual report on Form 10-K. This discussion contains forward-looking statements that are based on management’s current expectations, estimates and projections about our business and operations. Our actual results may differ materially from those currently anticipated and expressed in such forward-looking statements. See “Forward-Looking Statements.”

We are a diversified manufacturer of railcars and railcar components. We design and manufacture a broad variety of railcar types for transportation of bulk commodities and containerized freight products primarily in North America.

We rebuild railcars and sell forged, cast and fabricated parts for all of the railcars we produce, as well as those manufactured by others. Between November 2010, when we acquired the business assets of DTE Rail Services, Inc., and September 2015, when we sold our repair and maintenance services business, we provided railcar repair and maintenance for all types of freight railcars. We also lease freight cars. Our primary customers are railroads, shippers and financial institutions.

On August 1, 2016, we announced a cost reduction program whereby approximately 15% of our salaried administrative workforce would be eliminated, our Johnstown, Pennsylvania administrative facility would be closed and certain discretionary spending would be reduced. The total estimated costs of implementing this program are approximately $2.7 million, including approximately $1.1 million of employee-related costs and approximately $1.3 million of long-lived asset impairments. We currently estimate that the annualized cost savings resulting from this restructuring program will be approximately $5.0 million when fully implemented.

In connection with our cost reductions program during 2016, we recorded restructuring and impairment charges of $2.3 million, which consisted primarily of non-cash impairment charges of $1.3 million for property, plant and equipment at our Johnstown administrative facility and employee severance and other employment termination costs of $1.0 million.

Our railcar manufacturing facilities are located in Cherokee, Alabama (“Shoals”), Danville, Illinois and Roanoke, Virginia. Our Shoals facility is an important part of our long-term growth strategy as we continue to expand our railcar product and service offerings. Our Shoals facility delivered its first railcars during the fourth quarter of 2013 and additional production capacity became operational during the second quarter of 2015. Our Roanoke facility has the capacity to build a variety of railcar types in a cost effective manner and will continue to support our coal car products when market conditions improve. Our Danville facility resumed production in June 2014 after being idled for 14 months and, given the challenged coal market, operations there were again significantly curtailed in 2016. Our Danville facility will be idled for railcar production effective March 31, 2017.

In light of the current cyclical downturn in the railcar industry and the challenged coal market, on February 27, 2017 we announced further reductions to our salaried workforce and initiatives to reduce discretionary spending. These actions are expected to be completed by the end of the second quarter of 2017. Total estimated costs to implement these actions are approximately $1.0 million of employee-related costs. We currently estimate that the annualized cost savings resulting from these actions will be approximately $3.0 million when fully implemented.

Railcar deliveries totaled 5,559 units, consisting of 5,332 new railcars and 227 rebuilt railcars, for the year ended December 31, 2016, compared to 8,980 units, consisting of 6,280 new railcars, 2,600 rebuilt railcars and 100 railcars leased, for the year ended December 31, 2015. Our total backlog of firm orders for railcars decreased from 9,840 railcars as of December 31, 2015 to 4,259 railcars as of December 31, 2016.

The Company’s operations comprise two operating segments, Manufacturing and Parts, and one reportable segment, Manufacturing. The Company’s Manufacturing segment includes new railcar manufacturing, used railcar sales, railcar leasing and major railcar rebuilds. The Company’s Parts operating segment is not significant for reporting purposes and has been combined with corporate and other non-operating activities as Corporate and Other.

19

Table of Contents

FINANCIAL STATEMENT PRESENTATION

Revenues

Our Manufacturing segment revenues are generated primarily from sales of the railcars that we manufacture. Our Manufacturing segment sales depend on industry demand for new railcars, which is driven by overall economic conditions and the demand for railcar transportation of various products, such as coal, steel products, minerals, cement, motor vehicles, forest products and agricultural commodities. Our Manufacturing segment sales are also affected by competitive market pressures that impact our market share, the prices for our railcars and by the types of railcars sold. Our Manufacturing segment revenues also include revenues from major railcar rebuilds and lease rental payments received with respect to railcars under operating leases. Our Corporate and Other revenue sources include parts sales and, through September 30, 2015, revenues from our repair and maintenance business that was sold in September 2015.

We generally manufacture railcars under firm orders from our customers. We recognize revenue, when (1) we complete the individual railcars, (2) the railcars are accepted by the customer following inspection, (3) the risk of any damage or other loss with respect to the railcars passes to the customer and (4) title to the railcars transfers to the customer. Deliveries include new and used cars sold, cars built and contracted under operating leases and rebuilt cars. We value used railcars received at their estimated fair market value. Revenues derived from a single sales contract that contains multiple products and services are allocated based on the relative fair value of each item to be delivered and recognized in accordance with the applicable revenue recognition criteria for the specific unit of accounting. The variable purchase patterns of our customers and the timing of completion, delivery and customer acceptance of railcars may cause our revenues and income from operations to vary substantially each quarter, which will result in significant fluctuations in our quarterly results.

Cost of sales