Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - MASONITE INTERNATIONAL CORP | a2016form10-kxex322.htm |

| EX-32.1 - EXHIBIT 32.1 - MASONITE INTERNATIONAL CORP | a2016form10-kxex321.htm |

| EX-31.2 - EXHIBIT 31.2 - MASONITE INTERNATIONAL CORP | a2016form10-kxex312.htm |

| EX-31.1 - EXHIBIT 31.1 - MASONITE INTERNATIONAL CORP | a2016form10-kxex311.htm |

| EX-23.1 - EXHIBIT 23.1 - MASONITE INTERNATIONAL CORP | a2016form10-kxex231.htm |

| EX-21.1 - EXHIBIT 21.1 - MASONITE INTERNATIONAL CORP | a2016form10-kxex211.htm |

| EX-10.5(F) - EXHIBIT 10.5(F) - MASONITE INTERNATIONAL CORP | a2016form10-kxex105f.htm |

| EX-10.4(M) - EXHIBIT 10.4(M) - MASONITE INTERNATIONAL CORP | a2016form10-kxex104m.htm |

| EX-10.3(V) - EXHIBIT 10.3(V) - MASONITE INTERNATIONAL CORP | a2016form10-kxex103v.htm |

| EX-10.3(U) - EXHIBIT 10.3(U) - MASONITE INTERNATIONAL CORP | a2016form10-kxex103u.htm |

| EX-10.3(T) - EXHIBIT 10.3(T) - MASONITE INTERNATIONAL CORP | a2016form10-kxex103t.htm |

| EX-10.3(S) - EXHIBIT 10.3(S) - MASONITE INTERNATIONAL CORP | a2016form10-kxex103s.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K |

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended January 1, 2017

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____ to _____

Commission File Number: 001-11796

____________________________

|

Masonite International Corporation

(Exact name of registrant as specified in its charter)

____________________________

British Columbia, Canada (State or other jurisdiction of incorporation or organization) | 98-0377314 (I.R.S. Employer Identification No.) | |

2771 Rutherford Road

Concord, Ontario L4K 2N6 Canada

(Address of principal executive offices, zip code)

(800) 895-2723

(Registrant’s telephone number, including area code)

____________________________

Securities Registered Pursuant to Section 12(b) of the Act:

Common Stock (no par value) | New York Stock Exchange | |

(Title of class) | (Name of exchange on which registered) | |

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x | Accelerated filer | o | |||

Non-accelerated filer | o (Do not check if a smaller reporting company) | Smaller reporting company | o | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

As of July 3, 2016, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the shares of voting common stock held by non-affiliates of the registrant, computed by reference to the closing sales price of such shares on the New York Stock Exchange on July 3, 2016, was $2.0 billion.

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of the securities under a plan confirmed by a court. Yes x No o

The registrant had outstanding 29,769,978 shares of Common Stock, no par value, as of February 24, 2017.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for its 2017 Annual General Meeting of Shareholders scheduled to be held on May 11, 2017, to be filed with the Securities and Exchange Commission not later than 120 days after January 1, 2017, are incorporated by reference into Part III, Items 10-14 of this Annual Report on Form 10-K.

|

MASONITE INTERNATIONAL CORPORATION

INDEX TO ANNUAL REPORT ON FORM 10-K

January 1, 2017

Page No. | |||

PART I | |||

Item 1 | |||

Item 1A | |||

Item 1B | |||

Item 2 | |||

Item 3 | |||

Item 4 | |||

PART II | |||

Item 5 | |||

Item 6 | |||

Item 7 | |||

Item 7A | |||

Item 8 | |||

Item 9 | |||

Item 9A | |||

Item 9B | |||

PART III | |||

Item 10 | |||

Item 11 | |||

Item 12 | |||

Item 13 | |||

Item 14 | |||

PART IV | |||

Item 15 | |||

i

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains "forward-looking statements" within the meaning of the federal securities laws, including, without limitation, statements concerning the conditions in our industry, our operations, our economic performance and financial condition, including, in particular, statements relating to our business and growth strategy and product development efforts under "Management’s Discussion and Analysis of Financial Condition and Results of Operations." Forward-looking statements include all statements that do not relate solely to historical or current facts and can be identified by the use of words such as "may," "might," "will," "should," "estimate," "project," "plan," "anticipate," "expect," "intend," "outlook," "believe" and other similar expressions. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of their dates. These forward-looking statements are based on estimates and assumptions by our management that, although we believe to be reasonable, are inherently uncertain and subject to a number of risks and uncertainties. These risks and uncertainties include, without limitation, those identified under "Risk Factors" and elsewhere in this Annual Report.

The following list represents some, but not necessarily all, of the factors that could cause actual results to differ from historical results or those anticipated or predicted by these forward-looking statements:

• | our ability to successfully implement our business strategy; |

• | general economic, market and business conditions; |

• | levels of residential new construction; residential repair, renovation and remodeling; and non-residential building construction activity; |

• | the United Kingdom's vote to leave, and its eventual exit from, the European Union; |

• | competition; |

• | our ability to manage our operations including integrating our recent acquisitions and companies or assets we acquire in the future; |

• | our ability to generate sufficient cash flows to fund our capital expenditure requirements, to meet our pension obligations, and to meet our debt service obligations, including our obligations under our senior notes and our ABL Facility; |

• | labor relations (i.e., disruptions, strikes or work stoppages), labor costs and availability of labor; |

• | increases in the costs of raw materials or any shortage in supplies; |

• | our ability to keep pace with technological developments; |

• | the actions taken by, and the continued success of, certain key customers; |

• | our ability to maintain relationships with certain customers; |

• | the ability to generate the benefits of our restructuring activities; |

• | retention of key management personnel; |

• | environmental and other government regulations; and |

• | limitations on operating our business as a result of covenant restrictions under our existing and future indebtedness, including our senior notes and our ABL Facility. |

We caution you that the foregoing list of important factors is not exclusive. In addition, in light of these risks and uncertainties, the matters referred to in the forward-looking statements contained in this Annual Report may not in fact occur. We undertake no obligation to publicly update or revise any forward-looking statement as a result of new information, future events or otherwise, except as otherwise required by law.

ii

PART I

Unless we state otherwise or the context otherwise requires, in this Annual Report all references to "Masonite", "we", "us", "our" and the "Company" refer to Masonite International Corporation and its subsidiaries.

Item 1. Business

Overview

We are a leading global designer, manufacturer and distributor of interior and exterior doors for the new construction and repair, renovation and remodeling sectors of the residential and non-residential building construction markets. Since 1925, we have provided our customers with innovative products and superior service at compelling values. In order to better serve our customers and create sustainable competitive advantages, we focus on developing innovative products, advanced manufacturing capabilities and technology-driven sales and service solutions. Today, we believe we hold either the number one or two market positions in the seven product categories we target in North America: interior molded residential doors; interior stile and rail residential doors; exterior fiberglass residential doors; exterior steel residential doors; interior architectural wood doors; wood veneers and molded door facings; and door core.

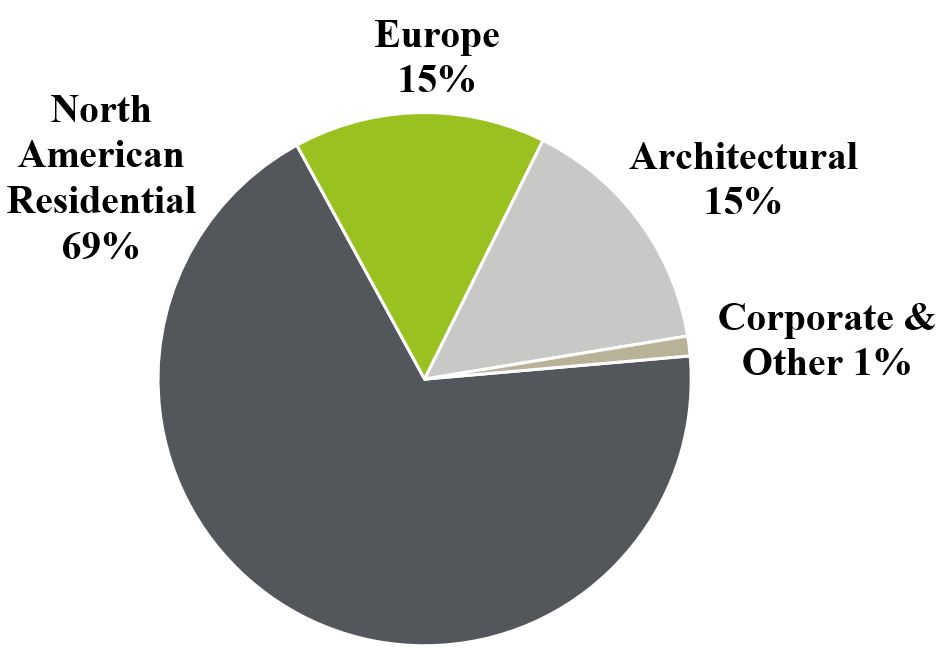

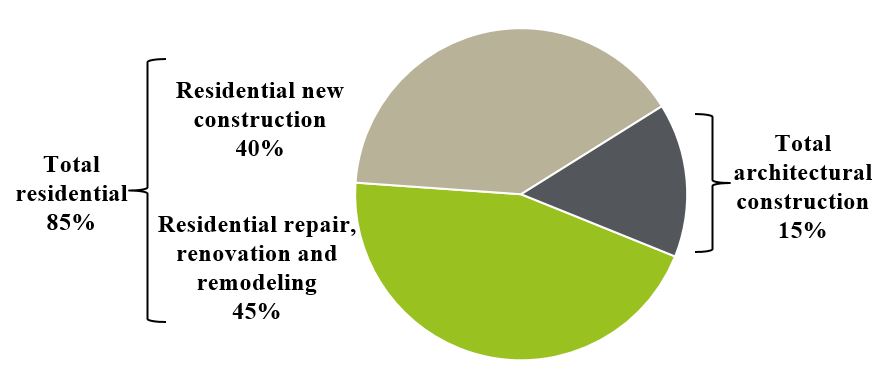

We market and sell our products to remodeling contractors, builders, homeowners, retailers, dealers, lumberyards, commercial and general contractors and architects through well-established wholesale and retail distribution channels. Our broad portfolio of brands, including Masonite®, Marshfield®, Premdor®, Mohawk®, Megantic®, Algoma®, Birchwood Best®, Lemieux®, Door-StopTM, Harring DoorsTM, Performance Doorset SolutionsTM and National HickmanTM are among the most recognized in the door industry and are associated with innovation, quality and value. In the year ended January 1, 2017, we sold approximately 35 million doors to more than 7,000 customers in 65 countries. Our fiscal year 2016 net sales by segment and global net sales of doors by end market are set forth below:

Net Sales by Segment - 2016 | Global Net Sales of Doors by End Market - 2016 | |

|  | |

See Note 15 to our consolidated financial statements for additional information about our segments.

Over the past several years, we have invested in advanced technologies to increase the automation of our manufacturing processes, increase quality and shorten lead times and introduced targeted e-commerce and other marketing initiatives to improve our sales and marketing efforts and customer experience. In addition, we implemented a disciplined acquisition strategy that solidified our presence in both the North American residential molded and stile and rail interior door markets and created leadership positions in the attractive North American commercial and architectural interior wood door, door core and wood veneer markets.

We operate 64 manufacturing and distribution facilities in 8 countries in North America, Europe, South America and Asia, which are strategically located to serve our customers. We are one of the few vertically integrated door manufacturers in the world and one of only two in the North American residential door industry as well as the only vertically integrated door manufacturer in the North American architectural interior wood door industry. Our vertical

1

integration extends to all steps of the production process from initial design, development and production of steel press plates to produce interior molded and exterior fiberglass door facings to the manufacturing of door components, such as door cores, wood veneers and molded facings, to door slab assembly. We also offer incremental value by pre-machining doors for hardware, hanging doors in frames with glass and hardware and pre-finishing doors with paint or stain. We believe that our vertical integration and automation enhance our ability to develop new and proprietary products, provide greater value and improved customer service and create high barriers to entry. We also believe vertical integration enhances our ability to cut costs, although our cost structure is subject to certain factors beyond our control, such as global commodity shocks.

Competitive Strengths

We believe the following competitive strengths differentiate us from other building product companies and position us for significant growth as part of a multi-year, multi stage recovery in our end markets.

Leading Market Positions in Targeted End Markets

Within the North American door market, we believe we hold either the number one or two market position in the seven product categories we target. We are one of the largest manufacturers of doors and door components in the world, selling approximately 35 million residential and architectural interior and exterior doors in 2016; approximately 23 million of which were sold in the United States, our largest market. We believe our scale and leadership positions support our commitment to invest in advanced manufacturing and e-commerce initiatives and develop innovative new products, to effectively service regional and national customers and to offer broad product lines across our markets, while reducing our materials and unit production costs.

Extensive Portfolio with Strong Brand Recognition

Our broad portfolio of brands is among the most recognized in the door industry and is associated with superior design, innovation, reliability and quality. Builder Magazine recognized the Masonite® brand as one of the leading interior door brands in the United States in 2016 in the following categories: Brand Familiarity, Brand Used in Past Two Years and Brand Used the Most.

Long-Term Customer Relationships and Well-Established Multi-Channel Distribution

As a result of our longstanding commitment to customer service and product innovation, we have well-established relationships within the wholesale and retail channels. All of our top 20 customers have purchased doors from us for at least 10 years, although we generally do not enter into long-term contracts with our customers and they generally do not have an obligation to purchase our products. In addition, our manufacturing and distribution facilities are strategically located to best serve our customers. We believe that our long-term relationships with leading retailers, wholesale distributors, major homebuilders, contractors and architects will enable us to continue to increase our market penetration in the residential and architectural construction markets.

Leading Technological Innovation Within the Door Industry

We believe we are a leader in technological innovation in the design of doors and door components and in the complex processes required to manufacture high quality products quickly and consistently. We intend to continue developing new and innovative products at our 145 thousand square foot innovation center in West Chicago, Illinois, while improving critical processes in the manufacturing and selling of our products. Our future success will depend on our ability to develop and introduce new or improved products, to continue to improve our manufacturing and product service processes, and to protect our rights to the technologies used in our products. We have also created proprietary web-based sales and marketing tools, including MAX Masonite Xpress Configurator® for our residential and DoorbuilderTM for our architectural customer networks, to improve selection and order processes, reduce order entry errors, create more accurate quotes, improve communication and facilitate a better customer experience. As of January 1, 2017, we had 223 design patents and design patent applications and 178 utility patents and patent applications in the United States, and 195 foreign design patents and patent applications and 271 foreign utility patents and patent applications.

2

Vertically Integrated Operations Across the Production Process

We are one of the few vertically integrated door manufacturers in the world. In North America, we are one of only two vertically integrated manufacturers of residential doors and the only vertically integrated manufacturer of non-residential interior wood doors. Our vertical integration extends across the production process, which we believe enhances our ability to develop products and respond quickly to changing consumer preferences, provides greater value and better service for our customers, and potentially lowers our costs. We leverage our assets through our vertically integrated operations in a manner that is difficult to replicate without significant capital investment.

Experienced Management Team with Extensive Experience and a Successful Track Record

We are managed by results-driven executives with a proven track record of successfully managing multiple brands, winning new business, reducing costs and identifying, executing and integrating strategic acquisitions. Several members of our management team previously worked at Fortune 500 companies, including Honeywell International Inc. (formerly AlliedSignal Inc.), General Motors Company, General Electric Company and Newell Rubbermaid Inc., where they utilized advanced technologies to improve cost structures and create competitive advantages.

Growth Strategy

Our vision is to be the premier provider of doors and door components for the global door industry. We are committed to executing the following balanced and complementary strategies to continue to further strengthen our leadership positions, create value for our customers, enhance our portfolio of leading brands and achieve our top and bottom line growth objectives.

Develop Innovative, Market-Leading Products

We intend to continue developing new and innovative products to grow our sales and enhance our returns. On average we have introduced more than 200 new products and designs in each of the last three years. We plan to capitalize on the anticipated growth in door demand by continuing to introduce new, value-added products to build upon our comprehensive portfolio of door styles, designs, textures, components, options, applications and materials. We have consistently demonstrated the ability to develop products that are differentiated by compelling design features and recognized for their reliability and quality. For example, we recently introduced the Heritage® Series of doors that feature recessed, flat panels and sharp, Shaker-style profiles which speak to a clean, modern aesthetic while retaining comfortable familiarity found in today’s interiors. We are extending our Heritage Series to exterior doors with the introduction of the Heritage Craftsman exterior fiberglass door line.

Expand our Presence in Attractive Markets to Accelerate Growth and Improve Margins

We plan to continue to focus our operations on attractive new market and channel opportunities. For example, we believe we can expand our leading position in the North American architectural wood door market by focusing on strategic sectors within this market, such as education, health care and hospitality. By expanding our market presence and achieving greater economies of scale, we intend to capitalize on the anticipated recovery in the U.S. non-residential construction market. Additionally, we believe we can expand our market growth in the architectural wood door market through the introduction of products with high design and performance attributes by focusing on certain markets within our Europe segment. We are also focused on expanding our business in the residential new construction market and with professional repair, renovation and remodeling contractors, both domestically and internationally.

We are also increasing our focus on multi-location in-home remodeling distributors and contractors. This channel is expected to grow with a shift in certain demographics from a "Do it Yourself" to a "Do it For You" offering. Using enhanced marketing, training and e-commerce tools, our teams plan to target specific multi-location remodeling distributors and contractors and attempt to increase our overall presence in the important repair, renovation and remodeling business.

3

Leverage Our Marketing, Sales and Customer Service Activities to Further Drive Sales

We intend to continue to pursue additional growth opportunities by leveraging our extensive sales, marketing and customer service efforts in innovative ways. For example, we have developed several proprietary web-based tools for our customers, including MAX Masonite Xpress Configurator®, MC2 and MConnectTM, to enhance communication and information flow with our customers in our wholesale dealer network by providing a more customized buying experience, customer leads and quoting capabilities and simplifying the procurement process. We also intend to capture additional share in the attractive professional repair, renovation and remodeling markets by helping professional contractors produce customized marketing materials to assist them in their sales efforts. In addition, we plan to continue developing effective marketing initiatives to expand our business with professional dealers and homebuilders.

Continue to Pursue Operational Excellence

As part of our commitment to continuous improvement we have launched initiatives to make our operations lean and efficient. We launched the Lean Six Sigma Continuous Improvement program in 2006. In 2015 we expanded our commitment by adopting a complete lean operating philosophy through the introduction of MVantage, Masonite’s Lean Advantage System. MVantage is a continuous improvement system centered around three key tenants: People, the Lean Management Operating System and Lean Tools. After a pilot program at two manufacturing sites, we introduced MVantage at 28 additional manufacturing sites in the United States, Canada, Mexico, Ireland and the United Kingdom in 2016. In 2017, we plan to implement MVantage in additional key operations in the United States and the United Kingdom. Our 2017 plans will focus on driving sustained rapid improvement through rigorous dedication to the key tenants of MVantage. We believe that our commitment to MVantage will not only assist Masonite in its efforts to set the industry benchmark for innovation, quality, delivery, service and support but also help improve safety, productivity, and financial performance.

Pursue Strategic Acquisitions to Create Leadership Positions

We intend to continue our disciplined approach to identifying, executing and integrating strategic acquisitions while maintaining a strong balance sheet, although we expect competition for the best candidates. We target companies who produce components for our existing operations, manufacture niche products and provide value-added services. Additionally, we target companies with strong brands, complementary technologies, attractive geographic footprints and opportunities for cost and distribution synergies. For example, from 2011 to 2016 we made twelve strategic acquisitions to create leadership positions in (i) the attractive North American architectural wood door and door core market through the acquisitions of Porta Industries, Inc. (“Marshfield”), Algoma Holding Company (“Algoma”), Les Portes Baillargeon, Inc. (“Baillargeon”), Harring Doors Corporation ("Harring"), USA Wood Door, Inc. ("USA Wood Door") and FyreWerks Inc. ("FyreWerks"), (ii) the North American interior stile and rail residential door market through the acquisitions of Portes Lemieux Inc. (“Lemieux”) and the assets of a door manufacturing operation located in Chile (the "Chile" acquisition) for servicing the North American market, (iii) the production and sale of wood veneers with the acquisition of Birchwood Lumber & Veneer Co., Inc. (“Birchwood”) and (iv) various markets in the United Kingdom with the acquisitions of Door-Stop International Limited ("Door-Stop"), Performance Doorset Solutions Limited ("PDS") and Hickman Industries Limited ("Hickman").

Product Lines

Residential Doors

We sell an extensive range of interior and exterior doors in a wide array of designs, materials, and sizes. While substantially all interior doors are made with wood and related materials such as hardboard (including wood composite molded and flat door facings), the use of wood in exterior doors in North America and Europe has declined over the last two decades as a result of the increased penetration of steel and fiberglass doors. Our exterior doors are made primarily of steel or fiberglass. Our residential doors are molded panel, flush, stile and rail, routed medium-density fiberboard (“MDF”), steel or fiberglass.

Molded panel doors are interior doors available either with a hollow or solid core and are made by assembling two molded door skin panels around a wood or MDF frame. Molded panel doors are routinely used for closets, bedrooms, bathrooms and hallways. Our molded panel product line is subdivided into five distinct product groups: our original Molded Panel series is a combination of classic styling, durable construction, and variety of design preferred by

4

our customers when price sensitivity is a critical component in the product selection; our Palazzo® series is comprised of three distinct patented designs that accentuate the beauty and flexibility of molding wood fiber to replicate high end, historically labor intensive door designs; the four doors within our Anniversary Collection® embody themed, period, and architectural style specific designs; the West EndTM Collection, strengthens our tradition of design innovation by introducing the clean and simple aesthetics found in modern linear designs to the molded panel interior door category; and our newest introduction to the molded panel line, the Heritage® Series, which features recessed, flat panels and sharp, Shaker-style profiles which speak to a clean, modern aesthetic while retaining comfortable familiarity found in today’s interiors. All of our molded panel doors except for the Palazzo® series can be upgraded with our proprietary, wheat straw based Safe ‘N Sound® door core or our environmentally friendly EmeraldTM door construction which enables home owners, builders, and architects to meet specific product requirements and “green” specifications to attain LEED certification for a building or dwelling.

Flush interior doors are available either with a hollow or solid core and are made by assembling two facings of plywood, MDF, composite wood, or hardboard over a wood or MDF frame. These doors can either have a wood veneer surface suitable for paint or staining or a composite wood surface suitable for paint. Our flush doors range from base residential flush doors consisting of unfinished composite wood, to the ultrahigh end exotic wood veneer doors.

Stile and rail doors are made from wood or MDF with individual vertical stiles, horizontal rails and panels, which have been cut, milled, veneered, and assembled from lumber such as clear pine, knotty pine, oak and cherry. Within our stile and rail line, glass panels can be inserted to create what is commonly referred to as a French door and we have over 50 glass designs for use in making French doors. Where horizontal slats are inserted between the stiles and rails, the resulting door is referred to as a louver door. For interior purposes stile and rail doors are primarily used for hallways, room dividers, closets and bathrooms. For exterior purposes these doors are used as entry doors with decorative glass inserts (known as lites) often inserted into these doors.

Routed MDF doors are produced by using a computer controlled router carver to machine a single piece of double refined MDF. Our routed MDF door category is comprised of two distinct product lines known as the Bolection® and CymaTM door. The offering of designs in this category is extensive, as the manufacturing of routed MDF doors is based on a routing program where the milling machine selectively removes material to reveal the final design.

Steel doors are exterior doors made by assembling two interlocking steel facings (paneled or flat) or attaching two steel facings to a wood or steel frame and injecting the core with polyurethane insulation. With our functional Utility Steel series, the design centric High Definition family, and the prefinished Sta-Tru® HD, we offer customers the freedom to select the right combination of design, protection, and compliance required for essentially any paint grade exterior door application. In addition, our product offering is significantly increased through our variety of compatible clear or decorative glass designs.

Fiberglass doors are considered premier exterior doors and are made by assembling two fiberglass door facings to a wood frame or composite material and injecting the core with polyurethane insulation. Led by the Barrington® door, our fiberglass door lines offer innovative designs, construction, and finishes. The Barrington® family of doors is specifically designed to replicate the construction, look, and feel of a real wood door. The Door-StopTM branded fiberglass doors are manufactured into prehung door sets and shipped to our customers with industry-leading lead times. We believe that our patented panel designs, sophisticated wood grain texturing and multiple application-specific construction processes will help our Barrington® and Belleville® fiberglass lines retain a distinct role in the exterior product category in the future.

Architectural Doors

Architectural doors are typically highly specified products designed, constructed, and tested to ensure regulatory compliance and that certification requirements such as FSC and LEED certifications are met. We offer an extensive line of architectural interior doors meeting custom market requirements and ranging from the entry level molded panel doors to the high end custom designed flush wood doors with exotic veneer inlay designs. Our architectural doors are molded panel, flush, stile and rail, or routed MDF and can be offered with varying levels of fire and sound rating as well as radiation shielding. Our architectural flush doors can also be produced with a laminate veneer facing. High pressure laminates are used when durability and aesthetics are the customer’s main concern, while low pressure laminates are utilized when consistency in surface color, texture, and value are equal requirements.

5

Components

In addition to residential and architectural doors, we also sell several door components to the building materials industry. Within the residential new construction market, we provide interior door facings, agri-fiber and particleboard door cores, MDF and wood cut-stock components to multiple manufacturers. Within the architectural building construction market, we are a leading component supplier of various critical door components and the largest wood veneer door skin supplier. Additionally, we are one of the leading providers of mineral and particleboard door cores to the North American architectural door market.

Molded door facings are thin sheets of molded hardboard produced by grinding or defibrating wood chips, adding resin and other ingredients, creating a thick fibrous mat composed of dry wood fibers and pressing the mat between two steel press plates to form a molded sheet, the surface of which may be smooth or may contain a wood grain pattern. Following pressing, molded door facings are trimmed, painted and shipped to door manufacturing plants where they are mounted on frames to produce molded doors.

Door framing materials, commonly referred to as cut stock, are wood or MDF components that constitute the frame on which interior and exterior door facings are attached. Door cores are pressed fiber mats of refined wood chips or agri-fiber used in the construction of solid core doors. For doors that must achieve a fire rating higher than 45 minutes, the door core consists of an inert mineral core or inorganic intumescent compounds.

New Products

We develop and engineer innovative products designed to influence the mix of products sold and provide the end user with doors and entry systems that enhance beauty and functionality while creating greater value to our customers. For example, on average we have introduced over 200 new products or product designs in each of the past three years, including three interior designs and a new exterior design in the Heritage Collection of doors that feature recessed, flat panels and sharp, Shaker-style profiles which speak to a clean, modern aesthetic while retaining comfortable familiarity found in today’s designs. We recently added new glass sizes and a fir textured offering to our Vista Grande line of exterior fiberglass doors that integrate glass into the door in a seamless assembly, giving a wider view through the door and clean, modern design lines. We also recently introduced our Barn Door Hardware kits to provide contemporary style to interior openings.

More consumers are requesting products that are factory finished. We continue to develop and invest in factory finished products tailored to the needs of our residential and architectural markets.

Sales and Marketing

Our sales and marketing efforts are focused around several key initiatives designed to drive organic growth, influence the mix sold and strengthen our customer relationships.

Multi-Level/Segment Distribution Strategy

We market our products through and to wholesale distributors, retail stores, independent and pro dealers, builders, remodelers, architects, door and hardware distributors and general contractors.

In the residential market, we deploy an "All Products" cross merchandising strategy, which provides certain of our retail and wholesale customers with access to our entire product range. Our "All Products" customers benefit from consolidating their purchases, leveraging our branding, marketing and selling strategies and improving their ability to influence the mix of products sold to generate greater value. We service our big box retail customers directly from our own door fabrication facilities which provide value added services and logistics, including store direct delivery of doors and entry systems and a full complement of in-store merchandising, displays and field service. Our wholesale residential channel customers are managed by our own sales professionals who focus on down channel initiatives designed to ensure our products are "pulled" through our North American wholesale distribution network.

6

Our architectural building construction customers are serviced by a separate and distinct sales team providing architects, door and hardware distributors, general contractors and project owners a wide variety of technical specifications, specific brand differentiation, compliance and regulatory approvals, product application advice and multisegment specialization work across North America. Additionally, our sales team is supported by marketing strategies aimed to drive product specification throughout our value chains via distributors, architects and end users.

Service Innovation

We leverage our marketing, sales and customer service activities to ensure our products are strategically pulled through our multiple distribution channels rather than deploying a more common, tactical "push" strategy like some of our competitors. Our marketing approach is designed to increase the value of each and every door opening we fill with our doors and entry systems, regardless of the channel being used to access our products.

Our proprietary web based tools accessible on our website also provide our customers with a direct link to our information systems to allow for accelerated and easier access to a wide variety of information and selling aids designed to increase customer satisfaction. Within our North American Residential business, our web-based tools include MConnect®, an online service allowing our customers access to several other E-Commerce tools designed to enhance the manufacturer-customer relationship. Once connected to our system, customers have access to MAX®,

Masonite’s Xpress Configurator®, a web based tool created to design customized door systems and influence the mix, improve selection and ordering processes, reduce order entry and quoting errors, and improve overall communication throughout the channel; MC2, our self-service, custom literature tool; the Product Corner, a section advising customers of the features and benefits of our newest products; Market Intelligence Section, which provides some of the latest economic statistics influencing our industry; the Treasure Chest, which is a collection of discontinued glass products providing customers with promotional based pricing on obsolete products; and Order Tracker, which allows customers to follow their purchase orders through the production process and confirm delivery dates. MConnect®, in conjunction with our website, improves transaction execution, enhances communication and information flow with our customers and their dealers providing a more customized buying experience. In Europe, our Door-Stop International website is a fully functional configuration and order platform that supports our entry door customers in the United Kingdom. The dynamic integration of Door-Stop's ERP and its website ensure that the products customers see, configure and order are in stock, which ensures that we are able to deliver on our promise of dependability. In our Architectural business, we have constructed a dedicated ordering platform for our distribution customers through our USA Wood Door website, which affords customers the ability to configure and purchase prefinished and machined wood doors through the streamlined Door Builder utility. Architectural distributors are able to make, retain and track quotes all within the USA Wood Door application.

Customers

During fiscal year 2016, we sold our products worldwide to more than 7,000 customers. We have developed strong relationships with these customers through our "All Products" cross merchandising strategy. Our vertical integration facilitates our "All Products" strategy with our door fabrication facilities in particular providing value-added fabrication and logistical services to our customers, including store delivery of pre-hung interior and exterior doors to our customers in North America. All of our top 20 customers have purchased doors from us for at least 10 years.

Although we have a large number of customers worldwide, our largest customer, The Home Depot, accounted for approximately 16% of our total net sales in fiscal year 2016. Due to the depth and breadth of the relationship with this customer, which operates in multiple North American geographic regions and which sells a variety of our products, our management believes that this relationship is likely to continue.

Distribution

Residential doors are primarily sold through wholesale and retail distribution channels.

• | Wholesale. In the wholesale channel, door manufacturers sell their products to homebuilders, contractors, lumber yards, dealers and building products retailers in two-steps or one step. Two-step distributors typically purchase doors from manufacturers in bulk and customize them by installing windows, or "lites", and pre-hanging them. One-step distributors sell doors directly to homebuilders and remodeling contractors who install the doors. |

7

• | Retail. The retail channel generally targets consumers and smaller remodeling contractors who purchase doors through retail home centers and smaller specialty retailers. Retail home centers offer large, warehouse size retail space with large selections, while specialty retailers are niche players that focus on certain styles and types of doors. |

Architectural doors are primarily sold through specialized one-step wholesale distribution channels where distributors sell to contractors and installers, or direct from manufacturers to contractors and installers.

Research and Development

We believe we are a leader in technological innovation and development of doors, door components and door entry systems and the manufacturing processes involved in making such products. We believe that research and development is a competitive advantage for us, and we intend to capitalize on our leadership in this area through the development of more new and innovative products. Our research and development and engineering capabilities enable us to develop and implement product and manufacturing process improvements that enhance the manufacturing efficiency of our products, improve quality and reduce costs.

As an integrated manufacturer, we believe that we are well positioned to take advantage of the growing global demand for a variety of molded door facing designs. We have an internal capability to create new molded door facing designs and manufacture our own molds for use in our own facilities. We believe this provides us with the ability to develop proprietary designs that enjoy a strong identity in the marketplace; more flexibility in meeting customer demand; quicker reaction time in the production of new designs or design changes; and greater responsiveness to customer needs. This capability also enables us to develop and implement product and process improvements with respect to the production of molded door facings and doors which enhance production efficiency and reduce costs.

In the past few years, our research and development activities have had a significant focus on process and material improvements in our products. These improvements have led to reductions in manufacturing costs and improvements in product quality. We have also directed our design innovation to address the growing need for safety and security, sound dampening and fire resistant products in the architectural wood door market.

Manufacturing Process

Our Manufacturing operations consist of three major manufacturing processes: (1) component manufacturing, (2) door slab assembly and (3) value-added ready to install door fabrication.

We have a leading position in the manufacturing of door components, including internal framing components (stile and rails), glass inserts (lites), door core, interior veneer and molded door facings, and exterior door facings. The manufacturing of interior molded door facings is the most complex of these processes requiring a significant investment in large scale wood fiber processing equipment. Interior molded door facings are produced by combining fine wood particles, synthetic resins and other additives under heat and pressure in large multi-opening automated presses utilizing Masonite proprietary steel plates. The facings are then painted, cut and inspected in a second highly automated continuous operation prior to being packed for shipping to our door assembly plants. We operate five interior molded door facing plants around the world, two in North America and one in each of South America, Europe and Asia. Our sole United States based plant in Laurel, Mississippi is one of the largest door facing plants in the world and we believe one of the most technologically advanced in the industry.

Interior residential hollow and solid core door manufacturing is an assembly operation that is primarily accomplished in the United States through the use of skilled manual labor and, at some plants, highly automated lines which are based on single flow principles and the use of advanced engineering processes and quality control features to assemble doors more quickly and reliably than before. Whether manual or automated, the construction process for a standard flush or molded interior door is based on assembly of door facings and various internal framing and support components, following which doors are trimmed to their final specifications.

The assembly process varies by type of door, from a relatively simple process for flush and molded doors, where the door facings are glued to a wood frame, to more complex processes where many pieces of solid and engineered wood are converted to louver or stile and rail door slabs. Architectural interior doors require another level of

8

customization and sophistication employing the use of solid cores with varying degrees of sound dampening and fire retarding attributes, furniture quality wood veneer facings, as well as secondary machining operations to incorporate more sophisticated commercial hardware, openers and locks. Additionally, architectural doors are typically pre-finished prior to sale.

The manufacturing of steel and fiberglass exterior door slabs is a semi-automated process that entails combining laminated wood or rot free composite framing components between two door facings and then injecting the resulting hollow core structure with insulating polyurethane expanding foam core materials. We invested in fiberglass manufacturing technology, including the vertical integration of our own fiberglass sheet molding compound plant at our Laurel, Mississippi, facility in 2006. In 2008 we consolidated fiberglass slab manufacturing from multiple locations throughout North America into a single highly automated facility in Dickson, Tennessee, significantly improving the reliability and quality of these products while simultaneously lowering cost and reducing lead times.

Short set-up times, proper production scheduling and coordinated material movement are essential to achieve a flexible process capable of producing a wide range of door types, sizes, materials and styles. We make use of our vertically integrated and flexible manufacturing operations together with scalable logistics primarily through the use of common carriers to fill customers’ orders and to minimize our investment in finished goods inventory.

Finally, interior flush and molded, stile and rail, louver and exterior door slabs manufactured at our door assembly plants are either sold directly to our customers or transferred to our door fabrication facilities where value added services are performed. These value added services include machining doors for hinges and locksets, installing the door slabs into ready to install frames, installing hardware, adding glass inserts and side lites, painting and staining, packaging and logistical services to our customers.

Raw Materials

While Masonite is vertically integrated, we require a regular supply of raw materials, such as wood chips and cut stock, various composites, steel, glass, paint, stain and primer as well as petroleum-based products such as binders, resins and plastic injection frames to manufacture and assemble our products. Our materials cost accounts for approximately 54% of the total cost of the finished product. In certain instances, we depend on a single or limited number of suppliers for these supplies. Wood chips, logs, resins, binders and other additives utilized in the manufacturing of interior molded facings, exterior fiberglass door facings and door cores are purchased from global, regional and local suppliers taking into consideration the relative freight cost of these materials. Internal framing components, MDF, cut stock and internal door cores are manufactured internally at our facilities and supplemented from suppliers located throughout the world. We utilize a network of suppliers based in North America, Europe, South America and Asia to purchase other components including steel coils for the stamping of steel door facings, MDF, plywood and hardboard facings, door jambs and frames and glass frames and inserts.

Safety

We believe that safety is as important to our success as productivity and quality. We also believe that incidents can be prevented through proper management, employee involvement, standardized operations and equipment and attention to detail. Safety programs and training are provided throughout the company to ensure employees and managers have effective tools to help identify and address both unsafe conditions and at-risk behaviors.

Through a sustained commitment to improve our safety performance, we have been successful in reducing the number of injuries sustained by our employees over the long term. However, in 2016 we experienced a total incident rate, or the annual number of injuries per 100 full time equivalent employees, of 1.7 compared to 1.4 in 2015. We believe that the increase was due to a combination of significant changes at many of our plants, including increasing production, converting temporary labor to full time employees and changes to our shift structures.

Environmental and Other Regulatory Matters

We strive to minimize any adverse environmental impact our operations might have to our employees, the general public and the communities of which we are a part. We are subject to extensive environmental laws and regulations. The geographic breadth of our facilities subjects us to environmental laws, regulations and guidelines in a number of jurisdictions, including, among others, the United States, Canada, Mexico, the United Kingdom, the

9

Republic of Ireland, the Czech Republic, Chile and Malaysia. Such laws, regulations and guidelines relate to, among other things, the discharge of contaminants into water and air and onto land, the storage and handling of certain regulated materials used in the manufacturing process, waste minimization, the disposal of wastes and the

remediation of contaminated sites. Many of our products are also subject to various regulations such as building and construction codes, product safety regulations, health and safety laws and regulations and mandates related to energy efficiency.

Our efforts to ensure environmental compliance include the review of our operations on an ongoing basis utilizing in-house staff and on a selective basis by specialized environmental consultants. The Environmental, Health and Safety team participates in industry groups to monitor developing regulatory actions and actively develop comments on specific issues. Furthermore, for our prospective acquisition targets, environmental assessments are conducted as part of our due diligence review process. Based on recent experience and current projections, environmental protection requirements and liabilities are not expected to have a material effect on our business, capital expenditures, operations or financial position.

In addition to the various environmental laws and regulations, our operations are subject to numerous foreign, federal, state and local laws and regulations, including those relating to the presence of hazardous materials and protection of worker health and safety, consumer protection, trade, labor and employment, tax, and others. We believe we are in compliance in all material respects with existing applicable laws and regulations affecting our operations.

Intellectual Property

In North America, our doors are marketed primarily under the Masonite® brand. Other North American brands include: Premdor®, Belleville®, Barrington®, Oakcraft®, Sta-Tru® HD, AvantGuard®, Flagstaff®, Hollister®, Sierra®, Specialty®, Fast-Frame®, Safe ’N Sound®, Palazzo Series®, Heritage®, Bellagio®, Capri®, Treviso®, Cheyenne®, Glenview®, Riverside®, Saddlebrook®, West EndTM, Mohawk®, Megantic®, Marshfield®, Birchwood Best®, Algoma®, NovodorTM, ArtisanTM, Artisan SFTM, RhinoDoor®, WeldrockTM, SuperstileTM, UnicolTM, Lemieux®, Harring DoorsTM and FyreWerks®. In Europe, doors are marketed under the Masonite®, Premdor®, CrosbyTM, Door-StopTM, Performance Doorset SolutionsTM and National HickmanTM brands. We consider the use of trademarks and trade names to be important in the development of product awareness, and for differentiating products from competitors and between customers.

We protect the intellectual property that we develop through, among other things, filing for patents in the United States and various foreign countries. In the United States, we currently have 223 design patents and design patent applications and 178 utility patents and patent applications. We currently have 195 foreign design patents and patent applications and 271 foreign utility patents and patent applications. Our U.S. utility patents are generally applicable for 20 years from the earliest filing date, our U.S. design patents for 15 years and our U.S. registered trademarks and trade names are generally applicable for 10 years and are renewable. Our foreign patents and trademarks have terms as set by the particular country, although trademarks generally are renewable.

Competition

The North American door industry is highly competitive and includes a number of global and local participants. In the North American residential interior door market, the primary participants are Masonite and JELD-WEN, which are the only vertically integrated manufacturers of door facings. There are also a number of smaller competitors in the residential interior door market that primarily source door facings from third party suppliers. In the North American residential exterior door market, the primary participants are Masonite, JELD-WEN, Plastpro, Therma-Tru, Feather River and Novatech. In the North American non-residential building construction door market, the primary participants are Masonite, VT Industries, Graham Wood Doors and Eggers Industries. Our primary market in Europe is the United Kingdom. The United Kingdom door industry is similarly competitive, including a number of global and local participants. The primary participants in the United Kingdom are our subsidiary Premdor, JELD-WEN, Vicaima and Distinction Doors. Competition in these markets is primarily based on product quality, design characteristics, brand awareness, service ability, distribution capabilities and value. We also face competition in the other countries in which we operate. In Europe, South America and Asia, we face significant competition from a number of regionally based competitors and importers.

10

A large portion of our products are sold through large home centers and other large retailers. The consolidation of our customers and our reliance on fewer larger customers has increased the competitive pressures as some of our largest customers, such as The Home Depot, perform periodic product line reviews to assess their product offerings and suppliers.

We are one of the largest manufacturers of molded door facings in the world. The rest of the industry consists of one other large, integrated door manufacturer and a number of smaller regional manufacturers. Competition in the molded door facing business is based on quality, price, product design, logistics and customer service. We produce molded door facings to meet our own requirements and outside of North America we serve as an important supplier to the door industry at large. We manufacture molded door facings at our facilities in Mississippi, Ireland, Chile, Canada and Malaysia.

Employees

As of January 1, 2017, we employed approximately 10,200 employees and contract personnel. This includes approximately 2,600 unionized employees, approximately 80% of whom are located in North America with the remainder in various foreign locations. Ten of our North American facilities have individual collective bargaining agreements, which are negotiated locally and the terms of which vary by location.

History and Reporting Status

Masonite was founded in 1925 in Laurel, Mississippi, by William H. Mason, to utilize vastly available quantities of sawmill waste to manufacture a usable end product. Masonite was acquired by Premdor from International Paper Company in August 2001.

Prior to 2005, Masonite was a public company with shares of our predecessor’s common stock listed on both the New York and Toronto Stock Exchanges. In March 2005, we were acquired by an affiliate of Kohlberg Kravis Roberts & Co. L.P.

On March 16, 2009, Masonite International Corporation and several affiliated companies, voluntarily filed to reorganize under the Company's Creditors Arrangement Act (the "CCAA") in Canada in the Ontario Superior Court of Justice. Additionally, Masonite International Corporation and Masonite Inc. (the former parent of the Company) and all of its U.S. subsidiaries filed voluntary petitions for reorganization under Chapter 11 of the U.S. Bankruptcy Code in the U.S. Bankruptcy Court in the District of Delaware. On June 9, 2009, we emerged from reorganization proceedings under the CCAA in Canada and under Chapter 11 of the U.S. Bankruptcy Code in the United States.

Effective July 4, 2011, pursuant to an amalgamation under the Business Corporations Act (British Columbia), Masonite Inc. amalgamated with Masonite International Corporation to form an amalgamated corporation named Masonite Inc., which then changed its name to Masonite International Corporation.

On September 9, 2013, our shares commenced listing on the New York Stock Exchange under the symbol "DOOR" and we became subject to periodic reporting requirements under the United States federal securities laws. We are currently not a reporting issuer, or the equivalent, in any province or territory of Canada and our shares are not listed on any recognized Canadian stock exchange.

Our United States executive offices are located at One Tampa City Center, 201 North Franklin Street, Suite 300, Tampa, Florida 33602 and our Canadian executive offices are located at 2771 Rutherford Road, Concord, Ontario L4K 2N6 Canada.

Available Information

We make our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 available through our website, free of charge, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission. Our website is www.masonite.com. Information on our website does not constitute part of this Annual Report on Form 10-K.

11

Item 1A. Risk Factors

You should carefully consider the following factors in addition to the other information set forth in this Annual Report before investing in our common shares. The risks and uncertainties described below are not the only ones facing us. If any of the following risks actually occur, our business, financial condition or results of operations would likely suffer. In such case, the trading price of our common shares could fall, and you may lose all or part of your investment.

Risks Related to Our Business

Downward trends in our end markets or in economic conditions could negatively impact our business and financial performance.

Our business may be adversely impacted by changes in United States, Canadian, European, Asian, South American or global economic conditions, including inflation, deflation, interest rates, availability and cost of capital, consumer spending rates, energy availability and costs, and the effects of governmental initiatives to manage economic conditions. Volatility in the financial markets in the regions in which we operate and the deterioration of national and global economic conditions have in the past and could in the future materially adversely impact our operations, financial results and liquidity.

Trends in our primary end markets (residential new construction, repair, renovation and remodeling and non-residential building construction) directly impact our financial performance because they are directly correlated to the demand for doors and door components. Accordingly, the following factors may have a direct impact on our business in the countries and regions in which our products are sold:

• | the strength of the economy; |

• | the amount and type of residential and non-residential construction; |

• | housing sales and home values; |

• | the age of existing home stock, home vacancy rates and foreclosures; |

• | non-residential building occupancy rates; |

• | increases in the cost of raw materials or any shortage in supplies or labor; |

• | the availability and cost of credit; |

• | employment rates and consumer confidence; and |

• | demographic factors such as immigration and migration of the population and trends in household formation. |

In the United States, the housing market crisis had a negative impact on residential housing construction and related product suppliers. In addition, the current housing recovery is characterized by new construction levels still well below historical levels, and at times including an increased number of multi-family new construction starts, which generally use fewer of our products and generate less net sales at a lower margin than typical single family homes.

In many of the non-North American markets in which we manufacture and sell our products, economic conditions deteriorated as various countries suffered from the after effects of the global financial downturn that began in the United States in 2006. Certain of our non-North American markets were acutely affected by the housing downturn and future downturns could cause excess capacity in housing and building products, including doors and door products, which may make it difficult for us to raise prices. Due in part to both market and operating conditions, we exited certain markets in the past several years, including the Ukraine, Turkey, Romania, Hungary, Poland, Israel, France and South Africa.

Our relatively narrow focus within the building products industry amplifies the risks inherent in a prolonged global market downturn. The impact of this weakness on our net sales, net income and margins will be determined by many factors, including industry capacity, industry pricing, and our ability to implement our business plan.

12

Increases in mortgage rates, changes in mortgage interest deductions and the reduced availability of financing for the purchase of new homes and home construction and improvements could have a material adverse impact on our sales and profitability.

In general, demand for new homes and home improvement products may be adversely affected by increases in mortgage rates and the reduced availability of consumer financing. Mortgage rates are near historic lows but have recently increased and will likely increase in the future. If mortgage rates increase and, consequently, the ability of prospective buyers to finance purchases of new homes or home improvement products is adversely affected, our business, financial condition and results of operations may be materially and adversely affected.

Members of Congress and government officials have from time to time suggested the elimination of the mortgage interest deduction for federal income tax purposes, either entirely or in part, based on borrower income, type of loan or principal amount. Future changes in policies set to encourage home ownership and improvement, such as changes to the tax rules allowing for deductions of mortgage interest, may adversely impact demand for our products and have a material adverse impact on us.

Our performance may also depend upon consumers having the ability to finance the purchase of new homes and other buildings and repair and remodeling projects with credit from third-parties. The ability of consumers to finance these purchases is affected by such factors as new and existing home prices, homeowners’ equity values, interest rates and home foreclosures. Adverse developments affecting any of these factors could result in a tightening of lending standards by financial institutions and reduce the ability of some consumers to finance home purchases or repair and remodeling expenditures. The most recent economic downturn, including declining home and other building values, increased home foreclosures and tightening of credit standards by lending institutions, have negatively impacted the home and other building new construction and repair and remodeling sectors. If these credit market trends continue or worsen, our net sales and net income may be adversely affected.

We operate in a competitive business environment. If we are unable to compete successfully, we could lose customers and our sales could decline.

The building products industry is highly competitive. Some of our principal competitors may have greater financial, marketing and distribution resources than we do and may be less leveraged than we are, providing them with more flexibility to respond to new technology or shifting consumer demand. Accordingly, these competitors may be better able to withstand changes in conditions within the industry in which we operate and may have significantly greater operating and financial flexibility than we do. Also, certain of our competitors may have excess production capacity, which may lead to pressure to decrease prices in order for us to remain competitive and may limit our ability to raise prices even in markets where economic and market conditions have improved. For these and other reasons, these competitors could take a greater share of sales and cause us to lose business from our customers or hurt our margins.

As a result of this competitive environment, we face pressure on the sales prices of our products. Because of these pricing pressures, we may in the future experience limited growth and reductions in our profit margins, sales or cash flows, and may be unable to pass on future raw material price, labor cost and other input cost increases to our customers which would also reduce profit margins.

Because we depend on a core group of significant customers, our sales, cash flows from operations and results of operations may be negatively affected if our key customers reduce the amount of products they purchase from us.

Our customers consist mainly of wholesalers, retail home centers and contractors. Our top ten customers together accounted for approximately 44% of our net sales in fiscal year 2016, while our largest customer, The Home Depot, accounted for approximately 16% of our net sales in fiscal year 2016. We expect that a small number of customers will continue to account for a substantial portion of our net sales for the foreseeable future. However, net sales from customers that have accounted for a significant portion of our net sales in past periods, individually or as a group, may not continue in future periods, or if continued, may not reach or exceed historical levels in any period. For example, our largest customer, The Home Depot, performs periodic line reviews to assess its product offerings, which have, on past occasions, led to loss of business and pricing pressures. In addition, as a result of competitive bidding processes, we may not be able to increase or maintain the margins at which we sell our products to our most significant customers. Moreover, if any of these customers fails to remain competitive in the respective markets or encounters

13

financial or operational problems, our net sales and profitability may decline. We generally do not enter into long-term contracts with our customers and they generally do not have an obligation to purchase products from us. Therefore, we could lose a significant customer with little or no notice. The loss of, or a significant adverse change in, our relationships with The Home Depot or any other major customer could cause a material decrease in our net sales.

Our competitors may adopt more aggressive sales policies and devote greater resources to the development, promotion and sale of their products than we do, which could result in a loss of customers. The loss of, or a reduction in orders from, any significant customers, losses arising from customer disputes regarding shipments, fees, merchandise condition or related matters, or our inability to collect accounts receivable from any major customer, could have a material adverse effect on us. Also, we have no operational or financial control over these customers and have limited influence over how they conduct their businesses.

Consolidation of our customers and their increasing size could adversely affect our results of operations.

In many of the countries in which we operate, an increasingly large number of building products are sold through large retail home centers and other large retailers. In addition, we have experienced consolidation of distributors in our wholesale distribution channel and among businesses operating in different geographic regions resulting in more customers operating nationally and internationally. If the consolidation of our customers and distributors were to continue, leading to the further increase of their size and purchasing power, we may be challenged to continue to provide consistently high customer service levels for increasing sales volumes, while still offering a broad portfolio of innovative products and on-time and complete deliveries. If we fail to provide high levels of service, broad product offerings, competitive prices and timely and complete deliveries, we could lose a substantial amount of our customer base and our profitability, margins and net sales could decrease. Consolidation of our customers could also result in the loss of a customer or a substantial portion of a customer's business.

If we are unable to accurately predict future demand preferences for our products, our business and results of operations could be materially affected.

A key element to our continued success is the ability to maintain accurate forecasting of future demand preferences for our products. Our business in general is subject to changing consumer and industry trends, demands and preferences. Changes to consumer shopping habits and potential trends towards "online" purchases could also impact our ability to compete as we currently sell our products mainly through our distribution channel. Our continued success depends largely on the introduction and acceptance by our customers of new product lines and improvements to existing product lines that respond to such trends, demands and preferences. Trends within the industry change often and our failure to anticipate, identify or quickly react to changes in these trends could lead to, among other things, rejection of a new product line and reduced demand and price reductions for our products, and could materially adversely affect us. In addition, we are subject to the risk that new products could be introduced that would replace or reduce demand for our products. Furthermore, new proprietary designs and/or changes in manufacturing technologies may render our products obsolete or we may not be able to manufacture products or designs at prices that would be competitive in the marketplace. We may not have sufficient resources to make necessary investments or we may be unable to make the investments or acquire the intellectual property rights necessary to develop new products or improve our existing products.

Our business is seasonal which may affect our net sales, cash flows from operations and results of operations.

Our business is moderately seasonal and our sales vary from quarter to quarter based upon the timing of the building season in our markets. Severe weather conditions in any quarter, such as unusually prolonged warm or cold conditions, rain, blizzards or hurricanes, could accelerate, delay or halt construction and renovation activity. The impact of these types of events on our business may adversely impact our sales, cash flows from operations and results of operations. Also, we cannot predict the effects on our business that may result from global climate change, including potential new related laws or regulations. If sales were to fall substantially below what we would normally expect during certain periods, our annual financial results would be adversely impacted. Moreover, our facilities are vulnerable to severe weather conditions.

14

A disruption in our operations could materially affect our operating results.

We operate facilities worldwide. Many of our facilities are located in areas that are vulnerable to hurricanes, earthquakes and other natural disasters. In the event that a hurricane, earthquake, natural disaster, fire or other catastrophic event were to interrupt our operations for any extended period of time, particularly at one or more of our door facing facilities or architectural door plants, such as when Marshfield experienced an autoclave explosion in July 2011, prior to our acquisition, it could delay shipment of merchandise to our customers, damage our reputation or otherwise have a material adverse effect on our financial condition and results of operations. Closure of one of our door facing facilities, which are our most capital intensive and least replaceable production facilities, could have a substantial negative effect on our earnings.

In addition, our operations may be interrupted by terrorist attacks or other acts of violence or war. These attacks may directly impact our suppliers’ or customers’ physical facilities. Furthermore, these attacks may make travel and the transportation of our supplies and products more difficult and more expensive and ultimately affect our operating results. The United States has entered into, and may enter into, additional armed conflicts which could have a further impact on our sales and our ability to deliver product to our customers in the United States and elsewhere. Political and economic instability in some regions of the world, including the current instabilities in the Middle East and North Africa, may also negatively impact our business. The consequences of any of these armed conflicts are unpredictable, and we may not be able to foresee events that could have an adverse effect on our business or your investment. More generally, any of these events could cause consumer confidence and spending to decrease or result in increased volatility in the United States and worldwide financial markets and economy. They could also result in economic recession in the United States or abroad. Any of these occurrences could have a significant impact on our operating results.

Manufacturing realignments may result in a decrease in our short-term earnings, until the expected cost reductions are achieved, as well as reduce our flexibility to respond quickly to improved market conditions.

We continually review our manufacturing operations and sourcing capabilities. Effects of periodic manufacturing realignments and cost savings programs have in the past and could in the future result in a decrease in our short-term earnings until the expected cost reductions are achieved. We also cannot assure you we will achieve all of our cost savings. Such programs may include the consolidation, integration and upgrading of facilities, functions, systems and procedures. The success of these efforts will depend in part on market conditions, and such actions may not be accomplished as quickly as anticipated and the expected cost reductions may not be achieved or sustained.

In connection with our manufacturing realignment and cost savings programs, we have closed or consolidated a substantial portion of our global operations and reduced our personnel, which may reduce our flexibility to respond quickly to improved market conditions. For example, in November 2016, we announced the closure of our Algoma, Wisconsin, facility in order to improve our cost structure, expand operational efficiencies and align our plant optimization portfolio. As a result, a failure to anticipate a sharp increase in levels of residential new construction, residential repair, renovation and remodeling and non-residential building construction activity could result in operational difficulties, adversely impacting our ability to provide our products to our customers. This may result in the loss of business to our competitors in the event they are better able to forecast or respond to market demand. There can be no assurance that we will be able to accurately forecast the level of market demand or react in a timely manner to such changes, which may have a material adverse effect on our business, financial condition and results of operations.

We are subject to the credit risk of our customers.

We provide credit to our customers in the normal course of business. We generally do not require collateral in extending such credit. An increase in the exposure, coupled with material instances of default, could have a material adverse effect on our business, financial condition, results of operations and cash flow.

Increased prices for raw materials or finished goods used in our products or interruptions in deliveries of raw materials or finished goods could adversely affect our profitability, margins and net sales.

Our profitability is affected by the prices of raw materials and finished goods used in the manufacture of our products. These prices have fluctuated and may continue to fluctuate based on a number of factors beyond our control, including world oil prices, changes in supply and demand, general economic or environmental conditions, labor costs,

15